Global Data Center Cooling System Market size and share Analysis 2026-2033

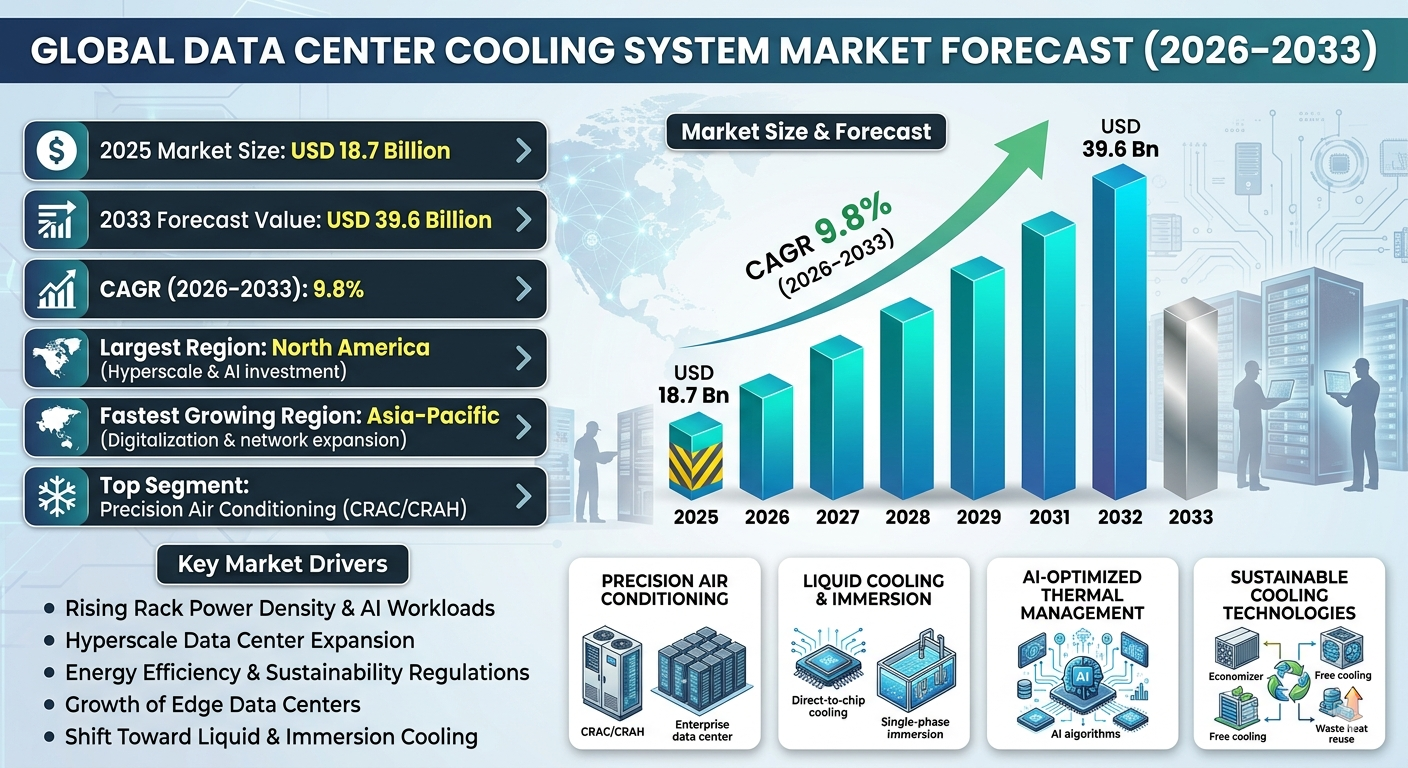

Global Data Center Cooling System Market Forecast Snapshot: 2026???2033

| Metric | Value |

| 2025 Market Size | USD 18.7 Billion |

| 2033 Market Size | USD 39.6 Billion |

| CAGR (2026???2033) | 9.8% |

| Largest Region | North America |

| Fastest Growing Region | Asia-Pacific |

| Top Segment | Precision Air Conditioning (CRAC/CRAH) Systems |

| Key Trend | Liquid Cooling & AI-Optimized Thermal Management |

| Future Focus | Immersion Cooling, Edge Data Center Cooling, Sustainable Cooling Technologies |

Global Data Center Cooling System Market Overview

The Global Data Center Cooling System Market is experiencing accelerated growth driven by hyperscale data center expansion, AI workload proliferation, cloud computing growth, and increasing rack power densities. Cooling systems are critical infrastructure components that ensure operational reliability, energy efficiency, and equipment longevity in modern data centers.

