Global Point-of-Care Testing (POCT) Market size and share Analysis 2026-2033

Global Point-of-Care Testing (POCT) Market Size & Forecast

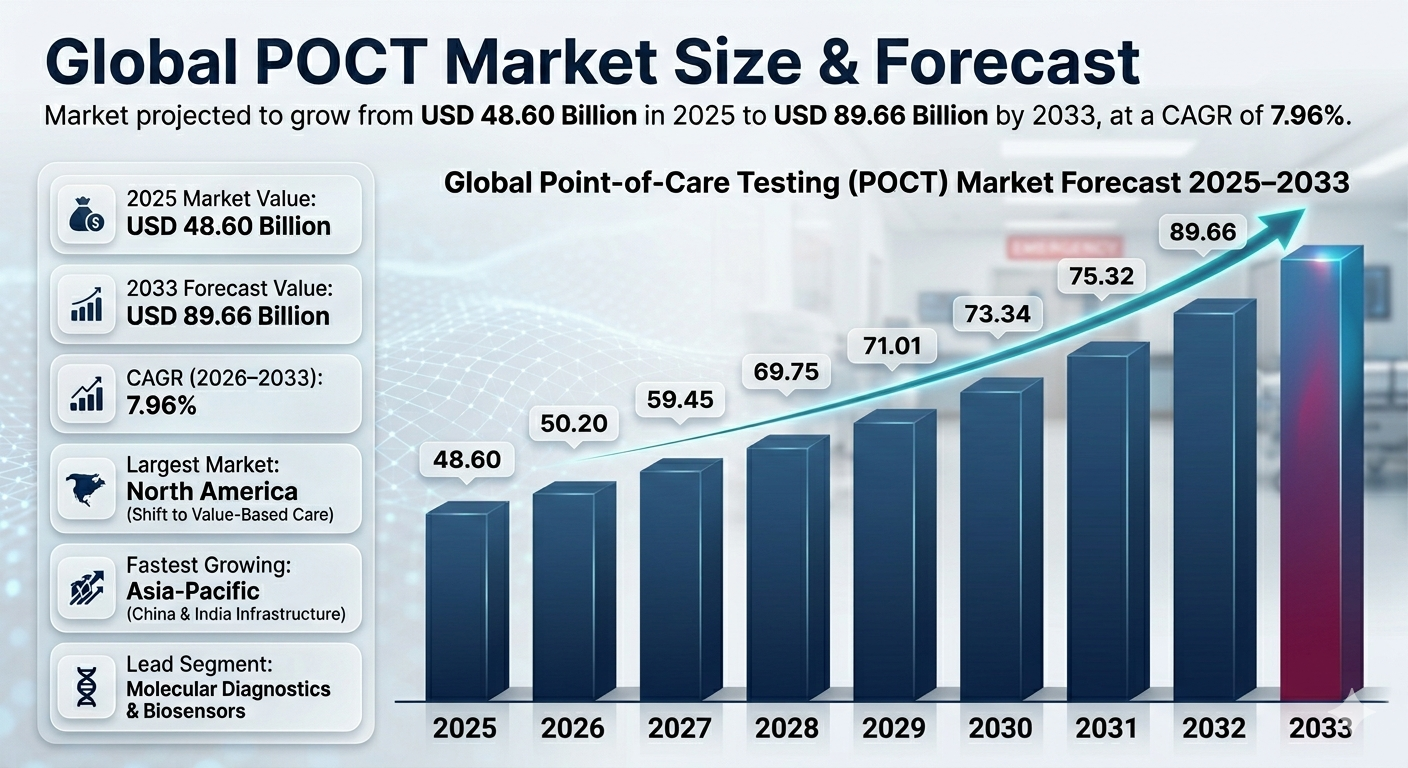

The Point-of-Care Testing (POCT) market is poised for substantial growth over the coming years. As of the base year 2025, the market size was estimated at USD 48.60 billion. This robust market is projected to expand at a compound annual growth rate (CAGR) of 7.96% from 2026 to 2033, ultimately reaching a forecasted market size of USD 89.66 billion by the end of the forecast period. This growth trajectory underscores the significant potential and interest in POCT solutions, driven by technological advancements and a growing demand for rapid, accessible diagnostic solutions.

The anticipated growth in the POCT market is reflective of the broader trends in healthcare, where there is a shift towards decentralized care models and immediate diagnostic results. The ability to conduct diagnostic tests at or near the site of patient care offers numerous advantages, including improved patient outcomes through timely decision-making and reduced burden on central laboratories. As healthcare systems around the world strive to improve efficiency and patient care, the demand for POCT solutions is expected to accelerate, driving both market size and market value.

Global Point-of-Care Testing (POCT) Market Overview

The Point-of-Care Testing market is characterized by its dynamic and rapidly evolving nature. With technological advancements at its core, the market is witnessing a transformation that is reshaping healthcare delivery. The integration of advanced technologies, such as biosensors and molecular diagnostics, has significantly enhanced the accuracy and speed of testing, making POCT an indispensable tool in modern healthcare settings.

The POCT market is moderately consolidated, with a competitive intensity level described as moderate. Key players such as Medtronic, Abbott Laboratories, and Amedisys are at the forefront, leveraging their technological prowess and market reach to drive innovation and expand their product portfolios. The competitive landscape is marked by a series of strategic mergers and acquisitions, as companies seek to bolster their positions and capitalize on the growing demand for POCT solutions.

Investment trends in the POCT market are on the rise, with medium capital intensity levels observed. Active investors, including Inception Health and Ballad Ventures, are channeling funds into healthcare technology and innovation sectors, underscoring the market's growth potential. Recent mergers and acquisitions highlight the strategic moves by companies to strengthen their capabilities and expand their geographic reach.

Regulatory dynamics play a crucial role in shaping the POCT market. The introduction of new regulations and standards by bodies such as the FDA impacts market operations, influencing product development and approval processes. The regulatory landscape is constantly evolving, with implications for market participants in terms of compliance and risk management.

The technological landscape of the POCT market is marked by high innovation intensity and patent activity, indicative of its emerging maturity stage. Key technologies such as biosensors, molecular testing, and next-generation sequencing (NGS) are driving advancements in the field, offering new opportunities for market growth.

Structural Drivers of Global Point-of-Care Testing (POCT) Market Growth

The growth of the Point-of-Care Testing market is driven by several structural factors, each contributing to the market's evolution and expansion.

Innovation and Commercialization Acceleration

One of the primary drivers is the acceleration of innovation and commercialization within the POCT market. Technological maturity, coupled with increased funding allocation, is compressing development-to-commercialization cycles. This rapid pace of innovation is expanding the range of applications for POCT solutions, thereby increasing adoption speed across various healthcare settings. For instance, the development of more sensitive and accurate POCT devices for non-communicable diseases presents a promising area of expansion. Technological advancements are not only enhancing the functionality of POCT devices but are also enabling their integration into broader healthcare ecosystems, thereby driving market growth.

Compliance and Risk Repricing

Regulatory tightening and risk repricing are reshaping the operational landscape of the POCT market. As regulations become more stringent, companies are compelled to shift their product roadmaps and elevate their execution standards. This regulatory environment is leading to a repricing of operating requirements, impacting cost structures and procurement strategies. For example, the FDA's plans to streamline regulatory approval processes for ultra-rare diseases have significant implications for POCT product development. Moreover, increased duties on imported laboratory supplies are affecting cost calculations, necessitating adjustments in laboratory operations and pricing strategies.

Competitive and Value-Chain Reconfiguration

The competitive dynamics and value-chain structures within the POCT market are undergoing reconfiguration. Competitive moves, such as mergers and acquisitions, are reallocating bargaining power and forcing portfolio repositioning. The relatively low profit margins in well-established industry markets are encouraging operators to consolidate their operations, cut costs, and enhance profitability. This industry consolidation is reshaping the competitive landscape, with implications for market concentration and competitive intensity.

Capital and Capacity Scaling

The scaling of capital and capacity is another pivotal driver of market growth. Investments in capacity and process upgrades are expanding throughput and reducing deployment friction, enabling faster scaling in high-demand segments. Key subsectors, including outpatient care and health IT, are attracting significant investment, highlighting the market's growth potential. As capital is deployed into these areas, companies are better positioned to meet the rising demand for POCT solutions, thereby driving market expansion.

