Global Herbal Tea Market size and share Analysis 2026-2033

Global Herbal Tea Market Forecast Snapshot: 2026–2033

| Metric | Value |

|---|---|

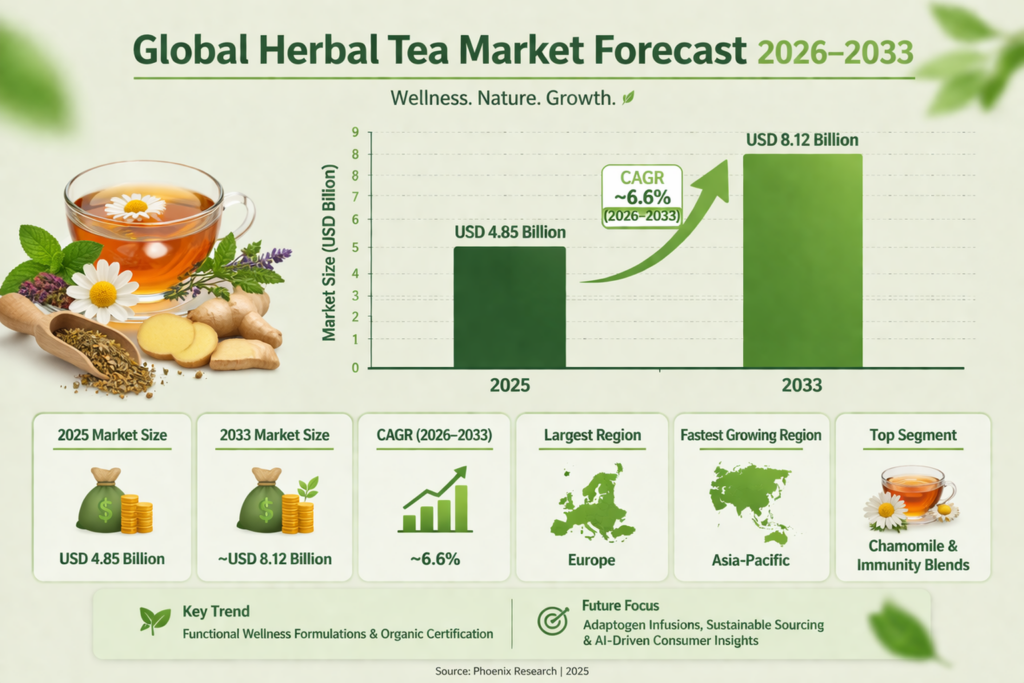

| 2025 Market Size | USD 4.85 Billion |

| 2033 Market Size | ~USD 8.12 Billion |

| CAGR (2026–2033) | ~6.6% |

| Largest Region | Europe |

| Fastest Growing Region | Asia-Pacific |

| Top Segment | Chamomile & Immunity Blends |

| Key Trend | Functional Wellness Formulations & Organic Certification |

| Future Focus | Adaptogen Infusions, Sustainable Sourcing & AI-Driven Consumer Insights |

Global Herbal Tea Market Overview

The Global Herbal Tea Market is experiencing robust growth, driven by rising consumer interest in health and wellness, functional beverages, and premium botanical blends. Herbal teas have evolved beyond traditional remedies into mainstream functional beverages, incorporating ingredients such as chamomile, peppermint, hibiscus, ginger, turmeric, rooibos, detox blends, and adaptogens.

According to Pheonix Research, the Global Herbal Tea Market is valued at USD 4.85 billion in 2025 and is projected to reach approximately USD 8.12 billion by 2033, registering a CAGR of ~6.6% (2026–2033). Growth is supported by increasing adoption of plant-based and clean-label products, rising demand for stress relief and immune-boosting beverages, and expanding organic certification penetration.

Europe leads the market due to strong herbal consumption traditions and high organic product adoption, while Asia-Pacific is the fastest-growing region, driven by traditional herbal medicine heritage, rising disposable incomes, and the expansion of modern retail networks.

The Post-2025 outlook emphasizes adaptogen-enriched formulations, AI-driven consumer personalization, sustainable herb sourcing, biodegradable packaging, and premium wellness positioning as key strategies accelerating market growth.

Key Drivers of Global Herbal Tea Market Growth

1. Rising Global Health & Wellness Awareness

Consumers increasingly prefer natural, caffeine-free beverages associated with immunity, digestion, relaxation, and detoxification.

2. Expansion of Functional & Medicinal Blends

Growing demand for adaptogens (ashwagandha, ginseng), anti-inflammatory herbs (turmeric, ginger), and sleep-support formulations is accelerating innovation.

3. Clean-Label & Organic Certification Demand

Non-GMO, organic-certified, preservative-free products are gaining traction among health-conscious buyers.

4. Premiumization & Specialty Tea Culture

Luxury loose-leaf blends, artisanal infusions, and single-origin botanicals command higher margins and brand differentiation.

5. Growth of E-Commerce & Subscription Models

Digital platforms enable direct-to-consumer sales, curated wellness boxes, and personalized tea blends.

