Global Connected Glucose Monitoring Device Market Report, Size and Forecast 2026-2033

Global Connected Glucose Monitoring Device Market Report Size and Forecast 2026–2033

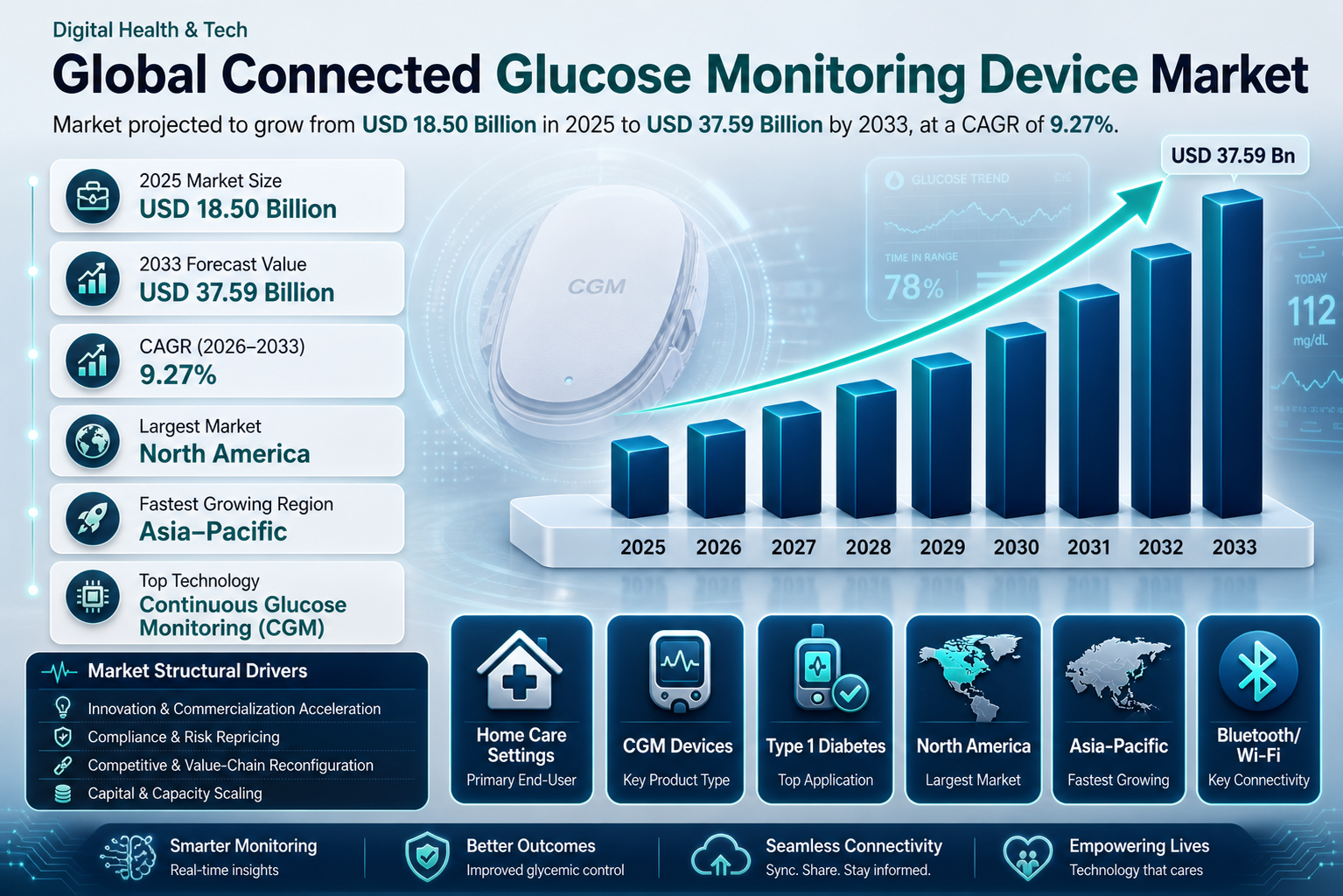

Market Forecast Snapshot (2025–2033)

| Metric | Value |

|---|---|

| Market Size (2025) | USD 18.50 Billion |

| Market Size (2033) | USD 37.59 Billion |

| CAGR (2026–2033) | ~9.27% |

| Largest Region | North America |

| Fastest Growing Region | Asia-Pacific |

| Leading Segment | Home Care Settings |

| Key Trend | Connected & AI-driven diabetes management |

Market Size & Forecast

The Global Connected Glucose Monitoring Device Market is projected to grow from USD 18.50 billion in 2025 to USD 37.59 billion by 2033, registering a CAGR of 9.27% during the forecast period. This strong growth is driven by the increasing global prevalence of diabetes, rising adoption of continuous glucose monitoring (CGM) systems, and rapid integration of digital health technologies. The expansion of connected healthcare ecosystems, including mobile health apps and telehealth platforms, is further accelerating adoption.Market Overview

The Connected Glucose Monitoring Device Market represents a convergence of healthcare, digital technology, and consumer electronics, enabling real-time glucose tracking and data-driven diabetes management. The market is highly competitive and moderately fragmented, with leading players such as Dexcom, Abbott Laboratories, Medtronic, and Roche driving innovation. A major transformation in the market is the shift toward connected and integrated monitoring systems, enabling seamless data sharing between patients, healthcare providers, and caregivers.Key Drivers of Market Growth

- Rising Diabetes Prevalence

- Increasing Adoption of Continuous Glucose Monitoring (CGM) Systems

- Integration with Digital Health Eglobal cosystems

- Advancements in Sensor Accuracy and Connectivity

- Expansion of Reimbursement Policies and Regulatory Support

Market Segmentation

By End User

- Home Care Settings (Largest Segment)

- Hospitals & Clinics

- Telehealth & Remote Monitoring

By Application

- Type 1 Diabetes Management

- Type 2 Diabetes Management (Largest Segment)

- Gestational Diabetes Monitoring

By Product Type

- Connected Blood Glucose Meters

- Connected Continuous Glucose Monitoring Devices (Fastest Growing)

By Distribution Channel

- Online Pharmacies (Fastest Growing)

- Retail Pharmacies

By Connectivity Technology

- Bluetooth (Dominant)

- Wi-Fi

- NFC

Regional Insights

- North America – Largest Market driven by advanced healthcare infrastructure and strong reimbursement systems

- Europe – Growth supported by public healthcare systems and regulatory frameworks

- Asia-Pacific – Fastest growing region due to rising diabetes prevalence and healthcare investments

- Latin America – Moderate growth with improving healthcare access

- Middle East & Africa – Emerging market with increasing healthcare development

Competitive Landscape

Companies are focusing on AI integration, real-time analytics, and closed-loop insulin delivery systems.Strategic Insights & Trends

- Growing adoption of hybrid closed-loop insulin delivery systems

- Increasing integration of AI and predictive analytics

- Expansion of telehealth and remote patient monitoring

- Rising demand for implantable and long-term CGM sensors

- Shift toward personalized diabetes management solutions

Why This Market Matters

- Enables real-time diabetes monitoring and proactive care

- Reduces complications through continuous tracking

- Supports remote healthcare and telemedicine expansion

- Improves patient engagement and adherence

- Drives transition toward personalized healthcare

Final Market Perspective

The Global Connected Glucose Monitoring Device Market is undergoing rapid transformation, driven by digital health integration, technological advancements, and rising diabetes prevalence. The shift toward connected, real-time monitoring systems is redefining diabetes care. Companies that invest in innovation, connectivity, and patient-centric solutions—while expanding into emerging markets—will be best positioned to capitalize on this growth opportunity through 2033.Table of Contents

