Global Silicone Based Catheters Market Report, Size and Forecast 2026-2033

Global Silicone Based Catheters Market Forecast Snapshot: 2026–2033

| Parameter | Value |

|---|---|

| Base Year | 2025 |

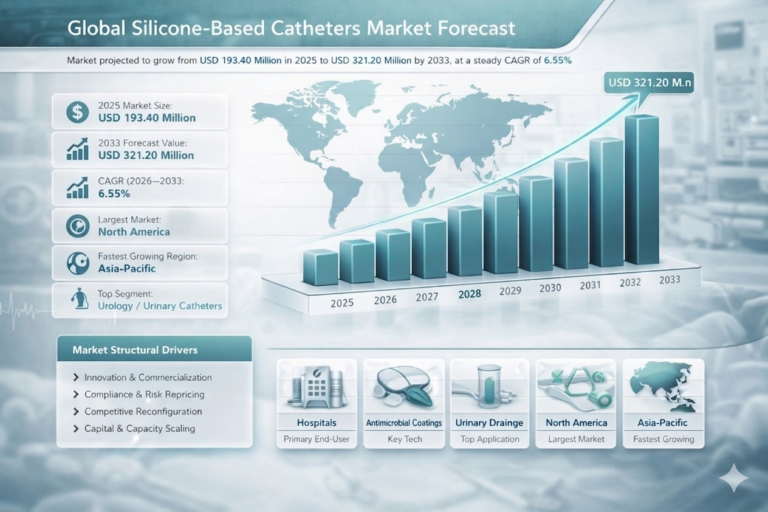

| Base Year Market Size | USD 193.40 Million |

| Forecast Period | 2026–2033 |

| Forecasted CAGR | ~6.55% |

| Forecasted Market Size (2033) | USD 321.20 Million |

Market Size & Forecast

The Global Silicone Based Catheters Market is projected to grow from USD 193.40 million in 2025 to approximately USD 321.20 million by 2033, expanding at a CAGR of ~6.55% during the forecast period. Market growth is driven by increasing prevalence of chronic diseases, rising geriatric population, and growing demand for minimally invasive procedures. Silicone-based catheters are increasingly preferred due to their superior biocompatibility, flexibility, and reduced infection risk compared to traditional latex-based alternatives. Additionally, advancements in catheter design, infection control technologies, and healthcare infrastructure expansion are supporting steady market adoption.Market Overview

Silicone-based catheters are widely used across multiple medical applications including urology, cardiovascular procedures, and critical care. Their non-reactive nature, durability, and patient comfort advantages make them a preferred choice in long-term catheterization and complex medical procedures. The market is highly fragmented with strong competition among global and regional players. Increasing emphasis on patient safety, infection prevention, and improved clinical outcomes is driving continuous innovation in catheter technologies. Advanced features such as antimicrobial coatings, hydrophilic surfaces, and improved material engineering are reshaping product development and adoption across healthcare systems.Structural Drivers of Market Growth

- Rising Prevalence of Chronic Diseases Increasing incidence of urinary disorders, cardiovascular conditions, and critical care requirements is driving catheter demand.

- Growing Geriatric Population Aging populations globally are contributing to higher demand for long-term catheterization and urological care.

- Expansion of Minimally Invasive Procedures Increasing preference for minimally invasive treatments is boosting demand for advanced catheter technologies.

- Technological Advancements in Catheter Design Innovations such as antimicrobial coatings, hydrophilic materials, and smart catheter systems are enhancing patient outcomes.

- Regulatory Focus on Infection Control Stringent guidelines to reduce catheter-associated infections are supporting adoption of silicone-based solutions.

Market Segmentation Analysis

Top-Level Segment Share Split

- By End User: 30%

- By Application: 30%

- By Catheter Type: 25%

- By Technology & Material Advancements: 15%

1. By End User

1.1 Hospitals 1.2 Specialty Clinics 1.3 Ambulatory Surgical Centers Hospitals dominate due to high procedural volume and need for post-operative and long-term catheterization.2. By Application

2.1 Urology (Largest Segment) 2.2 Critical Care 2.3 Cardiovascular Applications Urology applications lead due to widespread use in urinary retention and bladder management.3. By Catheter Type

3.1 Urinary Catheters 3.1.1 Foley Catheters 3.1.2 Suprapubic Catheters 3.1.3 Intermittent Catheters 3.2 Vascular Catheters 3.2.1 Central Venous Catheters 3.2.2 Peripheral Intravenous Catheters 3.3 Specialty Catheters Urinary catheters account for the largest share due to frequent usage and recurring replacement demand.4. By Technology

4.1 Standard Silicone Catheters 4.2 Antimicrobial Coated Catheters 4.3 Hydrophilic Coated Catheters 4.4 Advanced Smart Catheters (Emerging) Advanced coatings and infection-resistant technologies are the fastest-growing segment.Regional Market Insights

1. North America – Largest Market

Strong healthcare infrastructure, high chronic disease prevalence, and strict infection control standards drive market leadership.2. Europe

Growth supported by regulatory focus on patient safety, adoption of advanced catheter technologies, and sustainability initiatives.3. Asia-Pacific – Fastest Growing Region

Rising healthcare investments, growing elderly population, and increasing surgical procedures are accelerating market growth.4. Latin America

Moderate growth supported by improving healthcare access and rising awareness of infection control.5. Middle East & Africa

Emerging demand driven by healthcare infrastructure development and increasing chronic disease burden.Competitive Landscape

Leading companies in the Global Silicone Based Catheters Market include:- Becton, Dickinson and Company

- Cardinal Health

- Teleflex Incorporated

- B. Braun Melsungen AG

- Medtronic

- ConvaTec Group Plc

- Coloplast A/S

Strategic Intelligence & Pheonix AI-Backed Insights

- Pheonix Demand Forecast Engine Analyzes disease prevalence, procedure volumes, and catheter adoption trends.

- Infection Control & Safety Model Evaluates demand for antimicrobial and advanced coating technologies.

- Material Innovation Tracker Tracks advancements in silicone materials, coatings, and catheter durability.

