Global Playing Cards & Board Games Market Size and Share Analysis 2026-2033

Global Playing Cards & Board Games Market Size & Forecast

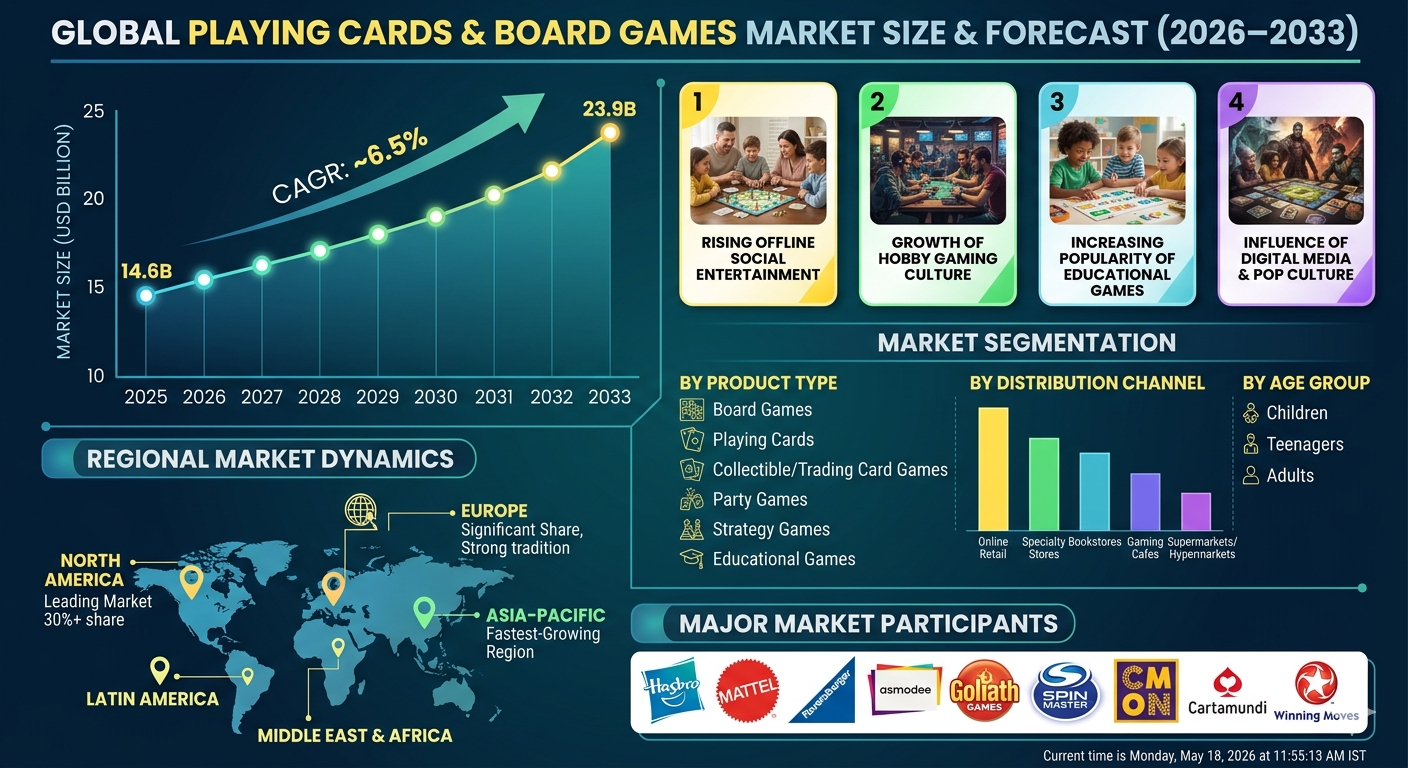

The global playing cards & board games market is projected to witness steady and sustained growth during the forecast period from 2026 to 2033. The market was valued at approximately USD 14.6 billion in 2025 and is expected to reach nearly USD 23.9 billion by 2033, expanding at a CAGR of around 6.5%. The market’s expansion is driven by rising demand for indoor entertainment, growing popularity of social and family gaming activities, increasing disposable incomes, and the resurgence of analog games in a digitally dominated entertainment landscape. Playing cards and board games include a wide range of recreational tabletop products such as traditional playing cards, strategy board games, educational games, card-based party games, collectible card games, and modern hobbyist tabletop games. These products are widely used for entertainment, education, cognitive development, and social engagement across all age groups. The market is also benefiting from a strong cultural revival of tabletop gaming, supported by cafes, gaming clubs, conventions, and online communities that encourage in-person social interaction and collaborative gameplay experiences. Additionally, the increasing influence of pop culture, fantasy franchises, and digital adaptations of board games is further fueling global demand for premium and themed gaming products.

Global Playing Cards & Board Games Market Overview

The playing cards and board games market represents a key segment of the global toys, games, and entertainment industry. It includes both mass-market casual games and premium hobbyist tabletop games that cater to children, families, and adult gaming communities. The market comprises traditional card decks, collectible card games (CCGs), trading card games (TCGs), strategy board games, party games, educational learning games, and role-playing tabletop systems. The industry is undergoing a transformation driven by innovation in game design, storytelling, and production quality, with manufacturers focusing on immersive gameplay experiences and high-quality physical components. Digital integration is also expanding the market, with hybrid board games that combine physical gameplay with mobile apps, augmented reality (AR) features, and online multiplayer connectivity. Major market participants include Hasbro, Mattel, Ravensburger, Asmodee, Goliath Games, Spin Master, Cartamundi Group, CMON Limited, and Winning Moves.Key Drivers of Global Playing Cards & Board Games Market Growth

Rising Demand for Offline Social Entertainment

Consumers are increasingly seeking offline and face-to-face entertainment experiences as a counterbalance to digital screen fatigue. Board games and playing cards provide interactive, social, and engaging experiences that strengthen family bonding and group interaction.Growth of Hobby Gaming Culture

The expansion of hobbyist tabletop gaming communities is significantly driving demand for complex strategy games and collectible card games. Board game cafes, gaming conventions, and organized tournaments are contributing to the rapid growth of enthusiast segments.Increasing Popularity of Educational Games