Global Herbal Tea Market Segmentation

1. By Product Type

1.1 Single-Herb Infusions

1.1.1 Chamomile Tea

1.1.1.1 Sleep Support Formulations

1.1.1.1.1 Mild Relaxation Blends

1.1.1.1.2 Extra-Strength Night Formulas

1.1.1.1.3 Melatonin-Infused Variants

1.1.1.1.4 Lavender-Enhanced Sleep Blends

1.1.1.2 Organic Chamomile

1.1.1.2.1 USDA Organic Certified

1.1.1.2.2 EU Organic Certified

1.1.1.2.3 Non-GMO Verified

1.1.1.2.4 Wild-Harvested Chamomile

1.1.1.3 Premium Loose-Leaf

1.1.1.3.1 Whole Flower Buds

1.1.1.3.2 Single-Origin Chamomile

1.1.1.3.3 Artisanal Handpicked

1.1.1.3.4 Luxury Gift Packaging

1.1.1.4 Tea Bag Variants

1.1.1.4.1 Biodegradable Tea Bags

1.1.1.4.2 Pyramid Sachets

1.1.1.4.3 Bulk Value Packs

1.1.1.4.4 Travel Packs

1.1.2 Peppermint Tea

1.1.2.1 Digestive Support

1.1.2.1.1 Post-Meal Blends

1.1.2.1.2 IBS Support Formulas

1.1.2.1.3 Mint & Fennel Combinations

1.1.2.1.4 Cooling Summer Variants

1.1.2.2 Cooling Mint Blends

1.1.2.2.1 Spearmint Combinations

1.1.2.2.2 Mint & Lemon

1.1.2.2.3 Mint & Ginger

1.1.2.2.4 Mint & Green Tea Fusion

1.2 Functional Blends

1.2.1 Immunity Blends

1.2.1.1 Turmeric-Ginger

1.2.1.1.1 Anti-Inflammatory Focus

1.2.1.1.2 Black Pepper Enhanced

1.2.1.1.3 Honey-Infused Variants

1.2.1.1.4 Winter Wellness Editions

1.2.1.2 Elderberry

1.2.1.2.1 Vitamin C Fortified

1.2.1.2.2 Zinc-Enriched Blends

1.2.1.2.3 Seasonal Defense Packs

1.2.1.2.4 Pediatric-Friendly Variants

1.2.2 Detox & Weight Management

1.2.2.1 Green Detox Blends

1.2.2.1.1 Chlorophyll-Enriched

1.2.2.1.2 Lemon & Mint Detox

1.2.2.1.3 Dandelion Root Formulations

1.2.2.1.4 Liver Cleanse Focus

1.2.2.2 Metabolism Support

1.2.2.2.1 Garcinia-Infused

1.2.2.2.2 Cinnamon Blends

1.2.2.2.3 Thermogenic Herbal Mixes

1.2.2.2.4 Slimming Wellness Packs

1.3 Adaptogen & Stress Relief Teas

1.3.1 Ashwagandha-Infused

1.3.1.1 Stress Reduction

1.3.1.2 Cortisol Balance

1.3.1.3 Focus & Calm Blends

1.3.1.4 Sleep-Support Adaptogen Mixes

1.3.2 Ginseng Blends

1.3.2.1 Energy Support

1.3.2.2 Cognitive Enhancement

1.3.2.3 Immunity Boost

1.3.2.4 Premium Korean Ginseng Variants

1.4 Specialty & Premium Herbal Teas

1.4.1 Rooibos

1.4.1.1 Red Rooibos

1.4.1.2 Green Rooibos

1.4.1.3 Vanilla Rooibos

1.4.1.4 Organic Fair-Trade Rooibos

1.4.2 Hibiscus

1.4.2.1 Blood Pressure Support

1.4.2.2 Vitamin C Rich

1.4.2.3 Floral Fusion Blends

1.4.2.4 Iced Herbal Variants

2. By Form

2.1 Tea Bags

2.1.1 Standard Paper Bags

2.1.2 Pyramid Sachets

2.1.3 Biodegradable Materials

2.1.4 Compostable Packaging

2.2 Loose Leaf

2.2.1 Whole Leaf

2.2.2 Crushed Herbal Mixes

2.2.3 Premium Gift Tins

2.2.4 Bulk Wellness Packs

2.3 Instant Herbal Powder

2.3.1 Single-Serve Sachets

2.3.2 Travel Packs

2.3.3 Vitamin-Fortified Powders

2.3.4 Sugar-Free Instant Mixes

2.4 RTD Herbal Tea

2.4.1 Bottled Herbal Infusions

2.4.2 Canned Functional Teas

2.4.3 Organic Certified RTDs

2.4.4 Low-Sugar Variants

3. By Distribution Channel

3.1 Off-Trade / Retail

3.1.1 Supermarkets & Hypermarkets

3.1.1.1 Premium Shelf Placement

3.1.1.2 Private Label Herbal Teas

3.1.1.3 Promotional Multipacks

3.1.1.4 Seasonal Campaign Displays

3.1.2 Specialty Tea Stores

3.1.2.1 Artisanal Boutiques

3.1.2.2 Wellness-Focused Chains

3.1.2.3 Organic Specialty Shops

3.1.2.4 Premium Gift Retailers

3.2 E-Commerce

3.2.1 Online Marketplaces

3.2.1.1 National Platforms

3.2.1.2 Cross-Border Sales

3.2.1.3 Flash Sales

3.2.1.4 Wellness Subscription Platforms

3.2.2 Brand-Owned Websites

3.2.2.1 Personalized Tea Blends

3.2.2.2 Subscription Boxes

3.2.2.3 Limited Edition Drops

3.2.2.4 Loyalty Programs

3.3 On-Trade

3.3.1 Cafés

3.3.1.1 Premium Herbal Menus

3.3.1.2 Seasonal Specials

3.3.1.3 Wellness Partnerships

3.3.1.4 Iced Herbal Offerings

4. By End-User

4.1 Individual Consumers

4.1.1 Millennials & Gen Z

4.1.1.1 Trend-Driven Buyers

4.1.1.2 Stress-Relief Seekers

4.1.1.3 Fitness-Oriented Consumers

4.1.1.4 Digital Subscription Users

4.1.2 Health-Conscious Adults

