Global ENT Surgery Devices Market Report, size & Forecast 2026-2033

Global ENT Surgery Devices Market Forecast Snapshot (2026–2033)

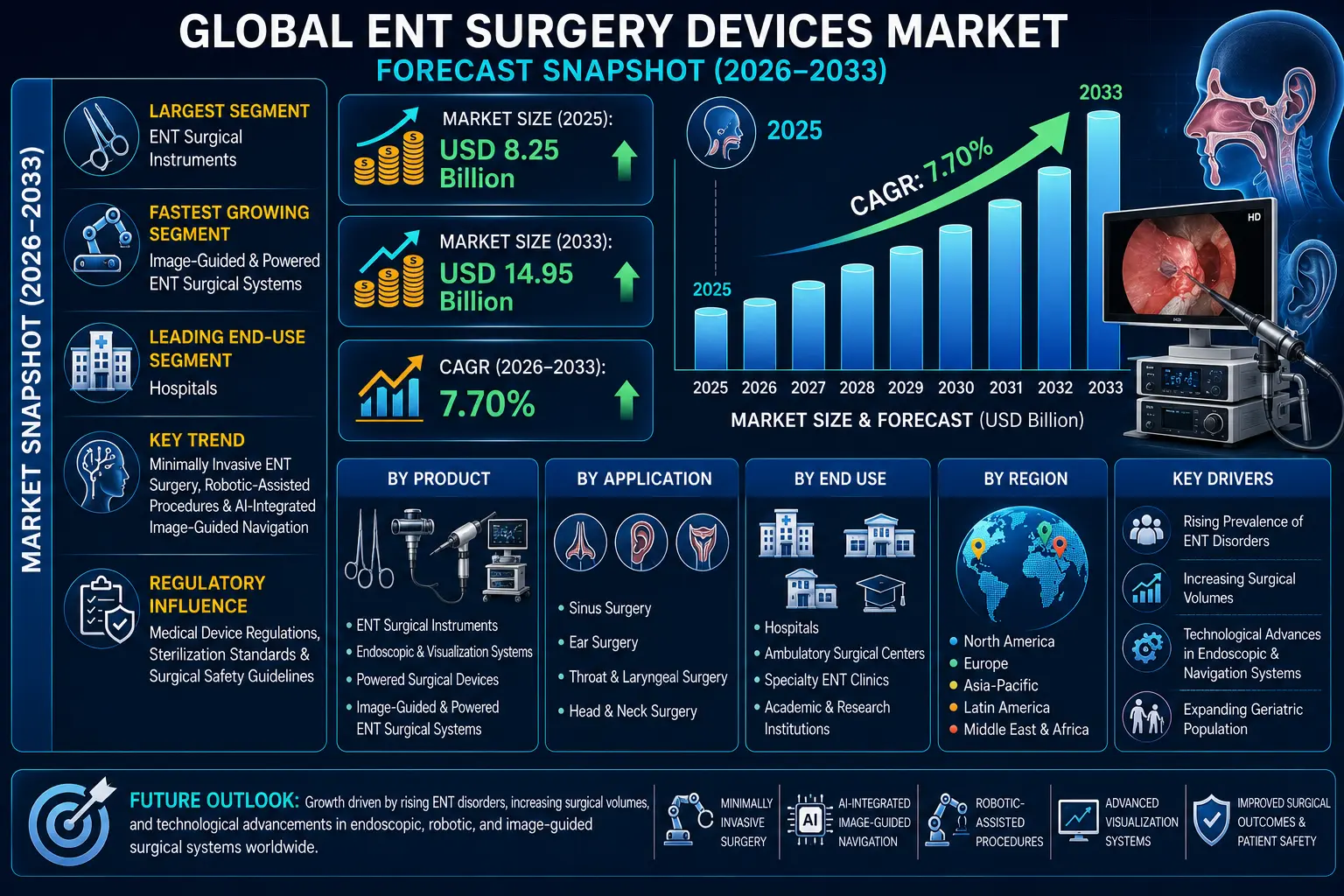

| Metric | Value |

|---|---|

| Market Size (2025) | USD 8.25 Billion |

| Market Size (2033) | USD 14.95 Billion |

| CAGR (2026–2033) | 7.70% |

| Largest Segment | ENT Surgical Instruments |

| Fastest Growing Segment | Image-Guided & Powered ENT Surgical Systems |

| Leading End-Use Segment | Hospitals |

| Key Trend | Minimally Invasive ENT Surgery, Robotic-Assisted Procedures & AI-Integrated Image-Guided Navigation |

| Regulatory Influence | Medical Device Regulations, Sterilization Standards & Surgical Safety Guidelines |

| Future Outlook | Growth Driven by Rising ENT Disorders, Increasing Surgical Volumes & Technological Advancements in Endoscopic and Navigation Systems |

Global ENT Surgery Devices Market Size & Forecast

The Global ENT Surgery Devices Market is expected to witness strong growth during the forecast period from 2026 to 2033. The market was valued at USD 8.25 billion in 2025 and is projected to reach approximately USD 14.95 billion by 2033, registering a CAGR of 7.70%. Market growth is primarily driven by the increasing prevalence of ear, nose, and throat disorders, rising incidence of chronic sinusitis and hearing loss, growing demand for minimally invasive surgical procedures, expanding geriatric population, and continuous innovation in endoscopic visualization, powered surgical instruments, and image-guided navigation technologies.Global ENT Surgery Devices Market Overview

ENT surgery devices are specialized medical instruments and systems used in the diagnosis and surgical treatment of disorders affecting the ear, nose, throat, head, and neck. The market includes handheld surgical instruments, powered surgical devices, endoscopes, visualization systems, laser systems, navigation platforms, and radiofrequency ablation devices. These products are widely utilized in hospitals, ambulatory surgical centers, specialty ENT clinics, and academic medical institutions for procedures including sinus surgery, tonsillectomy, adenoidectomy, cochlear implantation, laryngoscopy, and skull base surgery.Structural Drivers of Market Growth

1. Rising Prevalence of ENT Disorders

Increasing cases of chronic sinusitis, hearing impairment, obstructive sleep apnea, throat infections, and nasal disorders are driving demand for surgical interventions. Market Implications: Healthcare providers are expanding ENT surgical capabilities to address growing patient volumes.2. Growing Adoption of Minimally Invasive ENT Procedures

Endoscopic and image-guided surgical techniques reduce patient trauma, shorten hospital stays, and improve clinical outcomes. Market Implications: Demand for advanced endoscopic and powered surgical devices continues to increase.3. Technological Advancements in Surgical Navigation

AI-assisted navigation systems, high-definition imaging, and robotic-assisted technologies are improving surgical precision and safety. Market Implications: Advanced surgical platforms are enhancing physician confidence and procedural success rates.4. Expansion of Ambulatory Surgical Centers

Outpatient ENT procedures are increasing due to lower healthcare costs and improvements in minimally invasive surgical techniques. Market Implications: Manufacturers are developing compact, portable, and cost-efficient surgical systems for ambulatory care settings.Market Segmentation Analysis

By Product

- ENT Surgical Instruments Largest segment including forceps, speculums, curettes, scissors, retractors, and suction instruments used in routine ENT procedures.

