Global Eco-Friendly Medical Device Packaging Market size and share Analysis 2026-2033

Global Eco-Friendly Medical Device Packaging Market size & Forecast

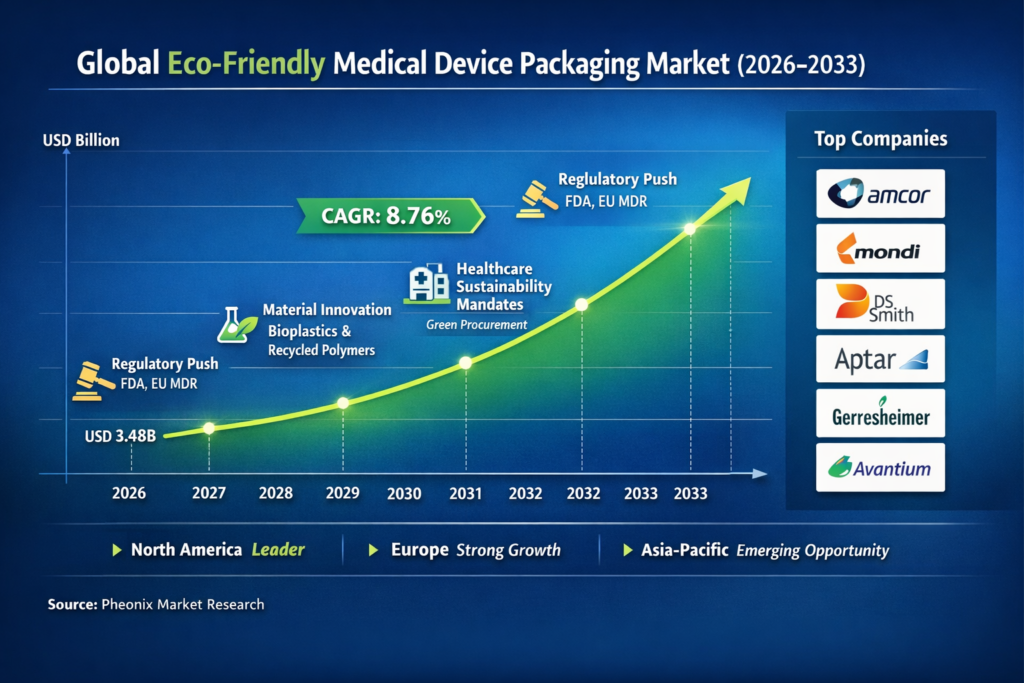

The Eco-Friendly Medical Device Packaging market is poised for significant growth over the forecast period from 2026 to 2033. Starting with a base year market size of USD 3.20 billion in 2025, this market is expected to more than double, reaching approximately USD 6.26 billion by the end of 2033. This growth trajectory is driven by a forecasted compound annual growth rate (CAGR) of 8.76%. The burgeoning demand for sustainability across industries, coupled with stringent regulatory frameworks, is increasingly compelling the medical device sector to adopt eco-friendly packaging solutions. This forecast captures not only the growing environmental consciousness but also the industry’s response to regulatory pressures and technological advancements that facilitate sustainable practices.

Several factors underpin this robust market expansion. Firstly, the global push towards reducing carbon footprints and minimizing environmental impacts is driving healthcare providers and manufacturers to re-evaluate their packaging choices. With regulations tightening around single-use plastics and waste management, the industry is compelled to innovate rapidly and adopt sustainable packaging solutions that meet compliance requirements while also aligning with consumer and stakeholder expectations.

The increased adoption of eco-friendly packaging is also a response to the healthcare sector’s growing emphasis on sustainability as a compliance imperative. Regulatory bodies such as the FDA and European counterparts are implementing stricter guidelines to ensure that healthcare packaging meets environmental standards. These regulations are not only shaping the packaging strategies of medical device manufacturers but are also influencing the procurement policies of healthcare facilities, driving the overall market growth.

Global Eco-Friendly Medical Device Packaging market Overview

The Eco-Friendly Medical Device Packaging market is characterized by a complex interplay of regulatory, technological, and consumer-driven factors. The market is witnessing a significant shift as healthcare providers, manufacturers, and consumers increasingly prioritize sustainability in their operations and purchasing decisions. This shift is reflected in the heightened demand for biodegradable, recyclable, and reusable packaging solutions within the medical device sector.

Technological innovation plays a critical role in this market transformation. Advancements in biopolymers and sustainable material technologies are enabling the development of eco-friendly packaging solutions that do not compromise on safety or efficacy. These innovations are crucial in accelerating the transition from traditional materials to more sustainable alternatives. Moreover, the integration of artificial intelligence and data analytics is optimizing supply chains and reducing environmental impact by enhancing material traceability and improving recycling processes.

Moreover, the market is seeing an increasing trend towards the adoption of sustainable practices as a competitive advantage. Companies are leveraging eco-friendly packaging as a differentiator in a highly fragmented and competitive market. This is evident in the strategic partnerships and collaborations between major players and sustainable packaging innovators, which are helping to drive market growth and reshape industry dynamics.

Structural Drivers of Global Eco-Friendly Medical Device Packaging market Growth

Innovation and Commercialization Acceleration

One of the primary drivers of growth in the Eco-Friendly Medical Device Packaging market is the acceleration of innovation and commercialization. Technological maturity and strategic funding allocations are compressing the development-to-commercialization cycles, thereby expanding the addressable applications for eco-friendly packaging solutions. This acceleration is largely supported by government regulations aimed at reducing single-use plastics and promoting sustainable practices, which have catalyzed increased adoption of eco-friendly packaging in healthcare facilities. The rapid pace of innovation ensures that new, sustainable packaging solutions are developed and brought to market more efficiently, enhancing market adoption and expanding the customer base.

Compliance and Risk Repricing

Another critical driver is the compliance and risk repricing mechanism, which compels market participants to realign their product roadmaps and raise their execution standards. Regulatory tightening, particularly around environmental sustainability, is reshaping operating requirements for medical device manufacturers. Regulations such as Title 21 of the Code of Federal Regulations (CFR) and Regulation (EU) 2017/745 on medical devices are setting new benchmarks for sustainable packaging. As a result, companies are investing significantly in research and development for sustainable packaging solutions to comply with these stringent standards, which in turn drives market growth.

Competitive and Value-Chain Reconfiguration

The reconfiguration of competitive dynamics and value chains represents another significant driver of market growth. Competitive moves, such as strategic partnerships and mergers, are reallocating bargaining power and forcing companies to reposition their portfolios. For instance, partnerships like the one between Avantium N.V. and Amor Rigid Packaging USA, LLC for plant-based polymers demonstrate the strategic shifts towards sustainable materials. These competitive and value-chain shifts are changing where margin and growth concentrate, leading to a more dynamic and competitive market landscape.

Capital and Capacity Scaling

Finally, the scaling of capital and capacity is a crucial driver in the expansion of the Eco-Friendly Medical Device Packaging market. The allocation of capital into upgrading production capacities and processes is expanding throughput and reducing deployment friction. This enables faster scaling in high-demand segments of the market. Government regulations supporting sustainable practices and waste reduction are catalyzing investment into these scaling efforts, further driving market growth and adoption of eco-friendly packaging solutions.

Global Eco-Friendly Medical Device Packaging market Segmentation Analysis

The Eco-Friendly Medical Device Packaging market is segmented by end user, application, material type, and packaging technology. This segmentation allows for a comprehensive understanding of the market dynamics and helps identify key growth areas.

By End User

Healthcare facilities and medical device manufacturers are the primary end users driving market demand. Within healthcare facilities, hospital supply chains are increasingly implementing sustainable procurement programs, such as green hospital packaging initiatives and medical waste reduction programs. These initiatives are critical in driving the adoption of eco-friendly packaging solutions, as hospitals strive to reduce their environmental impact and comply with regulatory requirements.

