Global Helium‑3 Market Size and Share Analysis 2026-2033

Global Helium-3 (He-3) Market Size & Forecast

The global helium-3 (He-3) market is an emerging, highly strategic, and supply-constrained niche market that is expected to witness strong long-term growth during the forecast period from 2026 to 2033. Although currently small in commercial scale, the market carries exceptionally high value due to its critical applications in nuclear fusion research, quantum computing, cryogenic technologies, and national security systems.

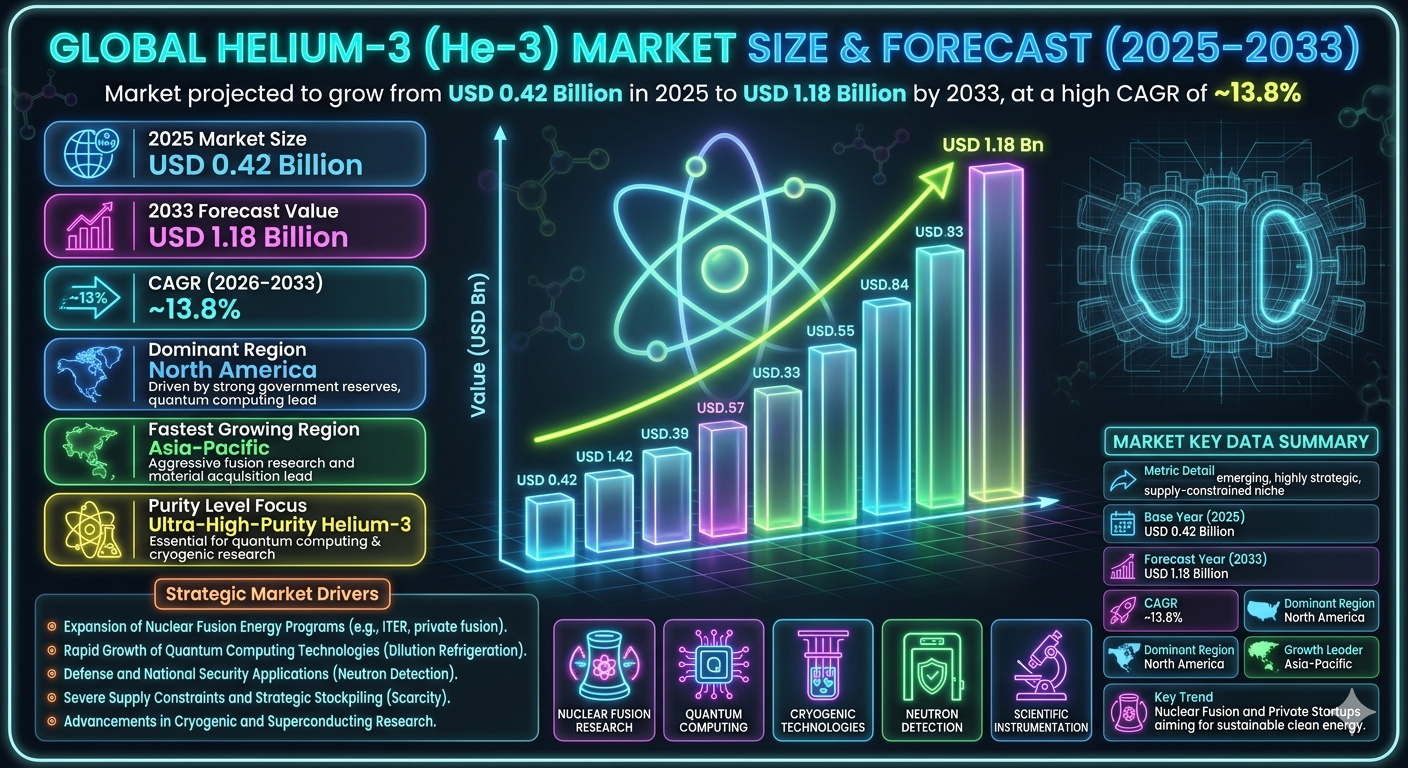

The market was valued at approximately USD 0.42 billion in 2025 and is projected to reach nearly USD 1.18 billion by 2033, expanding at a CAGR of around 13.8%. This high growth rate reflects increasing global investments in next-generation energy systems, advanced scientific research, and defense-grade detection technologies that rely on helium-3’s unique physical properties.

Helium-3 is a rare isotope of helium with extremely low natural abundance on Earth. It is primarily produced as a by-product of tritium decay in nuclear weapons programs or recovered in very limited quantities from specialized nuclear facilities. Because of this scarcity, helium-3 is considered a strategic material with geopolitical importance, often stockpiled by major economies for critical applications.

Demand for helium-3 is being driven by rapid expansion in nuclear fusion research programs such as ITER and private fusion startups aiming to achieve sustainable clean energy. In addition, quantum computing systems require ultra-low temperature environments, where helium-3 plays a vital role in dilution refrigeration systems. These high-tech applications are significantly increasing its strategic demand base.

Global Helium-3 Market Overview

The helium-3 market operates at the intersection of advanced energy research, defense technology, and scientific instrumentation. Unlike conventional industrial gases, helium-3 is not widely traded in open commodity markets, and its supply chain is tightly controlled by government agencies and nuclear institutions.

The market ecosystem includes government organizations such as the U.S. Department of Energy (DOE), national nuclear laboratories, defense agencies, aerospace research institutions, and a small number of specialized isotope suppliers. Commercial involvement is limited but expanding as private companies enter fusion energy development and quantum computing sectors.

One of the defining characteristics of this market is its extreme supply constraint. Global helium-3 availability is significantly lower than demand, creating persistent shortages and high strategic value. This imbalance has led to long-term procurement agreements, stockpiling strategies, and priority allocation for defense and research applications.

Technological advancements are gradually increasing potential demand channels. Helium-3 is increasingly being explored as a potential fuel in aneutronic nuclear fusion reactions, which could provide clean and high-efficiency energy in the future. While still experimental, this application could dramatically reshape the market if commercial fusion becomes viable.

Key Drivers of Global Helium-3 Market Growth

Expansion of Nuclear Fusion Energy Programs

One of the most significant growth drivers is the global push toward nuclear fusion as a next-generation clean energy source. Helium-3 is considered a potential fuel in advanced fusion reactions due to its ability to produce energy with minimal radioactive waste, making it highly valuable for future energy systems.

