Global Data center management market size and share Analysis 2026-2033

Global Data Center Management Market Forecast Snapshot: 2026???2033

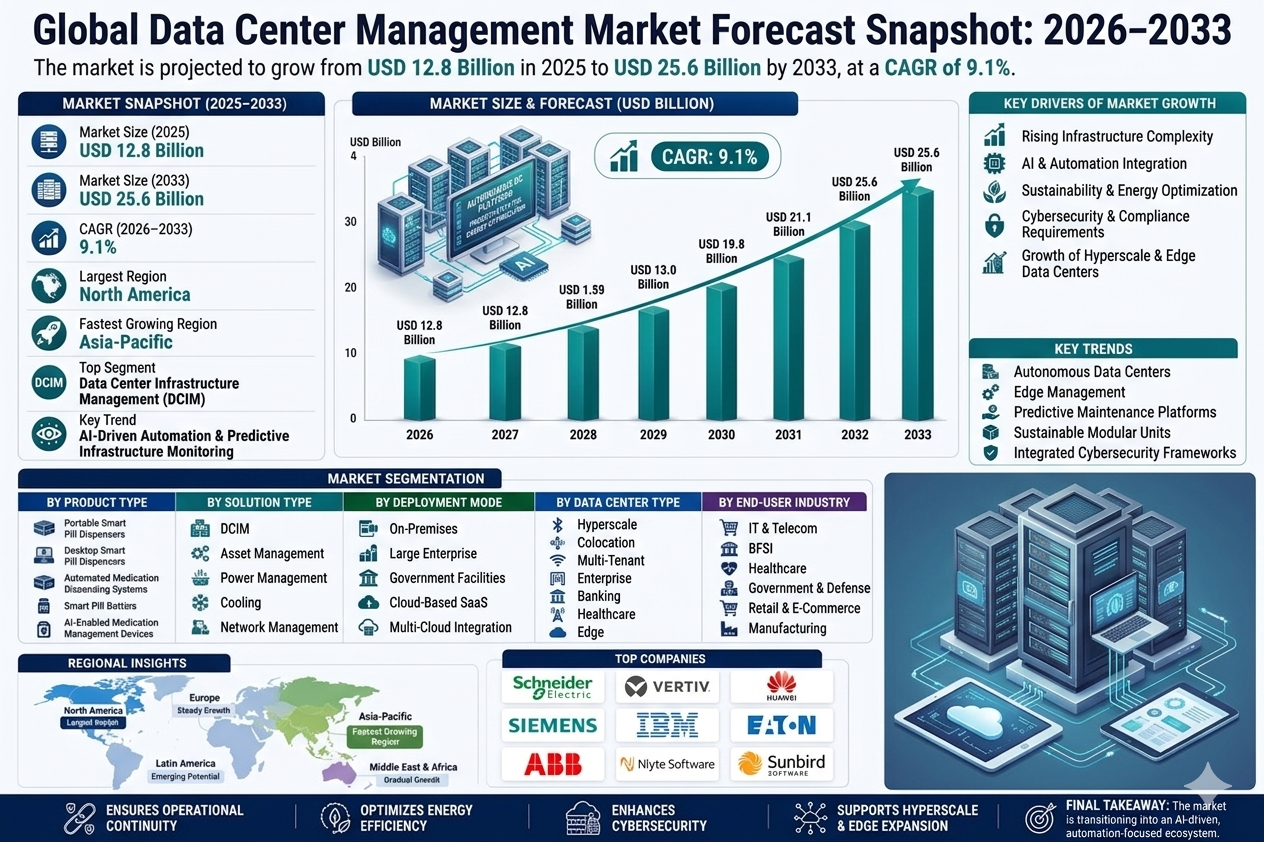

| Metric | Value |

| 2025 Market Size | USD 12.8 Billion |

| 2033 Market Size | USD 25.6 Billion |

| CAGR (2026???2033) | 9.1% |

| Largest Region | North America |

| Fastest Growing Region | Asia-Pacific |

| Top Segment | Data Center Infrastructure Management (DCIM) |

| Key Trend | AI-Driven Automation & Predictive Infrastructure Monitoring |

| Future Focus | Autonomous Data Centers, Edge Management, and Sustainable Operations |

Global Data Center Management Market Overview

The Global Data Center Management Market is undergoing structural transformation driven by hyperscale expansion, cloud migration, edge computing growth, and increasing infrastructure complexity. As organizations scale digital operations, managing power, cooling, assets, security, and performance across distributed data centers has become mission-critical.

According to Pheonix Research, the Global Data Center Management Market is valued at USD 12.8 billion in 2025 and is projected to reach USD 25.6 billion by 2033, registering a CAGR of 9.1% during 2026???2033. This revenue forecast reflects rising demand for automation, AI-enabled monitoring, cybersecurity integration, and operational efficiency.

