Global Extrusion Machinery Market Size and Share Analysis 2026-2033

Global Extrusion Machinery Market Size & Forecast

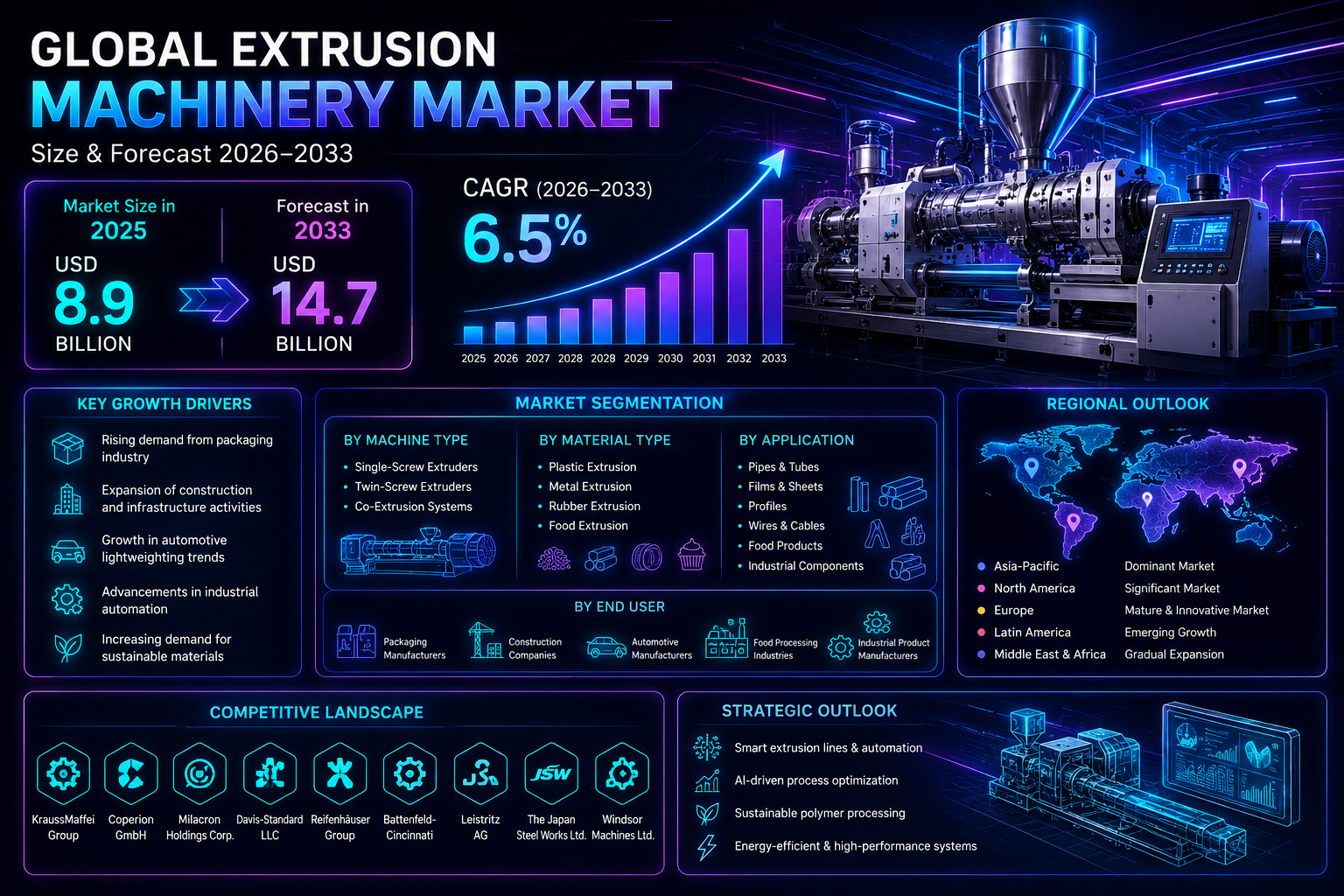

The global extrusion machinery market is projected to witness steady and technology-driven growth during the forecast period from 2026 to 2033. The market was valued at approximately USD 8.9 billion in 2025 and is expected to reach nearly USD 14.7 billion by 2033, expanding at a CAGR of around 6.5%. The market growth is driven by rising demand from packaging, construction, automotive, and plastic processing industries, along with increasing industrial automation and material innovation trends. Extrusion machinery is used to shape raw materials such as plastics, metals, rubber, and food products by forcing them through a die to create continuous profiles. These machines are widely used in manufacturing pipes, films, sheets, wires, tubes, profiles, and packaging materials. The market is undergoing transformation due to advancements in energy-efficient machinery, automated control systems, high-precision extrusion technologies, and integration of Industry 4.0-based monitoring and predictive maintenance systems. Additionally, rising demand for lightweight materials, sustainable packaging solutions, and high-performance industrial components is further accelerating global adoption of extrusion machinery.

