Global Agriculture Technologies market Size and Share Analysis 2026-2033

Global Agriculture Technologies market Forecast Snapshot (2026???2033)

| Metric | Value |

|---|---|

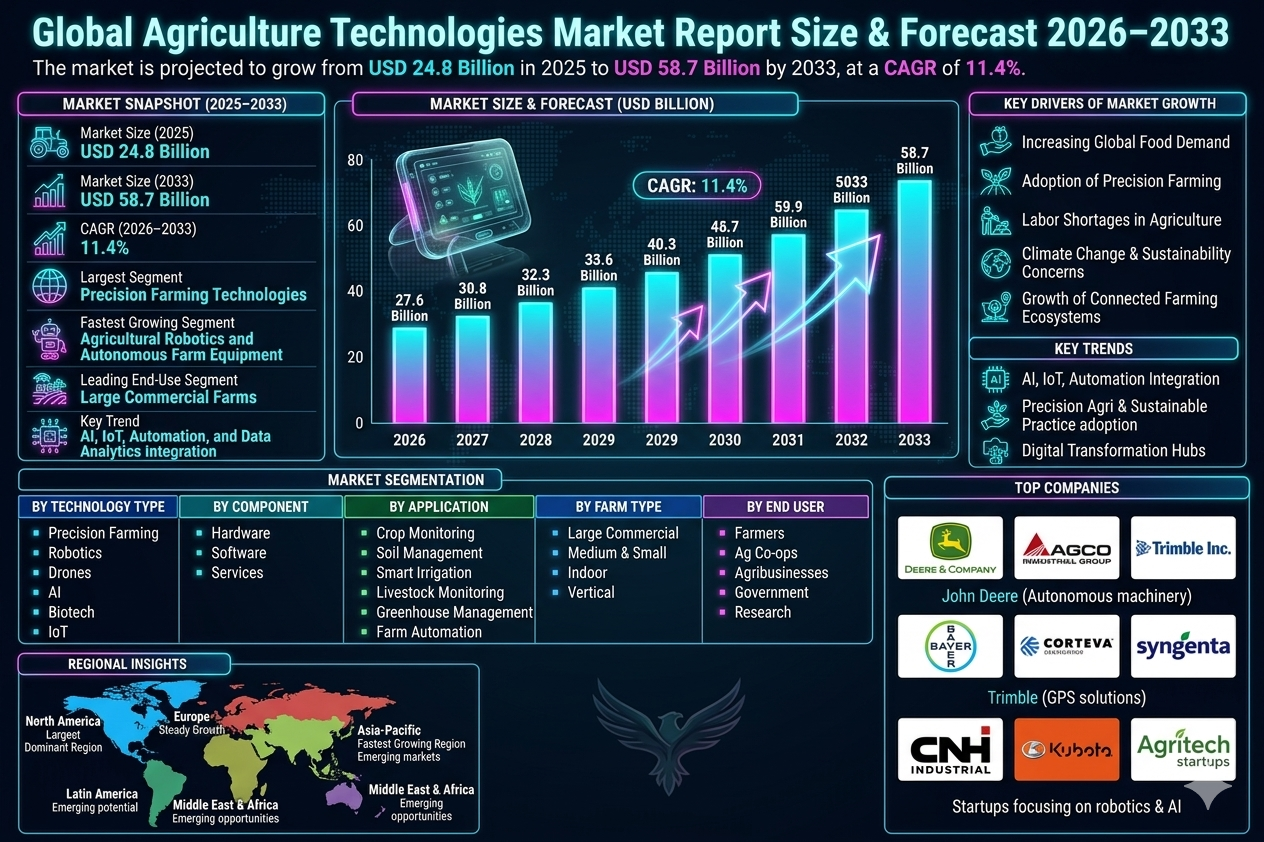

| Market Size (2025) | USD 24.8 Billion |

| Market Size (2033) | USD 58.7 Billion |

| CAGR (2026???2033) | 11.4% |

| Largest Segment | Precision Farming Technologies |

| Fastest Growing Segment | Agricultural Robotics and Autonomous Farm Equipment |

| Leading End-Use Segment | Large Commercial Farms |

| Key Trend | Integration of AI, IoT, Automation, and Data Analytics into Smart Farming Ecosystems |

| Dominant Region | North America |

| Fastest Growing Region | Asia-Pacific |

| Primary Growth Driver | Increasing Demand for Sustainable Agriculture and Higher Farm Productivity |

Global Agriculture Technologies Market Size & Forecast

The global agriculture technologies market is projected to witness substantial growth during the forecast period from 2026 to 2033. The market was valued at approximately USD 24.8 billion in 2025 and is expected to reach nearly USD 58.7 billion by 2033, expanding at a CAGR of around 11.4%. This growth is driven by increasing demand for sustainable farming solutions, rising global food consumption, and rapid adoption of digital technologies across the agricultural sector. The market is undergoing a major transformation as traditional farming practices increasingly integrate advanced technologies such as precision agriculture, artificial intelligence, IoT-enabled farm equipment, agricultural robotics, drones, smart irrigation systems, and data analytics platforms. These technologies are improving farm productivity, reducing operational costs, and enabling efficient resource utilization. In addition, growing concerns regarding climate change, soil degradation, water scarcity, and labour shortages are accelerating the adoption of smart farming technologies globally. Governments and agricultural organizations are investing heavily in modern farming infrastructure and digital agriculture initiatives to strengthen food security and optimize agricultural output. Technological advancements in automation, cloud computing, remote sensing, and autonomous farm machinery are further supporting market growth. Increasing venture capital investments and agritech startup activity are also contributing to innovation and commercialization of advanced agricultural technologies worldwide.Global Agriculture Technologies Market Overview

The agriculture technologies market encompasses a broad ecosystem of digital, mechanical, biological, and analytical technologies designed to improve agricultural efficiency, productivity, and sustainability. The market includes precision farming systems, farm management software, agricultural drones, robotics, biotechnology solutions, and connected farming equipment. The sector is rapidly evolving toward data-driven agriculture, where farmers utilize real-time analytics, satellite imaging, machine learning, and IoT sensors to monitor crop health, optimize irrigation, predict weather impacts, and improve decision-making processes. Key industry participants include Deere & Company, AGCO Corporation, Trimble Inc., Bayer AG, Corteva Agriscience, Syngenta, CNH Industrial, Kubota Corporation, and numerous agritech startups focusing on automation and digital farming innovations. The market is characterized by increasing collaboration between technology providers, agricultural equipment manufacturers, research institutions, and governments to accelerate smart agriculture adoption. Digital transformation initiatives in agriculture are becoming essential for addressing global food production challenges and sustainability goals.Key Drivers of Global Agriculture Technologies Market Growth

