Global Japanese Restaurant Market Report, Size & Forecast 2026-2033

Global Japanese Restaurant Market Forecast Snapshot: 2026???2033

| Metric | Value |

|---|---|

| 2025 Market Size | USD 19.61 Billion |

| 2033 Market Size | ~USD 25.50 Billion |

| CAGR (2026???2033) | ~3.99% |

| Largest Region | Asia-Pacific |

| Fastest Growing Region | Asia-Pacific |

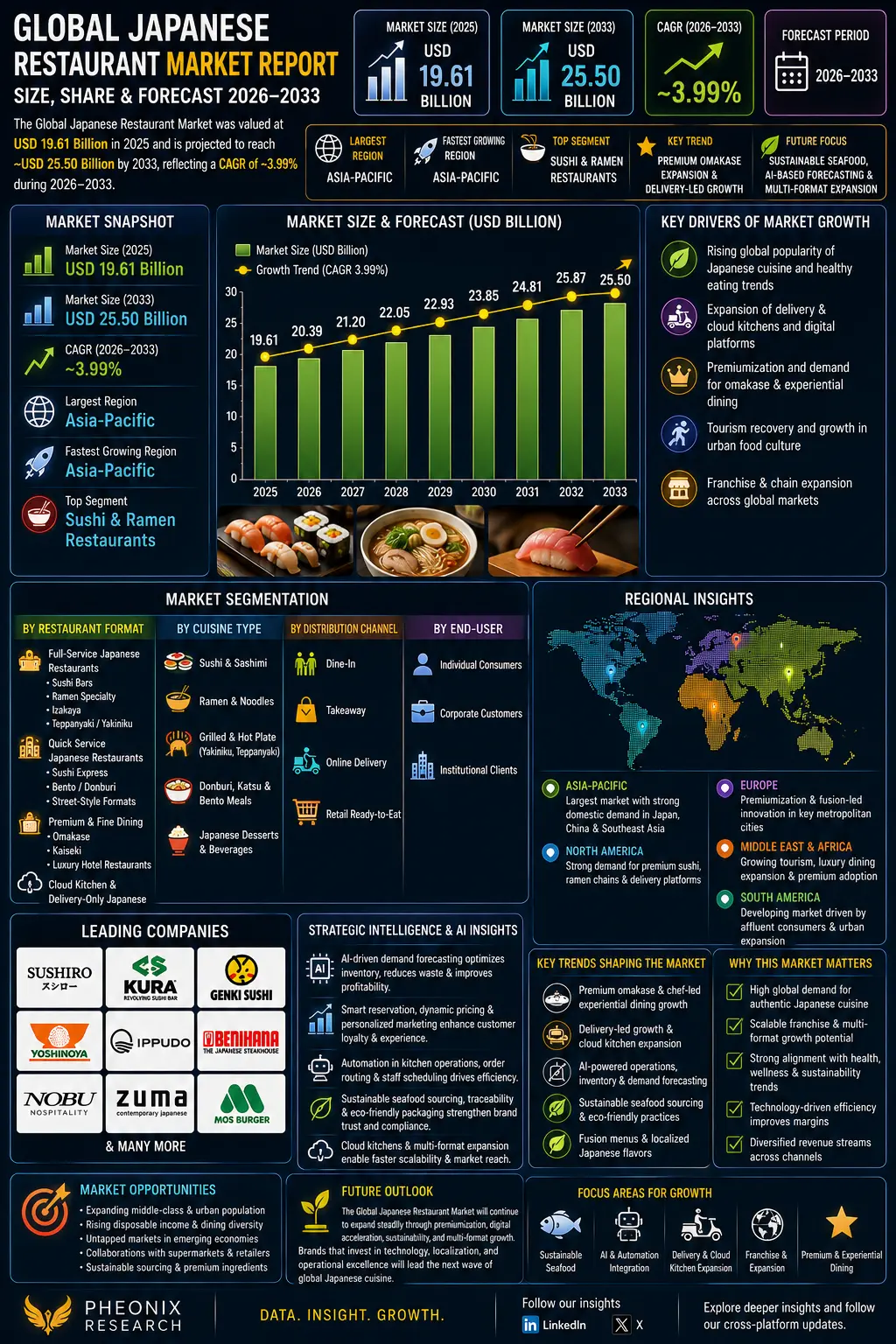

| Top Segment | Sushi & Ramen Restaurants |

| Key Trend | Premium Omakase Expansion & Delivery-Led Growth |

| Future Focus | Sustainable Seafood, AI-Based Demand Forecasting & Multi-Format Expansion |

Global Japanese Restaurant Market Overview

The Global Japanese Restaurant Market encompasses full-service restaurants, quick-service formats, premium omakase concepts, ramen specialty outlets, sushi chains, izakaya dining formats, and delivery-only cloud kitchens specializing in Japanese cuisine.

Japanese food has become super popular. It's because people worldwide love Japanese culture like sushi and ramen, healthy food is trending, fancy dining is in demand, and food delivery apps make it easy to get Japanese food

According to Pheonix Research, the Global Japanese Restaurant Market size is valued at USD 19.61 billion in 2025 and is projected to reach approximately USD 25.50 billion by 2033, reflecting a CAGR of ~3.99% during 2026???2033.

Asia-Pacific holds the largest share due to strong domestic consumption in Japan, China, and Southeast Asia. The region is also expected to register the fastest growth, supported by urban expansion, tourism recovery, and rising middle-class dining expenditure.

The Post-2025 outlook for the Global Japanese Restaurant Market indicates accelerated premiumization, wider adoption of delivery-first and cloud-kitchen formats, strengthened sustainable seafood sourcing practices, and greater integration of AI-powered inventory management and customer personalization systems to enhance operational efficiency and profitability.

Key Drivers of Global Japanese Restaurant Market Growth

1. Rising Global Popularity of Japanese Cuisine

Sushi, ramen, donburi, and teppanyaki are widely perceived as premium yet healthy dining options. The global acceptance of seafood-based diets and umami flavors continues to drive adoption.

2. Expansion of Delivery & Cloud Kitchens

Japanese cuisine is highly compatible with takeaway and delivery formats. Sushi boxes, ramen bowls, and bento meals are scalable across digital platforms, reducing capital-intensive dine-in dependency.

3. Premiumization & Experiential Dining

Omakase, chef-led tasting menus, and kaiseki experiences are gaining traction among high-income urban consumers seeking authenticity and exclusivity.

4. Tourism & Urban Food Culture

International tourism and metropolitan entertainment districts significantly boost Japanese restaurant footfall, especially in luxury and fine-dining segments.

5. Franchise & Chain Expansion

Global brands such as Sushiro, Kura Sushi, Yoshinoya, and Ippudo are expanding internationally through scalable franchise models.

