Global Virus Testing Kits Market Report, Size and Forecast 2026-2033

Global Virus Testing Kits Market Report Size and Forecast 2026???2033

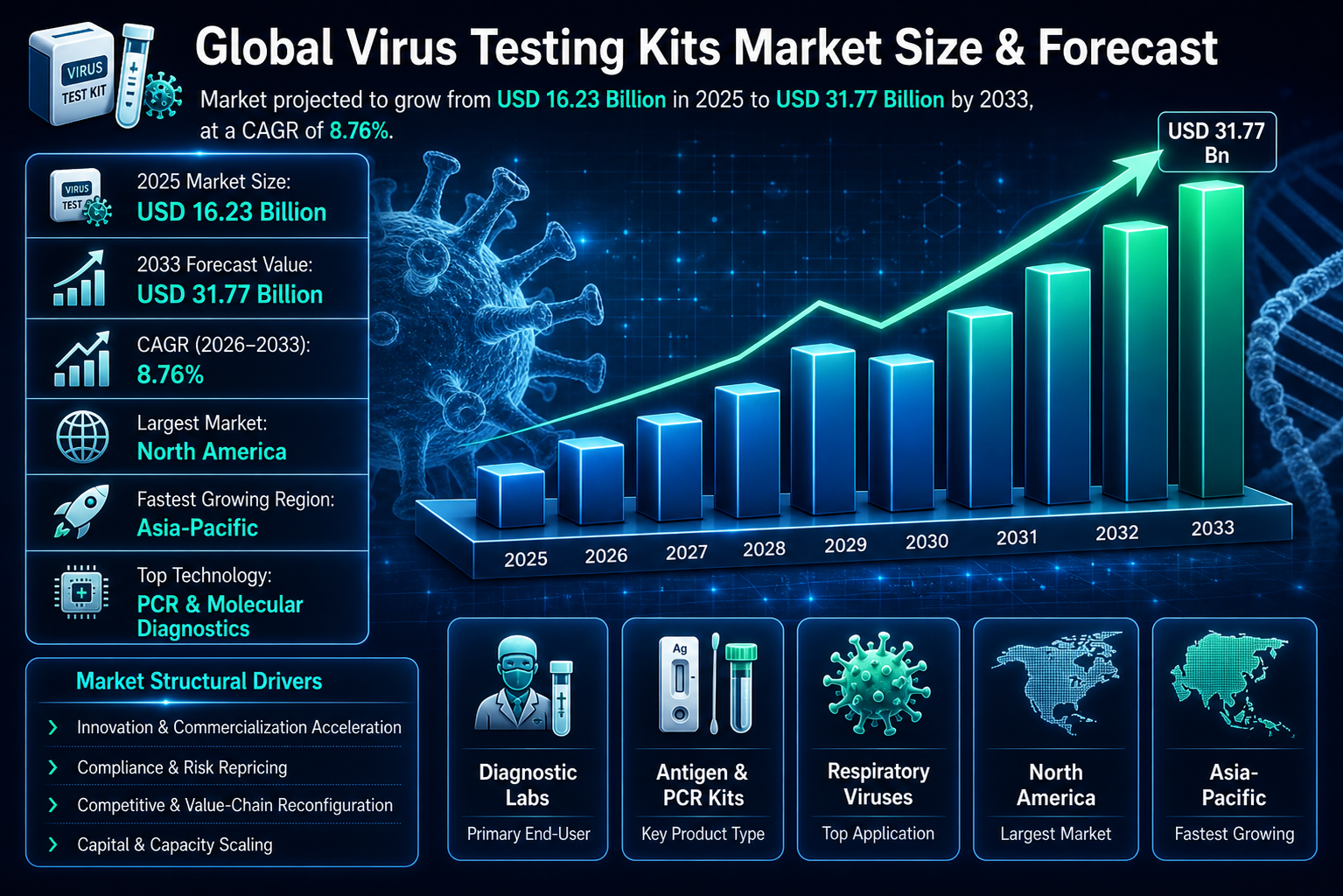

Market Forecast Snapshot (2025???2033)

| Metric | Value |

|---|---|

| Market Size (2025) | USD 16.23 Billion |

| Market Size (2033) | USD 31.77 Billion |

| CAGR (2026???2033) | ~8.76% |

| Largest Region | North America |

| Fastest Growing Region | Asia-Pacific |

| Leading Segment | Molecular Diagnostic Kits |

| Key Trend | Rapid & decentralized testing |

Market Size & Forecast

The Global Virus Testing Kits Market is projected to grow from USD 16.23 billion in 2025 to USD 31.77 billion by 2033, expanding at a CAGR of 8.76% during the forecast period. This growth is driven by increasing global prevalence of viral infections, rising awareness of infectious disease diagnostics, and the need for rapid, accurate, and decentralized testing solutions. The post-pandemic healthcare environment has significantly strengthened diagnostic infrastructure, accelerating adoption across hospitals, laboratories, and home-based settings. Advancements in molecular diagnostics, antigen testing, and point-of-care technologies are enabling faster turnaround times and improved accuracy, supporting large-scale screening and real-time disease monitoring.Market Overview

The Global Virus Testing Kits Market represents a critical segment within the in vitro diagnostics (IVD) ecosystem, focused on detecting viral pathogens across clinical, laboratory, and consumer environments. The market is highly fragmented with strong competitive intensity, characterized by continuous innovation, regulatory evolution, and strategic partnerships. Leading players such as Abbott Laboratories, Roche Diagnostics, Siemens Healthineers, and Thermo Fisher Scientific are actively expanding their diagnostic portfolios through acquisitions, collaborations, and technology integration. Technological advancements???including PCR, antigen, serology, and isothermal amplification???are significantly improving test performance and enabling decentralized testing models such as home diagnostics and point-of-care solutions. Regulatory frameworks from agencies such as the FDA and CMS continue to shape product development, approval pathways, and reimbursement structures, influencing overall market dynamics.Key Drivers of Market Growth

Rising Burden of Infectious Diseases Increasing incidence of respiratory, blood-borne, and emerging viral infections is sustaining long-term demand. Expansion of Rapid & Point-of-Care Testing Growing need for faster diagnostics is driving adoption of portable and decentralized testing solutions. Technological Advancements in Diagnostics Innovations in PCR, lateral flow assays, and biosensors are improving speed, sensitivity, and accessibility. Strengthening Public Health Infrastructure Government investments in screening programs and pandemic preparedness are boosting demand. Growth of Home-Based Testing Consumer preference for convenient, self-administered diagnostics is accelerating market expansion.Market Segmentation

By End User

- Hospitals & Clinics

- Diagnostic Laboratories

- Research & Academic Institutions

By Virus Type

- Respiratory Virus Testing Kits (COVID-19, Influenza)

- Blood-Borne Virus Testing Kits (HIV, Hepatitis)

- Emerging Virus Testing Kits (Zika, Ebola)

By Application

- Clinical Diagnosis

- Blood Screening

- Public Health Screening Programs

By Product Type

- Molecular Diagnostic Kits (PCR, NAAT)

- Antigen Test Kits

- Serology Test Kits

By Testing Setting

- Laboratory-Based Testing

- Point-of-Care Testing

- Home-Based Testing

Regional Insights

North America ??? Largest Market Driven by advanced healthcare infrastructure, high testing capacity, and strong presence of leading diagnostic companies. Europe ??? Regulatory-Driven Market Strong public health systems and stringent quality standards support widespread adoption. Asia-Pacific ??? Fastest Growing Region Growth fueled by rising healthcare investments, large population base, and increasing disease awareness. Latin America Steady growth supported by improving healthcare access and diagnostic capabilities. Middle East & Africa Emerging market driven by increasing disease burden and healthcare infrastructure development.Competitive Landscape

The market is highly competitive with both global leaders and emerging players focusing on innovation, scalability, and accessibility. Key companies include:- Abbott Laboratories

- Roche Diagnostics

- Siemens Healthineers

- Thermo Fisher Scientific

- Danaher Corporation

Strategic Insights & Trends

- Shift toward decentralized and home-based diagnostics

- Increasing integration of AI in diagnostic workflows

- Expansion of public-private partnerships for disease surveillance

- Focus on rapid response capabilities for future outbreaks

- Growth in multiplex testing platforms for detecting multiple pathogens simultaneously