Global Extrusion Machinery Market Overview

The extrusion machinery market is a key segment of the global industrial machinery and manufacturing equipment industry. It plays a critical role in producing continuous-form materials used across construction, automotive, consumer goods, packaging, and industrial applications. The market includes single-screw extruders, twin-screw extruders, co-extrusion systems, and specialized extrusion lines for plastics, metals, and food processing applications. Manufacturers are increasingly adopting automated extrusion systems equipped with real-time monitoring, temperature control precision, and digital process optimization technologies. Technological advancements in polymer processing, biodegradable plastics, and high-performance composite materials are expanding application areas for extrusion machinery. Major market participants include KraussMaffei Group, Coperion GmbH, Milacron Holdings Corp., The Japan Steel Works Ltd., Davis-Standard LLC, Reifenh??user Group, Battenfeld-Cincinnati, Leistritz AG, JSW Plastics Machinery, and Windsor Machines Ltd.Key Drivers of Global Extrusion Machinery Market Growth

Rising Demand from Packaging Industry

The growing global packaging industry, particularly flexible packaging and plastic films, is driving strong demand for extrusion machinery. Extrusion systems are widely used to manufacture multilayer films, containers, and packaging sheets.Expansion of Construction and Infrastructure Activities

Increasing construction activities worldwide are fueling demand for extruded pipes, profiles, and insulation materials. PVC pipes, window profiles, and construction sheets represent major application areas.Growth in Automotive Lightweighting Trends

The automotive industry is increasingly adopting lightweight materials to improve fuel efficiency and reduce emissions. Extrusion machinery is essential for producing plastic components, trims, seals, and structural parts.Advancements in Industrial Automation

Integration of Industry 4.0 technologies such as IoT sensors, AI-based monitoring, and predictive maintenance is enhancing extrusion efficiency and reducing downtime. Smart extrusion systems are improving production accuracy and operational efficiency.Increasing Demand for Sustainable Materials

Growing adoption of biodegradable plastics and recyclable materials is driving innovation in extrusion technology. Manufacturers are developing machinery capable of processing bio-based polymers and advanced composites.Global Extrusion Machinery Market Segmentation

By Machine Type

The market is segmented into single-screw extruders, twin-screw extruders, and co-extrusion systems. Twin-screw extruders dominate high-performance applications due to better mixing and processing capabilities.By Material Type

The market includes plastic extrusion, metal extrusion, rubber extrusion, and food extrusion machinery. Plastic extrusion holds the largest share due to widespread industrial usage across packaging and construction sectors.By Application

Applications include pipes & tubes, films & sheets, profiles, wires & cables, food products, and industrial components. Films and sheets represent a major segment driven by packaging industry demand.By End User

End users include packaging manufacturers, construction companies, automotive manufacturers, food processing industries, and industrial product manufacturers. Packaging and construction sectors remain the dominant end-user industries.Regional Market Dynamics

Asia-Pacific

Asia-Pacific dominates the global extrusion machinery market due to strong manufacturing bases, rapid industrialization, and expanding packaging and construction industries. China and India are major contributors supported by large-scale production facilities and infrastructure development.North America

North America holds a significant share due to advanced manufacturing technologies, strong packaging demand, and automation adoption. The United States leads regional demand in industrial extrusion applications.Europe

Europe is a mature market driven by technological innovation, sustainability initiatives, and strong automotive and packaging industries. Germany, Italy, and France are key manufacturing hubs.Latin America

Latin America is witnessing gradual growth due to rising industrialization and infrastructure development. Brazil and Mexico are leading regional markets.Middle East & Africa

The region is expanding due to construction growth, infrastructure investments, and increasing industrial diversification efforts.Competitive Landscape

The global extrusion machinery market is moderately consolidated with several established industrial machinery manufacturers competing on technology, efficiency, and customization. Key players include KraussMaffei Group, Coperion GmbH, Milacron Holdings Corp., Davis-Standard LLC, Reifenh??user Group, Battenfeld-Cincinnati, Leistritz AG, The Japan Steel Works Ltd., JSW Plastics Machinery, and Windsor Machines Ltd. Companies are focusing on automation integration, energy-efficient machinery designs, advanced control systems, and sustainable material processing capabilities. Strategic partnerships with packaging, automotive, and construction industries are driving market expansion.Strategic Outlook

The strategic outlook for the global extrusion machinery market remains positive due to increasing industrial automation and rising demand for high-performance manufacturing systems. Future opportunities include smart extrusion lines, AI-driven process optimization, sustainable polymer processing, and fully automated production systems. Growing focus on circular economy initiatives and recyclable material processing is expected to further reshape the market landscape. Manufacturers investing in digital transformation, energy-efficient systems, and advanced material compatibility are likely to gain strong competitive advantages.Final Market Perspective

The global extrusion machinery market continues to evolve as industries demand more efficient, automated, and sustainable manufacturing solutions. Rising demand from packaging, construction, automotive, and industrial sectors will continue driving market expansion throughout the forecast period. Companies that successfully integrate smart manufacturing technologies, process efficiency, and sustainable production capabilities will remain strongly positioned in the evolving extrusion machinery market.Table of Contents

Table of Contents

- Executive Summary

- Global Extrusion Machinery Market Overview (2026-2033)

- Market Size & CAGR Analysis

- Key Market Highlights

- Growth Outlook Through 2033

- Introduction & Market Overview

- Definition of Extrusion Machinery

- Scope of the Study

- Working Principle of Extrusion Systems

- Types of Extrusion Processes

- Industry Value Chain Analysis

- Technology Evolution in Extrusion Machinery

- Research Methodology

- Primary Research Approach

- Secondary Research Sources

- Market Estimation Model

- Forecast Assumptions (2026-2033)

- Data Validation & Triangulation

- Market Dynamics

- Drivers

- Rising Demand from Packaging Industry

- Expansion of Construction & Infrastructure Activities

- Growth in Automotive Lightweighting Trends

- Advancements in Industrial Automation (Industry 4.0)

