Thailand Japanese Restaurant Market Report Analysis, Size and Forecast 2026-2033

Thailand Japanese Restaurant Market Forecast Snapshot: 2026–2033

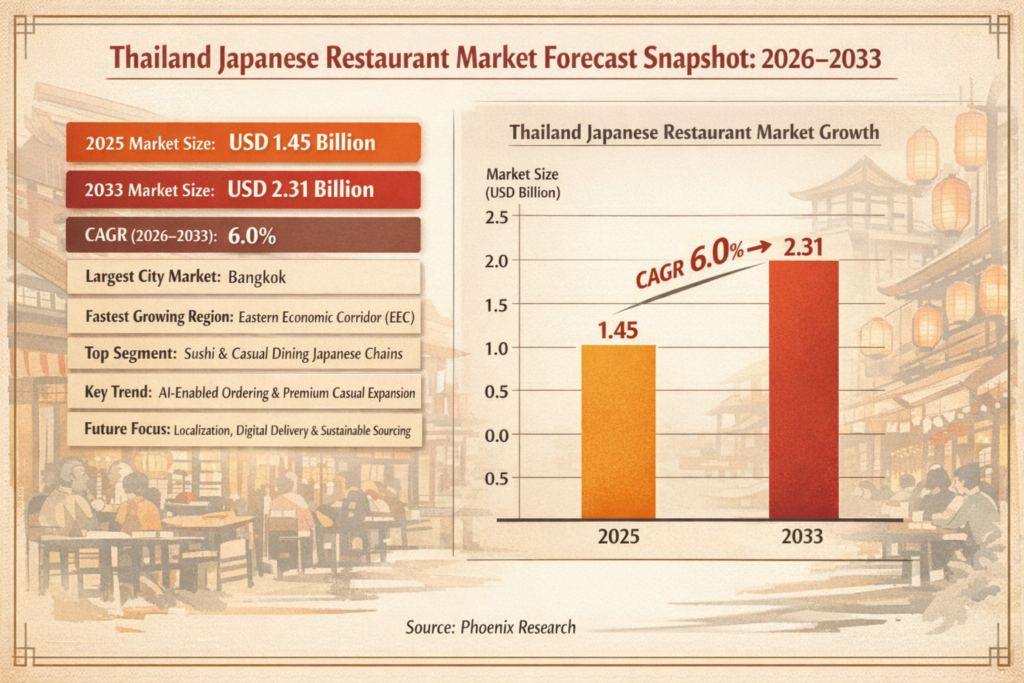

| Metric | Value |

|---|---|

| 2025 Market Size | USD 1.45 Billion |

| 2033 Market Size | USD 2.31 Billion |

| CAGR (2026–2033) | 6.0% |

| Largest City Market | Bangkok |

| Fastest Growing Region | Eastern Economic Corridor (EEC) |

| Top Segment | Sushi & Casual Dining Japanese Chains |

| Key Trend | AI-Enabled Ordering & Premium Casual Expansion |

| Future Focus | Localization, Digital Delivery & Sustainable Sourcing |

Thailand Japanese Restaurant Market Overview

The Thailand Japanese Restaurant Market represents one of the most mature and diversified Asian cuisine segments within the broader Thailand foodservice industry size 2026 landscape. Strong cultural affinity, long-standing trade relations between Thailand and Japan, and high consumer acceptance of Japanese cuisine have created a resilient and scalable restaurant ecosystem.

According to Pheonix Research modeling, the Thailand Japanese Restaurant Market size is valued at USD 1.45 billion in 2025 and is projected to reach USD 2.31 billion by 2033, registering a CAGR of 6.0% during 2026–2033. This steady Japanese Restaurant revenue forecast reflects premium dining expansion, franchise penetration, rising middle-class consumption, and tourism normalization.

Bangkok remains the primary revenue hub due to high mall density, premium retail dining clusters, and strong expatriate presence. Meanwhile, growth is accelerating across the Eastern Economic Corridor (EEC), Chiang Mai, and Phuket, supported by tourism inflows and urban development.

The Post-2025 outlook for Thailand Japanese Restaurant Market indicates deeper digital integration, AI-powered demand forecasting, menu localization strategies, and sustainability-driven sourcing models.

Key Drivers of Thailand Japanese Restaurant Market Growth

1. Strong Cultural Acceptance & Premium Perception

Japanese cuisine is widely perceived as high-quality, healthy, and premium. Sushi, ramen, yakiniku, and izakaya concepts continue expanding across mid-tier and premium price categories.

2. Tourism Recovery & Expat Population Growth

Thailand’s tourism recovery significantly strengthens demand in Bangkok, Phuket, and Pattaya. Japanese expatriates and business communities further stabilize consistent consumption patterns.

3. Expansion of Franchise & Chain Models

Large operators are scaling via mall-based expansion and structured franchise models. Brand standardization improves operational efficiency and customer trust.

4. Impact of AI on Thailand Japanese Restaurant Market

AI-driven ordering systems, POS-integrated analytics, smart inventory management, and demand prediction tools are improving margin control and reducing food waste. Digital loyalty programs and targeted promotions enhance repeat visits.

5. Sustainability Trends in Thailand Japanese Restaurant Market

Growing emphasis on responsibly sourced seafood, reduced plastic packaging, energy-efficient kitchens, and local farm partnerships supports long-term environmental positioning.

