Asia-Pacific Medical Aesthetic Market Report, Size and Forecast 2026-2033

Asia-Pacific Medical Aesthetic Market Report Size and Forecast 2026???2033

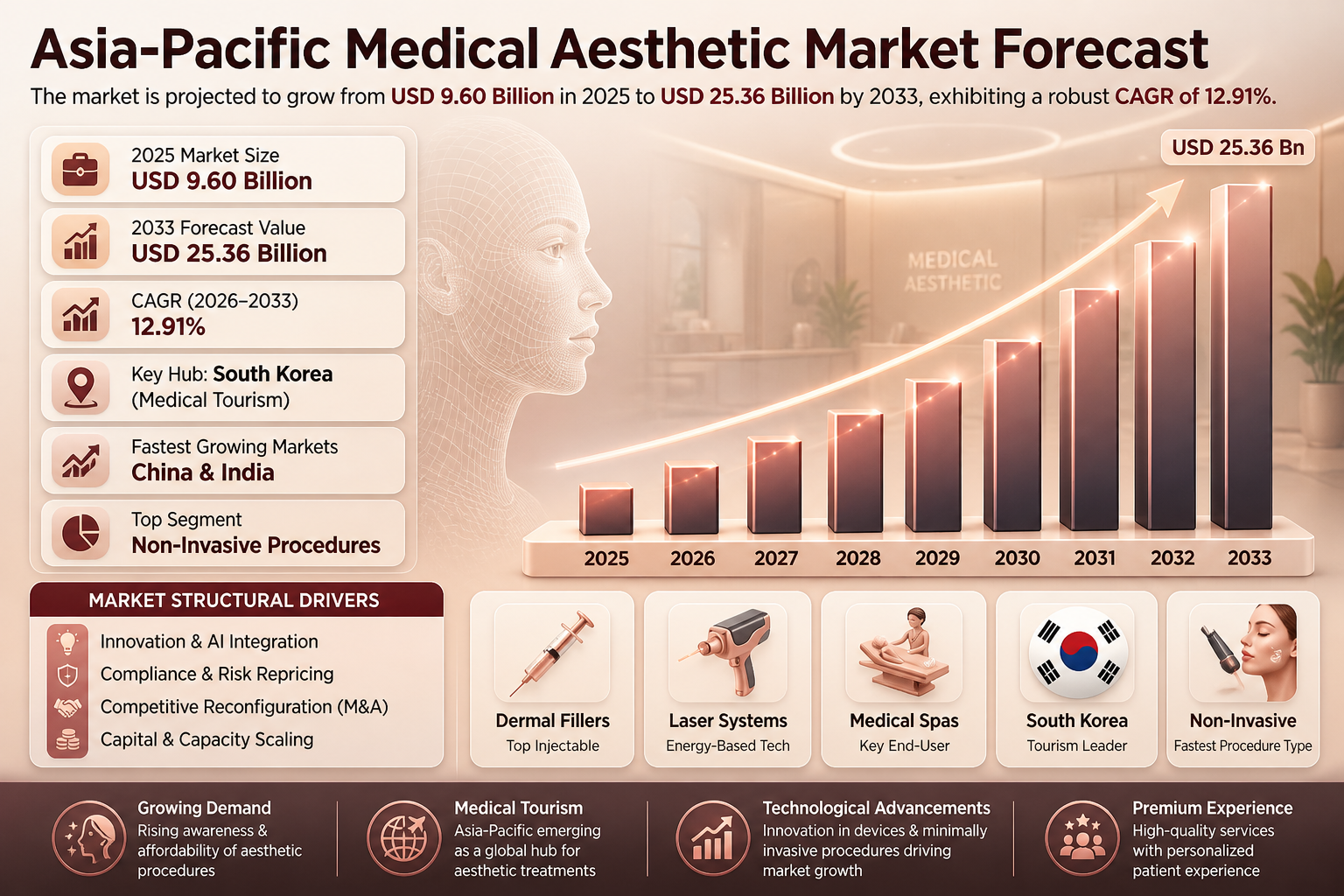

Market Forecast Snapshot (2025???2033)

| Metric | Value |

|---|---|

| Market Size (2025) | USD 9.60 Billion |

| Market Size (2033) | USD 25.36 Billion |

| CAGR (2026???2033) | ~12.91% |

| Largest Region | China |

| Fastest Growing Region | India & Southeast Asia |

| Leading Segment | Non-invasive Procedures |

| Key Trend | Minimally invasive & AI-driven aesthetic treatments |

Market Size & Forecast

The Asia-Pacific Medical Aesthetic Market is projected to grow from USD 9.60 billion in 2025 to USD 25.36 billion by 2033, registering a CAGR of 12.91% during the forecast period. This strong growth is driven by rising disposable incomes, increasing cultural acceptance of aesthetic procedures, and rapid advancements in minimally invasive technologies. The expansion of medical tourism hubs such as South Korea, Thailand, and Australia is further accelerating regional demand.Market Overview

The Asia-Pacific Medical Aesthetic Market is characterized by high growth momentum, fragmented competition, and strong consumer demand across diverse demographics. The market features key players such as AbbVie Inc., Lumenis, and Merz Aesthetics, alongside regional manufacturers and emerging startups. Technological innovation???particularly in laser systems, radiofrequency devices, and AI-based treatment planning???is significantly expanding treatment capabilities. At the same time, regulatory scrutiny across countries like Japan, South Korea, and Australia ensures safety but also raises entry barriers.Key Drivers of Market Growth

- Increasing demand for non-invasive and minimally invasive procedures

- Rising disposable income and expanding middle-class population

- Growth of medical tourism across South Korea, Thailand, and Australia

- Rapid technological advancements in laser, RF, and AI-driven systems

- Increasing awareness and acceptance of aesthetic treatments among younger consumers

Market Segmentation

By End User

- Hospitals

- Medical Spas

- Dermatology Clinics

By Application

- Skin Treatments (Largest Segment)

- Body Aesthetic Treatments

- Facial Aesthetic Treatments

By Product Type

- Energy-Based Devices (Laser, RF, Ultrasound, Cryolipolysis)

- Aesthetic Devices for Skin Resurfacing and Rejuvenation

By Procedure Type

- Non-Invasive Procedures (Fastest Growing)

- Minimally Invasive Procedures

By Injectable Products

- Dermal Fillers

- Botulinum Toxin

Regional Insights

- China ??? Largest market driven by healthcare investments and rising urban demand

- South Korea ??? Global hub for aesthetic procedures and medical tourism

- India ??? Fastest growth due to rising income and awareness

- Southeast Asia ??? Expanding demand supported by tourism and affordability

- Australia & New Zealand ??? Mature markets with strong regulatory frameworks

Competitive Landscape

- AbbVie Inc.

