Global Ethanol in Beverage Industry Market Report 2026-2033

Global Ethanol in Beverage Industry Market Forecast Snapshot: 2026–2033

| Metric | Value |

| 2025 Market Size | USD 412.7 Billion |

| 2033 Market Size | ~USD 568.9 Billion |

| CAGR (2026–2033) | ~4.1% |

| Largest Region | Europe |

| Fastest Growing Region | Asia-Pacific |

| Top Segment | Grain-Based Beverage Ethanol |

| Key Trend | Premium Alcoholic Beverages, Sustainable Fermentation & Clean-Label Spirits |

| Future Focus | Bio-Based Production Efficiency, AI-Driven Distillation Analytics & Low-Carbon Ethanol |

Global Ethanol in Beverage Industry Market Overview

The Global Ethanol in Beverage Industry Market is witnessing structural transformation, driven by rising global alcohol consumption, premiumization trends in spirits and craft beverages, and advancements in sustainable fermentation technologies. Beverage-grade ethanol remains a critical raw material across spirits, beer fortification, ready-to-drink (RTD) alcoholic beverages, and specialty liquors.

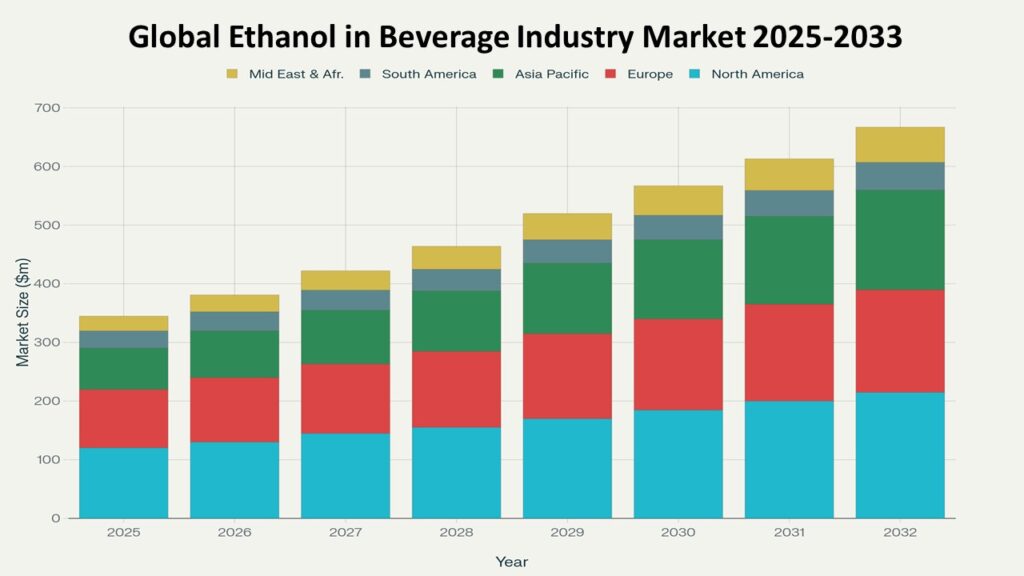

According to Phoenix Research, the Global Ethanol in Beverage Industry Market is valued at USD 412.7 billion in 2025 and is projected to reach approximately USD 568.9 billion by 2033, registering a CAGR of ~4.1% (2026–2033). This revenue forecast reflects stable alcohol demand across mature markets, premium craft expansion, increasing RTD adoption, and rising consumption in emerging economies.

Europe holds the largest market share, supported by established distillation infrastructure, strong spirits heritage, and premium export networks. Asia-Pacific is the fastest-growing region, fueled by urbanization, rising disposable incomes, and expanding beer and spirits consumption across China, India, Japan, and Southeast Asia.

The Post-2025 outlook highlights sustainable feedstock sourcing, low-carbon ethanol production, AI-enabled fermentation monitoring, premium craft distillation growth, and expanding RTD alcoholic beverage innovation as key long-term drivers

Key Drivers of Global Ethanol in Beverage Industry Market Growth

-

Growth in Premium & Craft Alcoholic Beverages

Rising consumer preference for premium spirits, craft gin, artisanal vodka, and boutique distilleries is driving higher-quality ethanol demand.

-

Expansion of Ready-to-Drink (RTD) Alcoholic Beverages

Hard seltzers, canned cocktails, and flavored malt beverages are accelerating ethanol usage in modern beverage formats.

