Global Antibody Drug Conjugates (ADC) Market Size and Share Analysis 2026-2033

Global Antibody Drug Conjugates (ADC) Market Forecast Snapshot (2026–2033)

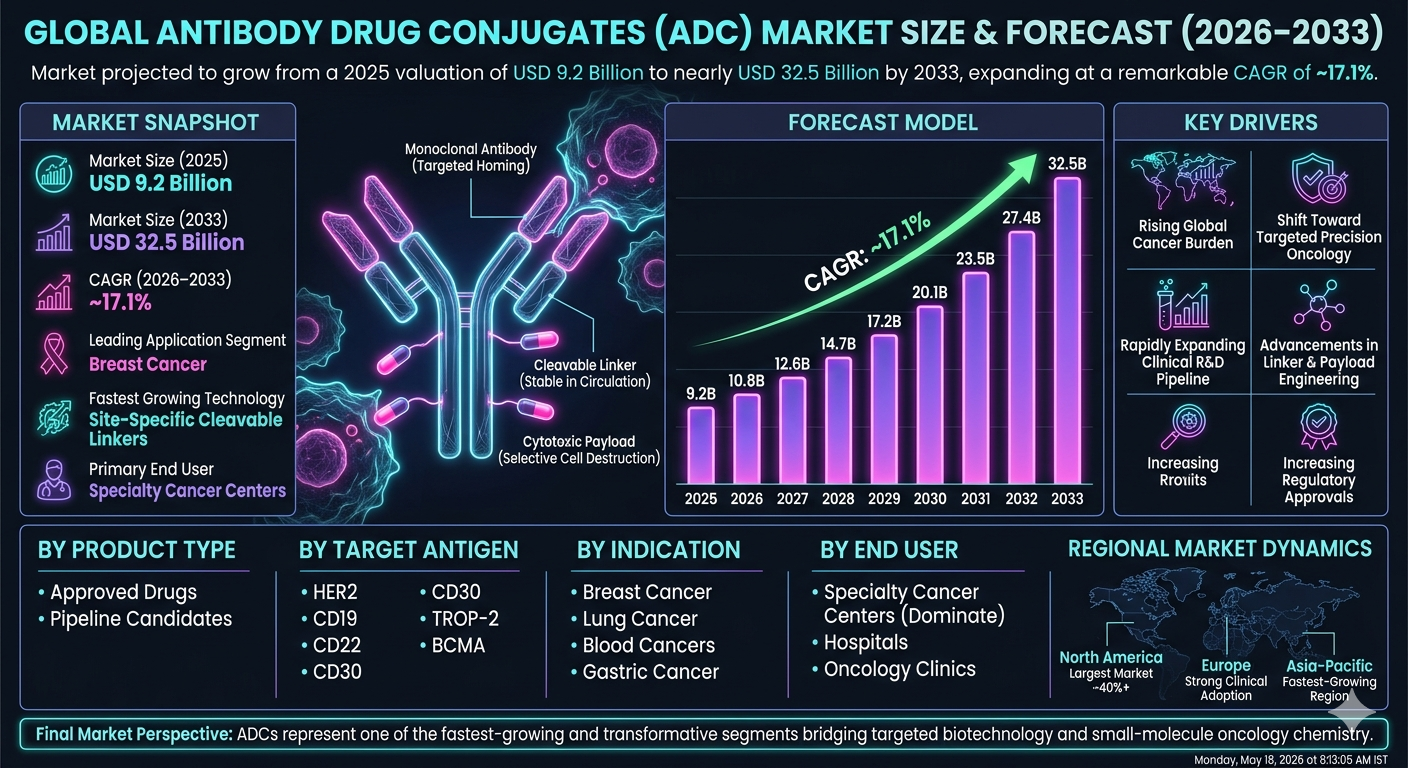

| Metric | Value |

|---|---|

| Market Size (2025) | USD 9.2 Billion |

| Market Size (2033) | USD 32.5 Billion |

| CAGR (2026–2033) | 17.1% |

| Largest Segment | Breast Cancer |

| Fastest Growing Segment | TROP-2 Targeted ADCs |

| Leading End-Use Segment | Specialty Cancer Centers |

| Key Growth Driver | Rising Cancer Prevalence and Increasing Adoption of Targeted Oncology Therapies |

| Major Opportunity | Next-Generation ADCs, Bispecific ADCs, and Immunotherapy Combination Treatments |

| Top Region | North America |

| Fastest Growing Region | Asia-Pacific |

Global Antibody Drug Conjugates (ADC) Market Size & Forecast

The Global Antibody Drug Conjugates (ADC) Market is expected to witness exceptional growth during the forecast period from 2026 to 2033. The market was valued at approximately USD 9.20 billion in 2025 and is projected to reach nearly USD 32.50 billion by 2033, registering a CAGR of 17.10%. The market growth is primarily driven by the increasing prevalence of cancer, rising demand for targeted therapies, growing investment in oncology drug development, and advancements in biologics and precision medicine. Antibody drug conjugates have emerged as one of the most promising therapeutic approaches in oncology by combining the targeting capability of monoclonal antibodies with the potency of cytotoxic drugs. In addition, expanding clinical pipelines, favorable regulatory approvals, and strategic collaborations between pharmaceutical and biotechnology companies are supporting long-term market expansion.Global Antibody Drug Conjugates (ADC) Market Overview

Antibody Drug Conjugates (ADCs) are targeted biopharmaceutical therapies that combine monoclonal antibodies with highly potent cytotoxic agents through specialized chemical linkers. The market includes approved ADC therapeutics, investigational ADC candidates, linker technologies, payload technologies, and ADC development and manufacturing services. ADCs are primarily utilized in oncology treatment, targeting specific cancer cells while minimizing damage to healthy tissues. The market is rapidly evolving toward next-generation ADCs with improved targeting precision, enhanced efficacy, reduced toxicity, and broader therapeutic applications.Structural Drivers of Market Growth

1. Innovation and Commercialization Acceleration

Rapid advancements in monoclonal antibody engineering, linker chemistry, payload development, and site-specific conjugation technologies are transforming ADC development. New-generation ADC platforms are improving therapeutic efficacy and expanding treatment options across multiple cancer indications.Market Implications

Companies investing in innovative ADC platforms, advanced payload technologies, and precision oncology research are expected to strengthen market leadership.2. Compliance and Risk Repricing

Stringent clinical trial requirements, biologics manufacturing standards, pharmacovigilance obligations, and oncology drug approval regulations are influencing market development. Regulatory agencies are increasingly supporting breakthrough cancer therapies through accelerated approval pathways.Market Implications

