Global Network as a Service Market size and share Analysis 2026-2033

Global Network as a Service Market Forecast Snapshot: 2026???2033

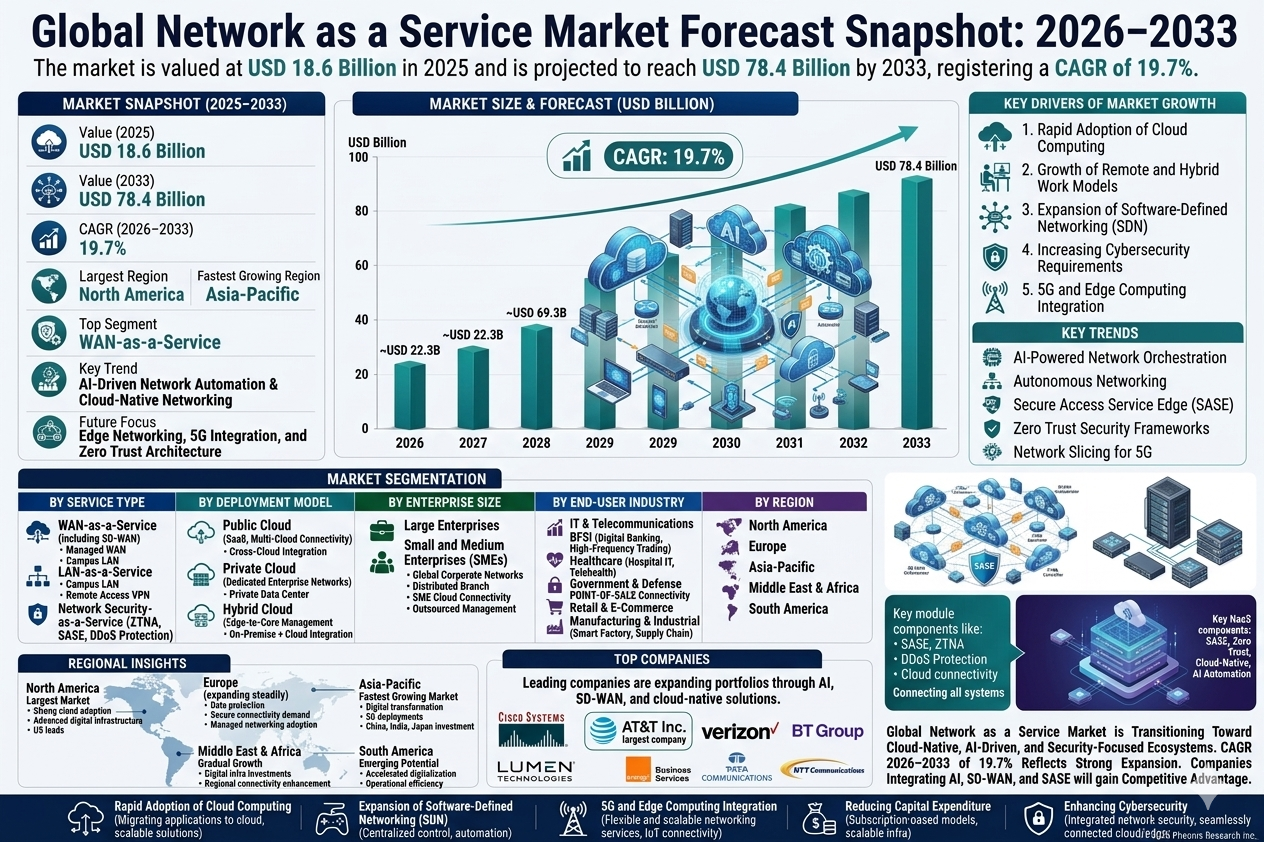

| Metric | Value |

| 2025 Market Size | USD 18.6 Billion |

| 2033 Market Size | USD 78.4 Billion |

| CAGR (2026???2033) | 19.7% |

| Largest Region | North America |

| Fastest Growing Region | Asia-Pacific |

| Top Segment | WAN-as-a-Service |

| Key Trend | AI-Driven Network Automation & Cloud-Native Networking |

| Future Focus | Edge Networking, 5G Integration, and Zero Trust Architecture |

Global Network as a Service Market Overview

Global Network as a Service Market is the new way companies handle networks, shifting to cloud-based networking for flexibility, scalability, and saving money. You outsource network management and pay like a utility bill ??? only for what you use, making it flexible, cost-efficient, and hassle-free, letting experts manage networks while you focus on biz.According to Pheonix Research, the Global Network as a Service Market is valued at USD 18.6 billion in 2025 and is projected to reach USD 78.4 billion by 2033, registering a CAGR of 19.7% during 2026???2033. Growth is fueled by increasing enterprise adoption of cloud computing, remote workforce expansion, and demand for agile networking solutions.

North America currently dominates the market due to advanced digital infrastructure, strong cloud adoption, and the presence of major technology providers. Meanwhile, Asia-Pacific is emerging as the fastest-growing region, driven by digital transformation, 5G deployment, and rapid expansion of enterprise IT infrastructure. The post-2025 outlook highlights increasing adoption of AI-powered network orchestration, software-defined networking (SDN), edge connectivity solutions, and zero-trust security frameworks, positioning NaaS as a key enabler of next-generation enterprise connectivity.Key Drivers of Global Network as a Service Market Growth

1. Rapid Adoption of Cloud Computing

Enterprises are migrating applications and workloads to cloud environments, increasing demand for scalable and cloud-integrated networking solutions.

2. Growth of Remote and Hybrid Work Models

Organizations require secure and flexible connectivity solutions to support distributed workforces and remote operations.

