Global Thermal Interface Market Report, Size and Forecast 2026-2033

Global Thermal Interface Material Market Report, Size, Share and Forecast 2026–2033

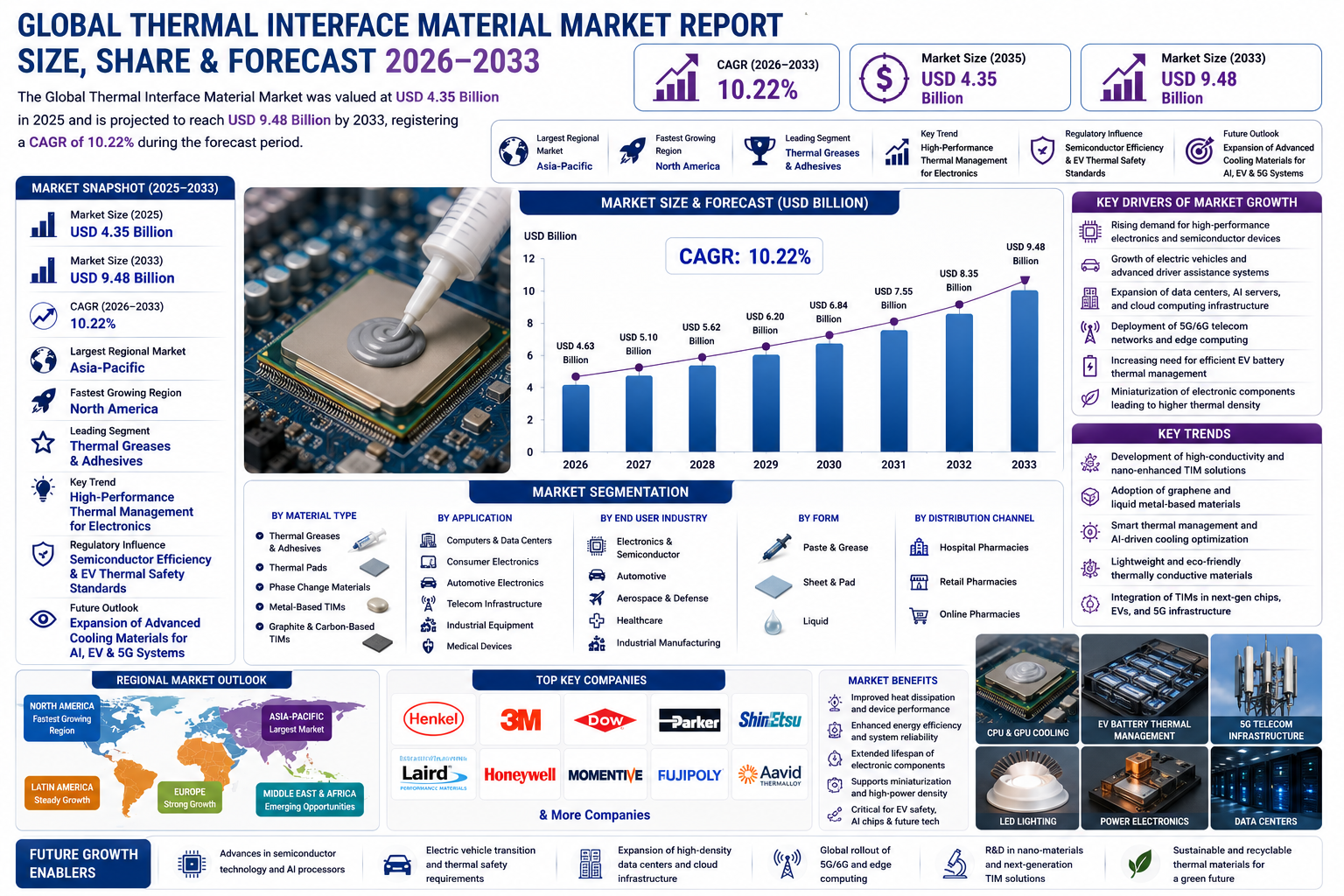

Market Forecast Snapshot (2025–2033)

| Metric | Value |

|---|---|

| Market Size (2025) | USD 4.35 Billion |

| Market Size (2033) | USD 9.48 Billion |

| CAGR (2026–2033) | 10.22% |

| Largest Regional Market | Asia-Pacific |

| Fastest Growing Region | North America |

| Leading Segment | Thermal Greases & Adhesives |

| Key Trend | High-Performance Thermal Management for Electronics |

| Regulatory Influence | Semiconductor Efficiency & EV Thermal Safety Standards |

| Future Outlook | Expansion of Advanced Cooling Materials for AI, EV & 5G Systems |

Market Size & Forecast

The Global Thermal Interface Material (TIM) Market is projected to witness strong growth during the forecast period from 2026 to 2033. The market was valued at USD 4.35 billion in 2025 and is expected to reach approximately USD 9.48 billion by 2033, registering a CAGR of 10.22%. The market growth is primarily driven by increasing demand for efficient heat dissipation solutions across semiconductors, consumer electronics, automotive electronics, data centers, and industrial equipment. As electronic devices become smaller, more powerful, and thermally intensive, advanced thermal interface materials are becoming essential for maintaining performance, reliability, and longevity. The rapid expansion of electric vehicles (EVs), AI-driven computing systems, 5G telecom infrastructure, and high-density power electronics is significantly accelerating market adoption. In addition, increasing investments in battery cooling technologies, high-performance processors, and miniaturized electronics are further contributing to market growth. Manufacturers are increasingly developing high-conductivity, lightweight, and application-specific TIM solutions to meet growing thermal management requirements.Global Thermal Interface Material Market Overview

Thermal Interface Materials (TIMs) are specialized materials used to improve heat transfer between heat-generating components and heat sinks, cooling systems, or other thermal dissipation structures. These materials help reduce thermal resistance and improve energy efficiency in high-performance electronic systems. TIMs are commonly used in semiconductors, CPUs, GPUs, EV battery packs, LED lighting, telecom infrastructure, medical devices, aerospace systems, and industrial machinery. The market is undergoing rapid transformation due to increasing thermal density in advanced electronics, rising EV battery performance requirements, and the growing deployment of cloud computing and data center infrastructure. Manufacturers are focusing on high thermal conductivity, phase stability, dielectric insulation, and lightweight formulations. Materials such as silicone-based greases, phase change materials, gap fillers, thermal pads, graphite sheets, and metal-based compounds are widely utilized. The growing convergence of semiconductor miniaturization, electrification, AI computing, and thermal safety regulations is expected to drive long-term industry growth.Structural Drivers of Market Growth

1. Innovation and Commercialization Acceleration

Rapid advancements in nanomaterials, graphene-based compounds, phase-change technologies, and high-conductivity polymers are significantly accelerating innovation across the TIM market. Manufacturers are introducing advanced thermal pads, liquid metal interfaces, and nano-enhanced greases that deliver improved thermal performance in compact devices.Market Implications