Global Point-of-Care Testing (POCT) Market Segmentation Analysis

The Point-of-Care Testing market is segmented across several dimensions, each offering insights into the diverse applications and adoption of POCT solutions.

By End User

The POCT market serves a range of end-users, including home care settings, hospitals and clinics, diagnostic laboratories, and pharmacies and retail clinics. In home care settings, self-testing patients and remote patient monitoring are key segments, reflecting the trend towards personalized and decentralized healthcare. Hospitals and clinics, particularly emergency departments and intensive care units, rely on POCT for rapid diagnostics and timely intervention. Diagnostic laboratories and retail clinics also represent significant segments, with a focus on rapid testing and near-patient testing centers.

By Technology

The technological segmentation of the POCT market highlights the diversity of diagnostic approaches. Molecular diagnostics, such as PCR-based POCT systems, play a crucial role in delivering rapid and accurate results. Immunoassay-based testing, including lateral flow immunoassays, is widely used for its simplicity and cost-effectiveness. Biosensor-based diagnostics, with innovations such as electrochemical biosensors and lab-on-a-chip systems, are at the forefront of technological advancements, driving market growth.

By Application

The application segmentation of the POCT market encompasses a variety of diagnostic needs, including coagulation testing, cardiometabolic testing, infectious disease testing, and pregnancy and fertility testing. Each application area addresses specific healthcare challenges, leveraging POCT solutions to enhance diagnostic accuracy and patient care. For instance, cardiometabolic testing, including blood glucose and cholesterol testing, is critical for managing chronic conditions and improving patient outcomes.

By Product Type

The market is also segmented by product type, encompassing POCT instruments, monitoring devices, and test kits and consumables. Portable diagnostic analyzers and handheld POCT devices are widely used for their convenience and ease of use. Monitoring devices, particularly blood glucose monitoring systems, are essential for chronic disease management. Test kits and consumables, including cartridge-based test kits and disposable diagnostic cartridges, represent a significant portion of the market, driven by their widespread use in various healthcare settings.

By Distribution Channel

The distribution of POCT products is facilitated through various channels, including online sales, direct manufacturer sales, and medical device distributors. Online sales channels, such as e-commerce healthcare platforms, offer direct-to-consumer diagnostic devices, reflecting the growing trend towards consumer-driven healthcare. Direct manufacturer sales and medical device distributors play a crucial role in supplying POCT products to hospitals, laboratories, and other healthcare facilities.

The Point-of-Care Testing market is characterized by its diverse applications and end-users, driven by technological advancements and evolving healthcare needs. As the market continues to grow, understanding its segmentation is essential for capturing opportunities and navigating the competitive landscape.

Regional Market Dynamics

The global Point-of-Care Testing (POCT) market exhibits varied dynamics across different regions, driven by a combination of technological adoption, healthcare infrastructure, regulatory environments, and economic conditions. Developed regions such as North America and Europe are characterized by advanced healthcare systems and high levels of technological integration. These regions have been at the forefront of adopting POCT technologies, spurred by robust investments in healthcare technology and a strong focus on improving patient outcomes. The presence of key market players such as Abbott Laboratories and Medtronic, recognized for their innovative capabilities, further strengthens these markets. In North America, the emphasis on healthcare efficiency and the ongoing shift towards value-based care models are major drivers, coupled with favorable reimbursement policies that encourage the use of rapid diagnostic solutions.

In contrast, emerging markets in Asia-Pacific, Latin America, and parts of Africa present a different set of dynamics. These regions are witnessing increasing demand for POCT solutions due to growing healthcare needs and efforts to improve healthcare access. In Asia-Pacific, particularly in countries like China and India, the large population base and rising prevalence of chronic diseases are driving the market. The region's rapid urbanization and improving healthcare infrastructure are also pivotal in fostering market growth. However, regulatory challenges and variability in healthcare system maturity can act as constraints.

Latin America and Africa, while still developing their healthcare frameworks, show promise due to increasing government initiatives aimed at improving healthcare access and quality. These regions often face challenges such as limited healthcare budgets and infrastructure constraints, but the demand for cost-effective and easily deployable diagnostic solutions like POCT is high. International collaborations and investments are crucial in these markets to overcome barriers and facilitate technology transfer.

Competitive Landscape

The competitive landscape of the Point-of-Care Testing market is shaped by a moderately consolidated market structure, with a handful of key players dominating the space. Companies such as Medtronic, Stryker, and Abbott Laboratories hold significant market share due to their expansive product portfolios, strong distribution networks, and continuous investment in research and development. Medtronic, for instance, leverages its technological prowess in medical devices to maintain a competitive edge, while Abbott's strength lies in its extensive range of diagnostic solutions and global reach.

Strategic acquisitions and partnerships are common strategies employed by these players to enhance their capabilities and expand market presence. For example, Family Resource Home Care's acquisition of Specialty Service Solutions, LLC, exemplifies the trend of consolidation aimed at boosting profit margins and operational efficiency. Additionally, Amedisys's implementation of molecular testing nationwide highlights the push towards integrating advanced diagnostics into routine healthcare services, thereby enhancing service offerings and market reach.

Emerging players in the market are focusing on niche segments and innovative product developments to carve out their space in the competitive landscape. The market's competitive intensity is moderate, with barriers to entry primarily arising from the need for substantial investment in technology development and compliance with stringent regulatory standards. As the market continues to evolve, competition is expected to intensify, driving further innovation and market consolidation.

Strategic Outlook

The strategic outlook for the Point-of-Care Testing market is centered on leveraging technological innovations, expanding market reach, and navigating regulatory landscapes. Innovation remains a critical driver, with advancements in biosensors, molecular diagnostics, and integration of artificial intelligence poised to shape the future of POCT. Companies are increasingly investing in R&D to develop next-generation POCT devices that offer higher accuracy, faster results, and broader application capabilities.

Strategic partnerships and collaborations are expected to play a vital role in expanding market reach and enhancing capabilities. Companies are likely to pursue alliances with technology firms, healthcare providers, and research institutions to co-develop innovative solutions and access new markets. This collaborative approach is particularly important in emerging regions, where local partnerships can facilitate market entry and adaptation to regional healthcare needs.

Navigating regulatory landscapes will be crucial as regulatory environments continue to evolve, particularly in relation to new technologies such as AI and personalized medicine. Companies must remain agile and proactive in their compliance strategies to ensure smooth market operations and product approvals. Additionally, addressing challenges related to supply chain disruptions and cost pressures will be essential for sustaining growth and maintaining competitive advantage.

Final Market Perspective

In summary, the Point-of-Care Testing market is set for significant growth, driven by technological advancements, increasing demand for rapid and decentralized diagnostic solutions, and evolving healthcare models. The market's trajectory is shaped by structural drivers such as innovation acceleration, compliance pressures, and competitive reconfiguration. As companies navigate these dynamics, strategic investments in technology, partnerships, and regulatory compliance will be key to capitalizing on market opportunities. The ongoing shift towards personalized and value-based healthcare, coupled with the integration of advanced diagnostic technologies, positions the POCT market for a transformative future. As the market continues to mature, stakeholders must remain vigilant and adaptable to the changing landscape to sustain growth and enhance patient care outcomes.