3. Expansion of Software-Defined Networking (SDN)

SDN technologies enable centralized network control and automation, improving efficiency and reducing operational complexity.

4. Increasing Cybersecurity Requirements

Zero-trust network architectures and secure access services are becoming essential as cyber threats continue to rise.

5. 5G and Edge Computing Integration

The growth of 5G networks and edge computing infrastructure is accelerating demand for flexible and scalable networking services.

Global Network as a Service Market Segmentation

?? 1.By Service Type

1.1 Wide Area Network (WAN)-as-a-Service

1.1.1 Managed WAN Services

1.1.1.1 Enterprise WAN Connectivity

1.1.1.2 Multi-Branch Networking

1.1.2 Software-Defined WAN (SD-WAN)

1.1.2.1 Cloud-Based SD-WAN Platforms

1.1.2.2 Hybrid WAN Infrastructure

1.2 Local Area Network (LAN)-as-a-Service

1.2.1 Managed LAN Solutions

1.2.1.1 Campus Network Management

1.2.1.2 Office Connectivity Solutions

1.2.2 Wireless LAN Services

1.2.2.1 Enterprise Wi-Fi Management

1.2.2.2 Smart Building Connectivity

1.3 Virtual Private Network (VPN)-as-a-Service

1.3.1 Secure Remote Access Solutions

1.3.1.1 Corporate Remote Workforce

1.3.1.2 Secure Mobile Access

1.3.2 Encrypted Data Transmission Services

1.3.2.1 Enterprise Data Security

1.3.2.2 Cross-Border Data Connectivity

1.4 Network Security-as-a-Service

1.4.1 Firewall-as-a-Service

1.4.2 Zero Trust Network Access (ZTNA)

1.4.3 Secure Access Service Edge (SASE)

1.4.4 Distributed Denial of Service (DDoS) Protection

?? ??2.By Deployment Model

2.1 Public Cloud

2.1.1 Cloud-Based Network Platforms

2.1.1.1 Public Cloud Networking Infrastructure

2.1.1.1.1 Enterprise Cloud Connectivity

2.1.1.1.2 SaaS Application Networking

2.1.2 Multi-Cloud Connectivity Solutions

2.1.2.1 Cross-Cloud Network Integration

2.1.2.1.1 Multi-Cloud Enterprise Deployments

2.1.2.1.2 Cloud Traffic Optimization Platforms

2.2 Private Cloud

2.2.1 Enterprise Private Network Services

2.2.1.1 Dedicated Corporate Networks

2.2.1.1.1 Financial Institution Networks

2.2.1.1.2 Government Secure Data Networks

2.2.2 Dedicated Network Infrastructure

2.2.2.1 Private Data Center Networking

2.2.2.1.1 Enterprise Data Center Connectivity

2.2.2.1.2 Mission-Critical IT Infrastructure

2.3 Hybrid Cloud

2.3.1 Integrated Cloud Networking

2.3.1.1 Hybrid Cloud Connectivity Platforms

2.3.1.1.1 On-Premise + Cloud Integration

2.3.1.1.2 Enterprise Hybrid IT Infrastructure

2.3.2 Edge-to-Core Network Management

2.3.2.1 Distributed Edge Networking

2.3.2.1.1 Edge Computing Data Networks

2.3.2.1.2 Industrial IoT Edge Connectivity

?? 3.By Enterprise Size

3.1 Large Enterprises

3.1.1 Global Corporate Networks

3.1.1.1 Multinational Enterprise Connectivity

3.1.1.1.1 Cross-Region Data Networks

3.1.1.1.2 Global Cloud Infrastructure

3.1.2 Multi-Branch Enterprise Infrastructure

3.1.2.1 Distributed Branch Networking

3.1.2.1.1 Retail Branch Connectivity

3.1.2.1.2 Banking Branch Infrastructure

3.2 Small and Medium Enterprises (SMEs)

3.2.1 Cloud-Based Networking Solutions

3.2.1.1 SaaS-Based Network Platforms

3.2.1.1.1 Startup IT Infrastructure

3.2.1.1.2 SME Cloud Connectivity

3.2.2 Managed Connectivity Services

3.2.2.1 Outsourced Network Management

3.2.2.1.1 Managed Security Services

3.2.2.1.2 Managed SD-WAN Platforms

?? ??4.By End-User Industry

4.1 IT & Telecommunications

4.1.1 Cloud Service Providers

4.1.1.1 Hyperscale Cloud Infrastructure

4.1.1.1.1 AI Data Center Connectivity

4.1.1.1.2 Edge Cloud Networking

4.1.2 Telecom Operators

4.1.2.1 5G Network Infrastructure

4.1.2.1.1 Mobile Core Network Connectivity

4.1.2.1.2 Telecom Edge Network Platforms

4.2 BFSI

4.2.1 Digital Banking Infrastructure

4.2.1.1 Secure Financial Networks

4.2.1.1.1 Online Banking Platforms

4.2.1.1.2 Payment Processing Networks

4.2.2 Financial Trading Infrastructure

4.2.2.1 High-Speed Data Networks

4.2.2.1.1 High-Frequency Trading Platforms

4.2.2.1.2 Global Financial Data Exchange

4.3 Healthcare

4.3.1 Hospital IT Infrastructure

4.3.1.1 Electronic Health Record Networks

4.3.1.1.1 Hospital Data Connectivity

4.3.1.1.2 Medical Imaging Networks

4.3.2 Telehealth Platforms

4.3.2.1 Remote Healthcare Connectivity

4.3.2.1.1 Telemedicine Services

4.3.2.1.2 Remote Patient Monitoring Networks

4.4 Government & Defense

4.4.1 Government Digital Infrastructure

4.4.1.1 Public Sector Data Networks

4.4.1.1.1 Smart Government Platforms

4.4.1.1.2 Citizen Digital Services

4.4.2 Defense Communication Systems

4.4.2.1 Secure Military Networks

4.4.2.1.1 Tactical Communication Systems

4.4.2.1.2 Defense Data Networks

4.5 Retail & E-Commerce

4.5.1 Retail Store Networks

4.5.1.1 Point-of-Sale Connectivity

4.5.1.1.1 Omnichannel Retail Systems

4.5.1.1.2 Smart Store Infrastructure

4.5.2 E-Commerce Platforms

4.5.2.1 Online Marketplace Infrastructure

4.5.2.1.1 Digital Payment Connectivity

4.5.2.1.2 Logistics Data Networks

4.6 Manufacturing & Industrial

4.6.1 Smart Factory Networks

4.6.1.1 Industrial IoT Connectivity

4.6.1.1.1 Automated Production Systems

4.6.1.1.2 Robotics Communication Networks

4.6.2 Supply Chain Connectivity

4.6.2.1 Logistics Data Networks

4.6.2.1.1 Warehouse Automation Systems

4.6.2.1.2 Industrial Edge Connectivity

?? ?? ??5.By Region

5.1 North America

5.2 Europe

5.3 Asia-Pacific

5.4 Middle East & Africa

5.5 South America

Regional Insights of Global Network as a Service Market