Educational board games and card-based learning tools are gaining traction among parents and educational institutions. These games help develop cognitive skills, problem-solving abilities, creativity, and teamwork among children.Influence of Digital Media and Pop Culture

Movies, TV series, video games, and fantasy franchises are inspiring themed board games and collectible card games. Licensed intellectual properties are becoming a major revenue driver in the premium gaming segment.Expansion of E-Commerce Distribution

Online retail platforms are making board games and playing cards more accessible globally, offering wider product variety and niche hobby games. E-commerce growth is also supporting indie game publishers and crowdfunding-driven board game launches.Global Playing Cards & Board Games Market Segmentation

By Product Type

The market is segmented into playing cards, board games, collectible card games (CCGs), trading card games (TCGs), party games, strategy games, and educational games. Board games represent the largest segment due to their broad appeal across families, schools, and hobby communities.By Age Group

The market includes children, teenagers, and adults. Adult gaming is the fastest-growing segment, driven by strategy games, hobby gaming culture, and social gaming communities.By Distribution Channel

The market includes online retail, specialty toy stores, supermarkets & hypermarkets, bookstores, and gaming cafes. Online retail channels are growing rapidly due to wider availability of niche and international board games.By Application

Applications include entertainment, education, social gatherings, cognitive development, and competitive gaming. Entertainment remains the dominant application segment across global markets.Regional Market Dynamics

North America

North America is a major market for board games and playing cards due to strong hobby gaming culture, high disposable income, and widespread presence of gaming communities. The United States leads the region, supported by major publishers, conventions such as Gen Con, and a growing board game café culture.Europe

Europe holds a significant share of the market, driven by strong tradition in tabletop gaming and leading game design industries. Germany, France, the United Kingdom, and the Nordic countries are key hubs for board game development and consumption. German-style strategy board games (Eurogames) continue to influence global market trends.Asia-Pacific

Asia-Pacific is the fastest-growing region due to rising urbanization, increasing disposable income, and growing youth engagement in recreational gaming. Japan and South Korea have strong gaming cultures, while China and India are emerging as high-growth markets for both traditional and modern board games.Latin America

Latin America is witnessing steady growth driven by increasing interest in family entertainment and affordable leisure activities. Brazil and Mexico are leading regional markets.Middle East & Africa

The region is gradually expanding due to rising youth population, increasing retail penetration, and growing demand for indoor entertainment options.Competitive Landscape

The global playing cards & board games market is moderately consolidated with strong presence of global entertainment giants and independent game publishers. Key players include Hasbro, Mattel, Ravensburger, Asmodee, Spin Master, Goliath Games, CMON Limited, Cartamundi Group, and Winning Moves. Companies are increasingly focusing on licensed content, innovative game mechanics, premium production quality, and digital hybrid game integration. Collaborations with entertainment franchises, crowdfunding platforms, and indie game designers are becoming important growth strategies.Strategic Outlook

The strategic outlook for the global playing cards & board games market remains positive due to the growing demand for social, educational, and immersive entertainment experiences. Future opportunities include hybrid digital-physical games, AI-enhanced gameplay systems, personalized board game design, and expansion of subscription-based gaming services. Indie game development and crowdfunding platforms will continue to play a major role in driving innovation and niche market expansion. Companies investing in storytelling, brand licensing, community engagement, and digital integration are likely to strengthen their long-term market position.Final Market Perspective

The global playing cards & board games market continues to thrive as consumers increasingly seek meaningful, interactive, and offline entertainment experiences. Rising hobby gaming culture, expanding digital distribution, and growing interest in educational and social games will continue to drive market expansion throughout the forecast period. Companies that successfully combine creativity, strong intellectual property, and community-driven engagement will remain strongly positioned in this evolving global entertainment market.Table of Contents

Table of Contents

- 1. Executive Summary

- 1.1 Global Playing Cards & Board Games Market Snapshot (2026-2033)

- 1.2 Market Size & CAGR Analysis

- 1.3 Largest & Fastest-Growing Product Segments

- 1.4 Key Regional Insights

- 1.5 Major Market Growth Drivers

- 1.6 Competitive Landscape Overview

- 1.7 Strategic Outlook Through 2033

- 2. Introduction & Market Overview

- 2.1 Definition of Playing Cards & Board Games Market

- 2.2 Scope of the Study

- 2.3 Evolution of Tabletop Gaming Industry

- 2.4 Product Categories & Game Ecosystem

- 2.5 Cultural & Social Importance of Board Gaming

- 2.6 Digital Transformation & Hybrid Gaming Trends

- 2.7 Licensing, IP Integration & Franchise Influence

- 3. Research Methodology

- 3.1 Primary Research

- 3.2 Secondary Research

- 3.3 Market Size Estimation Model

- 3.4 Forecast Assumptions (2026-2033)

- 3.5 Data Validation & Market Triangulation

- 4. Market Dynamics

- 4.1 Drivers

- 4.1.1 Rising Demand for Offline Social Entertainment

- 4.1.2 Growth of Hobby Gaming Culture

- 4.1.3 Increasing Popularity of Educational Games

- 4.1.4 Influence of Digital Media & Pop Culture

- 4.1.5 Expansion of E-Commerce Distribution Channels

- 4.2 Restraints

- 4.2.1 Strong Competition from Digital Gaming Platforms

- 4.2.2 High Production Costs for Premium Board Games

- 4.2.3 Short Product Lifecycle for Trend-Based Games

- 4.2.4 Market Fragmentation Across Indie Publishers

- 4.3 Opportunities

- 4.3.1 Hybrid Digital–Physical Gaming Models

- 4.3.2 Subscription-Based Board Game Services

- 4.3.3 AI-Assisted Game Design & Personalization

- 4.3.4 Expansion in Emerging Economies

- 4.4 Challenges

- 4.4.1 Intellectual Property & Licensing Complexity

- 4.4.2 Distribution Inefficiencies for Indie Publishers

- 4.4.3 Maintaining Long-Term Consumer Engagement

- 4.4.4 Seasonal Demand Fluctuations

- 4.1 Drivers

- 5. Global Playing Cards & Board Games Market Analysis (USD Billion), 2026-2033

- 5.1 Market Size Overview

- 5.2 CAGR Analysis

- 5.3 Regional Revenue Distribution

- 5.4 Product Type Revenue Analysis

- 5.5 Age Group Demand Trends

- 5.6 E-commerce vs Offline Sales Analysis

- 6. Market Segmentation (USD Billion), 2026-2033

- 6.1 By Product Type

- 6.1.1 Playing Cards

- 6.1.2 Board Games

- 6.1.3 Collectible Card Games (CCGs)

