Global Digital Pathology Market Report 2026-2033

Global Digital Pathology Market Size & Forecast

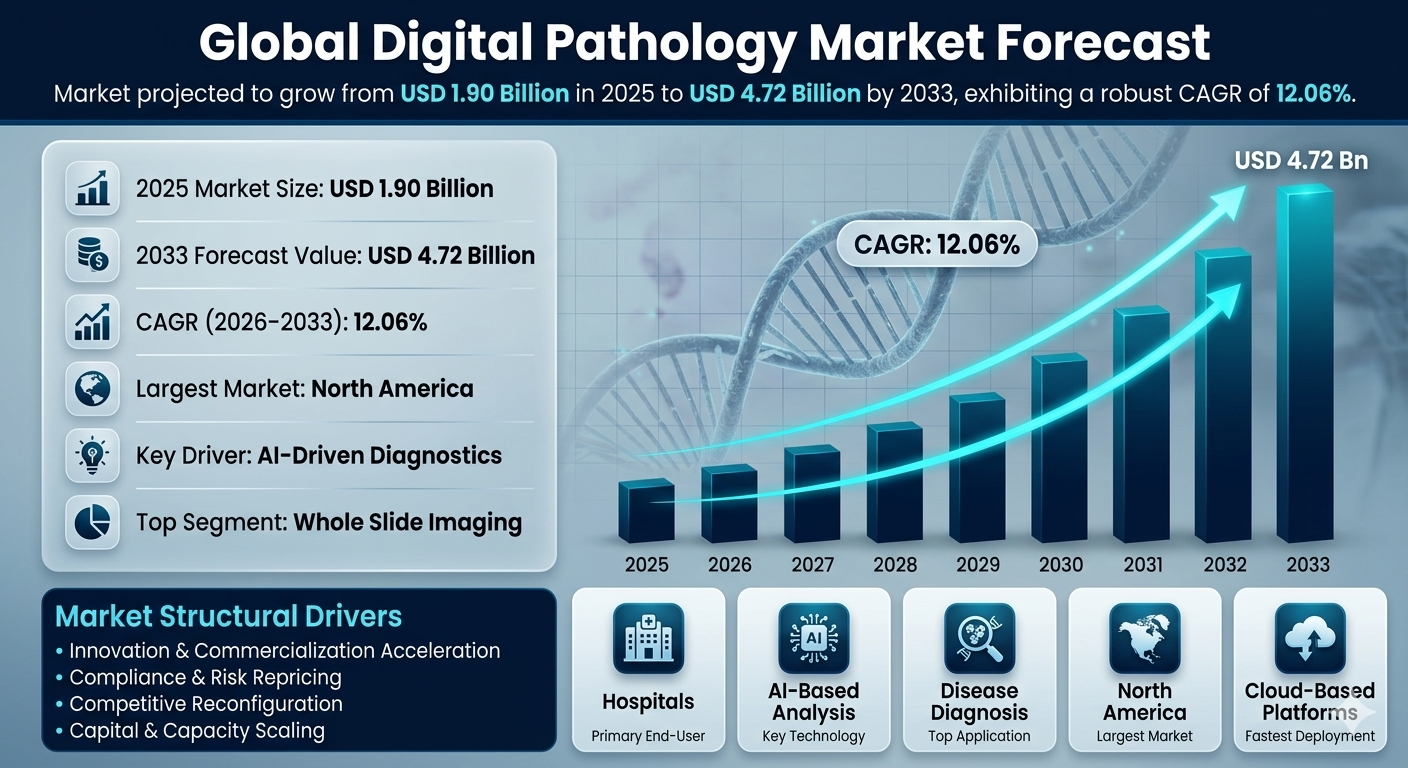

The Digital Pathology market is poised for a significant expansion, with its size expected to burgeon from USD 1.90 billion in 2025 to USD 4.72 billion by 2033. This growth trajectory is underlined by a robust compound annual growth rate (CAGR) of 12.06% over the forecast period of 2026 to 2033. The impressive CAGR is indicative of the transformative changes and technological advancements that are reshaping the landscape of digital pathology. As healthcare systems worldwide continue to grapple with rising patient volumes and the concomitant demand for precision medicine, the digital pathology market is set to play a crucial role in augmenting diagnostic capabilities.

The projected growth in market size underscores the increasing integration of digital technologies within pathology workflows. The acceleration towards digital pathology is driven by the need for more efficient, accurate, and scalable diagnostic solutions. This shift is likely to be further catalyzed by technological advancements such as AI-driven diagnostics and whole slide imaging, which are becoming increasingly integral to pathology practice. The growing market size reflects not only increased adoption but also the broadening scope of digital pathology applications, ranging from routine diagnostics to cutting-edge research in fields like oncology and personalized medicine.

Market Overview

Digital pathology stands at the confluence of technology and medicine, transforming the traditional practices of microscopy and histopathology through advanced digital solutions. At its core, digital pathology involves the digitization of pathology slides for interpretation, analysis, and storage, thereby enhancing the efficiency and accuracy of pathological evaluations. This shift from manual to digital approaches is driven by innovations such as whole slide imaging, machine learning, and artificial intelligence, which collectively streamline the diagnostic process.

The market is currently characterized by a moderately consolidated structure, with a high level of competitive intensity. Key players such as Proscia, LG AI Research, and Tempus AI are actively shaping the market through strategic partnerships, acquisitions, and technological innovations. For instance, Tempus AI's acquisition of Paige for USD 81.25 million exemplifies the strategic maneuvers companies are making to bolster their capabilities and market presence.

Digital pathology's integration into healthcare systems is further amplified by supportive regulatory frameworks, including FDA approvals for primary diagnostic use and the In Vitro Diagnostic Medical Devices Regulation (2017/746). These regulatory milestones not only validate the technology's clinical utility but also set the stage for broader adoption across healthcare institutions. Furthermore, the market's growth is bolstered by a global shortage of pathologists, necessitating more efficient tools to manage increasing workloads and improve diagnostic throughput.

Structural Drivers of Market Growth

The expansion of the Digital Pathology market is underpinned by several structural drivers that encapsulate the interplay of technology, investment, regulatory changes, and competitive dynamics.

Driver 1: Innovation and Commercialization Acceleration

The first critical driver of market growth is the rapid innovation and commercialization acceleration within the digital pathology sphere. Technology maturity, coupled with increased funding, is compressing development-to-commercialization cycles. Notably, there was a 54.80% increase in funding in 2024, with funding doubling in Q1 2025 compared to Q1 2024. This financial influx is facilitating the advancement and deployment of sophisticated diagnostic tools, thereby expanding addressable applications and increasing the speed of adoption.

The global shortage of pathologists further underscores the necessity for innovative solutions that can enhance diagnostic efficiency. FDA approvals for primary diagnosis serve as a pivotal signal of technological maturity, ensuring that digital pathology solutions meet stringent clinical standards. Consequently, as funding continues to flow into technology and infrastructure, digital pathology is poised to rapidly expand its footprint in healthcare settings.

Driver 2: Compliance and Risk Repricing

Regulatory tightening and risk repricing are reshaping the operating landscape of digital pathology. Regulatory frameworks such as the In Vitro Diagnostic Medical Devices Regulation (2017/746) and FDA approvals highlight the shifting compliance requirements that companies must navigate. These regulatory developments are repricing operating requirements, pushing companies to enhance product roadmaps and execution standards.

The collaboration between AI developers and institutions to address compliance and risk concerns further illustrates how regulatory pressures are catalyzing market evolution. As digital pathology solutions gain regulatory clearance, the emphasis on compliance ensures that these technologies adhere to the highest standards of safety and efficacy, thereby fostering market confidence and adoption.

Driver 3: Competitive and Value-Chain Reconfiguration

The digital pathology market is witnessing a reconfiguration of competitive dynamics and value chains. Competitive moves, such as Tempus AI's acquisition of Paige and strategic partnerships like those between FUJIFILM Healthcare Europe and Ibex Medical Analytics, are reallocating bargaining power. These strategic shifts force companies to reposition their portfolios, altering where margins and growth opportunities concentrate.

The shortage of skilled pathologists and technicians, coupled with regulatory and reimbursement uncertainties, underscores the market's evolving competitive landscape. As companies navigate these constraints, they are compelled to innovate and optimize their value chains to maintain competitive advantages. This reconfiguration not only influences market structure but also dictates which players emerge as leaders in the digital pathology domain.