North America leads the market due to advanced cloud ecosystems and early adoption of AI-driven management platforms. Asia-Pacific is the fastest-growing region, supported by rapid digitalization, hyperscale investments, and expanding edge infrastructure.

The Post-2025 outlook indicates accelerated transition toward autonomous data centers, predictive maintenance platforms, and sustainability-driven management solutions.

Key Drivers of Global Data Center Management Market Growth

1. Rising Infrastructure Complexity

Multi-cloud environments, hybrid IT deployments, and distributed edge networks require centralized monitoring and intelligent management platforms.

2. AI & Automation Integration

AI-powered analytics enable predictive maintenance, anomaly detection, workload optimization, and automated resource allocation.

3. Sustainability & Energy Optimization

Data centers are under pressure to reduce carbon footprint, optimize power consumption, and improve PUE through advanced management systems.

4. Cybersecurity & Compliance Requirements

Increasing regulatory mandates and cyber threats demand integrated monitoring, access control, and compliance management.

5. Growth of Hyperscale & Edge Data Centers

Rapid expansion of hyperscale facilities and micro-edge nodes increases the need for scalable, centralized infrastructure management solutions.

Global Data Center Management Market Segmentation

?? ??1.By Solution Type

1.1 Data Center Infrastructure Management (DCIM)

1.1.1 Asset Management

1.1.1.1 IT Asset Tracking

1.1.1.2 Lifecycle Management

1.1.1.3 Capacity Planning

1.1.1.4 Rack-Level Asset Visibility

1.1.2 Power Management

1.1.2.1 Energy Monitoring

1.1.2.2 Power Distribution Unit (PDU) Management

1.1.2.3 Load Balancing Optimization

1.1.2.4 Renewable Energy Integration

1.1.3 Cooling & Environmental Monitoring

1.1.3.1 Temperature Monitoring

1.1.3.2 Humidity Control

1.1.3.3 Airflow Optimization

1.1.3.4 Liquid Cooling Monitoring

1.1.4 Capacity & Space Management

1.1.4.1 Rack Space Utilization

1.1.4.2 Floor Layout Optimization

1.1.4.3 Expansion Planning

1.2 Network Management Solutions

1.2.1 Network Performance Monitoring

1.2.1.1 Latency Monitoring

1.2.1.2 Bandwidth Optimization

1.2.1.3 Traffic Analytics

1.2.2 Configuration Management

1.2.2.1 Automated Network Provisioning

1.2.2.2 Policy-Based Configuration

1.2.3 Security & Threat Monitoring

1.2.3.1 Intrusion Detection

1.2.3.2 Firewall & Access Management

1.3 IT Operations & Automation

1.3.1 AI-Based Predictive Maintenance

1.3.1.1 Failure Detection

1.3.1.2 Risk Forecasting

1.3.2 Workflow Automation

1.3.2.1 Incident Response Automation

1.3.2.2 Service Desk Integration

1.3.3 Autonomous Data Center Platforms

1.3.3.1 Self-Healing Systems

1.3.3.2 AI-Based Resource Allocation

1.4 Security & Compliance Management

1.4.1 Physical Security

1.4.1.1 Biometric Access Control

1.4.1.2 Surveillance Systems

1.4.2 Regulatory Compliance

1.4.2.1 GDPR Compliance

1.4.2.2 ISO & SOC Certifications

?? ??2.By Deployment Mode

2.1 On-Premises

2.1.1 Large Enterprise Data Centers

2.1.1.1 Tier III & Tier IV Enterprise Facilities

2.1.1.2 Private Cloud Infrastructure Management

2.1.1.3 AI-Optimized Enterprise Data Centers

2.1.1.4 High-Density Rack Management Systems

2.1.1.5 Legacy Infrastructure Modernization Platforms

2.1.2 Government Facilities

2.1.2.1 National Defense Data Centers

2.1.2.2 Smart City Control Centers

2.1.2.3 Public Sector Digital Infrastructure

2.1.2.4 Sovereign Cloud Deployments

2.1.2.5 Classified & Secure Network Operations

2.2 Cloud-Based

2.2.1 SaaS-Based DCIM (Data Center Infrastructure Management)

2.2.1.1 Energy Monitoring SaaS

2.2.1.2 Capacity Planning SaaS

2.2.1.3 Asset Lifecycle Management SaaS

2.2.1.4 AI-Based Predictive Maintenance Platforms

2.2.1.5 Carbon Footprint & ESG Reporting Tools

2.2.2 Multi-Cloud Integration Platforms

2.2.2.1 Hybrid Cloud Monitoring

2.2.2.2 Cross-Platform Orchestration Tools

2.2.2.3 Unified Dashboard Management