By Application

The market is also segmented by application, with surgical devices packaging, diagnostic device packaging, and implantable device packaging being the major categories. Each of these applications has unique requirements for packaging materials and technologies, influencing the choice of eco-friendly solutions. For example, sterile surgical device packaging requires materials that ensure sterility while being environmentally sustainable. This has driven innovations in biodegradable and recyclable packaging materials that meet both safety and sustainability criteria.

By Material Type

Material type segmentation reveals a growing preference for bioplastics, recycled plastics, and paper-based packaging in the market. Bioplastics, such as PLA-based materials, are gaining traction due to their biodegradability and ability to meet regulatory standards for medical device packaging. Recycled plastics are also being adopted, with post-consumer recycled materials being used to develop sustainable thermoformed packaging solutions. Paper-based packaging, particularly medical-grade paper, is being used for sterile barrier applications, providing an eco-friendly alternative to traditional plastic-based packaging.

By Packaging Technology

Advances in packaging technology are further driving market segmentation. Technologies such as molded fiber technology, thermoforming, and flexible packaging are enabling the development of eco-friendly packaging solutions that meet the stringent requirements of the medical device industry. Molded fiber technology, for instance, is being used to create protective device packaging and sustainable transport packaging. Similarly, flexible packaging technology is being leveraged to develop recyclable and biodegradable packaging films, supporting the market’s shift towards sustainability.

In conclusion, the Eco-Friendly Medical Device Packaging market is evolving rapidly, driven by technological advancements, regulatory pressures, and shifting consumer preferences. The market's segmentation provides a detailed view of the diverse applications and material preferences that are shaping the future of sustainable medical device packaging.

Regional Global Eco-Friendly Medical Device Packaging market

Dynamics

North America

In North America, the market benefits from stringent regulatory frameworks and a strong emphasis on sustainability. The U.S. FDA's guidance on eco-friendly packaging and the growing awareness of environmental issues among consumers are driving demand. Furthermore, the presence of large healthcare facilities committed to reducing their carbon footprint further supports market growth in this region.

Europe

In Europe, the market is propelled by comprehensive regulatory mandates like the EU MDR (2017/745) and initiatives such as the European Green Deal, which aim to make Europe the first climate-neutral continent. European consumers' high environmental awareness and preference for sustainable products bolster market expansion. Countries like Germany, the UK, and France are at the forefront, driven by advanced healthcare infrastructure and progressive policies supporting sustainable practices.

Asia-Pacific

Asia-Pacific presents a mixed regional dynamic, with countries like Japan and South Korea leading in eco-friendly initiatives due to rigorous government regulations on waste reduction and sustainable development. However, other parts of the region face challenges due to varying levels of regulatory implementation and economic development. Nonetheless, the growing healthcare sector and increasing investments in sustainable technology present significant opportunities for market growth.

Latin America and Middle East & Africa

In contrast, the Latin American and Middle Eastern markets are in the nascent stages of adopting eco-friendly medical device packaging. These regions are gradually aligning with global sustainability trends, driven by increasing regulatory pressures and consumer demand for sustainable healthcare products. However, economic constraints and limited infrastructure for recycling and waste management remain challenges that could impact market growth.

Competitive Landscape

The competitive landscape of the Eco-Friendly Medical Device Packaging market is characterized by high intensity and fragmentation, with no Tier 1 players dominating the field. Instead, the market is populated by various small and medium-sized enterprises focusing on innovation and sustainability to gain a competitive edge. Companies such as Avantium N.V. and Amor Rigid Packaging USA, LLC are leveraging strategic partnerships to develop plant-based polymers, reflecting their commitment to eco-friendly solutions.

Larger corporations like Philips and GE are leveraging their technological capabilities to enhance sustainable packaging solutions, while also capitalizing on their established market presence and extensive distribution networks. These companies maintain a strategic advantage through their ability to adapt quickly to regulatory changes and consumer preferences, integrating sustainable practices into their operations.

Startups are also making significant inroads by attracting substantial venture capital investments and scaling rapidly through innovation. Investment from firms like Bain Capital and KKR Co. L.P. is fueling the growth of these startups, enabling them to explore new materials and technologies that support sustainability. This influx of capital is crucial in maintaining their competitive edge and ability to disrupt traditional market structures.

Overall, the market's competitive intensity is driven by the constant need for innovation, regulatory compliance, and the ability to meet evolving consumer expectations. Companies that can effectively navigate these dimensions are likely to sustain their market positions and capitalize on growth opportunities.

Strategic Outlook

Looking ahead, the strategic outlook for the Eco-Friendly Medical Device Packaging market is shaped by several key trends and factors. One major strategic focus is on innovation and commercialization acceleration, where companies are investing in research and development to bring new eco-friendly packaging solutions to market more swiftly. This trend is supported by increased funding allocation and technological maturity, which facilitate the rapid development and scaling of sustainable packaging materials.

Another strategic priority is compliance and risk repricing, as companies respond to regulatory tightening and evolving risk landscapes. Organizations are increasingly investing in compliance strategies to align with global regulatory standards, which in turn influences product development roadmaps and operational practices. The ability to anticipate regulatory changes and adapt swiftly is crucial for maintaining competitive advantage.

Furthermore, competitive and value-chain reconfiguration is reshaping the market dynamics. Companies are reevaluating their portfolios and supply chains to secure a stronger position in the market. Strategic partnerships and collaborations are common strategies employed to enhance bargaining power and optimize value chain efficiencies.

Lastly, capital and capacity scaling remains a critical focus. Companies are deploying capital to upgrade processes and expand production capacity to meet the growing demand for eco-friendly medical device packaging. This strategic move is expected to lower deployment friction and enable companies to capture market share in high-demand segments.

Final Global Eco-Friendly Medical Device Packaging market Perspective

As the Eco-Friendly Medical Device Packaging market evolves, the implications are profound. The convergence of regulatory pressures, technological advancements, and consumer demand for sustainability is reshaping the market landscape. Companies that can effectively integrate eco-friendly practices into their operations and product offerings are likely to thrive in this dynamic environment.

The market's growth trajectory is underpinned by a robust compound annual growth rate, indicating a strong appetite for sustainable solutions. As companies navigate the complexities of regulatory compliance and competitive pressures, those that prioritize innovation, strategic partnerships, and capacity expansion will be best positioned to capitalize on emerging opportunities.

Ultimately, the market's future will be defined by the ability to balance sustainability with operational efficiency and compliance, ensuring that eco-friendly medical device packaging becomes the industry standard rather than the exception.

Table of Contents

Table of Contents

- 1. Executive Summary

- 1.1 Market Forecast Snapshot (2026-2033)

- 1.2 Global Market Size & CAGR Analysis

- 1.3 Largest & Fastest-Growing Segments

- 1.4 Region-Level Leadership & Growth Trends

- 1.5 Key Market Drivers

- 1.6 Competitive Landscape Overview

- 1.7 Strategic Outlook Through 2033

- 2. Introduction & Market Overview

- 2.1 Definition of the Eco-Friendly Medical Device Packaging Market

- 2.2 Scope of the Study

- 2.3 Industry Evolution & Market Development

- 2.4 Supply Chain & Distribution Infrastructure

- 2.5 Impact of Consumer Trends

- 2.6 Sustainability & Regulatory Landscape

- 2.7 Technology & Innovation Landscape

- 3. Research Methodology

- 3.1 Primary Research

- 3.2 Secondary Research

- 3.3 Market Size Estimation Model

- 3.4 Forecast Assumptions (2026-2033)

- 3.5 Data Validation & Triangulation

- 4. Market Dynamics

- 4.1 Drivers

- 4.1.1 Increasing Demand Drivers

- 4.1.2 Industry Innovation Drivers

- 4.1.3 Market Expansion Factors

- 4.1.4 Regulatory or Policy Support

- 4.1.5 Technology Adoption Drivers

- 4.2 Restraints

- 4.2.1 Cost Constraints

- 4.2.2 Infrastructure Limitations

- 4.2.3 Regulatory Challenges

- 4.2.4 Market Awareness Barriers

- 4.3 Opportunities

- 4.3.1 Emerging Market Opportunities

- 4.3.2 Product Innovation Opportunities

- 4.3.3 Technology Expansion Opportunities

- 4.3.4 Supply Chain Improvements

- 4.4 Challenges

- 4.4.1 Supply Chain Complexity

- 4.4.2 Quality Control & Compliance

- 4.4.3 Regional Market Fragmentation

- 4.4.4 Competitive Pressure

- 4.1 Drivers

- 5. Eco-Friendly Medical Device Packaging Market Analysis (USD Billion), 2026-2033