Driver 4: Capital and Capacity Scaling

Capital deployment into capacity and process upgrades is another pivotal driver propelling the digital pathology market forward. The surge in funding, evidenced by a 54.80% increase in 2024 and doubling in Q1 2025, is enabling companies to enhance their operational capabilities. This influx of capital facilitates capacity scaling, reduces deployment friction, and allows for faster scaling in high-demand segments.

The growing demand for precision medicine and the global shortage of pathologists necessitate scalable solutions that can efficiently handle large volumes of diagnostic data. As capital continues to flow into digital pathology, companies are poised to expand throughput and address the burgeoning need for advanced diagnostic services. This scaling capacity not only meets current demands but also positions the market to accommodate future growth.

Market Segmentation Analysis

The Digital Pathology market can be segmented across several dimensions, including end users, technology, applications, products, and deployment modes. Each segment offers unique insights into the market's dynamics and growth potential.

End Users

- Hospitals

- Diagnostic Laboratories

- Pharmaceutical Companies

- Biotechnology Companies

Digital pathology solutions are leveraged by a diverse range of end users, including hospitals, diagnostic laboratories, pharmaceutical and biotechnology companies. Hospital pathology laboratories and independent diagnostic laboratories are primary consumers, driven by the need for efficient and accurate diagnostic tools. These institutions utilize digital pathology for cancer diagnostics, tissue analysis, and centralized pathology services, underscoring the market's critical role in enhancing diagnostic precision and throughput.

Technology

- AI-Based Pathology Analysis

- Whole Slide Imaging

The technological segmentation of the market highlights the pivotal role of AI-based pathology analysis and whole slide imaging technologies. AI-driven image analysis, encompassing machine learning and deep learning platforms, is revolutionizing diagnostic workflows by enabling precise tissue pattern recognition and biomarker detection. Whole slide imaging technology further enhances diagnostic capabilities by providing high-resolution imaging systems that facilitate detailed tissue analysis.

Applications

- Disease Diagnosis

- Education and Training

- Drug Discovery and Development

Digital pathology finds application in various domains, including disease diagnosis, education and training, and drug discovery and development. Disease diagnosis remains a primary application, with digital pathology playing a crucial role in cancer and infectious disease diagnostics. Additionally, digital pathology teaching platforms and virtual slide libraries are transforming medical education, providing valuable resources for training and skill development.

Products

- Services

- Digital Pathology Scanners

- Software Solutions

The market's product segmentation encompasses services, digital pathology scanners, and software solutions. Digital pathology services, including maintenance, support, and implementation, are essential for the seamless operation of digital pathology systems. Scanners, such as brightfield and fluorescence slide scanners, are integral to digitizing pathology workflows, while software solutions facilitate image analysis, management, and integration within laboratory information systems.

Deployment Mode

- On-Premise Systems

- Cloud-Based Platforms

Digital pathology solutions are deployed through both on-premise systems and cloud-based platforms. On-premise systems cater to hospitals and laboratories requiring local data storage and processing capabilities. Conversely, cloud-based platforms offer remote data access and collaboration, facilitating multi-hospital image sharing and diagnostic collaboration. The choice of deployment mode is often influenced by institutional preferences, data management requirements, and operational scalability.

In summary, the Digital Pathology market is characterized by dynamic segmentation that reflects the diverse needs of healthcare institutions and the evolving technological landscape. As the market continues to grow, each segment offers unique opportunities and challenges, shaping the future trajectory of digital pathology.

Regional Market Dynamics

The Digital Pathology market's regional dynamics are shaped by a combination of technological advancements, regulatory frameworks, and healthcare infrastructure. North America, particularly the United States, leads the market due to a well-established healthcare system, early adoption of innovative technologies, and strong regulatory support. The presence of key players such as Tempus AI and Paige, alongside robust investment trends, underscores the region's dominance. The U.S. market benefits from the FDA's proactive stance on approving digital pathology solutions, which accelerates innovation and commercialization.

Europe follows closely, driven by stringent regulatory mechanisms such as the In Vitro Diagnostic Medical Devices Regulation (IVDR) and a focus on compliance and risk management. The region's commitment to maintaining high standards in medical devices ensures a steady demand for advanced digital pathology solutions. The UK, Germany, and France are notable contributors, with active involvement from companies like Philips and Roche, which leverage their strategic capabilities in AI and imaging technologies to strengthen market presence.

In Asia-Pacific, the market is experiencing rapid growth due to increasing healthcare expenditures and government support for healthcare innovation. Countries like China and India are investing heavily in digital healthcare infrastructure to address the rising prevalence of chronic diseases and the shortage of skilled pathologists. The region's dynamic market is characterized by collaborations between local and international players, aiming to enhance digital pathology capabilities and integrate AI-driven diagnostics into healthcare workflows.

Emerging markets in Latin America and the Middle East & Africa are also witnessing a gradual uptake of digital pathology solutions. These regions are focusing on upgrading healthcare infrastructure and integrating digital technologies to improve diagnostic accuracy and efficiency. While regulatory challenges persist, ongoing efforts to align with international standards are expected to bolster market growth.

Competitive Landscape

The Digital Pathology market is moderately consolidated, with high competitive intensity driven by technological advancements and strategic collaborations. Key players such as Proscia, LG AI Research, and FUJIFILM Healthcare Europe are at the forefront, leveraging their technological prowess to enhance product offerings and expand market share. Proscia's strategic capability lies in its AI-driven platform that streamlines pathology workflows, while FUJIFILM focuses on integrating imaging technologies to provide comprehensive diagnostic solutions.

Nvidia and Ibex Medical Analytics exemplify the market's focus on AI-driven diagnostics. Nvidia's strength in computational power supports advanced image analysis algorithms, while Ibex's AI solutions are designed to improve diagnostic accuracy and efficiency. The acquisition of Paige by Tempus AI for USD 81.25 million highlights the market's inclination towards consolidation, where larger entities absorb innovative startups to strengthen their technological capabilities and market reach.

Strategic partnerships and collaborations are common, as seen with Techcyte's partnership with Modella AI and the expansion of Philips' partnership with Ibex Medical Analytics. These alliances enable companies to pool resources, accelerate innovation, and navigate regulatory landscapes efficiently. The competitive landscape is further shaped by barriers to entry, such as high capital intensity and the need for regulatory compliance, which restrict smaller players from rapidly scaling operations.

Strategic Outlook

The strategic outlook for the Digital Pathology market is shaped by a confluence of innovation, regulatory compliance, and market consolidation. As the market matures, companies are expected to focus on enhancing AI algorithms for improved diagnostic accuracy and workflow efficiency. Investment in cloud-based solutions and teleconsultation platforms will continue to rise, driven by the need for seamless data access and collaboration across geographies.

Regulatory frameworks will play a pivotal role in shaping market strategies. Companies must navigate complex compliance requirements while fostering innovation, necessitating collaboration with regulatory bodies to ensure product approvals and market access. The growing emphasis on risk management and ethical AI practices will further influence strategic decisions, compelling companies to invest in robust machine learning models and data security measures.

Market consolidation is likely to persist, with larger players acquiring innovative startups to enhance technological capabilities and expand market presence. Strategic partnerships will remain crucial in driving innovation and addressing value-chain constraints. Companies must also focus on upskilling workforce capabilities to overcome the shortage of skilled pathologists and technicians, ensuring smooth adoption and integration of digital pathology solutions.

Final Market Perspective

In conclusion, the Digital Pathology market is poised for transformative growth, underpinned by technological advancements, regulatory compliance, and strategic consolidation. The anticipated expansion from USD 1.90 billion in 2025 to USD 4.72 billion by 2033 reflects the market's potential to redefine diagnostic workflows and enhance healthcare delivery. As innovation accelerates and regulatory landscapes evolve, market players must strategically position themselves to capture emerging opportunities and address challenges.

The integration of AI-driven diagnostics and cloud-based platforms represents a significant shift towards precision medicine and efficient healthcare delivery. Regulatory compliance and risk management will remain critical, necessitating robust collaboration between stakeholders. As the market continues to consolidate, companies must leverage strategic partnerships to enhance capabilities and sustain competitive advantage. Ultimately, the Digital Pathology market's trajectory will be shaped by its ability to adapt to dynamic technological, regulatory, and competitive landscapes, ensuring that it remains at the forefront of healthcare innovation.