2.2.2.4 AI-Driven Workload Optimization

2.2.2.5 Automated Compliance & Security Monitoring

2.3 Hybrid Deployment

2.3.1 Cloud + On-Prem Monitoring

2.3.1.1 Unified Infrastructure Visibility Platforms

2.3.1.2 Remote Data Center Operations

2.3.1.3 Edge-to-Core Monitoring Systems

2.3.1.4 AI-Integrated Control Rooms

2.3.1.5 Disaster Recovery & Backup Integration

2.3.2 Distributed Edge Integration

2.3.2.1 5G-Enabled Edge Infrastructure

2.3.2.2 Industrial IoT Edge Monitoring

2.3.2.3 Micro Data Center Management

2.3.2.4 Autonomous Edge Control Systems

2.3.2.5 Smart Grid & Utility Edge Systems

?? ??3.By Data Center Type

3.1 Hyperscale Data Centers

3.1.1 Cloud Service Providers

3.1.1.1 Public Cloud Infrastructure

3.1.1.2 Private Cloud Clusters

3.1.1.3 Multi-Region Cloud Campuses

3.1.1.4 Green Data Center Facilities

3.1.1.5 AI-Optimized Cloud Clusters

3.1.2 AI & HPC Facilities

3.1.2.1 GPU-Accelerated Data Centers

3.1.2.2 AI Training & Inference Clusters

3.1.2.3 High-Performance Computing (HPC) Labs

3.1.2.4 Research & Scientific Computing Centers

3.1.2.5 Quantum-Ready Data Infrastructure

3.2 Colocation Data Centers

3.2.1 Multi-Tenant Infrastructure

3.2.1.1 Shared Rack Management

3.2.1.2 SLA-Based Monitoring Tools

3.2.1.3 Power Usage Allocation Systems

3.2.1.4 Customer Self-Service Portals

3.2.1.5 Tenant-Level Energy Analytics

3.2.2 Modular Colocation Units

3.2.2.1 Containerized Data Centers

3.2.2.2 Rapid Deployment Modules

3.2.2.3 Edge Colocation Pods

3.2.2.4 Sustainable Modular Units

3.2.2.5 High-Density Rack Modules

3.3 Enterprise Data Centers

Enterprise data centers focus on business continuity, cybersecurity, and regulatory compliance.

3.3.1 Banking & Financial Services

3.3.1.1 Core Banking Infrastructure

3.3.1.2 Real-Time Trading Platforms

3.3.1.3 Fraud Detection & AI Analytics Systems

3.3.1.4 Regulatory Reporting Infrastructure

3.3.1.5 Secure Payment Processing Systems

3.3.2 Healthcare & Life Sciences

3.3.2.1 Electronic Health Records (EHR) Systems

3.3.2.2 Medical Imaging Data Centers

3.3.2.3 Genomics & Research Computing

3.3.2.4 Telemedicine Infrastructure

3.3.2.5 Compliance-Centric Data Storage

3.4 Edge Data Centers

3.4.1 Telecom Edge

3.4.1.1 5G Core Infrastructure

3.4.1.2 Mobile Network Data Hubs

3.4.1.3 Content Delivery Network (CDN) Nodes

3.4.1.4 Smart Tower Edge Sites

3.4.1.5 Low-Latency Computing Units

3.4.2 Industrial IoT Edge

3.4.2.1 Smart Factory Edge Systems

3.4.2.2 Autonomous Vehicle Data Nodes

3.4.2.3 Oil & Gas Remote Monitoring Centers

3.4.2.4 Smart Grid Data Units

3.4.2.5 AI-Based Predictive Industrial Analytics

?? ??4.By End-User Industry

4.1 IT & Telecom

4.1.1 Cloud Infrastructure Providers

4.1.2 5G Network Operators

4.1.3 Internet Service Providers

4.1.4 Managed Service Providers

4.1.5 CDN & Streaming Platforms

4.2 BFSI

4.2.1 Retail Banking

4.2.2 Investment Banking

4.2.3 FinTech Platforms

4.2.4 Insurance Providers

4.2.5 Digital Payment Networks

4.3 Healthcare

4.3.1 Hospitals & Clinics

4.3.2 Pharmaceutical Companies

4.3.3 Research Laboratories

4.3.4 Medical Device Companies

4.3.5 HealthTech Platforms

4.4 Government & Defense

4.4.1 Defense Intelligence Infrastructure

4.4.2 National Cybersecurity Centers

4.4.3 Public Cloud Sovereign Projects

4.4.4 Digital Governance Platforms

4.4.5 Smart City Infrastructure

4.5 Retail & E-Commerce

4.5.1 Omni-Channel Retailers

4.5.2 E-Commerce Platforms

4.5.3 Digital Payment Gateways

4.5.4 Warehouse Automation Systems

4.5.5 AI-Based Demand Forecasting Platforms

4.6 Manufacturing & Industrial

4.6.1 Smart Manufacturing Facilities

4.6.2 Industrial Automation Providers

4.6.3 Robotics & AI Integration Centers

4.6.4 Supply Chain Data Hubs

4.6.5 Energy & Utility Infrastructure

Regional Insights of Global Data Center Management Market

North America ??? Largest Market

??America leads due to advanced cloud infrastructure, early AI adoption, and strong hyperscale presence. The United States remains the primary revenue contributor.