Why This Market Matters

- Critical for infectious disease detection and control

- Enables rapid outbreak response and public health management

- High recurring demand due to consumable-based model

- Supports global healthcare preparedness and resilience

- Integral to modern diagnostics and epidemiological surveillance

Final Takeaway

The Global Virus Testing Kits Market is evolving into a core pillar of global healthcare infrastructure. Driven by technological innovation, regulatory support, and increasing disease burden, the market is transitioning toward faster, more accessible, and decentralized diagnostic solutions. Future growth will be shaped by advancements in molecular diagnostics, expansion of home-based testing, and stronger global preparedness for infectious diseases. Companies that prioritize innovation, scalability, and accessibility will lead this high-growth market through 2033.Table of Contents

Table of Contents

- 1. Executive Summary

- 1.1 Market Forecast Snapshot (2026-2033)

- 1.2 Global Market Size & CAGR Analysis

- 1.3 Largest & Fastest-Growing Segments

- 1.4 Region-Level Leadership & Growth Trends

- 1.5 Key Market Drivers

- 1.6 Competitive Landscape Overview

- 1.7 Strategic Outlook Through 2033

- 2. Introduction & Market Overview

- 2.1 Definition of the Virus Testing Kits Market

- 2.2 Scope of the Study

- 2.3 Industry Evolution & Market Development

- 2.4 Supply Chain & Distribution Infrastructure

- 2.5 Impact of Consumer Trends

- 2.6 Sustainability & Regulatory Landscape

- 2.7 Technology & Innovation Landscape

- 3. Research Methodology

- 3.1 Primary Research

- 3.2 Secondary Research

- 3.3 Market Size Estimation Model

- 3.4 Forecast Assumptions (2026-2033)