Table of Contents

Table of Contents

- 1. Executive Summary

- 1.1 Market Forecast Snapshot (2026-2033)

- 1.2 Global Market Size & CAGR Analysis

- 1.3 Largest & Fastest-Growing Segments

- 1.4 Region-Level Leadership & Growth Trends

- 1.5 Key Market Drivers

- 1.6 Competitive Landscape Overview

- 1.7 Strategic Outlook Through 2033

- 2. Introduction & Market Overview

- 2.1 Definition of the Digital Pathology Market

- 2.2 Scope of the Study

- 2.3 Industry Evolution & Market Development

- 2.4 Supply Chain & Distribution Infrastructure

- 2.5 Impact of Consumer Trends

- 2.6 Sustainability & Regulatory Landscape

- 2.7 Technology & Innovation Landscape

- 3. Research Methodology

- 3.1 Primary Research

- 3.2 Secondary Research

- 3.3 Market Size Estimation Model

- 3.4 Forecast Assumptions (2026-2033)

- 3.5 Data Validation & Triangulation

- 4. Market Dynamics

- 4.1 Drivers

- 4.1.1 Increasing Demand Drivers

- 4.1.2 Industry Innovation Drivers

- 4.1.3 Market Expansion Factors

- 4.1.4 Regulatory or Policy Support

- 4.1.5 Technology Adoption Drivers

- 4.2 Restraints

- 4.2.1 Cost Constraints

- 4.2.2 Infrastructure Limitations

- 4.2.3 Regulatory Challenges

- 4.2.4 Market Awareness Barriers

- 4.3 Opportunities

- 4.3.1 Emerging Market Opportunities

- 4.3.2 Product Innovation Opportunities

- 4.3.3 Technology Expansion Opportunities

- 4.3.4 Supply Chain Improvements

- 4.4 Challenges

- 4.4.1 Supply Chain Complexity

- 4.4.2 Quality Control & Compliance

- 4.4.3 Regional Market Fragmentation

- 4.4.4 Competitive Pressure

- 4.1 Drivers

- 5. Digital Pathology Market Analysis (USD Billion), 2026-2033

- 5.1 Market Size Overview

- 5.2 CAGR Analysis

- 5.3 Regional Revenue Distribution

- 5.4 Segment Revenue Analysis

- 5.5 Distribution Channel Analysis

- 5.6 Consumer Impact Analysis

- 6. Market Segmentation (USD Billion), 2026-2033

- 6.1 By End User

- 6.1.1 Diagnostic Laboratories

- 6.1.1.1 Independent Pathology Laboratories

- 6.1.1.1.1 Reference Pathology Laboratories

- 6.1.1.1.1.1 High Volume Tissue Analysis Labs

- 6.1.1.1.1.2 Centralized Pathology Diagnostic Centers

- 6.1.1.1.1 Reference Pathology Laboratories

- 6.1.1.1 Independent Pathology Laboratories

- 6.1.2 Hospitals

- 6.1.2.1 Hospital Pathology Laboratories

- 6.1.2.1.1 Diagnostic Histopathology Units

- 6.1.2.1.1.1 Cancer Diagnostic Laboratories

- 6.1.2.1.1.2 Tissue Analysis Laboratories

- 6.1.2.1.1 Diagnostic Histopathology Units

- 6.1.2.1 Hospital Pathology Laboratories

- 6.1.3 Pharmaceutical and Biotechnology Companies

- 6.1.3.1 Drug Development Laboratories

- 6.1.3.1.1 Translational Research Laboratories

- 6.1.3.1.1.1 Biomarker Discovery Platforms

- 6.1.3.1.1.2 Precision Medicine Research Programs

- 6.1.3.1.1 Translational Research Laboratories

- 6.1.3.1 Drug Development Laboratories

- 6.1.1 Diagnostic Laboratories

- 6.2 By Technology

- 6.2.1 AI Based Pathology Analysis

- 6.2.1.1 Deep Learning Pathology Platforms

- 6.2.1.1.1 Cancer Detection Algorithms

- 6.2.1.1.1.1 Tumor Classification Systems

- 6.2.1.1.1.2 Metastasis Detection Algorithms

- 6.2.1.1.1 Cancer Detection Algorithms

- 6.2.1.2 Machine Learning Image Analysis

- 6.2.1.2.1 Tissue Pattern Recognition Systems

- 6.2.1.2.1.1 Cellular Morphology Detection Algorithms

- 6.2.1.2.1.2 Biomarker Detection Systems

- 6.2.1.2.1 Tissue Pattern Recognition Systems

- 6.2.1.1 Deep Learning Pathology Platforms

- 6.2.2 Whole Slide Imaging Technology

- 6.2.2.1 High Resolution Imaging Systems

- 6.2.2.1.1 20x Slide Scanning Systems

- 6.2.2.1.1.1 Standard Diagnostic Slide Imaging

- 6.2.2.1.1.2 Routine Histopathology Imaging

- 6.2.2.1.2 40x Slide Scanning Systems

- 6.2.2.1.2.1 High Precision Pathology Imaging

- 6.2.2.1.2.2 Detailed Tissue Analysis Imaging

- 6.2.2.1.1 20x Slide Scanning Systems

- 6.2.2.1 High Resolution Imaging Systems

- 6.2.1 AI Based Pathology Analysis

- 6.3 By Application

- 6.3.1 Disease Diagnosis

- 6.3.1.1 Cancer Diagnosis

- 6.3.1.1.1 Histopathology Cancer Analysis

- 6.3.1.1.1.1 Tumor Tissue Diagnosis

- 6.3.1.1.1.2 Cancer Grading and Staging

- 6.3.1.1.1 Histopathology Cancer Analysis

- 6.3.1.2 Infectious Disease Diagnosis

- 6.3.1.2.1 Pathogen Detection in Tissue Samples

- 6.3.1.2.1.1 Viral Tissue Infection Analysis

- 6.3.1.2.1.2 Bacterial Tissue Infection Detection

- 6.3.1.2.1 Pathogen Detection in Tissue Samples

- 6.3.1.1 Cancer Diagnosis

- 6.3.2 Drug Discovery and Development

- 6.3.2.1 Preclinical Research

- 6.3.2.1.1 Tissue Biomarker Analysis

- 6.3.2.1.1.1 Drug Response Tissue Imaging

- 6.3.2.1.1.2 Target Biomarker Detection

- 6.3.2.1.1 Tissue Biomarker Analysis

- 6.3.2.1 Preclinical Research

- 6.3.3 Education and Training

- 6.3.3.1 Digital Pathology Teaching Platforms

- 6.3.3.1.1 Virtual Slide Libraries

- 6.3.3.1.1.1 Medical Education Platforms

- 6.3.3.1.1.2 Pathology Training Systems

- 6.3.3.1.1 Virtual Slide Libraries

- 6.3.3.1 Digital Pathology Teaching Platforms

- 6.3.1 Disease Diagnosis

- 6.4 By Product Type

- 6.4.1 Digital Pathology Scanners

- 6.4.1.1 Brightfield Slide Scanners

- 6.4.1.1.1 Histopathology Slide Scanners

- 6.4.1.1.1.1 Tissue Sample Imaging Systems

- 6.4.1.1.1.2 Diagnostic Slide Imaging Platforms

- 6.4.1.1.1 Histopathology Slide Scanners

- 6.4.1.2 Fluorescence Slide Scanners

- 6.4.1.2.1 Multiplex Imaging Systems

- 6.4.1.2.1.1 Fluorescence Tissue Imaging Systems

- 6.4.1.2.1.2 Biomarker Detection Imaging Platforms

- 6.4.1.2.1 Multiplex Imaging Systems

- 6.4.1.3 Whole Slide Imaging (WSI) Scanners

- 6.4.1.3.1 High Throughput Slide Scanners

- 6.4.1.3.1.1 Automated Slide Scanning Systems

- 6.4.1.3.1.2 Batch Slide Scanning Platforms

- 6.4.1.3.2 Low to Medium Throughput Slide Scanners

- 6.4.1.3.2.1 Laboratory Slide Digitization Systems

- 6.4.1.3.2.2 Compact Whole Slide Imaging Devices

- 6.4.1.3.1 High Throughput Slide Scanners

- 6.4.1.1 Brightfield Slide Scanners

- 6.4.2 Digital Pathology Software

- 6.4.2.1 Image Analysis Software

- 6.4.2.1.1 AI Based Tissue Analysis Software

- 6.4.2.1.1.1 Tumor Detection Algorithms

- 6.4.2.1.1.2 Biomarker Quantification Software

- 6.4.2.1.2 Quantitative Pathology Analysis Tools

- 6.4.2.1.2.1 Cell Counting Software

- 6.4.2.1.2.2 Tissue Morphology Analysis Systems

- 6.4.2.1.1 AI Based Tissue Analysis Software

- 6.4.2.2 Image Management Software

- 6.4.2.2.1 Digital Slide Storage Platforms

- 6.4.2.2.1.1 Pathology Image Archive Systems

- 6.4.2.2.1.2 Laboratory Image Data Management Systems

- 6.4.2.2.1 Digital Slide Storage Platforms

- 6.4.2.3 Laboratory Information Integration Software

- 6.4.2.3.1 Laboratory Information System (LIS) Integration

- 6.4.2.3.1.1 Pathology Workflow Management Platforms

- 6.4.2.3.1.2 Diagnostic Reporting Systems

- 6.4.2.3.1 Laboratory Information System (LIS) Integration

- 6.4.2.1 Image Analysis Software

- 6.4.3 Services

- 6.4.3.1 Digital Pathology Implementation Services

- 6.4.3.1.1 System Installation Services

- 6.4.3.1.1.1 Laboratory Digitalization Services

- 6.4.3.1.1.2 Pathology Infrastructure Deployment

- 6.4.3.1.1 System Installation Services

- 6.4.3.2 Maintenance and Support Services

- 6.4.3.2.1 Software Maintenance Services

- 6.4.3.2.1.1 AI Model Updating Services

- 6.4.3.2.1.2 Digital Pathology System Monitoring

- 6.4.3.2.1 Software Maintenance Services

- 6.4.3.1 Digital Pathology Implementation Services

- 6.4.1 Digital Pathology Scanners

- 6.5 By Deployment Mode

- 6.5.1 Cloud Based Digital Pathology Platforms

- 6.5.1.1 Cloud Image Storage Systems