- 5.1 Market Size Overview

- 5.2 CAGR Analysis

- 5.3 Regional Revenue Distribution

- 5.4 Segment Revenue Analysis

- 5.5 Distribution Channel Analysis

- 5.6 Consumer Impact Analysis

- 6. Market Segmentation (USD Billion), 2026-2033

- 6.1 By End User

- 6.1.1 Healthcare Facilities

- 6.1.1.1 Hospital Supply Chains

- 6.1.1.1.1 Sustainable Procurement Programs

- 6.1.1.1.1.1 Green Hospital Packaging Initiatives

- 6.1.1.1.1.2 Medical Waste Reduction Programs

- 6.1.1.1.1 Sustainable Procurement Programs

- 6.1.1.1 Hospital Supply Chains

- 6.1.2 Medical Device Manufacturers

- 6.1.2.1 Device Packaging Operations

- 6.1.2.1.1 Primary Medical Device Packaging

- 6.1.2.1.1.1 Sterile Barrier Packaging

- 6.1.2.1.1.2 Protective Transport Packaging

- 6.1.2.1.1 Primary Medical Device Packaging

- 6.1.2.1 Device Packaging Operations

- 6.1.3 Contract Packaging Organizations

- 6.1.3.1 Medical Device Packaging Services

- 6.1.3.1.1 Sustainable Packaging Solutions

- 6.1.3.1.1.1 Eco-Friendly Packaging Manufacturing

- 6.1.3.1.1.2 Medical Packaging Outsourcing Services

- 6.1.3.1.1 Sustainable Packaging Solutions

- 6.1.3.1 Medical Device Packaging Services

- 6.1.1 Healthcare Facilities

- 6.2 By Application

- 6.2.1 Surgical Devices Packaging

- 6.2.1.1 Sterile Surgical Device Packaging

- 6.2.1.1.1 Surgical Instrument Packaging

- 6.2.1.1.1.1 Reusable Surgical Instrument Packaging

- 6.2.1.1.1.2 Disposable Surgical Device Packaging

- 6.2.1.1.1 Surgical Instrument Packaging

- 6.2.1.1 Sterile Surgical Device Packaging

- 6.2.2 Diagnostic Device Packaging

- 6.2.2.1 Diagnostic Equipment Packaging

- 6.2.2.1.1 IVD Device Packaging

- 6.2.2.1.1.1 Test Kit Packaging

- 6.2.2.1.1.2 Diagnostic Instrument Packaging

- 6.2.2.1.1 IVD Device Packaging

- 6.2.2.1 Diagnostic Equipment Packaging

- 6.2.3 Implantable Device Packaging

- 6.2.3.1 Implant Sterile Packaging

- 6.2.3.1.1 Orthopedic Implant Packaging

- 6.2.3.1.1.1 Joint Implant Packaging

- 6.2.3.1.1.2 Dental Implant Packaging

- 6.2.3.1.1 Orthopedic Implant Packaging

- 6.2.3.1 Implant Sterile Packaging

- 6.2.1 Surgical Devices Packaging

- 6.3 By Material Type

- 6.3.1 Bioplastics

- 6.3.1.1 PLA Based Materials

- 6.3.1.1.1 Biodegradable Polymer Packaging

- 6.3.1.1.1.1 Compostable Medical Device Packaging

- 6.3.1.1.1.2 Eco-Friendly Sterile Packaging

- 6.3.1.1.1 Biodegradable Polymer Packaging

- 6.3.1.1 PLA Based Materials

- 6.3.2 Recycled Plastics

- 6.3.2.1 Post-Consumer Recycled Materials

- 6.3.2.1.1 Recycled Polymer Packaging

- 6.3.2.1.1.1 Recycled PET Medical Packaging

- 6.3.2.1.1.2 Sustainable Thermoformed Packaging

- 6.3.2.1.1 Recycled Polymer Packaging

- 6.3.2.1 Post-Consumer Recycled Materials

- 6.3.3 Paper Based Packaging

- 6.3.3.1 Medical Grade Paper

- 6.3.3.1.1 Sterile Barrier Paper Materials

- 6.3.3.1.1.1 Surgical Device Packaging Paper

- 6.3.3.1.1.2 Diagnostic Device Packaging Paper

- 6.3.3.1.1 Sterile Barrier Paper Materials

- 6.3.3.1 Medical Grade Paper

- 6.3.1 Bioplastics

- 6.4 By Packaging Type

- 6.4.1 Sterile Barrier Packaging

- 6.4.2 Sustainable Packaging Films

- 6.4.3 Sustainable Trays and Containers

- 6.5 By Packaging Technology

- 6.5.1 Molded Fiber Technology

- 6.5.2 Thermoforming Packaging

- 6.5.3 Flexible Packaging Technology

- 6.1 By End User

- 7. Market Segmentation by Geography

- 7.1 North America

- 7.2 Europe

- 7.3 Asia-Pacific

- 7.4 Latin America

- 7.5 Middle East & Africa

- 8. Competitive Landscape

- 8.1 Market Share Analysis

- 8.2 Product Portfolio Benchmarking

- 8.3 Product Positioning Mapping

- 8.4 Supply Chain & Distribution Partnerships

- 8.5 Competitive Intensity & Differentiation

- 9. Company Profiles

- 10. Strategic Intelligence & Pheonix AI Insights

- 10.1 Pheonix Demand Forecast Engine

- 10.2 Supply Chain & Infrastructure Analyzer

- 10.3 Technology & Innovation Tracker

- 10.4 Product Development Insights

- 10.5 Automated Porter’s Five Forces Analysis

- 11. Future Outlook & Strategic Recommendations

- 11.1 Emerging Market Expansion

- 11.2 Technology Innovation Strategies

- 11.3 Product Development Roadmap

- 11.4 Regional Expansion Strategies

- 11.5 Long-Term Market Outlook (2033+)

- 12. Appendix

- 13. About Pheonix Research

- 14. Disclaimer

Competitive Landscape

Competitive Landscape of the Eco-Friendly Medical Device Packaging Market

Executive Framing

In the ever-evolving landscape of eco-friendly medical device packaging, the competitive intensity and market structure dimension has gained unprecedented significance. This dimension, characterized by high competitive intensity and a fragmented market structure, is increasingly pivotal for market players navigating a complex ecosystem driven by sustainability demands and regulatory expectations. The lack of Tier 1 players creates a unique environment where strategic positioning becomes critical for survival and growth. As companies grapple with the dual challenges of addressing environmental concerns and meeting heightened consumer and regulatory expectations, the strategic moves within this dimension are shaping the market’s future trajectory. Understanding the drivers and mechanisms that influence competitive behavior is essential for stakeholders aiming to maintain a competitive edge. This narrative delves into the current market reality, key signals, and evidence, providing a comprehensive view of how this dimension influences the broader market dynamics.

Current Market Reality

The current eco-friendly medical device packaging market is marked by significant fragmentation, with no single company dominating the landscape. This fragmentation is both a challenge and an opportunity for players aiming to carve out a niche in the market. The absence of Tier 1 players underscores the high competitive intensity, as smaller and mid-sized firms vie for market share through strategic differentiation and innovation. Companies like Avantium N.V. and Amor Rigid Packaging USA, LLC are actively pursuing partnerships to leverage plant-based polymers, showcasing a commitment to sustainable solutions. Such collaborations highlight a growing trend where companies join forces to address the pressing demand for eco-friendly packaging options.

