Global Robotic Arm Market Size and Share Analysis 2026-2033

Global Robotic Arm Market Size & Forecast

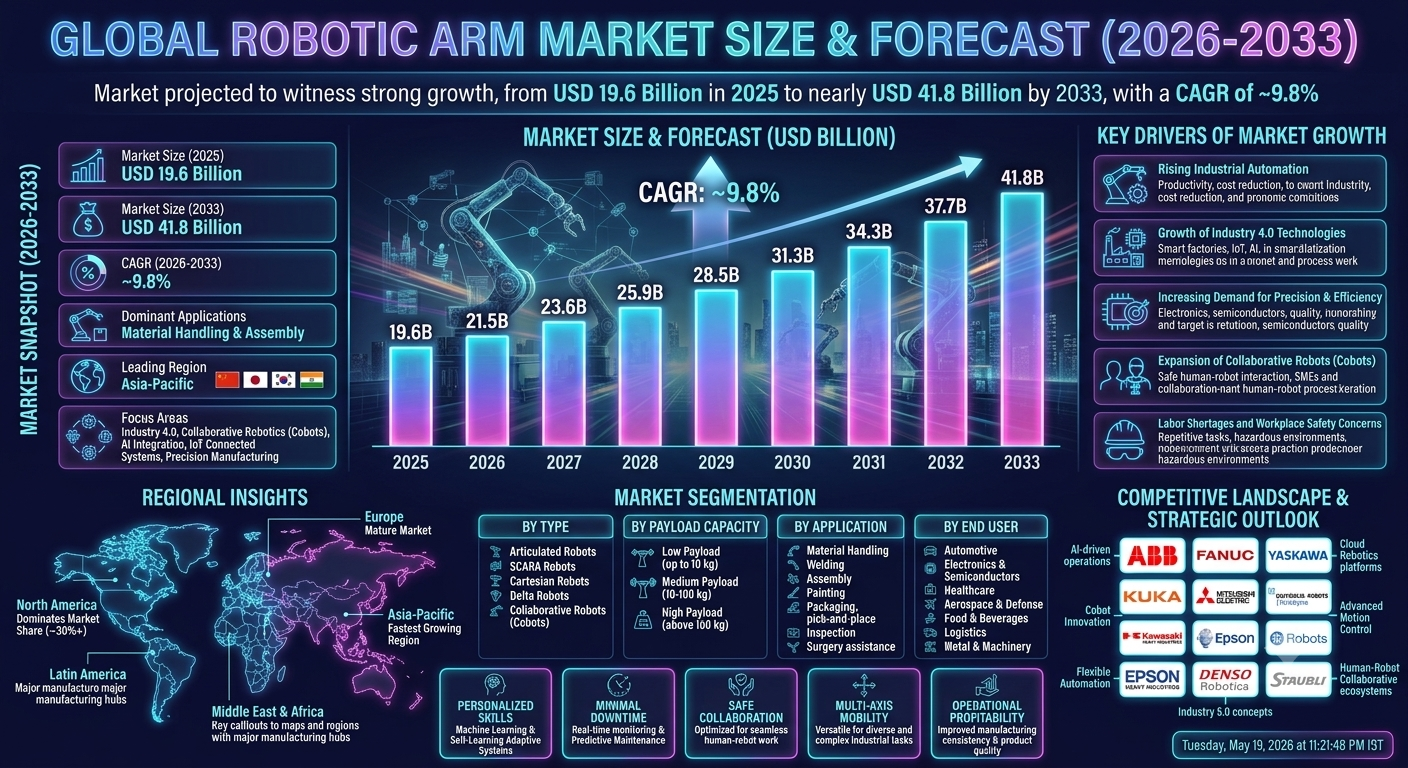

The global robotic arm market is projected to witness strong and sustained growth during the forecast period from 2026 to 2033. The market was valued at approximately USD 19.6 billion in 2025 and is expected to reach nearly USD 41.8 billion by 2033, expanding at a CAGR of around 9.8%. The market’s growth is driven by rapid industrial automation, rising demand for precision manufacturing, increasing adoption of Industry 4.0 technologies, and expanding use of robotics across automotive, electronics, healthcare, and logistics sectors. Robotic arms are programmable mechanical devices designed to perform automated tasks such as assembly, welding, painting, material handling, packaging, surgery assistance, and inspection. These systems replicate human arm movement with high precision and are widely used to improve productivity, safety, and operational efficiency across industries. The market is undergoing rapid transformation due to advancements in artificial intelligence, machine vision, sensor technology, and collaborative robotics (cobots), enabling safer human-robot interaction and greater flexibility in industrial environments.

Global Robotic Arm Market Overview

The robotic arm market is a key segment of the global industrial automation and robotics industry. It plays a critical role in enhancing manufacturing efficiency, reducing labor costs, and improving production consistency across multiple sectors. The market includes industrial robotic arms, collaborative robots (cobots), articulated robots, SCARA robots, Cartesian robots, and delta robots used in various applications ranging from heavy manufacturing to precision electronics assembly. Integration of AI, IoT, cloud robotics, and real-time data analytics is enabling smarter, more adaptive robotic systems capable of self-learning and predictive maintenance. The increasing shortage of skilled labor in manufacturing industries and rising safety concerns in hazardous work environments are further accelerating adoption globally. Major market participants include ABB Ltd., FANUC Corporation, Yaskawa Electric Corporation, KUKA AG, Mitsubishi Electric, Universal Robots (Teradyne), Kawasaki Heavy Industries, Epson Robots, DENSO Robotics, and Staubli International.Key Drivers of Global Robotic Arm Market Growth

Rising Industrial Automation

Manufacturers are increasingly adopting automation to improve productivity, reduce operational costs, and enhance product quality. Robotic arms are essential components in automated production lines across automotive, electronics, and heavy industries.Growth of Industry 4.0 Technologies

The adoption of smart factories, connected manufacturing systems, and cyber-physical production environments is driving demand for advanced robotic arms. Integration with IoT and AI is enabling real-time monitoring and intelligent decision-making in industrial operations.Increasing Demand for Precision and Efficiency

Industries such as electronics, semiconductors, and pharmaceuticals require high-precision operations that robotic arms can perform consistently without errors. This is significantly improving production quality and reducing waste.Expansion of Collaborative Robots (Cobots)

