Global Bus & Coach Tyres Market size, share & forecast 2026-2033

Market Forecast Snapshot (2026???2033)

| Metric | Value |

|---|---|

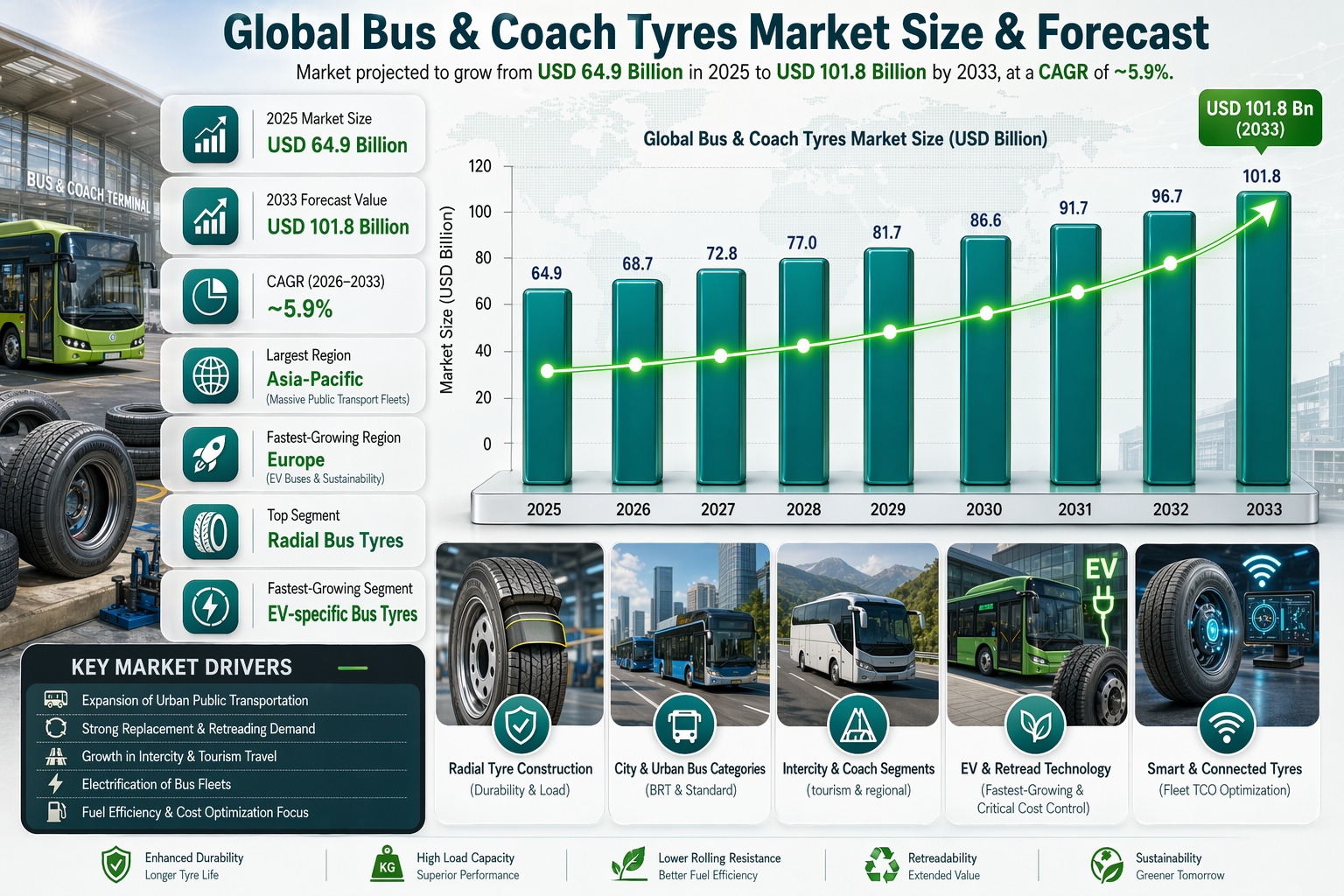

| 2025 Market Size | USD 64.9 Billion |

| 2033 Market Size | USD 101.8 Billion |

| CAGR (2026???2033) | ~5.9% |

| Largest Region | Asia-Pacific |

| Fastest-Growing Region | Europe |

| Largest Segment | Radial bus tyres |

| Fastest-Growing Segment | EV-specific bus tyres |

| Key Trend | Retreadable & low-rolling-resistance tyres |

Global Bus & Coach Tyres Market Overview

The Global Bus & Coach Tyres Market is all about tyres for buses and coaches that carry tons of people . These tyres are built tough to handle city traffic, long highway trips, and heavy loads - all while keeping passengers safe and comfortable.

Bus and coach tyres are built like tanks . They're designed to handle heavy loads, rough routes, and non-stop action - whether that's city traffic, long highways, or winding mountain roads . They're made with tough casings, deep treads, and can often be retreaded, which saves money. And because buses run all day, every day, there's a huge market for replacement tyres - it's a constant cycle! Makes sense that OEMs and aftermarket suppliers are both big players in this game.

The Global bus & coach tyres market is on the rise . Cities are growing, public transport is expanding, and more people are travelling - that's fuelling demand . Plus, with electric buses and eco-friendly fleets becoming more popular, tyre makers are stepping up with tyres that are efficient, quiet, and tough - driving growth in the market.

According to the Pheonix Demand Forecast Engine, the Global Bus & Coach Tyres Market size is estimated at USD 64.9 billion in 2025 and is projected to reach USD 101.8 billion by 2033, expanding at a CAGR of ~5.9% during the forecast period (2026???2033).

Asia-Pacific is the largest market due to massive public transport fleets in China and India, while Europe is the fastest-growing region driven by electric buses, sustainability mandates, and premium coach transportation.