Why the Silicone Based Catheters Market Remains Critical

- Essential for long-term patient care and critical procedures

- Reduces risk of catheter-associated infections

- Improves patient comfort and clinical outcomes

- Supports minimally invasive medical treatments

- High recurring demand due to replacement cycles

Final Takeaway of Global Silicone Based Catheters Market

The Global Silicone Based Catheters Market is a stable and steadily growing segment within the medical devices industry, driven by rising healthcare demand, technological advancements, and increasing focus on patient safety. Future growth will be shaped by infection-resistant technologies, smart catheter systems, and expanding healthcare access in emerging markets. Companies that prioritize innovation, regulatory compliance, and global distribution expansion will be best positioned to lead the market through 2033.Table of Contents

Table of Contents

- 1. Executive Summary

- 1.1 Market Forecast Snapshot (2026-2033)

- 1.2 Global Market Size & CAGR Analysis

- 1.3 Largest & Fastest-Growing Segments

- 1.4 Region-Level Leadership & Growth Trends

- 1.5 Key Market Drivers

- 1.6 Competitive Landscape Overview

- 1.7 Strategic Outlook Through 2033

- 2. Introduction & Market Overview

- 2.1 Definition of the Catheters Market

- 2.2 Scope of the Study

- 2.3 Industry Evolution & Market Development

- 2.4 Supply Chain & Distribution Infrastructure

- 2.5 Impact of Consumer Trends

- 2.6 Sustainability & Regulatory Landscape

- 2.7 Technology & Innovation Landscape

- 3. Research Methodology

- 3.1 Primary Research

- 3.2 Secondary Research

- 3.3 Market Size Estimation Model

- 3.4 Forecast Assumptions (2026-2033)