Rapid Growth of Quantum Computing Technologies

Quantum computers require extremely low temperatures close to absolute zero, achieved using helium-3-based dilution refrigeration systems. As quantum computing research accelerates globally, demand for helium-3 in cryogenic applications is increasing significantly.

Defense and National Security Applications

Helium-3 is widely used in neutron detection systems for monitoring nuclear materials, border security, and radiation detection. Governments are increasing investments in non-proliferation technologies, directly supporting demand for helium-3 detectors and systems.

Severe Supply Constraints and Strategic Stockpiling

Due to limited production sources, helium-3 is considered a strategic resource. Countries with nuclear capabilities often maintain controlled reserves, which leads to supply shortages and long-term procurement planning by research institutions and defense agencies.

Advancements in Cryogenic and Superconducting Research

Ongoing developments in superconductivity and low-temperature physics are expanding the use of helium-3 in experimental research environments, further strengthening its scientific importance.

Global Helium-3 Market Segmentation

By Application

The market is segmented into nuclear fusion research, neutron detection systems, quantum computing, cryogenics, medical imaging research, aerospace applications, and scientific instrumentation. Among these, nuclear fusion research and quantum computing are the fastest-growing segments due to increasing global investments in advanced technologies.

By End User

End users include government research organizations, defense and security agencies, nuclear laboratories, aerospace agencies, universities, and private technology companies. Government and defense sectors currently dominate due to strategic stockpiling and security-driven demand.

By Purity Level

The market includes low-purity helium-3, high-purity helium-3, and ultra-high-purity helium-3. Ultra-high-purity helium-3 is essential for quantum computing and advanced cryogenic research, making it the most valuable and scarce segment.

By Source

Helium-3 is primarily sourced from tritium decay in nuclear weapons programs, controlled nuclear reactor operations, and limited extraction from natural gas fields. Nuclear decay remains the dominant and most reliable source globally.

By Geography

The market is segmented into North America, Europe, Asia-Pacific, and Rest of the World, with supply and demand concentrated in technologically advanced and nuclear-capable regions.

Regional Market Dynamics

North America dominates the global helium-3 market due to strong government reserves, advanced nuclear infrastructure, and leadership in quantum computing and fusion energy research. The United States remains the largest holder and consumer of helium-3 resources.

Europe is actively involved in fusion energy development through ITER and other research collaborations. Countries such as France, Germany, and the UK are investing heavily in advanced physics and quantum research, supporting steady demand.

Asia-Pacific is emerging as a high-growth region, led by China’s aggressive expansion in nuclear fusion research, quantum computing, and strategic material acquisition programs. Japan and South Korea are also investing in advanced scientific applications.

Rest of the World includes limited but growing participation from regions investing in scientific infrastructure and defense modernization programs, particularly in the Middle East.

Competitive Landscape

The helium-3 market is not a traditional competitive commercial market but rather a strategically controlled ecosystem dominated by governments and nuclear institutions. Key stakeholders include the U.S. Department of Energy, national nuclear laboratories, European nuclear research organizations, and Russian nuclear agencies.

Commercial suppliers operate on a very limited scale, often under strict regulatory frameworks and government licensing systems. Private companies are primarily involved in research partnerships rather than open-market trade.

Competition is primarily driven by access to supply rather than pricing or branding. Countries and institutions with secured helium-3 reserves hold significant strategic advantages in defense, energy research, and advanced technology development.

Barriers to entry are extremely high due to scarcity of raw material, nuclear regulatory restrictions, and national security considerations, making the market highly exclusive.

Strategic Outlook

The strategic outlook for the helium-3 market is strongly tied to advancements in nuclear fusion, quantum computing, and defense technologies. As global interest in clean energy and next-generation computing increases, helium-3 is expected to gain further importance as a critical strategic isotope.

Governments are likely to continue controlling supply through strategic reserves and controlled distribution mechanisms. Private sector participation is expected to grow gradually through research collaborations and technology development partnerships.

If nuclear fusion becomes commercially viable in the long term, helium-3 demand could increase exponentially, potentially transforming it into one of the most strategically important isotopes globally.

Final Market Perspective

The global helium-3 market remains a highly specialized, supply-limited, and strategically critical segment with significant long-term growth potential. While current commercial volumes are extremely small, its importance in advanced science, defense systems, and future energy technologies is substantial.

The market’s future will be defined by breakthroughs in fusion energy, expansion of quantum computing infrastructure, and evolving geopolitical strategies around rare isotope control. Entities with secured access to helium-3 will maintain strong technological and strategic advantages in the global innovation ecosystem.

Table of Contents

Table of Contents

- 1. Executive Summary

- 1.1 Market Forecast Snapshot (2026–2033)

- 1.2 Global Helium-3 (He-3) Market Size & CAGR Analysis

- 1.3 Largest & Fastest-Growing Segments

- 1.4 Region-Level Leadership & Growth Trends

- 1.5 Key Market Drivers

- 1.6 Competitive Landscape Overview

- 1.7 Strategic Outlook Through 2033

- 2. Introduction & Market Overview

- 2.1 Definition of the Helium-3 (He-3) Market

- 2.2 Scope of the Study

- 2.3 Industry Evolution & Market Development

- 2.4 Supply Chain & Distribution Constraints

- 2.5 Impact of Nuclear & Advanced Technology Ecosystems

- 2.6 Regulatory & Geopolitical Control Framework

- 2.7 Technology & Innovation Landscape (Fusion, Quantum & Cryogenics)

- 3. Research Methodology

- 3.1 Primary Research

- 3.2 Secondary Research

- 3.3 Market Size Estimation Model

- 3.4 Forecast Assumptions (2026–2033)