According to Pheonix Research, the Global Data Center Cooling System Market is valued at USD 18.7 billion in 2025 and is projected to reach USD 39.6 billion by 2033, registering a CAGR of 9.8% during 2026???2033. This growth reflects rising global data traffic, rapid digital transformation, 5G deployment, and enterprise cloud migration.

North America leads the market due to strong hyperscale investments from major cloud providers and AI infrastructure expansion. Meanwhile, Asia-Pacific is emerging as the fastest-growing region, supported by digitalization, smart city development, and large-scale data center construction in India, China, Singapore, and Southeast Asia.

Post-2025, the industry is shifting toward liquid cooling technologies, immersion systems, modular cooling infrastructure, AI-driven energy optimization, and sustainable heat recovery systems, transforming traditional air-based cooling models into high-efficiency thermal ecosystems.

Key Drivers of Global Data Center Cooling System Market Growth

1. Rising Rack Power Density & AI Workloads

AI servers and GPU clusters generate significantly higher heat loads than traditional IT equipment, necessitating advanced liquid and high-efficiency cooling systems.

2. Hyperscale Data Center Expansion

Major cloud service providers are building mega data centers globally, increasing demand for scalable and modular cooling infrastructure.

3. Energy Efficiency & Sustainability Regulations

Governments and enterprises are prioritizing energy-efficient cooling systems to reduce PUE (Power Usage Effectiveness) and carbon emissions.

4. Growth of Edge Data Centers

The proliferation of 5G and IoT is driving small-scale edge data centers requiring compact, energy-efficient cooling solutions.

5. Shift Toward Liquid & Immersion Cooling

Traditional air cooling is becoming insufficient for high-density workloads, accelerating adoption of direct-to-chip and immersion cooling technologies.

