Global eSIM Market Size and Share Analysis 2026-2033

Global eSIM Market Size & Forecast

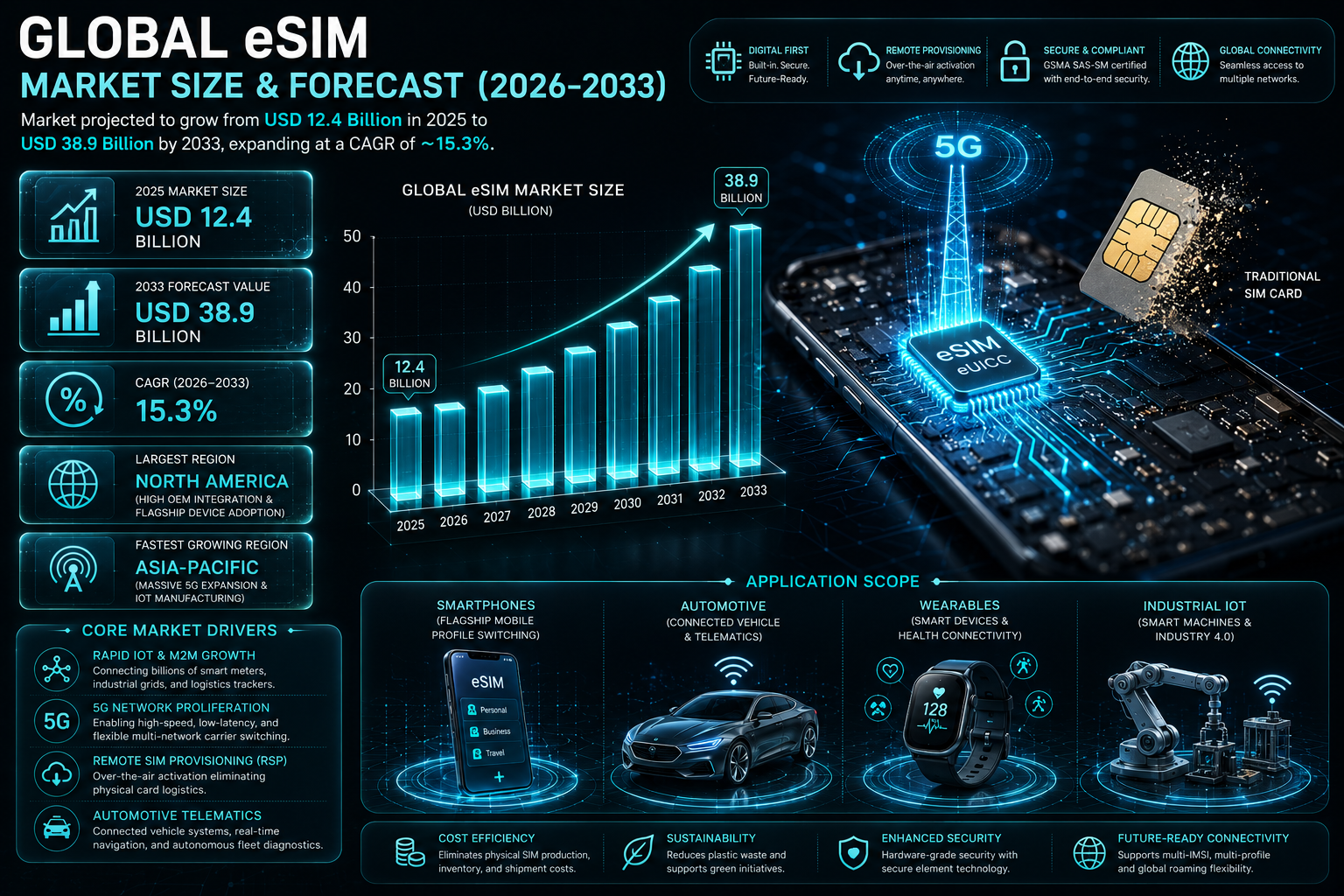

The global eSIM market is projected to witness exponential growth during the forecast period from 2026 to 2033. The market was valued at approximately USD 12.4 billion in 2025 and is expected to reach nearly USD 38.9 billion by 2033, expanding at a CAGR of around 15.3%. The market growth is driven by the rapid expansion of IoT connectivity, increasing adoption of smart devices, rising demand for seamless mobile network switching, and strong penetration of 5G-enabled smartphones and connected devices. eSIM (embedded SIM) is a digital SIM technology embedded directly into devices, eliminating the need for physical SIM cards. It enables remote provisioning of mobile network profiles and allows users to switch carriers without replacing SIM cards, significantly improving flexibility and connectivity management. The market is experiencing strong momentum due to increasing demand for connected devices, wearable technology, automotive telematics, and industrial IoT applications. The growing trend toward digital transformation and eSIM-enabled global roaming solutions is further accelerating adoption.

Global eSIM Market Overview

The eSIM market is a key segment of the global telecommunications and connected devices ecosystem. It supports seamless connectivity across smartphones, tablets, laptops, wearables, smart meters, automotive systems, and IoT-enabled industrial devices. Telecom operators, device manufacturers, and enterprise IoT providers are increasingly adopting eSIM technology to simplify connectivity management and reduce dependency on physical SIM logistics. The ecosystem includes eSIM hardware providers, mobile network operators (MNOs), mobile virtual network operators (MVNOs), device OEMs, and eSIM platform service providers. Advancements in remote SIM provisioning (RSP), embedded secure elements, and GSMA standards are enabling large-scale global deployment of eSIM technology. Major market participants include Apple Inc., Samsung Electronics, Qualcomm Technologies, Thales Group, STMicroelectronics, Giesecke+Devrient, NXP Semiconductors, Deutsche Telekom, Vodafone Group, AT&T Inc., and STC Group.Key Drivers of Global eSIM Market Growth

Rapid Adoption of Connected Devices

The increasing number of smartphones, wearables, tablets, laptops, and IoT devices is driving demand for embedded connectivity solutions. eSIM technology simplifies device activation and enables instant network connectivity across global markets.Expansion of IoT and M2M Communications

eSIM plays a critical role in machine-to-machine (M2M) communication and IoT ecosystems, enabling remote device management and scalable connectivity. Industries such as automotive, healthcare, logistics, and smart cities are major adopters.Growth of 5G Networks