- 3.5 Data Validation & Triangulation

- 4. Market Dynamics

- 4.1 Drivers

- 4.1.1 Expansion of Nuclear Fusion Energy Programs

- 4.1.2 Rapid Growth of Quantum Computing Technologies

- 4.1.3 Defense & National Security Applications

- 4.1.4 Strategic Stockpiling Due to Supply Constraints

- 4.1.5 Advancements in Cryogenic & Superconducting Research

- 4.2 Restraints

- 4.2.1 Extreme Supply Scarcity

- 4.2.2 High Geopolitical Control & Export Restrictions

- 4.2.3 Limited Commercial Availability

- 4.2.4 Dependence on Nuclear Infrastructure

- 4.3 Opportunities

- 4.3.1 Commercialization of Nuclear Fusion Energy

- 4.3.2 Expansion of Quantum Computing Industry

- 4.3.3 Growth in Advanced Cryogenic Systems

- 4.3.4 Defense Modernization Programs

- 4.4 Challenges

- 4.4.1 Extremely Limited Global Supply Base

- 4.4.2 High Security & Regulatory Barriers

- 4.4.3 Long Development Cycles for Fusion Applications

- 4.4.4 Restricted Private Sector Participation

- 4.1 Drivers

- 5. Helium-3 (He-3) Market Analysis (USD Billion), 2026–2033

- 5.1 Market Size Overview

- 5.2 CAGR Analysis

- 5.3 Regional Demand Distribution

- 5.4 Application Revenue Analysis

- 5.5 End-User Demand Analysis

- 5.6 Strategic Supply Analysis

- 6. Market Segmentation (USD Billion), 2026–2033

- 6.1 By Application

- 6.1.1 Nuclear Fusion Research

- 6.1.2 Quantum Computing

- 6.1.3 Neutron Detection Systems

- 6.1.4 Cryogenics & Low-Temperature Physics

- 6.1.5 Aerospace Applications

- 6.1.6 Scientific Instrumentation

- 6.1.7 Medical Imaging Research

- 6.2 By End User

- 6.2.1 Government Research Organizations

- 6.2.2 Defense & Security Agencies

- 6.2.3 Nuclear Laboratories

- 6.2.4 Aerospace Agencies

- 6.2.5 Universities & Academic Institutions

- 6.2.6 Private Technology Companies

- 6.3 By Purity Level

- 6.3.1 Low-Purity Helium-3

- 6.3.2 High-Purity Helium-3

- 6.3.3 Ultra-High-Purity Helium-3

- 6.4 By Source

- 6.4.1 Tritium Decay from Nuclear Programs

- 6.4.2 Nuclear Reactor By-Products

- 6.4.3 Limited Natural Gas Extraction

- 6.5 By Geography

- 6.5.1 North America

- 6.5.2 Europe

- 6.5.3 Asia-Pacific

- 6.5.4 Rest of the World

- 6.1 By Application

- 7. Market Segmentation by Geography

- 7.1 North America

- 7.2 Europe

- 7.3 Asia-Pacific

- 7.4 Rest of the World

- 8. Competitive Landscape

- 8.1 Market Structure Overview (Government-Dominated Ecosystem)

- 8.2 Supply Access & Strategic Control Analysis

- 8.3 Institutional & Government Stakeholder Mapping

- 8.4 Research Collaboration Networks

- 8.5 Competitive Intensity & Entry Barriers

- 9. Company & Institutional Profiles

- 10. Strategic Intelligence & Pheonix AI Insights

- 10.1 Pheonix Demand Forecast Engine

- 10.2 Nuclear Supply Chain & Isotope Availability Analyzer

- 10.3 Fusion & Quantum Technology Tracker

- 10.4 Defense & Strategic Material Monitoring

- 10.5 Automated Porter’s Five Forces Analysis

- 11. Future Outlook & Strategic Recommendations

- 11.1 Commercialization of Nuclear Fusion Energy

- 11.2 Expansion of Quantum Computing Ecosystem

- 11.3 Strategic Stockpiling & Global Policy Shifts

- 11.4 Growth in Cryogenic & Advanced Physics Applications

- 11.5 Long-Term Market Outlook (2033+)

- 12. Appendix

- 13. About Pheonix Research

- 14. Disclaimer

Competitive Landscape

Global Helium-3 (He-3) Market Competitive Intensity & Market Structure Overview

The Global Helium-3 (He-3) Market is an ultra-niche, strategically controlled, and supply-constrained ecosystem rather than a conventional competitive commodity market. It operates at the intersection of nuclear science, defense technology, quantum computing, and advanced energy research, making access to supply more important than pricing competition.

Competitive intensity is structurally low in a traditional commercial sense but extremely high in strategic and geopolitical terms. The market is dominated by government-controlled inventories, national laboratories, and tightly regulated nuclear infrastructure, where allocation decisions determine competitive positioning rather than open-market dynamics.

The market structure is highly centralized and monopolistic in supply nature, with the United States, Russia, and select nuclear-capable nations controlling most helium-3 production and reserves. Demand, however, is increasingly diversified across fusion energy programs, quantum computing firms, and defense agencies, creating persistent structural imbalance.

Global Helium-3 (He-3) Market Competitive Intensity & Market Structure Current Scenario

Leading Entity Profiles

U.S. Department of Energy (DOE): Global Supply Controller. Holds and manages one of the largest helium-3 reserves, allocating supply for defense, research, and quantum applications.

National Nuclear Security Administration (NNSA): Strategic Defense Authority. Oversees helium-3 extraction from tritium decay and prioritizes national security applications such as neutron detection systems.

ITER Organization: Fusion Research Consortium. Drives global demand through large-scale nuclear fusion experiments requiring advanced cryogenic and plasma research environments.

European Organization for Nuclear Research (CERN): Advanced Research Institution. Utilizes helium-3 in cryogenic systems and particle physics experiments requiring ultra-low temperature environments.

Rosatom (Russia): Nuclear Technology Leader. Controls strategic isotope production capabilities and contributes to global helium-3 supply through nuclear infrastructure.

China National Nuclear Corporation (CNNC): Emerging Strategic Player. Expanding investments in fusion energy, quantum computing, and isotope production capabilities.

National Laboratories (Los Alamos, Oak Ridge, etc.): Key Research Hubs. Critical centers for helium-3 extraction, storage, and application in advanced scientific systems.

Private Fusion Startups (Commonwealth Fusion Systems, TAE Technologies, etc.): Emerging Demand Drivers. Increasingly contributing to future demand through experimental fusion reactor development.

Quantum Computing Firms (IBM Quantum, Google Quantum AI, etc.): High-Growth Demand Segment. Require helium-3-based dilution refrigeration systems for ultra-low temperature qubit stabilization.

Defense & Aerospace Agencies (NATO-linked and national security bodies): Strategic End Users. Utilize helium-3 in neutron detection and radiation monitoring systems for security applications.