- 3.5 Data Validation & Triangulation

- 4. Market Dynamics

- 4.1 Drivers

- 4.1.1 Increasing Demand Drivers

- 4.1.2 Industry Innovation Drivers

- 4.1.3 Market Expansion Factors

- 4.1.4 Regulatory or Policy Support

- 4.1.5 Technology Adoption Drivers

- 4.2 Restraints

- 4.2.1 Cost Constraints

- 4.2.2 Infrastructure Limitations

- 4.2.3 Regulatory Challenges

- 4.2.4 Market Awareness Barriers

- 4.3 Opportunities

- 4.3.1 Emerging Market Opportunities

- 4.3.2 Product Innovation Opportunities

- 4.3.3 Technology Expansion Opportunities

- 4.3.4 Supply Chain Improvements

- 4.4 Challenges

- 4.4.1 Supply Chain Complexity

- 4.4.2 Quality Control & Compliance

- 4.4.3 Regional Market Fragmentation

- 4.4.4 Competitive Pressure

- 4.1 Drivers

- 5. Virus Testing Kits Market Analysis (USD Billion), 2026-2033

- 5.1 Market Size Overview

- 5.2 CAGR Analysis

- 5.3 Regional Revenue Distribution

- 5.4 Segment Revenue Analysis

- 5.5 Distribution Channel Analysis

- 5.6 Consumer Impact Analysis

- 6. Market Segmentation (USD Billion), 2026-2033

- 6.1 By End User

- 6.1.1 Diagnostic Laboratories

- 6.1.1.1 Independent Testing Laboratories

- 6.1.1.1.1 High Volume Diagnostic Labs

- 6.1.1.1.1.1 Molecular Diagnostics Laboratories

- 6.1.1.1.1.2 Infectious Disease Reference Labs

- 6.1.1.1.1 High Volume Diagnostic Labs

- 6.1.1.1 Independent Testing Laboratories

- 6.1.2 Hospitals and Clinics

- 6.1.2.1 Hospital Diagnostic Laboratories

- 6.1.2.1.1 Clinical Viral Testing Facilities

- 6.1.2.1.1.1 Infectious Disease Diagnostic Units

- 6.1.2.1.1.2 Hospital Laboratory Testing Centers

- 6.1.2.1.1 Clinical Viral Testing Facilities

- 6.1.2.1 Hospital Diagnostic Laboratories

- 6.1.3 Research Institutions

- 6.1.3.1 Virology Research Laboratories

- 6.1.3.1.1 Viral Pathogen Research Testing

- 6.1.3.1.1.1 Academic Virology Laboratories

- 6.1.3.1.1.2 Epidemiology Research Centers

- 6.1.3.1.1 Viral Pathogen Research Testing

- 6.1.3.1 Virology Research Laboratories

- 6.1.1 Diagnostic Laboratories

- 6.2 By Virus Type

- 6.2.1 Blood-Borne Virus Testing Kits

- 6.2.1.1 Hepatitis Virus Testing Kits

- 6.2.1.1.1 Hepatitis B Virus Testing Kits

- 6.2.1.1.1.1 HBV DNA Detection Kits

- 6.2.1.1.1.2 Hepatitis B Antigen Test Kits

- 6.2.1.1.2 Hepatitis C Virus Testing Kits

- 6.2.1.1.2.1 HCV RNA Detection Kits

- 6.2.1.1.2.2 HCV Antibody Detection Kits

- 6.2.1.1.1 Hepatitis B Virus Testing Kits

- 6.2.1.2 Human Immunodeficiency Virus (HIV) Testing Kits

- 6.2.1.2.1 HIV Antibody Detection Kits

- 6.2.1.2.1.1 Rapid HIV Screening Kits

- 6.2.1.2.1.2 Laboratory HIV ELISA Kits

- 6.2.1.2.1 HIV Antibody Detection Kits

- 6.2.1.1 Hepatitis Virus Testing Kits

- 6.2.2 Emerging Virus Testing Kits

- 6.2.2.1 Arbovirus Testing Kits

- 6.2.2.1.1 Dengue Virus Testing Kits

- 6.2.2.1.1.1 Dengue NS1 Antigen Test Kits

- 6.2.2.1.1.2 Dengue IgM and IgG Antibody Kits

- 6.2.2.1.2 Zika Virus Testing Kits

- 6.2.2.1.2.1 Zika PCR Detection Kits

- 6.2.2.1.2.2 Zika Antibody Detection Kits

- 6.2.2.1.1 Dengue Virus Testing Kits

- 6.2.2.2 Hemorrhagic Fever Virus Testing Kits

- 6.2.2.2.1 Ebola Virus Detection Kits

- 6.2.2.2.1.1 PCR Ebola Virus Test Kits

- 6.2.2.2.1.2 Rapid Ebola Detection Kits

- 6.2.2.2.1 Ebola Virus Detection Kits

- 6.2.2.1 Arbovirus Testing Kits

- 6.2.3 Respiratory Virus Testing Kits

- 6.2.3.1 Coronavirus Testing Kits

- 6.2.3.1.1 SARS-CoV-2 Detection Kits

- 6.2.3.1.1.1 COVID-19 PCR Diagnostic Kits

- 6.2.3.1.1.2 COVID-19 Rapid Antigen Testing Kits

- 6.2.3.1.1 SARS-CoV-2 Detection Kits

- 6.2.3.2 Influenza Virus Testing Kits

- 6.2.3.2.1 Influenza A Testing Kits

- 6.2.3.2.1.1 PCR Influenza Detection Kits

- 6.2.3.2.1.2 Rapid Flu Antigen Test Kits

- 6.2.3.2.2 Influenza B Testing Kits

- 6.2.3.2.2.1 Laboratory Influenza Diagnostic Kits

- 6.2.3.2.2.2 Point-of-Care Flu Testing Kits

- 6.2.3.2.1 Influenza A Testing Kits

- 6.2.3.1 Coronavirus Testing Kits

- 6.2.1 Blood-Borne Virus Testing Kits

- 6.3 By Application

- 6.3.1 Blood Screening

- 6.3.1.1 Blood Donation Testing

- 6.3.1.1.1 Blood Safety Screening

- 6.3.1.1.1.1 Viral Pathogen Screening in Blood Banks

- 6.3.1.1.1.2 Transfusion Safety Testing

- 6.3.1.1.1 Blood Safety Screening

- 6.3.1.1 Blood Donation Testing

- 6.3.2 Clinical Diagnosis

- 6.3.2.1 Infectious Disease Detection

- 6.3.2.1.1 Hospital Diagnostic Testing

- 6.3.2.1.1.1 Viral Infection Confirmation Testing

- 6.3.2.1.1.2 Acute Viral Disease Diagnosis

- 6.3.2.1.1 Hospital Diagnostic Testing

- 6.3.2.1 Infectious Disease Detection

- 6.3.3 Screening Programs

- 6.3.3.1 Population Screening

- 6.3.3.1.1 Public Health Surveillance Testing

- 6.3.3.1.1.1 Mass Viral Screening Programs

- 6.3.3.1.1.2 Epidemiological Monitoring Programs

- 6.3.3.1.1 Public Health Surveillance Testing

- 6.3.3.1 Population Screening

- 6.3.1 Blood Screening

- 6.4 By Product Type

- 6.4.1 Antigen Test Kits

- 6.4.1.1 Laboratory Antigen Detection Kits

- 6.4.1.1.1 Immunochromatographic Assay Kits

- 6.4.1.1.1.1 Clinical Antigen Detection Kits

- 6.4.1.1.1.2 High Throughput Antigen Testing Kits

- 6.4.1.1.1 Immunochromatographic Assay Kits

- 6.4.1.2 Rapid Antigen Test Kits

- 6.4.1.2.1 Lateral Flow Immunoassay Kits

- 6.4.1.2.1.1 Rapid Point-of-Care Antigen Detection Kits

- 6.4.1.2.1.2 Home Based Viral Detection Kits

- 6.4.1.2.1 Lateral Flow Immunoassay Kits

- 6.4.1.1 Laboratory Antigen Detection Kits

- 6.4.2 Molecular Diagnostic Test Kits

- 6.4.2.1 Isothermal Amplification Test Kits

- 6.4.2.1.1 Loop Mediated Isothermal Amplification (LAMP) Kits

- 6.4.2.1.1.1 Rapid Viral Detection Kits

- 6.4.2.1.1.2 Point-of-Care Molecular Testing Kits

- 6.4.2.1.2 Recombinase Polymerase Amplification Kits

- 6.4.2.1.2.1 Portable Viral Testing Kits

- 6.4.2.1.2.2 Rapid Field Diagnostic Kits

- 6.4.2.1.1 Loop Mediated Isothermal Amplification (LAMP) Kits

- 6.4.2.2 Polymerase Chain Reaction (PCR) Test Kits

- 6.4.2.2.1 Real-Time PCR Test Kits

- 6.4.2.2.1.1 Multiplex Viral Detection PCR Kits

- 6.4.2.2.1.2 High Sensitivity Viral RNA Detection Kits

- 6.4.2.2.2 Reverse Transcription PCR (RT-PCR) Test Kits

- 6.4.2.2.2.1 RNA Virus Detection Kits

- 6.4.2.2.2.2 Quantitative Viral Load Detection Kits

- 6.4.2.2.1 Real-Time PCR Test Kits

- 6.4.2.1 Isothermal Amplification Test Kits

- 6.4.3 Serology Test Kits

- 6.4.3.1 Antibody Detection Kits

- 6.4.3.1.1 IgG Antibody Detection Kits

- 6.4.3.1.1.1 Past Infection Identification Kits

- 6.4.3.1.1.2 Immunity Monitoring Test Kits

- 6.4.3.1.2 IgM Antibody Detection Kits

- 6.4.3.1.2.1 Early Stage Viral Infection Detection Kits

- 6.4.3.1.2.2 Acute Infection Screening Kits

- 6.4.3.1.1 IgG Antibody Detection Kits

- 6.4.3.2 ELISA Test Kits

- 6.4.3.2.1 Enzyme Linked Immunosorbent Assay Kits

- 6.4.3.2.1.1 Laboratory Viral Antibody Detection Kits

- 6.4.3.2.1.2 High Throughput ELISA Viral Testing Kits

- 6.4.3.2.1 Enzyme Linked Immunosorbent Assay Kits

- 6.4.3.1 Antibody Detection Kits

- 6.4.1 Antigen Test Kits

- 6.5 By Testing Setting

- 6.5.1 Home Based Testing

- 6.5.1.1 Self Testing Kits

- 6.5.1.1.1 Home Viral Diagnostic Kits

- 6.5.1.1.1.1 At Home Rapid Antigen Test Kits

- 6.5.1.1.1.2 Self Administered Viral Detection Kits

- 6.5.1.1.1 Home Viral Diagnostic Kits

- 6.5.1.1 Self Testing Kits

- 6.5.2 Laboratory Based Testing

- 6.5.2.1 Centralized Diagnostic Laboratories

- 6.5.2.1.1 High Throughput Viral Testing

- 6.5.2.1.1.1 Automated PCR Testing Systems

- 6.5.2.1.1.2 Clinical Viral Diagnostic Laboratories

- 6.5.2.1.1 High Throughput Viral Testing

- 6.5.2.1 Centralized Diagnostic Laboratories

- 6.5.3 Point of Care Testing

- 6.5.3.1 Hospital Based Rapid Testing

- 6.5.3.1.1 Emergency Viral Screening

- 6.5.3.1.1.1 Rapid Infectious Disease Detection Kits

- 6.5.3.1.1.2 Bedside Viral Diagnostic Systems

- 6.5.3.1.1 Emergency Viral Screening

- 6.5.3.1 Hospital Based Rapid Testing

- 6.5.1 Home Based Testing

- 6.1 By End User

- 7. Market Segmentation by Geography

- 7.1 North America

- 7.2 Europe

- 7.3 Asia-Pacific

- 7.4 Latin America

- 7.5 Middle East & Africa

- 8. Competitive Landscape

- 8.1 Market Share Analysis

- 8.2 Product Portfolio Benchmarking

- 8.3 Product Positioning Mapping

- 8.4 Supply Chain & Distribution Partnerships

- 8.5 Competitive Intensity & Differentiation

- 9. Company Profiles

- 10. Strategic Intelligence & Pheonix AI Insights

- 10.1 Pheonix Demand Forecast Engine

- 10.2 Supply Chain & Infrastructure Analyzer

- 10.3 Technology & Innovation Tracker

- 10.4 Product Development Insights

- 10.5 Automated Porter’s Five Forces Analysis

- 11. Future Outlook & Strategic Recommendations

- 11.1 Emerging Market Expansion

- 11.2 Technology Innovation Strategies

- 11.3 Product Development Roadmap

- 11.4 Regional Expansion Strategies

- 11.5 Long-Term Market Outlook (2033+)

- 12. Appendix

- 13. About Pheonix Research

- 14. Disclaimer

Competitive Landscape

Competitive Landscape of the Global Virus Testing Kits Market

Executive Framing

In the rapidly evolving landscape of virus testing kits, the competitive intensity and market structure have become critical dimensions that shape strategic decisions and market outcomes. As the world continues to grapple with the persistent threat of viral outbreaks, the demand for reliable and rapid diagnostic solutions has surged, prompting companies to reassess their competitive strategies. These dynamics are not just a response to immediate healthcare needs but are also reflective of broader shifts in market structure that carry significant implications for long-term industry stability and growth.

The virus testing kits market is characterized by high competitive intensity and a fragmented market structure. The absence of tier 1 players highlights a landscape where numerous entities vie for market share, fostering a highly competitive environment. This fragmentation is driven by several factors, including technological advancements, evolving consumer preferences towards home-based testing, and the heightened awareness of viral threats due to recent pandemics. As companies navigate this complex terrain, strategic moves such as partnerships, acquisitions, and product portfolio expansions have emerged as pivotal tactics to secure competitive advantages. Understanding these market dynamics is crucial for stakeholders looking to position themselves effectively in this high-stakes arena.

Current Market Reality

Presently, the virus testing kits market is witnessing a confluence of factors that underscore its fragmented nature and high competitive intensity. The landscape is populated by a diverse array of companies, each employing distinct strategies to capture market share. Notable entities such as Abbott Laboratories, Roche Diagnostics, Siemens Healthineers, and Thermo Fisher Scientific are actively shaping the market through strategic initiatives and product innovations. For instance, Abbott Laboratories recently secured a $150 million contract, which not only boosts its revenue stream but also solidifies its position in the competitive landscape.

Roche Diagnostics, on the other hand, has been proactive in forging collaborations with healthcare systems, facilitating broader distribution and adoption of its diagnostic solutions. These collaborations are instrumental in navigating the fragmented market, as they provide Roche with access to new customer segments and enhance its competitive positioning.

Thermo Fisher Scientific’s acquisition of PPD, a leading clinical research organization, exemplifies the strategic moves companies are making to enhance their market presence. This acquisition allows Thermo Fisher to integrate clinical research capabilities into its operations, thereby offering a more comprehensive suite of services to its clients. Such strategic acquisitions are indicative of the broader trend towards consolidation, as companies seek to strengthen their competitive positions in a highly fragmented market.

Moreover, the market is witnessing significant product innovation, as companies strive to meet the rising demand for rapid and accurate testing solutions. For example, the FDA approval for Roche’s cobas 6800/8800 systems marks a significant milestone, enabling the company to offer high-throughput testing capabilities that are crucial in managing large-scale viral outbreaks. Similarly, the launch of HiGenoMB RT-PCR kits to detect the JN.1 variant of SARS-CoV-2 reflects the market’s responsiveness to emerging viral threats and the need for continuous innovation in diagnostic technologies.

