Global Digital Health Market Size and Share Analysis 2026-2033

Global Digital Health Market Size & Forecast

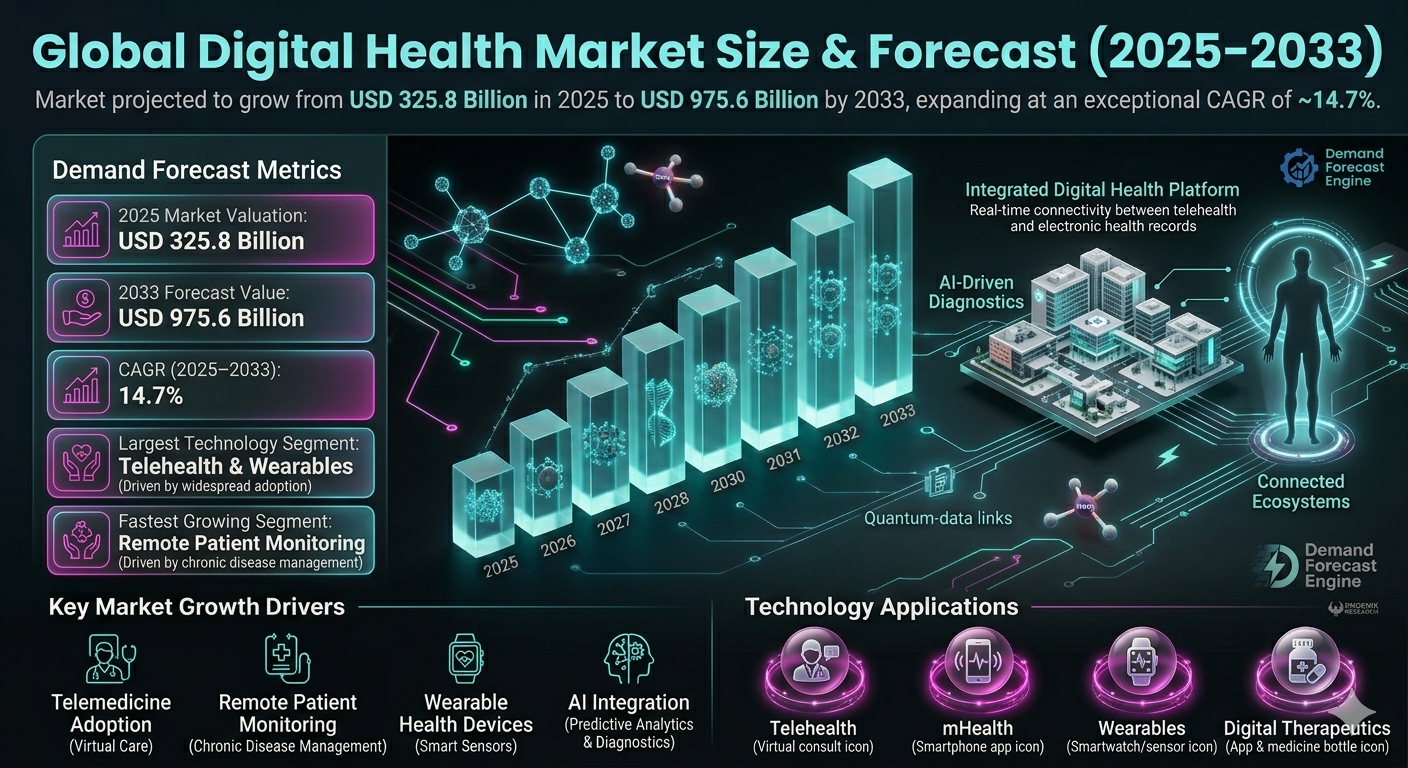

The global digital health market is projected to witness exceptional growth during the forecast period from 2026 to 2033. The market was valued at approximately USD 325.8 billion in 2025 and is expected to reach nearly USD 975.6 billion by 2033, expanding at a CAGR of around 14.7%. The market growth is driven by increasing adoption of telemedicine, rapid digitization of healthcare systems, rising use of wearable health devices, growing integration of artificial intelligence in diagnostics, and expanding demand for remote patient monitoring solutions. Digital health refers to the use of digital technologies, software platforms, connected devices, and data-driven solutions to improve healthcare delivery, patient monitoring, disease management, and clinical decision-making. It includes telehealth, mobile health (mHealth), health information technology, digital therapeutics, wearable medical devices, and AI-powered healthcare platforms. The market is witnessing significant transformation through advancements in cloud computing, AI-driven analytics, IoT-enabled health monitoring, blockchain-based medical records, and personalized digital treatment platforms. Additionally, increasing chronic disease prevalence, aging populations, healthcare accessibility challenges, and government initiatives promoting digital healthcare infrastructure are accelerating market expansion globally.

Global Digital Health Market Overview

The digital health market is a critical segment of the global healthcare technology ecosystem. It enables healthcare providers, hospitals, insurers, pharmaceutical companies, and patients to improve healthcare outcomes through connected, efficient, and data-driven solutions. The market includes telemedicine platforms, electronic health records (EHR), remote patient monitoring systems, mobile health applications, digital therapeutics, wearable devices, AI-based diagnostics, and clinical workflow automation solutions. Healthcare organizations are increasingly adopting digital tools to improve patient engagement, streamline clinical operations, reduce costs, and deliver personalized care. Technological innovations such as predictive analytics, virtual consultations, machine learning diagnostics, and connected health ecosystems are reshaping global healthcare delivery models. Major market participants include Teladoc Health Inc., Philips Healthcare, Cerner Corporation, GE HealthCare, Siemens Healthineers, Epic Systems Corporation, Medtronic plc, Oracle Health, Apple Inc., and Veradigm Inc.Key Drivers of Global Digital Health Market Growth

Rapid Adoption of Telemedicine and Virtual Care

The growing acceptance of virtual healthcare consultations is significantly driving digital health adoption worldwide. Telemedicine improves healthcare accessibility, reduces operational costs, and enables efficient patient management.Increasing Prevalence of Chronic Diseases

The rising burden of chronic conditions such as diabetes, cardiovascular diseases, and respiratory disorders is increasing demand for remote patient monitoring and digital disease management solutions. Continuous monitoring improves early intervention and treatment outcomes.Advancements in Wearable Health Devices

Wearable devices such as smartwatches, biosensors, and connected fitness trackers are enabling real-time health monitoring. These devices provide valuable health data for preventive care and clinical decision-making.Growing Integration of Artificial Intelligence

AI-powered diagnostic tools, predictive analytics, and automated clinical decision support systems are enhancing healthcare accuracy and efficiency. AI is transforming disease detection, treatment planning, and operational workflows.Government Support for Healthcare Digitization