Key Competitive Intensity & Market Structure Signals in Global Helium-3 (He-3) Market

A key structural signal is extreme supply scarcity combined with rising multi-sector demand. Helium-3 production is not commercially scalable, creating a permanent supply-demand gap that drives strategic competition among governments and high-technology institutions.

Another major signal is the geopolitical concentration of supply. Countries with nuclear infrastructure and tritium stockpiles hold disproportionate control over helium-3 availability, making access highly sensitive to international relations and defense agreements.

Demand fragmentation is increasing rapidly across fusion energy, quantum computing, cryogenics, and defense systems. Each of these sectors requires different purity levels and delivery systems, further complicating allocation and distribution frameworks.

There is also a strong innovation-driven demand acceleration trend. As fusion energy research and quantum computing scale globally, helium-3 is transitioning from a research isotope to a strategic enabling material for next-generation technologies.

Market entry barriers remain absolute due to nuclear regulatory restrictions, production limitations, and national security controls, ensuring that no traditional private-market competition structure can emerge.

Strategic Implications of Competitive Intensity & Market Structure in Global Helium-3 (He-3) Market

Control over helium-3 supply directly translates into technological and strategic advantage in quantum computing, defense systems, and future energy infrastructure. Entities with secured access are positioned to lead next-generation innovation ecosystems.

Long-term contracts, government allocation frameworks, and strategic stockpiling are replacing traditional market mechanisms, making procurement planning a geopolitical and institutional priority rather than a commercial negotiation process.

Fusion energy development is emerging as the most disruptive long-term factor. If commercially viable fusion using helium-3 is achieved, demand could shift from constrained scientific usage to large-scale energy deployment.

Quantum computing expansion is another structural driver, where helium-3 remains essential for cryogenic stabilization systems, linking its supply directly to the future of computational infrastructure.

Strategically, nations are increasingly treating helium-3 as a critical mineral equivalent, aligning it with national security, energy independence, and advanced technology leadership frameworks.

Global Helium-3 (He-3) Market Competitive Intensity & Market Structure Forward Outlook

The Global Helium-3 Market is expected to remain structurally supply-constrained and strategically controlled, with no meaningful shift toward open-market competition in the foreseeable future.

Competition will increasingly be defined by geopolitical positioning, research collaboration access, and technological leadership in fusion and quantum systems rather than commercial pricing dynamics.

Future supply expansion remains limited and dependent on nuclear infrastructure, tritium decay cycles, and state-level production decisions, ensuring continued scarcity-driven dynamics.

Demand is expected to accelerate significantly as quantum computing scales commercially and fusion energy research progresses toward pilot-scale reactors, increasing strategic pressure on global reserves.

Overall, the market will continue to function as a strategic allocation ecosystem rather than a traditional commodity market, where leadership is determined by access control, technological integration, and national-level policy decisions through 2033 and beyond.

Value Chain

Global Helium-3 (He-3) Market Value Chain & Supply Chain Evolution Overview

The Global Helium-3 (He-3) Market value chain is highly unique, strategically controlled, and fundamentally different from conventional industrial gas markets. It operates at the intersection of nuclear science, defense systems, quantum technologies, and next-generation energy research. Unlike commercially abundant gases, helium-3 is extremely scarce, supply-constrained, and tightly regulated by government and nuclear authorities, making its value chain highly centralized and geopolitically sensitive.

Helium-3 is a rare isotope of helium primarily produced as a by-product of tritium decay in nuclear weapons programs or recovered in very limited quantities from specialized nuclear facilities and isotope production systems. Due to its extremely low natural abundance, the entire supply chain is structurally constrained, with production, storage, and distribution controlled by national governments and strategic research institutions.

The upstream segment of the value chain is dominated by nuclear programs, isotope production facilities, and government-controlled laboratories such as the U.S. Department of Energy (DOE), national nuclear labs, and equivalent agencies in Russia, Europe, and China. These entities manage tritium inventories and helium-3 extraction as part of broader nuclear material management strategies.

The midstream segment includes purification, isotope separation, cryogenic processing, and ultra-high-purity refinement systems. These processes are highly specialized and require advanced nuclear-grade infrastructure to ensure helium-3 meets strict purity requirements for applications such as quantum computing and cryogenic physics research.

The downstream ecosystem consists of nuclear fusion research programs, quantum computing companies, neutron detection system manufacturers, aerospace research agencies, and academic institutions. Key applications include dilution refrigeration systems, radiation detection equipment, and experimental fusion reactors.

Unlike traditional commodity markets, helium-3 is not traded in open markets. Instead, it is distributed through long-term government contracts, strategic allocations, research partnerships, and defense procurement systems. This creates a controlled, non-market-based supply chain structure.

Key challenges across the value chain include extreme resource scarcity, geopolitical control over supply, limited production scalability, high extraction costs, and strict regulatory oversight governing nuclear materials and isotopes.

Global Helium-3 (He-3) Market Value Chain & Supply Chain Evolution Current Scenario

The current helium-3 ecosystem is defined by structural scarcity, strategic stockpiling, and increasing demand from advanced scientific and defense applications. Global supply remains significantly below potential demand, creating persistent allocation constraints across research and technology sectors.

Upstream production is almost entirely dependent on tritium decay from nuclear stockpiles and controlled reactor environments. As a result, helium-3 availability is directly linked to nuclear weapons programs, decommissioning cycles, and isotope management policies.

Governments maintain strict control over distribution, prioritizing defense applications such as neutron detection systems, border security monitoring, and nuclear non-proliferation technologies. Scientific research institutions receive allocations based on strategic importance and national priorities.

The quantum computing sector is emerging as a major new demand driver, as helium-3 is essential for dilution refrigeration systems required to achieve ultra-low temperatures. This is increasing pressure on already limited global supply chains.

Fusion energy research programs, particularly ITER and private fusion startups, are also expanding long-term demand expectations, although commercialization timelines remain uncertain.

Key Value Chain & Supply Chain Evolution Signals in Global Helium-3 (He-3) Market

Several structural forces are shaping the helium-3 supply ecosystem globally.

First, the expansion of nuclear fusion research programs is increasing long-term strategic demand expectations for helium-3 as a potential aneutronic fusion fuel.

Second, rapid growth in quantum computing infrastructure is driving immediate demand for ultra-high-purity helium-3 in cryogenic cooling systems.