Asia-Pacific ??? Fastest Growing Market

Rapid digitalization, 5G expansion, and new hyperscale investments across China, India, Japan, and Southeast Asia are accelerating demand.

Europe

Growth is driven by strict data protection regulations, carbon neutrality goals, and modernization of legacy infrastructure.

Middle East & Africa

Smart city initiatives and cloud infrastructure investments are driving management solution adoption.

South America

Growing enterprise digital transformation and colocation expansion are supporting steady market growth.

Leading Companies in the Global Data Center Management Market

-

Siemens AG

-

ABB Ltd.

-

IBM Corporation

-

Cisco Systems

-

Huawei Technologies

-

Eaton Corporation

-

Nlyte Software

-

Sunbird Software

Leading players are strengthening competitive positioning through AI-enabled automation, integrated DCIM platforms, cybersecurity enhancements, and cloud-native management systems.

Strategic Intelligence & AI-Backed Insights

Pheonix Demand Forecast Engine identifies AI-driven automation, hyperscale infrastructure growth, and edge deployment expansion as primary long-term catalysts.

Infrastructure Investment Analyzer highlights rising capital expenditure in smart monitoring platforms and energy optimization technologies.

Innovation Tracker underscores autonomous data centers, predictive analytics, and digital twin technology as key differentiators.

Porter???s Five Forces Analysis reveals high technological rivalry, moderate supplier power, and increasing differentiation through AI integration.

Why the Global Data Center Management Market Remains Critical

-

Ensures operational continuity of mission-critical infrastructure.

-

Optimizes energy efficiency and sustainability performance.

-

Enhances cybersecurity and regulatory compliance.

-

Enables predictive maintenance and cost reduction.

-

Supports hyperscale, colocation, and edge expansion.

-

Strengthens resilience of global digital infrastructure.

Final Takeaway of Global Data Center Management Market

The Global Data Center Management Market is transitioning into an AI-driven, automation-focused, and sustainability-aligned operational ecosystem. The Data Center Management CAGR 2026???2033 of 9.1% reflects steady expansion supported by cloud adoption, infrastructure modernization, and intelligent monitoring integration.

Companies that effectively integrate AI analytics, enhance operational automation, strengthen cybersecurity frameworks, and optimize energy management will be well positioned for long-term value creation.

At Pheonix Research, our advanced forecasting frameworks provide in-depth Data Center Management revenue forecast analysis, competitive benchmarking, and strategic intelligence ??? enabling stakeholders to capitalize on the Post-2025 outlook with data-backed confidence and scalable growth strategies.

???? Social Mentions & Publication Channels

??Explore deeper insights and follow our cross-platform updates on LinkedIn and??X??for continuous intelligence and market coverage.

LinkedIn : https://www.linkedin.com/feed/update/urn:li:activity:7433895263704113152

X : https://x.com/Pheonix_Insight/status/2028131429264372007?s=20

Competitive Landscape

Data Center Management Competitive Intensity & Market Structure Overview

The Global Data Center Management Market is characterized by a highly dynamic and technology-driven competitive ecosystem, shaped by rapid cloud adoption, hyperscale infrastructure expansion, and the increasing complexity of hybrid and edge environments. The market is transitioning from traditional monitoring tools to intelligent, AI-driven, and autonomous infrastructure management platforms.

Competitive intensity is high due to the convergence of IT infrastructure providers, cloud platform companies, and enterprise software vendors. Unlike legacy management systems, competition is now defined by AI-powered analytics, predictive maintenance capabilities, cybersecurity integration, and real-time infrastructure orchestration across distributed environments.

The market exhibits a moderately consolidated structure at the top, where Tier 1 global players dominate large enterprise and hyperscale deployments. At the same time, the ecosystem is expanding with specialized DCIM vendors and software-native innovators focusing on cloud-based management, automation, and digital twin technologies.

Data Center Management Competitive Intensity & Market Structure Current Scenario

Leading Company Profiles

Schneider Electric: Global Infrastructure Management Leader. Dominates in DCIM platforms, energy optimization, and AI-enabled data center operations.