Companies investing in material science innovation, nanotechnology, and application-specific cooling solutions are expected to strengthen competitive positioning.2. Compliance and Risk Repricing

Thermal safety standards in EV batteries, semiconductors, aerospace electronics, and telecom systems are increasing demand for reliable thermal management solutions. Regulatory focus on energy efficiency and overheating prevention is influencing product development. Manufacturers must ensure stability, flame resistance, electrical insulation, and durability under high-temperature operating environments.Market Implications

Companies maintaining compliance with advanced thermal safety standards and performance certifications are likely to gain long-term growth advantages.3. Competitive and Value-Chain Reconfiguration

The TIM market is witnessing increasing strategic partnerships between semiconductor manufacturers, EV battery companies, advanced materials firms, and cooling technology providers. The growing demand for localized semiconductor supply chains and EV manufacturing ecosystems is reshaping production strategies globally.Market Implications

Manufacturers focusing on vertical integration, customized material development, and strategic OEM partnerships are expected to capture larger market share.4. Capital and Capacity Scaling

Investments in semiconductor fabs, EV battery plants, AI data centers, and telecom infrastructure are significantly expanding TIM demand. Companies are scaling production capacity to support high-volume industrial and electronics applications. The growth of edge computing, autonomous vehicles, and power electronics is also accelerating capital deployment.Market Implications

Suppliers investing in scalable advanced material production and next-generation thermal solutions are expected to benefit from sustained demand.Market Segmentation Analysis

By Material Type

1. Thermal Greases & Adhesives

Thermal greases and adhesives dominate the market due to strong conductivity, wide electronics applications, and affordability.2. Thermal Pads

Thermal pads are increasingly used in EV batteries, telecom equipment, and power electronics.3. Phase Change Materials

These materials are gaining popularity for stable thermal transfer under varying temperatures.4. Metal-Based TIMs

Metal-based compounds, including liquid metals, are utilized in high-performance cooling applications.5. Graphite & Carbon-Based TIMs

Graphite sheets and carbon composites are witnessing rapid adoption due to lightweight and superior conductivity benefits.By Application

1. Computers & Data Centers

Servers, GPUs, CPUs, and AI processors represent major TIM demand centers.2. Consumer Electronics

Smartphones, tablets, laptops, and gaming devices require efficient thermal regulation.3. Automotive Electronics

EV battery systems, ADAS modules, and onboard electronics are major growth applications.4. Telecom Infrastructure

5G base stations and networking equipment are increasing demand for thermal pads and advanced cooling compounds.5. Industrial Equipment

Power modules and automation systems require stable heat dissipation materials.6. Medical Devices

Thermal solutions are increasingly used in imaging systems and precision electronic equipment.By End User Industry

1. Electronics & Semiconductor

The semiconductor sector remains the largest end-user due to chip miniaturization and heat density challenges.2. Automotive

EVs and intelligent vehicle systems are driving high-performance thermal management demand.3. Aerospace & Defense

Aerospace electronics require lightweight and high-stability thermal materials.4. Healthcare

Medical equipment increasingly uses advanced cooling solutions.5. Industrial Manufacturing

Automation and power electronics support market growth.By Form

1. Paste & Grease

Most widely used for processors and consumer electronics.2. Sheet & Pad

Widely adopted in EVs, telecom, and industrial systems.3. Liquid

High-performance systems increasingly use liquid TIMs.Regional Market Dynamics

Asia-Pacific

Asia-Pacific dominates the global TIM market due to strong semiconductor manufacturing capacity, consumer electronics production, and EV battery investments in China, Japan, South Korea, and Taiwan.North America

North America represents the fastest-growing region due to expanding AI infrastructure, EV production, data centers, and semiconductor reshoring investments.Europe

Europe continues experiencing strong demand driven by EV manufacturing, industrial automation, and sustainable electronics development.Latin America

Latin America is gradually expanding due to increasing electronics assembly and industrial modernization.Middle East & Africa

The Middle East & Africa region is witnessing emerging demand from telecom expansion and industrial energy applications.Competitive Landscape

The Global Thermal Interface Material Market is moderately consolidated with major advanced material companies focusing on conductivity enhancement, EV thermal solutions, and semiconductor cooling technologies. Key companies operating in the market include:- Henkel

- 3M

- Dow

- Parker Hannifin

- Shin-Etsu Chemical

- Laird Performance Materials

- Honeywell

- Momentive

- Fujipoly

- Aavid Thermalloy

Strategic Outlook

The future of the TIM market will be heavily influenced by semiconductor innovation, EV thermal safety, AI-driven computing infrastructure, and miniaturized electronics. Companies are increasingly investing in graphene-based TIMs, liquid metal cooling solutions, and smart thermal composites. The growing deployment of AI chips, 5G networks, battery storage systems, and autonomous vehicle electronics will significantly increase demand for high-efficiency thermal management solutions. Additionally, lightweight and sustainable thermal materials are expected to become major innovation priorities across electronics and automotive industries.Final Market Perspective

The Global Thermal Interface Material Market is entering a strong growth phase driven by semiconductor expansion, electrification, thermal safety needs, and increasing power density in modern electronics. TIMs are becoming essential components of advanced electronic and energy systems. Manufacturers capable of delivering high-conductivity, lightweight, stable, and application-specific thermal management materials will be best positioned to capitalize on long-term market growth opportunities. The convergence of AI, EVs, 5G, semiconductors, and advanced cooling technologies is expected to redefine the future of the thermal management industry globally.Table of Contents