Third, national security and defense applications continue to dominate allocation priorities, particularly for neutron detection and radiation monitoring systems.

Fourth, supply concentration in a limited number of nuclear-capable nations is reinforcing geopolitical sensitivity and strategic resource competition.

Fifth, increasing interest in low-temperature physics and superconductivity research is expanding scientific consumption across academic and national laboratories.

Strategic Implications of Value Chain & Supply Chain Evolution in Global Helium-3 (He-3) Market

The helium-3 market is strategically controlled rather than competitively commercial, meaning access to supply is more important than pricing or market share. Governments and nuclear agencies effectively determine global availability and allocation priorities.

Countries with established nuclear infrastructure and helium-3 reserves, particularly the United States and select other nuclear powers, hold significant strategic advantages in quantum computing, defense systems, and advanced energy research.

Private sector companies operating in quantum computing, cryogenics, and fusion energy rely heavily on government partnerships and long-term procurement agreements rather than open-market purchasing.

Strategic collaboration between national laboratories, defense agencies, and emerging technology firms is becoming increasingly important to ensure supply continuity and research scalability.

Long-term competitive advantage in helium-3-dependent industries will depend on secured access agreements, technological substitution strategies, and development of alternative cryogenic solutions.

Global Helium-3 (He-3) Market Value Chain & Supply Chain Evolution Forward Outlook

Between 2026 and 2033, the helium-3 value chain is expected to become increasingly strategic, research-driven, and tightly linked to breakthroughs in quantum computing and nuclear fusion technologies.

Demand is expected to expand steadily in quantum computing and cryogenic applications, with long-term upside potential from successful commercialization of fusion energy technologies.

Supply constraints are likely to persist due to limited production sources and dependence on nuclear material cycles, reinforcing helium-3’s status as a strategic isotope.

Governments are expected to strengthen control mechanisms, expand strategic reserves, and prioritize allocation for defense and high-impact scientific applications.

Private sector participation will gradually increase through research collaborations, but full commercialization of helium-3 supply chains is unlikely in the near term due to regulatory and geopolitical constraints.

Ultimately, the helium-3 value chain will remain a hybrid system dominated by state-controlled supply and high-tech demand from frontier science and defense ecosystems.

Market-Specific Value Chain

- Nuclear Source & Tritium Decay Systems: Nuclear weapons programs, research reactors, tritium storage facilities, isotope production units

- Isotope Extraction & Processing: Cryogenic separation systems, gas purification units, isotope enrichment facilities, nuclear-grade processing labs

- Ultra-High-Purity Refinement: Advanced cryogenic purification, contamination control systems, scientific-grade isotope validation, quality assurance laboratories

- Strategic Storage & Government Allocation: National helium-3 reserves, defense stockpiles, controlled distribution systems, strategic material management agencies

- Advanced Applications Deployment: Quantum computing systems, neutron detection devices, fusion research reactors, cryogenic refrigeration systems, aerospace instrumentation

- Research & Innovation Ecosystem: National laboratories, universities, defense R&D centers, private quantum computing firms, fusion startups

Company-to-Stage Mapping

- Nuclear Source & Tritium Systems: U.S. Department of Energy (DOE), Russian nuclear agencies, Chinese nuclear programs, European nuclear institutions

- Isotope Extraction & Processing: National laboratories, specialized isotope production facilities, government-controlled nuclear research centers

- Ultra-High-Purity Refinement: National labs, advanced cryogenic research facilities, defense-grade isotope processing units

- Strategic Storage & Allocation: U.S. strategic reserves, defense ministries, nuclear regulatory authorities

- Advanced Applications Deployment: IBM Quantum, Google Quantum AI, D-Wave Systems, ITER consortium, defense technology contractors

- Research & Innovation Ecosystem: MIT, CERN, national physics laboratories, private fusion startups (Helion, TAE Technologies, Commonwealth Fusion Systems)

Investment Activity

Global Helium-3 (He-3) Market Investment & Funding Dynamics Overview

Investment and funding dynamics in the Global Helium-3 (He-3) Market are being shaped by its extreme supply scarcity, strategic geopolitical importance, and rapidly expanding applications in nuclear fusion research, quantum computing, cryogenic systems, and defense technologies. Between 2026 and 2033, capital deployment is expected to remain highly concentrated in government-backed programs, national laboratories, and frontier technology collaborations rather than traditional commercial investment channels.

The market operates within a tightly controlled strategic framework where governments—particularly those with nuclear capabilities—dominate helium-3 production, allocation, and stockpiling. Institutions such as the U.S. Department of Energy (DOE), national nuclear laboratories, European research consortia, and Asian nuclear agencies act as primary funding drivers, ensuring supply security for critical scientific and defense applications.

A defining structural shift influencing investment flows is the accelerating global race toward nuclear fusion commercialization and quantum computing scalability. These next-generation technologies are significantly increasing long-term funding commitments toward helium-3 sourcing, cryogenic infrastructure, and isotope recovery systems.

Global Helium-3 (He-3) Market Investment & Funding Dynamics Current Scenario

Currently, investment activity in the helium-3 ecosystem is highly non-commercial and predominantly government-led. Funding is directed toward strategic reserves, nuclear infrastructure, advanced research programs, and controlled isotope recovery systems from tritium decay and nuclear facilities.

- North America: Dominates global investment due to U.S. federal control of helium-3 reserves, strong funding for fusion programs (DOE, national labs), and leadership in quantum computing research.

- Europe: Focused on collaborative fusion energy investments through ITER, along with quantum research funding across France, Germany, and the UK.

- Asia-Pacific: Rapidly expanding investment base led by China’s aggressive fusion energy programs, quantum technology funding, and strategic material acquisition initiatives.

- Rest of World: Limited but growing investments in defense modernization, scientific infrastructure, and research collaborations involving advanced isotope technologies.

Key Investment & Funding Dynamics Signals in Global Helium-3 (He-3) Market

- Rising global investment in nuclear fusion energy programs is driving long-term funding commitments for helium-3 sourcing and experimental fuel cycle research.

- Quantum computing expansion is increasing demand for ultra-high-purity helium-3 in dilution refrigeration systems, attracting funding into cryogenic infrastructure development.

- Defense and national security programs are reinforcing strategic stockpiling investments for neutron detection and radiation monitoring applications.

- Severe supply constraints are prompting governments to prioritize long-term procurement contracts and reserve accumulation strategies rather than open-market purchases.

