Global Sushi Restaurants Market Report, Size and Forecast 2026-2033

Global Sushi Restaurants Market Forecast Snapshot: 2026–2033

| Metric | Value |

|---|---|

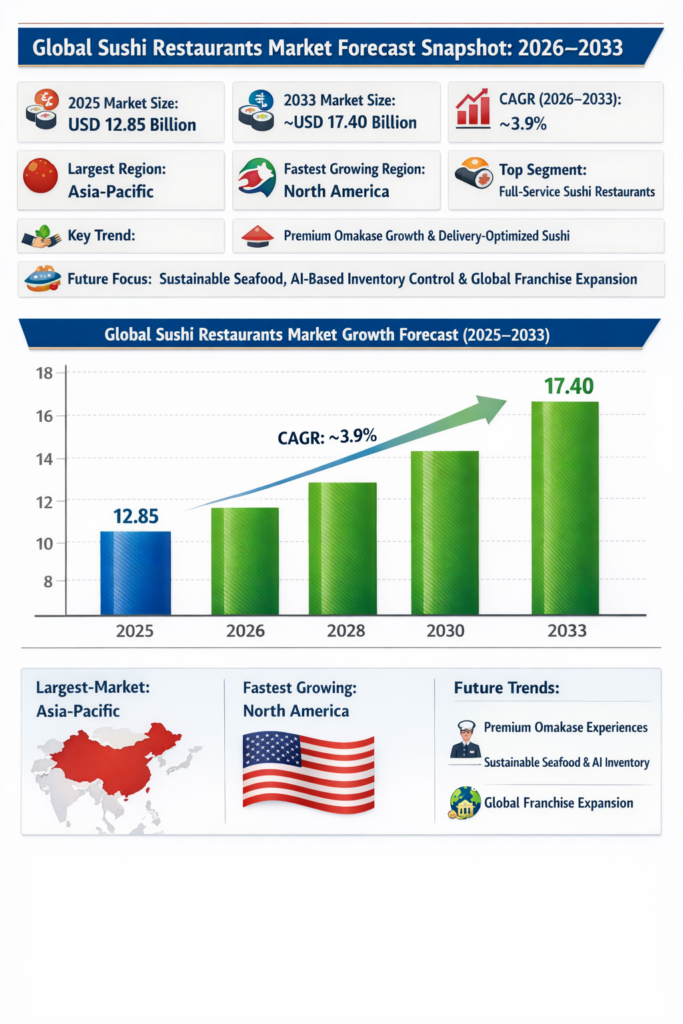

| 2025 Market Size | USD 12.85 Billion |

| 2033 Market Size | ~USD 17.40 Billion |

| CAGR (2026–2033) | ~3.9% |

| Largest Region | Asia-Pacific |

| Fastest Growing Region | North America |

| Top Segment | Full-Service Sushi Restaurants |

| Key Trend | Premium Omakase Growth & Delivery-Optimized Sushi Formats |

| Future Focus | Sustainable Seafood, AI-Based Inventory Control & Global Franchise Expansion |

Global Sushi Restaurants Market Overview

The Global Sushi Restaurants Market includes traditional sushi bars, conveyor-belt (kaiten-zushi) formats, premium omakase counters, sushi-focused casual dining chains, quick-service sushi kiosks, and delivery-only sushi cloud kitchens.

Sushi has evolved from a niche Japanese delicacy into a globally mainstream dining category. Its popularity is driven by increasing preference for seafood-based and perceived healthy meals, growing fascination with Japanese culinary culture, premium experiential dining demand, and strong compatibility with takeaway and delivery platforms.

According to Pheonix Research, the Global Sushi Restaurants Market size is valued at USD 12.85 billion in 2025 and is projected to reach approximately USD 17.40 billion by 2033, reflecting a CAGR of ~3.9% during 2026–2033.

Asia-Pacific holds the largest market share, supported by strong domestic consumption in Japan and expanding sushi chain penetration across China and Southeast Asia. North America represents the fastest-growing region, driven by premium sushi adoption, fusion innovation, and high online delivery penetration.

The Post-2025 outlook indicates rising premiumization through omakase experiences, automation in sushi preparation, AI-powered seafood inventory management, and expansion of scalable franchise-led sushi formats globally.