- 3.5 Data Validation & Triangulation

- 4. Market Dynamics

- 4.1 Drivers

- 4.1.1 Increasing Demand Drivers

- 4.1.2 Industry Innovation Drivers

- 4.1.3 Market Expansion Factors

- 4.1.4 Regulatory or Policy Support

- 4.1.5 Technology Adoption Drivers

- 4.2 Restraints

- 4.2.1 Cost Constraints

- 4.2.2 Infrastructure Limitations

- 4.2.3 Regulatory Challenges

- 4.2.4 Market Awareness Barriers

- 4.3 Opportunities

- 4.3.1 Emerging Market Opportunities

- 4.3.2 Product Innovation Opportunities

- 4.3.3 Technology Expansion Opportunities

- 4.3.4 Supply Chain Improvements

- 4.4 Challenges

- 4.4.1 Supply Chain Complexity

- 4.4.2 Quality Control & Compliance

- 4.4.3 Regional Market Fragmentation

- 4.4.4 Competitive Pressure

- 4.1 Drivers

- 5. Catheters Market Analysis (USD Billion), 2026-2033

- 5.1 Market Size Overview

- 5.2 CAGR Analysis

- 5.3 Regional Revenue Distribution

- 5.4 Segment Revenue Analysis

- 5.5 Distribution Channel Analysis

- 5.6 Consumer Impact Analysis

- 6. Market Segmentation (USD Billion), 2026-2033

- 6.1 By Application

- 6.1.1 Cardiovascular

- 6.1.1.1 Vascular Access Procedures

- 6.1.1.1.1 Diagnostic Catheterization Procedures

- 6.1.1.1.1.1 Coronary Artery Imaging Procedures

- 6.1.1.1.1.2 Peripheral Vascular Imaging

- 6.1.1.1.1 Diagnostic Catheterization Procedures

- 6.1.1.1 Vascular Access Procedures

- 6.1.2 Critical Care

- 6.1.2.1 Intensive Care Catheterization

- 6.1.2.1.1 Long-Term Catheter Access

- 6.1.2.1.1.1 ICU Infusion Catheter Systems

- 6.1.2.1.1.2 Continuous Medication Delivery Systems

- 6.1.2.1.1 Long-Term Catheter Access

- 6.1.2.1 Intensive Care Catheterization

- 6.1.3 Urology

- 6.1.3.1 Urinary Drainage

- 6.1.3.1.1 Acute Urinary Retention Management

- 6.1.3.1.1.1 Hospital Urinary Drainage Systems

- 6.1.3.1.1.2 Postoperative Urinary Drainage

- 6.1.3.1.1 Acute Urinary Retention Management

- 6.1.3.1 Urinary Drainage

- 6.1.1 Cardiovascular

- 6.2 By Catheter Type

- 6.2.1 Urinary Catheters

- 6.2.1.1 Foley Catheters

- 6.2.1.1.1 Three-Way Foley Catheters

- 6.2.1.1.1.1 Continuous Bladder Irrigation Catheters

- 6.2.1.1.1.2 Post-Surgical Drainage Catheters

- 6.2.1.1.2 Two-Way Foley Catheters

- 6.2.1.1.2.1 Standard Silicone Foley Catheters

- 6.2.1.1.2.2 Silicone-Coated Foley Catheters

- 6.2.1.1.1 Three-Way Foley Catheters

- 6.2.1.2 Intermittent Catheters

- 6.2.1.2.1 Coude Tip Catheters

- 6.2.1.2.1.1 Curved Tip Silicone Catheters

- 6.2.1.2.1.2 Prostatic Obstruction Catheters

- 6.2.1.2.2 Straight Tip Catheters

- 6.2.1.2.2.1 Male Intermittent Catheters

- 6.2.1.2.2.2 Female Intermittent Catheters

- 6.2.1.2.1 Coude Tip Catheters

- 6.2.1.3 Suprapubic Catheters

- 6.2.1.3.1 Balloon Retention Catheters

- 6.2.1.3.1.1 Silicone Balloon Catheters

- 6.2.1.3.1.2 Long-Term Suprapubic Catheters

- 6.2.1.3.1 Balloon Retention Catheters

- 6.2.1.1 Foley Catheters

- 6.2.1 Urinary Catheters

- 6.3 By End User

- 6.3.1 Ambulatory Surgical Centers

- 6.3.1.1 Minimally Invasive Surgical Facilities

- 6.3.1.1.1 Outpatient Catheterization Procedures

- 6.3.1.1.1.1 Day Surgery Catheter Use

- 6.3.1.1.1.2 Minimally Invasive Urological Procedures

- 6.3.1.1.1 Outpatient Catheterization Procedures

- 6.3.1.1 Minimally Invasive Surgical Facilities

- 6.3.2 Hospitals

- 6.3.2.1 Surgical Departments

- 6.3.2.1.1 Urology Surgery Units

- 6.3.2.1.1.1 Postoperative Catheterization

- 6.3.2.1.1.2 Long-Term Urinary Management

- 6.3.2.1.1 Urology Surgery Units

- 6.3.2.1 Surgical Departments

- 6.3.3 Specialty Clinics

- 6.3.3.1 Urology Clinics

- 6.3.3.1.1 Urinary Disorder Treatment Centers

- 6.3.3.1.1.1 Chronic Urinary Retention Management

- 6.3.3.1.1.2 Bladder Dysfunction Treatment

- 6.3.3.1.1 Urinary Disorder Treatment Centers

- 6.3.3.1 Urology Clinics

- 6.3.1 Ambulatory Surgical Centers

- 6.4 By Specialty Catheters

- 6.4.1 Cardiovascular Catheters

- 6.4.1.1 Angiography Catheters

- 6.4.1.1.1 Diagnostic Angiography Catheters

- 6.4.1.1.1.1 Coronary Angiography Catheters

- 6.4.1.1.1.2 Peripheral Angiography Catheters

- 6.4.1.1.1 Diagnostic Angiography Catheters

- 6.4.1.2 Balloon Catheters

- 6.4.1.2.1 Angioplasty Balloon Catheters

- 6.4.1.2.1.1 Coronary Balloon Catheters

- 6.4.1.2.1.2 Peripheral Balloon Catheters

- 6.4.1.2.1 Angioplasty Balloon Catheters

- 6.4.1.1 Angiography Catheters

- 6.4.2 Neurovascular Catheters

- 6.4.2.1 Microcatheters

- 6.4.2.1.1 Neurovascular Intervention Catheters

- 6.4.2.1.1.1 Aneurysm Treatment Microcatheters

- 6.4.2.1.1.2 Stroke Treatment Microcatheters

- 6.4.2.1.1 Neurovascular Intervention Catheters

- 6.4.2.1 Microcatheters

- 6.4.1 Cardiovascular Catheters

- 6.5 By Vascular Catheters

- 6.5.1 Central Venous Catheters

- 6.5.1.1 Non-Tunneled Central Venous Catheters

- 6.5.1.1.1 Short-Term Central Venous Catheters

- 6.5.1.1.1.1 Intensive Care Catheters

- 6.5.1.1.1.2 Emergency Venous Access Catheters

- 6.5.1.1.1 Short-Term Central Venous Catheters

- 6.5.1.2 Tunneled Central Venous Catheters

- 6.5.1.2.1 Hemodialysis Catheters

- 6.5.1.2.1.1 Double Lumen Dialysis Catheters

- 6.5.1.2.1.2 Silicone Hemodialysis Access Catheters

- 6.5.1.2.1 Hemodialysis Catheters

- 6.5.1.1 Non-Tunneled Central Venous Catheters

- 6.5.2 Peripheral Intravenous Catheters

- 6.5.2.1 Short Peripheral Catheters

- 6.5.2.1.1 Standard IV Catheters

- 6.5.2.1.1.1 Peripheral Infusion Catheters

- 6.5.2.1.1.2 Medication Delivery Catheters

- 6.5.2.1.1 Standard IV Catheters

- 6.5.2.1 Short Peripheral Catheters

- 6.5.1 Central Venous Catheters

- 6.1 By Application

- 7. Market Segmentation by Geography

- 7.1 North America

- 7.2 Europe

- 7.3 Asia-Pacific

- 7.4 Latin America

- 7.5 Middle East & Africa

- 8. Competitive Landscape

- 8.1 Market Share Analysis

- 8.2 Product Portfolio Benchmarking

- 8.3 Product Positioning Mapping

- 8.4 Supply Chain & Distribution Partnerships

- 8.5 Competitive Intensity & Differentiation

- 9. Company Profiles

- 10. Strategic Intelligence & Pheonix AI Insights

- 10.1 Pheonix Demand Forecast Engine

- 10.2 Supply Chain & Infrastructure Analyzer

- 10.3 Technology & Innovation Tracker

- 10.4 Product Development Insights

- 10.5 Automated Porter’s Five Forces Analysis

- 11. Future Outlook & Strategic Recommendations

- 11.1 Emerging Market Expansion

- 11.2 Technology Innovation Strategies

- 11.3 Product Development Roadmap

- 11.4 Regional Expansion Strategies

- 11.5 Long-Term Market Outlook (2033+)

- 12. Appendix

- 13. About Pheonix Research

- 14. Disclaimer

Competitive Landscape

Competitive Landscape of the Silicone Based Catheters Market

Executive Framing

The competitive intensity and market structure within the silicone-based catheters industry are increasingly becoming pivotal elements that define the strategic landscape from 2026 to 2033. This dimension matters now more than ever due to the confluence of accelerated technological advancements, regulatory shifts, and evolving healthcare demands. The market structure is described as fragmented, with numerous players vying for dominance, yet a clear delineation exists as Tier 1 entities lead the charge with significant market influence. Understanding this structure and its implications is essential for stakeholders aiming to navigate the complex web of competition and positioning effectively. As competition rises, driven by both innovation and strategic maneuvers, the ability to anticipate and adapt to these forces becomes crucial for maintaining market share and achieving growth.

The high competitive intensity in the silicone-based catheters sector is driven by several factors, including the increasing adoption of silicone Foley catheters over traditional latex alternatives. This shift is not merely a preference but a response to heightened awareness and regulatory oversight on infection control and patient safety. The market’s fragmentation, with a Tier 1 player count of five, underscores the competitive dynamics where entities like Becton, Dickinson and Company, Cardinal Health, Teleflex Incorporated, and others are continuously innovating and repositioning their strategies to gain an edge. Thus, the dynamics of market structure and competitive intensity are intricately linked to both the existing demand for more advanced and safer catheter technologies and the strategic initiatives taken by key market players.