Key Drivers of Global Bus & Coach Tyres Market Growth

Expansion of Urban Public Transportation

Cities are exploding . To keep people moving, governments are going all-in on public transport - more buses, BRT lanes, and mass transit systems ????. That means a surge in tyre demand, driving growth in the market.

Strong Replacement & Retreading Demand

Buses operate for long hours every day, resulting in high wear rates. Regular replacement and multi-life retreading form the backbone of market revenues.

Growth in Intercity & Tourism Travel

Tourism is booming . More people are travelling between cities in comfy coaches, and that means tyre makers are in demand . These coaches need high-performance tyres that deliver comfort and reliability, driving growth in the market.

Electrification of Bus Fleets

Electric buses are changing the game. They need tyres that can handle heavier batteries, roll smoothly to save energy, and be quieter - that's pushing tyre tech to the next level.

Fuel Efficiency & Cost Optimization Focus

Fleet operators prioritize tyres that reduce fuel consumption and total cost of ownership (TCO), boosting demand for premium and smart tyres.

Global Bus & Coach Tyres Market Segmentation

1. By Tyre Construction

1.1 Radial Tyres??

1.1.1 Steel-Belted Radial Tyres

1.1.1.1?? Single steel belt

1.1.1.2?? Double steel belt

1.1.1.3 Multi-layer steel belt

1.1.2 All-Steel Radial Tyres

1.1.2.1?? Long-haul coaches

1.1.2.2 Heavy-load city buses

1.2 Bias (Cross-Ply) Tyres

1.2.1 Nylon bias tyres

1.2.2 Polyester bias tyres

2. By Vehicle Type

2.1 City & Urban Buses (Largest Segment)

2.1.1 Standard city buses

2.1.2 Electric city buses

2.1.3 BRT buses

2.2 Intercity Buses

2.2.1 Regional transport buses

2.2.2 Highway buses

2.3 Coaches & Luxury Buses

2.3.1 Long-distance coaches

2.3.2 Tourism & premium coaches

3. By Application

3.1 On-Road / Highway Applications

3.1.1 Intercity travel

3.1.2 Long-haul coaches

3.2 Urban Stop-and-Go Applications

3.2.1 City public transport

3.2.2 Municipal services

3.3 Mixed-Service Applications

3.3.1 Suburban routes

3.3.2 School & staff transport

4. By Sales Channel

4.1 OEM (Original Equipment Manufacturer)

4.1.1 Bus OEM fitment

4.1.2 Electric bus OEM fitment

4.2 Aftermarket / Replacement (Largest Segment)

4.2.1 Authorized dealer networks

4.2.2 Independent commercial tyre retailers

4.2.3 Fleet service & retreading providers

4.2.4 Online & B2B procurement platforms

5. By Rim Size

5.1 Below 20 Inches

5.1.1 Mini buses

5.1.2 Urban shuttle buses

5.2 20???22.5 Inches (Largest Segment)

5.2.1 City buses

5.2.2 Intercity buses

5.3 Above 22.5 Inches (Fastest-Growing)

5.3.1 Luxury coaches

5.3.2 High-capacity electric buses

6. By Tyre Technology

6.1 Conventional Pneumatic Tyres

6.2 Low Rolling Resistance Tyres

6.2.1 Fuel-efficient compound tyres

6.2.2 EV-optimized bus tyres

6.3 Retreadable Tyres

6.3.1 Multi-life casing tyres

6.3.2 Pre-cured & mold-cure retreads

6.4 Smart & Connected Tyres

6.4.1 Embedded pressure & temperature sensors

6.4.2 Fleet-based tyre monitoring systems

7. By Geography

7.1 Asia-Pacific (Largest Region)

7.1.1 China, India, Japan, South Korea, Southeast Asia

7.2 Europe (Fastest-Growing)

7.2.1 Germany, France, U.K., Italy

7.3 North America

7.3.1 U.S., Canada

7.4 Latin America

7.4.1 Brazil, Mexico

7.5 Middle East & Africa

Regional Insights of Global Bus & Coach Tyres Market

Asia-Pacific ??? Largest Market

Massive public transport fleets, high urban population density, and strong replacement demand drive market leadership.

Europe ??? Fastest-Growing Market

Electric bus adoption, strict emissions regulations, and premium coach transportation fuel growth.

North America

Stable demand supported by school buses, intercity coaches, and municipal transport fleets.

Latin America & Middle East & Africa

Growth driven by urban transit expansion and infrastructure investments.

Leading Companies in the Global Bus & Coach Tyres Market

Michelin

Bridgestone Corporation

Goodyear Tire & Rubber Company

Continental AG

Pirelli & C. S.p.A.

Sumitomo Rubber Industries

Hankook Tire

Yokohama Rubber Company

Toyo Tires

Apollo Tyres

Michelin and Bridgestone are?? the largest players in the Global Bus & Coach Tyres Market.

Why the Bus & Coach Tyres Market Remains Critical

??? Backbone of urban mobility and public transportation

??? Strong recurring replacement and retreading demand

??? Direct impact on fuel efficiency, emissions, and fleet operating costs

??? Key enabler for electric and sustainable public transport systems

Strategic Intelligence & Pheonix AI-Backed Insights

Pheonix Demand Forecast Engine:

Models bus fleet growth, replacement cycles, urban transit expansion, and EV bus adoption.

EV Tyre Requirement Analyzer:

Assesses demand for low-noise, high-load, energy-efficient tyres for electric buses.

Raw Material Sensitivity Model:

Tracks rubber, steel cord, and oil price volatility impacting tyre margins.

