Global Colorants Market Report size and share Analysis 2026-2033

Global Colorants Market Forecast Snapshot: 2026???2033

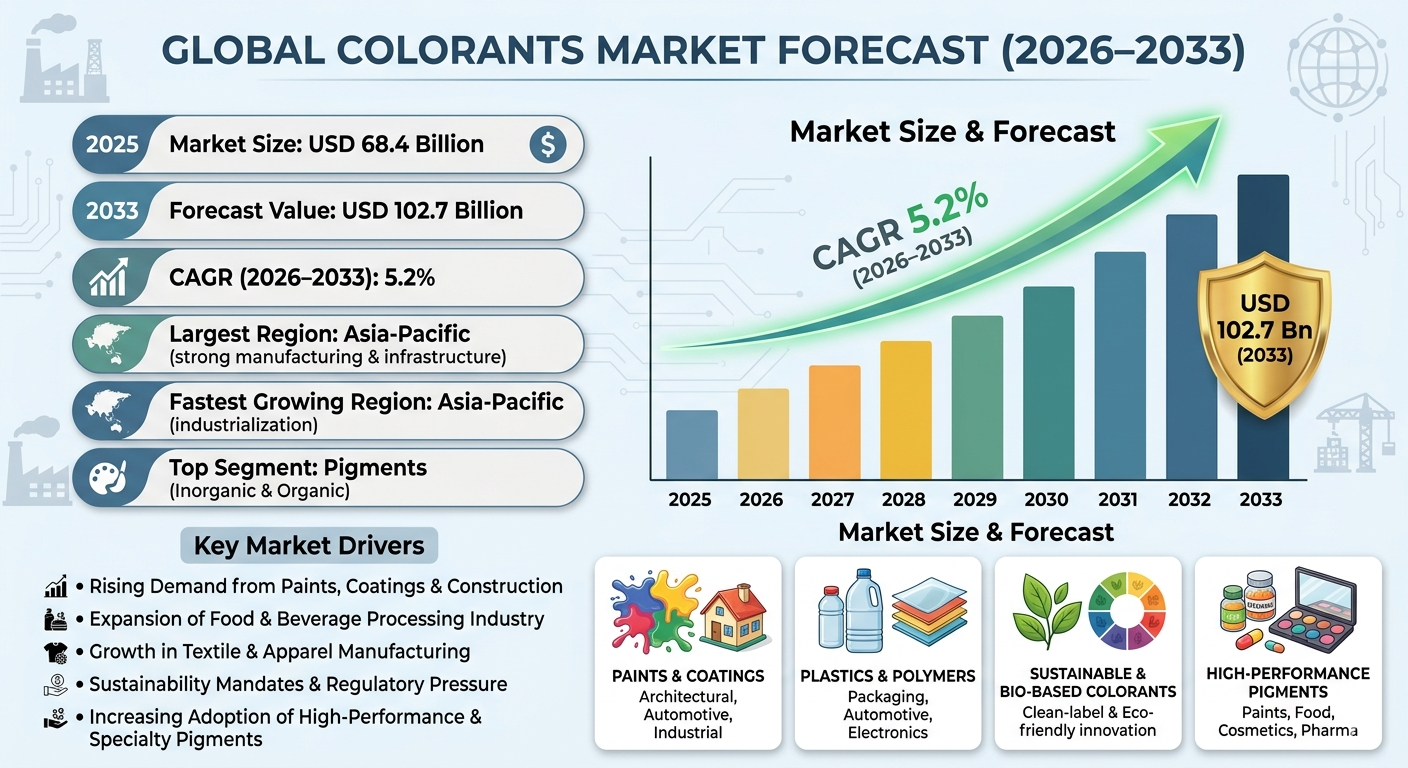

| Metric | Value |

| 2025 Market Size | USD 68.4 Billion |

| 2033 Market Size | USD 102.7 Billion |

| CAGR (2026???2033) | 5.2% |

| Largest Region | Asia-Pacific |

| Fastest Growing Region | Asia-Pacific |

| Top Segment | Pigments (Inorganic & Organic) |

| Key Trend | Sustainable & Bio-Based Colorant Innovation |

| Future Focus | High-Performance Pigments, Natural Colorants, and Smart Functional Coatings |

Global Colorants Market Overview

The Global Colorants Market is undergoing structural transformation driven by sustainability mandates, high-performance material requirements, and growing demand across food & beverages, textiles, plastics, paints & coatings, cosmetics, and pharmaceuticals.