- Increasing Demand for Sustainable Materials

- Restraints

- High Capital Investment Requirements

- Volatility in Raw Material Prices

- Complex Maintenance & Operational Requirements

- Energy Consumption Challenges

- Opportunities

- Adoption of Smart & Automated Extrusion Lines

- Growth in Biodegradable Polymer Processing

- Expansion of Lightweight Automotive Components

- Development of High-Performance Composite Materials

- Challenges

- Technological Integration Complexity

- Competition from Low-Cost Manufacturers

- Need for Skilled Workforce

- Environmental & Regulatory Compliance Pressures

- Drivers

- Global Extrusion Machinery Market Analysis (USD Billion), 2026-2033

- Market Size Overview

- Growth Rate (CAGR) Analysis

- Revenue Forecast by Region

- Segment-wise Revenue Breakdown

- Technology Adoption Trends

- Production & Consumption Insights

- Market Segmentation (2026-2033)

- By Machine Type

- Single-Screw Extruders

- Twin-Screw Extruders

- Co-Extrusion Systems

- By Material Type

- Plastic Extrusion

- Metal Extrusion

- Rubber Extrusion

- Food Extrusion

- By Application

- Pipes & Tubes

- Films & Sheets

- Profiles

- Wires & Cables

- Food Products

- Industrial Components

- By End User

- Packaging Manufacturers

- Construction Companies

- Automotive Manufacturers

- Food Processing Industry

- Industrial Product Manufacturers

- By Machine Type

- Market Segmentation by Geography

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East & Africa

- Competitive Landscape

- Market Share Analysis

- Technology & Product Benchmarking

- Innovation & R&D Trends

- Strategic Partnerships & Collaborations

- Sustainability & Energy Efficiency Initiatives

- Company Profiles

- KraussMaffei Group

- Coperion GmbH

- Milacron Holdings Corp.

- Davis-Standard LLC

- Reifenh??user Group

- Battenfeld-Cincinnati

- Leistritz AG

- The Japan Steel Works Ltd.

- JSW Plastics Machinery

- Windsor Machines Ltd.

- Strategic Insights & Future Outlook

- Smart Extrusion Systems & Automation

- AI-Driven Process Optimization

- Sustainable & Biopolymer Processing Trends

- Industry 4.0 Integration in Manufacturing

- Long-Term Market Outlook (2033+)

-

Appendix

-

About Pheonix Research

-

Disclaimer

Competitive Landscape

Global Extrusion Machinery Market Competitive Intensity & Market Structure Overview

The global extrusion machinery market is moderately consolidated and highly technology-driven, with competition primarily shaped by engineering capability, process efficiency, automation integration, customization flexibility, and after-sales service strength. Leading manufacturers compete on delivering high-precision, energy-efficient, and Industry 4.0-enabled extrusion systems across plastics, metals, rubber, and food processing applications.

The market structure consists of large multinational machinery manufacturers, specialized extrusion equipment producers, and regional engineering firms catering to localized industrial demand. Increasing demand from packaging, construction, automotive, and industrial manufacturing sectors is intensifying competition, particularly in high-output and multi-material extrusion systems.

Rapid industrial automation, sustainability requirements, and demand for high-performance materials are reshaping competitive dynamics, pushing manufacturers toward smart extrusion lines with predictive maintenance and real-time process optimization capabilities.

Global Extrusion Machinery Market Competitive Intensity & Market Structure Current Scenario

Leading Extrusion Machinery & Industrial Equipment Companies

KraussMaffei Group: A global leader in polymer processing machinery, offering advanced extrusion systems with strong capabilities in plastics, composites, and high-performance manufacturing applications.

Coperion GmbH: Major provider of twin-screw extrusion systems and compounding technologies widely used in plastics, chemicals, and food processing industries.

Davis-Standard LLC: Key player specializing in extrusion systems for packaging, film, pipe, and industrial applications with strong global service networks.

Milacron Holdings Corp.: Established manufacturer of plastics processing equipment, offering extrusion solutions integrated with automation and digital control systems.

Reifenh??user Group: Leading specialist in extrusion lines for packaging films, nonwovens, and sustainable polymer processing technologies.

Battenfeld-Cincinnati: Prominent provider of extrusion machinery for pipes, profiles, and sheet applications with strong focus on energy efficiency.

Leistritz AG: Key manufacturer of twin-screw extruders used in high-precision compounding, pharmaceuticals, and advanced material processing.

The Japan Steel Works Ltd.: Major industrial machinery producer with strong capabilities in large-scale extrusion systems and heavy engineering applications.

JSW Plastics Machinery: Specialized provider of high-performance plastic extrusion machinery with strong presence in Asia-Pacific markets.

Windsor Machines Ltd.: Regional leader offering cost-effective extrusion solutions for plastic processing industries, particularly in emerging markets.

Key Competitive Intensity & Market Structure Drivers

Increasing demand for packaging films, plastic pipes, and construction materials is driving strong competition among manufacturers to deliver high-output, energy-efficient extrusion systems.

The transition toward sustainable materials and biodegradable plastics is pushing companies to develop advanced extrusion technologies capable of processing bio-based and recycled polymers.

Industrial automation and Industry 4.0 integration are becoming key differentiators, with smart extrusion lines offering real-time monitoring, predictive maintenance, and AI-based process optimization.

Rising demand for lightweight automotive components and high-performance industrial materials is further intensifying competition in twin-screw and co-extrusion system segments.

Customization capability and modular machine design are increasingly important as end users demand flexible production systems for diverse material processing requirements.

Strategic Implications of Competitive Intensity & Market Structure

Manufacturers are increasingly focusing on digital transformation, integrating IoT-enabled sensors, advanced control systems, and cloud-based monitoring platforms to improve operational efficiency and reduce downtime.

Strategic collaborations with packaging, automotive, and construction industries are becoming essential for securing long-term equipment contracts and customized production solutions.

Energy efficiency and cost optimization are emerging as key purchasing criteria, pushing vendors to develop low-energy consumption extrusion systems with improved thermal management technologies.