Firms with strong clinical development capabilities and regulatory expertise are likely to gain competitive advantages and faster commercialization opportunities.3. Competitive and Value-Chain Reconfiguration

The market is highly competitive as pharmaceutical companies, biotechnology firms, contract development organizations, and research institutions expand ADC development programs. Strategic licensing agreements, mergers, acquisitions, and co-development partnerships are reshaping industry value chains.Market Implications

Companies focusing on differentiated ADC technologies and strategic collaborations may achieve stronger pipeline growth and market positioning.4. Capital and Capacity Scaling

Increasing investments in oncology R&D, biologics manufacturing facilities, and clinical trial programs are accelerating market growth. The expanding number of ADC candidates entering clinical development is creating significant manufacturing and commercialization opportunities.Market Implications

Organizations scaling ADC production capabilities and development infrastructure are expected to capture future market opportunities.Market Segmentation Analysis

By Product Type

1. Oncology-Focused ADC Therapeutics

This remains the largest segment due to widespread adoption in breast cancer, hematologic malignancies, and solid tumor treatments.2. Investigational ADC Candidates

Strong growth driven by expanding clinical trial pipelines and novel therapeutic targets.3. ADC Development Services

Increasing demand from biotechnology companies and pharmaceutical outsourcing initiatives.4. Linker & Payload Technologies

Critical segment supporting next-generation ADC innovation.By Technology

1. Cleavable Linker-Based ADCs

Largest segment due to broad clinical utilization and effective drug release mechanisms.2. Non-Cleavable Linker-Based ADCs

Growing adoption due to enhanced stability and targeted delivery capabilities.3. Site-Specific Conjugation Technologies

Fastest-growing segment driven by improved therapeutic precision and safety profiles.By End User

1. Hospitals & Cancer Treatment Centers

Largest segment due to high patient volumes and advanced oncology treatment capabilities.2. Specialty Oncology Clinics

Growing demand for targeted cancer therapies and personalized treatment approaches.3. Research & Academic Institutions

Significant utilization for oncology research and ADC innovation programs.4. Pharmaceutical & Biotechnology Companies

Increasing investment in ADC development and commercialization activities.Regional Market Dynamics

North America

North America dominates the global ADC market due to strong oncology research infrastructure, extensive biologics development, high healthcare expenditure, and favorable regulatory support.Europe

Europe remains a major market supported by advanced cancer treatment programs, pharmaceutical innovation, and increasing clinical research activities.Asia-Pacific

Asia-Pacific is the fastest-growing region due to expanding biotechnology industries, rising cancer incidence, growing healthcare investments, and increasing participation in clinical trials.Latin America

Latin America is gradually expanding due to improving oncology care infrastructure and increasing access to advanced therapeutics.Middle East & Africa

The region is witnessing emerging growth driven by healthcare modernization, rising cancer awareness, and expanding access to specialty treatments.Competitive Landscape

The Global Antibody Drug Conjugates Market is highly competitive with major pharmaceutical companies, biotechnology innovators, and ADC-focused developers actively expanding their portfolios.Key Companies Operating in the Market Include:

- Seagen Inc. (Pfizer)

- AstraZeneca plc

- Daiichi Sankyo Company, Limited

- Roche Holding AG

- Gilead Sciences, Inc.

- AbbVie Inc.

- Merck & Co., Inc.

- Bristol Myers Squibb

- Takeda Pharmaceutical Company Limited

- ImmunoGen, Inc.

Strategic Outlook

The future of the ADC market will be shaped by next-generation conjugation technologies, novel payload innovations, precision oncology advancements, and expanded therapeutic indications. Artificial intelligence-assisted drug discovery, biomarker-driven patient selection, and personalized cancer treatment approaches will significantly enhance clinical outcomes and market adoption. The rise of targeted therapies and growing oncology treatment demand is expected to create substantial long-term growth opportunities.Final Market Perspective

The Global Antibody Drug Conjugates Market remains one of the fastest-growing segments within the biopharmaceutical and oncology industries. Rising cancer prevalence, continuous therapeutic innovation, and increasing adoption of targeted treatments continue driving long-term market growth. Companies capable of delivering safe, effective, scalable, and clinically differentiated ADC therapies will be best positioned to capture future opportunities. The convergence of biologics innovation, precision medicine, and advanced drug delivery technologies is expected to redefine the future of cancer treatment worldwide.Table of Contents

Table of Contents

- 1. Executive Summary

- 1.1 Global Antibody Drug Conjugates (ADC) Market Snapshot (2026-2033)

- 1.2 Market Size & CAGR Analysis

- 1.3 Largest & Fastest-Growing Indications

- 1.4 Key Regional Insights

- 1.5 Major Market Growth Drivers

- 1.6 Competitive Landscape Overview

- 1.7 Strategic Outlook Through 2033

- 2. Introduction & Market Overview

- 2.1 Definition of Antibody Drug Conjugates (ADCs)

- 2.2 Scope of the Study

- 2.3 Evolution of Targeted Cancer Therapeutics

- 2.4 ADC Structure: Antibody–Linker–Payload Mechanism

- 2.5 Oncology Treatment Landscape & Precision Medicine Shift

- 2.6 Regulatory Approval Framework for ADCs

- 2.7 Technological Innovations in ADC Development

- 3. Research Methodology

- 3.1 Primary Research

- 3.2 Secondary Research

- 3.3 Market Size Estimation Model

- 3.4 Forecast Assumptions (2026-2033)