Automated Porter???s Five Forces (Concise)

Buyer Power: Moderate ??? fleet contracts balanced by aftermarket

Supplier Power: Moderate ??? rubber and steel inputs

Threat of New Entrants: Low ??? capital-intensive manufacturing

Threat of Substitutes: Low ??? essential consumable

Competitive Rivalry: High ??? global majors and regional players

Final Takeaway of Global Bus & Coach Tyres Market

The Global Bus & Coach Tyres Market is a resilient, infrastructure-driven market with predictable replacement demand and growing technological sophistication. Electrification of buses, smart fleet management, and fuel-efficient tyre solutions will shape the next growth phase. Manufacturers that focus on durability, retreadability, and fleet-centric innovation will remain best positioned through 2033.

Competitive Landscape

Bus & Coach Tyres Competitive Intensity & Market Structure Overview

The Global Bus & Coach Tyres Market is characterized by a moderately consolidated structure, with a relatively high level of competitive intensity among global manufacturers and regional suppliers. The market is dominated by a small group of Tier 1 multinational tyre companies that collectively hold significant OEM contracts with bus and coach manufacturers, while a wide network of regional and local players competes aggressively in the replacement segment. This structure is primarily driven by the dual nature of demand: long-term OEM supply agreements with bus manufacturers and highly fragmented aftermarket demand from public transport operators, fleet owners, and municipal authorities. As buses operate on fixed routes with high daily mileage, tyre performance, safety, durability, and retreadability become critical purchasing criteria, intensifying competition among suppliers. Two Tier 1 players’Michelin and Bridgestone’hold a dominant position in the Global Bus & Coach Tyres Market due to their strong OEM relationships, advanced radial tyre technologies, and extensive global service and retreading networks. These companies set industry benchmarks in fuel efficiency, low rolling resistance, and multi-life tyre solutions, particularly for high-utilization bus fleets. Other major global competitors such as Goodyear, Continental, Pirelli, and Sumitomo Rubber Industries also maintain strong positions through fleet-focused solutions, smart tyre technologies, and integrated service ecosystems. However, the market still allows space for regional manufacturers to compete on pricing and localized fleet servicing, especially in emerging economies. The competitive landscape is further shaped by the growing transition toward electric buses, which is increasing demand for specialized tyres with higher load-bearing capacity, reduced noise, and improved energy efficiency. This shift is pushing manufacturers to accelerate innovation cycles and differentiate through EV-specific tyre designs.

Bus & Coach Tyres Competitive Intensity & Market Structure Current Scenario

Leading Company Profiles

Michelin: Global Tyre Manufacturer. Leader in radial bus tyres, retreadable solutions, and low rolling resistance technologies. Bridgestone Corporation: Global Tyre Manufacturer. Strong OEM presence and advanced fleet tyre management solutions. Goodyear Tire & Rubber Company: Tyre Manufacturer. Focused on smart tyres and commercial fleet optimization solutions. Continental AG: Tyre & Technology Provider. Strong in sensor-based and connected tyre systems. Pirelli & C. S.p.A.: Premium Tyre Manufacturer. Focused on high-performance bus and coach applications. Sumitomo Rubber Industries: Tyre Manufacturer. Strong presence in Asia-Pacific commercial vehicle segment. Hankook Tire: Tyre Manufacturer. Expanding footprint in commercial and electric bus tyre segments. Yokohama Rubber Company: Tyre Manufacturer. Known for durable and fuel-efficient commercial tyres. Toyo Tires: Tyre Manufacturer. Focused on value-driven commercial tyre offerings. Apollo Tyres: Emerging Global Player. Strong in cost-efficient bus and fleet tyre solutions, especially in Asia and Europe.

Key Competitive Intensity & Market Structure Signals in Bus & Coach Tyres

The competitive dynamics in the Bus & Coach Tyres Market are strongly influenced by fleet-based procurement models, where large transport operators and municipal bodies negotiate long-term supply contracts. This creates a high-entry barrier for new players while reinforcing the dominance of established global manufacturers with proven reliability and service infrastructure. Another key signal is the importance of retreadability and lifecycle cost optimization. Since bus tyres undergo multiple retread cycles, manufacturers with advanced casing durability and retreading programs gain a significant competitive advantage. This has led to the emergence of integrated tyre lifecycle management services as a core differentiator. The shift toward electric buses is also reshaping competition. EV buses require tyres with higher load capacity due to battery weight, along with reduced rolling resistance and lower noise levels for urban environments. This has intensified R&D investment among Tier 1 manufacturers and increased competition in premium and EV-specific tyre segments. Price sensitivity remains high in public transport procurement, especially in emerging economies, where regional manufacturers compete aggressively on cost. However, safety standards, regulatory compliance, and uptime requirements often limit long-term displacement of established global brands.

Strategic Implications of Competitive Intensity & Market Structure in Bus & Coach Tyres

The competitive structure of the Bus & Coach Tyres Market highlights a clear strategic divide between global innovation leaders and cost-focused regional suppliers. Tier 1 manufacturers are increasingly focusing on value-added services such as predictive maintenance, smart tyre monitoring, and fleet efficiency optimization to lock in long-term contracts with transport operators. At the same time, regional players continue to compete effectively in price-sensitive markets by offering basic radial tyres and localized service networks. This dual structure creates sustained pricing pressure but also ensures high-volume replacement demand across all market tiers. Electrification of bus fleets is emerging as a key strategic inflection point. Companies that can successfully develop EV-optimized bus tyres with enhanced load-bearing capacity and energy efficiency are expected to capture premium market share over the forecast period. Fleet operators are also prioritizing total cost of ownership (TCO), which is pushing manufacturers to innovate in retreadability, durability, and fuel efficiency rather than competing solely on upfront pricing.