The global rollout of 5G networks is significantly boosting eSIM adoption due to its ability to support high-speed, low-latency, and flexible connectivity solutions. eSIM enhances multi-network switching capabilities required for advanced 5G applications.Increasing Demand for Seamless Roaming

International travelers and global enterprises are increasingly adopting eSIM solutions for hassle-free roaming and multi-country connectivity. This eliminates the need for physical SIM swaps and reduces roaming costs.Rising Adoption in Automotive Sector

Connected vehicles, infotainment systems, telematics, and autonomous driving technologies are increasingly integrated with eSIM technology. Automotive manufacturers are embedding eSIMs for real-time navigation, diagnostics, and safety services.Global eSIM Market Segmentation

By Application

The market includes smartphones, tablets, laptops, wearables, automotive, IoT devices, and industrial equipment. Smartphones dominate the market due to widespread adoption of eSIM-enabled flagship devices.By End User

End users include individual consumers, enterprises, automotive manufacturers, telecom operators, and industrial organizations. Enterprise and automotive segments are experiencing the fastest growth due to IoT integration.By Connectivity Type

The market includes consumer eSIM and M2M/IoT eSIM. M2M/IoT eSIM is witnessing rapid expansion due to increasing industrial automation and smart device deployment.By Distribution Channel

The market includes direct operator sales, device OEM integration, online platforms, and enterprise solution providers. OEM-integrated eSIM solutions are becoming the dominant distribution model globally.Regional Market Dynamics

North America

North America holds a significant share of the eSIM market due to early adoption of advanced mobile technologies, strong telecom infrastructure, and high smartphone penetration. The United States leads regional growth with strong participation from Apple, AT&T, and Verizon ecosystems.Europe

Europe is a mature market driven by strong telecom regulation, widespread IoT adoption, and increasing demand for digital connectivity solutions. Countries such as Germany, the United Kingdom, France, and the Netherlands are key contributors.Asia-Pacific

Asia-Pacific is the fastest-growing region due to rapid smartphone adoption, expanding 5G networks, and strong manufacturing ecosystems. China, India, Japan, and South Korea are leading markets for eSIM-enabled devices and IoT deployments.Latin America

Latin America is experiencing gradual adoption driven by increasing smartphone penetration and improving telecom infrastructure. Brazil and Mexico are key emerging markets.Middle East & Africa

The region is witnessing growing adoption supported by telecom modernization, smart city initiatives, and rising demand for digital connectivity services. GCC countries are leading eSIM adoption in enterprise and consumer segments.Competitive Landscape

The global eSIM market is highly competitive and technology-driven, with participation from semiconductor companies, telecom operators, and device manufacturers. Key players include Apple Inc., Samsung Electronics, Qualcomm Technologies, Thales Group, Giesecke+Devrient, STMicroelectronics, NXP Semiconductors, Deutsche Telekom, Vodafone Group, AT&T Inc., and STC Group. Companies are focusing on eSIM platform development, secure connectivity solutions, remote provisioning technologies, and global roaming partnerships. Strategic collaborations between telecom operators, OEMs, and IoT platform providers are accelerating market expansion.Strategic Outlook

The strategic outlook for the global eSIM market remains highly positive due to rapid digitalization and increasing demand for connected ecosystems. Future opportunities include fully embedded IoT ecosystems, autonomous vehicle connectivity, global unified roaming platforms, and enterprise-wide digital SIM management solutions. Advancements in 5G, edge computing, and secure identity management will further enhance eSIM capabilities and adoption. Companies investing in telecom partnerships, secure provisioning platforms, and cross-device integration will gain strong competitive advantages.Final Market Perspective

The global eSIM market is transforming the telecommunications landscape by enabling seamless, flexible, and scalable connectivity across devices and industries. Rising demand for IoT, 5G connectivity, and digital-first mobile experiences will continue driving strong market expansion throughout the forecast period. Organizations that successfully integrate secure eSIM infrastructure with global connectivity ecosystems will remain strongly positioned in the evolving digital connectivity market.Table of Contents

Table of Contents

- 1. Executive Summary

- 1.1 Global eSIM Market Snapshot (2026-2033)

- 1.2 Market Size & CAGR Analysis

- 1.3 Largest & Fastest-Growing Segments

- 1.4 Key Regional Insights

- 1.5 Market Growth Drivers

- 1.6 Competitive Landscape Overview

- 1.7 Future Industry Outlook

- 2. Introduction & Market Overview

- 2.1 Definition of eSIM (Embedded SIM)

- 2.2 Scope of the Study

- 2.3 Evolution of SIM Technology

- 2.4 eSIM Ecosystem Overview

- 2.5 Value Chain Analysis

- 2.6 Consumer & Enterprise Connectivity Trends

- 2.7 GSMA Standards & Regulatory Framework

- 3. Research Methodology

- 3.1 Primary Research

- 3.2 Secondary Research

- 3.3 Market Estimation Methodology

- 3.4 Forecast Assumptions (2026-2033)

- 3.5 Data Validation & Market Triangulation

- 4. Market Dynamics

- 4.1 Drivers

- 4.1.1 Rapid Adoption of Connected Devices

- 4.1.2 Expansion of IoT & M2M Communications

- 4.1.3 Growth of 5G Networks

- 4.1.4 Increasing Demand for Seamless Roaming

- 4.1.5 Rising Adoption in Automotive Sector

- 4.2 Restraints

- 4.2.1 Device Compatibility Limitations

- 4.2.2 Security & Privacy Concerns

- 4.2.3 Regulatory Variations Across Regions

- 4.2.4 Transition Costs for Telecom Operators

- 4.3 Opportunities

- 4.3.1 Fully Embedded IoT Ecosystems

- 4.3.2 Global Unified Roaming Platforms

- 4.3.3 Autonomous Vehicle Connectivity Solutions

- 4.3.4 Enterprise Digital SIM Management

- 4.4 Challenges

- 4.4.1 Standardization & Interoperability Issues

- 4.4.2 Carrier Resistance to SIM Disintermediation

- 4.4.3 Cybersecurity Risks in Remote Provisioning

- 4.4.4 Infrastructure Readiness in Emerging Markets

- 4.1 Drivers

- 5. Global eSIM Market Analysis (2026-2033)