Key Signals And Evidence

The current landscape of the virus testing kits market is shaped by a variety of key signals that highlight both the challenges and opportunities within the industry. One of the most significant developments is the public-private partnership between PerkinElmer, Inc. and the California government, which aims to provide up to 150,000 new daily tests. This move underscores the increasing collaboration between governmental bodies and private companies to enhance testing capabilities and address public health needs swiftly. Such partnerships are instrumental in scaling up testing infrastructure, ensuring that demand is met during critical periods of viral outbreaks.

Additionally, the launch of HiGenoMB RT-PCR kits to detect the JN.1 variant of SARS-CoV-2 represents a crucial step in addressing the ongoing demand for COVID-19 detection kits. The introduction of these kits not only caters to the immediate need for variant-specific testing but also highlights the rapid innovation and adaptability of companies in responding to emerging viral threats. This agility is a key competitive advantage in a fragmented market where differentiation can significantly impact market share.

Moreover, strategic acquisitions and collaborations continue to reshape the competitive landscape. Danaher Corp.’s acquisition of a diagnostics startup for $500.00 million is a testament to the ongoing consolidation efforts within the industry. Such acquisitions enable companies to expand their technological capabilities and product portfolios, thereby strengthening their competitive positioning. Similarly, the FDA approval for cobas 6800/8800 systems by Roche exemplifies the importance of regulatory endorsements in enhancing market credibility and facilitating broader adoption of testing solutions.

The acquisition of Luminex by DiaSorin in April 2021 further exemplifies the strategic moves companies are making to bolster their technological prowess and market penetration. This acquisition allows DiaSorin to integrate Luminex’s advanced multiplexing technologies into its offerings, thereby enhancing its value proposition in the market.

Furthermore, Thermo Fisher Scientific’s launch of a Modular Closed Cell Processing System for Cell Therapy Manufacturing highlights the diversification strategies companies are adopting to remain competitive. This move not only broadens Thermo Fisher’s product portfolio but also positions the company as a leader in the evolving field of cell therapy manufacturing.

Lastly, the increased public and private funding towards infectious diseases research signifies a growing recognition of the importance of diagnostics in disease management. This influx of funding is likely to fuel further innovation and development within the virus testing kits market, providing companies with the resources needed to develop cutting-edge solutions that address both current and future healthcare challenges.

Strategic Implications

The strategic implications of these developments are profound, as they signal a shift towards a more integrated and collaborative approach to diagnostics. For companies operating in this space, the ability to form strategic partnerships and collaborations will be crucial in maintaining a competitive edge. By aligning with governmental bodies and leveraging public-private partnerships, companies can enhance their testing capabilities and expand their market reach. This collaborative approach not only addresses immediate public health needs but also positions companies as key players in the long-term development of diagnostic infrastructure.

Furthermore, the focus on rapid innovation and adaptability is likely to drive a wave of product diversification and portfolio expansion. Companies that can swiftly respond to emerging viral threats with innovative solutions, such as the HiGenoMB RT-PCR kits, will be better positioned to capture market share and secure a dominant position in the industry. This emphasis on agility and innovation also underscores the importance of strategic acquisitions, as they enable companies to integrate new technologies and capabilities into their offerings, thereby strengthening their competitive positioning.

Regulatory approvals, such as the FDA endorsement of cobas 6800/8800 systems, play a pivotal role in shaping market dynamics. These approvals not only validate the efficacy and reliability of testing solutions but also facilitate their widespread adoption. Companies that can successfully navigate the regulatory landscape and secure such endorsements are likely to gain a significant competitive advantage, as they enhance their credibility and trustworthiness in the eyes of healthcare providers and consumers.

The ongoing consolidation efforts, as evidenced by Danaher Corp.’s acquisition of a diagnostics startup and DiaSorin’s acquisition of Luminex, highlight the importance of scale and technological capabilities in the virus testing kits market. By acquiring smaller, innovative companies, established players can enhance their technological prowess and expand their market presence. This trend towards consolidation is likely to continue as companies seek to strengthen their competitive positioning and capitalize on synergies that enhance operational efficiencies and market reach.

Forward Outlook

Looking ahead, the virus testing kits market is poised for significant transformation as companies continue to navigate the complex interplay of competitive forces, technological advancements, and evolving consumer preferences. The shift towards integrated diagnostics and syndromic testing platforms is likely to gain momentum, as healthcare providers increasingly seek comprehensive solutions that address multiple pathogens effectively. Companies that can successfully integrate these platforms into their product offerings and align with the evolving needs of healthcare providers will be well-positioned to capture a larger share of the market.

The increasing focus on home-based testing kits and point-of-care testing is expected to drive further innovation and development within the industry. As consumers become more proactive in managing their health, the demand for convenient and accessible testing solutions is likely to rise. Companies that can develop user-friendly, reliable, and accurate home-based testing kits will be at the forefront of this trend, capitalizing on the growing interest in personalized medicine and near-patient testing.

Furthermore, the ongoing investment in infectious diseases research and the influx of public and private funding are likely to fuel further advancements in testing technologies. This funding will provide companies with the resources needed to

Value Chain

Value Chain and Supply Chain Dynamics in the Global Virus Testing Kits market

Executive Framing

In the ever-evolving landscape of virus testing kits, the intricacies of the value chain and supply chain evolution are critical to understanding market dynamics from 2026 to 2033. The focus on bottlenecks, power distribution, and margin effects is particularly pertinent, given the unique challenges and opportunities within this sector. This dimension matters now more than ever due to a confluence of factors that have reshaped the operational frameworks and strategic imperatives for stakeholders in the virus testing kits market.

Central to this discussion is the hybrid operational model that combines traditional and modern approaches to virus testing, emphasizing both laboratory-based diagnostics and direct-to-consumer solutions. This model is increasingly significant as the demand for accessible and efficient testing rises globally. The direct-to-consumer distribution structure further complicates the landscape, as it demands robust logistics and regulatory compliance frameworks. The moderate complexity level of the supply chain reflects the diverse range of inputs and outputs involved in producing and distributing virus testing kits, from raw materials to end-user delivery.

Current Market Reality

The current state of the virus testing kits market is defined by several pressing bottlenecks that influence the entire value chain. One of the most significant challenges is the stringent regulatory environment, which dictates the pace of innovation and market entry for new diagnostic technologies. Regulatory uncertainty, particularly concerning adaptive algorithms used in testing kits, poses additional hurdles for companies striving to remain competitive. This uncertainty can delay product launches and increase compliance costs, affecting margins and the overall profitability of firms within the industry.

Another critical bottleneck is the global shortage of skilled molecular technologists. These professionals are essential for the development and deployment of advanced diagnostic solutions. The shortage restricts capacity utilization and slows down the production processes, potentially leading to delays in meeting market demand. Companies like PerkinElmer, Inc., which entered into a public-private partnership with the California government to provide up to 150,000 new daily tests, are directly impacted by this shortage. Their ability to scale operations and maintain service levels is contingent upon access to a skilled workforce.

The high cost of advanced diagnostic technologies also contributes to margin compression and shifts in bargaining power. Companies must navigate these costs while remaining competitive on pricing, as consumers increasingly seek affordable and reliable testing options. This is further compounded by donor-funding cuts disrupting HIV testing in low- and middle-income countries (LMICs), which limits market expansion and reduces financial resources available to invest in new technologies.

Finally, the market is contending with critical shortages of essential components such as plastic consumables, laboratory chemicals, and commercial laboratory equipment. This scarcity affects the supply chain’s complexity level and challenges companies to explore alternative sourcing strategies or risk disruptions in their production schedules. The rise of counterfeit products further complicates these efforts, as companies must ensure the integrity and reliability of their supply chains to maintain consumer trust.

Key Signals And Evidence

Several key signals underscore the current challenges and opportunities within the virus testing kits market. The rapid adoption of molecular point-of-care (POC) PCR platforms reflects a significant shift towards more decentralized and efficient testing solutions. This trend is driven by the need for rapid diagnostics in both clinical and home-based settings, enabling quicker decision-making and treatment interventions. Companies investing in these platforms can gain a competitive edge by offering innovative products that meet the growing demand for convenient testing solutions.

The expansion of wastewater-based viral surveillance is another critical signal, highlighting the increasing integration of environmental monitoring into public health strategies. This approach provides a valuable tool for early detection and tracking of viral outbreaks, offering insights that can inform policy decisions and resource allocation. By investing in technologies that support wastewater surveillance, companies can position themselves as leaders in the evolving landscape of virus detection and management.