- 6.5.1.1.1 Remote Pathology Data Platforms

- 6.5.1.1.1.1 Multi Hospital Image Sharing Systems

- 6.5.1.1.1.2 Cloud Based Diagnostic Collaboration

- 6.5.1.1.1 Remote Pathology Data Platforms

- 6.5.1.1 Cloud Image Storage Systems

- 6.5.2 On-Premise Digital Pathology Systems

- 6.5.2.1 Hospital Based Pathology Platforms

- 6.5.2.1.1 Local Slide Image Storage Systems

- 6.5.2.1.1.1 Hospital Pathology Data Centers

- 6.5.2.1.1.2 On-Site Digital Pathology Servers

- 6.5.2.1.1 Local Slide Image Storage Systems

- 6.5.2.1 Hospital Based Pathology Platforms

- 6.5.1 Cloud Based Digital Pathology Platforms

- 6.1 By End User

- 7. Market Segmentation by Geography

- 7.1 North America

- 7.2 Europe

- 7.3 Asia-Pacific

- 7.4 Latin America

- 7.5 Middle East & Africa

- 8. Competitive Landscape

- 8.1 Market Share Analysis

- 8.2 Product Portfolio Benchmarking

- 8.3 Product Positioning Mapping

- 8.4 Supply Chain & Distribution Partnerships

- 8.5 Competitive Intensity & Differentiation

- 9. Company Profiles

- 10. Strategic Intelligence & Pheonix AI Insights

- 10.1 Pheonix Demand Forecast Engine

- 10.2 Supply Chain & Infrastructure Analyzer

- 10.3 Technology & Innovation Tracker

- 10.4 Product Development Insights

- 10.5 Automated Porter’s Five Forces Analysis

- 11. Future Outlook & Strategic Recommendations

- 11.1 Emerging Market Expansion

- 11.2 Technology Innovation Strategies

- 11.3 Product Development Roadmap

- 11.4 Regional Expansion Strategies

- 11.5 Long-Term Market Outlook (2033+)

- 12. Appendix

- 13. About Pheonix Research

- 14. Disclaimer

Competitive Landscape

Competitive Landscape of the Global digital pathology market

Executive Framing

The digital pathology market is at a pivotal juncture where competitive intensity and market structure are undergoing significant transformations. This dimension is crucial because it determines how entities within the space align their strategies to leverage opportunities and mitigate challenges. With a forecast period extending from 2026 to 2033, the landscape is shaped by a moderately consolidated structure characterized by high competitive intensity. This dynamic environment is influenced by technological advancements, strategic partnerships, and significant investments, which collectively impact the positioning of companies within the market. The ability to navigate these complexities will define the success and sustainability of entities in the digital pathology sector.

A moderately consolidated market structure signifies that while a substantial number of players exist, a few dominate the market share. In the digital pathology domain, the presence of ten Tier 1 players, including Proscia, LG AI Research, Tempus AI, Paige, Nvidia, and others, underscores a competitive landscape where strategic moves such as acquisitions, partnerships, and funding are critical. This intensity is driven by the growing demand for precision medicine, the rising prevalence of chronic diseases, and technological advancements that push for digitization of pathological infrastructure. These elements collectively foster a highly competitive environment where companies must innovate and collaborate to maintain or enhance their market positions.

Current Market Reality

The current state of the digital pathology market reveals a scenario where companies are actively pursuing strategic initiatives to strengthen their market positions. Proscia’s recent securing of USD 50 million in funding exemplifies the drive for financial backing to support innovation and expansion efforts. This move highlights the ongoing necessity for capital to fuel technological development and market penetration. Similarly, Tempus AI’s acquisition of Paige for USD 81.25 million illustrates the trend of consolidation within the industry, aimed at harnessing synergies and expanding capabilities.

Strategic partnerships are another critical aspect shaping the market’s current reality. FUJIFILM Healthcare Europe’s partnership with Ibex Medical Analytics and the expanded collaboration between Philips and Ibex Medical Analytics are indicative of the emphasis on enhancing interoperability and integrating AI-driven solutions. These alliances are essential for companies seeking to deliver comprehensive digital pathology solutions that address the growing demand for efficient and accurate diagnostics.

The competitive landscape is further intensified by the entry of technology giants such as Microsoft, which has developed Prov-GigaPath, a testament to the increasing integration of AI technologies in healthcare. This development reflects a broader trend of tech-driven innovations reshaping the market, compelling traditional players to adapt and evolve. The shortage of pathologists, coupled with the rising demand for telepathology, underscores the necessity for digital solutions that can alleviate workforce constraints and enhance diagnostic capabilities.

Key Signals and Evidence

The digital pathology market’s structural drivers are intricately linked to key signals that provide a window into the evolving dynamics of competitive intensity and market structure. One pivotal signal is the FDA approval of Paige.AI’s Paige Prostate in 2021, which marks a significant regulatory milestone and underscores the growing acceptance of AI-driven diagnostic tools. This approval not only validates the technology but also catalyzes further adoption, influencing competitive positioning as companies race to achieve similar regulatory endorsements.

The acquisition of Paige by Tempus AI for USD 81.25 million is a strategic maneuver that consolidates expertise and resources, enhancing Tempus AI’s competitive edge. This move highlights the importance of acquisitions as a means to accelerate growth and expand market reach. Similarly, Proscia’s USD 50 million funding round underscores the crucial role of financial resources in advancing technological capabilities and expanding operational footprints.

Partnerships between key players, such as the collaboration between Koninklijke Philips N.V. and Ibex, serve as a mechanism for enhancing interoperability and delivering integrated solutions. These alliances are not merely transactional; they represent strategic alignments that enable participants to leverage each other’s strengths and address market demands more effectively. Furthermore, the multi-year partnerships announced by PathAI with Austrian pathology laboratories exemplify the trend of forming long-term collaborations to secure market share and drive innovation.

One of the most pressing signals is the shortage of pathologists, which necessitates a shift towards digital solutions. This shortage drives the adoption of AI and telepathology, offering companies opportunities to develop and deploy innovative solutions that address workforce challenges and improve diagnostic efficiency. The acquisition of Vesper Medical by Philips is an example of how companies are enhancing their medical device offerings to stay competitive in a rapidly evolving market.

Strategic Implications

In the digital pathology market, the confluence of strategic investments, technological advancements, and shifting competitive dynamics necessitates a nuanced understanding of the strategic implications for stakeholders. As companies vie for dominance in a market characterized by high competitive intensity and a moderately consolidated structure, their strategic maneuvers will have profound implications on market structure and positioning.

