U.K. Oat Milk Market Report 2026-2033

U.K. Oat Milk Market Forecast Snapshot: 2026–2033

| Metric | Value |

| 2025 Market Size | GBP 420 Million |

| 2033 Market Size | ~GBP 765 Million |

| CAGR (2026–2033) | ~7.4% |

| Largest Segment | Retail Packaged Oat Milk |

| Fastest Growing Segment | Flavored & Barista-Style Oat Milk |

| Key Trend | Plant-Based Innovation & Sustainability Focus |

| Future Focus | Functional Ingredients, Premium Barista Blends, and Eco-Friendly Packaging |

U.K. Oat Milk Market Overview

The UK Oat Milk Market is growing fast. People are choosing oat milk because it's a great option for those who follow plant-based diets, have lactose intolerance, or care about the environment. Oat milk is popular due to its creamy texture, versatility in coffee, tea, and recipes, and low environmental impact compared to dairy milk.

Major players in the market include Oatly, Alpro, Innocent, and Tesco's own brand. The market is expected to keep growing as consumers seek sustainable and healthy alternatives to traditional dairy.

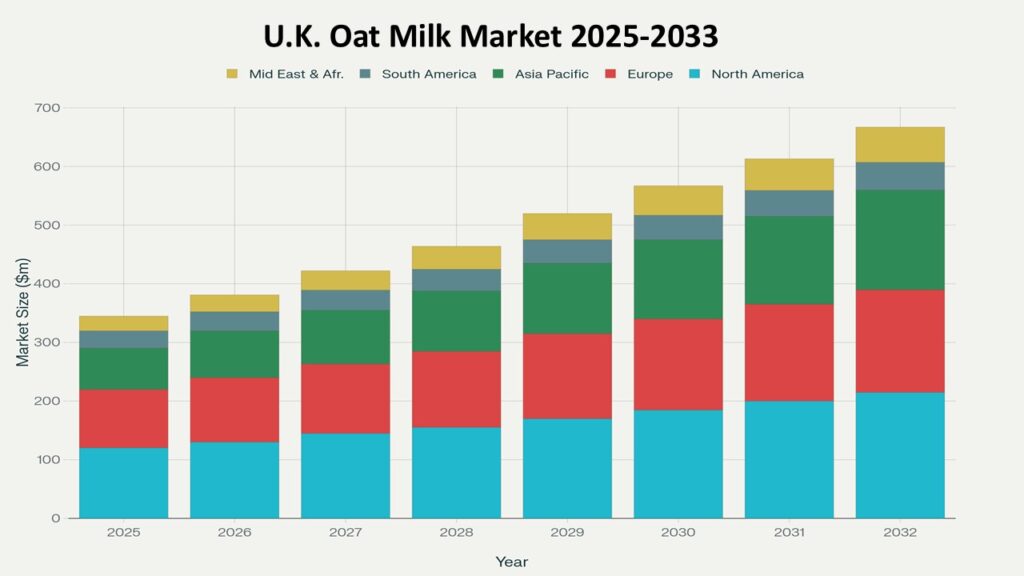

According to Phoenix Research, the U.K. Oat Milk Market was valued at GBP 420 million in 2025 and is projected to reach GBP 765 million by 2033, reflecting a CAGR of ~7.4% during 2026–2033.

The market is primarily driven by increased consumption in coffee shops and home use, expanding retail presence, and rising adoption of premium barista blends. Retail-packaged oat milk dominates in terms of volume, while flavored and fortified variants are witnessing the fastest growth.

The post-2025 outlook indicates further premiumization, adoption of functional ingredients (protein, vitamins, minerals), AI-enabled supply chain optimization, and eco-conscious packaging, reflecting evolving consumer expectations for health, taste, and sustainability.

Key Drivers of U.K. Oat Milk Market Growth

Rising Plant-Based & Vegan Diet Adoption

Growing interest in plant-based nutrition supports increased oat milk consumption.Lactose intolerance and dairy-free preference among millennials and Gen Z are key contributors.

Barista-Style Oat Milk Popularity

Specialty coffee shops and cafes drive demand for creamy, froth-friendly oat milk.Flavored and fortified variants enable differentiation and premium positioning.