Colorants are essential to product differentiation, branding, functionality, and regulatory compliance. As industries increasingly prioritize eco-friendly formulations and premium aesthetics, the market is shifting from traditional commodity pigments toward advanced, sustainable, and specialty solutions.

According to Pheonix Research, the Global Colorants Market size is valued at USD 68.4 billion in 2025 and is projected to reach USD 102.7 billion by 2033, registering a CAGR of 5.2% during 2026???2033. This revenue forecast reflects expansion in construction, packaging, processed food, personal care, and industrial manufacturing sectors.

Asia-Pacific dominates the market due to its strong textile, plastics, and coatings manufacturing base, while also emerging as the fastest-growing region due to rapid industrialization and infrastructure expansion.

The post-2025 outlook indicates accelerated innovation in bio-based pigments, nano-colorants, smart coatings, and regulatory-compliant food-grade natural colorants.

Key Drivers of Global Colorants Market Growth

1. Rising Demand from Paints, Coatings & Construction Sectors

Accelerating infrastructure development, urbanization, and real estate expansion are significantly increasing demand for architectural, decorative, and industrial coatings, thereby driving pigment consumption globally.

2. Expansion of Food & Beverage Processing Industry

Growing clean-label preferences and tightening regulatory standards are encouraging the adoption of natural and food-grade colorants, particularly in beverages, confectionery, dairy, and processed foods.

3. Growth in Textile & Apparel Manufacturing

Strong textile production, particularly across Asia-Pacific, continues to fuel global demand for dyes and specialty textile colorants, supported by fast fashion and technical textile innovation.

4. Sustainability Mandates & Regulatory Pressure

Stringent environmental regulations in Europe and North America are accelerating the transition toward eco-friendly, low-VOC, heavy-metal-free, and bio-based colorant solutions.

5. Increasing Adoption of High-Performance & Specialty Pigments

Industries such as automotive, packaging, electronics, and industrial manufacturing require advanced pigments offering enhanced durability, UV resistance, thermal stability, and long-term performance.

