Global System on Module Market size and share Analysis 2026-2033

Global System on Module Market Forecast Snapshot: 2026???2033

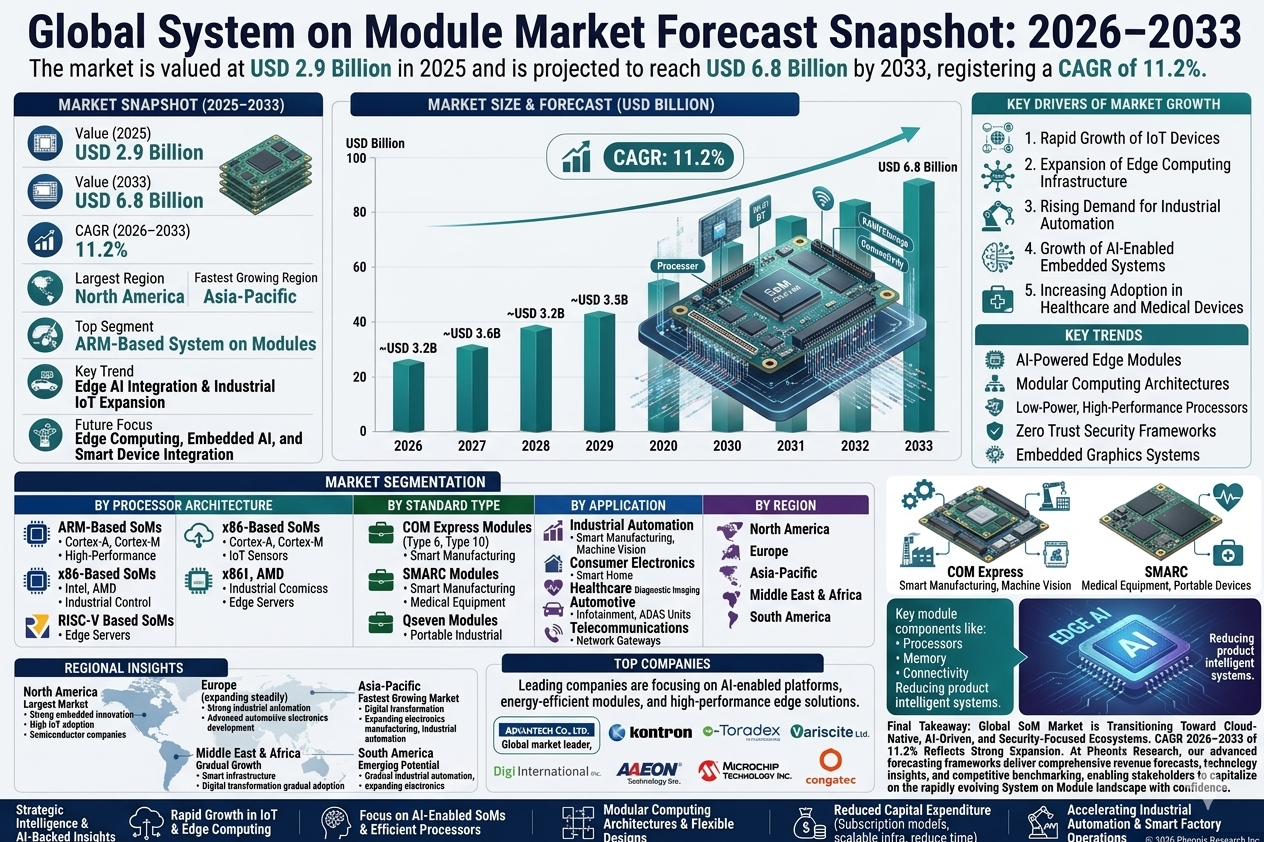

| Metric | Value |

| 2025 Market Size | USD 2.9 Billion |

| 2033 Market Size | USD 6.8 Billion |

| CAGR (2026???2033) | 11.2% |

| Largest Region | North America |

| Fastest Growing Region | Asia-Pacific |

| Top Segment | ARM-Based System on Modules |

| Key Trend | Edge AI Integration & Industrial IoT Expansion |

| Future Focus | Edge Computing, Embedded AI, and Smart Device Integration |

Global System on Module Market Overview

Global System on Module Market are the tiny brains powering big things. They're compact, plug-and-play modules with processors, memory, and connectivity ??? perfect for smart devices, industrial machines, healthcare gear, and IoT stuff. As tech gets smarter, SoMs are growing fast, making complex systems easier to build and innovate.

