Global CNC Machine Market Report size and share Analysis 2026-2033

Global CNC Machine Market Forecast Snapshot: 2026???2033

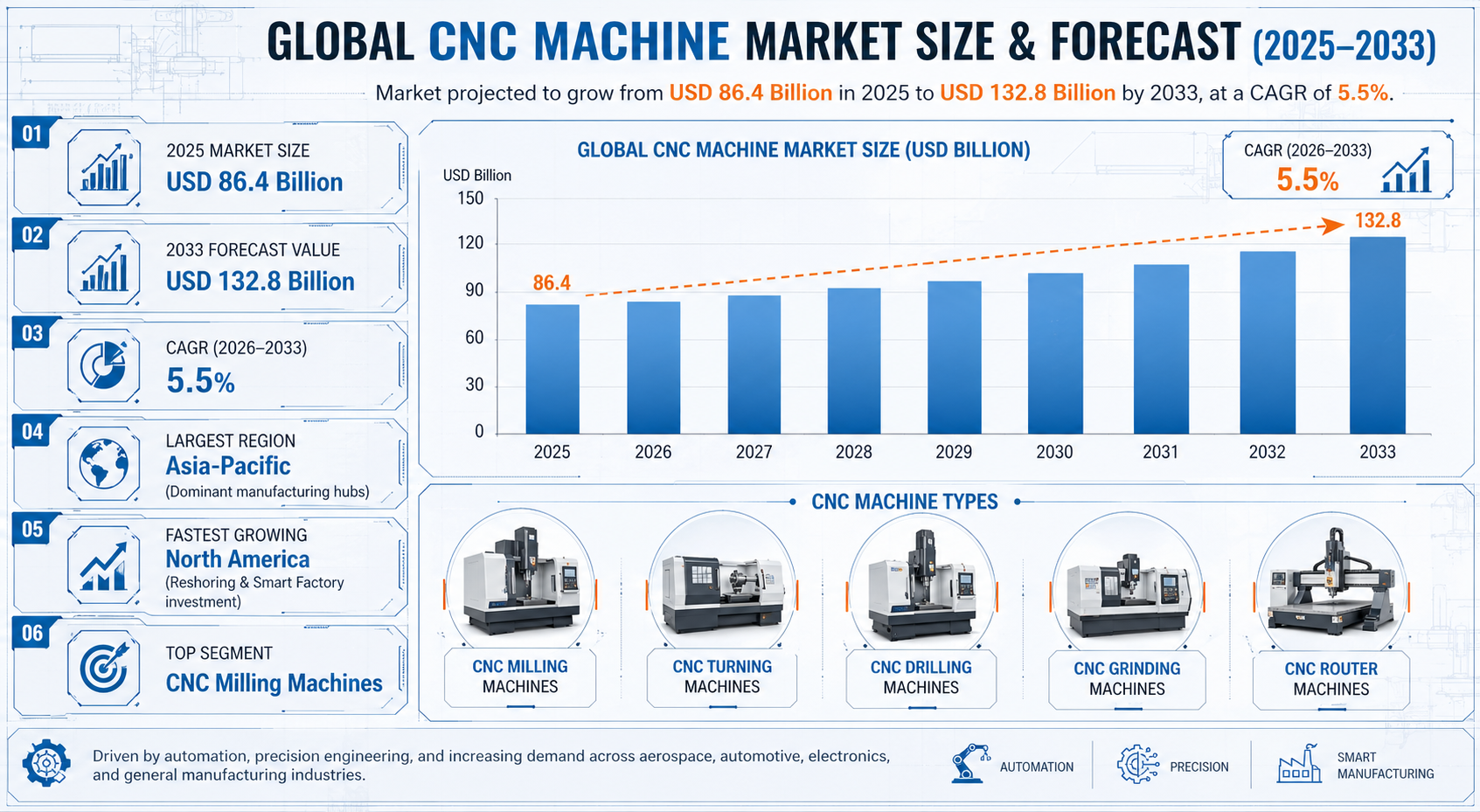

| Metric | Value |

| 2025 Market Size | USD 86.4 Billion |

| 2033 Market Size | USD 132.8 Billion |

| CAGR (2026???2033) | 5.5% |

| Largest Region | Asia-Pacific |

| Fastest Growing Region | North America |

| Top Segment | CNC Milling Machines |

| Key Trend | Industry 4.0 Integration & Smart Manufacturing |

| Future Focus | AI-Driven Automation, Multi-Axis Precision, and Digital Twin Technology |

Global CNC Machine Market Overview

The Global CNC Machine Market is undergoing significant transformation, driven by industrial automation, precision manufacturing requirements, and rapid adoption of Industry 4.0 technologies. CNC (Computer Numerical Control) machines are critical to modern manufacturing ecosystems, enabling high-accuracy machining across automotive, aerospace, defense, electronics, medical devices, and heavy industrial sectors.

According to Pheonix Research, the Global CNC Machine Market is valued at USD 86.4 billion in 2025 and is projected to reach USD 132.8 billion by 2033, registering a CAGR of 5.5% during 2026???2033. This CNC machine revenue forecast reflects increasing capital investment in automated production lines, demand for multi-axis machining solutions, and expansion of advanced manufacturing hubs worldwide.

Asia-Pacific holds the largest share of the Global CNC Machine Market, supported by strong manufacturing bases in China, Japan, South Korea, and India. Meanwhile, North America is emerging as the fastest-growing region, driven by reshoring initiatives, aerospace innovation, EV manufacturing expansion, and smart factory investments.