Bus & Coach Tyres Competitive Intensity & Market Structure Forward Outlook

The Bus & Coach Tyres Market is expected to remain moderately consolidated with continued dominance by Tier 1 global manufacturers. However, competitive intensity is likely to increase due to rapid technological changes, especially in smart tyre systems and electric bus applications. Market consolidation is expected to accelerate as major players pursue acquisitions and partnerships to strengthen their fleet service capabilities and expand in high-growth regions. Strategic collaborations with public transport operators and EV bus manufacturers will become increasingly important. Regulatory frameworks focused on emissions reduction, fuel efficiency, and urban mobility modernization will further push demand toward advanced tyre solutions, favoring technologically advanced players. In the long term, manufacturers that successfully combine durability, retreadability, and EV compatibility with integrated fleet services will be best positioned to lead the Bus & Coach Tyres Market through 2033.

Value Chain

Global Bus & Coach Tyres Market Value Chain & Supply Chain Evolution Overview

The value chain and supply chain dynamics within the Global Bus & Coach Tyres Market play a vital role in determining cost efficiency, operational reliability, and competitive positioning across the public transportation ecosystem. The market functions through a structured network of raw material suppliers, tyre manufacturers, OEM bus producers, fleet operators, distributors, and aftermarket service providers, ensuring continuous product flow across both OEM and replacement channels.

The supply chain is highly material-intensive, relying on natural rubber, synthetic rubber, carbon black, silica, steel cords, and advanced polymer compounds. Leading manufacturers such as Michelin, Bridgestone Corporation, Goodyear Tire & Rubber Company, and Continental AG maintain strong upstream sourcing strategies, long-term supplier contracts, and regional diversification to manage cost volatility and ensure stable production inputs.

Manufacturing in this segment involves specialized engineering focused on high-load endurance, reinforced carcass construction, optimized tread patterns for urban and highway usage, and retreadability enhancement. Increasing demand for low rolling resistance, noise reduction, and EV compatibility is pushing manufacturers toward more advanced compound technologies and precision manufacturing processes.

Distribution operates through a dual-channel structure, consisting of OEM supply for new bus and coach production and a dominant aftermarket segment driven by high utilization rates and frequent replacement cycles. The aftermarket ecosystem includes authorized dealers, fleet operators, retreading specialists, and B2B procurement platforms.

Supply chain challenges include raw material price fluctuations, logistics disruptions, regulatory compliance requirements, and increasing R&D investments in sustainable, EV-compatible, and high-durability tyre technologies. These factors collectively influence pricing strategies and margin structures across the value chain.

Global Bus & Coach Tyres Market Value Chain & Supply Chain Evolution Current Scenario

The Global Bus & Coach Tyres Market is currently characterized by steady demand growth driven by expanding public transport networks, urbanization, and rising passenger mobility. At the upstream level, volatility in rubber and petrochemical-based inputs continues to impact production costs, prompting manufacturers to adopt hedging strategies and diversified procurement models.

Manufacturers are increasingly focusing on developing high-performance bus and coach tyres with improved durability, reduced rolling resistance, and enhanced retreadability. EV bus adoption is accelerating innovation in noise reduction, load-bearing capacity, and energy efficiency.

OEM demand remains stable, particularly from city bus and electric bus manufacturers, while the aftermarket segment continues to dominate due to intensive daily usage and structured replacement cycles across fleet operations.

Distribution channels are undergoing gradual digital transformation, with fleet procurement platforms, online B2B ordering systems, and integrated service networks improving efficiency and accessibility for operators.

Aftermarket services such as retreading, tyre monitoring, alignment, and predictive maintenance are becoming key value-added offerings, strengthening long-term relationships between manufacturers and fleet operators.

Key Value Chain & Supply Chain Evolution Signals in Global Bus & Coach Tyres Market

Several key signals are shaping the evolution of the bus and coach tyres value chain. First, the expansion of urban public transport systems is increasing demand for high-durability, high-mileage tyres suitable for continuous operation.

Second, the strong dominance of replacement and retreading cycles highlights the importance of multi-life tyre designs that reduce total cost of ownership for fleet operators.

Third, electrification of bus fleets is driving demand for specialized tyres with higher load capacity, low noise characteristics, and improved energy efficiency.

Fourth, sustainability regulations are pushing manufacturers toward eco-friendly materials, low rolling resistance compounds, and recyclable tyre technologies.

Finally, digital transformation through smart tyre systems, IoT-enabled monitoring, and predictive maintenance is improving fleet efficiency and supply chain visibility.

Strategic Implications of Value Chain & Supply Chain Evolution in Global Bus & Coach Tyres Market

Leading manufacturers such as Michelin, Bridgestone, Continental, and Goodyear leverage their global production footprint, advanced R&D capabilities, and strong OEM relationships to maintain dominance in the market.

The capital-intensive nature of manufacturing, combined with stringent safety and performance requirements, creates high entry barriers and reinforces market consolidation among established players.

Fleet operators and distributors are increasingly shifting toward integrated service models, including retreading contracts, tyre management services, and digital fleet optimization solutions to reduce operational costs.

Cost efficiency, fuel savings, and sustainability remain central strategic priorities, especially as operators seek to optimize total cost of ownership across large bus fleets.

The transition toward electric buses presents both opportunities and challenges, requiring continuous innovation in tyre design, materials, and performance engineering.

Global Bus & Coach Tyres Market Value Chain & Supply Chain Evolution Forward Outlook

Between 2026 and 2033, the value chain is expected to evolve significantly due to electrification of public transport, digital fleet management adoption, and increasing sustainability mandates.

Manufacturers will increasingly focus on eco-friendly materials, energy-efficient production processes, and expansion of retreading ecosystems to support circular economy goals.

The aftermarket segment will remain the dominant revenue contributor, supported by high utilization rates and structured replacement cycles across global bus fleets.

Digital platforms and smart tyre solutions will continue to expand, improving predictive maintenance, fleet efficiency, and inventory optimization.

Overall, the future value chain will be defined by durability, electrification readiness, sustainability, and digital integration, with fleet-centric innovation emerging as a key competitive differentiator.