Global Data Center Cooling System Market Segmentation

1. By Cooling Type

1.1 Air-Based Cooling Systems

1.1.1 Computer Room Air Conditioners (CRAC)

1.1.1.1 DX-Based Cooling Units

1.1.1.1.1 Small Enterprise Data Centers

1.1.1.1.2 Colocation Facilities

1.1.2 Computer Room Air Handlers (CRAH)

1.1.2.1 Chilled Water-Based Systems

1.1.2.1.1 Hyperscale Facilities

1.1.2.1.2 Large Enterprise Data Centers

1.1.3 In-Row Cooling Systems

1.1.3.1 Close-Coupled Cooling

1.1.3.1.1 High-Density Racks

1.1.3.1.2 Modular Data Centers

1.2 Liquid-Based Cooling Systems

1.2.1 Direct-to-Chip Cooling

1.2.1.1 Cold Plate Systems

1.2.1.1.1 AI Servers

1.2.1.1.2 HPC Clusters

1.2.2 Immersion Cooling

1.2.2.1 Single-Phase Immersion

1.2.2.1.1 Edge Data Centers

1.2.2.1.2 Crypto Mining Facilities

1.2.2.2 Two-Phase Immersion

1.2.2.2.1 Hyperscale AI Workloads

1.2.2.2.2 Advanced HPC Deployments

1.3 Evaporative & Free Cooling

1.3.1 Air-Side Economizers

1.3.1.1 Climate-Based Deployment

1.3.1.1.1 Cold Region Data Centers

1.3.1.1.2 Renewable-Powered Sites

1.3.2 Water-Side Economizers

1.3.2.1 Hybrid Cooling Systems

1.3.2.1.1 Large Hyperscale Facilities

1.3.2.1.2 Sustainable Green Data Centers

2. By Component

2.1 Cooling Equipment

2.1.1 Chillers

2.1.1.1 Air-Cooled Chillers

2.1.1.1.1 Medium-Scale Data Centers

2.1.1.1.2 Enterprise IT Facilities

2.1.2 Cooling Towers

2.1.2.1 Open-Circuit Cooling Towers

2.1.2.1.1 Large Hyperscale Deployments

2.1.2.1.2 Industrial Data Centers

2.1.3 Pumps & Heat Exchangers

2.1.3.1 Plate Heat Exchangers

2.1.3.1.1 High-Density Workloads

2.1.3.1.2 Liquid Cooling Integration

2.2 Control & Monitoring Systems

2.2.1 Thermal Management Software

2.2.1.1 AI-Based Optimization Platforms

2.2.1.1.1 Predictive Maintenance

2.2.1.1.2 Energy Efficiency Optimization

2.2.2 Sensors & IoT Monitoring

2.2.2.1 Real-Time Environmental Monitoring

2.2.2.1.1 Temperature Control

2.2.2.1.2 Humidity Regulation

3. By Data Center Type

3.1 Hyperscale Data Centers

3.1.1 Cloud Service Providers

3.1.1.1 AI & Machine Learning Infrastructure

3.1.1.1.1 GPU Clusters

3.1.1.1.2 AI Training Systems

3.2 Colocation Data Centers

3.2.1 Multi-Tenant Facilities

3.2.1.1 Modular Cooling Systems

3.2.1.1.1 Scalable Infrastructure

3.2.1.1.2 Energy-Efficient Designs

3.3 Enterprise Data Centers

3.3.1 Banking & Financial Services

3.3.1.1 High-Security Cooling Systems

3.3.1.1.1 Mission-Critical Operations

3.3.1.1.2 Disaster Recovery Sites

3.4 Edge Data Centers

3.4.1 Telecom Edge Facilities

3.4.1.1 Compact Cooling Units

3.4.1.1.1 5G Infrastructure

3.4.1.1.2 IoT Deployments

4. By Region

4.1 North America

4.2 Asia-Pacific

4.3 Europe

4.4 Middle East & Africa

4.5 South America

Regional Insights of Global Data Center Cooling System Market

North America ??? Largest Market

North America leads the market due to strong hyperscale data center expansion, significant investments in AI infrastructure, and ongoing sustainability initiatives. The United States dominates the region with large-scale cloud facilities and colocation centers driving high cooling system demand.

Asia-Pacific ??? Fastest Growing Market

Rapid digitalization, 5G network deployment, and increasing data localization policies across China, India, and Southeast Asia are accelerating data center construction, driving strong growth in cooling system adoption.

Europe

Europe???s market growth is driven by strict energy efficiency regulations, ambitious carbon neutrality targets, and widespread adoption of sustainable cooling technologies, including air- and water-side economizers and free cooling systems.

Middle East & Africa

Growing investments in smart cities, digital transformation initiatives, and regional cloud infrastructure projects are fueling demand for advanced data center cooling solutions.

South America

Expansion of cloud services, enterprise digital adoption, and emerging colocation facilities are supporting steady growth in cooling system demand across the region.

Leading Companies in the Global Data Center Cooling System Market

??Schneider Electric ??Vertiv Group Corp. STULZ GmbH Rittal GmbH & Co. KG Johnson Controls Daikin Industries Mitsubishi Electric Huawei Digital Power Asetek (Liquid Cooling) Submer TechnologiesSchneider Electric and Vertiv are recognized as global leaders due to integrated cooling portfolios, strong global presence, and AI-driven energy optimization platforms.

Strategic Intelligence & AI-Backed Insights

Pheonix Demand Forecast Engine identifies AI server deployments, hyperscale investments, and liquid cooling adoption as primary long-term growth catalysts.

Infrastructure Investment Analyzer indicates increasing capital expenditure in modular and sustainable cooling systems globally.

Innovation Tracker highlights immersion cooling, direct-to-chip solutions, AI-powered thermal optimization, and waste heat reuse systems as major competitive differentiators.

Porter???s Five Forces Analysis reveals moderate supplier power, high capital intensity barriers, strong technological rivalry, and rising innovation-based differentiation.

Why the Global Data Center Cooling System Market Remains Critical

??? Ensures operational reliability of digital infrastructure

??? Enables high-performance AI & cloud computing

??? Reduces energy consumption and carbon footprint

??? Supports hyperscale and edge computing expansion

??? Strengthens global digital economy resilience

Final Takeaway of Global Data Center Cooling System Market

The Global Data Center Cooling System Market is rapidly transitioning toward high-efficiency, intelligent, and liquid-based thermal management ecosystems. The projected CAGR of 9.8% during 2026???2033 reflects strong hyperscale expansion, AI workload growth, and sustainability-driven infrastructure modernization.