According to Pheonix Research, the Global System on Module Market is valued at USD 2.9 billion in 2025 and is projected to reach USD 6.8 billion by 2033, registering a CAGR of 11.2% during 2026???2033. Market growth is driven by increasing demand for compact embedded computing platforms, expanding IoT ecosystems, and the rapid adoption of edge computing solutions.

North America currently leads the market due to strong innovation in embedded computing, widespread adoption of IoT technologies, and the presence of leading semiconductor and embedded system providers. Meanwhile, Asia-Pacific is emerging as the fastest-growing region, supported by expanding electronics manufacturing, industrial automation adoption, and growing demand for smart devices. The post-2025 outlook highlights increasing integration of AI-enabled edge computing modules, high-performance processors, and energy-efficient embedded systems, positioning SoMs as a critical building block for next-generation intelligent devices.Key Drivers of Global System on Module Market Growth

1. Rapid Growth of IoT Devices

Increasing adoption of connected devices across industries is driving demand for compact and scalable embedded computing solutions.

2. Expansion of Edge Computing Infrastructure

Edge computing requires efficient processing capabilities close to the data source, increasing the adoption of SoM platforms.

3. Rising Demand for Industrial Automation

Manufacturing industries are deploying embedded systems for robotics, automation, and smart factory operations.

4. Growth of AI-Enabled Embedded Systems

AI-powered devices require powerful and compact computing platforms that can efficiently process data locally.

5. Increasing Adoption in Healthcare and Medical Devices

Medical imaging systems, patient monitoring equipment, and wearable health devices increasingly rely on embedded computing modules.