Market Segmentation of Thailand Japanese Restaurant Market

By Restaurant Format

1.1 Casual Dining Japanese Restaurants

1.1.1 Sushi-Focused Chains

1.1.1.1 Conveyor Belt (Kaiten) Sushi

1.1.1.2 Made-to-Order Sushi Restaurants

1.1.1.3 All-You-Can-Eat Sushi Buffets

1.1.1.4 Premium Casual Sushi Concepts

1.1.2 Ramen Specialty Restaurants

1.1.2.1 Tonkotsu-Based Ramen Chains

1.1.2.2 Miso & Shoyu Variants

1.1.2.3 Udon & Soba Specialty Shops

1.1.2.4 Fusion Noodle Restaurants

1.1.3 Yakiniku & Grill Restaurants

1.1.3.1 Buffet-Style Yakiniku

1.1.3.2 À La Carte Japanese BBQ

1.1.3.3 Premium Wagyu Concepts

1.1.3.4 Family Group Grill Dining

1.1.4 Izakaya Concepts

1.1.4.1 Traditional Izakaya

1.1.4.2 Modern Themed Izakaya

1.1.4.3 Rooftop & Lifestyle Izakaya

1.1.4.4 Expat-Focused Authentic Izakaya

1.1.5 Family-Oriented Japanese Chains

1.1.5.1 Mall-Based Family Dining

1.1.5.2 Kids Menu & Combo Meals

1.1.5.3 Affordable Bento Concepts

1.1.5.4 Community-Based Japanese Restaurants

1.2 Quick Service Japanese Restaurants

1.2.1 Sushi Express Counters

1.2.1.1 Mall Food Court Counters

1.2.1.2 Grab-and-Go Sushi Packs

1.2.1.3 Transit Hub Kiosks

1.2.1.4 Micro-Franchise Units

1.2.2 Bento & Donburi Chains

1.2.2.1 Rice Bowl Quick Service

1.2.2.2 Japanese Curry Express

1.2.2.3 Teriyaki & Katsu Formats

1.2.2.4 Office Lunch Sets

1.3 Premium & Fine Dining Japanese

1.3.1 Omakase Restaurants

1.3.1.1 Chef-Led Tasting Menu

1.3.1.2 Imported Seasonal Ingredients

1.3.1.3 Counter-Only Seating

1.3.1.4 Reservation-Only Models

1.3.2 Teppanyaki Fine Dining

1.3.2.1 Live Cooking Experience

1.3.2.2 Luxury Hotel Integration

1.3.2.3 Corporate Event Dining

1.3.2.4 Private Dining Rooms

1.4 Cloud Kitchen & Delivery-Only Japanese

1.4.1 Single-Brand Cloud Kitchens

1.4.1.1 Sushi Delivery Brands

1.4.1.2 Ramen Delivery Brands

1.4.1.3 Aggregator-Based Operations

1.4.1.4 AI-Based Demand Forecasting

1.4.2 Multi-Brand Asian Cloud Kitchens

1.4.2.1 Shared Infrastructure Models

1.4.2.2 Japanese + Korean Hybrid Brands

1.4.2.3 Centralized Procurement

1.4.2.4 Delivery Radius Optimization

By Distribution Channel

2.1 Dine-In

2.1.1 Mall-Based Dining

2.1.1.1 Tier-1 Bangkok CBD Malls

2.1.1.2 Suburban Lifestyle Malls

2.1.1.3 Tourist Retail Complexes

2.1.1.4 Mixed-Use Developments

2.1.2 Standalone Street Locations

2.1.2.1 Premium High-Street Areas

2.1.2.2 Residential Communities

2.1.2.3 Expat Clusters

2.1.2.4 Tourist Streets

2.1.3 Hotel-Integrated Japanese Restaurants

2.1.3.1 Luxury Hotels

2.1.3.2 Business Hotels

2.1.3.3 Resort Dining

2.1.3.4 Airport Hotels

2.2 Takeaway

2.2.1 Counter Pickup

2.2.1.1 Walk-In Pickup

2.2.1.2 Pre-Order App Pickup

2.2.1.3 Express Lunch Pickup

2.2.1.4 Corporate Bulk Pickup

2.2.2 Supermarket & Retail Sushi Counters

2.2.2.1 Hypermarkets

2.2.2.2 Premium Supermarkets

2.2.2.3 Convenience Stores

2.2.2.4 In-Store Brand Partnerships

2.3 Online Delivery

2.3.1 Third-Party Aggregators

2.3.1.1 GrabFood

2.3.1.2 LINE MAN

2.3.1.3 Foodpanda

2.3.1.4 Robinhood

2.3.2 Brand-Owned Delivery

2.3.2.1 In-House Fleet

2.3.2.2 Hybrid Delivery Models

2.3.2.3 Subscription Meal Delivery

2.3.2.4 Loyalty App Integration

2.3.3 Cloud Kitchen Delivery

2.3.3.1 Single-Brand Virtual Kitchens

2.3.3.2 Multi-Brand Shared Facilities

2.3.3.3 Delivery-Only Sushi Brands

2.3.3.4 AI-Optimized Delivery Zones

By End-User

3.1 Individual Consumers

3.1.1 Millennials

3.1.1.1 Social Dining Consumers

3.1.1.2 Premium Casual Seekers

3.1.1.3 Value Combo Buyers

3.1.1.4 Health-Conscious Diners

3.1.2 Gen Z Consumers

3.1.2.1 Budget Sushi Buyers

3.1.2.2 Themed Izakaya Visitors

3.1.2.3 App-Based Ordering Users

3.1.2.4 Dessert & Beverage Focused

3.1.3 Working Professionals

3.1.3.1 Corporate Lunch Buyers

3.1.3.2 After-Work Izakaya Customers

3.1.3.3 Delivery-Based Consumers

3.1.3.4 Omakase Premium Customers

3.1.4 Families

3.1.4.1 Weekend Mall Dining

3.1.4.2 Buffet Yakiniku Visitors

3.1.4.3 Kids Menu Consumers

3.1.4.4 Group Celebration Diners

By Geography

4.1 Central Thailand

4.2 Northern Thailand

4.3 Southern Thailand

4.4 Northeastern Thailand (Isan Region)

Regional Insights of Thailand Japanese Restaurant Market

Bangkok – Largest Market

Bangkok accounts for the largest share of the Thailand Japanese Restaurant Market due to dense urban population, high disposable income, and premium mall ecosystems such as Siam Paragon and CentralWorld.

Eastern Economic Corridor (EEC) – Fastest Growing

Industrial growth, expatriate communities, and rising commercial infrastructure are accelerating Japanese dining demand across Chonburi and Rayong.

Northern Thailand

Chiang Mai is witnessing steady expansion supported by tourism and digital nomad communities.

Southern Thailand

Phuket and Pattaya benefit from tourism-driven premium Japanese dining demand.

Leading Companies in Thailand Japanese Restaurant Market

Prominent players include:

-

MK Restaurant Group (Japanese formats)

-

Yayoi (Plenus Thailand)

-

ZEN Corporation Group

-

Shabushi (Oishi)

-

Kagonoya Thailand

-

Kouen Group

Among these, Oishi Group PCL remains one of the most influential players due to strong brand presence, diversified Japanese concepts, and nationwide expansion. Market share remains moderately consolidated in Bangkok, while regional cities exhibit fragmented competitive structures.

Strategic Intelligence & AI-Backed Insights

Pheonix Demand Forecast Engine indicates consistent mid-single-digit growth supported by mall expansion and premiumization.

Consumer Behavior Analyzer identifies rising preference for:

-

Affordable sushi sets

-

Instagrammable dining experiences

-

Healthy, low-oil Japanese meals

Innovation Tracker highlights:

-

Tablet-based ordering systems

-

AI-driven kitchen automation

-

Digital queue management

-

Loyalty app ecosystems

Porter’s Five Forces Analysis reveals:

-

Moderate to high competitive rivalry

-

Moderate supplier power (seafood sourcing sensitivity)

-

Low switching costs for consumers

-

High differentiation through brand positioning

Why Thailand Japanese Restaurant Market Remains critical

-

Strong cultural affinity with Japanese cuisine

-

Expanding tourism and expatriate base

-

Digital ordering ecosystem integration

-

Sustainable seafood sourcing initiatives

-

Scalable franchise growth models

Final Takeaway

The Thailand Japanese Restaurant Market is evolving into a digitally integrated, premium-casual, and sustainability-oriented dining ecosystem. The projected CAGR (2026–2033) of 6.0% reflects steady demand growth supported by tourism normalization, mall-based expansion, AI-driven operational efficiency, and localization strategies.