Companies investing in immersion cooling, AI-powered optimization platforms, modular infrastructure, and energy-efficient heat recovery technologies will secure long-term competitive advantage in the post-2025 data center landscape.

At Pheonix Research, our advanced forecasting frameworks deliver in-depth revenue analysis, technology benchmarking, competitive intelligence, and infrastructure investment insights ??? empowering stakeholders to capitalize on next-generation data center cooling opportunities with data-driven confidence.

???? Social Mentions & Publication Channels

??Explore deeper insights and follow our cross-platform updates on??LinkedIn??and??X??for continuous intelligence and market coverage.

LinkedIn : https://www.linkedin.com/feed/update/urn:li:activity:7433756839244169216

X : https://x.com/Pheonix_Insight/status/2027994762461192287?s=20

Competitive Landscape

Global Data Center Cooling System Market Competitive Intensity & Market Structure Overview

The Global Data Center Cooling System Market is characterized by a highly technology-driven and competitive landscape, where innovation, energy efficiency, and scalability define market leadership. The market structure is moderately consolidated, with a group of global infrastructure and thermal management providers dominating large-scale deployments, particularly in hyperscale and colocation data centers.

Competitive intensity is elevated due to rapid technological evolution, increasing rack power densities, and the transition from traditional air-based systems to advanced liquid and immersion cooling solutions. Vendors compete not only on equipment performance but also on integrated solutions, lifecycle cost efficiency, and sustainability metrics such as Power Usage Effectiveness (PUE).

The market operates through a dual structure: large Tier 1 players secure long-term contracts with hyperscale cloud providers and enterprise clients, while niche and emerging players compete through specialized innovations such as liquid cooling, immersion systems, and AI-driven thermal optimization platforms.

Global Data Center Cooling System Market Competitive Intensity & Market Structure Current Scenario

Leading Company Profiles

Schneider Electric: Global Energy Management Leader. Offers integrated data center cooling, power, and infrastructure management solutions with strong AI-driven optimization capabilities.

Vertiv Group Corp.: Critical Digital Infrastructure Provider. Known for end-to-end thermal management systems, modular cooling solutions, and strong hyperscale partnerships.

STULZ GmbH: Precision Cooling Specialist. Focused on high-performance CRAC/CRAH systems and customized cooling solutions for mission-critical environments.

Rittal GmbH & Co. KG: Industrial Infrastructure Provider. Strong in modular and scalable cooling solutions for enterprise and edge data centers.

Johnson Controls: Building Technologies Leader. Provides energy-efficient HVAC and data center cooling systems with sustainability-focused solutions.

Daikin Industries: Global HVAC Leader. Offers advanced cooling technologies with a focus on energy efficiency and large-scale deployment capabilities.

Mitsubishi Electric: Advanced Cooling Systems Provider. Strong presence in precision air conditioning and energy-efficient cooling technologies.

Huawei Digital Power: Emerging Technology Player. Focused on AI-driven cooling optimization and integrated digital infrastructure solutions.

Asetek: Liquid Cooling Innovator. Specializes in direct-to-chip liquid cooling solutions for high-performance computing and AI workloads.

Submer Technologies: Immersion Cooling Specialist. Leading provider of sustainable immersion cooling systems for hyperscale and edge data centers.

Key Competitive Intensity & Market Structure Signals in Global Data Center Cooling System Market

A major competitive signal is the rapid shift toward liquid and immersion cooling technologies. As AI workloads and high-density racks increase thermal output, traditional air-based systems are becoming less effective, intensifying competition among vendors offering next-generation cooling solutions.

Long-term contracts with hyperscale cloud providers represent a critical competitive battleground. These contracts demand high reliability, scalability, and energy efficiency, creating high entry barriers for new players while strengthening the position of established vendors.

Sustainability and energy efficiency are central to competitive differentiation. Vendors are increasingly focusing on reducing PUE, enabling waste heat recovery, and integrating renewable energy-compatible cooling systems to align with global carbon reduction goals.

The emergence of edge data centers is introducing a new layer of competition, where compact, modular, and energy-efficient cooling solutions are essential. This is enabling smaller and specialized players to compete alongside established companies.

