Global Contact Lenses Market size and share Analysis 2026-2033

Global Contact Lenses Market Size & Forecast

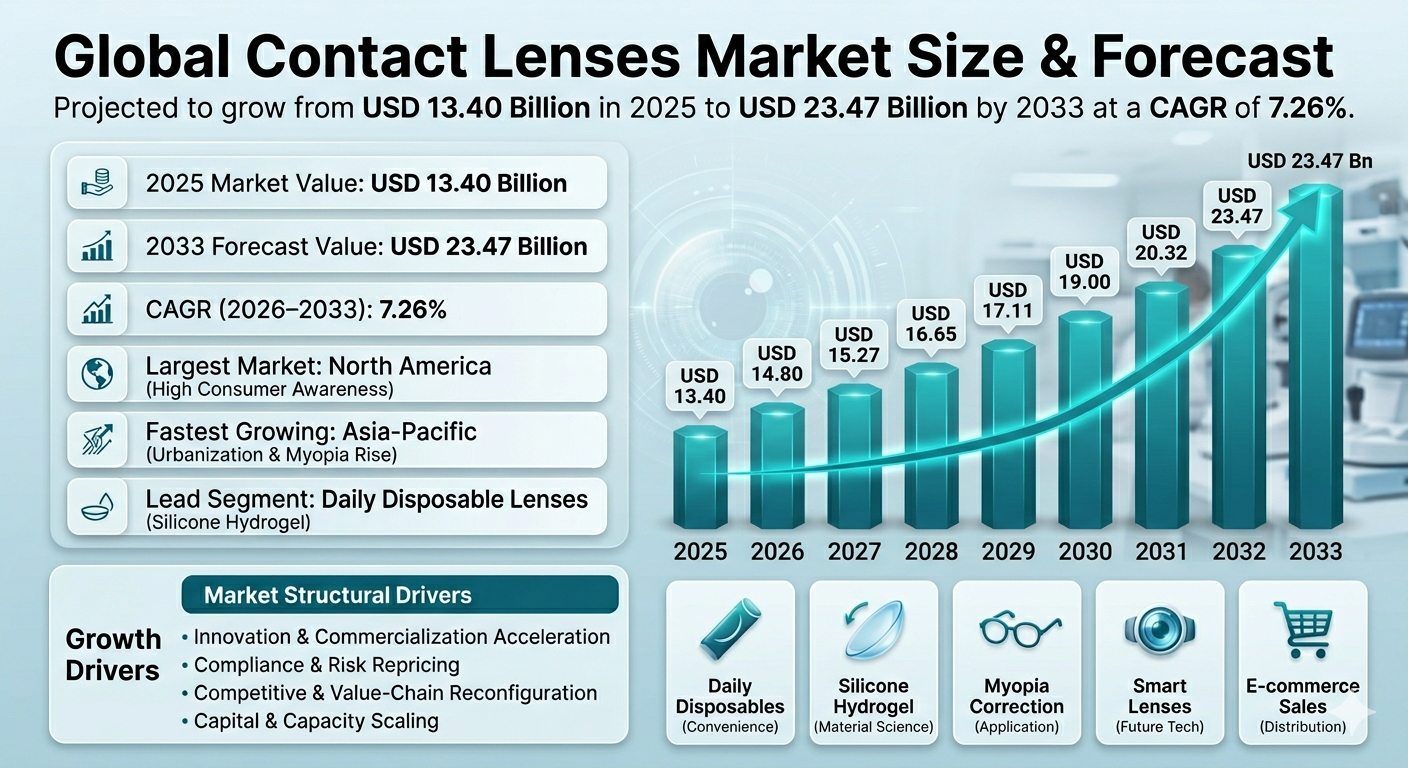

The global contact lenses market is poised for a significant expansion over the forecast period from 2026 to 2033. With an established base year market size of USD 13.40 billion in 2025, the industry is projected to achieve a market size of USD 23.47 billion by 2033, reflecting a steady compound annual growth rate (CAGR) of 7.26%. This growth trajectory underscores a robust demand and innovation landscape that is driving the contact lenses market forward.

Several factors contribute to this anticipated growth. The increasing prevalence of vision impairments, rising consumer preference for convenient and hygienic vision correction solutions, and technological advancements in lens materials are central drivers. Additionally, the growing awareness of eye health and hygiene is fostering a higher adoption rate of contact lenses over traditional spectacles. The market is witnessing a surge in demand for daily disposable lenses, which align with consumer preferences for convenience and hygiene, further propelling market expansion.

Moreover, the contact lenses market is experiencing an influx of investments, particularly in technology and innovative product development. Investment trends indicate a rising capital intensity level, with recent mergers and acquisitions reflecting a strategic focus on expanding product portfolios and enhancing market presence. Companies within the space are also exploring alliances and partnerships to leverage technological advancements and streamline supply chains, thus reinforcing market growth.

Global contact lenses market Overview

The contact lenses market is characterized by a fragmented competitive landscape with a high level of competitive intensity. Major players such as Johnson & Johnson Vision, Alcon, CooperVision, Bausch + Lomb, and Menicon dominate the market, actively engaging in product launches, strategic alliances, and technological innovations. The market structure is driven by dynamic competitive movements, including the launch of daily silicone hydrogel lenses and strategic mergers and acquisitions, which are reshaping the competitive dynamics.

The adoption of advanced technologies like silicone hydrogel lenses and smart contact lenses is enhancing product efficacy and user comfort, leading to increased consumer satisfaction and market penetration. Technological maturity is compressing development-to-commercialization cycles, enabling companies to bring innovative products to market more rapidly. This acceleration in technology adoption is supported by strong capital inflows and regulatory frameworks that streamline the approval process for new contact lens materials and designs.

Regulatory compliance remains a critical aspect of the market, with stringent government regulations guiding product approval and market entry. Key regulations, such as the Medical Device Regulation (EU) 2017/745 and various FDA guidelines, ensure product safety and performance, influencing product roadmaps and raising execution standards across the industry. Furthermore, regulatory tightening and risk signals are leading to a repricing of operating requirements, necessitating higher compliance and risk management measures among market participants.

Structural Drivers of Global contact lenses market Growth

Innovation and Commercialization Acceleration

The contact lenses market is experiencing a rapid pace of innovation and commercialization, primarily fueled by advancements in technology and increased funding for research and development. This driver is exemplified by the growing adoption of smart contact lenses and moisture-retaining materials, which enhance user experience and expand addressable applications. The compression of development-to-commercialization cycles allows companies to introduce cutting-edge products that cater to emerging consumer needs, thereby increasing the adoption speed and expanding market reach. As private equity investments continue to rise, the influx of capital supports this innovation trajectory, enabling companies to explore new technological frontiers and maintain competitive advantages.

Compliance and Risk Repricing

Regulatory tightening and evolving risk considerations are repricing operational requirements within the contact lenses market. This driver is underpinned by significant regulatory changes, such as the repeal of color additive regulations for FD&C Red No. 3 and the implementation of the Medical Device Regulation (EU) 2017/745. These regulatory shifts necessitate adjustments in product development and compliance strategies, raising execution standards across the industry. Companies are compelled to navigate complex regulatory environments while ensuring product safety and efficacy, leading to a shift in product roadmaps and heightened focus on compliance measures.

Competitive and Value-Chain Reconfiguration

The contact lenses market is undergoing competitive and value-chain reconfiguration, driven by strategic moves and constraints within the supply chain. Notably, strategic acquisitions, such as Alcon's intent to acquire STAAR Surgical Company, are reshaping competitive dynamics and reallocating bargaining power. These moves force portfolio repositioning and alter the concentration of margin and growth within the market. Additionally, value-chain constraints, including strict government regulations for contact lens approval and high regulation in regions like China, influence market entry and expansion strategies. As a result, companies are reevaluating their positioning within the value chain to optimize growth opportunities.

Capital and Capacity Scaling

Capital deployment into capacity and process upgrades is a critical driver enabling faster scale in high-demand segments of the contact lenses market. This driver is supported by increased private equity investments and regulatory requirements that necessitate capacity scaling and process enhancements. Companies are investing in advanced manufacturing processes and infrastructure to expand throughput and reduce deployment friction, thereby meeting growing consumer demand. This scaling effort is particularly evident in segments like daily disposable lenses, which align with consumer preferences for convenience and hygiene, further bolstering market growth.