Operators that successfully integrate AI-powered analytics, optimize seafood sourcing, expand into emerging urban corridors, and enhance experiential dining will be best positioned to capitalize on the Post-2025 outlook for Thailand Japanese Restaurant Market.

At Pheonix Research, our advanced forecasting frameworks deliver in-depth Thailand Japanese Restaurant revenue forecast, competitive benchmarking, and strategic intelligence — enabling stakeholders to unlock scalable growth opportunities with data-backed precision.

📢 Social Mentions & Publication Channels

Explore deeper insights and follow our cross-platform updates on LinkedIn, and X for continuous intelligence and market coverage.

LinkedIn : https://www.linkedin.com/feed/update/urn:li:activity:7429405297951195136

X : https://x.com/Pheonix_Insight/status/2023647084818428250?s=20

Table of Contents

Executive Summary

1.1 Market Forecast Snapshot (2026–2033)

1.2 Thailand Market Size & CAGR Analysis

1.3 Largest & Fastest-Growing Segments

1.4 Region-Level Leadership & Growth Trends

1.5 Key Market Drivers

1.6 Competitive Landscape Overview

1.7 Strategic Outlook Through 2033

Introduction & Market Overview

1.1 Definition of the Thailand Japanese Restaurant Market

1.2 Scope of the Study

1.3 Industry Evolution & Market Development

1.4 Supply Chain & Distribution Infrastructure

1.5 Impact of Consumer Trends

1.6 Sustainability & Regulatory Landscape

1.7 Technology & Innovation Landscape

Research Methodology

1.1 Primary Research

1.2 Secondary Research

1.3 Market Size Estimation Model

1.4 Forecast Assumptions (2026–2033)

1.5 Data Validation & Triangulation

Market Dynamics

1.1 Drivers

1.1.1 Strong Cultural Acceptance & Premium Perception

1.1.2 Tourism Recovery & Expat Population Growth

1.1.3 Expansion of Franchise & Chain Models

1.1.4 AI-Driven Ordering & Smart Restaurant Operations

1.1.5 Sustainability Trends & Responsible Sourcing

1.2 Restraints

1.2.1 Cost Pressures & Premium Ingredient Dependency

1.2.2 Infrastructure & Regional Expansion Limitations

1.2.3 Supply Chain Sensitivity (Seafood Sourcing)

1.2.4 Market Awareness & Localization Challenges

1.3 Opportunities

1.3.1 Expansion into Tier-2 & Emerging Tourism Cities

1.3.2 Premium Casual & Omakase Growth

1.3.3 Digital Ecosystem & AI-Based Personalization

1.3.4 Sustainable & Localized Menu Innovation

1.4 Challenges

1.4.1 Maintaining Authenticity vs Localization Balance

1.4.2 Operational Efficiency & Cost Management

1.4.3 Competitive Market Fragmentation

1.4.4 Brand Differentiation & Customer Retention

Thailand Japanese Restaurant Market Analysis (USD Billion), 2026–2033

1.1 Market Size Overview

1.2 CAGR Analysis

1.3 Regional Revenue Distribution

1.4 Segment Revenue Analysis

1.5 Distribution Channel Analysis

1.6 Consumer Impact Analysis

Market Segmentation (USD Billion), 2026–2033

1.1 By Restaurant Format

1.1.1 Casual Dining Japanese Restaurants

1.1.1.1 Sushi-Focused Chains

1.1.1.1.1 Conveyor Belt (Kaiten) Sushi

1.1.1.1.2 Made-to-Order Sushi Restaurants

1.1.1.1.3 All-You-Can-Eat Sushi Buffets

1.1.1.1.4 Premium Casual Sushi Concepts

1.1.1.2 Ramen Specialty Restaurants

1.1.1.2.1 Tonkotsu-Based Ramen Chains

1.1.1.2.2 Miso & Shoyu Variants

1.1.1.2.3 Udon & Soba Specialty Shops

1.1.1.2.4 Fusion Noodle Restaurants

1.1.1.3 Yakiniku & Grill Restaurants

1.1.1.3.1 Buffet-Style Yakiniku

1.1.1.3.2 À La Carte Japanese BBQ

1.1.1.3.3 Premium Wagyu Concepts

1.1.1.3.4 Family Group Grill Dining

1.1.1.4 Izakaya Concepts

1.1.1.4.1 Traditional Izakaya

1.1.1.4.2 Modern Themed Izakaya

1.1.1.4.3 Rooftop & Lifestyle Izakaya

1.1.1.4.4 Expat-Focused Authentic Izakaya

1.1.1.5 Family-Oriented Japanese Chains

1.1.1.5.1 Mall-Based Family Dining

1.1.1.5.2 Kids Menu & Combo Meals

1.1.1.5.3 Affordable Bento Concepts

1.1.1.5.4 Community-Based Japanese Restaurants

1.1.2 Quick Service Japanese Restaurants

1.1.2.1 Sushi Express Counters

1.1.2.1.1 Mall Food Court Counters

1.1.2.1.2 Grab-and-Go Sushi Packs

1.1.2.1.3 Transit Hub Kiosks

1.1.2.1.4 Micro-Franchise Units

1.1.2.2 Bento & Donburi Chains

1.1.2.2.1 Rice Bowl Quick Service

1.1.2.2.2 Japanese Curry Express

1.1.2.2.3 Teriyaki & Katsu Formats

1.1.2.2.4 Office Lunch Sets

1.1.3 Premium & Fine Dining Japanese

1.1.3.1 Omakase Restaurants

1.1.3.1.1 Chef-Led Tasting Menu

1.1.3.1.2 Imported Seasonal Ingredients

1.1.3.1.3 Counter-Only Seating

1.1.3.1.4 Reservation-Only Models

1.1.3.2 Teppanyaki Fine Dining

1.1.3.2.1 Live Cooking Experience

1.1.3.2.2 Luxury Hotel Integration

1.1.3.2.3 Corporate Event Dining

1.1.3.2.4 Private Dining Rooms

1.1.4 Cloud Kitchen & Delivery-Only Japanese

1.1.4.1 Single-Brand Cloud Kitchens

1.1.4.1.1 Sushi Delivery Brands

1.1.4.1.2 Ramen Delivery Brands

1.1.4.1.3 Aggregator-Based Operations

1.1.4.1.4 AI-Based Demand Forecasting

1.1.4.2 Multi-Brand Asian Cloud Kitchens

1.1.4.2.1 Shared Infrastructure Models

1.1.4.2.2 Japanese + Korean Hybrid Brands

1.1.4.2.3 Centralized Procurement

1.1.4.2.4 Delivery Radius Optimization

1.2 By Distribution Channel

1.2.1 Dine-In

1.2.1.1 Mall-Based Dining

1.2.1.1.1 Tier-1 Bangkok CBD Malls

1.2.1.1.2 Suburban Lifestyle Malls

1.2.1.1.3 Tourist Retail Complexes

1.2.1.1.4 Mixed-Use Developments

1.2.1.2 Standalone Street Locations

1.2.1.2.1 Premium High-Street Areas

1.2.1.2.2 Residential Communities