Cobots designed to safely work alongside humans are gaining popularity in SMEs and flexible manufacturing environments. They are easier to program, cost-effective, and suitable for small-scale automation needs.Labor Shortages and Workplace Safety Concerns

Global labor shortages in manufacturing and increasing focus on workplace safety are accelerating the shift toward robotic automation. Robotic arms help reduce human exposure to hazardous environments and repetitive strain tasks.Global Robotic Arm Market Segmentation

By Type

The market is segmented into articulated robots, SCARA robots, Cartesian robots, delta robots, and collaborative robots (cobots). Articulated robots dominate the market due to their flexibility, multi-axis movement, and wide industrial applications.By Payload Capacity

The market includes low payload (up to 10 kg), medium payload (10–100 kg), and high payload (above 100 kg) robotic arms. Medium payload robots account for a major share due to their versatility in manufacturing applications.By Application

Applications include material handling, welding, assembly, painting, packaging, pick-and-place, inspection, and surgery assistance. Material handling and assembly applications dominate due to widespread industrial usage.By End User

End users include automotive, electronics & semiconductors, healthcare, aerospace & defense, food & beverages, logistics, and metal & machinery industries. Automotive and electronics sectors represent the largest demand base for robotic arms.Regional Market Dynamics

Asia-Pacific

Asia-Pacific dominates the global robotic arm market due to strong manufacturing infrastructure, rapid industrialization, and high adoption of automation technologies. China, Japan, South Korea, and India are major contributors, with China leading global robot installations.North America

North America holds a significant market share driven by advanced manufacturing systems, strong robotics innovation, and high labor costs encouraging automation. The United States is a key market supported by automotive, aerospace, and electronics industries.Europe

Europe represents a mature robotics market with strong adoption in automotive manufacturing and industrial automation. Germany, Italy, France, and the Nordic countries are key contributors, with Germany leading industrial robotics deployment.Latin America

Latin America is witnessing gradual adoption of robotic arms driven by modernization of manufacturing and automotive industries. Brazil and Mexico are leading regional markets.Middle East & Africa

The region is slowly expanding its robotics adoption, supported by industrial diversification efforts and investments in smart manufacturing and logistics.Competitive Landscape

The global robotic arm market is highly competitive and dominated by established industrial automation companies and robotics manufacturers. Key players include ABB Ltd., FANUC Corporation, Yaskawa Electric Corporation, KUKA AG, Mitsubishi Electric, Universal Robots (Teradyne), Kawasaki Heavy Industries, Epson Robots, DENSO Robotics, and Staubli International. Companies are focusing on AI integration, cobot development, advanced motion control systems, and cloud-based robotics platforms to enhance competitiveness. Strategic partnerships, acquisitions, and R&D investments are central to maintaining technological leadership in the market.Strategic Outlook

The strategic outlook for the global robotic arm market remains highly positive due to increasing automation demand and technological advancements in robotics and AI. Future opportunities include autonomous manufacturing systems, AI-driven predictive robotics, cloud robotics, and human-robot collaborative ecosystems. The expansion of smart factories and Industry 5.0 concepts is expected to further enhance the role of robotic arms in industrial ecosystems. Companies investing in flexible automation, software-defined robotics, and intelligent control systems are expected to gain strong competitive advantages.Final Market Perspective

The global robotic arm market is rapidly evolving as industries transition toward fully automated, intelligent, and connected manufacturing systems. Rising demand for efficiency, precision, and safety will continue to drive adoption across multiple industrial sectors throughout the forecast period. Organizations that successfully combine robotics innovation, AI integration, and scalable automation solutions will remain strongly positioned in the evolving global robotics ecosystem.Table of Contents

Table of Contents

- 1. Executive Summary

- 1.1 Global Robotic Arm Market Snapshot (2026-2033)

- 1.2 Market Size & CAGR Analysis

- 1.3 Largest & Fastest-Growing Segments

- 1.4 Key Regional Insights

- 1.5 Market Growth Drivers

- 1.6 Competitive Landscape Overview

- 1.7 Future Industry Outlook

- 2. Introduction & Market Overview

- 2.1 Definition of Robotic Arms

- 2.2 Scope of the Study

- 2.3 Evolution of Industrial Robotics

- 2.4 Robotic Arm Industry Ecosystem

- 2.5 Value Chain Analysis

- 2.6 Industry 4.0 & Smart Manufacturing Trends

- 2.7 Regulatory & Safety Framework

- 3. Research Methodology

- 3.1 Primary Research

- 3.2 Secondary Research

- 3.3 Market Estimation Methodology

- 3.4 Forecast Assumptions (2026-2033)

- 3.5 Data Validation & Market Triangulation

- 4. Market Dynamics

- 4.1 Drivers

- 4.1.1 Rising Industrial Automation

- 4.1.2 Growth of Industry 4.0 Technologies

- 4.1.3 Increasing Demand for Precision & Efficiency

- 4.1.4 Expansion of Collaborative Robots (Cobots)

- 4.1.5 Labor Shortages & Workplace Safety Concerns

- 4.2 Restraints

- 4.2.1 High Initial Investment Costs

- 4.2.2 Complex Integration Requirements

- 4.2.3 Skilled Workforce Gap

- 4.2.4 Maintenance & Downtime Challenges

- 4.3 Opportunities

- 4.3.1 AI-Driven Autonomous Robotics

- 4.3.2 Cloud Robotics & IoT Integration

- 4.3.3 Expansion in SMEs Adoption of Cobots

- 4.3.4 Smart Factory & Industry 5.0 Adoption

- 4.4 Challenges

- 4.4.1 Cybersecurity Risks in Connected Systems

- 4.4.2 Rapid Technological Obsolescence

- 4.4.3 Regulatory & Safety Compliance Issues

- 4.4.4 High Dependency on Capital Investment Cycles

- 4.1 Drivers

- 5. Global Robotic Arm Market Analysis (USD Billion), 2026-2033

- 5.1 Market Size Overview

- 5.2 CAGR Analysis

- 5.3 Revenue Distribution by Region

- 5.4 Segment-Wise Revenue Analysis

- 5.5 Demand & Adoption Trends

- 5.6 Technology Innovation Trends

- 6. Market Segmentation (USD Billion), 2026-2033

- 6.1 By Type

- 6.1.1 Articulated Robots

- 6.1.2 SCARA Robots

- 6.1.3 Cartesian Robots

- 6.1.4 Delta Robots

- 6.1.5 Collaborative Robots (Cobots)