- 5.1 Market Size Overview

- 5.2 CAGR Analysis

- 5.3 Revenue Distribution by Region

- 5.4 Segment-Wise Market Analysis

- 5.5 Adoption & Usage Trends

- 5.6 Technology Innovation Trends

- 6. Market Segmentation

- 6.1 By Application

- 6.1.1 Smartphones

- 6.1.2 Tablets

- 6.1.3 Laptops

- 6.1.4 Wearables

- 6.1.5 Automotive

- 6.1.6 IoT Devices

- 6.1.7 Industrial Equipment

- 6.2 By End User

- 6.2.1 Individual Consumers

- 6.2.2 Enterprises

- 6.2.3 Automotive Manufacturers

- 6.2.4 Telecom Operators

- 6.2.5 Industrial Organizations

- 6.3 By Connectivity Type

- 6.3.1 Consumer eSIM

- 6.3.2 M2M / IoT eSIM

- 6.4 By Distribution Channel

- 6.4.1 Direct Operator Sales

- 6.4.2 Device OEM Integration

- 6.4.3 Online Platforms

- 6.4.4 Enterprise Solution Providers

- 6.1 By Application

- 7. Market Segmentation by Geography

- 7.1 North America

- 7.2 Europe

- 7.3 Asia-Pacific

- 7.4 Latin America

- 7.5 Middle East & Africa

- 8. Competitive Landscape

- 8.1 Market Share Analysis

- 8.2 eSIM Platform Innovation Benchmarking

- 8.3 Telecom Operator Ecosystem Analysis

- 8.4 OEM & Semiconductor Partnerships

- 8.5 Strategic Alliances & Roaming Agreements

- 9. Company Profiles

- 9.1 Apple Inc.

- 9.2 Samsung Electronics

- 9.3 Qualcomm Technologies

- 9.4 Thales Group

- 9.5 STMicroelectronics

- 9.6 Giesecke+Devrient

- 9.7 NXP Semiconductors

- 9.8 Deutsche Telekom

- 9.9 Vodafone Group

- 9.10 AT&T Inc.

- 10. Strategic Intelligence & Pheonix AI Insights

- 10.1 AI-Based Connectivity Analytics

- 10.2 Smart Device Provisioning Intelligence

- 10.3 Global Roaming Optimization Systems

- 10.4 eSIM Adoption Forecasting Models

- 10.5 Competitive Benchmarking Engine

- 11. Future Outlook & Strategic Recommendations

- 11.1 Expansion of Fully Digital Connectivity Ecosystems

- 11.2 Growth of Autonomous & Connected Mobility

- 11.3 AI-Driven Telecom Infrastructure

- 11.4 Secure Identity & Provisioning Platforms

- 11.5 Long-Term Market Outlook (2033+)

- 12. Appendix

- 13. About Pheonix Research

- 14. Disclaimer

Competitive Landscape

Global eSIM Market Competitive Intensity & Market Structure Overview

The global eSIM market is highly concentrated at the technology infrastructure level but widely distributed at the ecosystem level, making it a hybrid competitive structure dominated by semiconductor leaders, telecom operators, device OEMs, and secure connectivity platform providers. Competition is primarily driven by GSMA compliance leadership, remote SIM provisioning (RSP) capabilities, device integration scale, and global carrier partnerships.

While device manufacturers and chipset providers control key hardware and embedded security components, telecom operators and eSIM platform providers influence service delivery, subscription management, and global roaming experiences. This multi-layered ecosystem creates interdependency among stakeholders, accelerating collaboration while also intensifying strategic competition for ecosystem control.

The market is also undergoing rapid standardization and consolidation around secure connectivity platforms, with increasing emphasis on interoperability, cybersecurity, and seamless cross-border connectivity for consumers and enterprises.

Global eSIM Market Competitive Intensity & Market Structure Current Scenario

Leading Device Manufacturers, Semiconductor Firms & Telecom Operators

Apple Inc.: A global leader in eSIM adoption, driving large-scale consumer migration through eSIM-only device strategies in select smartphone models and strong ecosystem integration.

Samsung Electronics: Major Android ecosystem leader enabling widespread eSIM support across flagship smartphones, wearables, and IoT devices with global carrier compatibility.

Qualcomm Technologies: Key chipset provider enabling eSIM functionality across mobile devices through integrated modem and secure connectivity solutions.

Thales Group: Leading provider of secure eSIM modules, digital identity solutions, and remote SIM provisioning infrastructure for telecom operators and enterprises.

STMicroelectronics: Major semiconductor supplier delivering embedded secure elements and hardware components essential for eSIM-enabled devices.

Giesecke+Devrient (G+D): Global leader in eSIM management platforms, digital security solutions, and mobile connectivity lifecycle management systems.

NXP Semiconductors: Key player in secure connectivity and embedded solutions for automotive, IoT, and industrial eSIM applications.

Deutsche Telekom: Major telecom operator actively deploying eSIM-based consumer and enterprise connectivity solutions across Europe and global markets.

Vodafone Group: One of the leading global operators offering eSIM-based roaming, IoT connectivity, and enterprise digital SIM services.

AT&T Inc.: Strong North American telecom operator enabling large-scale consumer and enterprise eSIM adoption across mobile and IoT segments.

STC Group: Leading Middle Eastern telecom operator advancing eSIM deployment across consumer mobility, enterprise IoT, and smart city infrastructure.

Key Competitive Intensity & Market Structure Drivers

A major driver of competition in the eSIM market is control over remote SIM provisioning (RSP) platforms. Companies that own or manage provisioning ecosystems hold significant influence over subscriber management, carrier switching, and global connectivity orchestration.

Device OEM integration is another critical factor, as large-scale adoption depends heavily on embedding eSIM capabilities into smartphones, wearables, laptops, and connected vehicles at the manufacturing stage.

Telecom operator partnerships play a decisive role in market expansion, as eSIM functionality relies on carrier participation for profile activation, roaming agreements, and cross-border connectivity services.