Current Market Reality

At present, the silicone-based catheters market exhibits a complex landscape characterized by a blend of innovation-driven growth and strategic positioning. The market’s fragmented nature is evident in the way multiple companies are striving to carve out their niche while simultaneously expanding their product offerings and technological capabilities. The high competitive intensity is further fueled by notable market activities such as the FDA approval of Cook Medical’s Advance Evero™ 18 Everolimus-Coated PTA Balloon Catheter, which highlights the importance of regulatory milestones in shaping competitive advantage.

B. Braun Melsungen AG’s launch of the Clik-FIX® Epidural/Peripheral Nerve Block Catheter Securement Device is another significant event, illustrating the company’s commitment to enhancing its product portfolio to meet the growing demand for innovative catheter solutions. This launch not only marks a strategic move to strengthen B. Braun’s market position but also reflects the broader industry trend towards improving patient safety and comfort through advanced catheter technologies.

The current market reality is further underscored by the increasing adoption of silicone Foley catheters, driven by their superior biocompatibility and reduced risk of allergic reactions compared to latex catheters. This shift in product preference is supported by rising healthcare standards and the growing emphasis on infection prevention protocols. Moreover, the acquisition of the Clik-FIX catheter securement device portfolio by B. Braun signifies strategic consolidation efforts aimed at enhancing their competitive positioning and expanding their market share.

Companies like Teleflex Incorporated and Coloplast A/S are actively engaging in strategic initiatives such as forming partnerships and investing in R&D to develop infection-resistant designs. These efforts are a direct response to the tightening of healthcare regulations and the increasing awareness surrounding catheter-associated urinary tract infections (CAUTIs). The emphasis on developing advanced, infection-resistant catheter technologies is a testament to the industry’s commitment to addressing the critical challenges faced in infection control and patient safety.

Furthermore, the partnership between Becton, Dickinson and Company and the Danish Technical University for wireless monitoring highlights the integration of smart technologies in catheter design. This collaboration aims to leverage wireless technology to enhance patient monitoring and improve clinical outcomes, thereby catering to the growing demand for smart catheter solutions.

Key Signals And Evidence

- Increasing adoption of silicone Foley catheters, reshaping market demand and influencing competitive strategies due to their biocompatibility, flexibility, and reduced risk of allergic reactions.

- Regulatory incentives for CAUTI reduction, highlighting the importance of compliance with stringent healthcare regulations.

- B. Braun’s acquisition of the Clik-FIX catheter securement device portfolio, exemplifying strategic consolidation efforts.

- Partnerships between Becton, Dickinson and Company and the Danish Technical University for wireless monitoring, integrating smart technologies into catheter design.

- Increased R&D investment in infection-resistant designs, reflecting the industry’s commitment to addressing infection control and patient safety challenges.

Strategic Implications

- Prioritize innovation in product design and materials, exemplified by the adoption of silicone Foley catheters and securement solutions.

- Regulatory approvals, such as FDA endorsements, provide competitive advantage and market credibility.

- Strategic partnerships and collaborations enable accelerated product development and expansion of technological capabilities.

- Focus on infection-resistant designs to meet regulatory standards and patient safety requirements.

- Adapt to healthcare delivery shifts, including home healthcare and outpatient procedures, requiring tailored products and distribution networks.

Forward Outlook

- The market is expected to remain fragmented, with Tier 1 players exerting significant influence, while consolidation opportunities may increase.

- Acceleration of smart catheter technologies, integrating wireless monitoring and data-driven capabilities.

- Continued regulatory emphasis on infection prevention and CAUTI reduction will drive innovation and R&D investment.

- Growing geriatric population and chronic disease prevalence will sustain demand, offering growth opportunities.

- Environmental sustainability considerations will influence manufacturing and product design, balancing cost and eco-conscious practices.

Conclusion

The silicone-based catheters market is characterized by high competitive intensity and a fragmented structure, demanding strategic agility and innovation. Companies must navigate a complex landscape shaped by technological advancements, regulatory pressures, and evolving healthcare needs. By prioritizing innovation, strategic partnerships, and regulatory compliance, market players can position themselves for success. Stakeholders must remain vigilant and responsive to emerging trends and challenges to effectively navigate the competitive landscape and capitalize on growth opportunities.

Value Chain

Value Chain and Supply Chain Dynamics in the Silicone Based Catheters Market

Executive Framing

In the silicone-based catheters market, the value chain dimension plays a pivotal role in shaping the market structure and dynamics. This dimension is particularly significant now due to the evolving complexity of supply chains and the emergence of various bottlenecks that affect production and distribution. Unlike simpler latex alternatives, silicone catheters face unique challenges that influence cost structures and competitive positioning. With a primary operational model and distribution structure identified as hybrid, companies in this sector must navigate a moderate complexity level in their supply chains, which necessitates strategic agility to maintain margins and competitive advantage.

The current landscape is marked by labor-intensive production processes that drive up costs, posing a significant challenge in maintaining price competitiveness against latex catheters. Furthermore, the market is witnessing an increasing availability of alternative products such as external catheters, which puts additional pressure on silicone catheter manufacturers to innovate and differentiate their offerings. Regulatory requirements further complicate the operational landscape, as companies must meet stringent standards to ensure product safety and efficacy. This regulatory pressure is compounded by the emergence of biocompatible materials, which threaten silicone’s traditional dominance by offering potentially superior alternatives. Amid these challenges, the integration of advanced features such as sensors and antimicrobial coatings becomes crucial for maintaining market relevance and achieving competitive differentiation.

Current Market Reality

The current market reality of the silicone-based catheters industry is characterized by a confluence of factors that influence the operational and strategic decisions of companies. Labor-intensive production processes are a major bottleneck, leading to higher costs compared to latex catheters. This cost disparity directly affects pricing strategies and margin sustainability for manufacturers. The labor-intensive nature of silicone catheter production not only impacts costs but also limits capacity utilization and delivery performance. Optimizing supply chains is therefore a priority to ensure timely delivery and customer satisfaction.