- 6.2 By Payload Capacity

- 6.2.1 Low Payload (Up to 10 kg)

- 6.2.2 Medium Payload (10–100 kg)

- 6.2.3 High Payload (Above 100 kg)

- 6.3 By Application

- 6.3.1 Material Handling

- 6.3.2 Welding

- 6.3.3 Assembly

- 6.3.4 Painting

- 6.3.5 Packaging

- 6.3.6 Pick-and-Place

- 6.3.7 Inspection

- 6.3.8 Surgery Assistance

- 6.4 By End User

- 6.4.1 Automotive

- 6.4.2 Electronics & Semiconductors

- 6.4.3 Healthcare

- 6.4.4 Aerospace & Defense

- 6.4.5 Food & Beverages

- 6.4.6 Logistics

- 6.4.7 Metal & Machinery

- 6.1 By Type

- 7. Market Segmentation by Geography

- 7.1 North America

- 7.2 Europe

- 7.3 Asia-Pacific

- 7.4 Latin America

- 7.5 Middle East & Africa

- 8. Competitive Landscape

- 8.1 Market Share Analysis

- 8.2 Product Innovation Benchmarking

- 8.3 AI & Smart Robotics Technology Analysis

- 8.4 Strategic Partnerships & Collaborations

- 8.5 Brand Positioning Strategies

- 9. Company Profiles

- 9.1 ABB Ltd.

- 9.2 FANUC Corporation

- 9.3 Yaskawa Electric Corporation

- 9.4 KUKA AG

- 9.5 Mitsubishi Electric

- 9.6 Universal Robots (Teradyne)

- 9.7 Kawasaki Heavy Industries

- 9.8 Epson Robots

- 9.9 DENSO Robotics

- 9.10 Staubli International

- 10. Strategic Intelligence & Pheonix AI Insights

- 10.1 AI-Based Robotics Performance Analytics

- 10.2 Predictive Maintenance Systems

- 10.3 Smart Factory Optimization Engines

- 10.4 Autonomous Robotics Development Tracker

- 10.5 Competitive Automation Benchmarking System

- 11. Future Outlook & Strategic Recommendations

- 11.1 Expansion of Smart Manufacturing Ecosystems

- 11.2 Growth of AI-Integrated Robotics Systems

- 11.3 Adoption of Industry 5.0 Human-Robot Collaboration

- 11.4 Cloud Robotics & Edge Computing Integration

- 11.5 Long-Term Market Outlook (2033+)

- 12. Appendix

- 13. About Pheonix Research

- 14. Disclaimer

Competitive Landscape

Global Robotic Arm Market Competitive Intensity & Market Structure Overview

The global robotic arm market is highly competitive, technology-intensive, and strongly consolidated among a group of established industrial automation leaders. The market structure is characterized by multinational robotics manufacturers, industrial automation giants, and emerging collaborative robotics (cobot) innovators. Competition is primarily driven by technological innovation, precision performance, payload versatility, software integration, pricing efficiency, and after-sales service ecosystems.

The industry spans both traditional industrial robotic arms used in large-scale manufacturing and next-generation collaborative robots designed for flexible, human-assistive environments. While large enterprises dominate high-payload and heavy-duty applications, cobots and lightweight robotic arms are rapidly expanding adoption among small and medium-sized manufacturers.

The market is undergoing a major transition toward AI-enabled robotics, cloud-connected automation systems, and smart manufacturing ecosystems under Industry 4.0 and emerging Industry 5.0 frameworks. Software capabilities, including machine vision, predictive maintenance, and real-time adaptive control, are becoming as important as mechanical performance.

Global Robotic Arm Market Competitive Intensity & Market Structure Current Scenario

Leading Robotic Arm Manufacturers & Industrial Automation Companies

ABB Ltd.: One of the global leaders in industrial robotics, offering a broad portfolio of robotic arms for manufacturing, automotive, electronics, and logistics automation with strong AI and digital integration capabilities.

FANUC Corporation: A dominant player in factory automation and robotic arms, known for high reliability, precision engineering, and extensive deployment in automotive and electronics industries.

Yaskawa Electric Corporation: Major robotics manufacturer specializing in motion control, industrial robotic arms, and automation systems widely used in welding, assembly, and material handling.

KUKA AG: Key European robotics company offering advanced robotic arms for automotive manufacturing, smart factories, and integrated automation systems.

Mitsubishi Electric: Strong competitor in industrial robotics and automation systems with applications across electronics, semiconductors, and precision manufacturing.

Universal Robots (Teradyne): Leading innovator in collaborative robots (cobots), focusing on flexible, safe, and easy-to-program robotic arms for SMEs and light industrial applications.

Kawasaki Heavy Industries: Established robotics provider with strong presence in industrial automation, heavy-duty robotic arms, and precision manufacturing systems.

Epson Robots: Specializes in SCARA and compact robotic arms used in electronics assembly, packaging, and high-speed precision tasks.

DENSO Robotics: Automotive-focused robotics company providing high-precision robotic arms for assembly, welding, and production line automation.

Staubli International: Known for high-performance robotic arms used in demanding industrial environments including pharmaceuticals, aerospace, and electronics manufacturing.

Key Competitive Intensity & Market Structure Drivers

One of the most important competitive factors in the robotic arm market is continuous innovation in AI-driven automation, machine vision systems, and adaptive motion control technologies. Companies that integrate advanced intelligence into robotic systems are gaining significant market advantage.

Product differentiation based on payload capacity, precision, speed, and flexibility remains a key competitive battleground, particularly across automotive, semiconductor, and electronics manufacturing sectors.

The rise of collaborative robots is intensifying competition by lowering entry barriers for SMEs, enabling new vendors to compete with established industrial automation leaders in specific segments.

Software ecosystems, including robotics operating systems, cloud connectivity, and predictive maintenance platforms, are becoming critical differentiators beyond hardware capabilities.

Global supply chain integration, customization capabilities, and service network strength also play a crucial role in maintaining competitiveness in large-scale industrial deployments.

Strategic Implications of Competitive Intensity & Market Structure

Companies are increasingly investing in AI-integrated robotics platforms, edge computing, and cloud-based robotic management systems to enhance operational intelligence and scalability.