- Endoscopic & Visualization Systems Includes rigid and flexible endoscopes, HD cameras, and visualization platforms for minimally invasive surgeries.

- Powered Surgical Devices Comprises microdebriders, drills, and powered handpieces used in sinus and skull base surgeries.

- Image-Guided & Powered ENT Surgical Systems Fastest-growing segment driven by increasing adoption of navigation-assisted surgical procedures.

By Application

- Sinus Surgery Largest application segment due to the high prevalence of chronic rhinosinusitis and nasal disorders.

- Ear Surgery Includes cochlear implantation, tympanoplasty, mastoidectomy, and hearing restoration procedures.

- Throat & Laryngeal Surgery Supports treatment of vocal cord disorders, tumors, and airway abnormalities.

- Head & Neck Surgery Includes oncologic procedures, thyroid surgery support, and reconstructive interventions.

By End Use

- Hospitals Largest segment supported by comprehensive surgical infrastructure and multidisciplinary ENT care.

- Ambulatory Surgical Centers Fast-growing segment driven by increasing outpatient ENT procedures.

- Specialty ENT Clinics Provide diagnostic, therapeutic, and minimally invasive surgical services.

- Academic & Research Institutions Support surgical training, clinical research, and technology evaluation.

Regional Market Dynamics

North America

Leading region supported by advanced surgical infrastructure, widespread adoption of minimally invasive ENT procedures, favorable reimbursement policies, and continuous investment in surgical technologies.Europe

Driven by increasing prevalence of ENT disorders, strong public healthcare systems, expanding adoption of image-guided surgery, and growing demand for advanced medical devices.Asia-Pacific

Fastest-growing region supported by expanding healthcare infrastructure, rising surgical volumes, growing healthcare expenditure, and increasing access to specialized ENT care.Latin America

Growing market driven by improving healthcare services, expanding hospital infrastructure, and increasing availability of advanced ENT surgical equipment.Middle East & Africa

Emerging market supported by healthcare modernization initiatives, increasing investments in surgical facilities, and growing awareness of advanced ENT treatment options.Competitive Landscape

The Global ENT Surgery Devices Market is highly competitive with medical device manufacturers focusing on minimally invasive technologies, surgical navigation systems, robotic platforms, and high-definition visualization equipment. Key Companies Operating in the Market Include:- Medtronic plc

- Karl Storz SE & Co. KG

- Stryker Corporation

- Olympus Corporation

- Johnson & Johnson (Ethicon)

- Smith+Nephew plc

- Richard Wolf GmbH

- Integra LifeSciences Holdings Corporation

- Cook Medical

- B. Braun SE

Strategic Outlook

The future of the ENT surgery devices market will be driven by advancements in robotic-assisted surgery, artificial intelligence, image-guided navigation, and high-definition endoscopic visualization. Manufacturers are increasingly investing in compact surgical systems, smart navigation platforms, and ergonomically designed powered instruments to improve precision, workflow efficiency, and patient outcomes. Integration of digital operating rooms and real-time surgical imaging will further support procedural accuracy. Growing demand for minimally invasive surgery, increasing outpatient procedures, expansion of specialty ENT centers, and continuous technological innovation will create substantial market opportunities. Companies focusing on AI-enabled surgical platforms, advanced visualization technologies, and comprehensive ENT procedural solutions will strengthen their competitive position in the global market.Final Market Perspective

The Global ENT Surgery Devices Market is expected to maintain strong growth as healthcare providers increasingly adopt advanced surgical technologies for the treatment of ear, nose, and throat disorders. Rising disease prevalence, technological innovation, expanding surgical infrastructure, and increasing demand for minimally invasive procedures will continue to support long-term market expansion. Organizations delivering innovative, safe, and high-performance ENT surgical solutions will be well-positioned to capitalize on future opportunities across the global medical device industry.Table of Contents