- R&D funding in superconductivity, low-temperature physics, and advanced material science is indirectly increasing helium-3 demand across research institutions.

- Private sector involvement is growing through fusion startups and quantum computing firms, but remains heavily dependent on government-controlled supply access.

Strategic Implications of Investment & Funding Dynamics in Global Helium-3 (He-3) Market

- The investment ecosystem is highly centralized, with governments and national laboratories controlling supply access, funding allocation, and strategic distribution of helium-3.

- Access to helium-3 reserves is becoming a key geopolitical and technological advantage, influencing national competitiveness in defense and advanced computing sectors.

- Funding is increasingly focused on long-term strategic applications rather than short-term commercial returns, reflecting the isotope’s critical importance in future technologies.

- Partnerships between government agencies and private fusion or quantum computing companies are emerging as key investment mechanisms for applied research.

- Supply scarcity is driving investments in alternative production pathways, including tritium recovery optimization and potential lunar resource exploration research.

- Regulatory restrictions and nuclear security frameworks significantly limit commercialization, making strategic access more important than market competition.

Global Helium-3 (He-3) Market Investment & Funding Dynamics Forward Outlook

Looking ahead, the Global Helium-3 Market is expected to witness gradually increasing investment intensity driven by accelerating breakthroughs in nuclear fusion research, quantum computing scalability, and advanced defense technologies.

Future capital allocation will remain concentrated in government-backed fusion energy programs, national isotope reserve expansion, cryogenic technology development, and high-precision scientific instrumentation requiring helium-3-based systems.

- North America: Will continue to dominate investment through DOE-led programs, fusion research funding, and quantum computing leadership.

- Europe: Will maintain strong collaborative investments in ITER and advanced physics research initiatives.

- Asia-Pacific: Will emerge as the fastest-growing investment hub driven by China’s strategic focus on fusion energy and quantum technologies.

Private sector investment will gradually increase but remain dependent on government-controlled supply access and strategic partnerships. Emerging fusion startups and quantum computing firms will continue to play a growing role in downstream demand generation.

In the long term, successful commercialization of nuclear fusion technology could dramatically increase helium-3 demand, transforming it from a niche strategic isotope into a globally critical energy resource. Until then, the market will remain defined by controlled supply, strategic stockpiling, and government-led funding ecosystems.

Technology & Innovation

Global Helium-3 (He-3) Market Technology & Innovation Landscape Overview

The Global Helium-3 (He-3) Market technology and innovation landscape is shaped by extreme scarcity, high scientific value, and its role as a critical enabling material for next-generation technologies. Unlike conventional industrial gases, helium-3 innovation is not driven by mass production but by precision engineering, isotope management systems, and advanced cryogenic and quantum technology integration.

Technological advancement in this market is primarily centered on efficient extraction methods, ultra-low temperature systems, quantum computing hardware compatibility, and nuclear-grade detection systems. Because helium-3 is a by-product of nuclear processes, innovation is closely linked to nuclear fuel cycle management, tritium decay optimization, and advanced isotope recovery systems developed by government laboratories and defense institutions.

In addition, increasing global investment in nuclear fusion research (ITER and private fusion startups) and quantum computing ecosystems is accelerating demand for helium-3-based cryogenic cooling systems. This is pushing innovation in dilution refrigerators, superconducting systems, and ultra-high-vacuum containment technologies designed to operate at near absolute-zero temperatures.

The market is also witnessing emerging R&D activity in helium-3 recycling systems, cryogenic storage optimization, and advanced neutron detection technologies. These innovations are largely being developed within national laboratories, defense agencies, and specialized aerospace and scientific research institutions due to strict regulatory and strategic control over helium-3 supply chains.

Global Helium-3 Market Technology & Innovation Landscape Current Scenario

Currently, helium-3 technology development is highly centralized and controlled, with innovation primarily originating from government research institutions such as the U.S. Department of Energy (DOE), CERN collaborations, ITER research programs, and national nuclear laboratories in Europe and Asia.

One of the most significant technology areas is cryogenic engineering, where helium-3 is used in dilution refrigeration systems to achieve temperatures below 1 Kelvin. These systems are essential for quantum computing processors, superconducting circuits, and advanced particle physics experiments.

Quantum computing is a key innovation driver. Helium-3-based cryogenic cooling enables stable qubit performance by minimizing thermal noise and maintaining quantum coherence. As quantum hardware scales, demand for helium-3-compatible cooling architectures is increasing rapidly.

In nuclear fusion research, helium-3 is being explored for aneutronic fusion reactions, which theoretically produce clean energy with minimal radioactive byproducts. This is driving innovation in plasma confinement systems, fusion reactor design, and advanced fuel cycle modeling.

Another important innovation area is neutron detection technology, where helium-3 is used in radiation monitoring systems for nuclear security, border protection, and non-proliferation compliance. Due to helium-3 shortages, alternative detection technologies such as boron-10 and lithium-based systems are also being developed, but helium-3 remains the gold standard for sensitivity and reliability.

Supply-side innovation is focused on isotope recovery optimization from tritium decay, nuclear stockpile management systems, and advanced gas separation technologies. However, scalability remains limited due to geopolitical and regulatory constraints.

Key Technology & Innovation Trends in Global Helium-3 Market

- Cryogenic Dilution Refrigeration Systems: Advanced cooling systems enabling ultra-low temperature environments for quantum computing and physics research.

- Quantum Computing Cooling Integration: Helium-3-based thermal stability solutions for superconducting qubit architectures.

- Nuclear Fusion Fuel Cycle Research: Exploration of helium-3 in aneutronic fusion reactions for clean energy generation.

- Advanced Neutron Detection Systems: High-sensitivity radiation detection used in defense, border security, and nuclear monitoring.

- Isotope Recovery & Recycling Technologies: Systems designed to maximize helium-3 extraction from tritium decay processes.

- Ultra-High Purity Gas Processing: Refinement technologies ensuring helium-3 purity for quantum and cryogenic applications.

- Superconducting Material Integration: Support systems for superconducting magnets and quantum research infrastructure.

- Strategic Isotope Management Systems: Government-led inventory control and controlled distribution technologies for rare isotopes.

Strategic Implications of Technology & Innovation

Technological innovation in the helium-3 market has strong geopolitical and strategic implications due to its scarcity and dual-use applications in both civilian research and defense systems. Control over helium-3 technology development is closely tied to national security, scientific leadership, and future energy competitiveness.