The acquisition of Paige by Tempus AI for USD 81.25 million exemplifies the aggressive consolidation strategies employed by major players. This move not only signals Tempus AI’s ambition to expand its capabilities in AI-driven diagnostics but also underscores the importance of scale and technological integration in maintaining a competitive edge. As companies like Tempus AI consolidate their offerings, smaller players may face increased pressure to either innovate rapidly or seek strategic partnerships to remain viable. This consolidation trend may lead to a market where fewer, more powerful entities dominate, potentially stifling smaller innovators unless they align with larger partners.

Similarly, Proscia’s successful securing of USD 50 million in funding highlights the critical role of financial resources in driving innovation and maintaining competitive positioning. Such investments enable companies to enhance their technological offerings, expand their market reach, and invest in R&D, thereby solidifying their market presence. For competitors, this signals the necessity of securing substantial financial backing to remain competitive, particularly in an industry where rapid technological evolution is a key differentiator.

Partnerships, such as the one between Koninklijke Philips N.V. and Ibex Medical Analytics, are pivotal in enhancing interoperability and expanding service offerings. These collaborations allow companies to leverage each other’s strengths, improve diagnostic accuracy, and streamline workflows. By integrating AI technologies and expanding telepathology capabilities, these partnerships can significantly improve market positioning. Stakeholders must, therefore, prioritize strategic alliances that enhance their technological capabilities and extend their market reach.

The shortage of pathologists further exacerbates the need for digital and AI-driven solutions, creating a demand for innovative technologies that can compensate for workforce limitations. This demand presents an opportunity for companies to develop solutions that address these challenges, thus gaining a competitive advantage. The integration of AI in diagnostics, as evidenced by FDA approval of Paige.AI’s Paige Prostate in 2021, underlines the critical role of regulatory milestones in shaping market dynamics. Companies that achieve such regulatory approvals can leverage them as significant differentiators, enhancing their credibility and market positioning.

Forward Outlook

As we look towards the forecast period of 2026 to 2033, several key trends and strategic considerations will shape the future landscape of the digital pathology market. The ongoing consolidation and strategic partnerships will likely intensify, driving further market concentration and potentially creating barriers for new entrants. Established players will continue to seek acquisitions and partnerships to bolster their technological capabilities and expand their market share. This trend may lead to a bifurcation of the market, where a few dominant players control significant market segments, while niche players cater to specific needs or geographic regions.

Technological advancements and the integration of AI will remain at the forefront of competitive strategies. Companies that can harness these technologies to enhance diagnostic accuracy, reduce costs, and improve patient outcomes will likely secure a competitive edge. As AI becomes more integrated into diagnostic workflows, it will enable faster, more accurate analyses, addressing the shortage of pathologists and meeting the growing demand for precision medicine.

The rise of telepathology networks and the expansion of national telepathology initiatives will further influence market dynamics by enhancing access to diagnostics and enabling remote consultations. This expansion will create opportunities for companies to offer comprehensive telepathology solutions, thereby increasing their market presence and influence.

Regulatory landscapes will continue to evolve, with supportive regulatory progress encouraging innovation while regulatory and reimbursement uncertainties may pose challenges. Companies must remain agile, adapting to regulatory changes and leveraging approvals as competitive differentiators.

In conclusion, the digital pathology market’s trajectory will be shaped by strategic consolidations, technological advancements, and evolving regulatory landscapes. Companies that can navigate these complexities, leverage strategic partnerships, and invest in innovative solutions will be well-positioned to achieve sustainable competitive advantage in a highly dynamic market. Stakeholders must remain vigilant, continuously assessing market developments and adapting their strategies to capitalize on emerging opportunities and mitigate potential risks. As the market evolves, the ability to integrate advanced technologies, form strategic alliances, and respond to regulatory shifts will determine the success of companies in this competitive landscape.

Value Chain

Value Chain and Supply Chain Dynamics in the Global Digital Pathology Market

Executive Framing

In the rapidly evolving field of digital pathology, the dynamics of the value chain and supply chain evolution are pivotal in shaping market structure, particularly from 2026 to 2033. The transition towards platform-based operational models and hybrid distribution structures necessitates a comprehensive understanding of how these frameworks influence not only the efficiency of the supply chain but also the distribution of power and margin structures within the industry. As digital pathology matures, bottlenecks such as stock shortages, transportation delays, and interoperability challenges present significant hurdles, impacting both operational capabilities and market competitiveness.

This dimension is critical now because digital pathology is at a tipping point, driven by key signals such as increased adoption rates, government-backed initiatives, and a surge in cancer research activities. These factors are juxtaposed with challenges like a shortage of skilled pathologists and technicians, regulatory uncertainties, and high initial capital costs. Understanding how these elements interplay within the value chain is crucial for stakeholders aiming to optimize their strategic positioning and capitalize on emerging opportunities in digital pathology.

Current Market Reality

The current landscape of digital pathology is marked by a moderate level of supply chain complexity, with strategic implications for stakeholders across the spectrum. Companies such as Koninklijke Philips N.V. and Paige.AI are at the forefront of this transformation, leveraging advanced technologies and strategic partnerships to navigate existing constraints. For instance, Philips’ collaboration with Ibex aims to enhance interoperability, a critical bottleneck that hinders seamless integration of digital pathology systems with existing laboratory infrastructures. This partnership exemplifies how industry leaders are proactively addressing data interoperability issues to streamline operations and improve delivery performance.

Moreover, the shortage of skilled pathologists and technicians remains a formidable challenge, exacerbated by the increasing demand for digital pathology services. This shortage not only constrains capacity utilization but also shifts bargaining power towards entities that can offer comprehensive training and development programs. As a result, organizations that invest in workforce development are likely to gain a competitive edge by enhancing their operational capabilities and ensuring timely delivery of services.

The high initial capital cost of digital pathology systems further complicates the market dynamics, particularly for smaller players and emerging economies. This financial barrier limits the adoption of advanced technologies, thereby affecting market penetration and competitive parity. Companies that can provide cost-effective solutions or financing options will likely capture a larger market share by enabling broader access to digital pathology systems.

Regulatory and reimbursement uncertainties also play a significant role in shaping the current market reality. The evolving landscape of regulations, exemplified by the In Vitro Diagnostic Medical Devices Regulation (2017/746), creates an environment of ambiguity that can deter investment and slow the pace of innovation. Companies that navigate these regulatory challenges effectively, such as Paige.AI with its FDA-approved Paige Prostate, are well-positioned to leverage regulatory compliance as a strategic advantage.

Regulatory and reimbursement uncertainty remains a pervasive concern that affects the strategic decisions of companies operating in the digital pathology space. Navigating this complex regulatory landscape requires significant resources and expertise, which can be a barrier for smaller players. However, entities that successfully achieve regulatory compliance, as demonstrated by Paige.AI’s FDA approval, can leverage this as a competitive advantage to expand their market presence and enhance credibility with stakeholders.

In conclusion, the digital pathology market’s current reality is shaped by a delicate balance of opportunities and challenges. Stakeholders must strategically navigate these dynamics to optimize their value chain, enhance operational efficiency, and secure a favorable position in this rapidly evolving landscape. By addressing bottlenecks, leveraging key signals, and adapting to regulatory changes, companies can unlock significant value and drive sustainable growth in the digital pathology sector.

Key Signals and Evidence

To understand the evolving landscape of digital pathology, it is crucial to synthesize various primary and secondary signals that highlight the sector’s current and future trajectory. These signals provide insights into potential opportunities and challenges that stakeholders must navigate to optimize their operations and strategic positioning.

Firstly, the shortage of skilled pathologists and technicians stands as a significant bottleneck, affecting the capacity and efficiency of service delivery within the digital pathology market. This shortage is exacerbated by the increasing adoption of digital pathology systems, which require specialized skills for operation and maintenance. As such, companies that invest in training and upskilling initiatives are likely to enhance their operational capabilities and mitigate potential disruptions in service delivery.

The regulatory and reimbursement uncertainty in the digital pathology sector poses another critical challenge. The evolving regulatory landscape, influenced by frameworks such as the In Vitro Diagnostic Medical Devices Regulation (2017/746), requires companies to remain vigilant and adaptive. Paige.AI’s FDA approval of its Paige Prostate system illustrates the importance of regulatory compliance in gaining market traction and ensuring product reliability. The high initial capital cost associated with digital pathology systems further compounds these challenges, necessitating strategic investments and partnerships to alleviate financial burdens.

Moreover, the increased adoption of digital pathology is driven by the integration of artificial intelligence (AI) technologies, which enhance diagnostic accuracy and efficiency. This trend is supported by the growing interest in cancer research activities, as digital pathology offers advanced tools for tissue analysis and data management. Companies like Proscia, which secured USD 50 million in funding, are at the forefront of this technological advancement, positioning themselves as key players in the market’s evolution.