In addition to production challenges, the availability of alternative products such as latex and external catheters intensifies competition. These alternatives often offer lower price points and simpler manufacturing processes, prompting silicone catheter manufacturers to emphasize innovation and quality to justify premium pricing. Industry players are increasingly focusing on biocompatibility and advanced functionalities, such as antimicrobial coatings and sensor integration, to differentiate their products and enhance patient outcomes.

Companies like B. Braun Medical are actively addressing these market dynamics. For instance, B. Braun’s acquisition of the Clik-FIX catheter securement device portfolio highlights the company’s commitment to enhancing product offerings and securing a competitive edge. Partnerships with technological institutions, such as the collaboration with the Danish Technical University for wireless monitoring, underscore the industry’s focus on integrating cutting-edge technologies to improve product functionality and patient care.

Key Signals And Evidence

- Labor-intensive production processes create higher costs than latex alternatives, acting as a barrier to entry for new players and highlighting the need for process optimization.

- Availability of alternative products, such as latex and external catheters, exerts competitive pressure, pushing manufacturers to innovate and differentiate through antimicrobial coatings and integrated sensors.

- Rising demand for biocompatible materials is driven by the prevalence of urinary retention and incontinence, emphasizing the importance of material innovation and patient-centric product design.

- Strategic initiatives by key players, such as B. Braun’s acquisitions and partnerships, indicate proactive approaches to addressing market challenges and leveraging technological advancements.

Strategic Implications

- Manufacturers must address cost disparities between silicone and alternatives by enhancing production efficiencies through automation and process optimization.

- Innovation in product differentiation, such as advanced antimicrobial coatings and sensor integration, is essential to maintain competitive advantage.

- Investment in R&D is critical to explore new biocompatible materials and reinforce silicone’s market position amid emerging alternatives.

- Collaborations with academic and technological institutions can accelerate development of smart catheter solutions and enhance patient outcomes.

Forward Outlook

Looking ahead, the silicone-based catheters market is poised for significant transformation driven by evolving consumer preferences, regulatory landscapes, and technological advancements. Integration of sensors and monitoring capabilities is expected to become more prevalent, supported by partnerships such as those with the Danish Technical University for wireless monitoring technologies.

The focus on effective antimicrobial coatings will continue to grow, addressing infection control and patient safety concerns. Companies that innovate in this space will have a competitive edge, particularly in addressing urinary retention and incontinence prevalence.

Supply chain complexity is expected to remain moderate, requiring companies to maintain agility and responsiveness, optimize capacity utilization, and ensure timely delivery amid potential disruptions such as regulatory changes or material shortages.

Overall, while cost pressures and competitive threats persist, innovation and technological advancements provide promising growth opportunities. Companies that proactively address bottlenecks, leverage emerging technologies, and align strategies with market demands will be well-positioned for sustainable competitive advantage from 2026 to 2033.

Investment Activity

Investment and Funding Dynamics in the Silicone Based Catheters Market

Executive Framing

The investment landscape in the silicone-based catheters market is undergoing a significant transformation, driven by strategic capital allocation and robust funding dynamics. As the global healthcare sector pivots towards more advanced and patient-friendly solutions, the silicone-based catheters market is emerging as a focal point for investors. This dimension is particularly crucial now because it aligns with broader healthcare trends, such as the increasing prevalence of chronic diseases and the need for minimally invasive procedures. These trends not only underscore the rising demand for silicone catheters but also highlight the strategic importance of capital flows and investment decisions in shaping market outcomes. The dimension of investment and funding dynamics in this market is characterized by high capital intensity and a rising trend in investments. This is evidenced by recent mergers and acquisitions (M&A) activities and the presence of active investors such as Bard, Teleflex, ConvaTec, Medtronic, Medline, Coloplast, B. Braun, Create Medic, Cook Medical, and Fuji Systems. These entities are focusing on investment themes such as chronic diseases, home healthcare services, self-catheterization, advanced materials, geographic expansion, and technological advancements. The strategic allocation of resources in these areas is driven by the increasing prevalence of chronic diseases, technological advancements in coatings, and the rising demand for silicone catheters. Moreover, the market is witnessing a surge in FDA approvals and new product launches, further signaling the strategic importance of this investment dimension.

Current Market Reality

The current market reality for silicone-based catheters is shaped by a confluence of strategic investments, technological advancements, and demographic shifts. Active investors are channeling significant capital into this market, attracted by the high capital intensity and the potential for lucrative returns. The market is characterized by recent M&A activities, which underscore the strategic consolidation efforts by major players to enhance their market position and technological capabilities. For instance, B. Braun’s acquisition of the Clik-FIX catheter securement device portfolio exemplifies the strategic moves being made to secure technological advantages and expand product offerings. Additionally, the rising demand for silicone catheters is being propelled by the increasing prevalence of chronic diseases and the growing geriatric population. The demographic shift towards an aging population is driving the demand for home healthcare services and self-catheterization solutions, areas where silicone-based catheters offer significant advantages over traditional alternatives.

This demand is further augmented by technological advancements in catheter design, which are enhancing biocompatibility and infection control, thus offering safer and more effective solutions for patients. Active investors such as Medtronic and Cook Medical are capitalizing on these trends by increasing their R&D investments and launching new products. For example, Cook Medical’s FDA approval of the Advance Evero™ 18 Everolimus-Coated PTA Balloon Catheter and B. Braun’s launch of the Clik-FIX® Epidural/Peripheral Nerve Block Catheter Securement Device are indicative of the strategic focus on innovation and product differentiation. These developments are not only enhancing the competitive landscape but also driving market expansion through geographic diversification and strategic partnerships.

The market is also witnessing a shift towards minimally invasive procedures, which are becoming increasingly popular due to their reduced risk, shorter recovery times, and improved patient outcomes. This trend is compelling manufacturers and investors to focus on technological advancements that facilitate these procedures, thereby attracting further capital into the market. The acquisition of new technology firms by major players is a strategic move to bolster their technological capabilities and capture a larger share of this growing market segment.

Key Signals And Evidence

- The expansion of minimally invasive procedures, driving demand for advanced catheter technologies and enhanced patient outcomes.