Governments worldwide are investing in digital healthcare infrastructure, electronic health record systems, and telehealth reimbursement policies. These initiatives are accelerating digital health adoption across healthcare systems.Global Digital Health Market Segmentation

By Technology

The market is segmented into telehealth, mHealth, digital therapeutics, health analytics, electronic health records, wearable devices, and AI-powered healthcare platforms. Telehealth and wearable health technologies account for significant market share due to widespread consumer and provider adoption.By Component

The market includes software, hardware, and services. Software solutions dominate due to increasing deployment of cloud-based healthcare platforms.By Application

Applications include remote patient monitoring, chronic disease management, diagnostics, fitness & wellness, mental health management, and healthcare administration. Remote patient monitoring is among the fastest-growing application segments.By End User

End users include hospitals, clinics, healthcare providers, patients, insurance companies, and pharmaceutical companies. Hospitals and healthcare providers remain the largest end-user segment globally.Regional Market Dynamics

North America

North America dominates the global digital health market due to advanced healthcare infrastructure, high digital technology adoption, strong reimbursement frameworks, and significant healthcare IT investments. The United States leads regional growth with extensive telehealth deployment and AI healthcare innovation.Europe

Europe represents a major market driven by healthcare digitization initiatives, aging populations, and supportive regulatory frameworks. Germany, the United Kingdom, France, and Nordic countries are major contributors.Asia-Pacific

Asia-Pacific is the fastest-growing region due to rising smartphone penetration, expanding healthcare access, increasing chronic disease prevalence, and government digital health initiatives. China, India, Japan, and South Korea are key growth markets.Latin America

Latin America is witnessing increasing adoption due to healthcare modernization and growing telemedicine penetration. Brazil and Mexico are major regional markets.Middle East & Africa

The region is gradually expanding due to healthcare infrastructure investments, smart city initiatives, and digital transformation programs. GCC countries are leading digital health adoption.Competitive Landscape

The global digital health market is highly competitive and innovation-driven, with technology companies, healthcare providers, and medical device manufacturers competing through platform innovation and integrated healthcare solutions. Key players include Teladoc Health Inc., Philips Healthcare, Cerner Corporation, GE HealthCare, Siemens Healthineers, Epic Systems Corporation, Medtronic plc, Oracle Health, Apple Inc., and Veradigm Inc. Companies are increasingly investing in AI diagnostics, cloud healthcare platforms, wearable integration, predictive analytics, and personalized digital therapeutics. Strategic partnerships between technology firms, healthcare institutions, and insurers are shaping the competitive landscape.Strategic Outlook

The strategic outlook for the global digital health market remains highly positive due to increasing digital transformation across healthcare systems worldwide. Future opportunities include AI-driven personalized medicine, virtual hospitals, blockchain-secured medical records, interoperable digital health ecosystems, and advanced predictive healthcare analytics. Integration of 5G, IoT, and cloud-native healthcare infrastructure will further enhance digital health capabilities. Organizations investing in secure data management, patient-centric digital solutions, and scalable healthcare technology platforms are expected to strengthen their competitive positioning.Final Market Perspective

The global digital health market is fundamentally transforming healthcare delivery through connected, intelligent, and patient-focused digital solutions. Growing demand for accessible healthcare, remote monitoring, and data-driven clinical decision-making will continue driving strong market expansion throughout the forecast period. Companies that successfully combine technological innovation, regulatory compliance, and patient-centric digital healthcare ecosystems will remain strongly positioned in the evolving global digital health market.Table of Contents

Table of Contents

- 1. Executive Summary

- 1.1 Global Digital Health Market Snapshot (2026-2033)

- 1.2 Market Size & CAGR Analysis

- 1.3 Largest & Fastest-Growing Segments

- 1.4 Key Regional Insights

- 1.5 Major Market Growth Drivers

- 1.6 Competitive Landscape Overview

- 1.7 Strategic Outlook Through 2033

- 2. Introduction & Market Overview

- 2.1 Definition of Digital Health

- 2.2 Scope of the Study

- 2.3 Evolution of Digital Healthcare Technologies

- 2.4 Digital Health Value Chain Analysis

- 2.5 Healthcare IT Ecosystem Overview

- 2.6 Regulatory & Compliance Landscape

- 2.7 Emerging Technology Trends in Digital Health

- 3. Research Methodology

- 3.1 Primary Research

- 3.2 Secondary Research

- 3.3 Market Size Estimation Model

- 3.4 Forecast Assumptions (2026-2033)

- 3.5 Data Validation & Market Triangulation

- 4. Market Dynamics

- 4.1 Drivers

- 4.1.1 Rapid Adoption of Telemedicine and Virtual Care

- 4.1.2 Increasing Prevalence of Chronic Diseases

- 4.1.3 Advancements in Wearable Health Devices

- 4.1.4 Growing Integration of Artificial Intelligence

- 4.1.5 Government Support for Healthcare Digitization

- 4.2 Restraints

- 4.2.1 Data Privacy & Security Concerns

- 4.2.2 Regulatory Complexity Across Regions

- 4.2.3 High Implementation Costs

- 4.2.4 Limited Interoperability Between Platforms

- 4.3 Opportunities

- 4.3.1 Expansion of AI-Powered Personalized Medicine

- 4.3.2 Growth of Virtual Hospitals

- 4.3.3 Blockchain-Based Medical Records

- 4.3.4 Emerging 5G-Enabled Connected Healthcare

- 4.4 Challenges

- 4.4.1 Cybersecurity Threats

- 4.4.2 Digital Literacy Barriers

- 4.4.3 Integration with Legacy Healthcare Systems

- 4.4.4 Reimbursement & Policy Uncertainties

- 4.1 Drivers

- 5. Global Digital Health Market Analysis (USD Billion), 2026-2033

- 5.1 Market Size Overview

- 5.2 CAGR Analysis

- 5.3 Regional Revenue Distribution

- 5.4 Segment Revenue Analysis

- 5.5 Digital Healthcare Investment Trends

- 5.6 Adoption Rate Analysis

- 6. Market Segmentation (USD Billion), 2026-2033

- 6.1 By Technology

- 6.1.1 Telehealth

- 6.1.1.1 Virtual Consultation Platforms

- 6.1.1.1.1 Real-Time Patient Care Systems

- 6.1.1.1.1.1 Remote Clinical Engagement Solutions

- 6.1.1.1.1 Real-Time Patient Care Systems

- 6.1.1.1 Virtual Consultation Platforms

- 6.1.2 Mobile Health (mHealth)

- 6.1.2.1 Health Monitoring Applications

- 6.1.3 Digital Therapeutics

- 6.1.3.1 Personalized Treatment Platforms

- 6.1.4 Health Analytics

- 6.1.5 Electronic Health Records (EHR)