The post-2025 outlook for CNC machines indicates accelerated adoption of AI-enabled predictive maintenance, robotics integration, digital twin simulation, and cloud-connected machining platforms ??? transforming traditional machining into data-driven precision ecosystems.

Key Drivers of Global CNC Machine Market Growth

1. Accelerating Industrial Automation Adoption

Manufacturers worldwide are rapidly integrating CNC systems to achieve higher precision, minimize human intervention, and optimize productivity in high-volume and complex component manufacturing environments.

2. Expansion of Automotive & Electric Vehicle (EV) Manufacturing

The steady rise in global vehicle production ??? particularly electric vehicles ??? is increasing demand for precision-machined components such as battery enclosures, motor housings, lightweight structural parts, and advanced drivetrain systems.

3. Aerospace & Defense Sector Advancements

Modern aircraft, turbine systems, and defense equipment require ultra-precise, multi-axis machining capabilities. Continuous aerospace innovation and defense modernization programs are strengthening long-term CNC machine demand.

4. Integration of Industry 4.0 & Smart Manufacturing

The adoption of IoT-enabled sensors, AI-powered analytics, cloud connectivity, and real-time performance monitoring is transforming CNC machines into intelligent production assets, enhancing predictive maintenance and operational efficiency.

5. Rising Demand for High-Precision Medical Equipment

Growing production of surgical instruments, orthopedic implants, dental components, and diagnostic devices is driving demand for advanced CNC systems capable of delivering micron-level accuracy and repeatability.