- 6.1.4 Trading Card Games (TCGs)

- 6.1.5 Party Games

- 6.1.6 Strategy Games

- 6.1.7 Educational Games

- 6.2 By Age Group

- 6.2.1 Children

- 6.2.2 Teenagers

- 6.2.3 Adults

- 6.3 By Distribution Channel

- 6.3.1 Online Retail

- 6.3.2 Specialty Toy Stores

- 6.3.3 Supermarkets & Hypermarkets

- 6.3.4 Bookstores

- 6.3.5 Gaming Cafes & Hobby Stores

- 6.4 By Application

- 6.4.1 Entertainment

- 6.4.2 Education

- 6.4.3 Social Gatherings

- 6.4.4 Cognitive Development

- 6.4.5 Competitive Gaming

- 6.1 By Product Type

- 7. Market Segmentation by Geography

- 7.1 North America

- 7.2 Europe

- 7.3 Asia-Pacific

- 7.4 Latin America

- 7.5 Middle East & Africa

- 8. Competitive Landscape

- 8.1 Market Share Analysis

- 8.2 Franchise & Licensing Strategy Benchmarking

- 8.3 Indie Publisher Ecosystem Analysis

- 8.4 Crowdfunding & Community-Driven Game Development

- 8.5 Digital Integration & Hybrid Gaming Strategies

- 9. Company Profiles

- 9.1 Hasbro

- 9.2 Mattel

- 9.3 Ravensburger

- 9.4 Asmodee

- 9.5 Spin Master

- 9.6 Goliath Games

- 9.7 Cartamundi Group

- 9.8 CMON Limited

- 9.9 Winning Moves

- 9.10 Indie Game Publishers (Aggregated)

- 10. Strategic Intelligence & Pheonix AI Insights

- 10.1 Tabletop Gaming Demand Forecast Engine

- 10.2 Player Behavior & Engagement Analytics

- 10.3 Game Success Probability Modeling System

- 10.4 IP & Franchise Performance Tracker

- 10.5 Automated Porter’s Five Forces Analysis

- 11. Future Outlook & Strategic Recommendations

- 11.1 Growth of Hybrid Digital–Physical Gaming Ecosystems

- 11.2 Expansion of Subscription-Based Gaming Models

- 11.3 Rise of AI-Driven Game Design Innovation

- 11.4 Global Expansion of Hobby Gaming Communities

- 11.5 Long-Term Market Outlook (2033+)

- 12. Appendix

- 13. About Pheonix Research

- 14. Disclaimer

Competitive Landscape

Global Playing Cards & Board Games Market Competitive Intensity & Market Structure Overview

The global playing cards & board games market is moderately consolidated at the top but highly fragmented at the product and publisher level, making it a structurally diverse and creativity-driven industry. A small group of major global entertainment companies holds significant market share, while hundreds of independent publishers, indie designers, and crowdfunding-backed studios continuously expand the product landscape.

Competitive intensity in the market is shaped less by manufacturing scale and more by intellectual property strength, game design innovation, brand licensing, community engagement, and distribution reach. The resurgence of tabletop gaming culture has intensified competition across both mass-market family games and premium hobbyist segments.

The industry continues to evolve through hybridization of physical and digital gaming experiences, with companies integrating apps, online platforms, and augmented gameplay features to enhance engagement and extend product lifecycles.

Global Playing Cards & Board Games Market Competitive Intensity & Market Structure Current Scenario

Leading Global Board Game & Playing Cards Companies

Hasbro: A dominant global player with a strong portfolio of iconic board games and card games, supported by powerful licensed IPs and mass-market distribution capabilities.

Mattel: Major toy and games company with a diversified portfolio of family-oriented board games and branded entertainment products.

Ravensburger: Leading European board game publisher known for high-quality strategy games, puzzles, and family gaming products with strong global reach.

Asmodee: One of the largest tabletop game publishers globally, specializing in strategy games, hobbyist titles, and distribution networks across multiple regions.

Spin Master: Strong presence in children’s games and entertainment-focused board games, with increasing expansion into digital-hybrid formats.

Goliath Games: Key player in party games and mass-market entertainment board games with strong retail penetration.

Cartamundi Group: Global leader in playing card manufacturing and trading card production, serving both consumer and commercial gaming markets.

CMON Limited: Prominent hobbyist tabletop game publisher known for miniatures-based strategy games and crowdfunding-driven releases.

Winning Moves: Specializes in licensed classic board games and nostalgic game re-releases with global distribution.

Indie Publishers & Crowdfunded Studios: A large ecosystem of independent designers and Kickstarter-driven publishers continuously introduces innovative mechanics and niche gaming experiences.

Key Competitive Intensity & Market Structure Drivers

A major driver of competitive intensity is the rapid expansion of hobby gaming culture, where consumers actively seek complex, replayable, and strategy-driven tabletop experiences. This has increased demand for innovative mechanics and premium game design.

Intellectual property licensing is another critical competitive factor. Games based on movies, TV series, video games, and fantasy franchises significantly influence purchasing behavior and drive premium segment growth.

The rise of crowdfunding platforms has fundamentally reshaped competition by enabling independent creators to bypass traditional publishing barriers and directly access global consumer demand.

Distribution strategy is also a key differentiator, with strong competition across online retail platforms, specialty gaming stores, bookstores, and emerging board game cafés and community hubs.