- 6.1.6 Wearable Devices

- 6.1.7 AI-Powered Healthcare Platforms

- 6.1.1 Telehealth

- 6.2 By Component

- 6.2.1 Software

- 6.2.2 Hardware

- 6.2.3 Services

- 6.3 By Application

- 6.3.1 Remote Patient Monitoring

- 6.3.2 Chronic Disease Management

- 6.3.3 Diagnostics

- 6.3.4 Fitness & Wellness

- 6.3.5 Mental Health Management

- 6.3.6 Healthcare Administration

- 6.4 By End User

- 6.4.1 Hospitals

- 6.4.2 Clinics

- 6.4.3 Healthcare Providers

- 6.4.4 Patients

- 6.4.5 Insurance Companies

- 6.4.6 Pharmaceutical Companies

- 6.1 By Technology

- 7. Market Segmentation by Geography

- 7.1 North America

- 7.2 Europe

- 7.3 Asia-Pacific

- 7.4 Latin America

- 7.5 Middle East & Africa

- 8. Competitive Landscape

- 8.1 Market Share Analysis

- 8.2 Technology Benchmarking

- 8.3 Strategic Partnerships & Collaborations

- 8.4 Product Innovation Analysis

- 8.5 Mergers & Acquisitions

- 9. Company Profiles

- 9.1 Teladoc Health Inc.

- 9.2 Philips Healthcare

- 9.3 Oracle Health

- 9.4 GE HealthCare

- 9.5 Siemens Healthineers

- 9.6 Epic Systems Corporation

- 9.7 Medtronic plc

- 9.8 Apple Inc.

- 9.9 Veradigm Inc.

- 9.10 Cerner Corporation

- 10. Strategic Intelligence & Pheonix AI Insights

- 10.1 Pheonix Demand Forecast Engine

- 10.2 Digital Healthcare Adoption Analyzer

- 10.3 Patient Engagement Monitoring Tracker

- 10.4 AI Diagnostics Penetration Assessment

- 10.5 Automated Porter’s Five Forces Analysis

- 11. Future Outlook & Strategic Recommendations

- 11.1 Expansion of Virtual Healthcare Ecosystems

- 11.2 Growth of AI-Driven Personalized Care

- 11.3 Integration of Blockchain & Secure Data Platforms

- 11.4 Investment in Interoperable Digital Infrastructure

- 11.5 Long-Term Market Outlook (2033+)

- 12. Appendix

- 13. About Pheonix Research

- 14. Disclaimer

Competitive Landscape

Global Digital Health Market Competitive Intensity & Market Structure Overview

The global digital health market is highly competitive, rapidly evolving, and innovation-driven, with strong participation from healthcare technology companies, medical device manufacturers, software providers, cloud platform vendors, and digital-first healthcare service providers. Competition is primarily centered around platform interoperability, AI-driven clinical intelligence, patient engagement capabilities, data security, regulatory compliance, and integrated healthcare ecosystem development.

The market structure is moderately fragmented, with a mix of established healthcare technology leaders, specialized digital health startups, telehealth providers, wearable device companies, and enterprise software firms. Strategic consolidation through mergers, acquisitions, and partnerships is becoming increasingly common as organizations seek to build end-to-end digital healthcare ecosystems.

Rapid healthcare digitization, increasing telemedicine adoption, growing use of wearable technologies, and expanding demand for personalized and remote healthcare delivery are significantly intensifying global market competition.

Global Digital Health Market Competitive Intensity & Market Structure Current Scenario

Leading Digital Health & Healthcare Technology Companies

Teladoc Health Inc.: A leading telehealth and virtual care provider with strong capabilities in remote consultations, chronic care management, and digital health platform services.

Philips Healthcare: Major healthcare technology company offering connected patient monitoring systems, digital diagnostics, and integrated remote care solutions.

Oracle Health: Significant healthcare IT provider focused on electronic health records, cloud healthcare infrastructure, and data interoperability solutions.

GE HealthCare: Key participant in AI-powered diagnostics, digital imaging systems, and connected clinical workflow technologies.

Siemens Healthineers: Major innovator in digital diagnostics, AI-driven imaging platforms, and integrated healthcare analytics solutions.

Epic Systems Corporation: Leading provider of electronic health record systems and healthcare workflow management platforms.

Medtronic plc: Strong player in connected medical devices, remote patient monitoring, and digital therapeutic solutions.

Apple Inc.: Important participant driving wearable health technology adoption through connected health monitoring ecosystems and consumer digital wellness solutions.

Veradigm Inc.: Active provider of healthcare data analytics, clinical intelligence platforms, and value-based care technology solutions.

Cerner Corporation: Established healthcare information technology provider focused on digital clinical systems and integrated healthcare management solutions.

Key Competitive Intensity & Market Structure Drivers

The rapid adoption of telemedicine and virtual care platforms is significantly increasing competition among digital health providers to deliver seamless, scalable, and secure patient engagement experiences.

Artificial intelligence integration across diagnostics, predictive analytics, and clinical decision support systems is becoming a major competitive differentiator.

Healthcare interoperability and secure data exchange capabilities are increasingly important as healthcare systems demand integrated digital ecosystems across providers, insurers, and patients.

The growing adoption of wearable health devices and remote patient monitoring systems is intensifying competition between consumer technology firms and traditional medical device manufacturers.

Regulatory compliance, cybersecurity protection, and patient data privacy capabilities are becoming critical competitive requirements across global healthcare markets.

Strategic Implications of Competitive Intensity & Market Structure

Companies are increasingly investing in AI-powered diagnostics, predictive health analytics, and cloud-native healthcare platforms to improve scalability and clinical efficiency.

Strategic collaborations between healthcare providers, insurers, pharmaceutical companies, and technology firms are becoming essential for developing integrated patient-centric care ecosystems.

Platform interoperability and open healthcare data architecture are emerging as key strategic priorities to enable seamless information exchange across digital healthcare systems.

Mergers and acquisitions are accelerating as larger healthcare technology firms seek to strengthen capabilities in telehealth, digital therapeutics, wearable integration, and remote monitoring.

Personalized medicine, digital therapeutics, and value-based care platforms are becoming increasingly important strategic focus areas for long-term market leadership.

Global Digital Health Market Competitive Intensity & Market Structure Forward Outlook

The global digital health market is expected to remain highly innovation-intensive as healthcare systems increasingly prioritize connected care delivery, patient-centric solutions, and data-driven clinical decision-making.

Future competition is likely to intensify around AI-driven personalized healthcare, virtual hospitals, interoperable health ecosystems, digital therapeutics, and real-time predictive clinical intelligence platforms.