Global Japanese Restaurant Market Segmentation

1. By Restaurant Format

1.1 Full-Service Japanese Restaurants

1.1.1 Sushi-Focused Restaurants

1.1.1.1 Traditional Sushi Bars

1.1.1.2 Conveyor Belt Sushi (Kaiten-Zushi)

1.1.1.3 Premium Sushi Lounges

1.1.2 Ramen Specialty Restaurants

1.1.2.1 Tonkotsu Ramen Shops

1.1.2.2 Regional Ramen Concepts

1.1.2.3 Fast-Casual Ramen Chains

1.1.3 Izakaya & Small-Plate Concepts

1.1.3.1 Traditional Izakaya

1.1.3.2 Modern Fusion Izakaya

1.1.3.3 Bar-Led Japanese Dining

1.1.4 Teppanyaki & Yakiniku Restaurants

1.1.4.1 Live-Grill Teppanyaki

1.1.4.2 Yakiniku BBQ Dining

1.1.4.3 Interactive Chef-Led Formats

1.2 Quick Service Japanese Restaurants

1.2.1 Sushi Express Counters

1.2.1.1 Mall-Based Units

1.2.1.2 Transit Hub Counters

1.2.1.3 Grab-and-Go Sushi Bars

1.2.2 Bento & Donburi Chains

1.2.2.1 Rice Bowl Quick Service

1.2.2.2 Katsu & Tempura Counters

1.2.2.3 Value Meal Chains

1.2.3 Japanese Street-Style Formats

1.2.3.1 Takoyaki Stalls

1.2.3.2 Okonomiyaki Counters

1.2.3.3 Pop-Up Japanese Food Trucks

1.3 Premium & Fine Dining Japanese

1.3.1 Omakase Restaurants

1.3.1.1 Michelin-Star Omakase

1.3.1.2 Chef-Owned Boutique Concepts

1.3.1.3 Reservation-Only Dining

1.3.2 Kaiseki Dining

1.3.2.1 Seasonal Kaiseki

1.3.2.2 Cultural Experience Dining

1.3.3 Luxury Hotel Japanese Restaurants

1.3.3.1 Five-Star Hotel Concepts

1.3.3.2 Resort-Based Japanese Dining

1.4 Cloud Kitchen & Delivery-Only Japanese

1.4.1 Sushi Delivery Brands

1.4.1.1 App-Based Sushi Chains

1.4.1.2 Subscription Sushi Models

1.4.2 Multi-Brand Asian Cloud Kitchens

1.4.2.1 Japanese + Korean Hybrid Kitchens

1.4.2.2 Pan-Asian Delivery Brands

1.4.3 Aggregator-Led Virtual Brands

1.4.3.1 Platform-Owned Concepts

1.4.3.2 Influencer-Led Delivery Brands

2. By Cuisine Type

2.1 Sushi & Sashimi2.1.1 Nigiri Sushi

2.1.1.1 Traditional Tuna (Maguro)

2.1.1.2 Salmon (Sake)

2.1.1.3 Ebi (Shrimp)

2.1.1.4 Tamago (Egg)

2.1.2 Maki Rolls

2.1.2.1 Hosomaki (Thin Rolls)

2.1.2.2 Uramaki (Inside-Out Rolls)

2.1.2.3 Futomaki (Thick Rolls)

2.1.2.4 Specialty / Fusion Rolls

2.1.3 Sashimi

2.1.3.1 Tuna Sashimi

2.1.3.2 Salmon Sashimi

2.1.3.3 Yellowtail (Hamachi)

2.1.3.4 Premium Seasonal Fish

2.1.4 Premium Sushi Concepts

2.1.4.1 Omakase Sushi

2.1.4.2 Chef???s Signature Platters

2.1.4.3 Luxury Seafood (Uni, Toro, Caviar Fusion)

2.2 Ramen & Noodles

2.2.1 Ramen Varieties

2.2.1.1 Tonkotsu Ramen

2.2.1.2 Shoyu Ramen

2.2.1.3 Miso Ramen

2.2.1.4 Shio Ramen

2.2.2 Regional & Specialty Ramen

2.2.2.1 Hakata Style

2.2.2.2 Sapporo Style

2.2.2.3 Tokyo Style

2.2.3 Other Japanese Noodles

2.2.3.1 Udon

2.2.3.2 Soba

2.2.3.3 Cold Noodle Variants

2.3 Grilled & Hot Plate (Yakiniku, Teppanyaki)

2.3.1 Yakiniku (Japanese BBQ)

2.3.1.1 Beef Yakiniku

2.3.1.2 Wagyu Cuts

2.3.1.3 Mixed Meat Platters

2.3.2 Teppanyaki

2.3.2.1 Seafood Teppanyaki

2.3.2.2 Steak Teppanyaki

2.3.2.3 Interactive Chef-Led Dining

2.3.3 Robatayaki & Grill Variants

2.3.3.1 Skewered Meats

2.3.3.2 Grilled Vegetables

2.3.3.3 Seafood Skewers

2.4 Donburi, Katsu & Bento Meals

2.4.1 Donburi (Rice Bowls)

2.4.1.1 Gyudon (Beef Bowl)

2.4.1.2 Katsudon

2.4.1.3 Unadon (Eel Bowl)

2.4.2 Katsu Variants

2.4.2.1 Chicken Katsu

2.4.2.2 Pork Tonkatsu

2.4.2.3 Curry Katsu

2.4.3 Bento Meals

2.4.3.1 Standard Bento Boxes

2.4.3.2 Premium Executive Bento

2.4.3.3 Healthy / Low-Calorie Bento

2.5 Japanese Desserts &??Beverages

2.5.1 Traditional Desserts

2.5.1.1 Mochi

2.5.1.2 Dorayaki

2.5.1.3 Matcha-Based Desserts

2.5.2 Modern Japanese Sweets

2.5.2.1 Japanese Cheesecake

2.5.2.2 Matcha Tiramisu

2.5.2.3 Fusion Pastries

2.5.3 Beverages

2.5.3.1 Matcha & Green Tea

2.5.3.2 Japanese Soft Drinks

2.5.3.3 Sake & Japanese Alcoholic Beverages

??3. By Distribution Channel

3.1 Dine-In3.1.1 Casual Dining

3.1.1.1 Family-Oriented Restaurants

3.1.1.2 Urban Casual Outlets

3.1.2 Premium Dining

3.1.2.1 Omakase Counters

3.1.2.2 Fine Dining Japanese

3.1.3 Mall & Hospitality Dining

3.1.3.1 Shopping Mall Restaurants

3.1.3.2 Hotel-Based Japanese Restaurants

3.2 Takeaway

3.2.1 Counter Pickup

3.2.1.1 Sushi Grab-and-Go

3.2.1.2 Bento Express Counters

3.2.2 Pre-Order Pickup

3.2.2.1 App-Based Pickup

3.2.2.2 Scheduled Meal Pickup

3.3 Online Delivery

3.3.1 Third-Party Aggregators

3.3.1.1 App-Based Delivery

3.3.1.2 Subscription Delivery Models

3.3.2 Brand-Owned Delivery

3.3.2.1 In-House Delivery Fleet

3.3.2.2 Hybrid Delivery Model

3.3.3 Cloud Kitchen Delivery

3.3.3.1 Single-Brand Japanese Kitchens

3.3.3.2 Multi-Brand Asian Kitchens

3.4 Retail Ready-to-Eat

3.4.1 Supermarket Sushi

3.4.1.1 Fresh Sushi Packs

3.4.1.2 Value Sushi Combos

3.4.2 Meal Kits

3.4.2.1 Ramen Kits

3.4.2.2 DIY Sushi Kits

4. By End-User

4.1 Individual Consumers 4.1.1 Millennials4.1.1.1 Urban Professionals

4.1.1.2 Experience-Oriented Diners 4.1.2 Gen Z

4.1.2.1 Social Media-Driven Consumers

4.1.2.2 Trend-Focused Diners 4.1.3 Working Professionals

4.1.3.1 Lunch Crowd

4.1.3.2 After-Work Dining 4.1.4 Families

4.1.4.1 Weekend Dining

4.1.4.2 Celebration Dining

4.2 Corporate Customers 4.2.1 Corporate Catering

4.2.1.1 Executive Meetings

4.2.1.2 Corporate Events 4.2.2 Office Meal Programs

4.2.2.1 Subscription Lunch Plans

4.2.2.2 Bulk Bento Orders 4.2.3 Event Orders

4.2.3.1 Private Parties

4.2.3.2 Business Conferences

4.3 Institutional Clients 4.3.1 Universities

4.3.1.1 Campus Food Courts

4.3.1.2 Student Meal Contracts 4.3.2 Hospitals

4.3.2.1 Patient Meal Services

4.3.2.2 Staff Cafeterias 4.3.3 Office Complexes

4.3.3.1 IT Parks

4.3.3.2 Business District Cafeterias

Leading Companies in the Global Japanese Restaurant Market

-

Genki Sushi

-

Yoshinoya

-

Ippudo

-

Benihana

-

Nobu Hospitality

-

Zuma Restaurants

-

MOS Burger

The market remains highly fragmented, with a strong presence of independent premium operators alongside global franchise chains.