Global CNC Machine Market Segmentation

?? ??1. By Machine Type

1.1 CNC Milling Machines

1.1.1 Vertical Milling Machines

1.1.1.1 3-Axis Vertical Milling

1.1.1.1.1 Entry-Level Production Units

1.1.1.1.2 High-Speed Precision Units

1.1.1.2 4-Axis Vertical Milling

1.1.1.2.1 Rotary Table Integrated

1.1.1.2.2 Indexing-Based Systems

1.1.1.3 5-Axis Vertical Milling

1.1.1.3.1 Simultaneous 5-Axis

1.1.1.3.2 Continuous Contouring Systems

1.1.2 Horizontal Milling Machines

1.1.2.1 Single-Pallet Systems

1.1.2.1.1 Automotive Applications

1.1.2.1.2 Aerospace Components

1.1.2.2 Multi-Pallet Systems

1.1.2.2.1 High-Volume Production

1.1.2.2.2 Flexible Manufacturing Cells

1.2 CNC Turning Machines

1.2.1 CNC Lathes

1.2.1.1 Two-Axis Lathes

1.2.1.1.1 Basic Turning Operations

1.2.1.1.2 Shaft & Cylindrical Components

1.2.1.2 Multi-Axis Lathes

1.2.1.2.1 Complex Geometry Components

1.2.1.2.2 Precision Automotive Parts

1.2.2 Swiss-Type Lathes

1.2.2.1 Medical Component Manufacturing

1.2.2.1.1 Surgical Pins

1.2.2.1.2 Micro Implants

1.2.2.2 Electronics Micro-Parts

1.2.2.2.1 Connectors

1.2.2.2.2 Precision Screws

1.2.3 Multi-Spindle Turning Centers

1.2.3.1 High-Volume Automotive

1.2.3.1.1 Transmission Parts

1.2.3.1.2 Engine Shafts

1.2.3.2 Industrial Fasteners

1.2.3.2.1 Bolts

1.2.3.2.2 Threaded Components

1.3 CNC Grinding Machines

1.3.1 Surface Grinding

1.3.1.1 Flat Surface Components

1.3.1.1.1 Tooling Applications

1.3.1.1.2 Die Components

1.3.2 Cylindrical Grinding

1.3.2.1 Internal Grinding

1.3.2.1.1 Bearing Components

1.3.2.1.2 Precision Tubes

1.3.2.2 External Grinding

1.3.2.2.1 Shafts

1.3.2.2.2 Rollers

1.3.3 Tool & Cutter Grinding

1.3.3.1 Drill Bits

1.3.3.1.1 Carbide Tools

1.3.3.1.2 High-Speed Steel Tools

1.3.3.2 Milling Cutters

1.3.3.2.1 End Mills

1.3.3.2.2 Special Form Tools

1.4 CNC Electrical Discharge Machines (EDM)

1.4.1 Wire EDM

1.4.1.1 Precision Mold Manufacturing

1.4.1.1.1 Injection Molds

1.4.1.1.2 Die Casting Molds

1.4.1.2 Aerospace Components

1.4.1.2.1 Complex Contours

1.4.1.2.2 Hard Materials

1.4.2 Die-Sinking EDM

1.4.2.1 Tool & Die Industry

1.4.2.1.1 Stamping Dies

1.4.2.1.2 Forging Dies

1.4.2.2 Micro-EDM Applications

1.4.2.2.1 Electronics

1.4.2.2.2 Medical Components

1.5 CNC Laser & Plasma Cutting Machines

1.5.1 Fiber Laser Cutting

1.5.1.1 Sheet Metal Processing

1.5.1.1.1 Automotive Panels

1.5.1.1.2 Structural Frames

1.5.2 CO??? Laser Cutting

1.5.2.1 Non-Metal Materials

1.5.2.1.1 Plastics

1.5.2.1.2 Wood & Composites

1.5.3 Plasma Cutting Systems

1.5.3.1 Heavy Industrial Fabrication

1.5.3.1.1 Shipbuilding

1.5.3.1.2 Construction Equipment

?? ?? 2. By Application

2.1 Automotive

2.1.1 Engine Components

2.1.1.1 Cylinder Blocks

2.1.1.2 Crankshafts

2.1.2 Transmission Systems

2.1.2.1 Gear Systems

2.1.2.2 Drive Shafts

2.1.3 EV Battery & Motor Components

2.1.3.1 Battery Housings

2.1.3.2 Motor Casings

2.2 Aerospace & Defense

2.2.1 Structural Components

2.2.2 Turbine & Engine Parts

2.2.3 Defense Equipment

2.3 Electronics

2.3.1 Semiconductor Equipment

2.3.2 Consumer Electronics Components

2.4 Medical Devices

2.4.1 Surgical Instruments

2.4.2 Implants & Prosthetics

2.5 Industrial Machinery

2.5.1 Heavy Equipment Components

2.5.2 Construction Machinery Parts

?? ?? ?? 3. By End-User Industry

3.1 Large Manufacturing Enterprises

3.1.1 Automotive OEMs

3.1.1.1 Passenger Vehicle Manufacturers

3.1.1.1.1 ICE Vehicle Production Units

3.1.1.1.2 Electric Vehicle Production Units

3.1.1.2 Commercial Vehicle Manufacturers

3.1.1.2.1 Heavy-Duty Trucks

3.1.1.2.2 Buses & Fleet Vehicles

3.1.2 Aerospace Manufacturers

3.1.2.1 Commercial Aircraft Producers

3.1.2.1.1 Airframe Manufacturing

3.1.2.1.2 Engine Manufacturing

3.1.2.2 Space & Satellite Manufacturing

3.1.2.2.1 Launch Vehicle Components

3.1.2.2.2 Satellite Structural Parts

3.1.3 Heavy Industrial Equipment Manufacturers

3.1.3.1 Construction Equipment

3.1.3.1.1 Excavators

3.1.3.1.2 Loaders & Cranes

3.1.3.2 Mining Equipment

3.1.3.2.1 Drilling Systems

3.1.3.2.2 Material Handling Systems

3.2 Small & Medium Enterprises (SMEs)

3.2.1 Precision Component Manufacturers

3.2.1.1 Automotive Tier-2 & Tier-3 Suppliers

3.2.1.1.1 Engine Subcomponents

3.2.1.1.2 Fasteners & Small Parts

3.2.1.2 Electronics Component Suppliers

3.2.1.2.1 Micro-Mechanical Parts

3.2.1.2.2 Connector Systems

3.2.2 Tooling & Mold Makers

3.2.2.1 Injection Mold Manufacturers

3.2.2.1.1 Plastic Molds

3.2.2.1.2 Die Casting Molds

3.2.2.2 Die & Fixture Manufacturers

3.2.2.2.1 Stamping Dies

3.2.2.2.2 Jigs & Fixtures

3.2.3 Specialized Fabrication Units

3.2.3.1 Sheet Metal Fabricators

3.2.3.1.1 Enclosures

3.2.3.1.2 Structural Frames

3.2.3.2 Custom Machine Shops

3.2.3.2.1 Prototype Manufacturing

3.2.3.2.2 Low-Volume Production

3.3 Contract Manufacturing & Job Shops

3.3.1 High-Volume Contract Manufacturers

3.3.1.1 Automotive Component Outsourcing

3.3.1.1.1 Powertrain Parts

3.3.1.1.2 Chassis Components

3.3.1.2 Consumer Electronics Manufacturing

3.3.1.2.1 Metal Casings

3.3.1.2.2 Internal Structural Parts

3.3.2 Low-Volume / High-Mix Job Shops

3.3.2.1 Prototype Development

3.3.2.1.1 R&D Projects

3.3.2.1.2 Product Testing Components

3.3.2.2 Custom Engineering Projects

3.3.2.2.1 Industrial Retrofits

3.3.2.2.2 Specialized Machinery Parts

3.3.3 Export-Oriented Manufacturing Units

3.3.3.1 Global OEM Supply

3.3.3.1.1 Aerospace Exports

3.3.3.1.2 Automotive Exports

3.3.3.2 Cross-Border Precision Engineering

3.3.3.2.1 Medical Exports

3.3.3.2.2 Industrial Equipment Exports

3.4 Government & Defense Facilities

3.4.1 Defense Manufacturing Units

3.4.1.1 Weapons & Armament Systems

3.4.1.1.1 Precision Firearm Components

3.4.1.1.2 Missile System Components

3.4.1.2 Military Vehicle Manufacturing

3.4.1.2.1 Armored Vehicles

3.4.1.2.2 Naval Defense Equipment

3.4.2 Public Sector Manufacturing Enterprises

3.4.2.1 Railways & Transportation Equipment

3.4.2.1.1 Locomotive Components

3.4.2.1.2 Track Systems

3.4.2.2 Energy & Power Equipment

3.4.2.2.1 Turbine Components

3.4.2.2.2 Heavy Electrical Systems

3.4.3 Research & Development Institutions

3.4.3.1 Aerospace Research Labs

3.4.3.1.1 Prototype Engines

3.4.3.1.2 Experimental Materials

3.4.3.2 Advanced Manufacturing Research Centers

3.4.3.2.1 Robotics Integration

3.4.3.2.2 Smart Factory Testing

?? ?? ?? 4. By Region

4.1 Asia-Pacific

4.2 North America

4.3 Europe

4.4 Middle East & Africa

4.5 South America

Regional Insights of Global CNC Machine Market

Asia-Pacific ??? Largest Market

Asia-Pacific leads the global CNC machine market, supported by well-established manufacturing hubs in China, Japan, South Korea, and India. The region benefits from strong export-oriented production, proactive government industrialization programs, and large-scale automotive, electronics, and heavy machinery manufacturing. Continuous investment in factory automation and capacity expansion further strengthens its dominant position.