1. Executive Summary

1.1 Market Snapshot (2026–2033)

1.2 Key Growth Highlights

1.3 Demand-Supply Overview

1.4 Key Strategic Insights

1.5 Analyst Viewpoint

2. Market Overview

2.1 Introduction to Global ENT Surgery Devices Market

2.2 Industry Value Chain Analysis

2.3 Market Evolution & Historical Trends

2.4 Macro-Economic Impact Analysis

2.5 Rising Prevalence of ENT Disorders & Increasing Surgical Demand

2.6 Minimally Invasive ENT Surgery, AI-Guided Navigation & Robotic Surgical Transformation

3. Global ENT Surgery Devices Market Forecast Snapshot (USD Billion), 2026–2033

3.1 2025 Market Size

3.2 2033 Market Size

3.3 CAGR (2026–2033)

3.4 Largest Region

3.5 Fastest Growing Region

3.6 Largest Segment

3.7 Key Trend

3.8 Future Outlook

4. Key Drivers of Market Growth

4.1 Rising Prevalence of Ear, Nose & Throat Disorders

4.2 Growing Adoption of Minimally Invasive ENT Surgical Procedures

4.3 Technological Advancements in Image-Guided Navigation & Powered Surgical Systems

4.4 Increasing Surgical Volumes Across Hospitals & Ambulatory Surgical Centers

4.5 Continuous Innovation in Endoscopic Imaging, Robotics & AI-Assisted Surgery

5. Market Challenges

5.1 High Cost of Advanced ENT Surgical Equipment

5.2 Limited Access to Advanced ENT Care in Developing Regions

5.3 Regulatory Compliance & Product Approval Challenges

5.4 Shortage of Skilled ENT Surgeons & Technical Specialists

6. Market Segmentation by Product (USD Billion), 2026–2033

6.1 ENT Surgical Instruments

6.1.1 Handheld Surgical Instruments

6.1.1.1 Forceps

6.1.1.2 Scissors

6.1.1.3 Curettes

6.1.1.4 Speculums & Retractors

6.1.2 Suction & Dissection Instruments

6.1.2.1 Suction Tubes

6.1.2.2 Elevators

6.1.2.3 Dissectors

6.1.2.4 Surgical Hooks

6.2 Endoscopic & Visualization Systems

6.2.1 Rigid Endoscopes

6.2.1.1 Sinus Endoscopes

6.2.1.2 Otoscopes

6.2.1.3 Laryngoscopes

6.2.1.4 HD Camera Systems

6.3 Powered Surgical Devices

6.3.1 Microdebriders

6.3.1.1 Powered Handpieces

6.3.1.2 Surgical Drills

6.3.1.3 Burr Systems

6.3.1.4 Irrigation Systems

6.4 Image-Guided & Powered ENT Surgical Systems

6.4.1 Surgical Navigation Systems

6.4.2 AI-Guided Navigation Platforms

6.4.3 Robotic ENT Surgery Systems

6.4.4 Integrated Operating Room Solutions

7. Market Segmentation by Application (USD Billion), 2026–2033

7.1 Sinus Surgery

7.1.1 Functional Endoscopic Sinus Surgery (FESS)

7.1.2 Balloon Sinus Dilation

7.1.3 Nasal Polyp Removal

7.1.4 Revision Sinus Surgery

7.2 Ear Surgery

7.2.1 Cochlear Implantation

7.2.2 Tympanoplasty

7.2.3 Mastoidectomy

7.2.4 Stapedectomy

7.3 Throat & Laryngeal Surgery

7.3.1 Tonsillectomy

7.3.2 Adenoidectomy

7.3.3 Laryngoscopy Procedures

7.3.4 Vocal Cord Surgery

7.4 Head & Neck Surgery

7.4.1 Tumor Resection

7.4.2 Thyroid Surgery Support

7.4.3 Skull Base Surgery

7.4.4 Reconstructive Procedures

8. Market Segmentation by End Use (USD Billion), 2026–2033

8.1 Hospitals

8.1.1 Public Hospitals

8.1.2 Private Hospitals

8.1.3 Multispecialty Hospitals

8.1.4 Teaching Hospitals

8.2 Ambulatory Surgical Centers

8.2.1 Day Surgery Centers

8.2.2 Specialty Surgical Centers

8.2.3 Outpatient ENT Centers

8.2.4 Independent Surgical Facilities

8.3 Specialty ENT Clinics

8.3.1 ENT Diagnostic Clinics

8.3.2 Hearing Care Centers

8.3.3 Sinus Care Clinics

8.3.4 Voice & Airway Clinics

8.4 Academic & Research Institutions

8.4.1 Medical Universities

8.4.2 Clinical Research Centers

8.4.3 Surgical Training Institutes

8.4.4 Innovation Laboratories

9. Market Segmentation by Region (USD Billion), 2026–2033

9.1 North America

9.2 Europe

9.3 Asia-Pacific

9.4 Latin America

9.5 Middle East & Africa

10. Regional Market Analysis

10.1 North America – Market Leader

10.2 Asia-Pacific – Fastest Growing Region

10.3 Europe – Advanced ENT Surgical Devices Market

10.4 Latin America – Expanding Surgical Infrastructure

10.5 Middle East & Africa – Emerging ENT Healthcare Market

11. Competitive Landscape

11.1 Market Share Analysis

11.2 Competitive Positioning Matrix

11.3 Strategic Developments (M&A, Product Launches, Partnerships)

11.4 Innovation Benchmarking

11.5 Regulatory Compliance & Medical Device Assessment

12. Company Profiles

12.1 Medtronic plc

12.2 Karl Storz SE & Co. KG

12.3 Stryker Corporation

12.4 Olympus Corporation

12.5 Johnson & Johnson (Ethicon)

12.6 Smith+Nephew plc

12.7 Richard Wolf GmbH

12.8 Integra LifeSciences Holdings Corporation

12.9 Cook Medical

12.10 B. Braun SE

13. Strategic Intelligence & AI-Driven Insights

13.1 Pheonix Demand Forecast Engine

13.2 ENT Surgery Analytics Dashboard

13.3 AI-Powered Surgical Planning & Navigation Intelligence

13.4 Operating Room Performance Optimization Engine

13.5 Digital Surgery & Smart Hospital Intelligence

14. Investment & Growth Opportunities

14.1 Expansion of Image-Guided Surgical Systems

14.2 Robotic-Assisted ENT Surgery Platforms

14.3 AI-Based Surgical Navigation Technologies

14.4 Ambulatory Surgical Center Expansion

14.5 Emerging Market Healthcare Infrastructure Development

15. Why the Global ENT Surgery Devices Market Remains Critical

15.1 Rising Global Burden of ENT Disorders

15.2 Increasing Demand for Minimally Invasive Surgical Procedures

15.3 Continuous Innovation in Endoscopy, Robotics & AI Navigation

15.4 Expansion of Outpatient & Specialty ENT Care

15.5 Long-Term Growth Across the Global Medical Device Industry

16. Appendix

17. About Pheonix Research

18. Disclaimer

Competitive Landscape

Global ENT Surgery Devices Market Competitive Intensity & Market Structure Overview

The Global ENT Surgery Devices Market is highly competitive and characterized by the presence of multinational medical device manufacturers, surgical technology providers, endoscopy specialists, and healthcare equipment companies. Competitive intensity is driven by continuous innovation in minimally invasive surgical technologies, image-guided navigation systems, powered surgical instruments, robotic-assisted procedures, product reliability, regulatory approvals, and global distribution capabilities.

Companies compete across multiple product categories including ENT surgical instruments, endoscopic visualization systems, powered surgical devices, laser technologies, radiofrequency ablation systems, and image-guided navigation platforms. Increasing surgical volumes, growing prevalence of ENT disorders, and rising demand for precision-based surgical procedures are encouraging continuous product innovation and portfolio expansion.

The market structure is evolving toward digitally integrated operating rooms, AI-assisted surgical navigation, robotic technologies, and advanced visualization platforms. Market participants are investing in research and development, strategic acquisitions, product launches, surgeon training programs, and healthcare partnerships to strengthen technological capabilities and expand their global market presence.

Global ENT Surgery Devices Market Competitive Intensity & Market Structure Current Scenario

Leading Global ENT Surgery Devices Companies

- Medtronic plc: A global leader offering advanced ENT surgical systems, powered instruments, navigation platforms, and minimally invasive surgical technologies for otolaryngology procedures.

- Karl Storz SE & Co. KG: A leading provider of endoscopic visualization systems and minimally invasive surgical equipment with a strong presence across ENT surgery applications.

- Stryker Corporation: A major medical technology company delivering powered surgical instruments, imaging systems, and integrated surgical solutions supporting ENT procedures.

- Olympus Corporation: A global leader in endoscopy and visualization technologies offering advanced ENT imaging systems and minimally invasive surgical platforms.

- Johnson & Johnson (Ethicon): A diversified healthcare company providing surgical technologies, energy-based devices, and procedural solutions supporting ENT surgeries.

- Smith+Nephew plc: A medical technology company offering advanced surgical devices and minimally invasive technologies used across ENT and related surgical specialties.

- Richard Wolf GmbH: A specialized manufacturer of endoscopic systems, visualization technologies, and surgical instruments widely used in ENT procedures.

- Integra LifeSciences Holdings Corporation: A leading provider of surgical instruments and specialty medical technologies supporting cranial, head, neck, and ENT surgical interventions.

- Cook Medical: A global medical device company supplying minimally invasive devices and specialty procedural solutions for ENT and interventional applications.