Countries and institutions with access to helium-3 reserves and cryogenic technology infrastructure hold a significant advantage in quantum computing development, fusion energy research, and advanced defense systems. This creates a high barrier ecosystem where innovation is tightly linked to national strategic priorities rather than open commercial competition.

The convergence of quantum computing, nuclear fusion research, and cryogenic engineering is expected to redefine helium-3 demand patterns over the long term. As these technologies mature, helium-3 will transition from a niche research isotope to a critical enabler of next-generation computing and energy systems.

However, supply constraints will continue to shape innovation pathways, encouraging parallel development of alternative materials and substitute technologies, particularly in neutron detection and cryogenic cooling systems.

Global Helium-3 Market Technology & Innovation Forward Outlook

Looking ahead, the helium-3 market is expected to evolve through breakthrough advancements in nuclear fusion energy, quantum computing scalability, and cryogenic engineering systems. Innovation will remain concentrated in high-security research environments and national laboratories due to strict regulatory controls.

If commercial nuclear fusion becomes viable, helium-3 could experience a paradigm shift in demand, positioning it as a strategic fuel source for aneutronic fusion reactors. This would significantly expand its industrial relevance beyond research and defense applications.

In quantum computing, the scaling of qubit systems will require increasingly sophisticated helium-3-based cooling architectures, driving continued innovation in dilution refrigeration efficiency and system miniaturization.

Advances in isotope recovery, storage stability, and cryogenic transport systems are also expected to improve supply efficiency, although absolute availability will remain constrained in the foreseeable future.

In conclusion, the Global Helium-3 Market technology landscape is defined by high scientific complexity, strategic scarcity, and deep integration with frontier technologies. Innovation in this market will continue to be driven by nuclear research, quantum computing, and defense applications, making helium-3 one of the most strategically significant isotopes in the global advanced technology ecosystem.

Market Risk

Global Helium-3 (He-3) Market Risk Factors & Disruption Threats Overview

The Global Helium-3 (He-3) Market is an ultra-niche, strategically sensitive, and supply-constrained isotope market operating at the intersection of nuclear science, defense technology, and next-generation energy systems. Despite its strong long-term demand potential, the market carries an extremely high strategic and geopolitical risk profile due to severe supply limitations, national security controls, technological uncertainty, and dependence on state-level nuclear infrastructure.

One of the most critical risk factors is extreme supply scarcity. Helium-3 production is largely dependent on tritium decay from nuclear weapons programs and limited nuclear facility outputs, making global availability structurally constrained and highly non-scalable under current conditions.

Another major disruption factor is geopolitical control over supply chains. Since helium-3 is considered a strategic material, its production, stockpiling, and distribution are tightly regulated by a small number of nuclear-capable nations, creating long-term uncertainty in global access and pricing stability.

Additionally, demand uncertainty from emerging technologies such as nuclear fusion and quantum computing introduces volatility, as commercialization timelines remain highly experimental and dependent on long-term scientific breakthroughs.

Regulatory and national security restrictions further intensify market barriers, limiting international trade, restricting private sector participation, and centralizing control within government and defense institutions.

Global Helium-3 (He-3) Market Risk Factors & Disruption Threats Current Scenario

The current market environment is defined by extremely limited supply availability and high-priority allocation to defense, nuclear research, and critical scientific applications. Most helium-3 volumes are pre-allocated through long-term government contracts and strategic reserves.

However, demand from quantum computing and fusion research programs is rising rapidly, creating a widening gap between supply and emerging high-tech requirements. This imbalance is increasing procurement competition among research institutions and defense agencies.

The market is also experiencing growing dependency on government-controlled nuclear infrastructure, making supply vulnerable to policy shifts, geopolitical tensions, and changes in national defense priorities.

Private sector participation remains limited, with most companies operating through partnerships or government-funded research collaborations rather than open-market transactions.

At the same time, uncertainty surrounding the commercial viability of helium-3 fusion energy continues to delay large-scale investment decisions, keeping market expansion largely speculative in the short to medium term.

Key Risk Factors & Disruption Threats Signals in Global Helium-3 (He-3) Market

A major disruption signal is the accelerating global race in nuclear fusion research, where competing technologies may either significantly increase helium-3 demand or bypass its need altogether depending on reactor design outcomes.

Rapid advancements in quantum computing are increasing demand for ultra-low temperature cryogenic systems, directly intensifying pressure on limited helium-3 supplies used in dilution refrigeration technologies.

Geopolitical competition for strategic isotopes is emerging as a key signal, with nations increasingly prioritizing domestic stockpiling and supply security over international distribution.

Technological substitution risks are also present, particularly in cryogenics and neutron detection systems, where alternative materials and advanced sensor technologies could reduce long-term dependency on helium-3 in certain applications.

Additionally, lack of scalable production pathways remains a structural constraint, with no commercially viable large-scale helium-3 synthesis method currently available, reinforcing long-term supply rigidity.

Strategic Implications of Risk Factors & Disruption Threats in Global Helium-3 (He-3) Market

Market participants must prioritize long-term supply security strategies, including strategic stockpiling agreements, government partnerships, and exclusive procurement arrangements to ensure access to helium-3 resources.

Investment in alternative production research, including lunar exploration initiatives and advanced nuclear fuel cycle innovations, will become increasingly important for future supply diversification.

Countries and institutions with secured helium-3 reserves will maintain significant strategic leverage in quantum computing, defense systems, and fusion research, reinforcing the importance of resource concentration.

Collaborative frameworks between governments, national laboratories, and private technology firms will be essential to manage allocation efficiency and support innovation in high-demand applications.

Strategic risk management will increasingly depend on balancing scientific advancement with geopolitical stability, as helium-3 remains tightly linked to national security and advanced technology leadership.

Global Helium-3 (He-3) Market Risk Factors & Disruption Threats Forward Outlook

Looking ahead to 2026–2033, the Helium-3 Market is expected to remain structurally supply-constrained but strategically expanding in importance due to rising investments in nuclear fusion, quantum computing, and advanced defense systems.

Demand growth is likely to accelerate significantly if fusion energy technologies reach commercial viability, potentially transforming helium-3 into a critical global energy enabler.