Government-backed digitalization initiatives in emerging economies present a promising opportunity for market expansion. These initiatives aim to modernize healthcare infrastructure and improve access to advanced diagnostic tools, thereby driving the adoption of digital pathology. Entities that align their strategies with such governmental policies can capitalize on new market opportunities and expand their global footprint.

Lastly, data interoperability issues with existing laboratory systems remain a persistent barrier to seamless integration and information exchange. Partnerships, such as the one between Koninklijke Philips N.V. and Ibex, are crucial in addressing these challenges by enhancing system compatibility and facilitating efficient data flow across platforms.

Strategic Implications

The synthesis of these key signals underscores several strategic implications for stakeholders within the digital pathology market. Firstly, addressing the shortage of skilled pathologists and technicians is imperative for maintaining competitive advantage and operational efficiency. Companies should prioritize workforce development through targeted training programs and partnerships with educational institutions to ensure a steady pipeline of skilled professionals.

Regulatory and reimbursement uncertainties necessitate proactive engagement with regulatory bodies and continuous monitoring of policy changes. Entities that effectively navigate these complexities can differentiate themselves in the market by offering compliant and reliable solutions, as evidenced by Paige.AI’s regulatory success. Moreover, strategic collaborations with regulatory consultants and legal experts can aid in navigating this intricate landscape.

The high initial capital cost of digital pathology systems requires innovative financing solutions and strategic partnerships to mitigate financial risks. Leasing models, joint ventures, and public-private partnerships can provide viable alternatives for cost management, enabling broader market adoption without compromising financial stability.

To leverage the increasing adoption of digital pathology, companies must invest in AI-driven innovations that enhance diagnostic capabilities and streamline workflows. This investment not only improves product offerings but also strengthens competitive positioning in a technology-driven market. Additionally, aligning product development with government-backed digitalization initiatives can unlock growth opportunities in emerging economies and expand market reach.

Lastly, addressing data interoperability challenges is critical for enabling seamless integration and enhancing the overall efficiency of digital pathology systems. Collaborations with technology vendors and participation in industry consortia can facilitate the development of standardized protocols and improve system compatibility.

Forward Outlook

Looking ahead, the digital pathology market is poised to undergo significant transformations driven by technological advancements, regulatory developments, and evolving market demands. Stakeholders must remain agile and responsive to these changes to secure a favorable position in the competitive landscape.

The shortage of skilled professionals is likely to persist, necessitating continued investment in workforce development and training initiatives. Companies that successfully address this challenge will enhance their operational resilience and capacity to meet increasing demand for digital pathology services.

Regulatory and reimbursement landscapes are expected to evolve, with greater emphasis on compliance and patient safety. Entities that proactively engage with regulatory bodies and invest in robust compliance frameworks will benefit from enhanced credibility and market access. Furthermore, the integration of AI technologies will continue to shape the market, offering new opportunities for innovation and differentiation.

Government-backed digitalization efforts in emerging economies will drive market expansion, presenting lucrative opportunities for companies that align their strategies with these initiatives. By leveraging technological advancements and strategic partnerships, entities can tap into new markets and enhance their global presence.

Lastly, efforts to address data interoperability challenges will gain momentum, with increased collaboration among industry players to develop standardized solutions. These efforts will enhance system integration, improve data flow, and ultimately drive operational efficiency across the digital pathology value chain.

In conclusion, the digital pathology market’s future is characterized by both opportunities and challenges. Stakeholders must strategically navigate these dynamics to optimize their value chain, enhance operational efficiency, and secure a favorable position in this rapidly evolving landscape. By addressing bottlenecks,

Investment Activity

Investment Activity of the Global Digital Pathology Market

Executive Framing

The investment and funding dynamics within the digital pathology market have gained significant importance in recent years. This dimension is crucial as it directly impacts the pace of innovation, the adoption of new technologies, and the strategic direction of companies operating within this space. As digital pathology continues to evolve, the need for substantial capital investment becomes apparent, especially given the high capital intensity level required to develop cutting-edge AI-driven diagnostics, precision medicine platforms, and cloud-based solutions. This sector is marked by a rising investment trend, with notable increases in funding rounds and strategic partnerships that are reshaping the competitive landscape.

The market is currently witnessing an unprecedented surge in investment activities, driven by the growing demand for technologically advanced solutions and the need to address the shortage of pathologists through digital means. The strategic allocation of capital in digital pathology is not merely a financial exercise but a pivotal driver of market structure alteration. The influx of funds is enabling companies to expand their capabilities, invest in R&D, and forge strategic partnerships that enhance interoperability and service delivery.

This dimension matters now more than ever as it dictates the pace at which digital pathology can respond to healthcare challenges and capitalize on emerging opportunities. The presence of active investors such as Philips Healthcare, Roche Diagnostics, and Hamamatsu Photonics underscores the sector’s attractiveness, while recent M&A activity signals a consolidation trend aimed at achieving economies of scale and expanding market reach.

Current Market Reality

The current state of the digital pathology market is characterized by robust investment activity, driven by several key players and strategic themes. Active investors, including Philips Healthcare, Leica Biosystems, and Agilent Technologies, are at the forefront of this capital influx, channeling funds into innovations that promise to transform the diagnostic landscape. These companies are investing heavily in AI-driven diagnostics, precision medicine, and cloud-based imaging solutions, recognizing the potential of these technologies to deliver more accurate, efficient, and accessible diagnostic services.

A notable trend is the widespread adoption of digital workflows, which is revolutionizing the way pathology services are delivered. This shift is fueled by strategic partnerships with diagnostics companies and increased funding rounds, as organizations seek to leverage digital tools to streamline operations and improve patient outcomes. The market has seen a 54.8% increase in funding in 2024, with a doubling of funding in Q1 2025 compared to Q1 2024, reflecting renewed investor confidence and the sector’s growth potential.

Strategic investments by major Contract Research Organizations (CROs) are also shaping the market reality. These investments are aimed at enhancing service capabilities and expanding the reach of digital pathology solutions. Companies like Proscia, which secured USD 50 million in funding, exemplify the strategic focus on leveraging capital to drive innovation and market expansion. Additionally, partnerships such as the one between Koninklijke Philips N.V. and Ibex to enhance interoperability highlight the collaborative efforts to improve digital pathology infrastructure.

The market is further influenced by regulatory dynamics, such as the In Vitro Diagnostic Medical Devices Regulation (2017/746) and FDA approvals, which play a critical role in shaping the competitive landscape. These regulatory frameworks ensure that digital pathology solutions meet stringent quality and safety standards, thereby fostering investor confidence and encouraging further investment. The FDA approval of Paige.AI’s Paige Prostate in 2021, for instance, underscores the regulatory support for innovative diagnostic solutions, paving the way for increased adoption and market penetration.

Key Signals And Evidence

The digital pathology market is underpinned by several key signals that provide insights into the investment and funding dynamics at play. A primary signal is the doubling of funding in Q1 2025 compared to Q1 2024, which highlights the accelerated pace of investment and the growing confidence among investors in the sector’s potential. This surge in funding is indicative of a broader trend towards increased capital allocation to digital health solutions, driven by the need for more efficient and scalable diagnostic services.

Another critical signal is the 54.8% increase in funding in 2024, which reflects the heightened interest in digital pathology as a strategic area of investment. This increase is fueled by the widespread adoption of digital workflows, which are reshaping the operational frameworks of pathology services. As more healthcare providers transition to digital platforms, the demand for integrated and interoperable solutions is expected to rise, further driving investment in this area.

Strategic investments by major CROs are also a significant signal of the market’s direction. These investments not only enhance the service offerings of CROs but also signal a shift towards more collaborative and integrated service models. By investing in digital pathology, CROs can offer more comprehensive and efficient services, thereby attracting more clients and expanding their market presence.

Partnerships with diagnostics companies represent another key signal, as they facilitate the development and deployment of advanced diagnostic solutions. Such collaborations enable companies to combine expertise and resources, leading to the creation of more innovative and effective products. The partnership between Koninklijke Philips N.V. and Ibex, for example, aims to enhance interoperability, a crucial factor in ensuring seamless integration of digital pathology solutions into existing healthcare systems.

