Global Electrolyte Hydration Drinks Market Report Analysis, Size and Forecast 2026-2033

Market Forecast Snapshot (2026–2033)

| Metric | Value |

|---|---|

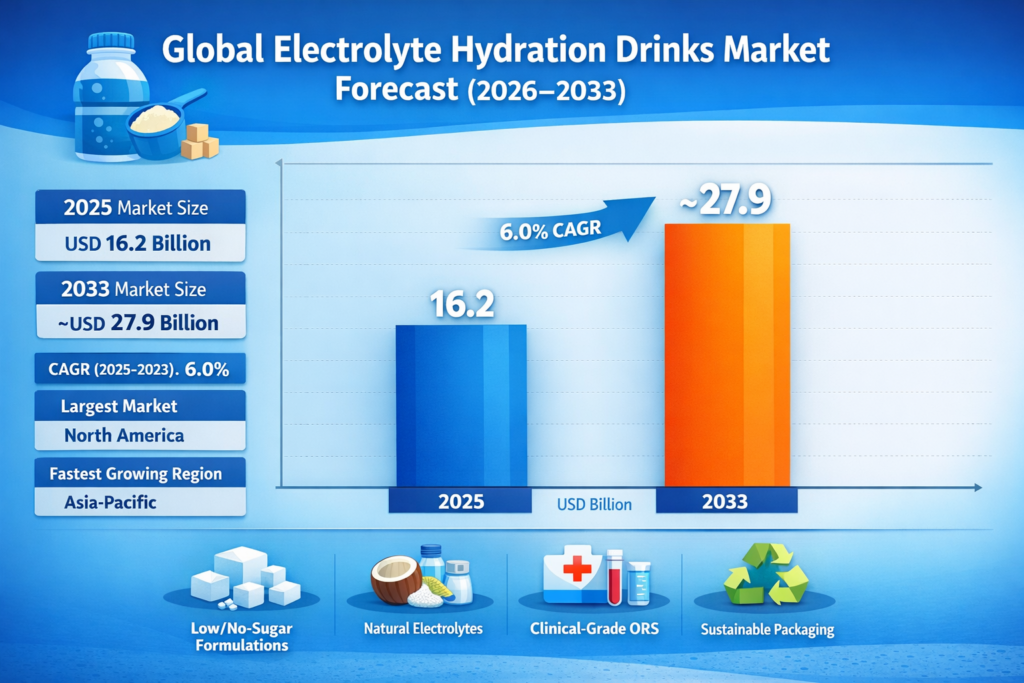

| 2025 Market Size | USD 16.2 Billion |

| 2033 Market Size | ~USD 27.9 Billion |

| CAGR (2025–2033) | 6.0% |

| Largest Market | North America |

| Fastest Growing Region | Asia-Pacific |

| Major Product Segment | RTD & Powdered Mixes |

| Key Trend | Low/No-Sugar Formulations, Natural Electrolyte Sources |

| Future Focus | Clinical-grade ORS, Personalized Hydration, Sustainable Packaging |

Global Electrolyte Hydration Drinks Market Overview

The Global Electrolyte Hydration Drinks Market includes ready-to-drink (RTD) beverages, powdered mixes and sachets, effervescent/dissolvable tablets, clinical oral rehydration solutions (ORS), and other functional hydration formats.

Electrolyte hydration drinks have evolved from niche sports beverages into a mainstream functional hydration category. Their popularity is driven by growing health and fitness awareness, demand for low/zero-sugar and natural formulations, adoption across pediatric and elderly care, and workplace hydration programs. Convenience, on-the-go formats, and compatibility with subscription/e-commerce models further fuel adoption. Rising demand for performance beverages is also shaping the market, catering to fitness enthusiasts and health-conscious consumers seeking optimal hydration solutions.The expanding role of functional and wellness-oriented beverages is increasingly intersecting with trends in premium and lifestyle beverages.

According to Pheonix Demand Forecast Engine, the Global Electrolyte Hydration Drinks Market is valued at USD 16.2 billion in 2025 and is projected to reach approximately USD 27.9 billion by 2033, reflecting a CAGR of ~6.0% during 2026–2033.

North America holds the largest market share, supported by established sports-drink brands, extensive retail and DTC distribution, and high consumer spending on fitness and functional beverages. Asia-Pacific represents the fastest-growing region, driven by rising fitness participation, hotter climates increasing demand for hydration, rapid expansion of sachet formats, and workplace hydration initiatives.

The post-2025 outlook indicates rising product personalization, clinical-grade oral rehydration solutions, sustainable packaging initiatives, and innovation in clean-label, plant-based, and fortified electrolyte formulations.

Key Drivers of Global Electrolyte Hydration Drinks Market Growth

1. Rising Health & Fitness Culture

Natural ingredient adoption is accelerating growth across the industry. Growing participation in gyms, endurance sports, marathons, and lifestyle fitness activities significantly boosts demand for performance, recovery, and daily hydration solutions across both amateur and professional users – electrolyte drinks fit the bill for active hydration needs

2. Shift Toward Low-Sugar & Functional Formulations

Consumers are increasingly favoring low/zero-sugar, natural, vitamin-fortified, and clean-label hydration beverages, driving reformulation strategies and premium product positioning.

3. Convenience & On-the-Go Consumption Trends

The increasing popularity of convenient, on-the-go hydration formats further supports growth in the market – Ready-to-drink (RTD) bottles, single-serve powder sachets, and dissolvable electrolyte tablets align with busy urban lifestyles, travel needs, and workplace hydration requirements.

4. Expanding Clinical, Pediatric & Elderly Applications

Rising adoption of oral rehydration solutions (ORS) in hospitals, pediatric care, elderly care facilities, and post-illness recovery programs supports stable institutional demand.

5. E-Commerce & Personalized Subscription Models

Digital retail channels and DTC subscription platforms enable customized electrolyte profiles, flavor personalization, and recurring revenue streams for emerging and niche brands.