Table of Contents

1. Executive Summary

1.1 Market Forecast Snapshot (2026–2033)

1.2 Global Thermal Interface Material Market Size & CAGR Analysis

1.3 Largest & Fastest-Growing Segments

1.4 Region-Level Leadership & Growth Trends

1.5 Key Market Drivers

1.6 Competitive Landscape Overview

1.7 Strategic Outlook Through 2033

2. Introduction & Market Overview

2.1 Definition of the Thermal Interface Material Market

2.2 Market Size & Forecast (2026–2033)

2.3 Industry Evolution & Market Development

2.4 Supply Chain & Raw Material Infrastructure

2.5 Impact of Semiconductor, EV & High-Performance Electronics Trends

2.6 Regulatory & Compliance Landscape

2.7 Technology & Innovation Landscape in Thermal Management Materials

3. Research Methodology

3.1 Primary Research

3.2 Secondary Research

3.3 Market Size Estimation Model

3.4 Forecast Assumptions (2026–2033)

3.5 Data Validation & Triangulation

4. Market Dynamics

4.1 Drivers

4.1.1 Rising Demand for Efficient Heat Dissipation in Electronics

4.1.2 Growth of EV Batteries & Automotive Electronics

4.1.3 Expansion of AI Computing & Data Center Infrastructure

4.1.4 Increasing 5G Telecom & Power Electronics Deployment

4.1.5 Advancements in High-Conductivity Thermal Materials

4.2 Restraints

4.2.1 High Cost of Advanced TIM Materials

4.2.2 Complex Material Integration & Compatibility Issues

4.2.3 Raw Material Volatility & Supply Chain Constraints

4.2.4 Limited Performance Stability in Extreme Conditions

4.3 Opportunities

4.3.1 Expansion of Graphene & Nano-Enhanced TIMs

4.3.2 Growth of Semiconductor Miniaturization & AI Chips

4.3.3 Rising Demand for Battery Cooling & Thermal Safety Solutions

4.3.4 Increasing Adoption in Aerospace & Medical Electronics

4.4 Challenges

4.4.1 High R&D Costs for Advanced Thermal Solutions

4.4.2 Regulatory & Thermal Safety Compliance Complexity

4.4.3 OEM Customization & Product Development Pressure

4.4.4 Competitive Pressure from Alternative Cooling Technologies

5. Global Thermal Interface Material Market Analysis (USD Billion), 2026–2033

5.1 Market Size Overview

5.2 CAGR Analysis

5.3 Regional Revenue Distribution

5.4 Segment Revenue Analysis

5.5 Distribution Channel Analysis

5.6 Thermal Performance & Industrial Demand Analysis

6. Market Segmentation (USD Billion), 2026–2033

6.1 By Material Type

6.1.1 Thermal Greases & Adhesives

6.1.1.1 Silicone-Based Thermal Greases

6.1.1.1.1 High-Conductivity Thermal Adhesives

6.1.1.1.1.1 CPU & GPU Cooling Compounds

6.1.1.1.1.2 Power Module Heat Dissipation Materials

6.1.2 Thermal Pads

6.1.2.1 Soft Gap Fillers

6.1.2.1.1 Dielectric Thermal Pads

6.1.2.1.1.1 EV Battery Thermal Insulation Pads

6.1.2.1.1.2 Telecom Cooling Interface Pads

6.1.3 Phase Change Materials

6.1.3.1 Wax-Based Phase Change Materials

6.1.3.1.1 Polymer Phase Change Compounds

6.1.3.1.1.1 High-Temperature Stable TIMs

6.1.3.1.1.2 Semiconductor Cooling Materials

6.1.4 Metal-Based TIMs

6.1.4.1 Liquid Metal Interfaces

6.1.4.1.1 Silver-Based Conductive TIMs

6.1.4.1.1.1 High-Performance Processor Cooling Solutions

6.1.4.1.1.2 Aerospace Heat Transfer Interfaces

6.1.5 Graphite & Carbon-Based TIMs

6.1.5.1 Graphite Sheets

6.1.5.1.1 Carbon Composite TIMs

6.1.5.1.1.1 Lightweight Thermal Conductivity Solutions

6.1.5.1.1.2 AI Processor Heat Spreading Systems

6.2 By Application

6.2.1 Computers & Data Centers

6.2.1.1 CPUs & GPUs

6.2.1.1.1 AI Processing Units

6.2.1.1.1.1 High-Density Server Cooling Systems

6.2.1.1.1.2 Cloud Infrastructure Heat Dissipation Solutions

6.2.2 Consumer Electronics

6.2.2.1 Smartphones & Tablets

6.2.2.1.1 Laptops & Gaming Devices

6.2.2.1.1.1 Compact Device Cooling Materials

6.2.2.1.1.2 Wearable Electronics Heat Interfaces

6.2.3 Automotive Electronics

6.2.3.1 EV Battery Systems

6.2.3.1.1 ADAS & Power Modules

6.2.3.1.1.1 EV Thermal Safety Solutions

6.2.3.1.1.2 Vehicle Control Unit Heat Management Systems

6.2.4 Telecom Infrastructure

6.2.4.1 5G Base Stations

6.2.4.1.1 Networking Equipment

6.2.4.1.1.1 Telecom Power Electronics Cooling Systems

6.2.4.1.1.2 High-Frequency Signal Heat Management Solutions

6.2.5 Industrial Equipment

6.2.5.1 Automation Systems

6.2.5.1.1 Power Electronics Modules

6.2.5.1.1.1 Heavy Machinery Thermal Interfaces

6.2.5.1.1.2 Industrial Heat Dissipation Materials

6.2.6 Medical Devices

6.2.6.1 Diagnostic Imaging Equipment

6.2.6.1.1 Precision Monitoring Devices

6.2.6.1.1.1 Surgical Electronics Cooling Systems

6.2.6.1.1.2 Portable Medical Heat Control Materials

6.3 By End User Industry

6.3.1 Electronics & Semiconductor

6.3.1.1 Chip Manufacturing

6.3.1.1.1 Advanced Processor Thermal Control

6.3.1.1.1.1 High-Density Semiconductor Cooling Solutions

6.3.1.1.1.2 Wafer-Level Thermal Management Systems

6.3.2 Automotive

6.3.2.1 EV Manufacturers

6.3.2.1.1 Smart Vehicle Electronics

6.3.2.1.1.1 Battery Pack Heat Dissipation Systems

6.3.2.1.1.2 Autonomous Vehicle Thermal Solutions

6.3.3 Aerospace & Defense

6.3.3.1 Aerospace Electronics

6.3.3.1.1 Defense Communication Systems

6.3.3.1.1.1 Lightweight Thermal Stability Solutions

6.3.3.1.1.2 Military Power Electronics Cooling Systems

6.3.4 Healthcare

6.3.4.1 Diagnostic Equipment Manufacturers

6.3.4.1.1 Medical Electronics Suppliers

6.3.4.1.1.1 High-Precision Cooling Materials

6.3.4.1.1.2 Clinical Electronics Thermal Interfaces

6.3.5 Industrial Manufacturing

6.3.5.1 Robotics & Automation Systems

6.3.5.1.1 Power Conversion Equipment

6.3.5.1.1.1 Factory Thermal Efficiency Solutions

6.3.5.1.1.2 High-Load Machinery Cooling Materials

6.4 By Form

6.4.1 Paste & Grease

6.4.1.1 Processor Cooling Paste

6.4.1.1.1 Electronics Heat Transfer Greases

6.4.1.1.1.1 Consumer Electronics Cooling Applications

6.4.1.1.1.2 Semiconductor Thermal Paste Solutions

6.4.2 Sheet & Pad

6.4.2.1 Gap Filler Sheets

6.4.2.1.1 Flexible Thermal Pads

6.4.2.1.1.1 Battery Cooling Sheet Materials

6.4.2.1.1.2 Industrial Heat Shielding Pads

6.4.3 Liquid

6.4.3.1 Liquid Metal TIMs

6.4.3.1.1 Advanced Cooling Fluids

6.4.3.1.1.1 High-Performance Processor Cooling Liquids

6.4.3.1.1.2 AI & HPC Thermal Interface Fluids

7. Market Segmentation by Geography

7.1 North America

7.2 Europe

7.3 Asia-Pacific

7.4 Latin America

7.5 Middle East & Africa

8. Competitive Landscape

8.1 Market Share Analysis

8.2 Product Portfolio Benchmarking

8.3 Product Positioning Mapping

8.4 Strategic Partnerships & OEM Supply Agreements

8.5 Competitive Intensity & Market Consolidation

9. Company Profiles

9.1 Henkel

9.2 3M

9.3 Dow

9.4 Parker Hannifin

9.5 Shin-Etsu Chemical

9.6 Laird Performance Materials

9.7 Honeywell

9.8 Momentive

9.9 Fujipoly

9.10 Aavid Thermalloy

10. Strategic Intelligence & Pheonix AI Insights

10.1 Pheonix Demand Forecast Engine

10.2 Semiconductor & Thermal Infrastructure Analyzer

10.3 Material Science Innovation Tracker

10.4 Product Development & Thermal Safety Insights

10.5 Automated Porter’s Five Forces Analysis

11. Future Outlook & Strategic Recommendations