- Acquisition of new technology firms, strengthening technological capabilities and expanding product portfolios.

- Surge in new product launches, supported by FDA approvals, indicating regulatory alignment and innovation focus.

- Rising elderly population and prevalence of chronic diseases, fueling demand for patient-centric healthcare solutions.

- Geographic expansion into emerging markets, diversifying revenue streams and capturing growth opportunities.

Companies like Bard and Teleflex are channeling resources into R&D to innovate catheter designs that facilitate less invasive procedures. Medtronic’s strategic acquisitions exemplify the market’s focus on maintaining a competitive edge through technological integration. Increased R&D investments by ConvaTec and Coloplast highlight the industry’s commitment to developing infection-resistant designs and biocompatible materials. Cook Medical’s FDA approval of the Advance Evero™ 18 Everolimus-Coated PTA Balloon Catheter exemplifies successful R&D outcomes, while B. Braun’s launch of the Clik-FIX® device emphasizes user-friendly innovations. Medline and Fuji Systems are pursuing geographic diversification into regions like Asia-Pacific and Latin America.

Strategic Implications

- Align product development strategies with minimally invasive procedures and technological integration trends.

- Acquisition of technology firms may lead to market consolidation, enhancing technological capabilities and operational efficiency.

- Prioritize innovation through R&D investments to maintain competitive advantage and meet regulatory standards.

- Focus on infection-resistant designs and biocompatibility to enhance patient safety and product adoption.

- Leverage geographic expansion to optimize market entry strategies and maximize growth potential.

Forward Outlook

Looking ahead, the silicone-based catheters market is poised for continued growth and transformation, driven by strategic capital allocation and evolving healthcare needs. The emphasis on minimally invasive procedures, technological integration, and geographic diversification will remain central to investment strategies, shaping the market’s trajectory over the forecast period from 2026 to 2033. In the near-to-medium term, we can expect to see an acceleration in mergers and acquisitions, as companies seek to consolidate their positions and expand their technological capabilities. This consolidation may lead to increased competition among major players, driving further innovation and efficiency improvements.

As the market matures, the focus will likely shift towards enhancing operational efficiency and optimizing supply chains to reduce costs and improve margins. The rising prevalence of chronic diseases and the growing geriatric population will continue to drive demand for silicone-based catheters, necessitating ongoing investment in R&D and new product development. Companies that can anticipate and respond to these demographic shifts will be well-positioned to capitalize on emerging opportunities and maintain their competitive edge. Overall, the silicone-based catheters market offers a compelling investment landscape, characterized by strategic capital flows and robust funding dynamics. As investors and stakeholders navigate this complex environment, the focus will be on leveraging innovative solutions.

Technology & Innovation

Technology and Innovation Landscape in the Silicone Based Catheters Market

Executive Framing

In the evolving landscape of medical technology, silicone-based catheters stand poised at the intersection of innovation and necessity. This dimension matters now more than ever due to the confluence of rising chronic disease prevalence, an aging population, and increased focus on patient comfort and infection control. Silicone-based catheters offer a compelling technological advantage with their inherent biocompatibility and adaptability for advanced features such as antimicrobial coatings and smart technology integration. As the healthcare industry shifts towards minimally invasive procedures and personalized medical devices, the role of silicone-based catheters becomes increasingly pivotal in transforming patient care experiences and outcomes.

The current market landscape for silicone-based catheters is characterized by a significant push towards innovation, driven by the necessity to address pressing healthcare challenges. The innovation intensity in this sector is high, with moderate patent activity indicating a steady flow of new ideas and solutions. The technology is at a growth stage, suggesting an ongoing expansion in both its application and market penetration. Companies like Cook Medical, B. Braun Medical Inc., Teleflex Incorporated, and others are at the forefront, leveraging advancements in catheter technologies to meet the evolving needs of the market. These companies are not only enhancing existing products but also exploring new horizons through strategic partnerships and acquisitions.

Current Market Reality

The silicone-based catheter market is currently navigating a transformative phase, fueled by a series of technological advancements and shifting healthcare priorities. The sector’s growth trajectory is supported by several key players who are actively investing in research and development to enhance catheter functionalities and patient outcomes. Cook Medical, for instance, has made significant strides with the FDA approval of its Advance Evero™ 18 Everolimus-Coated PTA Balloon Catheter, highlighting the sector’s focus on integrating drug delivery capabilities into catheter designs. Similarly, B. Braun Medical’s introduction of the Clik-FIX® Epidural/Peripheral Nerve Block Catheter Securement Device underscores the industry’s commitment to improving catheter securement and reducing associated risks.

The underlying market reality is shaped by a growing demand for minimally invasive surgical procedures, driven by the need for reduced recovery times and improved patient comfort. This demand is complemented by an increased awareness regarding infection control, a crucial factor given the risks associated with catheter-related infections. As healthcare systems worldwide place greater emphasis on infection prevention, the development of catheters with advanced antimicrobial properties becomes imperative. Companies like Bactiguard and Cardinal Health are exploring biofilm-resistant technologies to mitigate these risks and enhance patient safety.

Moreover, the rising prevalence of urinary tract disorders and chronic diseases necessitates the development of more sophisticated catheter technologies. The aging population further amplifies this need, as older adults are more likely to require catheterization due to various health conditions. This demographic shift is prompting companies to innovate, creating catheters that are not only effective but also tailored to the unique needs of geriatric patients.

Key Signals And Evidence

- The rising demand for minimally invasive surgical procedures is driving adoption of catheters with advanced balloon technologies and self-lubricating surfaces for smoother insertion and reduced discomfort.

- Increased awareness regarding infection control is encouraging development of antimicrobial coatings and biofilm-resistant properties to reduce catheter-associated urinary tract infections (CAUTIs).

- The growing prevalence of urinary tract disorders and chronic diseases underscores the necessity for durable and reliable catheter solutions, promoting the integration of hydrogel materials and biocompatible silicone.

- Development of personalized devices is gaining traction, enabling tailored catheter solutions for patient-specific anatomical and physiological needs, particularly in aging populations.