The integration of 5G, IoT-enabled health monitoring, blockchain-secured medical records, and edge-based healthcare analytics is expected to significantly reshape market dynamics.

North America is expected to maintain technological leadership, while Asia-Pacific will witness the fastest expansion driven by healthcare digitization initiatives and rising digital health accessibility.

Overall, organizations that successfully combine advanced healthcare analytics, secure interoperable platforms, regulatory compliance, and patient-centric digital innovation will remain strongly positioned in the evolving global digital health market.

Value Chain

Global Digital Health Market Value Chain & Supply Chain Evolution Overview

The global digital health market value chain is undergoing a profound transformation as healthcare systems worldwide increasingly transition toward connected, data-driven, patient-centric digital care ecosystems. Rapid advancements in telemedicine, wearable medical technologies, artificial intelligence (AI), cloud computing, Internet of Things (IoT)-enabled health monitoring, and digital therapeutics are reshaping healthcare delivery models across hospitals, clinics, payers, pharmaceutical companies, and home-care environments. Digital health is no longer viewed as a supplementary technology layer but as a core strategic enabler of modern healthcare infrastructure.

The digital health value chain encompasses software platform development, connected device manufacturing, cloud infrastructure integration, healthcare data management, cybersecurity systems, AI-enabled analytics, clinical workflow automation, interoperability frameworks, implementation services, and downstream patient care delivery applications. These interconnected layers enable digital health solutions to support telemedicine consultations, remote patient monitoring, predictive diagnostics, electronic health records (EHR), personalized care management, and intelligent clinical decision support systems.

The market ecosystem includes software developers, cloud service providers, medical device manufacturers, healthcare IT vendors, cybersecurity firms, systems integrators, telecom operators, hospitals, insurers, pharmaceutical companies, and digital care service providers. Leading companies including Teladoc Health, Philips Healthcare, Oracle Health, GE HealthCare, Siemens Healthineers, Epic Systems, Medtronic, Apple, Veradigm, and Cerner are investing heavily in AI-powered care platforms, cloud-native health systems, wearable integrations, and interoperable digital care ecosystems to strengthen their competitive positioning.

Upstream value chain activities increasingly rely on semiconductor suppliers, sensor manufacturers, cloud computing infrastructure, cybersecurity architecture, software engineering capabilities, AI training models, and healthcare data interoperability standards. Midstream operations focus on platform integration, software deployment, compliance validation, clinical workflow customization, API interoperability, and health data processing. Downstream applications span telehealth delivery, chronic disease management, hospital automation, remote diagnostics, preventive healthcare, personalized therapeutics, and patient engagement platforms.

Operational priorities across the digital health value chain increasingly emphasize scalability, data security, interoperability, AI integration, patient privacy compliance, user-centric design, and clinical reliability. However, the market continues to face challenges related to regulatory complexity, fragmented health data systems, cybersecurity vulnerabilities, reimbursement limitations, interoperability gaps, clinician adoption barriers, and infrastructure disparities across emerging healthcare systems.

Global Digital Health Market Value Chain & Supply Chain Evolution Current Scenario

The current digital health market is being shaped by accelerated healthcare digitization, rising demand for virtual care, increasing chronic disease prevalence, and growing investments in connected healthcare infrastructure. Healthcare organizations are replacing fragmented legacy systems with integrated digital platforms capable of delivering real-time patient monitoring, remote diagnostics, centralized clinical records, and AI-assisted decision-making.

North America currently leads the global digital health ecosystem due to advanced healthcare IT infrastructure, favorable reimbursement policies, strong venture capital investment, and rapid telehealth adoption. The United States remains the largest digital health market globally, driven by widespread deployment of virtual care platforms, AI-enabled clinical analytics, and hospital digital transformation initiatives.

Europe is experiencing strong growth through government-supported healthcare digitization strategies, interoperability regulations, aging population management programs, and expanding digital therapeutics adoption. Asia-Pacific is emerging as the fastest-growing regional market due to expanding smartphone penetration, healthcare accessibility initiatives, telemedicine deployment, and growing investments in AI-driven healthcare technologies.

Cloud-native digital health platforms are increasingly dominating new deployments due to their flexibility, scalability, remote accessibility, and cost efficiency advantages. Simultaneously, healthcare organizations are increasing investments in cybersecurity systems, blockchain-enabled medical record security, zero-trust architecture, and advanced patient data governance frameworks to address growing digital security risks.

Healthcare providers are increasingly demanding interoperable digital ecosystems capable of integrating EHR systems, remote monitoring devices, telehealth platforms, pharmacy systems, laboratory diagnostics, imaging systems, and payer platforms into unified care environments. This demand is accelerating partnerships between technology providers, healthcare institutions, telecom operators, and cloud service vendors.

Key Value Chain & Supply Chain Evolution Signals in Global Digital Health Market

One of the most significant transformation signals is the rapid expansion of virtual healthcare delivery models. Telemedicine and remote patient monitoring are becoming standard components of healthcare systems, enabling providers to improve accessibility, reduce operational costs, and deliver care beyond traditional clinical settings.

Another critical signal is the increasing integration of artificial intelligence across digital health platforms. AI-powered diagnostics, predictive analytics, automated clinical documentation, intelligent triage systems, and decision-support tools are significantly enhancing healthcare efficiency, diagnostic accuracy, and personalized treatment planning.

The rapid growth of wearable health technologies is also reshaping the value chain by generating continuous real-time patient health data. Smartwatches, biosensors, connected monitoring devices, and wearable medical platforms are enabling preventive care, chronic disease management, and early intervention strategies.

Interoperability is emerging as a major strategic priority across healthcare ecosystems. The increasing adoption of open APIs, FHIR-based standards, cloud interoperability frameworks, and connected health data exchange systems is enabling seamless information sharing across providers, payers, and patients.

Cybersecurity and privacy compliance are becoming defining value chain signals as healthcare data volumes grow rapidly. Digital health providers are investing heavily in encryption systems, AI-driven threat detection, secure cloud environments, and regulatory compliance infrastructure to protect sensitive patient information and maintain operational trust.

The growing convergence of healthcare delivery, consumer technology, pharmaceutical innovation, and digital therapeutics is also driving ecosystem integration, enabling highly personalized and data-driven healthcare experiences.

Strategic Implications of Value Chain & Supply Chain Evolution in Global Digital Health Market

Leading digital health providers are increasingly focusing on AI-driven platform innovation, cloud-native infrastructure development, ecosystem interoperability, and strategic healthcare partnerships to strengthen market positioning. Competitive differentiation increasingly depends on the ability to deliver secure, scalable, clinically validated, and patient-centric digital health ecosystems.

Companies capable of integrating AI diagnostics, predictive analytics, wearable device connectivity, remote care automation, and seamless interoperability with healthcare provider systems are expected to capture premium growth opportunities as healthcare digitization accelerates globally.