Global System on Module Market Segmentation

?? ??1.By Processor Architecture

1.1 ARM-Based System on Modules

1.1.1 Cortex-A Series Modules

1.1.1.1 High-Performance Embedded Systems

1.1.1.1.1 Industrial Automation Controllers

1.1.1.1.2 Smart Device Platforms

1.1.2 Cortex-M Series Modules

1.1.2.1 Low-Power Embedded Systems

1.1.2.1.1 IoT Sensors

1.1.2.1.2 Smart Home Devices

1.2 x86-Based System on Modules

1.2.1 Intel Processor-Based Modules

1.2.1.1 Industrial Embedded Platforms

1.2.1.1.1 Industrial Control Systems

1.2.1.1.2 Edge Computing Servers

1.2.2 AMD Processor-Based Modules

1.2.2.1 High-Performance Embedded Computing

1.2.2.1.1 Embedded Graphics Systems

1.2.2.1.2 Industrial Workstations

1.3 RISC-V Based System on Modules

1.3.1 Open Architecture Modules

1.3.1.1 Custom Embedded Platforms

1.3.1.1.1 Research and Development Systems

1.3.1.1.2 Specialized IoT Devices

?? 2.By Standard Type

2.1 COM Express Modules

2.1.1 Type 6 Modules

2.1.1.1 Industrial Computing Platforms

2.1.1.1.1 Smart Manufacturing Systems

2.1.1.1.2 Industrial Robotics

2.1.2 Type 10 Modules

2.1.2.1 Compact Embedded Platforms

2.1.2.1.1 Medical Equipment

2.1.2.1.2 Portable Devices

2.2 SMARC Modules

2.2.1 Low-Power Embedded Systems

2.2.1.1 Mobile Devices

2.2.1.1.1 Tablets and Handheld Devices

2.2.1.1.2 Portable Industrial Devices

2.3 Qseven Modules

2.3.1 Compact Embedded Platforms

2.3.1.1 Industrial IoT Systems

2.3.1.1.1 Edge Computing Devices

2.3.1.1.2 Smart Sensors

?? 3.By Application

3.1 Industrial Automation

3.1.1 Smart Manufacturing Systems

3.1.1.1 Industrial Robotics

3.1.1.1.1 Assembly Line Automation

3.1.1.1.2 Machine Vision Systems

3.2 Consumer Electronics

3.2.1 Smart Home Devices

3.2.1.1 Home Automation Controllers

3.2.1.1.2 Smart Security Systems

3.3 Healthcare

3.3.1 Medical Devices

3.3.1.1 Diagnostic Imaging Systems

3.3.1.1.2 Patient Monitoring Equipment

3.4 Automotive

3.4.1 Vehicle Electronics

3.4.1.1 Infotainment Systems

3.4.1.1.2 ADAS Processing Units

3.5 Telecommunications

3.5.1 Network Infrastructure Devices

3.5.1.1 Edge Network Gateways

3.5.1.1.2 Telecom Base Stations

?? 4.By Region

4.1North America

4.2 Europe

4.3 Asia-Pacific

4.4 Middle East & Africa

4.5 South America

Regional Insights of Global System on Module Market

North America ??? Largest Market

North America dominates the market due to strong innovation in embedded computing technologies, high adoption of IoT devices, and the presence of major semiconductor companies.

Asia-Pacific ??? Fastest Growing Market

Asia-Pacific is witnessing rapid growth driven by expanding electronics manufacturing industries, increasing adoption of industrial automation, and rising demand for smart consumer devices.

Europe

Europe???s market is supported by strong industrial automation adoption, advanced automotive electronics development, and increasing deployment of embedded systems in manufacturing.

Middle East & Africa

Growing investments in smart infrastructure and digital transformation initiatives are gradually increasing demand for embedded computing solutions.

South America

Emerging industrial automation and expanding electronics manufacturing are supporting steady market growth in the region.

Leading Companies in Global System on Module Market

-

Toradex AG

-

Variscite Ltd.

-

Digi International Inc.

-

AAEON Technology Inc.

-

Microchip Technology Inc.

-

Congatec GmbH

Strategic Intelligence & AI-Backed Insights

Pheonix Demand Forecast Engine identifies rapid growth in IoT devices, industrial automation systems, and edge computing infrastructure as key growth catalysts.

Innovation Tracker highlights AI-enabled SoM platforms, energy-efficient embedded processors, and modular computing architectures as major competitive differentiators.

Infrastructure Investment Analyzer indicates increasing global investment in smart manufacturing, IoT ecosystems, and digital infrastructure.

Porter???s Five Forces Analysis reveals moderate supplier power, high technological barriers for new entrants, and increasing competition among semiconductor and embedded system providers.

Why the Global System on Module Market is Critical

-

Enables compact and scalable embedded computing solutions.

-

Supports rapid development of IoT and edge computing devices.

-

Accelerates industrial automation and smart manufacturing.

-

Enhances performance of healthcare and medical devices.

-

Reduces product development time for electronic manufacturers.

Final Takeaway of Global System on Module Market

The Global System on Module Market is evolving into a key technology foundation for embedded computing, IoT, and edge AI applications. The System on Module Market CAGR 2026???2033 of 11.2% reflects strong growth driven by expanding connected device ecosystems and industrial automation. Companies investing in AI-enabled embedded platforms, high-performance processors, and modular computing architectures will be well positioned to capture long-term market opportunities. At Pheonix Research, our market intelligence frameworks deliver comprehensive revenue forecasts, technology insights, and competitive benchmarking, enabling stakeholders to capitalize on the rapidly evolving System on Module market with confidence.???? Social Mentions & Publication Channels

??Explore deeper insights and follow our cross-platform updates on LinkedIn and X for continuous intelligence and market coverage.

LinkedIn : https://www.linkedin.com/feed/update/urn:li:activity:7436748957373964288

X : https://x.com/Pheonix_Insight/status/2030986446375694443?s=20

Competitive Landscape

Global System on Module Market Competitive Intensity & Market Structure Overview

The Global System on Module (SoM) Market is characterized by a highly innovation-driven and rapidly evolving competitive ecosystem, fueled by the expansion of edge computing, industrial automation, embedded AI, and IoT-connected devices. The market is transitioning from conventional embedded hardware architectures toward modular, scalable, and AI-enabled computing platforms designed for next-generation intelligent systems.

Competitive intensity is high due to the convergence of semiconductor companies, embedded computing providers, industrial automation vendors, and edge AI technology developers. Competition is increasingly defined by processor performance, power efficiency, AI acceleration capability, compact modular architecture, and software ecosystem compatibility.

The market demonstrates a moderately consolidated structure, where established embedded computing and semiconductor firms dominate industrial and enterprise deployments, while emerging players compete through specialized ARM-based, RISC-V, and AI-optimized SoM platforms targeting edge intelligence and IoT applications.

