Global Humanoid Robot Market size, share and forecast 2026-2033

Global Humanoid Robot Market Forecast Snapshot: 2026???2033

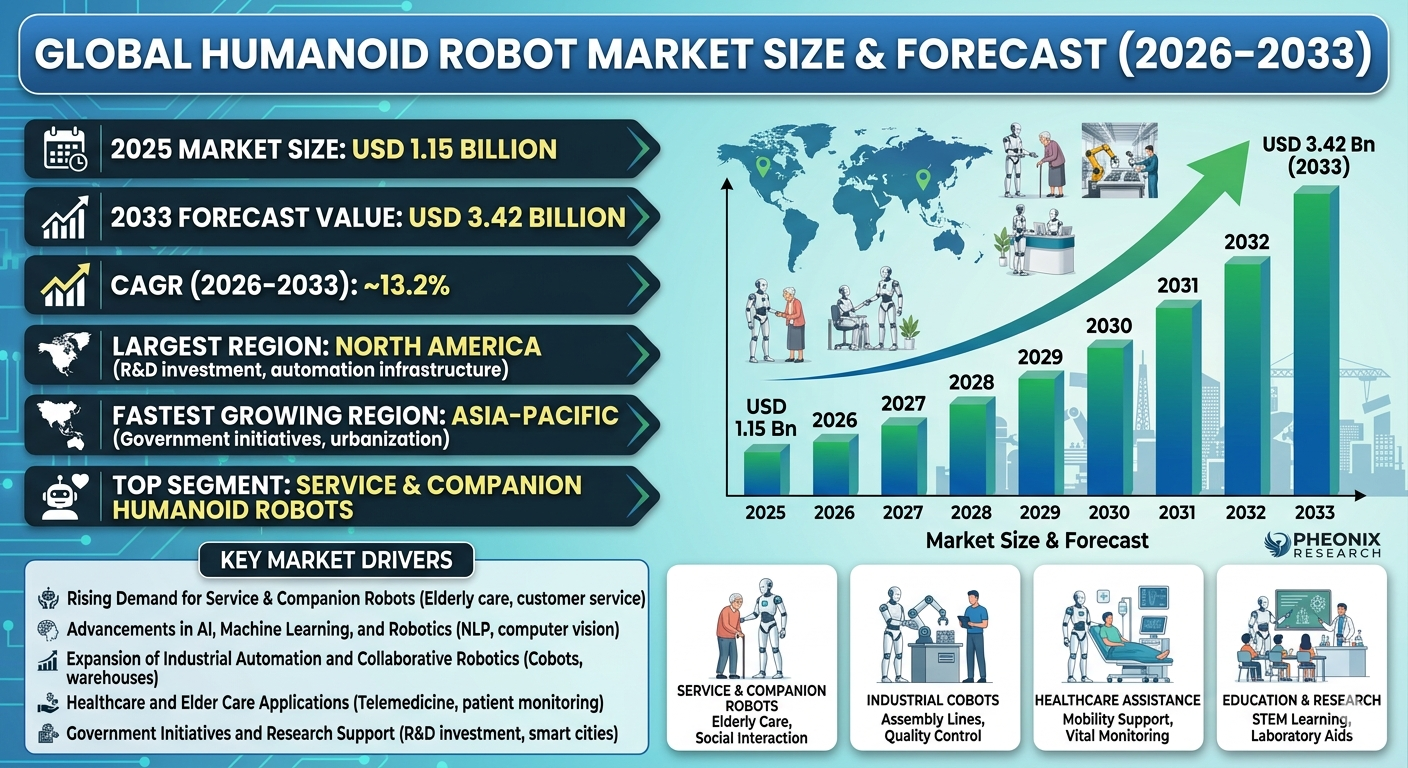

| Metric | Value |

| 2025 Market Size | USD 1.15 Billion |

| 2033 Market Size | USD 3.42 Billion |

| CAGR (2026???2033) | ~13.2% |

| Largest Region | North America |

| Fastest Growing Region | Asia-Pacific |

| Top Segment | Service & Companion Humanoid Robots |

| Key Trend | AI-Powered Interaction & Collaborative Robotics |

| Future Focus | Healthcare Assistance, Education, and Industrial Automation |

Global Humanoid Robot Market Overview

The Global Humanoid Robot Market is experiencing rapid expansion, driven by advancements in AI, robotics, machine learning, and sensor technologies. Humanoid robots???designed to mimic human behavior and interaction???are increasingly deployed across healthcare, education, retail, research, and industrial environments.

According to Pheonix Research, the Global Humanoid Robot Market was valued at USD 1.15 Billion in 2025 and is projected to reach USD 3.42 Billion by 2033, registering a CAGR of ~13.2% during 2026???2033. Growth is fueled by rising demand for intelligent service robots, automation in healthcare and manufacturing, and increased adoption of AI-enabled collaborative robots.

North America currently dominates due to high R&D investment, early adoption of advanced robotics, and a mature industrial automation ecosystem. Asia-Pacific is the fastest-growing region, supported by rapid urbanization, government incentives for robotics, and adoption of AI and IoT technologies in industrial and service sectors.