Strategic collaborations between healthcare providers, insurers, telecom operators, cloud providers, medical device companies, and pharmaceutical firms are becoming critical for expanding care delivery capabilities, improving patient engagement, and strengthening healthcare ecosystem integration.

Regulatory compliance and cybersecurity resilience are becoming central strategic differentiators. Organizations investing in HIPAA-compliant cloud architecture, advanced privacy protection systems, secure health data exchange, and audit-ready digital governance frameworks are expected to strengthen long-term competitive positioning.

Patient-centric innovation is also emerging as a key strategic focus area. Digital health companies are prioritizing intuitive interfaces, personalized health recommendations, digital therapeutics, remote care accessibility, and user engagement optimization to improve adoption and retention across patient populations.

As reimbursement models evolve, companies capable of demonstrating measurable clinical outcomes, cost efficiency, and evidence-based care improvements will be better positioned to scale partnerships with healthcare systems and insurers.

Global Digital Health Market Value Chain & Supply Chain Evolution Forward Outlook

Between 2026 and 2033, the digital health value chain is expected to become increasingly intelligent, interoperable, decentralized, and deeply integrated into mainstream healthcare delivery systems. AI-powered care ecosystems, predictive health analytics, personalized digital therapeutics, and connected virtual hospitals are expected to redefine future healthcare infrastructure.

Cloud-native digital health platforms will continue to dominate future deployments as healthcare providers prioritize scalable infrastructure, cross-platform accessibility, centralized data governance, and real-time clinical collaboration. Edge computing and 5G connectivity are expected to further improve remote diagnostics, real-time monitoring, and connected care responsiveness.

Advanced AI models, natural language processing systems, autonomous clinical assistants, and machine-learning-driven decision support tools will increasingly automate administrative workflows, diagnostic interpretation, patient triage, and personalized treatment optimization.

Wearable devices and IoT-enabled health ecosystems will evolve toward continuous, proactive, and predictive health monitoring. Real-time biometric data streams will support early disease detection, personalized interventions, and preventive care models across diverse patient populations.

Blockchain-enabled health data exchange, decentralized patient identity systems, and privacy-preserving interoperability frameworks are expected to strengthen healthcare security and patient data ownership across digital ecosystems.

Sustainability and healthcare equity will become increasingly important priorities. Digital health providers will focus on improving healthcare accessibility in underserved regions, reducing healthcare infrastructure burdens, and expanding low-cost digital care delivery models.

Ultimately, the future digital health value chain will evolve into a fully integrated intelligent healthcare ecosystem capable of delivering predictive, personalized, accessible, and highly efficient healthcare services across global populations.

Market-Specific Value Chain

- Technology Infrastructure & Core Development: Cloud computing platforms, semiconductor manufacturing, software engineering, AI model development, cybersecurity frameworks, telecom connectivity, and healthcare data architecture.

- Digital Health Platform & Device Development: Telemedicine software, EHR systems, wearable medical device manufacturing, remote monitoring systems, mobile health applications, and AI healthcare solution development.

- System Integration & Clinical Deployment: Healthcare IT integration, interoperability implementation, workflow customization, compliance validation, deployment services, staff training, and clinical onboarding support.

- Healthcare Delivery & Patient Engagement: Telehealth services, virtual consultations, remote patient monitoring, digital therapeutics delivery, chronic disease management, and connected patient care services.

- Data Analytics & Clinical Intelligence: Predictive analytics, AI diagnostics, population health analytics, decision support systems, personalized treatment recommendations, and real-time health monitoring intelligence.

- Long-Term Ecosystem Optimization: Preventive care automation, decentralized health data systems, digital therapeutics expansion, healthcare accessibility optimization, and continuous digital care ecosystem enhancement.

Company-to-Stage Mapping

- Technology Infrastructure & Core Development: Microsoft Azure, Amazon Web Services (AWS), Google Cloud, NVIDIA, cybersecurity solution providers.

- Digital Health Platform & Device Development: Teladoc Health, Apple Inc., Philips Healthcare, Medtronic, Siemens Healthineers, Oracle Health.

- System Integration & Clinical Deployment: Epic Systems, Cerner Corporation, Accenture, Deloitte, IBM Consulting, healthcare systems integrators.

- Healthcare Delivery & Patient Engagement: Hospitals, healthcare providers, telehealth networks, insurance providers, virtual care service companies.

- Data Analytics & Clinical Intelligence: GE HealthCare, Veradigm, AI healthcare analytics companies, predictive diagnostics solution providers.

- Long-Term Ecosystem Optimization: Digital therapeutics companies, blockchain health platform developers, connected healthcare ecosystem innovators, personalized medicine technology providers.

Investment Activity

Global Digital Health Market Investment & Funding Dynamics Overview

Investment activity in the global digital health market is accelerating rapidly due to increasing healthcare digitization, rising adoption of telemedicine, growing demand for remote patient monitoring, and expanding integration of artificial intelligence across healthcare systems. Between 2026 and 2033, funding is expected to increasingly focus on AI-powered diagnostics, virtual care platforms, wearable health technologies, interoperable healthcare data systems, and cloud-native digital health infrastructure.

The digital health market has evolved into one of the most attractive investment segments within the global healthcare technology ecosystem. Healthcare providers, technology companies, venture capital firms, private equity investors, insurers, and governments are significantly increasing investments to modernize healthcare delivery and improve patient outcomes through connected digital solutions.

A major transformation shaping investment dynamics is the transition from traditional hospital-centric care models toward decentralized, patient-centric, and data-driven healthcare delivery systems. This shift is accelerating investments into telehealth platforms, digital therapeutics, remote monitoring technologies, predictive analytics systems, and personalized healthcare solutions.

The market is also benefiting from increased funding for AI-assisted diagnostics, blockchain-secured health records, clinical workflow automation, wearable biosensors, and integrated healthcare analytics platforms. Rising healthcare cost pressures and increasing demand for scalable healthcare access are further strengthening long-term investment opportunities.

Current Investment & Funding Landscape

Current funding activity in the digital health market is strongly supported by large-scale healthcare digital transformation initiatives, increasing telehealth platform expansion, rapid wearable device innovation, and rising strategic partnerships between healthcare providers and technology companies. Organizations are actively investing in digital infrastructure modernization, cybersecurity frameworks, AI clinical support systems, and patient engagement platforms.

- North America: Dominates global investment activity due to advanced healthcare IT infrastructure, strong venture capital presence, high digital adoption rates, and extensive telehealth deployment across the United States and Canada.

- Europe: Witnessing strong funding growth supported by national healthcare digitization strategies, aging populations, and regulatory support for interoperable health systems.