Strategic partnerships with semiconductor manufacturers, automotive OEMs, and electronics companies are expanding application-specific robotic solutions and accelerating deployment across high-growth industries.

R&D investments in human-robot interaction safety systems, force sensing technologies, and energy-efficient robotics are shaping next-generation product development.

The growing importance of cobots is driving a dual-market structure where high-end industrial robots and flexible collaborative systems evolve in parallel, serving distinct but increasingly overlapping use cases.

Asia-Pacific is emerging as both a major manufacturing hub and innovation center, intensifying global competition as regional manufacturers scale rapidly in industrial automation and robotics deployment.

Global Robotic Arm Market Competitive Intensity & Market Structure Forward Outlook

The global robotic arm market is expected to become increasingly intelligent, autonomous, and software-defined as robotics converges with artificial intelligence, IoT, and cloud computing technologies.

Future competition will be shaped by advancements in autonomous manufacturing systems, predictive robotics, digital twin integration, and fully connected smart factory ecosystems.

The expansion of Industry 5.0 concepts will further emphasize human-robot collaboration, personalization of manufacturing processes, and adaptive production systems.

Market consolidation is likely to continue as major automation companies acquire AI startups, robotics software firms, and cobot innovators to strengthen their technological capabilities.

Overall, the market will remain highly competitive yet structurally stable, dominated by global robotics leaders with strong R&D capabilities and integrated automation ecosystems. Companies that successfully combine mechanical precision, AI intelligence, and scalable software platforms will remain strongly positioned in the evolving global robotic arm market.

Value Chain

Global Robotic Arm Market Value Chain & Supply Chain Evolution Overview

The global robotic arm market value chain is evolving from a traditional hardware-centric industrial machinery ecosystem into a highly integrated, software-enabled, AI-driven automation network. This transformation is being driven by rapid industrial automation, Industry 4.0 adoption, increasing demand for precision manufacturing, and the growing shift toward smart factories and connected production systems across global industries.

The value chain begins with upstream raw material sourcing, which includes high-grade steel, aluminum, specialized alloys, semiconductors, sensors, actuators, servo motors, control chips, wiring systems, and precision electronic components. These inputs form the foundation of robotic arm performance, durability, and precision. Semiconductor suppliers and advanced electronics manufacturers play a critical role in enabling motion control, AI processing, and machine vision capabilities.

The manufacturing and assembly layer represents the core of the robotic arm ecosystem and includes mechanical design engineering, robotic structure fabrication, motor integration, sensor embedding, controller development, firmware programming, and system calibration. Leading manufacturers are increasingly adopting digital twin modeling, AI-assisted design optimization, automated assembly lines, and precision testing systems to enhance product reliability and reduce production cycles.

Software development has become a critical value chain component, with robotics operating systems, motion control software, AI algorithms, computer vision modules, and cloud robotics platforms enabling intelligent automation. The integration of machine learning, IoT connectivity, and real-time data analytics is transforming robotic arms from pre-programmed machines into adaptive, self-learning systems capable of predictive maintenance and autonomous decision-making.

The distribution and integration layer includes industrial automation distributors, system integrators, robotics solution providers, and OEM partnerships. Robotic arms are rarely deployed as standalone products and are typically integrated into larger automated production systems, including smart factories, assembly lines, logistics hubs, and precision manufacturing environments. System integrators play a vital role in customizing robotic solutions for industry-specific applications.

After-sales services and lifecycle management form an increasingly important segment of the value chain, including maintenance services, software updates, calibration, spare parts supply, remote diagnostics, and performance optimization. Predictive maintenance powered by AI and IoT connectivity is significantly improving uptime and reducing operational disruptions across industrial installations.

Overall, the robotic arm value chain is evolving into a highly digitalized, software-defined, globally interconnected ecosystem that integrates mechanical engineering, artificial intelligence, industrial automation, and cloud computing into a unified production framework focused on efficiency, precision, and scalability.

Global Robotic Arm Market Value Chain & Supply Chain Evolution Current Scenario

The current robotic arm supply chain is characterized by strong global interdependence between component manufacturers, robotics OEMs, software developers, and industrial integrators. Asia-Pacific dominates large-scale manufacturing of robotic components, particularly China, Japan, and South Korea, which serve as major hubs for electronics, sensors, motors, and industrial robotics assembly.

Europe remains a key center for high-precision robotics engineering and industrial automation systems, while North America leads in AI-driven robotics software, advanced control systems, and innovation in collaborative robotics (cobots). Global supply chains are highly specialized, with different regions contributing distinct technological capabilities.

System integrators play a critical role in bridging hardware and software, ensuring robotic arms are seamlessly deployed into automotive manufacturing, electronics production, logistics automation, healthcare robotics, and aerospace applications. Demand for customized robotic solutions is increasing across SMEs and large enterprises alike.

Supply chain resilience has become a major priority due to semiconductor shortages, geopolitical tensions, and disruptions in global logistics networks. As a result, companies are diversifying suppliers, increasing regional manufacturing capabilities, and investing in localized production hubs to reduce dependency on single-source regions.

Digital transformation is reshaping the supply chain through cloud-based robotics management platforms, AI-driven demand forecasting, remote diagnostics, and predictive maintenance systems. These technologies are improving efficiency, reducing downtime, and enabling real-time performance optimization across distributed robotic installations.

Key Value Chain & Supply Chain Evolution Signals in Global Robotic Arm Market

One of the strongest evolution signals in the robotic arm market is the increasing integration of artificial intelligence and machine vision systems, enabling robots to perform complex, adaptive tasks with minimal human intervention. This shift is transforming robotic arms from fixed-function machines into intelligent automation systems.

The expansion of collaborative robots (cobots) is another major trend, enabling safe human-robot interaction in shared workspaces. This is significantly increasing adoption among small and medium-sized manufacturers who previously lacked access to high-cost automation systems.

Semiconductor dependency remains a critical supply chain factor, with advanced chips, GPUs, and AI accelerators becoming essential for real-time robotic decision-making and automation intelligence. This has led to increased investment in semiconductor localization and strategic sourcing partnerships.

Cloud robotics and IoT-enabled manufacturing systems are emerging as key enablers of remote monitoring, centralized control, and fleet-level robot management, allowing enterprises to optimize performance across multiple production facilities.