Post-2025, the market is expected to see deeper integration of AI-based personal assistants, cloud-enabled robot intelligence, human-robot collaboration frameworks, and enhanced mobility features, positioning humanoid robots as critical tools in healthcare, education, and industrial automation rather than niche innovations.

Key Drivers of Global Humanoid Robot Market Growth

Rising Demand for Service and Companion Robots

Growing needs in healthcare, eldercare, education, and customer service are fueling demand for humanoid robots capable of social interaction, task assistance, and automated support.

Advancements in AI, Machine Learning, and Robotics

Integration of AI, natural language processing, and computer vision enables humanoid robots to perceive, understand, and respond to human commands, enhancing functionality across healthcare, education, retail, and industrial applications.

Expansion of Industrial Automation and Collaborative Robotics

Humanoid robots are increasingly working alongside humans in factories, warehouses, and laboratories, performing repetitive, high-precision, and collaborative tasks that improve productivity and operational efficiency.

Healthcare and Elder Care Applications

Robots that assist with mobility, patient monitoring, telemedicine, and companionship are gaining traction as essential tools to address aging populations, labor shortages, and rising demand for personalized care solutions.

Government Initiatives and Research Support

Global investments in robotics R&D, smart city programs, and AI innovation policies are accelerating humanoid robot development, testing, and commercialization, supporting long-term market expansion.