- Asia-Pacific: Emerging as the fastest-growing investment region due to rising smartphone penetration, expanding digital healthcare access, increasing chronic disease burden, and strong government-backed digital health initiatives.

- Middle East & Latin America: Attracting growing investments through healthcare modernization programs, smart hospital development, and telemedicine infrastructure expansion.

Key Investment & Funding Drivers

- Rapid telemedicine adoption is increasing investments in scalable virtual care platforms and remote consultation infrastructure.

- Growing prevalence of chronic diseases is driving funding for remote patient monitoring and digital disease management systems.

- AI integration in diagnostics and clinical decision support is attracting substantial technology-focused investment.

- Wearable health device innovation is supporting investments in connected monitoring ecosystems and biosensor technologies.

- Government healthcare digitization programs are accelerating public and private capital deployment into health IT infrastructure.

- Rising demand for healthcare interoperability is increasing investments in cloud-based health data exchange platforms.

- Expansion of personalized medicine is creating funding opportunities for predictive analytics and digital therapeutics platforms.

Strategic Investment Implications

- The investment landscape increasingly favors companies capable of combining AI, secure data management, and scalable patient engagement solutions.

- Interoperability, regulatory compliance, and healthcare cybersecurity are becoming major competitive differentiators for investors.

- Strategic collaborations between hospitals, insurers, technology providers, and pharmaceutical companies are becoming critical to platform scalability.

- Regional diversification strategies are strengthening as digital health adoption accelerates across emerging healthcare systems.

- Organizations investing in integrated digital care ecosystems are expected to achieve stronger long-term competitive positioning.

- Patient-centric innovation and value-based care models are increasingly shaping capital allocation decisions.

- Companies with strong clinical validation, regulatory alignment, and scalable healthcare infrastructure are expected to attract stronger investment confidence.

Forward Investment Outlook

The global digital health market is expected to maintain exceptionally strong long-term investment momentum due to increasing healthcare digital transformation, rising demand for remote and personalized care, and rapid advancement of healthcare AI technologies.

Future funding activity is expected to prioritize virtual hospitals, AI-driven personalized medicine platforms, blockchain-enabled medical record systems, interoperable digital ecosystems, next-generation remote monitoring solutions, and predictive healthcare analytics infrastructure.

- North America: Will remain the leading investment hub due to healthcare technology innovation and continued expansion of digital care delivery systems.

- Asia-Pacific: Will strengthen its position through large-scale healthcare digitization and mobile-first digital health adoption.

- Europe: Will focus on secure interoperability frameworks, public health digitization, and integrated care ecosystems.

Future innovation investments are also expected across AI-assisted clinical automation, 5G-enabled healthcare delivery, digital therapeutics, smart wearable diagnostics, and autonomous health management platforms.

The convergence of AI, IoT, cloud computing, and advanced analytics will continue reshaping investment priorities and competitive dynamics across the digital health ecosystem.

Overall, the market is expected to remain one of the most attractive long-term healthcare technology investment opportunities as digital solutions become central to global healthcare delivery transformation.

Technology & Innovation

Global Digital Health Market Technology & Innovation Landscape Overview

The global digital health market is experiencing rapid technological transformation driven by artificial intelligence, cloud computing, Internet of Things (IoT), advanced analytics, and connected healthcare ecosystems. Innovation across the market is focused on improving healthcare accessibility, enabling personalized treatment, enhancing clinical decision-making, and optimizing operational efficiency across hospitals, clinics, and remote care environments.

Digital health technologies are increasingly integrating real-time patient monitoring, predictive analytics, wearable biosensors, virtual care platforms, and intelligent automation systems to create more connected, proactive, and patient-centric healthcare delivery models. These innovations are significantly improving disease prevention, diagnosis accuracy, treatment optimization, and long-term patient engagement.

The market is also witnessing accelerated adoption of cloud-native health platforms, interoperable electronic health records, AI-powered diagnostics, blockchain-based health data security systems, and mobile health applications that support continuous healthcare access and digital clinical workflows.

Global Digital Health Market Technology & Innovation Current Scenario

Currently, digital health innovation is centered around virtual care ecosystems, remote patient monitoring, AI-assisted diagnostics, and connected wearable technologies. Healthcare providers are increasingly adopting telemedicine platforms that support secure video consultations, digital triage systems, remote prescriptions, and integrated patient engagement tools.

Artificial intelligence is playing a transformative role across healthcare systems. AI-driven algorithms are being deployed for disease prediction, diagnostic imaging analysis, clinical decision support, personalized treatment planning, and operational workflow automation.

Wearable health technologies such as smartwatches, biosensors, ECG monitoring devices, and continuous glucose monitoring systems are generating real-time health data that enable early intervention and proactive disease management.

Cloud computing is becoming a critical foundation for scalable digital health ecosystems, enabling secure storage of medical records, interoperability across care networks, and rapid deployment of healthcare applications.

Blockchain technology is gaining momentum as a secure infrastructure for managing patient records, improving healthcare data integrity, enabling secure data sharing, and strengthening compliance with healthcare privacy regulations.

The rise of digital therapeutics is also transforming chronic disease management through software-based clinical interventions for conditions such as diabetes, mental health disorders, cardiovascular disease, and respiratory illnesses.

Key Technology & Innovation Trends in Global Digital Health Market

- AI-Powered Diagnostics: Machine learning algorithms enabling faster and more accurate disease detection and clinical decision support.

- Remote Patient Monitoring: Connected monitoring systems enabling continuous tracking of patient health outside traditional clinical settings.

- Wearable Health Devices: Smart biosensors and connected wearables providing real-time physiological health data.

- Cloud-Based Healthcare Platforms: Scalable digital infrastructure supporting interoperability, secure medical record management, and virtual care delivery.

- Telemedicine & Virtual Care: Advanced digital consultation platforms improving healthcare accessibility and reducing treatment delays.

- Digital Therapeutics: Software-driven treatment solutions supporting chronic disease management and behavioral health interventions.

- Blockchain Health Data Security: Decentralized systems improving patient data security, transparency, and trusted healthcare information exchange.

- Predictive Healthcare Analytics: Data-driven forecasting tools supporting early diagnosis and preventive healthcare interventions.

- IoT-Enabled Smart Healthcare: Connected medical devices and hospital infrastructure improving operational intelligence and care coordination.

- Personalized Digital Medicine: Data-driven treatment models tailored to individual patient health profiles and genomic insights.

Strategic Implications of Technology & Innovation

Technological innovation is fundamentally reshaping healthcare delivery by shifting systems from reactive treatment models toward predictive, preventive, and personalized care ecosystems. Healthcare organizations adopting advanced digital health technologies are improving clinical outcomes, operational efficiency, and patient engagement.