- B. Braun SE: An international healthcare company offering surgical instruments, operating room technologies, and medical devices supporting ENT surgical care.

Key Competitive Intensity & Market Structure Drivers

Increasing prevalence of chronic sinusitis, hearing disorders, obstructive sleep apnea, and head and neck diseases is driving demand for advanced ENT surgical technologies and intensifying competition among global manufacturers.

Rapid technological advancements in robotic-assisted surgery, AI-enabled navigation systems, high-definition endoscopic visualization, and powered surgical instruments are becoming key competitive differentiators across the market.

Growing demand for minimally invasive procedures, outpatient surgical care, and precision-guided interventions is encouraging companies to develop compact, efficient, and technologically advanced surgical platforms.

Expansion of ambulatory surgical centers, modernization of hospital operating rooms, and increasing investments in healthcare infrastructure are creating new opportunities for device manufacturers worldwide.

Strategic mergers, acquisitions, product launches, distribution partnerships, and continuous investment in research and development are strengthening competitive positioning while accelerating technological innovation.

Strategic Implications of Competitive Intensity & Market Structure

Companies with comprehensive ENT product portfolios, strong innovation capabilities, and established global distribution networks are expected to maintain significant competitive advantages.

Investment in AI-assisted surgical navigation, robotic technologies, advanced endoscopic imaging, and surgeon education programs is becoming increasingly important for long-term market leadership.

Organizations focusing on regulatory compliance, product quality, workflow optimization, and minimally invasive surgical solutions are likely to strengthen market share and revenue growth.

Strategic collaborations with hospitals, ambulatory surgical centers, academic institutions, and healthcare providers are accelerating product adoption while supporting clinical validation and commercialization.

Businesses capable of combining technological innovation, surgical precision, regulatory excellence, comprehensive service support, and global commercial reach will be best positioned to compete effectively in the evolving global ENT surgery devices market.

Global ENT Surgery Devices Market Competitive Intensity & Market Structure Forward Outlook

The competitive landscape of the global ENT surgery devices market is expected to become increasingly technology-driven, digitally connected, and innovation-focused as healthcare providers continue adopting advanced surgical platforms.

Future competition will be shaped by AI-powered surgical navigation, robotic-assisted ENT procedures, high-definition visualization systems, smart operating room integration, augmented reality-assisted surgery, and next-generation powered surgical devices.

Market participants are expected to increase investments in product innovation, digital healthcare integration, surgeon training, clinical research, and global expansion strategies to strengthen competitive positioning.

Over the forecast period, companies that successfully combine technological innovation, clinical performance, regulatory compliance, advanced visualization capabilities, and comprehensive surgical solutions will be best positioned to lead the evolving global ENT surgery devices market.

Value Chain

Global ENT Surgery Devices Market Value Chain & Supply Chain Evolution Overview

The Global ENT Surgery Devices Market operates through a sophisticated medical device value chain encompassing product design, component sourcing, device manufacturing, sterilization, regulatory approval, distribution, hospital procurement, surgical implementation, and post-operative support. The market includes ENT surgical instruments, endoscopic visualization systems, powered surgical devices, image-guided navigation platforms, laser systems, radiofrequency ablation devices, and robotic-assisted surgical technologies utilized across hospitals, ambulatory surgical centers, specialty ENT clinics, and academic medical institutions.

The industry is driven by the increasing prevalence of ear, nose, and throat disorders, rising demand for minimally invasive procedures, growing surgical volumes, expanding healthcare infrastructure, and continuous innovation in endoscopic imaging, powered instrumentation, and AI-enabled navigation systems. Healthcare providers are increasingly investing in advanced surgical technologies to improve procedural precision, patient safety, and clinical outcomes.

The adoption of high-definition endoscopic visualization, robotic-assisted surgery, image-guided navigation, digital operating rooms, and AI-powered surgical planning has significantly enhanced workflow efficiency, surgical accuracy, and operating room productivity. Manufacturers are strengthening global supply chains while improving product quality, regulatory compliance, and technology integration.

Advancements in artificial intelligence, robotic surgical platforms, augmented reality navigation, cloud-connected operating rooms, advanced sterilization technologies, and predictive equipment maintenance are transforming the industry’s value chain while improving surgical precision, operational efficiency, and patient outcomes.

Global ENT Surgery Devices Market Value Chain & Supply Chain Evolution Current Scenario

Market-Specific Value Chain

- Research, Design & Product Development: Clinical research, device engineering, ergonomic design, prototype development, software integration, and product validation.

- Raw Material & Component Procurement: Procurement of surgical-grade stainless steel, titanium alloys, optical components, imaging sensors, electronic modules, precision motors, and medical-grade polymers.

- Manufacturing & Device Assembly: Precision machining, endoscope manufacturing, powered surgical device assembly, navigation system integration, software installation, and system calibration.

- Sterilization, Quality Assurance & Regulatory Compliance: Device sterilization, performance validation, quality inspections, regulatory approvals, and compliance with international medical device standards.

- Distribution & Healthcare Procurement: Distribution through medical device suppliers, hospital procurement departments, group purchasing organizations (GPOs), and regional distributors.

- Surgical Deployment & Clinical Utilization: Installation, surgeon training, intraoperative use, equipment servicing, technical support, and workflow optimization.

- Post-Surgical Support & Lifecycle Management: Preventive maintenance, software updates, equipment servicing, replacement components, and long-term technical support.

Company-to-Stage Mapping

- Research, Design & Product Development: Medical device manufacturers, R&D centers, biomedical engineering teams, software developers, and clinical research organizations.

- Raw Material & Component Procurement: Suppliers of surgical metals, optical lenses, electronic components, imaging systems, precision motors, and medical-grade materials.

- Manufacturing & Device Assembly: Medtronic plc, Karl Storz SE & Co. KG, Stryker Corporation, Olympus Corporation, Johnson & Johnson (Ethicon), Smith+Nephew plc, Richard Wolf GmbH, Integra LifeSciences Holdings Corporation, Cook Medical, and B. Braun SE.

- Sterilization, Quality Assurance & Regulatory Compliance: Regulatory agencies, quality certification organizations, sterilization service providers, and medical device testing laboratories.

- Distribution & Healthcare Procurement: Medical device distributors, hospital procurement departments, group purchasing organizations (GPOs), healthcare distributors, and regional sales partners.

- Surgical Deployment & Clinical Utilization: Hospitals, ambulatory surgical centers, specialty ENT clinics, surgeons, operating room staff, and biomedical engineering teams.

- Post-Surgical Support & Lifecycle Management: Equipment service providers, OEM technical support teams, software maintenance providers, and hospital biomedical engineering departments.

Key Value Chain & Supply Chain Evolution Signals in Global ENT Surgery Devices Market

Expansion of Image-Guided Surgical Navigation

Healthcare providers are increasingly adopting image-guided navigation systems to improve surgical precision, reduce complications, and enhance patient safety during complex ENT procedures.