Global Colorants Market Segmentation

?? ?? ?? ??1.By Type

1.1 Dyes

1.1.1 Reactive Dyes

1.1.1.1 Textile Reactive Dyes

1.1.1.2 Fiber-Reactive Dyes

1.1.1.3 Low-Salt Reactive Dyes

1.1.2 Disperse Dyes

1.1.2.1 Polyester Dyes

1.1.2.2 High-Energy Disperse Dyes

1.1.3 Acid Dyes

1.1.3.1 Wool & Silk Dyes

1.1.3.2 Leather Dyes

1.1.4 Direct & Basic Dyes

1.1.4.1 Paper Dyes

1.1.4.2 Acrylic Fiber Dyes

1.2 Pigments (Largest Segment)

1.2.1 Organic Pigments

1.2.1.1 Azo Pigments

1.2.1.2 Phthalocyanine Pigments

1.2.1.3 Quinacridone Pigments

1.2.1.4 High-Performance Organic Pigments

1.2.2 Inorganic Pigments

1.2.2.1 Titanium Dioxide

1.2.2.2 Iron Oxide Pigments

1.2.2.3 Chromium Pigments

1.2.2.4 Carbon Black

1.2.3 Specialty Pigments

1.2.3.1 Metallic Pigments

1.2.3.2 Pearlescent Pigments

1.2.3.3 Fluorescent Pigments

1.2.3.4 Thermochromic Pigments

1.2.3.5 Photochromic Pigments

1.3 Natural Colorants

1.3.1 Plant-Based

1.3.1.1 Curcumin

1.3.1.2 Carotenoids

1.3.1.3 Anthocyanins

1.3.1.4 Chlorophyll

1.3.2 Animal-Based

1.3.2.1 Carmine

1.3.3 Microbial & Fermentation-Based Colorants

?? ?? ??2. By Application

2.1 Paints & Coatings

2.1.1 Architectural Coatings

2.1.1.1 Interior Wall Coatings

2.1.1.1.1 Emulsion Paints

2.1.1.1.2 Matte & Satin Finishes

2.1.1.2 Exterior Wall Coatings

2.1.1.2.1 Weather-Resistant Coatings

2.1.1.2.2 UV-Protection Coatings

2.1.1.3 Decorative & Specialty Coatings

2.1.1.3.1 Texture Finishes

2.1.1.3.2 Anti-Microbial Coatings

2.1.2 Industrial Coatings

2.1.2.1 Machinery & Equipment Coatings

2.1.2.1.1 Corrosion-Resistant Coatings

2.1.2.1.2 Heat-Resistant Coatings

2.1.2.2 Protective Metal Coatings

2.1.2.2.1 Anti-Rust Coatings

2.1.2.2.2 Powder Coatings

2.1.3 Automotive Coatings

2.1.3.1 OEM Automotive Coatings

2.1.3.1.1 Basecoat Pigments

2.1.3.1.2 Clearcoat Systems

2.1.3.2 Refinish Coatings

2.1.3.2.1 Aftermarket Repair Paints

2.1.3.2.2 Custom Color Coatings

2.1.4 Marine & Protective Coatings

2.1.4.1 Shipbuilding Coatings

2.1.4.1.1 Anti-Fouling Coatings

2.1.4.1.2 Saltwater-Resistant Coatings

2.1.4.2 Heavy-Duty Protective Coatings

2.1.4.2.1 Chemical-Resistant Coatings

2.1.4.2.2 Industrial Floor Coatings

2.2 Plastics & Polymers

2.2.1 Packaging Plastics

2.2.1.1 Flexible Packaging

2.2.1.1.1 Food Packaging Films

2.2.1.1.2 Multi-Layer Packaging

2.2.1.2 Rigid Packaging

2.2.1.2.1 Bottles & Containers

2.2.1.2.2 Caps & Closures

2.2.2 Automotive Plastics

2.2.2.1 Interior Components

2.2.2.1.1 Dashboard Panels

2.2.2.1.2 Trim Components

2.2.2.2 Exterior Components

2.2.2.2.1 Bumpers

2.2.2.2.2 Grilles

2.2.3 Consumer Goods

2.2.3.1 Household Products

2.2.3.1.1 Storage Containers

2.2.3.1.2 Kitchenware

2.2.3.2 Toys & Lifestyle Products

2.2.3.2.1 Educational Toys

2.2.3.2.2 Decorative Items

2.2.4 Electronics Components

2.2.4.1 Device Casings

2.2.4.1.1 Smartphone Bodies

2.2.4.1.2 Laptop Casings

2.2.4.2 Insulation & Functional Plastics

2.2.4.2.1 Heat-Resistant Plastics

2.2.4.2.2 Flame-Retardant Components

2.3 Food & Beverages

2.3.1 Bakery & Confectionery

2.3.1.1 Cakes & Pastries

2.3.1.1.1 Decorative Icing Colors

2.3.1.1.2 Fillings & Toppings

2.3.1.2 Candies & Chocolates

2.3.1.2.1 Coated Chocolates

2.3.1.2.2 Sugar Confections

2.3.2 Dairy Products

2.3.2.1 Flavored Milk

2.3.2.1.1 Chocolate Milk

2.3.2.1.2 Fruit-Flavored Milk

2.3.2.2 Yogurt & Ice Cream

2.3.2.2.1 Fruit Yogurt

2.3.2.2.2 Colored Ice Cream Variants

2.3.3 Beverages

2.3.3.1 Carbonated Drinks

2.3.3.1.1 Colas

2.3.3.1.2 Fruit-Flavored Sodas

2.3.3.2 Functional & Energy Drinks

2.3.3.2.1 Vitamin-Infused Beverages

2.3.3.2.2 Sports Drinks

2.3.4 Processed Foods

2.3.4.1 Ready-to-Eat Meals

2.3.4.1.1 Frozen Meals

2.3.4.1.2 Instant Noodles

2.3.4.2 Sauces & Seasonings

2.3.4.2.1 Tomato-Based Sauces

2.3.4.2.2 Spice Blends

2.4 Textiles

2.4.1 Apparel

2.4.1.1 Casual Wear

2.4.1.1.1 Cotton Fabrics

2.4.1.1.2 Polyester Blends

2.4.1.2 Sportswear

2.4.1.2.1 Performance Fabrics

2.4.1.2.2 Moisture-Wicking Textiles