-

Rising Consumption in Emerging Economies

Urbanization and increasing disposable income across Asia-Pacific and Latin America are expanding per-capita alcohol consumption.

-

Sustainable & Low-Carbon Production Initiatives

Distilleries are adopting renewable feedstocks, waste-to-energy systems, and carbon capture technologies to enhance ESG compliance.

-

AI-Driven Fermentation & Quality Optimization

Advanced analytics and automated distillation controls are improving yield efficiency, consistency, and cost optimization.

Global Ethanol in Beverage Industry Market Segmentation

-

By Source Type

1.1 Grain-Based Ethanol

1.1.1 Corn-Based Ethanol

1.1.1.1 Industrial Distillation Grade

1.1.1.2 Premium Beverage-Grade

1.1.1.3 Organic Corn Ethanol

1.1.1.4 Non-GMO Certified Ethanol

1.1.2 Wheat-Based Ethanol

1.1.2.1 Neutral Grain Spirit (NGS)

1.1.2.2 High-Purity Distilled Spirit

1.1.2.3 Craft Distillery Grade

1.1.2.4 Premium Export Grade

1.1.3 Barley-Based Ethanol

1.1.3.1 Malt-Derived Ethanol

1.1.3.2 Beer Fortification Grade

1.1.3.3 Specialty Distillation Grade

1.1.3.4 Organic Barley Ethanol

1.2 Sugar & Molasses-Based Ethanol

1.2.1 Sugarcane Ethanol

1.2.1.1 Caribbean Rum Grade

1.2.1.2 Premium Cane Spirit

1.2.1.3 Organic Cane Ethanol

1.2.1.4 Export Distillation Grade

1.2.2 Molasses-Based Ethanol

1.2.2.1 Industrial Beverage Grade

1.2.2.2 Bulk Distillery Supply

1.2.2.3 Blending & Fortification Grade

1.2.2.4 High-Proof Distillation Grade

1.3 Synthetic & Specialty Ethanol

1.3.1 Ultra-High Purity Ethanol

1.3.1.1 Neutral Spirit for Vodka

1.3.1.2 RTD Alcohol Base

1.3.1.3 Flavor-Infusion Base

1.3.1.4 Premium Blending Applications

2.By Application

2.1 Spirits Production

2.1.1 Vodka

2.1.1.1 Premium Vodka

2.1.1.2 Flavored Vodka

2.1.1.3 Craft Vodka

2.1.1.4 Luxury Small-Batch Vodka

2.1.2 Whiskey

2.1.2.1 Bourbon

2.1.2.2 Scotch

2.1.2.3 Rye Whiskey

2.1.2.4 Premium Aged Whiskey

2.1.3 Rum

2.1.3.1 White Rum

2.1.3.2 Dark Rum

2.1.3.3 Spiced Rum

2.1.3.4 Aged Reserve Rum

2.1.4 Gin & Specialty Spirits

2.1.4.1 London Dry Gin

2.1.4.2 Botanical Infused Spirits

2.1.4.3 Craft Small-Batch Gin

2.1.4.4 Limited-Edition Releases

2.2 Beer & Malt Beverages

2.2.1 Standard Beer Production

2.2.1.1 Lager

2.2.1.2 Ale

2.2.1.3 Craft Beer

2.2.1.4 Premium Imported Beer

2.2.2 Fortified & Specialty Beer

2.2.2.1 High-ABV Craft Variants

2.2.2.2 Seasonal Specialty Brews

2.2.2.3 Limited-Edition Releases

2.2.2.4 Barrel-Aged Variants

2.3 Ready-to-Drink (RTD) Alcoholic Beverages

2.3.1 Hard Seltzers

2.3.1.1 Fruit-Infused Variants

2.3.1.2 Low-Calorie Formulations

2.3.1.3 Premium Craft Seltzers

2.3.1.4 Organic RTD Options

2.3.2 Canned Cocktails

2.3.2.1 Classic Cocktail Variants

2.3.2.2 Premium Mixology Blends

2.3.2.3 Low-Sugar Options

2.3.2.4 Limited Seasonal Editions

-

By Distribution Channel

3.1 On-Trade / Hospitality

3.1.1 Bars & Nightclubs

3.1.1.1 Premium Cocktail Bars

3.1.1.2 Luxury Lounges

3.1.1.3 Resort Entertainment Venues

3.1.1.4 Event & Festival Catering

3.2 Off-Trade / Retail

3.2.1 Supermarkets & Liquor Stores

3.2.1.1 Private Label Spirits

3.2.1.2 Premium Imports

3.2.1.3 Bulk Retail Supply

3.2.1.4 Promotional Packs

3.3 Direct-to-Consumer (DTC) & E-Commerce

3.3.1 Online Liquor Platforms

3.3.1.1 National E-Commerce Retailers

3.3.1.2 Subscription Alcohol Clubs

3.3.1.3 Limited Digital Releases

3.3.1.4 Cross-Border Online Platforms

-

By Region

4.1 Europe

4.2 Asia-Pacific

4.3 North America

4.4 Latin America

4.5 Middle East & Africa

Regional Insights of the Global Ethanol in Beverage Industry Market

Europe – Largest Market

Europe maintains its leading position in the global beverage ethanol market, supported by a long-standing distillation legacy, globally recognized spirits brands, and well-established export networks. Countries such as Germany, France, the UK, and Poland play a significant role in vodka, whiskey, and gin production. Strong premiumization trends and consistent demand for high-quality neutral grain spirits continue to sustain regional ethanol consumption.