Digital integration, including app-supported gameplay, hybrid board games, and online multiplayer extensions, is increasingly shaping competitive positioning across both established publishers and emerging startups.

Strategic Implications of Competitive Intensity & Market Structure

Companies are increasingly prioritizing IP development and franchise-based game ecosystems to build long-term brand loyalty and recurring engagement across multiple product cycles.

Strategic collaborations with entertainment studios, streaming platforms, and gaming franchises are expanding the reach of themed board games and collectible card products.

Publishers are investing in community-driven marketing strategies, including tournaments, conventions, and influencer-led gameplay content, to strengthen consumer engagement and brand visibility.

The growing importance of direct-to-consumer (DTC) sales channels is reshaping distribution dynamics, enabling publishers to retain higher margins and build stronger customer relationships.

Asia-Pacific is emerging as a key competitive growth region due to rising disposable income, expanding youth population, and increasing adoption of both traditional and modern tabletop gaming formats.

Global Playing Cards & Board Games Market Competitive Intensity & Market Structure Forward Outlook

The global playing cards & board games market is expected to become increasingly innovation-driven, with strong emphasis on hybrid gaming experiences that merge physical and digital engagement.

Future competition will be heavily influenced by AI-assisted game design, personalized gameplay experiences, augmented reality integration, and subscription-based board game models.

Indie developers and crowdfunding ecosystems are expected to remain major sources of innovation, continuously challenging established publishers with niche and experimental game formats.

Market consolidation may increase moderately as larger publishers acquire successful indie studios and licensed IP portfolios to strengthen global competitiveness.

Overall, the market will remain structurally fragmented but creatively competitive, driven by storytelling innovation, strong intellectual property, and evolving consumer demand for social and immersive offline entertainment experiences through 2033.

Value Chain

Global Playing Cards & Board Games Market Value Chain & Supply Chain Evolution Overview

The global playing cards & board games market value chain is a structured yet increasingly innovation-driven ecosystem that spans creative game design, intellectual property development, manufacturing, distribution, and retail execution. The market is evolving from traditional print-and-manufacture models toward digitally integrated, IP-driven, and globally distributed entertainment systems supported by e-commerce and community-based consumption patterns.

The value chain begins with game design and intellectual property creation, where independent designers, publishing studios, and entertainment companies develop game mechanics, narratives, artwork, and thematic concepts. This stage is highly creativity-intensive and increasingly influenced by pop culture franchises, crowdfunding communities, and digital gaming trends that shape consumer expectations for immersive tabletop experiences.

The next stage involves publishing and licensing, where game publishers acquire rights, refine gameplay systems, conduct testing, and manage intellectual property partnerships. Licensing agreements with film studios, video game developers, and entertainment franchises play a significant role in expanding product appeal and global market penetration.

Manufacturing forms the core production layer of the value chain and includes printing, cardboard and plastic component production, packaging, and quality assembly of game boards, cards, tokens, and accessories. Manufacturers are increasingly adopting advanced printing technologies, eco-friendly materials, and precision cutting systems to enhance product durability, visual appeal, and sustainability compliance.

Distribution and logistics represent a critical operational layer, involving wholesalers, global supply chain operators, and regional distributors who ensure timely delivery to retail stores, specialty game shops, and online platforms. E-commerce fulfillment networks are becoming increasingly important as digital retail continues to expand across global markets.

The final retail and consumption stage includes supermarkets, bookstores, toy stores, specialty board game cafés, online marketplaces, and direct-to-consumer platforms. The rise of digital retail and community-driven gaming spaces has significantly broadened consumer access to niche, premium, and indie tabletop games.

Sustainability and regulatory compliance are emerging considerations in the value chain, with manufacturers increasingly focusing on recyclable materials, reduced plastic usage, and environmentally responsible packaging practices to align with evolving consumer expectations and environmental standards.

Global Playing Cards & Board Games Market Value Chain & Supply Chain Evolution Current Scenario

The current supply chain for the playing cards & board games market is characterized by strong globalization, cost-efficient manufacturing hubs, and a highly diversified distribution network. Asia-Pacific, particularly China, remains a dominant manufacturing base due to established printing infrastructure, low production costs, and scalable assembly capabilities.

North America and Europe continue to lead in game design, intellectual property creation, and premium publishing, while outsourcing production to Asia-based manufacturers for cost optimization. This global division of labor has created an efficient but sometimes vulnerable supply chain structure.

E-commerce platforms have significantly reshaped distribution dynamics, enabling direct-to-consumer sales and allowing independent publishers and crowdfunding-backed games to reach global audiences without traditional retail dependency. Platforms such as Kickstarter have become key launch mechanisms for innovative tabletop games.

Digital transformation is also influencing the ecosystem through hybrid game formats that integrate mobile applications, augmented reality features, and online multiplayer components, expanding engagement beyond traditional physical gameplay.

However, supply chain disruptions, shipping delays, and raw material price fluctuations have highlighted the need for more resilient and regionally diversified manufacturing strategies within the industry.

Key Value Chain & Supply Chain Evolution Signals in Global Playing Cards & Board Games Market

One of the strongest transformation signals in the market is the increasing dominance of intellectual property-driven gaming ecosystems. Licensed content from movies, television franchises, and video games is becoming a major growth driver, influencing production strategies and supply chain prioritization.

Another key signal is the rapid expansion of crowdfunding and indie game publishing, which is decentralizing traditional publishing models and enabling smaller creators to access global markets directly through digital platforms and community funding mechanisms.

The rise of hybrid digital-physical games is also reshaping product development and supply chain requirements, as manufacturers integrate QR codes, mobile apps, and augmented reality components into traditional board game formats.

Sustainability is becoming increasingly important, with manufacturers adopting eco-friendly materials, reduced plastic usage, and recyclable packaging to align with environmental regulations and consumer preferences.

Additionally, the expansion of e-commerce and global fulfillment networks is enabling faster international distribution, reducing reliance on traditional brick-and-mortar retail channels and increasing market accessibility for niche and premium products.