2.4.2 Home Textiles

2.4.2.1 Curtains & Upholstery

2.4.2.1.1 Printed Fabrics

2.4.2.1.2 Dyed Fabrics

2.4.2.2 Bedding & Linens

2.4.2.2.1 Sheets

2.4.2.2.2 Comforters

2.4.3 Technical Textiles

2.4.3.1 Industrial Fabrics

2.4.3.1.1 Filter Fabrics

2.4.3.1.2 Protective Wear

2.4.3.2 Automotive Textiles

2.4.3.2.1 Seat Fabrics

2.4.3.2.2 Interior Linings

2.5 Cosmetics & Personal Care

2.5.1 Makeup Products

2.5.1.1 Lip Products

2.5.1.1.1 Lipsticks

2.5.1.1.2 Lip Gloss

2.5.1.2 Eye Makeup

2.5.1.2.1 Eyeshadow

2.5.1.2.2 Mascara

2.5.2 Hair Colorants

2.5.2.1 Permanent Hair Color

2.5.2.1.1 Ammonia-Based

2.5.2.1.2 Ammonia-Free

2.5.2.2 Temporary & Semi-Permanent

2.5.2.2.1 Wash-Out Colors

2.5.2.2.2 Fashion Shades

2.5.3 Skincare Formulations

2.5.3.1 Creams & Lotions

2.5.3.1.1 Tinted Moisturizers

2.5.3.1.2 BB & CC Creams

2.5.3.2 Serums & Gels

2.5.3.2.1 Brightening Serums

2.5.3.2.2 Anti-Aging Formulations

2.6 Pharmaceuticals

2.6.1 Tablet Coatings

2.6.1.1 Film-Coated Tablets

2.6.1.1.1 Immediate Release

2.6.1.1.2 Extended Release

2.6.2 Capsules

2.6.2.1 Hard Gelatin Capsules

2.6.2.1.1 Prescription Drugs

2.6.2.1.2 Nutraceutical Capsules

2.6.2.2 Soft Gel Capsules

2.6.2.2.1 Vitamin Softgels

2.6.2.2.2 Oil-Based Formulations

2.6.3 Syrups

2.6.3.1 Pediatric Syrups

2.6.3.1.1 Flavored Antibiotics

2.6.3.1.2 Cough Syrups

2.6.3.2 Adult Liquid Medicines

2.6.3.2.1 Digestive Syrups

2.6.3.2.2 Tonics

?? ?? 3. By Form

3.1 Powder

3.1.1 Organic Pigment Powders

3.1.1.1 Azo Pigments

3.1.1.1.1 Monoazo Pigments

3.1.1.1.2 Diazo Pigments

3.1.1.2 Phthalocyanine Pigments

3.1.1.2.1 Phthalocyanine Blue

3.1.1.2.2 Phthalocyanine Green

3.1.2 Inorganic Pigment Powders

3.1.2.1 Titanium Dioxide

3.1.2.1.1 Rutile Grade

3.1.2.1.2 Anatase Grade

3.1.2.2 Iron Oxide Pigments

3.1.2.2.1 Red Iron Oxide

3.1.2.2.2 Yellow & Black Iron Oxide

3.1.3 Specialty Functional Powders

3.1.3.1 Anti-Corrosive Pigments

3.1.3.1.1 Zinc Phosphate

3.1.3.1.2 Chromate-Based Pigments

3.1.3.2 UV-Resistant Pigments

3.1.3.2.1 Weather-Stable Pigments

3.1.3.2.2 Heat-Resistant Grades

3.2 Liquid

3.2.1 Liquid Dyes

3.2.1.1 Water-Soluble Dyes

3.2.1.1.1 Textile Dyes

3.2.1.1.2 Food-Grade Dyes

3.2.1.2 Solvent-Based Dyes

3.2.1.2.1 Industrial Inks

3.2.1.2.2 Plastic Applications

3.2.2 Liquid Pigment Dispersions

3.2.2.1 Aqueous Dispersions

3.2.2.1.1 Architectural Coatings

3.2.2.1.2 Paper & Packaging

3.2.2.2 Solvent-Based Dispersions

3.2.2.2.1 Automotive Coatings

3.2.2.2.2 Industrial Applications

3.2.3 Food & Cosmetic Liquid Colorants

3.2.3.1 Natural Liquid Colors

3.2.3.1.1 Plant Extracts

3.2.3.1.2 Fruit-Based Colors

3.2.3.2 Synthetic Liquid Colors

3.2.3.2.1 Certified Food Dyes

3.2.3.2.2 Cosmetic-Grade Colors

3.3 Paste

3.3.1 Pigment Pastes for Coatings

3.3.1.1 Water-Based Pastes

3.3.1.1.1 Decorative Paints

3.3.1.1.2 Emulsion Systems

3.3.1.2 Solvent-Based Pastes

3.3.1.2.1 Industrial Paints

3.3.1.2.2 Automotive Refinish

3.3.2 Printing Ink Pastes

3.3.2.1 Offset Printing

3.3.2.1.1 Packaging Printing

3.3.2.1.2 Commercial Printing

3.3.2.2 Flexographic & Gravure Inks

3.3.2.2.1 Flexible Packaging

3.3.2.2.2 Label Printing

3.4 Granules

3.4.1 Pigment Granules

3.4.1.1 Dust-Free Pigments

3.4.1.1.1 Industrial Handling Applications

3.4.1.1.2 Bulk Manufacturing

3.4.1.2 High-Concentration Granules

3.4.1.2.1 Plastic Compounding

3.4.1.2.2 Rubber Processing

3.4.2 Dye Granules

3.4.2.1 Textile Dye Granules

3.4.2.1.1 Reactive Dyes

3.4.2.1.2 Disperse Dyes

3.4.2.2 Paper & Leather Dyes

3.4.2.2.1 Packaging Paper

3.4.2.2.2 Leather Finishing

3.5 Masterbatch (Plastic Coloring Compounds)

3.5.1 Color Masterbatch

3.5.1.1 Standard Color Masterbatch

3.5.1.1.1 Packaging Applications

3.5.1.1.2 Consumer Goods

3.5.1.2 Custom Color Masterbatch

3.5.1.2.1 Automotive Plastics

3.5.1.2.2 Electronics Casings

3.5.2 Additive Masterbatch

3.5.2.1 UV-Stabilizer Masterbatch

3.5.2.1.1 Outdoor Applications

3.5.2.1.2 Agricultural Films