Table of Contents

Table of Contents

- 1. Executive Summary

- 1.1 Market Forecast Snapshot (2026-2033)

- 1.2 Global Market Size & CAGR Analysis

- 1.3 Largest & Fastest-Growing Segments

- 1.4 Region-Level Leadership & Growth Trends

- 1.5 Key Market Drivers

- 1.6 Competitive Landscape Overview

- 1.7 Strategic Outlook Through 2033

- 2. Introduction & Market Overview

- 2.1 Definition of the Point-of-Care Testing Market

- 2.2 Scope of the Study

- 2.3 Industry Evolution & Market Development

- 2.4 Supply Chain & Distribution Infrastructure

- 2.5 Impact of Consumer Trends

- 2.6 Sustainability & Regulatory Landscape

- 2.7 Technology & Innovation Landscape

- 3. Research Methodology

- 3.1 Primary Research

- 3.2 Secondary Research

- 3.3 Market Size Estimation Model

- 3.4 Forecast Assumptions (2026-2033)

- 3.5 Data Validation & Triangulation

- 4. Market Dynamics

- 4.1 Drivers

- 4.1.1 Increasing Demand Drivers

- 4.1.2 Industry Innovation Drivers

- 4.1.3 Market Expansion Factors

- 4.1.4 Regulatory or Policy Support

- 4.1.5 Technology Adoption Drivers

- 4.2 Restraints

- 4.2.1 Cost Constraints

- 4.2.2 Infrastructure Limitations

- 4.2.3 Regulatory Challenges

- 4.2.4 Market Awareness Barriers

- 4.3 Opportunities

- 4.3.1 Emerging Market Opportunities

- 4.3.2 Product Innovation Opportunities

- 4.3.3 Technology Expansion Opportunities

- 4.3.4 Supply Chain Improvements

- 4.4 Challenges

- 4.4.1 Supply Chain Complexity

- 4.4.2 Quality Control & Compliance

- 4.4.3 Regional Market Fragmentation

- 4.4.4 Competitive Pressure

- 4.1 Drivers

- 5. Point-of-Care Testing Market Analysis (USD Billion), 2026-2033

- 5.1 Market Size Overview

- 5.2 CAGR Analysis

- 5.3 Regional Revenue Distribution

- 5.4 Segment Revenue Analysis

- 5.5 Distribution Channel Analysis

- 5.6 Consumer Impact Analysis

- 6. Market Segmentation (USD Billion), 2026-2033

- 6.1 By End User

- 6.1.1 Home Care Settings

- 6.1.1.1 Self-Testing Patients

- 6.1.1.1.1 Remote Patient Monitoring

- 6.1.1.1.1.1 Remote Patient Monitoring

- 6.1.1.1.1 Remote Patient Monitoring

- 6.1.1.1 Self-Testing Patients

- 6.1.2 Hospitals & Clinics

- 6.1.2.1 Emergency Departments

- 6.1.2.1.1 Intensive Care Units

- 6.1.2.1.1.1 Intensive Care Units

- 6.1.2.1.1 Intensive Care Units

- 6.1.2.1 Emergency Departments

- 6.1.3 Diagnostic Laboratories

- 6.1.3.1 Rapid Testing Laboratories

- 6.1.3.1.1 Near-Patient Testing Centers

- 6.1.3.1.1.1 Near-Patient Testing Centers

- 6.1.3.1.1 Near-Patient Testing Centers

- 6.1.3.1 Rapid Testing Laboratories

- 6.1.4 Pharmacies & Retail Clinics

- 6.1.4.1 Retail Diagnostic Testing

- 6.1.4.1.1 Pharmacy-Based Rapid Testing

- 6.1.4.1.1.1 Pharmacy-Based Rapid Testing

- 6.1.4.1.1 Pharmacy-Based Rapid Testing

- 6.1.4.1 Retail Diagnostic Testing

- 6.1.1 Home Care Settings

- 6.2 By Technology

- 6.2.1 Molecular Diagnostics

- 6.2.1.1 PCR-Based POCT Systems

- 6.2.1.1.1 Cartridge PCR Testing Platforms

- 6.2.1.1.1.1 Rapid Molecular Detection Systems

- 6.2.1.1.1 Cartridge PCR Testing Platforms

- 6.2.1.1 PCR-Based POCT Systems

- 6.2.2 Immunoassay-Based Testing

- 6.2.2.1 Lateral Flow Immunoassays

- 6.2.2.1.1 Rapid Antigen Detection Systems

- 6.2.2.1.1.1 Disposable Immunoassay Test Kits

- 6.2.2.1.1 Rapid Antigen Detection Systems

- 6.2.2.1 Lateral Flow Immunoassays

- 6.2.3 Biosensor-Based Diagnostics

- 6.2.3.1 Electrochemical Biosensors

- 6.2.3.1.1 Microfluidic Diagnostic Sensors

- 6.2.3.1.1.1 Lab-on-a-Chip Diagnostic Systems

- 6.2.3.1.1 Microfluidic Diagnostic Sensors

- 6.2.3.1 Electrochemical Biosensors

- 6.2.1 Molecular Diagnostics

- 6.3 By Application

- 6.3.1 Coagulation Testing

- 6.3.1.1 Prothrombin Time Testing

- 6.3.1.1.1 INR Monitoring Systems

- 6.3.1.1.1.1 Anticoagulation Therapy Monitoring

- 6.3.1.1.1 INR Monitoring Systems

- 6.3.1.1 Prothrombin Time Testing

- 6.3.2 Cardiometabolic Testing

- 6.3.2.1 Blood Glucose Testing

- 6.3.2.1.1 Cholesterol Testing

- 6.3.2.1.1.1 HbA1c Testing

- 6.3.2.1.1 Cholesterol Testing

- 6.3.2.1 Blood Glucose Testing

- 6.3.3 Infectious Disease Testing

- 6.3.3.1 Respiratory Infection Diagnostics

- 6.3.3.1.1 Viral Infection POCT

- 6.3.3.1.1.1 Rapid Pathogen Detection

- 6.3.3.1.1 Viral Infection POCT

- 6.3.3.1 Respiratory Infection Diagnostics

- 6.3.4 Pregnancy & Fertility Testing

- 6.3.4.1 Pregnancy Detection Tests

- 6.3.4.1.1 Ovulation Testing

- 6.3.4.1.1.1 Hormone Level Monitoring

- 6.3.4.1.1 Ovulation Testing

- 6.3.4.1 Pregnancy Detection Tests

- 6.3.1 Coagulation Testing

- 6.4 By Product Type

- 6.4.1 POCT Instruments

- 6.4.1.1 Portable Diagnostic Analyzers

- 6.4.1.1.1 Handheld POCT Devices

- 6.4.1.1.1.1 Integrated Point-of-Care Analyzers

- 6.4.1.1.1 Handheld POCT Devices

- 6.4.1.1 Portable Diagnostic Analyzers

- 6.4.2 POCT Monitoring Devices

- 6.4.2.1 Blood Glucose Monitoring Devices

- 6.4.2.1.1 Portable Glucose Testing Systems

- 6.4.2.1.1.1 Self-Monitoring Glucose Devices

- 6.4.2.1.1 Portable Glucose Testing Systems

- 6.4.2.1 Blood Glucose Monitoring Devices

- 6.4.3 POCT Test Kits & Consumables

- 6.4.3.1 Cartridge-Based Test Kits

- 6.4.3.1.1 Disposable Diagnostic Cartridges

- 6.4.3.1.1.1 Single-Use POCT Assay Kits

- 6.4.3.1.1 Disposable Diagnostic Cartridges

- 6.4.3.1 Cartridge-Based Test Kits

- 6.4.1 POCT Instruments

- 6.5 By Distribution Channel

- 6.5.1 Online Sales Channels

- 6.5.1.1 E-Commerce Healthcare Platforms

- 6.5.1.1.1 Direct-to-Consumer Diagnostic Devices

- 6.5.1.1.1.1 Direct-to-Consumer Diagnostic Devices

- 6.5.1.1.1 Direct-to-Consumer Diagnostic Devices

- 6.5.1.1 E-Commerce Healthcare Platforms

- 6.5.2 Direct Manufacturer Sales

- 6.5.2.1 Hospital Supply Contracts

- 6.5.2.1.1 Laboratory Equipment Supply

- 6.5.2.1.1.1 Laboratory Equipment Supply

- 6.5.2.1.1 Laboratory Equipment Supply

- 6.5.2.1 Hospital Supply Contracts

- 6.5.3 Medical Device Distributors

- 6.5.3.1 Diagnostic Equipment Suppliers

- 6.5.3.1.1 Institutional Procurement

- 6.5.3.1.1.1 Institutional Procurement

- 6.5.3.1.1 Institutional Procurement

- 6.5.3.1 Diagnostic Equipment Suppliers

- 6.5.1 Online Sales Channels

- 6.1 By End User

- 7. Market Segmentation by Geography

- 7.1 North America

- 7.2 Europe

- 7.3 Asia-Pacific

- 7.4 Latin America

- 7.5 Middle East & Africa

- 8. Competitive Landscape

- 8.1 Market Share Analysis

- 8.2 Product Portfolio Benchmarking

- 8.3 Product Positioning Mapping

- 8.4 Supply Chain & Distribution Partnerships

- 8.5 Competitive Intensity & Differentiation

- 9. Company Profiles

- 10. Strategic Intelligence & Pheonix AI Insights

- 10.1 Pheonix Demand Forecast Engine

- 10.2 Supply Chain & Infrastructure Analyzer

- 10.3 Technology & Innovation Tracker

- 10.4 Product Development Insights

- 10.5 Automated Porter’s Five Forces Analysis

- 11. Future Outlook & Strategic Recommendations

- 11.1 Emerging Market Expansion

- 11.2 Technology Innovation Strategies

- 11.3 Product Development Roadmap

- 11.4 Regional Expansion Strategies

- 11.5 Long-Term Market Outlook (2033+)

- 12. Appendix

- 13. About Pheonix Research

- 14. Disclaimer

Competitive Landscape

Competitive Landscape

Point-of-Care Testing Competitive Intensity & Market Structure Overview

The point-of-care testing (POCT) market is defined by its moderately consolidated structure, characterized by the presence of numerous key players such as Medtronic, Stryker, KARL STORZ SE, Hologic, and others. This market structure reflects a landscape where a limited number of companies hold significant market share, influencing competitive dynamics and strategic positioning. The moderately consolidated nature of the market suggests that while there is some level of market dominance, there is also room for competition and innovation among the top-tier companies.