North America ??? Fastest Growing Market

North America is emerging as the fastest-growing region, driven by reshoring initiatives, aerospace and defense innovation, rapid EV manufacturing growth, and rising adoption of smart manufacturing technologies. Increased capital expenditure in advanced automation, robotics integration, and digital production systems across the United States and Canada is accelerating CNC demand.

Europe

Europe???s CNC market is fueled by its strong legacy in precision engineering, particularly in Germany and Italy. Advanced automotive production, aerospace manufacturing, and widespread implementation of Industry 4.0 frameworks are supporting steady regional growth. Regulatory emphasis on efficiency and high-quality production standards also contributes to sustained demand.

Middle East & Africa

The Middle East & Africa region is witnessing gradual CNC adoption, supported by industrial diversification strategies, infrastructure development projects, and rising defense manufacturing investments. Governments are increasingly focusing on local production capabilities to reduce import dependency.

South America

South America is experiencing steady market growth, driven by modernization of manufacturing facilities and expansion of automotive assembly operations. Increasing industrial automation initiatives and growing demand for locally produced components are supporting long-term CNC adoption.

Leading Companies in the Global CNC Machine Market

Prominent players include:

-

Haas Automation, Inc.

-

Okuma Corporation

-

FANUC Corporation

-

Makino Milling Machine Co., Ltd.

-

Hyundai WIA

-

TRUMPF Group

-

Siemens AG (CNC Controls)

-

Doosan Machine Tools

Among these, DMG MORI and Mazak are considered global leaders due to advanced multi-axis solutions, digital integration capabilities, and strong global distribution networks.

Strategic Intelligence & AI-Backed Insights

Pheonix Demand Forecast Engine identifies sustained capital expenditure in automation, EV manufacturing, and aerospace precision components as primary long-term growth catalysts. Consumer (Industrial Buyer) Behavior Analyzer indicates rising demand for high-speed, energy-efficient, and multi-functional CNC systems among manufacturers seeking productivity optimization.Innovation Tracker highlights AI-driven predictive maintenance, digital twin simulations, cloud-connected CNC platforms, and robotics integration as key competitive differentiators.

Porter???s Five Forces Analysis reveals moderate supplier power, high capital intensity barriers, strong technological rivalry, and high differentiation potential in advanced multi-axis machining solutions.

Why the Global CNC Machine Market Remains Critical

-

Backbone of modern precision manufacturing across industries

-

Essential for EV, aerospace, semiconductor, and medical device production

-

Enables automation, cost efficiency, and quality consistency

-

Supports Industry 4.0 transformation and smart factory evolution

-

Drives national industrial competitiveness and export capabilities

Final Takeaway of Global CNC Machine Market

The Global CNC Machine Market is transitioning toward intelligent, connected, and high-precision manufacturing ecosystems. The projected CAGR of 5.5% during 2026???2033 reflects steady industrial automation growth, EV production expansion, and aerospace modernization.

Companies investing in AI-enabled machining systems, multi-axis capabilities, digital twin integration, and smart factory compatibility will secure long-term competitive advantage.

At Pheonix Research, our advanced forecasting frameworks provide in-depth CNC machine revenue analysis, com

???? Social Mentions & Publication Channels

??Explore deeper insights and follow our cross-platform updates on LinkedIn and X for continuous intelligence and market coverage.

LinkedIn : https://www.linkedin.com/feed/update/urn:li:activity:7433406159249715200

X : https://x.com/Pheonix_Insight/status/2027642968501588103?s=20

Competitive Landscape

Global CNC Machine Market Competitive Intensity & Market Structure Overview

The Global CNC Machine Market is characterized by a highly competitive, capital-intensive, and technology-driven ecosystem dominated by a select group of global machine tool manufacturers. These players compete across multi-axis machining systems, automation integration, software-driven controls, and smart manufacturing solutions.

The market operates within a structured hierarchy where Tier 1 manufacturers such as DMG MORI, Mazak, Haas, Okuma, and FANUC hold strong global influence due to their advanced product portfolios, strong OEM relationships, and extensive distribution networks. However, Tier 2 and regional manufacturers continue to compete aggressively on cost efficiency, localized servicing, and mid-range automation solutions.

Competitive intensity is high due to rising demand for precision manufacturing, EV component machining, aerospace-grade parts, and semiconductor tooling. Differentiation is increasingly driven by technological capability rather than price alone, with emphasis on automation, digital integration, and production efficiency.

The market is moderately consolidated at the top, while remaining fragmented in mid-range and entry-level CNC segments. Increasing adoption of Industry 4.0 technologies is further intensifying competition as manufacturers integrate AI, IoT, and digital twin systems into CNC platforms.

Global CNC Machine Market Competitive Intensity & Market Structure Current Scenario

Leading Company Profiles

DMG MORI Co., Ltd.: Global leader in advanced CNC machining solutions, multi-axis systems, and digital manufacturing ecosystems with strong Industry 4.0 integration capabilities.

