Global Medical Tourism Market size and share Analysis 2026-2033

Global Medical Tourism Market Forecast Snapshot: 2026???2033

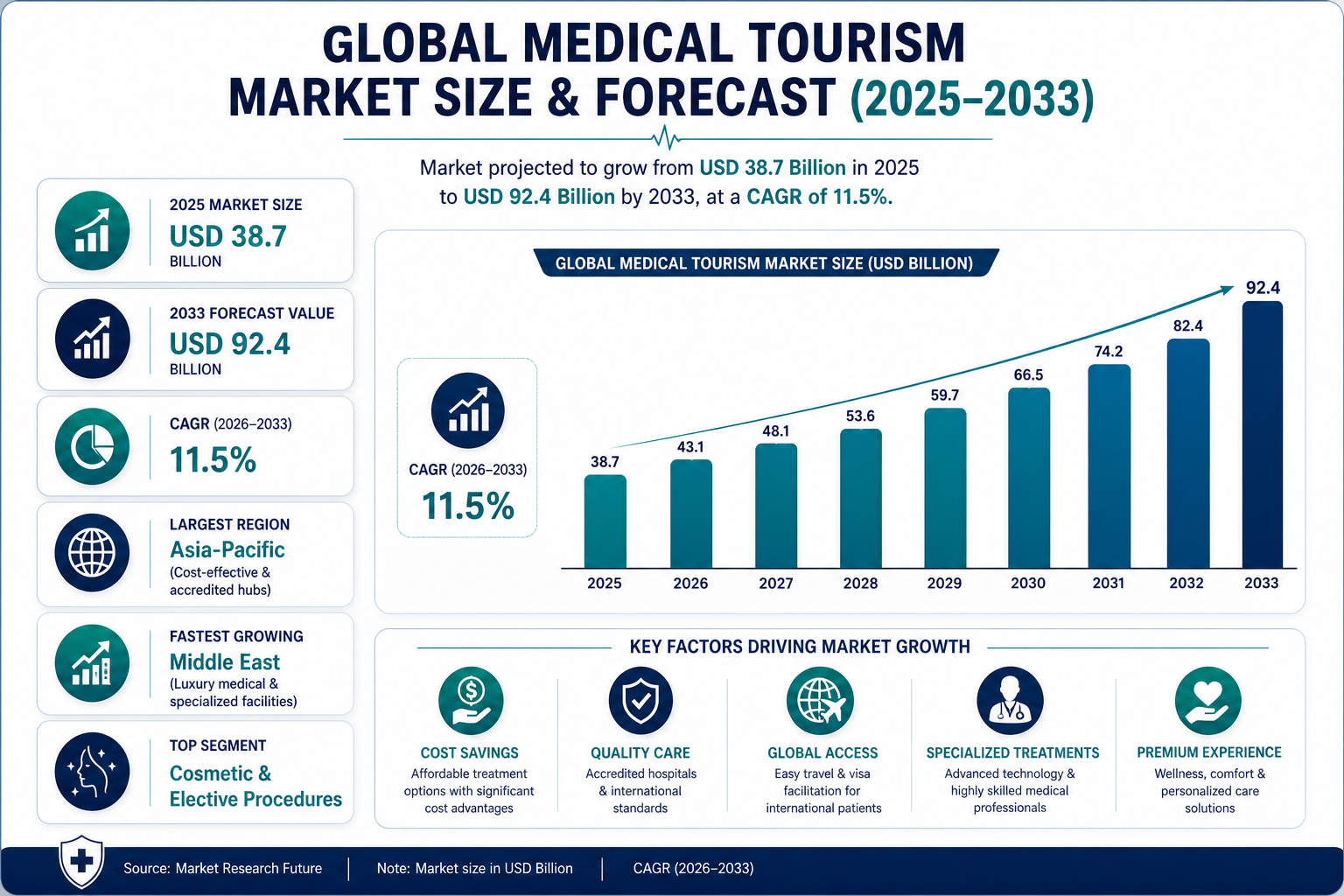

| Metric | Value |

| 2025 Market Size | USD 38.7 Billion |

| 2033 Market Size | USD 92.4 Billion |

| CAGR (2026???2033) | ~11.5% |

| Largest Region | Asia-Pacific |

| Fastest Growing Region | Middle East |

| Top Segment | Cosmetic & Elective Procedures |

| Key Trend | Cross-Border Specialized Healthcare & Cost Arbitrage |

| Future Focus | Digital Health Integration & Integrated Care Packages |

Global Medical Tourism Market Overview

The Global Medical Tourism Market is witnessing strong growth as patients increasingly travel across borders to access affordable, high-quality, and specialized medical treatments. Rising healthcare costs in developed nations, long waiting times for elective procedures, and growing global healthcare connectivity are accelerating cross-border patient mobility. According to Pheonix Research, the Global Medical Tourism Market was valued at USD 38.7 Billion in 2025 and is projected to reach USD 92.4 Billion by 2033, registering a CAGR of ~11.5% during 2026???2033. Growth is fueled by cost advantages, internationally accredited hospitals, advanced surgical capabilities, and expanding digital consultation platforms. Asia-Pacific currently dominates the market due to competitive treatment costs, strong private healthcare infrastructure, and government-supported medical tourism initiatives in countries such as India, Thailand, Malaysia, Singapore, and South Korea. The Middle East is emerging as the fastest-growing region, supported by luxury medical facilities, specialized treatment hubs, and strategic healthcare investments. Post-2025, the market is expected to shift toward integrated healthcare travel packages combining treatment, rehabilitation, telemedicine follow-ups, and hospitality services ??? positioning medical tourism as a structured global healthcare delivery model rather than a cost-driven alternative.Key Drivers of Global Medical Tourism Market Growth

Rising Healthcare Costs in Developed Economies

Patients from the United States, Canada, and Western Europe seek affordable treatment options abroad due to significantly lower procedural costs in emerging markets.Long Waiting Times for Elective Procedures

Delays in surgeries such as orthopedic replacements and cosmetic procedures are encouraging cross-border treatment.International Accreditation & Quality Standards

Growing adoption of JCI and NABH accreditations enhances patient trust in overseas healthcare providers.Growth of Cosmetic & Wellness Tourism

Rising demand for cosmetic surgery, dental aesthetics, fertility treatments, and wellness therapies contributes significantly to market expansion.Digital Health & Teleconsultation Platforms