The persistent global shortage of skilled molecular technologists continues to be a major constraint, affecting both production capacity and quality assurance. As companies strive to scale their operations in response to rising demand, the availability of trained personnel becomes a limiting factor. This shortage necessitates strategic investments in training programs and partnerships with educational institutions to build a sustainable talent pipeline.

Donor-funding cuts disrupting LMIC HIV testing present a significant challenge to market growth and accessibility. These cuts undermine efforts to expand testing services in regions with high infection rates, potentially leading to unchecked viral spread and increased public health risks. Companies operating in these markets must navigate these funding constraints while advocating for sustainable financing models that support long-term testing initiatives.

Lastly, digital signals such as Google searches for COVID shortage-related terms and Twitter tweets about COVID-related shortages provide real-time insights into consumer concerns and market disruptions. These signals highlight the ongoing challenges in maintaining adequate supplies of testing kits and related materials, underscoring the importance of robust supply chain management and strategic stockpiling.

As the virus testing kits market continues to evolve, stakeholders must carefully navigate these complex dynamics to optimize their operations, maintain competitive advantages, and meet the growing demands of consumers and healthcare providers worldwide.

Strategic Implications

The intricate landscape of virus testing kits presents a myriad of strategic implications for stakeholders, from manufacturers to healthcare providers. The first significant implication is the shifting of bargaining power within the supply chain. The global shortage of skilled molecular technologists has made human capital a pivotal factor in the operational efficiency of testing kit production and application. Companies that can secure and retain such talent will hold a strategic advantage, potentially commanding higher margins due to increased operational efficiency and the ability to meet demand spikes quickly.

This shortage, coupled with the rapid adoption of molecular point-of-care (POC) PCR platforms, signifies a shift towards more decentralized testing solutions. Firms that can innovate and scale these platforms efficiently are likely to capture larger market shares. This shift is supported by the expansion of wastewater-based viral surveillance, which requires robust integration with existing testing frameworks. Companies that can leverage AI-driven automated laboratory workflows will enhance their capacity utilization, thus improving delivery performance and reducing per-test costs, which is crucial for maintaining competitive pricing strategies.

The direct-to-consumer distribution model further alters the power dynamics within the value chain. This model empowers consumers, who now have more choices and greater access to testing solutions. Companies must therefore focus on brand loyalty and customer satisfaction to differentiate themselves in a competitive market. Additionally, the integration of digital health technologies into virus testing kits presents opportunities for enhancing consumer engagement through personalized health insights and seamless user experiences.

Meanwhile, the donor-funding cuts affecting low- and middle-income countries (LMICs) disrupt HIV testing initiatives, highlighting the need for strategic partnerships and diversified funding models. Companies operating in these regions must advocate for sustainable financing models that ensure the continuous supply of essential testing kits. These challenges necessitate strategic alliances, such as the public-private partnership between PerkinElmer, Inc. and the California government, to bolster testing capacities and mitigate supply chain disruptions.

Regulatory uncertainties, particularly concerning adaptive algorithms and the expiration of certain testing requirements, pose risks and opportunities. Companies that can navigate these uncertainties and secure regulatory clearances for novel assays will be better positioned to capitalize on emerging market opportunities. The FDA approval for systems like cobas 6800/8800 underscores the importance of regulatory agility and compliance in gaining market access and consumer trust.

Forward Outlook

Looking ahead to the period from 2026 to 2033, several key trends and potential scenarios will shape the virus testing kits market. The continued expansion of digital health technologies and home-based testing solutions will drive significant changes in consumer expectations and market structures. This evolution will likely necessitate increased investment in digital infrastructures and consumer data protection measures, creating new cost structures and requiring strategic recalibrations.

The potential for government stockpiling of multi-pathogen panels, driven by ongoing public health concerns, could alter demand patterns and create new markets for comprehensive testing solutions. Companies that can anticipate and respond to governmental procurement strategies will secure advantageous positions in these emerging markets. Furthermore, the rising prevalence of viral diseases and growing regulatory clearances for novel assays suggest an expanding market, albeit one that demands strategic foresight and adaptability.

In terms of supply chain dynamics, the persistent global shortage of critical components such as plastic consumables, laboratory chemicals, and commercial laboratory equipment will remain a challenge. Companies must invest in supply chain resilience and diversification to mitigate these risks. Strategic stockpiling and the development of alternative sourcing strategies will be crucial to maintaining operational continuity and meeting market demands.

Finally, the role of social media and digital platforms in shaping consumer perceptions and market trends cannot be understated. Real-time data from Google searches and Twitter tweets about COVID-related shortages provide valuable insights into consumer sentiment and potential supply chain disruptions. Companies that can effectively leverage these insights for agile decision-making will enhance their competitive edge in a rapidly evolving market landscape.

In conclusion, the virus testing kits market is poised for significant transformation over the next decade. Stakeholders must navigate a complex web of supply chain challenges, regulatory landscapes, and evolving consumer preferences to maintain their competitive positions. By strategically addressing these dynamics, companies can optimize their operations, drive innovation, and ultimately deliver better health outcomes in an increasingly interconnected world.

Investment Activity

Investment and Funding Dynamics in the Global Virus Testing Kits Market

Executive Framing

The investment and funding dynamics within the virus testing kits market have become a focal point of strategic interest due to the evolving landscape of global health challenges. The significance of this dimension lies not only in the immediate response to infectious disease outbreaks but also in the long-term strategic allocation of resources that can dictate the pace and direction of market expansion. As we look towards the forecast period of 2026-2033, the investment trend in virus testing kits is discernibly rising, underpinned by high capital intensity and a robust wave of mergers and acquisitions (M&A).

This trend reflects a broader recognition of the critical role that testing plays in public health infrastructure, prompting stakeholders from both the private and public sectors to recalibrate their strategies to capture emerging opportunities in this high-stakes market.

Capital is gravitating towards entities that demonstrate strategic foresight in enhancing testing capacities and expanding market reach. The presence of active investors such as Roche Diagnostics, Abbott Laboratories, and Danaher Corp. underscores the competitive pressures and the collective push towards innovation and geographical expansion. These investments are not merely reactive to current demands but are strategically poised to address future challenges, including the emergence of novel infectious agents and the increasing prevalence of infectious diseases globally.

As such, the strategic allocation of capital is not just about maintaining market position but is increasingly about anticipating and shaping future market dynamics through targeted investments in technology, capacity, and strategic collaborations.

Current Market Reality

Presently, the virus testing kits market is characterized by a dynamic interplay of heightened investment activity and strategic realignments among key industry players. The capital intensity is notably high, driven by the necessity to invest in advanced diagnostic technologies and the expansion of manufacturing capacities. Companies such as Thermo Fisher Scientific, Inc., and Becton, Dickinson and Company are actively engaging in capacity expansion initiatives, which are critical to meet the anticipated demand surge and to maintain a competitive edge in the market.

Recent M&A activity serves as a testament to the strategic consolidation occurring within the industry. Danaher Corp.’s acquisition of a diagnostics startup for $500.00 million exemplifies the aggressive pursuit of innovation and market share through strategic acquisitions. This move not only bolsters Danaher’s technological portfolio but also aligns with the broader industry trend of leveraging M&A to drive growth and enhance product offerings.

Such actions highlight the importance of agility and foresight in capital allocation decisions, as companies seek to optimize their asset portfolios in anticipation of future market shifts.

The strategic themes of geographical expansion and product launches are also pivotal in shaping the current market reality. Companies are increasingly looking to expand their geographical footprints to tap into emerging markets and to mitigate the risks associated with regional market fluctuations. This strategic focus on geographical expansion is further complemented by a surge in product launches, particularly in the realm of affordable point-of-care molecular diagnostics and rapid diagnostic technologies.

These initiatives are crucial for enhancing equitable access to tests and for addressing the growing demand for quick and accurate diagnostic solutions.

The market is also witnessing a concerted effort towards enhancing automation readiness and biosafety measures, driven by the need to streamline operations and ensure safety in the testing processes. These investments are indicative of a broader industry trend towards operational efficiency and risk mitigation, underscoring the strategic importance of aligning capital investment with technological advancements and safety standards.

Key Signals And Evidence

In analyzing the virus testing kits market, several key signals and evidence points emerge that illuminate the underlying dynamics of investment and funding. The most prominent signal is the increased testing capacity, which has become a critical factor in the market’s evolution. The capacity to conduct widespread and rapid testing is not only a response to the immediate demands of the COVID-19 pandemic but also a strategic measure to address potential future outbreaks of infectious diseases. This is supported by investments from major industry players such as Roche Diagnostics and Abbott Laboratories, who are focusing on expanding their testing capabilities to capture a larger share of the market.