AI-driven diagnostics and predictive analytics are reducing diagnostic errors, accelerating treatment decisions, and enabling earlier disease detection. This is creating significant opportunities for healthcare providers to improve quality of care while lowering long-term treatment costs.

The expansion of wearable technologies and remote monitoring solutions is enabling decentralized care delivery, reducing hospital readmissions, and supporting long-term chronic disease management.

Interoperability and secure data management are becoming critical strategic priorities as healthcare systems increasingly rely on integrated digital platforms for cross-provider collaboration and patient information exchange.

At the same time, cybersecurity risks, regulatory compliance complexity, data privacy concerns, and integration challenges remain important barriers that technology providers must address to ensure widespread adoption.

Global Digital Health Market Technology & Innovation Forward Outlook

Looking ahead, the digital health market is expected to evolve toward fully interconnected, AI-driven, and highly personalized healthcare ecosystems capable of delivering predictive and precision-based medical care.

Future innovation will focus on virtual hospitals, autonomous clinical decision support systems, AI-assisted robotic healthcare, digital twins for patient simulation, and advanced genomics-driven treatment platforms.

5G-enabled connected healthcare infrastructure will significantly enhance real-time telemedicine, wearable device performance, and remote surgical support capabilities.

Integration of augmented reality (AR) and virtual reality (VR) technologies is expected to expand applications in medical training, rehabilitation therapy, remote diagnostics, and mental health treatment.

Advanced interoperability frameworks and global health data exchange ecosystems will further strengthen collaborative care delivery and accelerate digital health scalability.

Overall, the technology and innovation landscape of the global digital health market is evolving toward intelligent, secure, data-centric, and patient-focused healthcare ecosystems that will redefine global healthcare delivery over the coming decade.

Market Risk

Global Digital Health Market Risk Factors & Disruption Threats Overview

The global digital health market is experiencing accelerated expansion driven by rapid healthcare digitization, increasing telemedicine adoption, wearable health device penetration, and growing integration of artificial intelligence across healthcare systems. Despite strong long-term growth potential, the market faces several critical risks including cybersecurity vulnerabilities, regulatory complexity, data privacy concerns, interoperability challenges, reimbursement uncertainty, and technological disruption.

One of the most significant disruption threats affecting the digital health market is the growing risk of cybersecurity breaches and healthcare data attacks. Digital health platforms process highly sensitive patient information, making them prime targets for ransomware, data theft, unauthorized access, and system breaches. Cyberattacks can disrupt patient care delivery, damage trust, trigger regulatory penalties, and significantly impact operational continuity.

Regulatory and compliance complexity also represents a major challenge for market participants. Digital health solutions must comply with strict healthcare regulations related to patient data protection, medical device approvals, software validation, and telemedicine licensing. Regulatory variations across countries create barriers to market expansion and increase compliance costs.

Interoperability remains another major risk factor. Healthcare systems often operate on fragmented legacy IT infrastructure, making seamless integration between digital platforms, electronic health records, wearable devices, and clinical systems difficult. Limited interoperability can reduce solution effectiveness and hinder large-scale adoption.

The market is also exposed to reimbursement uncertainty. Many digital health solutions rely on insurance reimbursement policies and healthcare funding support. Changes in telehealth reimbursement frameworks, insurance coverage limitations, or healthcare budget constraints could negatively affect adoption rates.

Rapid technological change presents additional disruption risks. Continuous innovation in AI diagnostics, remote monitoring technologies, wearable devices, and cloud healthcare platforms requires ongoing investment. Companies unable to adapt to rapidly evolving healthcare technology standards may lose competitiveness.

In addition, growing patient concerns regarding data privacy, algorithmic bias, digital accessibility, and over-reliance on automated decision-making may impact trust and adoption of digital health platforms.

Global Digital Health Market Risk Factors & Disruption Threats Current Scenario

The current digital health market environment reflects strong momentum as healthcare providers increasingly adopt telemedicine, remote monitoring systems, AI-driven diagnostics, and connected patient care solutions.

Healthcare systems worldwide are investing heavily in digital transformation initiatives to improve efficiency, reduce costs, expand healthcare access, and enhance clinical decision-making. Governments are actively promoting electronic health records, virtual care frameworks, and healthcare interoperability standards.

The widespread use of wearable health devices and mobile health applications is generating unprecedented volumes of health-related data. While this creates strong opportunities for predictive healthcare analytics, it also increases exposure to privacy risks and data governance challenges.

Artificial intelligence is becoming increasingly integrated into diagnostics, imaging analysis, patient monitoring, and treatment planning. However, concerns regarding algorithm transparency, clinical validation, and regulatory oversight remain significant.

At the same time, healthcare organizations continue to face challenges in integrating digital solutions with existing infrastructure, managing clinician adoption, and ensuring equitable access to digital care services across underserved populations.

Global Digital Health Market Key Risk Factors & Disruption Threat Signals

- Cybersecurity Threats: Rising risks of ransomware, data breaches, unauthorized access, and healthcare system cyberattacks.

- Regulatory Compliance Complexity: Strict and evolving regulations related to patient privacy, medical software approvals, and telemedicine licensing.

- Data Privacy Concerns: Growing patient sensitivity regarding personal health data collection, storage, and sharing practices.

- Interoperability Challenges: Difficulty integrating digital platforms with fragmented healthcare IT systems and legacy infrastructure.

- Reimbursement Uncertainty: Changing insurance policies and telehealth reimbursement frameworks affecting adoption.

- Rapid Technological Obsolescence: Continuous innovation requiring substantial ongoing investment in platform upgrades.

- Algorithm Bias & Clinical Validation Risks: Potential inaccuracies or biases in AI-powered diagnostic tools.

- Digital Accessibility Gaps: Unequal access to digital healthcare technologies across regions and patient populations.

- High Implementation Costs: Significant infrastructure and integration investments required for large-scale deployment.

- User Adoption Resistance: Hesitation among clinicians and patients to fully embrace digital healthcare workflows.

Strategic Implications of Risk Factors

Digital health companies must prioritize robust cybersecurity frameworks, encryption protocols, and real-time threat detection systems to protect patient data and maintain trust.

Organizations should focus on developing interoperable, standards-based solutions capable of seamless integration with diverse healthcare IT systems and electronic health record platforms.

Regulatory expertise and proactive compliance strategies will become increasingly essential for expanding across global healthcare markets and maintaining operational resilience.

Companies must invest heavily in clinical validation, algorithm transparency, and evidence-based product development to strengthen credibility and support regulatory approval.

Strategic partnerships with healthcare providers, insurers, technology firms, and government agencies will remain critical for reimbursement support, infrastructure integration, and large-scale deployment.