Vertiv Group Corp.: Critical Infrastructure Specialist. Strong in integrated monitoring, thermal management, and lifecycle service solutions for hyperscale and colocation environments.

Siemens AG: Industrial Digitalization Leader. Focused on smart infrastructure, automation, and digital twin-enabled data center optimization.

ABB Ltd.: Power & Automation Provider. Known for intelligent power management systems and energy-efficient infrastructure monitoring solutions.

IBM Corporation: Enterprise Technology Leader. Offers AI-powered infrastructure analytics, hybrid cloud management, and predictive maintenance platforms.

Cisco Systems: Network & Security Leader. Strong in network monitoring, cybersecurity integration, and software-defined infrastructure management.

Huawei Technologies: Digital Infrastructure Provider. Expanding in AI-driven data center management and integrated cloud-edge solutions.

Eaton Corporation: Intelligent Power Management Company. Focused on energy monitoring, sustainability analytics, and resilient infrastructure systems.

Nlyte Software: DCIM Specialist. Provides advanced asset tracking, capacity planning, and workflow automation solutions.

Sunbird Software: Data Center Operations Innovator. Known for simplified, cloud-based DCIM platforms and real-time infrastructure visibility tools.

Key Competitive Intensity & Market Structure Signals in Data Center Management

A major structural shift in the market is the transition from reactive monitoring to predictive and autonomous operations. AI-driven platforms capable of forecasting failures, optimizing workloads, and automating responses are becoming critical competitive differentiators.

Hyperscale cloud providers and colocation operators are emerging as the most influential buyers. Their demand for scalability, uptime assurance, and energy efficiency is reshaping vendor strategies and product development roadmaps.

Another key signal is the rise of hybrid and edge infrastructure, which requires unified visibility across geographically distributed assets. Vendors offering centralized, cloud-native management platforms are gaining significant traction.

Cybersecurity and compliance integration are becoming core requirements rather than add-ons. Vendors embedding real-time threat detection, access control, and regulatory compliance within management platforms are strengthening their market position.

Despite increasing innovation, established infrastructure players maintain dominance due to their global presence, integrated portfolios, and long-standing enterprise relationships.

Strategic Implications of Competitive Intensity & Market Structure in Data Center Management

The competitive landscape is pushing vendors toward platform-based ecosystems that integrate infrastructure monitoring, automation, cybersecurity, and sustainability management into a unified solution.

Total cost of ownership (TCO) is becoming a central decision factor. Enterprises are prioritizing solutions that reduce downtime, optimize energy consumption, and improve asset utilization rather than focusing solely on upfront costs.

AI, machine learning, and digital twin technologies are redefining operational strategies. Vendors investing in these areas are gaining long-term competitive advantage through predictive intelligence and automation capabilities.

The rise of subscription-based and SaaS delivery models is transforming revenue structures, enabling continuous updates, scalability, and integration across multi-cloud and hybrid environments.

Edge computing and distributed infrastructure are further driving demand for lightweight, scalable, and remotely managed solutions, creating opportunities for both established players and agile innovators.

Data Center Management Competitive Intensity & Market Structure Forward Outlook

The Data Center Management Market is expected to remain highly competitive and innovation-driven, with increasing convergence between cloud platforms, AI technology providers, and infrastructure management vendors.

Market consolidation is anticipated as leading companies acquire niche players specializing in AI analytics, cybersecurity, and edge management to strengthen their capabilities and expand market reach.

Regulatory requirements related to data security, energy efficiency, and sustainability will significantly influence product development and vendor differentiation strategies.

In the long term, the market will be defined by three core pillars: autonomous operations, AI-driven infrastructure intelligence, and sustainability optimization. Companies that successfully integrate these capabilities into scalable, cloud-native platforms will lead the Global Data Center Management Market through 2033 and beyond.

Value Chain

Global Data Center Management Market Value Chain & Supply Chain Evolution Overview

The Global Data Center Management Market value chain is evolving from traditional infrastructure monitoring toward intelligent, AI-driven, and highly automated operational ecosystems. This transformation is fueled by hyperscale data center expansion, multi-cloud complexity, edge computing proliferation, and increasing demand for real-time infrastructure optimization, cybersecurity, and sustainability.

Data center management solutions now extend beyond basic monitoring to include predictive analytics, autonomous operations, digital twin modeling, and integrated energy optimization platforms. These systems are becoming mission-critical for ensuring uptime, reducing operational costs, and managing increasingly complex hybrid and distributed environments.

The upstream supply chain depends on a combination of IT hardware providers, sensor manufacturers, and embedded system developers that enable real-time data collection and infrastructure visibility. Companies such as Schneider Electric, Siemens, ABB, and Cisco are strengthening ecosystems around smart infrastructure, IoT-enabled monitoring, and integrated hardware-software solutions.