Global Humanoid Robot Market Segmentation

?? ?? ?? ??1.By Robot Type

1. Service & Companion Robots1.1 Elderly Care & Healthcare Assistance Robots

1.1.1 Mobility Support Robots

1.1.1.1 Walking Assist Robots

1.1.1.2 Stair-Climbing Assist Robots

1.1.1.3 Exoskeleton-Assisted Mobility Robots

1.1.2 Patient Monitoring & Assistance Robots

1.1.2.1 Telepresence Healthcare Robots

1.1.2.2 Vital Sign Monitoring Robots

1.1.2.3 Medication Dispensing Robots

1.1.3 Social Companion Robots

1.1.3.1 Conversational AI Robots

1.1.3.2 Cognitive & Emotional Interaction Robots

1.1.3.3 Entertainment & Engagement Robots 1.2 Customer Service & Retail Robots

1.2.1 Reception & Concierge Robots

1.2.1.1 Lobby Reception Robots

1.2.1.2 Hotel Concierge Robots

1.2.1.3 Office & Enterprise Reception Robots

1.2.2 Information & Navigation Robots

1.2.2.1 Wayfinding Robots

1.2.2.2 Interactive Kiosk Robots

1.2.2.3 Shopping Assistance Robots

1.2.3 Entertainment & Hospitality Robots

1.2.3.1 Amusement Park Service Robots

1.2.3.2 Event Hosting & Performance Robots

1.2.3.3 Restaurant & Caf?? Service Robots 2. Industrial & Research Humanoid Robots

2.1 Manufacturing & Assembly Robots

2.1.1 Collaborative Industrial Robots (Cobots)

2.1.1.1 Assembly Line Cobots

2.1.1.2 Quality Control Cobots

2.1.1.3 Packing & Palletizing Cobots

2.1.2 Inspection & Quality Control Robots

2.1.2.1 Defect Detection Robots

2.1.2.2 Precision Measurement Robots

2.1.2.3 Visual Inspection Cobots

2.1.3 Material Handling Humanoids

2.1.3.1 Warehouse Transport Robots

2.1.3.2 Loading & Unloading Robots

2.1.3.3 Heavy Component Handling Robots 2.2 Research & Education Robots

2.2.1 Laboratory Assistants

2.2.1.1 Automated Experiment Assistants

2.2.1.2 Sample Handling Robots

2.2.1.3 AI-Enabled Lab Support Robots

2.2.2 Educational Teaching Assistants

2.2.2.1 Classroom Instruction Robots

2.2.2.2 STEM Learning Robots

2.2.2.3 Remote Learning Companion Robots

2.2.3 Experimental AI & Robotics Platforms

2.2.3.1 Prototype Development Robots

2.2.3.2 Simulation & Testing Humanoids

2.2.3.3 Research-Oriented Modular Robots 3. Military & Defense Humanoid Robots

3.1 Surveillance & Reconnaissance Humanoids

3.1.1 Border Patrol Robots

3.1.2 Facility Security Humanoids

3.1.3 Recon Drones with Humanoid Interfaces

3.2 Bomb Disposal & Hazardous Task Robots

3.2.1 Explosive Ordnance Disposal (EOD) Robots

3.2.2 Chemical & Biological Hazard Robots

3.2.3 Fire & Disaster Response Robots

3.3 Tactical Training & Simulation Robots

3.3.1 Combat Training Simulators

3.3.2 Tactical Scenario Humanoids

3.3.3 Military Skill Development Robots

?? ??2.By Payload & Mobility

1. Light-Duty Humanoids (<50 kg)1.1 Indoor Service Robots

1.1.1 Reception & Guidance

1.1.2 Entertainment & Education

1.1.3 Light Material Handling 2. Medium-Duty Humanoids (50???150 kg)

2.1 Industrial Cobots

2.1.1 Assembly Line Support

2.1.2 Inspection & QA

2.1.3 Warehouse Assistance 3. Heavy-Duty Humanoids (>150 kg)

3.1 Construction & Heavy Material Handling

3.1.1 Automotive Component Transport

3.1.2 Aerospace Assembly Support

3.1.3 Military Logistics Support 4. Wheeled Mobility Robots

4.1 Indoor Navigation

4.1.1 Hospital Transport Robots

4.1.2 Retail Delivery Robots

4.1.3 Educational & Research Platforms 5. Bipedal / Legged Mobility Robots

5.1 Terrain-Adaptive Robots

5.1.1 Elder Care Walking Assist

5.1.2 Industrial Floor Cobots

5.1.3 Military & Disaster Response

?? ?? ?? 3.By End-User Industry

1. Healthcare & Elder Care1.1 Hospitals & Clinics

1.1.1 Surgery Assistance Humanoids

1.1.2 Patient Transport Robots

1.1.3 Telemedicine Support Robots

1.2 Assisted Living & Nursing Homes

1.2.1 Mobility Support Humanoids

1.2.2 Social Companion Robots

1.2.3 Remote Monitoring Robots

1.3 Home Healthcare

1.3.1 Home Care Companion Robots

1.3.2 Medication & Reminder Robots

1.3.3 Telepresence Healthcare Robots 2. Education & Research

2.1 Schools & Universities

2.1.1 STEM Teaching Humanoids

2.1.2 Classroom Assistance Robots

2.1.3 Student Interaction & Learning Robots

2.2 Robotics Research Labs

2.2.1 Experimental AI Platforms

2.2.2 Collaborative Research Humanoids

2.2.3 Prototyping & Testing Robots

2.3 Technical Training Centers

2.3.1 Vocational Skill Humanoids

2.3.2 Industrial Simulation Robots

2.3.3 Laboratory Training Robots 3. Industrial & Manufacturing

3.1 Automotive & Electronics Assembly

3.1.1 Line Assembly Cobots

3.1.2 Inspection & QA Robots

3.1.3 Component Handling Humanoids

3.2 Consumer Goods Manufacturing

3.2.1 Packaging & Palletizing Robots

3.2.2 Warehouse Logistics Humanoids

3.2.3 Product Inspection Robots

3.3 Pharmaceutical & Chemical Processing

3.3.1 Lab Sample Handling

3.3.2 Precision Manufacturing Robots

3.3.3 Safety & Hazardous Material Robots 4. Retail & Hospitality

4.1 Hotels & Restaurants

4.1.1 Concierge & Reception Robots

4.1.2 Room Service Humanoids

4.1.3 Entertainment & Experience Robots

4.2 Shopping Malls & Customer Service

4.2.1 Wayfinding & Assistance Robots

4.2.2 Security & Monitoring Robots

4.2.3 Product Interaction Robots

4.3 Entertainment & Theme Parks

4.3.1 Performers & Host Robots

4.3.2 Interactive Guide Robots

4.3.3 Amusement Support Robots 5. Defense & Security

5.1 Military Training & Reconnaissance

5.1.1 Tactical Simulation Humanoids

5.1.2 Border Patrol & Surveillance Robots

5.1.3 Drone-Assisted Humanoids

5.2 Border & Facility Security

5.2.1 Guard & Monitoring Robots

5.2.2 Threat Detection Humanoids

5.2.3 AI-Integrated Security Robots

5.3 Hazardous Task Automation

5.3.1 Bomb Disposal Robots

5.3.2 Chemical/Biological Hazard Robots

5.3.3 Fire & Disaster Response Humanoids

?? ?? ??4. by Region

7.1 North America

7.2 Europe

7.3 Asia-Pacific

7.4 Middle East & Africa

7.5 South America

Regional Insights of Global Humanoid Robot Market

North America ??? Largest Market

North America leads the global humanoid robot market, driven by high adoption of AI-enabled robotics, substantial R&D investment, and advanced industrial automation infrastructure. The United States and Canada are at the forefront, leveraging technology integration in healthcare, research, and industrial applications to maintain market dominance.

Asia-Pacific ??? Fastest Growing Market

Asia-Pacific is the fastest-growing region, fueled by government-supported robotics initiatives, rapid urbanization, and industrial modernization. Key markets such as China, Japan, South Korea, and India are witnessing significant deployment of humanoid robots across manufacturing, service, healthcare, and research sectors.

Europe

Europe???s growth is underpinned by strong precision engineering capabilities, AI and machine learning integration, and expanding applications in healthcare and research. Germany, France, and the UK are emerging as innovation hubs for service, industrial, and collaborative humanoid robots.

Middle East & Africa

Growth in the Middle East & Africa is supported by defense and security automation, large-scale infrastructure projects, and early adoption of industrial and service humanoid robots. Urban centers are increasingly incorporating robotics into public service, logistics, and security operations.

South America

South America is experiencing steady expansion, driven by industrial modernization, university-led robotics research, and small-scale healthcare and service robotics initiatives. Brazil, Argentina, and Chile are key contributors to regional market development.

Leading Companies of Global Humanoid Robot Market

-

Toyota Motor Corporation

-

Boston Dynamics

-

PAL Robotics

-

FANUC Corporation

-

Kawada Robotics

-

Robotics Inventions & Startups

SoftBank Robotics and Honda remain the front-runners in social and service robotics due to their extensive deployment, brand recognition, and advanced AI capabilities.