Companies like Teleflex Incorporated, Medtronic, Bard, and ConvaTec are actively innovating to meet these evolving demands, highlighting the strategic importance of technology in shaping the market.

Strategic Implications

- Healthcare providers must re-evaluate procurement strategies to prioritize technologically advanced, infection-resistant catheters.

- Manufacturers must invest in R&D to create catheters that meet evolving clinical requirements, including personalized designs and smart technology integration.

- Regulatory considerations for infection prevention are likely to become more stringent, requiring companies to ensure compliance while leveraging innovation as a competitive differentiator.

- Partnerships with academic institutions and technology collaborators, such as the B. Braun Medical Inc. collaboration with the Danish Technical University, can accelerate product development and adoption of cutting-edge features.

Forward Outlook

Looking ahead, the silicone-based catheter market is poised for continued growth and transformation. The rising demand for minimally invasive procedures, infection-resistant technologies, and personalized catheter solutions will drive innovation. Integration of smart technology into catheter designs presents opportunities for real-time patient monitoring and improved clinical outcomes.

The aging global population and increasing prevalence of chronic conditions will further sustain demand for durable, comfortable, and effective catheter solutions. Companies that prioritize technological advancement, innovation, and responsiveness to healthcare trends are likely to capture significant market share.

In conclusion, the silicone-based catheter market is at a pivotal juncture, driven by advancements in technology and evolving healthcare priorities. The focus on minimally invasive procedures, infection control, and personalized medical solutions will continue to shape the future of this sector. Companies that embrace these trends and invest in cutting-edge technologies are well-positioned to thrive in this dynamic and evolving market landscape.

Market Risk

Risk Factors and Disruption Threats in the Silicone Based Catheters Market

Executive Framing

The silicone-based catheter market, projected to extend into 2033, is currently navigating a landscape marked by structural constraints and market impacts that raise moderate levels of risk. These constraints are shaped by demographic shifts, healthcare practices, and the inherent vulnerabilities associated with catheter use. As the global population ages, with an increasing proportion over 60, the demand for silicone-based catheters is expected to rise. This demographic trend introduces specific risks tied to older age and prolonged catheterization, both of which are associated with increased incidences of bacteriuria and urinary tract infections. This context demands a strategic examination of how these risks affect market dynamics, pricing power, and demand elasticity.

The risk dimension of this market is further underscored by the operational vulnerabilities that arise from the use of catheters. The frequent occurrence of catheter-associated urinary tract infections (CAUTIs), especially in critical care units where the prevalence of indwelling catheters is high, presents a significant challenge. These infections not only pose health risks but also impact operational resilience, as healthcare facilities must allocate resources to manage and mitigate these infections. The ability of market players to navigate these risks effectively will likely determine their competitive positioning and market share in the coming years.

Current Market Reality

The current landscape of the silicone-based catheter market is shaped by a confluence of risk factors and mitigation strategies. The high prevalence of indwelling urinary catheters in critical care units highlights the structural dependencies and vulnerabilities inherent in current healthcare practices. This prevalence not only increases the risk of CAUTIs but also underscores the reliance on silicone-based solutions, given their superiority over traditional latex catheters in terms of biocompatibility and lower allergenic potential.

The market is also witnessing a shift in healthcare protocols aimed at reducing infection rates and improving patient outcomes. Periodic in-service training for healthcare personnel has emerged as a critical mitigation strategy, equipping staff with the knowledge to minimize catheter use and manage duration effectively. Moreover, the consideration of closed versus open drainage systems is gaining traction, with evidence suggesting that closed systems may reduce infection rates by minimizing exposure to potential pathogens.

Entities such as B. Braun have been proactive in addressing these risks through innovation and strategic acquisitions. The launch of the Clik-FIX® Epidural/Peripheral Nerve Block Catheter Securement Device and the acquisition of the Clik-FIX portfolio reflect a commitment to enhancing securement and reducing the risk of catheter migration and associated complications. These actions align with broader industry trends towards developing infection-resistant designs, which are critical in mitigating the risk of CAUTIs.

Key Signals And Evidence

- Age-related risk factor: individuals over 60 years are more susceptible to catheter-associated complications.

- Longer catheterization is directly associated with higher levels of bacteriuria—a precursor to urinary tract infections.

- High prevalence of indwelling urinary catheters in critical care units increases risk exposure and operational challenges.

- FDA approvals, such as Cook Medical’s Advance Evero™ 18 Everolimus-Coated PTA Balloon Catheter, indicate ongoing innovation in catheter technology.

- Increased adoption of silicone Foley catheters over latex alternatives underscores the market’s shift toward safer, biocompatible materials.

These signals collectively highlight the importance of infection-resistant designs, robust training programs for healthcare personnel, and technological innovation in shaping market strategy and operational resilience.

Strategic Implications

- Prioritize innovation and quality improvement to maintain competitive advantage and market share.

- Develop infection-resistant designs and implement robust training programs to mitigate CAUTI risks.

- Address the needs of an aging population by creating age-appropriate care protocols and products.

- Invest in silicone Foley catheters to leverage their superior biocompatibility and lower allergenic potential.

- Balance pricing strategies with product value to reflect enhanced safety and reduced infection risk.

Companies must navigate the complex interplay of demographic trends, healthcare practices, and operational vulnerabilities, ensuring that their strategic actions align with market realities and patient safety requirements.

Forward Outlook

Looking ahead, the silicone-based catheter market is poised for significant growth, driven by demographic trends, technological advancements, and increasing demand for infection-resistant solutions. However, the market’s trajectory will be shaped by the ability of stakeholders to navigate the complex web of risks and structural constraints that characterize this landscape.

In the near-to-medium term, continued emphasis on R&D investments and innovation will be essential as companies strive to address the high incidence of CAUTIs and improve patient outcomes. Development of infection-resistant designs and securement solutions will reduce risks associated with catheter use and enhance operational resilience. Increasing adoption of silicone Foley catheters over latex alternatives will likely drive market growth, given their superior biocompatibility and reduced risk of allergic reactions.