Strategic Implications of Competitive Intensity & Market Structure in Global Data Center Cooling System Market

Companies are transitioning from standalone equipment providers to integrated infrastructure solution partners. End-to-end offerings that combine cooling, power management, monitoring, and AI-based optimization are becoming essential to secure large-scale contracts.

Innovation investment is a key strategic priority, particularly in liquid cooling, immersion systems, and AI-driven thermal management. Vendors that lead in these technologies gain a significant competitive advantage in high-growth AI and HPC segments.

Partnerships with hyperscale cloud providers, colocation operators, and semiconductor companies are increasingly shaping market positioning. Collaborative ecosystems enable faster deployment, customization, and long-term service agreements.

Cost competitiveness is evolving toward total cost of ownership (TCO), where energy savings, operational efficiency, and system longevity outweigh initial capital expenditure, influencing procurement decisions.

Global Data Center Cooling System Market Competitive Intensity & Market Structure Forward Outlook

The market is expected to remain highly competitive, with increasing consolidation among leading infrastructure providers and rapid growth of specialized cooling technology firms. Mergers, acquisitions, and strategic alliances will play a critical role in expanding technological capabilities and market reach.

Liquid cooling and immersion technologies are anticipated to become mainstream in hyperscale and AI-driven data centers, reshaping competitive dynamics and creating new leadership opportunities for innovation-focused companies.

AI-driven thermal optimization and predictive maintenance will become standard features, enhancing operational efficiency and reducing downtime, further intensifying competition on digital capabilities.

In the long term, the market will be defined by three core competitive pillars: energy efficiency, advanced cooling innovation, and integrated digital infrastructure management. Companies that align with these pillars while maintaining strong global partnerships will lead the Global Data Center Cooling System Market through 2033.

Value Chain

Global Data Center Cooling System Market Value Chain & Supply Chain Evolution Overview

The Global Data Center Cooling System Market value chain is evolving from traditional HVAC-based infrastructure into a highly advanced, energy-efficient, and AI-optimized thermal management ecosystem. With the rapid expansion of hyperscale data centers, AI workloads, and high-density computing environments, cooling systems are becoming critical enablers of performance, sustainability, and operational continuity.

The value chain spans component manufacturing, cooling system engineering, thermal design optimization, AI-based control systems, system integration, deployment, monitoring, and lifecycle management. Increasingly, the market is shifting toward liquid cooling technologies, modular cooling architectures, and intelligent thermal management platforms that optimize energy usage and reduce carbon footprints.

Upstream supply chain dynamics are driven by component manufacturers such as chiller producers, heat exchanger suppliers, pump manufacturers, refrigerant providers, and sensor developers. The rise of liquid cooling has also introduced specialized suppliers focused on immersion fluids, cold plates, and advanced thermal interface materials.

Midstream activities focus on system integration, including design engineering, cooling architecture planning, AI-based optimization software, and infrastructure deployment. Companies are integrating IoT sensors, predictive analytics, and automation systems to ensure real-time monitoring and adaptive cooling performance.

Downstream distribution includes hyperscale data centers, colocation providers, enterprise IT facilities, and edge data center deployments. Service providers also play a key role in installation, maintenance, retrofitting, and performance optimization services.

Key challenges across the value chain include high capital investment, energy consumption constraints, integration complexity, evolving sustainability regulations, and the transition from air-based to liquid-based cooling systems.

Global Data Center Cooling System Market Value Chain & Supply Chain Evolution Current Scenario

The current market landscape is shaped by increasing data generation, AI adoption, and the need for high-performance computing infrastructure.

Upstream, suppliers are innovating in energy-efficient components, advanced refrigerants, and liquid cooling technologies to meet rising thermal demands.

Midstream players are focusing on modular cooling systems, scalable architectures, and AI-driven thermal management platforms to enhance efficiency and reduce operational costs.

Downstream, hyperscale data centers dominate demand, while edge data centers are emerging as a new growth segment requiring compact and efficient cooling solutions.

Service ecosystems are expanding to include predictive maintenance, remote monitoring, and lifecycle optimization services, ensuring continuous system performance and reduced downtime.

Key Value Chain & Supply Chain Evolution Signals in Global Data Center Cooling System Market

Several transformative trends are reshaping the cooling system ecosystem globally.

First, liquid cooling technologies, including direct-to-chip and immersion cooling, are rapidly replacing traditional air-based systems in high-density environments.