- 3.5 Data Validation & Market Triangulation

- 4. Market Dynamics

- 4.1 Drivers

- 4.1.1 Rising Global Cancer Burden

- 4.1.2 Shift Toward Targeted Cancer Therapies

- 4.1.3 Expanding Clinical ADC Pipeline

- 4.1.4 Technological Advancements in Linkers & Payloads

- 4.1.5 Increasing Regulatory Approvals of ADC Drugs

- 4.2 Restraints

- 4.2.1 High Development & Manufacturing Costs

- 4.2.2 Complex Clinical Trial Design & Toxicity Management

- 4.2.3 Limited Target Antigen Availability

- 4.2.4 Supply Chain & Production Scalability Challenges

- 4.3 Opportunities

- 4.3.1 Next-Generation Bispecific ADC Development

- 4.3.2 Combination with Immunotherapy & Checkpoint Inhibitors

- 4.3.3 Expansion into Solid Tumor Indications

- 4.3.4 Biomarker-Driven Precision Oncology Applications

- 4.4 Challenges

- 4.4.1 Off-Target Toxicity Risks

- 4.4.2 Resistance Mechanisms in Cancer Cells

- 4.4.3 High Failure Rate in Late-Stage Trials

- 4.4.4 Intense Competitive Innovation Pressure

- 4.1 Drivers

- 5. Global ADC Market Analysis (USD Billion), 2026-2033

- 5.1 Market Size Overview

- 5.2 CAGR Analysis

- 5.3 Regional Revenue Distribution

- 5.4 Product Type Revenue Analysis

- 5.5 Indication-Based Market Performance

- 5.6 Target Antigen Revenue Trends

- 6. Market Segmentation (USD Billion), 2026-2033

- 6.1 By Product Type

- 6.1.1 Approved ADC Drugs

- 6.1.2 Pipeline ADC Candidates

- 6.2 By Indication

- 6.2.1 Breast Cancer

- 6.2.2 Lung Cancer

- 6.2.3 Blood Cancers (Lymphoma, Leukemia)

- 6.2.4 Gastric Cancer

- 6.2.5 Urothelial Cancer

- 6.2.6 Ovarian Cancer

- 6.2.7 Others

- 6.3 By Target Antigen

- 6.3.1 HER2

- 6.3.2 TROP-2

- 6.3.3 CD19

- 6.3.4 CD22

- 6.3.5 CD30

- 6.3.6 BCMA

- 6.3.7 Others

- 6.4 By End User

- 6.4.1 Hospitals

- 6.4.2 Oncology Clinics

- 6.4.3 Specialty Cancer Centers

- 6.4.4 Research Institutions

- 6.1 By Product Type

- 7. Market Segmentation by Geography

- 7.1 North America

- 7.2 Europe

- 7.3 Asia-Pacific

- 7.4 Latin America

- 7.5 Middle East & Africa

- 8. Competitive Landscape

- 8.1 Market Share Analysis

- 8.2 ADC Pipeline Benchmarking

- 8.3 Linker–Payload Technology Comparison

- 8.4 Strategic Partnerships & Licensing Deals

- 8.5 Mergers, Acquisitions & Co-development Strategies

- 9. Company Profiles

- 9.1 Seagen (Pfizer)

- 9.2 Daiichi Sankyo

- 9.3 Roche/Genentech

- 9.4 AstraZeneca

- 9.5 Gilead Sciences

- 9.6 ImmunoGen

- 9.7 Astellas Pharma

- 9.8 Takeda Pharmaceutical

- 9.9 Eisai Co., Ltd.

- 9.10 Mersana Therapeutics

- 10. Strategic Intelligence & Pheonix AI Insights

- 10.1 ADC Pipeline Forecast Engine

- 10.2 Payload Toxicity Prediction System

- 10.3 Clinical Success Probability Modeling

- 10.4 Biomarker & Target Discovery Analytics

- 10.5 Automated Porter’s Five Forces Analysis

- 11. Future Outlook & Strategic Recommendations

- 11.1 Expansion of Solid Tumor ADC Applications

- 11.2 Growth of Bispecific & Multi-Payload ADCs

- 11.3 Integration with Immuno-Oncology Therapies

- 11.4 Advances in Site-Specific Conjugation Technologies

- 11.5 Long-Term Market Outlook (2033+)

- 12. Appendix

- 13. About Pheonix Research

- 14. Disclaimer

Competitive Landscape

Global Antibody Drug Conjugates (ADC) Market Competitive Intensity & Market Structure Overview

The Global Antibody Drug Conjugates (ADC) Market is highly innovation-intensive, science-driven, and strategically consolidated around a small group of leading biopharmaceutical companies with strong oncology pipelines. The competitive landscape is defined by continuous R&D investment, rapid clinical pipeline expansion, and increasing focus on next-generation payload and linker technologies that improve efficacy and safety profiles.

The market structure is moderately consolidated at the top, with major players holding approved ADC portfolios and late-stage clinical assets, while a large number of biotechnology firms and academic collaborations contribute to early-stage innovation. Strategic alliances, licensing agreements, and acquisitions remain central to competitive positioning as companies seek to expand oncology portfolios and accelerate time-to-market.

Competition is primarily driven by clinical efficacy outcomes, regulatory approvals, biomarker-driven targeting strategies, and technological advancements in antibody engineering, linker stability, and payload potency. As ADCs expand across both hematologic malignancies and solid tumors, competitive intensity is expected to further increase.

Global Antibody Drug Conjugates (ADC) Market Competitive Intensity & Market Structure Current Scenario

Leading ADC Developers & Oncology Biopharmaceutical Companies

Seagen (Pfizer): A global leader in ADC innovation, with a strong commercial portfolio and deep expertise in linker-payload technology and hematologic malignancies.

Daiichi Sankyo: One of the fastest-growing ADC innovators, known for its HER2-targeting ADC advancements and strong oncology pipeline collaborations.

Roche / Genentech: A dominant player in oncology biologics with established ADC products and extensive clinical development programs across multiple tumor types.

AstraZeneca: Actively expanding its ADC portfolio through strategic collaborations and co-development agreements focused on solid tumor applications.

Gilead Sciences (ImmunoMedics legacy assets): Strengthening its oncology footprint through TROP-2 targeted ADC development and commercialization strategies.

ImmunoGen: A key ADC-focused biotechnology company specializing in novel payload technologies and antibody engineering platforms.

Astellas Pharma: Strong presence in hematologic malignancies and expanding ADC pipeline through global oncology partnerships.

Takeda: Focused on expanding oncology innovation through strategic investments in next-generation ADC research programs.

Eisai: Actively engaged in oncology drug development with growing interest in targeted ADC therapies.

Emerging Biotechnology Companies: Numerous mid-sized biotech firms and academic spin-offs are contributing to innovation in linker chemistry, payload design, and tumor-specific targeting mechanisms.

Key Competitive Intensity & Market Structure Dynamics in Global ADC Market

A major competitive driver in the ADC market is the rapid advancement of linker and payload technologies. Companies that successfully develop stable linkers and highly potent cytotoxic payloads are gaining a significant advantage in clinical efficacy and safety differentiation.

Another critical factor shaping competition is biomarker-driven patient selection. The ability to identify and target specific tumor antigens such as HER2, TROP-2, CD19, and BCMA is enabling more precise and effective treatment strategies, strengthening product differentiation.