3.5.2.2 Flame-Retardant Masterbatch

3.5.2.2.1 Electrical Components

3.5.2.2.2 Construction Materials

3.5.3 Specialty Masterbatch

3.5.3.1 Antimicrobial Masterbatch

3.5.3.1.1 Medical Plastics

3.5.3.1.2 Food Packaging

3.5.3.2 Biodegradable & Bio-Based Masterbatch

3.5.3.2.1 Compostable Packaging

3.5.3.2.2 Sustainable Consumer Products

?? ??4. By Region

4.1 North America

4.2 Europe

4.3 Asia-Pacific

4.4 Middle East & Africa

4.5 South America

Regional Insights of the Global Colorants Market

Asia-Pacific ??? Largest & Fastest-Growing Region

Asia-Pacific dominates the global colorants market, driven by robust textile manufacturing, expanding plastics and packaging industries, and rapid infrastructure development across China, India, and Southeast Asia. Strong industrialization, export-oriented production, and rising domestic consumption continue to accelerate regional growth.

North America

Market demand is supported by increasing adoption of specialty and high-performance pigments, growing preference for natural food-grade colorants, and strong demand from advanced coatings and automotive applications.

Europe

Europe???s market expansion is fueled by stringent environmental regulations and strong emphasis on REACH-compliant, sustainable, and eco-friendly colorant solutions. Innovation in bio-based and low-VOC pigments remains a key growth driver.

Middle East & Africa

Growth in this region is supported by expanding construction activities, infrastructure projects, and rising packaged food consumption, contributing to steady demand for industrial and food-grade colorants.

South America

Steady growth is driven by the textile manufacturing base and expanding food processing sector, particularly in Brazil and Argentina, supporting consistent demand for dyes and food colorants.

Leading Companies in the Global Colorants Market

-

Clariant AG

-

LANXESS AG

-

Sun Chemical Corporation

-

Huntsman Corporation

-

Cabot Corporation

-

Kronos Worldwide (Titanium Dioxide)

-

Sensient Technologies Corporation

-

DSM-Firmenich (Natural Food Colorants)

Among these, BASF SE and DIC Corporation are leading global players with diversified pigment and dye portfolios.

Strategic Intelligence & AI-Backed Insights

Pheonix Demand Forecast Engine indicates sustained long-term demand across key end-use sectors, particularly paints & coatings, plastics & packaging, and food-grade natural colorants, supported by global industrial expansion and consumer-driven product innovation.

Consumer Behavior Analyzer identifies a growing shift toward clean-label, sustainable, and premium-colored products, reflecting heightened environmental awareness and demand for transparency in food, cosmetics, and consumer goods.

Innovation Tracker highlights rapid advancements in nano-pigments, bio-based dyes, smart color-changing technologies, and high-durability performance coatings, positioning specialty colorants as a high-growth opportunity area.

Porter???s Five Forces Analysis suggests intense competitive rivalry and moderate raw material dependency, while indicating strong profitability potential within specialty, eco-friendly, and natural pigment segments driven by differentiation and regulatory compliance.

Why the Global Colorants Market Remains Critical

-

Essential for product differentiation and branding across industries

-

Regulatory compliance in food, pharma, and cosmetics

-

Infrastructure and construction expansion globally

-

Sustainability transition toward eco-friendly pigments

-

Growth in packaging, automotive, and consumer goods manufacturing

Final Takeaway of Global Colorants Market

The Global Colorants Market is steadily evolving from conventional bulk pigment production toward high-performance, sustainable, and specialty-driven solutions. A projected CAGR of 5.2% during 2026???2033 reflects consistent industrial growth, technological advancements, and increasing regulatory influence across major economies.