Global System on Module Market Competitive Intensity & Market Structure Current Scenario

Leading Company Profiles

Advantech Co., Ltd.: Global Embedded Computing Leader. Strong presence in industrial automation, edge AI computing, and modular embedded platforms.

Kontron AG: Industrial Embedded Systems Provider. Focused on high-performance SoM platforms for industrial IoT, transportation, and telecom applications.

Toradex AG: Embedded Computing Specialist. Known for ARM-based SoMs and developer-friendly edge computing ecosystems.

Variscite Ltd.: Embedded Module Innovator. Strong in low-power ARM-based SoM solutions for industrial and medical devices.

Digi International Inc.: IoT Connectivity Provider. Expanding embedded computing capabilities with secure and connected SoM platforms.

AAEON Technology Inc.: AI Edge Computing Player. Focused on AI-enabled SoMs and industrial edge processing solutions.

Microchip Technology Inc.: Semiconductor and Embedded Systems Provider. Offers integrated embedded processing and low-power computing solutions.

Congatec GmbH: High-Performance Embedded Computing Company. Strong expertise in COM Express and edge server-grade SoM architectures.

NVIDIA Corporation: AI Computing Leader. Driving adoption of GPU-enabled SoMs for robotics, autonomous systems, and edge AI applications.

NXP Semiconductors: Automotive & Industrial Embedded Solutions Provider. Strong in secure embedded processing and industrial IoT platforms.

Key Competitive Intensity & Market Structure Signals in Global System on Module Market

A major competitive signal is the rapid shift toward AI-enabled edge computing platforms. Enterprises increasingly require real-time local data processing, accelerating demand for SoMs with integrated AI acceleration and machine learning capabilities.

The expansion of industrial IoT and smart manufacturing ecosystems is intensifying competition among vendors offering rugged, energy-efficient, and scalable embedded computing platforms optimized for industrial environments.

Another important structural signal is the growing adoption of ARM-based and RISC-V architectures. Manufacturers are prioritizing low-power, flexible, and cost-efficient processor architectures capable of supporting edge intelligence and connected devices.Software ecosystem compatibility is becoming a major differentiator. Vendors that provide robust development kits, operating system compatibility, security frameworks, and long-term lifecycle support are gaining stronger market positioning.

Additionally, edge AI applications in robotics, autonomous systems, healthcare devices, and smart infrastructure are increasing demand for compact, high-performance modules capable of delivering advanced processing in space-constrained environments.

Strategic Implications of Competitive Intensity & Market Structure in Global System on Module Market

Manufacturers are transitioning from standalone hardware suppliers to integrated embedded computing ecosystem providers. Companies increasingly combine hardware, software, AI frameworks, and connectivity solutions into unified development platforms.

Innovation investment is heavily concentrated in AI acceleration, edge computing optimization, thermal efficiency, and high-speed connectivity technologies. Vendors that successfully balance processing power with energy efficiency gain a competitive advantage in industrial and mobile applications.

Partnerships with semiconductor companies, industrial automation firms, robotics developers, and cloud providers are becoming strategically important to accelerate product deployment and ecosystem integration.

Total cost of ownership (TCO) is evolving into a critical purchasing factor. Customers increasingly prioritize scalability, long-term support availability, software integration efficiency, and reduced product development timelines over initial hardware pricing.

The emergence of edge AI and embedded machine learning is also reshaping competitive dynamics, creating opportunities for specialized vendors focused on AI-native SoM architectures and intelligent edge platforms.

Global System on Module Market Competitive Intensity & Market Structure Forward Outlook

The Global System on Module Market is expected to remain highly competitive and innovation-centric, with increasing technological convergence between semiconductor companies, embedded computing vendors, and AI platform providers.

Market consolidation is likely as larger embedded technology firms acquire specialized AI and edge computing startups to strengthen embedded intelligence capabilities and accelerate product innovation.

AI-enabled edge computing, industrial automation, and smart connected devices will remain the primary long-term growth drivers, significantly influencing future product architectures and competitive positioning.

RISC-V adoption, energy-efficient computing, and embedded cybersecurity integration are expected to emerge as critical competitive battlegrounds over the forecast period.

In the long term, the market will be shaped by three core competitive pillars: AI-enabled edge intelligence, modular embedded scalability, and energy-efficient high-performance computing. Companies that effectively integrate these capabilities while maintaining strong software ecosystems and industrial partnerships will lead the Global System on Module Market through 2033.