Virtual consultations, online treatment planning, and remote follow-ups reduce perceived risk and improve international patient coordination.Global Medical Tourism Market Segmentation

-

By Treatment Type

2.By Service Provider

2.1 Public Hospitals 2.1.1 Government-Affiliated Hospitals 2.1.1.1 International Patient Departments 2.1.2 Teaching Hospitals 2.1.2.1 Advanced Research & Clinical Units 2.1.3 Specialty Public Institutes 2.1.3.1 Centers of Excellence 2.2 Private Hospitals 2.2.1 Multi-Specialty Hospitals 2.2.1.1 International Patient Divisions 2.2.2 Specialty Clinics 2.2.2.1 Procedure-Specific Centers 2.2.3 Internationally Accredited Hospitals 2.2.3.1 Quality & Compliance Units 2.3 Medical Tourism Facilitators 2.3.1 Travel Coordination Services 2.3.1.1 Comprehensive Treatment Packages 2.3.2 Insurance & Documentation Support 2.3.2.1 Claims & Reimbursement Management 2.3.3 Post-Treatment Follow-Up Services 2.3.3.1 Digital Continuity of Care Platforms?? ??3.By Patient Origin

3.1 North America 3.1.1 United States 3.1.1.1 Key Outbound Treatment Categories 3.1.2 Canada 3.1.2.1 Key Outbound Treatment Categories 3.2 Europe 3.2.1 Western Europe 3.2.1.1 Major Source Countries 3.2.2 Eastern Europe 3.2.2.1 Emerging Outbound Markets 3.3 Middle East 3.3.1 GCC Countries 3.3.1.1 Government-Sponsored Treatment Programs 3.3.2 Other Middle Eastern Nations 3.3.2.1 Private Outbound Patient Segment 3.4 Africa 3.4.1 Sub-Saharan Africa 3.4.1.1 High-Value Outbound Procedures 3.4.2 North Africa 3.4.2.1 Preferred Treatment Destinations-

ByRegion

Regional Insights of Global Medical Tourism Market

Asia-Pacific ??? Largest Market

Asia-Pacific dominates the global medical tourism landscape, supported by cost-effective treatment packages, internationally accredited hospitals, skilled medical professionals, and proactive government initiatives promoting healthcare tourism. Countries such as India, Thailand, Malaysia, and South Korea have emerged as leading global hubs, offering advanced procedures across cardiology, orthopedics, oncology, fertility, and cosmetic surgery.Middle East ??? Fastest Growing Market

The Middle East is witnessing rapid expansion, driven by large-scale investments in world-class healthcare infrastructure and premium medical facilities. The UAE, Turkey, and Saudi Arabia are positioning themselves as regional treatment destinations by combining specialized medical expertise with luxury hospitality services and streamlined patient facilitation programs.Europe

Europe maintains strong positioning in dental, cosmetic, and orthopedic tourism, particularly in countries such as Turkey, Hungary, Poland, and Spain. Competitive pricing, high clinical standards, and proximity to Western European patients continue to support steady inbound medical travel within the region.North America

North America represents a major outbound medical tourism source market due to elevated healthcare costs and insurance limitations. Patients from the United States and Canada frequently travel to destinations such as Mexico and Costa Rica for affordable dental, bariatric, and elective surgical procedures.South America

South America is gaining recognition for specialized cosmetic and plastic surgery services. Brazil and Colombia, in particular, are internationally known for surgical expertise, aesthetic innovation, and competitive pricing structures, attracting patients from North America and Europe.Leading Companies of the Global Medical Tourism Market

Apollo Hospitals Enterprise Ltd. Fortis Healthcare Bumrungrad International Hospital Raffles Medical Group Clemenceau Medical Center KPJ Healthcare Berhad Bangkok Dusit Medical Services Acibadem Healthcare Group Apollo Hospitals and Bumrungrad International Hospital remain among the most recognized global brands in medical tourism due to international accreditations, comprehensive specialty coverage, and strong international patient programs.Strategic Intelligence & AI-Backed Insights

Pheonix Demand Forecast Engine: Anticipates strong double-digit expansion across high-demand segments such as cosmetic surgery, orthopedic interventions, fertility treatments, and specialized oncology services, supported by rising cross-border patient mobility. Global Patient Flow Analyzer: Identifies North America and the Middle East as key outbound patient hubs, driven by high domestic healthcare costs, long waiting periods, and growing preference for internationally accredited treatment centers. Innovation & Technology Tracker: Emphasizes increasing adoption of telemedicine consultations, AI-powered diagnostic tools, robotic-assisted surgical procedures, and integrated digital patient management platforms as major competitive differentiators. Porter???s Five Forces Assessment: Reflects moderate competitive intensity with strong regional treatment clusters; strategic positioning through quality accreditation, cost transparency, specialized expertise, and brand reputation remains critical for sustainable market advantage.Why the Medical Tourism Market is Critical

- Reduces global healthcare cost disparities

- Expands access to advanced treatments

- Supports healthcare infrastructure development in emerging markets

- Drives economic growth through healthcare-linked tourism

Final Takeaway of Global Medical Tourism Market

The Global Medical Tourism Market is evolving from a price-driven healthcare alternative into a structured, quality-centric, and globally integrated medical ecosystem. With a projected CAGR of ~11.5% during 2026???2033, market expansion is being driven by international hospital accreditation, advanced surgical capabilities, digital health integration, and rising demand for specialized cross-border treatments. As competition intensifies, differentiation will increasingly depend on treatment excellence, transparent pricing frameworks, seamless patient coordination, and end-to-end care packages that combine medical services with travel, accommodation, and rehabilitation support. The integration of teleconsultation, AI-assisted diagnostics, and post-treatment remote monitoring will further strengthen patient confidence and long-term engagement in the post-2025 landscape. Providers that prioritize trust-building, global referral networks, strategic hospital partnerships, and technology-enabled care continuity will secure sustainable competitive advantage in this rapidly transforming healthcare segment. At Pheonix Research, our advanced forecasting models deliver comprehensive revenue analysis, patient mobility insights, competitive benchmarking, and strategic intelligence ??? empowering stakeholders to capitalize on expanding global healthcare mobility trends with data-driven precision and sustainable growth strategies.???? Social Mentions & Publication Channels

??Explore deeper insights and follow our cross-platform updates on??LinkedIn??and??X??for continuous intelligence and market coverage.