Organizations that prioritize investment in bio-based pigments, smart and functional color technologies, advanced performance coatings, and regulatory-compliant innovation strategies are likely to secure a sustainable competitive edge in the long term.

At Pheonix Research, our advanced forecasting models deliver comprehensive revenue analysis, competitive benchmarking, and strategic intelligence ??? empowering stakeholders to navigate the post-2025 transformation of the colorants industry with data-driven precision and long-term growth confidence.

???? Social Mentions & Publication Channels

??Explore deeper insights and follow our cross-platform updates on LinkedIn and X for continuous intelligence and market coverage.

LinkedIn : https://www.linkedin.com/feed/update/urn:li:activity:7433070085143052288

X :?? https://x.com/Pheonix_Insight/status/2027417711521976393?s=20

Value Chain

Global Colorants Market Value Chain & Supply Chain Evolution Overview

The Global Colorants Market value chain is evolving from traditional bulk pigment and dye manufacturing into a technologically advanced, sustainability-driven, and performance-engineered industrial ecosystem. Unlike earlier commodity-focused colorant systems primarily centered on cost and volume, the modern colorants market is increasingly shaped by regulatory compliance, bio-based innovation, functional material science, specialty chemistry, and application-specific customization across paints & coatings, plastics, food & beverages, textiles, cosmetics, and pharmaceuticals.

The colorants value chain spans raw material extraction, petrochemical and mineral feedstock sourcing, pigment and dye synthesis, specialty formulation engineering, natural colorant extraction, performance enhancement technologies, masterbatch production, industrial distribution, regulatory compliance systems, and downstream integration into diverse end-use sectors. As industries increasingly prioritize sustainability, durability, and product differentiation, the value chain is shifting from standard commodity supply toward premium, high-margin specialty solutions.

Upstream supply chain dynamics are shaped by petrochemical suppliers, mining companies, agricultural feedstock providers, specialty chemical producers, additive manufacturers, and pigment synthesis innovators. Titanium dioxide, iron oxide, carbon black, aromatic chemicals, plant-based extracts, and functional additives remain critical inputs, while volatility in oil markets, ESG pressures, mining regulations, and agricultural sourcing increasingly influence supply stability.

Manufacturing strategies increasingly prioritize eco-friendly chemistry, low-VOC systems, heavy-metal-free formulations, bio-based feedstocks, nano-pigments, smart coatings, and advanced dispersion technologies. Producers are moving beyond standard dyes and pigments toward high-performance, regulatory-compliant, and application-engineered solutions tailored to premium industrial use cases.

Distribution is increasingly globalized and sector-specific, with B2B industrial contracts, OEM partnerships, private-label production, chemical distributors, digital procurement platforms, and regulatory-certified supply chains driving commercialization. Specialty customization, formulation IP, and compliance expertise are increasingly central to competitive differentiation.

Supply chain challenges include petrochemical price volatility, environmental regulations, heavy metal restrictions, food-grade safety standards, sustainability compliance, feedstock diversification, and increasing pressure to reduce carbon intensity while maintaining product performance.

Global Colorants Market Value Chain & Supply Chain Evolution Current Scenario

The current colorants market is shaped by sustainability mandates, premium product differentiation, infrastructure expansion, clean-label food trends, advanced coatings demand, and industrial performance requirements.

Upstream, manufacturers are increasingly investing in sustainable feedstocks, natural extraction technologies, specialty additives, and advanced pigment chemistry to align with tightening environmental and regulatory standards.

Production ecosystems increasingly focus on specialty pigments, food-safe natural colorants, functional coatings, smart pigments, bio-based masterbatch, and high-performance industrial applications.

Technology infrastructure increasingly includes nano-dispersion systems, precision formulation software, AI-driven color matching, smart coating technologies, and advanced quality assurance systems.

Distribution networks are dominated by industrial B2B contracts, OEM integration, regional specialty distributors, packaging supply chains, food-grade certification channels, and multinational manufacturing partnerships.

Competitive positioning increasingly depends on formulation innovation, sustainability, compliance readiness, and downstream sector specialization rather than commodity volume alone.

Key Value Chain & Supply Chain Evolution Signals in Global Colorants Market

Several structural transformations are reshaping the global colorants ecosystem.

First, sustainable and bio-based colorants are becoming strategically critical due to tightening environmental regulations and rising clean-label consumer demand.

Second, specialty pigments including thermochromic, photochromic, metallic, pearlescent, and smart functional coatings are emerging as high-margin innovation categories.