Software and platform development is the core value creation layer, where DCIM platforms, AI-based analytics engines, cloud-based monitoring systems, and cybersecurity frameworks are developed and continuously enhanced. Vendors are increasingly focusing on SaaS-based delivery models, scalable architectures, and AI-driven automation capabilities.

Deployment and integration involve system integrators, managed service providers, and cloud specialists that ensure seamless implementation across on-premises, hybrid, and multi-cloud environments. These players enable interoperability, customization, and scalability across complex data center infrastructures.

Key supply chain challenges include integration complexity across legacy and modern systems, cybersecurity risks, high implementation costs, and the need for continuous upgrades to support AI workloads and sustainability targets.

Global Data Center Management Market Value Chain & Supply Chain Evolution Current Scenario

The current ecosystem is shaped by rapid cloud adoption, AI infrastructure growth, and increasing reliance on distributed edge environments.

Upstream hardware and sensor providers are focusing on enabling real-time monitoring through IoT devices, smart PDUs, and advanced environmental sensing technologies.

Software providers are prioritizing AI-driven analytics, predictive maintenance, and automation platforms to reduce downtime and improve operational efficiency.

Cloud-based and SaaS DCIM solutions are gaining strong traction as enterprises shift toward scalable, remote, and centralized management models.

System integrators and managed service providers play a critical role in bridging legacy infrastructure with modern AI-enabled platforms.

End-users across hyperscale, colocation, and enterprise environments are increasingly demanding unified dashboards, real-time insights, and sustainability reporting capabilities.

Key Value Chain & Supply Chain Evolution Signals in Global Data Center Management Market

Several transformative trends are reshaping the data center management ecosystem.

First, AI-driven automation is transforming management platforms into predictive and autonomous systems.

Second, hyperscale and edge data center expansion is increasing demand for scalable and distributed management solutions.

Third, sustainability requirements are pushing adoption of energy optimization, carbon tracking, and ESG reporting tools.

Fourth, cybersecurity integration is becoming a core component of data center management platforms.

Fifth, cloud-based and SaaS delivery models are redefining deployment and scalability across enterprises.

Strategic Implications of Value Chain & Supply Chain Evolution in Global Data Center Management Market

Leading players such as Schneider Electric, Vertiv, Siemens, IBM, Cisco, and ABB are strengthening their competitive positioning through AI-enabled platforms, integrated infrastructure solutions, and cloud-native management systems.

Competitive advantage increasingly depends on software intelligence, platform scalability, cybersecurity integration, and the ability to deliver unified infrastructure visibility across hybrid environments.

Companies with strong capabilities in AI analytics, automation, and digital twin technologies are best positioned to lead the next phase of market evolution.

Strategic partnerships between hardware providers, cloud platforms, and software vendors are becoming critical to delivering end-to-end solutions.

Cost optimization, energy efficiency, and regulatory compliance remain key decision factors, especially for large-scale and hyperscale operators.

Global Data Center Management Market Value Chain & Supply Chain Evolution Forward Outlook

Between 2026 and 2033, the data center management value chain is expected to become increasingly autonomous, AI-driven, cloud-integrated, and sustainability-focused.

Organizations will prioritize autonomous data center operations, predictive maintenance, and AI-based resource allocation to minimize human intervention and operational risks.

Edge computing growth will drive demand for distributed management platforms capable of handling thousands of micro data centers.

Sustainability will become a central focus, with increased adoption of energy optimization tools, carbon tracking systems, and green data center management platforms.

Digital twin technology and real-time simulation will play a growing role in infrastructure planning and optimization.

Ultimately, the value chain will evolve into a fully integrated, software-defined ecosystem enabling intelligent, self-optimizing data center operations.

Market-Specific Value Chain

- Hardware & Sensor Infrastructure: Servers, networking equipment, smart PDUs, cooling sensors, IoT monitoring devices

- Software & Platform Development: DCIM platforms, AI analytics engines, cloud-based monitoring systems, cybersecurity tools

- System Integration & Deployment: Infrastructure integration, hybrid cloud setup, customization, scalability implementation

- Data Center Operations: Hyperscale, colocation, enterprise, and edge data center management and monitoring

- Distribution & Service Delivery: SaaS platforms, managed services, consulting, and remote monitoring solutions

- Optimization & Lifecycle Services: Predictive maintenance, energy optimization, ESG reporting, digital twin simulation

Company-to-Stage Mapping

- Hardware & Sensor Infrastructure: Schneider Electric, ABB Ltd., Siemens AG, Cisco Systems

- Software & Platform Development: IBM Corporation, Nlyte Software, Sunbird Software, Huawei Technologies