Table of Contents

- 1. Executive Summary

- 1.1 Market Forecast Snapshot (2026-2033)

- 1.2 Global Market Size & CAGR Analysis

- 1.3 Largest & Fastest-Growing Segments

- 1.4 Region-Level Leadership & Growth Trends

- 1.5 Key Market Drivers

- 1.6 Competitive Landscape Overview

- 1.7 Strategic Outlook Through 2033

- 2. Introduction & Market Overview

- 2.1 Definition of the Connected Glucose Monitoring Device Market

- 2.2 Scope of the Study

- 2.3 Industry Evolution & Market Development

- 2.4 Supply Chain & Distribution Infrastructure

- 2.5 Impact of Consumer Trends

- 2.6 Sustainability & Regulatory Landscape

- 2.7 Technology & Innovation Landscape

- 3. Research Methodology

- 3.1 Primary Research

- 3.2 Secondary Research

- 3.3 Market Size Estimation Model

- 3.4 Forecast Assumptions (2026-2033)

- 3.5 Data Validation & Triangulation

- 4. Market Dynamics

- 4.1 Drivers

- 4.1.1 Increasing Demand Drivers

- 4.1.2 Industry Innovation Drivers

- 4.1.3 Market Expansion Factors

- 4.1.4 Regulatory or Policy Support

- 4.1.5 Technology Adoption Drivers

- 4.2 Restraints

- 4.2.1 Cost Constraints

- 4.2.2 Infrastructure Limitations

- 4.2.3 Regulatory Challenges

- 4.2.4 Market Awareness Barriers

- 4.3 Opportunities

- 4.3.1 Emerging Market Opportunities

- 4.3.2 Product Innovation Opportunities

- 4.3.3 Technology Expansion Opportunities

- 4.3.4 Supply Chain Improvements

- 4.4 Challenges

- 4.4.1 Supply Chain Complexity

- 4.4.2 Quality Control & Compliance

- 4.4.3 Regional Market Fragmentation

- 4.4.4 Competitive Pressure

- 4.1 Drivers

- 5. Connected Glucose Monitoring Device Market Analysis (USD Billion), 2026-2033

- 5.1 Market Size Overview

- 5.2 CAGR Analysis

- 5.3 Regional Revenue Distribution

- 5.4 Segment Revenue Analysis

- 5.5 Distribution Channel Analysis

- 5.6 Consumer Impact Analysis

- 6. Market Segmentation (USD Billion), 2026-2033

- 6.1 By End User

- 6.1.1 Home Care Settings

- 6.1.1.1 Personal Diabetes Monitoring

- 6.1.1.1.1 Self Monitoring Glucose Devices

- 6.1.1.1.1.1 Home Based Diabetes Monitoring Systems

- 6.1.1.1.1.2 Connected Personal Health Devices

- 6.1.1.1.1 Self Monitoring Glucose Devices

- 6.1.1.1 Personal Diabetes Monitoring

- 6.1.2 Hospitals and Clinics

- 6.1.2.1 Clinical Diabetes Monitoring

- 6.1.2.1.1 Hospital Diabetes Monitoring Programs

- 6.1.2.1.1.1 Inpatient Glucose Monitoring Systems

- 6.1.2.1.1.2 Clinical Blood Glucose Monitoring Devices

- 6.1.2.1.1 Hospital Diabetes Monitoring Programs

- 6.1.2.1 Clinical Diabetes Monitoring

- 6.1.3 Telehealth and Remote Patient Monitoring

- 6.1.3.1 Remote Diabetes Monitoring

- 6.1.3.1.1 Connected Healthcare Monitoring Systems

- 6.1.3.1.1.1 Telemedicine Diabetes Monitoring Devices

- 6.1.3.1.1.2 Cloud Based Glucose Monitoring Platforms

- 6.1.3.1.1 Connected Healthcare Monitoring Systems

- 6.1.3.1 Remote Diabetes Monitoring

- 6.1.1 Home Care Settings

- 6.2 By Application

- 6.2.1 Gestational Diabetes Monitoring

- 6.2.1.1 Pregnancy Diabetes Monitoring

- 6.2.1.1.1 Prenatal Blood Glucose Monitoring Devices

- 6.2.1.1.1.1 Maternal Diabetes Monitoring Systems

- 6.2.1.1.1.2 Pregnancy Blood Sugar Monitoring Devices

- 6.2.1.1.1 Prenatal Blood Glucose Monitoring Devices

- 6.2.1.1 Pregnancy Diabetes Monitoring

- 6.2.2 Type 1 Diabetes Management

- 6.2.2.1 Intensive Glucose Monitoring

- 6.2.2.1.1 Continuous Glucose Monitoring Systems

- 6.2.2.1.1.1 Insulin Dependent Diabetes Monitoring

- 6.2.2.1.1.2 Automated Diabetes Management Systems

- 6.2.2.1.1 Continuous Glucose Monitoring Systems

- 6.2.2.1 Intensive Glucose Monitoring

- 6.2.3 Type 2 Diabetes Management

- 6.2.3.1 Routine Blood Glucose Monitoring

- 6.2.3.1.1 Lifestyle Diabetes Monitoring Devices

- 6.2.3.1.1.1 Daily Blood Sugar Monitoring Systems

- 6.2.3.1.1.2 Long-Term Diabetes Management Platforms

- 6.2.3.1.1 Lifestyle Diabetes Monitoring Devices

- 6.2.3.1 Routine Blood Glucose Monitoring

- 6.2.1 Gestational Diabetes Monitoring

- 6.3 By Product Type

- 6.3.1 Connected Blood Glucose Meters (BGM)

- 6.3.1.1 Bluetooth Enabled Glucose Meters

- 6.3.1.1.1 Wireless Data Transmission Glucose Meters

- 6.3.1.1.1.1 Smartphone Connected Glucose Monitoring Devices

- 6.3.1.1.1.2 Mobile Application Integrated Glucose Meters

- 6.3.1.1.1 Wireless Data Transmission Glucose Meters

- 6.3.1.2 NFC Enabled Glucose Monitoring Devices

- 6.3.1.2.1 Contactless Data Transfer Devices

- 6.3.1.2.1.1 NFC Smartphone Connected Glucose Monitoring Devices

- 6.3.1.2.1.2 Contactless Diabetes Monitoring Devices

- 6.3.1.2.1 Contactless Data Transfer Devices

- 6.3.1.3 USB Enabled Glucose Meters

- 6.3.1.3.1 Data Sync Glucose Monitoring Devices

- 6.3.1.3.1.1 Computer Integrated Glucose Monitoring Devices

- 6.3.1.3.1.2 USB Data Transfer Glucose Meters

- 6.3.1.3.1 Data Sync Glucose Monitoring Devices

- 6.3.1.1 Bluetooth Enabled Glucose Meters

- 6.3.2 Connected Continuous Glucose Monitoring (CGM) Devices

- 6.3.2.1 Flash Glucose Monitoring Systems

- 6.3.2.1.1 Sensor Scan Glucose Monitoring Devices

- 6.3.2.1.1.1 Flash Glucose Monitoring Sensors

- 6.3.2.1.1.2 Smartphone Scannable Glucose Sensors

- 6.3.2.1.1 Sensor Scan Glucose Monitoring Devices

- 6.3.2.2 Real-Time Continuous Glucose Monitoring Systems

- 6.3.2.2.1 Real-Time Sensor Based Monitoring Devices

- 6.3.2.2.1.1 Wearable CGM Sensors

- 6.3.2.2.1.2 Real-Time Blood Glucose Monitoring Systems

- 6.3.2.2.1 Real-Time Sensor Based Monitoring Devices

- 6.3.2.1 Flash Glucose Monitoring Systems

- 6.3.1 Connected Blood Glucose Meters (BGM)