Global Electrolyte Hydration Drinks Market Segmentation

1. By Product Type

1.1 Ready-to-Drink (RTD) Beverages

1.1.1 Sports & Performance Drinks

1.1.1.1 Low-Calorie / Low-Sugar RTD Drinks

1.1.1.2 Standard Sugar RTD Sports Drinks

1.1.2 Functional Hydration Beverages

1.1.2.1 Vitamin-Fortified RTD Drinks

1.1.2.2 Amino Acid / Recovery RTD Drinks

1.1.3 Premium & Lifestyle Hydration RTD

1.1.3.1 Plant-Based Electrolyte RTD Drinks

1.1.3.2 Adaptogen-Infused RTD Beverages

1.2 Powdered Mixes & Sachets

1.2.1 Single-Serve Sachets

1.2.1.1 Isotonic Hydration Sachets

1.2.1.2 Hypotonic / Rapid-Absorption Sachets

1.2.1.3 Hypertonic / Energy + Electrolyte Sachets

1.2.2 Multi-Serve Powder Packs

1.2.2.1 Fitness & Gym-Oriented Packs

1.2.2.2 Workplace / Occupational Packs

1.2.2.3 Clinical & Pediatric Packs

1.3 Effervescent / Dissolvable Tablets

1.3.1 Single-Serving Tablets

1.3.1.1 Sports Performance Tablets

1.3.1.2 Recovery & Immunity Tablets

1.3.2 Multi-Serving Tubes

1.3.2.1 Fitness / Gym-Focused Tubes

1.3.2.2 General Wellness Tubes

1.4 Clinical Oral Rehydration Solutions (ORS)

1.4.1 Pediatric ORS

1.4.1.1 Sachet-Based Pediatric ORS

1.4.1.2 RTD Pediatric ORS

1.4.2 Geriatric / Elderly ORS

1.4.2.1 RTD Elderly Formulations

1.4.2.2 Powder-Based Elderly ORS

1.4.3 Hospital / Clinical ORS

1.4.3.1 Inpatient Hydration Packs

1.4.3.2 Outpatient & Emergency ORS Solutions

1.5 Others (Concentrates, Shots)

1.5.1 Concentrated Electrolyte Syrups

1.5.1.1 DIY RTD Mixing Syrups

1.5.1.2 Clinical Concentrates

1.5.2 Functional Shots

1.5.2.1 Energy + Electrolyte Shots

1.5.2.2 Recovery / Immunity Shots

2. By Formulation

2.1 Isotonic Drinks

2.1.1 Standard Isotonic Formulations

2.1.2 Low-Calorie Isotonic Drinks

2.2 Hypotonic Drinks

2.2.1 Rapid-Absorption Sports Drinks

2.2.2 Fitness / Gym Hydration

2.3 Hypertonic Drinks

2.3.1 Energy + Electrolyte Combinations

2.3.2 Recovery-Focused Hypertonic Drinks

2.4 Low/No Sugar / Natural Sweeteners

2.4.1 Stevia / Monk Fruit Sweetened Drinks

2.4.2 Naturally Flavored Electrolyte Drinks

2.5 Fortified Drinks

2.5.1 Vitamins & Minerals

2.5.2 Amino Acids & Adaptogens

3. By Ingredient Source

3.1 Natural Sources

3.1.1 Coconut Water-Based

3.1.1.1 Pure Coconut Water Electrolyte Drinks

3.1.1.2 Flavored Coconut Water Beverages

3.1.1.3 Blended Coconut + Fruit Extract Hydration Drinks

3.1.2 Fruit Extract-Based

3.1.2.1 Citrus-Based Electrolyte Drinks (Orange, Lemon, Lime)

3.1.2.2 Berry-Based Electrolyte Drinks (Strawberry, Blueberry, Acai)

3.1.2.3 Mixed Fruit & Tropical Blends

3.1.3 Sea Salt & Mineral Extracts

3.1.3.1 Natural Sea Salt-Based Electrolytes

3.1.3.2 Mineral-Rich Ocean Extract Blends

3.1.3.3 Trace Mineral Electrolyte Formulations

3.2 Synthetic / Mineral Salts

3.2.1 Sodium-Based Formulations

3.2.1.1 Standard Sodium Electrolytes

3.2.1.2 Low-Sodium Hydration Variants

3.2.1.3 Enhanced Sodium + Glucose ORS Formulations

3.2.2 Potassium-Based Formulations

3.2.2.1 Potassium Chloride-Based Drinks

3.2.2.2 Potassium Citrate / Bicarbonate Electrolytes

3.2.2.3 Potassium + Magnesium Balanced Formulations

3.2.3 Magnesium / Calcium Electrolytes

3.2.3.1 Magnesium-Fortified Drinks

3.2.3.2 Calcium + Magnesium Balanced Hydration Drinks

3.2.3.3 Mineral Complex Hydration Formulations

3.3 Plant-Based Electrolytes

3.3.1 Algae / Seaweed Extracts

3.3.1.1 Algae-Based Electrolyte Powders

3.3.1.2 Seaweed Extract RTD Drinks

3.3.1.3 Blended Plant-Based Electrolyte Beverages

3.3.2 Herbal & Botanical Sources

3.3.2.1 Herbal Electrolyte Infusions (Ginseng, Ashwagandha, etc.)

3.3.2.2 Botanical + Vitamin-Fortified Drinks

3.3.2.3 Adaptogen-Enhanced Hydration Formulations

4. By Distribution Channel

4.1 Supermarkets & Hypermarkets

4.1.1 Mass-Market Chains

4.1.1.1 National Chains (e.g., Walmart, Kroger, Tesco)

4.1.1.2 Regional / Local Chains

4.1.2 Premium Retail Outlets

4.1.2.1 Health-Focused Supermarkets (e.g., Whole Foods, Trader Joe’s)

4.1.2.2 Organic / Specialty Grocery Stores

4.2 Convenience Stores

4.2.1 Global Convenience Chains (e.g., 7-Eleven, Circle K)

4.2.1.1 Standard RTD Offerings

4.2.1.2 Premium / Functional Hydration RTD Drinks

4.2.2 Local / Independent Convenience Stores

4.2.2.1 Single-Serve Sachets / Powder Packs

4.2.2.2 Functional Shots & Tablets

4.3 Online Retail / E-commerce

4.3.1 DTC Subscription Platforms

4.3.1.1 Personalized Hydration Packs

4.3.1.2 Flavor / Electrolyte Customization Services

4.3.1.3 Bundled Fitness & Wellness Packages

4.3.2 E-commerce Marketplaces

4.3.2.1 Global Marketplaces (e.g., Amazon, Alibaba)

4.3.2.2 Regional / Local Online Retailers

4.3.2.3 Specialty Functional Beverage Stores Online

4.4 Specialty Sports & Nutrition Stores

4.4.1 Global Specialty Chains (e.g., GNC, Vitamin Shoppe)

4.4.1.1 Sports-Focused RTD & Powdered Mixes

4.4.1.2 Recovery & Immunity Fortified Products

4.4.2 Local / Independent Specialty Stores

4.4.2.1 Plant-Based & Natural Electrolyte Offerings

4.4.2.2 Clinical / Pediatric Hydration Products

4.5 Pharmacies & Hospitals

4.5.1 Retail Pharmacies

4.5.1.1 Clinical & Pediatric ORS Packs

4.5.1.2 Low-Sugar / Functional RTD Drinks

4.5.2 Hospitals & Clinical Institutions

4.5.2.1 Inpatient Hydration Solutions

4.5.2.2 Emergency & Outpatient ORS Packs

4.6 Foodservice & Vending

4.6.1 Workplace / Office Vending

4.6.1.1 RTD Beverages

4.6.1.2 Powder / Sachet-Based Solutions

4.6.2 Gyms / Fitness Centers Vending

4.6.2.1 Recovery & Performance Drinks

4.6.2.2 Single-Serve Tablets & Shots

4.6.3 Public Vending & Convenience Kiosks

4.6.3.1 RTD Beverages

4.6.3.2 Functional Shots

5. By End User

5.1 Athletes & Sports Enthusiasts

5.1.1 Professional Athletes

5.1.1.1 Team Sports Athletes (Football, Basketball, Soccer, etc.)