Global expansion strategies, particularly in Asia-Pacific and Latin America, are becoming critical as these regions experience rapid industrialization and manufacturing growth.

After-sales service networks, spare parts availability, and technical support capabilities are increasingly influencing competitive positioning in the global market.

Global Extrusion Machinery Market Competitive Intensity & Market Structure Forward Outlook

The extrusion machinery market is expected to become increasingly technology-intensive as manufacturers adopt AI-driven automation, smart manufacturing systems, and fully integrated digital production lines.

Future competition will be shaped by advancements in sustainable polymer processing, high-performance composite manufacturing, and fully automated extrusion ecosystems.

Demand for recyclable materials and circular economy-driven production systems is expected to create new opportunities for machinery innovation and process optimization.

Asia-Pacific is likely to remain the dominant growth region due to strong manufacturing expansion, while Europe will continue leading in sustainability-focused extrusion technologies.

Overall, companies that successfully combine engineering innovation, automation integration, energy efficiency, and material versatility will remain strongly positioned in the evolving global extrusion machinery market.

Value Chain

Global Extrusion Machinery Market Value Chain & Supply Chain Evolution Overview

The global extrusion machinery market value chain is evolving into a highly automated, technology-intensive, and sustainability-oriented industrial ecosystem driven by increasing demand from packaging, construction, automotive, and industrial manufacturing sectors. The industry is transitioning from conventional mechanical extrusion systems toward digitally integrated, energy-efficient, and smart manufacturing-enabled production platforms.

The value chain begins with upstream raw material and component sourcing, including high-grade steel, alloys, heating elements, screws and barrels, electric motors, gear systems, sensors, control panels, and polymer processing components. Suppliers of precision-engineered mechanical parts and industrial electronics play a critical role in ensuring machine durability, performance accuracy, and operational efficiency.

The machine design and engineering stage forms the technological core of the value chain, where manufacturers develop single-screw, twin-screw, and co-extrusion systems tailored for plastics, metals, rubber, and food processing applications. Advanced CAD/CAM design, simulation modeling, and process engineering are increasingly used to improve extrusion precision and energy efficiency.

The manufacturing and assembly segment includes fabrication of machine components, precision machining, system integration, testing, and calibration. Manufacturers are increasingly adopting automated production lines, robotic assembly systems, and digital quality control mechanisms to improve consistency and reduce production defects.

The installation and commissioning layer involves system integration at industrial facilities, including setup of extrusion lines, calibration of temperature and pressure systems, software configuration, and operator training. Industry 4.0-enabled extrusion systems are increasingly being integrated with IoT-based monitoring platforms and predictive maintenance systems.

The aftermarket services segment includes maintenance, spare parts supply, machine upgrades, software updates, and performance optimization services. Service-based revenue models are becoming increasingly important for manufacturers seeking long-term customer engagement and lifecycle revenue generation.

Sustainability and energy efficiency are becoming central pillars of the value chain. Manufacturers are increasingly focusing on low-energy consumption systems, recyclable material compatibility, and reduced carbon footprint production technologies to align with global environmental standards and circular economy initiatives.

Global Extrusion Machinery Market Value Chain & Supply Chain Evolution Current Scenario

The current extrusion machinery supply chain is characterized by strong industrial globalization, specialized manufacturing clusters, and increasing adoption of automation technologies. Asia-Pacific dominates production due to large-scale manufacturing capabilities, cost efficiency, and strong demand from packaging and construction industries.

China and India serve as major manufacturing hubs for extrusion machinery components and finished systems, supported by expanding industrial infrastructure and growing domestic demand. Europe remains a key innovation hub focusing on high-precision engineering, energy efficiency, and advanced material processing technologies.

North America plays a significant role in high-end industrial automation, smart manufacturing systems, and advanced extrusion solutions for automotive and packaging industries.

The industry is witnessing increasing adoption of Industry 4.0 technologies, including IoT-enabled sensors, AI-based process control, real-time production monitoring, and predictive maintenance systems that enhance operational efficiency and reduce downtime.

However, the market continues to face challenges related to raw material price fluctuations, high capital investment requirements, supply chain disruptions in industrial components, and increasing competition from low-cost manufacturers.

Key Value Chain & Supply Chain Evolution Signals in Global Extrusion Machinery Market

One of the most significant transformation signals is the rapid adoption of smart manufacturing technologies, including IoT-enabled extrusion lines, AI-driven process optimization, and real-time production analytics systems.

Another key signal is the growing demand for energy-efficient and low-carbon extrusion systems designed to reduce operational costs and support sustainability goals across industrial manufacturing sectors.

The increasing use of recyclable and biodegradable polymers is reshaping machinery design requirements, pushing manufacturers to develop systems capable of processing advanced sustainable materials.

Automation and robotics integration across extrusion production lines are significantly improving production speed, precision, and operational consistency while reducing labor dependency.

The expansion of circular economy initiatives is encouraging manufacturers to design machinery that supports material reuse, waste reduction, and environmentally responsible production processes.

Additionally, digital twin technology and predictive maintenance systems are becoming increasingly important for optimizing machine performance and minimizing operational downtime in industrial environments.

Strategic Implications of Value Chain & Supply Chain Evolution in Global Extrusion Machinery Market

The evolving value chain presents significant strategic implications for machinery manufacturers, industrial automation companies, component suppliers, and end-user industries. Companies offering highly automated, energy-efficient, and digitally integrated extrusion systems are gaining strong competitive advantages.

Vertical integration across component manufacturing, machine assembly, software development, and after-sales services is becoming increasingly important for improving cost efficiency and customer retention.