Asia-Pacific – Fastest Growing Market

Asia-Pacific is the fastest-growing regional market, driven by rapid urbanization, expanding middle-class populations, and increasing alcohol consumption across China, India, Japan, South Korea, and Southeast Asia. Rising disposable incomes, evolving lifestyle preferences, and growing popularity of beer, whiskey, and RTD alcoholic beverages are significantly boosting demand for beverage-grade ethanol in the region.

North America

North America demonstrates steady and resilient growth, led by the United States and Canada. Expansion of craft distilleries, premium bourbon and whiskey production, and strong penetration of hard seltzers and canned cocktails are key contributors to ethanol demand. Advanced production technologies and integrated supply chains further strengthen regional market stability.

Latin America

Latin America remains a strategically important region, particularly Brazil and Mexico, where sugarcane-based ethanol production supports both domestic consumption and export supply. Growth is reinforced by rising rum and spirits consumption, expanding urban populations, and improving distribution infrastructure.

Middle East & Africa

Market expansion in the Middle East & Africa is primarily concentrated in tourism-driven hospitality centers and regulated alcohol markets such as the UAE and South Africa. Demand is supported by premium hotels, expatriate populations, and upscale dining establishments, with gradual growth expected alongside hospitality and retail sector development.

Leading Companies in the Global Ethanol in Beverage Industry Market

Cargill Inc.

Archer Daniels Midland (ADM)

POET LLC

Green Plains Inc.

Cristalco

Raízen

MGP Ingredients

Wilmar International

Archer Daniels Midland (ADM) remains one of the largest global producers of beverage-grade ethanol, leveraging integrated grain sourcing, advanced fermentation technologies, and global distribution networks.

Strategic Intelligence & AI-Driven Insights

Phoenix Demand Forecast Engine – Identifies stable long-term revenue growth driven by RTD innovation, premium spirits expansion, and emerging market consumption trends.

Consumer Behavior Analyzer – Detects rising preference for premium, craft, and low-calorie alcoholic beverages, supporting higher-margin ethanol demand.

Innovation Tracker – Highlights AI-powered fermentation monitoring, carbon capture integration, renewable feedstock sourcing, and smart distillation systems improving yield efficiency.

Porter’s Five Forces Analysis – Reflects moderate supplier power (feedstock dependency), high competitive rivalry among distillers, and increasing differentiation through sustainability and premium branding.

Why the Global Ethanol in Beverage Industry Market Remains Critical

Strong foundational role in global alcoholic beverage production

Expanding premium and craft spirits ecosystem

RTD alcoholic beverage growth driving new demand streams

Sustainability initiatives enhancing production efficiency

AI-driven fermentation improving operational optimization

Final Takeaway of the Global Ethanol in Beverage Industry Market

The Global Ethanol in Beverage Industry Market is evolving into a premium-oriented, sustainability-driven, and technology-integrated ecosystem. The projected CAGR of ~4.1% (2026–2033) reflects stable yet resilient growth supported by premium spirits expansion, RTD innovation, and emerging market consumption.

Future leadership will be defined by producers that integrate AI-powered fermentation analytics, low-carbon production methods, diversified feedstock sourcing, and omnichannel beverage partnerships.