Increasing Global Food Demand

Rapid population growth and changing dietary preferences are significantly increasing food demand worldwide. Agriculture technologies help farmers maximize productivity, reduce crop losses, and improve farming efficiency to meet rising consumption needs.Adoption of Precision Farming

Precision agriculture technologies enable data-driven farming practices that optimize input usage, improve crop yields, and minimize waste. Farmers are increasingly adopting GPS systems, drones, and variable-rate technology for efficient field management.Labor Shortages in Agriculture

Declining agricultural labor availability in many countries is accelerating adoption of automated farming systems, robotics, and autonomous machinery to reduce dependency on manual labor.Climate Change and Sustainability Concerns

Environmental challenges such as water scarcity, unpredictable weather patterns, and soil degradation are driving demand for smart irrigation systems, climate monitoring technologies, and sustainable farming practices.Growth of Connected Farming Ecosystems

Integration of IoT sensors, cloud computing, and AI-powered analytics is creating connected farming ecosystems that improve operational visibility, predictive decision-making, and overall farm management efficiency.Global Agriculture Technologies Market Segmentation

By Technology Type

The market is segmented into precision farming, agricultural robotics, drones, artificial intelligence, biotechnology, IoT-enabled farming systems, smart irrigation technologies, and farm management software. Precision farming currently dominates the market due to widespread adoption across commercial agriculture operations.By Component

The market includes hardware, software, and services. Hardware components such as sensors, drones, automated machinery, and irrigation systems account for a major share, while software and analytics platforms are witnessing rapid growth.By Application

Applications include crop monitoring, soil management, irrigation management, livestock monitoring, greenhouse management, weather forecasting, supply chain optimization, and farm automation.By Farm Type

The market serves large commercial farms, small and medium-sized farms, indoor farming facilities, and vertical farming operations. Large-scale farms remain the primary adopters due to higher capital investment capacity.By End User

End users include farmers, agricultural cooperatives, agribusiness companies, government agencies, and research institutions. Commercial agribusinesses are increasingly investing in integrated smart farming systems.Regional Market Dynamics

North America dominates the global agriculture technologies market due to strong adoption of precision farming systems, advanced mechanization, and high investment in agritech innovation across the United States and Canada. Europe is witnessing steady growth driven by sustainability-focused agricultural policies, smart farming initiatives, and increasing adoption of digital agriculture technologies in countries such as Germany, France, and the Netherlands. Asia-Pacific is the fastest-growing region due to expanding agricultural modernization programs, rising food demand, and increasing agritech investments in China, India, Japan, and Southeast Asia. Latin America is emerging as a significant market with growing precision farming adoption in Brazil and Argentina, particularly in large-scale soybean and grain production. Middle East & Africa is gradually adopting agriculture technologies to address water scarcity, improve crop productivity, and strengthen food security through controlled environment agriculture systems.Competitive Landscape

The global agriculture technologies market is highly competitive and innovation-driven, with participation from agricultural equipment manufacturers, software companies, biotechnology firms, and agritech startups. Major companies include Deere & Company, AGCO Corporation, Trimble Inc., Bayer AG, CNH Industrial, Kubota Corporation, Corteva Agriscience, and Syngenta. Companies are increasingly focusing on integrated farming ecosystems that combine AI, IoT, automation, robotics, and predictive analytics. Strategic partnerships, acquisitions, and technology collaborations are becoming common to strengthen market positioning. John Deere remains a major leader in autonomous farming machinery and connected agricultural equipment, while Trimble specializes in GPS-based precision farming technologies and farm management software. Competition is centered around innovation, operational efficiency, sustainability, and data-driven decision-making capabilities. Startups focusing on robotics, indoor farming, and AI-powered analytics are also gaining traction globally.Strategic Outlook

The strategic outlook for the agriculture technologies market remains highly positive as global agriculture continues to shift toward automation, digitalization, and sustainability. Smart farming solutions are expected to become increasingly essential for improving food production efficiency and climate resilience. Future growth opportunities lie in autonomous tractors, robotic harvesting systems, AI-driven predictive farming, vertical farming technologies, and blockchain-enabled agricultural supply chains. Integration of advanced analytics with real-time farm monitoring systems will further optimize agricultural operations. Governments and private investors are expected to continue supporting agricultural innovation through funding programs, smart farming incentives, and infrastructure development initiatives.Final Market Perspective

The global agriculture technologies market is positioned for long-term expansion driven by increasing demand for efficient, sustainable, and technology-enabled farming systems. The integration of digital technologies into agriculture is fundamentally transforming how food is produced, managed, and distributed globally. As the agricultural sector faces growing pressure from population growth, climate challenges, and resource constraints, advanced farming technologies will play a critical role in ensuring future food security and environmental sustainability. Companies that successfully combine automation, analytics, and sustainable farming solutions are expected to lead the future of global agriculture.Table of Contents

Table of Contents

- 1. Executive Summary

- 1.1 Market Forecast Snapshot (2026-2033)

- 1.2 Global Market Size & CAGR Analysis

- 1.3 Largest & Fastest-Growing Segments

- 1.4 Region-Level Leadership & Growth Trends

- 1.5 Key Market Drivers

- 1.6 Competitive Landscape Overview

- 1.7 Strategic Outlook Through 2033

- 2. Introduction & Market Overview

- 2.1 Definition of the Agriculture Technologies Market

- 2.2 Scope of the Study

- 2.3 Industry Evolution & Smart Farming Transformation

- 2.4 Agricultural Technology Ecosystem & Value Chain

- 2.5 Impact of Digital Agriculture Adoption

- 2.6 Sustainability & Climate-Resilient Farming Trends

- 2.7 Technology & Innovation Landscape

- 3. Research Methodology

- 3.1 Primary Research

- 3.2 Secondary Research

- 3.3 Market Size Estimation Model

- 3.4 Forecast Assumptions (2026-2033)