4.1.2.1 Immunity-Focused

4.1.2.2 Detox-Oriented

4.1.2.3 Organic Preference Buyers

4.1.2.4 Preventive Wellness Consumers

4.2 Institutional Buyers

4.2.1 Hospitality Chains

4.2.1.1 Luxury Hotels

4.2.1.2 Spa Resorts

4.2.1.3 Boutique Wellness Retreats

4.2.1.4 Airline Hospitality

5. By Region

5.1 Europe

5.2 North America

5.3 Asia-Pacific

5.4 Latin America

5.5 Middle East & Africa

Leading Companies in the Global Herbal Tea Market

Unilever (Lipton Herbal Range)

Twinings

Traditional Medicinals

Celestial Seasonings

Yogi Tea

Tata Consumer Products

Dilmah

Pukka Herbs

Bigelow Tea

Unilever remains one of the largest global players in the herbal tea market due to its diversified tea portfolio and extensive international distribution network. The company operates across mass-market and premium segments, maintaining strong retail penetration worldwide.

Regional Insights of the Global Herbal Tea Market

Europe leads the global herbal tea market, supported by a long-standing tradition of herbal infusions, widespread adoption of organic products, and a strong culture of premium and specialty teas.

Asia-Pacific – Fastest Growing Market

Asia-Pacific is the fastest-growing region, driven by a rich heritage of traditional herbal medicine, rising disposable incomes, and increasing consumer awareness of wellness and functional beverages.

North America

North America shows steady growth, fueled by high demand for immunity-boosting, detox, and stress-relief formulations, with e-commerce channels playing a significant role in market penetration.

Latin America

Latin America is experiencing growth through expanding urban wellness trends and greater availability of specialty herbal tea brands across retail and hospitality channels.

Middle East & Africa

The Middle East & Africa market is expanding gradually, driven by rising demand for botanical wellness beverages in urban centers and growing consumption within the hospitality sector.

Why the Global Herbal Tea Market Remains Critical

-

Strong alignment with global wellness and immunity trends

-

High-margin premium and organic-certified segments

-

Expanding adaptogen and functional ingredient integration

-

Sustainable and ethical sourcing as brand differentiator

-

Strong scalability through digital and subscription commerce

Strategic Intelligence & AI-Driven Insights

Pheonix Demand Forecast Engine

Identifies sustained growth supported by rising wellness adoption and premium botanical innovation.

Consumer Behavior Analyzer

Highlights increasing demand for immunity blends, stress relief formulations, and organic-certified products among younger demographics.

Ingredient Innovation Tracker

Monitors adaptogen inclusion, plant-based functional compounds, and emerging botanical sourcing regions.

Supply Chain & Sustainability Analytics

Tracks ethical herb sourcing, carbon-neutral packaging adoption, and sustainable farming practices.

Final Takeaway of the Global Herbal Tea Market

The Global Herbal Tea Market is transitioning into a premium-focused, wellness-oriented, and sustainability-driven beverage ecosystem. The projected CAGR of ~6.6% (2026–2033) reflects strong long-term expansion supported by immunity-focused innovation, adaptogen integration, and clean-label consumer preferences.

Future market leadership will be defined by brands that integrate AI-driven consumer insights, organic sourcing strategies, premium positioning, and omnichannel distribution expansion.

At Pheonix Research, our advanced forecasting frameworks deliver comprehensive Herbal Tea Market revenue projections, competitive benchmarking, and AI-backed strategic intelligence — enabling stakeholders to capitalize on the Post-2025 wellness beverage landscape with data-driven precision and sustainable growth strategies.

📢 Social Mentions & Publication Channels

Explore deeper insights and follow our cross-platform updates on LinkedIn, and X for continuous intelligence and market coverage.