Investment in smart manufacturing technologies, including AI-based process control, IoT monitoring systems, and predictive maintenance platforms, is emerging as a key differentiator in industrial competitiveness.

Strategic partnerships with packaging, automotive, and construction industries are driving customized machinery development and expanding application-specific extrusion solutions.

Sustainability-focused innovation in machine design, energy efficiency, and recyclable material processing is becoming critical for long-term competitiveness in global industrial markets.

Long-term success in the extrusion machinery market will depend on balancing automation, energy efficiency, material adaptability, cost competitiveness, and digital transformation capabilities.

Global Extrusion Machinery Market Value Chain & Supply Chain Evolution Forward Outlook

Between 2026 and 2033, the extrusion machinery value chain is expected to become increasingly digitalized, automated, and sustainability-driven. Smart factories will integrate fully connected extrusion systems with AI-based process optimization and real-time production control.

Advanced robotics, digital twin technology, and predictive maintenance systems will significantly enhance machine performance, reduce downtime, and improve production efficiency across industrial applications.

The rising demand for biodegradable plastics, recycled materials, and high-performance composites will drive innovation in extrusion system design and material processing capabilities.

Energy-efficient machinery and low-emission production systems will become standard requirements as industries adopt stricter sustainability regulations and carbon reduction targets.

Global supply chains are expected to become more resilient and regionally diversified, with increased focus on localized manufacturing of critical components and reduced dependency on single-region suppliers.

Ultimately, the future extrusion machinery value chain will evolve into a highly intelligent, automated, and sustainable industrial ecosystem where digital integration, process efficiency, and environmental responsibility define long-term competitiveness.

Market-Specific Value Chain

- Component & Raw Material Sourcing: Steel suppliers, alloy manufacturers, motor and drive system providers, sensor manufacturers, industrial electronics suppliers

- Machine Design & Engineering: Extrusion system designers, CAD/CAM engineers, process simulation specialists, industrial automation developers

- Manufacturing & Assembly: Machinery manufacturers, CNC machining units, robotic assembly systems, quality testing facilities

- Installation & Integration: Industrial system integrators, automation engineers, plant setup providers, training service providers

- Aftermarket Services: Maintenance service providers, spare parts suppliers, software upgrade vendors, performance optimization companies

- End-Use Applications: Packaging manufacturing, construction materials, automotive components, industrial production, food processing, wire and cable manufacturing

Investment Activity

Global Critical Communication Market Investment & Funding Dynamics Overview

Investment and funding activity in the global critical communication market is accelerating due to rising public safety modernization programs, increasing geopolitical risks, growing cybersecurity concerns, and rapid deployment of LTE and 5G-based mission-critical communication infrastructure. Between 2026 and 2033, capital allocation is expected to increasingly focus on resilient broadband networks, AI-enabled emergency response platforms, satellite-integrated systems, private 5G deployments, and cloud-native command-and-control solutions.

The market is evolving into a strategically critical segment of the global telecommunications, defense, and public safety ecosystem. Governments, telecom operators, defense organizations, and industrial enterprises are expanding investments in secure, low-latency, and interoperable communication systems that support emergency response, disaster management, industrial safety, and military coordination.

A key structural shift shaping investment activity is the transition from legacy land mobile radio (LMR) systems to broadband-based mission-critical communication platforms. This shift is driving investments in systems capable of real-time video transmission, AI-assisted analytics, geolocation tracking, and integrated situational awareness capabilities.

Additional momentum is being driven by smart city programs, industrial digitalization, IoT-enabled infrastructure, autonomous emergency response systems, and advanced cybersecurity frameworks. The expansion of connected public safety ecosystems and cross-agency interoperability initiatives is further strengthening long-term funding pipelines.

Current Investment & Funding Landscape

Current investment activity is supported by increasing government spending on emergency communication infrastructure, rapid expansion of private LTE and 5G networks, and rising demand for resilient communication systems across defense, transportation, utilities, mining, and industrial sectors. Companies are investing in AI-driven dispatch systems, edge computing, secure communication architectures, and cloud-based operational intelligence platforms.

- North America: Leads global investment due to FirstNet expansion, strong defense spending, and advanced public safety broadband infrastructure in the United States and Canada.

- Europe: Growth supported by cross-border emergency communication initiatives, transportation modernization programs, and secure digital communication deployments.

- Asia-Pacific: Fastest-growing region driven by smart city development, urbanization, disaster management initiatives, and public safety infrastructure investments across China, India, Japan, South Korea, and Australia.

- Middle East & Africa: Expanding investments driven by homeland security modernization, oil & gas communication needs, and critical infrastructure protection programs.

Key Investment & Funding Drivers

- Expansion of LTE and 5G mission-critical networks driving broadband infrastructure investment.

- Rising public safety modernization programs increasing funding for AI-enabled emergency response systems.

- Growing cybersecurity risks accelerating investment in encrypted and resilient communication platforms.

- Increasing frequency of natural disasters driving demand for disaster-resilient communication systems.

- Industrial digitalization in utilities, mining, oil & gas, and transportation sectors supporting integrated communication investments.

- Integration of satellite communication and hybrid network architectures expanding innovation-led funding.

- Deployment of IoT sensors, drones, and edge analytics enabling real-time operational intelligence investments.

Strategic Investment Implications

- Preference for companies combining secure communications, broadband infrastructure, and AI-driven intelligence platforms.

- Increasing importance of interoperability, low latency, and predictive analytics capabilities.

- Growing strategic collaborations between telecom operators, defense agencies, and technology providers.

- Regional differentiation in investment strategies across North America, Europe, and Asia-Pacific.

- Rising demand for hybrid communication systems integrating LTE, 5G, satellite, and legacy networks.