Health & Functional Benefits

Low saturated fat, cholesterol-free content, and fortified nutrients appeal to health-conscious consumers.Functional ingredients such as protein, calcium, and vitamins enhance adoption.

Retail Expansion & E-Commerce Penetration

Supermarkets, hypermarkets, convenience stores, and online grocery platforms facilitate wider availability.Subscription-based and direct-to-consumer channels boost accessibility.

Sustainability & Eco-Conscious Packaging

Oat milk production generates lower carbon footprint than dairy milk. Brands emphasizing recyclable and plant-based packaging resonate with environmentally conscious consumers.

U.K. Oat Milk Market Segmentation

1. By Product Type

1.1 Retail Packaged Oat Milk

1.1.1 Standard Oat Milk

1.1.1.1 Original / Unsweetened

1.1.1.2 Low-Fat / Reduced-Calorie

1.1.1.3 Flavored Standard (Vanilla, Chocolate, etc.)

1.1.2 Barista-Style Oat Milk

1.1.2.1 Whole Barista Oat Milk

1.1.2.2 Low-Fat Barista Oat Milk

1.1.2.3 Organic Barista Oat Milk

1.1.3 Flavored / Sweetened Oat Milk

1.1.3.1 Vanilla Flavored

1.1.3.2 Chocolate Flavored

1.1.3.3 Seasonal / Limited Edition Flavors

1.2 Functional & Fortified Oat Milk

1.2.1 Protein-Enriched Oat Milk

1.2.1.1 Plant Protein Blend

1.2.1.2 Added Pea Protein

1.2.1.3 Multi-Protein Fortified

1.2.2 Vitamin & Mineral Fortified

1.2.2.1 Calcium Fortified

1.2.2.2 Vitamin D & B12 Fortified

1.2.2.3 Iron & Zinc Fortified

1.2.3 Organic & Clean Label Oat Milk

1.2.3.1 Certified Organic

1.2.3.2 Non-GMO & Chemical-Free

1.2.3.3 Eco-Friendly / Sustainable Packaging

1.3 Bulk / Institutional Oat Milk

1.3.1 Foodservice Packs

1.3.1.1 1L / 2L Retail Packs for Cafés

1.3.1.2 Bulk 5L / 10L Packs for Restaurants

1.3.1.3 Ready-to-Use Beverage Bases

1.3.2 HoReCa (Hotel, Restaurant, Café) Oat Milk

1.3.2.1 Premium Barista Oat Milk

1.3.2.2 Standard Café Oat Milk

1.3.2.3 Specialty Flavored Oat Milk

1.3.3 Industrial Ingredients

1.3.3.1 Oat Milk Powder

1.3.3.2 Concentrated Oat Extracts

1.3.3.3 Ready-to-Mix Oat Base for Food Processing

2. By Distribution Channel

2.1 Supermarkets & Hypermarkets

2.1.1 National Chains (Tesco, Sainsbury’s, ASDA)

2.1.2 Regional / Local Supermarkets

2.1.3 Discount Retailers (Aldi, Lidl)

2.2 Convenience Stores

2.2.1 Urban Convenience Chains

2.2.2 Independent Local Stores

2.2.3 Petrol Station / Transit Stores

2.3 Online Retail / E-Commerce

2.3.1 Direct-to-Consumer Brand Websites

2.3.2 E-Commerce Marketplaces (Amazon, Ocado)

2.3.3 Subscription / Delivery Services (Milk Delivery, Specialty Boxes)

2.4 Specialty & Health Stores

2.4.1 Organic & Natural Food Retailers

2.4.2 Vegan & Plant-Based Retailers

2.4.3 Boutique / Premium Health Stores

2.5 Foodservice & HoReCa Channels

2.5.1 Coffee Chains & Cafés

2.5.2 Hotels & Restaurants

2.5.3 Catering & Event Services

3. By End-User

3.1 Individual Consumers

3.1.1 Millennials & Gen Z

3.1.1.1 Urban Professionals

3.1.1.2 Social Media & Trend-Driven Consumers

3.1.2 Health-Conscious Adults

3.1.2.1 Fitness Enthusiasts

3.1.2.2 Diet-Specific Consumers (Keto, Vegan, Lactose-Free)

3.1.3 Families & Lactose-Intolerant Consumers

3.1.3.1 Parents Purchasing for Children

3.1.3.2 Lactose-Intolerant Adults

3.2 Corporate & Institutional Clients

3.2.1 Coffee Chains & Cafés

3.2.1.1 National Coffee Chains

3.2.1.2 Independent Specialty Cafés

3.2.2 Hotels & Restaurants

3.2.2.1 Boutique / Luxury Hotels

3.2.2.2 Chain Restaurants & Fast Casual

3.2.3 Healthcare & Educational Institutions

3.2.3.1 Hospitals & Clinics

3.2.3.2 Schools, Colleges & Universities

4. By Region