Second, AI-driven thermal optimization is enhancing real-time cooling efficiency through predictive analytics and automated control systems.

Third, modular and prefabricated cooling systems are gaining traction, enabling faster deployment and scalability for hyperscale and edge data centers.

Fourth, sustainability initiatives are driving the adoption of energy-efficient cooling systems, heat recovery technologies, and low-GWP refrigerants.

Fifth, integration with IoT sensors and digital twin technologies is improving system monitoring, fault detection, and performance optimization.

Sixth, edge data center growth is creating demand for compact, decentralized, and energy-efficient cooling solutions.

Strategic Implications of Value Chain & Supply Chain Evolution in Global Data Center Cooling System Market

Leading companies such as Schneider Electric, Vertiv, STULZ, Rittal, and Johnson Controls are strengthening their market positions through integrated cooling solutions, AI-based optimization platforms, and global service networks.

Competitive advantage increasingly depends on energy efficiency, scalability, system reliability, and the ability to integrate advanced technologies such as AI and liquid cooling.

Companies investing in sustainable cooling technologies and heat reuse systems are better positioned to meet regulatory requirements and corporate ESG goals.

Strategic partnerships between cooling providers, cloud companies, and infrastructure developers are becoming critical for large-scale deployments.

Lifecycle services, including maintenance, retrofitting, and performance optimization, are emerging as key revenue streams and differentiation factors.

Global Data Center Cooling System Market Value Chain & Supply Chain Evolution Forward Outlook

Between 2026 and 2033, the value chain is expected to become more intelligent, sustainable, and integrated with digital infrastructure ecosystems.

Liquid cooling and immersion technologies will become mainstream for AI and high-performance computing environments.

AI-driven energy optimization platforms will play a central role in reducing operational costs and improving system efficiency.

Edge data center expansion will drive demand for compact, modular, and autonomous cooling systems.

Sustainability will remain a key focus, with increasing adoption of renewable energy integration, waste heat recovery, and environmentally friendly cooling technologies.

Overall, the value chain will evolve toward a fully integrated thermal management ecosystem supporting next-generation digital infrastructure.

Market-Specific Value Chain

- Raw Materials & Component Manufacturing: Chillers, compressors, heat exchangers, pumps, refrigerants, sensors

- Cooling Technology Development: Air-based systems, liquid cooling, immersion cooling, thermal engineering

- System Integration & Software: AI-based thermal management, IoT monitoring, control systems, digital twins

- Infrastructure Deployment: Hyperscale, colocation, enterprise, and edge data center installations

- Distribution & End-Use Applications: Cloud providers, telecom operators, enterprises, colocation providers

- Services & Lifecycle Management: Maintenance, retrofitting, monitoring, optimization, sustainability solutions

Company-to-Stage Mapping

- Raw Materials & Component Manufacturing: Daikin Industries, Mitsubishi Electric, Johnson Controls

- Cooling Technology Development: STULZ, Rittal, Asetek, Submer Technologies

- System Integration & Software: Schneider Electric, Vertiv, Huawei Digital Power

- Infrastructure Deployment: Schneider Electric, Vertiv, global EPC contractors

- Distribution & End-Use Applications: AWS, Google Cloud, Microsoft Azure, colocation providers

- Services & Lifecycle Management: Vertiv Services, Schneider Electric Services, Johnson Controls

Investment Activity

Global Data Center Cooling System Market Investment & Funding Dynamics Overview

Investment and funding dynamics in the Global Data Center Cooling System Market are being strongly driven by the rapid expansion of hyperscale data centers, increasing AI workload intensity, rising rack power densities, and growing emphasis on energy efficiency and sustainability. Between 2026 and 2033, capital allocation is expected to increasingly focus on liquid cooling technologies, AI-driven thermal optimization platforms, modular cooling infrastructure, and sustainable heat management systems.

The market is becoming highly capital-intensive and innovation-driven, attracting significant investments from hyperscale cloud providers, colocation operators, and infrastructure funds. Leading players such as Schneider Electric, Vertiv, STULZ, Rittal, Johnson Controls, and emerging liquid cooling specialists are heavily investing in next-generation cooling architectures and integrated digital management platforms to address evolving data center requirements.