Strategic Implications of Value Chain & Supply Chain Evolution in Global Playing Cards & Board Games Market

The evolving value chain presents significant strategic opportunities for publishers, designers, manufacturers, and distributors. Companies that successfully integrate creative intellectual property development with scalable global manufacturing and strong digital distribution capabilities are expected to maintain competitive advantages.

Supply chain diversification is becoming increasingly important as companies seek to reduce dependency on single-region manufacturing hubs and mitigate risks associated with logistics disruptions and raw material volatility.

Digital transformation is reshaping competitive dynamics, with e-commerce platforms, crowdfunding ecosystems, and digital marketing channels enabling direct engagement with global gaming communities and reducing reliance on traditional retail intermediaries.

Innovation in hybrid gaming experiences is also creating new strategic opportunities, requiring closer collaboration between software developers, game designers, and physical product manufacturers.

Companies that invest in storytelling, licensed intellectual property, and community-driven engagement models are likely to achieve stronger long-term market positioning in an increasingly experience-driven entertainment industry.

Global Playing Cards & Board Games Market Value Chain & Supply Chain Evolution Forward Outlook

Between 2026 and 2033, the value chain is expected to become more digitally integrated, globally distributed, and innovation-focused. Hybrid gaming models combining physical components with digital platforms will become increasingly mainstream, reshaping both product design and manufacturing processes.

Manufacturing operations are expected to adopt more sustainable practices, including eco-friendly materials, reduced waste production systems, and energy-efficient printing technologies to meet rising environmental standards and consumer expectations.

E-commerce and direct-to-consumer channels will continue expanding, enabling smaller publishers and independent designers to reach global audiences more efficiently while reducing dependence on traditional retail structures.

Artificial intelligence and data analytics are expected to play a growing role in game development, helping publishers analyze player behavior, optimize game mechanics, and personalize gaming experiences.

Overall, the future value chain will evolve into a highly interconnected ecosystem where creativity, digital integration, sustainability, and global distribution efficiency collectively define market competitiveness.

Market-Specific Value Chain

- Game Design & Intellectual Property Development: Game designers, creative studios, storytelling teams, IP licensing agencies

- Publishing & Licensing: Board game publishers, entertainment franchise licensors, crowdfunding platforms, indie game publishers

- Manufacturing & Production: Printing facilities, component manufacturers, packaging providers, assembly plants

- Distribution & Logistics: Global distributors, warehousing providers, e-commerce fulfillment networks, wholesale suppliers

- Retail & Digital Sales Channels: Online marketplaces, toy stores, bookstores, gaming cafés, specialty hobby shops

- End User & Gaming Communities: Families, hobby gamers, educational institutions, board game clubs, competitive gaming communities

Investment Activity

Global Playing Cards & Board Games Market Investment & Funding Dynamics Overview

Investment activity in the global playing cards & board games market is steadily expanding, supported by the resurgence of analog entertainment, rising hobby gaming culture, and increasing consumer preference for social, offline leisure experiences. Between 2026 and 2033, funding is expected to flow into game publishing, intellectual property (IP) licensing, premium game design studios, and hybrid digital-physical gaming innovations.

The market is witnessing growing investor interest from entertainment companies, toy manufacturers, and private equity firms targeting scalable IP-driven businesses. Strong performance of collectible card games, strategy board games, and franchise-based tabletop products is encouraging sustained capital inflows into both established publishers and independent game developers.

Additionally, crowdfunding platforms and community-backed funding models are playing a major role in early-stage game development. These platforms enable indie creators to validate concepts, secure pre-orders, and reduce financial risk while building strong consumer communities around new board game launches.

Major industry players such as Hasbro, Mattel, Ravensburger, Asmodee, Spin Master, and CMON Limited are increasingly investing in portfolio expansion, licensed content acquisition, and cross-media integration strategies to strengthen long-term revenue streams.

Global Playing Cards & Board Games Market Investment & Funding Dynamics Current Scenario

Current investment trends in the market are shaped by rising demand for premium tabletop experiences, expansion of board game cafes, and increasing global popularity of gaming conventions and hobby communities. Capital allocation is focused on high-quality game production, digital integration, and franchise-based intellectual property development.

- North America: Leads investment activity due to strong hobby gaming culture, high consumer spending on entertainment products, and established publishing ecosystems in the United States and Canada.

- Europe: Remains a key investment hub supported by strong board game design traditions, particularly in Germany and France, along with growing demand for Euro-style strategy games.

- Asia-Pacific: Emerging as a high-growth investment region driven by rising youth population, expanding middle class, and increasing adoption of modern tabletop gaming formats in China, Japan, South Korea, and India.

- Latin America & Middle East & Africa: Gradually developing markets supported by growing retail penetration, increasing disposable incomes, and rising interest in affordable family entertainment products.

Key Investment & Funding Dynamics Signals in Global Playing Cards & Board Games Market

- Increasing investment in franchise-based and licensed board games linked to movies, TV series, and digital entertainment IPs.

- Rising funding toward collectible card games (CCGs) and trading card games (TCGs) driven by strong secondary markets and community engagement.

- Expansion of crowdfunding-driven game development, enabling independent designers to scale globally without traditional publishing constraints.

- Growing interest in hybrid gaming models combining physical board games with mobile apps, AR features, and online multiplayer connectivity.

- Investment in premium production quality, including high-end materials, miniatures, and immersive storytelling formats.

- Strategic acquisitions and partnerships between toy manufacturers, entertainment studios, and indie publishers to strengthen IP portfolios.

- Rising funding for educational and cognitive development-focused games targeting schools and early learning ecosystems.

Strategic Implications of Investment & Funding Dynamics in Global Market

- The market increasingly favors IP-rich companies capable of building long-term franchise ecosystems across physical and digital formats.

- Indie game developers supported by crowdfunding platforms are becoming a major source of innovation and niche market expansion.

- Digital transformation, including app-integrated board games and online multiplayer tabletop platforms, is reshaping investment priorities.

- Regional diversification is important, with North America leading commercial scale, Europe driving design innovation, and Asia-Pacific fueling rapid demand growth.