Strategic Intelligence & AI-Backed Insights

-

Pheonix Demand Forecast Engine: Projects robust double-digit growth across healthcare, eldercare, research, and industrial humanoid robot applications, driven by rising adoption and technological advancements.

-

Consumer Behavior Analyzer: Highlights key demand drivers, including elderly care, educational institutions, research laboratories, and industrial enterprises requiring collaborative and service-oriented humanoid robots.

-

Innovation Tracker: Emphasizes AI-assisted human interaction, advanced sensor integration, enhanced mobility and dexterity, and cloud-connected functionalities as core differentiators for next-generation humanoid robots.

-

Porter???s Five Forces Analysis: Indicates intense competitive rivalry, moderate supplier leverage, and significant opportunities for companies offering differentiated, AI-powered, and application-specific humanoid robot solutions.

Why the Humanoid Robot Market is Critical

-

Increasing demand for automation in healthcare, education, and industrial sectors.

-

AI-enabled humanoids improve operational efficiency, human-machine collaboration, and labor optimization.

-

Rising investments in research & development accelerate innovation and adoption.

-

Advanced humanoid robots address labor shortages, safety concerns, and precision requirements.

Final Takeaway of Global Humanoid Robot Market

The Global Humanoid Robot Market is rapidly transitioning from experimental prototypes to mainstream adoption across healthcare, industrial, research, and service sectors. With a projected CAGR of ~13.2% during 2026???2033, growth is driven by AI integration, robotics innovation, and increasing automation demand.

Companies that invest in AI-powered humanoid platforms, collaborative robotics, enhanced mobility, and cloud connectivity are positioned to capture long-term value. Strategic partnerships, R&D investment, and alignment with industry-specific automation needs will remain key differentiators in the post-2025 landscape.

At Pheonix Research, our advanced forecasting models provide in-depth revenue analysis, competitive benchmarking, and strategic intelligence ??? enabling stakeholders to capitalize on emerging opportunities in the humanoid robot market with data-backed confidence and sustainable growth strategies.

???? Social Mentions & Publication Channels

??Explore deeper insights and follow our cross-platform updates on LinkedIn??and X for continuous intelligence and market coverage.

LinkedIn : https://www.linkedin.com/feed/update/urn:li:activity:7433442331619520512

X : https://x.com/Pheonix_Insight/status/2027678437176123826?s=20

Competitive Landscape

Global Humanoid Robot Market Competitive Intensity & Market Structure Overview

The Global Humanoid Robot Market is characterized by a rapidly evolving, innovation-intensive, and moderately fragmented competitive ecosystem where advanced robotics companies, AI developers, industrial automation leaders, and emerging startups compete across service, healthcare, industrial, education, and defense applications.

Unlike mature industrial robotics segments, humanoid robotics remains in a developmental-commercialization transition phase, where competitive positioning is defined less by scale alone and more by AI capability, mobility sophistication, sensor integration, and human-machine interaction performance.

The market structure is bifurcated between established multinational technology firms such as SoftBank Robotics, Honda, Toyota, and Boston Dynamics, which leverage strong R&D resources and global deployment visibility, and emerging innovators focused on niche humanoid applications such as eldercare, industrial collaboration, or education.

Competitive intensity is high due to rapid technological innovation, increasing venture capital inflows, government-backed robotics programs, and expanding enterprise adoption. However, commercialization barriers remain substantial due to high development costs, hardware complexity, and long deployment cycles.

As AI-powered interaction, autonomous mobility, and collaborative robotics advance, the market is shifting from prototype competition toward scalable deployment ecosystems, creating a race for technological leadership, affordability, and industry specialization.

Global Humanoid Robot Market Competitive Intensity & Market Structure Current Scenario

Leading Company Profiles

SoftBank Robotics: Global leader in social and service robotics, known for Pepper and NAO platforms with strong presence in education, customer engagement, and enterprise service robotics.

Honda Motor Co., Ltd.: Pioneer in humanoid robotics through ASIMO and advanced mobility-focused AI systems emphasizing human interaction and assistive applications.

Toyota Motor Corporation: Expanding humanoid and assistive robotics through healthcare, mobility, and industrial automation initiatives.

Boston Dynamics: High-performance robotics innovator specializing in mobility, dynamic balance, and advanced humanoid movement systems with industrial and defense relevance.

PAL Robotics: European robotics company focused on research, healthcare, retail, and collaborative humanoid solutions.

FANUC Corporation: Industrial robotics powerhouse increasingly integrating humanoid-adjacent collaborative automation capabilities.

Kawada Robotics: Known for precision humanoid systems in research and industrial collaboration.

Tesla (Optimus Program): Emerging disruptive player targeting scalable industrial and general-purpose humanoid deployment.

Agility Robotics: Fast-growing innovator in warehouse and logistics humanoid robotics.

Sanctuary AI & Figure AI: Startup-driven competitors focused on AI-first humanoid intelligence and enterprise deployment models.

Key Competitive Intensity & Market Structure Signals in Humanoid Robot Market

A major structural signal is the increasing convergence of robotics hardware with AI software ecosystems. Competitive differentiation is increasingly centered on cognitive intelligence, adaptive learning, computer vision, and real-time interaction rather than physical robotics alone.