Table of Contents

Executive Summary

1.1 Market Forecast Snapshot (2026–2033)

1.2 Global Market Size & CAGR Analysis

1.3 Largest & Fastest-Growing Segments

1.4 Region-Level Leadership & Growth Trends

1.5 Key Market Drivers

1.6 Competitive Landscape Overview

1.7 Strategic Outlook Through 2033

Introduction & Market Overview

1.1 Definition of the Global Sushi Restaurants Market

1.2 Scope of the Study

1.3 Industry Evolution & Market Development

1.4 Supply Chain & Distribution Infrastructure

1.5 Impact of Consumer Trends

1.6 Sustainability & Regulatory Landscape

1.7 Technology & Innovation Landscape

Research Methodology

1.1 Primary Research

1.2 Secondary Research

1.3 Market Size Estimation Model

1.4 Forecast Assumptions (2026–2033)

1.5 Data Validation & Triangulation

Market Dynamics

1.1 Drivers

1.1.1 Global Acceptance of Sushi as a Mainstream Cuisine

1.1.2 Delivery & Takeaway Compatibility

1.1.3 Premium Omakase & Experiential Dining

1.1.4 Franchise Expansion of Sushi Chains

1.1.5 Sustainable Seafood & Traceability Demand

1.2 Restraints

1.2.1 High Cost of Premium Seafood

1.2.2 Supply Chain & Cold Chain Complexity

1.2.3 Regulatory & Food Safety Compliance

1.2.4 Market Fragmentation

1.3 Opportunities

1.3.1 Expansion into Emerging Markets

1.3.2 Growth of Delivery-Optimized Sushi Formats

1.3.3 AI-Based Inventory & Demand Forecasting

1.3.4 Sustainable & Plant-Based Sushi Innovation

1.4 Challenges

1.4.1 Maintaining Freshness & Quality Consistency

1.4.2 Operational Cost Management

1.4.3 Competitive Differentiation

1.4.4 Supply Chain Traceability

Global Sushi Restaurants Market Analysis (USD Billion), 2026–2033

1.1 Market Size Overview

1.2 CAGR Analysis

1.3 Regional Revenue Distribution

1.4 Segment Revenue Analysis

1.5 Distribution Channel Analysis

1.6 Consumer Impact Analysis

Market Segmentation (USD Billion), 2026–2033

1.1 By Restaurant Format

1.1.1 Full-Service Sushi Restaurants

1.1.1.1 Traditional Sushi Bars

1.1.1.1.1 Counter-Style Chef Interaction

1.1.1.1.2 Table-Service Sushi Dining

1.1.1.1.3 Family-Owned Independent Sushi Bars

1.1.1.1.4 Urban High-Street Sushi Restaurants

1.1.1.2 Premium Omakase Restaurants

1.1.1.2.1 Michelin-Star Omakase

1.1.1.2.2 Reservation-Only Boutique Concepts

1.1.1.2.3 Seasonal Tasting Menu Sushi

1.1.1.2.4 Luxury Seafood-Focused Omakase

1.1.1.3 Sushi Lounges

1.1.1.3.1 Fusion Sushi Concepts

1.1.1.3.2 Bar-Integrated Sushi Dining

1.1.1.3.3 Nightlife-Oriented Sushi Venues

1.1.1.3.4 Hotel-Integrated Sushi Lounges

1.1.1.4 Casual Dining Sushi Chains

1.1.1.4.1 Mid-Scale National Chains

1.1.1.4.2 Regional Franchise Sushi Brands

1.1.1.4.3 Family-Oriented Sushi Dining

1.1.1.4.4 Mall-Based Casual Sushi Restaurants

1.1.2 Conveyor Belt Sushi (Kaiten-Zushi)

1.1.2.1 Standard Conveyor Formats

1.1.2.1.1 Manual Plate Pricing Systems

1.1.2.1.2 Color-Coded Pricing Models

1.1.2.1.3 Volume-Based Discount Models

1.1.2.2 Technology-Integrated Conveyor Formats

1.1.2.2.1 Automated Plate Tracking (RFID)

1.1.2.2.2 Tablet-Based Ordering Systems

1.1.2.2.3 Smart Table & Digital Menu Integration

1.1.2.3 Premium Conveyor Concepts

1.1.2.3.1 High-Quality Ingredient Conveyor Sushi

1.1.2.3.2 Express Urban Conveyor Units

1.1.2.3.3 Airport & Transit Hub Conveyor Sushi

1.1.3 Quick-Service Sushi

1.1.3.1 Mall & Retail-Based Sushi Kiosks

1.1.3.1.1 Food Court Sushi Counters

1.1.3.1.2 Supermarket In-Store Sushi Counters

1.1.3.1.3 Hypermarket Sushi Outlets

1.1.3.2 Transit & High-Footfall Locations

1.1.3.2.1 Airport Sushi Counters

1.1.3.2.2 Railway & Metro Station Units

1.1.3.2.3 Business District Grab-and-Go Outlets

1.1.3.3 Express Sushi Chains

1.1.3.3.1 Bento + Sushi Combo Formats

1.1.3.3.2 Franchise-Led Quick Sushi Brands

1.1.4 Cloud Kitchen & Delivery-Only Sushi

1.1.4.1 Single-Brand Sushi Cloud Kitchens

1.1.4.1.1 App-Exclusive Sushi Brands

1.1.4.1.2 Subscription Sushi Delivery Models

1.1.4.1.3 Premium Delivery-Only Omakase

1.1.4.2 Multi-Brand Asian Cloud Kitchens

1.1.4.2.1 Japanese + Korean Hybrid Kitchens

1.1.4.2.2 Pan-Asian Sushi Aggregator Models

1.1.4.2.3 Shared Infrastructure Cloud Kitchens

1.1.4.3 Platform-Owned Virtual Sushi Brands

1.1.4.3.1 Aggregator-Launched Sushi Concepts

1.1.4.3.2 Influencer-Led Virtual Sushi Brands

1.1.4.3.3 Data-Driven Micro-Market Sushi Brands

1.2 By Product Type

1.2.1 Nigiri Sushi

1.2.1.1 Tuna (Maguro Variants)

1.2.1.2 Salmon (Sake Variants)

1.2.1.3 Shrimp & Shellfish

1.2.1.4 Premium Seasonal Seafood

1.2.1.5 Plant-Based & Vegan Nigiri

1.2.2 Maki Rolls

1.2.2.1 Traditional Rolls

1.2.2.1.1 Hosomaki

1.2.2.1.2 Futomaki

1.2.2.2 Fusion Rolls

1.2.2.2.1 Uramaki

1.2.2.2.2 Tempura Rolls

1.2.2.2.3 Cream Cheese & Avocado Rolls

1.2.2.3 Premium Specialty Rolls

1.2.2.3.1 Signature Chef Rolls

1.2.2.3.2 Luxury Ingredient Rolls

1.2.2.3.3 Seasonal Rolls

1.2.3 Sashimi

1.2.3.1 Tuna Varieties

1.2.3.2 Salmon Varieties

1.2.3.3 Yellowtail & Mackerel

1.2.3.4 Premium Imported Fish

1.2.3.5 Seafood Platter Assortments

1.2.4 Sushi Platters & Combos