4.1 United Kingdom – Core Market

4.2 Europe – Influence & Imports

Regional Insights of the U.K. Oat Milk Market

London & Southeast – Premium and Urban Adoption

London and Southeast England lead the U.K. oat milk market, driven by high consumer awareness, a strong café culture, and the presence of premium grocery retailers. These regions exhibit the highest consumption rates, reflecting early adoption of plant-based and specialty dairy alternatives.

Midlands & Northern England – Expanding Mass-Market Segment

Oat milk adoption in the Midlands and Northern England is growing rapidly, fueled by the expansion of supermarkets, retail chains, and mainstream distribution networks. These regions represent significant growth potential as oat milk becomes increasingly accessible to everyday households.

Scotland & Wales – Niche Premium and Sustainable Growth

Scotland and Wales show steady growth, supported by environmentally conscious consumers and lifestyle-driven purchasing patterns. Urban centers and younger demographics are the primary adopters, contributing to a niche but sustainable market expansion in these regions.

Leading Companies in the U.K. Oat Milk Market

Oatly AB

Alpro (Danone)

Plenish

Minor Figures

Rude Health

Oat-ly Good

Provamel

The Collective Dairy Alternative

Oatly AB remains one of the largest and most recognized oat milk brands in the U.K., leveraging strong retail presence, café partnerships, innovative product lines including barista-style and flavored oat milk, and a focus on sustainability and clean-label initiatives.

Strategic & Technological Insights

Phoenix Demand Forecast Engine highlights steady market growth driven by rising adoption of oat milk across retail, café, and HoReCa channels, supported by increasing consumer awareness of plant-based and health-focused alternatives.

The Consumer Behavior Analyzer identifies a growing preference for fortified, functional, and barista-style oat milk among Millennials, Gen Z, and health-conscious adults, alongside increasing demand for sustainable and clean-label products.

The Innovation Tracker emphasizes product fortification (vitamins, calcium, protein, probiotics), barista and culinary integration, eco-friendly packaging solutions, and renewable production practices as key competitive differentiators.

Porter’s Five Forces Analysis reveals moderate to high competitive rivalry, evolving supplier dynamics for sustainable oat sourcing, and significant opportunities for brands leveraging functional innovation, premium café partnerships, and e-commerce strategies to differentiate in the U.K. market.

Why the U.K. Oat Milk Market Remains Critical

-

Promotes healthy, dairy-free, and plant-based lifestyles.

-

Supports sustainability and eco-friendly consumption habits.

-

Encourages product innovation and premiumization in plant-based beverages.

-

Enhances availability across retail, café, and online channels.

-

Integrates nutrition, taste, and lifestyle trends to drive consumer loyalty.

Final Takeaway of U.K. Oat Milk Market

The U.K. Oat Milk Market is steadily evolving into a functional, sustainable, and digitally integrated plant-based beverage ecosystem. The market’s CAGR 2026–2033 reflects robust growth driven by rising health consciousness, premium barista adoption, and innovative product offerings such as fortified, flavored, and clean-label oat milk.

Companies that effectively integrate product innovation, e-commerce and retail expansion, barista and HoReCa partnerships, and sustainable production practices will be best positioned for long-term value creation.