11.1 Expansion of AI & High-Density Computing Cooling Solutions

11.2 EV Battery Thermal Safety & Innovation Strategies

11.3 Graphene & Nano-TIM Product Development Strategies

11.4 OEM Partnership & Supply Chain Expansion Strategies

11.5 Long-Term Market Outlook (2033+)

12. Appendix

13. About Pheonix Research

14. Disclaimer

Competitive Landscape

Global Thermal Interface Material Market Competitive Intensity & Market Structure Overview

The Global Thermal Interface Material (TIM) Market is characterized by a moderately consolidated competitive structure, driven by strong participation from advanced material manufacturers, specialty chemical companies, and thermal management solution providers. Competition is centered around high thermal conductivity, material innovation, EV battery cooling, semiconductor heat dissipation, and high-performance electronics applications.

The market is shaped by established players such as Henkel, 3M, Dow, Parker Hannifin, Shin-Etsu Chemical, Honeywell, and Fujipoly, which compete through product innovation, customized formulations, OEM partnerships, and advanced thermal engineering capabilities.

Growing demand from AI processors, EV battery systems, 5G telecom infrastructure, consumer electronics, and semiconductor packaging is intensifying competition globally. Companies are increasingly focusing on graphene-based TIMs, liquid metal interfaces, lightweight composites, and high-durability phase-change materials to strengthen market positioning.

Global Thermal Interface Material Market Competitive Landscape

Leading Company Profiles

- Henkel – Major supplier of thermal adhesives, gap fillers, and advanced thermal compounds for automotive, electronics, and industrial applications.

- 3M – Strong presence in thermal pads, tapes, and advanced heat transfer materials for electronics and telecom sectors.

- Dow – Key manufacturer of silicone-based TIM solutions for semiconductors, EVs, and industrial systems.

- Parker Hannifin – Specialized in engineered thermal management materials and cooling solutions.

- Shin-Etsu Chemical – Leading supplier of high-performance silicone greases and semiconductor thermal interface materials.

- Laird Performance Materials – Focused on EMI shielding and thermal management materials for electronics.

- Honeywell – Active in advanced thermal solutions for aerospace, electronics, and industrial systems.

- Momentive – Strong player in silicone-based thermal conductivity materials and specialty engineered compounds.

- Fujipoly – Known for ultra-soft thermal pads and gap fillers used in high-density electronics.

- Aavid Thermalloy – Focused on heat sinks, thermal compounds, and cooling technologies for power electronics.

Key Competitive Intensity Signals

- Rising demand for high-performance cooling solutions in semiconductors, GPUs, and AI chips is increasing R&D competition.

- Growth in EV battery thermal safety systems and power electronics is strengthening OEM-driven partnerships.

- Companies are investing heavily in graphite, nano-enhanced, and liquid metal TIM technologies for next-generation applications.

- Supply chain localization in semiconductors and EV manufacturing is reshaping regional production strategies.

- Product differentiation is increasingly based on thermal conductivity, dielectric strength, durability, flame resistance, and lightweight properties.

- Strategic acquisitions and cross-industry collaborations are improving innovation speed and market penetration.

Strategic Implications

- Material science innovation remains the core differentiator in long-term competitive positioning.

- Companies with strong semiconductor and EV OEM partnerships are expected to gain stronger market share.

- Expansion into AI data centers and 5G infrastructure creates high-growth opportunities.

- Regulatory compliance in thermal safety and electrical insulation is becoming a major entry barrier.

- Sustainable and lightweight thermal materials will increasingly influence procurement preferences.

Forward Outlook

The TIM market is expected to remain moderately consolidated with rising competitive intensity, driven by advanced electronics miniaturization, EV expansion, and AI computing infrastructure.

Future competition will increasingly center on:

- Graphene and nano-material-based TIM innovation

- Liquid metal and phase-change cooling technologies

- EV battery thermal safety solutions

- Semiconductor packaging and AI processor heat management

- Sustainable and lightweight thermal composites

- High-volume OEM supply partnerships

- Localized advanced material manufacturing capacity

The convergence of AI, EVs, semiconductors, 5G, and power-dense electronics will continue redefining the competitive structure of the global TIM market.

Value Chain

Global Thermal Interface Material (TIM) Market Value Chain & Supply Chain Evolution Overview

The Global Thermal Interface Material (TIM) Market is undergoing rapid transformation driven by semiconductor miniaturization, EV electrification, AI-driven computing expansion, and advanced thermal safety requirements. The market’s value chain is characterized by a hybrid operational model supported by integrated raw material sourcing, specialty material processing, OEM partnerships, and industrial distribution ecosystems.

A defining feature of this value chain is its dependence on advanced material science, thermal conductivity engineering, and precision manufacturing processes. As electronics, EV batteries, telecom systems, and data centers become more thermally intensive, TIM manufacturers are increasingly focusing on customized formulations, nanomaterials, and high-efficiency cooling compounds.

Supply chain complexity is high due to specialty raw material sourcing, semiconductor-linked demand cycles, thermal compliance requirements, precision formulation processes, and integration with high-performance industrial applications. Global supply volatility in silicones, graphite, metals, and engineered polymers also impacts operational resilience.

Manufacturers are investing heavily in nanotechnology, graphene composites, phase-change materials, localized production facilities, and strategic OEM collaborations to improve thermal efficiency, scalability, and market responsiveness. The market is evolving into a highly specialized advanced materials ecosystem aligned with electronics innovation and electrification trends.

Global Thermal Interface Material Market Value Chain & Supply Chain Evolution Current Scenario

Market-Specific Value Chain

1. Raw Material Sourcing & Specialty Inputs

Silicone compounds, graphite, engineered polymers, aluminum, copper, ceramics, phase-change materials, and nano-enhanced conductive additives.

2. Material Engineering & R&D

Thermal conductivity optimization, dielectric insulation development, graphene-based compounds, liquid metal research, and application-specific thermal design.