- Expansion of AI-based emergency management and predictive incident response solutions.

- Strong emphasis on cybersecurity, scalability, and integrated communication ecosystems.

Forward Investment Outlook

The global critical communication market is expected to attract sustained long-term investment driven by expanding public safety requirements, modernization of emergency infrastructure, and rapid adoption of mission-critical broadband technologies.

Future capital flows are expected to prioritize private 5G networks, AI-powered command centers, satellite-integrated communication systems, autonomous emergency coordination platforms, and advanced cybersecurity-enabled infrastructure.

- North America: Will remain the leading investment hub due to continued public safety broadband expansion and defense communication modernization.

- Asia-Pacific: Will see strong growth driven by smart city programs and large-scale emergency infrastructure investments.

- Europe: Will focus on interoperable, secure, and cross-border critical communication systems.

Future innovation will increasingly center on AI-assisted emergency response, IoT-enabled situational awareness, drone-integrated communication systems, and edge-based operational intelligence platforms. The convergence of AI, cloud computing, and mission-critical connectivity will continue reshaping investment priorities.

Overall, sustained funding momentum is expected as critical communication systems become essential to public safety, defense readiness, and industrial resilience worldwide.

Technology & Innovation

Global Extrusion Machinery Market Technology & Innovation Landscape Overview

The global extrusion machinery market is being reshaped by rapid advancements in automation, digital manufacturing, and material processing technologies. Modern extrusion systems are evolving from conventional mechanical setups into highly intelligent, sensor-driven production platforms capable of delivering higher precision, energy efficiency, and consistent product quality across large-scale industrial operations.

A key technological shift in the market is the integration of Industry 4.0 frameworks, where extrusion lines are equipped with IoT-enabled sensors, real-time monitoring systems, and cloud-based analytics. These technologies enable continuous tracking of temperature, pressure, screw speed, and material flow, allowing manufacturers to optimize production efficiency and reduce operational downtime.

In addition, advancements in screw design engineering, die technology, and polymer processing systems are significantly improving output quality and enabling the processing of complex and high-performance materials, including biodegradable plastics and advanced composite polymers.

Global Extrusion Machinery Market Technology & Innovation Current Scenario

Currently, the extrusion machinery industry is transitioning toward highly automated and digitally controlled production environments. Manufacturers are increasingly deploying twin-screw extruders with enhanced mixing capabilities and precision control systems to meet rising demand for high-quality plastic, rubber, and composite products.

Energy efficiency has become a major focus area, with companies developing low-energy consumption motors, optimized heating and cooling systems, and advanced thermal management technologies. These improvements are helping reduce operational costs while aligning with global sustainability goals.

Predictive maintenance technologies powered by AI and machine learning are also gaining traction. These systems analyze machine performance data in real time to predict potential failures, reduce unplanned downtime, and extend equipment lifespan.

Furthermore, digital twin technology is emerging as a powerful innovation in extrusion machinery, allowing manufacturers to simulate production processes virtually, optimize machine configurations, and test material behavior before actual production.

Key Technology & Innovation Trends in Global Extrusion Machinery Market

- Industry 4.0 Integration: IoT-enabled extrusion systems with real-time monitoring, data analytics, and remote control capabilities.

- AI-Based Process Optimization: Machine learning algorithms used to optimize temperature, pressure, and material flow for improved efficiency.

- Advanced Screw & Die Design: Enhanced mechanical engineering enabling better mixing, higher output quality, and reduced material waste.

- Energy-Efficient Systems: Low-power motors, optimized heating zones, and regenerative energy systems reducing operational costs.

- Predictive Maintenance: AI-driven diagnostics systems preventing breakdowns and minimizing unplanned downtime.

- Digital Twin Technology: Virtual simulation of extrusion processes for performance optimization and defect reduction.

- Sustainable Material Processing: Machinery capable of processing biodegradable plastics, recycled polymers, and bio-based materials.

- Automated Quality Control Systems: Integrated sensors and vision systems ensuring consistent product dimensions and quality.

- High-Performance Twin-Screw Extrusion: Advanced mixing and compounding capabilities for complex material applications.

- Smart Manufacturing Integration: Seamless connectivity with factory-wide MES and ERP systems for production optimization.

Strategic Implications of Technology & Innovation

Technological advancements are fundamentally transforming the extrusion machinery industry into a highly automated, data-driven, and efficiency-oriented manufacturing ecosystem. Companies that adopt smart manufacturing technologies are achieving significant improvements in production speed, material efficiency, and product consistency.

The integration of AI and IoT is enabling manufacturers to shift from reactive maintenance to predictive and prescriptive maintenance models, reducing operational risks and enhancing equipment reliability. This is particularly important in high-volume production environments such as packaging and construction materials manufacturing.

Sustainability is also emerging as a key competitive factor. Machinery capable of processing recyclable and bio-based materials is gaining strong demand as industries move toward circular economy models and stricter environmental regulations.

However, high capital investment requirements for advanced extrusion systems and the need for skilled technical expertise remain key challenges for small and mid-sized manufacturers.

Global Extrusion Machinery Market Technology & Innovation Forward Outlook

Looking ahead, the extrusion machinery market is expected to evolve toward fully autonomous and highly intelligent production systems. AI-driven control systems, digital twins, and cloud-connected extrusion lines will become standard features in advanced manufacturing facilities.

Future innovation will focus on ultra-efficient energy systems, zero-waste manufacturing processes, and highly flexible extrusion platforms capable of processing a wide range of traditional and sustainable materials.

The increasing adoption of smart factories and fully integrated production ecosystems will further enhance operational efficiency and reduce production costs across industries such as packaging, automotive, construction, and consumer goods.