Mazak Corporation: Major global CNC manufacturer specializing in multi-tasking machines, automation systems, and smart manufacturing solutions.

Haas Automation, Inc.: Leading U.S.-based CNC manufacturer known for cost-efficient machining centers and widespread SME adoption.

Okuma Corporation: Japanese CNC manufacturer focused on high-precision machining, thermal stability systems, and integrated control technologies.

FANUC Corporation: Global leader in CNC controls, robotics integration, and factory automation systems enabling smart manufacturing ecosystems.

Makino Milling Machine Co., Ltd.: Specializes in high-precision CNC milling and EDM systems for aerospace, automotive, and die-mold industries.

Hyundai WIA: Strong presence in automotive CNC machining solutions and mass production systems across Asia-Pacific.

TRUMPF Group: Key player in CNC laser cutting and smart sheet metal processing systems with strong Industry 4.0 capabilities.

Siemens AG: Leading provider of CNC control systems and digital factory automation platforms enabling connected machining environments.

Doosan Machine Tools: Emerging global competitor focused on high-performance CNC turning and milling machines for industrial applications.

Key Competitive Intensity & Market Structure Signals in CNC Machine Market

A key structural factor in the CNC Machine Market is the increasing shift toward smart manufacturing ecosystems. OEMs and industrial manufacturers are prioritizing machines that integrate seamlessly with digital platforms, enabling predictive maintenance, real-time monitoring, and production optimization.

High entry barriers exist due to significant capital requirements, technological complexity, and strong brand loyalty among industrial buyers. However, competition remains intense in mid-range CNC segments where cost-effective alternatives are widely available.

Another major competitive driver is the rapid growth of EV, aerospace, and semiconductor manufacturing, all of which require ultra-precision machining. This is pushing manufacturers to invest heavily in multi-axis systems, high-speed machining, and automation-enabled production lines.

The rise of Industry 4.0 is reshaping competition by making software integration, data analytics, and cloud connectivity core differentiators. CNC machines are evolving from standalone equipment into connected, intelligent manufacturing assets.

Regional manufacturers continue to play a strong role in price-sensitive markets, while global leaders dominate high-value precision and automated machining segments.

Strategic Implications of Competitive Intensity & Market Structure in CNC Machine Market

The competitive environment is driving manufacturers toward ecosystem-based strategies rather than standalone machine sales. Companies are increasingly offering integrated solutions that combine CNC hardware, automation systems, robotics, and software analytics platforms.

Total cost of ownership (TCO), rather than upfront machine cost, is becoming a key purchasing factor. This benefits manufacturers offering energy-efficient, low-maintenance, and high-durability CNC systems with predictive servicing capabilities.

Digital transformation is a major strategic differentiator. Companies investing in digital twin technology, AI-driven machining optimization, and cloud-connected factory systems are gaining strong competitive advantages in long-term OEM contracts.

Electrification and advanced mobility manufacturing are also reshaping demand patterns. EV production requires specialized CNC systems for battery components, motor housings, and lightweight structural parts, creating new premium opportunities.

Additionally, robotics integration is becoming central to competitive positioning, as fully automated machining cells reduce labor dependency and increase production scalability.

Global CNC Machine Market Competitive Intensity & Market Structure Forward Outlook

The Global CNC Machine Market is expected to remain highly competitive yet structurally stable, with continued dominance by Tier 1 global manufacturers and gradual consolidation through mergers, partnerships, and technology acquisitions.

Future competition will increasingly center on AI-enabled machining, autonomous production systems, and fully connected smart factories. Manufacturers that fail to adapt to digital transformation risk losing share in high-growth industrial segments.

Asia-Pacific will continue to dominate manufacturing demand, while North America will accelerate growth through reshoring, EV expansion, and aerospace modernization. Europe will remain a stronghold for precision engineering and Industry 4.0 adoption.

In the long term, three core competitive pillars will define the market: intelligent automation, multi-axis precision capability, and fully integrated digital manufacturing ecosystems. Companies aligned with these trends will lead the CNC Machine Market through 2033.

Value Chain

Global CNC Machine Market Value Chain & Supply Chain Evolution Overview

The Global CNC Machine Market value chain is evolving from traditional machine tool manufacturing into a highly integrated, digitally connected industrial automation ecosystem centered on precision engineering, smart production, and advanced manufacturing intelligence. Unlike conventional machining systems focused primarily on hardware performance, modern CNC ecosystems increasingly combine machine tools, software controls, sensors, automation platforms, robotics, AI-powered predictive systems, and cloud-enabled production management.

The CNC machine value chain spans raw material sourcing, precision component manufacturing, CNC controller systems, servo motors, spindle technologies, CAD/CAM software, robotics integration, machine assembly, industrial distribution, aftermarket servicing, predictive maintenance, and smart factory deployment. As global manufacturing shifts toward efficiency, automation, and micron-level precision, the market increasingly depends on integrated digital ecosystems rather than standalone machine sales.

Upstream supply chain dynamics are shaped by castings and structural materials suppliers, high-precision spindle manufacturers, ball screw and linear motion providers, semiconductor and CNC control manufacturers, servo motor suppliers, software developers, robotics integrators, and industrial IoT technology providers. Increasingly, advanced CNC systems depend on sophisticated electronics, sensors, AI diagnostics, and software architecture alongside traditional mechanical engineering.

Machine development strategies increasingly prioritize multi-axis precision, modular automation, digital twin simulation, predictive maintenance, cloud diagnostics, energy efficiency, and seamless Industry 4.0 compatibility. CNC companies are moving beyond equipment production toward intelligent manufacturing platforms capable of autonomous optimization and real-time operational analytics.