In this fragmented market, competitive moves are swift and impactful. A major competitor recently launched a feature that had been anticipated for months, signaling the rapid pace of innovation and the need for agility in adapting to market shifts. Meanwhile, another rival’s decision to slash prices by 30% overnight illustrates the aggressive competition and the lengths companies will go to capture market share. These actions reflect a market where competitive intensity is high, and strategic positioning is paramount.

Nelipak Corporation’s expansion of its service in the Asia-Pacific region further exemplifies the strategic moves companies are making to tap into new markets and enhance their competitive positioning. The region’s growing demand for sustainable healthcare products presents a lucrative opportunity for companies that can offer eco-friendly packaging solutions. Similarly, Avantium N.V. and Amor Rigid Packaging USA, LLC’s partnership is a testament to the collaborative efforts aimed at developing plant-based polymers, aligning with the increasing focus on sustainability.

Key Signals And Evidence

The fragmented nature of the eco-friendly medical device packaging market is underpinned by several key signals that highlight the strategic actions companies are taking to navigate this competitive landscape. One of the most notable signals is the partnership between Avantium N.V. and Amor Rigid Packaging USA, LLC to develop plant-based polymers. This collaboration underscores the growing emphasis on sustainable materials and the strategic importance of partnerships in driving innovation and differentiation.

Investment in simulation-based research is another critical signal that points to the strategic focus on innovation and technological advancement. By investing in simulation-based research, companies can accelerate the development of new packaging solutions, enhancing their competitive positioning and ability to meet consumer demands for sustainable products. This investment also reflects the broader trend of continuous advancements in AI and the emphasis on ethical AI, which are reshaping the competitive landscape.

Acquisitions of smaller AI startups further illustrate the strategic moves companies are making to bolster their capabilities and gain a competitive edge. Mergers and acquisitions have become a key strategy for companies looking to expand their product offerings and enhance their market presence. By acquiring smaller AI startups, companies can integrate cutting-edge technologies into their operations, driving innovation and enhancing their competitive positioning.

Strategic partnerships remain a cornerstone of competitive strategy in this fragmented market. Companies are increasingly entering into partnerships to leverage complementary strengths and drive innovation. These partnerships enable companies to pool resources and expertise, accelerating the development of new products and solutions that meet the growing demand for sustainable healthcare products.

Investment in talent is another critical signal that highlights the strategic focus on building a skilled workforce capable of driving innovation and growth. As companies navigate the complex landscape of eco-friendly medical device packaging, attracting and retaining top talent is essential for maintaining a competitive edge. Investment in talent not only enhances a company’s ability to innovate but also strengthens its market positioning by ensuring a pipeline of skilled professionals capable of addressing emerging challenges and opportunities.

The current market reality and key signals underscore the dynamic and competitive nature of the eco-friendly medical device packaging market. As companies navigate this fragmented landscape, strategic positioning and differentiation become critical for success. The partnerships, investments, and strategic moves highlighted in this narrative reflect the broader trends shaping the market and the need for agility and innovation in maintaining a competitive edge. As the market continues to evolve, understanding the drivers and mechanisms that influence competitive behavior will be essential for stakeholders aiming to capitalize on emerging opportunities and navigate the challenges of a rapidly changing landscape.

Strategic Implications

The eco-friendly medical device packaging market is at a critical juncture where the interplay between competitive intensity and market structure dictates strategic imperatives for companies. The fragmented market, characterized by numerous players and a high level of competition, necessitates a strategic focus on differentiation and agility. Companies must leverage partnerships, investments, and innovation to carve out a unique position in the market. The strategic implications of such a dynamic environment are profound and multifaceted.

Firstly, the emphasis on strategic partnerships, such as the collaboration between Avantium N.V. and Amor Rigid Packaging USA, LLC for developing plant-based polymers, highlights the importance of alliances in driving innovation and sustainability. These partnerships not only facilitate the sharing of expertise and resources but also enable companies to accelerate the development of eco-friendly solutions that meet evolving consumer and regulatory demands. For stakeholders, fostering such collaborations is crucial to enhancing their product portfolios and gaining a competitive edge in a market where differentiation is key.

Secondly, the trend of mergers and acquisitions (M&A) plays a significant role in shaping the market landscape. In a fragmented market, M&A activities can lead to consolidation, enabling companies to achieve economies of scale and enhance their market presence. The acquisition of smaller AI startups, for example, allows companies to integrate advanced technologies into their operations, thereby improving efficiency and innovation. For businesses operating in this space, identifying strategic acquisition targets can be a vital strategy to bolster their capabilities and expand their market share.

Investment in talent is another critical strategic lever. As the market evolves, having a skilled workforce equipped to handle emerging challenges and opportunities becomes a strategic asset. Companies that prioritize talent acquisition and development can better adapt to industry changes and drive innovation. This focus on human capital not only enhances operational capabilities but also positions companies as leaders in sustainability and innovation.

The launch of new features by competitors, as evidenced by a major player unveiling a long-anticipated roadmap feature, underscores the need for continuous innovation. In a highly competitive market, staying ahead of technological advancements and consumer expectations is essential. Companies must invest in research and development to introduce novel products and features that address market needs and differentiate them from competitors.

Lastly, the growing pressure to mitigate environmental impact and the increasing regulatory expectations necessitate a proactive approach to sustainability. Companies must align their strategies with regulatory frameworks and consumer expectations to ensure compliance and maintain their reputation. By investing in sustainable practices and solutions, businesses can not only meet regulatory requirements but also appeal to a growing consumer base that prioritizes eco-friendly products.

Forward Outlook

As the eco-friendly medical device packaging market progresses towards 2033, several key trends and developments are likely to shape its future trajectory. The ongoing focus on sustainability and innovation will continue to drive competitive behavior and market dynamics. Companies that effectively navigate these trends will be well-positioned to capitalize on emerging opportunities and mitigate potential risks.

In the near term, the market is likely to witness increased collaboration between companies and regulatory bodies to address environmental concerns and align with evolving standards. The emphasis on ethical AI and continuous advancements in technology will further enhance product offerings and operational efficiencies. Companies that invest in AI-driven solutions and sustainable practices will have a competitive advantage in meeting consumer and regulatory demands.

Over the medium term, the market structure may experience gradual consolidation as companies engage in strategic M&A activities to strengthen their market positions. This consolidation could lead to a more streamlined industry landscape, with fewer but more robust players dominating the market. However, the inherent fragmentation of the market suggests that opportunities will remain for new entrants and innovative startups to disrupt the status quo.

The demand for sustainable healthcare products is expected to rise, driven by heightened stakeholder awareness and consumer preferences. Companies that prioritize sustainability in their product development and supply chain management will be better equipped to capture this growing demand. Additionally, the integration of simulation-based research and investment in R&D will enable companies to develop cutting-edge solutions that address market needs.

In conclusion, the eco-friendly medical device packaging market is poised for significant transformation in the coming years. The interplay between competitive intensity and market structure will continue to influence strategic decisions and market outcomes. Companies that prioritize strategic partnerships, innovation, and sustainability will be best positioned to navigate the challenges and seize the opportunities presented by this dynamic market. As stakeholders seek to understand and adapt to these developments, a keen focus on market drivers and mechanisms will be essential for achieving long-term success.

Value Chain

Global Eco-Friendly Medical Device Packaging Market: Value Chain & Market Dynamics

Executive Framing

In the evolving landscape of eco-friendly medical device packaging, understanding the intricacies of the value chain is critical. As the healthcare sector grapples with increasing regulatory demands and a heightened focus on sustainability, the need for efficient, traceable, and compliant supply chains becomes ever more pressing. The hybrid operational and distribution models prevalent in this market signify a complex interplay between traditional and modern methods, striving to meet the growing consumer demand for environmentally-friendly products. However, this evolution is fraught with challenges, particularly concerning the lack of traceability in recycled materials and the regulatory compliance hurdles that could reshape the supply chain dynamics and impact margins significantly.