1.2.1.2.3 Expat Clusters

1.2.1.2.4 Tourist Streets

1.2.1.3 Hotel-Integrated Japanese Restaurants

1.2.1.3.1 Luxury Hotels

1.2.1.3.2 Business Hotels

1.2.1.3.3 Resort Dining

1.2.1.3.4 Airport Hotels

1.2.2 Takeaway

1.2.2.1 Counter Pickup

1.2.2.1.1 Walk-In Pickup

1.2.2.1.2 Pre-Order App Pickup

1.2.2.1.3 Express Lunch Pickup

1.2.2.1.4 Corporate Bulk Pickup

1.2.2.2 Supermarket & Retail Sushi Counters

1.2.2.2.1 Hypermarkets

1.2.2.2.2 Premium Supermarkets

1.2.2.2.3 Convenience Stores

1.2.2.2.4 In-Store Brand Partnerships

1.2.3 Online Delivery

1.2.3.1 Third-Party Aggregators

1.2.3.1.1 App-Based Delivery Platforms

1.2.3.1.2 Subscription Delivery Models

1.2.3.1.3 Promotional Campaign Delivery

1.2.3.1.4 Loyalty-Based Delivery Programs

1.2.3.2 Brand-Owned Delivery

1.2.3.2.1 In-House Fleet

1.2.3.2.2 Hybrid Delivery Models

1.2.3.2.3 Subscription Meal Delivery

1.2.3.2.4 Loyalty App Integration

1.2.3.3 Cloud Kitchen Delivery

1.2.3.3.1 Single-Brand Virtual Kitchens

1.2.3.3.2 Multi-Brand Shared Facilities

1.2.3.3.3 Delivery-Only Sushi Brands

1.2.3.3.4 AI-Optimized Delivery Zones

1.3 By End-User

1.3.1 Individual Consumers

1.3.1.1 Millennials

1.3.1.1.1 Social Dining Consumers

1.3.1.1.2 Premium Casual Seekers

1.3.1.1.3 Value Combo Buyers

1.3.1.1.4 Health-Conscious Diners

1.3.1.2 Gen Z Consumers

1.3.1.2.1 Budget Sushi Buyers

1.3.1.2.2 Themed Izakaya Visitors

1.3.1.2.3 App-Based Ordering Users

1.3.1.2.4 Dessert & Beverage Focused

1.3.1.3 Working Professionals

1.3.1.3.1 Corporate Lunch Buyers

1.3.1.3.2 After-Work Izakaya Customers

1.3.1.3.3 Delivery-Based Consumers

1.3.1.3.4 Omakase Premium Customers

1.3.1.4 Families

1.3.1.4.1 Weekend Mall Dining

1.3.1.4.2 Buffet Yakiniku Visitors

1.3.1.4.3 Kids Menu Consumers

1.3.1.4.4 Group Celebration Diners

1.4 By Geography

1.4.1 Central Thailand

1.4.2 Northern Thailand

1.4.3 Southern Thailand

1.4.4 Northeastern Thailand (Isan Region)

Market Segmentation by Geography

1.1 Thailand (National Overview)

1.2 Central Thailand

1.3 Northern Thailand

1.4 Southern Thailand

1.5 Northeastern Thailand (Isan Region)

Competitive Landscape

1.1 Market Share Analysis

1.2 Brand Positioning & Format Benchmarking

1.3 Menu Innovation & Differentiation Strategies

1.4 Supply Chain & Sourcing Partnerships

1.5 Competitive Intensity & Expansion Strategies

Company Profiles

Strategic Intelligence & Pheonix AI Insights

1.1 Pheonix Demand Forecast Engine

1.2 Consumer Behavior Analyzer

1.3 Innovation Tracker

1.4 Operational Efficiency Analyzer

1.5 Automated Porter’s Five Forces Analysis

Future Outlook & Strategic Recommendations

1.1 Expansion into Emerging Tourism & Industrial Corridors

1.2 AI Integration & Digital Ecosystem Optimization

1.3 Premium Casual & Omakase Expansion Strategy

1.4 Sustainable Seafood & Local Sourcing Models

1.5 Long-Term Market Outlook (2033+)

Appendix

About Pheonix Research

Disclaimer

Competitive Landscape

Competitive Landscape Content

Executive Framing

In the Thailand Japanese Restaurant Market, the competitive landscape is defined by a semi-consolidated structure in urban hubs and fragmented expansion across regional markets, creating a multi-layered competitive ecosystem. The market combines strong domestic chains, international Japanese brands, and a growing base of independent operators.

Leading players such as Oishi Group PCL, Fuji Japanese Restaurant Group, ZEN Corporation Group, MK Restaurant Group, and Yayoi dominate through extensive mall-based networks, standardized menus, and scalable franchise-like models.

Competitive intensity is moderate to high, driven by format diversification (casual dining, buffet, QSR), price segmentation, and continuous menu innovation. Unlike emerging Southeast Asian markets, Thailand exhibits higher maturity and brand saturation, particularly in Bangkok, making differentiation increasingly dependent on experience, efficiency, and brand positioning rather than mere presence.

Current Market Reality

The current competitive environment reflects a balanced mix of scale-driven chains and niche premium operators, with Bangkok acting as the epicenter of competition.

Large operators such as Oishi Group PCL and Fuji Japanese Restaurant Group maintain strong market control through:

- Mall-centric expansion strategies

- Affordable set menus and family dining formats

- High brand recall and operational consistency

Meanwhile, brands like Kouen Group and Kagonoya Thailand are capturing demand in buffet and premium casual segments, appealing to group dining and experiential consumption trends.

Key structural realities include:

- Mall Ecosystem Dominance:

Japanese restaurants are heavily concentrated in high-traffic retail environments such as Bangkok’s premium malls. - Format Diversification:

The market spans quick-service sushi counters, ramen chains, buffet yakiniku, and premium omakase, increasing intra-category competition. - Digital Integration:

Tablet-based ordering, POS analytics, and integration with delivery platforms such as GrabFood and foodpanda are now standard. - Regional Expansion Momentum:

Growth is accelerating in EEC, Chiang Mai, and Phuket, where competition is less saturated but rapidly intensifying. - Price Sensitivity with Premium Overlay:

Consumers demand value-for-money offerings, even within premium dining formats.