However, supply-side rigidity will continue to define market dynamics, with production remaining heavily dependent on nuclear decay processes and state-controlled inventories.

Emerging geopolitical competition for strategic isotopes is expected to intensify, reinforcing national-level control over production, storage, and distribution networks.

Overall, the market’s future will be shaped by a combination of scientific breakthroughs, geopolitical strategies, and technological evolution, where access to helium-3 will remain a decisive factor in next-generation energy and computing leadership.

Regulatory Landscape

Global Helium-3 (He-3) Market Regulatory & Policy Environment Overview

The regulatory and policy environment for the Global Helium-3 (He-3) Market is highly sensitive, tightly controlled, and strategically governed due to the isotope’s extreme scarcity and its critical role in nuclear research, quantum computing, and defense applications. Helium-3 is classified as a strategic material in many jurisdictions, and its production, storage, transfer, and utilization are subject to strict governmental oversight and nuclear regulatory frameworks.

Unlike conventional industrial commodities, helium-3 is primarily regulated through nuclear governance systems rather than open-market trade rules. Agencies such as the U.S. Department of Energy (DOE), Nuclear Regulatory Commission (NRC), International Atomic Energy Agency (IAEA), and equivalent national nuclear authorities oversee production pathways, particularly those linked to tritium decay and nuclear facility by-products.

Export control regimes such as the Wassenaar Arrangement and national defense export laws further restrict cross-border movement of helium-3 due to its dual-use potential in nuclear detection systems, advanced scientific instrumentation, and strategic defense applications. This makes helium-3 one of the most tightly controlled isotopes in global trade policy.

In addition, international nuclear non-proliferation treaties and strategic material security frameworks influence how helium-3 is allocated, stored, and distributed. Governments prioritize defense, energy research, and critical scientific applications, often maintaining centralized reserves to ensure national security and technological advantage.

Global Helium-3 Market Regulatory & Policy Environment Current Scenario

The current regulatory landscape is defined by centralized control, limited commercial availability, and strict allocation policies governed by national nuclear agencies. North America dominates regulatory control, with the United States maintaining the largest helium-3 reserves primarily through tritium decay programs associated with defense infrastructure.

In Europe, helium-3 utilization is primarily governed through research-focused frameworks linked to CERN, ITER, and national nuclear research programs. Regulatory oversight is coordinated through EU nuclear safety directives and member-state atomic energy authorities, ensuring controlled use in scientific and fusion energy applications.

Asia-Pacific is rapidly expanding its regulatory and strategic frameworks, particularly in China, which is investing heavily in fusion research, quantum computing, and strategic isotope acquisition. Japan and South Korea also maintain strict nuclear material governance systems aligned with advanced scientific research programs.

Russia continues to play a key role in nuclear isotope production and controlled distribution through its national nuclear agencies, maintaining strategic reserves and regulated export channels for helium-3 used in scientific and defense applications.

Across all regions, helium-3 remains subject to strict licensing, end-use verification, and national security clearance processes, limiting commercial accessibility and reinforcing its status as a strategic resource rather than a tradable commodity.

Key Regulatory & Policy Environment Signals in Global Helium-3 Market

- Nuclear Material Control Regulations: Helium-3 production and distribution are governed by national nuclear authorities due to its origin from tritium decay and reactor-based systems.

- Export Control & Dual-Use Restrictions: International trade is restricted under defense and dual-use export control frameworks such as the Wassenaar Arrangement.

- Strategic Material Stockpiling Policies: Governments maintain controlled reserves of helium-3 for defense, fusion research, and critical scientific applications.

- Nuclear Non-Proliferation Compliance: International treaties regulate isotope handling to prevent misuse in nuclear weaponization or unauthorized applications.

- Fusion Energy Research Governance: Regulatory frameworks supporting ITER and national fusion programs influence helium-3 allocation for energy research.

- Scientific & Defense End-Use Certification: Strict verification systems ensure helium-3 is used only in approved quantum, cryogenic, or security applications.

Strategic Implications of Regulatory & Policy Environment in Global Helium-3 Market

Regulatory control over helium-3 supply creates a highly centralized and geopolitically sensitive market structure where access is more important than pricing dynamics. Governments with nuclear infrastructure and tritium production capabilities hold a significant strategic advantage in controlling global supply distribution.

Export restrictions and national security classifications limit private sector participation, making helium-3 access dependent on government contracts, research partnerships, and defense agreements. This creates long-term procurement stability for approved institutions but restricts open-market commercialization.

Fusion energy research programs and quantum computing development initiatives are increasingly shaping allocation priorities. Governments are directing helium-3 supplies toward high-impact scientific programs, reinforcing its role as a strategic enabler of next-generation technologies.

Supply scarcity and regulatory bottlenecks are also driving increased investment in alternative isotope research and helium-3 recovery technologies. However, regulatory approval for new production pathways remains highly stringent due to nuclear safety and proliferation concerns.

Overall, regulatory frameworks are reinforcing helium-3’s position as a controlled strategic asset rather than a conventional industrial input, shaping long-term geopolitical and technological competition.

Global Helium-3 Market Regulatory & Policy Environment Forward Outlook

Between 2026 and 2033, the regulatory environment for the Global Helium-3 Market is expected to remain highly restrictive, with continued emphasis on national security, nuclear governance, and controlled scientific utilization. Expansion of fusion energy programs is likely to increase demand pressure, but supply will remain tightly regulated.

North America is expected to maintain dominant control over helium-3 reserves, with continued prioritization of defense applications, neutron detection systems, and quantum computing research under strict DOE and NRC oversight.

Europe will continue focusing on regulated scientific collaboration through ITER and quantum research initiatives, with helium-3 access governed by EU nuclear safety frameworks and member-state research allocations.

Asia-Pacific is expected to strengthen its strategic material policies, particularly in China, where fusion energy and quantum technology investments may drive increased state-controlled helium-3 acquisition and stockpiling strategies.

Globally, regulatory coordination through international nuclear governance bodies is expected to intensify, ensuring controlled distribution, end-use verification, and prevention of unauthorized applications of helium-3 in sensitive technologies.

Overall, the helium-3 regulatory landscape will continue to evolve as a geopolitically critical framework, balancing scientific advancement with national security priorities. Access to helium-3 will remain tightly controlled, and entities with secured governmental partnerships will retain a decisive advantage in advanced energy, defense, and quantum technology development.