LinkedIn : https://www.linkedin.com/feed/update/urn:li:activity:7431012287831846912

X : https://x.com/Pheonix_Insight/status/2025249828733944207?s=20

Table of Contents

1. Executive Summary

1.1 Market Snapshot (2026–2033)

1.2 Key Growth Highlights

1.3 Largest & Fastest Growing Regions

1.4 Dominant & Emerging Segments

1.5 Strategic Opportunity Areas

2. Global Herbal Tea Market Overview

2.1 Market Definition & Scope

2.2 Industry Evolution & Product Innovation

2.3 Value Chain Analysis

2.4 Business Models & Revenue Streams

2.5 Regulatory & Certification Landscape

2.6 Pricing Trends & Margin Analysis

3. Market Forecast Snapshot (2026–2033)

3.1 2025 Market Size: USD 4.85 Billion

3.2 2033 Market Size: ~USD 8.12 Billion

3.3 CAGR (2026–2033): ~6.6%

3.4 Largest Region: Europe

3.5 Fastest Growing Region: Asia-Pacific

3.6 Top Segment: Chamomile & Immunity Blends

3.7 Key Trend: Functional Wellness Formulations & Organic Certification

3.8 Future Focus: Adaptogen Infusions, Sustainable Sourcing & AI Consumer Insights

4. Market Dynamics

4.1 Key Growth Drivers

4.2 Market Restraints

4.3 Emerging Opportunities

4.4 Industry Challenges

4.5 Impact of Macroeconomic Factors

5. Market Segmentation by Product Type (USD Billion), 2026–2033

5.1 Single-Herb Infusions

5.1.1 Chamomile Tea

5.1.1.1 Sleep Support Formulations

5.1.1.1.1 Mild Relaxation Blends

5.1.1.1.2 Extra-Strength Night Formulas

5.1.1.1.3 Melatonin-Infused Variants

5.1.1.1.4 Lavender-Enhanced Sleep Blends

5.1.1.2 Organic Chamomile

5.1.1.2.1 USDA Organic Certified

5.1.1.2.2 EU Organic Certified

5.1.1.2.3 Non-GMO Verified

5.1.1.2.4 Wild-Harvested Chamomile

5.1.1.3 Premium Loose-Leaf

5.1.1.3.1 Whole Flower Buds

5.1.1.3.2 Single-Origin Chamomile

5.1.1.3.3 Artisanal Handpicked

5.1.1.3.4 Luxury Gift Packaging

5.1.1.4 Tea Bag Variants

5.1.1.4.1 Biodegradable Tea Bags

5.1.1.4.2 Pyramid Sachets

5.1.1.4.3 Bulk Value Packs

5.1.1.4.4 Travel Packs

5.1.2 Peppermint Tea

5.1.2.1 Digestive Support

5.1.2.1.1 Post-Meal Blends

5.1.2.1.2 IBS Support Formulas

5.1.2.1.3 Mint & Fennel Combinations

5.1.2.1.4 Cooling Summer Variants

5.1.2.2 Cooling Mint Blends

5.1.2.2.1 Spearmint Combinations

5.1.2.2.2 Mint & Lemon

5.1.2.2.3 Mint & Ginger

5.1.2.2.4 Mint & Green Tea Fusion

5.2 Functional Blends

5.2.1 Immunity Blends

5.2.1.1 Turmeric-Ginger

5.2.1.1.1 Anti-Inflammatory Focus

5.2.1.1.2 Black Pepper Enhanced

5.2.1.1.3 Honey-Infused Variants

5.2.1.1.4 Winter Wellness Editions

5.2.1.2 Elderberry

5.2.1.2.1 Vitamin C Fortified

5.2.1.2.2 Zinc-Enriched Blends

5.2.1.2.3 Seasonal Defense Packs

5.2.1.2.4 Pediatric-Friendly Variants

5.2.2 Detox & Weight Management

5.2.2.1 Green Detox Blends

5.2.2.1.1 Chlorophyll-Enriched

5.2.2.1.2 Lemon & Mint Detox

5.2.2.1.3 Dandelion Root Formulations

5.2.2.1.4 Liver Cleanse Focus

5.2.2.2 Metabolism Support

5.2.2.2.1 Garcinia-Infused

5.2.2.2.2 Cinnamon Blends

5.2.2.2.3 Thermogenic Herbal Mixes

5.2.2.2.4 Slimming Wellness Packs

5.3 Adaptogen & Stress Relief Teas

5.3.1 Ashwagandha-Infused

5.3.1.1 Stress Reduction

5.3.1.2 Cortisol Balance

5.3.1.3 Focus & Calm Blends

5.3.1.4 Sleep-Support Adaptogen Mixes

5.3.2 Ginseng Blends

5.3.2.1 Energy Support

5.3.2.2 Cognitive Enhancement

5.3.2.3 Immunity Boost

5.3.2.4 Premium Korean Ginseng Variants

5.4 Specialty & Premium Herbal Teas

5.4.1 Rooibos

5.4.1.1 Red Rooibos

5.4.1.2 Green Rooibos

5.4.1.3 Vanilla Rooibos

5.4.1.4 Organic Fair-Trade Rooibos

5.4.2 Hibiscus

5.4.2.1 Blood Pressure Support

5.4.2.2 Vitamin C Rich

5.4.2.3 Floral Fusion Blends

5.4.2.4 Iced Herbal Variants

6. Market Segmentation by Form (USD Billion), 2026–2033

6.1 Tea Bags

6.1.1 Standard Paper Bags

6.1.2 Pyramid Sachets

6.1.3 Biodegradable Materials

6.1.4 Compostable Packaging

6.2 Loose Leaf

6.2.1 Whole Leaf

6.2.2 Crushed Herbal Mixes

6.2.3 Premium Gift Tins

6.2.4 Bulk Wellness Packs

6.3 Instant Herbal Powder

6.3.1 Single-Serve Sachets

6.3.2 Travel Packs

6.3.3 Vitamin-Fortified Powders

6.3.4 Sugar-Free Instant Mixes

6.4 RTD Herbal Tea

6.4.1 Bottled Herbal Infusions

6.4.2 Canned Functional Teas

6.4.3 Organic Certified RTDs