3. Manufacturing & Formulation

Thermal greases, adhesives, thermal pads, gap fillers, graphite sheets, liquid TIMs, and metal-based compound processing.

4. Quality Testing & Compliance

Thermal resistance validation, flame resistance, dielectric performance testing, EV thermal safety compliance, semiconductor reliability certification, and industrial durability testing.

5. Distribution & Industrial Supply Networks

OEM supply chains, industrial distributors, electronics manufacturers, semiconductor ecosystem partners, automotive supply chains, and direct B2B logistics.

6. End-Use Integration & Application Deployment

Semiconductors, CPUs, GPUs, EV battery systems, AI chips, telecom infrastructure, aerospace electronics, industrial equipment, and medical devices.

Company-to-Stage Mapping

1. Raw Material Sourcing & Specialty Inputs

Chemical suppliers, specialty polymer producers, graphite processors, and engineered metal providers.

2. Material Engineering & R&D

Henkel, 3M, Dow, Shin-Etsu Chemical — thermal material innovation, polymer chemistry, and high-conductivity compound development.

3. Manufacturing & Formulation

Parker Hannifin, Honeywell, Momentive, Fujipoly — advanced TIM formulation, pads, adhesives, and thermal compound production.

4. Quality Testing & Compliance

Thermal testing laboratories, EV certification providers, semiconductor validation systems, and safety compliance bodies.

5. Distribution & Industrial Supply Networks

Industrial distributors, electronics OEMs, EV battery manufacturers, telecom suppliers, and semiconductor equipment partners.

6. End-Use Integration & Application Deployment

Data centers, automotive OEMs, semiconductor fabs, AI infrastructure providers, telecom operators, aerospace manufacturers.

Key Value Chain & Supply Chain Evolution Signals in Global TIM Market

1. Semiconductor & AI Demand Expansion

High-density chips, GPUs, and AI processors are driving demand for ultra-efficient thermal materials.

2. EV Battery Thermal Safety Growth

Battery cooling and thermal stability requirements are increasing adoption of pads, greases, and phase-change TIMs.

3. Shift Toward Advanced Materials

Graphene, nano-composites, liquid metal interfaces, and carbon-based TIMs are reshaping innovation priorities.

4. OEM-Centric Supply Chain Integration

Strategic collaboration with EV, semiconductor, and electronics OEMs is becoming critical.

5. Localization of Advanced Material Production

Regional manufacturing hubs are expanding to reduce geopolitical and supply risks.

6. Thermal Compliance & Reliability Pressure

Performance certification and thermal safety regulations are increasingly influencing product design.

7. Growth of High-Performance Cooling Ecosystems

AI data centers, telecom 5G infrastructure, and autonomous vehicles are expanding long-term TIM demand.

Strategic Implications of Value Chain & Supply Chain Evolution

1. Material Innovation Leadership

Companies must invest in nanomaterials, carbon composites, and application-specific conductivity solutions.

2. Vertical Integration Benefits

Control over specialty inputs and thermal engineering improves cost stability and performance reliability.

3. OEM Partnership Expansion

Long-term EV, semiconductor, and electronics partnerships are becoming major competitive advantages.

4. Capacity Scaling

Higher demand from AI, EVs, and telecom requires scalable advanced material manufacturing.

5. Compliance & Reliability Investment

Thermal safety certifications and long-life stability testing will shape premium market positioning.

6. Regional Production Diversification

Localized facilities reduce logistics disruptions and supply dependency.

7. Sustainable Thermal Materials Development

Eco-friendly, lightweight, and recyclable thermal compounds will become innovation priorities.

Global Thermal Interface Material Market Value Chain & Supply Chain Evolution Forward Outlook

Looking ahead, the Global TIM Market is expected to evolve into a highly specialized, innovation-intensive, and OEM-integrated advanced materials ecosystem.

Key future developments include:

- Expansion of graphene-based and nano-enhanced TIMs.

- Growth of liquid metal cooling solutions for AI & HPC systems.

- Rising integration with EV battery thermal ecosystems.

- Increased semiconductor-linked customized thermal materials.

- Localization of specialty chemical and thermal compound production.

- Smart thermal composites for autonomous vehicles and aerospace.

- Sustainable lightweight cooling materials for next-gen electronics.

In conclusion, the Global Thermal Interface Material Market represents a high-growth, engineering-driven, and technologically advanced materials ecosystem, where thermal innovation, OEM integration, compliance readiness, and specialty supply resilience will define long-term competitive leadership.

Investment Activity

Global Thermal Interface Material Market Investment & Funding Dynamics Overview

The Global Thermal Interface Material (TIM) Market is witnessing strong investment momentum driven by rapid semiconductor expansion, EV battery thermal management demand, and increasing deployment of AI, 5G, and high-performance computing infrastructure. Advanced material manufacturers, semiconductor suppliers, EV ecosystem players, and industrial cooling technology firms are actively investing in next-generation thermal conductivity solutions, lightweight composites, and application-specific heat dissipation materials.

Investment activity is being accelerated by rising thermal density in advanced electronics, battery safety requirements, and the need for energy-efficient cooling systems across automotive, telecom, and data center ecosystems. Growing adoption of graphene-based TIMs, liquid metal interfaces, nano-enhanced compounds, and high-conductivity polymers is further strengthening long-term capital deployment globally.

Additionally, increasing investments in semiconductor fabs, EV battery plants, AI data centers, and telecom infrastructure are expanding demand for scalable and high-performance thermal solutions.

Global Thermal Interface Material Market Investment & Funding Dynamics Current Scenario

Currently, the Global TIM Market demonstrates rising investment activity with high capital intensity due to advanced material R&D, precision manufacturing, and large-scale industrial application requirements. Companies are significantly investing in nanotechnology, polymer engineering, thermal conductivity enhancement, and high-temperature resistant compounds.

Major players are expanding production capacities for thermal greases, thermal pads, phase-change materials, graphite sheets, and liquid metal interfaces to meet growing demand from semiconductors, EVs, and power electronics.

The market is also witnessing selective merger and acquisition activity as material science companies, thermal technology providers, and electronics suppliers pursue strategic acquisitions, partnerships, and technology integration to strengthen product portfolios and regional manufacturing capabilities.

Key Investment & Funding Dynamics Signals in Global Thermal Interface Material Market

Several major investment signals are shaping funding activity:

- Rising investments in semiconductors, EV battery systems, AI processors, and 5G telecom infrastructure are accelerating TIM demand globally.

- Increasing adoption of graphene-based materials, nano-enhanced compounds, liquid metal interfaces, and phase-change materials is driving material science innovation investments.

- Expansion of EV battery cooling systems, data centers, and high-density electronics is increasing demand for scalable thermal solutions.

- Strategic investments in localized semiconductor supply chains and EV manufacturing ecosystems are reshaping production infrastructure.

- Growing partnerships between advanced material firms, OEMs, semiconductor manufacturers, and cooling solution providers are strengthening innovation ecosystems.