Strategic collaborations between large pharmaceutical companies and biotechnology innovators are intensifying, as ADC development requires significant scientific expertise, manufacturing capability, and clinical trial infrastructure.

Mergers and acquisitions remain highly active in this space, as leading players acquire specialized biotech firms to strengthen their ADC pipelines and secure next-generation oncology assets.

Competition is also increasingly influenced by expansion into solid tumor indications, where clinical complexity is higher and differentiation depends heavily on tumor penetration efficiency and toxicity management.

Strategic Implications of Competitive Intensity & Market Structure in ADC Market

Companies are prioritizing pipeline diversification by developing multi-target ADC portfolios that span both hematologic cancers and solid tumors. This reduces dependency on single indications and strengthens long-term revenue potential.

Investment in manufacturing scalability and site-specific conjugation technologies is becoming essential to support commercial expansion and ensure consistent drug quality and stability.

Pharmaceutical firms are increasingly adopting combination therapy strategies, integrating ADCs with immune checkpoint inhibitors, chemotherapy, and targeted therapies to improve treatment outcomes.

Geographic expansion into Asia-Pacific markets is becoming a key strategic priority due to rising cancer prevalence, increasing clinical trial activity, and strong biotechnology ecosystems in China and Japan.

Artificial intelligence and computational biology are also emerging as competitive enablers, supporting antigen discovery, payload optimization, and clinical trial design efficiency.

Global Antibody Drug Conjugates (ADC) Market Competitive Intensity & Market Structure Forward Outlook

The ADC market is expected to become increasingly competitive as next-generation therapies enter late-stage clinical development and gain regulatory approvals across multiple oncology indications.

Future innovation is expected to focus on bispecific ADCs, novel payload classes, improved tumor-selective activation mechanisms, and enhanced safety profiles that expand patient eligibility.

Market consolidation is likely to continue as larger pharmaceutical companies acquire specialized biotech firms to strengthen ADC technology platforms and accelerate global commercialization.

Precision oncology and biomarker-guided treatment approaches will further intensify competition by enabling more targeted and clinically differentiated therapies.

Overall, the Global ADC Market is expected to remain highly competitive but structurally growth-oriented, driven by continuous innovation, expanding clinical applications, and strong global demand for targeted cancer therapies through 2033.

Value Chain

Global Antibody Drug Conjugates (ADC) Market Value Chain & Supply Chain Evolution Overview

The global Antibody Drug Conjugates (ADC) market value chain represents a highly complex and innovation-intensive pharmaceutical ecosystem that integrates biologics, synthetic chemistry, and precision oncology manufacturing. The ADC value chain is evolving rapidly due to rising demand for targeted cancer therapies, increasing clinical success rates, and continuous advancements in linker chemistry, antibody engineering, and cytotoxic payload design.

The value chain begins with upstream biological and chemical input sourcing, including monoclonal antibody development, cell line engineering, antigen identification, and production of highly potent cytotoxic payloads. These inputs require advanced biotechnological capabilities, strict quality control systems, and highly specialized manufacturing environments due to the sensitivity and toxicity of ADC components.

The manufacturing stage forms the core of the ADC ecosystem and involves antibody production, linker-payload conjugation, purification, formulation, and fill-finish processes. This stage requires highly controlled bioprocessing facilities, advanced conjugation technologies such as site-specific binding, and strict containment systems for handling highly potent active pharmaceutical ingredients (HPAPIs).

Contract development and manufacturing organizations (CDMOs) play a critical role in scaling ADC production, as many pharmaceutical companies rely on external partners for antibody production, conjugation services, and clinical-to-commercial manufacturing transitions. The increasing complexity of ADC production has led to strong demand for specialized CDMOs with integrated biologics and HPAPI capabilities.

The downstream distribution network involves highly regulated pharmaceutical logistics systems, including cold chain storage, specialty drug distributors, hospital pharmacy channels, and oncology treatment centers. Due to the high potency and sensitivity of ADC therapies, strict handling, storage, and administration protocols are essential throughout the distribution process.

Regulatory compliance is a key pillar of the ADC value chain, with agencies such as the U.S. FDA, EMA, and PMDA enforcing stringent requirements related to clinical safety, manufacturing quality, and pharmacovigilance. Increasing regulatory scrutiny around oncology biologics is driving investment in advanced quality analytics, process validation systems, and real-time manufacturing monitoring technologies.

Global ADC Market Value Chain & Supply Chain Evolution Current Scenario

The current ADC supply chain is characterized by high specialization, limited manufacturing capacity, and strong reliance on a small number of technologically advanced CDMOs and pharmaceutical manufacturers. Production constraints remain a significant challenge due to the complexity of antibody engineering and the need for highly potent payload handling facilities.

North America, Europe, and Japan currently dominate ADC manufacturing and development activities, supported by strong biotechnology ecosystems, advanced R&D infrastructure, and established regulatory frameworks. However, Asia-Pacific is rapidly emerging as a key contributor to early-stage research, biosimilar development, and cost-efficient manufacturing support services.

Supply chain fragmentation is gradually decreasing as pharmaceutical companies adopt integrated development models, combining antibody discovery, linker technology innovation, and payload optimization under unified development pipelines. Strategic partnerships between biotech firms and large pharmaceutical companies are becoming increasingly common to accelerate commercialization timelines.

Digital transformation is also influencing the ADC value chain, with AI-driven drug discovery, predictive process modeling, and advanced analytics improving efficiency in antibody selection, conjugation stability testing, and clinical trial optimization.

Key Value Chain & Supply Chain Evolution Signals in Global ADC Market

One of the most significant transformation signals in the ADC value chain is the rapid advancement of linker and payload technologies, enabling higher stability, improved tumor targeting, and reduced off-target toxicity. These innovations are reshaping manufacturing requirements and increasing the need for specialized production platforms.

Another key signal is the growing reliance on CDMOs with integrated biologics and HPAPI capabilities. As ADC production complexity increases, outsourcing partnerships are becoming essential for scaling manufacturing capacity and accelerating clinical-to-commercial transitions.

The expansion of precision oncology is also reshaping supply chain dynamics, as biomarker-driven patient selection increases demand for highly specific and customized ADC therapies tailored to tumor antigen expression profiles.

Digitalization and automation are emerging as important enablers across the value chain, with AI-based process optimization, digital twins for biomanufacturing, and real-time quality monitoring systems improving production consistency and regulatory compliance.

Additionally, increasing regulatory harmonization across major markets is helping streamline global clinical trials and accelerate multi-region product approvals, supporting faster ADC commercialization cycles.