Additionally, the shift toward modular and software-defined robotics is enabling faster upgrades, easier customization, and longer product lifecycles, reducing dependency on hardware replacement cycles and increasing overall system flexibility.

Strategic Implications of Value Chain & Supply Chain Evolution in Global Robotic Arm Market

The evolving robotic arm value chain presents significant strategic implications for manufacturers, software providers, system integrators, and industrial end users. Companies that successfully integrate hardware excellence with advanced AI capabilities, software ecosystems, and cloud-based robotics platforms are expected to gain long-term competitive advantages.

Supply chain diversification is becoming a strategic necessity due to geopolitical risks, semiconductor shortages, and global logistics uncertainties. Manufacturers are increasingly investing in regional production facilities and multi-sourcing strategies to ensure supply continuity and operational resilience.

The rise of service-based robotics models, including Robotics-as-a-Service (RaaS), is reshaping revenue structures by shifting from one-time hardware sales to subscription-based automation solutions. This is creating recurring revenue streams and improving customer accessibility.

Investment in AI-driven predictive maintenance, digital twins, and real-time analytics is improving operational efficiency, reducing downtime, and enhancing robotic lifecycle management across industrial applications.

Long-term competitiveness in the robotic arm market will depend on the ability to combine automation hardware, intelligent software systems, scalable manufacturing capabilities, and flexible supply chain networks within a unified industrial ecosystem.

Global Robotic Arm Market Value Chain & Supply Chain Evolution Forward Outlook

Between 2026 and 2033, the robotic arm value chain is expected to become increasingly intelligent, decentralized, and software-defined, driven by rapid advancements in AI, machine learning, and industrial IoT technologies. Robotics systems will evolve into fully autonomous, self-optimizing production units integrated into smart factory ecosystems.

The adoption of Industry 5.0 concepts will further enhance human-robot collaboration, enabling more personalized, flexible, and adaptive manufacturing environments. Cobots will play a central role in bridging automation with human creativity and decision-making.

Semiconductor innovation will remain a key enabler, with next-generation AI chips and edge computing technologies enhancing real-time robotic decision-making and operational intelligence.

Cloud robotics platforms will expand significantly, enabling centralized monitoring, fleet coordination, and remote optimization of robotic systems across global manufacturing networks.

Ultimately, the future robotic arm value chain will be defined by deep integration between hardware precision, AI intelligence, cloud connectivity, and resilient global supply networks, creating a highly adaptive and efficient industrial automation ecosystem.

Market-Specific Value Chain

- Raw Material & Component Supply: Metals, alloys, semiconductors, sensors, actuators, servo motors, electronic chips, precision mechanical parts

- Robotics Design & Manufacturing: Robotic OEMs, mechanical engineering firms, assembly plants, automation hardware manufacturers

- Software & Control Systems: AI developers, robotics OS providers, motion control software firms, computer vision platforms

- System Integration & Deployment: Industrial automation integrators, OEM partners, factory automation solution providers

- Distribution & Industrial Implementation: Robotics distributors, industrial equipment suppliers, manufacturing contractors, logistics automation providers

- After-Sales & Lifecycle Services: Maintenance providers, predictive analytics platforms, remote monitoring services, spare parts and upgrade providers

Investment Activity

Global Robotic Arm Market Investment & Funding Dynamics Overview

Investment and funding activity in the global robotic arm market is accelerating significantly, driven by the rapid expansion of industrial automation, rising adoption of Industry 4.0 and Industry 5.0 frameworks, and increasing demand for intelligent manufacturing systems. Between 2026 and 2033, capital inflows are expected to concentrate heavily on AI-enabled robotics platforms, collaborative robots (cobots), cloud-based automation ecosystems, and advanced motion control technologies that enhance precision, flexibility, and operational efficiency.

The robotic arm industry is evolving from traditional hardware-centric automation toward software-defined, AI-integrated robotic ecosystems. This shift is attracting strong investments from venture capital firms, industrial conglomerates, and strategic corporate investors seeking exposure to next-generation manufacturing technologies. Key players such as ABB Ltd., FANUC Corporation, Yaskawa Electric Corporation, KUKA AG, Mitsubishi Electric, and Universal Robots (Teradyne) continue to allocate substantial resources toward R&D, acquisitions, and digital transformation initiatives.

A major driver of investment momentum is the global transition toward smart factories and connected production systems. Governments and private enterprises are increasingly funding automation infrastructure, robotics innovation hubs, and advanced manufacturing clusters to improve productivity and strengthen supply chain resilience. This is further supported by rising labor cost pressures and persistent skilled labor shortages across key industrial economies.

Additionally, growing demand from automotive, electronics, semiconductor, healthcare, and logistics industries is accelerating funding into application-specific robotic arm solutions. Investments are increasingly focused on high-precision robotics, human-robot collaboration systems, and energy-efficient automation technologies that reduce operational costs while improving safety and output quality.

Global Robotic Arm Market Investment & Funding Dynamics Current Scenario

Current investment trends in the robotic arm market reflect a strong shift toward AI-driven automation, predictive robotics, and integrated industrial software ecosystems. Companies are prioritizing funding for machine vision systems, real-time analytics, edge computing, and cloud robotics platforms to enable smarter and more adaptive production environments.

- Asia-Pacific: Leads global investment activity due to large-scale manufacturing expansion, strong government support for industrial automation, and rapid adoption of robotics in China, Japan, South Korea, and India.

- North America: Attracts significant venture capital and corporate funding focused on AI-powered robotics startups, cobot innovation, and advanced industrial automation systems, particularly in the United States.

- Europe: Witnesses strong investments driven by automotive automation demand, Industry 4.0 initiatives, and sustainability-focused smart manufacturing programs, with Germany playing a central role.

- Latin America & Middle East: Emerging investment regions supported by gradual industrial modernization, logistics automation, and increasing adoption of robotics in manufacturing and energy sectors.

Key Investment & Funding Dynamics Signals in Global Robotic Arm Market

- Increasing venture capital funding in collaborative robotics (cobots) startups focusing on SME automation and flexible manufacturing solutions.

- Rising corporate investments in AI-integrated robotics platforms, including machine vision, predictive maintenance, and autonomous decision-making systems.