- Lumenis

- Merz Aesthetics

- Cynosure

- Beijing Toplaser Technology Co., Ltd.

Strategic Insights & Trends

- Increasing adoption of preventive aesthetics among younger demographics

- Expansion of AI-driven treatment planning and personalized procedures

- Rising popularity of non-surgical body contouring treatments

- Growth in injectable aesthetics including fillers and botulinum toxin

- Increasing consolidation through mergers and acquisitions

Why This Market Matters

- Reflects growing consumer shift toward appearance and wellness

- Enables safer, faster, and minimally invasive treatments

- Supports growth of medical tourism economies

- Expands access to advanced aesthetic technologies in emerging markets

- Drives innovation in personalized and preventive healthcare

Final Market Perspective

The Asia-Pacific Medical Aesthetic Market is entering a high-growth phase, driven by technological innovation, rising consumer awareness, and expanding healthcare infrastructure. The transition toward minimally invasive, AI-enhanced, and personalized aesthetic treatments is reshaping the industry. Companies that strategically invest in innovation, regulatory compliance, and regional expansion will be best positioned to capture long-term growth opportunities in this rapidly evolving market.Table of Contents

Table of Contents

- 1. Executive Summary

- 1.1 Market Forecast Snapshot (2026-2033)

- 1.2 Global Market Size & CAGR Analysis

- 1.3 Largest & Fastest-Growing Segments

- 1.4 Region-Level Leadership & Growth Trends

- 1.5 Key Market Drivers

- 1.6 Competitive Landscape Overview

- 1.7 Strategic Outlook Through 2033

- 2. Introduction & Market Overview

- 2.1 Definition of the Asia Pacific Medical Aesthetic Market

- 2.2 Scope of the Study

- 2.3 Industry Evolution & Market Development

- 2.4 Supply Chain & Distribution Infrastructure

- 2.5 Impact of Consumer Trends

- 2.6 Sustainability & Regulatory Landscape

- 2.7 Technology & Innovation Landscape

- 3. Research Methodology

- 3.1 Primary Research

- 3.2 Secondary Research

- 3.3 Market Size Estimation Model

- 3.4 Forecast Assumptions (2026-2033)