Market Segmentation Analysis

Wear Type

The market is segmented into daily wear lenses, extended wear lenses, and continuous wear lenses. Daily disposable lenses, a subset of daily wear lenses, are witnessing significant demand due to their convenience and hygiene benefits. The preference for single-use contact lenses is driven by increasing consumer awareness of eye health and the rising prevalence of myopia, particularly among younger demographics. Extended wear lenses, which offer weekly or monthly replacement options, cater to consumers seeking longer-duration solutions, while continuous wear lenses provide high oxygen permeability for prolonged use.

Application

Contact lenses are utilized for therapeutic applications, cosmetic vision enhancement, and refractive error correction. Therapeutic applications, such as keratoconus management and corneal protection lenses, address specific medical needs and contribute to the market's growth. Cosmetic lenses, including colored and decorative options, appeal to consumers seeking aesthetic enhancements. Refractive error correction lenses, encompassing myopia, hyperopia, and astigmatism correction, represent a significant share of the market, driven by the increasing prevalence of vision impairments and rising consumer awareness.

Product Type

The market comprises soft contact lenses, hybrid contact lenses, specialty contact lenses, and rigid gas-permeable (RGP) lenses. Soft contact lenses, particularly those with silicone hydrogel materials, are gaining traction due to their comfort and moisture retention properties. Hybrid lenses, offering the benefits of both soft and RGP lenses, cater to consumers seeking high oxygen transmission and comfort. Specialty lenses, such as toric and multifocal options, address specific vision correction needs, while RGP lenses provide durability and precision for certain applications.

Material Type

The contact lenses market is segmented by material type, including hydrogel, silicone hydrogel, and fluoro-silicone acrylate materials. Silicone hydrogel lenses, known for their oxygen permeability and advanced breathable properties, are witnessing increased adoption. These materials enhance comfort and reduce the risk of complications, aligning with consumer preferences for high-performance lenses.

Distribution Channel

The market's distribution channels include online sales, optical retail stores, and hospital and clinical distribution. Online sales channels, particularly e-commerce platforms, are gaining prominence due to the convenience and accessibility they offer consumers. Optical retail stores and optometry clinics continue to play a crucial role in market distribution, providing personalized fitting and expert consultation services. Hospital and clinical distribution channels cater to therapeutic and specialized vision correction needs, supporting market growth through professional healthcare networks.

The contact lenses market's segmentation highlights the diverse range of products and applications driving industry dynamics. As consumer preferences evolve, manufacturers are focusing on innovation and strategic positioning to capture emerging opportunities within each segment.

Regional Market Dynamics

The contact lenses market exhibits varied dynamics across regions, influenced by factors such as consumer behavior, regulatory environments, technological adoption, and economic conditions. North America, with its mature healthcare infrastructure and high consumer awareness regarding eye health, remains a significant contributor to market growth. This region benefits from a high prevalence of vision impairments, robust spending on healthcare, and a strong optometry network that facilitates widespread adoption of advanced contact lenses. The presence of leading players like Johnson & Johnson Vision and Bausch + Lomb further enhances the market's competitive edge in North America.

In Europe, regulatory frameworks such as the Medical Device Regulation (EU) 2017/745 shape the market by ensuring high standards of safety and efficacy for contact lenses. The region's emphasis on compliance and quality assurance fosters consumer trust and market expansion. Additionally, European countries demonstrate a growing preference for sustainable and technologically advanced products, aligning with trends towards silicone hydrogel lenses and smart contact lenses. Companies like Alcon and CooperVision leverage their technological innovations to meet these evolving demands, contributing to the region's steady market growth.

The Asia-Pacific region represents a burgeoning opportunity for the contact lenses market, driven by increasing urbanization, rising disposable incomes, and heightened awareness of vision correction solutions. China and India, in particular, are witnessing a surge in demand due to large populations with unmet vision needs and a growing middle class. However, the high regulatory scrutiny in China presents challenges for market entry and expansion, requiring companies to navigate complex approval processes. Despite these hurdles, the region's potential for growth remains significant, with manufacturers focusing on localized strategies and partnerships to tap into this dynamic market.

Emerging markets in Latin America and the Middle East & Africa also present growth opportunities, albeit at a slower pace. These regions are characterized by improving healthcare access and a gradual shift towards modern vision correction solutions. While infrastructure limitations and economic variability pose challenges, targeted marketing initiatives and educational campaigns about eye health could enhance market penetration. As these regions develop, strategic investments in distribution networks and local partnerships will be crucial for capturing new growth avenues.

Competitive Landscape

The competitive landscape of the contact lenses market is marked by a fragmented structure with high competitive intensity. Leading companies such as Johnson & Johnson Vision, Alcon, CooperVision, Bausch + Lomb, and Menicon dominate the market, leveraging their extensive R&D capabilities and robust product portfolios. Johnson & Johnson Vision's expertise in silicone hydrogel technology positions it as a leader in high-performance lenses, while Alcon's focus on precision and comfort through products like PRECISION1 for Astigmatism underscores its strategic emphasis on addressing specific consumer needs.

CooperVision's strength lies in its innovation in daily disposable lenses, catering to the rising demand for convenience and hygiene. Bausch + Lomb's comprehensive range of vision care products, including its ULTRA® ONE DAY lenses, highlights its commitment to enhancing consumer experience through advanced material science. Menicon, a leader in specialty lenses, capitalizes on its niche expertise to serve specific segments like orthokeratology, offering customized solutions for vision correction.

Strategic alliances, mergers, and acquisitions further characterize the competitive landscape, as companies seek to expand their market reach and capabilities. The acquisition of STAAR Surgical Company by Alcon, for instance, exemplifies a strategic move to enhance its surgical portfolio and strengthen its position in the ophthalmic industry. This consolidation trend is driven by the need to optimize resources, achieve economies of scale, and address evolving consumer preferences.

Barriers to entry remain significant due to stringent regulatory requirements and the need for substantial investment in R&D to develop innovative lens technologies. The market's technological and compliance constraints necessitate a high level of expertise and capital, providing established players with a competitive advantage. As a result, larger companies with established distribution networks and brand recognition continue to dominate, while smaller players focus on niche markets and specialized offerings to carve out their presence.

Strategic Outlook

The strategic outlook for the contact lenses market is shaped by the intersection of innovation, regulatory compliance, and consumer-centric strategies. As technological advancements continue to redefine product offerings, companies are investing in R&D to develop lenses that offer enhanced comfort, convenience, and health benefits. The integration of smart technologies, such as augmented reality features in contact lenses, presents opportunities for differentiation and premium pricing.

Regulatory compliance remains a critical focus, with manufacturers ensuring adherence to evolving safety and performance standards. The repeal of color additive regulations for FD&C Red No. 3, for example, underscores the importance of navigating regulatory changes and adapting product formulations accordingly. Companies that proactively align with regulatory shifts are better positioned to mitigate risks and capitalize on market opportunities.

Consumer preferences for sustainable and personalized solutions are driving market innovation. The rising demand for eco-friendly materials and packaging, along with advances in lens customization, reflects a broader trend towards individualized and environmentally conscious choices. Companies are leveraging digital platforms and AI-driven personalization to cater to these preferences, enhancing customer engagement and loyalty.

Strategic partnerships and collaborations are also pivotal in shaping the market's trajectory. By forming alliances with technology firms and healthcare providers, contact lens manufacturers can access new capabilities and expand their distribution networks. These collaborations facilitate the development of integrated vision care solutions that address a wider range of consumer needs.

Final Market Perspective

The contact lenses market is poised for sustained growth, driven by technological innovation, regulatory compliance, and evolving consumer preferences. As the market expands, companies that prioritize investment in R&D, strategic partnerships, and consumer-centric approaches will be well-positioned to capture emerging opportunities. The emphasis on sustainability, personalization, and advanced technologies will continue to shape product offerings, aligning with consumer demands for high-performance, eco-friendly, and customized solutions.

In conclusion, the contact lenses market's future trajectory is characterized by a dynamic interplay of innovation, regulation, and consumer trends. Companies that navigate these elements effectively, maintaining a focus on quality and compliance, are likely to secure a competitive advantage and drive long-term growth in this evolving industry.