5.1.1.2 Individual Sport Athletes (Tennis, Swimming, Track & Field, etc.)

5.1.1.3 Endurance Athletes (Marathon, Triathlon, Cycling)

5.1.2 Amateur / Recreational Sports

5.1.2.1 Weekend / Hobbyist Athletes

5.1.2.2 Community & School Sports Participants

5.1.2.3 Adventure & Outdoor Sports Enthusiasts (Climbing, Hiking, etc.)

5.2 Fitness & Gym-Goers

5.2.1 Weight Training & Bodybuilding

5.2.1.1 Strength Training & Muscle Recovery

5.2.1.2 Pre-Workout & Post-Workout Hydration

5.2.2 Cardio & Endurance Training

5.2.2.1 Running & Cycling Enthusiasts

5.2.2.2 HIIT & Functional Fitness Participants

5.2.2.3 Aerobic / Spin Class Participants

5.3 General Wellness Consumers

5.3.1 Office / Urban Consumers

5.3.1.1 Daily Hydration for Work & Productivity

5.3.1.2 Stress-Related Recovery Drinks

5.3.2 Lifestyle & Health-Focused Individuals

5.3.2.1 Diet & Weight Management Consumers

5.3.2.2 Functional / Immunity-Boosting Hydration

5.3.2.3 Plant-Based & Clean-Label Enthusiasts

5.4 Pediatric & Geriatric Patients

5.4.1 Clinical Pediatric Use

5.4.1.1 Hospitalized Children (ORS & Clinical Hydration)

5.4.1.2 Outpatient Pediatric Hydration Packs

5.4.1.3 School / Daycare Hydration Solutions

5.4.2 Geriatric / Elderly Use

5.4.2.1 Assisted Living & Nursing Homes

5.4.2.2 Home Care & Elderly Hydration Packs

5.4.2.3 Clinical / Hospital Elderly Solutions

5.5 Occupational Workers

5.5.1 Construction & Outdoor Labor

5.5.1.1 High-Heat & Sun-Exposed Workers

5.5.1.2 Labor-Intensive Tasks (Mining, Agriculture, etc.)

5.5.1.3 On-Site RTD & Sachet Solutions

5.5.2 Logistics & Transportation Workers

5.5.2.1 Long-Haul Drivers & Delivery Personnel

5.5.2.2 Warehouse & Distribution Center Workers

5.5.2.3 Shift Workers & Rotational Teams

6.By Region

6.1North America

6.2 Europe

6.3 Asia-Pacific

6.4 Latin America

6.5 Middle East & Africa

Regional Insights of Global Electrolyte Hydration Drinks Market

Leading Companies in the Global Electrolyte Hydration Drinks Market

- PepsiCo (Gatorade) – largest global player

- The Coca-Cola Company (Powerade; BodyArmor)

- Abbott Laboratories – clinical nutrition & ORS

- Nestlé S.A. – sports nutrition & beverages

- Suntory Holdings Limited

- Vital Pharmaceuticals / BodyArmor

- Sixty Degrees / Emerging Functional Brands

- GlaxoSmithKline – oral rehydration

- Hector Beverage – regional functional drinks

- Regional DTC & Specialty Brands

Competition Focus: Product innovation, distribution reach, athlete endorsements, clinical validation. Conglomerates dominate retail; DTC brands capture niche/premium markets.PepsiCo is the largest company in the Electrolyte Hydration Drinks Market

Strategic Intelligence & AI-Backed Insights

- Market modeling: Pheonix Demand Forecast Engine analyzed hydration physiology, climate-driven dehydration incidence, and ingredient adoption across RTD/powder/ORS formats.

- Production mapping: Rising investments in beverage plants, powder-sachet filling, and ORS manufacturing in APAC and North America.

- Consumer sentiment: Strong shift toward clinically validated formulas, sustainability, and low/zero-sugar labeling.

- Porter’s Five Forces Analysis: Moderate supplier power for specialized blends; high buyer power in commoditized powder and RTD segments due to pricing pressure and substitution.

Why the Global Electrolyte Hydration Drinks Market Remains Critical

1. Prevents dehydration-related health risks in athletes, occupational workers, pediatric, and elderly populations.

2. Supports performance, recovery, and cognitive function, essential for fitness and workplace safety.

3. Enables rapid innovation bridging clinical and lifestyle applications.

4. Acts as a gateway category for functional beverage adoption and recurring subscription revenue.

5. Responds to climate and public-health pressures, making hydration a frontline mitigation.

Final Takeaway of Global Electrolyte Hydration Drinks Market

The Global Electrolyte Hydration Drinks Market is progressively evolving into a premium-focused, innovation-driven, and clinically validated functional beverage segment. The projected CAGR of ~6.0% during 2025–2033 reflects steady growth, fueled by rising global health and fitness awareness, increased demand for low/zero-sugar formulations, adoption of plant-based electrolytes, and expanding workplace hydration initiatives.

Future growth is expected to follow a dual-structure model, with high-margin RTD and personalized hydration solutions targeting athletes, wellness enthusiasts, and vulnerable populations such as pediatric and geriatric users, alongside scalable powdered mixes, sachets, and affordable ORS solutions designed for mass-market adoption and occupational hydration in emerging regions. Premiumization and flavor innovation strategies are increasingly overlapping with this, driving appeal through functional benefits and taste

Companies that invest in AI-driven formulation optimization, ingredient traceability, sustainable packaging, direct-to-consumer subscriptions, and omnichannel distribution across retail, e-commerce, workplace, and clinical channels are positioned to secure stronger competitive advantages and long-term profitability.

At Pheonix Research, our advanced forecasting and market intelligence frameworks deliver detailed revenue projections, competitive insights, and strategic growth recommendations, empowering manufacturers, retailers, and investors to capitalize on the evolving Post-2025 functional hydration landscape with data-backed, scalable expansion strategies.

📢 Social Mentions & Publication Channels

Explore deeper insights and follow our cross-platform updates on LinkedIn, and X for continuous intelligence and market coverage.

LinkedIn : https://www.linkedin.com/feed/update/urn:li:activity:7430119303322173440