North America ??? Largest Market

??North America holds the largest share of the Global Network as a Service Market, supported by strong cloud adoption, advanced digital infrastructure, and the presence of major technology and telecom service providers. The United States leads the region with widespread enterprise adoption of SD-WAN, cloud networking, and AI-driven network management platforms.

Asia-Pacific ??? Fastest Growing Market

Asia-Pacific is emerging as the fastest-growing region due to rapid digital transformation, expanding enterprise IT ecosystems, and large-scale 5G deployments. Countries such as China, India, Japan, and South Korea are investing heavily in cloud infrastructure and next-generation networking technologies.

Europe

The European market is expanding steadily, driven by strong regulatory frameworks for data protection, increasing demand for secure enterprise connectivity, and rising adoption of managed networking services across industries.

Middle East & Africa

Growth in the Middle East & Africa is supported by smart city initiatives, digital infrastructure investments, and the expansion of telecom networks aimed at enhancing regional connectivity.

South America

South America is witnessing gradual market growth as enterprises accelerate digitalization efforts and adopt cloud-based networking solutions to improve operational efficiency and connectivity.

Leading Companies in the Global Network as a Service Market

-

Verizon Communications

-

BT Group

-

Lumen Technologies

-

Orange Business Services

-

Tata Communications

-

NTT Communications

Leading companies are expanding their service portfolios through AI-driven network management platforms, SD-WAN integration, and cloud-native networking solutions. AT&T Inc. (USA) is the largest company in the Global Network as a Service Market.

Strategic Intelligence & AI-Backed Insights

Pheonix Demand Forecast Engine identifies cloud adoption, edge computing expansion, and SD-WAN deployment as primary long-term growth drivers.

Infrastructure Investment Analyzer highlights increasing enterprise investment in scalable and subscription-based networking solutions.

Innovation Tracker emphasizes AI-driven network orchestration, autonomous networking, and secure access service edge (SASE) platforms as key competitive differentiators.

Porter???s Five Forces Analysis indicates strong competition among global telecom providers, moderate entry barriers, and increasing differentiation through innovation and service integration.

Why the Global Network as a Service Market is Critical

-

Enables scalable and flexible enterprise networking infrastructure.

-

Reduces capital expenditure through subscription-based models.

-

Supports remote work and distributed enterprise operations.

-

Enhances cybersecurity through integrated network security solutions.

-

Enables seamless connectivity across cloud, edge, and enterprise environments.

Final Takeaway of Global Network as a Service Market

The Global Network as a Service Market is rapidly transitioning toward cloud-native, AI-driven, and security-focused networking ecosystems. The Network as a Service CAGR 2026???2033 of 19.7% reflects strong expansion supported by digital transformation, cloud adoption, and evolving enterprise connectivity requirements. Companies that effectively integrate AI-powered network automation, SD-WAN technologies, zero-trust security frameworks, and edge networking capabilities will be well positioned for long-term competitive advantage. At Pheonix Research, our advanced forecasting frameworks provide in-depth Network as a Service revenue forecast analysis, competitive benchmarking, and strategic intelligence, enabling stakeholders to capitalize on the Post-2025 networking landscape with confidence.???? Social Mentions & Publication Channels

??Explore deeper insights and follow our cross-platform updates on LinkedIn and X??for continuous intelligence and market coverage.

LinkedIn : https://www.linkedin.com/feed/update/urn:li:activity:7436640393368252416

X : https://x.com/Pheonix_Insight/status/2030877002346136037?s=20

Competitive Landscape

Global Network as a Service Market Competitive Intensity & Market Structure Overview

The Global Network as a Service (NaaS) Market is characterized by a highly competitive and rapidly evolving digital infrastructure ecosystem, driven by cloud adoption, enterprise digital transformation, and the increasing need for scalable and software-defined networking solutions. The market is shifting from traditional hardware-centric networking models toward flexible, subscription-based, and cloud-native connectivity services.

Competitive intensity is high due to the convergence of telecom operators, cloud service providers, cybersecurity firms, and enterprise networking companies. Vendors compete on network scalability, automation capability, security integration, service reliability, and multi-cloud interoperability.

The market structure is moderately consolidated, with large global telecom and networking providers dominating enterprise-grade deployments through extensive infrastructure ownership and integrated service portfolios. However, emerging cloud-native networking providers and managed service firms are increasingly gaining market traction through AI-driven orchestration, SD-WAN innovation, and agile deployment models.