LinkedIn : https://www.linkedin.com/feed/update/urn:li:activity:7433535557760147456

X : https://x.com/Pheonix_Insight/status/2027772298862989525?s=20

Table of Contents

1. Executive Summary

1.1 Market Snapshot (2026???2033)

1.2 Key Growth Highlights

1.3 Largest & Fastest Growing Regions

1.4 Dominant Treatment Segments

1.5 Key Trends & Future Outlook

2. Market Forecast Snapshot

2.1 2025 Market Size ??? USD 38.7 Billion

2.2 2033 Market Size ??? USD 92.4 Billion

2.3 CAGR (2026???2033) ??? ~11.5%

2.4 Largest Region ??? Asia-Pacific

2.5 Fastest Growing Region ??? Middle East

2.6 Top Segment ??? Cosmetic & Elective Procedures

2.7 Key Trend ??? Cross-Border Specialized Healthcare

2.8 Future Focus ??? Digital Health Integration

3. Global Medical Tourism Market Overview

3.1 Market Definition & Scope

3.2 Evolution of Cross-Border Healthcare

3.3 Cost Arbitrage & Competitive Pricing Models

3.4 International Accreditation & Quality Standards

3.5 Post-2025 Market Transformation

4. Market Dynamics

4.1 Market Drivers

4.1.1 Rising Healthcare Costs in Developed Economies

4.1.2 Long Waiting Times for Elective Procedures

4.1.3 Growth of Cosmetic & Wellness Tourism

4.1.4 Digital Health & Teleconsultation Adoption

4.1.5 Government-Supported Healthcare Tourism

4.2 Market Restraints

4.2.1 Regulatory & Visa Barriers

4.2.2 Post-Treatment Complications & Liability Risks

4.2.3 Insurance & Reimbursement Limitations

4.3 Market Opportunities

4.3.1 Integrated Healthcare Travel Packages

4.3.2 AI-Enabled Remote Patient Monitoring

4.3.3 Strategic Hospital & Hospitality Partnerships

5. Market Segmentation by Treatment Type

5.1 Cosmetic & Elective Procedures

5.1.1 Plastic & Reconstructive Surgery

5.1.1.1 Facial Aesthetic Surgery

5.1.1.1.1 Rhinoplasty

5.1.1.1.2 Facelift

5.1.1.1.3 Eyelid Surgery

5.1.1.2 Body Contouring Procedures

5.1.1.2.1 Liposuction

5.1.1.2.2 Tummy Tuck

5.1.1.2.3 Breast Augmentation

5.1.2 Non-Surgical Aesthetic Treatments

5.1.2.1 Botox & Fillers

5.1.2.2 Laser Treatments

5.1.2.3 Skin Rejuvenation

5.2 Cardiovascular Treatments

5.2.1 Bypass & Open-Heart Surgery

5.2.1.1 Coronary Artery Bypass

5.2.1.2 Valve Replacement

5.2.1.3 Minimally Invasive Cardiac Surgery

5.2.2 Interventional Cardiology

5.2.2.1 Angioplasty

5.2.2.2 Stent Placement

5.2.2.3 Pacemaker Implantation

5.3 Orthopedic Treatments

5.3.1 Joint Replacement Surgery

5.3.1.1 Knee Replacement

5.3.1.2 Hip Replacement

5.3.1.3 Shoulder Replacement

5.3.2 Spine Surgery

5.3.2.1 Disc Replacement

5.3.2.2 Spinal Fusion

5.3.2.3 Minimally Invasive Spine Surgery

5.4 Oncology Treatments

5.4.1 Surgical Oncology

5.4.1.1 Tumor Removal

5.4.1.2 Organ-Specific Cancer Surgery

5.4.2 Radiation Therapy

5.4.2.1 Proton Therapy

5.4.2.2 IMRT

5.4.3 Chemotherapy & Targeted Therapy

5.4.3.1 Immunotherapy

5.4.3.2 Precision Medicine

5.5 Fertility & Reproductive Treatments

5.5.1 In-Vitro Fertilization (IVF)

5.5.1.1 Egg Donation Programs

5.5.1.2 Surrogacy Services

5.5.1.3 Fertility Preservation

5.6 Dental Treatments

5.6.1 Cosmetic Dentistry

5.6.1.1 Veneers

5.6.1.2 Teeth Whitening

5.6.1.3 Smile Makeovers

5.6.2 Restorative Dentistry

5.6.2.1 Dental Implants

5.6.2.2 Crowns & Bridges

5.6.2.3 Root Canal Treatments

5.7 Wellness & Alternative Therapies

5.7.1 Traditional Medicine

5.7.1.1 Ayurveda

5.7.1.2 Traditional Chinese Medicine

5.7.2 Rehabilitation & Recovery Programs

5.7.2.1 Post-Surgery Rehab

5.7.2.2 Chronic Disease Management

6. Market Segmentation by Service Provider

6.1 Private Multi-Specialty Hospitals

6.1.1 Internationally Accredited Hospitals

6.1.1.1 JCI Accredited Facilities

6.1.1.2 NABH Accredited Hospitals

6.2 Specialty Clinics

6.2.1 Cosmetic Surgery Clinics

6.2.2 Fertility Clinics

6.2.3 Dental Specialty Centers

6.3 Medical Tourism Facilitators

6.3.1 Treatment Coordination Agencies

6.3.2 Travel & Accommodation Partners

6.3.3 Insurance & Financing Partners

7. Market Segmentation by Patient Origin

7.1 North America

7.1.1 United States

7.1.2 Canada

7.2 Europe

7.2.1 Western Europe

7.2.2 Eastern Europe

7.3 Middle East

7.3.1 GCC Countries

7.3.2 Non-GCC Nations

7.4 Asia-Pacific

7.4.1 Southeast Asia

7.4.2 South Asia

8. Market Segmentation by Destination Region

8.1 Asia-Pacific

8.2 Middle East

8.3 Europe

8.4 North America

8.5 South America

9. Regional Insights

9.1 Asia-Pacific ??? Largest Market

9.2 Middle East ??? Fastest Growing

9.3 Europe ??? Dental & Cosmetic Hub

9.4 North America ??? Outbound Source Market

9.5 South America ??? Aesthetic Surgery Destination

10. Competitive Landscape

10.1 Market Share Analysis

10.2 Strategic Partnerships & Global Networks

10.3 Accreditation & Brand Positioning

10.4 Pricing Transparency & Cost Models

10.5 Digital Platform Integration

11. Leading Companies

11.1 Apollo Hospitals Enterprise Ltd.

11.2 Fortis Healthcare

11.3 Bumrungrad International Hospital

11.4 Raffles Medical Group

11.5 Clemenceau Medical Center

11.6 KPJ Healthcare Berhad

11.7 Bangkok Dusit Medical Services

11.8 Acibadem Healthcare Group

12. Strategic Intelligence & AI-Backed Insights

12.1 Pheonix Demand Forecast Engine

12.2 Global Patient Flow Analyzer

12.3 Innovation & Technology Tracker

12.4 Porter???s Five Forces Analysis

13. Regulatory & Policy Landscape

13.1 Medical Visa Regulations

13.2 International Accreditation Standards

13.3 Cross-Border Insurance & Liability Framework

13.4 Ethical & Legal Considerations

14. Future Outlook (2026???2033)

14.1 Integrated Care Packages

14.2 Telemedicine & Remote Monitoring

14.3 AI-Driven Diagnostics & Surgical Robotics

14.4 Healthcare-Hospitality Convergence

15. Final Takeaway

15.1 Growth Outlook

15.2 Competitive Differentiation Strategies

15.3 Technology-Enabled Care Continuity

15.4 Investment & Partnership Roadmap

16. Appendix

17. About Pheonix Research

18. Disclaimer

Competitive Landscape

Global Medical Tourism Market Competitive Intensity & Market Structure Overview