- 6.4 By Distribution Channel

- 6.4.1 Online Pharmacies

- 6.4.1.1 Digital Healthcare Platforms

- 6.4.1.1.1 Direct to Consumer Diabetes Devices

- 6.4.1.1.1.1 Online Diabetes Monitoring Device Sales

- 6.4.1.1.1.2 E-Commerce Diabetes Care Distribution

- 6.4.1.1.1 Direct to Consumer Diabetes Devices

- 6.4.1.1 Digital Healthcare Platforms

- 6.4.2 Retail Pharmacies

- 6.4.2.1 Consumer Diabetes Monitoring Devices

- 6.4.2.1.1 Over the Counter Connected Glucose Devices

- 6.4.2.1.1.1 Pharmacy Distributed Diabetes Monitoring Devices

- 6.4.2.1.1.2 Retail Diabetes Care Products

- 6.4.2.1.1 Over the Counter Connected Glucose Devices

- 6.4.2.1 Consumer Diabetes Monitoring Devices

- 6.4.1 Online Pharmacies

- 6.5 By Connectivity Technology

- 6.5.1 Bluetooth Connectivity

- 6.5.1.1 Bluetooth Low Energy (BLE) Devices

- 6.5.1.1.1 Smartphone Integrated Monitoring Devices

- 6.5.1.1.1.1 Mobile App Enabled Glucose Monitoring Devices

- 6.5.1.1.1.2 Remote Data Transmission Glucose Monitoring Systems

- 6.5.1.1.1 Smartphone Integrated Monitoring Devices

- 6.5.1.1 Bluetooth Low Energy (BLE) Devices

- 6.5.2 Near Field Communication (NFC)

- 6.5.2.1 Contactless Data Communication Devices

- 6.5.2.1.1 Sensor Based Contactless Monitoring

- 6.5.2.1.1.1 Smartphone Scan Glucose Monitoring Systems

- 6.5.2.1.1.2 NFC Enabled Glucose Monitoring Sensors

- 6.5.2.1.1 Sensor Based Contactless Monitoring

- 6.5.2.1 Contactless Data Communication Devices

- 6.5.3 Wi-Fi Connectivity

- 6.5.3.1 Cloud Connected Monitoring Devices

- 6.5.3.1.1 Real-Time Data Upload Monitoring Devices

- 6.5.3.1.1.1 Remote Patient Monitoring Platforms

- 6.5.3.1.1.2 Hospital Integrated Diabetes Monitoring Systems

- 6.5.3.1.1 Real-Time Data Upload Monitoring Devices

- 6.5.3.1 Cloud Connected Monitoring Devices

- 6.5.1 Bluetooth Connectivity

- 6.1 By End User

- 7. Market Segmentation by Geography

- 7.1 North America

- 7.2 Europe

- 7.3 Asia-Pacific

- 7.4 Latin America

- 7.5 Middle East & Africa

- 8. Competitive Landscape

- 8.1 Market Share Analysis

- 8.2 Product Portfolio Benchmarking

- 8.3 Product Positioning Mapping

- 8.4 Supply Chain & Distribution Partnerships

- 8.5 Competitive Intensity & Differentiation

- 9. Company Profiles

- 10. Strategic Intelligence & Pheonix AI Insights

- 10.1 Pheonix Demand Forecast Engine

- 10.2 Supply Chain & Infrastructure Analyzer

- 10.3 Technology & Innovation Tracker

- 10.4 Product Development Insights

- 10.5 Automated Porter’s Five Forces Analysis

- 11. Future Outlook & Strategic Recommendations

- 11.1 Emerging Market Expansion

- 11.2 Technology Innovation Strategies

- 11.3 Product Development Roadmap

- 11.4 Regional Expansion Strategies

- 11.5 Long-Term Market Outlook (2033+)

- 12. Appendix

- 13. About Pheonix Research

- 14. Disclaimer

Competitive Landscape

Competitive Landscape of the Global connected glucose monitoring devices

Executive Framing

In the rapidly evolving market of connected glucose monitoring devices, understanding the dimension of competitive intensity and market structure is pivotal. As the prevalence of diabetes continues to rise globally, the demand for innovative solutions in glucose monitoring becomes increasingly critical. This dimension is essential now more than ever because it not only shapes the strategic actions of existing players but also dictates the entry barriers for new competitors. The competitive landscape is characterized by high intensity, driven by a fragmented market structure where no single player holds absolute dominance. The market’s fragmentation is underscored by the presence of five Tier 1 players, including Dexcom, Medtronic, FreeStyle, Abbott, and Roche, which are continuously vying for supremacy through innovation, strategic partnerships, and regulatory advancements.

This environment fosters a dynamic interplay of competitive moves such as FDA approvals for new devices, integration with mobile technologies, and the introduction of hybrid closed-loop systems. These developments not only heighten competitive intensity but also influence the strategic positioning of companies as they strive to differentiate their offerings and capture greater market share. Therefore, understanding this dimension is crucial for stakeholders to navigate the competitive landscape effectively and make informed strategic decisions.

Current Market Reality

The current market reality for connected glucose monitoring devices is marked by a high level of competitive intensity within a fragmented market structure. Tier 1 players, including Dexcom, Medtronic, FreeStyle, Abbott, and Roche, dominate the landscape, each leveraging their strengths to maintain and expand their market presence. These companies are at the forefront of technological innovation, regulatory approvals, and strategic partnerships, all of which are critical in shaping the competitive dynamics of the market.

Dexcom, for instance, has been a leader in integrating continuous glucose monitoring (CGM) with mobile technology, allowing users to seamlessly track their glucose levels via smartphones. Similarly, Abbott’s FreeStyle Libre has revolutionized glucose monitoring by offering a user-friendly, sensor-based system that eliminates the need for fingersticks. These innovations enhance patient convenience and drive increased adoption of CGM devices, serving as primary signals of competitive intensity.

The market is also witnessing a surge in FDA approvals for stand-alone CGM devices, validating technological advancements and paving the way for increased competition. Medtronic and Senseonics, for example, have secured FDA approvals for their latest CGM technologies, underscoring their commitment to innovation and regulatory compliance.

Further intensifying competition is the introduction of hybrid closed-loop systems, which integrate CGM with insulin delivery for comprehensive diabetes management. This development has driven adoption and pushed market players to innovate in offering sophisticated, user-friendly solutions.

Key Signals and Evidence

Several key signals highlight the drivers of competitive intensity and market structure in the connected glucose monitoring device market. Increased investment in diabetes technology fuels innovation and accelerates development of advanced CGM devices. Leading companies such as Dexcom, Medtronic, and Abbott continuously enhance their offerings to meet demand for personalized diabetes management solutions.

Another major signal is the adoption of hybrid closed-loop systems, combining CGM devices with insulin pumps to provide automated diabetes management. Companies like Tandem and Insulet have introduced innovative systems that improve glucose control and convenience. Clinical studies demonstrating improvements in A1C levels further drive patient adoption and interest.

Strategic partnerships also shape the competitive landscape. Collaborations with technology firms enhance connectivity and functionality, enabling CGM devices to integrate with mobile health applications. Roche and Abbott exemplify this trend, differentiating products and expanding market reach through such alliances.