Mergers and acquisitions (M&A) also stand out as a significant signal, with companies seeking to enhance their technological capabilities and expand their product portfolios. For instance, Danaher Corp.’s acquisition of a diagnostics startup for $500.00 million demonstrates an aggressive approach to securing innovative technologies that can drive future growth. Such M&A activities are not only about acquiring technology but also about gaining access to new markets and customer bases, which is essential for sustaining competitive advantage in a high-capital-intensity market.

Geographical expansion is another key signal, as companies aim to tap into new regional markets to drive growth. This strategy is particularly evident in the efforts of Thermo Fisher Scientific and QIAGEN N.V., which are expanding their presence in emerging markets where the demand for virus testing kits is expected to rise. The pursuit of geographical diversification is driven by the need to mitigate risks associated with market saturation in established regions and to leverage growth opportunities in areas with burgeoning healthcare infrastructure.

Another critical signal is the focus on product launches, particularly those aimed at addressing the ongoing demand for COVID-19 testing. The launch of new kits, such as the HiGenoMB RT-PCR kits for detecting the JN.1 variant of SARS-CoV-2, highlights the continuous innovation within the industry. These product launches are not only about meeting current testing needs but also about establishing a competitive edge through differentiation and technological advancement.

Affordable point-of-care molecular diagnostics also play a pivotal role in the market, as there is a growing emphasis on making testing accessible to wider populations. This approach is crucial for achieving equitable access to diagnostic testing, especially in low-resource settings. Companies are investing in the development of affordable testing solutions that can be deployed quickly and efficiently, which aligns with broader public health goals.

Strategic Implications

The strategic implications of these investment and funding dynamics are profound, shaping the competitive landscape and influencing corporate strategies. For stakeholders, understanding these implications is vital for navigating the complex market environment.

Firstly, the emphasis on increased testing capacity and capacity expansion suggests that companies must prioritize scaling their operations to meet potential surges in demand. This requires not only capital investment but also strategic partnerships that can enhance supply chain resilience and ensure the timely delivery of testing kits. Companies that can efficiently scale their operations and optimize their production capabilities are likely to gain a competitive advantage.

The wave of M&A activity indicates a consolidation trend within the industry, where larger players are acquiring smaller, innovative startups to bolster their technological capabilities. This consolidation can lead to a more competitive market environment, with a few dominant players exerting significant influence over pricing and market access. For smaller companies, this trend underscores the importance of differentiating their offerings and exploring niche markets to maintain relevance.

Geographical expansion strategies highlight the need for companies to adapt to diverse market conditions and regulatory environments. As companies enter new regions, they must navigate varying healthcare infrastructures, regulatory requirements, and cultural considerations. Successful geographical expansion requires a nuanced understanding of these factors and the ability to tailor product offerings to meet local needs.

Product innovation, particularly in the realm of affordable point-of-care diagnostics, is critical for addressing the challenges of accessibility and affordability. Companies that can deliver cost-effective testing solutions without compromising quality will likely capture a significant share of the market. This focus on innovation also drives the need for continuous research and development, as the emergence of novel infectious agents necessitates the rapid development of new diagnostic technologies.

Forward Outlook

Looking ahead to the forecast period of 2026-2033, the virus testing kits market is poised for continued growth, driven by the strategic allocation of capital towards key areas such as capacity expansion, technological innovation, and geographical diversification. The market’s trajectory will be shaped by several factors, including the ongoing threat of infectious diseases, advancements in diagnostic technologies, and the evolving regulatory landscape.

The increased testing capacity and focus on rapid diagnostic technologies will likely lead to a more resilient healthcare system, capable of responding swiftly to future outbreaks. This resilience is essential for maintaining public health and ensuring economic stability in the face of health crises.

M&A activity is expected to persist, as companies seek to acquire cutting-edge technologies and expand their market reach.

Technology & Innovation

Technology and Innovation Landscape in the Global Virus Testing Kits market

Executive Framing

The rapid evolution of virus testing kits is redefining the healthcare landscape, with significant implications for public health, economic stability, and technology adoption. As we move towards the forecast period of 2026-2033, the technology and innovation landscape of virus testing kits is poised to experience a transformative phase characterized by high innovation intensity and moderate patent activity. This dimension’s significance is underscored by the increased need for rapid and accurate diagnostic solutions, driven by the persistent threat of viral outbreaks and the rising demand for decentralized testing options.

A critical component of this transformation is the advancement in testing technologies such as PCR, antigen, and antibody tests, along with emerging innovations like isothermal amplification and microfluidics. These technologies not only enhance the accuracy and speed of diagnostics but also facilitate the adoption of testing in diverse settings beyond traditional healthcare facilities. Companies like Abbott Laboratories, Lucira Health, and Hologic Inc. are at the forefront of this innovation wave, pushing the boundaries of what virus testing kits can achieve. The growth stage of technology maturity signifies that while these technologies are not yet at peak adoption, they are rapidly gaining traction and reshaping the market structure.

Current Market Reality

The virus testing kits market is currently in a state of significant flux, characterized by the integration of advanced technologies and the strategic maneuvers of key industry players. The present reality is defined by the convergence of several factors: technological innovation, regulatory approvals, and market demand for rapid testing solutions. Companies such as Detect and Aptitude Medical Systems are driving innovation by developing tests that offer rapid results in just 10???15 minutes, with a high accuracy rate of over 98.00%. This level of precision and efficiency is crucial for addressing the ongoing need for quick diagnostic solutions, particularly in the face of emerging viral threats.

Regulatory landscapes are also playing a pivotal role in shaping the market dynamics. The granting of Emergency Use Authorization (EUA) by the FDA for various testing technologies has been instrumental in accelerating the deployment of new solutions. Such approvals not only validate the efficacy of these technologies but also enhance their credibility and adoption across diverse settings, from hospitals to home testing environments. The emphasis on decentralized testing is further supported by government initiatives aimed at enhancing infectious disease control, thereby increasing the overall testing capacity.

In terms of market players, companies like Luminex Corporation and Bio-Rad Laboratories, Inc. are making strategic investments in biosensor and microfluidics technologies, which promise to improve the throughput and economics of virus testing procedures. These advancements are crucial for meeting the growing demand for home-based testing solutions, a trend that has gained momentum in the wake of the COVID-19 pandemic. Moreover, the development of dual-purpose tests by firms like Beckman Coulter, Inc. highlights the industry’s focus on providing versatile diagnostic tools that can address multiple pathogens simultaneously.

Key Signals And Evidence

The current landscape of virus testing kits is defined by several key signals that underscore the ongoing transformation and its implications for the future. One of the most prominent signals is the adoption of testing in diverse settings, facilitated by the integration of advanced technologies such as lateral flow technology, isothermal amplification, and biosensors. These innovations have enabled testing to extend beyond traditional healthcare environments into schools, workplaces, and homes, thus increasing accessibility and convenience for end-users.

This shift is supported by the trend towards home-based testing kits, which meets the growing demand for rapid and decentralized testing options. Companies like Lucira Health and Detect are at the forefront of this movement, developing user-friendly tests that can provide rapid results in 10???15 minutes with high accuracy of over 98.00%.

Another critical signal is the increased testing capacity, which is being bolstered by government initiatives aimed at enhancing infectious disease control. The collaboration between PerkinElmer, Inc. and the California government to provide up to 150,000 new daily tests exemplifies the public-private partnerships driving this expansion. These efforts are crucial in ensuring that testing capabilities can meet the demands of potential future outbreaks, as well as routine public health surveillance.

FDA approval is another significant signal, reflecting the stringent regulatory standards that companies must meet to ensure the efficacy and safety of their testing kits. The approval of advanced systems such as the cobas 6800/8800 underscores the importance of regulatory compliance in maintaining market credibility and driving consumer confidence. Companies like Abbott Laboratories and Hologic Inc. have successfully navigated this regulatory landscape, securing approvals for their innovative testing solutions.

The demand for rapid and accurate diagnostic solutions is further emphasized by the development of dual-purpose tests and multiplex assays, which can detect multiple pathogens simultaneously. This innovation not only enhances diagnostic efficiency but also provides a strategic advantage in competitive markets. The acquisition of Luminex by DiaSorin in April 2021 highlights the strategic moves companies are making to strengthen their capabilities in this area.

Strategic Implications

The strategic implications of these developments are profound, particularly for stakeholders looking to capitalize on the evolving market dynamics. The adoption in diverse settings indicates a shift towards more personalized healthcare delivery models, where accessibility and convenience are paramount. This trend is likely to drive demand for compact, easy-to-use testing kits, prompting companies to prioritize user experience in their product development strategies.