Distribution is increasingly enterprise-centric, with OEM sales networks, industrial distributors, system integrators, contract manufacturing channels, aerospace and automotive partnerships, and government-backed industrialization programs driving expansion. Capital equipment financing, lifecycle service contracts, software subscriptions, and predictive maintenance packages are reshaping monetization structures globally.

Supply chain challenges include semiconductor shortages, precision component lead times, geopolitical manufacturing shifts, capital expenditure cycles, skilled labor shortages, cybersecurity risks in connected systems, and balancing advanced technological capability with cost competitiveness.

Global CNC Machine Market Value Chain & Supply Chain Evolution Current Scenario

The current CNC machine market is shaped by accelerating factory automation, EV manufacturing expansion, aerospace modernization, reshoring strategies, and Industry 4.0 deployment.

Upstream, CNC manufacturers are increasingly investing in advanced electronics, AI software systems, servo technologies, robotics integration, and digital controls to differentiate product capabilities and improve long-term operational value.

Production ecosystems increasingly focus on CNC milling machines, turning centers, laser systems, EDM technologies, and integrated machining cells optimized for productivity, flexibility, and precision.

Technology infrastructure increasingly includes cloud connectivity, AI-powered predictive maintenance, machine vision, digital twin platforms, adaptive machining algorithms, and real-time production intelligence.

Distribution networks are dominated by industrial OEM partnerships, automation solution providers, large enterprise manufacturing contracts, government industrial projects, and specialized SME machine tool channels.

Customer retention increasingly depends on software ecosystems, service reliability, upgrade pathways, operator training, spare parts availability, and long-term lifecycle productivity enhancement.

Key Value Chain & Supply Chain Evolution Signals in Global CNC Machine Market

Several structural transformations are reshaping the CNC ecosystem globally.

First, CNC machines are increasingly evolving into intelligent smart factory assets through AI diagnostics, IoT integration, and predictive maintenance capabilities.

Second, EV production, aerospace precision engineering, and semiconductor manufacturing are emerging as major long-term demand accelerators due to their high-complexity machining requirements.

Third, digital twin technology is increasingly improving design simulation, machine optimization, and operational forecasting across advanced production systems.

Fourth, robotics integration is expanding through automated tool handling, lights-out manufacturing, and flexible manufacturing cells that reduce labor dependency.

Fifth, software ecosystems such as CAD/CAM, machine analytics, and cloud-based control platforms are becoming strategically important competitive differentiators.

Sixth, supply chain localization and reshoring initiatives are increasingly influencing regional machine demand, especially in North America and Europe.

Strategic Implications of Value Chain & Supply Chain Evolution in Global CNC Machine Market

Leading companies such as DMG MORI, Mazak, Haas Automation, FANUC, Okuma, and TRUMPF are strengthening market positions through advanced automation, AI integration, software ecosystems, and global industrial partnerships.

Long-term competitive advantage increasingly depends on technology integration, precision capability, software compatibility, and lifecycle service ecosystems rather than machine hardware alone.

Companies with strong multi-axis machining portfolios, digital connectivity, and predictive service capabilities are better positioned to capture high-value industrial demand.

AI-enabled predictive maintenance, digital twin ecosystems, and robotics integration are becoming increasingly important for premium differentiation.

Supply chain resilience increasingly depends on balancing component sourcing security, electronics availability, production scalability, and geopolitical manufacturing diversification.

As competition intensifies, CNC manufacturers must increasingly evolve from machine suppliers into full-spectrum intelligent manufacturing solution providers.

Global CNC Machine Market Value Chain & Supply Chain Evolution Forward Outlook

Between 2026 and 2033, the CNC machine market value chain is expected to become more AI-automated, software-defined, cloud-connected, and digitally autonomous.

CNC platforms will increasingly prioritize adaptive machining intelligence, robotics-led automation, predictive operational analytics, digital twin manufacturing ecosystems, and integrated smart factory compatibility.

Distribution ecosystems will increasingly expand through industrial digital platforms, OEM software subscriptions, robotics partnerships, aerospace modernization programs, EV supply chain integration, and advanced manufacturing government incentives.

Monetization ecosystems are likely to evolve toward lifecycle manufacturing intelligence models combining equipment sales, SaaS-based machine optimization, predictive maintenance subscriptions, and production-as-a-service frameworks.

Advanced analytics, machine learning optimization, and autonomous production scheduling are expected to redefine industrial productivity models.

Ultimately, the CNC machine value chain will evolve from standalone precision equipment manufacturing toward broader intelligent industrial infrastructure supporting global automation, industrial sovereignty, and next-generation manufacturing competitiveness.