The Global Medical Tourism Market operates within a highly dynamic and competitive ecosystem, characterized by the convergence of healthcare providers, travel facilitators, insurance entities, and digital health platforms. The market structure is semi-fragmented, with strong regional hubs competing globally to attract international patients through cost advantages, clinical excellence, and integrated service offerings.

Competitive intensity is driven by the need to balance affordability with high-quality medical care, international accreditation standards, and seamless patient experience. Hospitals and healthcare networks compete not only on treatment pricing but also on outcomes, technology adoption, physician expertise, and end-to-end service delivery including travel, accommodation, and post-treatment care.

Asia-Pacific leads the competitive landscape due to its cost-efficient treatment ecosystem and large network of internationally accredited hospitals, while the Middle East and Europe are strengthening their positions through premium healthcare infrastructure and specialized treatment offerings.

Global Medical Tourism Market Competitive Intensity & Market Structure Current Scenario

Leading Company Profiles

Apollo Hospitals Enterprise Ltd.: Leading Indian Healthcare Provider. Strong international patient services, multi-specialty expertise, and cost-effective treatment packages.

Fortis Healthcare: Multi-Specialty Hospital Network. Focused on advanced clinical care and global patient outreach programs.

Bumrungrad International Hospital: Thailand-Based Global Medical Tourism Leader. Renowned for high-quality care, international accreditations, and premium patient experience.

Raffles Medical Group: Singapore-Based Healthcare Provider. Known for integrated healthcare services and strong international patient management systems.

Clemenceau Medical Center: Middle East Premium Healthcare Provider. Focused on high-end medical tourism and specialized treatments.

KPJ Healthcare Berhad: Malaysia-Based Hospital Group. Strong regional presence with expanding international patient services.

Bangkok Dusit Medical Services: One of the Largest Private Hospital Networks in Thailand. Comprehensive specialty coverage and strong global patient inflow.

Acibadem Healthcare Group: Turkey-Based Healthcare Provider. Strong European and Middle Eastern patient base with advanced medical technologies.

Key Competitive Intensity & Market Structure Signals in Global Medical Tourism Market

A defining feature of the market is the emergence of regional healthcare clusters that specialize in specific treatments such as cardiac care, orthopedics, cosmetic surgery, and fertility services. These clusters create concentrated competition among hospitals within the same geography while strengthening global positioning.

Pricing transparency and package-based offerings are becoming critical competitive factors. Providers are increasingly offering bundled services that include treatment, travel, accommodation, and rehabilitation, enhancing value perception among international patients.

Digital transformation is another major competitive signal. Teleconsultation platforms, AI-driven diagnostics, and remote patient monitoring are improving pre- and post-treatment engagement, enabling providers to build long-term relationships with global patients.

Accreditation and regulatory compliance continue to serve as key differentiators. Hospitals with international certifications such as JCI and NABH gain higher patient trust and global visibility, intensifying competition among providers to maintain quality benchmarks.

Strategic Implications of Competitive Intensity & Market Structure in Global Medical Tourism Market

Healthcare providers are shifting from standalone treatment models to integrated care ecosystems. Strategic partnerships between hospitals, travel agencies, insurance companies, and hospitality providers are becoming essential to deliver seamless patient experiences.

Brand positioning and reputation management are increasingly critical, as patients rely heavily on reviews, success rates, and international accreditations when selecting treatment destinations. Investment in global marketing and digital presence is therefore a key strategic priority.

Technology integration is redefining competitive advantage. Hospitals that leverage telemedicine, AI-based diagnostics, robotic surgeries, and digital patient management systems are better positioned to attract international patients seeking advanced and reliable care.

Additionally, governments are playing an active role in shaping competitive dynamics through medical visas, policy support, and healthcare infrastructure investments, further intensifying competition among destination countries.

Global Medical Tourism Market Competitive Intensity & Market Structure Forward Outlook

The Global Medical Tourism Market is expected to become increasingly structured, with stronger consolidation among leading hospital networks and expansion of organized medical tourism facilitators. Competitive intensity will continue to rise as new destinations enter the market with aggressive pricing and infrastructure investments.

Integrated healthcare travel packages will become the standard, combining treatment, wellness, rehabilitation, and digital follow-up care into a single offering. This evolution will shift competition toward holistic patient experience rather than standalone medical procedures.

Emerging technologies such as AI diagnostics, robotic surgery, and digital health platforms will further differentiate providers, while data-driven patient engagement strategies will enhance retention and long-term trust.

In the long term, the market will be defined by three core competitive pillars: clinical excellence, cost transparency, and digital care integration. Organizations that successfully align with these factors while maintaining strong global partnerships and accreditation standards will lead the Global Medical Tourism Market through 2033.