The competitive intensity within this market structure is moderate, indicating that while competition exists, it is not overly aggressive. This level of competition is shaped by several factors, including the strategic maneuvers of key players, the development of innovative testing solutions, and the evolving needs of healthcare providers and patients. As a result, companies are compelled to engage in strategic actions such as mergers and acquisitions, partnerships, and technological advancements to maintain or enhance their market position.

In this context, the competitive intensity and market structure of the POCT market are influenced by the strategic choices of leading companies. For instance, the recent acquisition by Family Resource Home Care of Specialty Service Solutions, LLC demonstrates a strategic move to integrate and expand operations, reflecting a broader trend of consolidation within the industry. Furthermore, companies like Amedisys are pioneering the implementation of molecular testing nationwide, highlighting the importance of innovation and differentiation in competitive positioning.

Point-of-Care Testing Competitive Intensity & Market Structure Current Scenario

Currently, the POCT market is witnessing a phase of strategic realignment and consolidation, driven by the need to enhance profitability and streamline operations. The relatively low profit margins in established industry markets have encouraged operators to pursue mergers and acquisitions as a means to boost profits and reduce costs. This trend is evident in the actions of companies like Family Resource Home Care, which has expanded its footprint from eight locations in 2019 to 35 across Washington, Oregon, and Idaho through strategic acquisitions.

The consolidation trend is further reinforced by the actions of leading players in the market, such as Medtronic and Stryker, who dominate the hysteroscopes market in the US. These companies, along with others like KARL STORZ SE, Hologic, and Olympus, hold significant market share, shaping the competitive landscape through strategic investments and product innovations. The presence of these dominant players creates barriers to entry for new entrants, reinforcing the moderately consolidated market structure.

Additionally, the implementation of advanced testing solutions, such as molecular testing by Amedisys, underscores the importance of innovation in maintaining competitive advantage. As the first home health company to implement molecular testing nationwide, Amedisys sets a precedent for other companies in the market, emphasizing the role of technological advancements in shaping competitive dynamics.

The current scenario also highlights the strategic importance of differentiation and specialization. Companies are increasingly focusing on developing unique product offerings and enhancing service delivery to differentiate themselves from competitors. This focus on differentiation is driven by the need to meet the evolving demands of healthcare providers and patients, who seek more accurate, efficient, and accessible testing solutions.

Key Competitive Intensity & Market Structure Signals in Point-of-Care Testing

The competitive intensity and market structure of the POCT market are shaped by several key signals that provide insights into the strategic positioning and market dynamics. One of the most significant signals is the trend of mergers and acquisitions, driven by the relatively low profit margins in established industry markets. This trend highlights the strategic importance of consolidation as a means to enhance profitability and streamline operations. The acquisition of Specialty Service Solutions, LLC by Family Resource Home Care serves as a concrete example of this trend, demonstrating the strategic moves companies are making to expand their market presence and enhance operational efficiency.

Another critical signal is the implementation of innovative testing solutions, such as the nationwide rollout of molecular testing by Amedisys. This move underscores the strategic importance of technological advancements in maintaining competitive advantage and meeting the evolving needs of healthcare providers and patients. By pioneering molecular testing, Amedisys sets a benchmark for other companies in the market, emphasizing the role of innovation in shaping competitive dynamics.

The presence of dominant players like Medtronic, Stryker, and others in the hysteroscopes market further highlights the moderately consolidated nature of the market structure. These companies hold significant market share, creating barriers to entry for new entrants and shaping the competitive landscape through strategic investments and product innovations. The dominance of these players reinforces the importance of strategic positioning and differentiation in maintaining competitive advantage.

In conclusion, the competitive intensity and market structure of the POCT market are influenced by a combination of consolidation trends, technological advancements, and the strategic maneuvers of leading players. These factors shape the market dynamics and determine the strategic positioning of companies within the industry. As the market continues to evolve, companies must navigate these competitive forces to maintain their market position and drive growth.

Strategic Implications of Competitive Intensity & Market Structure in Point-of-Care Testing

The strategic implications of competitive intensity and market structure in the POCT market are profound, influencing how companies position themselves and make strategic decisions. The trend towards consolidation through mergers and acquisitions suggests that companies are seeking to strengthen their market positions by expanding their operational capabilities and geographical reach. This is evident in the case of Family Resource Home Care, which has scaled from eight locations in 2019 to 35, spanning across Washington, Oregon, and Idaho. Such expansion strategies not only increase market share but also enhance the company’s ability to offer comprehensive services across a broader geographic area.

Technological advancements, such as the implementation of molecular testing by Amedisys, highlight the importance of innovation in maintaining competitive advantage. Companies that invest in cutting-edge technologies are better positioned to meet the evolving needs of healthcare providers and patients, thereby enhancing their market appeal. This shift towards more sophisticated diagnostic solutions also presents opportunities for differentiation, allowing companies to distinguish themselves from competitors through unique value propositions.

The dominance of key players in specific market segments presents both challenges and opportunities for smaller companies and new entrants. While the concentration of market power can create barriers to entry, it also encourages smaller players to explore niche markets and develop specialized solutions that cater to unmet needs. This dynamic fosters an environment of innovation and differentiation, where companies must continuously adapt and innovate to remain competitive.

Point-of-Care Testing Competitive Intensity & Market Structure Forward Outlook

Looking ahead, the competitive intensity and market structure of the POCT market are likely to be shaped by several key trends and developments. The continued emphasis on mergers and acquisitions as a strategy for growth and consolidation is expected to persist, driven by the need to enhance profitability and achieve operational efficiencies. As companies seek to expand their market presence and strengthen their competitive positions, we can anticipate further consolidation within the industry, leading to a more concentrated market structure.

Technological advancements will continue to play a pivotal role in shaping the competitive landscape. The adoption of innovative diagnostic solutions, such as liquid biopsies and molecular testing, will redefine the way healthcare providers deliver care and manage patient outcomes. Companies that invest in research and development to advance these technologies will be well-positioned to capture market share and establish themselves as leaders in the industry.

The regulatory environment will also influence the competitive dynamics of the POCT market. As regulatory bodies introduce new guidelines and standards for diagnostic testing, companies must navigate these changes to ensure compliance and maintain their market positions. Those that are agile and responsive to regulatory shifts will have a competitive advantage, enabling them to adapt their strategies and offerings in line with evolving requirements.

In conclusion, the competitive intensity and market structure of the Point-of-Care Testing market are driven by consolidation trends, technological advancements, and strategic maneuvers by leading players. As the market continues to evolve, companies must navigate these forces to maintain their market positions and drive growth. By leveraging mergers and acquisitions, adopting innovative technologies, and staying attuned to regulatory developments, companies can enhance their competitive advantage and capitalize on emerging opportunities in the POCT market.

Value Chain

Value Chain

Point-of-Care Testing Value Chain & Supply Chain Evolution Overview

The value chain and supply chain of the point-of-care testing (POCT) market are experiencing significant transformations driven by technological advancements, strategic investments, and evolving operational models. These changes are reshaping the market structure, particularly in how POCT products are developed, distributed, and utilized across various healthcare settings. The primary operational and distribution model for this market is hybrid, which combines traditional and innovative approaches to enhance efficiency and reach. This hybrid model is pivotal in addressing current bottlenecks and optimizing the supply chain’s complexity level, which is moderate.