A major transformation influencing funding flows is the shift from traditional air-based cooling toward liquid and immersion cooling technologies. This transition is directing investments toward high-efficiency cooling systems capable of supporting AI, HPC, and GPU-intensive workloads while minimizing energy consumption and carbon emissions.

Global Data Center Cooling System Market Investment & Funding Dynamics Current Scenario

Currently, investment activity is accelerating due to large-scale data center construction, cloud expansion, AI infrastructure deployment, and regulatory pressure for energy-efficient operations. Cooling infrastructure is now a strategic investment priority rather than a support function.

- North America: Leads global investment due to hyperscale data center expansion, AI infrastructure investments, and strong presence of major cloud service providers.

- Asia-Pacific: Fastest-growing investment region driven by rapid digitalization, data localization policies, and large-scale data center construction across China, India, and Southeast Asia.

- Europe: Significant investments focused on sustainable cooling technologies, carbon neutrality targets, and regulatory-compliant energy-efficient systems.

- Middle East & Africa: Emerging investment hub supported by smart city initiatives, cloud infrastructure development, and increasing digital transformation programs.

Key Investment & Funding Dynamics Signals in Global Data Center Cooling System Market

- Rising AI and high-density computing workloads are accelerating investments in liquid cooling, immersion systems, and direct-to-chip technologies.

- Hyperscale data center expansion is driving large-scale capital deployment in modular and scalable cooling infrastructure.

- Energy efficiency regulations and sustainability mandates are increasing funding toward low-PUE cooling systems and carbon reduction technologies.

- Edge data center growth is creating new investment opportunities in compact, decentralized, and energy-efficient cooling solutions.

- Digital transformation is boosting investments in AI-powered thermal management software, IoT-based monitoring systems, and predictive maintenance platforms.

Strategic Implications of Investment & Funding Dynamics in Global Data Center Cooling System Market

- The investment landscape favors companies with strong capabilities in liquid cooling technologies and AI-driven energy optimization solutions.

- Integration of hardware and software-based cooling management systems is becoming critical for competitive differentiation.

- Partnerships between cooling solution providers, cloud operators, and semiconductor companies are increasing to co-develop next-generation thermal systems.

- Regional diversification is essential, with North America leading hyperscale investments and Asia-Pacific driving future growth momentum.

- Sustainability-focused innovation, including heat reuse and renewable-powered cooling, is becoming a key investment priority.

Global Data Center Cooling System Market Investment & Funding Dynamics Forward Outlook

Looking ahead, the Global Data Center Cooling System Market is expected to attract substantial and sustained investment as digital infrastructure continues to expand globally and AI workloads redefine thermal management requirements.

Future capital allocation will increasingly prioritize immersion cooling, direct-to-chip liquid cooling, AI-driven optimization platforms, modular edge cooling systems, and sustainable heat recovery technologies.

- North America: Will maintain leadership in hyperscale and AI-driven cooling investments supported by major cloud and technology companies.

- Asia-Pacific: Will dominate future investment growth due to rapid data center expansion and digital economy acceleration.

- Europe: Will continue focusing on sustainable and regulatory-compliant cooling innovations.

Advancements in AI-based thermal analytics, autonomous cooling systems, and circular energy models will increasingly shape funding strategies across the market.

Overall, the market will remain a high-growth and innovation-centric investment segment through 2033, supported by its critical role in enabling global digital infrastructure, AI computing, and sustainable data center operations. Companies that lead in liquid cooling innovation, digital integration, and energy-efficient solutions will define the future competitive landscape.

Technology & Innovation

Global Data Center Cooling System Market Technology & Innovation Landscape Overview

The technology and innovation landscape within the Global Data Center Cooling System Market is rapidly evolving toward high-efficiency, intelligent, and sustainable thermal management ecosystems. As data centers become the backbone of digital infrastructure, cooling technologies are transitioning from traditional support systems into critical enablers of performance, scalability, and energy optimization.

Innovation intensity in this market is accelerating due to the exponential growth of AI workloads, hyperscale data centers, and high-density computing environments. Leading companies such as Schneider Electric, Vertiv, STULZ, Rittal, and emerging liquid cooling specialists are investing heavily in next-generation cooling architectures that combine hardware innovation with software-driven intelligence.