- 3.5 Data Validation & Triangulation

- 4. Market Dynamics

- 4.1 Drivers

- 4.1.1 Increasing Global Food Demand

- 4.1.2 Adoption of Precision Farming

- 4.1.3 Labor Shortages in Agriculture

- 4.1.4 Climate Change & Sustainability Concerns

- 4.1.5 Growth of Connected Farming Ecosystems

- 4.2 Restraints

- 4.2.1 High Initial Technology Investment Costs

- 4.2.2 Limited Digital Infrastructure in Rural Areas

- 4.2.3 Data Security & Privacy Concerns

- 4.2.4 Lack of Technical Expertise Among Farmers

- 4.3 Opportunities

- 4.3.1 Expansion of AI & Automation in Farming

- 4.3.2 Growth of Vertical & Indoor Farming

- 4.3.3 Smart Irrigation & Water Management Solutions

- 4.3.4 Agritech Startup & Venture Capital Expansion

- 4.4 Challenges

- 4.4.1 Integration Complexity Across Farming Systems

- 4.4.2 Connectivity & Network Limitations

- 4.4.3 High Dependence on Climate Conditions

- 4.4.4 Fragmented Agricultural Market Structure

- 4.1 Drivers

- 5. Agriculture Technologies Market Analysis (USD Billion), 2026-2033

- 5.1 Market Size Overview

- 5.2 CAGR Analysis

- 5.3 Regional Revenue Distribution

- 5.4 Segment Revenue Analysis

- 5.5 Technology Adoption Trends

- 5.6 Agricultural Productivity Impact Analysis

- 6. Market Segmentation (USD Billion), 2026-2033

- 6.1 By Technology Type

- 6.1.1 Precision Farming

- 6.1.2 Agricultural Robotics

- 6.1.3 Agricultural Drones

- 6.1.4 Artificial Intelligence

- 6.1.5 Biotechnology Solutions

- 6.1.6 IoT-Enabled Farming Systems

- 6.1.7 Smart Irrigation Technologies

- 6.1.8 Farm Management Software

- 6.2 By Component

- 6.2.1 Hardware

- 6.2.2 Software

- 6.2.3 Services

- 6.3 By Application

- 6.3.1 Crop Monitoring

- 6.3.2 Soil Management

- 6.3.3 Irrigation Management

- 6.3.4 Livestock Monitoring

- 6.3.5 Greenhouse Management

- 6.3.6 Weather Forecasting

- 6.3.7 Supply Chain Optimization

- 6.3.8 Farm Automation

- 6.4 By Farm Type

- 6.4.1 Large Commercial Farms

- 6.4.2 Small & Medium-Sized Farms

- 6.4.3 Indoor Farming Facilities

- 6.4.4 Vertical Farming Operations

- 6.5 By End User

- 6.5.1 Farmers

- 6.5.2 Agricultural Cooperatives

- 6.5.3 Agribusiness Companies

- 6.5.4 Government Agencies

- 6.5.5 Research Institutions

- 6.1 By Technology Type

- 7. Market Segmentation by Geography

- 7.1 North America

- 7.2 Europe

- 7.3 Asia-Pacific

- 7.4 Latin America

- 7.5 Middle East & Africa

- 8. Competitive Landscape

- 8.1 Market Share Analysis

- 8.2 Product Portfolio Benchmarking

- 8.3 Technology Integration Mapping

- 8.4 Strategic Partnerships & Collaborations

- 8.5 Competitive Intensity & Differentiation

- 9. Company Profiles

- 10. Strategic Intelligence & Pheonix AI Insights

- 10.1 Pheonix Demand Forecast Engine

- 10.2 Smart Farming Infrastructure Analyzer

- 10.3 Precision Agriculture Technology Tracker

- 10.4 Agricultural Automation & Robotics Insights

- 10.5 Automated Porter???s Five Forces Analysis

- 11. Future Outlook & Strategic Recommendations

- 11.1 Expansion of Autonomous Farming Systems

- 11.2 AI-Driven Agricultural Decision Platforms

- 11.3 Sustainable Farming & Climate Resilience Strategies

- 11.4 Regional Expansion & Agritech Investments

- 11.5 Long-Term Market Outlook (2033+)

- 12. Appendix

- 13. About Pheonix Research

- 14. Disclaimer

Competitive Landscape

Global Agriculture Technologies Market Competitive Intensity & Market Structure Overview

The Global Agriculture Technologies Market operates within a highly innovation-driven and rapidly evolving competitive ecosystem, supported by increasing digital transformation across global agriculture. The market is transitioning from conventional mechanized farming toward integrated smart agriculture systems powered by AI, IoT, robotics, precision farming, automation, and predictive analytics technologies.

Competitive intensity is high due to accelerating technology adoption, rising agritech investments, and increasing demand for sustainable and productivity-focused farming solutions. Companies compete aggressively through automation capabilities, platform integration, data analytics performance, equipment efficiency, and scalability across different agricultural environments.

The market structure is moderately fragmented, combining large multinational agricultural machinery manufacturers, technology companies, biotechnology firms, and fast-growing agritech startups. Established players dominate large-scale farming equipment and integrated farm ecosystems, while startups focus on niche innovations such as agricultural robotics, drone analytics, indoor farming, and AI-powered crop intelligence.

Global Agriculture Technologies Market Competitive Intensity & Market Structure Current Scenario

Leading Company Profiles

Deere & Company (John Deere): Global leader in smart agricultural machinery, autonomous tractors, connected farming systems, and AI-powered precision agriculture solutions.

AGCO Corporation: Major agricultural equipment manufacturer focused on precision farming technologies, automated machinery, and digital farm management platforms.

Trimble Inc.: Leading provider of GPS-guided precision agriculture systems, farm management software, and real-time field analytics technologies.

Bayer AG: Strong player in digital agriculture through Climate Corporation platforms, predictive farming analytics, and crop optimization technologies.

CNH Industrial: Global agricultural machinery company investing in autonomous farming systems, smart tractors, and connected agricultural equipment.

Kubota Corporation: Advanced agricultural machinery manufacturer focused on automation, compact smart farming equipment, and sustainable farming solutions.

Corteva Agriscience: Agricultural science company integrating digital farming platforms, seed technologies, and data-driven crop management systems.

Syngenta: Key agritech and crop science company leveraging AI, precision agriculture, and digital advisory systems to improve farming efficiency.

IBM Corporation: Technology provider supporting AI-driven agriculture analytics, weather intelligence, and cloud-based farm management infrastructure.

DroneDeploy & Agribotix: Emerging agritech innovators specializing in drone-based crop monitoring, aerial analytics, and precision agriculture imaging systems.

Key Competitive Intensity & Market Structure Signals in Global Agriculture Technologies Market

A major competitive signal is the growing shift toward integrated smart farming ecosystems that combine machinery, software, IoT sensors, AI analytics, and automation into unified operational platforms.