Another defining factor is sector-specific specialization. Healthcare and eldercare prioritize empathy, communication, and patient support; industrial environments prioritize strength, endurance, and safety; while education emphasizes interactivity and programmability.

Government funding and national robotics strategies are also shaping market structure, particularly in Asia-Pacific where China, Japan, and South Korea are accelerating commercialization through public-private investment.

Despite technological excitement, high production costs, battery limitations, and deployment scalability remain major barriers, limiting widespread commoditization and preserving competitive advantages for well-capitalized firms.

Strategic partnerships between AI firms, semiconductor companies, cloud providers, and robotics manufacturers are increasingly critical, signaling that humanoid robotics is becoming an ecosystem competition rather than a standalone hardware market.

Strategic Implications of Competitive Intensity & Market Structure in Humanoid Robot Market

Manufacturers must prioritize integrated platform strategies combining robotics hardware, conversational AI, cloud intelligence, and sector-specific software to remain competitive.

First-mover advantage in real-world deployment is becoming increasingly valuable, particularly in healthcare, logistics, and industrial automation where data collection and iterative learning improve long-term product performance.

Cost reduction through modular design, scalable manufacturing, and battery innovation will be critical to unlocking broader enterprise and consumer adoption.

Trust, safety compliance, and ethical AI frameworks are emerging as strategic necessities, particularly for humanoids deployed in healthcare, education, and public environments.

The rise of collaborative humanoids (working alongside humans) rather than fully autonomous replacements suggests that companies emphasizing augmentation, safety, and productivity enhancement may achieve stronger adoption than purely disruptive automation models.

Global Humanoid Robot Market Competitive Intensity & Market Structure Forward Outlook

The Global Humanoid Robot Market is expected to remain highly dynamic and innovation-led through 2033, with increasing consolidation around companies capable of combining AI leadership, mobility engineering, and scalable deployment economics.

North America is likely to maintain technological leadership through AI innovation and startup ecosystems, while Asia-Pacific is expected to dominate manufacturing scale and deployment expansion.

Future competition will increasingly focus on three strategic pillars: AI-powered cognition, mobility dexterity, and commercial scalability.

As humanoid robots transition from pilot projects to enterprise and institutional deployment, strategic alliances between robotics developers, cloud AI providers, semiconductor firms, and healthcare or industrial operators will intensify.

Long term, the market will likely evolve toward a hybrid structure where premium advanced humanoids dominate specialized sectors, while lower-cost functional humanoids expand into broader commercial applications. Companies that successfully align intelligence, safety, and cost efficiency will lead the Global Humanoid Robot Market through 2033.

Value Chain

Global Humanoid Robot Market Value Chain & Supply Chain Evolution Overview

The Global Humanoid Robot Market value chain is rapidly evolving from experimental robotics innovation into a scalable, AI-driven automation ecosystem that integrates advanced manufacturing, software intelligence, sensor fusion, mobility engineering, and industry-specific deployment models. Unlike traditional industrial robotics focused solely on repetitive automation, humanoid robots are increasingly designed for human-like interaction, mobility, decision-making, and collaborative task execution across healthcare, education, manufacturing, defense, hospitality, and research sectors.

The humanoid robot value chain spans upstream semiconductor and sensor suppliers, AI software development, robotic hardware engineering, actuator systems, battery technologies, machine vision platforms, cloud intelligence systems, systems integration, OEM manufacturing, application deployment, enterprise partnerships, and lifecycle support services. As humanoid robots transition from prototype development to real-world operational systems, value creation increasingly depends on intelligent autonomy, adaptability, and industry specialization.

Upstream supply chain dynamics are shaped by high-performance chip manufacturers, computer vision developers, LiDAR and sensor providers, servo motor suppliers, battery technology innovators, robotic chassis engineers, and AI software platforms. Advanced humanoid functionality increasingly relies on breakthroughs in edge computing, generative AI, machine learning, real-time perception systems, and mobility frameworks.

Platform development strategies increasingly prioritize modular robotics architectures, AI-powered cognitive systems, cloud-connected robotics, digital twin simulation, multi-environment adaptability, and vertical-specific customization for healthcare, industrial automation, defense, and service applications.

Distribution models are evolving through direct enterprise sales, robotics-as-a-service (RaaS), healthcare partnerships, educational deployments, government defense contracts, and industrial automation integration. Humanoid robot monetization is shifting from hardware-only sales toward recurring software upgrades, AI licensing, predictive maintenance, and cloud-based operational intelligence.

Supply chain challenges include high production costs, semiconductor dependencies, AI safety concerns, battery limitations, regulatory scrutiny, workforce displacement debates, ethical governance, and technological complexity in balancing mobility, dexterity, and cognitive functionality.

Global Humanoid Robot Market Value Chain & Supply Chain Evolution Current Scenario

The current humanoid robot market is shaped by rising AI maturity, labor shortages, industrial automation priorities, aging populations, and increasing demand for collaborative robotics solutions.

Upstream, manufacturers are heavily investing in AI chips, robotic actuators, machine vision systems, advanced battery systems, and precision engineering to improve humanoid dexterity, movement efficiency, and decision-making capabilities.