The strategic implications of these signals are profound, as they suggest a market that is rapidly evolving towards more integrated and technology-driven solutions. The increased funding rounds and strategic partnerships are indicative of a competitive environment where companies are vying for leadership positions through innovation and strategic alliances.

As the market continues to grow, stakeholders must navigate a complex landscape characterized by rapid technological advancements and shifting regulatory requirements. The digital pathology market’s current reality is one of dynamic change and opportunity, driven by significant investment and strategic initiatives. As companies and investors continue to prioritize this sector, the implications for market structure, competitive behavior, and technological innovation are profound.

The next sections will delve deeper into the strategic implications of these developments and outline the forward outlook for the digital pathology market, focusing on how stakeholders can best position themselves to capitalize on emerging opportunities and navigate potential challenges.

Strategic Implications

The strategic implications of the dynamic investment and funding landscape in digital pathology are multifaceted, affecting various stakeholders, including technology providers, healthcare organizations, investors, and regulatory bodies. As the market is propelled by significant capital influx, stakeholders must carefully consider their positions and strategies to ensure they can leverage the opportunities presented by these developments.

Firstly, the rising trend in investment and funding, characterized by a 54.8% increase in 2024 and a doubling of funding in Q1 2025 compared to Q1 2024, indicates a strong investor appetite for digital pathology solutions. This surge in capital is predominantly driven by the need to develop AI-driven diagnostics, cloud-based solutions, and precision medicine platforms. Companies such as Philips Healthcare, Roche Diagnostics, and Agilent Technologies are leading the charge through strategic investments and partnerships, positioning themselves as key players in this evolving market.

These organizations are not only expanding their technological capabilities but also enhancing their market reach through alliances with diagnostics companies and major CROs.

The strategic partnerships and collaborations in the market, such as the partnership between Koninklijke Philips N.V. and Ibex to enhance interoperability, highlight the importance of interoperability and integration in digital pathology solutions. This is crucial for healthcare providers seeking to implement seamless digital workflows and improve diagnostic accuracy.

As the market continues to evolve, companies that can offer integrated, interoperable solutions will likely gain a competitive edge, appealing to healthcare organizations looking to streamline operations and improve patient outcomes.

Moreover, the strategic investments by major CROs signal a growing recognition of the importance of digital pathology in clinical research and drug development. As CROs invest in digital pathology solutions, they are better positioned to offer advanced research capabilities, improve data accuracy, and enhance the efficiency of clinical trials. This trend underscores the strategic value of digital pathology in the broader healthcare ecosystem, where precision and efficiency are paramount.

However, stakeholders must also navigate potential challenges, including regulatory complexities and the shortage of pathologists. The adoption of digital pathology solutions is contingent upon regulatory approval, as evidenced by the FDA approval of Paige.AI’s Paige Prostate in 2021 and the IVDR certifications in the EU. Companies must ensure compliance with these regulations to bring their solutions to market successfully.

Furthermore, the shortage of pathologists presents both a challenge and an opportunity. While it underscores the need for automated and AI-driven solutions, it also necessitates investment in training and education to ensure the effective implementation of these technologies.

For investors, the current market dynamics present a compelling case for continued investment in digital pathology. The increasing focus on AI-driven diagnostics and precision medicine offers substantial growth potential, with opportunities for high returns on investment. However, investors must be discerning, identifying companies that not only have innovative technologies but also possess the strategic vision and operational capabilities to navigate the complexities of the healthcare landscape.

Forward Outlook

Looking ahead, the digital pathology market is poised for continued growth and transformation, driven by advancements in technology, strategic investments, and evolving healthcare needs. The forward outlook for this sector suggests several key trends and developments that stakeholders should monitor closely.

One of the most significant trends is the widespread adoption of digital workflows across healthcare organizations. As more institutions recognize the benefits of digital pathology, including improved diagnostic accuracy, faster turnaround times, and enhanced patient care, the demand for these solutions is expected to rise. This, in turn, will drive further investment in technology development and infrastructure, creating opportunities for companies to expand their offerings and capture a larger share of the market.

The increasing focus on precision medicine and AI-driven diagnostics will continue to shape the strategic direction of the market. Companies that can harness the power of AI to deliver personalized diagnostic solutions will likely lead the way, attracting investment and forging strategic partnerships. This shift towards precision medicine will also necessitate greater collaboration between technology providers, healthcare organizations, and regulatory bodies to ensure the successful integration of these solutions into clinical practice.

Additionally, the role of strategic partnerships will become increasingly important as companies seek to enhance their capabilities and extend their market reach. Collaborations between technology providers and healthcare institutions, as well as partnerships with diagnostics companies and major CROs, will be crucial in driving innovation and facilitating the adoption of digital pathology solutions. These alliances will enable companies to pool resources, share expertise, and accelerate the development of cutting-edge technologies.

However, stakeholders must also remain vigilant to potential challenges, particularly in terms of regulatory compliance and market competition. As the market becomes more crowded, companies will need to differentiate themselves by offering unique value propositions and demonstrating the clinical efficacy of their solutions. Regulatory hurdles will also require careful navigation, with companies needing to stay abreast of evolving standards and ensure compliance to avoid delays in market entry.

Technology & Innovation

Technology and Innovation Landscape in the Global Digital Pathology Market

Executive Framing

The digital pathology market is currently experiencing a transformative phase within the technology and innovation landscape. As healthcare systems globally grapple with a shortage of pathologists, the integration of advanced digital technologies is not merely beneficial but imperative. This dimension of digital pathology is crucial now because it serves as the linchpin for addressing critical operational challenges, enhancing diagnostic accuracy, and augmenting healthcare delivery efficiencies. The evolution from traditional pathology to digital methodologies is reshaping how medical professionals approach diagnosis, leading to faster and more reliable outcomes. This transition is primarily driven by the adoption of artificial intelligence (AI), machine learning (ML), and whole-slide imaging technologies, which are beginning to redefine diagnostic workflows and economic models in pathology.

In this era of rapid technological advancement, companies like Iron Mountain and Amazon Web Services (AWS) are playing pivotal roles by leveraging their robust cloud infrastructures to facilitate the secure and efficient storage and sharing of vast pathology data. Meanwhile, healthcare-focused entities like Roche, Paige, and Deep Bio are innovating with AI-driven solutions that aim to standardize and enhance diagnostic practices. These developments are not occurring in isolation; they are deeply intertwined with ongoing regulatory adjustments and a global push towards sustainable healthcare models. As such, understanding the current market dynamics within this dimension is essential for stakeholders aiming to align with future trends and capitalize on emerging opportunities.

Current Market Reality

The current state of the digital pathology market is a complex interplay of technological advancements and market demands. Central to this landscape are the advancements in AI-driven image analysis, which have significantly improved cancer detection capabilities. AI technologies are no longer experimental but are being increasingly integrated into standard pathology workflows. This integration is reflected in the FDA’s approval for primary diagnosis, underscoring the technology’s reliability and its potential to become a cornerstone of modern pathology practice.

Entities like Paige and Tempus exemplify the aggressive investment and innovation efforts currently underway. Paige’s acquisition by Tempus for USD 81.25 million demonstrates the high value placed on AI capabilities in pathology. This acquisition is not just a financial transaction but a strategic move aimed at consolidating AI-driven diagnostic capabilities to enhance personalized medicine approaches. Moreover, Paige’s earlier FDA approval for its prostate cancer diagnostic tool further validates the efficacy and regulatory acceptance of AI applications in this field.

Another significant entity, Roche, continues to push the boundaries of digital pathology through its AI and ML capabilities. Roche’s focus is on improving diagnostic speed and accuracy, which is critical in addressing the global shortage of pathologists. This shortage is a pressing issue that amplifies the need for technologies that can augment human intelligence and streamline diagnostic processes.

Iron Mountain and AWS are critical enablers in this ecosystem, providing the necessary digital infrastructure to support the storage and accessibility of large volumes of pathology data. Their involvement ensures that digital pathology solutions can be effectively scaled and integrated across various healthcare settings, thereby enhancing collaboration and data-driven decision-making.

In this context, the role of regulatory frameworks cannot be overlooked. The EU AI Act and GDPR are shaping how AI technologies are developed and deployed, ensuring that innovations are aligned with ethical guidelines and privacy standards. These regulations are crucial for maintaining transparency in AI applications, which is essential for building trust among healthcare providers and patients.