X : https://x.com/Pheonix_Insight/status/2024363907826274702?s=20

Table of Contents

1. Market Forecast Snapshot (2026–2033)

1.1 2025 Market Size – USD 16.2 Billion

1.2 2033 Market Size – ~USD 27.9 Billion

1.3 CAGR (2025–2033) – ~6.0%

1.4 Largest Market – North America

1.5 Fastest Growing Region – Asia-Pacific

1.6 Major Product Segment – RTD & Powdered Mixes

1.7 Key Trend – Low/No-Sugar Formulations, Natural Electrolyte Sources

1.8 Future Focus – Clinical-grade ORS, Personalized Hydration, Sustainable Packaging

2. Global Market Overview

2.1 Product Categories

2.1.1 Ready-to-Drink (RTD) Beverages

2.1.2 Powdered Mixes & Sachets

2.1.3 Effervescent / Dissolvable Tablets

2.1.4 Clinical Oral Rehydration Solutions (ORS)

2.1.5 Others (Concentrates, Shots)

2.2 Market Evolution & Drivers

2.2.1 Rising Health & Fitness Awareness

2.2.2 Demand for Low/Zero-Sugar & Natural Formulations

2.2.3 Pediatric & Geriatric Adoption

2.2.4 Workplace Hydration Programs

2.2.5 Convenience & On-the-Go Formats

2.2.6 E-commerce & Subscription Models

3. Key Drivers of Market Growth

3.1 Rising Health & Fitness Culture

3.2 Shift to Low-Sugar & Functional Drinks

3.3 Convenience & On-the-Go Formats

3.4 Clinical & Pediatric Use

3.5 E-commerce & Subscriptions

3.6 Climate & Occupational Needs

4. Market Segmentation by Product Type

4.1 Ready-to-Drink (RTD) Beverages

4.1.1 Sports & Performance Drinks

4.1.1.1 Low-Calorie / Low-Sugar RTD Drinks

4.1.1.2 Standard Sugar RTD Sports Drinks

4.1.2 Functional Hydration Beverages

4.1.2.1 Vitamin-Fortified RTD Drinks

4.1.2.2 Amino Acid / Recovery RTD Drinks

4.1.3 Premium & Lifestyle Hydration RTD

4.1.3.1 Plant-Based Electrolyte RTD Drinks

4.1.3.2 Adaptogen-Infused RTD Beverages

4.2 Powdered Mixes & Sachets

4.2.1 Single-Serve Sachets

4.2.1.1 Isotonic Hydration Sachets

4.2.1.2 Hypotonic / Rapid-Absorption Sachets

4.2.1.3 Hypertonic / Energy + Electrolyte Sachets

4.2.2 Multi-Serve Powder Packs

4.2.2.1 Fitness & Gym-Oriented Packs

4.2.2.2 Workplace / Occupational Packs

4.2.2.3 Clinical & Pediatric Packs

4.3 Effervescent / Dissolvable Tablets

4.3.1 Single-Serving Tablets

4.3.1.1 Sports Performance Tablets

4.3.1.2 Recovery & Immunity Tablets

4.3.2 Multi-Serving Tubes

4.3.2.1 Fitness / Gym-Focused Tubes

4.3.2.2 General Wellness Tubes

4.4 Clinical Oral Rehydration Solutions (ORS)

4.4.1 Pediatric ORS

4.4.1.1 Sachet-Based Pediatric ORS

4.4.1.2 RTD Pediatric ORS

4.4.2 Geriatric / Elderly ORS

4.4.2.1 RTD Elderly Formulations

4.4.2.2 Powder-Based Elderly ORS

4.4.3 Hospital / Clinical ORS

4.4.3.1 Inpatient Hydration Packs

4.4.3.2 Outpatient & Emergency ORS Solutions

4.5 Others (Concentrates, Shots)

4.5.1 Concentrated Electrolyte Syrups

4.5.1.1 DIY RTD Mixing Syrups

4.5.1.2 Clinical Concentrates

4.5.2 Functional Shots

4.5.2.1 Energy + Electrolyte Shots

4.5.2.2 Recovery / Immunity Shots

5. Market Segmentation by Formulation

5.1 Isotonic Drinks

5.1.1 Standard Isotonic Formulations

5.1.2 Low-Calorie Isotonic Drinks

5.2 Hypotonic Drinks

5.2.1 Rapid-Absorption Sports Drinks

5.2.2 Fitness / Gym Hydration

5.3 Hypertonic Drinks

5.3.1 Energy + Electrolyte Combinations

5.3.2 Recovery-Focused Hypertonic Drinks

5.4 Low/No Sugar / Natural Sweeteners

5.4.1 Stevia / Monk Fruit Sweetened Drinks

5.4.2 Naturally Flavored Electrolyte Drinks

5.5 Fortified Drinks

5.5.1 Vitamins & Minerals

5.5.2 Amino Acids & Adaptogens

6. Market Segmentation by Ingredient Source

6.1 Natural Sources

6.1.1 Coconut Water-Based

6.1.1.1 Pure Coconut Water Electrolyte Drinks

6.1.1.2 Flavored Coconut Water Beverages

6.1.1.3 Blended Coconut + Fruit Extract Hydration Drinks

6.1.2 Fruit Extract-Based

6.1.2.1 Citrus-Based Electrolyte Drinks

6.1.2.2 Berry-Based Electrolyte Drinks

6.1.2.3 Mixed Fruit & Tropical Blends

6.1.3 Sea Salt & Mineral Extracts

6.1.3.1 Natural Sea Salt-Based Electrolytes

6.1.3.2 Mineral-Rich Ocean Extract Blends

6.1.3.3 Trace Mineral Electrolyte Formulations

6.2 Synthetic / Mineral Salts

6.2.1 Sodium-Based Formulations

6.2.1.1 Standard Sodium Electrolytes

6.2.1.2 Low-Sodium Hydration Variants

6.2.1.3 Enhanced Sodium + Glucose ORS Formulations

6.2.2 Potassium-Based Formulations

6.2.2.1 Potassium Chloride-Based Drinks

6.2.2.2 Potassium Citrate / Bicarbonate Electrolytes

6.2.2.3 Potassium + Magnesium Balanced Formulations

6.2.3 Magnesium / Calcium Electrolytes

6.2.3.1 Magnesium-Fortified Drinks

6.2.3.2 Calcium + Magnesium Balanced Hydration Drinks

6.2.3.3 Mineral Complex Hydration Formulations

6.3 Plant-Based Electrolytes

6.3.1 Algae / Seaweed Extracts

6.3.1.1 Algae-Based Electrolyte Powders

6.3.1.2 Seaweed Extract RTD Drinks

6.3.1.3 Blended Plant-Based Electrolyte Beverages

6.3.2 Herbal & Botanical Sources

6.3.2.1 Herbal Electrolyte Infusions

6.3.2.2 Botanical + Vitamin-Fortified Drinks

6.3.2.3 Adaptogen-Enhanced Hydration Formulations

7. Market Segmentation by Distribution Channel

7.1 Supermarkets & Hypermarkets

7.1.1 Mass-Market Chains

7.1.1.1 National Chains (Walmart, Kroger, Tesco)

7.1.1.2 Regional / Local Chains

7.1.2 Premium Retail Outlets

7.1.2.1 Health-Focused Supermarkets (Whole Foods, Trader Joe’s)

7.1.2.2 Organic / Specialty Grocery Stores

7.2 Convenience Stores

7.2.1 Global Convenience Chains (7-Eleven, Circle K)

7.2.1.1 Standard RTD Offerings

7.2.1.2 Premium / Functional Hydration RTD Drinks

7.2.2 Local / Independent Convenience Stores

7.2.2.1 Single-Serve Sachets / Powder Packs

7.2.2.2 Functional Shots & Tablets

7.3 Online Retail / E-commerce

7.3.1 DTC Subscription Platforms

7.3.1.1 Personalized Hydration Packs

7.3.1.2 Flavor / Electrolyte Customization Services

7.3.1.3 Bundled Fitness & Wellness Packages

7.3.2 E-commerce Marketplaces

7.3.2.1 Global Marketplaces (Amazon, Alibaba)

7.3.2.2 Regional / Local Online Retailers

7.3.2.3 Specialty Functional Beverage Stores Online

7.4 Specialty Sports & Nutrition Stores

7.4.1 Global Specialty Chains (GNC, Vitamin Shoppe)

7.4.1.1 Sports-Focused RTD & Powdered Mixes

7.4.1.2 Recovery & Immunity Fortified Products

7.4.2 Local / Independent Specialty Stores

7.4.2.1 Plant-Based & Natural Electrolyte Offerings

7.4.2.2 Clinical / Pediatric Hydration Products

7.5 Pharmacies & Hospitals

7.5.1 Retail Pharmacies

7.5.1.1 Clinical & Pediatric ORS Packs

7.5.1.2 Low-Sugar / Functional RTD Drinks

7.5.2 Hospitals & Clinical Institutions

7.5.2.1 Inpatient Hydration Solutions

7.5.2.2 Emergency & Outpatient ORS Packs

7.6 Foodservice & Vending

7.6.1 Workplace / Office Vending

7.6.1.1 RTD Beverages

7.6.1.2 Powder / Sachet-Based Solutions

7.6.2 Gyms / Fitness Centers Vending

7.6.2.1 Recovery & Performance Drinks

7.6.2.2 Single-Serve Tablets & Shots

7.6.3 Public Vending & Convenience Kiosks

7.6.3.1 RTD Beverages

7.6.3.2 Functional Shots

8. Market Segmentation by End User

8.1 Athletes & Sports Enthusiasts

8.1.1 Professional Athletes

8.1.1.1 Team Sports (Football, Basketball, Soccer)

8.1.1.2 Individual Sports (Tennis, Swimming, Track & Field)

8.1.1.3 Endurance Athletes (Marathon, Triathlon, Cycling)

8.1.2 Amateur / Recreational Sports

8.1.2.1 Weekend / Hobbyist Athletes

8.1.2.2 Community & School Sports Participants

8.1.2.3 Adventure & Outdoor Sports Enthusiasts

8.2 Fitness & Gym-Goers

8.2.1 Weight Training & Bodybuilding

8.2.1.1 Strength Training & Muscle Recovery

8.2.1.2 Pre-Workout & Post-Workout Hydration

8.2.2 Cardio & Endurance Training

8.2.2.1 Running & Cycling Enthusiasts

8.2.2.2 HIIT & Functional Fitness Participants

8.2.2.3 Aerobic / Spin Class Participants

8.3 General Wellness Consumers

8.3.1 Office / Urban Consumers