The aging population will continue to influence market dynamics, presenting both opportunities and challenges for stakeholders. Companies must remain vigilant in assessing these trends’ impact on strategic positioning, ensuring offerings meet evolving market needs. Additionally, ongoing focus on quality improvement and training programs for healthcare personnel will be critical in maintaining market share and operational resilience amidst structural constraints.

In conclusion, the silicone-based catheter market offers significant growth potential, but stakeholders must navigate a complex web of risks and constraints to capitalize on these opportunities. By prioritizing innovation, quality improvement, and strategic adaptation to demographic trends, market participants can position themselves for success in the coming years. The ability to anticipate and respond to these challenges will be critical in shaping the trajectory of the silicone-based catheter market from 2026 to 2033.

Regulatory Landscape

Regulatory and Policy Landscape of the Silicone Based Catheters Market

Executive Framing

In the rapidly evolving landscape of medical devices, the regulatory and policy environment surrounding silicone-based catheters plays a critical role in shaping market dynamics. As these medical devices become increasingly integral to patient care, understanding the regulatory framework is crucial for manufacturers, healthcare providers, and policymakers. This environment influences everything from market entry barriers and innovation timelines to competitive behavior and cost structures. The period from 2026 to 2033 is set to be transformative for this market, requiring stakeholders to navigate complex regulatory landscapes that impact product development, approval processes, and market competition.

The significance of this dimension lies in its capacity to dictate the pace and direction of market transformation. Regulatory compliance, FDA approvals, and adherence to international standards such as ISO 20857 are not merely procedural hurdles but strategic imperatives that can determine the success or failure of new product introductions. As the demand for safer and more efficient medical devices grows, driven by factors such as an aging population and increasing prevalence of chronic illnesses, the regulatory environment will be a decisive factor in shaping the future of silicone-based catheters. The focus on safety, efficacy, and innovation underscores the importance of understanding and anticipating regulatory changes.

Current Market Reality

The current regulatory landscape for silicone-based catheters is characterized by a complex web of standards and approvals that manufacturers must navigate to bring their products to market. Key regulations, such as 21 CFR 177.2600 and 21 CFR 876.5130, set stringent requirements for the materials used in these devices and their performance standards. These regulations ensure that silicone-based catheters meet safety and efficacy benchmarks, reducing the risk of adverse patient outcomes.

The U.S. Food and Drug Administration (FDA) is a pivotal regulatory body in this sector, responsible for premarket notifications (510(k)) and approvals that dictate which products can be commercially distributed. The FDA’s role in approving antiseptic preparations and ensuring compliance with guidelines for preventing intravascular catheter-related infections is crucial for maintaining high safety standards in the market. Additionally, the Centers for Disease Control and Prevention (CDC) and the Joint Commission on Accreditation of Healthcare Organizations (JCAHO) provide evidence-based recommendations and performance indicators that further influence market practices.

In recent developments, companies such as Cook Medical and B. Braun Medical have been active in the market, with Cook Medical receiving FDA approval for its Advance Evero™ 18 Everolimus-Coated PTA Balloon Catheter and B. Braun launching its Clik-FIX® Epidural/Peripheral Nerve Block Catheter Securement Device. These actions highlight the ongoing innovation and adaptation within the industry to meet regulatory requirements and consumer needs.

The current market reality is also shaped by international standards like ISO 20857, which provide a framework for sterilization of healthcare products, ensuring that manufacturers adhere to globally recognized safety protocols. Compliance with these standards not only facilitates international trade but also instills confidence in healthcare providers and patients regarding the safety and reliability of silicone-based catheters.

Key Signals And Evidence

- FDA approval for antiseptic preparations emphasizes infection control in catheter use, encouraging innovation in integrated antiseptic technologies.

- Premarket notification (510(k)) requires manufacturers to demonstrate substantial equivalence to legally marketed devices, ensuring safety and efficacy.

- Regulations such as 21 CFR 177.2600 and 21 CFR 876.5130 set benchmarks for materials and performance standards in catheter manufacturing.

- Guidance for Content of Premarket Notifications for Conventional and Antimicrobial Foley Catheters provides a structured framework for device submissions.

- Conventional Foley Catheters – Performance Criteria for Safety and Performance Based Pathway outlines performance expectations and simplifies the approval process.

These regulatory signals indicate a market driven by stringent safety standards, encouraging manufacturers to leverage compliance as a strategic tool for innovation and competitive advantage.

Strategic Implications

- Navigate FDA approval and 510(k) pathways efficiently to reduce time to market and enhance competitive positioning.

- Invest in R&D to meet regulatory requirements for antiseptic preparations and develop innovative, high-quality catheter solutions.

- Ensure compliance with 21 CFR standards and ISO 20857 to build trust with healthcare providers and enable international market access.

- Use regulatory adherence as a differentiator to strengthen reputation and demonstrate commitment to patient safety and efficacy.

- Integrate regulatory insights into strategic planning to anticipate changes and maintain alignment with evolving standards.

Forward Outlook

Looking towards the forecast period of 2026 to 2033, the regulatory landscape for silicone-based catheters is likely to continue evolving. The increasing emphasis on safety and efficacy will drive further innovation in product design and development. Manufacturers will need to remain agile, adapting to changes in regulatory requirements and leveraging these changes to their advantage.

The potential for product recalls due to safety concerns underscores the importance of maintaining rigorous quality control processes. Companies that can demonstrate a commitment to continuous improvement and safety will be better positioned to retain the trust of healthcare providers and patients alike.

Furthermore, the growing focus on infection-resistant designs will likely spur increased investment in R&D. Companies that can develop innovative solutions to address infection risks will find themselves at the forefront of the market. Partnerships with academic institutions and research organizations, such as the Danish Technical University for wireless monitoring, highlight opportunities for collaboration and innovation in next-generation products.

In conclusion, the regulatory and policy environment for silicone-based catheters is a critical determinant of market dynamics. Companies that can effectively navigate this landscape, leveraging regulatory requirements as a strategic tool for innovation and differentiation, will be well-positioned to capitalize on emerging opportunities. As the market continues to evolve, stakeholders must remain vigilant, adapting their strategies to align with regulatory changes and ensuring that their products meet the highest standards of safety and efficacy.