Global Network as a Service Market Competitive Intensity & Market Structure Current Scenario

Leading Company Profiles

Cisco Systems: Global Networking Technology Leader. Strong presence in SD-WAN, cloud networking, AI-driven network automation, and enterprise connectivity platforms.

AT&T Inc.: Largest Market Playerhttps://www.att.com/. Expanding managed NaaS solutions through integrated telecom infrastructure, private networking, and 5G-enabled enterprise services.

Verizon Communications: Telecommunications Infrastructure Provider. Focused on secure enterprise connectivity, edge networking, and managed SD-WAN solutions.

BT Group: Global Connectivity Provider. Strong in cloud-integrated networking services, multinational enterprise connectivity, and cybersecurity-enabled NaaS platforms.

Lumen Technologies: Cloud and Edge Networking Specialist. Expanding edge computing, AI-enabled networking, and low-latency enterprise connectivity solutions.

Orange Business Services: Enterprise Digital Infrastructure Provider. Focused on hybrid cloud networking, secure connectivity, and international managed network services.

Tata Communications: Global Enterprise Connectivity Provider. Known for large-scale global network infrastructure and cloud-based enterprise networking solutions.

NTT Communications: Managed Network Services Leader. Expanding AI-powered networking, data center interconnectivity, and enterprise cloud networking capabilities.

Key Competitive Intensity & Market Structure Signals in Global Network as a Service Market

A major structural signal in the market is the rapid transition toward cloud-native and software-defined networking architectures. Enterprises are increasingly replacing traditional hardware-based networking systems with scalable and subscription-driven NaaS platforms.

The growing adoption of hybrid work environments and distributed enterprise operations is intensifying competition among providers to deliver secure, flexible, and globally scalable connectivity solutions.

Another major competitive signal is the rising integration of AI-driven network automation and orchestration platforms. Vendors capable of delivering predictive analytics, automated traffic management, and self-optimizing networks are gaining competitive advantages.

Cybersecurity integration has become a critical differentiator. Zero Trust Network Access (ZTNA), Secure Access Service Edge (SASE), and cloud-native security services are increasingly embedded within NaaS offerings to address rising enterprise security concerns.

The rapid deployment of 5G and edge computing infrastructure is also reshaping market dynamics. Enterprises require low-latency, edge-enabled networking services capable of supporting IoT ecosystems, industrial automation, and real-time analytics applications.

Despite growing innovation, large telecom and networking providers continue to dominate due to their global infrastructure footprint, carrier-grade reliability, and enterprise customer relationships.

Strategic Implications of Competitive Intensity & Market Structure in Global Network as a Service Market

The competitive environment is driving providers toward integrated digital networking ecosystems rather than standalone connectivity services. Vendors are increasingly combining networking, cybersecurity, cloud integration, and AI-driven management into unified NaaS platforms.

Total cost of ownership (TCO) is becoming a critical purchasing factor for enterprises. Subscription-based NaaS models reduce capital expenditure while improving scalability, operational agility, and network management efficiency.

5G expansion and edge computing adoption are reshaping infrastructure investment priorities. Providers are accelerating investments in edge networking nodes, low-latency architectures, and distributed cloud connectivity platforms.

Strategic alliances between telecom operators, hyperscale cloud providers, and cybersecurity firms are becoming increasingly important. Collaborative ecosystems enable faster deployment of integrated enterprise networking solutions and strengthen long-term service revenues.

Additionally, AI-driven autonomous networking capabilities are emerging as a major competitive frontier, enabling predictive maintenance, traffic optimization, and real-time network performance management.

Global Network as a Service Market Competitive Intensity & Market Structure Forward Outlook

The Global Network as a Service Market is expected to remain highly competitive and innovation-driven as enterprises accelerate digital transformation, cloud migration, and distributed networking adoption.

Market consolidation is likely to increase as telecom operators and networking technology companies expand capabilities through acquisitions, cloud partnerships, and AI networking investments.

AI-powered network automation, SD-WAN integration, edge networking, and zero-trust security frameworks will become the primary drivers of future competitive differentiation.

Private 5G networks, intelligent edge connectivity, and cloud-native networking ecosystems are expected to create significant long-term growth opportunities across enterprise, industrial, and public sector environments.

In the long term, the market will be defined by three core competitive pillars: cloud-native networking, AI-driven automation, and integrated cybersecurity architecture. Companies that successfully combine scalable global infrastructure with intelligent software-defined networking capabilities will lead the Global Network as a Service Market through 2033.

Value Chain

Global Network as a Service Market Value Chain & Supply Chain Evolution Overview

The Global Network as a Service (NaaS) Market value chain is evolving from traditional hardware-centric networking models toward cloud-native, software-defined, AI-driven, and subscription-based connectivity ecosystems. This transformation is primarily driven by enterprise digital transformation, cloud migration, remote workforce expansion, 5G deployment, and increasing demand for scalable, flexible, and secure network infrastructure.

Network as a Service solutions enable enterprises to consume networking infrastructure, connectivity, and security capabilities through subscription-based delivery models rather than investing in large-scale on-premise networking hardware. NaaS platforms increasingly integrate SD-WAN, cloud networking, network security, edge connectivity, AI-driven orchestration, and zero-trust frameworks into unified service architectures.

The value chain extends beyond conventional telecom infrastructure into cloud computing ecosystems, hyperscale data centers, AI-based network management, cybersecurity integration, edge computing infrastructure, and software-defined networking platforms. Leading companies such as Cisco Systems, AT&T Inc., Verizon Communications, BT Group, Lumen Technologies, Orange Business Services, Tata Communications, and NTT Communications are expanding integrated networking ecosystems through strategic cloud and telecom partnerships.