Value Chain

Global System on Module Market Value Chain & Supply Chain Evolution Overview

The Global System on Module (SoM) Market value chain is evolving from traditional embedded computing hardware manufacturing toward highly integrated, AI-enabled, edge-optimized, and software-driven embedded ecosystem architectures. This transformation is primarily driven by expanding IoT deployments, industrial automation growth, edge AI adoption, smart device proliferation, and increasing demand for compact, scalable, and energy-efficient embedded computing platforms.

System on Modules integrate processors, memory, connectivity, storage, and power management components into compact embedded computing platforms that simplify product development and accelerate deployment across industrial, healthcare, automotive, consumer electronics, and telecommunications applications.

The value chain increasingly extends beyond semiconductor manufacturing into AI acceleration technologies, edge computing infrastructure, embedded software ecosystems, industrial automation platforms, and intelligent device integration frameworks. Leading companies such as Advantech Co., Ltd., Kontron AG, Toradex AG, Variscite Ltd., Digi International Inc., AAEON Technology Inc., Microchip Technology Inc., and Congatec GmbH are strengthening vertically integrated embedded computing ecosystems through processor innovation, software optimization, and industrial partnerships.

The upstream supply chain depends heavily on semiconductor foundries, processor manufacturers, PCB suppliers, memory manufacturers, embedded software developers, wireless connectivity providers, and edge AI chipset vendors. Supply chain resilience and semiconductor availability remain critical due to growing global demand for embedded processing solutions.

Manufacturing strategies increasingly focus on compact module integration, energy-efficient architectures, AI acceleration capability, thermal optimization, high-speed connectivity integration, and scalable modular design frameworks. Embedded computing vendors are increasingly adopting flexible and standardized module architectures such as COM Express, SMARC, and Qseven to improve interoperability and product scalability.

Key supply chain challenges include semiconductor shortages, advanced chip fabrication dependency, thermal management complexity, cybersecurity vulnerabilities in connected devices, component cost volatility, and rapidly evolving embedded AI processing requirements.

Global System on Module Market Value Chain & Supply Chain Evolution Current Scenario

The current SoM ecosystem is shaped by rapid expansion of industrial IoT, increasing edge computing deployment, rising AI-enabled embedded system adoption, and accelerating digital transformation across industries.Upstream semiconductor suppliers are increasingly prioritizing energy-efficient processors, AI accelerators, low-power chipsets, and integrated wireless connectivity solutions to support advanced embedded applications.

Manufacturers are focusing on scalable modular computing architectures, edge AI processing optimization, industrial-grade reliability, and compact system integration to meet evolving application requirements across industrial automation, healthcare, transportation, and telecommunications sectors.Industrial automation and smart manufacturing applications remain major demand drivers, as enterprises increasingly deploy embedded computing platforms for robotics, machine vision systems, predictive maintenance, and industrial edge analytics.

Healthcare and medical device integration is accelerating demand for compact embedded systems capable of supporting diagnostic imaging, patient monitoring, wearable healthcare devices, and portable medical equipment.

AI-enabled edge processing, low-latency computing, and real-time analytics are becoming increasingly important competitive differentiators across next-generation SoM platforms.

Key Value Chain & Supply Chain Evolution Signals in Global System on Module Market

Several transformative trends are reshaping the SoM ecosystem globally.

First, edge AI integration is accelerating demand for embedded platforms capable of real-time local data processing and intelligent analytics.

Second, industrial IoT expansion is increasing deployment of modular embedded systems across smart manufacturing and automation environments.

Third, standardized SoM architectures such as COM Express, SMARC, and Qseven are improving interoperability, scalability, and faster product development.

Fourth, energy-efficient embedded processing and thermal optimization technologies are becoming increasingly important for portable and industrial edge applications.

Fifth, rising adoption of connected smart devices is driving integration of wireless connectivity, AI acceleration, and edge computing functionality into compact embedded modules.

Strategic Implications of Value Chain & Supply Chain Evolution in Global System on Module Market

Industry leaders such as Advantech Co., Ltd., Kontron AG, Toradex AG, Variscite Ltd., Digi International Inc., AAEON Technology Inc., Microchip Technology Inc., and Congatec GmbH are strengthening competitive positioning through AI-enabled embedded platforms, scalable module architectures, edge computing optimization, and industrial automation partnerships.