Precision farming technologies remain the core competitive segment, with companies increasingly investing in GPS systems, real-time field monitoring, and predictive analytics to improve productivity and resource efficiency.

Agricultural robotics and autonomous machinery are rapidly reshaping competition, particularly in large-scale farming operations facing labor shortages and rising operational costs.

Cloud-based farm management platforms and AI-driven decision support systems are becoming key differentiators, enabling farmers to optimize irrigation, crop health monitoring, and yield forecasting in real time.

Strategic collaborations between machinery manufacturers, software developers, agritech startups, and government agencies are accelerating commercialization and global market expansion.

Strategic Implications of Competitive Intensity & Market Structure in Global Agriculture Technologies Market

The market is increasingly shifting from standalone agricultural products toward integrated digital farming ecosystems where hardware, software, and analytics operate together.

Investment in automation, AI-powered analytics, satellite imaging, and connected farm infrastructure is becoming essential for maintaining long-term competitiveness.

Scalability across commercial farms, smallholder agriculture, and controlled environment farming systems is emerging as a major strategic differentiator among global providers.

Sustainability-focused innovation is gaining importance as governments and agricultural organizations prioritize climate resilience, water efficiency, and reduced chemical usage in farming practices.

Data ownership and agricultural intelligence platforms are becoming increasingly valuable strategic assets, strengthening long-term customer retention and ecosystem control.

Global Agriculture Technologies Market Competitive Intensity & Market Structure Forward Outlook

The Global Agriculture Technologies Market is expected to witness increasing consolidation as major agricultural machinery companies, software firms, and agritech providers expand through acquisitions, partnerships, and ecosystem integration strategies.

Autonomous farming systems, robotic harvesting, AI-driven crop intelligence, and connected precision agriculture platforms are expected to define the next phase of market competition.

Cloud-based agriculture platforms and real-time predictive analytics will become central to future farm operations, improving productivity, sustainability, and operational efficiency.

Emerging technologies such as vertical farming systems, blockchain-enabled agricultural supply chains, and regenerative farming analytics are expected to create new competitive growth opportunities.

In the long term, the market will be shaped by three core competitive pillars: intelligent automation, integrated digital farming ecosystems, and sustainable agriculture innovation. Companies that successfully combine advanced technology infrastructure with scalable farming solutions will lead the Global Agriculture Technologies Market through 2033.

Value Chain

Global Agriculture Technologies Market Value Chain & Supply Chain Evolution Overview

The Global Agriculture Technologies Market value chain is evolving from conventional agricultural machinery and manual farming systems into highly connected, data-driven, automated, and intelligent farming ecosystems. This transformation is being accelerated by rising global food demand, climate change pressures, labor shortages, sustainability goals, and rapid digitalization across agricultural operations.

Agriculture technologies integrate advanced systems such as precision farming, AI-powered analytics, IoT-enabled sensors, agricultural robotics, drones, autonomous machinery, biotechnology solutions, and cloud-based farm management platforms. These technologies enable farmers to improve productivity, optimize resource utilization, reduce environmental impact, and enhance operational efficiency.

The value chain now extends beyond traditional farm equipment manufacturing into semiconductor supply, IoT device production, AI software development, satellite imaging, connectivity infrastructure, agricultural data analytics, and autonomous farming ecosystems. Leading companies such as Deere & Company, AGCO Corporation, Trimble Inc., Bayer AG, CNH Industrial, Kubota Corporation, Corteva Agriscience, and Syngenta are investing heavily in integrated smart agriculture platforms.

The upstream supply chain increasingly relies on sensor manufacturers, semiconductor suppliers, GPS technology providers, drone component manufacturers, cloud computing companies, and biotechnology developers to support advanced agricultural systems.

Manufacturing and technology integration strategies are increasingly focused on automation, predictive analytics, autonomous equipment, precision application technologies, and connected farming infrastructure capable of real-time decision-making.

Key supply chain challenges include limited rural connectivity infrastructure, high technology implementation costs, fragmented farm data systems, interoperability limitations, cybersecurity concerns, and dependence on semiconductor and electronics supply chains.

Global Agriculture Technologies Market Value Chain & Supply Chain Evolution Current Scenario

The current agriculture technology ecosystem is shaped by rising adoption of precision farming systems, increasing automation across large-scale agricultural operations, and growing integration of AI, IoT, and cloud computing technologies.

Hardware suppliers are rapidly expanding production of smart tractors, autonomous farming equipment, drones, precision irrigation systems, and IoT-enabled field sensors to support digital agriculture adoption.

Software providers are strengthening AI-driven analytics platforms capable of delivering real-time crop intelligence, predictive weather analysis, soil health monitoring, and yield optimization recommendations.

Agricultural equipment manufacturers are increasingly collaborating with software firms, agritech startups, and cloud infrastructure providers to build fully integrated connected farming ecosystems.

Government-supported smart agriculture programs, digital farming incentives, and sustainability-focused agricultural modernization initiatives are accelerating technology deployment globally.

Large commercial farms are currently the primary adopters of advanced agriculture technologies, while small and medium-sized farms are gradually adopting cloud-based and subscription-driven smart farming solutions.

Key Value Chain & Supply Chain Evolution Signals in Global Agriculture Technologies Market

Several transformative trends are reshaping the agriculture technologies ecosystem globally.

First, precision farming adoption is accelerating demand for AI-powered analytics, GPS-guided equipment, and real-time field monitoring systems.

Second, labor shortages across agricultural sectors are increasing investment in autonomous tractors, robotic harvesting systems, and automated crop management technologies.

Third, climate change and water scarcity are driving adoption of smart irrigation systems, predictive weather analytics, and sustainability-focused farming technologies.

Fourth, IoT-enabled connected farming ecosystems are enabling real-time operational visibility, automated resource management, and predictive maintenance capabilities.

Fifth, cloud-based farm management platforms and agricultural data analytics are becoming central to digital agriculture transformation strategies.

Strategic Implications of Value Chain & Supply Chain Evolution in Global Agriculture Technologies Market

Industry leaders such as Deere & Company, AGCO Corporation, Trimble Inc., Bayer AG, CNH Industrial, and Kubota Corporation are strengthening competitive positioning through integrated smart farming ecosystems that combine machinery, AI analytics, automation, and cloud connectivity.

Competitive advantage increasingly depends on precision farming capability, AI-driven analytics performance, autonomous equipment integration, connectivity infrastructure, and scalability across different agricultural environments.