Key Signals and Evidence

The digital pathology landscape is pivoting on critical advancements in AI-driven technologies and strategic collaborations that illuminate a path to enhanced diagnostic capabilities. One of the most significant signals in this realm is the FDA’s approval for primary diagnosis using digital pathology systems. This milestone not only validates the reliability and safety of digital methodologies but also signals a broader acceptance and integration of these technologies into clinical workflows. It is a clear indication that the regulatory environment is progressively aligning with technological advancements, paving the way for increased adoption in medical institutions globally.

The global shortage of pathologists is another critical driver necessitating the transition towards digital pathology. This scarcity has heightened the demand for technologies that can augment human capabilities. AI-driven image analysis, for instance, is a key technology that has demonstrated substantial improvements in cancer detection, significantly enhancing diagnostic speed and accuracy. As the F1 accuracy of detection and classification reaches 77.4% and 83%, respectively, the potential for AI to standardize diagnoses and reduce error rates becomes increasingly apparent. This not only benefits patient outcomes but also alleviates the workload on existing pathologists, thereby addressing the shortage issue.

Furthermore, the integration of AI algorithms into digital pathology workflows is evidenced by metrics such as a Mean Average Precision (MAP) of 0.95 on the ICPR-12 dataset and an Average Precision (AP) of 0.81. These metrics underscore the capability of AI to deliver precise and reliable results, which is crucial for the acceptance of these technologies in clinical settings. Companies like Paige and Tempus are at the forefront of these innovations. Paige’s acquisition by Tempus for USD 81.25 million exemplifies the strategic moves being made to consolidate AI capabilities and expand the reach of digital pathology solutions.

Another pivotal development is the emphasis on transparency in AI applications, which is becoming increasingly important given the regulatory frameworks like the GDPR and the EU AI Act. These regulations are driving companies to ensure that AI systems are not only effective but also ethical and transparent. The development of Good Machine Learning Practices is a step towards achieving this goal, ensuring that AI technologies are used responsibly within the healthcare domain.

Strategic Implications

The strategic implications of these developments are profound, impacting stakeholders across the healthcare ecosystem. For healthcare providers, the adoption of AI-driven digital pathology solutions can lead to significant improvements in diagnostic throughput and accuracy. By leveraging these technologies, hospitals can offer quicker turnaround times for test results, directly enhancing patient care and satisfaction. Moreover, the integration of AI and digital pathology can facilitate remote consultations, expanding access to specialized care in underserved regions and potentially reducing healthcare disparities.

For technology companies, the growing demand for digital pathology solutions presents a lucrative opportunity to innovate and capture market share. Companies like Amazon Web Services and Iron Mountain, with their cloud-based collaboration platforms, are well-positioned to support the infrastructure needs of digital pathology implementations. These platforms enable seamless data integration and sharing, essential for the collaborative nature of modern healthcare practices.

Pharmaceutical companies and research institutions can also benefit from these advancements. The ability of AI to integrate diverse patient data for personalized treatment plans offers a new dimension for drug development and clinical trials. By utilizing digital pathology data, these entities can enhance the precision of their research, leading to more effective therapeutics and interventions.

However, stakeholders must also be cognizant of the challenges and risks associated with the rapid adoption of digital pathology technologies. Ensuring data privacy and security in a digital environment is paramount, especially given the sensitive nature of medical information. Companies must invest in robust cybersecurity measures and comply with evolving regulatory standards to mitigate these risks.

Forward Outlook

Looking ahead, the digital pathology market is poised for continued growth, driven by the maturation of AI technologies and the increasing integration of digital solutions in healthcare. As AI-driven algorithms become more sophisticated, their ability to enhance diagnostic accuracy and efficiency will likely accelerate the adoption of digital pathology systems. This technological evolution will be instrumental in addressing the global shortage of pathologists, enabling healthcare systems to maintain high standards of care amidst growing demand.

In the near-to-medium term, we can anticipate a surge in strategic partnerships and collaborations aimed at furthering the development and deployment of digital pathology solutions. These alliances will be crucial in creating interoperable systems that facilitate seamless data exchange and integration across platforms. As evidenced by the partnership between Koninklijke Philips N.V. and Ibex, such collaborations will be key to overcoming current technological limitations and expanding the scope of digital pathology applications.

Moreover, the regulatory landscape will continue to play a pivotal role in shaping the future of digital pathology. As regulations like the EU AI Act and GDPR evolve, they will drive the industry towards greater transparency and ethical AI practices. Companies that can navigate these regulatory waters effectively will gain a competitive edge, setting new standards for responsible innovation in healthcare.

In summary, the digital pathology market is on the cusp of a transformative era, with AI and digital technologies at its core. The strategic implications for stakeholders are vast, offering opportunities to enhance diagnostic capabilities, improve patient outc

Market Risk

Risk Factors and Disruption Threats in the Global Digital Pathology Market

Executive Framing

The digital pathology market, a rapidly evolving sector within the healthcare industry, is currently navigating a landscape fraught with structural risks and potential disruptions. As the industry progresses towards 2026 and beyond, the interplay of technological advancements and regulatory frameworks will define its trajectory. The high overall market risk level indicates that stakeholders must be acutely aware of the potential for volatility and unpredictability in this domain. While digital pathology promises to enhance diagnostic accuracy and efficiency through AI and machine learning, it simultaneously faces significant challenges such as lack of regulation, high implementation costs, and technological limitations.

These factors not only threaten market stability but also pose risks to operational resilience and competitive dynamics. The moderate geopolitical exposure level further complicates the market scenario, as international collaborations and cross-border data sharing are integral to the growth of digital pathology. Moreover, the high substitution risk level underscores the vulnerability of traditional pathology practices to being overshadowed by digital and AI-driven methodologies. As the healthcare landscape becomes increasingly digitized, the imperative to address these structural constraints and mitigate associated risks becomes more pressing. The need for ethical AI practices, institutional support, and regulatory clarity will be pivotal in steering the market towards a sustainable future.

Current Market Reality

At present, the digital pathology market is characterized by a juxtaposition of promise and peril. Companies like Paige.AI and Proscia are at the forefront of this digital revolution, with Paige.AI having achieved a significant milestone through FDA approval of its Paige Prostate product in 2021. This endorsement not only validates the technological capabilities of digital pathology solutions but also sets a precedent for future regulatory alignments. Similarly, Proscia’s securing of USD 50 million in funding signals investor confidence in the potential of digital pathology to transform diagnostic paradigms.

However, the lack of regulation remains a critical impediment, creating uncertainties around compliance and operational legality. The absence of a cohesive regulatory framework can lead to disparate standards and practices, undermining the credibility and reliability of digital pathology solutions. This gap highlights the urgent need for collaboration between AI developers and regulatory bodies to establish robust guidelines that ensure safety, efficacy, and ethical AI deployment.

Furthermore, the evolving job market dynamics pose another layer of complexity. The fear of job market reduction for pathologists due to automation and AI integration is palpable, yet contradictory signals such as the growing need for pathologists specializing in Digital and AI Pathology (DAIP) suggest a potential realignment rather than a reduction. This dichotomy underscores the necessity for ongoing training and change management to equip pathologists with the skills required in a digital-first landscape.

Additionally, the high implementation costs associated with adopting digital pathology solutions present a formidable barrier to entry for many healthcare institutions. While advancements in AI algorithms have increased diagnostic accuracy and workflow efficiency, the financial burden of transitioning to digital systems can deter widespread adoption. Here, the focus on reducing implementation costs becomes crucial, necessitating strategic investments in quality equipment and collaboration with institutions to foster shared capabilities and resources.

Key Signals And Evidence

The digital pathology market is at a crossroads where structural constraints and market dynamics are shaping its future. A primary signal of concern is the lack of regulation, which presents a significant risk to stakeholders. The absence of comprehensive guidelines can lead to inconsistencies in AI deployment and varying standards of practice, potentially undermining trust and reliability in the technology. This regulatory gap invites a high substitution risk, where unregulated or poorly regulated AI solutions might replace traditional pathology methods without adequate validation.

The market’s reaction to this uncertainty is evident in the increased collaboration between AI developers and institutions, as they seek to establish best practices and create frameworks that could preempt regulatory directives.

Collaboration between AI developers and institutions emerges as a vital signal, signifying a concerted effort to bridge the gap between technology and practice. This collaboration is essential for developing AI tools that are not only technically sound but also clinically relevant. Institutions play a crucial role in providing real-world insights, ensuring that AI solutions align with clinical workflows and deliver tangible benefits. The partnership between Koninklijke Philips N.V. and Ibex, aimed at enhancing interoperability, exemplifies how collaborative efforts are driving the integration of AI into existing healthcare systems.