Competitive advantage increasingly depends on semiconductor integration capability, embedded software ecosystem strength, AI processing performance, energy efficiency, industrial-grade reliability, and long-term product lifecycle support.Manufacturers capable of delivering modular, compact, secure, and AI-optimized embedded systems are best positioned to capture growth opportunities across industrial, healthcare, automotive, and smart infrastructure applications.

Strategic collaboration between semiconductor vendors, embedded software providers, industrial automation companies, and edge computing ecosystem partners is becoming increasingly important for innovation acceleration and product differentiation.Long-term success will increasingly depend on balancing computing performance, thermal efficiency, cybersecurity resilience, scalability, and cost optimization across embedded device ecosystems.

Global System on Module Market Value Chain & Supply Chain Evolution Forward Outlook

Between 2026 and 2033, the SoM value chain is expected to become increasingly AI-driven, edge-centric, software-defined, and connectivity-integrated.

Manufacturers will increasingly prioritize AI acceleration, low-power embedded processing, advanced wireless connectivity, real-time edge analytics, and compact high-performance module architectures.Industrial edge computing, autonomous systems, robotics, medical devices, telecommunications infrastructure, and smart mobility platforms will continue driving demand for advanced embedded computing modules.

Embedded AI frameworks, machine learning optimization, and secure edge processing technologies will increasingly shape next-generation SoM product strategies.Standardized modular architectures and scalable embedded ecosystems will further accelerate faster product development cycles and lower system integration complexity.

Ultimately, the future SoM value chain will evolve from modular embedded hardware manufacturing into intelligent edge computing ecosystem enablement platforms.

Market-Specific Value Chain

- Semiconductor & Component Supply: Processors, AI accelerators, memory chips, wireless connectivity modules, PCBs, power management components

- Embedded Software & Platform Development: Operating systems, AI frameworks, embedded firmware, edge computing software, cybersecurity integration

- System on Module Manufacturing: Compact module integration, thermal optimization, low-power design, standardized module architecture production

- System Integration & Device Development: Industrial automation systems, medical devices, automotive electronics, IoT devices, telecom infrastructure integration

- Deployment & Connectivity Integration: Edge computing deployment, industrial IoT integration, smart device enablement, AI-enabled embedded applications

- Lifecycle Support & Embedded Services: Technical support, software updates, cybersecurity management, predictive maintenance, long-term product lifecycle services

Company-to-Stage Mapping

- Semiconductor & Component Supply: Microchip Technology Inc., Advantech Co., Ltd., AAEON Technology Inc., Congatec GmbH

- Embedded Software & Platform Development: Toradex AG, Kontron AG, Digi International Inc., Variscite Ltd.

- System on Module Manufacturing: Advantech Co., Ltd., Congatec GmbH, AAEON Technology Inc., Kontron AG

- System Integration & Device Development: Digi International Inc., Toradex AG, Variscite Ltd., Advantech Co., Ltd.

- Deployment & Connectivity Integration: Kontron AG, Digi International Inc., AAEON Technology Inc., industrial ecosystem partners

- Lifecycle Support & Embedded Services: Toradex AG, Congatec GmbH, Advantech Co., Ltd., embedded solution ecosystem partners

Technology & Innovation

Global System on Module Market Technology & Innovation Landscape Overview

The technology and innovation landscape within the Global System on Module (SoM) Market is rapidly evolving as industries shift toward compact, modular, and high-performance embedded computing architectures. System on Modules are becoming a foundational building block for IoT devices, industrial automation systems, automotive electronics, healthcare equipment, and edge AI applications, enabling faster product development and scalable embedded system design.

Innovation in the SoM ecosystem is being driven by rising demand for edge computing, industrial IoT expansion, AI-enabled embedded systems, and smart connected devices. Leading companies such as Advantech Co., Ltd., Kontron AG, Toradex AG, Variscite Ltd., Digi International Inc., AAEON Technology Inc., Microchip Technology Inc., and Congatec GmbH are investing heavily in high-performance processor integration, energy-efficient module designs, and AI-ready embedded computing platforms.

A key technological transformation in the market is the integration of AI acceleration capabilities, heterogeneous computing architectures, and advanced connectivity interfaces within compact SoM platforms. These advancements are enabling real-time data processing, intelligent decision-making at the edge, and seamless integration with cloud ecosystems for distributed computing environments.