A major transformation is the shift from air-based cooling to advanced liquid cooling technologies, including direct-to-chip and immersion cooling systems. These innovations enable efficient heat dissipation for high-performance computing (HPC), AI servers, and GPU clusters, where traditional cooling methods are no longer sufficient.

Simultaneously, the integration of AI, IoT sensors, and cloud-based thermal management platforms is enabling real-time monitoring, predictive maintenance, and dynamic optimization of cooling performance. This convergence is transforming data center cooling into a smart, autonomous, and adaptive system.

Global Data Center Cooling System Market Technology & Innovation Landscape Current Scenario

Currently, the market is focused on improving energy efficiency, managing increasing heat loads, and reducing operational costs. Data center operators are adopting innovative cooling technologies that balance performance with sustainability objectives.

Liquid cooling technologies are gaining strong traction, particularly in hyperscale and AI-driven environments. Direct-to-chip cooling systems use cold plates to remove heat directly from processors, while immersion cooling submerges hardware in thermally conductive fluids for maximum efficiency.

AI-driven thermal management systems are emerging as a key innovation pillar. These platforms use machine learning algorithms to analyze temperature patterns, workload distribution, and environmental conditions to optimize cooling operations in real time.

Free cooling and economizer technologies are being widely adopted in regions with favorable climates. Air-side and water-side economizers leverage ambient environmental conditions to reduce reliance on mechanical cooling, significantly improving energy efficiency.

Modular and scalable cooling infrastructure is also gaining importance, particularly in colocation and edge data centers. These systems allow operators to expand capacity incrementally while maintaining optimal thermal performance.

Additionally, heat recovery and reuse systems are being integrated into data center designs, enabling waste heat to be repurposed for district heating or industrial applications, contributing to sustainability goals.

Key Technology & Innovation Trends in Global Data Center Cooling System Market

- Liquid Cooling Adoption: Direct-to-chip and immersion cooling for high-density workloads.

- AI-Driven Thermal Optimization: Predictive analytics and real-time cooling management.

- Edge Data Center Cooling Solutions: Compact and energy-efficient systems for distributed infrastructure.

- Free Cooling & Economizers: Leveraging ambient conditions for energy savings.

- Modular Cooling Infrastructure: Scalable and flexible deployment models.

- IoT-Enabled Monitoring Systems: Real-time temperature and humidity tracking.

- Heat Recovery Systems: Reusing waste heat for sustainability and cost efficiency.

- High-Efficiency Cooling Equipment: Advanced chillers, heat exchangers, and cooling towers.

Strategic Implications of Technology & Innovation

Technological advancements are transforming data center cooling into a strategic differentiator rather than a supporting function. Companies that adopt advanced cooling technologies can achieve lower energy consumption, improved system reliability, and reduced operational costs.

For hyperscale operators and cloud providers, innovation in cooling is critical to supporting AI workloads and maintaining competitive performance levels. Efficient cooling systems directly impact power usage effectiveness (PUE) and overall sustainability metrics.

However, the adoption of advanced cooling technologies requires significant capital investment, specialized expertise, and infrastructure redesign, creating barriers for smaller operators.

Governments and regulatory bodies are also influencing innovation by enforcing energy efficiency standards and carbon reduction targets, pushing companies toward greener cooling solutions.

Strategically, organizations that invest in intelligent, liquid-based, and sustainable cooling systems will be better positioned to meet future demand while maintaining environmental compliance.

Global Data Center Cooling System Market Technology & Innovation Forward Outlook

Looking ahead, the market is expected to transition toward fully autonomous and self-optimizing cooling ecosystems powered by AI and advanced analytics. These systems will continuously adapt to workload fluctuations and environmental conditions to maximize efficiency.

Liquid cooling, particularly immersion technologies, is anticipated to become mainstream as AI and high-performance computing workloads continue to grow. Hybrid cooling models combining air and liquid systems will also gain traction.

Sustainability will remain a central focus, with increased adoption of renewable energy integration, zero-water cooling technologies, and advanced heat reuse systems.

Edge data center expansion will drive demand for compact, energy-efficient, and easily deployable cooling solutions tailored for distributed computing environments.

In conclusion, the Global Data Center Cooling System Market is evolving into an intelligent, energy-efficient, and sustainability-driven ecosystem. Companies that lead in liquid cooling innovation, AI-based optimization, and modular infrastructure design will define the future of data center thermal management through 2033.