- 3.5 Data Validation & Triangulation

- 4. Market Dynamics

- 4.1 Drivers

- 4.1.1 Increasing Demand Drivers

- 4.1.2 Industry Innovation Drivers

- 4.1.3 Market Expansion Factors

- 4.1.4 Regulatory or Policy Support

- 4.1.5 Technology Adoption Drivers

- 4.2 Restraints

- 4.2.1 Cost Constraints

- 4.2.2 Infrastructure Limitations

- 4.2.3 Regulatory Challenges

- 4.2.4 Market Awareness Barriers

- 4.3 Opportunities

- 4.3.1 Emerging Market Opportunities

- 4.3.2 Product Innovation Opportunities

- 4.3.3 Technology Expansion Opportunities

- 4.3.4 Supply Chain Improvements

- 4.4 Challenges

- 4.4.1 Supply Chain Complexity

- 4.4.2 Quality Control & Compliance

- 4.4.3 Regional Market Fragmentation

- 4.4.4 Competitive Pressure

- 4.1 Drivers

- 5. Asia Pacific Medical Aesthetic Market Analysis (USD Billion), 2026-2033

- 5.1 Market Size Overview

- 5.2 CAGR Analysis

- 5.3 Regional Revenue Distribution

- 5.4 Segment Revenue Analysis

- 5.5 Distribution Channel Analysis

- 5.6 Consumer Impact Analysis

- 6. Market Segmentation (USD Billion), 2026-2033

- 6.1 By End User

- 6.1.1 Hospitals

- 6.1.1.1 Plastic Surgery Departments

- 6.1.1.1.1 Cosmetic Surgery Units

- 6.1.1.1.1.1 Facial Cosmetic Surgery Centers

- 6.1.1.1.1.2 Body Contouring Surgery Centers

- 6.1.1.1.1 Cosmetic Surgery Units

- 6.1.1.1 Plastic Surgery Departments

- 6.1.2 Medical Spas

- 6.1.2.1 Aesthetic Treatment Centers

- 6.1.2.1.1 Non-Surgical Cosmetic Clinics

- 6.1.2.1.1.1 Skin Treatment Clinics

- 6.1.2.1.1.2 Laser Aesthetic Clinics

- 6.1.2.1.1 Non-Surgical Cosmetic Clinics

- 6.1.2.1 Aesthetic Treatment Centers

- 6.1.3 Dermatology Clinics

- 6.1.3.1 Cosmetic Dermatology Centers

- 6.1.3.1.1 Anti-Aging Treatment Clinics

- 6.1.3.1.1.1 Laser Treatment Clinics

- 6.1.3.1.1.2 Skin Rejuvenation Centers

- 6.1.3.1.1 Anti-Aging Treatment Clinics

- 6.1.3.1 Cosmetic Dermatology Centers

- 6.2 By Application

- 6.2.1 Skin Treatments

- 6.2.1.1 Dermatological Aesthetic Treatments

- 6.2.1.1.1 Pigmentation Treatment

- 6.2.1.1.1.1 Hyperpigmentation Reduction

- 6.2.1.1.1.2 Melasma Treatment

- 6.2.1.1.1 Pigmentation Treatment

- 6.2.1.1 Dermatological Aesthetic Treatments

- 6.2.2 Body Aesthetic Treatments

- 6.2.2.1 Body Contouring

- 6.2.2.1.1 Non-Surgical Fat Reduction

- 6.2.2.1.1.1 Abdominal Fat Reduction

- 6.2.2.1.1.2 Thigh Contouring Treatments

- 6.2.2.1.1 Non-Surgical Fat Reduction

- 6.2.2.1 Body Contouring

- 6.2.3 Facial Aesthetic Treatments

- 6.2.3.1 Facial Rejuvenation

- 6.2.3.1.1 Anti-Aging Treatments

- 6.2.3.1.1.1 Wrinkle Reduction Procedures

- 6.2.3.1.1.2 Skin Tightening Treatments

- 6.2.3.1.1 Anti-Aging Treatments

- 6.2.3.1 Facial Rejuvenation

- 6.3 By Product Type

- 6.3.1 Energy-Based Aesthetic Devices

- 6.3.1.1 Cryolipolysis Devices

- 6.3.1.1.1 Fat Freezing Systems

- 6.3.1.1.1.1 Non-Invasive Fat Reduction Devices

- 6.3.1.1.1.2 Body Contouring Cryotherapy Systems

- 6.3.1.1.1 Fat Freezing Systems

- 6.3.1.2 Ultrasound Aesthetic Devices

- 6.3.1.2.1 Focused Ultrasound Systems

- 6.3.1.2.1.1 High Intensity Focused Ultrasound Devices

- 6.3.1.2.1.2 Non-Invasive Skin Lifting Systems

- 6.3.1.2.1 Focused Ultrasound Systems

- 6.3.1.3 Laser-Based Aesthetic Devices

- 6.3.1.3.1 Ablative Laser Systems

- 6.3.1.3.1.1 CO2 Laser Skin Resurfacing Systems

- 6.3.1.3.1.2 Er:YAG Laser Treatment Systems

- 6.3.1.3.2 Non-Ablative Laser Systems

- 6.3.1.3.2.1 Fractional Laser Therapy Devices

- 6.3.1.3.2.2 Skin Rejuvenation Laser Systems

- 6.3.1.3.1 Ablative Laser Systems

- 6.3.1.4 Radiofrequency Aesthetic Devices

- 6.3.1.4.1 Skin Tightening RF Systems

- 6.3.1.4.1.1 Monopolar RF Skin Tightening Devices

- 6.3.1.4.1.2 Bipolar RF Skin Rejuvenation Systems

- 6.3.1.4.1 Skin Tightening RF Systems

- 6.3.1.1 Cryolipolysis Devices

- 6.4 By Procedure Type

- 6.4.1 Non-Invasive Procedures

- 6.4.1.1 Body Contouring Procedures

- 6.4.1.1.1 Non-Surgical Fat Reduction

- 6.4.1.1.1.1 Cryolipolysis Fat Reduction

- 6.4.1.1.1.2 RF Body Contouring Treatments

- 6.4.1.1.1 Non-Surgical Fat Reduction

- 6.4.1.2 Skin Rejuvenation Procedures

- 6.4.1.2.1 Laser Skin Resurfacing

- 6.4.1.2.1.1 Anti-Aging Laser Treatments

- 6.4.1.2.1.2 Skin Texture Improvement Procedures

- 6.4.1.2.1 Laser Skin Resurfacing

- 6.4.1.1 Body Contouring Procedures

- 6.4.2 Minimally Invasive Procedures

- 6.4.2.1 Dermal Filler Procedures

- 6.4.2.1.1 Facial Contouring Treatments

- 6.4.2.1.1.1 Lip Augmentation Procedures

- 6.4.2.1.1.2 Facial Volume Restoration Procedures

- 6.4.2.1.1 Facial Contouring Treatments

- 6.4.2.2 Injectable Cosmetic Procedures

- 6.4.2.2.1 Botulinum Toxin Injections

- 6.4.2.2.1.1 Wrinkle Reduction Treatments

- 6.4.2.2.1.2 Facial Muscle Relaxation Procedures

- 6.4.2.2.1 Botulinum Toxin Injections

- 6.4.2.1 Dermal Filler Procedures

- 6.5 By Injectable Aesthetic Products

- 6.5.1 Dermal Fillers

- 6.5.1.1 Collagen-Based Fillers

- 6.5.1.1.1 Facial Contouring Fillers

- 6.5.1.1.1.1 Nasolabial Fold Fillers

- 6.5.1.1.1.2 Skin Volume Restoration Fillers

- 6.5.1.1.1 Facial Contouring Fillers

- 6.5.1.2 Hyaluronic Acid Fillers

- 6.5.1.2.1 Facial Volume Restoration

- 6.5.1.2.1.1 Lip Enhancement Fillers

- 6.5.1.2.1.2 Cheek Augmentation Fillers

- 6.5.1.2.1 Facial Volume Restoration

- 6.5.1.1 Collagen-Based Fillers

- 6.5.2 Botulinum Toxin Products

- 6.5.2.1 Cosmetic Botulinum Toxin

- 6.5.2.1.1 Facial Wrinkle Reduction

- 6.5.2.1.1.1 Forehead Line Treatments

- 6.5.2.1.1.2 Crows Feet Treatment

- 6.5.2.1.1 Facial Wrinkle Reduction

- 6.5.2.1 Cosmetic Botulinum Toxin

- 6.5.1 Dermal Fillers

- 7. Market Segmentation by Geography

- 7.1 North America

- 7.2 Europe

- 7.3 Asia-Pacific

- 7.4 Latin America

- 7.5 Middle East & Africa

- 8. Competitive Landscape

- 8.1 Market Share Analysis

- 8.2 Product Portfolio Benchmarking

- 8.3 Product Positioning Mapping

- 8.4 Supply Chain & Distribution Partnerships

- 8.5 Competitive Intensity & Differentiation

- 9. Company Profiles

- 10. Strategic Intelligence & Pheonix AI Insights

- 10.1 Pheonix Demand Forecast Engine

- 10.2 Supply Chain & Infrastructure Analyzer

- 10.3 Technology & Innovation Tracker

- 10.4 Product Development Insights

- 10.5 Automated Porter’s Five Forces Analysis

- 11. Future Outlook & Strategic Recommendations

- 11.1 Emerging Market Expansion

- 11.2 Technology Innovation Strategies

- 11.3 Product Development Roadmap

- 11.4 Regional Expansion Strategies

- 11.5 Long-Term Market Outlook (2033+)

- 12. Appendix

- 13. About Pheonix Research

- 14. Disclaimer

- 6.4.1 Non-Invasive Procedures

- 6.3.1 Energy-Based Aesthetic Devices

- 6.2.1 Skin Treatments

- 6.1.1 Hospitals

- 6.1 By End User

Competitive Landscape

Competitive Landscape of the Asia-Pacific Medical Aesthetic Market

Executive Framing

In the dynamic landscape of the Asia Pacific medical aesthetic market, understanding the dimension of competitive intensity and market structure has never been more crucial. The market is characterized by its fragmented nature, where numerous players jostle for dominance amidst high barriers to entry and a complex regulatory environment. The competitive intensity is notably high, with the presence of Tier 1 players like AbbVie Inc., Lumenis, and Valeant Pharmaceuticals International Inc., amongst others, making strategic positioning imperative for survival and growth. This dimension matters now because it influences how companies maneuver to capture market share, optimize their portfolios, and engage with the evolving consumer preferences that drive demand. As market dynamics continue to evolve, driven by a surge in aesthetic awareness and technological advancements, stakeholders need to strategically position themselves to leverage opportunities and mitigate risks.

Current Market Reality

The current state of the Asia Pacific medical aesthetic market is marked by a fragmented structure, with a significant presence of both multinational corporations and regional players. Tier 1 companies, numbering five, dominate significant portions of the market, exerting a considerable influence on pricing strategies, product offerings, and technological innovations. This fragmentation is a result of varying regulatory landscapes, diverse consumer preferences, and the rapid pace of technological innovation, which creates opportunities for both established giants and nimble entrants. Companies like AbbVie Inc., which acquired Allergan, are leveraging acquisitions to consolidate their market position and expand product lines. Meanwhile, firms like Lumenis and Valeant Pharmaceuticals are investing in technology and expanding their service offerings to capture the growing demand for minimally invasive procedures.