Security and compliance standards are central to competition, with GSMA certification, encryption protocols, and secure element integration acting as key barriers to entry for new participants.

The expansion of IoT and M2M ecosystems is further intensifying competition, particularly in automotive and industrial segments where large-scale device provisioning and lifecycle management are essential.

Strategic Implications of Competitive Intensity & Market Structure

Companies are increasingly focusing on ecosystem partnerships that integrate chipset manufacturers, device OEMs, and telecom operators to ensure seamless end-to-end eSIM deployment across multiple device categories.

Platform-based business models are gaining traction, with eSIM management platforms evolving into centralized connectivity hubs for enterprises managing global device fleets and IoT deployments.

Telecom operators are shifting toward digital-first subscription models, leveraging eSIM to reduce physical SIM distribution costs while expanding global roaming revenues and enterprise connectivity services.

Device manufacturers are using eSIM integration as a competitive differentiator, enabling slimmer device designs, multi-network support, and enhanced user onboarding experiences.

Automotive and industrial IoT adoption is driving long-term strategic investments in scalable, secure, and autonomous connectivity systems powered by eSIM-enabled architectures.

Global eSIM Market Competitive Intensity & Market Structure Forward Outlook

The global eSIM market is expected to become increasingly platform-driven, with ecosystem orchestration platforms playing a central role in managing connectivity across billions of devices worldwide.

Future competition will be shaped by advancements in fully embedded connectivity (iSIM), convergence of eSIM with edge computing, and expansion of autonomous device networks across industries.

Consolidation is expected among connectivity management platform providers as telecom operators and technology firms seek integrated solutions for global-scale device provisioning and lifecycle management.

Interoperability, cybersecurity resilience, and seamless global roaming experiences will remain key differentiators as the market matures into a standardized digital connectivity infrastructure layer.

Overall, companies that successfully combine secure eSIM infrastructure, global carrier partnerships, scalable IoT platforms, and strong OEM integration will remain strongly positioned in the evolving global eSIM ecosystem.

Value Chain

Global eSIM Market Value Chain & Supply Chain Evolution Overview

The global eSIM market value chain is evolving into a highly digitalized, software-driven, and ecosystem-integrated telecommunications infrastructure, shaped by the rapid expansion of IoT connectivity, 5G adoption, and the shift toward embedded, hardware-independent mobile identity management. Unlike traditional SIM-based ecosystems, the eSIM value chain is increasingly defined by platform interoperability, remote provisioning capabilities, and cross-industry collaboration between telecom operators, device manufacturers, and semiconductor providers.

The upstream segment of the value chain is anchored by semiconductor manufacturers and secure element providers responsible for developing embedded SIM chips, eUICC (embedded Universal Integrated Circuit Card) components, and secure hardware modules. Companies in this layer focus on advanced chip miniaturization, cryptographic security, and compliance with GSMA standards to ensure global interoperability and secure identity management across devices.

The midstream segment includes eSIM platform providers, mobile network operators (MNOs), and mobile virtual network operators (MVNOs), which collectively manage remote SIM provisioning (RSP), subscriber profile management, and network authentication systems. This layer is increasingly software-centric, with cloud-based orchestration platforms enabling real-time activation, switching, and lifecycle management of mobile subscriptions across global networks.

Device manufacturers and OEMs form a critical integration layer within the value chain, embedding eSIM modules into smartphones, wearables, laptops, automotive systems, and IoT devices. This integration is becoming standard in flagship devices, driven by consumer demand for seamless connectivity and operator flexibility. Automotive manufacturers are also emerging as major stakeholders, embedding eSIM technology into connected vehicles for telematics, navigation, and autonomous driving applications.

The downstream ecosystem includes telecom operators, enterprise IoT solution providers, digital connectivity platforms, and end users across consumer, enterprise, and industrial segments. Distribution is increasingly shifting toward digital-first activation models, eliminating physical SIM logistics and enabling instant onboarding through QR-based or app-based provisioning systems.

Regulatory frameworks and industry standards, particularly those governed by GSMA, play a central role in ensuring interoperability, security compliance, and global roaming compatibility. Increasing emphasis on cybersecurity, identity protection, and cross-border data governance is driving continuous enhancement of eSIM security architectures and provisioning protocols.

Global eSIM Market Value Chain & Supply Chain Evolution Current Scenario

The current eSIM supply chain is characterized by rapid digital convergence, strong platform centralization, and increasing vertical integration between telecom operators and device ecosystems. Major technology companies are consolidating control over provisioning platforms, enabling seamless device activation and reducing dependency on physical distribution networks.

Smartphone manufacturers, particularly premium OEMs, have largely standardized eSIM integration, accelerating global adoption and reducing reliance on physical SIM production and logistics. This shift is significantly disrupting traditional SIM card manufacturing and distribution ecosystems.

Telecom operators are transitioning from hardware-centric distribution models to software-defined connectivity services. Remote provisioning platforms now enable instant subscription activation, multi-profile management, and cross-border connectivity solutions, especially for frequent travelers and global enterprises.

IoT and M2M connectivity represent the fastest-growing segment within the current supply chain structure. Industries such as automotive, logistics, healthcare, and smart cities increasingly rely on large-scale eSIM deployments to manage distributed device networks efficiently and securely.

Cloud-based orchestration platforms and API-driven connectivity management systems are becoming central to operational efficiency, allowing enterprises to manage thousands of connected devices in real time with minimal physical intervention.

Key Value Chain & Supply Chain Evolution Signals in Global eSIM Market

One of the most significant transformation signals is the rapid decline of physical SIM dependency, driven by OEM-led adoption of embedded connectivity solutions across consumer electronics and IoT ecosystems.

Another major shift is the increasing dominance of software-defined telecom infrastructure, where connectivity provisioning, subscriber management, and network switching are fully controlled through cloud-native platforms rather than physical distribution channels.

The expansion of IoT-driven connectivity ecosystems is also reshaping the value chain, with eSIM becoming a foundational technology for smart cities, industrial automation, connected vehicles, and wearable technologies.

Strategic collaboration between semiconductor companies, telecom operators, and device manufacturers is intensifying, leading to vertically integrated ecosystems that reduce activation friction and improve global scalability.