- Companies investing in community engagement, tournaments, and gaming events are achieving stronger brand loyalty and recurring revenue streams.

- Educational and skill-based games are gaining importance as schools and parents increasingly adopt gamified learning solutions.

- Cross-media integration with streaming platforms, gaming franchises, and entertainment IPs is becoming a key long-term growth strategy.

Global Playing Cards & Board Games Market Investment & Funding Dynamics Forward Outlook

Looking ahead, investment in the global playing cards & board games market is expected to remain strong, supported by continued demand for immersive, social, and experiential entertainment. Capital inflows will increasingly focus on hybrid gaming ecosystems, franchise expansion, and digital integration of traditional tabletop formats.

Future funding priorities include AI-assisted game design, personalized gameplay experiences, blockchain-based collectible card systems, and subscription-based board game services. Expansion of gaming cafes, global tournaments, and community-driven platforms will further support market monetization opportunities.

- North America: Will continue leading investment due to strong consumer demand and established entertainment ecosystems.

- Europe: Will remain a global innovation hub for board game design and strategic gameplay development.

- Asia-Pacific: Will emerge as a key growth engine driven by youth engagement and rapid digital-physical gaming adoption.

Overall, the market is expected to maintain steady investment momentum as consumer interest in social, interactive, and offline entertainment continues to grow. Companies that successfully combine strong intellectual property, innovative gameplay design, and digital ecosystem integration will remain strongly positioned in the evolving global playing cards & board games market through 2033.

Technology & Innovation

Global Playing Cards & Board Games Market Technology & Innovation Landscape Overview

The technology and innovation landscape of the global playing cards and board games market is evolving as traditional tabletop gaming increasingly integrates digital enhancements, advanced printing technologies, and hybrid gameplay systems. Innovation in this market is primarily driven by the convergence of physical gaming experiences with digital platforms, improved game design methodologies, and enhanced production technologies that elevate user engagement and replay value.

A major area of technological advancement is the development of hybrid board games that combine physical components with mobile applications, augmented reality (AR), and companion software. These integrations enable dynamic storytelling, automated rule enforcement, immersive gameplay environments, and real-time score tracking, significantly enhancing the overall gaming experience.

Advancements in game manufacturing and printing technologies are also transforming product quality and customization capabilities. High-definition printing, premium finishing techniques, eco-friendly materials, and precision-cut components are enabling publishers to create visually appealing and durable game products that enhance consumer satisfaction and brand differentiation.

Digital transformation in game design is another key innovation driver. Game developers are increasingly using simulation tools, AI-assisted game balancing systems, and digital prototyping platforms to accelerate development cycles and improve gameplay mechanics. These tools help designers refine rules, optimize player experience, and ensure better engagement across different player demographics.

The integration of online communities and digital platforms is also reshaping the tabletop gaming ecosystem. Online matchmaking systems, virtual board game platforms, and digital rulebooks are extending the lifecycle of physical games and enabling global player interaction beyond traditional in-person sessions.

Global Playing Cards & Board Games Market Technology & Innovation Landscape Current Scenario

Currently, the global playing cards and board games market is experiencing strong innovation momentum driven by rising demand for immersive, social, and interactive entertainment experiences. Traditional tabletop gaming continues to evolve with the integration of digital enhancements that bridge physical and virtual gameplay environments.

One of the most significant current trends is the rise of digital companion apps that support board games by providing tutorials, automated scoring, story progression, and interactive event triggers. These applications reduce complexity for new players while increasing engagement for experienced users.

Crowdfunding platforms and independent game development ecosystems are also playing a critical role in innovation. Platforms such as Kickstarter have enabled indie developers to introduce highly creative and niche board games, often incorporating unique mechanics, storytelling techniques, and premium production designs that challenge traditional publishing models.

Artificial intelligence is gradually entering the tabletop gaming space through adaptive game design, procedural content generation, and smart difficulty balancing systems. These technologies allow for more personalized and replayable gaming experiences that adjust based on player behavior and skill level.

In addition, sustainability has become an important focus area in the current market environment. Manufacturers are increasingly adopting recycled materials, biodegradable packaging, and eco-conscious production processes to reduce environmental impact while meeting growing consumer expectations for sustainable products.

Digital distribution channels are also expanding rapidly, with online marketplaces enabling global access to niche and premium board games. This has significantly improved market reach for independent publishers and small-scale game designers.

Key Technology & Innovation Trends in Global Playing Cards & Board Games Market

- Hybrid Digital-Physical Games: Integration of mobile apps, AR features, and companion software with traditional tabletop gameplay.

- AI-Assisted Game Design: Use of artificial intelligence for game balancing, rule optimization, and procedural content generation.

- Advanced Printing & Component Manufacturing: High-definition printing, premium materials, and precision-cut game components for enhanced product quality.

- Digital Companion Applications: Apps for tutorials, scoring, storytelling, and interactive gameplay enhancements.

- Crowdfunding-Driven Innovation: Indie game development supported by platforms enabling global funding and niche game creation.

- Online Gaming Communities: Digital platforms enabling global multiplayer tabletop experiences and community engagement.

- Sustainable Game Production: Eco-friendly materials, recyclable packaging, and green manufacturing processes.

- Virtual Tabletop Platforms: Online systems replicating board game experiences in digital environments.

- Personalized Game Experiences: Adaptive gameplay systems tailored to player behavior and preferences.

- IP-Driven Game Development: Integration of movies, TV franchises, and gaming universes into licensed board game formats.

Strategic Implications of Technology & Innovation

Technological innovation is reshaping the playing cards and board games market by enhancing engagement, accessibility, and replayability of tabletop gaming experiences. The integration of digital tools with physical gameplay is enabling a new generation of hybrid entertainment products that appeal to both traditional gamers and digitally native audiences.

For manufacturers and publishers, investment in digital integration, AI-assisted design tools, and high-quality production technologies is becoming increasingly important for differentiation in a competitive market. Companies that successfully combine creativity with technological enhancement are better positioned to capture both mainstream and niche gaming segments.