The high competitive intensity is further underscored by strategic moves such as the acquisition of Aesthetic Healthcare Holdings by SBC Medical Group, and the launch of new products like the 24K gold-coated microneedle skincare products. These actions highlight the aggressive strategies companies are employing to differentiate themselves in a crowded market. The presence of companies like Beijing Toplaser Technology Co., Ltd., Lutronic Corporation, and Asclepion Laser Technologies indicates the diverse range of offerings and innovations that are driving competition. These entities are not only competing on the basis of price and product quality but also on their ability to offer cutting-edge solutions that resonate with the evolving consumer expectations.

Moreover, the market is witnessing a rising influence of social media and celebrity-driven beauty trends, which are reshaping consumer perceptions and fueling the demand for aesthetic treatments. The increasing societal acceptance of aesthetic procedures, coupled with the growing middle class and rising disposable incomes in the region, are key factors contributing to the market’s expansion. This is illustrated by the 30% increase in male clientele in China in 2023 and the projected influx of 1.17 million foreign patients for medical services in South Korea by 2024. These trends underscore the shifting demographics and preferences that companies must navigate to remain competitive.

Key Signals And Evidence

A pivotal signal in the competitive landscape is the acquisition of a regional distributor in Australia by Merz Aesthetics in January 2024. This move aims to streamline its supply chain and enhance product availability, reflecting a strategic focus on operational efficiency and market penetration. The acquisition not only strengthens Merz Aesthetics’ foothold in the region but also underscores the importance of supply chain optimization in maintaining competitive advantage.

Similarly, Allergan’s launch of a comprehensive training program for aesthetic practitioners across Southeast Asia in March 2023 highlights the emphasis on skill development and practitioner engagement. By investing in training, Allergan is not only enhancing the quality of service delivery but also fostering brand loyalty and establishing itself as a leader in practitioner support. This strategic move is crucial in a market where the shortage of skilled and certified practitioners poses a significant challenge.

The introduction of innovative products like the 24K gold-coated microneedle skincare products further exemplifies the industry’s focus on differentiation through technological innovation. As consumer demand for novel and effective treatments grows, companies are investing in product development to capture market share. This is complemented by the launch of the VISIA?? Facial Skin Analysis system, which leverages AI and real-time feedback systems to offer personalized skincare solutions. Such innovations not only enhance the consumer experience but also position companies at the forefront of technological advancement in the aesthetic market.

Furthermore, the acquisition of Aesthetic Healthcare Holdings by SBC Medical Group signifies the ongoing trend of consolidation within the industry. This acquisition reflects a strategic intent to expand service offerings and integrate capabilities, thereby enhancing competitive positioning. In a fragmented market, consolidation enables companies to achieve economies of scale, diversify their product portfolios, and strengthen their market presence.

Lastly, the launch of the YOUTHLY brand by GC Aesthetics in China is indicative of the growing demand for non-invasive procedures and the increasing influence of cultural and societal trends on aesthetic preferences. This move aligns with the broader trend of rising consumer awareness and demand for safer, more effective treatments. By introducing a new brand in a key market, GC Aesthetics is tapping into the burgeoning demand for aesthetic solutions and catering to the evolving needs of consumers.

These signals collectively highlight the market’s dynamic nature and the strategic maneuvers companies are undertaking to navigate the complexities of the Asia Pacific medical aesthetic industry. The interplay between technological advancements, consumer preferences, and regulatory frameworks is shaping the competitive landscape, necessitating strategic agility and innovation. As the market continues to evolve, companies must remain attuned to these signals to effectively position themselves for future growth and success.

Strategic Implications

The strategic implications of these developments in the Asia Pacific medical aesthetic market are manifold, encompassing competitive behavior, market positioning, and strategic decision-making. The fragmented market structure, coupled with high competitive intensity, presents both challenges and opportunities for incumbents and new entrants alike. Companies need to craft strategies that leverage technological advancements, consumer preferences, and regulatory landscapes to secure a competitive edge.

The acquisition of Allergan by AbbVie, for instance, exemplifies a strategic move aimed at consolidating market presence and enhancing product portfolios. By integrating Allergan???s extensive aesthetic product line, AbbVie strengthens its competitive positioning, allowing it to offer a broader range of solutions to meet diverse consumer needs. This move also highlights the importance of acquisitions as a strategic tool for achieving scale and unlocking synergies in a fragmented market.

Similarly, the launch of the VISIA?? Facial Skin Analysis system underscores the role of innovation in gaining a competitive advantage. By investing in cutting-edge technologies that offer real-time feedback and personalized solutions, companies can differentiate themselves from competitors and cater to the growing demand for sophisticated aesthetic treatments. This strategic focus on technology not only enhances product offerings but also strengthens brand loyalty and customer engagement.

The introduction of AI and real-time feedback systems further emphasizes the strategic importance of technological integration in the medical aesthetic industry. By harnessing the power of AI, companies can streamline operations, improve treatment outcomes, and enhance customer experiences. This technological shift is particularly significant in a market where consumer expectations are rapidly evolving, and personalized solutions are increasingly sought after.

The acquisition of Aesthetic Healthcare Holdings by SBC Medical Group is another strategic maneuver that highlights the importance of expanding geographic reach and diversifying service offerings. By acquiring a regional player, SBC Medical Group can tap into new markets, access a wider customer base, and enhance its operational footprint. This acquisition-driven strategy is particularly relevant in a fragmented market where scale and reach can be critical determinants of success.

Moreover, the launch of 24K gold-coated microneedle skincare products by various players signifies a trend towards product innovation and premiumization. In a market characterized by discerning consumers and increasing disposable incomes, offering high-end, innovative products can be a key differentiator. This trend also reflects the growing influence of social media and celebrity-driven beauty trends, which are shaping consumer preferences and driving demand for premium aesthetic solutions.

Forward Outlook

Looking ahead, the Asia Pacific medical aesthetic market is poised for significant transformation, driven by evolving consumer preferences, technological advancements, and regulatory developments. The interplay between these factors will continue to shape the competitive landscape, necessitating strategic agility and innovation from market players.

In the near-to-medium term, we can expect continued consolidation as companies seek to strengthen their market positions and achieve economies of scale. Strategic acquisitions and partnerships will likely remain a focal point, enabling companies to enhance their product portfolios, expand geographic reach, and access new customer segments. This trend towards consolidation will also intensify competition among Tier 1 players, prompting them to innovate and differentiate their offerings to maintain market leadership.

Technological advancements will play a pivotal role in shaping the future of the market. The integration of AI and real-time feedback systems is expected to become more prevalent, driving improvements in treatment outcomes and customer experiences. As companies invest in research and development to create cutting-edge solutions, we may see a surge in the introduction of new products and technologies that cater to the diverse needs of consumers.