Market-Specific Value Chain

- Raw Materials & Precision Components: Castings, steel structures, spindles, bearings, linear guides, ball screws, motors, semiconductors, servo systems

- Control Systems & Digital Infrastructure: CNC controllers, CAD/CAM software, AI diagnostics, digital twin systems, IoT sensors, cloud connectivity

- Machine Manufacturing & Productization: CNC milling, turning, grinding, EDM, laser systems, robotics integration, modular automation cells

- Distribution & Industrial Deployment: OEM networks, industrial distributors, automation integrators, aerospace/automotive contracts, government industrialization channels

- Aftermarket Services & Lifecycle Monetization: Maintenance, software upgrades, predictive analytics, tooling services, operator training, retrofit solutions

- Smart Manufacturing Ecosystem Expansion: Industry 4.0 integration, autonomous production, robotics ecosystems, cloud manufacturing, digital factory transformation

Company-to-Stage Mapping

- Raw Materials & Precision Components: THK, NSK, Bosch Rexroth, Siemens motion systems, FANUC servo technologies

- Control Systems & Digital Infrastructure: Siemens AG, FANUC, Mitsubishi Electric, Heidenhain, Autodesk CAM ecosystems

- Machine Manufacturing & Productization: DMG MORI, Mazak, Haas Automation, Okuma, Makino, TRUMPF

- Distribution & Industrial Deployment: Global OEM dealer networks, industrial distributors, automation integrators, enterprise manufacturing partners

- Aftermarket Services & Lifecycle Monetization: DMG MORI service ecosystems, Haas support systems, FANUC predictive maintenance, Siemens digital service platforms

- Smart Manufacturing Ecosystem Expansion: Siemens Industry 4.0, FANUC robotics, TRUMPF smart factory systems, DMG MORI digital transformation platforms

Investment Activity

Global CNC Machine Market Investment & Funding Dynamics Overview

Investment and funding dynamics in the Global CNC Machine Market are being strongly driven by the global shift toward industrial automation, precision manufacturing, EV production expansion, aerospace modernization, and Industry 4.0 adoption. Between 2026 and 2033, capital expenditure is increasingly focused on smart factory infrastructure, multi-axis CNC systems, AI-enabled machining platforms, robotics integration, and digital twin-based manufacturing ecosystems.

The market is highly capital-intensive and technology-driven, making it one of the most strategically important segments in the global industrial machinery landscape. Leading companies such as DMG MORI, Mazak, FANUC, Haas Automation, Okuma, Makino, and TRUMPF are heavily investing in next-generation CNC technologies, cloud-connected machining systems, and predictive maintenance solutions to strengthen long-term competitive positioning.

A key structural transformation shaping investment flows is the transition from conventional standalone machining systems to fully integrated intelligent manufacturing ecosystems. This shift is directing funding toward AI-powered automation, real-time machine monitoring, digital production optimization, and high-precision multi-axis machining platforms designed for EV, aerospace, semiconductor, and medical applications.

Global CNC Machine Market Investment & Funding Dynamics Current Scenario

Current investment activity is being fueled by rising global demand for precision components, manufacturing reshoring initiatives, and rapid expansion of EV and aerospace production. Governments and private manufacturers are increasing capital deployment into advanced production technologies to improve productivity, reduce dependency on manual labor, and enhance manufacturing efficiency.

- Asia-Pacific: Dominates investment activity due to large-scale manufacturing ecosystems in China, Japan, South Korea, and India, supported by strong export-driven industrial growth.

- North America: Fastest-growing investment region driven by reshoring strategies, aerospace innovation, EV manufacturing expansion, and smart factory modernization.

- Europe: Strong funding base supported by precision engineering leadership, Industry 4.0 adoption, and advanced automotive manufacturing ecosystems.

- Middle East, Africa & South America: Emerging investment regions focused on industrial diversification, infrastructure development, and gradual automation adoption.

Key Investment & Funding Dynamics Signals in Global CNC Machine Market

- Rapid expansion of EV manufacturing is driving capital inflows into high-precision machining systems for battery housings, motor components, and lightweight structures.

- Aerospace and defense modernization programs are increasing demand for multi-axis CNC machines capable of ultra-precise machining of complex components.

- Industry 4.0 transformation is accelerating investment in AI-enabled CNC systems, IoT-connected machines, and smart factory platforms.

- Digital twin technology adoption is attracting funding for simulation-based manufacturing optimization and predictive production planning.

- Demand for energy-efficient and high-speed machining solutions is driving innovation-focused capital allocation across OEMs and industrial buyers.

Strategic Implications of Investment & Funding Dynamics in Global CNC Machine Market

- Competitive advantage is increasingly defined by automation capabilities, precision engineering, and digital integration rather than hardware alone.

- Companies with strong AI, robotics, and software-driven machining ecosystems are attracting higher valuation and investment interest.

- Regional manufacturing reshoring trends are reshaping global investment flows, particularly in North America and Europe.

- Vertical integration across hardware, software, and service ecosystems is becoming essential for long-term profitability.

- Strategic partnerships between CNC manufacturers, software providers, and industrial automation firms are accelerating ecosystem development.

Global CNC Machine Market Investment & Funding Dynamics Forward Outlook

Looking ahead, the Global CNC Machine Market is expected to witness sustained investment growth as industries transition toward fully automated, intelligent, and connected manufacturing environments.

Future capital allocation will increasingly focus on AI-driven machining optimization, cloud-based CNC platforms, robotics-integrated production lines, and digital twin-enabled manufacturing systems designed to improve efficiency, accuracy, and scalability.

- Asia-Pacific: Will remain the largest investment hub due to its manufacturing dominance and continuous industrial expansion.

- North America: Will lead growth in smart manufacturing, EV-driven machining demand, and aerospace precision engineering investment.

- Europe: Will continue to drive innovation in Industry 4.0, sustainable manufacturing, and high-precision engineering systems.

Technological evolution in AI automation, predictive maintenance, and cloud-connected manufacturing platforms will significantly redefine funding priorities across the CNC machine industry.

Overall, the Global CNC Machine Market is positioned as a foundational pillar of modern industrial transformation through 2033. Companies that invest early in intelligent manufacturing systems, multi-axis automation, and digital production ecosystems will secure long-term leadership in the next phase of global industrial competitiveness.