Table of Contents

Executive Summary

1.1 Market Forecast Snapshot (2026???2033)

1.2 Global Market Size & CAGR Analysis

1.3 Largest & Fastest-Growing Segments

1.4 Region-Level Leadership & Growth Trends

1.5 Key Market Drivers

1.6 Competitive Landscape Overview

1.7 Strategic Outlook Through 2033

Introduction & Market Overview

1.1 Definition of the Global Japanese Restaurant Market

1.2 Scope of the Study

1.3 Industry Evolution & Market Development

1.4 Supply Chain & Distribution Infrastructure

1.5 Impact of Consumer Trends

1.6 Sustainability & Regulatory Landscape

1.7 Technology & Innovation Landscape

Research Methodology

1.1 Primary Research

1.2 Secondary Research

1.3 Market Size Estimation Model

1.4 Forecast Assumptions (2026???2033)

1.5 Data Validation & Triangulation

Market Dynamics

1.1 Drivers

1.1.1 Rising Global Popularity of Japanese Cuisine

1.1.2 Expansion of Delivery & Cloud Kitchens

1.1.3 Premiumization & Experiential Dining

1.1.4 Tourism & Urban Food Culture

1.1.5 Franchise & Chain Expansion

1.2 Restraints

1.2.1 High Cost of Premium Seafood & Ingredients

1.2.2 Supply Chain Complexity & Import Dependency

1.2.3 Regulatory & Food Safety Compliance

1.2.4 Market Fragmentation & Brand Standardization Challenges

1.3 Opportunities

1.3.1 Expansion into Emerging Markets & Urban Clusters

1.3.2 Growth of Premium Omakase & Fine Dining

1.3.3 AI-Based Demand Forecasting & Personalization

1.3.4 Sustainable Seafood & Plant-Based Innovation

1.4 Challenges

1.4.1 Maintaining Authenticity Across Global Markets

1.4.2 Operational Cost & Margin Pressure

1.4.3 Competitive Differentiation in Saturated Markets

1.4.4 Supply Chain Traceability & Sustainability

Global Japanese Restaurant Market Analysis (USD Billion), 2026???2033

1.1 Market Size Overview

1.2 CAGR Analysis

1.3 Regional Revenue Distribution

1.4 Segment Revenue Analysis

1.5 Distribution Channel Analysis

1.6 Consumer Impact Analysis

Market Segmentation (USD Billion), 2026???2033

1.1 By Restaurant Format

1.1.1 Full-Service Japanese Restaurants

1.1.1.1 Sushi-Focused Restaurants

1.1.1.1.1 Traditional Sushi Bars

1.1.1.1.2 Conveyor Belt Sushi (Kaiten-Zushi)

1.1.1.1.3 Premium Sushi Lounges

1.1.1.2 Ramen Specialty Restaurants

1.1.1.2.1 Tonkotsu Ramen Shops

1.1.1.2.2 Regional Ramen Concepts

1.1.1.2.3 Fast-Casual Ramen Chains

1.1.1.3 Izakaya & Small-Plate Concepts

1.1.1.3.1 Traditional Izakaya

1.1.1.3.2 Modern Fusion Izakaya

1.1.1.3.3 Bar-Led Japanese Dining

1.1.1.4 Teppanyaki & Yakiniku Restaurants

1.1.1.4.1 Live-Grill Teppanyaki

1.1.1.4.2 Yakiniku BBQ Dining

1.1.1.4.3 Interactive Chef-Led Formats

1.1.2 Quick Service Japanese Restaurants

1.1.2.1 Sushi Express Counters

1.1.2.1.1 Mall-Based Units

1.1.2.1.2 Transit Hub Counters

1.1.2.1.3 Grab-and-Go Sushi Bars

1.1.2.2 Bento & Donburi Chains

1.1.2.2.1 Rice Bowl Quick Service

1.1.2.2.2 Katsu & Tempura Counters

1.1.2.2.3 Value Meal Chains

1.1.2.3 Japanese Street-Style Formats

1.1.2.3.1 Takoyaki Stalls

1.1.2.3.2 Okonomiyaki Counters

1.1.2.3.3 Pop-Up Japanese Food Trucks

1.1.3 Premium & Fine Dining Japanese

1.1.3.1 Omakase Restaurants

1.1.3.1.1 Michelin-Star Omakase

1.1.3.1.2 Chef-Owned Boutique Concepts

1.1.3.1.3 Reservation-Only Dining

1.1.3.2 Kaiseki Dining

1.1.3.2.1 Seasonal Kaiseki

1.1.3.2.2 Cultural Experience Dining

1.1.3.3 Luxury Hotel Japanese Restaurants

1.1.3.3.1 Five-Star Hotel Concepts

1.1.3.3.2 Resort-Based Japanese Dining

1.1.4 Cloud Kitchen & Delivery-Only Japanese

1.1.4.1 Sushi Delivery Brands

1.1.4.1.1 App-Based Sushi Chains

1.1.4.1.2 Subscription Sushi Models

1.1.4.2 Multi-Brand Asian Cloud Kitchens

1.1.4.2.1 Japanese + Korean Hybrid Kitchens

1.1.4.2.2 Pan-Asian Delivery Brands

1.1.4.3 Aggregator-Led Virtual Brands

1.1.4.3.1 Platform-Owned Concepts

1.1.4.3.2 Influencer-Led Delivery Brands

1.2 By Cuisine Type

1.2.1 Sushi & Sashimi

1.2.1.1 Nigiri Sushi

1.2.1.1.1 Traditional Tuna (Maguro)

1.2.1.1.2 Salmon (Sake)

1.2.1.1.3 Ebi (Shrimp)

1.2.1.1.4 Tamago (Egg)

1.2.1.2 Maki Rolls

1.2.1.2.1 Hosomaki (Thin Rolls)

1.2.1.2.2 Uramaki (Inside-Out Rolls)

1.2.1.2.3 Futomaki (Thick Rolls)

1.2.1.2.4 Specialty / Fusion Rolls

1.2.1.3 Sashimi

1.2.1.3.1 Tuna Sashimi

1.2.1.3.2 Salmon Sashimi

1.2.1.3.3 Yellowtail (Hamachi)

1.2.1.3.4 Premium Seasonal Fish

1.2.1.4 Premium Sushi Concepts

1.2.1.4.1 Omakase Sushi

1.2.1.4.2 Chef???s Signature Platters

1.2.1.4.3 Luxury Seafood (Uni, Toro, Caviar Fusion)

1.2.2 Ramen & Noodles

1.2.2.1 Ramen Varieties

1.2.2.1.1 Tonkotsu Ramen

1.2.2.1.2 Shoyu Ramen

1.2.2.1.3 Miso Ramen

1.2.2.1.4 Shio Ramen