Within this framework, key stages such as the development of biosensors, point-of-care testing, and remote patient monitoring are critical. These stages are intertwined, creating a dynamic value chain that requires careful management to mitigate bottlenecks like supply chain challenges and patient overcrowding in emergency departments. The evolution of this value chain is influenced by the increasing application of biosensors in various fields, including environmental monitoring and the pharmaceutical industry, which underscores their versatility and significance in the POCT market.

The hybrid operational model emphasizes flexibility and adaptability, allowing stakeholders to respond to supply chain disruptions effectively. This model supports a distribution structure that integrates both centralized and decentralized elements, ensuring that POCT products can be delivered efficiently to various healthcare environments. As the market continues to evolve, the value chain’s ability to adapt to these changes will be crucial in maintaining competitive advantage and ensuring the delivery of high-quality healthcare services.

Point-of-Care Testing Value Chain & Supply Chain Evolution Current Scenario

Currently, the POCT market is navigating a complex landscape characterized by moderate supply chain complexity and significant strategic shifts. The hybrid distribution structure is enabling companies to leverage both traditional supply chain networks and innovative distribution channels to reach a broader range of healthcare providers and patients. This approach is essential in addressing the challenges posed by supply chain disruptions, which have been exacerbated by global events and increased demand for healthcare services.

The development of biosensors is a critical component of the POCT value chain, as these devices are integral to the functionality and effectiveness of POCT systems. Biosensors are increasingly being used in diverse applications beyond healthcare, such as environmental monitoring and biotechnological processes, highlighting their broad utility and potential impact on the market. This diversification in application is driving innovation and investment in the development of more advanced biosensors, which in turn enhances the capabilities of POCT systems.

One significant bottleneck in the current scenario is the challenge of patient overcrowding in emergency departments. This issue underscores the need for efficient POCT systems that can provide rapid and accurate diagnostic results, thereby reducing the burden on healthcare facilities and improving patient outcomes. The integration of remote patient monitoring technologies further complements this by allowing for continuous patient assessment, reducing the need for frequent hospital visits, and lowering hospitalization costs.

In terms of power distribution and margin effects, the hybrid operational model is redistributing bargaining power across the value chain. Companies that can effectively integrate technological advancements and strategic investments are gaining a competitive edge, allowing them to command higher margins and influence market dynamics. The integration of AI technologies, as predicted by analysts at International Data Corp. (IDC), could further enhance this power shift by optimizing operational efficiencies and driving economic impact.

Key Value Chain & Supply Chain Evolution Signals in Point-of-Care Testing

The POCT market is witnessing several key signals that indicate significant shifts in the value chain and supply chain evolution. These signals are shaping strategic directions and impacting how companies operate within this market.

One major signal is the significant investment in key subsectors such as outpatient care, dental care, health IT, pharma services, and medtech. These investments are driving innovation and creating new opportunities for growth within the POCT market. For instance, the launch of the first commercial radioimmunoassay kit in 1968 was a pivotal moment that stimulated research into diabetes and the development of a lucrative immunoassay industry. This historical precedent highlights the potential for similar innovations in the current market landscape, as companies continue to explore new diagnostic technologies.

Another critical signal is the acquisition activities within the industry, such as Family Resource Home Care’s acquisition of Specialty Service Solutions, LLC. This move not only integrates operations in the Washington state area but also reflects a broader trend of consolidation within the market. Such acquisitions are strategic actions aimed at enhancing operational capabilities, expanding market reach, and achieving economies of scale.

The adoption of remote patient monitoring technologies is another key signal impacting the POCT value chain. Patients who were remotely monitored incurred slightly lower hospitalization costs compared to those who received standard care, indicating the potential for cost savings and improved patient outcomes. This trend is driving the integration of digital technologies into healthcare delivery, facilitating more efficient and effective patient management.

These signals collectively indicate a market that is poised for transformation, driven by strategic investments, technological advancements, and evolving operational models. The implications for the POCT value chain are profound, with potential shifts in market structure, demand dynamics, and competitive behavior. As companies navigate these changes, the ability to adapt and innovate will be critical in maintaining a competitive edge and delivering value to stakeholders.

Strategic Implications of Value Chain & Supply Chain Evolution in Point-of-Care Testing

The strategic implications of these signals on the POCT value chain are multifaceted, affecting market structure, pricing, margins, and competitive behavior.

First, the integration of AI and advanced diagnostic technologies is likely to reshape the competitive landscape by enhancing the capabilities of early adopters. Companies that effectively leverage AI in their operations can expect improved diagnostic accuracy, faster turnaround times, and reduced operational costs. This technological edge will likely confer a significant competitive advantage, enabling these firms to capture a larger market share and command premium pricing for their enhanced services.

Second, the trend towards consolidation, as seen in the acquisition activities like that of Family Resource Home Care, is set to continue as companies seek to enhance their operational capabilities and market reach. Such consolidations can lead to increased bargaining power with suppliers and distributors, enabling firms to negotiate better terms and improve their margin profiles. However, this trend also poses risks for smaller players who may struggle to compete with larger, more integrated entities.

The development and deployment of advanced POCT devices, such as the Stat Profile Critical Care Xpress analyzer, are addressing critical supply chain bottlenecks by improving diagnostic accuracy and efficiency. This technological progress is essential for managing patient flow in healthcare settings, particularly in emergency departments. By alleviating these bottlenecks, healthcare providers can enhance their capacity utilization and delivery performance, ultimately leading to improved patient outcomes and higher satisfaction levels.

Remote patient monitoring represents a strategic shift towards more decentralized healthcare delivery models. This evolution is likely to drive demand for digital health solutions and biosensors, creating new opportunities for companies operating in these segments. As RPM becomes more prevalent, companies will need to invest in robust digital infrastructure and data management capabilities to support this transition effectively.

Point-of-Care Testing Value Chain & Supply Chain Evolution Forward Outlook

Looking ahead, the POCT value chain and supply chain are poised for continued evolution, driven by technological advancements, strategic investments, and shifting healthcare paradigms. The market is expected to witness increased adoption of AI and digital technologies, further enhancing diagnostic capabilities and operational efficiencies.

As AI becomes more integrated into healthcare delivery, companies will need to navigate regulatory challenges and data privacy concerns to fully realize its potential benefits. The successful deployment of AI-driven solutions will depend on robust data governance frameworks and collaboration with regulatory bodies to ensure compliance and trust.

Consolidation within the industry is likely to accelerate, with companies seeking to bolster their market positions through strategic mergers and acquisitions. This trend will create a more competitive landscape, with larger entities wielding greater influence over supply chain dynamics. Smaller players will need to differentiate themselves through niche offerings or strategic partnerships to remain viable.

The continued development of advanced POCT devices and remote patient monitoring solutions will drive demand for innovative diagnostic platforms and biosensors. Companies that invest in R&D and collaborate with technology providers will be well-positioned to capitalize on these growth opportunities.

In conclusion, the POCT market is undergoing significant transformations, driven by technological, strategic, and operational shifts. Companies that can adapt to these changes, leverage technological advancements, and strategically position themselves within the evolving value chain will be best placed to succeed in this dynamic market environment.

Investment Activity

Investment Activity

Point-of-Care Testing Investment & Funding Dynamics Overview

The landscape of investment and funding in the Point-of-Care Testing (POCT) market is undergoing a notable evolution. This evolution is driven by a combination of rising demand for rapid diagnostics, technological advancements, and strategic capital allocation by investors. The POCT market, characterized by its capacity to deliver immediate diagnostic results at or near the site of patient care, is attracting increasing attention from investors eager to capitalize on its potential to revolutionize healthcare delivery.

The investment trend direction in the POCT market is unequivocally rising, reflecting the growing recognition of its strategic importance. This upward trajectory is supported by a medium level of capital intensity, indicating that while significant investments are being made, there is still room for growth without overwhelming financial barriers. Recent mergers and acquisitions activity further underscores the dynamic nature of the market, as companies seek to consolidate and enhance their capabilities to meet the burgeoning demand for point-of-care solutions.

Active investors, including Inception Health, Ballad Ventures, Baycrest’s Center for Aging + Brain Health Innovation, AARP, Blue Lion Global, and FHS Capital, are at the forefront of this investment surge. Their focus is on key investment themes such as healthcare, technology, artificial intelligence (AI), remote patient monitoring, and immunoassays. These themes are shaping the contours of the market, driving innovation and fostering the development of cutting-edge diagnostic tools that are poised to transform patient care.