Growing Adoption of Robotic-Assisted ENT Surgery

Robotic surgical platforms are improving visualization, instrument control, and procedural accuracy while enabling minimally invasive surgical approaches.

Increasing Integration of AI and Digital Operating Rooms

Artificial intelligence, real-time imaging, and connected operating room technologies are optimizing surgical planning, workflow management, and clinical decision support.

Advancements in High-Definition Endoscopic Visualization

Next-generation endoscopic imaging systems are providing enhanced visualization, improved tissue differentiation, and greater surgical precision.

Expansion of Ambulatory Surgical Centers

Growing outpatient ENT procedures are increasing demand for compact, portable, and cost-efficient surgical systems designed for ambulatory care environments.

Strengthening Global Medical Device Supply Chains

Manufacturers are improving supplier diversification, localized manufacturing, inventory management, and logistics resilience to ensure uninterrupted device availability.

Strategic Implications of Value Chain & Supply Chain Evolution

Investment in Smart Surgical Technologies

Organizations investing in AI-enabled navigation systems, robotic platforms, and advanced visualization technologies can improve surgical outcomes and strengthen market competitiveness.

Expansion of Digital Operating Room Integration

Integrated surgical ecosystems improve workflow efficiency, equipment connectivity, data management, and multidisciplinary collaboration.

Strengthening Manufacturing and Quality Systems

Advanced manufacturing technologies and rigorous quality management enhance product reliability, regulatory compliance, and operational efficiency.

Optimization of Medical Device Distribution Networks

Efficient logistics, regional warehousing, and responsive technical support improve product availability and customer satisfaction.

Enhancement of Surgeon Training and Clinical Support

Comprehensive education programs, simulation platforms, and ongoing technical assistance improve technology adoption and procedural performance.

Leveraging Connected Healthcare Ecosystems

Collaboration among manufacturers, hospitals, digital health providers, and surgical specialists strengthens innovation, patient care, and long-term technology adoption.

Global ENT Surgery Devices Market Value Chain & Supply Chain Evolution Forward Outlook

Looking ahead, the ENT surgery devices value chain is expected to become increasingly intelligent, automated, and digitally connected. Continued advances in artificial intelligence, robotic-assisted surgery, augmented reality navigation, cloud-enabled operating rooms, advanced imaging technologies, and predictive equipment management will further transform surgical workflows while improving clinical outcomes and operational efficiency.

Key Future Developments Include:

- Expansion of AI-assisted surgical navigation and intraoperative decision-support systems.

- Increasing adoption of robotic-assisted ENT surgical platforms across healthcare facilities.

- Greater deployment of high-definition and 3D endoscopic visualization technologies.

- Broader implementation of connected digital operating rooms and cloud-based surgical data platforms.

- Growing use of predictive maintenance and smart equipment lifecycle management.

- Strengthening resilient global supply chains through localized manufacturing and strategic sourcing.

As the market evolves, competitive advantage will increasingly depend on technological innovation, product reliability, regulatory compliance, manufacturing excellence, digital integration, and comprehensive clinical support capabilities.

Companies that successfully integrate AI-powered surgical platforms, advanced visualization systems, robotic technologies, resilient supply chain strategies, and connected operating room solutions will be well-positioned to achieve long-term growth in the Global ENT Surgery Devices Market.

Investment Activity

Global ENT Surgery Devices Market Investment & Funding Dynamics Overview (2026–2033)

The Global ENT Surgery Devices Market is witnessing robust investment activity driven by the increasing prevalence of ear, nose, and throat disorders, growing demand for minimally invasive surgical procedures, expanding surgical infrastructure, and rapid advancements in image-guided and robotic-assisted surgical technologies. Medical device manufacturers, healthcare technology companies, venture capital firms, institutional investors, hospitals, and research organizations are actively investing in advanced endoscopic systems, powered surgical instruments, AI-integrated surgical navigation platforms, robotic-assisted ENT surgery, high-definition visualization technologies, and smart operating room solutions.

Investment momentum is accelerating as healthcare providers focus on improving surgical precision, reducing procedural complications, and enhancing patient outcomes through technology-enabled ENT interventions. Capital allocation is increasingly directed toward image-guided navigation systems, AI-assisted surgical planning, robotic surgical platforms, powered microdebriders, advanced endoscopic imaging systems, and digital operating room integration.

Additionally, growing investments in minimally invasive surgical innovation, medical imaging technologies, surgical robotics, digital healthcare infrastructure, and collaborative clinical research programs are creating substantial long-term opportunities across the global ENT surgery devices ecosystem.

Current Investment & Funding Landscape

The current investment landscape reflects strong participation from medical device manufacturers, healthcare technology companies, private equity investors, venture capital firms, academic medical centers, hospitals, and research institutions. Industry participants are investing heavily in product innovation, surgical navigation technologies, AI-enabled imaging systems, operating room modernization, advanced visualization platforms, global commercialization strategies, and next-generation ENT surgical solutions.

Significant funding is being directed toward robotic-assisted surgery development, clinical validation of navigation technologies, high-definition endoscopic imaging, powered surgical instrument innovation, digital workflow optimization, and surgeon training programs to improve procedural efficiency and strengthen long-term market positioning.

Strategic collaborations among medical device manufacturers, hospitals, academic institutions, healthcare providers, digital health companies, and surgical technology developers are accelerating innovation and expanding adoption of advanced ENT surgical technologies worldwide.

Key Investment & Funding Dynamics Signals

- Growing demand for minimally invasive ENT surgery and image-guided navigation technologies is driving increased investment in advanced surgical platforms.

- Expansion of robotic-assisted surgery, AI-integrated visualization systems, and digital operating rooms is attracting significant funding from public and private investors.

- Increasing investment in high-definition endoscopy, powered surgical devices, and intelligent navigation systems is improving surgical precision and clinical outcomes.

- Rising funding for surgical innovation, operating room modernization, and advanced ENT treatment technologies is accelerating innovation across healthcare systems.

- Strategic investment in AI-powered surgical planning, real-time imaging platforms, and integrated surgical workflow solutions is strengthening physician decision-making and procedural efficiency.

- Growing collaboration between medical device manufacturers, healthcare providers, academic institutions, and technology companies is accelerating product development and global market expansion.

- Expansion into emerging healthcare markets with increasing investments in hospital infrastructure and advanced surgical capabilities is creating attractive long-term investment opportunities.

Strategic Implications of Investment & Funding Dynamics

- Continuous investment in image-guided surgery, robotic-assisted platforms, and AI-powered surgical technologies will be essential for sustaining long-term competitive advantage.

- Capital allocation toward advanced endoscopic systems, digital operating rooms, and smart surgical navigation platforms will strengthen commercialization opportunities.

- Companies developing integrated ENT surgical ecosystems, scalable medical device platforms, and strong intellectual property portfolios are expected to secure stronger market positions.