Key Signals And Evidence

The competitive dynamics are reinforced by several key signals:

- Chain Dominance with Expanding Networks:

Major groups like Oishi Group PCL continue aggressive expansion, reinforcing brand-led consolidation in urban centers. - Buffet & Value Dining Growth:

The rise of all-you-can-eat sushi and yakiniku formats reflects consumer preference for high perceived value. - Technology Standardization:

Tablet ordering, AI-enabled demand forecasting, and digital queue systems are becoming baseline operational features. - Delivery Ecosystem Integration:

Platforms such as GrabFood and LINE MAN are critical for demand capture beyond dine-in. - Tourism-Driven Premium Demand:

Cities like Phuket and Bangkok are witnessing growth in premium omakase and fine dining concepts. - Sustainability Pressures:

Increasing scrutiny on seafood sourcing is influencing procurement strategies and brand positioning.

These signals highlight a transition toward a hybrid competitive model, combining scale efficiency, digital integration, and experiential differentiation.

Strategic Implications

The Thailand Japanese restaurant competitive landscape requires multi-tier strategic alignment, balancing operational scale with differentiated consumer experiences.

1. Scale Advantage vs Market Saturation

Large chains benefit from scale, but saturation in Bangkok necessitates innovation and regional expansion strategies.

2. Value Positioning is Critical

Affordable premium offerings (buffets, combo meals) are essential to maintain high customer turnover and loyalty.

3. Digital Integration as Baseline Capability

Technology adoption is no longer a differentiator but a minimum requirement for operational efficiency and customer engagement.

4. Localization Within Authenticity Framework

Menus must balance authentic Japanese flavors with Thai preferences to ensure mass adoption and repeat consumption.

5. Expansion into Emerging Corridors

EEC and secondary cities present high-growth opportunities with lower competitive density.

6. Supply Chain Sensitivity

Dependence on imported seafood creates cost volatility and supply risk, requiring strategic sourcing diversification.

Forward Outlook

Looking ahead, the Thailand Japanese Restaurant Market is expected to evolve into a digitally optimized, value-driven, and experience-enhanced ecosystem.

Key forward trends include:

- AI-Driven Operational Optimization:

Advanced analytics will improve demand forecasting, reduce waste, and enhance profitability. - Expansion of Premium Casual Segment:

The intersection of affordability and quality will define the fastest-growing competitive segment. - Sustainability as Competitive Requirement:

Ethical sourcing and eco-friendly practices will increasingly influence brand perception and regulatory compliance. - Growth of Hybrid Dining Models:

Restaurants will integrate dine-in, delivery, and cloud kitchen operations to maximize revenue streams. - Regional Market Acceleration:

EEC, Chiang Mai, and Phuket will emerge as key competitive battlegrounds. - Experience-Led Differentiation:

Ambiance, presentation, and social dining appeal will become central to competitive positioning.

In conclusion, the Thailand Japanese Restaurant Market is transitioning toward a structured yet dynamic competitive environment, where leadership will be defined by the ability to integrate scale, digital intelligence, value positioning, and experiential dining into a cohesive strategy.

Operators that successfully balance cost efficiency with premium perception and technological advancement will secure long-term competitive advantage in this evolving market.

Value Chain

Executive Framing

In the Thailand Japanese Restaurant Market, the value chain is highly structured, franchise-driven, and increasingly digitized, reflecting one of the most mature Japanese dining ecosystems in Southeast Asia. With market growth from USD 1.45 billion in 2025 to USD 2.31 billion by 2033 (CAGR 6.0%), value chain efficiency is central to sustaining profitability amid rising competition and premiumization trends.

The operational backbone is defined by standardized chain and franchise networks, supported by omnichannel distribution (dine-in, takeaway, delivery, and retail counters). Supply chain complexity remains moderate but quality-sensitive, particularly due to dependence on seafood sourcing and consistency requirements across multi-location formats.

As the market scales across Bangkok and emerging regions like the Eastern Economic Corridor (EEC), the value chain must balance cost efficiency, menu standardization, and localized adaptability, making operational precision a key competitive differentiator.

Current Market Reality

The Thailand Japanese restaurant value chain operates within a well-organized, multi-tier ecosystem, combining centralized procurement with decentralized service delivery.

Core structural characteristics:

- Centralized sourcing with regional distribution

Large chains manage procurement of seafood, meats, and specialty ingredients through centralized systems, ensuring consistency and cost control. - Mall-centric distribution infrastructure

High reliance on shopping malls and retail complexes creates predictable footfall but also introduces rental cost pressures. - Franchise-led scalability

Structured franchise and chain expansion models enable rapid replication of standardized menus and service formats. - Integrated digital systems

AI-powered POS systems, tablet ordering, and loyalty platforms are embedded across operations to enhance throughput and customer retention.

Key constraints:

- Seafood sourcing sensitivity

Quality and price volatility in seafood supply directly impact margins and menu pricing strategies. - High competition density in urban hubs

Bangkok’s saturation increases customer acquisition costs and compresses margins. - Labor and service quality dependency

Maintaining consistent service standards across chains remains a challenge, particularly in expanding regions. - Aggregator dependency for delivery channels

Third-party delivery platforms introduce commission pressures, impacting profitability.

Despite these challenges, operators are leveraging:

- AI-driven inventory and demand planning

- Cloud kitchens for delivery optimization

- Retail sushi counters in supermarkets for volume expansion

Key Signals And Evidence

Several strong signals are shaping the Thailand Japanese restaurant value chain:

1. Expansion of Franchise and Chain Dominance

The increasing dominance of organized chains is driving standardization in procurement, pricing, and operations, improving efficiency but intensifying competition.

2. AI-Enabled Operational Optimization

Adoption of AI in ordering, kitchen workflows, and demand forecasting is improving table turnover, cost control, and waste reduction.

3. Growth of Omnichannel Distribution

Integration of dine-in, takeaway, and delivery channels is enhancing revenue diversification, but also adding complexity to logistics and operations.

4. Rising Importance of Seafood Supply Stability

Dependence on high-quality seafood introduces supplier power dynamics and cost volatility, making sourcing strategy a critical value chain component.

5. Premium Casual Segment Expansion

The growth of mid-premium dining formats is shifting the value chain toward experience + efficiency hybrid models, balancing cost and quality.

6. Sustainability and Responsible Sourcing Pressure

Increasing focus on eco-friendly packaging and sustainable seafood sourcing is adding compliance and cost layers to procurement systems.

Strategic Implications

The evolving value chain signals translate into several strategic priorities:

- Strengthening Centralized Procurement Systems

Efficient sourcing and supplier partnerships are critical to managing cost volatility and maintaining quality consistency. - Franchise Model Optimization

Enhancing franchise governance and operational standardization ensures scalability without compromising brand integrity. - Omnichannel Integration Strategy

Seamless coordination between dine-in, delivery, and takeaway channels is essential for maximizing asset utilization and revenue streams. - AI as a Core Efficiency Driver

Investment in AI-driven analytics, smart kitchens, and digital ordering systems is key to sustaining margins in a competitive environment. - Seafood Supply Chain Risk Mitigation

Diversifying sourcing and establishing long-term supplier contracts can reduce exposure to price fluctuations and supply disruptions. - Experience-Led Differentiation

Combining operational efficiency with strong brand experience (ambiance, service, presentation) is essential for customer retention.