The investment and funding dynamics in the POCT market are further influenced by signals such as the $2.5 million seed financing raised by Homecare Hub, a testament to the growing interest in home-based healthcare solutions. Additionally, the Private Equity Stakeholder Project’s identification of 1,049 private equity-backed healthcare deals in the U.S. in 2024 highlights the sustained interest and financial commitment to the healthcare sector at large. The emergence of biosensors as crucial research areas for diseases like diabetes, cardiac diseases, and cancer also points to the expanding scope and impact of POCT technologies.

Point-of-Care Testing Investment & Funding Dynamics Current Scenario

The current scenario of investment and funding dynamics within the POCT market is characterized by a strategic focus on key subsectors that are attracting significant capital influxes. These subsectors include outpatient care, dental care, health IT, pharmaceutical services, and medtech. The focus on these areas is driven by the potential for substantial returns on investment, as they align with broader healthcare trends emphasizing efficiency, patient-centered care, and technological integration.

A notable historical driver of the POCT market has been the development of the immunoassay industry, which was catalyzed by the launch of the first commercial radioimmunoassay kit in 1968. This breakthrough stimulated extensive research into diabetes management and laid the groundwork for the lucrative immunoassay market we see today. The immunoassay market was valued at approximately $35 billion in 2023, with projections to reach $46.7 billion by 2028, reflecting its continued relevance and growth potential.

However, the market is not without its challenges. Increased duties on imported plastics, reagents, personal protective equipment, and other laboratory supplies have begun to push up procurement costs. These rising costs impact cost per test calculations, particularly in laboratories operating with tight margins and fixed reimbursement structures. This cost pressure is prompting companies to explore mergers and acquisitions as a strategy to boost profits and cut costs, allowing them to remain competitive in a demanding market environment.

In alignment with these trends, Family Resource Home Care’s acquisition of Specialty Service Solutions, LLC, exemplifies the strategic moves companies are making to expand their operational capabilities and market reach. Such acquisitions are not only about consolidating resources but also about enhancing service delivery to meet the evolving needs of the healthcare landscape.

Investing in the care economy is increasingly recognized as critical to strengthening the broader economy, particularly through private and public partnerships. This recognition underscores the importance of strategic capital allocation in driving both market and societal benefits, as investors seek to leverage their financial resources to support initiatives that improve healthcare outcomes and accessibility.

Key Investment & Funding Dynamics Signals in Point-of-Care Testing

The POCT market is witnessing several key signals that are shaping its investment and funding dynamics. These signals provide insight into the strategic directions being pursued by investors and the implications for the market’s future trajectory.

Firstly, the focus on key subsectors such as outpatient care, dental care, health IT, pharmaceutical services, and medtech highlights the areas where investors see the greatest potential for growth and return on investment. This focus is driven by the increasing demand for solutions that enhance healthcare delivery, improve patient outcomes, and integrate cutting-edge technology into medical practices.

The historical significance of the immunoassay industry, catalyzed by the introduction of the first commercial radioimmunoassay kit, continues to influence investment decisions. Immunoassays have become a cornerstone of diagnostic testing, offering reliable and efficient solutions for disease detection and management. As the immunoassay market continues to grow, it presents lucrative opportunities for investors seeking to capitalize on its established market presence and expanding applications.

Recent increases in duties on imported laboratory supplies are exerting cost pressures on laboratories, affecting their operational margins and pricing strategies. This environment is prompting companies to explore consolidation and cost-cutting measures through mergers and acquisitions. These strategic moves are aimed at enhancing operational efficiency, reducing overheads, and securing a competitive advantage in a challenging market landscape.

The acquisition of Specialty Service Solutions, LLC by Family Resource Home Care is a concrete example of how companies are leveraging acquisitions to strengthen their market position. By integrating operations in the Washington state area, Family Resource Home Care is expanding its service offerings and geographical reach, positioning itself for sustained growth in the homecare sector.

Investments in the care economy, underscored by private and public partnerships, are increasingly recognized as vital to economic resilience. These investments not only support the development of innovative healthcare solutions but also contribute to broader economic stability by creating jobs, enhancing healthcare accessibility, and improving population health outcomes.

In conclusion, the investment and funding dynamics in the POCT market are being shaped by a combination of historical drivers, strategic capital allocation, and emerging market signals. These dynamics are fostering an environment conducive to innovation, expansion, and enhanced healthcare delivery, setting the stage for a transformative impact on the healthcare landscape.

Strategic Implications of Investment & Funding Dynamics in Point-of-Care Testing

Economic and Strategic Integration

The economic rationale behind investments in POCT is both clear and compelling. The ability to perform diagnostics at the point of care reduces the reliance on centralized laboratories, which in turn cuts down on overhead costs and accelerates the delivery of care. This paradigm shift is particularly appealing to healthcare systems operating under tight financial constraints. The substantial cost savings and improved patient outcomes associated with POCT are driving healthcare providers to integrate these technologies into their care models more extensively.

The integration of POCT into healthcare systems also aligns with broader economic strategies aimed at enhancing efficiency and reducing costs. For instance, the increasing duties on imported plastics and laboratory supplies underscore the need for cost-effective solutions like POCT, which mitigate the financial impact of such tariffs. This economic logic is encouraging healthcare providers to adopt POCT technologies as a means of hedging against rising operational costs.

Investor-driven Innovation and Market Expansion

Investors, recognizing the strategic importance of POCT, are channeling funds into companies and technologies that promise to deliver innovative solutions. The involvement of active investors such as Inception Health, Ballad Ventures, and Blue Lion Global highlights the sector’s attractiveness. Their investments are not just financial endorsements but also signals of confidence in the sector’s potential to drive significant healthcare improvements.

This investor interest is spurring innovation across several key subsectors, including health IT and medtech. By backing technologies that facilitate remote patient monitoring and advanced immunoassays, investors are enabling healthcare providers to offer more personalized and efficient care. The focus on AI and technology within these investments indicates a strategic shift towards leveraging data analytics to enhance diagnostic accuracy and patient outcomes.

Mergers and Acquisitions as Catalysts for Growth

The competitive landscape of POCT is being reshaped by a wave of mergers and acquisitions, driven by the strategic need to consolidate resources and expand market reach. Companies are increasingly pursuing M&A activities to gain a competitive edge, as evidenced by Family Resource Home Care’s acquisition of Specialty Service Solutions, LLC. Such strategic acquisitions allow companies to streamline operations, reduce costs, and enter new markets more effectively.

M&A activities are also a response to the relatively low profit margins associated with established industry markets. By consolidating operations and resources, companies can achieve economies of scale, enhance operational efficiencies, and ultimately improve profitability. This trend is likely to continue as companies seek to strengthen their market positions and capitalize on the growing demand for POCT solutions.

Strategic Partnerships and Public-Private Collaborations

The strategic implications of investment and funding dynamics in the POCT market extend beyond private sector activities. Public-private partnerships are playing an increasingly critical role in driving innovation and ensuring the sustainability of healthcare systems. Investments in the care economy, supported by both private and public entities, are facilitating the development of innovative healthcare solutions and improving access to care.

These collaborations are also vital for addressing broader economic challenges, such as job creation and healthcare accessibility. By fostering innovation and supporting the deployment of POCT technologies, public-private partnerships are contributing to economic resilience and improved population health outcomes. This collaborative approach is essential for ensuring that the benefits of POCT are widely accessible and that healthcare systems can adapt to evolving patient needs and market conditions.

Point-of-Care Testing Investment & Funding Dynamics Forward Outlook

Technological Advancements and Market Expansion

Technological innovations will continue to be a driving force in the POCT market, with advancements in AI, remote patient monitoring, and biosensors leading the way. These technologies are expected to enhance diagnostic accuracy, improve patient outcomes, and expand the range of conditions that can be effectively managed at the point of care. As these technologies mature, they will open up new opportunities for market expansion and drive further investment in the sector.

The global economic impact of AI, projected to reach $19.9 trillion through 2030, underscores the transformative potential of technology in healthcare. Investors and healthcare providers alike are likely to prioritize technologies that leverage AI to improve diagnostics and patient care. This focus will drive continued investment in POCT and support the development of innovative solutions that address unmet healthcare needs.