Upstream supply chain activities increasingly depend on cloud infrastructure providers, telecom equipment manufacturers, fiber-optic network suppliers, edge infrastructure developers, AI orchestration software vendors, and cybersecurity technology providers. Network infrastructure modernization and automation are becoming critical for supporting dynamic enterprise connectivity demands.

Service delivery is increasingly centered around cloud-native platforms, SD-WAN orchestration, multi-cloud integration, edge-to-core connectivity management, and automated network optimization technologies. Enterprises are increasingly prioritizing flexible networking architectures that support hybrid work environments, distributed enterprise operations, and real-time digital applications.

Key supply chain challenges include cybersecurity risks, integration complexity across multi-cloud environments, network latency optimization, interoperability management, telecom infrastructure modernization costs, and regulatory compliance across global regions.

Global Network as a Service Market Value Chain & Supply Chain Evolution Current Scenario

The current NaaS ecosystem is shaped by rapid cloud adoption, rising enterprise digitalization, increasing cybersecurity concerns, and accelerating deployment of software-defined networking technologies.

Upstream infrastructure providers are increasingly investing in fiber networks, cloud interconnection infrastructure, edge computing platforms, and AI-powered network orchestration systems to support scalable and low-latency networking services.

Service providers are strengthening integration between SD-WAN, SASE, zero-trust security frameworks, cloud networking platforms, and AI-driven network automation technologies to improve service agility and operational efficiency.

Enterprise demand is rising across BFSI, healthcare, retail, manufacturing, telecom, and government sectors due to the need for secure, scalable, and flexible connectivity solutions that support hybrid cloud environments and remote workforces.

Telecom operators and managed service providers are increasingly transitioning from hardware deployment models toward subscription-based, cloud-managed networking services that reduce enterprise capital expenditure and improve scalability.

AI-driven traffic optimization, predictive network maintenance, and intelligent security monitoring are emerging as critical competitive differentiators across next-generation NaaS platforms.

Key Value Chain & Supply Chain Evolution Signals in Global Network as a Service Market

Several transformative trends are reshaping the NaaS ecosystem globally.

First, cloud-native networking architectures are replacing traditional hardware-centric enterprise networking models.

Second, AI-driven network automation and autonomous orchestration technologies are increasingly optimizing network performance, scalability, and operational efficiency.

Third, SD-WAN and SASE adoption are accelerating due to growing enterprise demand for secure and flexible distributed connectivity.

Fourth, 5G deployment and edge computing expansion are driving demand for low-latency, intelligent, and scalable networking infrastructures.

Fifth, zero-trust cybersecurity frameworks are becoming core components of enterprise networking strategies as cyber threats continue to increase globally.

Strategic Implications of Value Chain & Supply Chain Evolution in Global Network as a Service Market

Industry leaders such as Cisco Systems, AT&T Inc., Verizon Communications, BT Group, Lumen Technologies, Orange Business Services, Tata Communications, and NTT Communications are strengthening competitive positioning through AI-driven networking platforms, SD-WAN integration, cloud-native service architectures, and advanced cybersecurity capabilities.

Competitive advantage increasingly depends on scalable cloud infrastructure, telecom backbone strength, AI-powered automation capabilities, multi-cloud interoperability, and integrated security frameworks.

Companies capable of delivering unified networking, security, edge connectivity, and cloud integration services through subscription-based models are best positioned to capture long-term enterprise demand.

Strategic partnerships between telecom operators, hyperscale cloud providers, cybersecurity vendors, and edge infrastructure developers are becoming increasingly important for ecosystem expansion and service differentiation.

Long-term success will increasingly rely on balancing network scalability, cybersecurity resilience, operational efficiency, latency optimization, and cost-effective service delivery across diverse enterprise environments.

Global Network as a Service Market Value Chain & Supply Chain Evolution Forward Outlook

Between 2026 and 2033, the NaaS value chain is expected to become increasingly cloud-centric, AI-orchestrated, edge-enabled, and security-integrated.

Service providers will increasingly prioritize autonomous network management, predictive AI analytics, intelligent traffic routing, cloud-native security integration, and edge computing optimization to enhance service performance and enterprise scalability.

5G-enabled enterprise networking, private cellular networks, IoT connectivity platforms, and distributed edge architectures will further expand NaaS deployment opportunities across industrial, commercial, and public infrastructure sectors.

AI-driven network analytics and self-healing network architectures will increasingly improve operational reliability, cybersecurity resilience, and bandwidth optimization.

Subscription-based networking models will continue gaining enterprise adoption due to lower capital expenditure requirements, faster deployment flexibility, and simplified infrastructure management.

Ultimately, the future NaaS value chain will evolve from outsourced connectivity services into intelligent, autonomous, and fully integrated digital networking ecosystems.

Market-Specific Value Chain

- Infrastructure & Hardware Supply: Fiber-optic infrastructure, telecom equipment, routers, switches, edge computing infrastructure, data center hardware

- Cloud & Software Platform Development: SD-WAN platforms, cloud-native networking software, AI orchestration systems, SASE platforms, zero-trust security frameworks

- Network Integration & Service Deployment: Multi-cloud integration, edge connectivity deployment, enterprise network orchestration, managed networking services, hybrid cloud networking

- Enterprise Connectivity Services: WAN-as-a-Service, LAN-as-a-Service, VPN-as-a-Service, secure remote access, private 5G networking

- Security & Network Optimization: AI-driven traffic management, cybersecurity monitoring, predictive maintenance, performance analytics, intelligent routing optimization

- Lifecycle Management & Support Services: Managed services, software updates, technical support, network monitoring, scalability optimization, compliance management

Company-to-Stage Mapping

- Infrastructure & Hardware Supply: Cisco Systems, Ericsson, Verizon Communications, AT&T Inc.