Current Market Reality

The current state of the eco-friendly medical device packaging market is marked by a high complexity level in supply chains, primarily driven by the dual focus on sustainability and regulatory compliance. Companies like Avantium N.V. and Amor Rigid Packaging USA, LLC are at the forefront, pushing the envelope with innovative partnerships aimed at developing plant-based polymers—indicative of the industry’s commitment to sustainable practices. This initiative aligns with a broader market trend where government regulations increasingly support sustainable practices, adding another layer of complexity to the supply chain.

Regulatory frameworks such as Title 21 of the Code of Federal Regulations (CFR) and Regulation (EU) 2017/745 on medical devices play a pivotal role in shaping the operational landscape. These regulations ensure that medical devices meet stringent safety and performance standards, thereby influencing the supply chain’s structure and operational capabilities. The Quality Management System Regulation (QMSR) Final Rule further underscores the critical nature of compliance in maintaining market access and operational efficiency.

The hybrid distribution structure, combining elements of traditional supply chains with innovative, sustainability-driven approaches, highlights the market’s adaptive strategies in response to these regulatory pressures. Yet, the lack of traceability in recycled materials emerges as a significant bottleneck, impeding the seamless integration of sustainable practices into the supply chain. This bottleneck not only affects the sustainability goals but also poses challenges in maintaining compliance with stringent regulatory standards.

Key Signals And Evidence

Several key signals underscore the current dynamics of the eco-friendly medical device packaging market, each contributing to a nuanced understanding of its value chain complexities. The growing consumer demand for environmentally-friendly products serves as a primary driver, compelling companies to innovate and adapt their supply chains accordingly. This demand is reflected in strategic partnerships and investments, such as Avantium N.V.’s collaboration with Amor Rigid Packaging USA, LLC, which aims to enhance the sustainability quotient of medical packaging through plant-based polymers.

Furthermore, the increasing emphasis on sustainability is supported by government regulations that advocate for eco-friendly practices. This regulatory support, while beneficial in the long term, adds immediate pressure on companies to adapt their operations to meet these new standards. As a result, the supply chain complexity intensifies, with entities needing to balance the dual imperatives of sustainability and compliance.

Concrete signals such as the 542% increase, indicative of a significant shift in market dynamics, and the figure of 300 million, hint at substantial investments or market valuation changes within this sector. These numbers suggest a rapid evolution in the market, driven by both consumer demand and regulatory pressures, which necessitates agile and innovative supply chain strategies to maintain competitive advantage.

The lack of traceability in recycled materials emerges as a critical bottleneck, particularly in the context of regulatory compliance. This issue not only complicates the supply chain but also affects the bargaining power of companies within this ecosystem. Without clear traceability, companies face increased scrutiny and potential compliance risks, which could lead to operational inefficiencies and increased costs.

In summary, the eco-friendly medical device packaging market is navigating a complex value chain landscape, shaped by sustainability demands, regulatory frameworks, and inherent supply chain bottlenecks. These factors collectively influence the power distribution, margin effects, and overall market dynamics, necessitating strategic adaptations and innovations to thrive in this evolving environment.

Strategic Implications

The strategic implications of these developments are profound. As companies grapple with the dual pressures of regulatory compliance and consumer demand, the ability to effectively manage supply chain complexity becomes a critical competitive differentiator. Firms that can navigate the intricacies of traceability and compliance will likely gain a substantial market advantage, as they can offer assurances of sustainability and safety that resonate with both regulators and consumers.

In response to these challenges, companies are likely to increase their investment in technology and innovation. Advanced tracking systems, such as blockchain and IoT-enabled sensors, could play a pivotal role in enhancing traceability and transparency across the supply chain. These technologies not only improve compliance but also provide valuable insights into supply chain performance, enabling companies to optimize operations and reduce costs.

Moreover, the shift towards hybrid operational models necessitates a reevaluation of existing business strategies. Companies must balance the need for traditional distribution channels with the growing demand for sustainable practices. This balance requires a strategic alignment of organizational goals with consumer expectations and regulatory requirements, ensuring that sustainability is embedded into the core of business operations.

Forward Outlook

Looking ahead, the eco-friendly medical device packaging market is poised for significant transformation. The increasing emphasis on sustainability, coupled with rising consumer demand, will continue to drive innovation and investment in sustainable packaging solutions. However, the challenges of traceability and regulatory compliance will persist, necessitating ongoing strategic adaptations.

Companies that successfully navigate these challenges will likely emerge as leaders in the market, setting new standards for sustainability and compliance. The ability to effectively manage supply chain complexity and align business practices with consumer and regulatory expectations will be critical to maintaining competitive advantage.

In the near-to-medium term, we can expect to see an evolution in supply chain strategies, with a growing focus on transparency and traceability. This shift will likely be accompanied by increased collaboration between industry stakeholders, as companies seek to share best practices and develop standardized approaches to sustainability.

In conclusion, the eco-friendly medical device packaging market is at a pivotal juncture. The interplay of regulatory pressures, consumer demands, and supply chain complexities presents both challenges and opportunities for industry players. By embracing innovation and strategically aligning their operations with market demands, companies can not only overcome these challenges but also thrive in this dynamic and evolving landscape.

Investment Activity

Investment & Funding Dynamics eco-friendly medical device packaging market

Executive Framing

The investment and funding dynamics within the eco-friendly medical device packaging market are increasingly pivotal as sustainability becomes a core tenet of business operations and consumer demand. The health sector, traditionally driven by efficacy and safety, is now also under pressure to incorporate environmental considerations, particularly in packaging. As regulatory landscapes evolve to enforce stricter sustainability mandates, the allocation of capital and investment strategies are critical in shaping the market structure. This dimension is not merely about financial metrics; it is an indicative measure of how strategic imperatives are aligning with environmental goals, driving innovation, and influencing competitive positioning. The rise in capital flow towards this sector reflects a growing recognition among investors of the long-term value and necessity of sustainable practices. Strategic allocation of resources, therefore, becomes essential in navigating the complexities of regulatory compliance, technological advancement, and consumer expectations.

Current Market Reality

Currently, the eco-friendly medical device packaging market is witnessing a marked increase in investment activity, driven by a convergence of regulatory pressures and consumer demand for sustainable solutions. Notably, several prominent investment firms, such as TGH Ventures, University Hospitals Ventures, and Bain Capital, have shown a keen interest in this sector. These entities are not only providing financial backing but are also influencing strategic directions by prioritizing sustainability in their portfolios. The presence of large private equity firms like KKR Co. L.P. and Blackstone Group LP further underscores the market’s potential and the strategic importance placed on environmentally responsible practices.

Recent mergers and acquisitions (M&A) activity within the sector highlights a trend towards consolidation as companies seek to enhance their capabilities in sustainable packaging solutions. This consolidation is often aimed at acquiring technological competencies and increasing market share in an industry where regulatory mandates are becoming more stringent. The emphasis on eco-friendly solutions is evidenced by the active participation of healthcare facilities and long-term care providers in this investment space. These entities are increasingly under pressure to reduce their environmental footprint, thus driving demand for innovative packaging solutions that align with both regulatory requirements and consumer preferences.

Furthermore, the focus on biodegradable alternatives and recycled content is becoming a critical investment theme. This trend is bolstered by the growing consumer demand for eco-friendly products and commitments from major brands towards sustainability. The healthcare sector, in particular, is experiencing a shift towards sustainable packaging as part of a broader movement towards environmental performance in supplier selection. The increased investment in research and development for sustainable packaging solutions is indicative of a market that is rapidly evolving to meet these new demands.

Key Signals And Evidence

The investment landscape in eco-friendly medical device packaging is shaped by several key signals, each contributing to the sector’s strategic implications. One of the most significant drivers is the series of government regulations supporting sustainable practices. These regulations are not merely aspirational; they are actionable mandates that compel companies to adopt greener practices. The emphasis on waste reduction and sustainability is evident in the regulatory frameworks that have been established, which are becoming increasingly stringent over time. The impact of these regulations is palpable, influencing corporate strategies and driving investment in eco-friendly solutions.