Additionally, the rise of global roaming simplification and multi-network switching capabilities is pushing operators toward more competitive and flexible pricing models, reshaping traditional telecom revenue structures.

Strategic Implications of Value Chain & Supply Chain Evolution in Global eSIM Market

The evolving eSIM value chain presents significant strategic implications for telecom operators, device manufacturers, semiconductor companies, and enterprise connectivity providers. Competitive advantage is increasingly determined by platform control, ecosystem integration, and global provisioning capabilities rather than physical distribution scale.

Telecom operators are under pressure to transition into digital-first connectivity service providers, focusing on API-driven offerings, enterprise IoT solutions, and cross-border roaming platforms to remain competitive in a rapidly digitizing landscape.

Device manufacturers are gaining stronger influence in the connectivity ecosystem by embedding eSIM functionality as a default feature, effectively shifting control of subscriber onboarding closer to the hardware layer.

Investment in secure provisioning infrastructure, identity management systems, and interoperable cloud platforms is becoming a critical differentiator for long-term competitiveness in the global connectivity ecosystem.

Enterprise adoption of eSIM-based IoT connectivity is creating new revenue opportunities for managed connectivity services, lifecycle management platforms, and intelligent network orchestration solutions.

Global eSIM Market Value Chain & Supply Chain Evolution Forward Outlook

Between 2026 and 2033, the eSIM value chain is expected to evolve into a fully software-defined, globally interoperable, and highly automated connectivity ecosystem. Physical SIM infrastructure will continue to decline as embedded connectivity becomes the default standard across devices and industries.

Advancements in 5G, edge computing, and network slicing technologies will further enhance eSIM capabilities, enabling dynamic network selection, ultra-low latency connectivity, and seamless cross-border mobility for both consumers and enterprises.

IoT expansion will remain a dominant growth driver, with billions of connected devices relying on scalable eSIM provisioning systems for real-time connectivity management and secure authentication.

The integration of AI-driven network optimization, predictive connectivity management, and automated provisioning systems will significantly enhance operational efficiency and reduce latency in global telecom ecosystems.

Ultimately, the future eSIM value chain will be defined by a fully integrated digital connectivity architecture where semiconductor design, telecom infrastructure, cloud orchestration, and device ecosystems operate as a unified global network, enabling seamless, secure, and scalable connectivity across all industries.

Market-Specific Value Chain

- Semiconductor & Secure Element Manufacturing: eSIM chip manufacturers, secure element providers, cryptographic hardware developers

- Platform & Remote Provisioning Systems: eSIM management platforms, GSMA-compliant RSP providers, cloud connectivity orchestration systems

- Telecom Network Operators: MNOs, MVNOs, global roaming service providers, connectivity API platforms

- Device & OEM Integration: smartphone manufacturers, wearable device makers, automotive OEMs, IoT hardware producers

- Enterprise & IoT Connectivity Management: industrial IoT platforms, fleet management systems, smart city infrastructure providers

- End-User Applications: consumers, enterprises, automotive systems, industrial automation, connected devices ecosystems

Investment Activity

Global eSIM Market Investment & Funding Dynamics Overview

Investment and funding activity in the Global eSIM Market is accelerating rapidly due to the global shift toward digital connectivity, rapid expansion of IoT ecosystems, 5G network deployment, and increasing demand for seamless cross-border mobile connectivity. Between 2026 and 2033, capital inflows are expected to focus heavily on telecom infrastructure modernization, embedded connectivity platforms, semiconductor innovation, and secure remote SIM provisioning (RSP) technologies.

The market is attracting strong investments from telecom operators, device OEMs, semiconductor companies, and digital infrastructure funds. Strategic funding is increasingly directed toward building scalable eSIM ecosystems that support smartphones, wearables, automotive telematics, and industrial IoT applications.

A key investment trend is the rapid transition from physical SIM logistics to fully digital connectivity frameworks. This shift is encouraging large-scale capital deployment in cloud-based SIM management platforms, global roaming orchestration systems, and embedded connectivity APIs for enterprises and device manufacturers.

At the same time, semiconductor firms and secure element providers are receiving significant funding to enhance embedded security, chip-level integration, and authentication technologies required for next-generation eSIM deployments.

Global eSIM Market Investment & Funding Current Scenario

Current investment activity in the eSIM market is strongly driven by the expansion of 5G networks, rising IoT device deployments, and increasing enterprise demand for centralized connectivity management. Telecom operators are investing heavily in eSIM-enabled service platforms to reduce operational costs and improve customer onboarding efficiency.

- North America: Leading investment region due to strong participation from Apple, Qualcomm, AT&T, and Verizon ecosystems, along with advanced telecom infrastructure and early technology adoption.

- Europe: Significant investments driven by strong regulatory support for digital telecom infrastructure, IoT expansion, and cross-border connectivity initiatives.

- Asia-Pacific: Fastest-growing investment hub supported by large-scale smartphone manufacturing, expanding 5G deployment, and strong telecom ecosystems in China, India, Japan, and South Korea.

- Middle East & Africa: Emerging investment destination driven by smart city programs, telecom modernization, and enterprise digital transformation initiatives.

Key Investment & Funding Drivers in Global eSIM Market

- Rapid expansion of 5G networks is driving investments in advanced connectivity platforms and multi-network switching technologies.

- Growing IoT and M2M device adoption is attracting funding into scalable embedded connectivity management systems.

- Rising demand for seamless international roaming is encouraging investment in global eSIM orchestration and unified connectivity platforms.

- Automotive connectivity growth is driving capital inflows into telematics, connected vehicle platforms, and autonomous driving communication systems.

- Semiconductor and secure element innovation is attracting funding for chip-level integration and advanced encryption technologies.

- Enterprise digital transformation is supporting investments in centralized SIM lifecycle management and cloud-based connectivity solutions.

- Strategic telecom partnerships are accelerating funding for global roaming alliances and cross-operator eSIM interoperability frameworks.

Strategic Implications of Investment & Funding Dynamics

- Companies offering integrated eSIM platforms combining hardware, software, and network orchestration are gaining strong investor interest.

- Telecom operators are shifting from traditional SIM distribution models to fully digital onboarding ecosystems, improving scalability and reducing costs.