FDA approvals for new devices, including stand-alone CGM systems, signal a supportive regulatory environment that encourages innovation and competition. This is particularly relevant for companies like Senseonics seeking market expansion. Additionally, patient-driven innovations such as open-source artificial pancreas systems challenge traditional players to adapt rapidly.

The growing integration of mobile health applications further influences competition. Patients increasingly demand devices compatible with digital lifestyles, prompting companies like Dexcom and Abbott to enhance device connectivity and functionality.

Strategic Implications

The strategic landscape for connected glucose monitoring devices is evolving with several key implications. First, hybrid closed-loop system adoption reshapes competitive dynamics, favoring companies like Medtronic and Tandem. These systems improve glycemic control and user convenience, creating a competitive edge. Companies lacking this technology may struggle to maintain market position.

Second, the surge in FDA approvals and product launches signals a race to innovate and expand portfolios. Regulatory successes offer market advantages, but continuous innovation is critical. Delays in approvals may result in lost opportunities and reduced credibility.

Third, partnerships for technology integration are increasingly strategic. Collaborations with tech firms facilitate seamless mobile integration, improving user experience and differentiating products. These alliances expand market reach and generate cross-industry synergies.

Increased investment in diabetes technology also drives innovation and competitive pricing. Companies like FreeStyle and Senseonics can introduce cost-effective solutions, expanding adoption and market size. Balancing affordability with innovation is crucial for profitability.

Finally, patient demand for personalized diabetes management is rising. Products offering tailored alerts and data insights enhance loyalty and outcomes. Companies that deliver personalized solutions gain a competitive advantage.

Forward Outlook

Looking ahead, competitive intensity in the connected glucose monitoring device market will remain high. Market fragmentation and technological advancements will continue to drive strategic actions among key players. Hybrid closed-loop adoption and FDA approvals will catalyze further innovation.

Companies must remain agile, embracing technology integration and strategic partnerships to maintain advantage. Differentiation through personalized, cost-effective solutions will become vital for growth. Market saturation may increase competition, prompting consolidation strategies for existing players.

Overall, the connected glucose monitoring device market presents a dynamic competitive landscape. Stakeholders must leverage technological innovations, regulatory support, and patient-centric solutions to navigate effectively. Companies adapting to evolving preferences and technological shifts will be best positioned to thrive in this rapidly expanding market.

Value Chain

Value Chain and Supply Chain Dynamics in the Global Usb Glucose Monitoring Device Market

Executive Framing

In the rapidly evolving landscape of healthcare technology, the connected glucose monitoring (CGM) device market is becoming a pivotal focus for stakeholders aiming to harness data-driven insights for diabetes management. While the market is poised to grow significantly from 2026 to 2033, driven by advancements in digital health platforms and increased investment in diabetes technology, the value chain faces unique challenges that will shape its evolution. Understanding the value chain through the lenses of bottlenecks, power distribution, and margin effects is crucial. This dimension matters now because it determines how effectively industry players can capitalize on technological advancements while navigating the operational complexities and constraints that define the CGM landscape.

The primary operational model for CGM devices is platform-based, emphasizing the integration of hardware and software to deliver real-time glucose monitoring and analytics. This model inherently involves complex interactions between device manufacturers, software developers, and data analytics platforms. Moreover, the hybrid distribution structure—which combines direct-to-consumer sales with partnerships with healthcare providers—further complicates the supply chain. The complexity level is moderate, yet it is precisely this intricate web of relationships and dependencies that can lead to bottlenecks if not managed adeptly.

Current Market Reality

As of now, the CGM device market is grappling with several critical bottlenecks that affect the efficiency and effectiveness of the value chain. Key among these are data security, affordability, and awareness of CGM devices. Data security is a paramount concern as CGM devices collect sensitive health data, which necessitates robust cybersecurity measures to protect patient information and maintain trust. The increasing frequency of cyber-attacks and data breaches in the healthcare sector underscores the urgency of addressing this bottleneck. Companies like Dexcom and Abbott Laboratories, which are at the forefront of CGM technology, are investing in advanced encryption and secure cloud-based platforms to safeguard user data, yet the challenge remains formidable.

Affordability is another significant barrier, particularly in markets where healthcare costs are already a burden on patients and healthcare systems. The cost of CGM devices and the associated subscription fees for cloud-based data services can be prohibitive for some users, limiting the adoption of this technology. Companies are exploring various strategies to mitigate this issue, such as offering tiered pricing models or partnering with insurance providers to subsidize costs. Despite these efforts, affordability remains a key factor influencing market penetration and demand elasticity.

Awareness of CGM devices, while improving, is still not at the desired level. Many potential users are either unaware of the benefits of continuous glucose monitoring or are hesitant to adopt new technology due to a lack of understanding. This is particularly true in regions with lower healthcare literacy. To address this, companies are investing in educational campaigns and leveraging healthcare professionals to advocate for the use of CGM devices. The role of awareness is not merely about informing potential users; it also involves dispelling myths and misconceptions that may hinder adoption.

Key Signals And Evidence

The signals around data security, affordability, and awareness of CGM devices are integral to understanding the market dynamics at play. Each of these signals represents a structural driver with distinct implications for the value chain.

Firstly, the heightened focus on data security is a direct response to the increasing volume of health data being generated and transmitted through CGM devices. This growing data landscape offers an opportunity for enhanced diabetes management through data analytics and personalized care plans. However, the trade-off is the heightened risk of data breaches, which can have severe ramifications, not just for individual users, but also for the credibility and trustworthiness of the entire CGM industry. Companies are therefore compelled to prioritize cybersecurity, which in turn influences their cost structures and operational strategies. This necessitates increased investment in IT infrastructure and the ongoing development of secure data handling protocols.

Secondly, the affordability of CGM devices remains a critical challenge that influences market accessibility and customer base expansion. The cost factor acts as a gatekeeper, determining who can access these advanced monitoring solutions. This has implications for competitive dynamics, as companies that can effectively reduce costs or offer more affordable alternatives stand to gain significant market share. For instance, initiatives funded by the European Commission’s Horizon 2020 Research and Innovation Program aim to foster innovations that could lower production costs and enhance device affordability. This, combined with potential regulatory approvals for monitoring additional health parameters beyond glucose, could expand the market’s reach and utility.

Lastly, the importance of increasing awareness cannot be overstated. Awareness campaigns are not just about marketing; they are strategic initiatives aimed at creating informed consumers who can advocate for themselves within healthcare systems. By enhancing awareness, companies can drive demand and improve patient outcomes. This requires a concerted effort from device manufacturers, healthcare providers, and regulatory bodies to ensure that the messaging is consistent, accurate, and impactful.

In conclusion, the current market reality for CGM devices is shaped by the interplay of data security, affordability, and awareness. These factors not only present challenges but also offer opportunities for those willing to innovate and adapt. Companies that can effectively address these bottlenecks will be better positioned to leverage the full potential of the CGM market, ultimately leading to improved margins, a stronger bargaining position, and more efficient capacity utilization. The strategic actions taken today will have lasting implications for the value chain as the market continues to evolve over the forecast period.

Strategic Implications

The interplay of these signals presents several strategic implications for stakeholders within the CGM value chain. First and foremost, companies must recognize the importance of addressing the identified bottlenecks to maintain and enhance their competitive position. Those that can surmount the challenges of data security, affordability, and awareness will likely experience improved margins and greater market share.

Data security, for example, should not be seen merely as a compliance requirement but as a strategic asset. Companies that invest in cutting-edge security technologies and transparent data handling practices will cultivate trust with their users. This trust translates into customer loyalty, which can lead to sustained revenue streams and a stronger bargaining position with partners and suppliers.