- Growing M&A activity among leading robotics companies to acquire AI startups, sensor technology firms, and industrial automation software providers.

- Expanding investments in semiconductor-driven robotics innovation, supporting advanced processing power and real-time control systems.

- Strong funding into logistics and warehouse automation systems driven by e-commerce growth and supply chain optimization needs.

- Increased R&D spending on human-robot collaboration technologies, safety systems, and force-sensing robotic arms.

- Rising government-backed initiatives promoting smart manufacturing, industrial digitalization, and robotics adoption across key economies.

Strategic Implications of Investment & Funding Dynamics in Global Robotic Arm Market

- Companies with integrated hardware-software robotics ecosystems are attracting the highest levels of investment due to scalability and long-term competitiveness.

- AI and software capabilities are becoming critical investment priorities, shifting value creation from mechanical systems to intelligent automation platforms.

- Strategic collaborations between robotics manufacturers, automotive OEMs, electronics companies, and logistics providers are accelerating commercialization of advanced robotic solutions.

- The dual growth of industrial robots and collaborative robots is shaping a diversified investment landscape with distinct funding strategies for high-end and SME-focused solutions.

- Asia-Pacific continues to strengthen its position as a global manufacturing and robotics investment hub, intensifying competition across international markets.

- Sustainability-focused investments in energy-efficient robotics and low-carbon manufacturing systems are gaining increasing importance among institutional investors.

- Companies with strong intellectual property portfolios and AI-driven automation capabilities are expected to secure long-term funding advantages and market leadership.

Global Robotic Arm Market Investment & Funding Dynamics Forward Outlook

Looking ahead, investment activity in the global robotic arm market is expected to remain strong and structurally sustained, supported by continuous advancements in artificial intelligence, industrial automation, and digital manufacturing ecosystems. Future capital allocation will increasingly focus on autonomous production systems, digital twin-enabled robotics, and fully integrated smart factory solutions.

Key future investment areas include cloud robotics platforms, AI-powered predictive manufacturing systems, next-generation collaborative robots, and fully autonomous industrial automation networks. The integration of robotics with IoT, edge computing, and 5G connectivity will further expand investment opportunities across global industries.

- Asia-Pacific: Will remain the dominant investment hub due to large-scale manufacturing ecosystems and strong government-backed automation initiatives.

- North America: Will continue driving high-value investments in AI robotics startups, software-defined automation, and advanced industrial technologies.

- Europe: Will focus on sustainable robotics development, precision manufacturing systems, and Industry 4.0/5.0 integration strategies.

Overall, the robotic arm market is expected to witness sustained funding momentum as industries increasingly shift toward intelligent, automated, and data-driven manufacturing systems. Companies that successfully combine robotics innovation, AI integration, and scalable industrial automation platforms will remain strongly positioned to attract long-term investment and strategic funding.

Technology & Innovation

Global Robotic Arm Market Technology & Innovation Landscape Overview

The global robotic arm market is undergoing a rapid technological transformation driven by advancements in artificial intelligence (AI), machine vision, sensor fusion, edge computing, and industrial Internet of Things (IIoT). Innovation in the market is increasingly centered on intelligent automation systems, adaptive robotics, collaborative human-robot interaction, and fully connected smart manufacturing ecosystems under Industry 4.0 and emerging Industry 5.0 frameworks.

Modern robotic arms are no longer purely mechanical systems; they are becoming software-defined, data-driven automation platforms. Integration of AI algorithms enables robotic arms to perform real-time decision-making, path optimization, anomaly detection, and predictive maintenance. These capabilities are significantly improving operational efficiency, precision, and flexibility across industrial applications.

Machine vision technology is a core innovation pillar in the market. High-resolution cameras combined with deep learning models allow robotic arms to identify objects, detect defects, and perform complex pick-and-place or assembly tasks with near-human accuracy. This is especially critical in electronics, automotive, and semiconductor manufacturing where micro-level precision is required.

Sensor technology advancements are further enhancing robotic performance. Force sensors, torque sensors, tactile feedback systems, and 3D spatial sensors enable robotic arms to interact safely and accurately with dynamic environments. This is particularly important for collaborative robots (cobots), which are designed to work alongside human operators.

Global Robotic Arm Market Technology & Innovation Current Scenario

Currently, the robotic arm industry is shifting from traditional pre-programmed automation toward intelligent, adaptive, and self-learning robotic systems. Industrial manufacturers are increasingly deploying AI-enabled robotic arms that can adjust movement patterns based on real-time production data and environmental feedback.

Collaborative robots (cobots) represent one of the fastest-growing innovation segments. These systems are equipped with advanced safety sensors, force limitation mechanisms, and intuitive programming interfaces, enabling safe interaction with human workers. Cobots are widely adopted in small and medium-sized enterprises due to their flexibility and lower deployment complexity.

Cloud robotics is emerging as a key technological trend, enabling robotic arms to connect to centralized data platforms for remote monitoring, software updates, and fleet management. This allows manufacturers to optimize performance across multiple production facilities and implement predictive maintenance strategies at scale.

Digital twin technology is also gaining strong traction. Manufacturers are creating virtual replicas of robotic systems to simulate performance, optimize workflows, and test production scenarios before physical deployment. This significantly reduces downtime and improves operational planning accuracy.

Edge computing is playing a critical role in reducing latency and improving real-time responsiveness. By processing data locally on robotic systems rather than relying solely on cloud infrastructure, manufacturers are achieving faster decision-making and improved reliability in mission-critical applications.

Key Technology & Innovation Trends in Global Robotic Arm Market

- Artificial Intelligence & Machine Learning: AI-powered robotics enabling autonomous decision-making, adaptive motion control, and predictive maintenance.

- Machine Vision Systems: Deep learning-based visual recognition for inspection, defect detection, and precision assembly tasks.

- Collaborative Robotics (Cobots): Safe human-robot interaction systems designed for flexible and shared workspaces.

- Industrial IoT (IIoT): Connected robotic systems enabling real-time monitoring, diagnostics, and performance optimization.

- Cloud Robotics: Centralized data platforms supporting remote control, software updates, and multi-site coordination.

- Digital Twin Technology: Virtual simulation models used for process optimization and predictive system modeling.

- Edge Computing Integration: On-device data processing for low-latency control and real-time robotic responsiveness.