Simultaneously, advancements in RISC-V architectures, ARM-based high-efficiency processors, and x86 embedded platforms are expanding design flexibility and enabling customized computing solutions across industrial, automotive, and healthcare applications.

Global System on Module Market Technology & Innovation Landscape Current Scenario

Currently, the System on Module industry is focused on improving processing efficiency, reducing power consumption, enhancing modular scalability, and enabling faster embedded system development cycles. Manufacturers are prioritizing SoM platforms that support AI workloads, real-time analytics, and edge computing deployments.

AI-enabled embedded computing is one of the most significant innovation areas. Advanced SoM platforms now integrate neural processing units (NPUs), GPU acceleration, and AI inference engines, enabling real-time decision-making in industrial automation, robotics, and smart device applications.ARM-based System on Modules dominate the market due to their high energy efficiency, compact design, and strong ecosystem support. These modules are widely used in IoT sensors, smart home devices, industrial controllers, and portable embedded systems.

x86-based SoMs are gaining traction in high-performance edge computing applications, industrial PCs, and advanced automation systems due to their superior computing power and compatibility with enterprise software environments. RISC-V-based SoM architectures are emerging as a disruptive innovation trend, offering open-source flexibility, customization potential, and cost efficiency for specialized embedded applications and next-generation IoT ecosystems.

Edge computing integration is another key innovation driver, enabling SoM platforms to process data locally with minimal latency, reducing dependency on centralized cloud infrastructure and improving real-time responsiveness in mission-critical applications.

Additionally, advancements in modular computing standards such as COM Express, SMARC, and Qseven are improving interoperability, scalability, and system integration efficiency across embedded computing ecosystems.

Key Technology & Innovation Trends in Global System on Module Market

- AI-Enabled Embedded Computing: Integration of NPUs and AI accelerators for real-time edge intelligence.

- ARM-Based Low-Power Architecture: Energy-efficient SoMs for IoT, industrial, and portable applications.

- Edge AI Integration: Localized data processing for reduced latency and improved real-time decision-making.

- RISC-V Open Architecture Adoption: Flexible and customizable embedded computing platforms.

- Industrial IoT Expansion: SoMs enabling smart manufacturing, robotics, and automation systems.

- High-Performance x86 Embedded Modules: Advanced computing for edge servers and industrial control systems.

- Modular Computing Standards: COM Express, SMARC, and Qseven improving system interoperability.

- Cloud-Edge Integration: Seamless connectivity between embedded devices and cloud ecosystems.

Strategic Implications of Technology & Innovation

The technological evolution of the System on Module Market is transforming embedded computing into a highly modular, scalable, and AI-driven ecosystem that supports rapid innovation across multiple industries.

For manufacturers, SoM platforms enable faster time-to-market, reduced development complexity, and lower system integration costs, making them a preferred solution for next-generation electronic product development.As embedded systems become more intelligent and connected, competition is intensifying around performance optimization, power efficiency, AI integration, and ecosystem compatibility.

Industries such as automotive, healthcare, industrial automation, and telecommunications are increasingly relying on SoM-based architectures to support digital transformation, edge intelligence, and real-time data processing requirements. Cybersecurity, hardware reliability, and long-term scalability are becoming critical design considerations as SoM deployments expand across mission-critical and industrial environments.

Global System on Module Market Technology & Innovation Forward Outlook

Looking ahead, the Global System on Module Market is expected to evolve toward highly intelligent, AI-integrated, and edge-optimized embedded computing ecosystems. Future SoM platforms will increasingly support autonomous decision-making, real-time analytics, and deep integration with cloud-native infrastructures.

Advancements in AI acceleration, low-power semiconductor design, and heterogeneous computing architectures will drive the next phase of innovation, enabling smarter devices with enhanced computational efficiency and adaptive performance capabilities.Mass adoption will be driven by growing demand for industrial automation, smart consumer electronics, autonomous systems, and connected healthcare devices, all requiring scalable embedded computing solutions.

Hybrid computing architectures combining edge AI, cloud connectivity, and modular hardware design are expected to become the standard framework for future embedded systems.In conclusion, the Global System on Module Market is transitioning into a core enabler of intelligent embedded computing ecosystems. Companies that lead in AI-enabled SoM platforms, energy-efficient architectures, and modular embedded solutions will define the future of edge computing and smart device innovation through 2033.