6.4.4 Low-Sugar Variants

7. Market Segmentation by Distribution Channel (USD Billion), 2026–2033

7.1 Off-Trade / Retail

7.1.1 Supermarkets & Hypermarkets

7.1.1.1 Premium Shelf Placement

7.1.1.2 Private Label Herbal Teas

7.1.1.3 Promotional Multipacks

7.1.1.4 Seasonal Campaign Displays

7.1.2 Specialty Tea Stores

7.1.2.1 Artisanal Boutiques

7.1.2.2 Wellness-Focused Chains

7.1.2.3 Organic Specialty Shops

7.1.2.4 Premium Gift Retailers

7.2 E-Commerce

7.2.1 Online Marketplaces

7.2.1.1 National Platforms

7.2.1.2 Cross-Border Sales

7.2.1.3 Flash Sales

7.2.1.4 Wellness Subscription Platforms

7.2.2 Brand-Owned Websites

7.2.2.1 Personalized Tea Blends

7.2.2.2 Subscription Boxes

7.2.2.3 Limited Edition Drops

7.2.2.4 Loyalty Programs

7.3 On-Trade / Hospitality

7.3.1 Cafés

7.3.1.1 Premium Herbal Menus

7.3.1.2 Seasonal Specials

7.3.1.3 Wellness Partnerships

7.3.1.4 Iced Herbal Offerings

8. Market Segmentation by End-User (USD Billion), 2026–2033

8.1 Individual Consumers

8.1.1 Millennials & Gen Z

8.1.1.1 Trend-Driven Buyers

8.1.1.2 Stress-Relief Seekers

8.1.1.3 Fitness-Oriented Consumers

8.1.1.4 Digital Subscription Users

8.1.2 Health-Conscious Adults

8.1.2.1 Immunity-Focused

8.1.2.2 Detox-Oriented

8.1.2.3 Organic Preference Buyers

8.1.2.4 Preventive Wellness Consumers

8.2 Institutional Buyers

8.2.1 Hospitality Chains

8.2.1.1 Luxury Hotels

8.2.1.2 Spa Resorts

8.2.1.3 Boutique Wellness Retreats

8.2.1.4 Airline Hospitality

9. Market Segmentation by Region (USD Billion), 2026–2033

9.1 Europe

9.1.1 Western Europe

9.1.2 Eastern Europe

9.1.3 Nordic Countries

9.1.4 Mediterranean Region

9.2 North America

9.2.1 United States

9.2.2 Canada

9.2.3 Mexico

9.3 Asia-Pacific

9.3.1 China

9.3.2 India

9.3.3 Japan

9.3.4 Southeast Asia

9.4 Latin America

9.5 Middle East & Africa

10. Regional Insights

10.1 Europe – Market Leadership

10.2 Asia-Pacific – Rapid Growth

10.3 North America – Immunity & Stress-Relief Focus

10.4 Latin America – Urban Wellness Adoption

10.5 Middle East & Africa – Hospitality & Urban Centers

11. Competitive Landscape

11.1 Market Share Analysis

11.2 Competitive Positioning Matrix

11.3 Mergers & Acquisitions

11.4 Product Launch & Innovation Trends

12. Company Profiles

12.1 Unilever (Lipton Herbal Range)

12.2 Twinings

12.3 Traditional Medicinals

12.4 Celestial Seasonings

12.5 Yogi Tea

12.6 Tata Consumer Products

12.7 Dilmah

12.8 Pukka Herbs

12.9 Bigelow Tea

13. Strategic Intelligence & AI-Backed Insights

13.1 Pheonix Demand Forecast Engine

13.2 Consumer Behavior Analytics

13.3 Ingredient Innovation Tracker

13.4 Supply Chain & Sustainability Analytics

13.5 Porter’s Five Forces Analysis

14. Why the Global Herbal Tea Market Remains Critical

14.1 Alignment with Global Wellness & Immunity Trends

14.2 Premium & Organic-Certified Segment Expansion

14.3 Adaptogen & Functional Ingredient Integration

14.4 Sustainability & Ethical Sourcing Differentiation

14.5 Scalability Through Digital & Subscription Commerce

15. Appendix

16. About Pheonix Research

17. Disclaimer

Competitive Landscape

Competitive Landscape of the Global Herbal Tea Market

Executive Framing

The Global Herbal Tea Market is moderately fragmented, characterized by a blend of multinational beverage companies, established specialty tea brands, and emerging wellness-focused startups. Leading players such as Unilever, Twinings, Tata Consumer Products, and Pukka Herbs maintain strong market positions through diversified product portfolios, global distribution networks, and brand credibility. Meanwhile, niche and regional brands are intensifying competition by focusing on organic certification, functional wellness blends, and premium artisanal offerings.

Current Market Reality

The competitive environment operates across multiple product tiers, including single-herb infusions, functional blends, adaptogen teas, and premium specialty offerings. Large players leverage economies of scale, established retail presence, and brand recognition, while smaller companies differentiate through innovation in adaptogens, clean-label formulations, and sustainable sourcing practices.