Table of Contents

Table of Contents

- 1. Executive Summary

- 1.1 Market Forecast Snapshot (2026-2033)

- 1.2 Global Market Size & CAGR Analysis

- 1.3 Largest & Fastest-Growing Segments

- 1.4 Region-Level Leadership & Growth Trends

- 1.5 Key Market Drivers

- 1.6 Competitive Landscape Overview

- 1.7 Strategic Outlook Through 2033

- 2. Introduction & Market Overview

- 2.1 Definition of the Contact Lenses Market

- 2.2 Scope of the Study

- 2.3 Industry Evolution & Market Development

- 2.4 Supply Chain & Distribution Infrastructure

- 2.5 Impact of Consumer Trends

- 2.6 Sustainability & Regulatory Landscape

- 2.7 Technology & Innovation Landscape

- 3. Research Methodology

- 3.1 Primary Research

- 3.2 Secondary Research

- 3.3 Market Size Estimation Model

- 3.4 Forecast Assumptions (2026-2033)

- 3.5 Data Validation & Triangulation

- 4. Market Dynamics

- 4.1 Drivers

- 4.1.1 Increasing Demand Drivers

- 4.1.2 Industry Innovation Drivers

- 4.1.3 Market Expansion Factors

- 4.1.4 Regulatory or Policy Support

- 4.1.5 Technology Adoption Drivers

- 4.2 Restraints

- 4.2.1 Cost Constraints

- 4.2.2 Infrastructure Limitations

- 4.2.3 Regulatory Challenges

- 4.2.4 Market Awareness Barriers

- 4.3 Opportunities

- 4.3.1 Emerging Market Opportunities

- 4.3.2 Product Innovation Opportunities

- 4.3.3 Technology Expansion Opportunities

- 4.3.4 Supply Chain Improvements

- 4.4 Challenges

- 4.4.1 Supply Chain Complexity

- 4.4.2 Quality Control & Compliance

- 4.4.3 Regional Market Fragmentation

- 4.4.4 Competitive Pressure

- 4.1 Drivers

- 5. Contact Lenses Market Analysis (USD Billion), 2026-2033

- 5.1 Market Size Overview

- 5.2 CAGR Analysis

- 5.3 Regional Revenue Distribution

- 5.4 Segment Revenue Analysis

- 5.5 Distribution Channel Analysis

- 5.6 Consumer Impact Analysis

- 6. Market Segmentation (USD Billion), 2026-2033

- 6.1 By Wear Type

- 6.1.1 Daily Wear Lenses

- 6.1.1.1 Daily Disposable Lenses

- 6.1.1.1.1 Single Use Contact Lenses

- 6.1.1.1.1.1 Single Use Contact Lenses

- 6.1.1.1.1 Single Use Contact Lenses

- 6.1.1.1 Daily Disposable Lenses

- 6.1.2 Extended Wear Lenses

- 6.1.2.1 Weekly Wear Contact Lenses

- 6.1.2.1.1 Monthly Replacement Lenses

- 6.1.2.1.1.1 Monthly Replacement Lenses

- 6.1.2.1.1 Monthly Replacement Lenses

- 6.1.2.1 Weekly Wear Contact Lenses

- 6.1.3 Continuous Wear Lenses

- 6.1.3.1 Long Duration Wear Lenses

- 6.1.3.1.1 Continuous Oxygen Permeable Lenses

- 6.1.3.1.1.1 Continuous Oxygen Permeable Lenses

- 6.1.3.1.1 Continuous Oxygen Permeable Lenses

- 6.1.3.1 Long Duration Wear Lenses

- 6.1.1 Daily Wear Lenses

- 6.2 By Application

- 6.2.1 Therapeutic Applications

- 6.2.1.1 Keratoconus Management

- 6.2.1.1.1 Corneal Protection Lenses

- 6.2.1.1.1.1 Bandage Contact Lenses

- 6.2.1.1.1 Corneal Protection Lenses

- 6.2.1.1 Keratoconus Management

- 6.2.2 Cosmetic Vision Enhancement

- 6.2.2.1 Colored Contact Lenses

- 6.2.2.1.1 Decorative Contact Lenses

- 6.2.2.1.1.1 Fashion Contact Lenses

- 6.2.2.1.1 Decorative Contact Lenses

- 6.2.2.1 Colored Contact Lenses

- 6.2.3 Refractive Error Correction

- 6.2.3.1 Myopia Correction

- 6.2.3.1.1 Hyperopia Correction

- 6.2.3.1.1.1 Astigmatism Correction

- 6.2.3.1.1 Hyperopia Correction

- 6.2.3.1 Myopia Correction

- 6.2.1 Therapeutic Applications

- 6.3 By Product Type

- 6.3.1 Soft Contact Lenses

- 6.3.1.1 Daily Disposable Contact Lenses

- 6.3.1.1.1 Silicone Hydrogel Contact Lenses

- 6.3.1.1.1.1 Moisture Retention Soft Lenses

- 6.3.1.1.1 Silicone Hydrogel Contact Lenses

- 6.3.1.1 Daily Disposable Contact Lenses

- 6.3.2 Hybrid Contact Lenses

- 6.3.2.1 Soft Skirt Hybrid Lenses

- 6.3.2.1.1 RGP Center Hybrid Lenses

- 6.3.2.1.1.1 High Oxygen Hybrid Lenses

- 6.3.2.1.1 RGP Center Hybrid Lenses

- 6.3.2.1 Soft Skirt Hybrid Lenses

- 6.3.3 Specialty Contact Lenses

- 6.3.3.1 Toric Contact Lenses

- 6.3.3.1.1 Multifocal Contact Lenses

- 6.3.3.1.1.1 Orthokeratology Lenses

- 6.3.3.1.1 Multifocal Contact Lenses

- 6.3.3.1 Toric Contact Lenses

- 6.3.4 Rigid Gas Permeable Contact Lenses

- 6.3.4.1 Standard RGP Lenses

- 6.3.4.1.1 Fluoro-Silicone Acrylate Lenses

- 6.3.4.1.1.1 Oxygen Permeable RGP Lenses

- 6.3.4.1.1 Fluoro-Silicone Acrylate Lenses

- 6.3.4.1 Standard RGP Lenses

- 6.3.1 Soft Contact Lenses

- 6.4 By Material Type

- 6.4.1 Hydrogel Contact Lenses

- 6.4.2 Fluoro-Silicone Acrylate

- 6.4.3 Silicone Hydrogel Contact Lenses

- 6.5 By Distribution Channel

- 6.5.1 Online Sales Channels

- 6.5.2 Optical Retail Stores

- 6.5.3 Hospital & Clinical Distribution

- 6.1 By Wear Type

- 7. Market Segmentation by Geography

- 7.1 North America

- 7.2 Europe

- 7.3 Asia-Pacific

- 7.4 Latin America

- 7.5 Middle East & Africa

- 8. Competitive Landscape

- 8.1 Market Share Analysis

- 8.2 Product Portfolio Benchmarking

- 8.3 Product Positioning Mapping

- 8.4 Supply Chain & Distribution Partnerships

- 8.5 Competitive Intensity & Differentiation

- 9. Company Profiles

- 10. Strategic Intelligence & Pheonix AI Insights

- 10.1 Pheonix Demand Forecast Engine

- 10.2 Supply Chain & Infrastructure Analyzer

- 10.3 Technology & Innovation Tracker

- 10.4 Product Development Insights

- 10.5 Automated Porter’s Five Forces Analysis

- 11. Future Outlook & Strategic Recommendations

- 11.1 Emerging Market Expansion

- 11.2 Technology Innovation Strategies

- 11.3 Product Development Roadmap

- 11.4 Regional Expansion Strategies

- 11.5 Long-Term Market Outlook (2033+)

- 12. Appendix

- 13. About Pheonix Research

- 14. Disclaimer

Competitive Landscape

Competitive Landscape of the Global contact lenses market

Executive Framing

The competitive intensity and market structure within the contact lens industry from 2026 to 2033 are poised to play pivotal roles in shaping the industry’s future trajectory. This dimension is critical due to the dynamic interplay between fragmentation, strategic positioning, and competitive behavior among leading entities. The market’s fragmented nature, characterized by a high level of competitive intensity, means that companies must continuously innovate and differentiate their offerings to maintain or enhance their market positions. This environment encourages strategic alliances, mergers, and technological advancements, all of which are central to navigating and capitalizing on market opportunities. The competitive landscape is further defined by the presence of significant players such as Johnson & Johnson Vision, Alcon, CooperVision, and Bausch + Lomb, who are actively engaged in strategic maneuvers to secure their dominance. Understanding these dynamics is essential for stakeholders aiming to steer their strategies effectively in a rapidly evolving market.