Companies capable of integrating advanced hardware, software, robotics, and predictive analytics into unified agricultural ecosystems are best positioned to capture long-term market opportunities.

Strategic collaboration between agricultural equipment manufacturers, agritech startups, cloud technology providers, and biotechnology companies is becoming increasingly important for ecosystem expansion and innovation acceleration.

Long-term success will increasingly rely on balancing technology affordability, interoperability, data security, scalability, and sustainable agricultural performance across global farming operations.

Global Agriculture Technologies Market Value Chain & Supply Chain Evolution Forward Outlook

Between 2026 and 2033, the agriculture technologies value chain is expected to become increasingly autonomous, AI-driven, cloud-connected, and sustainability-focused.

Manufacturers will increasingly prioritize autonomous machinery development, AI-powered predictive farming systems, robotic harvesting technologies, and climate-resilient smart agriculture solutions.

Connected farming ecosystems integrating drones, IoT sensors, edge computing, satellite imaging, and real-time analytics will continue transforming agricultural productivity and operational decision-making.

Digital twin farming models, blockchain-enabled agricultural traceability systems, and AI-powered supply chain optimization platforms are expected to play a growing role across future agriculture ecosystems.

Vertical farming systems, indoor agriculture technologies, and precision-controlled environment farming are expected to expand rapidly as food security and sustainability priorities intensify globally.

Ultimately, the future agriculture technologies value chain will evolve from traditional mechanized farming into intelligent, fully connected, data-driven agricultural ecosystems.

Market-Specific Value Chain

- Core Technology & Component Supply: Sensors, semiconductors, GPS systems, drone components, AI processors, biotechnology inputs, connectivity modules

- Digital Infrastructure & Software Development: AI analytics platforms, cloud computing systems, farm management software, machine learning models, satellite imaging platforms

- Agricultural Equipment & System Manufacturing: Smart tractors, autonomous machinery, robotic harvesters, precision irrigation systems, connected farming equipment

- Integrated Smart Farming Deployment: Precision farming systems, IoT-enabled monitoring, autonomous field operations, climate monitoring integration

- Farm Operations & Data Optimization: Yield prediction, resource optimization, predictive maintenance, crop health analytics, automated farm management

- Supply Chain & Sustainability Management: Agricultural logistics optimization, blockchain traceability, sustainability tracking, food supply analytics

Company-to-Stage Mapping

- Core Technology & Component Supply: Trimble Inc., semiconductor suppliers, drone technology providers, IoT sensor manufacturers

- Digital Infrastructure & Software Development: Microsoft, IBM Corporation, Bayer AG (Climate Corporation), agritech software startups

- Agricultural Equipment & System Manufacturing: Deere & Company, AGCO Corporation, CNH Industrial, Kubota Corporation

- Integrated Smart Farming Deployment: Deere & Company, Trimble Inc., AGCO Corporation, precision agriculture service providers

- Farm Operations & Data Optimization: Bayer AG, Corteva Agriscience, Syngenta, digital agriculture platform providers

- Supply Chain & Sustainability Management: Agribusiness companies, food supply chain technology providers, blockchain agriculture startups

Investment Activity

Global Agriculture Technologies Market Investment & Funding Dynamics Overview

Investment and funding dynamics in the Global Agriculture Technologies Market are being driven by increasing global food demand, rising pressure for sustainable farming practices, and rapid digital transformation across agricultural ecosystems. Between 2026 and 2033, capital allocation is expected to accelerate toward precision farming platforms, AI-powered farm analytics, autonomous agricultural machinery, smart irrigation systems, and connected IoT-enabled farming infrastructure.

The market is highly innovation-driven, requiring continuous investment in artificial intelligence, robotics, satellite imaging, agricultural drones, predictive analytics, and cloud-based farm management systems. Major companies such as Deere & Company, AGCO Corporation, Trimble Inc., Bayer AG, CNH Industrial, and Kubota Corporation are significantly increasing investments in smart farming technologies and integrated digital agriculture ecosystems.

A major structural shift influencing investment flows is the global transition from traditional farming toward data-driven and climate-resilient agriculture. This transformation is accelerating funding into automation technologies, autonomous farm equipment, regenerative farming systems, and resource-efficient agricultural solutions designed to improve productivity while reducing environmental impact.

Global Agriculture Technologies Market Investment & Funding Dynamics Current Scenario

Currently, investment activity is strongly supported by rising agritech venture capital funding, government-backed digital agriculture initiatives, and increasing adoption of precision farming technologies among commercial farms and agribusinesses. Strategic collaborations between technology companies, agricultural equipment manufacturers, and research institutions are becoming increasingly important for accelerating innovation and market expansion.

- North America: Leads global investment activity due to strong adoption of precision agriculture, advanced farm mechanization, and significant agritech startup funding across the United States and Canada.

- Europe: Witnessing strong investments driven by sustainability-focused agricultural policies, climate-smart farming initiatives, and increasing adoption of digital farming technologies.

- Asia-Pacific: Fastest-growing investment region supported by agricultural modernization programs, rising food demand, and expanding smart farming initiatives in China, India, Japan, and Southeast Asia.

- Latin America & Middle East & Africa: Emerging investment regions driven by increasing precision farming adoption, water management technologies, and growing focus on food security and agricultural productivity.

Key Investment & Funding Dynamics Signals in Global Agriculture Technologies Market

- Rapid adoption of precision farming technologies is increasing investment in GPS-enabled systems, drones, soil monitoring sensors, and AI-driven farm analytics platforms.

- Growing labor shortages across agricultural sectors are accelerating capital inflows into agricultural robotics, autonomous tractors, and automated harvesting systems.

- Climate change and water scarcity concerns are driving investments into smart irrigation technologies, climate-monitoring systems, and sustainable farming infrastructure.

- Expansion of connected farming ecosystems is encouraging funding into IoT-enabled farm equipment, cloud-based farm management software, and real-time predictive analytics solutions.

- Increasing venture capital activity in agritech startups is supporting innovation in vertical farming, regenerative agriculture, AI-powered crop monitoring, and blockchain-based agricultural supply chains.

Strategic Implications of Investment & Funding Dynamics in Global Agriculture Technologies Market

- The investment landscape strongly favors companies capable of integrating AI, IoT, automation, and analytics into scalable smart farming ecosystems.

- Strategic partnerships between agritech firms, agricultural equipment manufacturers, cloud technology providers, and governments are becoming critical for market expansion and technology commercialization.

- Technological innovation is emerging as the primary competitive differentiator, particularly in autonomous machinery, predictive analytics, and precision resource optimization.