Strategic Implications of Value Chain & Supply Chain Evolution in Global ADC Market

The evolving ADC value chain presents significant strategic opportunities for pharmaceutical companies, biotech innovators, and CDMO service providers. Firms that successfully integrate antibody discovery, linker technology innovation, and payload development into unified platforms are expected to gain strong competitive advantages.

Supply chain resilience is becoming a strategic priority due to the limited number of qualified ADC manufacturing facilities globally. Companies are increasingly investing in capacity expansion, strategic partnerships, and geographic diversification to mitigate production bottlenecks.

Technological leadership in linker chemistry, site-specific conjugation, and next-generation payload development will be a key differentiator in future ADC competitiveness. Organizations that fail to invest in these areas risk losing long-term market positioning.

Increasing demand for combination therapies involving ADCs and immunotherapies is also reshaping development strategies, requiring more integrated clinical and manufacturing coordination across multiple therapeutic platforms.

Global ADC Market Value Chain & Supply Chain Evolution Forward Outlook

Between 2026 and 2033, the ADC value chain is expected to become more integrated, technologically advanced, and globally distributed. Continuous innovation in antibody engineering, linker stability, and payload design will further expand therapeutic applications across both hematologic malignancies and solid tumors.

Manufacturing capacity is expected to scale significantly as new HPAPI-compliant facilities and specialized CDMO partnerships emerge globally. Modular and flexible manufacturing systems will play a key role in improving production efficiency and reducing time-to-market for new ADC candidates.

Artificial intelligence, machine learning, and advanced bioinformatics will increasingly support ADC discovery and development, improving target selection, toxicity prediction, and clinical trial success rates.

Sustainability and regulatory compliance will also gain importance, with manufacturers focusing on waste reduction, containment efficiency, and environmentally responsible production practices for highly potent oncology compounds.

Ultimately, the future ADC value chain will evolve into a highly specialized, technology-driven, and globally interconnected ecosystem where innovation, precision manufacturing, and strategic collaboration define long-term market leadership.

Market-Specific Value Chain

- Antibody Discovery & Target Identification: Biotech research labs, monoclonal antibody developers, antigen mapping platforms, genomics companies

- Linker & Payload Development: Specialty chemical firms, HPAPI manufacturers, cytotoxic drug developers, medicinal chemistry platforms

- ADC Manufacturing & Conjugation: Biologics manufacturing facilities, conjugation technology providers, GMP-certified CDMOs, fill-finish operators

- Quality Control & Regulatory Compliance: Analytical testing laboratories, regulatory affairs organizations, pharmacovigilance systems, GMP inspection bodies

- Distribution & Oncology Supply Chain: Specialty pharmaceutical distributors, hospital pharmacies, oncology clinics, cold chain logistics providers

- Clinical Application & End Use: Hospitals, cancer treatment centers, research institutions, precision oncology programs

Investment Activity

Global Antibody Drug Conjugates (ADC) Market Investment & Funding Dynamics Overview

Investment and funding activity in the global Antibody Drug Conjugates (ADC) market is accelerating rapidly, driven by strong clinical validation of ADC therapies, rising oncology demand, and continued breakthroughs in linker-payload chemistry. Between 2026 and 2033, capital allocation is expected to concentrate on next-generation ADC platforms, bispecific ADC development, and expanded clinical pipelines targeting both hematologic malignancies and solid tumors.

ADCs have become a core strategic focus for oncology-focused pharmaceutical companies as well as biotech innovators due to their ability to combine precision targeting with potent cytotoxic activity. This has led to increased funding from venture capital firms, strategic pharmaceutical partnerships, and large-scale biopharma investments aimed at expanding ADC discovery platforms and accelerating late-stage clinical development.

A significant portion of investment is directed toward technological advancements in antibody engineering, site-specific conjugation methods, and novel payload development. These innovations are improving therapeutic index, reducing off-target toxicity, and enabling expansion into previously difficult-to-treat cancer types, thereby strengthening commercial potential across global oncology markets.

Growing collaboration between biotech firms, academic institutions, and global pharmaceutical companies is further supporting innovation in ADC development. Licensing agreements, co-development partnerships, and mergers and acquisitions are increasingly shaping funding flows as companies seek to strengthen their oncology portfolios and secure competitive advantage in precision cancer therapy.

Global ADC Market Investment & Funding Dynamics Current Scenario

Current investment trends in the ADC market are strongly influenced by rising FDA and EMA approvals, expanding late-stage clinical pipelines, and increasing adoption of targeted cancer therapies. Pharmaceutical companies are prioritizing ADC platform expansion and lifecycle management strategies for approved therapies while simultaneously investing in next-generation candidates.

- North America: Dominates investment activity due to strong oncology R&D infrastructure, high healthcare spending, and leadership in ADC clinical trials and commercialization.

- Europe: Supports steady funding growth through academic-industry collaboration, government-backed cancer research initiatives, and expanding access to biologic oncology therapies.

- Asia-Pacific: Emerging as a high-growth investment hub driven by increasing biotech innovation in Japan and China, rising cancer burden, and expanding clinical trial participation.

- Latin America & Middle East & Africa: Gradually expanding investment base supported by improving oncology infrastructure and increasing access to advanced cancer therapeutics.

Key Investment & Funding Dynamics Signals in Global ADC Market

- Rising funding toward next-generation ADCs with improved linker stability and novel cytotoxic payloads.

- Increasing investments in bispecific and multi-target ADC platforms designed to enhance tumor selectivity and overcome resistance mechanisms.

- Strong capital inflow into HER2, TROP-2, CD19, and BCMA-targeted ADC programs across multiple cancer indications.

- Growing emphasis on combination therapies integrating ADCs with immunotherapy, checkpoint inhibitors, and targeted small molecules.

- Expansion of clinical trial networks globally to accelerate regulatory approvals and broaden patient access across multiple geographies.

- Increased M&A activity and licensing deals as pharmaceutical companies seek to strengthen oncology pipelines and acquire ADC-focused biotech assets.

- Rising investment in biomarker-driven patient stratification and precision oncology platforms to improve treatment outcomes and clinical success rates.

Strategic Implications of Investment & Funding Dynamics in Global ADC Market

- The investment landscape strongly favors companies with advanced ADC platforms and strong clinical-stage oncology pipelines.

- Technological innovation in linker chemistry, payload optimization, and antibody engineering is becoming a primary competitive differentiator.

- Strategic partnerships between large pharmaceutical companies and biotech innovators are accelerating development timelines and reducing R&D risk.