1.2.4.1 Family Sharing Platters

1.2.4.2 Party & Event Trays

1.2.4.3 Corporate Sushi Boxes

1.2.4.4 Value Combo Meals

1.2.5 Specialty & Emerging Categories

1.2.5.1 Vegan & Plant-Based Sushi

1.2.5.2 Low-Carb / Keto Sushi

1.2.5.3 Brown Rice & Health-Focused Sushi

1.2.5.4 Sushi Burritos & Hybrid Formats

1.3 By Distribution Channel

1.3.1 Dine-In

1.3.1.1 Casual Dining

1.3.1.1.1 Family-Oriented Sushi Restaurants

1.3.1.1.2 Urban High-Street Sushi

1.3.1.1.3 Mall-Based Dining Units

1.3.1.1.4 Mid-Scale Franchise Chains

1.3.1.2 Premium Omakase

1.3.1.2.1 Reservation-Only Counters

1.3.1.2.2 Michelin-Star Concepts

1.3.1.2.3 Chef-Owned Boutique Bars

1.3.1.2.4 Seasonal Tasting Menus

1.3.1.3 Hotel & Resort Dining

1.3.1.3.1 Five-Star Hotel Sushi

1.3.1.3.2 Luxury Resort Dining

1.3.1.3.3 Business Hotel Concepts

1.3.1.3.4 Cruise & Hospitality Dining

1.3.1.4 Entertainment District Dining

1.3.1.4.1 Nightlife Sushi Lounges

1.3.1.4.2 Bar & Sushi Hybrid Concepts

1.3.1.4.3 Event-Centric Venues

1.3.1.4.4 Tourist Hub Restaurants

1.3.2 Takeaway

1.3.2.1 Counter Pickup

1.3.2.1.1 In-Store Pickup

1.3.2.1.2 Express Counters

1.3.2.1.3 Combo Pickup Units

1.3.2.1.4 Pre-Packed Displays

1.3.2.2 Pre-Order App Pickup

1.3.2.2.1 Scheduled Pickup

1.3.2.2.2 Click-and-Collect Models

1.3.2.2.3 Loyalty App Pickup

1.3.2.2.4 QR-Based Pickup

1.3.2.3 Drive-Thru Sushi Units

1.3.2.3.1 Standalone Drive-Thru

1.3.2.3.2 Hybrid Units

1.3.2.3.3 Highway Locations

1.3.2.3.4 Automated Lockers

1.3.2.4 Grab-and-Go Displays

1.3.2.4.1 Supermarket Sushi

1.3.2.4.2 Convenience Store Displays

1.3.2.4.3 Office Grab-and-Go

1.3.2.4.4 Airport Displays

1.3.3 Online Delivery

1.3.3.1 Third-Party Aggregators

1.3.3.1.1 App-Based Delivery

1.3.3.1.2 Commission Models

1.3.3.1.3 Data Partnerships

1.3.3.1.4 Cross-Border Delivery

1.3.3.2 Brand-Owned Apps

1.3.3.2.1 Direct-to-Consumer Apps

1.3.3.2.2 Loyalty Integration

1.3.3.2.3 Geo-Targeted Promotions

1.3.3.2.4 AI Personalization

1.3.3.3 Subscription Delivery

1.3.3.3.1 Weekly Sushi Boxes

1.3.3.3.2 Omakase-at-Home

1.3.3.3.3 Corporate Plans

1.3.3.3.4 Family Subscriptions

1.3.3.4 Corporate Bulk Delivery

1.3.3.4.1 Executive Catering

1.3.3.4.2 Event Orders

1.3.3.4.3 Office Programs

1.3.3.4.4 Institutional Contracts

1.3.4 Retail Ready-to-Eat

1.3.4.1 Supermarket Sushi Packs

1.3.4.1.1 Private Label

1.3.4.1.2 Premium Counters

1.3.4.1.3 Value Combos

1.3.4.1.4 Organic Options

1.3.4.2 Convenience Store Sushi

1.3.4.2.1 Single Serve Packs

1.3.4.2.2 Budget Options

1.3.4.2.3 Daily Fresh Models

1.3.4.2.4 24/7 Availability

1.3.4.3 Airport Retail Sushi

1.3.4.3.1 Duty-Free Counters

1.3.4.3.2 Travel Boxes

1.3.4.3.3 Lounge Catering

1.3.4.3.4 Transit Packs

1.3.4.4 Meal Kits & DIY Sushi

1.3.4.4.1 Home Sushi Kits

1.3.4.4.2 Premium Ingredient Kits

1.3.4.4.3 Family DIY Boxes

1.3.4.4.4 Subscription Kits

1.4 By End-User

1.4.1 Individual Consumers

1.4.1.1 Millennials

1.4.1.1.1 Urban Professionals

1.4.1.1.2 Experience-Oriented Diners

1.4.1.1.3 Health-Conscious Consumers

1.4.1.2 Gen Z

1.4.1.2.1 Social Media-Driven Consumers

1.4.1.2.2 Fusion-Oriented Diners

1.4.1.2.3 Delivery-First Consumers

1.4.1.3 Working Professionals

1.4.1.3.1 Office Lunch Crowd

1.4.1.3.2 After-Work Dining

1.4.1.3.3 Business Dining

1.4.1.4 Families

1.4.1.4.1 Weekend Dining

1.4.1.4.2 Celebration Dining

1.4.1.4.3 Bulk Orders

1.4.2 Corporate Customers

1.4.2.1 Catering Contracts

1.4.2.2 Executive Catering

1.4.2.3 Office Meal Programs

1.4.2.4 Event Catering

1.4.3 Institutional Clients

1.4.3.1 Universities

1.4.3.2 Hospitals

1.4.3.3 Office Complexes

1.4.3.4 Transport Catering

1.5 By Region

1.5.1 Asia-Pacific

1.5.2 North America

1.5.3 Europe

1.5.4 Middle East

1.5.5 Latin America

Market Segmentation by Geography

1.1 Asia-Pacific

1.2 North America

1.3 Europe

1.4 Middle East & Africa

1.5 Latin America

Competitive Landscape

1.1 Market Share Analysis

1.2 Brand Positioning & Format Benchmarking

1.3 Menu Innovation & Differentiation Strategies

1.4 Supply Chain & Sourcing Partnerships

1.5 Competitive Intensity & Expansion Strategies

Company Profiles

Strategic Intelligence & Pheonix AI Insights

1.1 Pheonix Demand Forecast Engine

1.2 Consumer Behavior Analyzer

1.3 Innovation Tracker

1.4 Supply Chain Intelligence Analyzer

1.5 Automated Porter’s Five Forces Analysis

Future Outlook & Strategic Recommendations

1.1 Expansion into Emerging Markets

1.2 AI Integration & Digital Ecosystem Optimization

1.3 Premium Omakase & Experiential Dining Strategy

1.4 Sustainable Seafood & Supply Chain Optimization

1.5 Long-Term Market Outlook (2033+)

Appendix

About Pheonix Research

Disclaimer

Competitive Landscape

Competitive Landscape Content

Executive Framing

In the Global Sushi Restaurants Market, the competitive landscape is defined by a fragmented yet chain-strengthening structure, where scalable global sushi brands coexist with premium independent operators and rapidly emerging delivery-first formats.