Current Market Reality

The contact lens market is currently experiencing a high level of competitive intensity, driven by a fragmented market structure. This fragmentation is characterized by the presence of multiple players, with five Tier 1 companies—Johnson & Johnson Vision, Alcon, CooperVision, Bausch + Lomb, and Menicon—dominating the landscape. The competition among these entities is fierce, as they vie for market share through strategic initiatives such as product innovation, mergers and acquisitions, and alliances.

The market’s fragmentation is underscored by the constant introduction of new products and technologies. For example, Bausch Health Companies Inc. launched Bausch + Lomb ULTRA® ONE DAY in 2022, emphasizing the growing demand for daily disposable lenses. This product launch is indicative of the broader trend towards daily disposables, which are preferred by consumers for their convenience and hygiene benefits. Similarly, Alcon Inc.’s launch of PRECISION1 for Astigmatism in January 2021 highlights the industry’s focus on catering to specific vision correction needs, further intensifying competition.

In addition to product innovation, strategic alliances and mergers are pivotal in shaping the market structure. These moves are often driven by the need to enhance technological capabilities, expand market reach, and streamline operations. A notable example is the acquisition of a 10% stake in Ocumeda AG by ZEISS Vision Care in October 2025, a strategic move aimed at bolstering its position in the market through enhanced technological expertise.

The market is also characterized by significant regulatory and technological drivers. For example, Johnson & Johnson’s receipt of FDA approval for Acuvue Theravision with Ketotifen in 2022 represents a regulatory milestone that not only enhances the company’s product portfolio but also sets a precedent for innovation in contact lens technology.

Key Signals And Evidence

The narrative of the contact lens market is shaped by several key signals and evidence that highlight the ongoing competitive dynamics and market structure. One of the primary signals is the rising demand for daily disposable lenses, driven by increasing consumer preference for convenience and hygiene. This trend is evidenced by Bausch & Lomb’s launch of INFUSE for Astigmatism daily disposable contact lenses in 2024, which reflects the industry’s response to evolving consumer needs and the emphasis on product differentiation.

Technological advancements in lens manufacturing are another critical signal influencing the market. These advancements enable companies to offer innovative products that cater to specific consumer demands, such as lenses for astigmatism or myopia control. The launch of Bausch + Lomb INFUSE in August 2020 and Johnson & Johnson’s ACUVUE® OASYS MAX in September 2022 are prime examples of how companies leverage technology to enhance their product offerings and maintain a competitive edge.

Strategic moves such as mergers and acquisitions also play a significant role in shaping the market structure. In August 2025, Alcon Company’s intent to acquire STAAR Surgical Company signifies a strategic effort to expand its technological capabilities and product portfolio, thereby strengthening its competitive position. Such consolidation efforts are indicative of the broader trend towards strategic partnerships aimed at achieving synergies and enhancing market presence.

Moreover, regulatory developments have a profound impact on the competitive landscape. The FDA’s approval of new and innovative products, such as Johnson & Johnson’s Acuvue Theravision with Ketotifen, not only validates the efficacy and safety of these products but also encourages other players to invest in research and development to gain similar approvals. This regulatory environment fosters a culture of innovation and differentiation, further intensifying competition among market players.

In conclusion, the contact lens market is characterized by a fragmented structure and high competitive intensity, driven by product innovation, strategic alliances, technological advancements, and regulatory developments. These dynamics are critical in shaping the market’s future trajectory and determining the strategic positioning of key players. As companies navigate this complex landscape, their ability to adapt to changing consumer preferences, leverage technological advancements, and pursue strategic partnerships will be pivotal in sustaining their competitive edge.

Strategic Implications

The strategic implications of the current market structure and competitive dynamics in the contact lens industry are multifaceted and profound. Given the fragmented nature of the market and the high level of competitive intensity, stakeholders must adopt agile and innovative strategies to remain relevant and competitive. The presence of five Tier 1 players, including Johnson & Johnson Vision, Alcon, CooperVision, Bausch + Lomb, and Menicon, underscores the need for continuous differentiation and strategic agility.

One of the immediate strategic imperatives for these key players involves investment in research and development to drive innovation. The FDA approval of Johnson & Johnson’s Acuvue Theravision with Ketotifen is a testament to the competitive advantage that can be gained through innovative product offerings. This product not only addresses the dual needs of vision correction and allergy relief but also sets a precedent for combining therapeutic benefits with traditional contact lens functionalities. Other companies, therefore, must consider investing in similar multifaceted products to tap into niche segments and strengthen their market positions.

Furthermore, the strategic alliances and mergers observed in the market signal a trend towards consolidation as a means to enhance market share and operational efficiencies. Alcon’s announced intent to acquire STAAR Surgical Company in August 2025 exemplifies how strategic acquisitions can be leveraged to enhance technological capabilities and expand product portfolios. Such moves can also provide access to new markets and customer bases, thereby fostering growth in a highly competitive environment. Companies that fail to engage in strategic partnerships or acquisitions may find themselves at a disadvantage, lacking the scale and resources needed to compete effectively.

As the market shifts towards daily disposable lenses, companies must also prioritize the development of sustainable and cost-effective manufacturing processes. The rising demand for convenience and hygiene, coupled with technological advancements in lens materials, presents opportunities for players to differentiate through sustainability. For instance, the growing acceptance of daily disposable silicone hydrogel lenses indicates a consumer preference for products that offer both comfort and health benefits. Companies that can innovate in this area, perhaps by incorporating eco-friendly materials or reducing production waste, will likely gain a competitive edge and appeal to environmentally conscious consumers.

Forward Outlook

Looking forward to the 2026-2033 forecast period, the contact lens industry is expected to witness continued evolution in market structure and competitive dynamics. The fragmented nature of the market is likely to persist, with ongoing innovation and strategic maneuvers shaping the competitive landscape. Companies that excel in adapting to consumer trends, such as the increased adoption of daily disposable and myopia control lenses, will be better positioned to capitalize on growth opportunities.

The strategic implications of rising e-commerce channels cannot be overstated. As more consumers turn to online platforms for their contact lens purchases, companies must enhance their digital presence and streamline their supply chains to ensure timely and cost-effective distribution. This shift towards e-commerce is not only a response to consumer preferences but also a strategic necessity in a market where convenience and accessibility are paramount.

In terms of technological advancements, the industry is poised for further innovation in lens materials and manufacturing processes. As companies continue to invest in research and development, we can expect to see new products that offer enhanced comfort, clearer vision, and additional health benefits. These innovations will likely drive competitiveness, encouraging players to differentiate through unique product offerings and customer experiences.

Finally, regulatory developments will play a crucial role in shaping market dynamics. Strict government regulations for the approval of contact lenses, while presenting challenges, also offer opportunities for differentiation through compliance and quality assurance. Companies that can navigate these regulatory landscapes effectively will not only gain consumer trust but also set industry standards for safety and efficacy.

In conclusion, the contact lens industry is set for a dynamic future characterized by technological innovation, strategic consolidation, and evolving consumer preferences. As companies navigate this complex landscape, their ability to adapt and innovate will be critical in maintaining competitive advantage and driving long-term success. Those who can anticipate market trends and respond proactively will emerge as leaders in this highly competitive and ever-evolving market.

Value Chain

Global contact lens market :Value Chain & Market Dynamics

Executive Framing

In the contact lens market, the value chain is an intricate web of production, regulation, distribution, and consumer interaction. The dynamics of this chain are undergoing significant changes, driven by evolving consumer preferences, stringent regulatory environments, and the ongoing push for innovation by manufacturers. Understanding the value chain’s current state and anticipating its future evolution is critical for stakeholders, as it influences everything from production costs to market positioning and competitive advantage.