- Regional diversification is increasingly important, with North America leading innovation, Europe supporting structured research ecosystems, and Asia-Pacific driving rapid clinical expansion.

- Combination therapy development is emerging as a key value driver, particularly ADC integration with immuno-oncology treatments.

- Companies investing in early-stage discovery platforms and scalable manufacturing capabilities are expected to gain long-term competitive advantage.

- Regulatory momentum and expanding oncology approvals are reinforcing investor confidence in ADC commercialization potential.

Global ADC Market Investment & Funding Dynamics Forward Outlook

Looking ahead, investment in the global ADC market is expected to remain highly robust, supported by continuous innovation in targeted cancer therapies and strong clinical success rates. Capital inflows will increasingly focus on next-generation ADC formats, including bispecific ADCs, immune-stimulating ADCs, and combination regimens designed to improve efficacy across resistant tumor types.

Future funding priorities are expected to include expansion into earlier-line cancer treatments, AI-driven drug discovery platforms, advanced biomarker diagnostics, and precision oncology integration. Additionally, manufacturing scalability and cost optimization of complex biologics will become increasingly important for commercial success.

- North America: Will continue to lead global investment driven by strong oncology innovation ecosystems and high adoption of ADC therapies.

- Europe: Will expand investment in translational research, regulatory-supported oncology innovation, and collaborative clinical development programs.

- Asia-Pacific: Will emerge as a major growth engine for ADC clinical trials, manufacturing expansion, and biotech innovation.

Overall, the ADC market is expected to attract sustained long-term investment due to its strong clinical validation and expanding therapeutic potential. Companies that successfully integrate innovation in antibody engineering, payload development, and precision oncology strategies will remain strongly positioned in the rapidly evolving global ADC market through 2033.

Technology & Innovation

Global Antibody Drug Conjugates (ADC) Market Technology & Innovation Landscape Overview

The technology and innovation landscape of the global Antibody Drug Conjugates (ADC) market is evolving rapidly as next-generation oncology research continues to enhance targeted cancer therapy design, linker chemistry, payload engineering, and antibody optimization. Innovation in this market is primarily focused on improving tumor selectivity, increasing therapeutic index, reducing off-target toxicity, and expanding applicability across both hematologic malignancies and solid tumors.

A key technological foundation of the ADC market lies in the integration of monoclonal antibody engineering with highly potent cytotoxic payloads through advanced chemical linker systems. Continuous improvements in antibody specificity, antigen targeting precision, and payload potency are enabling more effective tumor cell eradication while minimizing systemic toxicity compared to traditional chemotherapy.

Linker technology innovation represents one of the most critical advancements in the ADC space. The development of cleavable and non-cleavable linkers with improved stability and controlled drug release mechanisms is significantly enhancing drug performance. Site-specific conjugation technologies are also replacing older random conjugation methods, resulting in more consistent drug-to-antibody ratios and improved clinical predictability.

Payload innovation is another major driver of technological progress in the ADC market. New classes of cytotoxic agents, including topoisomerase inhibitors, DNA-damaging agents, and microtubule inhibitors, are being optimized for higher potency and better stability. These advancements are enabling ADCs to target previously resistant cancer types and improve overall treatment outcomes.

Bioconjugation chemistry and protein engineering advancements are also playing a significant role in improving ADC design. Enhanced antibody humanization techniques, improved protein folding stability, and advanced conjugation platforms are increasing the safety, efficacy, and manufacturability of ADC therapies.

Global ADC Market Technology & Innovation Landscape Current Scenario

Currently, the global ADC market is experiencing strong innovation momentum supported by an expanding clinical pipeline and increasing regulatory approvals of targeted oncology therapies. ADCs have progressed from experimental treatments to commercially successful oncology drugs with demonstrated efficacy in multiple cancer indications, particularly breast cancer, lymphoma, and urothelial cancers.

Clinical research activity is a major component of the current ADC innovation landscape. Hundreds of ADC candidates are in various stages of development, with increasing focus on next-generation constructs that improve tumor penetration, reduce immunogenicity, and enhance payload delivery efficiency. Combination therapy trials involving ADCs and immune checkpoint inhibitors are also expanding rapidly.

Manufacturing technology advancements are significantly improving ADC scalability and commercial viability. Innovations in bioprocessing, conjugation control systems, purification techniques, and analytical characterization tools are enabling more efficient and consistent production of complex biologic-drug conjugates.

Artificial intelligence and computational biology are increasingly being integrated into ADC discovery and development processes. AI-driven molecular modeling, antigen selection algorithms, and predictive toxicity screening tools are accelerating candidate identification and optimizing clinical trial design.

In addition, regulatory frameworks are evolving to support faster approval pathways for breakthrough ADC therapies. Adaptive clinical trial designs and accelerated approval mechanisms are enabling quicker market entry for promising oncology drugs with strong early-stage efficacy data.

Key Technology & Innovation Trends in Global ADC Market

- Site-Specific Conjugation Technology: Enables precise attachment of cytotoxic payloads, improving drug consistency and therapeutic performance.

- Next-Generation Linker Systems: Cleavable and stable linkers designed for controlled drug release within tumor microenvironments.

- Advanced Payload Engineering: Development of highly potent cytotoxic agents such as topoisomerase inhibitors and DNA-damaging compounds.

- Antibody Optimization & Humanization: Improved antibody design for enhanced tumor targeting and reduced immunogenicity.

- AI-Driven Drug Discovery: Machine learning models for antigen selection, toxicity prediction, and ADC candidate optimization.

- Combination Immuno-Oncology Therapies: ADCs combined with immune checkpoint inhibitors and targeted therapies for synergistic effects.

- Bioprocessing & Manufacturing Innovation: Advanced purification, conjugation control, and scalable production technologies for biologics.

- Biomarker-Guided Therapy Selection: Use of diagnostic biomarkers for patient stratification and treatment optimization.

- Bispecific ADC Development: Emerging ADCs targeting multiple tumor antigens for improved selectivity and efficacy.

- Real-World Evidence Integration: Use of clinical data analytics to evaluate long-term safety and effectiveness in oncology populations.

Strategic Implications of Technology & Innovation

Technological innovation is fundamentally transforming the ADC market by improving therapeutic precision, expanding clinical applications, and increasing drug development efficiency. The integration of advanced linker chemistry, payload innovation, and site-specific conjugation is enabling more predictable clinical outcomes and expanding the use of ADCs across multiple cancer types.