1.2.2.2 Regional & Specialty Ramen

1.2.2.2.1 Hakata Style

1.2.2.2.2 Sapporo Style

1.2.2.2.3 Tokyo Style

1.2.2.3 Other Japanese Noodles

1.2.2.3.1 Udon

1.2.2.3.2 Soba

1.2.2.3.3 Cold Noodle Variants

1.2.3 Grilled & Hot Plate (Yakiniku, Teppanyaki)

1.2.3.1 Yakiniku (Japanese BBQ)

1.2.3.1.1 Beef Yakiniku

1.2.3.1.2 Wagyu Cuts

1.2.3.1.3 Mixed Meat Platters

1.2.3.2 Teppanyaki

1.2.3.2.1 Seafood Teppanyaki

1.2.3.2.2 Steak Teppanyaki

1.2.3.2.3 Interactive Chef-Led Dining

1.2.3.3 Robatayaki & Grill Variants

1.2.3.3.1 Skewered Meats

1.2.3.3.2 Grilled Vegetables

1.2.3.3.3 Seafood Skewers

1.2.4 Donburi, Katsu & Bento Meals

1.2.4.1 Donburi (Rice Bowls)

1.2.4.1.1 Gyudon (Beef Bowl)

1.2.4.1.2 Katsudon

1.2.4.1.3 Unadon (Eel Bowl)

1.2.4.2 Katsu Variants

1.2.4.2.1 Chicken Katsu

1.2.4.2.2 Pork Tonkatsu

1.2.4.2.3 Curry Katsu

1.2.4.3 Bento Meals

1.2.4.3.1 Standard Bento Boxes

1.2.4.3.2 Premium Executive Bento

1.2.4.3.3 Healthy / Low-Calorie Bento

1.2.5 Japanese Desserts & Beverages

1.2.5.1 Traditional Desserts

1.2.5.1.1 Mochi

1.2.5.1.2 Dorayaki

1.2.5.1.3 Matcha-Based Desserts

1.2.5.2 Modern Japanese Sweets

1.2.5.2.1 Japanese Cheesecake

1.2.5.2.2 Matcha Tiramisu

1.2.5.2.3 Fusion Pastries

1.2.5.3 Beverages

1.2.5.3.1 Matcha & Green Tea

1.2.5.3.2 Japanese Soft Drinks

1.2.5.3.3 Sake & Japanese Alcoholic Beverages

1.3 By Distribution Channel

1.3.1 Dine-In

1.3.1.1 Casual Dining

1.3.1.1.1 Family-Oriented Restaurants

1.3.1.1.2 Urban Casual Outlets

1.3.1.2 Premium Dining

1.3.1.2.1 Omakase Counters

1.3.1.2.2 Fine Dining Japanese

1.3.1.3 Mall & Hospitality Dining

1.3.1.3.1 Shopping Mall Restaurants

1.3.1.3.2 Hotel-Based Japanese Restaurants

1.3.2 Takeaway

1.3.2.1 Counter Pickup

1.3.2.1.1 Sushi Grab-and-Go

1.3.2.1.2 Bento Express Counters

1.3.2.2 Pre-Order Pickup

1.3.2.2.1 App-Based Pickup

1.3.2.2.2 Scheduled Meal Pickup

1.3.3 Online Delivery

1.3.3.1 Third-Party Aggregators

1.3.3.1.1 App-Based Delivery

1.3.3.1.2 Subscription Delivery Models

1.3.3.2 Brand-Owned Delivery

1.3.3.2.1 In-House Delivery Fleet

1.3.3.2.2 Hybrid Delivery Model

1.3.3.3 Cloud Kitchen Delivery

1.3.3.3.1 Single-Brand Japanese Kitchens

1.3.3.3.2 Multi-Brand Asian Kitchens

1.3.4 Retail Ready-to-Eat

1.3.4.1 Supermarket Sushi

1.3.4.1.1 Fresh Sushi Packs

1.3.4.1.2 Value Sushi Combos

1.3.4.2 Meal Kits

1.3.4.2.1 Ramen Kits

1.3.4.2.2 DIY Sushi Kits

1.4 By End-User

1.4.1 Individual Consumers

1.4.1.1 Millennials

1.4.1.1.1 Urban Professionals

1.4.1.1.2 Experience-Oriented Diners

1.4.1.2 Gen Z

1.4.1.2.1 Social Media-Driven Consumers

1.4.1.2.2 Trend-Focused Diners

1.4.1.3 Working Professionals

1.4.1.3.1 Lunch Crowd

1.4.1.3.2 After-Work Dining

1.4.1.4 Families

1.4.1.4.1 Weekend Dining

1.4.1.4.2 Celebration Dining

1.4.2 Corporate Customers

1.4.2.1 Corporate Catering

1.4.2.1.1 Executive Meetings

1.4.2.1.2 Corporate Events

1.4.2.2 Office Meal Programs

1.4.2.2.1 Subscription Lunch Plans

1.4.2.2.2 Bulk Bento Orders

1.4.2.3 Event Orders

1.4.2.3.1 Private Parties

1.4.2.3.2 Business Conferences

1.4.3 Institutional Clients

1.4.3.1 Universities

1.4.3.1.1 Campus Food Courts

1.4.3.1.2 Student Meal Contracts

1.4.3.2 Hospitals

1.4.3.2.1 Patient Meal Services

1.4.3.2.2 Staff Cafeterias

1.4.3.3 Office Complexes

1.4.3.3.1 IT Parks

1.4.3.3.2 Business District Cafeterias

Market Segmentation by Geography

1.1 Asia-Pacific

1.2 North America

1.3 Europe

1.4 Middle East & Africa

1.5 South America

Competitive Landscape

1.1 Market Share Analysis

1.2 Brand Positioning & Format Benchmarking

1.3 Menu Innovation & Differentiation Strategies

1.4 Supply Chain & Sourcing Partnerships

1.5 Competitive Intensity & Expansion Strategies

Company Profiles

Strategic Intelligence & Pheonix AI Insights

1.1 Pheonix Demand Forecast Engine

1.2 Consumer Behavior Analyzer

1.3 Innovation Tracker

1.4 Supply Chain Intelligence Analyzer

1.5 Automated Porter???s Five Forces Analysis

Future Outlook & Strategic Recommendations

1.1 Expansion into Emerging Global Markets

1.2 AI Integration & Digital Ecosystem Optimization

1.3 Premium Omakase & Experiential Dining Strategy

1.4 Sustainable Seafood & Supply Chain Optimization

1.5 Long-Term Market Outlook (2033+)

Appendix

About Pheonix Research

Disclaimer

Competitive Landscape

Competitive Landscape Content

Executive Framing

In the Global Japanese Restaurant Market, the competitive landscape is characterized by a highly fragmented yet globally scalable structure, where international chains, regional operators, and independent premium restaurants coexist across multiple formats and price tiers.