Forward Outlook

Looking ahead, the Thailand Japanese restaurant value chain is set to evolve into a highly optimized, technology-driven, and sustainability-aligned ecosystem.

Key future developments:

- Deeper AI integration across ordering, kitchen operations, and supply chain management

- Expansion of cloud kitchens and retail-integrated formats

- Advanced seafood traceability and sustainable sourcing systems

- Greater penetration into emerging urban corridors beyond Bangkok

- Enhanced personalization through data-driven customer engagement

As competition intensifies, value chain excellence—rather than concept novelty—will define long-term success.

Operators that effectively integrate:

- centralized sourcing,

- digital infrastructure, and

- franchise scalability

will achieve superior margin control, operational efficiency, and market expansion in Thailand’s increasingly sophisticated Japanese dining landscape.

Investment Activity

Executive Summary – Investment Activity

Investment Framing

The Thailand Japanese Restaurant Market is experiencing structured and sustained investment momentum, supported by its mature consumer base, strong cultural alignment with Japanese cuisine, and expanding tourism economy. With the market projected to grow from USD 1.45 billion in 2025 to USD 2.31 billion by 2033 (CAGR 6.0%), capital allocation is increasingly focused on scalable formats, premium-casual expansion, and technology-enabled operations.

Investment activity reflects a balanced risk-return profile, where investors are leveraging Thailand’s stable demand environment while targeting operational efficiency, brand standardization, and geographic expansion beyond Bangkok.

Current Investment Landscape

The investment ecosystem is defined by chain-led expansion and franchise scalability, with major players such as Oishi Group, Fuji Group, and ZEN Corporation driving multi-format growth strategies.

Capital is being deployed across:

- Mall-based dining ecosystems (core revenue drivers)

- Tourism-centric premium formats (Bangkok, Phuket, Pattaya)

- Emerging regional clusters (EEC, Chiang Mai)

- Cloud kitchens and delivery-first brands

Investors are prioritizing:

- Standardized franchise models for rapid scaling

- Mid-premium casual dining formats with high repeat consumption

- Operational digitization to enhance margins and efficiency

Key Investment Signals

The market exhibits several strong investment signals:

- Franchise and Chain Dominance:

Expansion of structured chains indicates investor preference for predictable, scalable business models. - Premium-Casual Expansion:

Capital is flowing into mid-to-premium dining formats, balancing affordability with experience. - Tourism-Linked Capital Allocation:

Investment concentration in Bangkok and Southern Thailand reflects high ROI from tourist-driven demand. - Technology Integration:

Adoption of AI-powered ordering, POS analytics, and kitchen automation is improving cost control and throughput. - Localization Strategy Investment:

Brands are investing in menu adaptation and pricing strategies tailored to Thai consumer preferences.

Structural Investment Drivers

- Mature Demand with Cultural Affinity

Strong acceptance of Japanese cuisine ensures consistent revenue visibility and lower market risk. - Tourism and Expat Consumption Stability

High tourist inflows and expatriate communities provide premium demand support. - Mall-Centric Retail Infrastructure

Thailand’s развит mall ecosystem enables high footfall and scalable restaurant deployment. - Digital Ecosystem Penetration

Delivery platforms and AI tools are driving efficiency, personalization, and repeat consumption.

Strategic Implications for Investors

- Preference for Scalable Chains:

Franchise and multi-unit formats offer predictable expansion and operational consistency. - Balanced Portfolio Strategy:

Investors should combine premium formats (omakase, yakiniku) with high-volume casual chains. - Regional Diversification Opportunity:

Growth in EEC and secondary cities provides early-stage expansion advantages. - Technology as Core Differentiator:

Digital integration is no longer optional — it is central to margin optimization and customer retention.

Forward Investment Outlook

Investment activity is expected to remain steady and expansion-oriented, with:

- Short-term (1–3 years):

Franchise scaling and mall-based expansion - Mid-term (3–7 years):

Regional penetration and cloud kitchen growth - Long-term:

Fully integrated AI-driven, omni-channel restaurant ecosystems

Final Investment Perspective

The Thailand Japanese Restaurant Market represents a moderate-growth, low-volatility investment environment, supported by strong fundamentals and scalable business models.

Capital will increasingly favor:

- Chain-driven expansion

- Premium-casual positioning

- Technology-enabled operations

- Tourism-aligned locations

Overall, the market offers stable, repeatable returns with strategic upside, particularly for investors focused on brand strength, operational efficiency, and regional expansion leverage.

Technology & Innovation

Executive Framing

The Thailand Japanese Restaurant market is evolving into a digitally integrated, premium-casual dining ecosystem, where technology enhances operational precision while preserving culinary authenticity. With strong cultural affinity toward Japanese cuisine and rising demand for high-quality, experience-driven dining, technology is increasingly embedded across service, kitchen operations, and customer engagement layers.

This transformation is particularly significant as operators adopt AI-enabled ordering systems, POS-integrated analytics, and smart inventory management, enabling scalable growth across both premium and casual dining formats. The market reflects a shift from traditional restaurant operations toward data-driven, efficiency-optimized foodservice models.

The innovation landscape is characterized by moderate innovation intensity with low-to-moderate patent activity, where differentiation is driven by execution, service experience, and digital integration rather than proprietary technology ownership. The ecosystem is transitioning into a digitally mature but still expanding operational framework.

Current Market Reality

The current market is defined by broad adoption of digital ordering, kitchen automation, and delivery integration, especially across Bangkok and major urban clusters. Leading players such as Oishi Group PCL, ZEN Corporation Group, Yayoi (Plenus Thailand), and Fuji Japanese Restaurant Group are actively leveraging technology to enhance service speed, cost efficiency, and customer retention.

Core technology layers include:

- Tablet-based and QR-driven ordering systems

- AI-assisted demand forecasting and inventory optimization

- Digital queue and reservation management platforms

- Cloud kitchen integration for delivery-first expansion

For instance, Oishi Group PCL has scaled buffet automation and digital ordering systems, while ZEN Corporation Group focuses on loyalty ecosystems and data-driven customer engagement.

The market is in a growth-to-early maturity stage, where digital infrastructure is widely implemented, but AI-driven personalization and full automation are still evolving.