The contact lens industry operates within a hybrid operational and distribution model, where manufacturers must navigate a moderate level of supply chain complexity. Bottlenecks such as the risk of infection associated with contact lens wear and strict government regulations for product approval present substantial challenges. These hurdles impact the entire value chain, from raw material sourcing and manufacturing to marketing and end-user delivery. Furthermore, the high regulatory environment, particularly in China, imposes additional constraints, affecting the pace and scope of market expansion.

Current Market Reality

The contact lens market is characterized by a growing preference for lenses over traditional spectacles. This shift is fueled by cultural preferences for discreet vision correction and an increasing awareness of the long-term cost efficiency of contact lenses. Companies like Bausch & Lomb and Johnson & Johnson have been at the forefront, innovating and expanding their product offerings to meet consumer demand. For instance, Johnson & Johnson’s FDA-approved Acuvue Theravision with Ketotifen and Bausch & Lomb’s launch of INFUSE for Astigmatism highlight the industry’s focus on enhancing product efficacy and consumer satisfaction.

However, this burgeoning demand is met with significant regulatory hurdles. Strict government regulations for the approval of contact lenses create a bottleneck that can delay product launches and increase compliance costs. This regulatory landscape is particularly stringent in China, where high regulation levels can impact market entry and expansion strategies for international players. The complexity of navigating these regulations affects the entire value chain, from research and development to distribution and retail.

Moreover, the risk of infection associated with contact lens wear remains a critical concern, influencing consumer perception and regulatory scrutiny. Manufacturers must invest in research and development to mitigate these risks, often resulting in higher production costs and extended timelines for product approval. This, in turn, affects the pricing strategies and profit margins across the value chain.

Key Signals And Evidence

The contact lens market is experiencing a clear shift, influenced by several critical signals. One of the most prominent is the increasing marketing and promotional activities by manufacturers to capture a larger market share. Companies are investing heavily in marketing campaigns to educate consumers about the benefits of contact lenses over traditional spectacles, emphasizing aspects like cultural preferences for discreet vision correction and personal aesthetics.

The growing preference for contact lenses is further supported by the increasing incidences of vision impairments, which drive demand for more effective and convenient vision correction solutions. This trend is reflected in the actions of companies like Bausch & Lomb and Alcon, which have launched new products and pursued strategic acquisitions to enhance their market presence. For instance, Alcon’s announcement of its intent to acquire STAAR Surgical Company underscores the strategic moves being made to consolidate market position and expand product portfolios.

However, the extended adaptation period required for rigid gas permeable (RGP) lenses presents a challenge within the value chain. The limited availability of comprehensive RGP services and the higher initial costs compared to soft lenses can deter consumers, impacting demand and market penetration. This bottleneck requires strategic adjustments at various stages of the value chain to ensure that consumer needs are met without compromising on cost efficiency or product accessibility.

As the market evolves, the strategic implications of these signals are profound. Companies must navigate a complex landscape of regulatory challenges, consumer preferences, and competitive pressures. The ability to effectively manage these dynamics will determine the success or failure of market players in capturing and sustaining a competitive edge in the rapidly evolving contact lens market.

Strategic Implications

The strategic implications of these key signals are manifold and demand careful consideration by stakeholders across the contact lens value chain. As regulatory landscapes tighten, companies must invest in robust compliance strategies and maintain strong relationships with regulatory bodies to ensure seamless product approvals. This will likely drive up operational costs but can also serve as a competitive advantage for companies that successfully navigate these hurdles.

Consumer preferences are shifting toward more personalized and aesthetically pleasing vision solutions, prompting companies to innovate and diversify their product offerings. This necessitates significant investment in research and development to create lenses that not only meet regulatory standards but also align with consumer desires for comfort, convenience, and style. The successful launch of daily disposable lenses by Bausch + Lomb and others illustrates a strategic pivot towards products that cater to modern consumer lifestyles.

Moreover, China’s high regulation poses both a challenge and an opportunity – companies that leverage local partnerships and tailor strategies to the market’s unique demands may find growth, but this requires understanding local regulations and consumer behavior, which is resource-intensive. The risk of infection with contact lens wear necessitates a dual focus on product innovation and consumer education; companies must develop safe materials and solutions while educating on proper lens care, enhancing trust and mitigating liabilities.

Finally, the extended adaptation period for RGP lenses highlights the need for comprehensive consumer support services. Companies must enhance their service offerings to include personalized fitting consultations, educational resources, and ongoing customer support to facilitate a smoother transition for RGP lens users. This can enhance customer satisfaction and foster brand loyalty, ultimately driving market penetration.

Forward Outlook

Looking ahead to the forecast period of 2026-2033, the contact lens market is poised to undergo significant transformation. The interplay of regulatory constraints, consumer preferences, and competitive dynamics will continue to shape the value chain, creating both challenges and opportunities for market participants.

Regulatory pressures will likely intensify, prompting companies to refine their compliance strategies and streamline their approval processes. This could lead to increased consolidation within the industry, as smaller players may struggle to meet the stringent requirements and opt for mergers or acquisitions with larger, more established companies. Such consolidation could result in a more concentrated market, with a few dominant players wielding significant influence over pricing and product availability.

Consumer preferences will continue to evolve, driven by advancements in lens technology and changing lifestyle trends. As manufacturers invest in developing lenses that offer superior comfort, convenience, and aesthetics, we can expect a surge in demand for premium and specialized lenses. This shift will likely drive up average selling prices and improve margins for companies that successfully capitalize on these trends.

In China, high regulation will remain a critical factor influencing market dynamics. Companies that can navigate the complex regulatory environment and adapt their strategies to meet local demands stand to gain a significant competitive advantage. However, this requires a long-term commitment to understanding the intricacies of the Chinese market and investing in localized operations.

The risk of infection will continue to be a focal point of innovation and consumer education. As new materials and solutions emerge to address this concern, companies that prioritize health and safety in their product development and marketing strategies will be well-positioned to capture consumer trust and loyalty.

Overall, the contact lens market is on the cusp of a transformative period characterized by regulatory challenges, shifting consumer preferences, and strategic realignment. Companies that can effectively navigate these dynamics while maintaining a focus on innovation and consumer satisfaction will be best positioned to thrive in this evolving landscape. The stakes are high, but so are the opportunities for those who can anticipate and adapt to the changing tides of the contact lens value chain.

Investment Activity

Investment & Funding Dynamics in the Global contact lenses market

Executive Framing

In the rapidly evolving landscape of the contact lenses market, the dynamics of investment and funding are pivotal in shaping the industry’s future. As we look towards the forecast period of 2026-2033, it becomes increasingly critical to understand how capital flows and strategic allocations are influencing market structures. The contact lenses sector is not only a hub for innovation but also a focal point for strategic investments driven by emerging trends in consumer preferences and technological advancements.

The investment trend direction within this market is on the rise, characterized by a medium level of capital intensity and significant recent mergers and acquisitions (M&A) activity. This environment presents a unique opportunity for investors to align their portfolios with trends such as clean beauty, sustainable products, and the convergence of healthcare and cosmetics. The presence of active investors like L’Oréal, Estée Lauder Companies, and Electric Feel Ventures indicates a strong interest in capitalizing on these themes.

Current Market Reality

The current state of the contact lenses market reflects a dynamic interplay between investment drivers and market realities. Recent M&A activity, such as Alcon Company’s announcement to acquire STAAR Surgical Company in August 2025, underscores the strategic maneuvers being undertaken to capture emerging opportunities. This move highlights the importance of expanding product portfolios and leveraging synergies between eye care and advanced lens technologies.

Moreover, companies like Bausch & Lomb and Johnson & Johnson have been at the forefront of innovation, with new product launches and FDA approvals. For instance, Bausch & Lomb’s INFUSE for Astigmatism daily disposable contact lenses, launched in 2024, exemplifies the industry’s commitment to addressing specific consumer needs while maintaining regulatory compliance. Similarly, Johnson & Johnson’s FDA-approved Acuvue Theravision with Ketotifen provides a glimpse into the future of therapeutic lenses that cater to both vision correction and allergy relief.