Key global players such as Sushiro, Kura Sushi, Genki Sushi, Yoshinoya, Ippudo, Benihana, Nobu Hospitality, and Zuma Restaurants compete across quick-service, casual dining, and premium experiential segments.

Competitive intensity is high, driven by global expansion strategies, franchise scalability, premium dining growth, and digital transformation. The market does not exhibit tight consolidation due to the strong presence of independent operators, particularly in premium omakase and localized sushi formats.

As a result, competition is defined by a dual structure: scalable global chains competing on efficiency and reach, and independent or boutique operators competing on authenticity, craftsmanship, and experience.

Current Market Reality

The current global market reflects a multi-layered competitive environment, where different business models operate simultaneously across regions and consumer segments.

Global chains such as Sushiro and Kura Sushi are expanding aggressively through:

- Franchise and company-owned international outlets

- Standardized menus and automated operations

- Technology-enabled dining formats (conveyor systems, tablet ordering)

Meanwhile, premium brands like Nobu Hospitality and Zuma Restaurants dominate high-end segments through:

- Luxury positioning and experiential dining

- Global presence in major metropolitan cities

- High-margin chef-led concepts

Key structural realities include:

- High Fragmentation Across Regions:

Independent sushi bars, ramen shops, and izakayas dominate local markets globally. - Delivery & Cloud Kitchen Expansion:

Japanese cuisine???s compatibility with delivery has accelerated digital-first competition. - Premiumization Trend:

Omakase and kaiseki formats are expanding rapidly in global cities. - Regional Competitive Variability:

Asia-Pacific is more structured with strong domestic chains, while Western markets remain more fragmented. - Technology Integration:

AI-based inventory management, automated sushi preparation, and digital reservations are becoming competitive necessities.

Key Signals And Evidence

Several key signals highlight evolving competitive dynamics:

- Global Franchise Expansion:

Chains like Yoshinoya and Ippudo are scaling internationally, reinforcing chain-led globalization. - Automation & Efficiency Models:

Kura Sushi is leveraging automation to enhance scalability and reduce labor dependency. - Premium Brand Proliferation:

Nobu Hospitality continues expanding globally, reflecting strong demand for luxury Japanese dining experiences. - Cloud Kitchen Growth:

Delivery-only Japanese brands are increasing supply density and lowering entry barriers. - Sustainability Focus:

Ethical seafood sourcing and traceability are becoming central to brand differentiation. - Consumer Behavior Shift:

Increasing preference for healthy, seafood-based, and premium dining experiences is reshaping competitive strategies.

These signals indicate a shift toward global scalability combined with localized differentiation, where success depends on balancing efficiency with authenticity.

Strategic Implications

The global competitive landscape requires multi-dimensional strategic alignment, where operators must navigate both scale-driven expansion and premium differentiation.

1. Dual Business Model Strategy

Companies must balance mass-market scalability (QSR, delivery) with high-margin premium formats (omakase, fine dining).

2. Technology as a Competitive Enabler

AI-driven forecasting, automation, and digital ordering are essential for cost optimization and customer engagement.

3. Localization for Market Penetration

Adapting menus to regional tastes while maintaining Japanese authenticity is critical for global expansion success.

4. Brand Positioning & Experience

Premium brands must invest in ambiance, storytelling, and chef-led experiences to sustain differentiation.

5. Supply Chain Management

Global seafood sourcing introduces complexity, requiring robust procurement and traceability systems.

6. Competition from Independent Operators

Local restaurants maintain strong influence, particularly in premium segments, increasing competitive intensity at the micro-market level.

Forward Outlook

Looking ahead, the Global Japanese Restaurant Market will evolve into a digitally integrated, sustainability-driven, and experience-focused ecosystem.

Key forward trends include:

- AI-Driven Operational Transformation:

Automation and predictive analytics will redefine efficiency and cost structures. - Expansion of Premium Dining Formats:

Omakase and fine dining will continue to grow in global metropolitan hubs. - Sustainability as Core Strategy:

Ethical sourcing and eco-friendly practices will become fundamental to brand positioning. - Omnichannel Business Models:

Integration of dine-in, takeaway, and delivery will optimize revenue streams. - Emerging Market Expansion:

Southeast Asia, Latin America, and the Middle East will present new growth opportunities. - Experience-Led Differentiation:

Restaurants will increasingly compete on culinary storytelling, presentation, and personalization.

In conclusion, the competitive landscape is defined by a globally fragmented yet strategically evolving structure, where success depends on the ability to integrate scalability, authenticity, digital innovation, and sustainability into a cohesive global strategy.

Operators that effectively balance efficiency-driven expansion with premium experiential value will emerge as leaders in the next phase of the Global Japanese Restaurant Market.

Value Chain

Executive Framing

In the Global Japanese Restaurant Market, the value chain is dual-structured, globally distributed, and increasingly technology-integrated, balancing premium experiential dining with scalable quick-service and delivery models. With market expansion from USD 19.61 billion in 2025 to ~USD 25.50 billion by 2033 (CAGR ~3.99%), value chain efficiency is critical for maintaining profitability in a fragmented and competitive global landscape.

The operational model is characterized by a hybrid ecosystem combining franchise-led scalability, independent premium dining, and cloud kitchen formats, while distribution operates through a fully hybrid omnichannel structure (dine-in, takeaway, delivery, and retail-ready formats). Supply chain complexity is moderate but globally sensitive, driven by cross-border seafood sourcing, perishability, and regulatory variability.

As global demand rises for sushi, ramen, and omakase experiences, the value chain must optimize quality consistency, sourcing reliability, and digital integration, making end-to-end coordination a key determinant of competitive advantage.

Current Market Reality

The global Japanese restaurant value chain operates across a multi-layered structure:

1. Global Franchise & Chain Layer

- Standardized procurement and centralized sourcing contracts

- Scalable formats across regions (Asia-Pacific, North America, Europe)

- Strong integration of digital ordering and AI-driven inventory systems

2. Premium & Experiential Dining Layer

- High reliance on imported, high-grade seafood and seasonal ingredients

- Chef-driven operations with emphasis on authenticity and cultural experience

- Limited scalability but higher per-unit margins

3. Delivery & Cloud Kitchen Layer

- Asset-light, delivery-first models expanding rapidly

- Integration with aggregator platforms and digital ecosystems

- Focus on cost efficiency and high-volume throughput

Key constraints:

- Global seafood sourcing dependency

Cross-border logistics, regulatory compliance, and perishability increase risk and cost volatility. - Fragmented market structure

Presence of numerous independent operators reduces standardization and increases competitive pressure. - Delivery platform margin pressure

Aggregator commissions impact profitability, particularly for small and mid-sized operators. - Regional infrastructure disparities

Developed markets have advanced cold chains, while emerging markets face supply inconsistencies.