Market-Specific Value Chain

- Raw Material Procurement: Natural rubber, synthetic rubber, carbon black, silica, steel cords sourcing

- Research & Development: Load optimization, noise reduction engineering, EV-compatible bus tyre development

- Manufacturing: Reinforced carcass construction, compounding, molding, curing, and durability testing

- OEM Integration: Supply of tyres for city buses, intercity buses, and electric buses

- Distribution & Retail: Dealer networks, fleet operators, B2B platforms, and distributors

- Aftermarket Services: Replacement, retreading, maintenance, alignment, and smart tyre monitoring

Company-to-Stage Mapping

- Raw Material Procurement: Michelin, Bridgestone Corporation, Continental AG, Goodyear Tire & Rubber Company

- Research & Development: Michelin, Continental AG, Pirelli & C. S.p.A., Hankook Tire

- Manufacturing: Bridgestone Corporation, Goodyear Tire & Rubber Company, Yokohama Rubber Company, Hankook Tire

- OEM Integration: Michelin, Bridgestone Corporation, Continental AG, Apollo Tyres

- Distribution & Retail: Goodyear Tire & Rubber Company, Apollo Tyres, Toyo Tires, Yokohama Rubber Company

- Aftermarket Services: Michelin, Bridgestone Corporation, Goodyear Tire & Rubber Company, Continental AG

Investment Activity

Global Bus & Coach Tyres Market Investment & Funding Dynamics Overview

Investment and funding dynamics in the global bus & coach tyres market are strongly shaped by expanding public transportation systems, rising urban mobility demand, and increasing electrification of bus fleets. Between 2026 and 2033, capital deployment is expected to concentrate on low rolling resistance technologies, retreadable tyre systems, and EV-optimized bus tyre solutions that enhance efficiency, durability, and passenger comfort. The market demonstrates a moderately high capital intensity level due to the need for reinforced tyre construction, advanced compound engineering, and large-scale manufacturing capabilities. Continuous investment in R&D is essential, particularly for radial bus tyres, which dominate the market due to their durability, load-bearing capacity, and fuel efficiency advantages. Leading global manufacturers such as Michelin, Bridgestone, Goodyear, Continental AG, and Pirelli are actively directing capital toward smart tyre technologies, sustainable material development, and expansion of retreading infrastructure to strengthen lifecycle value and reduce total cost of ownership for fleet operators.

Global Bus & Coach Tyres Market Investment & Funding Dynamics Current Scenario

Currently, investment activity is driven by the rapid expansion of urban public transport networks and increasing demand for intercity and tourism travel. This is resulting in steady capital inflows into OEM supply chains and aftermarket distribution systems, particularly in high-growth urban regions. Asia-Pacific remains the dominant investment hub, supported by large-scale bus fleets in China and India and continuous government investment in mass transit infrastructure. Manufacturers are expanding production facilities and strengthening local supply chains to meet rising demand efficiently. In Europe, investment is increasingly focused on electrification and sustainability. Funding is directed toward EV-specific bus tyres, noise reduction technologies, and low rolling resistance solutions to comply with strict environmental regulations and support green mobility initiatives. North America continues to attract stable investment, driven by school bus fleets, intercity transport systems, and municipal transit operations. Meanwhile, Latin America and the Middle East & Africa are witnessing gradual investment growth supported by expanding urbanization and infrastructure development. The market’s projected growth from USD 64.9 billion in 2025 to USD 101.8 billion by 2033, at a CAGR of ~5.9%, reinforces its position as a stable, infrastructure-driven, and replacement-led investment segment.

Key Investment & Funding Dynamics Signals in Global Bus & Coach Tyres Market

A key investment signal is the continuous expansion of urban public transportation systems, which is driving sustained demand for bus tyres and encouraging long-term capital allocation in OEM partnerships and fleet supply agreements. Strong replacement and retreading cycles form a core funding driver, as buses operate continuously under heavy loads, resulting in frequent tyre wear and multi-life usage through retreading processes. The rapid electrification of bus fleets is accelerating investment in EV-compatible tyre technologies that offer higher load capacity, reduced rolling resistance, and improved acoustic performance. Increasing focus on fuel efficiency and fleet cost optimization is pushing manufacturers to invest in advanced compound formulations and smart tyre technologies that reduce operational expenses. Technological advancements such as embedded sensors, predictive maintenance systems, and IoT-enabled fleet monitoring are further shaping capital flows toward digital tyre ecosystems.

Strategic Implications of Investment & Funding Dynamics in Global Bus & Coach Tyres Market

The investment structure highlights a highly consolidated market dominated by global tyre manufacturers with strong OEM relationships and extensive aftermarket networks. High capital requirements and strict performance standards create significant barriers to entry. The dominance of the aftermarket segment ensures stable long-term revenue streams, as fleet operators rely heavily on replacement and retreading cycles to maintain operational efficiency. The transition toward electric buses is reshaping the industry, increasing the importance of innovation-led capital allocation focused on EV-specific tyre performance, durability, and noise reduction. Regional diversification remains essential, with Asia-Pacific driving volume growth, Europe leading sustainability-driven innovation, and North America providing steady demand from established transit systems. Volatility in raw material costs, particularly rubber and steel, continues to influence margins, prompting investments in supply chain optimization and material efficiency strategies.

Global Bus & Coach Tyres Market Investment & Funding Dynamics Forward Outlook

Looking ahead, investment dynamics in the bus & coach tyres market will remain stable and growth-oriented, supported by expanding public transportation networks and increasing adoption of electric buses worldwide. Capital deployment will continue to prioritize durability, fuel efficiency, and lifecycle cost optimization. Asia-Pacific will remain the largest investment destination due to its scale and infrastructure expansion, while Europe will lead innovation in EV and sustainable tyre technologies. North America will maintain steady investment flows supported by established public transport systems. Future investment cycles will increasingly focus on EV-optimized bus tyres, smart fleet integration, and advanced retreading technologies that enhance tyre lifecycle value. Digital transformation will also play a key role, with rising investments in IoT-based tyre monitoring systems, predictive analytics, and fleet optimization platforms. Overall, the bus & coach tyres market will continue to attract consistent capital inflows due to its essential role in public transportation systems, predictable replacement demand, and ongoing electrification trends. Manufacturers that align innovation with durability, efficiency, and fleet-focused solutions will remain best positioned through 2033.