8.3.1.1 Daily Hydration for Work & Productivity

8.3.1.2 Stress-Related Recovery Drinks

8.3.2 Lifestyle & Health-Focused Individuals

8.3.2.1 Diet & Weight Management Consumers

8.3.2.2 Functional / Immunity-Boosting Hydration

8.3.2.3 Plant-Based & Clean-Label Enthusiasts

8.4 Pediatric & Geriatric Patients

8.4.1 Clinical Pediatric Use

8.4.1.1 Hospitalized Children (ORS & Clinical Hydration)

8.4.1.2 Outpatient Pediatric Hydration Packs

8.4.1.3 School / Daycare Hydration Solutions

8.4.2 Geriatric / Elderly Use

8.4.2.1 Assisted Living & Nursing Homes

8.4.2.2 Home Care & Elderly Hydration Packs

8.4.2.3 Clinical / Hospital Elderly Solutions

8.5 Occupational Workers

8.5.1 Construction & Outdoor Labor

8.5.1.1 High-Heat & Sun-Exposed Workers

8.5.1.2 Labor-Intensive Tasks (Mining, Agriculture)

8.5.1.3 On-Site RTD & Sachet Solutions

8.5.2 Logistics & Transportation Workers

8.5.2.1 Long-Haul Drivers & Delivery Personnel

8.5.2.2 Warehouse & Distribution Center Workers

8.5.2.3 Shift Workers & Rotational Teams

9. Market Segmentation by Region

9.1 North America

9.2 Europe

9.3 Asia-Pacific

9.4 Latin America

9.5 Middle East & Africa

10. Regional Insights

10.1 North America – Market Leader

10.2 Europe – Mature Market

10.3 Asia-Pacific – Fastest Growing

10.4 Latin America – Growing Demand

10.5 Middle East & Africa – Climate-Driven Adoption

11. Leading Companies

11.1 PepsiCo (Gatorade) – Largest Global Player

11.2 The Coca-Cola Company (Powerade; BodyArmor)

11.3 Abbott Laboratories – Clinical Nutrition & ORS

11.4 Nestlé S.A. – Sports Nutrition & Beverages

11.5 Suntory Holdings Limited

11.6 Vital Pharmaceuticals / BodyArmor

11.7 Sixty Degrees / Emerging Functional Brands

11.8 GlaxoSmithKline – Oral Rehydration

11.9 Hector Beverage – Regional Functional Drinks

11.10 Regional DTC & Specialty Brands

12. Strategic Intelligence & AI Insights

12.1 Market Modeling & Forecast Engine

12.2 Production & Manufacturing Mapping

12.3 Consumer Sentiment Analysis

12.4 Porter’s Five Forces Analysis

13. Market Significance

13.1 Health & Dehydration Prevention

13.2 Performance & Recovery Enhancement

13.3 Clinical & Lifestyle Bridging

13.4 Subscription & Recurring Revenue Opportunities

13.5 Climate & Public-Health Relevance

14. Final Takeaway

14.1 Market Evolution – Premium & Clinically Validated

14.2 Projected Growth – CAGR ~6.0% (2025–2033)

14.3 Dual-Structure Growth Model – RTD & Personalized Hydration + Powdered/ORS Mass Market

14.4 Strategic Investment Areas – AI Formulation, Traceability, Sustainable Packaging, Omnichannel Distribution

14.5 Pheonix Research Insights – Forecast, Competitive Intelligence & Growth Strategy

15. References

16. Appendix

17. About Us

18. Disclaimer

Competitive Landscape

Competitive Landscape of the Global Electrolyte Hydration Drinks Market

Executive Framing

The global electrolyte hydration drinks market is characterized by high competitive intensity and a semi-consolidated structure, where Tier 1 beverage conglomerates dominate large-scale retail distribution while emerging direct-to-consumer (DTC) and niche functional brands aggressively compete in premium and personalized hydration segments. This dual-structure competition creates a dynamic ecosystem where scale, branding, and distribution power coexist with innovation, agility, and specialization.

As hydration evolves from a traditional sports-drink category into a broader functional and clinical wellness segment, companies are increasingly competing across multiple dimensions—formulation science, low/zero-sugar innovation, clean-label positioning, and clinical validation. Strategic differentiation is no longer limited to taste or branding; it now includes electrolyte composition, ingredient sourcing, and targeted health outcomes such as recovery, immunity, and cognitive hydration.

Understanding the competitive behavior within this landscape is critical, as companies navigate shifting consumer preferences, regulatory scrutiny on sugar and claims, and growing demand for sustainable and personalized hydration solutions.

Current Market Reality

The current market is led by global beverage giants such as PepsiCo (Gatorade) and The Coca-Cola Company (Powerade, BodyArmor), which leverage extensive distribution networks, strong brand equity, and athlete endorsements to maintain dominant positions, particularly in North America and Europe. These players benefit from economies of scale and shelf visibility across supermarkets, convenience stores, and vending channels.

However, the market is simultaneously witnessing rapid fragmentation at the premium and functional end. Emerging brands and regional players are capitalizing on trends such as plant-based electrolytes, adaptogen-infused drinks, and low/zero-sugar formulations. Companies like Abbott Laboratories and GlaxoSmithKline differentiate themselves through clinical-grade oral rehydration solutions (ORS), targeting hospitals, pediatric, and geriatric segments—areas less penetrated by traditional beverage companies.

Competitive actions in this market are increasingly aggressive and innovation-driven. Major brands are continuously reformulating products to reduce sugar content and introduce natural sweeteners such as stevia and monk fruit. At the same time, new entrants are leveraging e-commerce and subscription models to bypass traditional retail barriers and offer personalized hydration solutions.

Regional expansion is another defining feature. Asia-Pacific has become a hotspot for investment, with companies expanding sachet-based and affordable hydration formats tailored to local consumption patterns and climate conditions. Similarly, workplace hydration programs and institutional sales channels are emerging as new battlegrounds for competition.

Key Signals And Evidence

Several key signals highlight the evolving competitive dynamics of the electrolyte hydration drinks market. One of the most prominent is the shift toward low/zero-sugar and clean-label formulations. Leading players are investing heavily in reformulation strategies to align with regulatory pressures and consumer demand for healthier alternatives.

The rise of personalized hydration is another critical signal. Companies are increasingly offering customized electrolyte blends through DTC platforms, enabling consumers to select formulations based on activity levels, climate, and health needs. This trend reflects a broader move toward precision nutrition and recurring revenue models.

Strategic partnerships and product innovation are also shaping the market. Collaborations between ingredient suppliers and beverage manufacturers are accelerating the development of plant-based and mineral-rich electrolyte sources, including coconut water, sea minerals, and botanical extracts. These innovations enhance product differentiation and support premium pricing strategies.Investment in manufacturing capabilities, particularly in powder-sachet filling and RTD production, indicates strong confidence in long-term demand. Companies are expanding production footprints in Asia-Pacific and North America to meet rising consumption and improve supply chain efficiency.

Strategic Implications

The competitive dynamics of the electrolyte hydration drinks market necessitate a multi-pronged strategic approach. For established players, maintaining leadership requires continuous investment in product innovation, brand positioning, and global distribution expansion. Leveraging athlete endorsements and large-scale marketing campaigns remains essential, but must now be complemented by health-focused messaging and clean-label transparency.