Demand drivers include:

- Growth in mall-based dining ecosystems

- Increasing adoption of delivery and takeaway channels

- Rising consumer expectations for fast, seamless service

- Need for cost control amid rising ingredient prices (especially seafood)

Key Signals And Evidence

- AI Integration in Core Operations

Restaurants are increasingly deploying AI for sales forecasting, staffing optimization, and inventory control, improving margins and reducing waste. - Expansion of Digital Ordering Ecosystems

Platforms like GrabFood, LINE MAN, and foodpanda are accelerating demand aggregation and delivery scalability. - Rise of Premium-Casual Technology Integration

Casual dining formats are adopting fine-dining-like reservation systems and digital engagement tools, blurring segment boundaries. - Sustainability as an Operational Requirement

Increased adoption of traceable seafood sourcing, energy-efficient kitchens, and reduced plastic packaging. - Localization Through Data Analytics

Operators are leveraging data insights to tailor menus to Thai preferences while maintaining Japanese authenticity. - Cloud Kitchen & Delivery Optimization

Delivery-only formats are using AI-based location intelligence and demand clustering to optimize operations.

Strategic Implications

For Restaurant Operators:

Operators must transition toward digitally enabled multi-channel business models, integrating dine-in, takeaway, and delivery seamlessly. Technology directly impacts:

- Table turnover rates

- Customer experience consistency

- Profitability through waste reduction

However, maintaining authentic Japanese dining experience alongside digital efficiency remains critical.

For Technology Providers:

Opportunities lie in:

- AI-based restaurant management systems

- Digital ordering and payment ecosystems

- Supply chain traceability solutions

Challenges include:

- Customization for diverse restaurant formats (buffet, omakase, QSR)

- Integration across fragmented operator ecosystems

For Market Structure:

- Established chains gain advantage through scale, brand trust, and digital investment capacity

- Mid-tier players compete via price positioning and delivery optimization

- Independent operators rely on aggregator platforms and niche experiences

Risk Layer:

- High dependency on seafood supply chains

- Competitive saturation in Bangkok

- Technology cost vs ROI balance for smaller operators

Forward Outlook (2026–2033)

The Thailand Japanese Restaurant market is expected to evolve into a highly optimized, AI-assisted, and sustainability-driven dining ecosystem.

Key future developments include:

- AI-Personalized Dining Experiences

Real-time menu recommendations based on user behavior, dietary preferences, and past orders. - Advanced Kitchen Automation

Semi-robotic systems supporting chefs in preparation, consistency, and hygiene. - Blockchain-Based Seafood Traceability

Ensuring authenticity, safety, and sustainability of imported ingredients. - Hybrid Dining + Delivery Models

Restaurants functioning as both experience centers and fulfillment hubs. - Immersive Premium Dining

Technology-enhanced omakase and themed dining experiences integrating storytelling and digital interaction. - Expansion into Secondary Cities via Tech Enablement

Scalable digital systems enabling rapid expansion beyond Bangkok into EEC and regional clusters.

The market will continue to be driven by:

- Tourism recovery and premium dining demand

- Urban middle-class expansion

- Increasing reliance on digital ordering and delivery

Final Strategic View

The Thailand Japanese Restaurant market is transitioning into a technology-enabled premium casual ecosystem, where competitive advantage lies in balancing operational efficiency with authentic dining experiences.

Brands that successfully integrate:

- AI-driven operational intelligence

- Digital customer engagement platforms

- Sustainable sourcing systems

- Localization through data analytics

will emerge as market leaders, while others risk losing relevance in an increasingly experience-driven and digitally competitive landscape.

Market Risk

Executive Framing

The Thailand Japanese Restaurant Market is entering a phase of structured expansion accompanied by moderate but multi-dimensional risk exposure, primarily driven by supply chain sensitivity, tourism dependence, and competitive saturation in urban centers. While the overall market risk level remains moderate, the interplay between premium casual positioning and cost-sensitive consumer segments introduces a complex risk equilibrium.

Japanese dining in Thailand operates within a hybrid model—spanning affordable sushi chains to high-end omakase experiences—making it simultaneously scalable and operationally sensitive. The reliance on imported seafood, particularly from Japan and global markets, exposes operators to currency fluctuations, geopolitical trade frictions, and supply inconsistencies.

Additionally, the market’s strong linkage with tourism and expatriate consumption creates demand cyclicality, especially in cities like Bangkok and Phuket. As competition intensifies across mall-based formats and cloud kitchens, pricing pressure and brand differentiation challenges are becoming more pronounced. These structural dynamics are reshaping profitability, operational stability, and long-term market positioning.

Current Market Reality

The current Thailand Japanese Restaurant Market reflects a mature yet highly competitive ecosystem. Key players such as Oishi Group PCL, Fuji Japanese Restaurant Group, and ZEN Corporation are expanding through mall-centric formats, franchise scalability, and technology-enabled dining experiences.

Digital transformation is well embedded, with tablet-based ordering, AI-powered inventory systems, and delivery platform integrations becoming standard across mid-tier and premium segments. The widespread adoption of aggregators such as GrabFood and LINE MAN has significantly enhanced accessibility and demand reach.

However, operational pressures remain evident. High rental costs in premium malls, combined with rising labor and ingredient expenses, are compressing margins. The dependency on imported seafood continues to create volatility in cost structures, particularly for sushi and sashimi segments.

Furthermore, the market is experiencing increasing fragmentation in regional cities, where local operators and cloud kitchens are intensifying competition. While Bangkok remains relatively consolidated, emerging regions exhibit price-driven competition and lower brand loyalty, adding complexity to expansion strategies.

Key Signals And Evidence

A primary signal shaping the risk landscape is the continued dependence on imported seafood and premium ingredients. Fluctuations in global logistics, exchange rates, and sourcing regulations directly impact menu pricing and profitability, particularly for high-end and authenticity-focused formats.

Another critical signal is the strong correlation between tourism flows and restaurant demand. Tourist-heavy regions such as Phuket and Pattaya exhibit revenue volatility based on seasonal and macroeconomic travel patterns, increasing demand unpredictability.

The proliferation of cloud kitchens and delivery-first Japanese brands is lowering entry barriers and intensifying competition. This trend is contributing to pricing pressure, especially in the quick-service and mid-range segments, while also challenging traditional dine-in models.

Consumer behavior is also evolving rapidly, with increasing demand for affordable sushi sets, health-conscious meals, and visually appealing dining experiences. This diversification in demand is increasing menu complexity and operational strain.

Additionally, rising labor costs and the limited availability of highly skilled Japanese chefs present ongoing operational constraints, particularly for premium and experiential dining formats.

Strategic Implications

These signals highlight the need for strategic recalibration across multiple dimensions.

First, supply chain resilience must be prioritized through diversified sourcing strategies, including regional procurement and strategic supplier partnerships to mitigate import dependency risks.

Second, operators must balance premium positioning with affordability by introducing tiered menu pricing and hybrid dining formats that cater to both mass and high-end segments.

Third, reducing reliance on tourism-driven demand will be critical. Expanding into local consumer segments and secondary cities with tailored offerings can stabilize revenue streams.

Fourth, technology investments should focus on enhancing operational efficiency and customer retention, including AI-driven demand forecasting, personalized promotions, and integrated loyalty ecosystems.