Affordability challenges necessitate a strategic reevaluation of cost structures and pricing models. Manufacturers should explore partnerships with governments and NGOs to subsidize costs and improve device accessibility. Additionally, leveraging technology to streamline production processes can reduce costs and improve margins. Companies that can effectively balance cost reduction with quality maintenance will likely dominate the market.

Awareness campaigns should be strategically targeted to reach underserved populations and regions with low CGM adoption rates. Collaborations with healthcare providers and patient advocacy groups can amplify messaging and improve the outreach. By increasing awareness, companies can drive demand, which in turn can lead to economies of scale and reduced production costs.

Forward Outlook

Looking ahead, the CGM market is poised for significant transformation as stakeholders navigate the complexities of the value chain. The period from 2026 to 2033 will likely see increased consolidation within the industry, as companies seek to optimize their operations and enhance their competitive advantage. Strategic mergers and acquisitions could become more prevalent as firms aim to expand their capabilities and market reach.

The regulatory landscape will also continue to evolve, with possible new guidelines focusing on data security and device interoperability. Companies that proactively engage with regulatory bodies and align their strategies with anticipated changes will find themselves better positioned to capitalize on emerging opportunities.

Technological advancements, particularly in AI and machine learning, will play a critical role in shaping the future of CGM devices. These technologies can enhance device functionality, improve user experience, and provide more accurate data insights—factors that are crucial for maintaining a competitive edge.

In conclusion, the CGM market’s value chain is at a pivotal juncture, where strategic decisions made today will dictate the trajectory of growth and innovation in the coming years. By addressing the key bottlenecks of data security, affordability, and awareness, stakeholders can unlock significant value and drive the market forward. The strategic implications outlined here offer a roadmap for navigating the complexities of this evolving landscape, ensuring that companies can leverage these insights to achieve sustained success.

Investment Activity

Investment Activity of the Global Usb Glucose Monitoring Device Market

Executive Framing

In the evolving landscape of healthcare technology, the investment and funding dynamics surrounding connected glucose monitoring devices represent a critical dimension that is shaping market structures and influencing strategic decision-making. As the global burden of diabetes continues to escalate, the demand for innovative monitoring solutions is driving substantial capital flows into this sector. This dimension is pivotal now due to a convergence of factors, including advancing digital health technologies, the integration of artificial intelligence, and significant shifts in payer criteria and insurance coverage.

Investors and stakeholders are increasingly focusing on the burgeoning market for connected glucose monitoring devices, given the high capital intensity and rising investment trend direction. The absence of recent mergers and acquisitions activity underscores a strategic preference for organic growth and technological advancement rather than consolidation. The sector’s attractiveness is further enhanced by investment themes such as digital health technology, continuous glucose monitoring (CGM), remote monitoring, patient engagement, and telehealth. These themes are not just buzzwords but are driving investment logic and capital allocation strategies.

Current Market Reality

The present state of the connected glucose monitoring device market is characterized by a blend of high capital intensity and strategic investment focus, reflecting the sector’s potential for significant growth and innovation. Despite the lack of recent mergers and acquisitions activity, investment in this space is on an upward trajectory, driven by the increasing integration of digital health technologies and artificial intelligence in healthcare solutions. These technologies are enabling more precise, personalized, and efficient patient care, which is attracting substantial investment from both private and institutional investors.

The growing demand for CGMs is a primary catalyst in this market. With the prevalence of diabetes steadily increasing, more patients and healthcare providers are turning to CGMs for real-time glucose monitoring. This demand is further amplified by the expansion of payer criteria and increased insurance coverage, making CGMs more accessible to a broader patient population. These developments are indicative of a market that is not only expanding but also becoming more inclusive in terms of patient access and affordability.

Companies such as Dexcom and Abbott Laboratories are at the forefront of this market evolution. Dexcom, for instance, has been making significant strides in enhancing its CGM technology, focusing on user-friendly interfaces and integration with other digital health platforms. Abbott, on the other hand, has been working on advancing its FreeStyle Libre system, which has gained considerable traction due to its affordability and ease of use. These companies are channeling investments into research and development to maintain a competitive edge, reflecting a strategic emphasis on innovation and technological advancement.

Moreover, the European Commission’s Horizon 2020 Research and Innovation Program is providing substantial funding to support advancements in diabetes technology, further reinforcing the sector’s growth potential. This funding is not only facilitating innovation but also encouraging collaboration between various stakeholders, including tech companies, healthcare providers, and regulatory bodies.

Key Signals and Evidence

The investment landscape for connected glucose monitoring devices is characterized by several key signals that are shaping market dynamics and influencing strategic decisions. Among these, the expansion of payer criteria stands out as a significant driver of market growth. As payers broaden their criteria to cover a wider range of CGM devices, more patients can access these technologies, thereby increasing market penetration and driving demand.

Increased insurance coverage is another critical signal that is reshaping the investment terrain. As insurers recognize the long-term cost benefits of CGMs in managing diabetes and preventing complications, they are more willing to cover these devices, thus reducing the financial burden on patients and encouraging adoption. This shift is creating a more favorable environment for investors, who are keen to capitalize on the expanding market opportunities.

The integration of digital health technology and artificial intelligence into CGMs is also driving investment interest. These technologies are enhancing the functionality and efficacy of CGMs, making them more appealing to both patients and healthcare providers. Investors are particularly attracted to companies that are leveraging these technologies to develop next-generation CGMs with advanced features such as predictive analytics and seamless integration with other health monitoring systems.

Patient engagement is another investment theme gaining traction in this market. As healthcare becomes more patient-centric, there is a growing emphasis on empowering patients to take control of their health through user-friendly and accessible technologies. Companies that prioritize patient engagement by developing intuitive and interactive CGMs are likely to attract more investment, as they align with the broader trend of personalized healthcare.

The growing demand for CGMs, coupled with these investment themes, is creating a dynamic and competitive market environment. Investors are increasingly looking for opportunities in companies that are not only innovating but also demonstrating a clear understanding of market needs and regulatory requirements. This strategic focus is crucial in a market where regulatory approval, such as the FDA’s 510(k) clearance for CGM devices, plays a significant role in determining market entry and competitive positioning.

Strategic Implications

The confluence of these signals presents significant strategic implications for stakeholders in the connected glucose monitoring device market. For investors, the expansion of payer criteria and increased insurance coverage reduce investment risk by ensuring a more predictable and wider revenue stream. This makes the market more attractive to venture capitalists and institutional investors looking for stable, long-term returns. Companies that can navigate these payer dynamics effectively are likely to secure a competitive advantage and attract significant capital inflows.

Healthcare providers and device manufacturers must also adapt to these evolving dynamics. The growing demand for CGMs necessitates increased production capacity and supply chain resilience. Companies that can scale efficiently while maintaining quality will be better positioned to capture market share. Moreover, manufacturers should focus on incorporating AI and digital health technologies into their devices, as these features are increasingly demanded by both patients and healthcare providers.

For insurers, the shift towards more inclusive coverage of CGMs presents an opportunity to align with value-based care models. By covering CGMs, insurers can potentially lower overall healthcare costs by preventing diabetes-related complications. This alignment with long-term healthcare savings is likely to drive further expansion of payer criteria, creating a positive feedback loop that benefits all stakeholders.

Forward Outlook

Looking ahead, the connected glucose monitoring device market is poised for substantial growth, driven by the interplay of technological advancements, evolving payer landscapes, and increasing patient demand. By 2030, it is anticipated that the market will continue to expand, with more than 45 million patients potentially utilizing CGMs. This growth will be supported by ongoing improvements in device accuracy, affordability, and user experience.