- Cloud & Software Platform Development: Cisco Systems, Lumen Technologies, NTT Communications, BT Group

- Network Integration & Service Deployment: Orange Business Services, Tata Communications, Verizon Communications, AT&T Inc.

- Enterprise Connectivity Services: AT&T Inc., Verizon Communications, BT Group, Orange Business Services

- Security & Network Optimization: Cisco Systems, Lumen Technologies, NTT Communications, Tata Communications

- Lifecycle Management & Support Services: BT Group, Orange Business Services, Verizon Communications, managed network ecosystem partners

Investment Activity

Global Network as a Service Market Investment & Funding Dynamics Overview

Investment and funding activity in the Global Network as a Service Market is accelerating rapidly as enterprises transition toward cloud-native networking, AI-driven network automation, and scalable subscription-based connectivity models. Between 2026 and 2033, capital investment is expected to rise significantly across SD-WAN infrastructure, edge networking platforms, secure access service edge (SASE) ecosystems, and zero trust network architectures.

The market is evolving into a strategic digital infrastructure segment supported by increasing enterprise cloud migration, remote workforce expansion, 5G deployment, and growing demand for agile networking environments. Leading companies such as Cisco Systems, AT&T Inc., Verizon Communications, BT Group, Lumen Technologies, Orange Business Services, Tata Communications, and NTT Communications are investing heavily in AI-powered network orchestration, cloud-native connectivity platforms, and intelligent security-integrated networking services.

A major structural shift influencing investment activity is the increasing adoption of software-defined networking (SDN) and edge computing architectures. This transformation is directing funding toward automated network management platforms, multi-cloud connectivity systems, low-latency edge infrastructure, and cybersecurity-focused networking solutions capable of supporting highly distributed enterprise environments.

Global Network as a Service Market Investment & Funding Dynamics Current Scenario

Current investment momentum is being driven by enterprise digital transformation, rising demand for flexible networking infrastructure, and rapid deployment of cloud-integrated connectivity platforms across industries.

- North America: Leads investment activity due to strong cloud adoption, mature telecom infrastructure, and increasing enterprise deployment of SD-WAN, SASE, and AI-driven network management systems.

- Asia-Pacific: Witnessing the fastest investment growth supported by rapid digitalization, large-scale 5G rollout, and expanding enterprise IT ecosystems across China, India, Japan, and South Korea.

- Europe: Strong investment activity is driven by rising demand for secure enterprise connectivity, regulatory focus on cybersecurity, and increasing cloud infrastructure modernization.

- Middle East & Africa: Emerging investment opportunities are supported by smart city initiatives, telecom infrastructure modernization, and growing cloud connectivity adoption.

Key Investment & Funding Dynamics Signals in Global Network as a Service Market

- Rapid enterprise cloud migration is accelerating investment in scalable cloud-native networking infrastructure and multi-cloud connectivity platforms.

- Expansion of remote and hybrid work environments is driving funding toward secure remote access solutions and zero trust network architectures.

- Telecom operators and enterprises are increasing capital expenditure on SD-WAN deployment and AI-powered network orchestration technologies.

- Growing edge computing adoption is creating investment opportunities in low-latency edge networking and distributed infrastructure management systems.

- Integration of cybersecurity frameworks such as SASE and ZTNA is becoming a major funding priority across enterprise networking ecosystems.

- 5G infrastructure expansion is supporting long-term investment in intelligent network automation and next-generation enterprise connectivity solutions.

Strategic Implications of Investment & Funding Dynamics in Global Network as a Service Market

- The investment landscape increasingly favors companies with strong capabilities in AI-driven networking automation and cloud-native infrastructure platforms.

- Development of integrated SD-WAN and SASE ecosystems is becoming a major competitive differentiator among global networking providers.

- Strategic partnerships between telecom operators, hyperscale cloud providers, and cybersecurity vendors are increasing globally.

- Regional infrastructure diversification is becoming critical as enterprises seek resilient and distributed networking ecosystems.

- Investment in edge computing and low-latency connectivity infrastructure is becoming essential to support Industry 4.0, IoT, and real-time digital applications.

- Companies focusing on autonomous networking, predictive analytics, and AI-enabled traffic optimization are expected to strengthen long-term market positioning.

Global Network as a Service Market Investment & Funding Dynamics Forward Outlook

Looking ahead, the Global Network as a Service Market is expected to attract sustained investment as cloud computing, edge connectivity, AI-based automation, and zero trust security frameworks continue reshaping enterprise networking infrastructure.

Future funding activity will increasingly focus on autonomous networking platforms, AI-powered network analytics, secure edge connectivity systems, 5G-integrated enterprise networking, and intelligent multi-cloud orchestration technologies.

- North America: Will continue leading investment activity supported by advanced cloud ecosystems, AI-driven networking innovation, and strong enterprise digital infrastructure spending.

- Asia-Pacific: Will remain the fastest-growing investment region driven by large-scale digital transformation initiatives, rapid telecom expansion, and accelerating 5G deployment.

- Europe: Will strengthen investment in secure enterprise networking, regulatory-compliant cloud infrastructure, and next-generation cybersecurity-integrated connectivity platforms.

Technological advancements in AI-powered network orchestration, software-defined infrastructure, edge-to-core networking systems, and zero trust security frameworks will continue influencing capital allocation strategies across the industry.