The rise of crowdfunding and indie development ecosystems has democratized innovation in the market, allowing smaller creators to compete with established publishers. This has led to a surge in experimental game mechanics, storytelling formats, and unique player experiences.

However, challenges such as high production costs for premium games, fragmentation of digital platforms, and balancing complexity with accessibility remain key concerns. Publishers must carefully manage innovation while ensuring usability and mass-market appeal.

Global Playing Cards & Board Games Market Technology & Innovation Forward Outlook

Looking ahead, the global playing cards and board games market is expected to evolve into a more digitally integrated and experience-driven industry. Hybrid gaming systems combining augmented reality, mobile connectivity, and AI-enhanced gameplay are likely to become more mainstream, offering richer and more immersive player experiences.

Artificial intelligence will continue to play a growing role in game development, enabling smarter game design, adaptive storytelling, and personalized difficulty scaling. These capabilities will significantly enhance replay value and player engagement across different demographics.

The expansion of virtual tabletop platforms and online gaming ecosystems will further blur the lines between physical and digital gaming, enabling global multiplayer experiences without geographic limitations. This shift will expand the market reach of traditional board games significantly.

Sustainability and eco-friendly production practices are also expected to become central to future innovation strategies. Manufacturers will increasingly adopt recyclable materials, reduced packaging designs, and environmentally responsible production processes.

In conclusion, the global playing cards and board games market is undergoing a significant technological transformation driven by digital integration, AI innovation, and evolving consumer expectations. Companies that successfully combine creativity, technology, sustainability, and strong intellectual property development will remain strongly positioned in the future global tabletop gaming ecosystem.

Market Risk

Global Playing Cards & Board Games Market Risk Factors & Disruption Threats Overview

The global playing cards and board games market is experiencing steady growth supported by rising demand for offline social entertainment, expanding hobby gaming culture, and increasing interest in educational and strategy-based games. However, despite its resilient consumer base, the market faces several structural, technological, and behavioral risks that may influence long-term growth. The industry is highly dependent on discretionary consumer spending, cultural trends, intellectual property licensing, and evolving entertainment preferences, making it sensitive to shifts in lifestyle and digital media consumption.

One of the primary risk factors in the market is the strong competition from digital entertainment platforms. Video games, mobile gaming, streaming services, and social media continue to capture significant consumer attention and leisure time. This ongoing digital shift can reduce demand for traditional tabletop games, especially among younger demographics who are more engaged in interactive digital ecosystems.

Another key risk factor is the cyclical and trend-driven nature of board game demand. Many products rely heavily on pop culture relevance, licensed intellectual properties, or viral popularity. If consumer interest in specific themes or franchises declines, sales can drop sharply, leading to inventory imbalance and revenue volatility for publishers and retailers.

Intellectual property dependency also represents a significant vulnerability. A large portion of high-value board games and collectible card games rely on licensed characters, movies, or franchises. Any disruption in licensing agreements, rising royalty costs, or expiration of rights can directly impact product portfolios and profitability.

In addition, rising production and logistics costs are affecting global manufacturers. The market depends on paper, cardboard, plastic components, printing materials, and international distribution networks. Inflation in raw material prices, shipping disruptions, and supply chain inefficiencies can increase product costs and reduce price competitiveness.

Global Playing Cards & Board Games Market Risk Factors & Disruption Threats Current Scenario

The current market environment reflects a healthy resurgence of tabletop gaming, driven by social engagement trends and a growing desire for offline entertainment experiences. Board game cafés, gaming conventions, and community-driven events continue to support strong consumer engagement across multiple regions.

At the same time, competition from digital entertainment ecosystems remains intense. Hybrid entertainment experiences that blend physical and digital gameplay are emerging, but traditional board games still face challenges in maintaining relevance among digitally native consumers.

Supply chain stability is another key concern. Many board games are produced through global manufacturing networks concentrated in specific regions. Disruptions in printing, packaging, or shipping can delay product launches, especially for seasonal or crowdfunding-based releases.

The market is also experiencing increasing fragmentation due to the rise of independent game designers and crowdfunding platforms. While this supports innovation, it also creates intense competition and short product life cycles, making it difficult for individual titles to sustain long-term market presence.

Additionally, rising expectations for premium game quality, including high-end components, artwork, and immersive storytelling, are increasing production complexity and costs for publishers.

Global Playing Cards & Board Games Market Key Risk Factors & Disruption Threat Signals

One major disruption signal in the market is the continued convergence of physical and digital gaming. Hybrid board games that integrate mobile apps, augmented reality, and online multiplayer features are reshaping consumer expectations and increasing pressure on traditional game formats.

Another important trend is the growing influence of crowdfunding platforms such as Kickstarter, which are changing how board games are developed, funded, and distributed. While this enables innovation, it also introduces unpredictability in demand forecasting and production scaling.

The expansion of collectible card games and live-service tabletop ecosystems represents both opportunity and disruption. These models often rely on continuous content updates and competitive play structures, which may shift consumer focus away from traditional standalone board games.

Changing consumer attention spans and increasing digital saturation are also key signals. Younger audiences increasingly prefer fast-paced, interactive entertainment formats, which may reduce engagement with longer-duration tabletop gameplay experiences.

Macroeconomic conditions, including inflation and reduced discretionary spending, may further impact demand for premium board games and collectible products, particularly in non-essential entertainment categories.

Global Playing Cards & Board Games Market Strategic Implications of Risk Factors

Manufacturers and publishers must increasingly focus on intellectual property diversification to reduce reliance on licensed content and improve long-term product stability. Developing original game concepts and strong proprietary franchises will be critical for sustainable growth.

Investment in hybrid gaming models that integrate physical gameplay with digital enhancements will become increasingly important to maintain relevance among younger and tech-oriented consumers.

Companies should also strengthen supply chain resilience by diversifying manufacturing locations, optimizing inventory planning, and improving logistics coordination to reduce delays and cost fluctuations.

Community-driven marketing, influencer engagement, and crowdfunding strategies will continue to play a key role in product launch success, but must be balanced with scalable production planning to avoid fulfillment risks.