The integration of AI and digital health technologies will likely become standard features in CGMs, further enhancing their value proposition. As these devices become more sophisticated, they will play a central role in personalized medicine, offering tailored insights that empower patients and healthcare providers alike.

However, this promising outlook is not without challenges. Regulatory hurdles and the need for robust data security measures will require continuous attention from manufacturers and investors. Companies that can demonstrate compliance with evolving regulations and prioritize patient data protection will be better positioned to capitalize on market opportunities.

In conclusion, the investment and funding dynamics of the connected glucose monitoring device market are characterized by a high level of capital intensity, driven by a convergence of key signals that are reshaping the healthcare landscape. As stakeholders navigate this complex environment, the ability to innovate and adapt will be critical to capturing value in this burgeoning market. The strategic allocation of capital towards technologies and business models that align with these signals will determine the future leaders in the field of connected glucose monitoring. As the market continues to evolve, stakeholders must remain vigilant, agile, and forward-thinking to thrive amidst these transformative changes.

Technology & Innovation

Technology and Innovation Landscape in the Global Usb Glucose Monitoring Device Market

Executive Framing

The connected glucose monitoring device market is experiencing a transformative phase, driven by technological innovations that promise to redefine diabetes management. This dimension of technology and innovation is critical because it directly influences how these devices integrate into daily healthcare routines, their adoption rates, and ultimately, their effectiveness in managing diabetes. The innovation intensity level in this market is high, indicating rapid advancements and a dynamic landscape where new technologies are frequently introduced. The moderate patent activity level suggests a steady stream of new inventions, yet the field is not overly saturated, allowing room for new entrants and ideas. The technology maturity stage being in growth signals that while some technologies are well-established, there is still significant potential for further advancements and wider market penetration.

Key technologies such as continuous glucose monitors (CGMs), insulin pumps, smartphone applications, and real-time glucose monitoring are paving the way for a more integrated and efficient approach to diabetes care. These innovations have the potential to enhance procedure economics by reducing the costs associated with diabetes management, improving patient outcomes by providing more accurate and timely data, and increasing throughput by allowing healthcare providers to manage more patients effectively. The integration of these technologies is also altering adoption patterns, as they become more accessible and user-friendly, encouraging more patients to make the switch from traditional glucose monitoring methods to connected devices.

Current Market Reality

The current reality of the connected glucose monitoring device market is characterized by significant advancements in technology and a shift towards more integrated solutions. The increased adoption of continuous glucose monitors is a clear signal of this shift. CGMs provide real-time glucose monitoring, which is crucial for patients who require constant vigilance over their glucose levels. This real-time data allows for more precise insulin delivery, reducing the risk of both hyperglycemia and hypoglycemia, thereby improving patient outcomes.

Entities such as Dexcom, Abbott, and Medtronic are at the forefront of this technological wave. Dexcom’s continuous glucose monitors are widely recognized for their accuracy and integration capabilities with other devices, such as insulin pumps. Abbott has made significant strides with its FreeStyle Libre systems, which offer a user-friendly interface and reliable data transmission to smartphones. Medtronic, on the other hand, is leading the charge in integrating CGMs with insulin delivery devices, creating a seamless experience for users.

The integration of insulin delivery systems with glucose monitoring devices is a critical development in this market. This integration not only improves the efficiency of diabetes management but also enhances the user experience by reducing the number of devices a patient must manage. Companies like Tandem Diabetes Care are making notable advancements in this area, offering hybrid closed-loop systems that adjust insulin delivery based on CGM data, effectively creating an artificial pancreas.

Another significant development is the regulatory approval for monitoring other electrolytes. This expands the functionality of glucose monitoring devices, potentially broadening their application beyond diabetes management. Such approvals indicate a willingness from regulatory bodies to embrace innovation and adapt standards to accommodate new technological capabilities.

Smartphone applications are also playing a pivotal role in the evolution of connected glucose monitoring devices. These apps not only provide real-time data visualization but also offer insights and recommendations based on the data collected. This empowers patients to make informed decisions about their health and facilitates better communication with healthcare providers. Moreover, the widespread use of smartphones ensures that these applications are accessible to a large portion of the population, further driving adoption.

Key Signals and Evidence

The primary signals driving the current and future landscape of the connected glucose monitoring device market revolve around the integration of technologies and increased adoption rates. The integration of CGMs with insulin delivery systems is a game-changer, offering a more comprehensive solution for diabetes management. This integration is not just a technological advancement but a strategic move that positions companies at the forefront of innovation in this space.

Increased adoption of CGMs is further supported by the trend towards real-time glucose monitoring. Patients are increasingly recognizing the benefits of having continuous access to their glucose levels, which allows for more proactive management of their condition. This trend is reflected in the growing market share of companies offering CGMs, as well as in the increasing number of patients transitioning from traditional fingerstick methods to continuous monitoring.

Regulatory approval for monitoring other electrolytes is another key signal that indicates a broader application of these technologies. This development suggests that glucose monitoring devices are evolving into more versatile diagnostic tools, capable of providing valuable health insights beyond glucose levels. Such versatility is likely to increase the attractiveness of these devices to both healthcare providers and patients, potentially expanding their market reach.

Finally, the role of smartphone applications cannot be overstated. These applications not only enhance the functionality of glucose monitoring devices but also facilitate their integration into the digital health ecosystem. By providing a platform for data analysis, insights, and remote monitoring, smartphone apps are essential components of modern diabetes management solutions.

In conclusion, the connected glucose monitoring device market is witnessing a significant transformation driven by technological advancements. The integration of CGMs with insulin delivery systems, increased adoption of real-time monitoring, regulatory approvals for expanded functionalities, and the widespread use of smartphone applications are key signals shaping the current market reality. These developments are likely to have profound implications for market dynamics, affecting everything from adoption rates and competitive behavior to pricing strategies and market structure.

Strategic Implications

The strategic implications of these signals are profound, as they suggest a shift in how diabetes management is approached. For stakeholders in the healthcare industry, these developments signal a need to adapt strategies to incorporate new technologies and workflows. Healthcare providers must consider integrating CGMs and insulin delivery systems into their practice, as these technologies offer significant benefits in terms of patient outcomes and efficiency. For instance, clinics and hospitals may need to invest in training programs for their staff to ensure they are equipped to use these advanced systems effectively.

For device manufacturers, the increased demand for integrated systems presents both opportunities and challenges. Companies must invest in research and development to stay ahead of the competition and meet the evolving needs of the market. This may involve forming strategic partnerships with other technology providers to enhance the functionality of their devices. Additionally, manufacturers will need to navigate the regulatory landscape carefully to ensure their products meet the necessary standards for approval.

The growing role of smartphone applications in diabetes management also presents strategic opportunities. Companies that can develop intuitive, user-friendly apps that integrate seamlessly with glucose monitoring devices are likely to gain a competitive edge. These apps not only enhance the user experience but also provide valuable data that can be used to improve treatment plans and outcomes.

Forward Outlook

Looking ahead, the connected glucose monitoring device market is poised for continued growth and innovation. In the near-to-medium term, we can expect to see further advancements in the integration of CGMs with insulin delivery systems. This will likely lead to the development of more sophisticated hybrid closed-loop systems that offer even greater control over diabetes management. The regulatory approval for monitoring other electrolytes is likely to drive innovation, as companies explore new functionalities and applications for their devices.