Despite these challenges, the market benefits from:

- Strong global demand for Japanese cuisine

- Increasing AI adoption in operations and demand forecasting

- Expansion of franchise and cloud kitchen models

Key Signals And Evidence

Several global signals are reshaping the value chain:

1. Growth of Delivery-First and Cloud Kitchen Models

Delivery-compatible formats such as sushi and bento are driving asset-light expansion, reducing reliance on physical dining infrastructure.

2. Premiumization Through Omakase and Experiential Dining

High-end dining formats are increasing dependency on premium imported ingredients, elevating supplier influence and cost sensitivity.

3. Expansion of Global Franchise Networks

International chains are driving standardization, procurement efficiency, and scalability, particularly in Asia-Pacific and North America.

4. AI-Driven Demand Forecasting and Inventory Optimization

AI tools are improving waste reduction, supply-demand alignment, and operational efficiency, especially for perishable seafood.

5. Sustainability and Traceability Requirements

Global consumers and regulators are pushing for responsible seafood sourcing and transparent supply chains, reshaping procurement strategies.

6. Localization of Menus and Supply Chains

Operators are adapting menus and sourcing locally to reduce costs and improve regional market fit, adding complexity but enhancing resilience.

Strategic Implications

These signals translate into several strategic priorities:

- Global Supply Chain Diversification

Reducing reliance on single-source imports and building regional supplier networks improves resilience and cost stability. - Hybrid Model Optimization

Balancing premium dine-in experiences with scalable delivery and quick-service formats enables revenue diversification. - Digital Ecosystem Control

Investing in proprietary ordering platforms and loyalty systems reduces dependency on third-party aggregators. - AI as a Core Operational Backbone

AI-driven inventory, demand forecasting, and kitchen automation are essential for margin optimization and waste reduction. - Sustainability Integration Across the Value Chain

Responsible sourcing and eco-friendly packaging enhance brand positioning and regulatory compliance. - Localization Strategy for Market Expansion

Adapting menus and sourcing to local markets improves scalability while maintaining core brand identity.

Forward Outlook

Looking ahead, the global Japanese restaurant value chain is expected to evolve into a fully integrated, data-driven, and sustainability-aligned system.

Key future developments:

- End-to-end AI integration across sourcing, operations, and delivery

- Advanced global seafood traceability systems ensuring quality and compliance

- Expansion of cloud kitchens and decentralized production models

- Increased localization of supply chains to reduce cross-border dependency

- Enhanced personalization through data-driven customer engagement

As the market continues to globalize, value chain excellence will become the primary driver of competitive advantage, surpassing traditional brand differentiation.

Operators that successfully integrate:

- resilient global sourcing networks,

- technology-enabled operations, and

- multi-format distribution strategies

will achieve superior scalability, cost efficiency, and long-term value creation in the Global Japanese Restaurant Market.

Investment Activity

Executive Summary ??? Investment Activity

Investment Framing

The Global Japanese Restaurant Market is experiencing selective and strategically distributed investment activity, aligned with its moderate growth profile (CAGR ~3.99%) and evolving dual-structure model of premium dining and scalable delivery formats. With market size projected to grow from USD 19.61 billion in 2025 to ~USD 25.50 billion by 2033, capital allocation is increasingly focused on efficiency optimization, franchise expansion, and premium experience differentiation.

Investment flows are not uniformly aggressive but are instead precision-targeted, favoring high-return formats such as omakase dining, sushi chains, and delivery-first cloud kitchens.

Current Investment Landscape

The global investment environment reflects a fragmented yet opportunity-rich structure, where both large chains and independent premium operators attract capital through differentiated strategies.

Investment is concentrated across:

- Premium experiential formats (omakase, kaiseki, chef-led dining)

- Quick-service and franchise chains (sushi, ramen, donburi)

- Cloud kitchens and delivery-first ecosystems

- Technology integration platforms (AI, automation, inventory systems)

Global brands such as Sushiro, Kura Sushi, and Yoshinoya are driving cross-border expansion, while independent operators attract capital through high-margin niche positioning.

Key Investment Signals

The market presents several defining investment signals:

- Dual-Engine Investment Model:

Capital is split between premium high-margin dining and scalable mass-market formats, ensuring diversified return streams. - Delivery and Cloud Kitchen Acceleration:

Investment in asset-light, delivery-centric models is increasing due to scalability and lower capital requirements. - Premiumization as Margin Strategy:

Omakase and fine dining concepts are attracting capital for their high ticket size and brand prestige. - Technology-Driven Efficiency:

AI-based demand forecasting, inventory control, and automation are becoming core investment priorities. - Global Franchise Expansion:

International rollout of sushi and ramen chains reflects confidence in standardized and replicable models.

Structural Investment Drivers

- Global Demand for Healthy & Premium Cuisine

Japanese food???s positioning as healthy, premium, and authentic supports long-term investment stability. - Omnichannel Consumption Shift

Growth in dine-in, takeaway, and delivery enables diversified revenue streams. - Franchise Scalability Across Regions

Proven business models allow efficient global replication and expansion. - Sustainability and Supply Chain Focus

Investments in traceable seafood sourcing and eco-friendly practices are becoming critical.

Strategic Implications for Investors

- Balanced Portfolio Approach:

Combining premium dining investments with scalable QSR formats optimizes risk-return balance. - Asset-Light Expansion Models:

Cloud kitchens and delivery brands offer capital-efficient scaling opportunities. - Technology as a Competitive Necessity:

AI and automation are key for margin control and operational efficiency. - Regional Diversification Strategy:

Asia-Pacific leads growth, but North America and Europe provide premium margin opportunities.

Forward Investment Outlook

Investment activity will remain measured but opportunity-focused, characterized by:

- Short-term (1???3 years):

Expansion of delivery-first and premium dining formats - Mid-term (3???7 years):

Franchise globalization and regional diversification - Long-term:

Fully integrated, AI-driven, omnichannel restaurant ecosystems

Final Investment Perspective

The Global Japanese Restaurant Market represents a stable, moderate-growth investment landscape, where returns are driven by strategic positioning rather than aggressive expansion.

Capital will increasingly favor:

- Premium experiential dining

- Scalable franchise chains

- Delivery and cloud kitchen ecosystems

- Technology-enabled operations

- Sustainable sourcing strategies

Overall, the market offers consistent, risk-balanced investment opportunities, particularly for stakeholders leveraging dual-format strategies, global scalability, and operational innovation.

Technology & Innovation

Executive Framing

The Global Japanese Restaurant market is transitioning into a technology-integrated, dual-engine ecosystem, where premium experiential dining and scalable digital delivery models coexist and reinforce each other. As global consumers increasingly demand authentic, healthy, and high-quality cuisine, technology is becoming a critical enabler of consistency, scalability, and personalization across diverse formats.

This market dimension is particularly important now due to the convergence of AI-based demand forecasting, automation in food preparation, and omnichannel distribution systems, which are reshaping operational efficiency and customer engagement globally. The rise of cloud kitchens, delivery-first brands, and premium omakase formats further accelerates this transformation.

The innovation landscape reflects a moderate innovation intensity with moderate patent activity, driven by process optimization, AI integration, and supply chain traceability rather than deep proprietary breakthroughs. The market is steadily evolving toward a digitally enabled, globally scalable dining ecosystem.