For pharmaceutical and biotechnology companies, investment in ADC platform technologies has become a key competitive differentiator. Firms focusing on next-generation payload design, proprietary linker systems, and antibody engineering platforms are strengthening their leadership positions in the oncology therapeutics space.

The increasing use of AI and computational modeling in drug discovery is also accelerating innovation cycles, reducing development timelines, and improving candidate selection accuracy. This is helping companies optimize R&D investments and enhance clinical success rates.

However, challenges such as manufacturing complexity, high development costs, payload toxicity management, and regulatory requirements remain significant barriers. Continued advancements in scalable biomanufacturing, quality control systems, and safety profiling will be essential for long-term market expansion.

Global ADC Market Technology & Innovation Forward Outlook

Looking ahead, the global ADC market is expected to evolve toward highly sophisticated, multi-functional, and precision-engineered oncology therapies. Future innovation will focus on bispecific ADCs, smarter tumor-targeting mechanisms, and combination regimens that integrate immunotherapy, targeted therapy, and next-generation biologics.

AI and digital biology platforms are expected to play an increasingly important role in ADC design, clinical trial optimization, and biomarker discovery. These technologies will enable faster identification of optimal targets and improve success rates in late-stage clinical development.

Combination therapies involving ADCs and immune checkpoint inhibitors are expected to become a dominant treatment strategy, significantly improving patient outcomes across both solid tumors and hematologic cancers.

Advancements in precision medicine, genomic profiling, and real-world evidence generation will further enhance patient selection and expand therapeutic applicability. Emerging ADC platforms targeting novel tumor antigens are expected to open new frontiers in cancer treatment.

In conclusion, the global ADC market is undergoing a major technological transformation driven by linker innovation, payload engineering, antibody optimization, and AI-enabled drug discovery. Companies that successfully integrate advanced bioconjugation technologies, precision oncology strategies, and scalable manufacturing capabilities will remain strongly positioned in the rapidly evolving ADC landscape.

Market Risk

Global Antibody Drug Conjugates (ADC) Market Risk Factors & Disruption Threats Overview

The global Antibody Drug Conjugates (ADC) market is experiencing rapid expansion driven by rising cancer prevalence, strong clinical pipeline growth, and increasing adoption of precision oncology therapies. Despite its strong growth trajectory, the market remains highly complex and exposed to scientific, clinical, manufacturing, regulatory, and commercial risks. As ADCs combine biologics, cytotoxic payloads, and highly specialized linker technologies, even minor inefficiencies in development or production can significantly impact safety, efficacy, and market performance.

One of the most critical risk factors in the ADC market is the high scientific and technical complexity of drug development. ADCs require precise antibody targeting, stable linker chemistry, and highly potent payload integration. Any instability in conjugation processes or suboptimal target selection can lead to reduced efficacy, increased toxicity, or clinical trial failures, making development risk significantly higher than conventional oncology drugs.

Manufacturing and scale-up challenges represent another major constraint. ADC production requires specialized facilities for biologics handling, cytotoxic payload management, and strict containment protocols. High production costs, batch variability, and complex quality control requirements can limit scalability and delay commercialization timelines.

Clinical safety concerns also remain a key risk area. While ADCs are designed to reduce systemic toxicity, off-target effects, payload release instability, and immune-related adverse reactions can still occur. These safety challenges may result in trial delays, label restrictions, or limited patient eligibility in approved indications.

In addition, intense competition within the oncology therapeutics market poses a strategic risk. ADCs compete directly with immunotherapies, bispecific antibodies, CAR-T therapies, and next-generation targeted drugs. Rapid innovation cycles in oncology may reduce the long-term exclusivity or market dominance of individual ADC products.

Global ADC Market Risk Factors & Disruption Threats Current Scenario

The current ADC market environment reflects strong clinical momentum supported by multiple regulatory approvals and a rapidly expanding pipeline. However, commercialization is still concentrated in specialized oncology centers due to administration complexity and patient monitoring requirements.

At the same time, pricing pressure and reimbursement constraints are becoming more prominent. ADC therapies are among the most expensive oncology treatments, and healthcare systems are increasingly demanding real-world evidence, cost-effectiveness justification, and comparative clinical benefit data before broad reimbursement approval.

Supply chain sensitivity is another important factor. ADC manufacturing depends on a tightly controlled ecosystem involving biologics production, linker synthesis, and high-potency drug handling. Any disruption in raw material sourcing, cold-chain logistics, or contract manufacturing capacity can significantly impact supply continuity.

Clinical trial complexity is also increasing due to the need for biomarker-driven patient selection and combination therapy strategies. While these approaches improve efficacy, they also lengthen development timelines and increase trial costs.

Additionally, rapid advancements in competing oncology modalities such as bispecific antibodies and cell therapies are reshaping treatment standards, potentially challenging ADC positioning in certain indications over the long term.

Global ADC Market Key Risk Factors & Disruption Threat Signals

One major disruption signal in the ADC market is the emergence of next-generation oncology platforms, including bispecific T-cell engagers, CAR-T cell therapies, and tumor microenvironment-targeting drugs. These therapies may compete directly with ADCs in both hematologic malignancies and solid tumors.

Another key trend is the evolution of highly potent payload technologies and novel linker systems. While these innovations improve efficacy, they also increase development risk, regulatory scrutiny, and manufacturing complexity.

Expansion into earlier-line treatment settings and combination regimens with immunotherapies represents both an opportunity and a risk. While these strategies expand market size, they also introduce uncertainties related to toxicity management, drug-drug interactions, and clinical outcome variability.

Biosimilar and follow-on biologic development may also emerge as a long-term competitive pressure as key ADC patents mature, potentially impacting pricing power and market exclusivity.

Macroeconomic pressures, healthcare budget constraints, and uneven access to advanced oncology care in emerging markets further contribute to demand variability and adoption delays.

Global ADC Market Strategic Implications of Risk Factors

Companies operating in the ADC market must prioritize innovation in linker stability, payload optimization, and site-specific conjugation technologies to reduce clinical and manufacturing risks while improving therapeutic performance.

Strengthening manufacturing infrastructure and investing in specialized high-potency production facilities will be critical to ensuring scalable and compliant ADC production. Strategic partnerships with contract development and manufacturing organizations (CDMOs) can also help mitigate capacity constraints.

Expanding biomarker-driven patient selection and companion diagnostic integration will be essential to improving clinical success rates and optimizing treatment outcomes across oncology indications.

Companies should also focus on lifecycle management strategies, including label expansion, combination therapy development, and earlier-line treatment approvals to maximize long-term revenue potential.