The increased testing capacity, supported by public-private partnerships and government initiatives, suggests a growing emphasis on preparedness and resilience in public health infrastructure. This focus on scalability and rapid deployment capabilities will likely influence procurement strategies and investment decisions, as stakeholders seek to strengthen their supply chains and operational frameworks to meet fluctuating demand levels.

FDA approval continues to be a crucial determinant of market entry and competitive positioning. Companies that can secure regulatory endorsements for their innovative solutions will have a distinct advantage in terms of market credibility and consumer trust. This underscores the importance of maintaining rigorous quality standards and investing in compliance processes to navigate the complex regulatory landscape effectively.

The demand for rapid and accurate diagnostic solutions presents both opportunities and challenges for industry players. While the need for advanced testing capabilities is clear, the competitive landscape will likely intensify as companies vie for market share. This is expected to drive innovation and differentiation efforts, with companies leveraging technologies such as AI and machine learning to enhance the accuracy, speed, and usability of their testing solutions.

Forward Outlook

Looking ahead to the forecast period of 2026-2033, the technology and innovation landscape of virus testing kits is poised for continued evolution. The advancements in diagnostic technologies and the strategic actions of key industry players are likely to reshape market dynamics, with significant implications for pricing, margins, and competitive behavior.

The trend towards home-based testing kits is expected to gain momentum, driven by consumer preferences for convenience and autonomy in healthcare management. This shift will likely spur further innovation in user-friendly designs and integrated digital platforms that facilitate seamless data sharing and remote monitoring.

Government initiatives for infectious disease control will remain a pivotal factor in shaping the market, as policymakers prioritize preparedness and resilience in the face of ongoing and emerging public health threats. This focus is expected to drive continued investments in testing infrastructure and capabilities, as well as collaborations between public and private sectors to enhance testing accessibility and affordability.

The competitive landscape will likely see increased consolidation and strategic partnerships, as companies seek to bolster their technological capabilities and market reach. The acquisition of startups and emerging players with specialized expertise in areas such as biosensors and microfluidics will be a key strategy for established companies looking to maintain their competitive edge.

In conclusion, the technology and innovation landscape of virus testing kits is set to undergo substantial transformation in the coming years, driven by advancements in diagnostic technologies, regulatory developments, and evolving consumer preferences. Stakeholders across the industry must remain vigilant and adaptive to these changes, leveraging strategic insights and collaborative efforts to navigate the opportunities and challenges that lie ahead. As the market continues to evolve, those who can effectively integrate cutting-edge technologies, regulatory compliance, and consumer-centric approaches will be well-positioned to lead in this dynamic and rapidly changing landscape.

Market Risk

Risk Factors and Disruption Threats in the Global Virus Testing Kits market

Executive Framing

The risk landscape for virus testing kits from 2026 to 2033 is defined by structural constraints and market impacts that could fundamentally alter the competitive dynamics and operational efficacy of this market. As global health systems continue to grapple with the ongoing threat of emerging infectious diseases, the virus testing kit market stands at a critical juncture. The high overall market risk level is compounded by factors such as contamination of test kits, design flaws in testing procedures, and regulatory approval challenges. These risks threaten not only the operational resilience of manufacturers but also the efficacy of health responses worldwide.

The moderate geopolitical exposure and substitution risk levels reflect a market intertwined with international supply chains and potential technological advancements. The growing demand for rapid and accurate testing solutions, driven by the emergence of new variants and increased consumer awareness of at-home testing, underscores the urgency for stakeholders to navigate these risks adeptly. Strategic investments in research and development (R&D), partnerships with local firms, and collaborations within the supply chain emerge as critical mitigation strategies that could redefine competitive advantage in this high-stakes environment.

Current Market Reality

The current state of the virus testing kits market is characterized by a complex interplay of supply chain challenges, regulatory hurdles, and evolving consumer demands. A slow regulatory approval process is a significant bottleneck, impacting the speed at which new testing solutions can be brought to market. This delay is exacerbated by regulatory approval challenges, which require manufacturers to navigate a labyrinthine regulatory landscape to ensure compliance and secure timely market entry.

PerkinElmer, Inc.’s public-private partnership with the California government, aimed at delivering up to 150,000 new daily tests, exemplifies the strategic collaborations that are becoming increasingly vital in this market. Such partnerships not only enhance operational capacity but also bolster market positioning by aligning with governmental health initiatives. However, the expiration of Clinical Laboratory Improvement Amendments (CLIA) regulations requiring the reporting of SARS-CoV-2 test results introduces an additional layer of complexity, potentially impacting the transparency and reliability of testing data.

Moreover, component shortages have emerged as a critical risk factor, disrupting the production and distribution of test kits. This challenge is compounded by the supply chain complexity inherent in sourcing the diverse components necessary for test kit manufacturing. The acquisition of diagnostics startups, such as Danaher Corp.’s $500.00 million acquisition, reflects strategic investments aimed at mitigating these risks by integrating new technologies and capabilities into existing operations.

The launch of HiGenoMB RT-PCR kits to detect the JN.1 variant of SARS-CoV-2 highlights the ongoing need for innovation in response to the evolving pathogen landscape. The introduction of new variants necessitates continuous adaptation of testing methodologies, placing additional pressure on manufacturers to maintain the accuracy and reliability of their products. The FDA approval for cobas 6800/8800 systems underscores the importance of gaining regulatory endorsements to enhance market credibility and consumer trust.

Key Signals And Evidence

The primary signals shaping the virus testing kits market are deeply intertwined with the identified risk factors and mitigation strategies. The slow regulatory approval process and regulatory approval challenges are pivotal in influencing market dynamics, driving companies to seek strategic partnerships and investments in R&D. Such collaborations are exemplified by partnerships with local firms, which not only facilitate market entry but also enable manufacturers to leverage local expertise and infrastructure.

Strategic investments in R&D are critical in addressing the substitution risk level, as they enable the development of innovative testing solutions that can meet the evolving needs of healthcare providers and consumers. The development of multi-analyte tests and laboratory quality plans are indicative of the industry’s focus on enhancing test accuracy and reliability, thereby mitigating the risks associated with contamination and design flaws.

Component shortages, a significant operational challenge, necessitate a re-evaluation of supply chain strategies. By fostering collaborations with supply chain partners, manufacturers can enhance their resilience against disruptions and ensure the timely delivery of test kits. This approach is further supported by the development of documented processes for future responses, which provide a framework for maintaining operational continuity in the face of unforeseen challenges.

The increased demand for accurate testing solutions, driven by factors such as the growing prevalence of infectious diseases and government initiatives for free testing, underscores the need for robust quality control protocols. The high false negative rate on initial testing and variable sensitivity of antigen tests highlight the importance of serial testing and the need for continuous quality improvements in testing methodologies. These challenges are further compounded by the increased pressure to diagnose cases rapidly, necessitating a balance between speed and accuracy in testing processes.

In summary, the virus testing kits market is navigating a landscape fraught with structural risks and operational challenges. The interplay of regulatory hurdles, supply chain complexities, and evolving consumer demands necessitates strategic adaptations that can enhance market resilience and ensure the continued delivery of reliable testing solutions. As the market continues to evolve in response to these dynamics, stakeholders must remain vigilant in addressing these risks to maintain competitive advantage and operational efficacy.

Strategic Implications

The strategic implications of the identified risks and signals in the virus testing kit market are profound, necessitating a nuanced approach to both market participation and stakeholder engagement. The slow regulatory approval process and challenges associated with regulatory compliance pose significant barriers to market entry and expansion. Companies like PerkinElmer, Inc. have mitigated these challenges through strategic partnerships, as evidenced by their public-private partnership with the California government to provide up to 150,000 new daily tests. This collaboration not only circumvents some regulatory hurdles but also secures a stable demand through government contracts, highlighting the importance of aligning with public health initiatives.

Strategic investments in research and development (R&D) are crucial for maintaining competitive advantage in this high-risk environment. The acquisition of a diagnostics startup by Danaher Corp. for $500.00 million exemplifies a proactive approach to bolstering R&D capabilities, enabling the development of innovative testing solutions that can address emerging variants and improve test accuracy. Such investments are not only strategic for product innovation but also vital for enhancing operational resilience against unforeseen market disruptions.

Component shortages remain a critical concern, impacting the production capacity and pricing power of virus testing kits. Companies must strategize to secure their supply chains through diversification and redundancy. Partnerships with local firms can mitigate these risks by ensuring a more stable supply chain and reducing the dependency on single-source suppliers. This approach also supports localized manufacturing and potentially reduces lead times, which can be critical during surges in demand.