- Device manufacturers embedding native eSIM support are strengthening long-term ecosystem control and recurring revenue opportunities.

- Semiconductor firms with secure element technologies are becoming critical enablers of next-generation connectivity infrastructure.

- Global partnerships between OEMs, telecom operators, and IoT platform providers are shaping competitive funding landscapes.

- Edge computing and cloud-native connectivity platforms are emerging as high-value investment segments within the eSIM ecosystem.

- Companies focusing on secure identity management and regulatory-compliant connectivity solutions are gaining stronger institutional backing.

Global eSIM Market Investment & Funding Forward Outlook

Looking ahead, investment in the Global eSIM Market is expected to remain highly robust, supported by continuous expansion of connected devices, rapid 5G rollout, and increasing demand for unified global connectivity solutions.

Future capital allocation will focus on fully autonomous IoT ecosystems, AI-driven connectivity management, next-generation automotive telematics platforms, and global roaming optimization networks. Strong investment growth is also expected in secure cloud-based SIM provisioning and multi-device orchestration systems.

- North America: Will continue leading innovation in device integration, telecom platforms, and secure connectivity ecosystems.

- Europe: Will focus on regulatory-driven digital connectivity expansion and cross-border telecom integration frameworks.

- Asia-Pacific: Will remain the largest growth hub due to manufacturing scale, telecom expansion, and IoT adoption.

Overall, the eSIM market will continue attracting strong funding momentum as digital connectivity becomes a foundational layer of global communication infrastructure. Companies that successfully integrate secure eSIM technology with scalable cloud platforms and global telecom partnerships will remain strongly positioned in the evolving digital connectivity investment landscape.

Technology & Innovation

Global eSIM Market Technology & Innovation Landscape Overview

The global eSIM market is being reshaped by rapid advancements in embedded connectivity architecture, remote SIM provisioning (RSP), cloud-native telecom infrastructure, and secure digital identity management systems. eSIM technology is evolving from a connectivity enabler into a foundational layer for fully digital, programmable, and remotely managed telecom ecosystems across consumer devices, enterprises, and IoT networks.

At its core, eSIM replaces physical SIM cards with embedded secure elements that allow dynamic provisioning of mobile network profiles. This shift is enabling a fully software-defined approach to connectivity management, where network access can be activated, switched, and managed remotely without physical intervention.

Global eSIM Market Technology & Innovation Current Scenario

The current eSIM ecosystem is built around GSMA-standardized Remote SIM Provisioning (RSP) platforms, which enable secure over-the-air (OTA) profile activation and lifecycle management. These platforms are increasingly integrated with cloud-native telecom infrastructure, allowing operators to manage millions of connected devices in real time.

Embedded Secure Elements (eSE) and integrated SIM architectures are being widely deployed across smartphones, wearables, laptops, automotive telematics units, and industrial IoT modules. These hardware security components ensure encrypted authentication, tamper resistance, and secure identity storage.

Telecom operators are also transitioning toward virtualized network functions and 5G core integration, enabling dynamic network slicing, real-time policy control, and intelligent roaming management for eSIM-enabled devices.

Key Technology & Innovation Trends in Global eSIM Market

- Remote SIM Provisioning (RSP) Platforms: Cloud-based systems enabling secure OTA activation, profile switching, and lifecycle management of eSIM identities.

- Embedded Secure Element (eSE) Architecture: Hardware-based cryptographic modules ensuring secure storage of SIM credentials and identity protection.

- iSIM Integration (Next-Gen Evolution): SIM functionality embedded directly into device chipsets, reducing hardware footprint and cost.

- 5G Network Integration: Enhanced support for low-latency, high-speed connectivity with multi-network switching capabilities.

- IoT & M2M Connectivity Platforms: Scalable connectivity management systems for industrial IoT, smart cities, and connected devices.

- Cloud-Native Telecom Infrastructure: Virtualized core networks enabling real-time device management and global scalability.

- Zero-Touch Device Provisioning: Automated activation and configuration of devices without manual SIM installation or setup.

- AI-Driven Network Optimization: Intelligent algorithms optimizing carrier selection, roaming performance, and connectivity cost efficiency.

- Advanced Encryption & Identity Security: Hardware-backed security protocols ensuring secure authentication and fraud prevention.

- Edge Computing Integration: Distributed processing for real-time connectivity decisions in IoT and automotive environments.

Strategic Implications of Technology & Innovation

Technological innovation is transforming the eSIM ecosystem into a fully software-defined connectivity layer that supports global, device-agnostic network access. This is significantly reducing dependence on physical SIM logistics while enabling scalable, real-time connectivity orchestration across industries.

The convergence of eSIM with 5G, IoT, and cloud-native telecom systems is enabling highly flexible network architectures, where devices can dynamically switch between operators based on performance, cost, and availability.

Telecom operators and OEMs are increasingly competing on digital ecosystem capabilities rather than traditional connectivity services, with emphasis on platform integration, API-driven provisioning, and global roaming partnerships.

However, rising complexity in interoperability standards, cybersecurity risks, and cross-border regulatory frameworks continues to challenge large-scale deployment consistency.

Global eSIM Market Technology & Innovation Forward Outlook

The future of the eSIM ecosystem is expected to move toward fully embedded connectivity models driven by iSIM technology, where SIM functionality is integrated directly into device processors, eliminating dedicated SIM hardware entirely.

Artificial intelligence will play a critical role in next-generation connectivity management, enabling autonomous network selection, predictive roaming optimization, and real-time connectivity performance tuning.

The convergence of 5G Advanced, edge computing, and distributed cloud telecom infrastructure will further enhance eSIM capabilities, enabling ultra-reliable connectivity for autonomous vehicles, industrial automation systems, and mission-critical IoT applications.

Additionally, enterprise adoption of centralized connectivity management platforms will expand significantly, enabling global organizations to manage millions of connected devices through unified digital dashboards.

Overall, the eSIM technology landscape is evolving toward a fully programmable, intelligent, and globally scalable connectivity ecosystem that forms the backbone of next-generation digital communication infrastructure.