At Phoenix Research, our advanced forecasting models deliver comprehensive U.K. Oat Milk revenue projections, competitive benchmarking, and strategic intelligence — enabling stakeholders to capitalize on post-2025 market opportunities with data-backed confidence and growth-focused strategies.

📢 Social Mentions & Publication Channels

Explore deeper insights and follow our cross-platform updates on LinkedIn, and X for continuous intelligence and market coverage.

LinkedIn : https://www.linkedin.com/feed/update/urn:li:activity:7432099387507384321

X : https://x.com/Pheonix_Insight/status/2026338392460722622?s=20

Table of Contents

1. Market Forecast Snapshot (2026–2033)

1.1 2025 Market Size – GBP 420 Million

1.2 2033 Market Size – ~GBP 765 Million

1.3 CAGR (2026–2033) – ~7.4%

1.4 Largest Segment – Retail Packaged Oat Milk

1.5 Fastest Growing Segment – Flavored & Barista-Style Oat Milk

1.6 Key Trend – Plant-Based Innovation & Sustainability Focus

1.7 Future Focus – Functional Ingredients, Premium Barista Blends, Eco-Friendly Packaging

2. U.K. Oat Milk Market Overview

2.1 Market Definition & Scope

2.2 Evolution of the U.K. Oat Milk Industry

2.3 Plant-Based & Vegan Consumer Adoption

2.4 Premiumization & Barista-Style Oat Milk Growth

2.5 E-Commerce & Retail Expansion

2.6 Post-2025 Market Outlook

3. Key Drivers of U.K. Oat Milk Market Growth

3.1 Rising Plant-Based & Vegan Diet Adoption

3.2 Popularity of Barista-Style Oat Milk

3.3 Health & Functional Benefits (Protein, Vitamins, Minerals)

3.4 Retail Expansion & E-Commerce Penetration

3.5 Sustainability & Eco-Conscious Packaging

3.6 Product Innovation & Flavored Variants

4. Market Segmentation by Product Type

4.1 Retail Packaged Oat Milk

4.1.1 Standard Oat Milk

4.1.1.1 Original / Unsweetened

4.1.1.2 Low-Fat / Reduced-Calorie

4.1.1.3 Flavored Standard (Vanilla, Chocolate, etc.)

4.1.2 Barista-Style Oat Milk

4.1.2.1 Whole Barista Oat Milk

4.1.2.2 Low-Fat Barista Oat Milk

4.1.2.3 Organic Barista Oat Milk

4.1.3 Flavored / Sweetened Oat Milk

4.1.3.1 Vanilla Flavored

4.1.3.2 Chocolate Flavored

4.1.3.3 Seasonal / Limited Edition Flavors

4.2 Functional & Fortified Oat Milk

4.2.1 Protein-Enriched Oat Milk

4.2.1.1 Plant Protein Blend

4.2.1.2 Added Pea Protein

4.2.1.3 Multi-Protein Fortified

4.2.2 Vitamin & Mineral Fortified

4.2.2.1 Calcium Fortified

4.2.2.2 Vitamin D & B12 Fortified

4.2.2.3 Iron & Zinc Fortified

4.2.3 Organic & Clean Label Oat Milk

4.2.3.1 Certified Organic

4.2.3.2 Non-GMO & Chemical-Free

4.2.3.3 Eco-Friendly / Sustainable Packaging

4.3 Bulk / Institutional Oat Milk

4.3.1 Foodservice Packs

4.3.1.1 1L / 2L Retail Packs for Cafés

4.3.1.2 Bulk 5L / 10L Packs for Restaurants

4.3.1.3 Ready-to-Use Beverage Bases

4.3.2 HoReCa (Hotel, Restaurant, Café) Oat Milk

4.3.2.1 Premium Barista Oat Milk

4.3.2.2 Standard Café Oat Milk

4.3.2.3 Specialty Flavored Oat Milk

4.3.3 Industrial Ingredients

4.3.3.1 Oat Milk Powder

4.3.3.2 Concentrated Oat Extracts

4.3.3.3 Ready-to-Mix Oat Base for Food Processing

5. Market Segmentation by Distribution Channel

5.1 Supermarkets & Hypermarkets

5.1.1 National Chains (Tesco, Sainsbury’s, ASDA)

