Global Industrial Ethanol Market 2025-2033

Overview

The Global Industrial Ethanol Market is witnessing steady growth as industries increasingly rely on ethanol as a key feedstock for solvents, paints, coatings, and household as well as industrial applications. Rising demand across chemical manufacturing, personal care, and cleaning products, coupled with sustainability initiatives and regulatory support for low-carbon solvents, is driving the adoption of industrial ethanol globally.

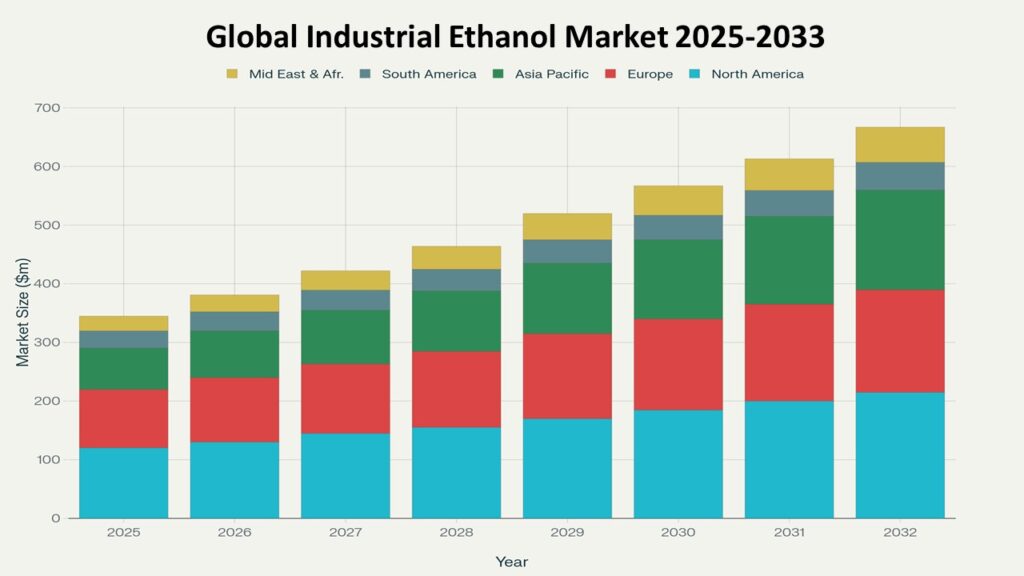

According to Phoenix’s Demand Forecast Engine, the global Industrial Ethanol Market is expected to grow from USD 28.7 billion in 2025 to approximately USD 58.9 billion by 2033, registering a CAGR of 9.1%. In 2024, North America accounted for the largest market share, while Asia Pacific is anticipated to be the fastest-growing region over the forecast period.

Key Drivers of Market Growth

Rising Demand in Chemical and Coatings Industries

The Industrial Ethanol Market is being fueled by increasing consumption in solvents, coatings, paints, and adhesives. Ethanol serves as a versatile, high-purity solvent, supporting both traditional industrial processes and emerging green chemistry solutions.

Household and Personal Care Applications

Ethanol is a critical component in personal care products, disinfectants, and cleaning agents. Post-COVID awareness around hygiene and disinfectants has significantly contributed to the growth of the Industrial Ethanol Market globally.

Sustainability and Regulatory Support

Environmental policies and regulations promoting low-VOC solvents and renewable chemicals are positively impacting the Industrial Ethanol Market. Industries are increasingly replacing petrochemical solvents with bioethanol-derived solutions to meet ESG compliance and carbon reduction targets.

Integration Across the Ethanol Value Chain

The Industrial Ethanol Market is closely connected to upstream segments such as Ethanol Production, Ethanol Feedstock, Ethanol Processing & Refining, Second-Generation Ethanol, and downstream applications like Ethanol Fuel Blending, Pharmaceutical Ethanol, Beverage Ethanol, Sustainable Ethanol, and global trade flows in Bioethanol Export Markets.

Market Segmentation

By Application

- Solvents & Cleaning Agents – High-purity ethanol for industrial cleaning, degreasing, and chemical processes.

- Paints, Coatings & Adhesives – Ethanol as a solvent and carrier in paints, varnishes, inks, and coatings.

- Household Products – Disinfectants, cleaning liquids, and personal care formulations.

- Others – Industrial intermediates, extraction processes, and specialty chemical production.

By Type

- Denatured Ethanol – For industrial use where purity is regulated but ingestion is prohibited.

- Absolute / Anhydrous Ethanol – High-purity ethanol for specialty solvents and chemical reactions.

- Synthetic Ethanol – Produced via ethylene hydration, often used in regions with feedstock constraints.

By End-User Industry

- Chemical & Pharmaceutical – Raw material for chemical synthesis and pharmaceutical formulations.

- Personal Care & Cosmetics – Fragrances, lotions, and sanitizers.

- Paints, Coatings & Adhesives – Industrial and commercial construction applications.

- Food Processing & Beverage – Minor applications overlapping with beverage ethanol.