Investment themes such as clean beauty and sustainable products are gaining traction, driven by increased consumer demand for natural ingredients and environmentally friendly solutions. This shift is supported by signals like the growing interest in private equity investments and the expansion of regulatory requirements, which are reshaping the competitive landscape. Such developments not only impact product offerings but also influence corporate strategies, as evidenced by the actions of companies like L’Oréal and Coty, which are actively seeking to integrate sustainability into their business models.

Key Signals And Evidence

The investment landscape in the contact lenses market is shaped by several key signals that highlight the strategic directions being pursued by stakeholders. A growing interest in private equity investments is a notable trend, as investors seek to capitalize on the convergence of healthcare, cosmetics, and technology. This interest is further fueled by the expansion of regulatory requirements, which necessitate compliance and innovation in product design and manufacturing processes.

Social commerce expansion is another critical signal, reflecting the shift towards digital platforms and direct-to-consumer models. This trend is driven by the rising prevalence of e-commerce and the growing demand for convenience and comfort among consumers. As social commerce becomes more integrated into the shopping experience, companies are leveraging digital channels to enhance customer engagement and streamline distribution.

The increased demand for non-invasive monitoring tools is reshaping the contact lenses market, with technological advancements in lens materials playing a pivotal role. These innovations are enabling the development of lenses that offer enhanced functionality, such as real-time health monitoring and personalized vision correction. As regulatory support for wearable medical devices continues to grow, the market is witnessing a proliferation of products that bridge the gap between medical and consumer applications.

The heightened consumer demand for natural ingredients is a driving force behind the clean beauty and sustainable products movement. This demand is not only influencing product formulations but also prompting companies to adopt eco-friendly practices throughout their supply chains. As a result, investors are increasingly drawn to brands that prioritize sustainability and ethical sourcing.

Strategically, these signals indicate a shift towards a more integrated approach to eye care, where the lines between healthcare, cosmetics, and technology are increasingly blurred. The market’s response to these trends is evident in the actions of key players, who are investing in R&D, expanding their product offerings, and exploring new business models to stay competitive.

In summary, the investment and funding dynamics in the contact lenses market are being reshaped by a confluence of factors, including regulatory changes, technological advancements, and evolving consumer preferences. These dynamics are driving strategic decisions and influencing the allocation of capital, ultimately shaping the future of the industry. As we delve deeper into the implications of these developments, it becomes clear that stakeholders must navigate a complex landscape to capitalize on emerging opportunities and mitigate potential risks.

Strategic Implications

1. Emphasis on Technological Integration

Technological advancements, particularly in lens materials and AI-driven personalization, are reshaping the contact lenses market. This shift necessitates substantial investment in R&D to develop products that not only meet consumer demand for functionality and comfort but also align with regulatory requirements. Companies like Bausch & Lomb and Johnson & Johnson, with their recent product launches such as INFUSE for Astigmatism and Acuvue Theravision, are exemplifying the market’s pivot towards innovative solutions. This focus on technology is driving a need for strategic partnerships and collaborations, particularly with tech firms, to leverage expertise and enhance product offerings.

Implication: To remain competitive, companies must allocate capital towards innovative R&D and forge strategic alliances with technology partners. This approach can help in delivering cutting-edge products that meet regulatory standards and consumer expectations, ultimately capturing a larger market share.

2. Regulatory Compliance and Market Access

The expansion of regulatory requirements is a critical factor that companies must navigate. As regulatory bodies impose stricter standards, particularly concerning product safety and environmental impact, companies are compelled to invest in compliance measures. The increased regulatory support for wearable medical devices presents both a challenge and an opportunity. Companies that can swiftly adapt to these changes and achieve compliance will gain a significant advantage in market access and consumer trust.

Implication: To capitalize on this, stakeholders must enhance their regulatory strategies, investing in compliance infrastructure that ensures swift adaptation to new regulations. This proactive approach will not only mitigate risks associated with non-compliance but also position companies as leaders in regulatory adherence, fostering consumer confidence and loyalty.

3. Rising Consumer Demand for Sustainability and Natural Ingredients

The growing consumer preference for sustainable products and natural ingredients is reshaping investment priorities. Active investors like L’Oréal and Estée Lauder Companies are channeling capital into clean beauty and sustainable product lines, reflecting this trend. This shift is not merely a reaction to consumer demand but a strategic realignment towards long-term sustainability goals.

Implication: Companies must prioritize sustainable practices and natural ingredient sourcing in their product development strategies. This requires strategic investments in sustainable supply chains and production processes, which can enhance brand reputation and attract environmentally conscious consumers. Additionally, aligning with sustainability trends can open up new market segments and drive revenue growth.

4. Social Commerce and Direct-to-Consumer Models

The expansion of social commerce and direct-to-consumer (DTC) models is revolutionizing how contact lenses are marketed and sold. With increased e-commerce penetration, consumers are seeking more personalized and convenient purchasing experiences. This shift is prompting companies to invest in digital transformation and e-commerce capabilities, as evidenced by the rise of digitally native brands and consumer technology integration.

Implication: Companies that effectively leverage social commerce platforms and DTC models can enhance customer engagement and drive sales growth. Strategic investments in digital marketing, personalized customer experiences, and robust e-commerce infrastructure are essential to capitalize on this trend. Firms must also focus on data analytics to understand consumer behaviors and preferences, enabling targeted marketing strategies.

Forward Outlook

1. Increased Private Equity Interest

The growing interest in private equity investments is expected to bring significant capital inflows into the contact lenses sector. Private equity firms are likely to target companies that demonstrate strong growth potential, innovative product offerings, and robust market positions. This influx of capital will enable companies to accelerate R&D efforts, expand market reach, and enhance operational efficiencies.

Outlook: Companies should prepare for increased competition for private equity funding by strengthening their market positions and showcasing their growth trajectories. Successful firms will be those that can articulate a compelling value proposition to attract private equity investments, facilitating rapid expansion and innovation.

2. Continued Emphasis on Regulatory Adaptation

As regulatory landscapes continue to evolve, companies must remain vigilant in adapting to new requirements. The emphasis on regulatory compliance will drive strategic investments in quality assurance and compliance infrastructure, ensuring that products meet the highest standards of safety and efficacy.

Outlook: Firms that proactively engage with regulatory bodies and invest in compliance will not only mitigate risks but also gain a competitive edge in market access and consumer trust. This strategic focus on regulatory adaptation will be crucial in navigating the complex landscape of the contact lenses market.

3. Expansion of Sustainable and Personalized Product Offerings

The demand for sustainable and personalized products will continue to grow, driving companies to innovate and diversify their product portfolios. Investments in sustainability and personalization will be key differentiators, as consumers increasingly seek products that align with their values and lifestyle preferences.

Outlook: Companies that lead in sustainability and personalization will capture a larger share of the market, benefiting from increased consumer loyalty and brand equity. Strategic investments in these areas will not only drive revenue growth but also position firms as leaders in the evolving contact lenses sector.

In conclusion, the contact lenses market is undergoing a significant transformation driven by technological innovation, regulatory changes, and shifting consumer preferences. The strategic implications of these developments are profound, necessitating careful consideration of investment and funding dynamics. Stakeholders must navigate this complex landscape with agility and foresight, leveraging strategic investments to capitalize on emerging opportunities and mitigate potential risks. As the market continues to evolve, those who align their strategies with these key drivers will be best positioned to thrive in the competitive contact lenses industry.

Technology & Innovation

Global contact lens market :Technology & Innovation

Executive Framing

The contact lens market is experiencing a dynamic shift driven by technological innovation and evolving consumer needs. The technology and innovation landscape within this market dimension is critical for several reasons. With the growing complexity of consumer demands for enhanced vision solutions and comfort, there is a continuous push towards integrating advanced materials and smart technologies into contact lenses. This dimension is particularly important now due to the convergence of several high-impact factors, including the adoption of smart technologies, the expansion of healthcare capabilities, and the increasing demand for personalized vision correction solutions. As the market shifts from traditional corrective lenses to more advanced offerings, understanding the technological landscape becomes imperative for stakeholders looking to navigate and leverage these changes effectively.