- Rising regulatory focus on thermal safety, energy efficiency, and overheating prevention is improving long-term investor confidence.

- Increasing demand for lightweight, stable, and high-conductivity materials is accelerating R&D funding.

Strategic Implications of Investment & Funding Dynamics in Global Thermal Interface Material Market

- Continuous investment in advanced materials, nanotechnology, and high-conductivity thermal solutions is essential for long-term competitiveness.

- High capital intensity requires strong allocation toward R&D labs, production scalability, and industrial certifications.

- Companies capable of delivering customized and application-specific TIM solutions will strengthen market positioning.

- Strategic OEM collaborations with semiconductor, EV, and electronics manufacturers are becoming critical.

- Investment in scalable manufacturing and next-generation cooling materials will improve long-term profitability.

- Compliance with thermal safety and performance standards remains a major strategic focus.

Global Thermal Interface Material Market Investment & Funding Dynamics Forward Outlook

Looking ahead, the Global TIM Market is expected to maintain strong investment growth driven by AI computing, EV electrification, semiconductor miniaturization, and advanced cooling requirements.

Future capital deployment will increasingly focus on graphene TIMs, smart thermal composites, liquid cooling materials, sustainable polymers, and next-generation battery heat dissipation systems. Expanding semiconductor reshoring and AI infrastructure projects will continue creating strong long-term opportunities.

In conclusion, the Global Thermal Interface Material Market represents a high-growth, innovation-driven investment landscape where advanced materials, semiconductor cooling, EV thermal safety, and scalable heat management systems will define future capital strategies.

Technology & Innovation

Global Thermal Interface Material (TIM) Market Technology & Innovation Landscape Overview

The Global Thermal Interface Material (TIM) Market is undergoing rapid technological transformation driven by advancements in material science, nanotechnology, graphene-based compounds, liquid metal cooling systems, phase-change materials, and high-performance thermal composites. The market demonstrates a high innovation intensity level, supported by increasing thermal management requirements across semiconductors, EVs, AI computing, 5G infrastructure, and high-density electronics.

At the center of this transformation are next-generation high-conductivity materials designed to improve heat transfer, reduce thermal resistance, and maintain operational stability under extreme thermal loads. Manufacturers are increasingly developing nano-enhanced greases, advanced thermal pads, liquid TIMs, graphite sheets, and metal-based thermal compounds to support compact and thermally intensive devices.

Nanotechnology and graphene innovation are significantly reshaping the market. Graphene-based TIMs, carbon composites, and nano-particle-enhanced polymers are enabling superior conductivity, lightweight structures, dielectric insulation, and improved thermal stability for advanced electronics and battery systems.

Another major innovation area is phase-change materials (PCMs) and smart thermal composites that adapt to temperature variations and improve heat dissipation efficiency in CPUs, GPUs, AI processors, EV battery packs, and telecom systems.

The market is also seeing rapid adoption of liquid metal interfaces, high-conductivity silicone compounds, and application-specific cooling materials for ultra-high-performance electronics, data centers, and autonomous vehicle systems.

Technological advancements in flame-resistant formulations, electrically insulating compounds, lightweight composites, and sustainable thermal materials are further improving safety, efficiency, and regulatory compliance.

The convergence of semiconductor miniaturization, EV electrification, AI infrastructure expansion, and advanced thermal engineering is fundamentally transforming the future innovation landscape of the TIM industry globally.

Global Thermal Interface Material Market Technology & Innovation Landscape Current Scenario

Currently, the Global TIM Market demonstrates high patent activity and strong commercialization across advanced cooling materials, nanotechnology-enhanced interfaces, and application-specific thermal management solutions.

1. Graphene & Carbon-Based TIM Innovation

Graphene sheets, carbon composites, and nano-enhanced thermal materials are improving conductivity and reducing weight.

2. Liquid Metal & High-Performance Cooling Interfaces

Liquid metal TIMs and advanced conductive fluids are gaining adoption in high-density electronics and AI processors.

3. Nano-Enhanced Greases & Thermal Adhesives

Manufacturers are developing nano-particle-enhanced greases and adhesives for improved thermal transfer and device reliability.

4. Phase-Change & Smart Thermal Materials

Temperature-responsive phase-change materials are improving efficiency across EVs, semiconductors, and telecom systems.

5. High-Conductivity Thermal Pads & Gap Fillers

Thermal pads and gap fillers are expanding rapidly in EV battery systems, 5G infrastructure, and industrial electronics.

6. Sustainable & Flame-Resistant TIM Solutions

Eco-friendly formulations, flame-retardant compounds, and recyclable thermal materials are gaining strategic importance.

Key Technology & Innovation Landscape Signals in Global Thermal Interface Material Market

Several innovation signals are shaping the market:

1. Rapid Expansion of AI & Data Center Cooling Technologies

AI chips, GPUs, and high-performance servers are increasing demand for ultra-efficient thermal materials.

2. Growth of EV Thermal Safety Systems

Battery packs, power electronics, and EV modules are accelerating innovation in thermal safety materials.

3. Increasing Semiconductor Miniaturization

Smaller, high-power chips require advanced heat dissipation and stable thermal interfaces.

4. Rising Adoption of Graphene & Nanotechnology

Next-generation nano-materials are becoming central to premium thermal performance solutions.

5. Expansion of 5G & Telecom Infrastructure

5G base stations and networking systems are increasing demand for thermal pads and cooling composites.

6. Focus on Lightweight & Sustainable Materials

Automotive and electronics manufacturers are prioritizing low-weight, energy-efficient, and eco-friendly TIM solutions.

Strategic Implications of Technology & Innovation Landscape in Global Thermal Interface Material Market

The evolving technology landscape is significantly reshaping competition across the TIM market. Companies are increasingly competing on thermal conductivity, material stability, nanotechnology capabilities, flame resistance, lightweight engineering, and application-specific cooling performance.

Manufacturers investing in graphene innovation, advanced polymers, liquid cooling interfaces, and customized OEM thermal solutions are expected to strengthen long-term market positioning.

Strategic collaborations between semiconductor firms, EV battery manufacturers, cooling technology providers, and advanced materials companies are accelerating commercialization and reshaping supply chains globally.

The growing convergence of AI infrastructure, EV electrification, telecom expansion, semiconductor innovation, and advanced thermal engineering is creating new long-term opportunities for specialized thermal materials.

Additionally, regulatory focus on energy efficiency, EV battery safety, and overheating prevention is pushing companies toward stronger R&D, compliance validation, and high-reliability product development.

Global Thermal Interface Material Market Technology & Innovation Landscape Forward Outlook

Looking ahead to 2026–2033, the Global TIM Market is expected to evolve toward highly advanced, nano-engineered, and AI-driven thermal management ecosystems.

Future technological developments are likely to include:

1. Graphene-Based Ultra-High Conductivity TIMs

Advanced graphene and hybrid carbon materials will significantly improve heat dissipation and device efficiency.