For emerging and DTC brands, differentiation through formulation, personalization, and digital engagement is critical. The ability to offer tailored hydration solutions and build strong consumer relationships through subscription models provides a competitive edge in premium segments.Clinical-grade hydration represents a significant opportunity for both pharmaceutical and beverage companies. Expanding into pediatric, geriatric, and hospital-based applications allows companies to tap into stable, high-trust demand segments with less price sensitivity.

Sustainability is becoming a key competitive lever. Companies investing in eco-friendly packaging, recyclable materials, and reduced carbon footprints are likely to gain favor among environmentally conscious consumers and regulators.

Additionally, omnichannel distribution strategies are essential. Success in this market increasingly depends on the ability to integrate retail, e-commerce, workplace vending, and institutional sales channels into a cohesive go-to-market strategy.

Forward Outlook

Looking ahead to 2033, the electrolyte hydration drinks market is expected to evolve into a more innovation-driven and segmented ecosystem. While large players will continue to dominate volume-driven RTD categories, high-growth opportunities will emerge in personalized hydration, clinical-grade solutions, and plant-based electrolyte formulations.

In the near term, intensified competition around low/zero-sugar products and natural ingredient sourcing will shape product pipelines. Companies that can balance taste, functionality, and health benefits will gain a competitive advantage.

Over the medium term, the market may experience selective consolidation as larger players acquire innovative startups to strengthen their portfolios and accelerate entry into niche segments. However, the relatively low barriers to entry in DTC and functional beverage categories will continue to encourage new entrants.

Technological integration, including AI-driven formulation and consumer analytics, will further enhance product development and personalization capabilities. Companies leveraging these technologies will be better positioned to respond to evolving consumer needs and optimize their offerings.

In the long term, the convergence of clinical and lifestyle hydration will redefine the competitive landscape. Brands that successfully bridge this gap—offering scientifically validated, consumer-friendly products—will emerge as leaders in the next phase of market evolution. As climate conditions, health awareness, and functional beverage adoption continue to rise, the electrolyte hydration drinks market will remain a critical and highly competitive segment within the global beverage industry.

Value Chain

Global Electrolyte Hydration Drinks Market: Value Chain & Market Dynamics

Executive Framing

In the rapidly expanding electrolyte hydration drinks market, the value chain is becoming increasingly sophisticated, driven by the convergence of functional nutrition, consumer health awareness, and scalable beverage manufacturing. As hydration shifts from a basic necessity to a performance and wellness-driven category, the underlying supply chain must support diverse product formats, ingredient sourcing strategies, and omnichannel distribution models.

The market operates through a hybrid value chain, combining large-scale beverage manufacturing with niche, innovation-led formulation ecosystems. While traditional beverage giants leverage established bottling and distribution infrastructure, emerging brands focus on customization, clinical validation, and direct-to-consumer (DTC) channels. This dual structure introduces both efficiency and fragmentation across the value chain.

However, challenges persist in ingredient traceability, especially for natural electrolyte sources such as coconut water, plant-based minerals, and botanical extracts. Additionally, regulatory oversight on sugar content, health claims, and clinical efficacy introduces compliance complexities that directly impact formulation, labeling, and go-to-market strategies.

Current Market Reality

The current value chain of the electrolyte hydration drinks market is characterized by moderate-to-high complexity, reflecting the balance between mass production efficiency and increasing product differentiation. Leading players such as PepsiCo (Gatorade) and The Coca-Cola Company (Powerade, BodyArmor) dominate upstream procurement and downstream distribution through vertically integrated operations.

At the upstream level, sourcing strategies vary significantly. Synthetic electrolyte blends (sodium, potassium, magnesium salts) provide cost efficiency and consistency, while natural and plant-based sources introduce variability in quality, pricing, and supply continuity. This divergence creates a tiered supplier ecosystem, influencing cost structures and margin distribution.

Midstream operations involve formulation, blending, and packaging across multiple formats—RTD beverages, powdered sachets, effervescent tablets, and clinical ORS solutions. Increasing demand for low/zero-sugar, fortified, and clean-label products has intensified R&D requirements, pushing manufacturers toward advanced formulation technologies and AI-assisted product development.

Downstream, the market exhibits a highly diversified distribution network, including supermarkets, convenience stores, e-commerce platforms, specialty nutrition outlets, and clinical channels. The rise of DTC subscription models and personalized hydration solutions is reshaping traditional retail dominance, enabling smaller brands to bypass conventional distribution barriers.

Despite these advancements, traceability gaps in natural ingredients and sustainability concerns in packaging remain key bottlenecks, particularly as regulatory scrutiny intensifies across major markets.

Key Signals and Evidence

Several critical signals highlight the evolving dynamics of the electrolyte hydration drinks value chain:

- The market’s projected growth from USD 16.2 billion (2025) to ~USD 27.9 billion (2033) at a CAGR of ~6.0% reflects steady expansion driven by both lifestyle and clinical demand.

- A strong shift toward low/zero-sugar formulations and natural electrolyte sources is reshaping upstream sourcing and midstream formulation priorities.

- The dominance of RTD and powdered mixes indicates a dual-demand structure—premium convenience versus scalable affordability.

- Rapid growth in Asia-Pacific underscores the importance of localized sourcing, sachet-based distribution, and cost-efficient manufacturing models.

- Increasing adoption of clinical-grade ORS and personalized hydration signals convergence between healthcare and consumer beverage value chains.

Additionally, the rise of e-commerce and subscription-based models introduces new power dynamics, strengthening the position of brands with strong digital capabilities while reducing reliance on traditional retail intermediaries.

However, supplier power remains moderate for specialized and natural ingredients, while buyer power is high in commoditized segments such as standard RTD sports drinks and powdered mixes, where price sensitivity and brand switching are prevalent.

Strategic Implications

The evolving value chain presents both opportunities and structural challenges for market participants. Companies must strategically manage the trade-off between scale efficiency and product differentiation.

Large beverage companies are expected to continue leveraging their distribution dominance and manufacturing scale, while simultaneously investing in premium product lines, sustainable packaging, and functional innovation to defend market share against agile DTC brands.

For emerging and niche players, value chain agility becomes a key competitive advantage. The ability to source unique ingredients, develop targeted formulations (e.g., pediatric ORS, athlete-specific hydration), and leverage digital distribution channels enables differentiation without requiring large-scale infrastructure.

Technology integration will play a pivotal role in optimizing value chain performance. AI-driven formulation, demand forecasting, and supply chain analytics, along with blockchain-enabled ingredient traceability, are expected to enhance transparency, reduce inefficiencies, and improve regulatory compliance.

Furthermore, sustainable packaging and circular supply chain models will become increasingly critical, not only for regulatory alignment but also for meeting evolving consumer expectations around environmental responsibility.

Forward Outlook

Looking ahead, the electrolyte hydration drinks market value chain is set to undergo significant transformation, driven by innovation, digitalization, and sustainability imperatives.

The near-to-medium term will likely witness:

- Greater integration of clinical and consumer hydration ecosystems, particularly through ORS and medically validated products

- Expansion of personalized hydration solutions, enabled by data-driven insights and subscription platforms

- Increased investment in regional manufacturing hubs, especially in Asia-Pacific, to support localized demand and cost optimization

- Enhanced focus on sustainable sourcing and packaging, addressing both regulatory pressures and consumer preferences

As the market evolves, companies that can ensure ingredient transparency, optimize multi-format production, and build resilient omnichannel distribution networks will be best positioned to capture long-term value.