At Phoenix Research, our advanced forecasting frameworks deliver comprehensive Ethanol in Beverage Industry revenue projections, competitive intelligence, and AI-backed strategic insights — empowering stakeholders to navigate the Post-2025 landscape with data-driven precision and long-term value creation.

📢 Social Mentions & Publication Channels

Explore deeper insights and follow our cross-platform updates on LinkedIn, and X for continuous intelligence and market coverage.

LinkedIn : https://www.linkedin.com/feed/update/urn:li:activity:7430870229393514496

X : https://x.com/Pheonix_Insight/status/2025109197730545914?s=20

Table of Contents

1. Executive Summary

1.1 Market Snapshot (2026–2033)

1.2 Key Financial Highlights

1.3 Growth Outlook & CAGR Analysis

1.4 Largest & Fastest Growing Regions

1.5 Key Trends & Strategic Focus

1.6 Analyst Recommendations

2. Market Overview

2.1 Introduction to Beverage-Grade Ethanol

2.2 Industry Value Chain Analysis

2.3 Production Process Overview

2.4 Feedstock Landscape

2.5 Regulatory Framework & Compliance

2.6 Sustainability & ESG Landscape

2.7 Post-2025 Industry Outlook

3. Global Market Forecast Snapshot (USD Billion), 2026–2033

3.1 2025 Market Size

3.2 2033 Projected Market Size

3.3 CAGR Analysis (2026–2033)

3.4 Revenue Trend Analysis

3.5 Demand-Supply Outlook

4. Market Dynamics

4.1 Market Drivers

4.1.1 Premium & Craft Beverage Growth

4.1.2 RTD Alcohol Expansion

4.1.3 Emerging Market Consumption

4.1.4 Sustainable Production Adoption

4.1.5 AI-Driven Fermentation Optimization

4.2 Market Restraints

4.2.1 Feedstock Price Volatility

4.2.2 Regulatory & Taxation Constraints

4.2.3 Environmental Compliance Costs

4.3 Market Opportunities

4.3.1 Organic & Clean-Label Ethanol

4.3.2 Low-Carbon Production Technologies

4.3.3 Premium Export Markets

4.3.4 Advanced Distillation Automation

4.4 Porter’s Five Forces Analysis

5. Market Segmentation by Source Type (USD Billion), 2026–2033

5.1 Grain-Based Ethanol

5.1.1 Corn-Based Ethanol

5.1.1.1 Industrial Distillation Grade

5.1.1.2 Premium Beverage-Grade

5.1.1.3 Organic Corn Ethanol

5.1.1.4 Non-GMO Certified Ethanol

5.1.2 Wheat-Based Ethanol

5.1.2.1 Neutral Grain Spirit (NGS)

5.1.2.2 High-Purity Distilled Spirit

5.1.2.3 Craft Distillery Grade

5.1.2.4 Premium Export Grade

5.1.3 Barley-Based Ethanol

5.1.3.1 Malt-Derived Ethanol

5.1.3.2 Beer Fortification Grade

5.1.3.3 Specialty Distillation Grade

5.1.3.4 Organic Barley Ethanol

5.2 Sugar & Molasses-Based Ethanol

5.2.1 Sugarcane Ethanol

5.2.1.1 Caribbean Rum Grade

5.2.1.2 Premium Cane Spirit

5.2.1.3 Organic Cane Ethanol

5.2.1.4 Export Distillation Grade

5.2.2 Molasses-Based Ethanol

5.2.2.1 Industrial Beverage Grade

5.2.2.2 Bulk Distillery Supply

5.2.2.3 Blending & Fortification Grade

5.2.2.4 High-Proof Distillation Grade

5.3 Synthetic & Specialty Ethanol

5.3.1 Ultra-High Purity Ethanol

5.3.1.1 Neutral Spirit for Vodka

5.3.1.2 RTD Alcohol Base

5.3.1.3 Flavor-Infusion Base

5.3.1.4 Premium Blending Applications

6. Market Segmentation by Application (USD Billion), 2026–2033

6.1 Spirits Production

6.1.1 Vodka