- Advanced Sensor Fusion: Multi-sensor integration for improved spatial awareness, force control, and environmental adaptability.

- Human-Robot Interaction Systems: Safety-enhanced robotics enabling intuitive collaboration with human operators.

- Software-Defined Robotics: Modular and upgradable robotic systems driven by programmable software ecosystems.

Strategic Implications of Technology & Innovation

Technological innovation is fundamentally reshaping the competitive structure of the robotic arm market. Companies that integrate AI, machine vision, and cloud-based robotics platforms are gaining significant advantages in productivity, customization, and scalability.

The shift toward software-defined robotics is reducing dependence on hardware differentiation alone and increasing the importance of software ecosystems, data analytics capabilities, and digital service offerings. This is creating new revenue models based on robotics-as-a-service (RaaS) and subscription-based automation solutions.

Innovation in cobots is expanding market accessibility by enabling SMEs to adopt automation without large-scale infrastructure investments. This is accelerating democratization of robotics across small and mid-sized manufacturing units globally.

At the same time, integration of AI and predictive analytics is improving operational reliability and reducing unplanned downtime. However, increasing system complexity is also driving demand for specialized robotics software engineers and AI-trained automation professionals.

Global Robotic Arm Market Technology & Innovation Forward Outlook

Looking ahead, the robotic arm market is expected to evolve into a fully autonomous, intelligent, and interconnected industrial ecosystem. Robotics systems will increasingly operate with minimal human intervention, supported by AI-driven orchestration and real-time adaptive control systems.

Future innovation will be shaped by advancements in autonomous manufacturing, swarm robotics, and fully integrated smart factory ecosystems where robotic arms communicate and coordinate with other machines in real time.

The expansion of Industry 5.0 will further emphasize human-centric automation, where robotic arms enhance human capabilities rather than replace them. This will drive innovation in safety systems, cognitive robotics, and adaptive collaboration technologies.

In the long term, convergence of robotics, AI, cloud computing, and advanced semiconductor technologies will redefine industrial production models. Companies investing in integrated robotics platforms, AI-native automation systems, and scalable software ecosystems are expected to lead the next phase of market evolution.

Overall, the technology and innovation landscape of the global robotic arm market is set to become increasingly intelligent, connected, and autonomous, enabling a new era of high-efficiency, flexible, and data-driven industrial automation.

Market Risk

Global Robotic Arm Market Risk Factors & Disruption Threats Overview

The global robotic arm market, despite strong growth driven by industrial automation, Industry 4.0 adoption, and increasing demand for precision manufacturing, faces several structural and operational risk factors. These risks are shaping investment decisions, slowing adoption in certain segments, and influencing long-term competitiveness across the robotics ecosystem.

One of the most significant risk factors is the high capital investment required for robotic arm deployment. The upfront cost of robotic systems, along with integration, programming, and maintenance expenses, creates a major barrier for small and medium-sized enterprises. This limits widespread adoption in cost-sensitive markets and slows down penetration in developing economies.

Another key risk is rapid technological obsolescence. The robotic arm industry is evolving quickly with continuous advancements in artificial intelligence, machine vision, sensor technologies, and collaborative robotics. As product lifecycles shorten, manufacturers face constant pressure to upgrade systems and invest heavily in research and development to remain competitive.

Supply chain dependency also presents a critical vulnerability. Robotic arms rely heavily on semiconductors, precision motors, advanced sensors, rare earth materials, and electronic components. Any disruption in global semiconductor supply chains, geopolitical tensions, or trade restrictions can significantly impact production timelines, increase costs, and delay deployments.

Cybersecurity risks are becoming increasingly important as robotic systems become more connected and integrated into smart factory ecosystems. Networked robotic arms are exposed to potential cyberattacks, data breaches, and system manipulation risks, which can disrupt production processes and compromise operational safety.

Workforce-related and regulatory challenges also act as indirect risk factors. Increasing automation adoption raises concerns about job displacement in manufacturing sectors, which may lead to stricter labor regulations or resistance to adoption in certain regions. Additionally, differing safety standards and regulatory frameworks across countries create compliance complexities for global manufacturers.

Global Robotic Arm Market Risk Factors & Disruption Threats Current Scenario

The current market environment reflects strong demand from automotive, electronics, and logistics industries, but also increasing cost pressure and competitive intensity. Rising raw material costs and semiconductor price volatility are impacting manufacturing margins and overall profitability for robotics companies.

Demand volatility from key end-use industries, particularly automotive and semiconductor manufacturing, is affecting procurement cycles and investment planning. Economic uncertainty and cyclical downturns in industrial production can lead to delayed automation projects and reduced capital expenditure.

The growing adoption of collaborative robots (cobots) is reshaping competitive dynamics. While cobots are expanding the market base, they are also intensifying price competition and reducing differentiation in entry-level automation solutions. This is creating margin pressure for established industrial robotics manufacturers.

In addition, integration complexity across AI platforms, industrial software, and factory systems remains a challenge. Lack of standardization and interoperability issues between robotics systems and enterprise software can increase deployment time and operational inefficiencies.

Global Robotic Arm Market Key Risk Factors & Disruption Threat Signals

- High Capital Costs: Expensive robotic systems and integration costs limiting SME adoption.

- Technological Obsolescence: Rapid innovation cycles requiring continuous upgrades and R&D investment.

- Supply Chain Disruptions: Dependency on semiconductors, sensors, and precision components.

- Cybersecurity Threats: Increased vulnerability due to connected and cloud-based robotics systems.

- Demand Volatility: Fluctuations in automotive and electronics manufacturing investment cycles.

- Intensifying Price Competition: Entry of low-cost manufacturers creating margin pressure.

- Regulatory Variations: Different safety and automation standards across global markets.

- Workforce Resistance: Concerns over job displacement slowing adoption in certain regions.

- Integration Complexity: Challenges in connecting robotics with AI, IoT, and industrial software systems.

- Geopolitical Risks: Trade restrictions and international tensions affecting supply chains.

Strategic Implications of Risk Factors

Robotic arm manufacturers must focus on building resilient supply chains by diversifying suppliers for critical components such as semiconductors and sensors. Reducing dependency on single-source suppliers is essential to mitigate production risks.

Companies need to accelerate innovation in software-defined robotics, AI integration, and modular system design to reduce product obsolescence risk and improve upgrade flexibility for customers.