Moreover, the increased adoption of CGMs suggests a shift towards more personalized and proactive diabetes management strategies. As these devices become more widespread, healthcare providers and patients will have access to more detailed and timely data, enabling them to make more informed decisions about treatment. This trend is likely to lead to improved patient outcomes and a reduction in the long-term complications associated with diabetes.

In conclusion, the connected glucose monitoring device market is undergoing a significant transformation, driven by technological innovations and changing regulatory landscapes. Stakeholders must remain agile and adaptive, leveraging these developments to improve patient care and gain a competitive advantage. As the market continues to evolve, those who can effectively integrate these technologies into their offerings and strategies will be well-positioned to succeed in this dynamic and rapidly changing environment.

Market Risk

Risk Factors and Disruption Threats in the Global Usb Glucose Monitoring Device Market

Executive Framing

In the rapidly evolving landscape of connected glucose monitoring devices, understanding structural constraints and market impacts is crucial. As the industry heads towards a digital and connected future, there is a growing need to address the risks that could potentially disrupt operations and market dynamics. These risks include data breaches, lack of regulatory approval, and the challenge of integrating advanced technologies into existing healthcare frameworks. The market faces a moderate overall risk level with a low geopolitical exposure but a high substitution risk due to emerging technologies and innovations. This dimension matters now more than ever as stakeholders navigate through a complex web of technological advancements, regulatory landscapes, and market expectations. The focus on connected glucose monitoring devices is driven by the increasing prevalence of diabetes and the need for real-time, accurate glucose monitoring. However, the path to widespread adoption is fraught with challenges. The lack of regulatory approval in some regions, coupled with regional differences in the availability of insulin pumps and continuous glucose monitoring (CGM) systems, presents significant hurdles. These issues are compounded by the potential for data breaches and unapproved access, which could undermine consumer confidence and stall market growth. Therefore, understanding and mitigating these risks is vital for stakeholders looking to capitalize on this burgeoning market.

Current Market Reality

The current state of the connected glucose monitoring device market is shaped by a confluence of technological, regulatory, and consumer-driven factors. While there is a noticeable increase in the uptake of automated insulin delivery (AID) solutions, driven by the convenience and accuracy they offer, several structural constraints remain. A significant barrier is the lack of regulatory approval, which varies across regions and impacts the availability and adoption of these technologies. This discrepancy creates uneven market opportunities and poses risks for companies looking to expand their reach globally.

Entities such as the European Commission have played a pivotal role in supporting the development and adoption of these technologies. Funding from the European Commission’s Horizon 2020 Research and Innovation Program has been instrumental in driving research and development, enabling companies to explore new pathways and bring innovative solutions to market. However, despite these efforts, the lack of regulatory approval continues to be a significant roadblock. This regulatory challenge is not just a matter of compliance but affects pricing power, demand elasticity, and ultimately, the operational resilience of companies in this space.

Moreover, there is a growing movement towards open-source solutions, exemplified by the collaboration and support from the #WeAreNotWaiting community. This grassroots initiative has been pivotal in driving innovation and providing users with alternatives to traditional commercial offerings. By advocating for open access prospective data collection tools and comprehensive data entry by users and healthcare teams, this community has highlighted the potential of decentralized and user-led innovation. However, this also raises concerns about consistent quality, safety, and regulatory oversight, which are crucial for maintaining trust in connected healthcare solutions.

In addition to regulatory and community-driven challenges, the market also faces structural constraints related to technical skills and support. The lack of sufficient programming skills and limited support by medical professionals can hinder the effective adoption and integration of these technologies. Furthermore, concerns about the maintenance of AID systems, including software updates and system reliability, add to the complexity of managing these devices. These challenges underscore the need for robust educational resources for both users and healthcare professionals to ensure that they are equipped to handle the intricacies of connected glucose monitoring systems.

Key Signals And Evidence

Funding and Regulatory Environment

The European Commission’s Horizon 2020 Research and Innovation Program has been a pivotal source of funding for innovations in diabetes technology, including connected glucose monitoring devices. This funding underscores the importance of sustained investment in research and development to drive technological advancements and improve market readiness. However, the persistent lack of regulatory approval remains a significant barrier. Without regulatory clearance, particularly from bodies like the FDA, companies face hurdles in introducing new products to the market, which stifles innovation and limits consumer access to potentially life-saving technologies.

Regional Disparities and Community Initiatives

Another critical signal comes from the regional differences in the availability of insulin pumps and CGM systems. These discrepancies are often influenced by varying healthcare policies, reimbursement structures, and the economic capabilities of different regions. Such disparities can create uneven market growth and limit the scalability of technologies across borders. In response to these challenges, the #WeAreNotWaiting community exemplifies grassroots innovation, fostering collaboration and support among patients, developers, and healthcare professionals. This community has been instrumental in pushing for open-source solutions and advocating for patient-centered care models, demonstrating the power of collective action in overcoming systemic barriers.

Data Collection and Educational Resources

The creation of open access prospective data collection tools represents a significant advancement in understanding and improving connected glucose monitoring systems. These tools enable comprehensive data entry by users and healthcare teams, facilitating better insights into device performance and patient outcomes. Moreover, educational resources for healthcare professionals are increasingly pivotal. As devices become more sophisticated, ensuring that healthcare providers have the necessary skills and knowledge is critical for successful integration into clinical practice.

Strategic Implications

Navigating Regulatory Challenges

For companies operating in this space, the lack of regulatory approval is a double-edged sword. On one hand, it limits the ability to market new products, but it also presents an opportunity to engage in proactive dialogue with regulatory bodies. By participating in regulatory processes and contributing to the development of standards, companies can help shape a more favorable environment for innovation. Additionally, securing early approvals can provide a competitive advantage, allowing for first-mover benefits in a rapidly evolving market.

Addressing Regional Disparities

To mitigate the impact of regional disparities, companies must adopt flexible business models that can adapt to local healthcare environments. This may involve developing tiered product offerings or engaging in partnerships with local distributors to enhance accessibility. Additionally, advocating for policy changes that support broader adoption of glucose monitoring technologies can help level the playing field across different regions.

Leveraging Community and Data-Driven Insights

The #WeAreNotWaiting community exemplifies the potential of patient-driven innovation in shaping market dynamics. Companies can benefit from engaging with such communities to co-create solutions that meet the real-world needs of users. Furthermore, the wealth of data generated through open access tools and comprehensive data collection initiatives can inform product development, improve user experiences, and drive efficiencies in care delivery.

Enhancing Educational Initiatives

Education remains a cornerstone for the successful adoption of connected glucose monitoring devices. Companies and healthcare organizations must invest in training programs that equip healthcare professionals with the skills needed to navigate new technologies. These programs should not only focus on technical aspects but also encompass regulatory, ethical, and operational considerations to ensure holistic integration into clinical practice.

Forward Outlook

Increasing Regulatory Engagement

As regulatory bodies become more attuned to the potential benefits of connected health solutions, there is likely to be greater engagement and collaboration between industry players and regulators. This could lead to the development of clearer guidelines and faster approval processes, facilitating the introduction of new technologies to the market.

Expansion of Community-Driven Models

The influence of the #WeAreNotWaiting community and similar initiatives is set to grow, encouraging more patient-centered innovation and open-source solutions. These models offer a blueprint for how technology can be leveraged to address unmet needs and empower patients in managing their health.

Broader Adoption and Integration

With advancements in data collection and educational efforts, the adoption of connected glucose monitoring devices is expected to increase. This will likely lead to more integrated care models, where technology plays a central role in monitoring and managing chronic conditions. As these devices become more ubiquitous, the focus will shift towards optimizing their use within broader healthcare ecosystems.