Additionally, focusing on premium-quality production, immersive storytelling, and educational game design can help differentiate products in an increasingly competitive and fragmented market.

Global Playing Cards & Board Games Market Forward Risk Outlook

Looking ahead to 2026–2033, the playing cards and board games market is expected to maintain steady growth, supported by strong hobby gaming culture, rising demand for social entertainment, and increasing interest in educational and collectible gaming formats. However, the competitive landscape will continue to evolve rapidly due to digital entertainment expansion and hybrid gaming innovation.

Future growth will increasingly depend on the ability to balance traditional tabletop appeal with digital integration, community engagement, and intellectual property innovation. Companies that fail to adapt to hybrid entertainment trends may face gradual demand erosion, particularly among younger consumer segments.

Overall, while the market remains resilient due to its strong social and cultural foundations, long-term success will depend on innovation, franchise strength, production efficiency, and the ability to remain relevant in a digitally dominated entertainment ecosystem.

Regulatory Landscape

Global Playing Cards & Board Games Market Regulatory & Policy Environment Overview

The regulatory and policy environment governing the global playing cards & board games market is relatively moderate compared to other consumer goods sectors, but it is increasingly influenced by consumer protection laws, intellectual property regulations, product safety standards, and digital commerce governance. As the market expands across educational, entertainment, and hobby gaming segments, regulatory oversight is gradually evolving to address safety labeling, fair trade practices, and licensing compliance.

In addition, the growing integration of licensed intellectual properties, branded content, and cross-media franchises has increased the importance of copyright enforcement, trademark protection, and licensing agreements. Governments and regulatory bodies are also focusing on ensuring transparency in advertising, especially for products targeted at children and educational markets.

While traditional board games and playing cards are generally low-risk consumer products, regulatory attention is increasing around materials used in manufacturing, child safety standards, and digital hybrid gaming components that connect physical products with online platforms.

Global Playing Cards & Board Games Market Regulatory & Policy Environment Current Scenario

The current regulatory landscape for the playing cards & board games market is primarily governed by consumer product safety regulations, labeling requirements, and intellectual property laws. In most regions, these products are classified as toys or recreational goods and must comply with age-appropriateness standards, non-toxic material requirements, and safety certifications.

In North America, regulatory oversight is led by agencies such as the U.S. Consumer Product Safety Commission (CPSC), which enforces safety standards for toys and games, including restrictions on hazardous materials, choking hazards, and labeling for age suitability. Intellectual property protection is also strongly enforced due to the prevalence of licensed board games and collectible card games.

In Europe, regulations under the EU Toy Safety Directive and CE marking requirements ensure that board games and playing cards meet strict safety, chemical, and labeling standards. European markets also emphasize sustainability, encouraging the use of recyclable materials and environmentally friendly packaging.

Asia-Pacific markets such as China, Japan, South Korea, and India are strengthening product quality control and safety compliance frameworks as demand for imported and domestically produced games increases. China plays a major role in manufacturing, while Japan and South Korea have advanced regulatory environments for entertainment and gaming products.

Latin America and the Middle East are gradually aligning with international toy safety and import standards, focusing on product quality certification, consumer protection, and expanding retail compliance systems.

Key Regulatory & Policy Environment Signals in Global Playing Cards & Board Games Market

- Consumer Product Safety Standards: Board games and playing cards must comply with non-toxic material requirements, age labeling, and choking hazard regulations.

- Intellectual Property & Licensing Regulations: Strong enforcement of copyright, trademark, and licensing agreements is critical due to widespread use of branded and franchise-based games.

- Advertising & Marketing Transparency Rules: Regulations ensure fair marketing practices, especially for products targeted at children and educational segments.

- Material & Environmental Compliance: Increasing focus on recyclable materials, sustainable packaging, and reduced plastic usage in game manufacturing.

- E-Commerce & Digital Distribution Regulations: Online sales platforms must comply with consumer protection laws, return policies, and digital transaction transparency requirements.

- Educational Product Certification Standards: Educational board games may require compliance with curriculum alignment or child development safety guidelines in some markets.

Strategic Implications of Regulatory & Policy Environment

The regulatory environment is shaping product design, licensing strategies, and manufacturing practices in the global board games industry. Companies are increasingly investing in compliant material sourcing, sustainable packaging, and standardized safety testing to meet global regulatory requirements.

Intellectual property protection has become a major strategic focus, particularly for games based on films, television series, video games, and fantasy franchises. Strong licensing agreements and legal enforcement are essential for protecting brand value and revenue streams.

Environmental regulations are encouraging manufacturers to shift toward recyclable cardboard, biodegradable components, and plastic-free packaging designs, particularly in European and North American markets.

Digital hybrid board games introduce additional regulatory considerations related to data privacy, online interaction safety, and digital content moderation, especially when games include mobile apps or online connectivity features.

In parallel, expanding e-commerce regulations are influencing global distribution strategies, requiring companies to ensure compliance with cross-border taxation, consumer rights, and digital retail transparency standards.

Global Playing Cards & Board Games Market Regulatory & Policy Environment Forward Outlook

Between 2026 and 2033, the regulatory environment for the playing cards & board games market is expected to become more sustainability-driven, digitally integrated, and IP-focused. Governments are likely to strengthen environmental regulations related to packaging waste and material recyclability, particularly for mass-produced consumer games.

Intellectual property enforcement is expected to become more stringent as cross-media franchises and licensed gaming content continue expanding globally. This will further formalize licensing agreements and content protection frameworks across digital and physical gaming formats.

Digital hybrid gaming systems may face increasing oversight related to data privacy, child online safety, and digital content regulation as physical board games integrate more deeply with mobile applications and online platforms.

At the same time, sustainability initiatives are expected to drive broader adoption of eco-friendly materials, reduced plastic usage, and circular design principles in game manufacturing.

Overall, the regulatory and policy environment will remain a moderate but increasingly influential factor shaping innovation, production standards, and global distribution strategies in the playing cards & board games market. Companies that prioritize compliance, intellectual property management, and sustainable product design will be best positioned for long-term success.