2. Smart Adaptive Thermal Materials

AI-responsive and temperature-adaptive TIMs may optimize thermal performance dynamically.

3. Liquid Metal Cooling Expansion

Liquid metal TIM adoption will increase in AI processors, hyperscale data centers, and high-performance computing.

4. EV Battery Thermal Safety Innovation

Advanced TIMs for battery packs, charging systems, and EV power electronics will become critical.

5. Sustainable & Recyclable Thermal Composites

Eco-friendly, low-carbon, and recyclable thermal materials will gain importance.

6. Semiconductor-Specific Nano TIM Solutions

Customized nano-structured TIMs for advanced chips and 3D packaging technologies will expand rapidly.

7. High-Density Cooling for 5G & AI Systems

Telecom and AI-driven electronics will demand ultra-thin, lightweight, and high-efficiency cooling solutions.

Overall, companies capable of combining material science innovation, nanotechnology, thermal efficiency, EV safety alignment, semiconductor integration, sustainability, and scalable production will be best positioned to lead the future evolution of the Global Thermal Interface Material Market.

Market Risk

Global Thermal Interface Material (TIM) Market Risk & Disruption Analysis

The Global Thermal Interface Material (TIM) Market operates within a moderate-to-high disruption environment, driven by semiconductor innovation cycles, EV battery thermal safety requirements, raw material dependencies, geopolitical semiconductor risks, and rapid advancements in high-performance cooling technologies. While long-term growth fundamentals remain strong due to rising heat-density challenges across electronics, AI infrastructure, EVs, and 5G systems, the market remains exposed to supply volatility, substitution pressure, pricing instability, and evolving performance regulations.

A defining structural characteristic of the market is its close dependency on downstream semiconductor, electronics, automotive, telecom, and industrial manufacturing ecosystems. Since TIM demand is directly linked to chip production, EV battery manufacturing, server infrastructure expansion, and advanced electronics deployment, fluctuations in these industries can significantly impact volume growth and profitability.

The market is also undergoing rapid transformation as next-generation materials such as graphene composites, liquid metals, carbon-based interfaces, phase-change compounds, and nano-enhanced thermal solutions increasingly challenge traditional silicone-based greases and thermal pads. This creates continuous innovation pressure for manufacturers to improve conductivity, stability, safety, and product-specific customization.

Global Thermal Interface Material Market Current Risk Environment

The current market environment is characterized by rising semiconductor demand, expanding electrification, and growing supply chain complexity.

One of the most significant disruption factors involves raw material and specialty chemical dependency. TIM production often relies on silicone compounds, aluminum, copper, graphite, boron nitride, phase-change polymers, specialty fillers, and rare advanced materials. Volatility in specialty chemicals, metal pricing, and global logistics can directly affect production costs and supply reliability.

Another major risk area involves geopolitical concentration in semiconductor and electronics manufacturing hubs, particularly across Asia-Pacific. Since major downstream demand originates from China, Taiwan, South Korea, and Japan, geopolitical tensions, export restrictions, trade barriers, or semiconductor supply disruptions could materially affect TIM production ecosystems and OEM partnerships.

The market also faces rapid technological obsolescence risk, as increasing processor heat density, AI accelerator deployment, EV battery redesigns, and miniaturized electronics continuously reshape performance requirements. Traditional TIM solutions may lose competitiveness if unable to meet ultra-high conductivity or low-resistance requirements.

Additionally, stringent thermal safety standards across EV batteries, aerospace electronics, and telecom systems are increasing compliance and validation costs. Product failure in thermal management can lead to overheating, efficiency loss, fire hazards, and major OEM liability concerns.

In parallel, cost sensitivity in high-volume consumer electronics applications continues creating pricing pressure for TIM suppliers.

Key Market Risk & Disruption Signals in Global Thermal Interface Material Market

1. Raw Material & Specialty Chemical Volatility

Dependence on silicone compounds, graphite, metal fillers, polymers, and specialty chemicals creates exposure to cost fluctuations and sourcing instability.

2. Semiconductor Supply Chain & Geopolitical Exposure

High reliance on Asia-Pacific semiconductor and electronics ecosystems increases vulnerability to geopolitical disruptions, export restrictions, and trade tensions.

3. Rapid Material Innovation & Technology Obsolescence

Graphene-based TIMs, liquid metal interfaces, and carbon composites are accelerating innovation cycles and replacement risks.

4. EV Battery Thermal Safety Risks

Rising adoption in EV battery packs and automotive electronics increases exposure to product liability, flame resistance, and overheating performance risks.

5. High OEM Qualification & Validation Complexity

TIM suppliers must meet strict qualification requirements for semiconductors, aerospace, telecom, and automotive systems, extending commercialization timelines.

6. Downstream Electronics Demand Cyclicality

Demand remains sensitive to fluctuations in semiconductor production, consumer electronics sales, AI infrastructure spending, and EV manufacturing activity.

7. Sustainability & Regulatory Pressure

Increasing pressure for low-toxicity, lightweight, recyclable, and environmentally safe thermal materials is reshaping product development priorities.

8. Competitive Margin Pressure

Price competition remains high in commodity-grade greases, adhesives, and thermal pads across consumer electronics applications.

Strategic Implications of Market Risk & Disruption in Global Thermal Interface Material Market

The evolving disruption environment creates both operational risks and strong long-term innovation opportunities.

One of the most critical strategic implications is the increasing need for application-specific material engineering. Companies must develop differentiated TIM solutions for AI processors, EV battery packs, 5G systems, aerospace electronics, and data center infrastructure rather than relying on generalized thermal materials.

Manufacturers are increasingly required to invest heavily in nanomaterials, graphene-based interfaces, lightweight conductive compounds, and flame-resistant high-stability formulations to improve competitiveness.

Vertical integration and strategic supply partnerships are also becoming essential. Companies with stronger control over specialty chemical sourcing, advanced fillers, and thermal composite production can better mitigate raw material volatility.

The convergence of semiconductor miniaturization, EV electrification, AI computing, and smart thermal design is also reshaping value chains. Suppliers capable of working closely with OEMs and semiconductor fabs will gain stronger long-term positioning.

Additionally, investment in recyclable materials, sustainable thermal compounds, and lower-carbon manufacturing processes is expected to become increasingly important as ESG and environmental regulations strengthen.

Companies focusing on high-margin premium TIMs, localized manufacturing, and customized OEM-grade solutions are expected to outperform commodity-driven competitors.

Global Thermal Interface Material Market Risk & Disruption Forward Outlook

Looking ahead to 2026–2033, the Global TIM Market is expected to become increasingly innovation-driven, strategically important, and performance-critical across advanced electronics ecosystems.

1. Expansion of AI & High-Performance Computing Thermal Needs

AI accelerators, GPUs, and dense processors will significantly increase demand for ultra-high conductivity TIMs.