Technology ecosystems increasingly focus on conversational AI, natural language processing, mobility enhancement, cloud robotics, machine learning adaptation, and real-time environmental responsiveness.

Deployment infrastructure is expanding across healthcare assistance, eldercare, customer service, industrial manufacturing, warehouse logistics, education, and defense simulation programs.

Distribution is currently dominated by enterprise contracts, robotics labs, institutional adoption, industrial OEM partnerships, and pilot deployments in healthcare and service industries.

Competitive advantage increasingly depends on AI sophistication, hardware reliability, operational flexibility, human-safe interaction, and application-specific ROI.

Key Value Chain & Supply Chain Evolution Signals in Global Humanoid Robot Market

Several transformational trends are reshaping the humanoid robotics ecosystem globally.

First, AI-powered interaction systems are becoming the dominant differentiator, enabling humanoids to move beyond mechanical automation into socially intelligent and adaptive systems.

Second, healthcare and eldercare applications are emerging as major growth catalysts due to demographic aging, labor shortages, and demand for personalized support systems.

Third, collaborative industrial humanoids are increasingly being integrated into smart factories, logistics centers, and precision manufacturing environments.

Fourth, robotics-as-a-service (RaaS) models are expanding accessibility by reducing upfront capital costs for enterprises and institutions.

Fifth, cloud-connected robotics and digital twin ecosystems are improving scalability, software updates, predictive diagnostics, and operational optimization.

Sixth, government-backed robotics innovation initiatives are accelerating commercialization, safety testing, and industrial competitiveness globally.

Strategic Implications of Value Chain & Supply Chain Evolution in Global Humanoid Robot Market

Leading companies such as SoftBank Robotics, Honda, Boston Dynamics, Toyota, and PAL Robotics are strengthening competitive positions through AI integration, mobility innovation, industry specialization, and large-scale deployment partnerships.

Long-term competitive leadership increasingly depends on balancing hardware innovation with scalable AI ecosystems, software monetization, and vertical integration.

Companies specializing in healthcare support, industrial collaboration, and human-interactive service robotics are better positioned to capture sustained commercial adoption.

Strategic differentiation increasingly requires cloud intelligence, adaptive learning systems, modular engineering, and safety-certified robotics frameworks.

Supply chain resilience will increasingly depend on semiconductor access, actuator efficiency, software scalability, and regulatory adaptability.

As commercialization accelerates, humanoid robotics firms must increasingly evolve from hardware manufacturers into intelligent automation ecosystem providers.

Global Humanoid Robot Market Value Chain & Supply Chain Evolution Forward Outlook

Between 2026 and 2033, the humanoid robot value chain is expected to become more AI-native, cloud-connected, healthcare-integrated, and enterprise-deployed.

Humanoid platforms will increasingly prioritize autonomous learning, emotion-aware interaction, advanced mobility systems, and specialized industry deployment capabilities.

Supply chains are expected to increasingly integrate semiconductor optimization, battery innovation, robotics software platforms, and advanced sensor ecosystems.

Distribution frameworks will likely expand through healthcare systems, industrial automation providers, education systems, logistics enterprises, and public infrastructure deployments.

Recurring monetization models are expected to evolve through AI subscription frameworks, software licensing, predictive maintenance, and Robotics-as-a-Service platforms.

Ultimately, the humanoid robot market will transition from hardware-centric robotics innovation toward a broader intelligent human-machine infrastructure supporting healthcare, education, industrial productivity, and next-generation automation.

Market-Specific Value Chain

- Core Technology & Component Supply: Semiconductors, AI chips, sensors, LiDAR, cameras, servo motors, actuators, battery systems, robotics processors

- AI Software & Cognitive Infrastructure: Machine learning, NLP, computer vision, cloud robotics, edge AI, digital twins, predictive intelligence

- Hardware Engineering & Robot Manufacturing: Chassis design, humanoid assembly, mobility systems, dexterity platforms, OEM robotics manufacturing

- Platform Integration & Application Development: Healthcare robots, industrial humanoids, education robots, service robots, defense platforms

- Distribution & Commercial Deployment: Enterprise sales, RaaS models, healthcare systems, government contracts, industrial automation partnerships

- Lifecycle Services & Ecosystem Expansion: AI software upgrades, maintenance, predictive diagnostics, cloud intelligence, robotics ecosystems

Company-to-Stage Mapping

- Core Technology & Component Supply: NVIDIA, Intel, Qualcomm Robotics, Sony Sensors, Bosch Sensortec

- AI Software & Cognitive Infrastructure: Boston Dynamics AI systems, SoftBank Robotics AI, Toyota AI Labs, cloud robotics developers

- Hardware Engineering & Robot Manufacturing: Honda, SoftBank Robotics, PAL Robotics, Kawada Robotics, Tesla Optimus

- Platform Integration & Application Development: Healthcare humanoid developers, industrial robotics OEMs, educational robotics firms

- Distribution & Commercial Deployment: Enterprise automation providers, defense agencies, hospitals, schools, logistics operators

- Lifecycle Services & Ecosystem Expansion: Robotics-as-a-Service providers, AI software partners, predictive maintenance platforms, cloud robotics ecosystems

Investment Activity

Global Humanoid Robot Market Investment & Funding Dynamics Overview

Investment and funding dynamics in the Global Humanoid Robot Market are accelerating rapidly as AI innovation, robotics engineering, automation priorities, and human-machine collaboration reshape next-generation technology ecosystems. Between 2026 and 2033, capital deployment is expected to expand aggressively across service robotics, industrial humanoids, healthcare support systems, mobility platforms, AI software frameworks, and cloud-connected robotic intelligence.