E-commerce and direct-to-consumer (DTC) platforms are significantly reshaping the competitive dynamics, enabling brands to offer personalized tea blends, subscription-based wellness packages, and limited-edition product launches. Additionally, partnerships with wellness centers, cafés, and hospitality chains are expanding brand visibility and consumption occasions globally.

Key Signals and Evidence

Several indicators highlight the evolving competitive landscape:

- Rapid expansion of functional, immunity-boosting, and stress-relief herbal tea formulations.

- Growing adoption of organic-certified, non-GMO, and clean-label products.

- Increased focus on premiumization through artisanal, single-origin, and luxury packaging.

- Rising penetration of e-commerce, subscription models, and personalized wellness offerings.

- Heightened investment in sustainable sourcing, biodegradable packaging, and ethical supply chains.

Strategic Implications

Market participants must adopt multi-dimensional strategies to sustain competitive advantage:

- Portfolio Diversification: Expanding across functional blends, adaptogen teas, and premium specialty segments.

- Health & Wellness Innovation: Developing immunity, detox, stress-relief, and sleep-support formulations.

- Omnichannel Expansion: Strengthening presence across retail, e-commerce, and direct-to-consumer platforms.

- Premiumization Strategy: Leveraging artisanal positioning, organic certification, and luxury packaging.

- Sustainability Leadership: Investing in ethical sourcing, biodegradable packaging, and transparent supply chains.

Forward Outlook

By 2033, the Global Herbal Tea Market is projected to reach approximately USD 8.12 billion, growing at a CAGR of ~6.6%. Europe will continue to lead due to strong herbal consumption traditions and organic adoption, while Asia-Pacific will remain the fastest-growing region driven by traditional medicine heritage and rising wellness awareness.

The competitive landscape will evolve through functional innovation, adaptogen integration, and digital transformation. Companies that successfully integrate AI-driven consumer insights, sustainable sourcing strategies, and premium wellness positioning will secure long-term leadership in this increasingly health-focused and experience-driven beverage market.

Value Chain

Global Herbal Tea Market: Value Chain & Market Dynamics

Executive Framing

The global herbal tea market operates within a botanical-centric and wellness-driven value chain, shaped by increasing consumer demand for natural, functional, and clean-label beverages. As herbal teas transition from traditional remedies to mainstream wellness products, the value chain has evolved into a multi-layered ecosystem encompassing raw herb cultivation, functional formulation, premium branding, and omnichannel distribution.

The market follows a hybrid structure, where large multinational players leverage global sourcing networks, standardized production, and strong retail presence, while emerging and niche brands focus on organic certification, artisanal blends, and direct-to-consumer (DTC) engagement. This dual model supports both large-scale commercialization and rapid innovation in adaptogens and functional botanicals.

However, the market is increasingly influenced by regulatory standards on organic labeling, sustainability practices, and quality assurance, alongside challenges related to herb sourcing variability, climate impact on agriculture, and premium pricing pressures.

Current Market Reality

The herbal tea value chain is characterized by moderate-to-high complexity, driven by diverse botanical inputs, fragmented sourcing ecosystems, and increasing demand for functional and premium formulations. Leading companies such as Unilever, Twinings, and Tata Consumer Products operate with globally integrated sourcing and distribution frameworks.

Upstream activities involve the cultivation and sourcing of herbs, botanicals, and adaptogens such as chamomile, peppermint, turmeric, ginger, ashwagandha, and rooibos. Supply variability due to seasonal cycles, geographic dependency, and sustainable farming practices significantly impacts procurement strategies.

Midstream operations include blending, drying, processing, flavor enhancement, and packaging across formats such as tea bags, loose leaf, instant powders, and RTD herbal infusions. Increasing R&D investments are focused on functional blends, immunity formulations, and organic-certified products.

Downstream distribution spans supermarkets, specialty tea stores, cafés, e-commerce platforms, and subscription-based wellness models, enabling strong consumer reach and personalized product experiences.

Key Signals and Evidence

Key indicators highlighting the evolution of the herbal tea market include:

- Market growth from USD 4.85 billion (2025) to ~USD 8.12 billion (2033) at a CAGR of ~6.6%, reflecting strong and sustained expansion.

- Rising demand for functional wellness formulations, immunity blends, and adaptogen-infused teas.

- Dominance of chamomile and immunity blends as high-demand product segments.

- Leadership of Europe driven by organic adoption and traditional herbal consumption, with Asia-Pacific as the fastest-growing region.

- Expansion of e-commerce, subscription models, and personalized tea offerings enhancing consumer engagement.

Additionally, buyer power remains high due to product variety and brand differentiation, while supplier power is moderate to high, influenced by dependence on agricultural outputs and sustainable sourcing constraints.

Strategic Implications

Companies must balance premium positioning with supply chain resilience to remain competitive in an increasingly wellness-focused market. Large players are expected to strengthen their market presence through portfolio expansion, organic certifications, and global distribution scale.

Emerging brands can differentiate through adaptogen innovation, clean-label transparency, and digital-first strategies, targeting niche consumer segments seeking personalized wellness solutions.