2. Greater EV Battery & Power Electronics Integration

Battery thermal safety, energy storage, and onboard electronics will become major growth and risk centers.

3. Accelerating Shift Toward Advanced TIM Materials

Graphene, carbon composites, liquid metals, and nano-enhanced solutions are expected to reshape competitive differentiation.

4. Semiconductor Reshoring & Regional Supply Diversification

North America and Europe may reduce geographic concentration risks through localized semiconductor ecosystems.

5. Rising Thermal Safety & Certification Requirements

Regulators and OEMs will likely strengthen standards around thermal stability, dielectric safety, and fire resistance.

6. Growing Sustainability Expectations

Demand for low-toxicity, recyclable, and energy-efficient thermal materials will increase across industries.

7. Increasing Automation & Smart Manufacturing

Industrial automation, robotics, and power electronics will expand non-consumer TIM applications.

8. Competitive Consolidation in Premium Materials

M&A activity and strategic alliances may intensify as advanced materials companies compete for high-performance OEM contracts.

In conclusion, the Global Thermal Interface Material Market represents a high-growth, technology-sensitive, and performance-critical materials ecosystem, where conductivity innovation, supply chain resilience, OEM integration, thermal safety compliance, and material science leadership will define long-term competitive success.

Regulatory Landscape

Global Thermal Interface Material (TIM) Market Regulatory & Policy Environment Overview

The regulatory and policy environment plays a significant role in shaping the Global Thermal Interface Material (TIM) Market as governments, industrial bodies, and electronics safety authorities increasingly emphasize semiconductor efficiency, EV battery safety, thermal reliability, and material sustainability standards. Regulatory frameworks governing heat dissipation materials, dielectric insulation, flame resistance, hazardous substance control, and thermal safety performance significantly influence product development, manufacturing quality, and commercialization strategies globally.

TIMs are increasingly used in high-performance electronics, EV battery packs, semiconductors, aerospace systems, telecom infrastructure, and industrial automation. As these applications operate under high thermal density and critical safety conditions, regulatory oversight around overheating prevention, fire resistance, material stability, and long-term operational durability is becoming increasingly important.

The market is also influenced by evolving environmental and chemical compliance standards, including restrictions on hazardous substances, recyclability requirements, and sustainability initiatives related to advanced materials and industrial electronics. As TIMs integrate into next-generation AI chips, 5G systems, and EV platforms, compliance with energy efficiency and safety certification frameworks is becoming a key competitive requirement.

In addition, global semiconductor reshoring policies, EV manufacturing regulations, and industrial safety standards are further shaping supply chain strategies and product qualification processes across the industry.

Global Thermal Interface Material Market Regulatory & Policy Environment Current Scenario

Currently, the Global TIM Market operates under a moderately structured industrial and materials compliance framework involving electronics safety standards, automotive thermal safety requirements, aerospace certifications, and advanced material handling regulations.

One of the most significant regulatory trends influencing the market is the growing oversight of EV battery thermal safety and overheating prevention. Governments and automotive safety agencies are increasingly enforcing stricter thermal runaway prevention, insulation reliability, and high-temperature stability standards for EV battery systems and power electronics.

Semiconductor and high-performance computing infrastructure are also subject to energy efficiency, thermal reliability, and electronics performance regulations. As AI processors, GPUs, and compact chips generate higher heat density, TIM manufacturers must meet precise conductivity and stability benchmarks.

Another major regulatory development involves environmental compliance and chemical safety. Authorities are strengthening rules related to hazardous substances, volatile compounds, recyclability, and sustainable advanced material usage in electronics manufacturing.

Additionally, aerospace, telecom, and industrial sectors require application-specific certifications covering vibration resistance, flame retardancy, dielectric insulation, and long-term operational durability under harsh environments.

Supply chain localization policies, particularly in semiconductor and EV ecosystems, are also indirectly influencing product qualification and sourcing strategies globally.

Key Regulatory & Policy Environment Signals in Global Thermal Interface Material Market

1. Rising EV Thermal Safety Standards

Battery safety regulations and thermal runaway prevention requirements are increasing demand for certified high-stability TIM solutions.

2. Semiconductor Efficiency & Reliability Compliance

AI chips, CPUs, GPUs, and advanced processors require strict thermal conductivity and durability standards.

3. Expansion of Chemical & Environmental Regulations

Restrictions on hazardous substances and sustainability-focused material regulations are influencing TIM formulation strategies.

4. Growing Application-Specific Certification Requirements

Aerospace, telecom, medical, and industrial systems require sector-specific thermal safety and performance certifications.

5. Supply Chain & Localization Policy Influence

Semiconductor reshoring and EV manufacturing localization policies are impacting sourcing, qualification, and material partnerships.

Strategic Implications of Regulatory & Policy Environment in Global Thermal Interface Material Market

The evolving regulatory environment creates major strategic implications for advanced material manufacturers, semiconductor suppliers, EV battery companies, and thermal engineering firms. One of the most critical implications is the growing need for certified high-performance materials capable of meeting thermal safety, dielectric insulation, flame resistance, and durability standards.

Manufacturers must invest heavily in R&D validation, compliance testing, thermal certification programs, and sustainable material engineering to remain competitive across high-growth sectors.

The increasing convergence of semiconductor innovation, electrification, and industrial automation is also pushing companies toward specialized TIM solutions tailored for AI infrastructure, EV batteries, telecom equipment, and aerospace electronics.

Environmental and chemical regulations are likely to further accelerate innovation in lightweight, recyclable, and low-toxicity thermal materials.

Additionally, companies with strong OEM partnerships, vertically integrated supply chains, and application-specific regulatory capabilities will gain stronger long-term market positioning.

Global Thermal Interface Material Market Regulatory & Policy Environment Forward Outlook

Looking ahead to 2026–2033, the regulatory environment for TIMs is expected to become increasingly performance-driven, sustainability-focused, and safety-oriented as electronics miniaturization, EV adoption, and AI computing infrastructure continue expanding globally.

Future regulations are likely to place stronger emphasis on EV battery fire prevention, high-temperature endurance, semiconductor thermal efficiency, and smart electronics reliability.

Regulatory agencies may also strengthen sustainability requirements related to recyclable compounds, environmentally safe formulations, and carbon-efficient advanced material manufacturing.

The expansion of AI chips, autonomous vehicles, telecom systems, and next-generation power electronics is expected to increase demand for application-specific validation and long-term operational certifications.

Governments may also continue supporting semiconductor localization, EV manufacturing ecosystems, and energy-efficient infrastructure, indirectly strengthening demand for advanced compliant thermal solutions.

Overall, the regulatory and policy environment will remain a critical factor influencing innovation, safety validation, product qualification, sustainability, and competitive positioning within the Global Thermal Interface Material Market. Companies capable of balancing conductivity performance, compliance excellence, material innovation, environmental sustainability, and supply chain resilience will be best positioned to capture long-term growth opportunities.