Value Chain

Global Medical Tourism Market Value Chain & Supply Chain Evolution Overview

The Global Medical Tourism Market value chain is transforming from a fragmented cross-border treatment model into a highly integrated global healthcare delivery ecosystem combining clinical excellence, travel logistics, digital health platforms, and patient experience management. Unlike traditional healthcare systems limited by geography, medical tourism enables patients to access cost-effective, high-quality, and specialized treatments across international borders through coordinated healthcare and travel networks.

The value chain spans international patient acquisition, pre-treatment consultation, hospital selection, medical procedure execution, travel coordination, accommodation services, insurance processing, post-treatment care, and long-term follow-up through digital health platforms. Increasingly, the ecosystem is evolving toward end-to-end integrated care packages that combine healthcare delivery with hospitality and wellness services.

Upstream supply chain dynamics are shaped by internationally accredited hospitals, specialist surgeons, diagnostic centers, telemedicine platforms, insurance providers, and medical tourism facilitators. Digital infrastructure???including AI-based consultation tools, patient data management systems, and remote monitoring technologies???is becoming critical in improving transparency, trust, and patient outcomes.

Platform development strategies increasingly focus on seamless patient journeys, multilingual support, treatment cost transparency, digital documentation, and integrated care coordination across borders. Medical tourism facilitators are evolving into full-service healthcare travel orchestrators, combining hospital networks, travel agencies, and digital platforms.

Distribution channels are expanding through online medical tourism platforms, hospital international patient departments, insurance partnerships, government-sponsored programs, and global referral networks. Direct-to-patient digital engagement is becoming a dominant acquisition strategy.

Supply chain challenges include regulatory complexity, visa constraints, treatment standardization, post-operative risk management, insurance limitations, geopolitical uncertainties, and maintaining continuity of care across borders.

Global Medical Tourism Market Value Chain & Supply Chain Evolution Current Scenario

The current market is shaped by rising healthcare costs, long waiting periods, increasing demand for specialized procedures, and growing adoption of digital health solutions.

Upstream, hospitals and healthcare providers are investing in international accreditations, advanced surgical technologies, robotic-assisted procedures, and specialized treatment centers to attract global patients.

Patient acquisition ecosystems increasingly rely on digital platforms offering teleconsultations, treatment comparisons, cost transparency, and physician selection.

Medical tourism facilitators play a critical role in coordinating travel logistics, treatment scheduling, documentation, and on-ground patient support services.

Technology integration includes telemedicine consultations, AI-assisted diagnostics, electronic health records (EHR), and remote patient monitoring for post-treatment continuity.

Competitive differentiation increasingly depends on clinical quality, patient experience, cost efficiency, international accreditation, and seamless care coordination.

Key Value Chain & Supply Chain Evolution Signals in Global Medical Tourism Market

Several structural trends are reshaping the medical tourism ecosystem globally.

First, integrated healthcare travel packages are becoming the dominant model, combining treatment, accommodation, rehabilitation, and tourism experiences.

Second, telemedicine and virtual consultation platforms are reducing pre-treatment uncertainty and improving international patient engagement.

Third, accreditation and quality assurance are becoming critical trust factors influencing patient decision-making.

Fourth, specialized treatment hubs are emerging across regions, focusing on cardiology, orthopedics, fertility, oncology, and cosmetic procedures.

Fifth, insurance integration and cross-border healthcare financing are gradually improving affordability and accessibility.

Sixth, digital patient management systems are enhancing continuity of care through post-treatment follow-ups and remote monitoring.

Strategic Implications of Value Chain & Supply Chain Evolution in Global Medical Tourism Market

Leading providers such as Apollo Hospitals, Bumrungrad International Hospital, Fortis Healthcare, and Raffles Medical Group are strengthening market positions through international accreditation, specialized treatment offerings, and integrated patient services.

Long-term competitive advantage increasingly depends on trust, clinical outcomes, brand reputation, and seamless patient experience rather than cost alone.

Hospitals that offer comprehensive international patient programs, multilingual support, and digital care coordination are better positioned to capture global demand.

Strategic partnerships with travel operators, insurance providers, and digital health platforms are becoming essential for ecosystem expansion.

Supply chain resilience increasingly depends on regulatory compliance, global healthcare standards alignment, and the ability to manage cross-border patient journeys efficiently.

As competition intensifies, providers must evolve from standalone healthcare institutions into integrated global healthcare service ecosystems.

Global Medical Tourism Market Value Chain & Supply Chain Evolution Forward Outlook

Between 2026 and 2033, the medical tourism value chain is expected to become more digitally integrated, patient-centric, and globally standardized.

Healthcare providers will increasingly adopt AI-driven diagnostics, telehealth platforms, and personalized treatment planning to enhance patient engagement and outcomes.

Cross-border healthcare ecosystems will expand through partnerships between hospitals, insurers, governments, and travel platforms.

Integrated care models combining treatment, recovery, wellness, and long-term monitoring will become standard offerings.

Digital health records, remote monitoring systems, and virtual follow-ups will strengthen continuity of care across geographies.

Ultimately, the market will evolve into a global healthcare access network enabling seamless, high-quality, and cost-efficient treatment mobility.

Market-Specific Value Chain

- Healthcare Infrastructure & Clinical Expertise: Hospitals, surgeons, specialists, diagnostic centers, accredited healthcare institutions

- Digital Health & Consultation Platforms: Telemedicine, AI diagnostics, EHR systems, patient engagement platforms

- Facilitation & Care Coordination: Medical tourism agencies, travel coordinators, documentation, visa assistance

- Treatment Delivery & Hospital Services: Surgical procedures, inpatient care, rehabilitation, specialized treatments

- Travel, Hospitality & Patient Experience: Accommodation, transportation, concierge services, wellness packages

- Post-Treatment Care & Continuity: Remote monitoring, tele-follow-ups, rehabilitation programs, long-term care management

Company-to-Stage Mapping

- Healthcare Infrastructure & Clinical Expertise: Apollo Hospitals, Fortis Healthcare, Bumrungrad International Hospital, Acibadem Healthcare

- Digital Health & Consultation Platforms: Telemedicine providers, hospital digital platforms, AI diagnostic solution providers

- Facilitation & Care Coordination: Medical tourism facilitators, travel agencies, global healthcare coordinators

- Treatment Delivery & Hospital Services: Multi-specialty hospitals, specialty clinics, accredited healthcare providers

- Travel, Hospitality & Patient Experience: Hospitality partners, medical travel coordinators, wellness resorts

- Post-Treatment Care & Continuity: Telehealth platforms, rehabilitation centers, remote monitoring providers

Investment Activity

Global Medical Tourism Market Investment & Funding Dynamics Overview

Investment and funding dynamics in the Global Medical Tourism Market are expanding rapidly as cross-border healthcare demand, cost arbitrage opportunities, and global healthcare accessibility continue to reshape the industry. Between 2026 and 2033, capital allocation is expected to increase significantly across international hospital infrastructure, specialty treatment centers, digital health platforms, and integrated medical travel ecosystems.