- Strategic partnerships among medical device manufacturers, hospitals, healthcare providers, academic institutions, and technology developers will accelerate product innovation and market growth.

- Investments in AI-assisted navigation, robotic surgery, advanced visualization systems, powered surgical instruments, and digital surgical infrastructure will enhance clinical outcomes and operational efficiency.

- Compliance with medical device regulations, sterilization standards, surgical safety guidelines, and healthcare quality requirements will continue influencing investment decisions.

- Organizations building integrated capabilities across surgical device development, digital health technologies, regulatory affairs, manufacturing, and global commercialization are expected to capture significant long-term value.

Forward Outlook

Looking ahead, the Global ENT Surgery Devices Market is expected to maintain strong investment momentum driven by rising ENT surgical volumes, increasing adoption of minimally invasive procedures, growing implementation of AI-powered surgical technologies, and continued modernization of operating rooms.

Future capital deployment will increasingly focus on robotic-assisted ENT surgery, image-guided navigation platforms, AI-assisted surgical planning, advanced endoscopic visualization systems, powered surgical instruments, and digital operating room technologies.

As healthcare providers continue investing in advanced surgical capabilities and smart operating room infrastructure, investment activity is expected to expand across ENT surgical instruments, endoscopic imaging, surgical robotics, navigation systems, digital healthcare technologies, and minimally invasive procedural solutions.

In conclusion, the Global ENT Surgery Devices Market represents a highly attractive medical technology investment landscape where artificial intelligence, robotic-assisted surgery, image-guided navigation, advanced visualization technologies, and minimally invasive surgical innovation will define future funding priorities, competitive differentiation, and long-term market expansion.

Technology & Innovation

Global ENT Surgery Devices Market Technology & Innovation Landscape Overview

The Global ENT Surgery Devices Market is undergoing rapid technological transformation as minimally invasive surgical techniques, robotic-assisted procedures, artificial intelligence (AI), image-guided navigation, high-definition endoscopy, and advanced energy-based surgical systems redefine otolaryngology care. Hospitals, ambulatory surgical centers, and specialty ENT clinics are increasingly investing in next-generation surgical technologies to improve procedural precision, enhance visualization, reduce surgical trauma, and optimize patient outcomes. These innovations are enabling surgeons to perform complex ENT procedures with greater accuracy while minimizing complications and shortening patient recovery times.

The market is also benefiting from advancements in digital operating rooms, three-dimensional (3D) imaging, intraoperative navigation systems, smart powered surgical instruments, and cloud-enabled surgical data platforms. These technologies are improving workflow efficiency, enhancing real-time clinical decision-making, supporting surgical training, and facilitating better procedural planning. As demand for advanced ENT procedures and personalized surgical care continues to increase, technology is becoming a key driver of innovation, operational excellence, and long-term market growth.

Global ENT Surgery Devices Market Technology & Innovation Current Scenario

Current innovation within the ENT surgery devices market is primarily focused on AI-assisted surgical navigation, robotic-assisted ENT procedures, high-definition endoscopic visualization, image-guided surgical systems, and intelligent powered surgical devices. Healthcare providers are rapidly adopting navigation platforms integrated with real-time imaging and advanced visualization technologies to improve precision during sinus, skull base, ear, and head & neck surgeries. These technologies are enabling surgeons to accurately identify anatomical structures while reducing procedural risks and improving clinical outcomes.

Automation and digital technologies including robotic surgical platforms, smart microdebriders, powered drills, laser-assisted systems, and radiofrequency ablation devices are improving surgical efficiency and consistency. In addition, advances in augmented reality (AR), three-dimensional visualization, intraoperative imaging, and AI-powered surgical planning are enhancing complex ENT procedures. Artificial intelligence is increasingly supporting image interpretation, anatomical mapping, navigation guidance, and workflow optimization, enabling greater surgical confidence and improved patient safety.

Key Technology & Innovation Trends in Global ENT Surgery Devices Market

- AI-Integrated Surgical Navigation: Utilizing artificial intelligence to improve anatomical mapping, surgical planning, navigation accuracy, and intraoperative decision support.

- Robotic-Assisted ENT Surgery: Expanding the use of robotic platforms for minimally invasive head & neck, laryngeal, and transoral surgical procedures with enhanced precision.

- High-Definition Endoscopic Visualization: Delivering superior image clarity through HD and 4K endoscopy systems for improved visualization during minimally invasive ENT surgeries.

- Image-Guided Surgery Systems: Enhancing surgical accuracy with real-time navigation technologies for sinus, skull base, and complex anatomical procedures.

- Advanced Powered Surgical Instruments: Improving procedural efficiency through intelligent microdebriders, surgical drills, and powered handpieces designed for precise tissue removal.

- Laser & Radiofrequency Surgical Technologies: Supporting minimally invasive tissue ablation with improved precision, reduced bleeding, and faster postoperative recovery.

- Augmented Reality (AR) Surgical Guidance: Integrating digital overlays with intraoperative imaging to improve anatomical orientation and surgical visualization.

- Digital Operating Room Integration: Connecting imaging systems, surgical devices, patient data, and workflow management platforms to improve procedural coordination and efficiency.

- Smart Surgical Data Analytics: Leveraging real-time procedural data and performance analytics to optimize surgical outcomes, quality assurance, and clinician training.

- Cloud-Based Surgical Connectivity: Enabling secure storage, remote collaboration, surgical planning, and post-procedure documentation across healthcare networks.

Strategic Implications of Technology & Innovation

Technological advancements are enabling hospitals, ambulatory surgical centers, and medical device manufacturers to improve surgical precision, increase operational efficiency, and strengthen competitive positioning. Organizations investing in robotic-assisted surgery, AI-enabled navigation, advanced visualization systems, and digital operating room technologies are accelerating minimally invasive surgical adoption while improving patient outcomes and procedural consistency.

As ENT surgery becomes increasingly integrated within digitally connected healthcare ecosystems, organizations are focusing on interoperable surgical platforms, intelligent imaging technologies, and data-driven clinical workflows. Companies that successfully combine automation, artificial intelligence, advanced visualization, and precision surgical technologies are expected to gain significant competitive advantages. However, regulatory compliance, medical device safety, cybersecurity, clinical validation, surgeon training, and interoperability remain critical considerations for successful technology adoption and commercialization.

Global ENT Surgery Devices Market Technology & Innovation Forward Outlook

The future of the Global ENT Surgery Devices Market is expected to be shaped by continued advancements in artificial intelligence, robotic-assisted surgery, augmented reality, image-guided navigation, digital operating rooms, and intelligent visualization technologies. Emerging innovations such as AI-powered intraoperative guidance, autonomous robotic assistance, predictive surgical analytics, mixed reality visualization, and next-generation navigation platforms are expected to redefine ENT surgical practice. Companies are likely to increase investments in scalable surgical technologies, advanced imaging systems, and integrated digital surgery ecosystems to improve procedural efficiency and expand precision surgical capabilities.