Third, natural food-grade and cosmetic-grade colorants are rapidly expanding due to increasing health awareness, transparency demands, and regulatory scrutiny.

Fourth, nano-pigments and advanced dispersion systems are improving product durability, precision, UV stability, and industrial efficiency.

Fifth, plastic masterbatch innovation is expanding through biodegradable, antimicrobial, and high-performance sustainable polymer applications.

Sixth, regulatory compliance and ESG adaptation are becoming critical competitive differentiators, especially across Europe, North America, food, cosmetics, and pharmaceutical applications.

Strategic Implications of Value Chain & Supply Chain Evolution in Global Colorants Market

Leading companies such as BASF SE, DIC Corporation, Clariant AG, LANXESS AG, Sun Chemical, and Sensient Technologies are strengthening their market positions through sustainability investment, specialty innovation, regulatory alignment, and advanced performance chemistry.

Long-term competitive advantage increasingly depends on raw material diversification, specialty formulation capabilities, eco-compliance, and application-specific technological leadership.

Companies with strong bio-based portfolios, food-grade compliance, smart pigment technologies, and advanced coatings capabilities are better positioned to capture premium growth opportunities.

Natural colorant scalability, sustainable feedstock sourcing, and high-performance industrial customization are becoming increasingly important for strategic resilience.

Supply chain resilience increasingly depends on balancing cost efficiency, sustainability mandates, raw material security, innovation speed, and regulatory adaptability.

As competition intensifies, colorant producers must increasingly evolve from chemical suppliers into integrated specialty material science and sustainability solution providers.

Global Colorants Market Value Chain & Supply Chain Evolution Forward Outlook

Between 2026 and 2033, the colorants market value chain is expected to become more sustainability-centric, technologically advanced, bio-based, and specialty-performance oriented.

Colorant manufacturers will increasingly prioritize natural extraction systems, smart coatings, nano-engineered pigments, circular chemistry, biodegradable masterbatch, and regulatory-certified premium solutions.

Distribution ecosystems will increasingly expand through digital B2B procurement, sustainable packaging partnerships, clean-label food ecosystems, and premium industrial application channels.

Supply chain ecosystems are likely to evolve toward lower-emission manufacturing, renewable feedstocks, ESG-integrated sourcing, and circular innovation frameworks.

Advanced analytics, AI-assisted color precision, smart functionality, and environmental performance scoring are expected to redefine product differentiation models.

Ultimately, the colorants value chain will evolve from conventional industrial chemistry toward a broader sustainability-driven material innovation ecosystem supporting product differentiation, regulatory compliance, and advanced industrial performance globally.

Market-Specific Value Chain

- Raw Material Sourcing & Feedstock Supply: Petrochemical suppliers, mineral extraction, titanium dioxide, iron oxide, agricultural feedstocks, plant extracts, specialty additives

- Chemical Processing & Intermediate Manufacturing: Organic pigment synthesis, inorganic pigment processing, natural extraction, additive engineering, specialty intermediates

- Manufacturing & Productization: Pigments, dyes, natural colorants, masterbatch, smart pigments, specialty coatings, functional formulations

- Distribution & Industrial Integration: B2B contracts, OEM supply chains, food-grade channels, chemical distributors, digital procurement, industrial partnerships

- Monetization & Competitive Differentiation: Specialty customization, sustainability premiums, compliance certification, premium industrial contracts, innovation IP

- Sustainability & Future Innovation: Bio-based pigments, smart coatings, circular chemistry, low-VOC systems, biodegradable masterbatch, ESG integration

Company-to-Stage Mapping

- Raw Material Sourcing & Feedstock Supply: Kronos Worldwide, Cabot Corporation, mining suppliers, petrochemical providers, agricultural extractors

- Chemical Processing & Intermediate Manufacturing: BASF SE, DIC Corporation, Clariant AG, LANXESS AG

- Manufacturing & Productization: Sun Chemical, Huntsman Corporation, Sensient Technologies, DSM-Firmenich

- Distribution & Industrial Integration: Global chemical distributors, OEM manufacturers, food processors, coatings manufacturers, packaging companies

- Monetization & Competitive Differentiation: BASF specialty solutions, DIC advanced pigments, Sensient natural colorants, Clariant sustainable formulations

- Sustainability & Future Innovation: Bio-based pigment developers, smart coating innovators, natural food colorant leaders, circular chemistry platforms

Investment Activity

Global Colorants Market Investment & Funding Dynamics Overview

Investment and funding dynamics in the Global Colorants Market are being shaped by the accelerating transition toward sustainable formulations, specialty performance materials, regulatory-compliant innovation, and expanding end-use demand across paints & coatings, plastics, food & beverages, textiles, cosmetics, and pharmaceuticals. Between 2026 and 2033, capital deployment is expected to increasingly prioritize bio-based pigments, natural food-grade colorants, smart functional coatings, advanced pigment dispersion technologies, and regional manufacturing expansion.