Regulatory Environment and Market Adaptation

The regulatory environment will play a crucial role in shaping the future of the POCT market. As regulatory bodies introduce new guidelines and standards, companies will need to adapt their strategies to ensure compliance and capitalize on emerging opportunities. The FDA’s plans to streamline regulatory approval for ultra-rare diseases, for example, could facilitate the development and deployment of novel POCT solutions, particularly in niche markets.

Companies will need to navigate this evolving regulatory landscape carefully, balancing the need for compliance with the pursuit of innovation. Those that can effectively adapt to regulatory changes will be well-positioned to capitalize on the growing demand for POCT and achieve sustained market success.

Strategic Partnerships and Collaborative Innovation

Strategic partnerships will continue to be a key driver of innovation and market growth in the POCT sector. Public-private collaborations, in particular, will be essential for ensuring the sustainability and scalability of POCT solutions. By working together, public and private entities can pool resources, share expertise, and drive the development of innovative healthcare solutions that meet the needs of diverse patient populations.

These partnerships will also play a critical role in addressing economic challenges, such as rising healthcare costs and workforce shortages. By fostering collaboration and innovation, public-private partnerships can help healthcare systems adapt to changing market conditions and deliver high-quality care to patients.

Conclusion

In conclusion, the investment and funding dynamics in the Point-of-Care Testing market are characterized by a complex interplay of economic, technological, and strategic factors. As the market continues to evolve, stakeholders will need to navigate these dynamics carefully to capitalize on emerging opportunities and drive meaningful improvements in healthcare delivery. By focusing on strategic capital allocation, technological innovation, and collaborative partnerships, the POCT market is well-positioned to deliver transformative benefits to patients and healthcare systems alike.

Technology & Innovation

Technology & Innovation

Point-of-Care Testing Technology & Innovation Landscape Overview

The landscape of point-of-care testing (POCT) technology is undergoing a significant transformation driven by rapid advancements in biosensors, molecular diagnostics, and artificial intelligence. The market is characterized by high innovation intensity and patent activity, indicating a vibrant and competitive field with substantial opportunities for growth and development. At the forefront of this evolution are companies like Abbott Laboratories, Amedisys, Homecare Hub, and VedaBio, which are pioneering innovations that promise to redefine healthcare delivery and patient outcomes.

Central to the technological advancements in POCT is the development of biosensors. These devices convert biological responses to chemical molecules into signals with various properties, such as optical or electrical, enabling quick and accurate diagnostics. This capability is particularly crucial for managing chronic and acute conditions, such as diabetes and cardiac diseases, where timely intervention can significantly improve patient outcomes. The increasing sophistication of biosensors is transforming them into autonomous diagnostic platforms capable of detecting biomarkers for disease development, recurrence, and drug monitoring.

The integration of next-generation sequencing (NGS) and molecular testing into POCT is another pivotal development. These technologies allow for the rapid identification and analysis of genetic material, which can be crucial for diagnosing infectious diseases and genetic disorders. Amedisys, for example, has implemented molecular testing nationwide across its care centers, setting a precedent for home health companies and highlighting the growing importance of molecular diagnostics in decentralized healthcare settings.

Furthermore, the application of generative AI in POCT is emerging as a revolutionary force. This technology, introduced to the public through platforms like ChatGPT, offers unprecedented potential for data analysis, predictive modeling, and personalized medicine. By leveraging AI, healthcare providers can enhance diagnostic accuracy, optimize treatment plans, and improve patient engagement through tailored healthcare solutions.

Point-of-Care Testing Technology & Innovation Landscape Current Scenario

The current scenario in the POCT technology and innovation landscape is marked by a dynamic interplay between technological advancements and market demands. As the healthcare industry increasingly shifts towards patient-centered care, the demand for rapid, accurate, and cost-effective diagnostic solutions is rising. POCT meets these needs by providing immediate results at the point of care, enabling healthcare providers to make timely diagnoses and initiate treatment without delay.

Technological advancements are a significant driving force behind the increasing adoption of POCT in clinical settings. The development of more sensitive and accurate POCT devices for non-communicable diseases is a promising area of expansion. These devices are becoming essential tools in the management of chronic conditions, offering continuous monitoring capabilities that can revolutionize medical diagnosis and patient management. The emphasis on enhancing POCTs for diseases requiring ongoing monitoring underscores the potential for these technologies to transform healthcare delivery.

The competitive landscape is also being shaped by the introduction of platforms with comprehensive compliance capabilities. These platforms offer features like 21 CFR Part 11 electronic signatures, audit trails, ISO/IEC 17025 support, and robust cybersecurity, ensuring that POCT solutions meet stringent regulatory and safety standards. This focus on compliance is crucial for building trust among healthcare providers and patients, facilitating broader adoption of POCT technologies.

In addition, companies like VedaBio are forging strategic partnerships and securing investments to advance their technological offerings. VedaBio’s recent agreement with Siemens Healthineers, valued at up to $25 million, aims to further develop its CRISPR platform, highlighting the growing interest in leveraging gene-editing technologies in diagnostic applications.

Key Technology & Innovation Landscape Signals in Point-of-Care Testing

The landscape of point-of-care testing (POCT) is rich with signals that underscore the transformative potential of emerging technologies. A prominent driver in this landscape is the production of more sensitive and accurate POCT devices, particularly for non-communicable diseases. This direction is not just a technological pursuit but a strategic response to the increasing prevalence of chronic conditions such as diabetes, cardiac disorders, and cancer. The integration of advanced biosensors into POCT systems, for instance, is revolutionizing how these diseases are diagnosed and managed. By enabling the detection of specific biomarkers associated with disease progression and treatment efficacy, biosensors are augmenting the capabilities of POCT devices, making them indispensable in modern healthcare settings.

The strategic implications of these advancements are profound. For healthcare providers, the adoption of more sophisticated POCT devices translates to improved patient outcomes through timely diagnosis and personalized treatment strategies. This shift not only enhances clinical decision-making but also optimizes healthcare delivery by reducing the need for extensive lab-based testing. For companies like Abbott Laboratories, this presents an opportunity to capture market share by offering innovative products that cater to the evolving demands of healthcare systems worldwide.

Another significant signal in the POCT technology landscape is the role of molecular testing, particularly as implemented by companies such as Amedisys. As the first home health company to deploy molecular testing nationwide, Amedisys exemplifies how strategic innovation can lead to competitive differentiation. Molecular testing’s ability to provide rapid and accurate results—up to 97% accuracy compared to traditional methods—demonstrates its value in enhancing diagnostic precision and patient care. This level of accuracy and efficiency is a game-changer, particularly in home health settings, where timely intervention is critical.

The implications for market dynamics are substantial. As molecular testing becomes more prevalent, it is likely to drive a shift in healthcare delivery models, encouraging more decentralized and patient-centered approaches. This shift could lead to increased demand for home-based diagnostics, prompting companies to invest in technologies that facilitate remote testing and monitoring. For investors, this presents a lucrative opportunity to back companies that are at the forefront of this transition, as the demand for innovative home health solutions is expected to grow steadily.

Strategic Implications of Technology & Innovation Landscape in Point-of-Care Testing

The strategic landscape of point-of-care testing is being reshaped by technological advancements that promise to redefine the economics and operational dynamics of healthcare delivery. One of the critical mechanisms driving this transformation is the integration of artificial intelligence (AI) into POCT systems. Generative AI, in particular, is being leveraged to enhance the predictive capabilities of diagnostic tools, allowing for more precise and personalized treatment plans. The introduction of AI into POCT workflows not only improves diagnostic accuracy but also optimizes throughput by automating routine processes and reducing the burden on healthcare professionals.

For companies operating in the POCT space, the strategic implications of AI integration are manifold. Firms like VedaBio, which recently announced a strategic agreement with Siemens Healthineers to advance its CRISPR platform, are positioning themselves at the cutting edge of this technological evolution. By harnessing AI, these companies can offer solutions that are not only more effective but also more efficient, thereby gaining a competitive edge in a rapidly evolving market. This strategic positioning is crucial as the demand for high-performance diagnostic tools continues to rise, driven by the increasing focus on precision medicine and personalized healthcare.