Innovation intensity in the contact lens space is high, fueled by moderate patent activity and a market that is in the growth stage of technology maturity. Companies like Johnson & Johnson, Bausch & Lomb, CooperVision, and emerging players such as TheiaNova and Epion Therapeutics are at the forefront, pushing the boundaries of what contact lenses can achieve. Key technologies such as silicone hydrogel, smart contact lenses, moisture-retaining materials, and blue light-blocking lenses are not only redefining product capabilities but are also reshaping consumer expectations. These innovations are designed to enhance comfort, improve vision clarity, and address specific consumer needs, such as UV protection and digital eye strain from prolonged screen exposure.

Current Market Reality

The present state of the contact lens market is characterized by notable advancements in lens technology and a shift in consumer preferences towards more specialized solutions. Johnson & Johnson’s FDA approval for Acuvue Theravision with Ketotifen in 2022 exemplifies the industry’s move towards multifunctional lenses that cater to specific medical needs, such as allergy relief. Similarly, Bausch & Lomb’s launch of INFUSE for Astigmatism daily disposable contact lenses in 2024 highlights the ongoing trend towards daily disposables that offer convenience and hygiene benefits, crucial in a post-pandemic world.

The market is experiencing a surge in demand for lenses that offer both corrective and protective functions. This is evidenced by the increasing popularity of blue light-blocking and UV-blocking contact lenses, which cater to the modern lifestyle’s demands, particularly with the rise in digital device usage. Companies are also investing in technologies that enhance lens comfort and hydration, such as Wetting agents and TearStable Technology, to address common issues like dry eye syndrome, which affects a significant portion of lens wearers.

Furthermore, the approval of corneal cross-linking and Epioxa by the FDA indicates a regulatory environment that is supportive of innovative treatment options. This is crucial for the development and adoption of new contact lens technologies that promise improved health outcomes and personalized treatment approaches. The clinical success rates associated with these advancements, such as the 90% graft survival rate for PK at 5 years and the rapid improvement in vision post-corneal transplantation, underscore the tangible benefits of integrating cutting-edge technologies into ocular healthcare.

Key Signals And Evidence

Strategic Implications

The technological advancements and market signals discussed above have profound strategic implications for stakeholders within the contact lens industry. For manufacturers, the integration of advanced materials and smart technologies into contact lenses presents a dual opportunity: to differentiate their products in a competitive market and to address the growing consumer demand for multifunctional eyewear. Companies that invest in research and development to innovate new product features are likely to capture a significant share of the market, particularly among tech-savvy consumers.

For healthcare providers, these advancements necessitate a shift in how eye care is delivered. The availability of more sophisticated diagnostic tools and personalized treatment options means that providers must stay informed about the latest technologies to offer the best possible care. This could lead to increased collaboration between eye care professionals and technology companies, fostering a more integrated approach to vision health.

Retailers, on the other hand, must adapt their sales strategies to accommodate the growing range of technologically advanced contact lenses. As consumers become more informed and demanding, retailers will need to provide comprehensive information and guidance on the benefits of smart lenses and other innovative products. This may also involve investing in training for staff to ensure they can adequately support and educate customers.

From a regulatory perspective, the approval of new technologies such as corneal cross-linking sets a precedent for future innovations. Regulatory bodies will need to balance the need for rigorous safety standards with the desire to foster innovation and expedite the approval of new technologies that can significantly benefit public health.

Forward Outlook

Looking ahead, the contact lens market is poised for continued growth and transformation driven by technological innovation. As smart technologies become more prevalent, we can expect to see a wider adoption of smart contact lenses that offer features beyond traditional vision correction. These lenses may include functionalities such as health monitoring, augmented reality, and seamless integration with digital ecosystems.

The focus on personalized treatment approaches is likely to intensify, with companies leveraging AI and other technologies to offer highly customized solutions tailored to individual patient needs. This trend will enhance patient satisfaction and improve clinical outcomes, as lenses are optimized for each user’s unique ocular characteristics. Additionally, the expansion of smart city infrastructure will create opportunities for contact lenses that interact with urban technology systems, blurring the lines between personal health devices and wearable tech.

In conclusion, the technology and innovation landscape within the contact lens market is set to redefine the industry over the coming years. Stakeholders must remain agile and forward-thinking, leveraging technological advancements to meet evolving consumer needs and capitalize on emerging opportunities. By doing so, they can ensure their place at the forefront of this dynamic and rapidly evolving market.

Market Risk

Global contact lenses market: Structural Constraints & Market Impacts

Executive Framing

In the competitive landscape of the contact lens market, understanding the intricate dynamics of structural constraints and market impact is critical. This dimension is highly relevant now, as it underscores potential vulnerabilities that could disrupt market stability and influence the strategic decisions of key players. As the market navigates a moderate overall risk level, with specific threats such as corneal infections and dry eye syndrome looming, stakeholders must grapple with these challenges to maintain operational resilience and competitive advantage.

The contact lens market’s structural risks are compounded by the potential for substitution, which remains moderate. This suggests that consumers might pivot to alternative solutions if the risks associated with contact lens use outweigh the perceived benefits. Furthermore, the geopolitical exposure level is low, indicating that while international tensions might not significantly impact the market, localized issues could still pose threats. This nuanced risk profile necessitates a strategic approach to mitigate potential disruptions and safeguard market integrity.

Current Market Reality

The current state of the contact lens market is shaped by a complex interplay of risk factors, consumer behavior, and regulatory actions. Companies like Bausch & Lomb and Johnson & Johnson are at the forefront, actively engaging in product launches and innovations to address prevalent issues such as corneal infections and irritation. Bausch & Lomb’s launch of INFUSE for Astigmatism daily disposable contact lenses in 2024, along with Johnson & Johnson’s FDA-approved Acuvue Theravision with Ketotifen in 2022, exemplify proactive measures to enhance product offerings and meet evolving consumer needs.

Despite these advancements, the market is not without its challenges. The prevalence of risk factors such as bacterial keratitis, protein deposits, and corneal ulcers underscores the importance of rigorous hygiene practices and regular eye check-ups. These health-related risks not only affect consumer confidence but also impact the demand elasticity of contact lenses. As consumers become increasingly aware of potential health implications, their purchasing decisions may sway towards products perceived as safer or more reliable.

Additionally, the market faces operational vulnerabilities stemming from administrative barriers and provider hesitancy. The cautious approach of healthcare providers regarding biosimilars and the potential for market manipulation by Pharmacy Benefit Managers (PBMs) contribute to a complex regulatory environment. These factors can influence pricing dynamics and affect the market’s overall stability, as companies must navigate these hurdles to ensure consistent supply and competitive pricing strategies.

Key Signals And Evidence

The contact lens market is experiencing a shift driven by several key signals, which collectively highlight underlying structural risks and market impacts. One of the most significant signals is the expansion of public and private charging networks, which, while primarily associated with the automotive sector, serves as a metaphor for the increasing demand for infrastructure that supports safe and reliable product use. Just as electric vehicles require robust charging networks, contact lenses necessitate a comprehensive framework for safe usage, including excellent hygiene practices and adherence to lens replacement schedules.

Barriers to technology adoption also play a crucial role in shaping the market’s trajectory. The hesitancy among providers and patients regarding new contact lens technologies can stifle innovation and slow market penetration. This is further compounded by inadequate safety investments, which can erode consumer trust and limit the market’s growth potential. Transparency in pricing, another critical signal, directly influences consumer perceptions and purchasing behaviors. As companies strive to offer competitive pricing, the need for clear and consistent pricing strategies becomes paramount to maintaining consumer loyalty and market share.

Moreover, advancements in hybrid technology improving durability, although primarily linked to the automotive industry, offer valuable insights into the contact lens market. The emphasis on improved reliability and durability is mirrored in the contact lens sector, where companies are investing in research and development to enhance product longevity and reduce the incidence of complications such as dryness and irritation.

Entities like Alcon Company, which announced its intent to acquire STAAR Surgical Company in August 2025, are actively engaged in strategic maneuvers that reflect the market’s evolving landscape. Such acquisitions signal a consolidation trend, where companies seek to bolster their market positions and expand their product portfolios to address emerging risks and opportunities.

In conclusion, the contact lens market is navigating a complex risk environment characterized by health-related concerns, regulatory challenges, and consumer behavior shifts. As companies like Bausch & Lomb and Johnson & Johnson continue to innovate and adapt, the market must remain vigilant in addressing structural risks and leveraging strategic opportunities to sustain growth and resilience.