Technology & Innovation

Global CNC Machine Market Technology & Innovation Landscape Overview

The technology and innovation landscape within the Global CNC Machine Market is rapidly evolving toward intelligent manufacturing systems, where precision engineering is increasingly driven by data, automation, and digital connectivity. Traditional CNC machining is transitioning into a fully integrated smart manufacturing ecosystem supported by AI, IoT, robotics, and advanced simulation technologies.

Innovation intensity in the CNC machine industry is high, driven by the need for ultra-precision manufacturing, reduced production cycles, energy efficiency, and seamless integration with Industry 4.0 frameworks. Modern CNC systems are no longer standalone machines; they are becoming connected nodes within digital factories that continuously communicate, optimize, and self-correct.

A key transformation is the integration of AI-driven control systems, where machining parameters such as speed, feed rate, tool wear, and vibration are continuously optimized in real time. This shift significantly enhances productivity, reduces material waste, and improves component accuracy across automotive, aerospace, and medical manufacturing sectors.

Another major innovation trend is the adoption of digital twin technology, which enables manufacturers to create virtual replicas of machining processes. These simulations allow engineers to test, predict, and optimize machining operations before physical production begins, reducing downtime and improving operational efficiency.

Global CNC Machine Market Technology & Innovation Landscape Current Scenario

Currently, the CNC machine industry is experiencing a strong shift toward smart, connected, and automated production systems. Manufacturers are focusing on improving machine intelligence, operational flexibility, and predictive maintenance capabilities to enhance overall equipment effectiveness (OEE).

AI-enabled predictive maintenance systems are widely being deployed to monitor machine health in real time. By analyzing vibration patterns, thermal data, and spindle performance, these systems can predict potential failures before they occur, minimizing unplanned downtime and maintenance costs.

IoT-enabled CNC machines are also becoming standard in modern factories. These machines are equipped with sensors that continuously collect operational data and transmit it to centralized cloud platforms, enabling remote monitoring, performance tracking, and data-driven decision-making across global production networks.

Multi-axis machining technology, particularly 5-axis and 7-axis CNC systems, is gaining strong traction due to its ability to produce complex geometries in a single setup. This reduces production time, improves precision, and eliminates multiple machining steps, especially in aerospace and medical component manufacturing.

Robotics integration is another key advancement, where CNC machines are combined with robotic arms for automated loading, unloading, and tool handling. This is significantly improving production efficiency and enabling fully automated manufacturing cells.

Cloud-based CNC platforms are emerging as a critical innovation layer, enabling centralized control, software updates, and production optimization across multiple facilities. This connectivity is enhancing scalability and operational transparency in global manufacturing networks.

In addition, advanced cutting tool materials such as carbide composites, ceramic coatings, and diamond-coated tools are improving machining durability, reducing tool wear, and enabling high-speed precision manufacturing.

Key Technology & Innovation Trends in Global CNC Machine Market

- AI-Driven Machining Optimization: Real-time adjustment of cutting parameters for improved efficiency and precision.

- Digital Twin Integration: Virtual simulation of machining operations for predictive optimization and reduced downtime.

- IoT-Connected Smart Factories: CNC machines integrated into cloud-based industrial ecosystems.

- Multi-Axis High-Precision Machining: 5-axis and 7-axis systems enabling complex component manufacturing.

- Predictive Maintenance Systems: Sensor-driven failure prediction and automated maintenance scheduling.

- Robotics & Automation Integration: Fully automated production cells with robotic handling systems.

- Cloud-Based CNC Control Platforms: Remote monitoring, analytics, and centralized production control.

- Advanced Tooling Materials: High-durability coatings and next-generation cutting tools improving lifespan and precision.

Strategic Implications of Technology & Innovation

The ongoing technological evolution is fundamentally reshaping competitive dynamics in the CNC machine industry. Manufacturers that adopt AI-enabled machining, digital twins, and cloud-based systems are achieving significant gains in productivity, cost efficiency, and product quality.

For industrial users, advanced CNC technologies are enabling faster production cycles, reduced operational costs, and higher design flexibility. This is particularly important in sectors such as electric vehicles, aerospace components, and precision medical devices, where accuracy and speed are critical.

Automation and smart manufacturing adoption are also increasing entry barriers for traditional machining providers, favoring technology-driven manufacturers with integrated digital ecosystems.

Sustainability is becoming an important innovation driver, with energy-efficient CNC systems, reduced material waste technologies, and optimized machining processes contributing to lower carbon footprints in manufacturing operations.

Future Outlook of CNC Machine Technology & Innovation

Looking ahead, the CNC machine industry is expected to evolve into fully autonomous manufacturing ecosystems powered by AI, robotics, and real-time data intelligence. Machines will increasingly self-optimize, self-diagnose, and adapt to production requirements without manual intervention.

The adoption of hyper-connected factories will accelerate, where CNC machines, ERP systems, robotics, and supply chain networks operate as a unified digital system. This will significantly improve production efficiency, responsiveness, and customization capabilities.

Next-generation CNC systems will also integrate advanced machine learning algorithms capable of learning from historical machining data to continuously improve performance over time.

In conclusion, the Global CNC Machine Market is transitioning from traditional precision machining to intelligent, connected, and autonomous manufacturing. Companies that invest in AI-driven automation, digital twin ecosystems, and smart factory integration will lead the next phase of industrial transformation through 2033.