The market is evolving from fragmented medical travel services into a structured, high-value healthcare delivery model, attracting private equity firms, healthcare conglomerates, sovereign wealth funds, and strategic investors. Leading hospital groups such as Apollo Hospitals, Bumrungrad International Hospital, Fortis Healthcare, and Acibadem are actively investing in international patient departments, advanced surgical capabilities, and global referral networks.

A key structural shift influencing investment flows is the transition toward integrated care packages, combining treatment, diagnostics, travel, accommodation, rehabilitation, and telemedicine follow-ups. This is directing funding toward end-to-end patient journey platforms, digital coordination tools, and internationally accredited healthcare ecosystems.

Global Medical Tourism Market Investment & Funding Dynamics Current Scenario

Currently, investment activity is supported by rising healthcare costs in developed economies, long waiting times for elective procedures, increasing international accreditation, and rapid adoption of teleconsultation platforms. Strong demand for cosmetic, dental, orthopedic, and fertility treatments is further driving capital inflows.

- Asia-Pacific: Dominates investment activity due to cost competitiveness, large patient inflows, strong private healthcare infrastructure, and government-backed medical tourism initiatives.

- Middle East: Fastest-growing investment region driven by luxury healthcare infrastructure, premium service offerings, and strategic positioning as global healthcare hubs.

- Europe: Strong investment in dental, cosmetic, and orthopedic treatment clusters supported by high clinical standards and regional patient mobility.

- North America: Major outbound market with increasing investments in cross-border partnerships and patient referral networks.

Key Investment & Funding Dynamics Signals in Global Medical Tourism Market

- Rising demand for cost-effective and high-quality treatments is driving investments in emerging healthcare destinations.

- Expansion of internationally accredited hospitals is attracting global patient trust and institutional funding.

- Digital health platforms, including teleconsultation and remote monitoring, are becoming major investment areas.

- Growth of cosmetic, fertility, and elective procedures is generating high-margin investment opportunities.

- Medical tourism facilitators and integrated service providers are receiving funding to streamline patient journeys.

Strategic Implications of Investment & Funding Dynamics in Global Medical Tourism Market

- Investment success increasingly depends on international accreditation, clinical quality, and brand reputation.

- End-to-end service integration, including travel, treatment, and post-care, is becoming a key competitive differentiator.

- Digital transformation through telemedicine and AI-enabled diagnostics is critical for patient acquisition and retention.

- Regional diversification strategies are essential to capture inbound and outbound patient flows.

- Partnerships between hospitals, travel agencies, insurers, and digital platforms are shaping the competitive landscape.

Global Medical Tourism Market Investment & Funding Dynamics Forward Outlook

Looking ahead, the Global Medical Tourism Market is expected to attract sustained and high-growth investment as global patient mobility increases and healthcare systems become more interconnected.

Future capital allocation will focus on smart hospitals, robotic surgery capabilities, AI-assisted diagnostics, telehealth ecosystems, and integrated healthcare travel platforms that enhance patient experience and clinical outcomes.

- Asia-Pacific: Will continue leading investment due to cost advantage, large-scale infrastructure, and strong inbound patient demand.

- Middle East: Will emerge as a premium global healthcare destination with high-end infrastructure and specialized treatment hubs.

- Europe: Will strengthen its position in specialized and short-distance medical travel within the region.

Digital health integration, cross-border insurance frameworks, and AI-powered patient management systems will increasingly define future funding strategies.

Overall, the market is positioned for strong double-digit growth through 2033, supported by rising global healthcare demand, affordability gaps, and increasing trust in international treatment standards. Organizations that invest in quality care, seamless patient experience, and technology-enabled healthcare delivery will lead the next phase of global medical tourism expansion.

Technology & Innovation

Global Medical Tourism Market Technology & Innovation Landscape Overview

The technology and innovation landscape within the Global Medical Tourism Market is rapidly evolving toward a digitally connected, patient-centric, and globally integrated healthcare ecosystem. Medical tourism is no longer limited to cost-driven cross-border treatment; it is increasingly shaped by advanced digital health platforms, AI-driven clinical systems, and seamless care coordination technologies that enhance patient experience, clinical outcomes, and operational efficiency.

Innovation intensity in the medical tourism sector is accelerating, driven by advancements in telemedicine, artificial intelligence, robotic-assisted surgery, digital health records, and healthcare data interoperability. Leading hospitals, healthcare facilitators, and digital health startups are investing in integrated care platforms that combine medical expertise with travel, hospitality, and post-treatment support services.

A major transformation is the convergence of telehealth, AI diagnostics, and remote monitoring technologies, enabling patients to access global healthcare services without geographical constraints. This shift is positioning medical tourism as a structured, technology-enabled global healthcare delivery model rather than a fragmented international service.

Simultaneously, advancements in cloud computing, cybersecurity, and blockchain-based health data systems are improving cross-border data exchange, ensuring patient privacy, and enabling seamless coordination between international healthcare providers.

Global Medical Tourism Market Technology & Innovation Landscape Current Scenario

Currently, the medical tourism industry is focused on enhancing patient accessibility, improving treatment transparency, and ensuring continuity of care across borders. Technology adoption is centered on reducing patient uncertainty while optimizing treatment outcomes and operational efficiency.

Telemedicine and virtual consultation platforms have become foundational, allowing patients to interact with international doctors for diagnosis, treatment planning, and follow-up care. These platforms significantly reduce the need for multiple physical visits and enhance pre- and post-treatment engagement.

AI-powered diagnostics and decision-support systems are increasingly used to improve clinical accuracy, accelerate diagnosis, and personalize treatment plans. These technologies are particularly impactful in oncology, cardiology, and complex surgical procedures.

Robotic-assisted surgery and minimally invasive techniques are gaining widespread adoption in leading medical tourism destinations. These innovations enable high-precision procedures, reduced recovery time, and improved patient outcomes, making cross-border treatment more attractive.