5.1.2 Regional / Local Supermarkets

5.1.3 Discount Retailers (Aldi, Lidl)

5.2 Convenience Stores

5.2.1 Urban Convenience Chains

5.2.2 Independent Local Stores

5.2.3 Petrol Station / Transit Stores

5.3 Online Retail / E-Commerce

5.3.1 Direct-to-Consumer Brand Websites

5.3.2 E-Commerce Marketplaces (Amazon, Ocado)

5.3.3 Subscription / Delivery Services (Milk Delivery, Specialty Boxes)

5.4 Specialty & Health Stores

5.4.1 Organic & Natural Food Retailers

5.4.2 Vegan & Plant-Based Retailers

5.4.3 Boutique / Premium Health Stores

5.5 Foodservice & HoReCa Channels

5.5.1 Coffee Chains & Cafés

5.5.2 Hotels & Restaurants

5.5.3 Catering & Event Services

6. Market Segmentation by End-User

6.1 Individual Consumers

6.1.1 Millennials & Gen Z

6.1.1.1 Urban Professionals

6.1.1.2 Social Media & Trend-Driven Consumers

6.1.2 Health-Conscious Adults

6.1.2.1 Fitness Enthusiasts

6.1.2.2 Diet-Specific Consumers (Keto, Vegan, Lactose-Free)

6.1.3 Families & Lactose-Intolerant Consumers

6.1.3.1 Parents Purchasing for Children

6.1.3.2 Lactose-Intolerant Adults

6.2 Corporate & Institutional Clients

6.2.1 Coffee Chains & Cafés

6.2.1.1 National Coffee Chains

6.2.1.2 Independent Specialty Cafés

6.2.2 Hotels & Restaurants

6.2.2.1 Boutique / Luxury Hotels

6.2.2.2 Chain Restaurants & Fast Casual

6.2.3 Healthcare & Educational Institutions

6.2.3.1 Hospitals & Clinics

6.2.3.2 Schools, Colleges & Universities

7. Market Segmentation by Region

7.1 United Kingdom – Core Market

7.2 Europe – Influence & Imports

8. Regional Insights

8.1 London & Southeast – Premium and Urban Adoption

8.2 Midlands & Northern England – Expanding Mass-Market Segment

8.3 Scotland & Wales – Niche Premium and Sustainable Growth

9. Competitive Landscape

9.1 Market Share Analysis

9.2 Competitive Positioning Matrix

9.3 Retail & HoReCa Expansion Strategies

9.4 Barista-Style & Flavored Oat Milk Innovation

9.5 Pricing, Sustainability & Premiumization Strategies

10. Leading Companies

10.1 Oatly AB

10.2 Alpro (Danone)

10.3 Plenish

10.4 Minor Figures

10.5 Rude Health

10.6 Oat-ly Good

10.7 Provamel

10.8 The Collective Dairy Alternative

11. Strategic Intelligence & AI-Backed Insights

11.1 Phoenix Demand Forecast Engine

11.2 Consumer Behavior & Trend Analytics

11.3 Innovation Tracker – Functional, Barista, Sustainable Packaging

11.4 Porter’s Five Forces Analysis

12. Sustainability & Regulatory Landscape

12.1 Eco-Friendly Packaging & Carbon Footprint Reduction

12.2 Plant-Based Ingredient Sourcing Standards

12.3 Food Safety & Health Regulations

12.4 Responsible Consumption & Labeling

13. Market Significance

13.1 Promotion of Plant-Based & Health-Conscious Lifestyles

13.2 Contribution to Retail, Café & HoReCa Ecosystem

13.3 Employment & Supply Chain Impact

13.4 Integration of Innovation, Sustainability & Consumer Trends

13.5 Repeat Purchase & Brand Loyalty

14. Final Takeaway

14.1 Growth Outlook (2026–2033)

14.2 Dual-Engine Growth Model (Retail Packaged vs. Barista & Functional)

14.3 Premiumization & Mass-Market Expansion Strategy

14.4 E-Commerce, Café & HoReCa Integration

14.5 Strategic Recommendations for Stakeholders