Current Market Reality

The current market is defined by broad adoption of digital ordering systems, automation in kitchen workflows, and delivery platform integration across regions. Leading players such as Kura Sushi, Sushiro, Yoshinoya, Ippudo, and Nobu Hospitality are leveraging technology to enhance operational efficiency, global scalability, and premium dining experiences.

Core technology layers include:

- AI-based inventory and demand forecasting systems

- Automated sushi preparation and conveyor-based serving systems

- Digital ordering platforms (mobile apps, kiosks, tablets)

- Cloud kitchen and delivery-first infrastructure

For example, Kura Sushi integrates automated serving belts and AI plate tracking, while Nobu Hospitality focuses on digitally enhanced premium dining experiences and reservation systems.

The market is in a growth-stage maturity, where foundational digital infrastructure is established globally, but AI-driven personalization and advanced automation are still scaling across regions.

Demand is driven by:

- Rising global preference for Japanese cuisine and healthy eating

- Expansion of delivery and cloud kitchen formats

- Growth in premium experiential dining (omakase, kaiseki)

- Need for cost optimization and waste reduction (especially seafood)

Key Signals And Evidence

- AI-Led Demand Forecasting Adoption

Restaurants are increasingly using AI to predict demand, optimize procurement, and reduce food waste in perishable seafood categories. - Expansion of Global Delivery Platforms

Platforms like Uber Eats, DoorDash, and Deliveroo are enabling rapid international scaling of Japanese cuisine. - Automation in Food Preparation

Robotic sushi systems and semi-automated kitchen tools are improving consistency, speed, and hygiene standards. - Premium Experience Digitization

High-end dining formats are integrating digital reservations, customer profiling, and curated tasting journeys. - Sustainability Through Technology

Adoption of traceability systems, sustainable seafood sourcing technologies, and waste management tools. - Global Localization via Data Analytics

Menu innovation is increasingly driven by regional taste data and consumer behavior insights, enabling localized offerings at scale.

Strategic Implications

For Restaurant Operators:

Operators must balance global scalability with local authenticity, leveraging technology to:

- Optimize operations and reduce costs

- Deliver consistent quality across locations

- Enhance customer engagement and retention

The key challenge remains maintaining culinary authenticity while scaling digitally.

For Technology Providers:

Opportunities lie in:

- AI-based restaurant intelligence platforms

- Automation systems for food preparation

- Supply chain traceability and sustainability tools

Challenges include:

- Standardization across diverse global markets

- Integration with varying regulatory and operational environments

For Market Structure:

- Large global chains gain advantage through technology investment and franchise scalability

- Premium brands differentiate via experience and exclusivity

- Smaller operators compete through niche positioning and aggregator reliance

Risk Layer:

- Volatility in seafood supply chains

- High competition in mature markets (Japan, U.S., Europe)

- Technology cost barriers in emerging markets

Forward Outlook (2026???2033)

The Global Japanese Restaurant market is expected to evolve into a fully integrated, AI-enabled, and sustainability-driven global ecosystem.

Key future trajectories include:

- AI-Personalized Dining at Scale

Real-time customization of menus based on consumer preferences, dietary patterns, and behavioral data. - Advanced Automation in Kitchen Operations

Robotic assistance improving efficiency, consistency, and labor optimization. - Blockchain-Based Seafood Traceability

Ensuring transparency, authenticity, and sustainability across global supply chains. - Omnichannel Dining Ecosystems

Seamless integration of dine-in, takeaway, and delivery models across all formats. - Autonomous Delivery & Logistics

Expansion of robotics and AI in last-mile delivery systems. - Hybrid Global-Local Expansion Models

Combining standardized global operations with localized menu innovation.

The market will continue to be driven by:

- Rising global demand for premium and healthy cuisine

- Expansion of digital delivery infrastructure

- Growth in experiential dining segments

Final Strategic View

The Global Japanese Restaurant market is transitioning into a technology-optimized, experience-driven, and globally scalable ecosystem, where success depends on integrating AI, automation, and sustainability with authentic culinary experiences.

Companies that effectively leverage:

- AI-driven demand forecasting and personalization

- Automation in preparation and service

- Sustainable and traceable supply chains

- Omnichannel delivery ecosystems

will emerge as global leaders, while others risk fragmentation in an increasingly competitive and digitally advanced market landscape.

Market Risk

Executive Framing

The Global Japanese Restaurant Market is entering a phase of structurally balanced growth accompanied by moderate but globally distributed risk exposure. While the overall market risk level remains moderate, the sector is increasingly influenced by supply chain dependencies, premiumization pressures, and global demand variability across regions.

Japanese cuisine operates within a dual-market structure???premium experiential dining (omakase, kaiseki) and scalable quick-service formats (sushi, ramen, bento)???each with distinct risk profiles. The premium segment is highly sensitive to imported seafood availability, cost volatility, and consumer discretionary spending, while the mass-market segment faces intense competition, pricing pressure, and operational standardization challenges.

Additionally, the globalization of Japanese cuisine has increased exposure to cross-border trade dynamics, sustainability regulations, and sourcing constraints, particularly for high-quality seafood. These structural factors are shaping cost frameworks, pricing flexibility, and long-term scalability across international markets.

Current Market Reality

The current market reflects steady expansion supported by global adoption of Japanese cuisine and the integration of digital and delivery ecosystems. Leading operators such as Sushiro, Kura Sushi, Yoshinoya, Ippudo, and Nobu Hospitality are expanding through franchise models, premium dining formats, and multi-market penetration strategies.

Technology adoption is accelerating, with AI-driven inventory systems, automated food preparation, and digital ordering platforms improving operational efficiency and customer engagement. Delivery-first and cloud kitchen models are enabling rapid scalability, particularly in urban markets.

However, structural challenges persist. The reliance on imported seafood and specialty ingredients exposes operators to fluctuations in global supply chains, regulatory restrictions, and currency volatility. Additionally, rising labor costs in developed markets and inconsistent labor quality in emerging markets create operational disparities.

Market fragmentation remains high, with a large number of independent operators competing alongside global chains, intensifying competitive rivalry and limiting pricing power. This creates a complex operating environment where growth is steady but margins are tightly managed.

Key Signals And Evidence

A primary signal is the continued volatility in global seafood supply chains. Factors such as overfishing regulations, sustainability certifications, and logistics disruptions are impacting availability and pricing of key ingredients like tuna and salmon.

Another significant signal is the increasing role of tourism and urban dining culture in driving demand. Regions with high tourism dependency exhibit fluctuating demand patterns, particularly affecting premium dining formats.

The rapid expansion of cloud kitchens and delivery-first Japanese brands is lowering entry barriers and intensifying competition globally. This trend is contributing to price sensitivity and margin pressure, especially in mid-range and quick-service segments.

Consumer preferences are also evolving toward plant-based and alternative dining options, introducing substitution pressure for traditional seafood-heavy Japanese cuisine.

Additionally, regulatory emphasis on sustainability and traceability is increasing compliance requirements, particularly in Europe and North America, adding complexity to sourcing and operations.

Strategic Implications

These signals highlight the need for globally adaptive strategies.