Key players such as Sushiro, Kura Sushi, Genki Sushi, and Zensho Holdings compete alongside premium operators and luxury dining brands like Nobu Hospitality.

Competitive intensity is moderate to high, shaped by format diversification (premium omakase vs mass sushi chains), global franchise expansion, and increasing delivery ecosystem penetration. The market’s structure supports a dual competitive model, where high-volume standardized chains compete on efficiency, while boutique operators differentiate through craftsmanship, exclusivity, and dining experience.

Current Market Reality

The current market reflects a multi-layered competitive environment, combining global scalability with localized differentiation.

Large chains such as Sushiro and Kura Sushi dominate through:

- Automated and standardized operations

- Conveyor-belt (kaiten) sushi models enabling high throughput

- Aggressive international franchise expansion

Simultaneously, premium players like Nobu Hospitality capture high-margin segments through:

- Omakase and chef-led experiential dining

- Luxury positioning and global brand prestige

Key structural realities include:

- High Fragmentation at Independent Level:

Thousands of standalone sushi restaurants globally intensify localized competition. - Delivery-Led Competitive Expansion:

Sushi’s portability has accelerated cloud kitchen and aggregator-driven competition. - Premium vs Mass Market Segmentation:

Clear separation between affordable sushi chains and premium omakase concepts. - Technology Integration:

AI-driven inventory, automated sushi preparation, and digital ordering systems are increasingly standard. - Regional Competitive Variation:

Asia-Pacific exhibits stronger chain consolidation, while Western markets remain more fragmented.

Key Signals And Evidence

The competitive trajectory is reinforced by several signals:

- Franchise Expansion Momentum:

Sushiro and Kura Sushi are scaling globally, reinforcing chain-led consolidation within organized segments. - Automation as Competitive Lever:

Conveyor systems and robotic preparation are enhancing efficiency and reducing labor dependency. - Premiumization Acceleration:

Nobu Hospitality continues expansion, reflecting strong demand for high-end sushi experiences. - Delivery Ecosystem Growth:

Sushi’s compatibility with takeaway drives intense competition in digital channels and cloud kitchens. - Sustainability Investment:

Increasing focus on traceable seafood sourcing is shaping brand differentiation. - Hybrid Business Models:

Operators are integrating dine-in, takeaway, and delivery to maximize revenue streams.

These signals indicate a transition toward a hybrid competitive ecosystem, where scalability, efficiency, and premium differentiation coexist.

Strategic Implications

The competitive environment requires balanced strategic execution, where operators must align scale, experience, and technology.

1. Dual-Format Strategy is Essential

Companies must combine high-volume chain operations with premium experiential offerings to maximize margins.

2. Technology as a Core Differentiator

AI, automation, and digital ordering systems are critical for cost control and operational efficiency.

3. Delivery-First Competition Intensification

Cloud kitchens and aggregator platforms are lowering entry barriers, increasing supply density.

4. Brand Positioning Drives Value Creation

Premium brands must emphasize authenticity, chef expertise, and exclusivity.

5. Franchise Scalability Advantage

Global expansion is driven by replicable and standardized sushi formats.

6. Supply Chain Optimization is Critical

Efficient seafood sourcing and cold-chain management directly impact profitability and consistency.

Forward Outlook

Looking ahead, the Global Sushi Restaurants Market will evolve into a technology-driven, sustainability-focused, and format-diversified ecosystem.

Key forward trends include:

- AI-Driven Operational Transformation:

Automation and predictive analytics will enhance efficiency and reduce waste. - Expansion of Premium Omakase Dining:

High-margin experiential formats will grow in global urban centers. - Delivery & Cloud Kitchen Dominance:

Digital-first models will continue expanding, intensifying competition. - Sustainability as Competitive Baseline:

Ethical seafood sourcing and eco-friendly practices will become standard. - Global Franchise Expansion:

Chains will scale into emerging markets through asset-light models. - Experience-Led Differentiation:

Dining experience, presentation, and personalization will drive brand loyalty.

In conclusion, the competitive landscape is defined by a fragmented yet strategically evolving structure, where success depends on integrating scalable operations, premium positioning, digital ecosystems, and sustainable sourcing into a unified competitive strategy.

Operators that effectively balance efficiency-driven growth with experiential differentiation will lead the next phase of the Global Sushi Restaurants Market.