Additionally, strategic collaborations, licensing agreements, and co-development partnerships will remain important for sharing development risk and accelerating time-to-market in highly competitive oncology segments.

Global ADC Market Forward Risk Outlook

Looking ahead to 2026–2033, the ADC market is expected to maintain strong growth momentum driven by continued clinical validation, expanding indications, and increasing adoption of precision oncology approaches. However, competition within the oncology landscape will intensify as multiple advanced therapeutic modalities evolve simultaneously.

Future market dynamics will be shaped by next-generation ADC innovations, including bispecific ADCs, improved payload classes, and combination strategies with immunotherapy and targeted agents. These advancements will enhance efficacy but also increase development complexity and regulatory scrutiny.

Overall, while the ADC market presents substantial growth opportunities, long-term success will depend on balancing innovation with manufacturing scalability, clinical safety, cost efficiency, and strategic differentiation in an increasingly competitive oncology ecosystem.

Regulatory Landscape

Global Antibody Drug Conjugates (ADC) Market Regulatory & Policy Environment Overview

The regulatory and policy environment governing the global Antibody Drug Conjugates (ADC) market is highly stringent, science-intensive, and closely aligned with advanced oncology biologics frameworks. ADCs are complex targeted therapies that combine monoclonal antibodies with potent cytotoxic payloads, making them subject to multi-layered regulatory evaluation covering biologics, small-molecule toxicity, and combination product safety standards.

Regulatory agencies globally are increasingly focused on ensuring robust clinical validation, manufacturing consistency, and long-term safety monitoring for ADC therapies due to their dual-mechanism structure and high potency. As ADC pipelines expand rapidly across hematologic malignancies and solid tumors, regulatory oversight has intensified across clinical development, manufacturing, and post-market surveillance stages.

In addition, growing use of novel linker technologies, highly potent payloads, and next-generation conjugation methods has introduced additional regulatory complexity, requiring more detailed assessment of stability, off-target toxicity, and pharmacokinetic behavior.

Global ADC Market Regulatory & Policy Environment Current Scenario

The current regulatory landscape for ADCs is characterized by accelerated oncology approval pathways, stringent biologics manufacturing standards, and increasing reliance on biomarker-driven clinical evidence. Regulatory agencies are actively supporting innovation while ensuring strict safety controls due to the cytotoxic nature of ADC payloads.

In North America, the U.S. Food and Drug Administration (FDA) regulates ADCs under biologics licensing frameworks with additional scrutiny on combination drug components. Many ADC therapies receive Breakthrough Therapy Designation, Priority Review, or Accelerated Approval based on strong clinical efficacy in oncology indications, followed by mandatory post-marketing studies.

In Europe, the European Medicines Agency (EMA) evaluates ADCs through centralized authorization procedures under advanced biologics and oncology guidelines. EMA places strong emphasis on manufacturing quality, pharmacovigilance systems, and benefit-risk assessments, particularly for therapies targeting rare or aggressive cancers.

Asia-Pacific regulatory bodies, including Japan’s PMDA and China’s NMPA, are increasingly active in approving ADC therapies, supported by strong domestic oncology pipelines. Japan plays a particularly important role due to early adoption of ADC innovations by companies such as Daiichi Sankyo and Astellas Pharma.

Latin America and the Middle East are gradually strengthening oncology drug approval frameworks, focusing on faster access to advanced cancer therapies through reliance pathways, international clinical data acceptance, and expanded oncology care programs.

Key Regulatory & Policy Environment Signals in Global ADC Market

- Complex Biologic-Small Molecule Combination Regulation: ADCs require dual assessment of antibody biologics and cytotoxic payload components under integrated regulatory frameworks.

- Accelerated Oncology Approval Pathways: Fast-track, breakthrough therapy, and accelerated approvals are commonly used for high-unmet-need cancer indications.

- Manufacturing & Quality Control Standards: Strict GMP compliance is required for antibody production, linker chemistry, payload handling, and conjugation consistency.

- Potent Cytotoxic Safety Regulations: Regulatory agencies enforce enhanced safety protocols due to the high toxicity of ADC payloads during manufacturing and administration.

- Biomarker-Guided Clinical Development: Increasing use of companion diagnostics and target antigen validation is shaping approval decisions and trial designs.

- Pharmacovigilance & Long-Term Monitoring: Continuous monitoring is required to assess off-target toxicity, immunogenicity, and long-term patient outcomes.

Strategic Implications of Regulatory & Policy Environment

The evolving regulatory landscape is significantly influencing ADC development strategies, manufacturing investments, and clinical trial designs. Companies are increasingly prioritizing early regulatory engagement to streamline approval timelines for complex oncology indications.

Manufacturing complexity is a major regulatory focus area, requiring advanced facilities capable of handling highly potent cytotoxic compounds with strict containment and quality assurance systems. This has led to increased investment in specialized biomanufacturing infrastructure and automation technologies.

Biomarker-driven oncology is becoming central to regulatory approvals, with companion diagnostics playing a critical role in identifying patient populations most likely to benefit from ADC therapies. This is shaping precision oncology strategies across the industry.

Combination therapy development involving ADCs and immunotherapies is introducing additional regulatory complexity, requiring integrated evaluation of multi-modal treatment safety and efficacy.

Post-market surveillance requirements are also expanding, with regulators emphasizing real-world evidence generation to monitor long-term outcomes and rare adverse events associated with ADC therapies.

Global ADC Market Regulatory & Policy Environment Forward Outlook

Between 2026 and 2033, the regulatory environment for ADCs is expected to become more structured, globally harmonized, and technologically integrated. Regulatory agencies will likely refine specialized frameworks tailored specifically to ADCs due to their hybrid biologic-chemical nature.

Accelerated approval pathways are expected to expand further for oncology indications with high unmet need, while post-approval evidence requirements will become more stringent to ensure long-term safety validation.

Advancements in linker chemistry, novel payload classes, and bispecific ADC platforms will drive the development of more detailed regulatory evaluation models focusing on multi-component drug interactions and tumor-selective delivery mechanisms.

Global harmonization of oncology regulatory frameworks is expected to improve consistency in clinical trial design, manufacturing standards, and pharmacovigilance practices across major markets.

Overall, the regulatory and policy environment will remain a critical determinant of innovation speed and commercialization success in the ADC market. Companies that effectively integrate regulatory strategy, manufacturing excellence, biomarker-driven development, and global compliance readiness will be best positioned to lead in this rapidly evolving oncology segment.