Technology & Innovation

Global Bus & Coach Tyres Market Technology & Innovation Landscape Overview

The technology and innovation landscape within the global bus & coach tyres market is driven by the need for durability, passenger safety, fuel efficiency, and lifecycle cost optimization. Since buses operate under continuous high-utilization conditions, innovation in this segment is heavily focused on tread longevity, heat resistance, retreadability, and load-bearing efficiency rather than performance styling.

Innovation intensity in the market is moderate but steadily advancing, supported by improvements in radial construction, compound engineering, and casing durability. While core tyre architectures are mature, incremental advancements in low rolling resistance materials, reinforced steel belt structures, and multi-life retread designs are significantly enhancing operational efficiency for fleet operators. Leading manufacturers such as Michelin, Bridgestone Corporation, Goodyear Tire & Rubber Company, Continental AG, and Pirelli & C. S.p.A. are prioritizing fleet-focused innovation and EV-ready bus tyre development.

A key technological shift is the development of EV-optimized bus tyres, driven by the electrification of public transport fleets. These tyres require higher load-bearing capacity due to heavy battery systems, reduced rolling resistance for extended range, and noise-reduction capabilities for urban mobility applications. Additionally, smart tyre technologies are increasingly being integrated into fleet operations, enabling real-time monitoring and predictive maintenance to reduce downtime and improve operational efficiency.

Global Bus & Coach Tyres Market Technology & Innovation Landscape Current Scenario

Currently, the technology landscape in the global bus & coach tyres market is centered on durability enhancement, cost efficiency, and fuel optimization. Manufacturers are refining tread patterns and compound formulations to extend tyre life while maintaining stability under heavy passenger loads and long operating hours.

Low rolling resistance technology is a major focus area, helping reduce fuel consumption in diesel buses and extend driving range in electric buses. Silica-based compounds and optimized tread geometries are widely adopted to balance energy efficiency with braking performance and wet-road safety.

Retreadability remains a critical innovation pillar in this market. Multi-life casing designs allow bus operators to reuse tyre structures multiple times, significantly reducing lifecycle costs. This is especially important for public transport systems where operational budgets are tightly managed.

Smart and connected tyre technologies are gradually gaining traction in fleet operations. Embedded sensors enable continuous monitoring of pressure, temperature, and wear conditions, allowing predictive maintenance and minimizing unexpected breakdowns. This is particularly valuable in urban bus fleets where service reliability is essential.

Noise reduction technologies are becoming increasingly important due to the rise of electric buses, where engine noise is minimal and tyre noise becomes more noticeable. Acoustic tread designs and optimized pitch sequencing are being introduced to improve passenger comfort and meet urban noise regulations.

Manufacturing innovation is also advancing, with automation, precision curing processes, and sustainability-driven production methods improving efficiency and consistency. The use of eco-friendly materials and recycling-based inputs is increasing in response to environmental regulations and fleet sustainability goals.

Key Technology & Innovation Landscape Signals in Global Bus & Coach Tyres Market

- EV-Optimized Bus Tyres: Rising demand for high-load, low-noise, energy-efficient tyres designed for electric buses.

- Low Rolling Resistance Adoption: Increasing focus on fuel-efficient and range-optimized tyre technologies.

- Retreadable Multi-Life Tyres: Strong emphasis on casing durability and multiple lifecycle usage to reduce fleet costs.

- Smart & Connected Tyres: Integration of IoT-based sensors for real-time monitoring and predictive maintenance.

- Reinforced Structural Engineering: Advanced steel belt and carcass designs to handle continuous heavy loads.

- Noise Reduction Technologies: Development of quieter tyres to enhance passenger comfort in urban and electric buses.

- Sustainability Initiatives: Adoption of recycled materials and eco-efficient manufacturing processes.

Strategic Implications of Technology & Innovation Landscape in Global Bus & Coach Tyres Market

The evolving technology landscape has significant strategic implications for tyre manufacturers, fleet operators, and OEMs. Continuous investment in R&D is essential to improve durability, efficiency, and EV compatibility. Companies that deliver high-mileage, low-cost-per-kilometer tyre solutions will gain a strong competitive advantage in public transport and fleet-driven markets.

The shift toward electric bus fleets is reshaping product development priorities, requiring tyres that can handle increased vehicle weight while improving energy efficiency and reducing noise levels. This is driving deeper collaboration between tyre manufacturers and bus OEMs for co-developed EV-specific solutions.

Smart tyre technologies are enabling value-added services such as predictive maintenance, fleet performance analytics, and operational optimization. This is gradually shifting the industry toward service-based business models beyond traditional tyre sales.

Sustainability is becoming a core strategic pillar, with growing adoption of retreading programs, circular economy practices, and eco-friendly material usage. Compliance with environmental regulations and alignment with green mobility initiatives are becoming essential for long-term competitiveness.

For fleet operators, tyre innovation directly impacts operational efficiency, safety, and total cost of ownership. Adoption of advanced tyre technologies is critical for minimizing downtime, improving fuel or energy efficiency, and ensuring reliable passenger transport services.

Global Bus & Coach Tyres Market Technology & Innovation Landscape Forward Outlook

Looking ahead, the global bus & coach tyres market is expected to evolve toward more intelligent, durable, and energy-efficient tyre solutions. Electrification of public transport will remain the key growth driver, significantly increasing demand for EV-optimized bus tyres with improved load handling and low noise characteristics.