Value Chain

Executive Framing

In the Global Sushi Restaurants Market, the value chain is precision-driven, globally interconnected, and highly sensitive to perishability, where sourcing, handling, and delivery speed directly influence quality and margins. With the market expanding from USD 12.85 billion in 2025 to ~USD 17.40 billion by 2033 (CAGR ~3.9%), value chain efficiency is essential to balance premiumization with scalability.

The operational structure reflects a hybrid model combining franchise-led chains, independent premium sushi bars, and cloud kitchen formats, while distribution operates through a fully hybrid omnichannel ecosystem (dine-in, takeaway, delivery, and retail-ready formats). Supply chain complexity is moderate but highly time- and quality-sensitive, driven by global seafood sourcing and strict freshness requirements.

As sushi transitions into a global mainstream category, the value chain must optimize cold-chain logistics, inventory turnover, and sourcing traceability, making operational precision a critical competitive factor.

Current Market Reality

The global sushi value chain operates within a three-tiered structure:

1. Premium & Omakase Layer

- Heavy reliance on imported, high-grade seafood

- Chef-led preparation with minimal standardization

- High margins but limited scalability

2. Franchise & Chain Layer

- Standardized procurement and centralized sourcing

- Conveyor-belt (kaiten-zushi) and casual sushi formats

- High throughput with optimized cost structures

3. Delivery & Retail Layer

- Sushi boxes, platters, and ready-to-eat formats

- Integration with aggregators and retail channels (supermarkets, convenience stores)

- Focus on volume-driven scalability

Key constraints:

- Extreme perishability of raw seafood

Requires advanced cold-chain logistics and rapid inventory turnover, increasing operational risk. - Global seafood sourcing volatility

Price fluctuations, regulatory constraints, and environmental factors impact supply stability. - High dependency on quality control and handling

Any disruption in storage or logistics directly affects product integrity and brand trust. - Aggregator-driven margin pressure

Delivery platforms compress margins while expanding reach.

Despite these challenges, the market is supported by:

- Increasing adoption of AI-based inventory control systems

- Growth of automation in sushi preparation and conveyor systems

- Expansion of franchise-led global sushi chains

Key Signals And Evidence

Several strong signals are shaping the sushi value chain globally:

1. Rapid Growth of Delivery-Optimized Sushi Formats

Sushi’s compatibility with takeaway and delivery is driving high-volume, standardized production models, improving scalability but increasing logistics complexity.

2. Premium Omakase Expansion

Rising demand for high-end dining is increasing reliance on imported premium seafood, elevating supplier influence and cost sensitivity.

3. Automation in Sushi Preparation

Conveyor systems, robotic sushi-making, and smart kitchens are improving consistency, speed, and labor efficiency.

4. AI-Based Inventory and Waste Reduction

AI tools are optimizing stock levels, demand forecasting, and spoilage reduction, critical in a highly perishable supply chain.

5. Sustainability and Traceability Requirements

Consumers and regulators are demanding responsibly sourced seafood and transparent supply chains, reshaping procurement strategies.

6. Expansion of Retail-Ready Sushi Channels

Supermarkets, convenience stores, and meal kits are adding new downstream layers, increasing accessibility but requiring strict quality control systems.

Strategic Implications

These signals translate into several strategic priorities:

- Cold-Chain Optimization as Core Capability

Efficient temperature-controlled logistics and storage systems are essential to maintain product quality and reduce losses. - Supply Chain Diversification for Seafood Sourcing

Building multi-source supplier networks reduces exposure to price volatility and supply disruptions. - Hybrid Distribution Strategy

Balancing dine-in premium formats with delivery, takeaway, and retail channels enables revenue diversification and scalability. - Automation for Consistency and Cost Efficiency

Robotic preparation and conveyor systems improve throughput while reducing labor dependency. - AI-Driven Inventory Management

Advanced demand forecasting minimizes waste and enhances margin control in a perishable product environment. - Sustainability as a Competitive Differentiator

Transparent sourcing and eco-friendly practices strengthen brand positioning and regulatory compliance.

Forward Outlook

Looking ahead, the global sushi restaurant value chain is expected to evolve into a highly synchronized, technology-driven, and sustainability-focused ecosystem.

Key future developments:

- End-to-end AI integration across sourcing, inventory, and operations

- Advanced cold-chain and seafood traceability systems

- Expansion of cloud kitchens and retail-ready sushi formats

- Greater automation in sushi preparation and service delivery

- Localization of sourcing to reduce global dependency risks

As the market matures, value chain precision and speed will become the defining factors of success, surpassing traditional brand differentiation.

Operators that successfully integrate:

- resilient seafood sourcing,

- AI-driven inventory control, and

- multi-channel distribution systems

will achieve superior quality consistency, margin stability, and global scalability in the evolving Global Sushi Restaurants Market.

Investment Activity

Executive Summary – Investment Activity

Investment Framing

The Global Sushi Restaurants Market is experiencing measured and strategically targeted investment activity, reflecting its stable growth trajectory (~3.9% CAGR) and strong positioning across both premium and scalable dining formats. With market size projected to expand from USD 12.85 billion in 2025 to ~USD 17.40 billion by 2033, capital flows are increasingly directed toward efficiency optimization, premium dining experiences, and franchise-led global expansion.

Investment strategies are centered on a dual-structure model, combining high-margin omakase concepts with high-volume, delivery-optimized sushi formats, enabling balanced risk-return profiles.

Current Investment Landscape

The market demonstrates a fragmented yet innovation-driven investment environment, where capital is distributed across both global chains and independent premium operators.

Key investment areas include:

- Premium omakase and chef-led sushi counters

- Conveyor-belt and casual sushi chains

- Delivery-first and cloud kitchen sushi brands

- AI-enabled inventory and kitchen automation systems

Global leaders such as Sushiro and Kura Sushi are accelerating cross-border franchise expansion, while boutique operators attract investment through luxury positioning and differentiated dining experiences.