Integration of advanced technologies such as AI-driven consumer insights, demand forecasting, and product personalization will be critical in optimizing operations and enhancing customer engagement.

Sustainability is becoming a key strategic pillar, with growing emphasis on ethical herb sourcing, biodegradable packaging, and carbon-conscious supply chains.

Forward Outlook

The herbal tea market is expected to undergo continued transformation driven by wellness trends, premiumization, and sustainability initiatives.

Key future developments include:

- Expansion of functional and adaptogen-based herbal tea formulations

- Growth in organic-certified and clean-label product offerings

- Increased adoption of sustainable and biodegradable packaging solutions

- Rising role of AI-powered personalization and consumer analytics

Companies that successfully integrate innovation, sustainable sourcing, and omnichannel distribution will be best positioned to capture long-term growth opportunities.

In conclusion, the herbal tea market is evolving into a premium, health-focused, and sustainability-driven ecosystem, where authenticity, functionality, and supply chain transparency define competitive advantage.

Investment Activity

Investment & Funding Dynamics – Global Herbal Tea Market

Executive Framing

Current Market Reality

Valued at USD 4.85 billion in 2025 and projected to reach ~USD 8.12 billion by 2033 (CAGR ~6.6%), the market reflects strong growth momentum supported by rising demand for immunity-boosting, stress-relief, and detox beverages. Europe leads investment activity due to established herbal traditions and premium product penetration, while Asia-Pacific is emerging as a high-growth region attracting new capital. Key players such as Unilever, Twinings, and Tata Consumer Products are investing in organic product lines, premium blends, and digital distribution channels.

Key Signals and Evidence

- Functional Product Innovation: Investments in adaptogen-infused, immunity-boosting, and stress-relief formulations.

- Organic & Clean-Label Growth: Rising funding toward organic certification, non-GMO sourcing, and clean-label positioning.

- Premiumization Strategy: Expansion of artisanal, single-origin, and luxury herbal tea offerings.

- Sustainable Sourcing: Increasing focus on ethical herb sourcing, fair-trade practices, and eco-friendly packaging.

- E-Commerce Expansion: Growth in direct-to-consumer platforms, subscription models, and personalized wellness products.

- Emerging Market Penetration: Investment in Asia-Pacific and Latin America for long-term growth opportunities.

- M&A Activity: Selective acquisitions and partnerships among premium and specialty tea brands.

Strategic Implications

Companies that combine strong brand storytelling, functional product innovation, and sustainable sourcing practices are best positioned for growth. Investors are prioritizing agile brands capable of addressing evolving wellness trends and leveraging digital distribution channels. Premium positioning and transparency in ingredient sourcing are becoming key differentiators in competitive strategy.

Forward Outlook

From 2026 to 2033, investment in the Global Herbal Tea Market is expected to continue rising, with increasing focus on adaptogen integration, organic cultivation, and AI-driven consumer insights. Capital allocation will expand toward sustainable supply chains, biodegradable packaging, and personalized wellness offerings. M&A activity is expected to remain selective but strategic, particularly in premium and niche botanical segments.

Technology & Innovation

Global Herbal Tea Market: Technology & Innovation

Executive Framing

Technology and innovation in the global herbal tea market are focused on enhancing functional efficacy, ensuring ingredient purity, and supporting sustainable sourcing practices. While rooted in traditional herbal knowledge, the market is increasingly integrating modern formulation science, AI-driven consumer insights, and advanced processing techniques to meet rising demand for wellness-oriented and premium botanical beverages.

Current Market Reality

The herbal tea market reflects a balanced mix of traditional practices and modern innovation. Manufacturers are incorporating functional botanicals such as adaptogens, anti-inflammatory herbs, and immunity-boosting ingredients into advanced formulations. AI-driven analytics are being used to track consumer preferences and personalize product offerings. Additionally, innovations in drying, extraction, and blending technologies are improving flavor consistency, shelf life, and nutrient retention. Sustainable sourcing and biodegradable packaging have also become central to product development and brand positioning.

Key Signals and Evidence

- Functional & Adaptogen Innovation: Integration of herbs like ashwagandha, ginseng, turmeric, and elderberry enhances wellness positioning.

- Clean-Label & Organic Certification: Increasing demand for non-GMO, preservative-free, and certified organic herbal teas.

- AI-Driven Consumer Insights: Data analytics enable personalized blends, targeted marketing, and demand forecasting.

- Advanced Processing Techniques: Improved drying, extraction, and blending technologies enhance quality and shelf stability.

- Sustainable Sourcing & Packaging: Ethical herb sourcing, biodegradable tea bags, and eco-friendly packaging support ESG goals.

Strategic Implications

For herbal tea companies, innovation is essential to differentiate in a competitive and fragmented market. Functional formulations allow brands to target specific health benefits such as immunity, stress relief, and digestion. AI-enabled insights enhance product development and consumer targeting, while sustainability initiatives strengthen brand trust and compliance. Companies that successfully combine traditional herbal expertise with modern technology will gain a competitive edge in premium and wellness segments.