- Regional diversification remains essential, with North America leading technological innovation, Europe focusing on sustainable agriculture, and Asia-Pacific driving large-scale adoption and agricultural modernization.

- High initial implementation costs and digital infrastructure limitations in developing regions continue to create barriers, encouraging investments in affordable and scalable smart farming solutions.

Global Agriculture Technologies Market Investment & Funding Dynamics Forward Outlook

Looking ahead, the Global Agriculture Technologies Market is expected to attract strong and sustained investment as global agriculture increasingly shifts toward automation, sustainability, and data-driven farming systems.

Future capital allocation will prioritize AI-powered precision agriculture, autonomous farming equipment, vertical farming systems, smart irrigation technologies, and climate-resilient agricultural infrastructure.

- North America: Will continue leading innovation in autonomous farming systems and AI-driven agricultural analytics.

- Europe: Will remain a major hub for sustainable agriculture technologies and climate-smart farming investments.

- Asia-Pacific: Will witness the fastest investment growth due to large-scale agricultural modernization and rising food security initiatives.

Digital transformation will further reshape investment patterns, with increasing focus on connected farming ecosystems, blockchain-enabled supply chains, remote farm monitoring, and predictive crop intelligence platforms.

Overall, the market is expected to maintain a strong long-term growth trajectory supported by rising food demand, sustainability requirements, and rapid technological innovation. Companies that successfully combine automation, precision analytics, and sustainable farming solutions will be best positioned to lead the Global Agriculture Technologies Market through 2033.

Technology & Innovation

Global Agriculture Technologies Market Technology & Innovation Landscape Overview

The technology and innovation landscape of the Global Agriculture Technologies Market is rapidly transforming agriculture into a digitally connected, automated, and intelligence-driven ecosystem. Innovation across the market is focused on integrating precision farming, artificial intelligence, IoT-enabled equipment, robotics, drones, remote sensing, biotechnology, and advanced analytics into modern agricultural operations.

Agriculture technologies are increasingly being deployed across the full farming value chain, including soil preparation, planting, irrigation management, crop monitoring, harvesting, storage, and supply chain optimization. These innovations are helping farmers improve productivity, reduce operational costs, optimize resource utilization, and strengthen climate resilience.

A major technology shift within the market is the expansion of precision agriculture systems that utilize real-time field analytics, GPS-enabled machinery, satellite imaging, and AI-based decision support platforms. These technologies enable site-specific farming practices that maximize yields while reducing environmental impact.

The market is also witnessing strong adoption of connected farming ecosystems where IoT sensors, cloud computing platforms, and predictive analytics work together to provide continuous operational visibility across farms. These systems improve irrigation efficiency, fertilizer management, weather forecasting, and disease monitoring capabilities.

In addition, advancements in autonomous agricultural machinery and robotics are reshaping labor-intensive farming operations. Autonomous tractors, robotic harvesters, AI-powered spraying systems, and automated greenhouse technologies are significantly improving efficiency and scalability in commercial farming.

Global Agriculture Technologies Market Technology & Innovation Landscape Current Scenario

Currently, the agriculture technologies market is experiencing accelerated digital transformation as governments, agribusinesses, and farmers increasingly invest in smart farming infrastructure. Precision agriculture and connected farming systems are becoming mainstream across large-scale commercial farming operations.

AI-powered predictive analytics platforms are being widely used for crop forecasting, irrigation optimization, pest management, and yield monitoring. Machine learning algorithms analyze large agricultural datasets to generate real-time insights that support data-driven farming decisions.

IoT-enabled agricultural systems are increasingly deployed to monitor soil moisture, weather conditions, crop health, greenhouse environments, and livestock performance. These systems provide real-time farm intelligence and enable automated control of irrigation and nutrient delivery systems.

Agricultural drones equipped with multispectral imaging technologies are widely used for field mapping, crop scouting, aerial spraying, and vegetation analysis. Drone analytics improve precision farming efficiency while reducing labor and chemical application costs.

Cloud-based farm management platforms are emerging as a critical component of digital agriculture ecosystems. These platforms integrate operational data from multiple farm sources and provide centralized dashboards for monitoring productivity, equipment performance, and resource consumption.

Controlled environment agriculture technologies such as vertical farming, hydroponics, and automated greenhouse systems are also gaining momentum as demand for sustainable and year-round crop production increases globally.

Key Technology & Innovation Trends in Global Agriculture Technologies Market

- Precision Agriculture Systems: GPS-guided equipment, field analytics, and variable-rate technologies improving productivity and resource efficiency.

- AI-Powered Farm Analytics: Machine learning platforms enabling predictive crop management, yield forecasting, and disease detection.

- IoT-Connected Smart Farming: Real-time monitoring of soil, weather, irrigation, and crop conditions through connected sensor ecosystems.

- Autonomous Agricultural Machinery: AI-enabled tractors, robotic harvesters, and automated spraying systems reducing labor dependency.

- Agricultural Drone Technologies: Drone-based crop monitoring, aerial imaging, spraying, and precision field analysis applications.

- Cloud-Based Farm Management Platforms: Centralized digital platforms improving operational visibility and farm coordination.

- Vertical Farming & Controlled Environment Agriculture: Indoor farming technologies enabling year-round sustainable food production.

- Biotechnology & Gene Editing: Development of climate-resilient and disease-resistant crop varieties using advanced biological technologies.

- Smart Irrigation Technologies: Automated irrigation systems optimizing water usage and improving sustainability.

- Blockchain in Agricultural Supply Chains: Enhanced traceability, food safety, and transparency across global agricultural distribution networks.

Strategic Implications of Technology & Innovation

Technology innovation is fundamentally reshaping global agricultural systems by enabling higher productivity, improved sustainability, and more efficient resource management. Digital transformation in agriculture is becoming increasingly essential for addressing rising food demand and environmental challenges.

For agribusinesses and commercial farms, adoption of integrated smart farming ecosystems is becoming a key competitive advantage. Companies leveraging AI, IoT, robotics, and predictive analytics are improving operational efficiency, reducing input costs, and increasing crop yields.

The integration of climate-smart farming technologies is also strengthening agricultural resilience against unpredictable weather patterns, water scarcity, and soil degradation. Smart irrigation systems, weather analytics, and precision nutrient management are helping farmers adapt to changing environmental conditions.

However, challenges such as high technology implementation costs, limited rural digital infrastructure, and lack of technical expertise among small-scale farmers continue to restrict widespread adoption in certain regions.