Key Investment Signals

- Premiumization as a Core Investment Theme:

Strong capital allocation toward high-end omakase formats reflects a focus on margin expansion. - Delivery-Centric Investment Growth:

Sushi’s compatibility with takeaway is driving investment into asset-light, scalable delivery models. - Franchise Expansion Momentum:

Global rollout of sushi chains signals confidence in standardized and replicable formats. - Technology Integration:

AI-based seafood inventory control and automation are becoming essential investment priorities. - Sustainability-Driven Capital Allocation:

Increasing investment in traceable seafood sourcing and eco-compliance enhances brand positioning.

Structural Investment Drivers

- Rising Demand for Healthy, Seafood-Based Diets

Sushi’s health positioning supports long-term investment stability. - Omnichannel Scalability (Dine-In + Delivery)

Strong alignment with delivery and takeaway enables diversified revenue streams. - Global Franchise Replication Potential

Proven chain models allow efficient international scaling. - Perishable Supply Chain Optimization Needs

Investments in AI and cold-chain logistics are critical for profitability.

Strategic Implications for Investors

- Dual Strategy is Critical:

Balance premium experiential formats with scalable chain models. - Asset-Light Expansion Advantage:

Cloud kitchens and delivery brands offer capital-efficient growth. - Technology as a Margin Lever:

AI and automation are essential for waste reduction and cost control. - Sustainability as Differentiation:

Ethical sourcing strengthens brand trust and long-term competitiveness.

Forward Investment Outlook

- Short-term (1–3 years):

Expansion of delivery-first formats and premium dining - Mid-term (3–7 years):

Franchise globalization and automation adoption - Long-term:

Fully AI-integrated, supply-chain-optimized sushi ecosystems

Final Investment Perspective

The Global Sushi Restaurants Market represents a stable, moderate-growth investment environment, where success is driven by operational efficiency, premium positioning, and scalable business models.

Capital will continue to favor:

- Premium omakase dining

- Conveyor-belt and casual sushi chains

- Delivery and cloud kitchen ecosystems

- AI-enabled operations

- Sustainable seafood sourcing

Overall, the market offers consistent and risk-balanced investment opportunities, particularly for stakeholders leveraging technology integration, franchise scalability, and premium differentiation strategies.

Technology & Innovation

Executive Framing

The Global Sushi Restaurants market is undergoing a precision-driven technological transformation, where automation, AI-based inventory systems, and delivery optimization are reshaping both operational efficiency and customer experience. As sushi evolves from a traditional culinary craft into a globally scalable foodservice category, technology is becoming essential to maintain consistency, freshness, and speed in a highly perishable product environment.

This market dimension is particularly critical due to the increasing need for real-time seafood inventory control, cold-chain optimization, and delivery-compatible formats, which require advanced digital infrastructure. At the same time, premium omakase dining continues to demand technology-enabled personalization without compromising authenticity.

The innovation landscape reflects a moderate innovation intensity with moderate patent activity, where differentiation is driven by process automation, supply chain intelligence, and service optimization rather than deep core-tech inventions. The market is advancing toward a globally standardized yet digitally enhanced sushi ecosystem.

Current Market Reality

The current market is defined by integration of automation, AI-driven inventory management, and omnichannel delivery systems across both full-service and quick-service sushi formats. Leading players such as Sushiro, Kura Sushi, Genki Sushi, and Nobu Hospitality are leveraging technology to ensure operational precision, scalability, and premium customer engagement.

Core technology layers include:

- AI-based seafood inventory and demand forecasting systems

- Automated sushi preparation and conveyor-belt (RFID-enabled) serving systems

- Tablet and app-based ordering platforms

- Cloud kitchen and delivery-first sushi infrastructure

For example, Kura Sushi utilizes RFID-based plate tracking and automated service systems, while Sushiro focuses on high-throughput conveyor automation and digital ordering integration.

The market is in a growth-stage maturity, where core digital and automation systems are widely deployed, but advanced AI personalization and full kitchen automation are still scaling globally.

Demand is driven by:

- Need for freshness control in perishable seafood supply chains

- Expansion of delivery-optimized sushi formats

- Growth in premium omakase and experiential dining

- Increasing demand for operational efficiency and waste reduction

Key Signals And Evidence

- AI-Based Inventory & Waste Optimization

Sushi operators are deploying AI to manage real-time seafood inventory, reduce spoilage, and optimize procurement cycles. - Automation in Conveyor & Kitchen Systems

RFID-enabled conveyor belts and robotic sushi preparation are improving speed, accuracy, and consistency. - Delivery Ecosystem Expansion

Platforms like Uber Eats, DoorDash, and Deliveroo are enabling global scalability of sushi formats. - Premium Dining Digitization

Omakase formats are integrating digital reservations, customer profiling, and curated tasting experiences. - Sustainability & Traceability Technologies

Increasing adoption of blockchain-based seafood tracking, eco-label certifications, and transparent sourcing systems. - Retail & Ready-to-Eat Integration

Technology-enabled cold storage, packaging, and logistics systems are expanding sushi into retail and supermarket channels.

Strategic Implications

For Sushi Operators:

Technology is critical for managing perishability, consistency, and scalability. Operators must:

- Invest in AI-driven inventory and supply chain systems

- Optimize delivery and takeaway formats

- Maintain quality standards across locations

Balancing automation with artisanal sushi craftsmanship remains a key strategic challenge.