Smart tyre technologies are expected to become standard across modern bus fleets, enabling real-time data integration, AI-driven analytics, and predictive maintenance capabilities. This will improve fleet reliability and reduce operational disruptions.

Material innovation will continue to advance, focusing on high-durability compounds, sustainable raw materials, and tread designs that enhance performance while reducing environmental impact. Retreadability will remain a critical value driver for cost-sensitive fleet operators.

Manufacturing processes will become more automated and digitally integrated, improving production efficiency, consistency, and scalability. Smart factories and AI-driven quality systems will accelerate innovation cycles and enhance product reliability.

In conclusion, the Global Bus & Coach Tyres Market is undergoing steady technological evolution where durability, efficiency, and electrification readiness are the core innovation pillars. Companies that successfully integrate EV compatibility, smart technologies, and lifecycle cost optimization will be best positioned to lead the market through 2033.

Market Risk

Global Bus & Coach Tyres Market Risk Factors & Disruption Threats Overview

The Global Bus & Coach Tyres Market operates within a highly utilization-intensive and infrastructure-dependent environment, where demand is closely tied to public transportation systems, urban mobility expansion, and intercity travel networks. The market carries a moderate overall risk profile, supported by stable replacement cycles but exposed to cost volatility, regulatory shifts, and electrification-driven technological change. A key structural risk factor is raw material price volatility, particularly natural rubber, synthetic rubber, steel cord, carbon black, and petroleum-based inputs. Given the heavy-duty nature and large size of bus tyres, fluctuations in input costs significantly impact production economics and long-term supply contracts with fleet operators and governments. Another major disruption driver is the rapid electrification of bus fleets. Electric buses require tyres with higher load-bearing capacity due to heavy battery systems, lower rolling resistance to improve range, and reduced noise levels for passenger comfort. This transition is accelerating product innovation requirements and increasing R&D intensity across the industry. The market is also influenced by high operational intensity. City buses and coaches run continuously with minimal downtime, leading to accelerated wear and tear. While this ensures strong replacement demand, it also increases pressure on manufacturers to deliver higher durability, safety, and cost efficiency. Additionally, increasing government involvement in public transport procurement introduces policy-driven risks. Subsidies, electrification mandates, and procurement standards can significantly influence demand patterns across regions, particularly in Europe and Asia-Pacific.

Global Bus & Coach Tyres Market Risk Factors & Disruption Threats Current Scenario

The current market environment reflects strong recovery in public transportation usage and rising intercity travel demand. However, it is challenged by cost inflation, supply chain disruptions, and tightening regulatory frameworks around emissions and sustainability. Fleet operators are increasingly prioritizing total cost of ownership (TCO), driving demand for fuel-efficient, durable, and retreadable tyres. While this supports premium product adoption, it also intensifies price competition among global manufacturers. Supply chain constraints, particularly in raw material sourcing and logistics, continue to affect production stability. Delays in steel and rubber supply chains can impact OEM production schedules and aftermarket availability. The aftermarket segment remains the dominant revenue contributor, but digital fleet management systems and centralized procurement platforms are reshaping purchasing behavior. This is increasing pricing transparency and shifting bargaining power toward large transit operators. At the same time, electrification of bus fleets is accelerating, especially in China and Europe. This is creating a dual-product environment where traditional diesel bus tyres coexist with EV-optimized solutions, increasing portfolio complexity for manufacturers.

Key Risk Factors & Disruption Threats Signals in Global Bus & Coach Tyres Market

A key disruption signal is the rapid expansion of electric bus fleets. These vehicles require specialized tyre designs that support higher weight loads, improved energy efficiency, and reduced rolling resistance, forcing manufacturers to accelerate innovation cycles. Raw material cost instability remains a persistent signal, driven by global commodity market fluctuations. This creates continuous uncertainty in production costs and pricing strategies. Another important signal is the increasing dominance of government-backed procurement systems in public transportation. Large-scale tenders and long-term contracts influence demand concentration and competitive dynamics. Retreading adoption is also a structural signal. As public transport operators focus on cost efficiency and sustainability, multi-life tyre usage is increasing, particularly in mature markets, which can moderate new tyre demand growth. Sustainability and emission regulations are becoming more stringent, pushing demand for low rolling resistance and eco-friendly tyre solutions, especially in Europe and developed Asian markets.

Strategic Implications of Risk Factors & Disruption Threats in Global Bus & Coach Tyres Market

Manufacturers must prioritize innovation in durability, fuel efficiency, and EV compatibility to remain competitive. Continuous R&D investment is essential to meet evolving fleet and regulatory requirements. Strengthening relationships with fleet operators and government procurement bodies is increasingly important. Companies must move beyond product supply and offer integrated lifecycle solutions, including maintenance and retreading services. Supply chain resilience is a key strategic focus. Diversifying sourcing networks and optimizing regional production capabilities can reduce exposure to raw material volatility and logistical disruptions. Pricing strategies must align with total cost of ownership models, as fleet operators prioritize long-term operational savings over upfront costs. This creates opportunities for premium, high-performance tyre offerings. Digital transformation is also becoming essential. Smart tyre systems, IoT-based monitoring, and predictive maintenance solutions are increasingly important for securing long-term fleet contracts and improving operational efficiency.