Market Risk

Global eSIM Market Risk Factors & Disruption Threats Overview

The global eSIM market is experiencing rapid expansion driven by rising adoption of connected devices, 5G rollout, IoT growth, and increasing demand for seamless digital connectivity. However, despite strong growth prospects, the market faces several critical risks including cybersecurity vulnerabilities, telecom regulatory fragmentation, high implementation complexity, dependency on carrier ecosystems, interoperability challenges, and evolving global compliance standards.

One of the key risk factors in the eSIM market is cybersecurity and digital identity exposure. Since eSIM technology relies on remote SIM provisioning and cloud-based profile management, it increases the attack surface for potential hacking attempts, unauthorized access, and identity spoofing. Any breach in eSIM provisioning platforms or telecom infrastructure can disrupt connectivity for large-scale user bases and compromise sensitive subscriber data.

Regulatory fragmentation across countries and telecom operators also poses a significant challenge. Different regions follow varying rules regarding SIM registration, data privacy, lawful interception, and telecom licensing. This lack of global standardization can slow down cross-border adoption of eSIM technology and increase compliance costs for operators and device manufacturers.

Another major risk factor is dependency on telecom operator ecosystems. eSIM adoption requires strong collaboration between device manufacturers, mobile network operators (MNOs), and mobile virtual network operators (MVNOs). Resistance from traditional SIM business models or slow onboarding by telecom operators may delay market expansion and limit consumer flexibility in certain regions.

Interoperability and standardization challenges also remain important. Although GSMA standards support eSIM deployment, differences in implementation across devices, networks, and provisioning platforms can create compatibility issues. This may impact user experience, roaming efficiency, and large-scale enterprise IoT deployments.

High implementation and integration complexity further adds to market risk. Enterprises and OEMs must invest in secure provisioning platforms, backend connectivity systems, and device-level integration. These technical requirements can increase upfront costs and slow down adoption, particularly for small and mid-sized organizations.

Supply chain dependency on semiconductor components and secure hardware modules also impacts the market. eSIM technology relies on embedded secure elements and advanced chip manufacturing, making it vulnerable to semiconductor shortages, geopolitical restrictions, and manufacturing disruptions.

Global eSIM Market Risk Factors & Disruption Threats Current Scenario

The current eSIM market environment reflects strong acceleration in smartphone integration, automotive connectivity, and IoT deployments. Leading device manufacturers and telecom operators are actively expanding eSIM support, particularly in premium smartphones, wearables, and connected vehicles.

However, adoption is uneven across regions due to varying telecom readiness and regulatory frameworks. Developed markets such as North America and parts of Europe are leading adoption, while several emerging economies continue to rely heavily on traditional SIM infrastructure.

At the same time, increasing reliance on digital connectivity has made telecom ecosystems more sensitive to service disruptions. Network outages, provisioning failures, or platform downtime can have widespread impacts on enterprise operations, logistics systems, and consumer connectivity.

The rise of IoT and M2M applications is also increasing operational pressure on eSIM platforms. Large-scale device deployments require highly scalable and secure provisioning systems, and any inefficiencies in orchestration or authentication can lead to connectivity failures across industrial networks.

Competitive dynamics are intensifying as telecom operators, semiconductor companies, and cloud service providers compete to control eSIM infrastructure and ecosystem platforms. This competition may lead to fragmented solutions and slower global harmonization in the short term.

Global eSIM Market Key Risk Factors & Disruption Threat Signals

- Cybersecurity & Data Privacy Risks: Exposure of remote SIM provisioning systems to hacking, identity theft, and unauthorized access.

- Regulatory Fragmentation: Differing telecom laws, SIM registration rules, and compliance requirements across countries.

- Telecom Ecosystem Dependency: Reliance on operator adoption and resistance from traditional SIM business models.

- Interoperability Challenges: Inconsistent implementation of GSMA standards across devices and networks.

- High Integration Complexity: Significant technical and infrastructure requirements for deployment and management.

- Semiconductor Supply Chain Risk: Dependence on secure elements and chip manufacturing vulnerable to global shortages.

- Platform Reliability Issues: Risk of service outages affecting large-scale connectivity and enterprise operations.

- Slow Emerging Market Adoption: Continued reliance on physical SIM infrastructure in developing regions.

- Competitive Platform Fragmentation: Multiple ecosystem providers creating non-uniform global standards.

- Enterprise Deployment Complexity: Large-scale IoT and M2M deployments requiring advanced orchestration systems.

Strategic Implications of Risk Factors

To mitigate risks, eSIM ecosystem players must prioritize cybersecurity strengthening, including encrypted provisioning systems, multi-layer authentication, and real-time threat monitoring. Ensuring secure digital identity management will be critical for maintaining trust in large-scale deployments.

Greater regulatory alignment and collaboration between telecom authorities, device manufacturers, and global standard bodies will be essential to reduce fragmentation and enable smoother cross-border connectivity.

Telecom operators and OEMs must also invest in interoperable platforms and unified provisioning systems to improve compatibility across devices and networks. Standardization will be a key factor in scaling enterprise and IoT adoption.

Strengthening semiconductor supply chains and diversifying chip sourcing strategies will be important to reduce hardware dependency risks. Investments in resilient manufacturing ecosystems will support long-term stability.

Global eSIM Market Forward Risk Outlook

Looking ahead to 2026–2033, the eSIM market is expected to expand significantly as digital connectivity becomes central to consumer devices, enterprise systems, and industrial IoT networks. However, the market’s long-term stability will depend heavily on cybersecurity resilience, regulatory harmonization, and ecosystem interoperability.

Future growth will be shaped by advancements in 5G, autonomous vehicles, smart cities, and fully connected IoT ecosystems. These developments will increase demand for scalable and secure eSIM infrastructure while also amplifying system complexity and risk exposure.

The convergence of telecom, cloud computing, and device manufacturing will continue to redefine competitive dynamics. Companies that fail to align with global standards or invest in secure provisioning ecosystems may face adoption barriers.

Overall, while the eSIM market presents strong long-term growth potential, sustained success will depend on balancing innovation, security, regulatory compliance, and global interoperability across an increasingly connected digital ecosystem.