Global Digital Health Market Forward Risk Outlook

Looking ahead to 2026–2033, the digital health market is expected to remain one of the fastest-growing healthcare technology sectors, driven by virtual care expansion, AI-enabled clinical intelligence, connected health ecosystems, and personalized medicine.

Future market evolution will be shaped by advanced predictive analytics, virtual hospitals, digital therapeutics, interoperable healthcare ecosystems, and 5G-enabled real-time remote care capabilities.

However, cybersecurity risks, regulatory scrutiny, reimbursement uncertainties, and data governance challenges are expected to remain major strategic concerns for market participants.

The growing convergence of healthcare, AI, cloud computing, and wearable technologies will create both significant growth opportunities and heightened operational complexity.

Overall, while the global digital health market offers exceptional long-term growth potential, sustained competitiveness will depend on cybersecurity resilience, regulatory adaptability, interoperability capabilities, patient trust, and continuous technological innovation.

Regulatory Landscape

Global Digital Health Market Regulatory & Policy Environment Overview

The regulatory and policy environment governing the global digital health market is shaped by healthcare data privacy laws, medical device regulations, telemedicine policies, cybersecurity standards, interoperability mandates, and digital healthcare reimbursement frameworks. As digital health technologies increasingly integrate into clinical care delivery, regulatory oversight is expanding to ensure patient safety, data security, system reliability, and ethical use of emerging technologies such as artificial intelligence.

Digital health solutions including telemedicine platforms, wearable devices, remote patient monitoring systems, AI-based diagnostics, digital therapeutics, and electronic health record (EHR) systems are subject to varying levels of regulatory scrutiny depending on their intended clinical use and impact on patient care decisions.

Governments and healthcare regulators worldwide are actively modernizing policy frameworks to accelerate digital healthcare adoption while maintaining compliance with clinical standards, privacy protection, cybersecurity requirements, and medical device safety regulations.

At the same time, policy initiatives focused on healthcare digitization, universal healthcare access, reimbursement reform, and interoperability are creating strong regulatory support for digital health innovation and infrastructure development globally.

Global Digital Health Market Regulatory & Policy Environment Current Scenario

The current regulatory landscape for digital health is characterized by rapidly evolving frameworks that seek to balance innovation with patient safety, privacy, and healthcare system integrity. Regulatory agencies are increasingly establishing digital-specific guidance for software as a medical device (SaMD), AI-enabled diagnostics, remote monitoring platforms, and digital therapeutics.

In the United States, digital health solutions are regulated through the Food and Drug Administration (FDA), the Health Insurance Portability and Accountability Act (HIPAA), and Centers for Medicare & Medicaid Services (CMS) reimbursement policies. The FDA’s Digital Health Center of Excellence is actively guiding regulation of AI-powered healthcare software, connected devices, and digital therapeutic platforms.

In Europe, digital health solutions must comply with the Medical Device Regulation (MDR), General Data Protection Regulation (GDPR), and the European Health Data Space (EHDS) initiatives. The European Union is also strengthening interoperability requirements and advancing policy support for cross-border digital healthcare services.

Asia-Pacific countries including China, India, Japan, South Korea, and Australia are rapidly strengthening digital health governance through telemedicine regulations, data localization requirements, healthcare IT standards, and digital public health initiatives. National digital health missions and smart healthcare infrastructure investments are accelerating regulatory development across the region.

Latin America and the Middle East & Africa are progressively introducing telehealth licensing frameworks, electronic health data regulations, and healthcare digitization strategies to improve access and modernize healthcare systems.

Key Regulatory & Policy Environment Signals in Global Digital Health Market

- Healthcare Data Privacy Regulations: Strict patient data protection laws govern digital health platforms, health record storage, data sharing, and patient consent management.

- Software as a Medical Device (SaMD) Regulation: AI-powered healthcare software and clinical decision tools are increasingly subject to medical device approval frameworks.

- Telemedicine Licensing and Practice Standards: Governments are formalizing regulations for remote consultations, practitioner licensing, and cross-border digital healthcare delivery.

- Cybersecurity Compliance Requirements: Healthcare organizations must comply with robust cybersecurity standards to protect sensitive patient data and digital infrastructure.

- Interoperability and Health Data Exchange Policies: Regulatory frameworks increasingly promote seamless exchange of health data across providers, systems, and digital platforms.

- Digital Health Reimbursement Policies: Expanding reimbursement frameworks for telehealth, remote monitoring, and digital therapeutics are improving commercial adoption.

- AI Ethics and Algorithm Transparency Standards: Regulators are focusing on explainability, bias mitigation, and clinical accountability for AI-enabled healthcare applications.

Strategic Implications of Regulatory & Policy Environment

The evolving regulatory environment is significantly influencing product development, market entry strategies, and operational models across the digital health ecosystem. Companies must increasingly prioritize regulatory compliance, privacy-by-design architecture, cybersecurity resilience, and clinical validation to achieve market approval and adoption.

Data privacy and cybersecurity requirements are driving significant investment in secure cloud infrastructure, encryption technologies, access controls, and regulatory audit readiness across digital health platforms.

The expansion of telehealth reimbursement policies and supportive healthcare digitization programs is improving commercialization opportunities for virtual care providers, remote monitoring companies, and digital therapeutics developers.

Interoperability mandates are encouraging stronger collaboration between healthcare providers, technology vendors, and health information exchanges to create integrated digital health ecosystems.

Regulatory scrutiny around AI-based healthcare tools is also encouraging companies to invest in transparent algorithm design, clinical evidence generation, and explainable AI capabilities to build trust and accelerate regulatory approvals.

Global Digital Health Market Regulatory & Policy Environment Forward Outlook

Between 2026 and 2033, the regulatory environment for the global digital health market is expected to become more structured, globally harmonized, and technology-specific. Regulatory agencies are likely to introduce clearer pathways for approval and oversight of AI diagnostics, digital therapeutics, remote monitoring systems, and autonomous healthcare decision-support tools.

Healthcare data interoperability frameworks and digital identity initiatives are expected to expand significantly, enabling more connected and patient-centric healthcare ecosystems.

Cybersecurity requirements will become increasingly stringent as healthcare systems face growing digital threats, driving stronger compliance obligations for software developers and healthcare organizations.

AI governance frameworks will continue to evolve, with increased focus on algorithm accountability, bias detection, transparency standards, and post-market surveillance of digital health applications.

Government investment in public digital health infrastructure, smart hospitals, telehealth reimbursement modernization, and universal healthcare digitization initiatives will further strengthen market growth opportunities.

Overall, the regulatory and policy environment will remain a defining force in the evolution of the digital health market, with organizations investing in secure, compliant, interoperable, and clinically validated digital health solutions expected to maintain strong long-term competitive advantages.