Global Bus & Coach Tyres Market Risk Factors & Disruption Threats Forward Outlook

Looking ahead to 2026-2033, the Global Bus & Coach Tyres Market is expected to grow steadily, supported by urbanization, public transport expansion, and rising intercity mobility. However, the risk environment will become more complex due to electrification, sustainability mandates, and evolving procurement structures. Electric buses will remain the most transformative force, driving demand for specialized tyre technologies and reshaping product development priorities. Manufacturers leading in EV tyre innovation will gain a long-term competitive advantage. Retreading will continue to play a critical role in fleet cost optimization, particularly in developed markets. While this supports sustainability, it may moderate growth in new tyre demand. Digital fleet ecosystems will expand, increasing demand for connected tyres and real-time performance monitoring. This will shift competition toward integrated service providers rather than standalone product manufacturers. Overall, the market will remain structurally stable but moderately risk-exposed, with success dependent on balancing durability, efficiency, innovation, and strategic partnerships with public and private fleet operators.

Regulatory Landscape

Global Bus & Coach Tyres Market Regulatory & Policy Environment Overview

The regulatory and policy environment governing the Global Bus & Coach Tyres Market is highly influential, as these tyres directly affect passenger safety, urban mobility efficiency, fuel consumption, and environmental performance. Governments and transport authorities impose strict compliance frameworks to ensure that bus and coach fleets meet safety, durability, and emissions-related standards, especially given the high-frequency, high-load nature of public transport operations. Key regulatory structures such as the European Union Tyre Labelling Regulation (EU) 2020/740 and UNECE tyre safety standards define mandatory performance benchmarks for rolling resistance, wet grip, and external noise. These regulations significantly shape product design, pushing manufacturers toward low rolling resistance, high-durability, and noise-reducing tyre solutions tailored for city buses and long-distance coaches. In parallel, fleet-level regulatory policies focused on carbon reduction and urban air quality are accelerating adoption of fuel-efficient and retreadable tyres. Public transport authorities increasingly require operators to comply with emission reduction targets, indirectly increasing demand for advanced tyre technologies that improve fuel economy and reduce lifecycle emissions. Additionally, regulatory frameworks in emerging economies such as India and China are evolving toward stricter safety inspections, tyre quality certification, and fleet modernization programs. These initiatives are strengthening structured replacement cycles and increasing reliance on certified, high-performance tyre manufacturers.

Global Bus & Coach Tyres Market Regulatory & Policy Environment Current Scenario

The current regulatory landscape is characterized by tightening emissions standards, expansion of electric bus deployment policies, and growing emphasis on lifecycle efficiency in public transport systems. The EU remains the most mature regulatory region, where tyre labeling standards strongly influence procurement decisions by public transport operators. In Europe, low-noise regulations are particularly important due to dense urban mobility networks. This has accelerated adoption of noise-optimized tread designs and advanced rubber compounds in bus and coach tyres. Fleet operators are increasingly required to adopt environmentally compliant tyres to meet municipal sustainability goals. In Asia-Pacific, large-scale public transport expansion programs in China and India are driving standardization in tyre quality and safety certifications. Government-backed urban transit initiatives, including Bus Rapid Transit (BRT) systems and electric bus fleets, are reinforcing demand for durable and EV-compatible tyre solutions. North America maintains strong regulatory oversight through DOT and EPA-aligned efficiency programs, while fleet modernization initiatives in school and intercity bus segments are supporting steady demand for retreadable and fuel-efficient tyres. The rapid electrification of bus fleets globally is also influencing regulatory frameworks, introducing new requirements for load-bearing capacity, torque resistance, and noise reduction performance, reshaping the next generation of tyre standards.

Key Regulatory & Policy Environment Signals in Global Bus & Coach Tyres Market

- EU Tyre Labelling Regulation (EU 2020/740): Drives transparency in fuel efficiency, wet grip, and noise performance for fleet procurement.

- UNECE Tyre Safety Standards: Establish global benchmarks for durability, load capacity, and structural integrity.

- Urban Emission Reduction Policies: Encourage adoption of low rolling resistance and retreadable tyres in public transport fleets.

- Electric Bus Deployment Mandates: Promote EV-compatible tyres with higher load-bearing and noise-reduction capabilities.

- Fleet Sustainability Programs: Incentivize lifecycle efficiency and reduced CO emissions through advanced tyre technologies.

- Asia-Pacific Transport Modernization Policies: Support standardization and improved safety compliance in public bus fleets.

Strategic Implications of Regulatory & Policy Environment in Global Bus & Coach Tyres Market

The regulatory environment significantly increases entry barriers, favoring established global manufacturers with strong compliance capabilities and R&D infrastructure. Smaller players face challenges in meeting evolving safety, environmental, and performance requirements, reinforcing market consolidation. Compliance-driven innovation is becoming a key competitive advantage. Manufacturers are investing heavily in low rolling resistance compounds, retreadable casing technologies, and smart tyre monitoring systems to align with fleet efficiency and regulatory expectations. Fleet operators are increasingly influenced by regulatory labeling systems, shifting purchasing decisions toward certified, high-performance tyres that offer measurable fuel savings and safety improvements. This is strengthening the premium segment within the bus and coach tyre market. Regional regulatory divergence is also shaping supply chain strategies, encouraging localization of production and partnerships with fleet operators and public transport agencies to ensure compliance and cost efficiency.

Global Bus & Coach Tyres Market Regulatory & Policy Environment Forward Outlook

Between 2026 and 2033, the regulatory landscape is expected to become more stringent and sustainability-focused, driven by global decarbonization goals and urban mobility transformation programs. Governments will continue tightening fuel efficiency and noise standards for public transport systems. Europe is likely to expand tyre lifecycle and carbon footprint regulations, while Asia-Pacific will accelerate standardization of safety and performance benchmarks across public bus fleets. These developments will further harmonize global tyre quality expectations. The rapid growth of electric bus fleets will introduce new regulatory requirements focused on energy efficiency, load durability, and acoustic performance, leading to the next generation of EV-optimized bus and coach tyres. Overall, the regulatory environment will continue to act as a strong growth enabler while simultaneously raising compliance complexity, favoring manufacturers that integrate sustainability, durability, and smart mobility technologies into their product portfolios.