For Technology Providers:

Opportunities lie in:

- AI-based inventory and cold-chain optimization tools

- Automation systems for sushi preparation

- Supply chain traceability and sustainability platforms

Challenges include:

- Integration with diverse restaurant formats

- Cost barriers for independent sushi operators

For Market Structure:

- Large chains gain advantage through automation scale and supply chain control

- Premium players differentiate via experience and ingredient quality

- Smaller operators rely on niche positioning and aggregator platforms

Risk Layer:

- High dependency on seafood supply chains

- Price volatility of premium ingredients

- Technology investment vs ROI constraints

Forward Outlook (2026–2033)

The Global Sushi Restaurants market is expected to evolve into a highly automated, AI-optimized, and sustainability-driven ecosystem.

Key future trajectories include:

- AI-Driven Precision Inventory Systems

Fully automated procurement and waste reduction for seafood supply chains. - Advanced Sushi Automation

Robotic preparation systems ensuring consistency and scalability across global chains. - Blockchain-Based Seafood Traceability

End-to-end transparency in sourcing, improving consumer trust and regulatory compliance. - Hyper-Personalized Dining Experiences

AI-driven menu customization based on dietary preferences and consumption behavior. - Omnichannel Sushi Distribution

Seamless integration across dine-in, delivery, retail-ready, and subscription models. - Cold-Chain & Packaging Innovation

Advanced packaging systems ensuring freshness in long-distance delivery and retail formats.

The market will continue to be driven by:

- Global demand for healthy, seafood-based diets

- Expansion of delivery-first food ecosystems

- Premium experiential dining trends

Final Strategic View

The Global Sushi Restaurants market is transitioning into a technology-intensive, precision-driven, and globally scalable dining ecosystem, where success depends on integrating AI, automation, and supply chain intelligence with culinary authenticity.

Companies that effectively leverage:

- AI-based inventory and demand forecasting

- Automation in preparation and service systems

- Sustainable and traceable seafood sourcing

- Omnichannel delivery and retail integration

will emerge as global leaders, while others risk inefficiencies in a highly competitive and perishability-sensitive market environment.

Market Risk

Executive Framing

The Global Sushi Restaurants Market is evolving within a structurally sensitive framework defined by high dependency on perishable seafood supply chains, premiumization pressures, and globally fragmented competition. While the overall market risk level remains moderate, sushi as a category carries elevated operational and sourcing risks compared to broader Japanese cuisine segments.

Sushi restaurants operate within a precision-driven, freshness-critical model where ingredient quality, cold-chain logistics, and sourcing reliability are essential. This creates inherent vulnerabilities linked to seafood price volatility, sustainability regulations, and global supply disruptions.

Additionally, the market’s dual structure—premium omakase dining and scalable quick-service sushi formats—introduces divergent risk dynamics. Premium formats are highly sensitive to discretionary spending and economic cycles, while mass-market formats face intense competition, price sensitivity, and margin compression. These combined pressures influence cost structures, pricing flexibility, and long-term scalability across regions.

Current Market Reality

The current market reflects steady growth supported by global sushi adoption and strong omnichannel integration. Leading operators such as Sushiro, Kura Sushi, and Genki Sushi are expanding through franchise-led models, technology-integrated conveyor systems, and delivery-optimized formats.

AI-based inventory management, automated sushi preparation, and digital ordering systems are improving operational efficiency and reducing waste in a highly perishable category. Delivery platforms and retail-ready sushi formats are further enhancing accessibility and volume growth.

However, operational constraints remain significant. The reliance on high-quality seafood—often imported—creates exposure to cost fluctuations, supply inconsistencies, and regulatory compliance challenges. Cold-chain logistics failures or delays can directly impact product quality and brand reputation.

Additionally, increasing competition from cloud kitchens, supermarket sushi, and convenience retail formats is intensifying price pressure. Labor challenges, particularly the need for skilled sushi chefs in premium segments, further add to operational complexity.

Key Signals And Evidence

A primary signal is the volatility in global seafood supply chains. Overfishing regulations, climate-related disruptions, and sustainability certification requirements are affecting availability and pricing of key ingredients such as tuna and salmon.

Another critical signal is the rise of retail-ready and supermarket sushi formats, which are expanding consumer access but increasing substitution pressure for traditional dine-in restaurants.

The growth of delivery-first and cloud kitchen sushi brands is lowering entry barriers and intensifying competition, particularly in urban markets. This trend is contributing to margin compression and price sensitivity in mid-range segments.

Consumer preferences are also shifting toward plant-based and alternative sushi options, reflecting broader dietary trends and introducing substitution risks for traditional seafood-based offerings.

Additionally, the high perishability of sushi products increases operational risk, as inventory mismanagement or demand forecasting errors can lead to waste, financial losses, and quality inconsistencies.

Strategic Implications

The market’s risk structure requires targeted and efficiency-driven strategic responses.

First, strengthening cold-chain logistics and supply chain traceability is critical to ensure consistent quality and mitigate sourcing risks. Investments in AI-based inventory forecasting and supplier diversification will enhance resilience.

Second, operators must balance premiumization with affordability by adopting multi-format strategies that include both high-end omakase experiences and scalable quick-service or delivery formats.

Third, differentiation through quality, sourcing transparency, and brand authenticity will be essential to counter increasing competition from retail and cloud kitchen formats.

Fourth, menu innovation should incorporate plant-based and health-oriented alternatives to address evolving consumer preferences while expanding addressable markets.

Finally, reducing dependency on third-party delivery platforms through proprietary digital ecosystems can help protect margins and strengthen customer relationships.

Forward Outlook

Looking ahead to 2026–2033, the Global Sushi Restaurants Market is expected to maintain steady growth, supported by rising global demand for seafood-based cuisine, premium dining experiences, and convenient takeaway formats.

However, the market will become increasingly operationally intensive, with supply chain resilience, cost control, and waste reduction emerging as critical success factors. Technological integration will play a key role in optimizing inventory management, improving efficiency, and enhancing customer personalization.