- System Integration & Deployment: Vertiv Group Corp., Siemens AG, Schneider Electric, Eaton Corporation

- Data Center Operations: Amazon Web Services, Microsoft Azure, Google Cloud, Equinix

- Distribution & Service Delivery: Cisco Systems, IBM Corporation, Huawei Technologies, managed service providers

- Optimization & Lifecycle Services: Schneider Electric, Vertiv Group Corp., ABB Ltd., digital infrastructure partners

Investment Activity

Global Data Center Management Market Investment & Funding Dynamics Overview

Investment activity in the Global Data Center Management Market is gaining strong momentum, driven by the rapid expansion of hyperscale infrastructure, increasing complexity of hybrid and multi-cloud environments, and the growing need for AI-driven operational intelligence. Between 2026 and 2033, capital allocation is expected to focus heavily on Data Center Infrastructure Management (DCIM), AI-powered monitoring platforms, cybersecurity-integrated management systems, and autonomous data center technologies.

The market is evolving into a high-value, software-driven investment segment within the broader data center ecosystem, attracting funding from cloud providers, enterprise IT leaders, infrastructure funds, and private equity investors. Leading companies such as Schneider Electric, Vertiv, Siemens, IBM, Cisco, and Eaton are investing aggressively in intelligent management platforms that enhance operational efficiency, scalability, and sustainability.

A major structural shift influencing investment flows is the transition toward distributed and edge computing environments, which require centralized, real-time monitoring and automation. This is accelerating funding into cloud-based management platforms, AI-driven analytics, and integrated control systems capable of managing complex, geographically dispersed infrastructure.

Global Data Center Management Market Investment & Funding Dynamics Current Scenario

Currently, investment trends are being shaped by rapid cloud adoption, AI integration, and the need for operational efficiency across increasingly complex data center ecosystems. Organizations are prioritizing intelligent management solutions to optimize performance, reduce downtime, and improve energy efficiency.

- North America: Leads global investment due to strong hyperscale presence, early adoption of AI-driven management systems, and continuous innovation in cloud infrastructure.

- Asia-Pacific: Fastest-growing investment region driven by digital transformation, expanding data center capacity, and government-backed infrastructure initiatives.

- Europe: Strong investment focus on sustainability, regulatory compliance, and energy-efficient data center operations.

- Middle East & Africa: Emerging investment landscape supported by smart city development, cloud adoption, and digital infrastructure expansion.

Key Investment & Funding Dynamics Signals in Global Data Center Management Market

- AI-driven automation and predictive analytics are attracting significant investment across management platforms.

- Rising hyperscale and colocation expansion is driving funding into scalable DCIM and monitoring solutions.

- Cybersecurity integration within management systems is becoming a key investment priority.

- Edge computing growth is creating demand for decentralized and cloud-based management platforms.

- Sustainability initiatives are accelerating funding toward energy optimization and carbon tracking solutions.

Strategic Implications of Investment & Funding Dynamics in Global Data Center Management Market

- Companies with strong AI and automation capabilities are gaining competitive advantage in attracting investment.

- Integration of cloud-native platforms with on-premise systems is becoming a critical differentiator.

- Partnerships between software providers, hardware vendors, and cloud operators are increasing.

- Regional diversification strategies are essential to capture growth in Asia-Pacific and emerging markets.

- Focus on ESG compliance and energy efficiency is shaping long-term investment decisions.

Global Data Center Management Market Investment & Funding Dynamics Forward Outlook

Looking ahead, the Global Data Center Management Market is expected to attract sustained investment driven by the increasing reliance on digital infrastructure, AI-enabled operations, and the need for autonomous and resilient data center ecosystems.

Future capital allocation will focus on autonomous data center platforms, AI-powered predictive maintenance, digital twin technology, edge infrastructure management, and integrated cybersecurity solutions.

- North America: Will continue leading innovation-driven investments in AI-enabled and autonomous data center management.

- Asia-Pacific: Will dominate future investment growth supported by hyperscale expansion and rapid digital adoption.

- Europe: Will emphasize sustainable, compliant, and energy-efficient management solutions.

Technological advancements in digital twins, real-time analytics, and self-healing infrastructure will further shape investment strategies across the market.

Overall, the market will remain a high-growth, innovation-driven investment segment through 2033, supported by its critical role in managing next-generation digital infrastructure. Companies that lead in AI integration, automation, scalability, and sustainability will define the future competitive landscape.

Technology & Innovation

Global Data Center Management Market Technology & Innovation Landscape Overview

The technology and innovation landscape within the Global Data Center Management Market is rapidly evolving toward intelligent, autonomous, and highly integrated infrastructure ecosystems. As data centers scale in size, complexity, and geographic distribution, management platforms are transitioning from traditional monitoring tools to AI-driven, predictive, and self-optimizing systems.