The competitive landscape is further influenced by strategic partnerships among industry players. Collaborations, such as those for developing multi-analyte tests, can drive innovation and expand market offerings. This is crucial in meeting the increased consumer demand for comprehensive and accurate testing solutions. Additionally, the growing prevalence of infectious diseases necessitates a swift response mechanism, which can be achieved through such strategic alliances.

From an operational perspective, the failure of initial test kits and high false negative rates underscore the importance of quality control. Implementing rigorous review processes and developing a Laboratory Quality Plan are essential for maintaining product reliability and consumer trust. Training resources for performing point-of-care tests and guidance on personal protective equipment further enhance the operational readiness of stakeholders in this market.

Forward Outlook

Looking ahead, the virus testing kit market is poised to undergo significant transformations as stakeholders adapt to the evolving risk landscape. The interplay between regulatory challenges, supply chain complexities, and consumer demand will continue to shape market dynamics through 2033. Companies that effectively navigate these challenges through strategic investments, partnerships, and innovations will likely emerge as market leaders.

The strategic pivot towards R&D and innovation will be crucial in addressing the high demand for accurate testing solutions amidst the emergence of new variants. This focus will not only enhance the accuracy and reliability of testing kits but also ensure that companies remain at the forefront of technological advancements. Furthermore, the development of multi-analyte tests and improvements in testing methodologies will cater to the growing consumer awareness and demand for at-home testing solutions.

Government initiatives for free testing and the expiration of certain regulations may also influence market dynamics by altering the competitive landscape and shaping consumer expectations. Companies must remain agile in their strategic planning to capitalize on these regulatory shifts and align with public health goals.

In conclusion, the virus testing kit market is navigating a complex risk environment that demands strategic foresight and adaptability. The ability to anticipate and respond to regulatory, supply chain, and consumer-driven challenges will be critical in securing long-term market success. Stakeholders must prioritize strategic partnerships, investment in R&D, and operational excellence to maintain resilience and competitiveness in this rapidly evolving market. As the market continues to respond to these dynamics, the strategic implications outlined here will serve as a guide for navigating the uncertainties and opportunities that lie ahead.

Regulatory Landscape

Regulatory and Policy Landscape of the Global Virus Testing Kits market

Executive Framing

The regulatory and policy environment surrounding virus testing kits, particularly amid the ongoing evolution of global health dynamics, is a crucial determinant of market structure and competitive behavior. As we look toward the forecast period of 2026 to 2033, the regulatory landscape is poised to exert significant influence over market entry barriers, cost structures, and innovation trajectories. This dimension matters now more than ever as the healthcare sector grapples with the aftermath of the COVID-19 pandemic and prepares for potential future public health emergencies.

The interplay of regulatory approvals, compliance requirements, and policy shifts will shape the strategic direction of companies operating in the virus testing kit market, demanding a nuanced understanding of how these elements affect market outcomes.

Regulatory frameworks, such as those governed by the Centers for Medicare & Medicaid Services (CMS) and the U.S. Food and Drug Administration (FDA), are central to the approval and distribution of virus testing kits. These frameworks not only determine the speed and efficiency of bringing new testing kits to market but also influence pricing, reimbursement, and ultimately, accessibility for consumers.

The expiration of certain regulations, alongside the introduction of new reimbursement codes and evolving approval processes, will dictate the pace at which companies can innovate and respond to public health needs. Moreover, state-level authorizations add another layer of complexity, as they can either expedite or hinder the approval of testing kits, impacting the competitive landscape.

Current Market Reality

The current regulatory environment presents a mixed bag of opportunities and challenges for stakeholders in the virus testing kit market. As we stand today, several key regulations and signals are at play, each with distinct implications for market dynamics.

The expiration of Clinical Laboratory Improvement Amendments (CLIA) regulations requiring the reporting of SARS-CoV-2 test results is a pivotal change that may alter reporting obligations for manufacturers and laboratories. This shift could reduce administrative burdens but may also impact data accuracy and transparency, influencing public health monitoring and decision-making.

In addition, the introduction of new codes by CMS for the reimbursement of COVID-19 tests is reshaping financial incentives for manufacturers and healthcare providers. These codes are designed to ensure that testing remains financially viable and accessible, thereby encouraging continued investment in testing capabilities. However, they also necessitate a comprehensive understanding of reimbursement policies, which can vary significantly across states and healthcare systems.

Furthermore, the regulatory environment is characterized by ongoing delays in the FDA’s approval processes. The agency’s slow approval process has been a point of contention, impacting the timely availability of new testing technologies. This delay can stifle innovation and limit the competitive edge of companies eager to introduce cutting-edge solutions to the market.

In contrast, some state governments have been authorized to review and approve COVID-19 tests independently, potentially offering a faster route to market entry. This decentralization of approval authority can create disparities in market access and competition, with companies needing to navigate a patchwork of state-specific regulations.

The presence of robust CLIA regulations for point-of-care testing remains a critical factor in ensuring the quality and reliability of testing kits. These regulations set high performance standards for rapid tests, which are essential for maintaining public trust and supporting timely diagnosis. However, the stringent nature of these regulations can also pose challenges for manufacturers, particularly smaller entities with limited resources, as they strive to meet compliance requirements.

Several companies are actively responding to these regulatory dynamics. For instance, PerkinElmer, Inc. has entered into a public-private partnership with the California government to provide up to 150,000 new daily tests, demonstrating a strategic alignment with state-level initiatives. Similarly, the launch of HiGenoMB RT-PCR kits to detect the JN.1 variant of SARS-CoV-2 highlights the ongoing innovation within the industry, albeit within the constraints of existing regulatory frameworks. Such actions underscore the importance of regulatory compliance and strategic partnerships in navigating the current market reality.

Key Signals And Evidence

As the regulatory landscape for virus testing kits continues to evolve, the signals currently emerging provide a window into future market dynamics. One of the most impactful signals is the expiration of CLIA regulations requiring reporting of SARS-CoV-2 test results. This shift may streamline operations for testing kit manufacturers by reducing the reporting burden, potentially lowering compliance costs. However, it also raises concerns about data transparency and public health monitoring.

The absence of mandatory federal reporting could lead to fragmented data collection, challenging public health officials in tracking virus spread and managing future outbreaks.

Another significant development is the introduction of new CMS codes for the reimbursement of COVID-19 tests. These codes aim to standardize billing practices, thereby enhancing the financial viability of offering virus testing. This regulatory move is likely to encourage market entry by reducing financial uncertainty for providers and increasing access to testing services.

However, the impact of these codes on pricing structures and competitive dynamics remains to be fully understood, particularly as providers adjust to this new reimbursement landscape.

The CLIA regulations for point-of-care testing are also pivotal. These regulations set stringent quality standards, ensuring high-performance benchmarks for rapid tests. While this ensures reliability, it may raise barriers to entry for smaller players who might struggle to meet these requirements.

For established companies like PerkinElmer and Danaher Corp., which have the resources to comply with these standards, this presents an opportunity to consolidate market leadership.

FDA delays in approval processes, compounded by the agency’s historically slow approval process, continue to be a bottleneck for bringing new testing kits to market. This regulatory inertia can stifle innovation, as companies may be hesitant to invest heavily in product development without a clear timeline for approval.

On the other hand, the slow pace of FDA approvals can serve as a protective barrier for incumbents, reducing competitive pressures from new entrants who might otherwise disrupt the market with innovative offerings.

Finally, the authorization of state governments to review and approve COVID-19 tests introduces a dual-layer regulatory environment. This decentralization could lead to faster approvals in states with more progressive policies, providing a competitive edge to companies that can quickly adapt to local regulatory landscapes.

However, this patchwork approach may also lead to inconsistencies in testing standards, complicating compliance for companies operating nationwide.

Strategic Implications

The strategic landscape for companies in the virus testing kit market is heavily influenced by these regulatory signals. Companies must navigate a complex web of federal and state-level regulations, balancing the need for compliance with the agility to respond to rapid market changes.

The expiration of CLIA reporting requirements presents an opportunity to streamline operations, but it also necessitates the development of robust internal data tracking mechanisms to ensure public health objectives are met.

The introduction of CMS reimbursement codes can alter competitive dynamics by making virus testing more financially sustainable for providers. Companies that can align their pricing strategies with these reimbursement structures stand to gain significant market share. This may also drive innovation in cost-effective testing solutions, as providers seek to maximize reimbursement while minimizing operational costs.

For established players like PerkinElmer and Danaher Corp., the stringent CLIA regulations for point-of-care testing represent both a challenge and an opportunity. These companies can leverage their resources to meet high-performance standards, potentially increasing their market dominance. However, they must also remain vigilant to the threat of new entrants who could disrupt the market with innovative testing methodologies that meet regulatory requirements at lower costs.