Sustainability will become a defining competitive factor, particularly in seafood sourcing, with stricter regulations and consumer expectations driving industry transformation.

Competitive intensity will remain high due to low entry barriers in delivery and retail formats, requiring continuous innovation and differentiation.

In conclusion, the Global Sushi Restaurants Market presents a stable but structurally sensitive growth environment, where success will depend on the ability to manage supply chain volatility, maintain product quality, and build scalable, technology-enabled, and resilient business models.

Regulatory Landscape

Executive Framing

The regulatory and policy environment in the Global Sushi Restaurants Market is critically centered on food safety, seafood traceability, cold chain logistics, and international compliance standards. Due to the inherent risk associated with raw seafood consumption, regulatory frameworks are significantly more stringent compared to broader foodservice segments, directly influencing operational protocols, sourcing strategies, and quality assurance systems.

As the market expands from USD 12.85 billion in 2025 to approximately USD 17.40 billion by 2033, regulatory oversight becomes a key determinant of scalability, particularly for global franchise expansion and premium omakase formats. Policies governing seafood imports, hygiene standards, sustainability certifications, and digital delivery systems are shaping both competitive dynamics and cost structures.

With increasing adoption of AI-driven inventory systems and delivery-optimized sushi formats, regulatory alignment is essential for ensuring safety, minimizing waste, and maintaining consumer trust across diverse global markets during the 2026–2033 forecast period.

Current Market Reality

The current regulatory landscape in the Global Sushi Restaurants Market is highly stringent and multi-layered, primarily driven by food safety enforcement, seafood import controls, and increasing sustainability mandates.

Food safety regulations are the most critical component, with strict requirements for hygiene, storage, preparation, and handling of raw seafood. Regulatory authorities mandate precise temperature control, contamination prevention, and routine inspections, especially for sushi and sashimi products.

Seafood sourcing is governed by comprehensive import regulations, certification standards, and traceability requirements. Restaurants must ensure compliance with international quality benchmarks, which directly affects supplier selection, procurement timelines, and cost structures.

Cold chain compliance is essential, requiring uninterrupted temperature-controlled logistics from sourcing to final consumption. Any lapse in cold chain integrity can result in regulatory penalties and significant reputational damage.

The growth of delivery-first sushi models and cloud kitchens introduces additional compliance requirements related to packaging standards, food safety during transit, and digital transaction governance.

Sustainability regulations are also intensifying globally, encouraging responsible fishing practices, certified sourcing, and reduction of environmental impact through eco-friendly packaging and waste management.

Key Signals and Evidence

The Global Sushi Restaurants Market is shaped by several key regulatory signals:

- Strict Raw Seafood Handling and Food Safety Regulations:

Mandatory compliance with hygiene, temperature control, and preparation standards ensures consumer safety in a high-risk food category. - Seafood Import, Certification, and Traceability Frameworks:

International sourcing regulations require documented traceability and quality certification, impacting supply chain design. - Cold Chain Logistics Compliance:

Continuous temperature monitoring and controlled transportation are essential regulatory requirements for maintaining product integrity. - Digital Delivery and Packaging Regulations:

Expansion of online delivery introduces compliance related to packaging safety, transit handling, and digital payment systems. - Sustainability and Responsible Sourcing Policies:

Increasing regulatory focus on certified sustainable seafood and eco-friendly operations is influencing procurement and branding strategies. - Multi-Jurisdictional Operational Compliance:

Global expansion requires adherence to diverse regulatory frameworks across regions, increasing complexity in franchise and operational models.

These signals collectively establish a highly compliance-driven ecosystem focused on safety, traceability, and sustainability.

Strategic Implications

The regulatory environment creates significant strategic considerations:

- High Entry Barriers:

Stringent food safety, import, and cold chain requirements increase capital investment and operational complexity, limiting entry for smaller players. - Supply Chain Risk and Cost Sensitivity:

Dependence on regulated seafood imports exposes operators to compliance risks, price volatility, and logistical challenges. - Operational Cost Intensification:

Investments in cold chain infrastructure, certification processes, and sustainability compliance elevate overall cost structures. - Technology as a Compliance Enabler:

AI-based inventory management, traceability systems, and automated monitoring enhance compliance efficiency and reduce waste. - Franchise Expansion Constraints:

Multi-country regulatory differences require localized strategies, impacting the speed and scalability of global expansion. - Sustainability as Differentiation:

Early adoption of certified sourcing and eco-friendly practices strengthens brand credibility and aligns with evolving regulatory expectations.

Forward Outlook (2026–2033)

Looking ahead, the regulatory landscape in the Global Sushi Restaurants Market is expected to become more advanced, technology-integrated, and sustainability-driven.

Food safety regulations will likely incorporate real-time monitoring technologies, stricter inspection protocols, and enhanced traceability systems across seafood supply chains. Cold chain compliance will become more digitized, with increased use of IoT-enabled tracking systems.

Sustainability regulations will intensify, enforcing stricter adherence to certified fishing practices, carbon footprint reduction, and elimination of single-use plastics.

Digital regulations will evolve alongside AI adoption, requiring enhanced data security, transparency in automated systems, and compliance with global digital commerce standards.

Cross-border regulatory harmonization may improve to support global trade, but regional variations will continue to require adaptive compliance strategies.

Companies that invest in compliance-driven innovation, advanced supply chain systems, and sustainable sourcing networks will be best positioned to capitalize on the projected ~3.9% CAGR and sustain long-term competitive advantage.

Final Insight

The regulatory landscape in the Global Sushi Restaurants Market is a high-complexity, compliance-intensive system where food safety, cold chain integrity, and seafood traceability are paramount. Operators that effectively integrate regulatory compliance with technological innovation and global scalability will define the next phase of growth in this precision-driven and globally expanding market.