As demand for minimally invasive procedures, precision surgery, and technologically advanced operating environments continues to grow, innovation will play an increasingly important role in driving market evolution. The convergence of AI, robotics, cloud connectivity, navigation systems, advanced endoscopy, and digital surgical platforms is expected to create significant growth opportunities while accelerating the long-term transformation of the global ENT surgery devices market.

Market Risk

Global ENT Surgery Devices Market Risk Factors & Disruption Threats Overview

The Global ENT Surgery Devices Market operates within the broader medical devices, surgical technologies, minimally invasive surgery, and healthcare infrastructure ecosystem. While the market benefits from the rising prevalence of ear, nose, and throat disorders, increasing surgical volumes, and continuous technological innovation, it faces several risks related to regulatory compliance, reimbursement pressures, supply chain disruptions, high capital investment requirements, and rapid technological evolution.

One of the most significant structural risks is the increasingly stringent regulatory environment governing medical devices. Manufacturers must comply with evolving international regulations, sterilization standards, product safety requirements, clinical evidence expectations, and post-market surveillance obligations. Delays in regulatory approvals or non-compliance can significantly affect product commercialization and market expansion.

The market is also exposed to supply chain vulnerabilities involving precision surgical components, optical systems, semiconductors, and specialized medical-grade materials. Disruptions in global manufacturing, logistics, or raw material availability may delay production schedules, increase procurement costs, and affect product availability for healthcare providers.

Another major disruption factor involves the high capital cost associated with advanced ENT surgical technologies, including image-guided navigation systems, robotic-assisted platforms, powered surgical devices, and high-definition visualization equipment. Budget constraints and limited reimbursement may slow adoption, particularly among smaller hospitals and healthcare facilities in emerging markets.

Additionally, increasing competition among medical device manufacturers, surgical technology companies, and digital health providers is intensifying pricing pressure while accelerating innovation across AI-assisted navigation, robotic surgery, advanced endoscopy, and integrated operating room solutions.

Global ENT Surgery Devices Market Risk Factors & Disruption Threats Current Scenario

The current market environment is characterized by increasing adoption of minimally invasive ENT procedures, high-definition endoscopic visualization, image-guided navigation systems, powered surgical instruments, and AI-assisted surgical planning technologies. Healthcare providers continue investing in advanced surgical platforms to improve procedural precision, reduce complications, and enhance patient outcomes.

However, the industry remains affected by regulatory complexity, rising healthcare cost pressures, shortages of trained ENT surgeons in certain regions, and significant capital investment requirements for advanced surgical systems. These challenges continue to influence purchasing decisions and technology adoption across healthcare organizations.

Healthcare providers are increasingly demanding integrated surgical solutions that combine advanced imaging, navigation technologies, real-time visualization, and ergonomic powered instruments to improve surgical workflow, accuracy, and operating room efficiency.

Regulatory authorities are strengthening oversight related to medical device safety, software validation, sterilization protocols, cybersecurity for connected surgical systems, and quality management standards, requiring continuous investment in compliance and product lifecycle management.

Meanwhile, competitive intensity continues to increase as global medical device companies expand product portfolios through innovation, strategic acquisitions, research collaborations, and investments in AI-enabled surgical technologies and digital operating room ecosystems.

Key Risk Factors & Disruption Threat Signals in Global ENT Surgery Devices Market

A major disruption signal is the accelerating adoption of artificial intelligence, robotic-assisted surgery, image-guided navigation, and augmented visualization technologies that enable greater surgical precision, workflow optimization, and improved patient safety. Companies that fail to invest in these innovations may experience declining market competitiveness.

Another important signal is the growing shift toward minimally invasive and outpatient ENT procedures, increasing demand for compact, portable, and highly efficient surgical systems suitable for ambulatory surgical centers and specialty clinics.

The convergence of artificial intelligence, robotic platforms, digital imaging, cloud connectivity, and advanced navigation technologies is transforming ENT surgery into a more intelligent, data-driven, and precision-focused surgical discipline.

Advancements in high-definition imaging, three-dimensional visualization, augmented reality guidance, powered instrumentation, and real-time intraoperative navigation are continuously improving procedural accuracy while reducing surgical complications and recovery times.

Growing emphasis on healthcare efficiency, patient safety, infection prevention, and operating room optimization is encouraging healthcare providers to invest in integrated surgical technologies that enhance clinical outcomes and operational productivity.

The expansion of digital operating rooms, connected surgical ecosystems, and remote clinical collaboration platforms is reshaping surgical workflows while creating new opportunities for innovation, training, and procedural standardization.

Strategic Implications of Risk Factors & Disruption Threats in Global ENT Surgery Devices Market

Medical device manufacturers should prioritize investments in artificial intelligence, robotic-assisted surgery, image-guided navigation systems, advanced visualization technologies, and minimally invasive surgical platforms to improve procedural performance and strengthen competitive positioning.

Companies should strengthen supply chain resilience by diversifying manufacturing operations, securing critical component suppliers, improving inventory management, and expanding regional production capabilities to reduce operational risks.

Organizations should accelerate development of interoperable surgical platforms capable of integrating imaging systems, navigation technologies, hospital information systems, and digital operating room infrastructure to improve workflow efficiency and clinical decision-making.

Investment in clinician education, surgical simulation, technical training, and post-market clinical support can improve technology adoption while maximizing the clinical value of advanced ENT surgical systems.

Strategic collaborations among medical device manufacturers, hospitals, academic institutions, research organizations, and digital technology providers can accelerate innovation, product validation, and commercialization of next-generation ENT surgical solutions.

Manufacturers should continuously monitor evolving medical device regulations, sterilization standards, cybersecurity requirements, surgical safety guidelines, and international quality management frameworks to ensure long-term compliance and sustainable market growth.

Global ENT Surgery Devices Market Risk Factors & Disruption Threats Forward Outlook

Looking ahead to 2026–2033, the Global ENT Surgery Devices Market is expected to maintain strong growth as healthcare systems continue modernizing surgical infrastructure and expanding access to minimally invasive ENT procedures. Future market expansion will increasingly depend on technological innovation, regulatory adaptability, affordability, and integration of intelligent surgical platforms.

Artificial intelligence, robotic-assisted procedures, image-guided navigation, advanced endoscopic visualization, augmented reality, and digital operating room technologies are expected to become key competitive differentiators, enabling greater surgical precision, improved workflow efficiency, and enhanced patient outcomes.

Medical device regulations, sterilization standards, cybersecurity requirements, and software validation frameworks are likely to become increasingly rigorous as connected surgical technologies and AI-enabled medical devices gain broader clinical adoption.