Global Agriculture Technologies Market Technology & Innovation Forward Outlook

Looking ahead, the agriculture technologies market is expected to evolve toward highly autonomous and fully connected farming ecosystems where AI-driven systems manage end-to-end agricultural operations with minimal human intervention.

The convergence of artificial intelligence, robotics, IoT, edge computing, and 5G connectivity will significantly enhance real-time farm automation and operational intelligence. These technologies will enable faster decision-making, predictive farm management, and highly efficient agricultural workflows.

Advanced robotics and autonomous farming systems are expected to become increasingly common across large-scale farming operations, particularly in harvesting, planting, spraying, and greenhouse management applications.

Digital twin technology for agriculture is also anticipated to gain traction, allowing farmers to create virtual farm models for simulating crop performance, irrigation strategies, environmental impact, and operational planning before real-world implementation.

In addition, sustainability-focused innovation will continue driving growth in precision irrigation, regenerative agriculture, vertical farming, and climate-resilient crop development technologies.

In conclusion, the Global Agriculture Technologies Market is undergoing a major technological transformation as agriculture becomes increasingly automated, connected, and intelligence-driven. Companies that successfully integrate advanced analytics, automation, AI, and sustainable farming technologies will lead the future evolution of global agriculture.

Market Risk

Global Agriculture Technologies Market Risk Factors & Disruption Threats Overview

The Global Agriculture Technologies Market is undergoing rapid transformation as digitalization, automation, and precision farming systems reshape traditional agricultural operations worldwide. While the market presents strong long-term growth potential, it carries a moderate-to-high operational and technology adoption risk profile due to infrastructure limitations, cybersecurity vulnerabilities, climate uncertainty, high implementation costs, and fragmented global agricultural ecosystems.

One of the primary risk factors is uneven technological adoption across farming communities. Large commercial farms are rapidly integrating advanced technologies, while small and medium-scale farmers often face financial, technical, and infrastructure barriers that limit widespread deployment of smart farming systems.

Another major disruption factor is dependence on digital infrastructure and connected ecosystems. Agriculture technologies increasingly rely on cloud platforms, IoT networks, satellite connectivity, and real-time analytics, making operations vulnerable to connectivity disruptions, cyber threats, and data reliability issues.

Climate variability and unpredictable weather conditions also pose significant risks, as changing environmental patterns can reduce the effectiveness of predictive farming models, crop analytics systems, and automated irrigation planning.

Additionally, rising competition among agritech companies, rapid technological obsolescence, and integration complexity across different farming systems are accelerating market disruption and increasing operational uncertainty for technology providers and end users.

Global Agriculture Technologies Market Risk Factors & Disruption Threats Current Scenario

The current market environment reflects strong investment momentum in precision agriculture, farm automation, AI-driven analytics, and connected farming ecosystems. Governments and private investors are actively supporting smart farming initiatives to improve food security and agricultural productivity.

However, high upfront costs associated with drones, robotics, autonomous machinery, and digital infrastructure continue to restrict adoption among cost-sensitive farming operations, particularly in developing regions.

Data interoperability challenges remain a key issue, as many agricultural systems operate on fragmented software platforms that lack standardized integration capabilities, limiting seamless farm management and analytics optimization.

The market is also facing growing concerns regarding agricultural data ownership, privacy, and vendor dependency, as farmers become increasingly reliant on proprietary cloud-based farming ecosystems managed by large technology providers.

At the same time, supply chain disruptions affecting semiconductors, sensors, batteries, and electronic components are impacting production timelines and increasing equipment costs across the agriculture technology sector.

Key Risk Factors & Disruption Threats Signals in Global Agriculture Technologies Market

A major disruption signal is the rapid expansion of AI-powered autonomous farming systems, which are transforming traditional agricultural labor structures and accelerating demand for robotics and self-operating machinery.

Increasing cybersecurity risks targeting connected farm equipment, cloud platforms, and IoT-based agricultural networks are emerging as a critical threat to operational continuity and data security.

The widening digital divide between technologically advanced commercial farms and resource-constrained smallholder farmers is creating unequal productivity gains and fragmented adoption rates across regions.

Climate change and environmental volatility are also disrupting predictive farming models by introducing greater uncertainty in weather forecasting, water availability, and crop disease management systems.

Additionally, regulatory developments related to AI governance, drone operations, agricultural data usage, and sustainability compliance are creating evolving operational requirements for agritech companies worldwide.

Strategic Implications of Risk Factors & Disruption Threats in Global Agriculture Technologies Market

Market participants must prioritize development of scalable and cost-efficient technologies that can support adoption across both large commercial farms and smaller agricultural operations.

Investment in interoperable digital ecosystems, edge computing solutions, and secure cloud infrastructure will become essential to improve system reliability and enable seamless integration across agricultural technologies.

Companies should strengthen cybersecurity frameworks and data governance capabilities to address rising concerns regarding farm data privacy, operational resilience, and digital infrastructure protection.

Strategic collaboration between agritech firms, telecom providers, governments, and agricultural cooperatives will be critical for expanding rural connectivity and supporting broader smart farming adoption.

Focus on climate-resilient agriculture technologies, including predictive weather analytics, water optimization systems, and AI-driven crop management tools, will become increasingly important in mitigating environmental risks.

Global Agriculture Technologies Market Risk Factors & Disruption Threats Forward Outlook

Looking ahead to 2026???2033, the Agriculture Technologies Market is expected to transition toward highly automated, AI-driven, and sustainability-focused farming ecosystems. However, market growth will remain closely tied to infrastructure development, affordability, and regulatory evolution.

Autonomous machinery, precision farming systems, digital twins, and robotics integration are expected to become central components of large-scale agricultural operations, significantly improving productivity and resource efficiency.

At the same time, adoption disparities between developed and emerging agricultural economies may continue to create uneven market penetration and competitive fragmentation.

Cybersecurity, data ownership, and AI governance regulations are likely to become more prominent as agriculture becomes increasingly dependent on connected digital infrastructure and automated decision-making systems.

Overall, while the market offers substantial long-term opportunities, sustainable competitive advantage will depend on balancing innovation, accessibility, operational resilience, and environmental sustainability within an increasingly technology-driven global agricultural landscape.

Regulatory Landscape

Global Agriculture Technologies Market Regulatory & Policy Environment Overview

The regulatory and policy environment for the Global Agriculture Technologies Market is evolving rapidly as governments, agricultural agencies, and international organizations prioritize food security, sustainable farming, climate resilience, and digital transformation across agricultural systems. Agriculture technologies such as precision farming, AI-powered analytics, drones, autonomous machinery, IoT-enabled monitoring systems, and biotechnology solutions are increasingly becoming central to modern agricultural development strategies worldwide.