In conclusion, the electrolyte hydration drinks market is transitioning from a traditional beverage category into a multi-dimensional functional ecosystem, where value chain efficiency, innovation capability, and regulatory alignment collectively determine competitive success.

Investment Activity

Investment & Funding Dynamics – Global Electrolyte Hydration Drinks Market

Executive Framing

The investment and funding dynamics within the global electrolyte hydration drinks market are becoming increasingly strategic as the category evolves from conventional sports beverages into a broader functional and clinical hydration ecosystem. Capital allocation in this market is no longer driven solely by volume growth; instead, it reflects a convergence of health trends, formulation innovation, and distribution transformation. Investors are recognizing electrolyte hydration as a resilient, repeat-consumption category with strong cross-demographic demand spanning athletes, wellness consumers, and clinical users.

As regulatory scrutiny around sugar content, labeling, and health claims intensifies, and as consumer expectations shift toward clean-label, low-sugar, and functional beverages, investment strategies are increasingly focused on companies that can deliver differentiated, science-backed hydration solutions. Sustainability considerations, particularly in packaging and ingredient sourcing, are also emerging as critical factors influencing capital deployment.

The rising influx of venture capital, private equity, and strategic corporate investments signals a broader transition toward premiumization, personalization, and clinical integration, positioning the market as an attractive long-term investment opportunity within the global functional beverage landscape.

Current Market Reality

The electrolyte hydration drinks market is witnessing strong and diversified investment activity across multiple layers of the value chain. Major beverage conglomerates such as PepsiCo, The Coca-Cola Company, and Nestlé continue to invest heavily in expanding their hydration portfolios while acquiring or partnering with emerging brands to capture premium and niche segments.

Private equity firms and venture capital investors are actively backing DTC hydration startups, plant-based beverage innovators, and clinical-grade ORS companies. These investments are complemented by growing capital allocation toward manufacturing infrastructure, including RTD bottling plants and powder-sachet production facilities, particularly in North America and Asia-Pacific.

Mergers and acquisitions are accelerating, with large players acquiring fast-growing niche brands to expand into low/zero-sugar, functional, and clinical hydration segments. At the same time, digital-first brands leveraging e-commerce and subscription models are attracting funding due to their scalability and recurring revenue potential.

Key Signals And Evidence

A major investment driver is the global shift toward health-conscious consumption, pushing companies to invest in functional ingredients such as vitamins, amino acids, and plant-based electrolytes. This trend is driving increased funding in research and development, including AI-enabled formulation and personalized hydration technologies.

Declining consumer preference for high-sugar beverages is accelerating reformulation efforts, leading to investments in natural sweeteners, clean-label ingredients, and low-calorie product innovation. Additionally, the rapid growth of e-commerce and DTC channels is encouraging investments in subscription-based models and consumer data-driven product development.

Climate-driven demand patterns, particularly in Asia-Pacific, Latin America, and the Middle East, are further reinforcing investment in regional production and distribution. Meanwhile, rising clinical adoption of oral rehydration solutions (ORS) is creating a stable institutional demand base, encouraging funding for medically validated hydration products.

Strategic Implications

Companies must strategically diversify their portfolios across premium RTD beverages and scalable powdered formats while investing in clean-label formulations, sustainable packaging, and omnichannel distribution strategies. Brands that successfully combine clinical credibility with lifestyle positioning are likely to gain stronger investor confidence and competitive advantage.

For investors, the market offers a balanced mix of high-growth premium segments and stable mass-market opportunities. However, careful evaluation of brand differentiation, supply chain scalability, and regulatory compliance is essential. Strategic partnerships across beverage, ingredient, and technology ecosystems are becoming increasingly important to accelerate innovation and market penetration.

Forward Outlook

The investment environment is expected to remain highly active through 2033, driven by innovation and evolving consumer preferences. Key areas of focus will include AI-driven personalized hydration, expansion of clinical-grade ORS solutions, and advancements in sustainable packaging and circular supply chains.

M&A activity is expected to intensify, particularly targeting DTC brands and regional leaders in high-growth markets such as Asia-Pacific. Large corporations will continue to pursue acquisitions to maintain market leadership, while startups will attract funding through niche innovation and digital-first strategies.

Overall, investment trends reflect a broader shift toward health-centric, technology-enabled, and sustainability-driven consumption. Companies that combine scientific validation, consumer-focused innovation, and scalable business models will be best positioned to capitalize on long-term growth opportunities in the electrolyte hydration drinks market.

Technology & Innovation

Global Electrolyte Hydration Drinks Market: Technology & Innovation

Executive Framing

In the rapidly evolving functional beverage landscape, electrolyte hydration drinks are emerging as a critical innovation-driven segment reshaping consumer health and wellness behavior. As global awareness around hydration, fitness, and preventive healthcare intensifies, manufacturers are increasingly focusing on technologically advanced formulations and delivery formats. This shift is not merely driven by consumer preference but represents a strategic transformation toward personalized, clinically validated, and sustainable hydration solutions.

The intersection of nutrition science, ingredient innovation, and digital health is unlocking new growth avenues. From low/zero-sugar formulations to plant-based electrolyte sources, companies are leveraging technology to enhance performance, recovery, and daily hydration outcomes. This dimension is particularly relevant as demand expands beyond athletes to include pediatric, geriatric, and occupational user groups.

The market exhibits high innovation intensity and moderate patent activity, with technology maturity in a growth phase. Advancements in formulation science, AI-driven personalization, and sustainable packaging are central to this transformation. Leading players such as PepsiCo, Abbott Laboratories, and Nestlé are investing in R&D, digital platforms, and clinical validation to strengthen competitive positioning.

Current Market Reality

The current market is characterized by rapid product innovation and diversification across formats such as RTD beverages, powdered sachets, effervescent tablets, and clinical ORS solutions. Increasing consumer preference for low-sugar, clean-label, and functional beverages is pushing companies toward reformulation and premiumization strategies.

Technological advancements in ingredient sourcing—such as coconut water, plant-based electrolytes, and mineral blends—are enabling differentiation. Additionally, digital platforms and e-commerce ecosystems are facilitating personalized hydration solutions through subscription-based models.

Investment activity is accelerating, particularly in plant-based ingredients, sustainable packaging, and AI-driven nutrition platforms. Companies are also integrating smart supply chain technologies to optimize production and distribution efficiency.

Key Signals and Evidence

- Rising demand for low/zero-sugar and clean-label electrolyte formulations

- Growing adoption of plant-based and natural electrolyte sources

- Expansion of RTD and single-serve sachet formats for convenience

- Increased investment in AI-driven personalized hydration solutions

- Emergence of clinical-grade ORS and medically validated hydration products

- Shift toward sustainable packaging and eco-friendly production processes

Strategic Implications

For manufacturers, the focus is shifting toward innovation in formulation, functionality, and delivery formats. Companies must invest in R&D to develop differentiated products that meet evolving consumer expectations for health, convenience, and sustainability.

Retailers and distributors benefit from expanding omnichannel strategies, including e-commerce and direct-to-consumer models, which enable personalized offerings and recurring revenue streams. Digital engagement is becoming a critical competitive lever.

Healthcare and institutional stakeholders are increasingly adopting clinical hydration solutions, creating stable demand for ORS and medically validated products. Regulatory compliance and clinical validation will play a key role in shaping market credibility.

Forward Outlook

The future of the electrolyte hydration drinks market will be defined by personalization, clinical integration, and sustainability. AI and data analytics will enable customized hydration solutions based on individual health profiles, activity levels, and environmental conditions.

Innovation in plant-based ingredients, functional additives, and clean-label formulations will continue to drive premiumization. Additionally, sustainable packaging solutions will become a core focus as environmental concerns intensify.