Cybersecurity integration at both hardware and software levels is becoming essential as factories transition toward fully connected smart manufacturing ecosystems. Secure-by-design robotics systems will gain stronger market preference.

To address cost barriers, industry players are increasingly exploring robotics-as-a-service (RaaS) models, enabling customers to adopt automation with lower upfront investment while creating recurring revenue streams for manufacturers.

Global Robotic Arm Market Forward Risk Outlook

Looking ahead, the robotic arm market is expected to remain highly growth-oriented but structurally complex, with increasing dependence on digital ecosystems, AI-driven automation, and global supply chain stability.

Future disruption risks are expected from low-cost robotics manufacturers, AI-native automation systems, and fully autonomous manufacturing platforms that may redefine traditional industrial robotics models.

Geopolitical uncertainty, semiconductor supply constraints, and evolving industrial regulations will continue to influence market stability and expansion strategies.

Overall, while the market presents strong long-term growth potential, sustained competitiveness will depend on innovation speed, cost efficiency, cybersecurity strength, and supply chain resilience.

Regulatory Landscape

Global Robotic Arm Market Regulatory & Policy Environment Overview

The regulatory and policy environment governing the global robotic arm market is evolving rapidly as industrial automation, artificial intelligence, and human-robot collaboration become increasingly embedded in manufacturing ecosystems. Regulatory oversight primarily focuses on workplace safety standards, industrial automation compliance, machine safety certification, data security in connected robotics, and ethical use of autonomous systems.

Robotic arms used in industrial and commercial applications are subject to strict safety and operational regulations to ensure safe interaction with humans and machines. Standards organizations and regulatory bodies across regions define guidelines for mechanical safety, electrical safety, emergency shutdown systems, and risk mitigation in automated environments.

In parallel, the integration of AI, IoT, and cloud-based robotics platforms has introduced new regulatory considerations related to cybersecurity, data privacy, algorithm transparency, and cross-border data transfer. Governments are increasingly focusing on ensuring that connected robotic systems are secure, reliable, and resistant to cyber threats.

Additionally, labor and occupational safety regulations play a critical role in shaping adoption, as robotic arms are widely deployed to reduce human exposure to hazardous tasks, repetitive strain injuries, and high-risk industrial environments.

Global Robotic Arm Market Regulatory & Policy Environment Current Scenario

The current regulatory landscape for the robotic arm market is defined by established industrial safety frameworks and emerging digital and AI governance policies. Compliance requirements vary by region but generally emphasize machine safety, operational reliability, and human-robot interaction standards.

In North America, organizations such as the Occupational Safety and Health Administration (OSHA) and standards bodies like ANSI and ISO provide guidelines for industrial robot safety, installation protocols, and workplace hazard prevention. Cybersecurity frameworks are also increasingly applied to connected industrial systems.

In Europe, robotic systems are governed under the EU Machinery Directive and evolving Machinery Regulation, alongside strict CE marking requirements. European standards place strong emphasis on safety validation, risk assessment, and harmonized industrial automation compliance across member states.

Asia-Pacific markets, particularly China, Japan, and South Korea, are strengthening regulatory frameworks to support large-scale industrial automation while ensuring safety and quality standards. Japan maintains highly advanced robotics safety standards, while China is expanding industrial robotics governance under broader smart manufacturing policies.

Emerging economies in Latin America and the Middle East are gradually adopting international safety and automation standards to support industrial modernization and foreign investment in manufacturing and logistics sectors.

Key Regulatory & Policy Environment Signals in Global Robotic Arm Market

- Industrial Safety Standards: Robotic arms must comply with ISO, IEC, and regional machine safety standards governing installation, operation, and maintenance protocols.

- Workplace Health & Safety Regulations: Regulations aim to minimize human exposure to hazardous environments through automation and enforce safe human-robot interaction guidelines.

- Cybersecurity & Data Protection: Connected robotic systems are increasingly subject to cybersecurity compliance requirements to prevent system breaches and operational disruptions.

- AI & Automation Governance: Emerging policies address ethical AI use, algorithm transparency, and accountability in autonomous industrial systems.

- Import, Certification & Compliance Requirements: Robotic arms must meet regional certification standards such as CE marking, UL certification, and other industrial conformity assessments.

- Industrial Automation & Smart Manufacturing Policies: Governments are promoting robotics adoption through Industry 4.0 incentives, manufacturing modernization programs, and tax benefits.

Strategic Implications of Regulatory & Policy Environment

The evolving regulatory framework is significantly influencing product design, deployment strategies, and market entry requirements in the robotic arm industry. Manufacturers are increasingly investing in safety engineering, compliance testing, and certification processes to meet stringent global standards.

Cybersecurity and AI governance requirements are driving the development of secure-by-design robotic systems with embedded encryption, real-time monitoring, and anomaly detection capabilities. This is becoming a key differentiator in industrial automation procurement decisions.

Workplace safety regulations are accelerating the adoption of collaborative robots (cobots), which are designed to operate safely alongside human workers, reducing the need for physical safety barriers and enabling flexible manufacturing environments.

Government initiatives supporting smart manufacturing, industrial automation, and digital transformation are further encouraging robotics adoption, particularly in automotive, electronics, logistics, and precision engineering sectors.

At the same time, compliance complexity is increasing operational costs and encouraging companies to develop globally standardized robotic platforms that can meet multi-region certification requirements more efficiently.

Global Robotic Arm Market Regulatory & Policy Environment Forward Outlook

Between 2026 and 2033, the regulatory environment for the global robotic arm market is expected to become more integrated, AI-aware, and cybersecurity-focused. Governments are likely to strengthen regulations around autonomous systems, human-robot collaboration, and data security in connected industrial environments.

International standardization efforts are expected to increase, enabling greater harmonization of safety, performance, and certification requirements across major manufacturing regions. This will help reduce trade barriers and accelerate global deployment of robotic technologies.

Future regulatory frameworks are also expected to address ethical considerations in AI-driven robotics, including accountability, transparency, and decision-making autonomy in industrial systems.

Overall, the regulatory and policy landscape will continue to play a critical role in shaping innovation, market expansion, and competitive positioning. Companies that proactively align with evolving safety standards, cybersecurity requirements, and smart manufacturing policies will be strongly positioned in the global robotic arm market.