Overall, the market will remain a strategically critical digital infrastructure investment segment through 2033, supported by its essential role in enabling cloud transformation, secure enterprise connectivity, and next-generation intelligent networking ecosystems. Companies leading in AI automation, SD-WAN integration, cybersecurity innovation, and cloud-native networking platforms will shape the future competitive landscape.

Technology & Innovation

Global Network as a Service Market Technology & Innovation Landscape Overview

The technology and innovation landscape within the Global Network as a Service (NaaS) Market is evolving rapidly as enterprises transition from traditional hardware-centric networking models toward cloud-native, software-defined, and subscription-based connectivity ecosystems. Network as a Service solutions are enabling organizations to deploy scalable, flexible, and secure networking infrastructure while reducing operational complexity and capital expenditure.

Innovation intensity across the NaaS ecosystem is accelerating due to rising cloud adoption, hybrid workforce expansion, edge computing growth, and increasing demand for agile enterprise connectivity. Leading companies such as Cisco Systems, AT&T, Verizon Communications, BT Group, Tata Communications, and NTT Communications are investing heavily in AI-driven network orchestration, software-defined networking (SDN), secure access service edge (SASE), and cloud-integrated networking platforms.

A major technological transformation is the convergence of AI-powered automation, cloud-native networking, 5G integration, and zero-trust security frameworks. This evolution is enabling NaaS platforms to move beyond conventional connectivity services toward intelligent, self-optimizing, and policy-driven network ecosystems capable of supporting dynamic enterprise workloads and distributed digital operations.

Simultaneously, advancements in edge networking, network virtualization, API-driven infrastructure management, and real-time analytics are improving scalability, performance visibility, and service agility across enterprise networking environments.

Global Network as a Service Market Technology & Innovation Landscape Current Scenario

Currently, the Network as a Service industry is focused on improving network flexibility, operational automation, cybersecurity resilience, and multi-cloud connectivity. Vendors are prioritizing technologies that enhance enterprise agility while simplifying network deployment and management.

AI-driven network automation is one of the most significant innovation areas. Advanced machine learning algorithms and predictive analytics platforms are enabling autonomous traffic management, anomaly detection, self-healing capabilities, and intelligent bandwidth optimization across enterprise networks.

Software-defined WAN (SD-WAN) technologies are gaining strong momentum by enabling centralized control, cloud-optimized connectivity, and application-aware traffic routing. These innovations are helping enterprises improve performance while reducing dependence on legacy MPLS infrastructure.

Cloud-native networking architectures are transforming enterprise connectivity through virtualized network functions, scalable cloud integration, and API-driven orchestration platforms. Organizations are increasingly adopting hybrid and multi-cloud networking solutions to support distributed digital operations and remote work environments.

Zero Trust Network Access (ZTNA) and Secure Access Service Edge (SASE) platforms are emerging as major innovation pillars. These security-centric networking models combine secure connectivity, identity verification, and policy-based access control to address evolving cybersecurity threats.

Edge networking and 5G integration are also reshaping the market by enabling ultra-low latency connectivity, distributed data processing, and real-time communication for IoT devices, industrial automation systems, and smart infrastructure applications.

Real-time network analytics, programmable networking interfaces, and intent-based networking technologies are improving visibility, automation, and service customization across enterprise and telecom environments.

Key Technology & Innovation Trends in Global Network as a Service Market

- AI-Driven Network Automation: Autonomous traffic optimization, predictive maintenance, and intelligent network orchestration.

- Software-Defined WAN (SD-WAN): Cloud-optimized connectivity and centralized network management platforms.

- Cloud-Native Networking: Virtualized network infrastructure supporting hybrid and multi-cloud environments.

- Zero Trust Security Architecture: Identity-based secure access frameworks and continuous authentication systems.

- Secure Access Service Edge (SASE): Integrated networking and cybersecurity delivered through cloud-native platforms.

- 5G & Edge Networking Integration: Low-latency connectivity supporting IoT, edge computing, and industrial automation.

- Network Virtualization & NFV: Flexible deployment of virtual network functions reducing hardware dependency.

- Real-Time Network Analytics: Performance monitoring, traffic visibility, and AI-powered operational intelligence.

Strategic Implications of Technology & Innovation

The technological evolution of Network as a Service is reshaping enterprise networking from static infrastructure environments into intelligent, service-oriented connectivity ecosystems capable of supporting digital transformation and distributed business operations.

For enterprises, advanced NaaS platforms provide scalable solutions for hybrid workforces, cloud migration, multi-site operations, and secure remote connectivity. Telecom providers and technology vendors that deliver AI-driven automation, integrated security, and cloud-native scalability are likely to strengthen long-term competitive positioning.

As enterprise networking becomes increasingly software-defined and security-focused, competitive barriers are rising due to infrastructure complexity, cybersecurity requirements, interoperability challenges, and continuous innovation demands.

Governments and enterprises are increasingly viewing next-generation networking infrastructure as strategic digital infrastructure essential for cloud computing, smart cities, industrial IoT, and national digital transformation initiatives.

Cybersecurity resilience, regulatory compliance, and operational reliability are becoming strategic priorities as organizations increasingly depend on cloud-based and distributed networking environments.

Global Network as a Service Market Technology & Innovation Forward Outlook

Looking ahead, the Global Network as a Service Market is expected to evolve toward fully autonomous, AI-driven, and security-centric networking ecosystems. Future NaaS platforms will increasingly function as intelligent digital connectivity layers supporting cloud-native enterprises, edge infrastructure, industrial IoT, and hyper-connected business environments.

AI-powered orchestration, edge computing integration, and advanced 5G networking capabilities will likely drive the next phase of innovation, enabling dynamic bandwidth allocation, real-time service optimization, and ultra-low latency enterprise communication.