Regulatory developments will also continue to influence the market dynamics. As countries in the Asia Pacific region impose stringent regulatory requirements, companies will need to navigate complex approval processes and ensure compliance to maintain their market presence. Regulatory compliance will increasingly serve as a competitive moat, protecting established players from new entrants and enabling them to maintain their market positions.

The growing demand for minimally invasive and non-invasive procedures presents a significant growth opportunity for market players. As consumer awareness of aesthetic treatments increases and societal acceptance grows, companies that offer safe, effective, and innovative solutions are likely to thrive. This trend towards non-invasive treatments aligns with the broader shift towards wellness and self-care, further fueling market growth.

In conclusion, the Asia Pacific medical aesthetic market is undergoing a period of dynamic transformation, characterized by high competitive intensity, technological innovation, and evolving consumer preferences. Companies that can effectively navigate this complex landscape, leveraging strategic acquisitions, technological advancements, and regulatory compliance, will be well-positioned to capitalize on the growth opportunities and achieve long-term success. As the market continues to evolve, strategic agility, innovation, and consumer-centricity will be the keys to thriving in this competitive arena.

Value Chain

Value Chain and Supply Chain Dynamics in the Asia-Pacific Medical Aesthetic Market

Executive Framing

In the rapidly evolving Asia Pacific medical aesthetic market, the value chain and supply chain dynamics are under intense scrutiny due to several critical factors shaping this dimension. As the region experiences a surge in demand for advanced dermatology treatments and aesthetic procedures, understanding the underlying supply chain complexities and value chain bottlenecks becomes crucial. This dimension matters now because it directly impacts market structure, cost management, and strategic positioning of key players. The region’s hybrid operational model and platform marketplace distribution structure further emphasize the importance of navigating these challenges effectively. Companies operating in this space must contend with high initial investments, stringent regulatory requirements, and a shortage of skilled practitioners, all of which have significant implications for margins, bargaining power, and capacity utilization.

Current Market Reality

Presently, the Asia Pacific medical aesthetic market is characterized by a moderate level of supply chain complexity. However, the landscape is fraught with bottlenecks that can impede growth and profitability. One of the most significant challenges is the high initial investment required for advanced dermatology treatment devices. These devices are crucial for delivering cutting-edge aesthetic procedures but necessitate substantial capital outlays, which can be a barrier to entry for new market participants and a constraint on expansion for existing players.

Regulatory scrutiny across the region, particularly in countries like Japan, Australia, and South Korea, adds another layer of complexity. These countries have stringent approval processes for new treatments and devices, often delaying product launches and increasing compliance costs. This regulatory landscape not only affects the speed at which companies can bring innovations to market but also influences their strategic decisions regarding product development and market entry.

Moreover, the limited availability of skilled dermatologists and trained operators in certain APAC regions exacerbates the supply chain challenges. This shortage of certified aesthetic practitioners hinders the ability of companies to meet rising demand and maintain quality standards, particularly in tier-3 Asian cities where social-commerce-fueled demand is growing. As a result, companies like Allergan have initiated comprehensive training programs for aesthetic practitioners across Southeast Asia to address this gap and enhance their service delivery capabilities.

The prevalence of counterfeit and substandard products further complicates the market landscape. These products undermine consumer trust and pose safety risks, leading to increased regulatory scrutiny and potential reputational damage for legitimate players. Companies must navigate these challenges by ensuring stringent quality control measures and fostering consumer awareness to differentiate themselves in a crowded marketplace.

Key Signals and Evidence

- High Initial Investment: Advanced dermatology treatment devices require substantial capital outlay, acting as a barrier to entry and affecting expansion strategies.

- Regulatory Scrutiny: Stringent approvals in Japan, Australia, and South Korea increase compliance costs and delay product launches, influencing strategic decision-making.

- Skills Shortage: Limited availability of certified aesthetic practitioners affects service delivery and capacity utilization. Companies like Allergan are addressing this through training programs.

- Social-Commerce Demand: Rising demand in tier-3 Asian cities highlights the need for digital and social commerce strategies to capture emerging consumer segments.

- Clean and Sustainable Beauty Trends: Consumer preference is shifting toward environmentally friendly and ethical products, impacting product development and supply chain decisions.

Strategic Implications

- Balancing Regulatory Complexities and Market Opportunities: Companies must allocate resources to navigate approvals, ensuring compliance while minimizing delays. Strategic acquisitions, like Merz Aesthetics??? regional distributor acquisition in Australia, help optimize local operations.

- Addressing the Skills Gap: Workforce development through training programs is essential to enhance service quality, operational efficiency, and competitive positioning.

- Embracing Technological Advancements: Integration of AI and advanced dermatology devices enhances treatment effectiveness and customer experience but requires high initial investment, possibly driving industry consolidation.

- Leveraging Social-Commerce and Digital Platforms: Digital transformation allows companies to tap into emerging consumer segments in tier-3 cities, enhancing market reach and engagement.

- Navigating the Shift Towards Sustainable Beauty: Adopting sustainable practices strengthens brand reputation but requires supply chain adjustments and cost management.

Forward Outlook

The Asia Pacific medical aesthetic market is poised for continued transformation as companies navigate regulatory complexities, address skills gaps, and embrace technological advancements. In the near-to-medium-term, several key trends are likely to shape the market landscape and influence strategic decision-making.

Increasing Consolidation and Strategic Partnerships

High investment barriers and regulatory challenges will drive mergers, acquisitions, and strategic partnerships, enabling companies to achieve economies of scale, enhance market presence, and access new capabilities. Local partnerships provide insights into regional market dynamics and support regulatory navigation.

Growing Importance of Digital Transformation

Integration of AI and digital platforms will continue reshaping the value chain, enabling personalized experiences, optimized resource allocation, and operational efficiency.

Emphasis on Workforce Development

Investments in training and certification programs will be critical to bridge the skills gap, ensuring high-quality service delivery and sustaining market growth.

Sustainability as a Competitive Differentiator

Companies that integrate sustainable practices into operations and product offerings will appeal to environmentally conscious consumers, creating a competitive advantage and expanding market reach.

Conclusion

The Asia Pacific medical aesthetic market is undergoing dynamic transformation driven by regulatory challenges, technological advancements, and shifting consumer preferences. Strategic navigation of these complexities???including regulatory compliance, workforce development, digital transformation, and sustainability initiatives???will enable companies to capture growth opportunities and maintain long-term competitive advantage in this evolving landscape.

Investment Activity

Investment Activity of the Asia-Pacific Medical Aesthetic Market

Executive Framing

The Asia Pacific Medical Aesthetic market is undergoing a transformative shift, driven by significant changes in investment and funding dynamics. This dimension is critical because it not only influences the strategic allocation of resources but also shapes the competitive landscape and innovation trajectories within the region. With a forecast period of 2026-2033, understanding the nuances of capital logic and strategic allocation is essential for stakeholders aiming to capitalize on emerging opportunities.