The impact of these innovations on market structure is significant. As POCT technologies become more advanced, there is likely to be a shift in competitive dynamics, with companies that can effectively integrate AI and other cutting-edge technologies gaining a distinct advantage. This could lead to increased consolidation in the market, as firms seek to acquire the capabilities needed to remain competitive. Additionally, the adoption of AI-powered POCT systems could lead to changes in pricing strategies, as companies leverage their technological superiority to command premium pricing for their products.

Furthermore, the strategic implications extend to regulatory and compliance considerations. As the complexity of POCT systems increases, so too does the need for robust regulatory frameworks to ensure their safety and efficacy. This necessitates a proactive approach from companies, which must navigate a landscape of evolving regulations while maintaining compliance with standards such as ISO/IEC 17025. The ability to effectively manage these compliance requirements will be a key determinant of success in the POCT market, influencing both market entry strategies and long-term operational viability.

Point-of-Care Testing Technology & Innovation Landscape Forward Outlook

Looking ahead, the point-of-care testing technology and innovation landscape is poised for continued evolution, driven by ongoing advancements in biosensors, molecular diagnostics, and AI. As these technologies mature, they are expected to further enhance the capabilities of POCT systems, making them even more integral to healthcare delivery. The production of more sensitive and accurate diagnostic devices will likely accelerate, fueled by the need to address the growing burden of chronic diseases and the rising demand for personalized healthcare solutions.

In this forward outlook, the role of companies like Abbott Laboratories and Amedisys will be pivotal. As industry leaders, their continued investment in R&D and strategic partnerships will shape the trajectory of POCT innovation. For instance, Abbott’s focus on developing next-generation biosensors and molecular diagnostics will likely set new benchmarks for diagnostic accuracy and efficiency, reinforcing its leadership position in the market. Similarly, Amedisys’ pioneering efforts in molecular testing underscore the potential for home health companies to drive innovation and expand the reach of POCT technologies.

The implications for the broader healthcare ecosystem are profound. As POCT technologies become more advanced and accessible, they are likely to drive a paradigm shift in healthcare delivery, moving towards more decentralized and patient-centric models. This shift will necessitate changes in healthcare infrastructure and resource allocation, as providers adapt to new diagnostic capabilities and patient care pathways. For policymakers, this evolution presents both opportunities and challenges, as they seek to balance innovation with the need for robust regulatory oversight.

In conclusion, the technology and innovation landscape of point-of-care testing is characterized by rapid advancements and strategic initiatives that are reshaping the future of healthcare diagnostics. As companies continue to leverage cutting-edge technologies to develop innovative solutions, the potential for POCT to transform healthcare delivery is immense. The strategic implications for market dynamics, competitive behavior, and regulatory frameworks are significant, underscoring the need for stakeholders to remain agile and forward-thinking in this rapidly evolving landscape.

Market Risk

Market Risk

Point-of-Care Testing Risk Factors & Disruption Threats Overview

The point-of-care testing (POCT) market faces a multifaceted landscape of risks and disruption threats that shape its structure and strategic trajectory. With an overall high market risk level, the industry is susceptible to volatility influenced by various factors, including economic fluctuations, geopolitical dynamics, and technological advancements. These factors collectively impact market pricing, demand elasticity, and operational resilience, presenting both challenges and opportunities for stakeholders.

Key structural drivers in the POCT market include the rapid evolution of technology, regulatory shifts, and the increasing demand for accessible and efficient healthcare solutions. These drivers, coupled with external pressures such as tariffs and supply chain disruptions, underscore the complexity of navigating the POCT landscape. As the market continues to evolve, understanding these risk factors and disruption threats becomes crucial for companies aiming to maintain competitive advantage and drive innovation.

Point-of-Care Testing Risk Factors & Disruption Threats Current Scenario

In the current scenario, the POCT market is characterized by significant structural constraints and market risks. One of the primary risk factors is the rising cost of imported materials due to increased duties and tariffs. These tariffs can result in a 5-15% increase in the cost of reagents, plastics, and instrument components, significantly impacting cost-per-test calculations in high-throughput environments. For laboratories operating on tight margins and fixed reimbursement structures, these cost increases pose substantial challenges to maintaining profitability and operational efficiency.

Moreover, the regulatory environment for the POCT market is in a state of flux, particularly with the integration of artificial intelligence (AI) technologies. The regulatory landscape for AI is constantly changing, and laws that might benefit a company today could become obstacles tomorrow. This uncertainty creates a precarious situation for companies investing in AI-driven POCT solutions, as they must remain agile and adaptable to shifting regulations to avoid compliance risks and potential disruptions to their operations.

Another critical factor influencing the current POCT market is the demand for rapid and reliable testing solutions, particularly in emergency and remote settings. The adoption of point-of-care assays has the potential to address emergency department overcrowding by enabling rapid decision-making and improving patient throughput. This demand for efficient testing solutions is further amplified by the ongoing challenges faced by healthcare systems, such as patient overcrowding and long waiting hours in emergency departments. As a result, there is a growing need for POCT solutions that can enhance patient care and streamline healthcare operations.

The current scenario is also shaped by the broader economic and political landscape, which introduces additional layers of complexity to the POCT market. Geopolitical tensions and economic uncertainties can lead to fluctuations in currency values and trade policies, impacting the cost of imports and exports for POCT products. Additionally, world events such as pandemics and natural disasters can disrupt supply chains and create demand surges for specific testing solutions, further complicating market dynamics.

Key Risk Factors & Disruption Threats Signals in Point-of-Care Testing

The POCT market’s key risk factors and disruption threats are underscored by several compelling signals that highlight the market’s vulnerabilities and the potential for transformative change. One such signal is the increasing duties on imported plastics, reagents, personal protective equipment, and other laboratory supplies, which have begun to elevate procurement costs. These cost pressures affect laboratories with tight margins, challenging their ability to deliver affordable testing services while maintaining quality standards.

Another critical signal is the regulatory uncertainty surrounding AI technologies. As AI continues to play a more prominent role in POCT solutions, companies must navigate a complex and evolving regulatory landscape. The risk of regulatory changes can hinder innovation and limit the adoption of AI-driven solutions, affecting the market’s ability to meet growing demand for advanced testing capabilities.

Furthermore, the need for efficient testing solutions in emergency scenarios is driving the adoption of point-of-care assays. This demand is fueled by the challenges faced by healthcare systems, such as emergency department overcrowding and decision-making regarding patient treatment priorities. The ability of POCT solutions to provide rapid and reliable test results is a key factor in addressing these challenges, highlighting the market’s potential to enhance healthcare delivery.

In addition to these signals, the broader economic and geopolitical environment also plays a significant role in shaping the POCT market’s risk landscape. Fluctuations in currency values, trade policies, and world events can create uncertainties that impact the cost and availability of POCT products. These factors underscore the need for companies to adopt strategies that enhance resilience and adaptability in the face of external pressures.

Overall, the POCT market is at a critical juncture, with significant risks and opportunities shaping its future trajectory. Companies must navigate a complex landscape of structural constraints and market disruptions, leveraging innovative solutions and strategic partnerships to maintain competitiveness and drive growth. As the market continues to evolve, understanding and addressing these risk factors and disruption threats will be essential for success in the POCT industry.

Strategic Implications of Risk Factors & Disruption Threats in Point-of-Care Testing

The strategic implications of the identified risk factors and disruption threats for the POCT market are profound, influencing market structure, pricing power, demand elasticity, and operational resilience.

Market Structure and Pricing Power

The evolving regulatory landscape and technological advancements necessitate that companies in the POCT market re-evaluate their competitive strategies. Firms that can navigate regulatory complexities and integrate advanced technologies effectively will likely gain a competitive edge, potentially reshaping the market structure. These companies may establish themselves as leaders in innovation, commanding higher pricing power due to the superior capabilities of their offerings.

However, the increased costs associated with tariffs and supply chain disruptions could erode pricing power for some companies, particularly those unable to pass these costs onto consumers. In such scenarios, firms may need to focus on operational efficiencies and cost-control measures to maintain their margins while remaining competitive on pricing.

Demand Elasticity and Consumer Behavior

The adoption of advanced technologies in POCT can enhance demand elasticity by offering new capabilities that meet evolving consumer needs. For example, point-of-care assays that enable rapid decision-making in emergency departments can drive demand by addressing critical healthcare challenges. However, the success of these innovations depends on consumer acceptance and the perceived value of these advancements, which can be influenced by factors such as cost, ease of use, and compatibility with existing healthcare systems.