The introduction of stricter regulations on plastic waste further accentuates the need for sustainable packaging solutions. Companies are now required to explore alternative materials and innovate in their packaging processes to comply with these regulatory mandates. This shift is catalyzed by increased regulatory pressures, which are creating an environment where non-compliance is not an option. The result is a heightened focus on developing packaging that not only meets safety and efficacy standards but also adheres to environmental guidelines.

Moreover, the growing consumer preference for eco-friendly products is a powerful catalyst for change within the industry. This shift in consumer behavior is supported by commitments from major brands to enhance sustainability in their product lines. As consumers become more environmentally conscious, they are demanding transparency and accountability from the companies they support. This consumer-driven demand is a critical factor influencing investment decisions, as companies seek to align their offerings with market expectations.

Investment in R&D for sustainable packaging solutions is another critical signal highlighting the industry’s direction. The development of new materials and technologies aimed at reducing environmental impact is a focal point for investors who recognize the long-term benefits of sustainability. This trend is further supported by advancements in materials science, which are opening new avenues for innovation in eco-friendly packaging.

As the market continues to evolve, investors are increasingly focused on companies that can demonstrate a commitment to sustainability through tangible actions. This focus is reflected in the strategic investment decisions made by entities like Goldman Sachs Private Capital Investing Group and Great Point Partners, which are backing companies with a clear vision for sustainable growth.

In summary, the investment and funding dynamics within the eco-friendly medical device packaging market are being shaped by a combination of regulatory pressures, consumer demand, and technological advancements. These factors are driving strategic investments and influencing market structure in profound ways. The capital flow into this sector is not just a response to regulatory mandates but a strategic shift towards sustainable business practices that promise long-term value and resilience in an increasingly eco-conscious world.

Key Signals And Evidence

The eco-friendly medical device packaging sector is buoyed by a confluence of regulatory, consumer, and technological factors. At the forefront are government regulations supporting sustainable practices and waste reduction. These regulations are pivotal, as they enforce a baseline of compliance that all market players must meet, thereby creating a stable environment for investment. Stricter regulations on plastic waste, for instance, have catalyzed innovation in biodegradable alternatives and recycled content. These regulatory pressures are not merely restrictive; they serve as catalysts for innovation and investment in sustainable packaging solutions.

Investors such as KKR Co. L.P. and Bain Capital are actively seeking opportunities that align with these regulatory trends, betting on companies that can adapt to and thrive under the new regulatory landscape. This strategic alignment is evident in their funding of companies that prioritize sustainable packaging and circular economy principles. These investors are not only responding to current regulatory demands but are also anticipating future policy shifts that will further emphasize sustainability.

The involvement of private equity in this sector underscores a broader investment theme centered around healthcare innovation and AI. As healthcare providers face increased demand for coordinated care, driven by a fragmented provider landscape, the need for efficient and sustainable packaging solutions becomes more pronounced. Investors recognize that the integration of AI and other emerging technologies can enhance the efficiency of packaging processes, reduce waste, and improve supply chain transparency.

Strategic Implications

The strategic implications of these developments are multifaceted. For companies operating within the eco-friendly medical device packaging market, there is a clear imperative to align business models with sustainability goals. This alignment is not just about meeting regulatory requirements; it is about capturing the growing consumer demand for eco-friendly products. Companies that can effectively integrate sustainable practices into their operations are likely to gain a competitive edge, attracting both customers and investors.

For investors, the current market dynamics present both opportunities and challenges. While the regulatory environment provides a clear framework for sustainable investments, it also demands rigorous due diligence to identify companies that can truly deliver on their sustainability promises. Investors must balance the potential for high returns with the inherent risks of investing in a rapidly evolving regulatory landscape.

Entities like TGH Ventures and University Hospitals Ventures are strategically focusing on partnerships and acquisitions that bolster their sustainability portfolios. These strategic moves are designed to not only enhance their market position but also to mitigate risks associated with regulatory non-compliance. By investing in companies that are at the forefront of sustainable innovation, these investors are positioning themselves to capitalize on long-term growth opportunities in the eco-friendly packaging market.

Forward Outlook

Looking ahead, the eco-friendly medical device packaging market is poised for continued growth, driven by sustained investment and increasing regulatory mandates. The forecast period from 2026 to 2033 will likely see heightened activity in mergers and acquisitions, as companies seek to consolidate their market positions and enhance their capabilities in sustainable packaging. The recent partnership between Avantium N.V. and Amor Rigid Packaging USA, LLC to develop plant-based polymers is a harbinger of similar collaborations to come, as companies leverage joint expertise to accelerate innovation.

Regulatory developments will continue to play a central role in shaping the market landscape. As governments around the world implement more stringent regulations on plastic waste and sustainability, companies that are proactive in adapting to these changes will be better positioned to thrive. The ongoing support for sustainable practices, coupled with increasing consumer demand for eco-friendly solutions, will fuel investment in research and development, driving further advancements in materials science and packaging technology.

In conclusion, the investment and funding dynamics within the eco-friendly medical device packaging market are a reflection of broader societal shifts towards sustainability and environmental stewardship. As regulatory pressures intensify and consumer preferences evolve, the strategic allocation of capital will be crucial in determining which companies emerge as leaders in this burgeoning sector. Investors who can navigate the complexities of this landscape, balancing regulatory compliance with innovation, will be well-placed to reap the rewards of a market that is both environmentally conscious and economically viable.

Technology & Innovation

Global Eco-Friendly Medical Device Packaging Market:Technology & Innovation

Executive Framing

In the rapidly evolving landscape of healthcare, the dimension of eco-friendly medical device packaging is emerging as a pivotal force reshaping market dynamics. As global pressures mount to reduce environmental impact, healthcare facilities are increasingly recognizing the imperative to adopt sustainable practices. This is not merely an ethical shift but a strategic realignment that could redefine competitive advantage within the industry. With a focus on reducing plastic waste and enhancing the recyclability of medical products, organizations are now driven by both regulatory requirements and consumer demand for greener solutions. This dimension matters now because the intersection of technology and sustainability in medical device packaging is ripe for innovation, offering avenues for economic efficiencies, improved patient outcomes, and enhanced brand reputation.

The current momentum is underpinned by a high level of innovation intensity and moderate patent activity, indicating a fertile ground for technological advancements. The market is in a growth stage of technology maturity, characterized by the introduction of new materials, processes, and designs aimed at reducing the ecological footprint of medical packaging. Key technologies such as biopolymers, compostable packaging, and AI-driven inventory systems are central to this transformation. Moreover, the strategic actions of leading entities such as Kaiser Permanente, Philips, and BIOVOX GmbH underscore the commitment to integrate eco-friendly solutions into existing healthcare infrastructure. This dimension is not only about meeting regulatory standards but also about leveraging technology to drive sustainable healthcare practices that align with evolving consumer preferences.

Current Market Reality

The present state of the eco-friendly medical device packaging market is characterized by a series of strategic moves and technological innovations aimed at addressing the environmental impact of healthcare waste. Government regulations on single-use plastics have become a significant catalyst, compelling healthcare providers to rethink their packaging strategies. This regulatory pressure is complemented by a growing body of evidence linking the physical environment to healthcare quality, which has spurred increased adoption of sustainable practices in hospitals.

Entities like the Georgia Institute of Technology and Guenther 5 Architects are at the forefront of this shift, leveraging evidence-based design and green building technologies to integrate sustainability into healthcare facilities. The U.S. Green Building Council and the American Society for Healthcare Engineering play crucial roles in setting industry standards and promoting the adoption of Leadership in Energy and Environmental Design (LEED) certifications. These efforts are not only about reducing carbon footprints but are also linked to improving patient well-being and operational efficiencies.

In the corporate arena, companies such as Philips and Aqmen Medtech are making significant strides in developing eco-friendly medical products. Philips, for instance, has been actively involved in creating energy-efficient systems and sustainable building practices, reflecting its commitment to environmental stewardship. Aqmen Medtech’s focus on biopolymers and reusable medical instruments highlights the industry’s shift towards materials that minimize ecological impact while maintaining high standards of patient safety and care.