The humanoid robot sector is transitioning from R&D-intensive experimentation into commercialization-led investment cycles, attracting venture capital, sovereign innovation funds, industrial automation investors, and strategic corporate partnerships. Major players including SoftBank Robotics, Honda, Toyota, Boston Dynamics, and emerging robotics startups are securing substantial investments to scale manufacturing, improve AI interaction capabilities, and expand sector-specific humanoid applications.

A major transformation shaping investment flow is the shift from novelty-based robotics toward productivity-driven humanoid deployment, where funding increasingly prioritizes healthcare assistance, industrial labor augmentation, eldercare, logistics, defense, and education. This transition is directing capital toward advanced sensors, autonomous movement systems, generative AI integration, and robotic operating ecosystems.

Global Humanoid Robot Market Investment & Funding Dynamics Current Scenario

Currently, global investment activity is supported by rising labor shortages, AI breakthroughs, increasing eldercare demands, industrial automation expansion, and government-backed robotics innovation strategies. Funding momentum is strongest in AI-enabled humanoid design, collaborative industrial robotics, healthcare companions, and research-grade robotics platforms.

- North America: Leads investment activity due to strong venture capital ecosystems, advanced AI development, defense robotics, and large-scale R&D funding.

- Asia-Pacific: Fastest-growing investment hub supported by robotics-friendly industrial policies, smart manufacturing expansion, and large-scale humanoid commercialization in China, Japan, and South Korea.

- Europe: Strong funding momentum driven by precision robotics engineering, healthcare innovation, and collaborative industrial automation.

- Middle East & Africa and South America: Emerging investment markets focusing on security robotics, public service automation, and industrial modernization.

Key Investment & Funding Dynamics Signals in Global Humanoid Robot Market

- AI-powered interaction systems are attracting significant funding for conversational intelligence, adaptive learning, and human-behavior simulation.

- Healthcare and eldercare robotics are becoming major capital magnets due to demographic aging and workforce shortages.

- Industrial humanoids are drawing investment as manufacturers seek flexible automation beyond fixed robotic arms.

- Cloud robotics and Robotics-as-a-Service (RaaS) business models are unlocking recurring revenue investment opportunities.

- Government-backed robotics innovation grants and defense modernization programs are accelerating commercialization pipelines.

Strategic Implications of Investment & Funding Dynamics in Global Humanoid Robot Market

- Investment leadership increasingly favors companies capable of combining advanced AI software with scalable robotic hardware manufacturing.

- Healthcare, industrial automation, and education represent the highest long-term ROI segments for humanoid robotics investors.

- Strategic partnerships between robotics firms, AI developers, semiconductor suppliers, and cloud providers are becoming essential for ecosystem dominance.

- Regional diversification is critical, with North America leading AI innovation while Asia-Pacific scales production and deployment.

- Cost reduction, mobility enhancement, and real-world functional reliability remain primary funding priorities.

Global Humanoid Robot Market Investment & Funding Dynamics Forward Outlook

Looking ahead, the Global Humanoid Robot Market is expected to attract robust long-term investment as humanoids increasingly evolve into commercially viable assets across healthcare, manufacturing, logistics, education, and defense.

Future funding will increasingly prioritize autonomous mobility systems, dexterous manipulation, generative AI integration, real-time decision intelligence, battery optimization, and sector-specific humanoid platforms.

- North America: Will remain the innovation capital for AI software, defense robotics, and advanced humanoid intelligence systems.

- Asia-Pacific: Will dominate manufacturing-scale investment and commercial deployment expansion.

- Europe: Will strengthen its role in precision engineering, collaborative robotics, and healthcare humanoid development.

The rise of Robotics-as-a-Service, AI subscription ecosystems, and enterprise humanoid deployment models will increasingly shape future capital allocation strategies.

Overall, the market is positioned as one of the highest-growth frontier technology sectors through 2033, supported by AI maturity, labor economics, demographic demand, and automation necessity. Companies that successfully combine affordability, intelligence, scalability, and application-specific humanoid functionality will define the next era of global robotics investment leadership.

Technology & Innovation

Global Humanoid Robot Market Technology & Innovation Landscape Overview

The technology and innovation landscape within the Global Humanoid Robot Market is rapidly advancing toward intelligent, adaptive, and collaborative robotics ecosystems where humanoid machines increasingly replicate human interaction, movement, and decision-making. Humanoid robots are transitioning from experimental engineering platforms into commercially viable service, industrial, healthcare, and educational assets powered by AI, machine learning, sensor fusion, and cloud robotics.

Innovation intensity in the humanoid robotics sector is exceptionally high, driven by breakthroughs in artificial intelligence, natural language processing (NLP), computer vision, actuator precision, mobility engineering, and human-robot interaction frameworks. Leading companies such as SoftBank Robotics, Honda, Tesla Robotics, Boston Dynamics, Toyota, and emerging robotics startups are investing aggressively in next-generation humanoid platforms that combine physical dexterity with cognitive intelligence.