Finally, differentiation through brand identity, dining experience, and authenticity will be essential to sustain competitive advantage in an increasingly crowded market.

Forward Outlook

Looking ahead to 2026–2033, the Thailand Japanese Restaurant Market is expected to sustain steady growth, supported by continued urbanization, tourism recovery, and digital ecosystem expansion. However, the market will become increasingly segmented, with clear distinctions between premium, mid-range, and delivery-driven formats.

Technological integration will deepen, enabling operators to optimize inventory, reduce waste, and enhance customer personalization. At the same time, sustainability will become a more critical factor, particularly in seafood sourcing and packaging practices, driven by regulatory and consumer expectations.

Competitive intensity is expected to rise further, especially in urban and tourist-centric regions, requiring stronger brand positioning and operational efficiency.

In conclusion, the Thailand Japanese Restaurant Market presents a balanced risk-reward profile. While growth prospects remain strong, success will depend on the ability to manage supply chain volatility, navigate demand fluctuations, and build resilient, technology-enabled, and differentiated dining ecosystems.

Regulatory Landscape

Executive Framing

The regulatory and policy environment in the Thailand Japanese Restaurant Market plays a foundational role in maintaining food safety standards, ensuring supply chain integrity, governing franchise expansion, and supporting sustainable dining practices. As the market matures into a premium-casual and digitally integrated ecosystem, regulatory frameworks are increasingly influencing operational efficiency, cost structures, and innovation adoption.

With the market projected to grow from USD 1.45 billion in 2025 to USD 2.31 billion by 2033, regulatory oversight becomes essential in areas such as seafood quality control, restaurant licensing, labor compliance, and digital transaction governance. These frameworks are particularly critical given the high reliance on imported ingredients, tourism-driven demand, and the integration of AI-enabled ordering systems.

As operators expand across Bangkok and emerging regions like the Eastern Economic Corridor (EEC), navigating regulatory requirements becomes central to scalability, brand consistency, and long-term competitiveness during the 2026–2033 forecast period.

Current Market Reality

The current regulatory landscape in the Thailand Japanese Restaurant Market is shaped by a structured yet evolving framework centered on food safety, import regulations, licensing, and digital commerce compliance.

Food safety regulations are rigorously enforced, particularly for Japanese cuisine that relies heavily on raw seafood. Restaurants must comply with strict hygiene protocols, cold chain logistics, and quality verification standards to ensure consumer safety. This is especially critical in premium segments such as sushi and omakase dining.

Seafood import regulations play a significant role, as many Japanese restaurants depend on imported fish and specialty ingredients. Compliance with import quality standards, inspection procedures, and traceability requirements directly impacts procurement strategies and operational timelines.

Restaurant licensing and zoning policies are well-established, particularly in urban hubs like Bangkok and tourist regions such as Phuket. Operators must obtain multiple permits related to food service, business operations, and location-specific approvals, especially in mall-based and hotel-integrated environments.

The rapid growth of digital ordering and delivery platforms such as GrabFood, LINE MAN, and Foodpanda introduces additional regulatory layers related to taxation, digital payments, and platform accountability. AI-enabled ordering systems and loyalty platforms must align with data protection and digital transaction regulations.

Sustainability is also emerging as a regulatory focus area, with increasing emphasis on responsible seafood sourcing, reduction of single-use plastics, and energy-efficient restaurant operations, particularly in premium and internationally positioned dining formats.

Key Signals and Evidence

The regulatory environment in the Thailand Japanese Restaurant Market is influenced by several key signals:

- Food Safety and Hygiene Enforcement:

Strict compliance requirements for food handling, preparation, and storage ensure safety and consistency, particularly for raw seafood-based cuisine. - Seafood Import and Traceability Regulations:

Regulations governing imported seafood quality, certification, and traceability are critical for maintaining authenticity and safety in Japanese dining. - Business Licensing and Zoning Frameworks:

Multi-tier licensing requirements influence restaurant setup, expansion, and location strategies across urban and tourism-driven regions. - Digital Commerce and Platform Regulations:

Growth in app-based ordering and delivery services introduces compliance requirements around taxation, digital payments, and consumer data protection. - Labor and Operational Compliance:

Employment regulations and wage standards impact staffing models, particularly in labor-intensive dining formats. - Sustainability and Environmental Signals:

Increasing regulatory focus on eco-friendly packaging, waste reduction, and sustainable sourcing is shaping procurement and operational practices.

These signals collectively create a compliance-driven environment that balances consumer safety, operational transparency, and sustainability.

Strategic Implications

The regulatory framework creates both constraints and strategic leverage points:

- Moderate Entry Barriers with Structured Compliance:

Licensing, food safety, and import regulations create manageable but essential entry requirements, favoring organized and well-capitalized operators. - Supply Chain Sensitivity:

Dependence on imported seafood increases exposure to regulatory checks, impacting cost structures and supply stability. - Cost and Margin Pressures:

Compliance with safety, sustainability, and labor standards increases operational costs, influencing pricing and profitability. - Technology as a Compliance Enabler:

AI-driven ordering systems, inventory tracking, and digital platforms enhance regulatory adherence and operational transparency. - Location-Based Strategy Optimization:

Zoning and licensing frameworks influence expansion into high-growth regions such as EEC, Phuket, and Chiang Mai. - Sustainability as a Competitive Differentiator:

Early adoption of responsible sourcing and eco-friendly practices strengthens brand positioning in premium and tourist-driven markets.

Forward Outlook (2026–2033)

Looking ahead, the regulatory landscape in the Thailand Japanese Restaurant Market is expected to become more integrated, sustainability-driven, and digitally aligned.

Food safety regulations will likely become more advanced, incorporating stricter monitoring of seafood quality, enhanced traceability systems, and tighter inspection protocols. Import regulations may also evolve to ensure higher standards of quality and sustainability for seafood sourcing.

Digital regulations will expand alongside AI adoption, requiring improved data protection, transparent algorithm usage, and secure digital payment ecosystems across ordering platforms.

Environmental policies are expected to intensify, driving stricter compliance with sustainable sourcing, waste management, and reduction of plastic usage, particularly in urban and tourism-centric markets.

Regional development zones such as the Eastern Economic Corridor (EEC) may introduce more structured regulatory frameworks to support organized restaurant expansion while maintaining quality and sustainability standards.

Companies that proactively align with these evolving regulations, invest in compliance-driven innovation, and integrate sustainability into their core operations will be best positioned to capitalize on the projected 6.0% CAGR and strengthen long-term market leadership.

Final Insight

The regulatory landscape in the Thailand Japanese Restaurant Market is evolving into a structured, compliance-driven, and sustainability-oriented system that supports premiumization and digital transformation. Operators that successfully integrate regulatory adherence with technological innovation, supply chain optimization, and localized expansion strategies will define the next phase of growth in Thailand’s dynamic Japanese dining ecosystem.