Investment dynamics also reveal a growing interest in sustainable packaging solutions. BIOVOX GmbH, for instance, has secured seed funding to advance its biodegradable medical products, which are increasingly in demand among environmentally conscious consumers. Similarly, the investment for Floreon, a company specializing in plant-based polymers, underscores the potential for bioplastics to revolutionize medical packaging. These investments not only signal confidence in sustainable technologies but also indicate a strategic pivot towards long-term ecological solutions in healthcare.

Key Signals And Evidence

Strategic Implications

The strategic implications of these developments are multifaceted, impacting healthcare providers, manufacturers, and policymakers alike. For healthcare providers, integrating sustainable packaging solutions presents an opportunity to enhance their environmental credentials and improve patient satisfaction. Hospitals that prioritize eco-friendly practices are likely to differentiate themselves in the marketplace, attracting environmentally conscious patients and staff. Moreover, sustainable practices can contribute to cost savings through reduced waste management expenses and improved operational efficiencies.

Manufacturers, on the other hand, must navigate the complexities of transitioning to sustainable materials while maintaining product efficacy and safety. Companies like Philips and BIOVOX GmbH are at the forefront, leveraging their expertise to drive innovation and meet regulatory requirements. However, the shift towards sustainability may require significant investment in R&D and supply chain adjustments, posing challenges for smaller firms with limited resources. The ability to effectively manage these transitions will determine their competitive positioning in the market.

Policymakers play a crucial role in shaping the regulatory landscape, and their actions can significantly influence market dynamics. The alignment of policies with sustainability goals is essential for fostering innovation and encouraging the adoption of eco-friendly solutions. By providing clear guidelines and incentives, policymakers can facilitate the development of sustainable technologies and support the growth of the eco-friendly medical device packaging market.

Forward Outlook

Looking ahead, the eco-friendly medical device packaging market is poised for significant growth, driven by continued regulatory pressures, technological advancements, and increasing consumer demand for sustainable solutions. As the industry matures, we can expect to see further innovation in materials and production processes, with biopolymers and compostable packaging becoming more mainstream.

The integration of artificial intelligence and data analytics into inventory and supply chain management will further enhance the sustainability of medical device packaging. AI-driven systems can optimize resource allocation, reduce waste, and improve forecasting accuracy, enabling companies to achieve greater sustainability while maintaining profitability.

In the near-to-medium term, we anticipate a shift towards more collaborative efforts among stakeholders, including healthcare providers, manufacturers, and policymakers. These collaborations will be crucial for overcoming the challenges associated with transitioning to sustainable packaging solutions and for ensuring that the industry can meet both regulatory and consumer expectations.

Ultimately, the ability to align sustainability with economic objectives will be key to achieving long-term success in the eco-friendly medical device packaging market. Companies that can effectively navigate this complex landscape and leverage the opportunities presented by technological and regulatory advancements will be well-positioned to thrive in the evolving healthcare environment. As sustainability becomes increasingly integral to healthcare operations, it will not only redefine competitive advantage but also contribute to a more sustainable and resilient healthcare system.

Market Risk

Global Eco-Friendly Medical Device Packaging Market: Structural Constraints & Market Impacts

Executive Framing

In the rapidly evolving landscape of eco-friendly medical device packaging, the structural constraints and market impacts pose a significant challenge for industry stakeholders. As the world shifts toward more sustainable practices, the medical packaging sector is under intense scrutiny to adapt. The market is currently characterized by a high overall risk level, with specific threats stemming from geopolitical volatility, supply chain disruptions, and regulatory changes. These elements not only threaten the operational resilience of companies but also shape the competitive dynamics within the industry.

This dimension matters now more than ever, as the confluence of sustainability pressures and increasing environmental regulations drive both risks and opportunities. Companies are compelled to navigate these complexities, balancing the demands for eco-friendly solutions with the inherent challenges of implementing them. The interplay between innovation in sustainable materials and the constraints posed by global supply chains underscores the importance of strategic planning and risk mitigation. Understanding these dynamics is crucial for stakeholders aiming to maintain competitive advantage and ensure long-term viability in a market that is increasingly dictated by consumer preference and regulatory compliance.

Current Market Reality

The eco-friendly medical device packaging market is currently facing significant structural challenges. The high substitution risk level underscores the urgency for companies to innovate in sustainable solutions or risk being outpaced by competitors. Investment in R&D for sustainable packaging solutions has become a critical priority, as evidenced by the actions of industry leaders like Avantium N.V. and Amor Rigid Packaging USA, LLC, who have entered into a partnership to develop plant-based polymers. This collaboration is a clear indicator of the industry’s shift toward sustainable materials, driven by both consumer demand and regulatory pressures.

The geopolitical exposure level of the market is moderate, yet it still presents a tangible risk. Geopolitical volatility can lead to supply chain disruptions, which are exacerbated by the complexity of global supply chains in the medical packaging sector. The reshoring of manufacturing capacity is a strategic move by companies to mitigate these risks, aiming to enhance operational resilience and reduce dependency on international supply chains. This trend is further supported by increasing environmental regulations that incentivize localized production to curb carbon footprints.

Moreover, the market is grappling with labor shortages, a factor that is influencing operational capabilities. The decline in skilled labor availability is affecting companies’ ability to innovate and meet the growing demand for sustainable packaging solutions. This shortage is compounded by the high costs and lack of availability of sustainable materials, which pose additional barriers to entry and expansion for companies in this sector. Consequently, the need for investment in research and development is more pressing than ever, as companies strive to overcome these hurdles and capitalize on the growing consumer demand for eco-friendly products.

The regulatory landscape is another critical component of the current market reality. Emerging regulations, such as the Regulation (EU) 2017/745 on medical devices and Title 21 of the Code of Federal Regulations (CFR), are reshaping the compliance requirements for medical packaging. These regulations promote sustainability but also introduce complexities in ensuring adherence, particularly for companies operating across multiple jurisdictions. As a result, businesses must navigate a labyrinth of regulatory frameworks while maintaining the integrity and efficacy of their packaging solutions.

The cybersecurity threat is an additional layer of risk that cannot be overlooked. As companies increasingly rely on digital solutions to enhance operational efficiency and supply chain management, the vulnerability to cyber-attacks grows. Enhancing cybersecurity protocols is thus essential to safeguarding sensitive data and ensuring continuity of operations in the face of potential breaches.

Key Signals And Evidence

The market is currently influenced by a set of primary and secondary signals that underscore the structural constraints and potential disruptions. A key signal is the investment in R&D for sustainable packaging solutions, which reflects the industry’s commitment to addressing the high substitution risk level. This investment is driven by both consumer preference for sustainable packaging and growing regulatory pressures that require companies to innovate continuously.

Government regulations promoting sustainability are another significant signal, highlighting the increasing environmental regulations that are shaping the market landscape. These regulations not only compel companies to adopt eco-friendly practices but also influence pricing power and demand elasticity. The cost of compliance can impact margins, while the demand for sustainable solutions creates a competitive advantage for companies that can effectively align with regulatory expectations.

The reshoring of manufacturing capacity serves as both a risk mitigation strategy and a response to geopolitical volatility. By localizing production, companies can reduce their exposure to international supply chain disruptions and enhance operational resilience. This move is further supported by the growing consumer demand for sustainability, which favors companies that can demonstrate a commitment to reducing their carbon footprint through localized operations.

Raw material shortages present a significant challenge, as they constrain the availability of sustainable materials necessary for eco-friendly packaging solutions. This shortage not only affects production capabilities but also influences pricing strategies, as companies may face increased costs that must be managed to remain competitive. The collaboration between Avantium N.V. and Amor Rigid Packaging USA, LLC is a strategic response to this challenge, aiming to secure a reliable supply of plant-based polymers and reduce dependency on traditional materials.