In the long term, extrusion machinery will continue evolving toward adaptive manufacturing systems capable of real-time optimization, self-correction, and autonomous operation, significantly transforming global industrial production standards.

Market Risk

Global Extrusion Machinery Market Risk Factors & Disruption Threats Overview

The global extrusion machinery market is witnessing steady expansion driven by rising demand from packaging, construction, automotive, and industrial manufacturing sectors. However, despite stable long-term growth prospects, the industry is exposed to multiple structural risks and disruption threats including raw material price volatility, cyclical industrial demand, supply chain disruptions, energy cost fluctuations, technological substitution, and increasing regulatory pressure on environmental sustainability.

One of the key risk factors impacting the extrusion machinery market is its strong dependency on capital investment cycles across end-use industries. Sectors such as construction, automotive, and packaging are highly cyclical, and any slowdown in infrastructure spending, manufacturing output, or consumer demand can significantly reduce machinery procurement and delay expansion projects.

Supply chain instability represents another major disruption threat. Extrusion machinery relies on critical components such as precision mechanical parts, motors, control systems, sensors, and electronic automation modules. Global disruptions in steel pricing, semiconductor availability, logistics bottlenecks, and geopolitical trade restrictions can lead to production delays and increased manufacturing costs.

Energy price volatility is also a growing concern for manufacturers and end-users. Extrusion processes are energy-intensive, and rising electricity and fuel costs can directly impact operational expenses, reduce profit margins, and discourage new machinery investments, particularly in cost-sensitive markets.

Technological disruption is reshaping competitive dynamics within the market. Rapid adoption of advanced manufacturing technologies such as 3D printing, additive manufacturing, and alternative forming processes in certain applications may partially substitute traditional extrusion-based production in niche segments over time.

Environmental regulations and sustainability requirements are increasingly influencing machinery design and production processes. Stricter rules on plastic usage, carbon emissions, and industrial waste management are pushing manufacturers to redesign equipment for biodegradable materials and recyclable polymers, increasing R&D costs and compliance burdens.

Global Extrusion Machinery Market Risk Factors & Disruption Threats Current Scenario

The current extrusion machinery market environment reflects strong demand recovery from packaging and infrastructure sectors, supported by automation adoption and increasing industrial production in emerging economies. Manufacturers are focusing on efficiency improvements, digital monitoring systems, and energy-optimized machinery to remain competitive.

Asia-Pacific continues to dominate demand due to large-scale manufacturing expansion in China and India, while Europe and North America are prioritizing automation upgrades and sustainable manufacturing technologies. However, uneven global economic conditions are influencing investment timing and capital expenditure decisions across industries.

The shift toward sustainable packaging and bio-based materials is also reshaping machinery requirements. While this creates new opportunities, it also introduces technical challenges in processing compatibility, requiring continuous innovation in screw design, temperature control systems, and material handling capabilities.

At the same time, manufacturers face rising competition from low-cost regional players, particularly in Asia-Pacific, where pricing pressure is intensifying. Global players are responding by investing in smart extrusion systems, predictive maintenance, and Industry 4.0-enabled production lines.

Digitalization is becoming a key differentiator, with increasing adoption of IoT-based monitoring, AI-driven process optimization, and real-time quality control systems improving efficiency and reducing downtime across extrusion operations.

Global Extrusion Machinery Market Key Risk Factors & Disruption Threat Signals

- Capital Investment Cyclicality: Dependence on construction, automotive, and packaging industry cycles affecting machinery demand.

- Raw Material Price Volatility: Fluctuations in steel, polymers, and industrial components impacting manufacturing costs.

- Supply Chain Disruptions: Delays in sourcing motors, sensors, control systems, and precision mechanical components.

- Energy Cost Fluctuations: High energy consumption in extrusion processes increasing operational and production costs.

- Technological Substitution Risk: Emerging manufacturing technologies such as additive manufacturing reducing reliance on extrusion in select applications.

- Environmental Regulations: Increasing restrictions on plastics, emissions, and industrial waste affecting equipment design requirements.

- Intense Price Competition: Growing presence of low-cost manufacturers creating pricing pressure on global players.

- Skilled Labor Shortage: Need for trained operators and technicians for advanced automated extrusion systems.

- Demand Volatility in End-Use Industries: Fluctuating demand from packaging, construction, and automotive sectors.

- Technology Upgrade Pressure: Continuous need for innovation in automation, control systems, and material processing capabilities.

Strategic Implications of Risk Factors

Extrusion machinery manufacturers must prioritize automation, energy efficiency, and digital integration to maintain competitiveness in an increasingly technology-driven industrial environment.

Diversification across end-use industries such as packaging, construction, automotive, and food processing will be critical to reducing exposure to cyclical demand fluctuations.

Strengthening supply chain resilience through multi-regional sourcing strategies and localized manufacturing can help mitigate risks associated with global component shortages and trade disruptions.

Investment in R&D for sustainable material processing, including biodegradable polymers and recyclable plastics, will become increasingly important as environmental regulations tighten globally.

Companies adopting smart manufacturing technologies, predictive maintenance systems, and AI-driven process optimization are likely to achieve stronger operational efficiency and long-term competitive advantage.

Global Extrusion Machinery Market Forward Risk Outlook

Looking ahead to 2026???2033, the extrusion machinery market is expected to remain stable but highly competitive, with growth driven by industrial automation, infrastructure expansion, and packaging demand. However, volatility in raw material costs, energy pricing, and global economic conditions will continue to influence investment cycles.

Future market transformation will be shaped by smart manufacturing ecosystems, fully automated extrusion lines, AI-integrated process control systems, and sustainable material processing technologies. These advancements will improve efficiency but also increase technological complexity and capital requirements.