Collaborative ecosystems involving manufacturers, healthcare providers, and technology platforms will accelerate innovation and market expansion. Companies that effectively integrate technology with consumer-centric strategies will be best positioned for long-term growth.

Market Risk

Global Electrolyte Hydration Drinks Market: Structural Constraints & Market Impacts

Executive Framing

In the rapidly evolving landscape of electrolyte hydration drinks, structural constraints and market dynamics are creating both opportunities and competitive pressures for industry stakeholders. As hydration shifts from a sports-centric category to a mainstream functional necessity, the market is increasingly influenced by health trends, climate conditions, and evolving consumer preferences. Despite strong growth potential, the market faces challenges such as pricing pressure, ingredient sourcing volatility, and regulatory scrutiny around sugar content and health claims.

This dimension is becoming increasingly critical as hydration integrates into preventive healthcare, workplace productivity, and lifestyle wellness. Companies must balance innovation in low/zero-sugar, plant-based, and clinically validated formulations with scalability and affordability. The interplay between premium innovation and mass-market accessibility highlights the need for strategic planning and operational efficiency to maintain long-term competitiveness.

Current Market Reality

The electrolyte hydration drinks market is currently characterized by strong demand growth coupled with rising competitive intensity. Global beverage leaders dominate the ready-to-drink (RTD) segment, while emerging brands leverage e-commerce and direct-to-consumer channels to target niche and premium consumers through personalized hydration solutions.

A key structural challenge lies in maintaining a balance between affordability and innovation. Premium RTD beverages drive margins, whereas powdered mixes and ORS solutions cater to price-sensitive markets, particularly in emerging economies. This dual-market structure requires differentiated strategies across regions and consumer segments.

Supply chain dependencies on natural ingredients such as coconut water, mineral salts, and botanical extracts introduce cost volatility and sourcing risks. At the same time, regulatory pressures regarding sugar reduction and labeling transparency are pushing companies to continuously reformulate products while maintaining taste and functionality.

Key Signals And Evidence

The market is shaped by several converging signals. A major driver is the rapid shift toward low/zero-sugar and clean-label formulations, reflecting changing consumer preferences for healthier and natural hydration options. Companies are actively reformulating products using natural sweeteners and functional ingredients.

The growth of e-commerce and subscription-based models is another strong signal, enabling personalized hydration solutions and recurring revenue streams. Brands are increasingly offering customized electrolyte blends and direct engagement with consumers through digital platforms.Climate-driven demand is also a significant factor, particularly in Asia-Pacific, Latin America, and the Middle East, where high temperatures and outdoor work conditions are increasing the need for effective hydration solutions. This has accelerated demand for both RTD and affordable powdered formats.

Strategic Implications

The market presents a dual opportunity structure, combining premiumization through advanced RTD and personalized hydration products with volume-driven growth through affordable powdered and ORS solutions. Companies must strategically align their portfolios to capture both segments effectively.

Investment in R&D is essential for developing differentiated formulations, including plant-based electrolytes, vitamin fortification, and clinically validated hydration products. These innovations enhance brand positioning and support long-term growth.

Distribution strategies are also evolving, with omnichannel approaches becoming critical. Integration across retail, e-commerce, workplace, and clinical channels enables broader reach and improved consumer engagement.

Forward Outlook

Looking ahead, the electrolyte hydration drinks market is expected to evolve toward greater personalization, clinical integration, and sustainability. Advances in data analytics and AI will enable tailored hydration solutions based on individual needs, activity levels, and environmental conditions.

Sustainability will play a growing role, with increasing emphasis on eco-friendly packaging and responsible sourcing of ingredients. Companies that invest in sustainable practices will gain competitive advantage, particularly in developed markets.

As emerging markets drive volume growth and developed markets focus on premium innovation, the industry will continue to expand under a dual-structure model. Companies that successfully balance innovation, affordability, and distribution will be best positioned to capitalize on future opportunities in the global hydration landscape.

Regulatory Landscape

Regulatory & Policy Landscape: Global Electrolyte Hydration Drinks Market

Executive Framing

The regulatory and policy environment for the Global Electrolyte Hydration Drinks Market is becoming increasingly significant as the category transitions from sports beverages to a broader functional and clinical hydration segment. Regulatory oversight is expanding across food safety, nutritional labeling, sugar reduction, and clinical claims, shaping how manufacturers develop, market, and distribute hydration products globally.

Authorities such as the U.S. Food and Drug Administration (FDA), European Food Safety Authority (EFSA), Food Safety and Standards Authority of India (FSSAI), and other regional regulators are enforcing stricter compliance standards. These frameworks focus on ingredient transparency, health claims validation, and sugar content regulation, while also addressing emerging concerns related to functional and fortified beverages.

As electrolyte drinks increasingly overlap with clinical nutrition (ORS) and wellness categories, regulatory frameworks are evolving to ensure safety, efficacy, and accurate consumer communication. This makes regulatory compliance both a critical requirement and a strategic differentiator.

Current Market Reality

The current regulatory landscape is fragmented across regions, with varying standards for classification, labeling, and permissible claims. In the United States, electrolyte drinks are primarily regulated as functional beverages under FDA food and beverage guidelines, while clinical oral rehydration solutions (ORS) may fall under more stringent medical or pharmaceutical regulations.

In Europe, EFSA imposes strict rules on health claims, ingredient usage, and sugar reduction initiatives, significantly influencing product formulation strategies. Clean-label requirements and sustainability directives are also gaining traction, particularly around packaging and ingredient sourcing.

In Asia-Pacific markets such as India and China, regulatory bodies like FSSAI and NMPA are tightening standards around labeling, sugar thresholds, and functional claims. These markets are also witnessing increased scrutiny on imported products and growing emphasis on local compliance.

Globally, rising concerns around sugar consumption, artificial additives, and misleading health claims are pushing companies to reformulate products and enhance transparency in labeling and marketing.

Key Signals and Evidence

- Stricter sugar reduction policies and taxation on sugary beverages across multiple regions.

- Increased scrutiny on functional and health claims by FDA and EFSA.

- Growing regulatory distinction between sports drinks and clinical ORS products.

- Rising compliance requirements for clean-label, natural, and plant-based ingredients.

- Expansion of sustainability and packaging regulations globally.

- Increased monitoring of e-commerce and DTC channels for product claims and labeling accuracy.

Strategic Implications

The evolving regulatory environment presents both compliance challenges and growth opportunities. Companies must invest in regulatory expertise, product reformulation, and transparent labeling practices to remain competitive. Increasing sugar taxes and labeling restrictions are accelerating the shift toward low/zero-sugar and natural formulations.

For companies operating in the clinical hydration segment, compliance requirements are significantly higher, requiring clinical validation, standardized formulations, and adherence to medical-grade regulations. This creates higher entry barriers but also enables premium positioning.

Global players benefit from scale and regulatory capabilities, while emerging brands must navigate complex regional frameworks, often relying on partnerships or localized strategies for market entry.

Forward Outlook

Looking ahead, regulatory frameworks will continue to tighten, particularly around sugar reduction, functional claims, and sustainability. Governments are expected to expand policies targeting obesity, diabetes, and public health, directly impacting electrolyte drink formulations and marketing strategies.

The clinical hydration segment, including ORS, will see increased regulatory standardization, potentially blurring the lines between food, supplement, and pharmaceutical classifications. This will drive demand for clinically validated and medically endorsed products.

Sustainability regulations related to packaging, recycling, and carbon footprint reduction will also gain prominence, influencing production and supply chain decisions. Companies that proactively align with these regulatory trends will be better positioned for long-term growth and competitive advantage.