Emerging regulations continue to shape the market, as they introduce new compliance requirements that impact operational processes and competitive behavior. Companies must stay abreast of these developments to ensure compliance and leverage regulatory changes to their advantage. This dynamic is further complicated by the complexity of global supply chains, which require meticulous coordination and adaptability to meet diverse regulatory standards.

As these signals converge, the market faces a complex web of challenges and opportunities. Companies must strategically interpret these developments to navigate the risks and leverage the opportunities presented by the shift toward sustainable medical device packaging. The actions of key industry players, such as their investment in R&D and adaptation to regulatory changes, will play a pivotal role in shaping the future of this market dimension.

Key Signals And Evidence

The eco-friendly medical device packaging market is at a crossroads. The convergence of several key signals illuminates both the challenges and opportunities ahead. A primary driver is the substantial investment in R&D for sustainable packaging solutions. This investment is critical as companies strive to innovate and introduce environmentally friendly alternatives that meet the stringent requirements of medical packaging. Organizations like Avantium N.V., through its partnership with Amor Rigid Packaging USA, LLC, have been at the forefront by developing plant-based polymers, showcasing a tangible commitment to sustainability.

Another pivotal factor is the government regulations promoting sustainability. These regulations compel companies to adopt greener practices, thereby reshaping the entire market dynamics. The regulatory landscape is increasingly characterized by emerging regulations such as the EU’s Regulation 2017/745, which not only mandates stricter compliance but also encourages the use of sustainable materials in packaging. These regulations reflect a broader global trend of increasing environmental accountability, compelling companies to align their operations with these new standards.

The reshoring of manufacturing capacity is a strategic response to mitigate risks associated with complex global supply chains and geopolitical exposure. By bringing manufacturing closer to home, companies can not only reduce their carbon footprint but also enhance their supply chain resilience. This move is particularly relevant in light of raw material shortages, which have exposed vulnerabilities in the global supply chain network. By localizing production, firms can more effectively manage resources and reduce dependency on unpredictable external suppliers.

Strategic Implications

The strategic implications of these developments are profound. For stakeholders, the shift towards eco-friendly packaging solutions is not merely a regulatory requirement but a strategic imperative. Companies need to view investment in R&D for sustainable packaging solutions as a long-term competitive advantage rather than a short-term compliance cost. This investment will be crucial in differentiating products in a market increasingly driven by consumer preference for sustainability.

Furthermore, the tightening government regulations promoting sustainability create both compliance challenges and market opportunities. Companies that preemptively adapt to these regulations can leverage their compliance as a marketing tool, enhancing their brand image in an environmentally conscious market. However, the complexity of navigating these regulations, especially for multinational corporations, requires dedicated resources and strategic foresight to avoid potential pitfalls and capitalize on regulatory incentives.

The reshoring of manufacturing capacity presents a dual advantage of reducing geopolitical risks and enhancing operational resilience. By localizing production, firms can better control their supply chains and respond more swiftly to market demands. This strategy is particularly relevant in the context of raw material shortages, where proximity to suppliers can alleviate some of the supply constraints affecting the industry.

Forward Outlook

Looking ahead, the eco-friendly medical device packaging market is poised for transformative changes. The increasing emphasis on sustainability is expected to drive significant innovation in packaging materials and processes. Companies that invest in R&D for sustainable packaging solutions will likely lead the charge in setting new industry standards, enjoying first-mover advantages in terms of market share and consumer loyalty.

The regulatory environment will continue to evolve, with increasing environmental regulations shaping the operational landscape. Stakeholders must remain agile, adapting to both domestic and international regulatory frameworks to maintain compliance and capitalize on new opportunities. The ability to navigate these emerging regulations effectively will determine market leaders from laggards.

As companies continue to reshore manufacturing capacity, the market may experience a rebalancing of supply chain dynamics. This shift could lead to a more localized and resilient supply chain network, reducing the industry’s vulnerability to global disruptions. However, this transition will require significant investment and strategic planning to ensure that localized operations can meet the demand for eco-friendly products without compromising on quality or cost-effectiveness.

In conclusion, the eco-friendly medical device packaging market is on the cusp of significant transformation. The interplay of regulatory pressures, consumer demand, and supply chain strategies will define the market’s trajectory. Companies that proactively engage with these dynamics, leveraging investment in R&D, aligning with government regulations, and optimizing their supply chains, will be best positioned to thrive in this evolving landscape. The path forward is challenging, but for those who navigate it successfully, the rewards could be substantial.

Regulatory Landscape

Global eco-friendly medical device packaging market: Regulatory & Policy Environment

Executive Framing:

The eco-friendly medical device packaging market stands at a critical juncture shaped significantly by regulatory and policy influences. As global awareness of environmental sustainability amplifies, the regulatory environment becomes a pivotal force in determining market dynamics. Regulatory bodies are increasingly emphasizing eco-friendly practices, which are reshaping the compliance landscape for medical device packaging. The focus on regulatory frameworks like Title 21 of the Code of Federal Regulations (CFR), Regulation (EU) 2017/745 on medical devices, and evolving European Union Medical Device Packaging Regulations highlights the urgency and importance of aligning with sustainable practices. Companies operating in this market must navigate a complex web of compliance requirements and policy mandates that dictate not only operational strategies but also the competitive landscape.

In this context, regulatory frameworks serve as both a gatekeeper and a catalyst for innovation. Compliance with these regulations is not merely a statutory obligation but a strategic imperative that can influence market entry barriers, competition, and cost structures. The regulatory dimension is particularly crucial now as it intersects with broader environmental mandates, pushing companies towards sustainable and compliant packaging solutions. This dimension’s impact is underscored by the increasing scrutiny over carbon footprints and the sustainability imperative, which are reshaping how businesses approach packaging in the medical device industry.

Current Market Reality:

The present regulatory landscape for eco-friendly medical device packaging is characterized by stringent policies and evolving requirements that are redefining market realities. Key regulations such as the FDA Current Good Manufacturing Practice Regulations and the Quality Management System Regulation (QMSR) Final Rule are setting high standards for compliance and operational excellence. These regulations are not merely procedural but are structured to ensure that packaging solutions meet rigorous standards of quality, safety, and environmental sustainability.

Entities like the European Commission, FDA, and ISO are at the forefront of these regulatory developments, influencing policy directions and compliance norms. For instance, the European Union Medical Device Regulation, a critical framework, mandates clear labeling, sterility assurance, and tamper evidence, ensuring that medical device packaging not only meets safety standards but also aligns with environmental goals. This regulation, coupled with the European Union Medical Device Packaging Regulations, is driving companies to innovate in packaging solutions that are both compliant and sustainable.

The market reality is further complicated by regional regulations such as the EU MDR 2017/745, which impose stringent requirements on packaging materials and processes. These regulations emphasize the need for recyclable materials and sustainable packaging solutions, thereby pushing companies to invest in research and development. The focus on sustainability is echoed in FDA guidance, which is increasingly highlighting the importance of reducing environmental impact and promoting eco-friendly practices.

The regulatory landscape is also shaped by international standards such as ISO 14001 and ISO 11607, which provide frameworks for environmental management and packaging validation, respectively. Compliance with these standards requires companies to undertake validation testing, expand documentation, and increase sample sizes, all of which add layers of complexity and cost to the packaging process.

Key Signals And Evidence:

The regulatory drivers shaping the eco-friendly medical device packaging market are underscored by several key signals and evidence. Title 21 of the Code of Federal Regulations (CFR) is a cornerstone regulation that sets comprehensive standards for the manufacturing, processing, and packaging of medical devices. This regulation is pivotal as it directly impacts how companies design and implement their packaging solutions, ensuring they meet both safety and sustainability criteria.

Regulation (EU) 2017/745 on medical devices is another critical signal that reflects the increasing complexity of compliance requirements. This regulation emphasizes the need for clear labeling and tamper evidence, highlighting the importance of transparency and accountability in packaging solutions. The regulation also mandates sterility assurance, which is crucial for maintaining the integrity and safety of medical devices.