First, supply chain diversification and traceability will be critical. Operators must invest in sustainable sourcing partnerships and alternative procurement strategies to reduce dependency on volatile seafood imports.

Second, balancing premiumization with affordability will be essential. Multi-format strategies???combining high-margin experiential dining with scalable quick-service formats???can help stabilize revenue streams.

Third, operators must strengthen direct-to-consumer ecosystems to reduce reliance on third-party delivery platforms and protect margins.

Fourth, menu innovation should incorporate plant-based and localized offerings to address evolving consumer preferences while maintaining brand authenticity.

Finally, global expansion strategies must be region-specific, accounting for local demand patterns, regulatory environments, and cost structures to ensure sustainable scalability.

Forward Outlook

Looking ahead to 2026???2033, the Global Japanese Restaurant Market is expected to maintain steady growth, supported by continued globalization of Japanese cuisine, digital transformation, and rising demand for premium dining experiences.

However, the market will become increasingly efficiency-driven, with profitability and supply chain resilience emerging as key success factors. Technological integration will deepen, enabling predictive demand planning, waste reduction, and personalized customer engagement.

Sustainability will play a defining role, particularly in seafood sourcing and packaging, driven by regulatory frameworks and consumer awareness. This will reshape procurement strategies and brand positioning globally.

Competitive intensity will remain high due to market fragmentation and low entry barriers in delivery-first formats. Operators that successfully integrate technology, optimize supply chains, and maintain strong brand differentiation will be best positioned for long-term success.

In conclusion, the Global Japanese Restaurant Market presents a stable yet structurally complex growth environment, where strategic agility, operational efficiency, and global adaptability will define competitive advantage in the evolving international foodservice landscape.

Regulatory Landscape

Executive Framing

The regulatory and policy environment in the Global Japanese Restaurant Market plays a critical role in ensuring food safety, maintaining seafood sourcing standards, regulating cross-border operations, and enabling digital commerce integration. As the market expands globally across diverse regulatory jurisdictions, compliance frameworks are becoming increasingly complex and influential in shaping operational strategies, cost structures, and competitive positioning.

With the market projected to grow from USD 19.61 billion in 2025 to approximately USD 25.50 billion by 2033, regulatory oversight is essential in managing food hygiene, international seafood trade, labor standards, and environmental sustainability. Given the global nature of Japanese cuisine???particularly its reliance on raw seafood and imported ingredients???regulatory compliance becomes a key determinant of quality assurance and consumer trust.

As operators scale through franchise expansion, cloud kitchens, and delivery-first models, navigating multi-country regulatory systems will be critical to sustaining growth and innovation during the 2026???2033 forecast period.

Current Market Reality

The current regulatory landscape in the Global Japanese Restaurant Market is highly fragmented, with significant variation across regions such as Asia-Pacific, North America, and Europe, yet unified by core compliance themes including food safety, import regulations, and sustainability.

Food safety regulations are universally stringent, particularly for sushi, sashimi, and other raw seafood-based offerings. Governments enforce strict hygiene, storage, and preparation standards, requiring restaurants to maintain robust compliance systems and undergo regular inspections.

Seafood import and trade regulations are a critical component, as Japanese restaurants often rely on globally sourced fish and specialty ingredients. Compliance with international trade standards, certification requirements, and traceability protocols directly impacts procurement strategies and supply chain resilience.

Franchise and business licensing frameworks differ significantly across countries, requiring operators to adapt to local legal, tax, and operational requirements when expanding internationally. This creates a multi-layered compliance environment for global brands.

The rapid expansion of digital ordering platforms and cloud kitchens introduces additional regulatory considerations related to data privacy, digital payments, taxation, and platform governance, particularly in highly digitized markets.

Environmental and sustainability regulations are also gaining importance globally, with increasing focus on responsible seafood sourcing, reduction of single-use plastics, and waste management practices across developed and emerging markets.

Key Signals and Evidence

Several regulatory signals define the structure and evolution of the Global Japanese Restaurant Market:

- Global Food Safety and Hygiene Standards:

Strict enforcement of sanitation, food handling, and storage protocols ensures safety and consistency across markets, particularly for raw seafood-based cuisine. - International Seafood Trade and Traceability Regulations:

Compliance with import/export standards, quality certifications, and traceability systems is essential for maintaining product authenticity and safety. - Multi-Country Licensing and Franchise Regulations:

Diverse legal frameworks across regions influence expansion strategies, operational models, and compliance requirements for global chains. - Digital Commerce and Data Protection Laws:

Growth in app-based ordering, AI-driven personalization, and delivery platforms introduces regulatory requirements related to consumer data security and digital transactions. - Labor and Employment Regulations:

Workforce-related policies, including wages, working conditions, and benefits, vary across regions and impact operational costs. - Sustainability and Environmental Policies:

Increasing regulatory emphasis on sustainable seafood sourcing, eco-friendly packaging, and carbon footprint reduction is shaping long-term industry practices.

These signals collectively create a complex regulatory ecosystem that balances safety, globalization, digital transformation, and sustainability.

Strategic Implications

The regulatory landscape creates both operational challenges and strategic opportunities:

- High Regulatory Complexity Across Markets:

Multi-jurisdictional compliance requirements increase operational complexity for global operators, particularly in supply chain and franchise expansion. - Supply Chain Risk and Cost Pressures:

Strict seafood import regulations and sustainability requirements elevate procurement costs and necessitate robust traceability systems. - Barrier to Entry for Smaller Players:

Compliance with global standards, certifications, and licensing frameworks requires significant investment, favoring established brands. - Technology as a Compliance Enabler:

AI-driven inventory management, digital traceability tools, and automated compliance systems improve efficiency and reduce regulatory risks. - Localized Strategy Necessity:

Operators must adapt menus, sourcing practices, and operational models to meet region-specific regulatory requirements. - Sustainability as a Competitive Advantage:

Early alignment with environmental regulations enhances brand credibility and supports long-term differentiation in premium segments.

Forward Outlook (2026???2033)

Looking ahead, the regulatory landscape in the Global Japanese Restaurant Market is expected to become more harmonized yet increasingly stringent, particularly in areas of food safety, sustainability, and digital governance.

Food safety regulations will likely incorporate advanced monitoring technologies, stricter traceability requirements, and enhanced global standardization for seafood handling and storage.

Digital regulations will expand alongside AI adoption, requiring greater transparency in data usage, algorithm accountability, and stronger cybersecurity frameworks for digital ordering ecosystems.

Environmental policies are expected to intensify globally, driving stricter compliance with sustainable seafood sourcing, reduction of plastic waste, and adoption of circular economy practices.

Cross-border regulatory coordination may improve to facilitate global trade and franchise expansion, but regional differences will continue to require localized compliance strategies.

Companies that proactively invest in compliance infrastructure, adopt technology-driven regulatory solutions, and integrate sustainability into their core operations will be best positioned to capitalize on the projected ~3.99% CAGR and sustain long-term global growth.

Final Insight

The regulatory landscape in the Global Japanese Restaurant Market is a multi-jurisdictional, compliance-intensive system that directly influences market scalability, supply chain resilience, and innovation pathways. Operators that successfully navigate global regulatory complexities while aligning with sustainability and digital transformation trends will define the future of this premium and globally expanding culinary ecosystem.