Growing adoption of outpatient surgery, expansion of ambulatory surgical centers, increasing demand for personalized surgical planning, and broader implementation of integrated digital healthcare ecosystems will continue supporting demand for advanced ENT surgical technologies.

Technological convergence across artificial intelligence, robotics, cloud computing, surgical navigation, advanced imaging, and digital health platforms will continue reshaping ENT surgery while creating significant opportunities for product innovation and healthcare transformation.

Overall, the market will remain strongly growth-oriented but increasingly influenced by AI innovation, minimally invasive surgery, regulatory evolution, digital operating rooms, and precision surgical technologies. Long-term market leaders will be defined by their ability to deliver intelligent, safe, scalable, and clinically integrated ENT surgical solutions that improve procedural efficiency and patient care across the evolving global healthcare ecosystem.

Regulatory Landscape

Global ENT Surgery Devices Market Regulatory & Policy Environment Overview

The regulatory and policy environment governing the Global ENT Surgery Devices Market is becoming increasingly significant as healthcare providers adopt advanced surgical technologies for the diagnosis and treatment of ear, nose, and throat disorders. Regulatory authorities, medical device agencies, healthcare accreditation bodies, and international standards organizations establish comprehensive frameworks governing medical device safety, product quality, sterilization, clinical performance, software validation, and post-market surveillance to ensure safe and effective surgical outcomes.

Manufacturers of ENT surgical instruments, endoscopic visualization systems, powered surgical devices, image-guided navigation platforms, robotic-assisted surgical technologies, and radiofrequency ablation systems must comply with stringent regulations covering Good Manufacturing Practice (GMP), Quality Management Systems (QMS), medical device regulations, sterilization standards, biocompatibility requirements, and clinical evaluation guidelines. Regulatory compliance is essential to ensure product reliability, patient safety, and successful commercialization across global healthcare markets.

As minimally invasive surgery, robotic-assisted procedures, AI-integrated surgical navigation, and digital operating rooms continue advancing, policymakers are strengthening regulatory oversight while encouraging innovation, interoperability, cybersecurity, and evidence-based surgical practices.

Global ENT Surgery Devices Market Regulatory & Policy Environment Current Scenario

The current regulatory landscape primarily focuses on medical device safety, surgical quality, sterilization validation, clinical effectiveness, software reliability, and post-market monitoring. Manufacturers are required to demonstrate compliance with rigorous quality and performance standards before receiving regulatory approval for commercial distribution.

Medical device regulations govern the design, manufacturing, clinical evaluation, labeling, and lifecycle management of ENT surgical devices, ensuring safety, effectiveness, and consistent product performance throughout clinical use.

Sterilization standards establish validated requirements for sterilization processes, infection prevention, packaging integrity, reprocessing instructions for reusable instruments, and contamination control to minimize the risk of healthcare-associated infections.

Clinical evaluation and surgical safety guidelines support evidence-based adoption of advanced ENT technologies by establishing requirements for clinical performance validation, human factors engineering, usability assessment, and surgeon training.

Healthcare authorities continue strengthening post-market surveillance, adverse event reporting, cybersecurity oversight for connected surgical systems, and quality monitoring to ensure ongoing compliance and patient safety throughout the product lifecycle.

Key Regulatory & Policy Environment Signals in Global ENT Surgery Devices Market

- Medical Device Regulations:

Frameworks governing product development, clinical evaluation, manufacturing quality, labeling, safety certification, software validation, and regulatory approval for ENT surgical devices. - Sterilization & Infection Prevention Standards:

Requirements supporting validated sterilization processes, packaging integrity, contamination control, reusable device reprocessing, and infection prevention practices. - Quality Management Systems (QMS) & Good Manufacturing Practice (GMP):

Standards promoting manufacturing consistency, quality assurance, risk management, documentation, product traceability, and continuous process improvement. - Clinical Evaluation & Surgical Safety Guidelines:

Policies governing clinical performance validation, usability testing, human factors engineering, surgeon training, and evidence-based surgical practices. - Digital Health & Connected Medical Device Regulations:

Guidelines addressing AI-enabled navigation systems, connected surgical platforms, interoperability, software lifecycle management, cybersecurity, and data security. - Post-Market Surveillance & Vigilance Requirements:

Regulations supporting adverse event reporting, field safety corrective actions, product recalls, long-term device performance monitoring, and continuous regulatory oversight.

Strategic Implications of Regulatory & Policy Environment

The evolving regulatory environment is encouraging medical device manufacturers, healthcare providers, and surgical technology companies to strengthen regulatory affairs capabilities, quality management systems, clinical evidence generation, and compliance programs. Regulatory readiness has become a critical competitive advantage in the global ENT surgical device industry.

Increasing medical device and sterilization requirements are driving investments in advanced manufacturing technologies, validated sterilization methods, high-quality materials, automated quality control systems, and lifecycle risk management to enhance product safety and regulatory compliance.

Growing regulatory oversight of AI-integrated navigation systems, robotic-assisted surgery, and digital operating room technologies is encouraging manufacturers to improve software validation, cybersecurity protection, interoperability, and real-world clinical performance evaluation.

Expanding emphasis on clinical safety and healthcare quality is motivating organizations to strengthen surgeon education, standardized surgical protocols, post-market surveillance programs, and evidence-based product development to improve patient outcomes and market acceptance.

Companies capable of maintaining regulatory compliance, demonstrating superior clinical performance, and delivering safe, innovative, and technologically advanced ENT surgical solutions will be well positioned to strengthen their leadership within the global medical device market.

Global ENT Surgery Devices Market Regulatory & Policy Environment Forward Outlook

Between 2026 and 2033, the regulatory environment for the Global ENT Surgery Devices Market is expected to become increasingly comprehensive as minimally invasive surgery, robotic-assisted technologies, AI-driven surgical navigation, and digital operating rooms continue expanding across healthcare systems worldwide.

Healthcare authorities are expected to strengthen medical device regulations through enhanced clinical evidence requirements, software validation standards, cybersecurity frameworks, quality management expectations, and expanded post-market surveillance for advanced surgical technologies.

Regulatory agencies are likely to place greater emphasis on international harmonization of medical device standards, sterilization protocols, interoperability requirements, electronic regulatory submissions, and lifecycle quality management to facilitate global commercialization while maintaining patient safety.

Policymakers are also expected to encourage greater adoption of intelligent surgical technologies, standardized surgical quality measures, digital health integration, and value-based healthcare initiatives that improve procedural outcomes and healthcare efficiency.

Overall, the future regulatory landscape will be shaped by the convergence of medical device regulations, sterilization standards, surgical safety guidelines, Good Manufacturing Practice (GMP) requirements, Quality Management Systems (QMS), digital health governance, cybersecurity frameworks, and post-market surveillance requirements. Organizations capable of delivering compliant, innovative, high-quality, and patient-centric ENT surgical solutions will be best positioned to capitalize on long-term growth opportunities within the expanding global surgical device and healthcare technology market.