Mass adoption scalability will depend heavily on seamless multi-cloud interoperability, cybersecurity integration, service reliability, and simplified subscription-based deployment models.

Hybrid enterprise networking, industrial edge connectivity, and secure remote workforce infrastructure are expected to become major growth areas, while autonomous networking and intent-based management platforms may emerge as transformative technologies across the market.

In conclusion, the Global Network as a Service Market is transitioning from traditional enterprise networking infrastructure into a scalable intelligent connectivity ecosystem. Companies that lead in AI-powered automation, cloud-native networking, zero-trust security, and edge-integrated connectivity solutions will shape the future of enterprise networking through 2033.

Regulatory Landscape

Global Network as a Service Market Investment & Funding Dynamics Overview

Investment and funding activity in the Global Network as a Service Market is accelerating rapidly as enterprises transition toward cloud-native networking, AI-driven network automation, and scalable subscription-based connectivity models. Between 2026 and 2033, capital investment is expected to rise significantly across SD-WAN infrastructure, edge networking platforms, secure access service edge (SASE) ecosystems, and zero trust network architectures.

The market is evolving into a strategic digital infrastructure segment supported by increasing enterprise cloud migration, remote workforce expansion, 5G deployment, and growing demand for agile networking environments. Leading companies such as Cisco Systems, AT&T Inc., Verizon Communications, BT Group, Lumen Technologies, Orange Business Services, Tata Communications, and NTT Communications are investing heavily in AI-powered network orchestration, cloud-native connectivity platforms, and intelligent security-integrated networking services.

A major structural shift influencing investment activity is the increasing adoption of software-defined networking (SDN) and edge computing architectures. This transformation is directing funding toward automated network management platforms, multi-cloud connectivity systems, low-latency edge infrastructure, and cybersecurity-focused networking solutions capable of supporting highly distributed enterprise environments.

Global Network as a Service Market Investment & Funding Dynamics Current Scenario

Current investment momentum is being driven by enterprise digital transformation, rising demand for flexible networking infrastructure, and rapid deployment of cloud-integrated connectivity platforms across industries.

- North America: Leads investment activity due to strong cloud adoption, mature telecom infrastructure, and increasing enterprise deployment of SD-WAN, SASE, and AI-driven network management systems.

- Asia-Pacific: Witnessing the fastest investment growth supported by rapid digitalization, large-scale 5G rollout, and expanding enterprise IT ecosystems across China, India, Japan, and South Korea.

- Europe: Strong investment activity is driven by rising demand for secure enterprise connectivity, regulatory focus on cybersecurity, and increasing cloud infrastructure modernization.

- Middle East & Africa: Emerging investment opportunities are supported by smart city initiatives, telecom infrastructure modernization, and growing cloud connectivity adoption.

Key Investment & Funding Dynamics Signals in Global Network as a Service Market

- Rapid enterprise cloud migration is accelerating investment in scalable cloud-native networking infrastructure and multi-cloud connectivity platforms.

- Expansion of remote and hybrid work environments is driving funding toward secure remote access solutions and zero trust network architectures.

- Telecom operators and enterprises are increasing capital expenditure on SD-WAN deployment and AI-powered network orchestration technologies.

- Growing edge computing adoption is creating investment opportunities in low-latency edge networking and distributed infrastructure management systems.

- Integration of cybersecurity frameworks such as SASE and ZTNA is becoming a major funding priority across enterprise networking ecosystems.

- 5G infrastructure expansion is supporting long-term investment in intelligent network automation and next-generation enterprise connectivity solutions.

Strategic Implications of Investment & Funding Dynamics in Global Network as a Service Market

- The investment landscape increasingly favors companies with strong capabilities in AI-driven networking automation and cloud-native infrastructure platforms.

- Development of integrated SD-WAN and SASE ecosystems is becoming a major competitive differentiator among global networking providers.

- Strategic partnerships between telecom operators, hyperscale cloud providers, and cybersecurity vendors are increasing globally.

- Regional infrastructure diversification is becoming critical as enterprises seek resilient and distributed networking ecosystems.

- Investment in edge computing and low-latency connectivity infrastructure is becoming essential to support Industry 4.0, IoT, and real-time digital applications.

- Companies focusing on autonomous networking, predictive analytics, and AI-enabled traffic optimization are expected to strengthen long-term market positioning.

Global Network as a Service Market Investment & Funding Dynamics Forward Outlook

Looking ahead, the Global Network as a Service Market is expected to attract sustained investment as cloud computing, edge connectivity, AI-based automation, and zero trust security frameworks continue reshaping enterprise networking infrastructure.

Future funding activity will increasingly focus on autonomous networking platforms, AI-powered network analytics, secure edge connectivity systems, 5G-integrated enterprise networking, and intelligent multi-cloud orchestration technologies.

- North America: Will continue leading investment activity supported by advanced cloud ecosystems, AI-driven networking innovation, and strong enterprise digital infrastructure spending.

- Asia-Pacific: Will remain the fastest-growing investment region driven by large-scale digital transformation initiatives, rapid telecom expansion, and accelerating 5G deployment.

- Europe: Will strengthen investment in secure enterprise networking, regulatory-compliant cloud infrastructure, and next-generation cybersecurity-integrated connectivity platforms.

Technological advancements in AI-powered network orchestration, software-defined infrastructure, edge-to-core networking systems, and zero trust security frameworks will continue influencing capital allocation strategies across the industry.

Overall, the market will remain a strategically critical digital infrastructure investment segment through 2033, supported by its essential role in enabling cloud transformation, secure enterprise connectivity, and next-generation intelligent networking ecosystems. Companies leading in AI automation, SD-WAN integration, cybersecurity innovation, and cloud-native networking platforms will shape the future competitive landscape.