Digital patient management systems are streamlining the entire medical journey, from appointment scheduling and documentation to billing, travel coordination, and treatment tracking. Patients benefit from centralized platforms that provide real-time updates and seamless communication with healthcare providers.

Remote patient monitoring through wearable devices and connected health technologies is enabling continuous care beyond hospital settings. Patients can return home while remaining under the supervision of their international healthcare providers.

Additionally, integration of healthcare with travel technology platforms is improving the overall patient experience by offering bundled medical travel packages, including treatment, accommodation, logistics, and rehabilitation services.

Key Technology & Innovation Trends in Global Medical Tourism Market

- Telemedicine & Virtual Consultations: Pre- and post-treatment care through digital platforms.

- AI-Powered Diagnostics: Enhanced clinical decision-making and personalized treatment planning.

- Robotic-Assisted Surgery: High-precision procedures with faster recovery times.

- Digital Patient Management Platforms: End-to-end coordination of medical travel journeys.

- Blockchain for Health Records: Secure and interoperable cross-border data exchange.

- Remote Patient Monitoring: Wearables and connected devices for post-treatment care.

- Integrated Medical Travel Platforms: Bundled healthcare, travel, and hospitality services.

- Precision & Personalized Medicine: Genomics-based and patient-specific treatment approaches.

Strategic Implications of Technology & Innovation

The integration of advanced technologies is transforming medical tourism into a highly coordinated and quality-driven global healthcare model. Providers that invest in digital infrastructure, AI-enabled clinical systems, and patient experience platforms are gaining competitive advantage.

Healthcare providers can leverage these innovations to expand international patient reach, improve treatment outcomes, and build long-term patient relationships through continuous care models.

However, technological advancement also introduces challenges, including data privacy regulations, cross-border compliance requirements, and the need for significant capital investment in digital infrastructure.

Governments and healthcare organizations are increasingly viewing medical tourism as a strategic economic sector, investing in smart hospitals, digital health ecosystems, and international accreditation standards.

Trust, transparency, and data security are becoming critical success factors, particularly as patients rely more on digital platforms for healthcare decision-making and coordination.

Global Medical Tourism Market Technology & Innovation Forward Outlook

Looking ahead, the Global Medical Tourism Market is expected to evolve into a fully integrated digital healthcare ecosystem where physical treatment is complemented by continuous virtual care and intelligent patient management systems.

AI, predictive analytics, and digital twins in healthcare may enable highly personalized treatment simulations and outcome predictions, further enhancing patient confidence in cross-border care.

Telehealth and remote monitoring will continue to expand, enabling long-term global care relationships between patients and providers beyond the initial treatment phase.

The integration of smart hospitals, robotics, and advanced diagnostics will further elevate treatment quality, positioning leading medical tourism destinations as global centers of excellence.

In conclusion, the Global Medical Tourism Market is transitioning toward a technology-driven, patient-centric, and globally connected healthcare ecosystem. Organizations that lead in digital health integration, AI-enabled care, secure data management, and seamless patient experience will define the future of medical tourism through 2033.

Market Risk

Global Medical Tourism Market Risk Factors & Disruption Threats Overview

The Global Medical Tourism Market operates within a highly interconnected healthcare and travel ecosystem, where affordability, quality of care, and international accessibility drive patient mobility. Despite strong growth momentum, the market carries a moderate-to-high strategic risk profile due to regulatory variability, geopolitical uncertainties, patient safety concerns, and dependency on cross-border logistics and trust frameworks.

A major structural risk is regulatory inconsistency across countries. Differences in medical standards, accreditation systems, malpractice laws, and patient rights frameworks create complexity and potential legal exposure for both providers and patients, particularly in cases of post-treatment complications.

Another critical disruption factor is geopolitical instability and travel dependency. Medical tourism is highly sensitive to visa policies, international relations, pandemics, and travel restrictions, all of which can abruptly impact patient flows and revenue stability.

Quality perception and trust deficits also pose challenges. While many hospitals are internationally accredited, variability in clinical outcomes, hygiene standards, and follow-up care can influence global patient confidence and brand reputation.

Additionally, the increasing role of digital platforms introduces data privacy and cybersecurity risks, as cross-border patient data sharing, teleconsultations, and digital health records become integral to the medical tourism journey.

Global Medical Tourism Market Risk Factors & Disruption Threats Current Scenario

The current market landscape reflects strong demand from cost-sensitive patients, particularly from North America and Europe, seeking affordable and timely treatments. However, growth is increasingly shaped by operational and regulatory complexities.

Leading destinations such as India, Thailand, and Turkey continue to attract high patient volumes, but competition among these hubs is intensifying, leading to pricing pressure and increased marketing expenditure.

Post-pandemic recovery has restored international travel, yet healthcare providers remain cautious due to potential disruptions from future global health crises or sudden border restrictions.

Insurance integration remains limited, with many treatments still requiring out-of-pocket payments, creating affordability and reimbursement challenges for patients.

Furthermore, continuity of care remains a key concern, as patients often face difficulties in post-treatment monitoring and follow-up once they return to their home countries.

Key Risk Factors & Disruption Threats Signals in Global Medical Tourism Market

A major disruption signal is the increasing shift toward domestic healthcare improvements in developed countries, which may reduce outbound patient flows over time as waiting periods decrease and cost structures evolve.

Digital health platforms and telemedicine are reshaping patient decision-making, enabling remote consultations but also increasing competition by allowing patients to compare global providers more easily.

Rising scrutiny around medical malpractice, treatment transparency, and ethical practices is influencing patient choice and regulatory oversight.

Currency fluctuations and economic instability in destination countries can impact pricing competitiveness and patient affordability.

Additionally, environmental and sustainability concerns related to long-distance medical travel are emerging as potential long-term disruption factors.

Strategic Implications of Risk Factors & Disruption Threats in Global Medical Tourism Market

Healthcare providers must prioritize international accreditation, standardized treatment protocols, and transparent pricing structures to build long-term patient trust and credibility.

Developing integrated care models that include pre-treatment consultation, travel coordination, in-hospital care, and post-treatment follow-up is essential to reduce patient risk and improve outcomes.

Strategic partnerships with insurance providers, governments, and global healthcare networks can enhance patient accessibility and financial coverage.