Strategic Implications

The landscape of the contact lens market is shifting, influenced by a blend of health risks, technological advancements, and strategic corporate maneuvers. Companies operating within this sector must consider several key implications as they navigate these changes. Firstly, the moderate substitution risk level suggests that companies need to focus on differentiating their products to maintain market share. The introduction of innovative products like Bausch & Lomb’s INFUSE for Astigmatism and Johnson & Johnson’s Acuvue Theravision with Ketotifen indicates a strategic pivot towards addressing specific consumer needs and enhancing product efficacy. These innovations are not just about meeting consumer demand but also about preemptively tackling health risks such as corneal infections and dry eye syndrome, which can deter contact lens use.

The strategic decision by Alcon to acquire STAAR Surgical Company underscores a significant trend towards consolidation in the industry. This move is indicative of a broader strategy where companies seek to diversify their product offerings and strengthen their market position. Such consolidations can enhance operational resilience by pooling resources and expertise, thereby mitigating the impact of potential disruptions. However, this strategy also necessitates careful integration planning to ensure that the expanded operations do not introduce new vulnerabilities, such as supply chain disruptions or cultural misalignments within the merged entities.

As companies innovate and expand, the importance of transparency in pricing cannot be overstated. With increased competition and consumer awareness, pricing strategies will need to be more transparent to build trust and loyalty. This transparency is crucial in maintaining pricing power, especially in a market where consumers have access to a wide range of options. Moreover, the trend towards regulatory scrutiny in healthcare means that opaque pricing strategies might attract unwanted attention and potential penalties, further impacting profitability.

Another strategic implication is the ongoing need for companies to invest in safety technologies and adhere to stringent hygiene practices. As evidenced by the risk factors highlighted, such as bacterial keratitis and protein deposits, maintaining high safety standards is essential for building consumer confidence and avoiding legal liabilities. Regular eye exams and proper lens hygiene are not just consumer responsibilities; they are integral to the value proposition of contact lens manufacturers. Companies that can effectively communicate the importance of these practices and integrate them into their brand messaging will likely see enhanced customer retention.

Forward Outlook

Looking ahead, the contact lens market is poised to navigate a complex interplay of risks and opportunities. The medium-term outlook suggests that companies will continue to face challenges related to health risks and consumer behavior shifts. However, those that can strategically leverage technological advancements and consolidate their market positions are likely to thrive. The expansion of public and private charging networks, while primarily relevant to the automotive sector, metaphorically underscores the necessity for robust infrastructure development in the contact lens industry, particularly in terms of distribution and supply chain resilience.

Moreover, as hybrid technology advancements in other sectors highlight improved reliability and durability, the contact lens industry can draw parallels in enhancing the longevity and safety of their products. This focus on durability and safety will be crucial in addressing consumer concerns and differentiating products in a crowded market. Companies that invest in research and development to reduce the incidence of complications like dryness and irritation will be better positioned to capture market share.

In conclusion, the contact lens market’s trajectory from 2026 to 2033 will be shaped by a confluence of strategic decisions, technological innovations, and consumer-centric approaches. While the path is fraught with risks, the potential for growth and resilience is substantial for those who navigate these challenges with foresight and agility. As companies like Bausch & Lomb and Alcon continue to adapt and innovate, the market will need to remain vigilant in addressing structural risks and leveraging strategic opportunities to sustain growth and resilience.

Regulatory Landscape

Global contact lens market : Regulatory & Policy Environment

Executive Framing

The regulatory and policy environment surrounding the contact lens market is more than just a backdrop; it is a powerful driver that shapes how companies operate, innovate, and compete. As we look forward to the period from 2026 to 2033, understanding this dimension becomes crucial for stakeholders across the sector. The regulatory landscape is undergoing significant changes, with a focus on color additive regulations, Medical Device Regulation (EU) 2017/745, and FDA guidelines that collectively redefine market boundaries, compliance costs, and entry barriers.

These regulatory shifts are not mere formalities. They carry the potential to alter the competitive dynamics by influencing the timelines for product approvals, the cost of compliance, and the strategic decisions companies make. For instance, the FDA’s repeal of color additive regulations for FD&C Red No. 3 and the expansion of approved natural colorings signal a move towards more stringent safety standards, potentially affecting manufacturing processes and supply chains. Moreover, the Medical Device Regulation (EU) 2017/745 introduces a new layer of compliance requirements that could redefine market entry strategies for companies operating in or entering the European market.

These regulatory developments demand careful attention from industry players, as they will have to navigate a complex web of policies that not only dictate what products can be brought to market but also how they are produced and marketed. Failure to comply could lead to significant financial and reputational risks, making regulatory strategy a critical component of corporate planning.

Current Market Reality

The contact lens market is currently navigating a series of regulatory transformations that have significant implications for both existing players and new entrants. At the forefront is the FDA’s evolving stance on color additives, which is reshaping product development processes across the industry. The FDA has signaled its intention to phase out certain synthetic dyes, such as those containing FD&C Red No. 3, in favor of safer, natural alternatives. This shift not only affects the formulation of contact lenses but also aligns with broader consumer trends favoring transparency and safety in product ingredients.

Companies like Bausch & Lomb and Johnson & Johnson, which have historically been at the forefront of contact lens innovation, are now tasked with ensuring compliance with these new regulations. For example, Bausch & Lomb’s recent FDA approval for daily disposable contact lenses underscores the importance of aligning product development with regulatory expectations. Similarly, Johnson & Johnson’s Acuvue Theravision with Ketotifen, approved in 2022, highlights the need for companies to integrate new regulatory requirements into their research and development pipelines early on.

The Medical Device Regulation (EU) 2017/745 further complicates the regulatory landscape for companies operating in the European Union. This regulation mandates stricter requirements for clinical evaluations and post-market surveillance, thereby increasing the burden of compliance for manufacturers. As a result, companies must now invest more heavily in regulatory affairs and compliance departments to ensure adherence to these rigorous standards.

Moreover, the FDA’s approval process for color additives, which requires specific approval for intended use and batch certification, adds another layer of complexity. Companies must navigate these stringent requirements to market their products legally, impacting everything from product design to marketing strategies. The FDA’s draft guidance on color additives and the expansion of approved natural colorings demonstrate the agency’s commitment to enhancing product safety while also encouraging innovation within set boundaries.

Key Signals And Evidence

Several key signals within the regulatory and policy environment are shaping the contact lens market’s trajectory. These signals provide insight into how companies must adapt to remain competitive and compliant.

1. Repeal of Color Additive Regulations for FD&C Red No. 3: The FDA’s decision to repeal regulations related to FD&C Red No. 3 marks a significant shift in how color additives are perceived and utilized in contact lenses. This repeal is part of a broader move to phase out petroleum-based synthetic dyes, which are increasingly scrutinized for their potential health risks. The implication for manufacturers is clear: there is a pressing need to reformulate products to exclude these additives and seek FDA approval for alternative, safer ingredients. This regulatory change underscores the importance of proactive compliance and innovation in product formulation.

2. Medical Device Regulation (EU) 2017/745: The introduction of this regulation has fundamentally altered the landscape for medical device manufacturers in the EU, including those producing contact lenses. It demands more comprehensive documentation, rigorous clinical evaluations, and enhanced post-market surveillance. For companies, this means longer lead times for product approvals and increased costs associated with compliance. The regulation effectively raises the barriers to entry for new players and could potentially lead to market consolidation as smaller companies struggle to meet these demanding requirements.

3. FDA’s Expansion of Approved Natural Colorings: In response to growing consumer demand for safer products, the FDA has expanded its list of approved natural colorings. This move aligns with the agency’s commitment to promoting public health while supporting industry innovation. For companies, this presents an opportunity to differentiate their products by emphasizing the use of natural ingredients. However, it also requires investment in research and development to identify suitable natural alternatives that meet both regulatory standards and consumer expectations.

These signals collectively highlight the evolving nature of the regulatory landscape and its impact on the contact lens market. Companies must remain vigilant and adaptable, leveraging regulatory changes as opportunities for innovation and competitive advantage. The strategic implications of these developments are far-reaching, influencing everything from product development and marketing to supply chain management and corporate strategy.

Strategic Implications