Regulatory Landscape

Global eSIM Market Regulatory & Policy Environment Overview

The regulatory and policy environment governing the global eSIM market is evolving rapidly as embedded SIM technology becomes a core enabler of modern telecommunications, IoT connectivity, and digital mobility ecosystems. Regulatory frameworks primarily focus on telecom licensing, remote SIM provisioning (RSP) standards, data privacy, cybersecurity, cross-border connectivity, and interoperability requirements across devices and networks.

Unlike traditional SIM cards, eSIM technology introduces a software-defined approach to mobile connectivity, which places greater emphasis on digital security protocols, identity management, and standardized provisioning systems. As a result, global telecom regulators and standards bodies such as GSMA, national telecommunications authorities, and data protection agencies play a central role in shaping market structure and compliance requirements.

The market is also influenced by broader digital policy initiatives, including 5G rollout regulations, IoT connectivity frameworks, digital identity programs, and cybersecurity legislation. Governments are increasingly encouraging secure and flexible connectivity solutions to support smart cities, connected vehicles, industrial IoT, and cross-border digital services.

Additionally, data sovereignty laws and privacy regulations such as GDPR in Europe and similar frameworks in other regions are shaping how eSIM profiles are managed, stored, and transferred across networks and jurisdictions.

Global eSIM Market Regulatory & Policy Environment Current Scenario

The current regulatory landscape for the eSIM market is defined by the adoption of GSMA Remote SIM Provisioning (RSP) standards, which ensure interoperability between mobile network operators (MNOs), device manufacturers, and eSIM platform providers. These standards govern how eSIM profiles are securely downloaded, activated, and managed across devices.

In North America, regulatory oversight is primarily driven by the Federal Communications Commission (FCC), which supports flexible connectivity models while ensuring network security and consumer protection. Telecom operators in the United States and Canada are actively deploying eSIM-enabled services across smartphones, wearables, and IoT ecosystems under relatively innovation-friendly regulatory conditions.

In Europe, the regulatory environment is more structured, with strong emphasis on data privacy, consumer rights, and interoperability. The European Electronic Communications Code (EECC) and GDPR framework influence how eSIM data and subscriber identities are managed. European regulators also promote competition and multi-operator access, supporting wider adoption of eSIM-based services.

Asia-Pacific presents a diverse regulatory landscape. Countries such as Japan and South Korea have well-developed telecom frameworks supporting advanced eSIM deployment, particularly in 5G and IoT applications. China maintains stricter control over telecom infrastructure and SIM provisioning, with eSIM adoption progressing under regulated pilot programs. India is gradually expanding eSIM support under its broader digital communication and telecom modernization policies.

In Latin America, regulatory frameworks are evolving, with increasing adoption of eSIM-friendly policies aimed at improving mobile penetration and enabling digital services. Countries such as Brazil and Mexico are leading regional adoption with gradual alignment toward international standards.

The Middle East & Africa region is witnessing growing regulatory modernization, particularly in GCC countries, where telecom regulators are actively supporting smart city initiatives, digital transformation programs, and IoT expansion through eSIM-enabled connectivity frameworks.

Key Regulatory & Policy Environment Signals in Global eSIM Market

- GSMA Remote SIM Provisioning (RSP) Standards: Core global framework enabling secure eSIM activation, profile management, and interoperability across networks and devices.

- Telecom Licensing & Spectrum Regulations: National telecom authorities regulate mobile operators and ensure compliance for eSIM-enabled services across 4G and 5G networks.

- Data Privacy & Digital Identity Laws: Regulations such as GDPR and similar frameworks govern subscriber data protection, identity verification, and cross-border data transfers.

- Cybersecurity & Device Security Compliance: Strong focus on secure element integration, encryption protocols, and protection against unauthorized SIM profile access.

- IoT & Machine-to-Machine (M2M) Connectivity Policies: Governments are promoting standardized frameworks for industrial IoT, connected vehicles, and smart infrastructure using eSIM technology.

- Roaming & Cross-Border Connectivity Regulations: Policies enabling seamless international roaming and multi-network access are supporting global eSIM adoption.

Strategic Implications of Regulatory & Policy Environment

The evolving regulatory environment is significantly shaping the competitive structure of the eSIM market. Compliance with GSMA standards and national telecom regulations has become a critical entry requirement for eSIM platform providers, telecom operators, and device manufacturers.

Strict data privacy and cybersecurity regulations are driving increased investment in secure provisioning platforms, encrypted identity management systems, and advanced authentication technologies. This is strengthening the role of specialized eSIM infrastructure providers within the ecosystem.

The growing emphasis on IoT connectivity and smart infrastructure policies is accelerating eSIM adoption across automotive, industrial, and enterprise applications. Governments are actively supporting connected vehicle frameworks, smart city deployments, and industrial automation initiatives that rely on embedded connectivity solutions.

At the same time, regulatory complexity across regions is encouraging strategic partnerships between telecom operators, OEMs, and platform providers to ensure compliance and interoperability across global markets.

Countries with innovation-friendly regulatory environments are emerging as early adopters of advanced eSIM applications, while stricter regulatory regimes are shaping more controlled and phased deployment models.

Global eSIM Market Regulatory & Policy Environment Forward Outlook

Between 2026 and 2033, the regulatory environment for the global eSIM market is expected to move toward greater harmonization, standardization, and digital security enforcement. GSMA standards are likely to become even more deeply integrated into national telecom regulations, ensuring consistent global interoperability.

Governments are expected to expand policy support for 5G, IoT, and connected mobility ecosystems, further strengthening the role of eSIM technology in digital infrastructure development. Regulatory frameworks will increasingly focus on enabling seamless cross-border connectivity and multi-network switching capabilities.

Cybersecurity and digital identity regulations are expected to become more stringent, particularly as eSIM becomes widely used in mission-critical applications such as autonomous vehicles, healthcare devices, and industrial automation systems.

At the same time, global efforts toward digital inclusion and connectivity expansion are likely to accelerate eSIM adoption in emerging markets, supported by telecom liberalization and infrastructure modernization initiatives.

Overall, the regulatory and policy landscape will remain a key determinant of innovation speed, market entry strategies, and ecosystem partnerships in the global eSIM market. Companies that align early with evolving telecom standards, cybersecurity frameworks, and data governance policies will maintain a strong competitive advantage in the expanding digital connectivity ecosystem.