Forward Outlook

The global herbal tea market is expected to see continued innovation driven by adaptogen integration, personalized nutrition, and sustainable production practices. Future developments will focus on AI-powered blend customization, next-generation botanical extracts, and circular packaging solutions. As consumers increasingly prioritize health, transparency, and environmental responsibility, innovation will remain a key driver of long-term growth in the post-2026 herbal tea ecosystem.

Market Risk

Risk Factors and Disruption Threats in the Global Herbal Tea Market

Executive Framing

The Global Herbal Tea Market is a fast-growing, wellness-driven segment within the broader beverage industry, supported by rising demand for functional, natural, and plant-based products. With a projected CAGR of ~6.6% from 2026–2033, the market demonstrates strong growth potential but faces risks related to supply chain variability, regulatory scrutiny on health claims, and increasing competitive intensity.

Current Market Reality

Europe leads the market, while Asia-Pacific is the fastest-growing region. The industry benefits from strong alignment with health and wellness trends; however, dependence on agricultural raw materials such as herbs and botanicals introduces supply volatility due to climate conditions and seasonal variability. Additionally, fragmented competition and premium pricing in organic segments create barriers to mass-market scalability.

Key Signals and Evidence

Key signals include rising demand for immunity, detox, and stress-relief formulations, rapid expansion of organic-certified products, and strong growth in e-commerce and subscription models. However, increasing regulatory oversight on functional and medicinal claims, along with competition from green tea, functional beverages, and nutraceutical drinks, are key risk indicators. Variability in raw material quality and sourcing further impacts consistency.

Strategic Implications

Companies must invest in sustainable and diversified sourcing strategies to mitigate raw material risks. Strengthening quality control, certification compliance, and transparent labeling will be critical to maintain consumer trust. Additionally, brands should focus on premium positioning, functional innovation (adaptogens, immunity blends), and omnichannel distribution expansion to sustain growth and competitiveness.

Forward Outlook

The Global Herbal Tea Market is expected to maintain strong growth momentum, driven by wellness trends and clean-label demand. However, long-term success will depend on managing sourcing risks, regulatory compliance, and increasing competition from adjacent functional beverage categories.

Regulatory Landscape

Regulatory & Policy Landscape: Global Herbal Tea Market

Executive Framing

The Global Herbal Tea Market operates within a moderately complex regulatory framework, influenced by food safety standards, herbal ingredient approvals, organic certification systems, and regulations governing health and functional claims. As herbal teas increasingly position themselves as wellness and functional beverages, regulatory scrutiny is expanding across both food and nutraceutical domains.

Key regulatory authorities include the U.S. Food and Drug Administration (FDA), European Food Safety Authority (EFSA), Food Safety and Standards Authority of India (FSSAI), and various national herbal and botanical regulatory bodies. These organizations oversee ingredient safety, permissible health claims, labeling requirements, and contamination limits for herbal products.

Current Market Reality

Europe maintains one of the most stringent regulatory environments, particularly regarding herbal ingredient approvals and health claims under EFSA guidelines. Organic certification standards (EU Organic) are widely enforced, supporting premium product positioning but increasing compliance complexity.

In North America, herbal teas are regulated primarily as food products, but functional and medicinal claims are tightly controlled. The U.S. FDA requires clear labeling, ingredient transparency, and limits on unverified health claims, especially for adaptogens and immunity-focused blends.

Asia-Pacific markets reflect a mix of traditional herbal medicine frameworks and modern food safety regulations. Countries such as China and India have established systems for herbal ingredient approval, but export-oriented products must comply with international standards for pesticide residues, heavy metals, and microbial safety.

Globally, sustainability certifications—including organic, fair-trade, and ethically sourced ingredients—are increasingly becoming both regulatory requirements and competitive differentiators.

Key Signals and Evidence

- Strict regulation of herbal ingredient safety, contaminants, and permissible usage levels.

- Mandatory labeling requirements including ingredient disclosure and origin transparency.

- Tight control over health and functional claims, particularly for adaptogens and medicinal herbs.

- Widespread adoption of organic and fair-trade certification standards.

- Compliance with pesticide residue limits and heavy metal testing.

- Growing regulatory emphasis on sustainable and ethical sourcing practices.

Strategic Implications

Regulatory frameworks significantly influence product innovation, especially in functional and adaptogen-based herbal teas. Companies must invest in scientific validation, certification processes, and supply chain traceability to support health claims and ensure compliance.

Organic certification and clean-label positioning provide strong competitive advantages but require adherence to strict cultivation, processing, and documentation standards. Export-oriented brands must align with multiple regional regulations, increasing operational complexity.

Sustainability compliance is becoming a key differentiator, with consumers and regulators increasingly prioritizing ethical sourcing, biodiversity protection, and environmentally responsible packaging.

Forward Outlook

The regulatory landscape is expected to become more stringent, particularly regarding functional health claims, adaptogen usage, and organic certification standards. Governments and regulatory bodies may introduce clearer frameworks for herbal wellness products, bridging the gap between food and nutraceutical classifications.

Increased global trade will require harmonization of safety standards, testing protocols, and certification systems. Digital traceability, blockchain-enabled sourcing verification, and AI-driven quality monitoring are expected to play a larger role in regulatory compliance.

Companies that proactively align with evolving regulations, invest in sustainable sourcing, and ensure transparency across the value chain will be best positioned to achieve long-term growth and consumer trust in the global herbal tea market.