Governments and regulatory bodies are implementing frameworks related to smart farming technologies, agricultural data governance, drone operations, environmental sustainability, water management, and food traceability. Policies supporting precision agriculture, digital farming infrastructure, and climate-smart agriculture are significantly influencing investment and adoption patterns across the sector.

In addition, rising concerns over greenhouse gas emissions, soil degradation, pesticide overuse, and water scarcity are encouraging stricter environmental regulations and sustainable farming mandates. These regulations are driving demand for technologies that optimize fertilizer use, improve irrigation efficiency, reduce waste, and support regenerative agricultural practices.

The market is also being shaped by increasing government subsidies, rural digitalization programs, agritech startup funding initiatives, and smart agriculture incentives. However, regulatory fragmentation across regions regarding agricultural drones, AI usage, biotechnology approvals, and digital farm data ownership continues to create operational and compliance challenges for technology providers and agribusiness companies.

Global Agriculture Technologies Market Regulatory & Policy Environment Current Scenario

The current regulatory landscape is characterized by increasing policy support for sustainable agriculture, digital farming transformation, and climate-resilient food production systems. North America remains a major innovation hub supported by precision agriculture incentives, agricultural automation policies, and research funding for AI-enabled farming technologies.

Europe is strengthening its regulatory framework through sustainability-focused agricultural policies under the European Green Deal and Common Agricultural Policy (CAP). Regulations related to pesticide reduction, carbon emissions, traceability, and environmental compliance are accelerating adoption of precision farming technologies and smart irrigation systems across the region.

Asia-Pacific is witnessing rapid regulatory expansion driven by rising food demand, agricultural modernization programs, and digital farming investments. Countries such as China, India, Japan, and Australia are introducing policies supporting smart agriculture, drone usage in farming, AI-based crop monitoring, and agricultural mechanization initiatives.

In Latin America, governments are increasingly supporting precision farming and agricultural export modernization through technology adoption programs and digital infrastructure investments. Meanwhile, Middle East & Africa nations are focusing on controlled environment agriculture, water-efficient farming technologies, and food security strategies to address climate-related agricultural challenges.

Across all major regions, policymakers are increasingly emphasizing sustainable food production, agricultural efficiency, and climate adaptation, creating strong long-term demand for advanced agriculture technologies and digital farming ecosystems.

Key Regulatory & Policy Environment Signals in Global Agriculture Technologies Market

- Precision Agriculture & Smart Farming Policies: Governments are promoting AI-enabled farming, GPS-guided machinery, and data-driven agriculture through subsidies and modernization programs.

- Environmental Sustainability Regulations: Policies focused on reducing fertilizer usage, water waste, pesticide emissions, and soil degradation are accelerating adoption of sustainable agriculture technologies.

- Agricultural Drone & Autonomous Equipment Regulations: Regulatory frameworks governing drone operations, autonomous tractors, and robotic farming systems are shaping market deployment strategies.

- Agricultural Data Governance & Cybersecurity: Growing concerns over farm data ownership, cloud security, and digital privacy are driving new governance standards for connected farming ecosystems.

- Climate-Smart Agriculture Initiatives: Governments and international organizations are promoting technologies that improve climate resilience, carbon efficiency, and resource optimization in agriculture.

- Biotechnology & Gene-Editing Policies: Evolving regulations surrounding genetically modified crops, CRISPR technologies, and agricultural biotechnology are influencing innovation and commercialization strategies.

Strategic Implications of Regulatory & Policy Environment in Global Agriculture Technologies Market

Regulatory developments are transforming the agriculture technologies market from a productivity-focused sector into a sustainability-driven and compliance-oriented ecosystem. Companies must increasingly align their technologies with environmental regulations, carbon reduction targets, and resource efficiency standards.

Precision farming technologies are gaining strategic importance as governments encourage optimized use of water, fertilizers, and pesticides to improve sustainability outcomes. This is accelerating investments in AI-powered analytics, remote sensing platforms, and IoT-enabled monitoring systems capable of supporting regulatory compliance and operational transparency.

Drone regulations and autonomous machinery standards are also significantly influencing market expansion. Vendors must ensure compliance with aviation regulations, operational safety standards, and regional certification requirements before deploying automated farming solutions at scale.

Data governance policies are becoming increasingly important as connected farming ecosystems generate large volumes of agricultural data. Agritech companies are expected to strengthen cybersecurity frameworks, cloud infrastructure security, and transparent data ownership models to maintain farmer trust and regulatory compliance.

Meanwhile, climate-focused agricultural policies are encouraging investments in regenerative agriculture technologies, carbon monitoring platforms, and precision irrigation systems. Companies capable of delivering sustainable, scalable, and regulation-compliant smart farming solutions are expected to gain strong competitive advantages in the evolving market landscape.

Global Agriculture Technologies Market Regulatory & Policy Environment Forward Outlook

Between 2026 and 2033, the regulatory environment for the Global Agriculture Technologies Market is expected to become increasingly sustainability-focused, digitally integrated, and innovation-driven as governments strengthen food security and climate resilience strategies.

North America is expected to continue expanding support for AI-enabled farming, autonomous agricultural equipment, and precision agriculture systems through public-private partnerships and agricultural innovation funding programs. Europe will likely remain a global leader in sustainable agriculture regulation, carbon reduction policies, and environmentally compliant farming technologies.

Asia-Pacific is projected to witness rapid policy development supporting smart agriculture infrastructure, agricultural robotics, digital advisory platforms, and drone-based crop monitoring systems. China and India are expected to remain major investment hubs for agricultural modernization initiatives.

Global regulations related to carbon emissions, water efficiency, biodiversity protection, and agricultural traceability are expected to become stricter, increasing demand for advanced analytics platforms and sustainability-focused farming technologies.

AI governance frameworks and digital agriculture standards are also expected to evolve significantly, particularly around algorithm transparency, autonomous machinery safety, and agricultural data management. This will drive further adoption of secure, intelligent, and compliance-ready agriculture technology platforms.

Overall, the regulatory and policy landscape will play a critical role in shaping the future evolution of the Global Agriculture Technologies Market. Companies that proactively align with sustainability goals, climate-smart agriculture initiatives, and digital compliance frameworks will be best positioned to lead the next generation of global agricultural transformation.