As industrial sectors increasingly require high-performance, eco-friendly, and premium aesthetic solutions, the colorants market is evolving from a traditional commodity chemical segment into a strategic innovation-led materials industry. Major global players such as BASF, DIC Corporation, Clariant, LANXESS, Sun Chemical, Cabot, and DSM-Firmenich are actively investing in sustainable product development, natural ingredient pipelines, advanced pigment technologies, and compliance-focused manufacturing capabilities.

A major structural transformation influencing investment flows is the shift from synthetic, low-cost bulk colorants toward differentiated, high-margin specialty solutions including heavy-metal-free pigments, biodegradable masterbatches, functional coatings, thermochromic pigments, and clean-label food colorants. This is directing global funding toward R&D, advanced chemical engineering, sustainable sourcing, and smart coloration technologies.

Global Colorants Market Investment & Funding Dynamics Current Scenario

Current investment activity is being driven by rising industrial production, sustainability mandates, clean-label consumer preferences, infrastructure growth, and tightening environmental regulations. Manufacturers are increasingly allocating capital toward innovation, production modernization, and portfolio diversification to address both regulatory complexity and premium demand.

- Asia-Pacific: Leads global investment activity due to large-scale textile, plastics, coatings, and manufacturing ecosystems across China, India, Japan, and Southeast Asia.

- Europe: Strong funding momentum driven by REACH compliance, sustainability mandates, low-VOC innovation, and bio-based pigment commercialization.

- North America: Significant investment focused on specialty pigments, food-grade natural colorants, performance coatings, and advanced packaging applications.

- Middle East, Africa & South America: Emerging investment regions supported by infrastructure development, food processing expansion, and rising industrial manufacturing demand.

Key Investment & Funding Dynamics Signals in Global Colorants Market

- Sustainability regulations are accelerating capital inflows into bio-based, heavy-metal-free, biodegradable, and low-emission colorant technologies.

- Clean-label food and beverage trends are increasing investment in natural, plant-derived, and fermentation-based colorants.

- Construction and automotive sector growth is driving funding into high-durability pigments, UV-resistant coatings, and advanced performance color solutions.

- Plastics and packaging transformation is boosting investment in specialty masterbatch, recyclable formulations, and functional additive technologies.

- Innovation in smart pigments, nano-colorants, and responsive coatings is attracting strategic R&D investment for next-generation applications.

Strategic Implications of Investment & Funding Dynamics in Global Colorants Market

- The investment landscape increasingly favors companies with strong specialty portfolios, sustainability capabilities, and regulatory adaptability.

- Natural colorants and bio-based chemistry are emerging as major long-term capital priorities due to food, cosmetics, and consumer safety demand.

- Vertical integration into raw material sourcing, formulation science, and advanced processing technologies is becoming essential for profitability and resilience.

- Regional diversification strategies remain critical, with Asia-Pacific leading scale, Europe driving sustainable innovation, and North America focusing on premiumization.

- Competitive advantage is increasingly linked to performance differentiation, regulatory compliance, and sustainable product innovation rather than price alone.

Global Colorants Market Investment & Funding Dynamics Forward Outlook

Looking ahead, the Global Colorants Market is expected to attract sustained strategic investment as sustainability transformation, industrial expansion, and premium product innovation continue reshaping market priorities.

Future capital allocation will increasingly focus on bio-based pigments, smart coatings, natural food-grade formulations, advanced masterbatch technologies, AI-assisted formulation systems, and circular manufacturing processes.

- Asia-Pacific: Will remain the dominant investment hub due to manufacturing scale, infrastructure expansion, and strong textile/plastics production.

- Europe: Will continue leading sustainable innovation, regulatory-driven product development, and eco-friendly pigment commercialization.

- North America: Will expand investments in specialty pigments, clean-label food colorants, and high-performance industrial applications.

Technological advancements in functional pigments, digital color systems, sustainable sourcing, and circular production models will increasingly define funding priorities across the industry.

Overall, the Global Colorants Market is transitioning into a highly strategic materials innovation ecosystem through 2033. Companies that successfully lead in sustainable chemistry, specialty functionality, regulatory excellence, and high-performance product innovation will capture the greatest long-term value in this evolving global market.