Region-Level Insights

North America – CAGR (2025–2033): 8.7%

North America dominates the Industrial Ethanol Market, driven by large-scale chemical manufacturing, stringent solvent regulations, and strong industrial infrastructure.

Europe – CAGR (2025–2033): 7.9%

Europe’s market growth is supported by environmental regulations, VOC reduction mandates, and rising adoption of bio-based solvents in industrial applications.

Asia Pacific – CAGR (2025–2033): 11.5% (Fastest Growing Region)

Rapid industrialization, increasing production of paints, coatings, and personal care products, along with policy incentives for renewable chemicals, are fueling the Industrial Ethanol Market in India, China, and Southeast Asia.

Latin America

Emerging industrial hubs in Brazil and Mexico are contributing to growth through integration with ethanol feedstock availability and downstream applications like fuel blending and industrial chemicals.

Leading Companies in the Market

Key players influencing the Industrial Ethanol Market include:

- POET LLC

- Green Plains Inc.

- Cargill Inc.

- Archer Daniels Midland (ADM)

- Louis Dreyfus Company

These companies are expanding production capacities, investing in sustainable ethanol technologies, and integrating with downstream industrial applications.

Strategic Insights

- The Industrial Ethanol Market plays a central role in the global ethanol value chain, connecting upstream production, feedstock supply, processing, and refining with downstream applications like fuel blending, beverage ethanol, pharmaceutical ethanol, sustainable ethanol, and global trade.

- Rising regulatory and sustainability focus is encouraging industrial users to adopt ethanol-based solvents, driving higher volumes and diversification.

- Scenario analysis suggests that Asia Pacific will see rapid adoption of bioethanol-derived solvents and industrial chemicals by 2033.

Forecast Snapshot: 2025–2033

| Metric | Value |

| 2025 Market Size | USD 28.7 Billion |

| 2033 Market Size | ~USD 58.9 Billion |

| CAGR (2025–2033) | 9.1% |

| Largest Region | North America |

| Key Application | Solvents & Coatings |

| Trend | Bio-based Solvents & Sustainable Industrial Applications |

| Future Focus | Asia Pacific Expansion & Industrial Integration |

Why the Market Remains Critical

- The Industrial Ethanol Market ensures a steady supply of ethanol for chemical, coatings, personal care, and household applications.

- It strengthens the ethanol ecosystem by linking upstream production, feedstock, refining, and sustainable ethanol initiatives.

- Serves as a foundation for downstream markets like fuel blending, beverage ethanol, pharmaceutical ethanol, and global trade.

Final Takeaway

The Global Industrial Ethanol Market is a pivotal segment of the ethanol ecosystem, enabling the transition toward sustainable industrial processes. Driven by increasing adoption in chemicals, paints, coatings, and personal care products, the market is poised for consistent growth from 2025 to 2033.

Integration with related markets—Ethanol Production, Ethanol Feedstock, Ethanol Processing & Refining, Second-Generation Ethanol, Ethanol Fuel Blending, Beverage Ethanol, Pharmaceutical Ethanol, Bioethanol Trade & Export, and Sustainable Ethanol—forms a cohesive and high-value ethanol value chain globally.

Table of Contents

Executive Summary

1.1. Market Snapshot (2025–2033)

1.2. Key Market Insights & Trends

1.3. Analyst Recommendations

1.4. Strategic Importance of Ethanol in Global Energy, Industrial, and Bioeconomy Applications

1.5. Phoenix AI Strategic Insights

Market Overview

2.1. Definition & Scope of the Global Ethanol Market

2.2. Ethanol Production & Processing Overview (Fermentation, Distillation, Dehydration, Purification, By-product Utilization)

2.3. Market Dynamics

2.3.1. Drivers

2.3.2. Restraints

2.3.3. Opportunities

2.3.4. Challenges

2.4. Impact of Sustainability Goals & Energy Transition Policies

2.5. Phoenix AI Insights: Future Production & Consumption Landscape

Ethanol Industry Ecosystem

3.1. Raw Material Supply Chain (Corn, Sugarcane, Molasses, Wheat, Cellulosic Biomass, Lignocellulosic Residues, Other By-products)

3.2. Technology Providers & Equipment Manufacturers

3.3. Production Plant Operators

3.4. Distribution & Logistics Partners

3.5. Downstream Industries Consuming Ethanol (Fuel, Industrial, F&B, Pharmaceuticals, Chemicals, Bioenergy)

Market Segmentation – By Processing Technology

4.1. Distillation & Rectification – Traditional and Advanced Distillation for Fuel and Industrial-Grade Ethanol

4.2. Dehydration Technologies – Molecular Sieves, Azeotropic, and Membrane-Based Dehydration for High-Purity Ethanol

4.3. Filtration & Purification – Activated Carbon, Ion Exchange, and Ceramic Filtration for Impurity Removal

4.4. By-Product Utilization – Dried Distillers Grains (DDGS), Lignin, and Other Co-Products Management

Market Segmentation – By Feedstock Input

5.1. Corn-Based Ethanol – Most Prevalent Feedstock in North America

5.2. Sugarcane-Based Ethanol – Major Contributor in Latin America and Parts of Asia

5.3. Cellulosic & Lignocellulosic Biomass – Includes Crop Residues, Wood, and Grasses; Fast-Growing Segment

5.4. Molasses & Other Fermentation By-Products – Niche but Valuable for Specialized Ethanol Production

Market Segmentation – By End-Use Application

6.1. Fuel Blending

6.1.1. Blend Type

-

E10 (10% ethanol, 90% gasoline) – Standard vehicles in North America, Europe, Asia