Regulatory Landscape

Regulatory and Policy Landscape of the Global Usb Glucose Monitoring Device Market

Executive Framing

In the rapidly evolving landscape of connected glucose monitoring devices, the regulatory and policy environment emerges as a pivotal determinant of market dynamics. As healthcare technology continues to advance, the intersection of innovation and regulation becomes increasingly significant. The regulatory dimension is crucial in shaping the market structure by either facilitating or constraining the entry of new players, altering competitive landscapes, and influencing the strategic decisions of existing market participants. This dimension matters now more than ever due to the increasing regulatory scrutiny on healthcare technologies, driven by the need to ensure patient safety, data privacy, and the efficacy of medical devices. As we look toward the forecast period of 2026 to 2033, understanding the regulatory mechanisms and their implications on the connected glucose monitoring device market becomes essential for stakeholders aiming to navigate this complex environment effectively.

The connected glucose monitoring device market is particularly susceptible to regulatory influences due to the critical nature of its applications and the potential risks associated with device malfunctions or data breaches. Regulatory frameworks such as the FDA’s 510(k) approval process and the National Coverage Determination (NCD) for Home Blood Glucose Monitors significantly impact the market by setting the standards for device safety and efficacy. Moreover, the increasing emphasis on privacy and data protection, as reflected in regulations like HIPAA and GDPR, adds another layer of complexity for companies operating in this space. These regulatory requirements not only dictate the pace of innovation but also influence the cost structures and competitive dynamics within the market.

Current Market Reality

Presently, the connected glucose monitoring device market is characterized by a stringent regulatory landscape, where compliance with FDA regulations and obtaining 510(k) approval are prerequisites for market entry. The FDA’s role as a regulatory body is crucial, given its authority to approve or reject devices based on rigorous safety and efficacy standards. The 510(k) process, in particular, requires manufacturers to demonstrate that their device is substantially equivalent to a legally marketed device, thereby ensuring that new products do not compromise patient safety. This regulatory requirement serves as a significant barrier to entry, potentially limiting the influx of new competitors and affecting the overall competitive equilibrium.

At the same time, the Consumer Product Safety Commission (CPSC) regulations impose additional safety standards that manufacturers must adhere to, further shaping the market dynamics. These regulations ensure that devices meet specific safety criteria, thereby protecting consumers from potential hazards. As a result, companies are compelled to invest in robust safety features and comprehensive testing procedures, which can increase the cost of development and delay product launches.

The issue of improper payments related to glucose monitors also highlights the regulatory challenges facing the market. With an improper payment rate of 25.2%, and no documentation accounting for 67.6% of these payments, regulatory bodies are likely to tighten documentation and reporting requirements. This situation underscores the need for companies to maintain meticulous records and adhere to stringent documentation practices to avoid financial penalties and ensure compliance with reimbursement policies.

Moreover, the National Coverage Determination (NCD) and Local Coverage Determination (LCD) for glucose monitors establish the criteria for insurance reimbursement, directly impacting the market’s financial dynamics. The NCD for Home Blood Glucose Monitors (40.2) and the LCD for Glucose Monitors (L33822) set forth specific guidelines that influence the eligibility for coverage and reimbursement, affecting the demand for these devices and the overall market potential.

Key Signals And Evidence

The regulatory landscape for connected glucose monitoring devices is defined by several key signals that illustrate the current and future challenges faced by market participants. One of the most significant signals is the FDA 510(k) approval process, which continues to be a critical determinant of market access. This approval pathway not only ensures that devices meet the necessary safety and efficacy standards but also serves as a benchmark for innovation, as manufacturers strive to develop devices that meet or exceed existing standards.

The CPSC regulations further emphasize the importance of safety in product design and manufacturing processes. These regulations mandate rigorous safety testing and compliance, which can increase the complexity and cost of bringing new devices to market. As a result, companies must allocate substantial resources to research and development, quality assurance, and regulatory compliance to meet these stringent requirements.

Improper payment rates and documentation issues also serve as significant signals of the regulatory challenges in this market. With insufficient documentation accounting for 26.6% of improper payments, there is a clear need for companies to enhance their documentation practices to comply with reimbursement policies and avoid financial penalties. This situation highlights the importance of maintaining comprehensive records and implementing robust documentation processes to ensure compliance and avoid disruptions in reimbursement.

The NCD and LCD guidelines further underscore the regulatory complexities in the connected glucose monitoring device market. These guidelines establish the criteria for insurance coverage and reimbursement, directly influencing the financial viability of these devices. Compliance with these guidelines is essential for manufacturers to secure reimbursement and ensure market access, thereby affecting the overall demand and competitive dynamics in the market.

In addition to these primary signals, secondary signals such as the increased adoption of hybrid closed loop systems and partnerships for technology integration indicate a broader trend towards innovation and collaboration in the market. These developments suggest that regulatory approval for monitoring other electrolytes and increased investment in diabetes technology are likely to become important factors in shaping the future regulatory landscape.

Strategic Implications

The interconnectedness of regulatory frameworks and market dynamics necessitates a strategic approach for stakeholders within the connected glucose monitoring device market. The rigorous FDA 510(k) approval process, while ensuring safety and efficacy, also acts as a barrier to entry, particularly for smaller companies with limited resources. This could lead to a consolidation of market power among established players who have the financial and operational capacity to navigate these regulatory waters effectively.

For new entrants and smaller companies, strategic partnerships and collaborations become essential. By aligning with established firms or leveraging technological integrations, these entities can share the burden of compliance costs and accelerate their time-to-market. Furthermore, as the market gravitates towards hybrid closed-loop systems, companies that can integrate seamlessly with these technologies will likely gain a competitive edge.

The significant improper payment rates due to documentation issues highlight the need for companies to invest in robust documentation and compliance systems. This not only minimizes financial risks but also enhances credibility with both regulatory bodies and consumers. Companies that can demonstrate a high level of transparency and compliance are likely to foster stronger relationships with insurers and healthcare providers, improving their market positioning.

The growing emphasis on ethical sourcing and compliance with international agreements like the Paris Agreement and the EU Emissions Trading System indicates a shift towards sustainability in the healthcare technology sector. Companies that proactively adopt sustainable practices and demonstrate compliance with these broader regulatory expectations may benefit from improved brand reputation and increased consumer trust.

Forward Outlook

Looking ahead to the forecast period of 2026 to 2033, the regulatory and policy environment for connected glucose monitoring devices is poised to become even more complex. The continued evolution of FDA regulations and potential updates to the National and Local Coverage Determinations will likely introduce new compliance challenges and opportunities for innovation.

As digital health technologies continue to integrate with broader healthcare systems, there will be an increased focus on data privacy and cybersecurity. The intersection of healthcare regulation with data protection laws such as the GDPR and HIPAA will necessitate a dual focus on device efficacy and data integrity. Companies that prioritize cybersecurity measures and ensure compliance with data protection regulations will be better positioned to maintain consumer trust and avoid costly breaches.

Moreover, as the market for connected glucose monitoring devices expands globally, companies will need to navigate varying international regulatory standards. This will require a strategic focus on global compliance strategies, potentially driving the need for localized partnerships and market-specific adaptations.

In summary, the regulatory and policy environment for connected glucose monitoring devices will continue to shape the market landscape significantly. Stakeholders must adopt a proactive approach to compliance, leveraging strategic partnerships, and investing in sustainable practices to navigate this complex environment successfully. By aligning with evolving regulatory expectations and consumer demands, companies can position themselves for long-term success in this dynamic market.