As the demand for medical aesthetic services continues to rise, the market is witnessing a heightened level of capital intensity. Investment trends are on an upward trajectory, signaling growing investor confidence in the long-term potential of this sector. This confidence is further bolstered by recent mergers and acquisitions (M&A) activity, which underscores the strategic realignments taking place within the industry.

Active investors, including prominent entities such as Sumitomo Corporation, UnitedHealth Group, and AXA, are channeling significant resources into healthcare technology, integrated care, and consumer health, among other themes. These developments are not only indicative of a robust investment climate but also reflect the evolving priorities of investors who are increasingly focusing on digital health solutions, telemedicine, and AI in healthcare.

Current Market Reality

The present state of the Asia Pacific Medical Aesthetic market is characterized by dynamic investment flows and strategic maneuvers by key players. The involvement of heavyweight investors like Berkshire Hathaway Inc. and MetLife Services and Solutions LLC demonstrates the allure of the market’s growth potential. Such entities are leveraging their capital to back business models and assets that align with emerging health care trends, such as personalized care and chronic disease management.

A notable feature of the current market reality is the rise in partnerships between technology and healthcare companies. These collaborations are pivotal in driving innovation and expanding service offerings, as they enable the integration of cutting-edge technologies into healthcare delivery. For example, the growing interest in telemedicine and digital health solutions is prompting investors to support ventures that facilitate remote patient monitoring and virtual consultations. This trend is further fueled by the increasing consumer acceptance of AI and digital health services, which is reshaping how healthcare is accessed and consumed.

Moreover, the expansion of universal health coverage across the region is another critical factor attracting investment. This policy shift is set to increase the accessibility of healthcare services, thereby driving demand for medical aesthetic procedures. As a result, companies are strategizing to position themselves advantageously within this expanding market. For instance, the expansion of retail chains and partnerships with retailers are emerging as viable strategies to enhance service delivery and customer engagement. These moves are not only expanding the reach of medical aesthetic services but also creating new revenue streams for businesses.

The shortage of healthcare workers presents both a challenge and an opportunity for the market. On one hand, it underscores the need for innovative solutions to optimize resource utilization and maintain service quality. On the other hand, it presents an opportunity for investors to back technological advancements that can mitigate workforce constraints. The development and deployment of telehealth services and AI-driven solutions are gaining traction as they promise to enhance operational efficiency and patient outcomes.

Key Signals and Evidence

In synthesizing the primary and secondary signals, several structural drivers emerge that are shaping the investment landscape in the Asia Pacific Medical Aesthetic market:

- Technology???Healthcare Partnerships: The rise in partnerships between technology and healthcare companies reflects a broader shift towards integrated care models that leverage technology to improve patient outcomes. Companies like Sumitomo Corporation and UnitedHealth Group are at the forefront of this trend.

- Expansion of Universal Health Coverage: Increasing access to healthcare services is prompting investors to allocate capital towards scalable business models that can cater to a larger patient base.

- Healthcare Workforce Shortages: The shortage of healthcare workers compels the market to explore telehealth and AI-driven solutions to alleviate workforce pressures and improve care delivery.

- Retail Partnerships and Expansion: Collaborations with retailers are facilitating the integration of medical aesthetic services into everyday consumer experiences, enhancing accessibility and convenience.

- Telemedicine Growth: The expansion of telemedicine and related services is attracting significant investment, with companies backing platforms offering virtual consultations and remote monitoring.

In conclusion, the Asia Pacific Medical Aesthetic market is at a pivotal juncture, characterized by rising investment trends and strategic realignments. Understanding the interplay between capital flows, investment themes, and market dynamics will be crucial for stakeholders to capitalize on emerging opportunities.

Strategic Implications

The evolving investment landscape in the Asia Pacific Medical Aesthetic market presents several strategic implications for stakeholders:

- Integrated Care Solutions: Stakeholders must invest in digital health platforms and AI-driven solutions to enhance service delivery, patient outcomes, and operational efficiency.

- Aligning with Universal Health Coverage: Companies should strategically align with government initiatives to expand access and tap into new customer segments, fostering long-term growth and consumer trust.

- Workforce Optimization: Investments in automation, AI, and telehealth are critical to address workforce shortages while maintaining service quality.

- Retail Partnerships: Leveraging collaborations with retailers enhances accessibility, convenience, brand visibility, and consumer engagement.

- Telemedicine Investments: Prioritizing telehealth platforms ensures companies can meet consumer demand for accessible healthcare and remain competitive in the digital health space.

Investment Activity of the Asia-Pacific Medical Aesthetic Market

Forward Outlook

Looking ahead, the Asia Pacific Medical Aesthetic market is poised for significant growth, driven by strategic investments and evolving market dynamics. The rise in partnerships between technology and healthcare companies is expected to accelerate, leading to innovative solutions that enhance service delivery and patient outcomes. This trend will likely drive increased competition among stakeholders, necessitating continuous investment in digital health platforms to maintain market leadership.

The expansion of universal health coverage is anticipated to further broaden consumer access to medical aesthetic services, creating new growth opportunities for stakeholders. Companies that strategically align with government initiatives and invest in service delivery enhancements will likely benefit from increased consumer spending and market share growth. The ongoing shortage of healthcare workers will continue to influence investment priorities and the adoption of AI and telehealth solutions.

Technology & Innovation

Technology and Innovation Landscape in the Asia-Pacific Medical Aesthetic Market

Executive Framing

The Asia Pacific medical aesthetic market is undergoing a transformative phase, primarily driven by technology and innovation. This dimension is crucial now more than ever because it directly influences the market’s evolution in terms of procedure economics, patient outcomes, and adoption rates. With a forecast period extending from 2026 to 2033, understanding the role of technology is imperative for stakeholders aiming to capitalize on emerging opportunities. The integration of advanced technologies such as AI-driven treatment mapping, High-Intensity Focused Ultrasound (HIFU) devices, and Radiofrequency (RF) based aesthetic devices is reshaping the landscape, offering enhanced precision, efficiency, and patient satisfaction.

This technological evolution is not just about new devices or software; it represents a paradigm shift in how aesthetic procedures are perceived and delivered. The increasing innovation intensity and moderate patent activity indicate a vibrant ecosystem fostering continuous product development and improvement. Key players such as Candela Corporation, Lumenis Ltd., Cynosure, and others are at the forefront, driving this change through significant investments in R&D, strategic acquisitions, and the integration of cutting-edge technologies into their product lines.

Current Market Reality

The Asia Pacific region is witnessing a growing demand for non-invasive and minimally invasive aesthetic procedures. This trend is fueled by rising consumer awareness and the influence of social media, which plays a pivotal role in normalizing and promoting cosmetic treatments. Companies like Merz Pharma GmbH & Co. KGaA and Venus Concept are capitalizing on this trend by expanding their product offerings and investing in technologies that promise natural-looking results without the need for extensive surgery.