-

E15 (15% ethanol, 85% gasoline) – Higher renewable fuel mandates

-

E85 (Flexible-Fuel Vehicles) – North America and Brazil

-

Other Blends (E20, E25, etc.) – Emerging markets and industrial/fleet applications

6.1.2. Vehicle Type

-

Passenger Vehicles – Compact cars, sedans, SUVs (E10/E15)

-

Commercial Vehicles – Light-duty trucks, buses, delivery fleets (higher blends)

-

Flexible-Fuel Vehicles (FFVs) – Operate on E85/intermediate blends

-

Two/Three-Wheelers – Low-carbon solutions in Asia/LATAM

6.1.3. Distribution Channel

-

Fuel Stations & Retail Networks – Blended gasoline via service stations

-

Direct Industrial & Fleet Supply – Bulk blending for corporate fleets, public transport, industrial operations

-

Infrastructure & Storage – Ethanol-compatible pipelines, storage tanks, terminals

6.2. Industrial & Specialty Applications

6.2.1. Application

-

Solvents & Cleaning Agents – Industrial cleaning, degreasing, chemical processes

-

Paints, Coatings & Adhesives – Solvent & carrier in paints, varnishes, inks, coatings

-

Household Products – Disinfectants, cleaning liquids, personal care formulations

-

Others – Industrial intermediates, extraction processes, specialty chemicals

6.2.2. Type

-

Denatured Ethanol – Industrial use, regulated purity, not for ingestion

-

Absolute / Anhydrous Ethanol – High-purity for specialty solvents & reactions

-

Synthetic Ethanol – Produced via ethylene hydration; alternative feedstock regions

6.2.3. End-User Industry

-

Chemical & Pharmaceutical – Raw materials for chemical synthesis & pharma formulations

-

Personal Care & Cosmetics – Fragrances, lotions, sanitizers

-

Paints, Coatings & Adhesives – Industrial & commercial construction applications

-

Food Processing & Beverage – Minor overlaps with beverage ethanol

6.3. Pharmaceutical & Healthcare Applications – Disinfectants, Sanitizers, High-Purity Ethanol for Drug Formulations

6.4. Beverage Applications – Distilleries and Breweries Using Refined Ethanol for Spirits and Liquors

Regional Market Analysis

7.1. North America

7.1.1. U.S.

7.1.2. Canada

7.2. Latin America

7.2.1. Brazil

7.2.2. Argentina

7.2.3. Rest of LATAM

7.3. Europe

7.3.1. Germany

7.3.2. France

7.3.3. UK

7.3.4. Rest of Europe

7.4. Asia-Pacific

7.4.1. China

7.4.2. India

7.4.3. Japan

7.4.4. Rest of APAC

7.5. Middle East & Africa

Competitive Landscape

8.1. Market Share Analysis of Leading Players

8.2. Production Capacity & Plant Location Mapping

8.3. Strategic Developments (Expansions, Partnerships, Mergers, Acquisitions)

8.4. Company Profiles (Up to Top 15 Players)

– Archer Daniels Midland Company

– POET, LLC

– Green Plains Inc.

– Raízen S.A.

– Valero Renewable Fuels Company LLC

– Flint Hills Resources

– Others

Market Forecast & Outlook (2025–2033)

9.1. Global Ethanol Production Volume Outlook (Billion Liters)

9.2. Global Ethanol Market Value Outlook (USD Billion)

9.3. Regional Growth Projections

9.4. Phoenix AI Predictive Modelling Scenarios

Regulatory & Policy Framework

10.1. Global Renewable Energy Directives

10.2. Country-Level Ethanol Production Incentives & Mandates

10.3. Trade Regulations & Tariff Impacts

Emerging Trends & Innovations

11.1. Second-Generation (2G) & Advanced Ethanol Production

11.2. Enzyme & Bioprocess Innovations

11.3. AI, IoT & Process Optimization

11.4. Distillation, Dehydration & Waste-to-Ethanol Technology

Strategic Recommendations

12.1. Entry Strategies for New Market Entrants

12.2. Capacity Expansion Strategies for Existing Players

12.3. Diversification into Co-Products (DDGS, Lignin, CO₂, Biodiesel)

12.4. Investment Hotspots by Region & Technology

Appendix

13.1. Abbreviations & Glossary

13.2. Research Methodology

13.3. Data Sources

13.4. Phoenix AI Research Credentials