Innovation intensity is high, driven by the convergence of artificial intelligence, machine learning, IoT, digital twins, and cloud-native architectures. Leading players such as Schneider Electric, Vertiv, Siemens, IBM, Cisco, and emerging software providers are investing in next-generation Data Center Infrastructure Management (DCIM) platforms that combine real-time analytics with automation and orchestration capabilities.

A key transformation is the shift toward autonomous data center operations, where AI-powered systems can monitor, analyze, and optimize infrastructure performance without human intervention. This includes predictive maintenance, automated workload distribution, energy optimization, and intelligent fault detection.

Simultaneously, the integration of edge computing, hybrid cloud environments, and distributed IT architectures is pushing innovation toward unified, scalable, and cloud-based management platforms capable of providing end-to-end visibility across core, colocation, and edge facilities.

Global Data Center Management Market Technology & Innovation Landscape Current Scenario

Currently, the market is focused on enhancing operational efficiency, improving infrastructure visibility, and reducing downtime through advanced monitoring and automation technologies. Vendors are prioritizing solutions that deliver real-time insights, predictive analytics, and centralized control.

AI-driven predictive maintenance is one of the most significant innovations, enabling early detection of equipment failures, anomaly identification, and proactive issue resolution. This minimizes downtime and reduces operational costs in mission-critical environments.

Digital twin technology is gaining traction, allowing operators to create virtual replicas of data center environments for simulation, optimization, and scenario planning. This enhances decision-making and improves capacity planning and infrastructure design.

Cloud-based DCIM platforms are expanding rapidly, offering scalable, SaaS-based solutions that enable remote monitoring, multi-site management, and seamless integration with hybrid and multi-cloud environments.

IoT-enabled sensors and real-time monitoring systems are enhancing visibility across power, cooling, and IT infrastructure. These technologies provide granular insights into temperature, energy consumption, airflow, and equipment performance.

Cybersecurity integration is also becoming a critical innovation focus, with management platforms incorporating advanced threat detection, access control, and compliance monitoring to protect critical infrastructure.

Key Technology & Innovation Trends in Global Data Center Management Market

- AI-Driven Automation: Predictive maintenance, anomaly detection, and automated resource optimization.

- Autonomous Data Centers: Self-healing and self-optimizing infrastructure systems.

- Digital Twin Technology: Virtual simulation models for capacity planning and performance optimization.

- Cloud-Based DCIM Platforms: Scalable SaaS solutions for multi-site and hybrid environment management.

- IoT & Real-Time Monitoring: Sensor-driven insights for power, cooling, and environmental conditions.

- Edge Data Center Management: Centralized control of distributed micro data centers.

- Cybersecurity Integration: Advanced threat monitoring and compliance management within DCIM systems.

- Energy Optimization & Sustainability: AI-based power management and carbon footprint tracking.

Strategic Implications of Technology & Innovation

The evolution of data center management technologies is transforming infrastructure operations into intelligent, automated ecosystems. Organizations adopting advanced management platforms are achieving higher efficiency, reduced downtime, and improved scalability.

For hyperscale operators and cloud providers, AI-driven management systems enable efficient handling of massive, distributed infrastructure, ensuring optimal performance and cost control. These capabilities are becoming critical for supporting AI workloads and high-density computing environments.

Enterprises benefit from improved operational visibility, enhanced cybersecurity, and better compliance management, particularly in regulated industries such as BFSI and healthcare.

However, high implementation costs, integration complexity, and the need for skilled workforce present challenges, increasing the importance of vendor partnerships and platform standardization.

Sustainability is emerging as a strategic priority, with management platforms playing a key role in optimizing energy usage, reducing emissions, and supporting ESG goals through real-time monitoring and reporting.

Global Data Center Management Market Technology & Innovation Forward Outlook

Looking ahead, the market is expected to evolve toward fully autonomous, AI-driven, and sustainability-focused data center ecosystems. Management platforms will increasingly leverage advanced analytics, machine learning, and automation to deliver real-time optimization and decision-making.

Autonomous data centers will become more prevalent, with systems capable of self-monitoring, self-healing, and dynamically adjusting to workload demands without human intervention.

Digital twin integration will expand further, enabling predictive modeling, risk assessment, and continuous optimization across infrastructure lifecycles.

Edge data center management will become a major focus area, requiring scalable, lightweight, and cloud-connected solutions to manage distributed computing environments efficiently.

In conclusion, the Global Data Center Management Market is transitioning into an intelligent, automated, and highly resilient infrastructure management ecosystem. Companies that lead in AI integration, automation, digital twin capabilities, and sustainability-driven innovation will define the future of data center operations through 2033.