A major technological transformation is the convergence of generative AI, real-time environmental sensing, and embodied intelligence, enabling humanoid robots to move beyond scripted functionality toward autonomous reasoning, contextual awareness, and dynamic task adaptation. This shift is positioning humanoid robots as scalable workforce augmentation tools across eldercare, industrial automation, logistics, education, and customer-facing service environments.

Simultaneously, advancements in edge computing, cloud robotics, battery efficiency, and robotic operating systems are accelerating deployment feasibility by improving responsiveness, lowering latency, and enabling continuous software upgrades across distributed humanoid fleets.

Global Humanoid Robot Market Technology & Innovation Landscape Current Scenario

Currently, the humanoid robot industry is focused on improving mobility realism, cognitive intelligence, human safety, and deployment scalability. Companies are prioritizing technologies that enhance practical usability while reducing cost barriers and expanding commercial applications.

AI-powered conversational intelligence is one of the most significant innovation pillars. Advanced NLP systems, multimodal AI, and emotional recognition technologies are enabling humanoid robots to understand speech, interpret context, and interact naturally with humans in healthcare, retail, hospitality, and educational settings.

Mobility and locomotion systems are undergoing major breakthroughs through bipedal balancing algorithms, force-feedback control, gyroscopic stability systems, and advanced actuators. These innovations are allowing humanoid robots to navigate stairs, uneven terrain, warehouses, and public spaces with increasing agility.

Sensor fusion technologies combining LiDAR, cameras, ultrasonic sensors, tactile sensors, and computer vision are significantly enhancing environmental awareness. This enables humanoids to identify objects, avoid obstacles, interpret gestures, and safely collaborate alongside humans.

Collaborative industrial humanoids are gaining momentum in manufacturing and logistics through precision gripping systems, autonomous navigation, and task-learning AI. These systems are increasingly designed to perform repetitive, hazardous, or ergonomically challenging tasks.

Cloud-connected robotic intelligence is emerging as a major innovation driver, where humanoid robots can continuously improve through shared learning models, remote updates, and fleet-wide behavioral optimization.

Battery innovation and lightweight materials engineering are also reshaping the market by extending operating time, improving movement efficiency, and reducing deployment limitations across mobile applications.

Key Technology & Innovation Trends in Global Humanoid Robot Market

- AI-Powered Human Interaction: NLP, emotional AI, and conversational intelligence enabling natural engagement.

- Advanced Mobility & Dexterity: Bipedal locomotion, balance systems, and fine motor skill development.

- Sensor Fusion & Environmental Awareness: LiDAR, vision systems, tactile sensors, and contextual recognition.

- Cloud Robotics & Shared Learning: Centralized intelligence improving fleet-wide performance.

- Collaborative Industrial Humanoids: Workforce augmentation in factories, warehouses, and hazardous environments.

- Healthcare & Eldercare Robotics: Patient assistance, mobility support, telepresence, and emotional companionship.

- Generative AI Integration: Adaptive reasoning and contextual decision-making capabilities.

- Lightweight Materials & Battery Efficiency: Extended mobility and lower energy constraints.

Strategic Implications of Technology & Innovation

The technological evolution of humanoid robotics is reshaping automation from machine-centric systems into human-centric collaborative ecosystems. Companies leading in AI cognition, mobility engineering, and scalable deployment frameworks are likely to dominate future market share.

For healthcare providers, humanoid innovation offers scalable solutions for labor shortages, patient monitoring, rehabilitation, and eldercare support. In industrial settings, humanoid robots can significantly improve productivity, workplace safety, and operational continuity.

As humanoids become more commercially practical, competitive barriers are rising due to high R&D costs, software complexity, hardware precision requirements, and regulatory safety standards.

Governments and enterprises investing in robotics innovation are increasingly viewing humanoid robots as strategic infrastructure assets capable of supporting economic productivity, public services, and national technological competitiveness.

Ethical AI, safety compliance, and trust-building frameworks are also becoming strategic priorities, particularly in social, educational, and healthcare deployments.

Global Humanoid Robot Market Technology & Innovation Forward Outlook

Looking ahead, the Global Humanoid Robot Market is expected to evolve toward fully autonomous, emotionally intelligent, and industry-specialized robotic ecosystems. Future humanoids will increasingly function as integrated service providers, industrial collaborators, and adaptive assistants rather than standalone programmable machines.

Generative AI and embodied intelligence will likely drive the next phase of humanoid innovation, enabling robots to learn continuously, adapt independently, and perform increasingly complex cognitive and physical tasks.

Mass commercialization will depend heavily on reducing production costs, improving battery longevity, and creating modular hardware architectures that support broad vertical customization.

Industrial and logistics humanoids are expected to expand rapidly, while healthcare and eldercare humanoids may become one of the most transformative segments due to demographic aging and workforce shortages.

In conclusion, the Global Humanoid Robot Market is transitioning from prototype-led innovation into a scalable intelligent robotics economy. Companies that lead in AI-powered interaction, embodied cognition, mobility engineering, cloud robotics, and safety-centric deployment will shape the next generation of human-machine collaboration through 2033.