The market’s current reality is also shaped by regulatory dynamics. Stringent regulatory approvals in major markets such as Japan, Australia, and South Korea ensure that only safe and effective technologies reach consumers. This regulatory environment, while challenging, also serves as a quality filter, ensuring that innovations are robust and reliable. For instance, Merz Aesthetics’ strategic acquisition of a regional distributor in Australia highlights the importance of streamlining supply chains to enhance product availability and compliance with local regulatory standards.

Moreover, the adoption of AI and digital tools in clinics is revolutionizing the way treatments are planned and executed. AI-driven treatment mapping allows for personalized aesthetic solutions, enhancing patient satisfaction and optimizing resource utilization. Companies like Lumenis Ltd. and Cynosure are integrating AI into their platforms, offering practitioners tools to deliver more precise and tailored treatments.

Key Signals and Evidence

- Adoption of Non-Invasive Treatments: Growing popularity of HIFU, RF-based, and IPL devices to deliver effective results with minimal downtime and discomfort. Companies like Alma Lasers and Cutera are leading this trend.

- Medical Tourism Expansion: Asia Pacific countries such as Thailand and South Korea are attracting international patients, supported by R&D investments and advanced technologies by companies like Sciton, Inc.

- Regulatory Approvals: Approvals in Japan, Australia, and South Korea validate safety and efficacy, boosting consumer confidence. Examples include 24K gold-coated microneedle skincare product launches.

- Integration of AI and Digital Tools: Enhances diagnostics, treatment planning, and personalized care. Companies like Lumenis and Cynosure are providing platforms for precision-driven procedures.

- Innovation Intensity and R&D: Moderate patent activity and continuous product development indicate a growing ecosystem, with key players investing in hybrid and multi-energy platforms to address diverse aesthetic concerns.

Strategic Implications

- Technology Adoption: Companies must integrate AI and digital tools to improve patient outcomes and operational efficiency, and adapt product portfolios to support non-invasive treatments.

- Regulatory Navigation: Success in navigating stringent approvals enhances market credibility and competitive advantage. Strategic acquisitions like Merz Pharma???s distributor acquisition streamline compliance and supply chains.

- Medical Tourism Leverage: Collaborations with local clinics and tourism operators are essential to capture international patients and expand revenue streams.

- R&D Investment: Ongoing investment in innovation ensures the development of advanced technologies, hybrid platforms, and AI integration for sustained market growth.

- Consumer Education: Transparent communication and digital engagement are necessary to counter misinformation, build trust, and promote advanced aesthetic solutions.

Forward Outlook

Looking ahead, the Asia Pacific medical aesthetic market is poised for continued growth and transformation. The convergence of technological advancements, regulatory developments, and evolving consumer preferences will shape the market’s trajectory over the forecast period. Integration of AI and digital tools will drive improvements in procedural efficiency and patient outcomes.

Non-invasive treatments will continue to gain traction, with investments in hybrid and multi-energy platforms offering comprehensive solutions. Regulatory environments will remain critical, and companies that navigate these successfully will gain a competitive edge. Medical tourism will further support market expansion by attracting international patients, creating broader revenue opportunities.

Overall, the Asia Pacific medical aesthetic market is entering a dynamic phase driven by technology, regulatory evolution, and shifting consumer behavior. Stakeholders who can align with these trends and leverage emerging opportunities will be well-positioned to thrive.

Market Risk

Risk Factors and Disruption Threats in the Asia-Pacific Medical Aesthetic Market

Executive Framing

The Asia Pacific medical aesthetic market is currently navigating a complex landscape of structural constraints and market vulnerabilities that could significantly alter its trajectory from 2026 to 2033. This dimension is crucial at this moment due to the moderate overall market risk level and the high geopolitical exposure level that characterizes this region.

As the demand for cosmetic procedures continues to rise, driven by increased disposable incomes and a growing demographic of younger clients seeking non-invasive treatments, the market must also reckon with disruptive threats. These include regulatory inconsistencies, unregulated clinics, and the risks associated with medical tourism, all of which have the potential to reshape market dynamics profoundly.

The intricacies of regulatory environments across different countries within the Asia Pacific region present a significant challenge. The disparities in medical standards and the presence of unlicensed practitioners create an uneven playing field, leading to patient safety concerns and an increased risk of botched procedures. Moreover, the rise in medical tourism, while initially seen as a lucrative opportunity, has introduced additional layers of risk, including inflated fees and complications from unqualified practitioners. These issues are compounded by the lack of a unified regulatory framework, which makes the market susceptible to disruptions and limits the operational resilience of stakeholders.

Current Market Reality

The present state of the Asia Pacific medical aesthetic market is marked by complex and interrelated challenges that are already impacting its structure and operational dynamics. One pressing issue is the shortage of skilled and certified practitioners in certain geographical areas, limiting the market’s ability to meet rising demand for cosmetic procedures. This shortage is exacerbated by stringent regulatory requirements and complex approval processes for new treatments, particularly in countries such as Japan, Australia, and South Korea.

In response, some companies are taking proactive measures to bolster their market positions and address the skill gap. For instance, Allergan’s launch of a comprehensive training program for aesthetic practitioners across Southeast Asia in March 2023 is a strategic move to enhance practitioner competency and ensure safer outcomes. Similarly, Merz Aesthetics’ acquisition of a regional distributor in Australia in January 2024 aims to streamline its supply chain and improve product availability, mitigating operational constraints.

Despite these efforts, the market is experiencing a decline in foreign investment, indicative of broader concerns about regulatory unpredictability and geopolitical tensions. This decline limits the influx of capital necessary for innovation and expansion. Additionally, the lack of regulation in certain areas continues to pose significant risks, evidenced by government crackdowns on unregistered clinics and reports of complications from overseas procedures. Patient testimonials and complaints from foreign patients underscore the urgent need for increased regulatory scrutiny and standardization efforts.

Key Signals and Evidence

The synthesis of primary and secondary signals reveals a multifaceted narrative that underscores structural vulnerabilities and market risks:

- Regulatory Complexity: Stringent approval processes and disparities across countries pose barriers to market entry and innovation. Global trends, such as the Modernisation of Cosmetics Regulation Act of 2022 (MoCRA), exemplify the move towards stricter regulatory frameworks.

- Skill Shortages: A shortage of highly skilled aesthetic professionals limits scalability, impacts pricing, and affects demand elasticity. Rising demand for minimally invasive treatments exacerbates the issue, creating inconsistent patient experiences.

- Decline in Foreign Investment: Geopolitical risks and regulatory uncertainties have reduced foreign capital inflows, emphasizing the need for risk mitigation strategies and strategic alliances.