The increasing shift toward circular economy models and environmentally sustainable production practices will require continuous innovation in machinery design and polymer processing capabilities.

Overall, while the global extrusion machinery market offers steady long-term growth potential, sustained competitiveness will depend on technological innovation, operational efficiency, supply chain resilience, and adaptability to evolving environmental and industrial standards.

Regulatory Landscape

Global Extrusion Machinery Market Regulatory & Policy Environment Overview

The regulatory and policy environment governing the global extrusion machinery market is shaped by industrial safety standards, manufacturing equipment compliance requirements, environmental sustainability regulations, and energy efficiency mandates. As extrusion machinery is widely used across plastics, packaging, construction, automotive, and food processing industries, it falls under multiple regulatory frameworks related to machinery safety, material processing, emissions control, and workplace safety.

Governments and regulatory bodies across regions are increasingly emphasizing sustainable manufacturing practices, reduced industrial emissions, and improved energy efficiency in heavy machinery operations. This is driving stricter compliance requirements for extrusion equipment manufacturers, particularly in relation to energy consumption, waste reduction, and compatibility with recyclable and bio-based materials.

In addition, the growing focus on circular economy policies and plastic waste reduction initiatives is influencing the design and operation of extrusion systems. Manufacturers are being encouraged to develop machinery capable of processing biodegradable polymers, recycled plastics, and advanced composite materials in line with evolving environmental regulations.

Global Extrusion Machinery Market Regulatory & Policy Environment Current Scenario

The current regulatory landscape for extrusion machinery is primarily governed by industrial machinery safety directives, environmental protection laws, and occupational health and safety standards. These regulations ensure safe operation, reduced environmental impact, and improved efficiency of extrusion systems used in industrial production environments.

In the United States, extrusion machinery is regulated under Occupational Safety and Health Administration (OSHA) standards, Environmental Protection Agency (EPA) guidelines for industrial emissions, and equipment safety requirements set by ANSI (American National Standards Institute). These frameworks focus on machine safety, operator protection, and environmental compliance in manufacturing facilities.

In Europe, extrusion machinery must comply with the EU Machinery Directive, CE marking requirements, and REACH regulations for chemical and material safety. The region also enforces strict energy efficiency and sustainability standards under the Ecodesign Directive, encouraging the adoption of low-energy, high-efficiency industrial equipment.

Asia-Pacific countries, particularly China, India, Japan, and South Korea, are strengthening regulatory oversight through industrial modernization policies, manufacturing safety standards, and environmental compliance frameworks. China???s ???Made in China 2025??? initiative and India???s industrial safety regulations are promoting automation, efficiency, and cleaner production technologies in machinery sectors.

Latin America and the Middle East & Africa are gradually aligning with global machinery safety and environmental standards, focusing on industrial modernization, infrastructure development, and improved manufacturing efficiency across key end-use industries such as packaging, construction, and automotive.

Key Regulatory & Policy Environment Signals in Global Extrusion Machinery Market

- Machinery Safety Standards: Strict industrial safety regulations ensure safe design, installation, and operation of extrusion equipment across manufacturing facilities.

- Energy Efficiency Regulations: Governments are promoting low-energy consumption machinery through efficiency standards and industrial decarbonization policies.

- Environmental Compliance Requirements: Regulations are increasingly focused on reducing emissions, waste generation, and environmental impact of manufacturing processes.

- Plastic Waste & Recycling Policies: Global initiatives targeting plastic reduction are driving demand for extrusion systems compatible with recycled and biodegradable materials.

- Industrial Automation & Digitalization Policies: Governments are supporting Industry 4.0 adoption, encouraging smart manufacturing and automated production systems.

- Workplace Safety Regulations: Occupational safety frameworks mandate protective systems, operator safety features, and risk mitigation in heavy machinery operations.

Strategic Implications of Regulatory & Policy Environment

The evolving regulatory landscape is significantly influencing technology development and investment strategies in the extrusion machinery market. Manufacturers are increasingly focusing on energy-efficient designs, automation integration, and compliance-ready systems to meet stringent global standards.

Sustainability regulations are accelerating innovation in machinery capable of processing recyclable and bio-based materials, supporting the global shift toward circular economy models. This is particularly important for packaging and plastics applications, where regulatory pressure on single-use plastics is increasing.

Industrial automation and digital manufacturing policies are driving adoption of smart extrusion systems equipped with IoT sensors, AI-based monitoring, and predictive maintenance capabilities. These technologies help manufacturers meet efficiency and compliance requirements while reducing operational downtime.

Stricter environmental and energy regulations are also encouraging companies to invest in next-generation extrusion machinery with lower carbon footprints, improved thermal efficiency, and optimized material usage.

Global Extrusion Machinery Market Regulatory & Policy Environment Forward Outlook

Between 2026 and 2033, the regulatory environment for the global extrusion machinery market is expected to become increasingly sustainability-focused and technology-driven. Governments are likely to tighten energy efficiency standards and expand regulations governing industrial emissions and material recyclability.

Circular economy policies and global plastic reduction initiatives will continue to drive demand for extrusion machinery capable of handling recycled polymers and biodegradable materials, reshaping product development strategies across the industry.

The expansion of Industry 4.0 frameworks and smart manufacturing policies will further accelerate adoption of digitally enabled extrusion systems with real-time monitoring, automation, and AI-driven process optimization.

Overall, the regulatory and policy environment will remain a key driver of innovation and modernization in the extrusion machinery market, with companies investing in sustainable technologies, advanced automation, and energy-efficient systems expected to maintain strong long-term competitiveness.