6.1.1.1 Premium Vodka

6.1.1.2 Flavored Vodka

6.1.1.3 Craft Vodka

6.1.1.4 Luxury Small-Batch Vodka

6.1.2 Whiskey

6.1.2.1 Bourbon

6.1.2.2 Scotch

6.1.2.3 Rye Whiskey

6.1.2.4 Premium Aged Whiskey

6.1.3 Rum

6.1.3.1 White Rum

6.1.3.2 Dark Rum

6.1.3.3 Spiced Rum

6.1.3.4 Aged Reserve Rum

6.1.4 Gin & Specialty Spirits

6.1.4.1 London Dry Gin

6.1.4.2 Botanical Infused Spirits

6.1.4.3 Craft Small-Batch Gin

6.1.4.4 Limited-Edition Releases

6.2 Beer & Malt Beverages

6.2.1 Standard Beer Production

6.2.1.1 Lager

6.2.1.2 Ale

6.2.1.3 Craft Beer

6.2.1.4 Premium Imported Beer

6.2.2 Fortified & Specialty Beer

6.2.2.1 High-ABV Craft Variants

6.2.2.2 Seasonal Specialty Brews

6.2.2.3 Limited-Edition Releases

6.2.2.4 Barrel-Aged Variants

6.3 Ready-to-Drink (RTD) Alcoholic Beverages

6.3.1 Hard Seltzers

6.3.1.1 Fruit-Infused Variants

6.3.1.2 Low-Calorie Formulations

6.3.1.3 Premium Craft Seltzers

6.3.1.4 Organic RTD Options

6.3.2 Canned Cocktails

6.3.2.1 Classic Cocktail Variants

6.3.2.2 Premium Mixology Blends

6.3.2.3 Low-Sugar Options

6.3.2.4 Limited Seasonal Editions

7. Market Segmentation by Distribution Channel (USD Billion), 2026–2033

7.1 On-Trade / Hospitality

7.1.1 Bars & Nightclubs

7.1.1.1 Premium Cocktail Bars

7.1.1.2 Luxury Lounges

7.1.1.3 Resort Entertainment Venues

7.1.1.4 Event & Festival Catering

7.1.2 Hotels & Resorts

7.1.2.1 Luxury Hotels

7.1.2.2 Business Hotels

7.1.2.3 Boutique Hotels

7.1.2.4 All-Inclusive Resorts

7.2 Off-Trade / Retail

7.2.1 Supermarkets & Liquor Stores

7.2.1.1 Private Label Spirits

7.2.1.2 Premium Imports

7.2.1.3 Bulk Retail Supply

7.2.1.4 Promotional Packs

7.2.2 Specialty Retailers

7.2.2.1 Premium Wine & Spirits Stores

7.2.2.2 Craft Beverage Retailers

7.2.2.3 Organic & Specialty Stores

7.2.2.4 Duty-Free Shops

7.3 Direct-to-Consumer (DTC) & E-Commerce

7.3.1 Online Liquor Platforms

7.3.1.1 National E-Commerce Retailers

7.3.1.2 Subscription Alcohol Clubs

7.3.1.3 Limited Digital Releases

7.3.1.4 Cross-Border Online Platforms

7.3.2 Distillery-Owned Platforms

7.3.2.1 Brand-Owned Online Stores

7.3.2.2 Membership & Loyalty Programs

7.3.2.3 Direct Subscription Models

7.3.2.4 Exclusive Online Product Launches

8. Market Segmentation by Region (USD Billion), 2026–2033

8.1 Europe

8.2 Asia-Pacific

8.3 North America

8.4 Latin America

8.5 Middle East & Africa

9. Competitive Landscape

9.1 Market Share Analysis

9.2 Company Benchmarking

9.3 Strategic Initiatives

9.4 Mergers & Acquisitions

9.5 Capacity Expansion Analysis

10. Company Profiles

10.1 Cargill Inc.

10.2 Archer Daniels Midland (ADM)

10.3 POET LLC

10.4 Green Plains Inc.

10.5 Cristalco

10.6 Raízen

10.7 MGP Ingredients

10.8 Wilmar International

11. Strategic Intelligence & AI Insights

11.1 Demand Forecast Engine Analysis

11.2 Consumer Behavior Insights

11.3 Innovation & Technology Tracker

11.4 ESG & Sustainability Scorecard

12. Future Outlook & Strategic Recommendations

12.1 Market Outlook 2033

12.2 Technology Evolution Roadmap

12.3 Investment Opportunities

12.4 Strategic Risk Assessment

13. Appendix

14. About Us

15. Disclaimer