- Regulatory Enforcement Efforts: Government crackdowns on unregistered clinics aim to improve patient safety and market credibility but introduce compliance challenges and operational hurdles.

- Market Vulnerabilities: Patient complaints, unregulated clinics, and complications from medical tourism highlight the need for enhanced consumer education and trust-building initiatives.

Strategic Implications

The identified risks and structural constraints have profound implications for stakeholders:

- Navigating Regulatory Complexities: Firms must invest in practitioner training and robust compliance frameworks to align with varying national regulations. Allergan’s regional training program exemplifies proactive adaptation.

- Addressing Skill Shortages: Investments in comprehensive training programs and supply chain enhancements, as demonstrated by Merz Aesthetics’ regional acquisition, can improve operational resilience and treatment outcomes.

- Mitigating Investment Declines: Transparency, regulatory compliance, and strategic alliances are crucial to restoring investor confidence. Mergers and acquisitions can demonstrate market stability and growth potential.

- Enhancing Consumer Trust: Education campaigns and patient support initiatives can reduce risks associated with unregulated clinics and build brand credibility. Stakeholders that prioritize safety and transparency gain a competitive advantage.

Forward Outlook

As the Asia Pacific medical aesthetic market moves forward, the interplay of regulatory pressure, skill shortages, and investment dynamics will significantly shape its trajectory. Stakeholders must remain agile and responsive to these evolving challenges to sustain growth and capitalize on emerging opportunities.

In the near term, increased regulatory scrutiny and standardization efforts may drive market consolidation, improving overall stability and service quality. Smaller, non-compliant players may exit the market, benefiting compliant providers and patients.

In the medium term, targeted training programs and international collaborations will address skill shortages, strengthening operational resilience and supporting sustained growth and innovation.

Efforts to enhance transparency and regulatory compliance may gradually restore foreign investor confidence. Strategic partnerships and mergers will continue to play a critical role in fostering market expansion.

Ultimately, the strategic actions taken today will determine the market’s ability to navigate structural constraints and vulnerabilities. Proactive risk management and alignment with regulatory standards can position the Asia Pacific medical aesthetic market for a resilient and prosperous future.

Regulatory Landscape

Regulatory and Policy Landscape of the Asia-Pacific Medical Aesthetic Market

Executive Framing

The regulatory and policy environment in the Asia Pacific medical aesthetic market is undergoing significant transformations that are reshaping the landscape in which companies operate. This dimension is paramount now due to the accelerating pace of regulatory changes and the increasing complexity of compliance requirements. These shifts are not merely administrative hurdles; they are pivotal factors that influence market entry, product development timelines, and competitive dynamics. As aesthetic treatments and devices gain popularity across the region, the need for a robust regulatory framework becomes critical to ensure safety, efficacy, and consumer protection.

The regulatory landscape is marked by heightened scrutiny and evolving standards, driving companies to adapt swiftly to maintain compliance and market presence. The introduction of new regulations and amendments to existing ones, coupled with increased oversight from regulatory bodies, necessitates strategic agility from market participants. Understanding and navigating these regulatory developments is essential for stakeholders seeking to capitalize on the growing demand for medical aesthetic products and services in the Asia Pacific region.

Current Market Reality

The current state of the Asia Pacific medical aesthetic market is characterized by a complex interplay of regulatory requirements and market dynamics. Key regulatory bodies such as the Medical Device Authority (MDA) of Malaysia, China’s National Medical Products Administration (NMPA), and the US Food and Drug Administration (USFDA) play crucial roles in defining the compliance landscape. These bodies have introduced or are implementing regulations that significantly impact the development and commercialization of aesthetic devices and treatments.

For instance, the Modernisation of Cosmetics Regulation Act of 2022 (MoCRA) represents a major overhaul in the regulatory framework governing cosmetics, including those used in aesthetic treatments. This act emphasizes stricter guidelines for labeling, promotion, and advertising, ensuring claims made by companies are substantiated and not misleading. The introduction of differentiated microbial limits for sensitive product categories underscores the increasing focus on product safety and consumer protection.

Phased enforcement schedules for new regulations indicate a deliberate approach by regulatory bodies to allow companies time to adapt while ensuring compliance. This phased approach mitigates the risk of market disruptions and allows smoother transitions to new norms. However, it also poses challenges for companies in managing compliance timelines and resource allocation.

Scrutiny on sustainable claims and greenwashing is another significant aspect of the current regulatory environment. With growing consumer preference for environmentally friendly products, regulators are tightening oversight on sustainability claims to prevent misleading information. This trend is exemplified by the proposed ban on Per- and polyfluoroalkyl substances (PFAS), which are under scrutiny due to environmental and health concerns.

Key Signals and Evidence

- Modernisation of Cosmetics Regulation Act of 2022 (MoCRA): Introduces comprehensive guidelines for cosmetic labeling, promotion, and advertising, enhancing transparency and consumer trust.

- Regulation on Safety Standards for Cosmetics: Establishes stringent safety requirements for products, ensuring they meet efficacy and quality criteria before entering the market.

- Phased Enforcement Schedule: Allows gradual adaptation to new regulations, reducing the risk of market disruptions while requiring strategic planning and resource allocation.

- Scrutiny on Labeling, Promotion, and Advertising: Prevents misleading claims, greenwashing, and emphasizes ingredient transparency, particularly regarding new ingredient standards.

- Company Initiatives: Allergan’s training programs for practitioners and Merz Aesthetics’ regional distributor acquisition demonstrate proactive adaptation to regulatory changes.

Strategic Implications

- Compliance and Operational Strategy: Companies must invest in research, development, and documentation processes to meet new safety and efficacy standards.

- Marketing Transparency: Increased scrutiny over labeling and promotion necessitates verifiable evidence for claims, influencing marketing strategies and consumer trust.

- Phased Implementation: Provides opportunity to align strategies with evolving regulations, requiring proactive planning, monitoring, and capacity-building initiatives.

- Sustainability and Greenwashing: Companies with credible sustainability practices can differentiate themselves, while those with unsubstantiated claims face compliance risks.

Forward Outlook

Looking ahead, the Asia Pacific medical aesthetic market is expected to continue evolving in response to the dynamic regulatory landscape. Emphasis on safety, transparency, and sustainability will remain central to regulatory developments, shaping company strategies.

Differentiated microbial limits and new ingredient standards signal a shift toward stringent safety and quality requirements. The proposed PFAS ban and fragrance allergen labeling requirements further highlight regulatory focus on consumer safety and environmental sustainability, driving innovation in product formulation and packaging.

In the near-to-medium term, companies must prioritize compliance and strategic alignment with evolving regulations. This includes proactive monitoring, collaboration with stakeholders, and investment in R&D. By embracing these changes, companies can position themselves for success in the dynamic and evolving Asia Pacific medical aesthetic market.