Investment in digital health infrastructure, including secure telemedicine platforms and patient data protection systems, will be critical for maintaining competitiveness and compliance.

Diversification of source markets and reduced dependence on specific geographies can help mitigate geopolitical and travel-related risks.

Global Medical Tourism Market Risk Factors & Disruption Threats Forward Outlook

Looking ahead to 2026???2033, the Global Medical Tourism Market is expected to evolve into a more regulated, technology-enabled, and patient-centric ecosystem. However, risk factors related to global mobility, regulatory alignment, and trust will remain central to market dynamics.

Integration of telemedicine, AI diagnostics, and remote monitoring will improve continuity of care but also increase the need for robust cybersecurity and data governance frameworks.

Healthcare providers are likely to expand bundled service offerings combining treatment, travel, rehabilitation, and digital follow-up, creating more resilient and differentiated value propositions.

Countries that invest in international accreditation, infrastructure quality, and seamless patient experience will strengthen their competitive positioning.

Overall, while the market presents strong growth potential, long-term success will depend on risk mitigation strategies, global standardization efforts, and the ability to build sustained patient trust across borders.

Regulatory Landscape

Global Medical Tourism Market Regulatory & Policy Environment Overview

The regulatory and policy environment for the Global Medical Tourism Market is becoming increasingly structured as governments, healthcare regulators, and international accreditation bodies work to ensure patient safety, treatment quality, cross-border compliance, and ethical medical practices. As medical tourism evolves into a global healthcare delivery model, regulations are focusing on standardization of care, transparency in pricing, malpractice accountability, and continuity of care across borders.

International accreditation frameworks such as Joint Commission International (JCI), National Accreditation Board for Hospitals & Healthcare Providers (NABH), and other regional certification bodies play a central role in establishing trust and quality benchmarks for healthcare providers catering to international patients. These standards cover clinical quality, patient safety, infection control, and operational excellence.

Governments are also implementing policies to regulate medical visas, cross-border insurance portability, telemedicine practices, and patient data protection. Legal clarity around malpractice liability, dispute resolution, and patient rights is becoming increasingly important as cross-border treatment volumes grow.

Regional regulatory approaches vary significantly. Asia-Pacific emphasizes growth and facilitation through medical tourism promotion policies, Europe focuses on patient rights and healthcare quality directives, while the Middle East is rapidly building regulatory frameworks aligned with international standards to position itself as a premium healthcare destination.

Global Medical Tourism Market Regulatory & Policy Environment Current Scenario

The current regulatory landscape is a mix of well-established accreditation systems and evolving cross-border healthcare policies. Most countries regulate medical tourism through existing healthcare laws, immigration policies, and private healthcare guidelines rather than dedicated medical tourism legislation.

In Asia-Pacific, leading destinations such as India, Thailand, Malaysia, and Singapore have implemented structured medical tourism policies, including fast-track medical visas, international patient departments, and government-backed promotion councils. Accreditation and pricing transparency are increasingly emphasized to maintain global competitiveness.

The Middle East is emerging with strong regulatory backing, particularly in the UAE, Saudi Arabia, and Turkey, where governments are investing in world-class healthcare infrastructure and implementing strict licensing, quality control, and international partnership frameworks.

Europe maintains strict healthcare regulations under EU directives, ensuring patient safety, cross-border healthcare rights, and data privacy compliance (GDPR). Countries such as Turkey and Hungary are aligning with European standards to attract international patients while maintaining cost competitiveness.

North America, while primarily an outbound market, enforces strict regulations on insurance, telehealth, and patient data, influencing how international providers coordinate care with U.S. and Canadian patients.

Key Regulatory & Policy Environment Signals in Global Medical Tourism Market

- International Accreditation Standards (JCI, NABH): Critical for ensuring treatment quality, safety, and global patient trust.

- Medical Visa & Cross-Border Travel Policies: Governments are streamlining visa processes to attract international patients.

- Patient Rights & Legal Protection Frameworks: Increasing focus on malpractice laws, dispute resolution, and treatment transparency.

- Healthcare Pricing Transparency Regulations: Policies promoting clear cost structures to enhance patient confidence.

- Data Privacy & Telemedicine Compliance: Regulations such as GDPR and digital health laws govern cross-border patient data exchange.

- Insurance Portability & Reimbursement Policies: Expanding frameworks to support international treatment coverage.

Strategic Implications of Regulatory & Policy Environment in Global Medical Tourism Market

Regulatory compliance is becoming a key competitive differentiator in the medical tourism ecosystem. Hospitals and healthcare providers with internationally recognized accreditations, transparent pricing models, and strong legal compliance frameworks are more likely to attract global patients.

Providers must invest in international patient management systems, legal compliance teams, multilingual communication capabilities, and digital health platforms to meet evolving regulatory expectations. This increases operational complexity but enhances long-term credibility and scalability.

Telemedicine integration introduces additional regulatory layers, requiring compliance with cross-border licensing, data protection laws, and remote consultation guidelines. Providers that effectively manage digital compliance will gain a significant advantage.

Insurance partnerships and global referral networks are also influenced by regulatory alignment. Hospitals that meet international insurance and compliance standards can access a broader patient base and institutional partnerships.

Smaller clinics and unaccredited providers may face increasing barriers as regulations tighten, shifting market share toward organized, accredited healthcare institutions.

Global Medical Tourism Market Regulatory & Policy Environment Forward Outlook

Between 2026 and 2033, the regulatory environment for medical tourism is expected to become more harmonized and stringent, particularly around patient safety, digital health integration, and cross-border legal accountability.

Asia-Pacific will continue strengthening accreditation frameworks and regulatory oversight while maintaining cost competitiveness. The Middle East is expected to accelerate policy development to position itself as a global premium healthcare hub with strong governance standards.

Europe will likely expand cross-border healthcare directives and patient protection laws, while North America may see increased regulation of outbound care coordination, telehealth integration, and insurance coverage for international treatments.

Emerging trends such as AI-assisted diagnostics, remote patient monitoring, and integrated care packages will require new regulatory frameworks addressing data security, treatment liability, and digital healthcare delivery standards.

Overall, the regulatory and policy environment will play a critical role in shaping trust, safety, and scalability in the Global Medical Tourism Market. Stakeholders that proactively align with international accreditation, legal frameworks, and digital compliance standards will be best positioned to capitalize on the growing demand for cross-border healthcare services through 2033.