Global CBRN Protection Equipment Market size and share Analysis 2026-2033

Market Size & Forecast

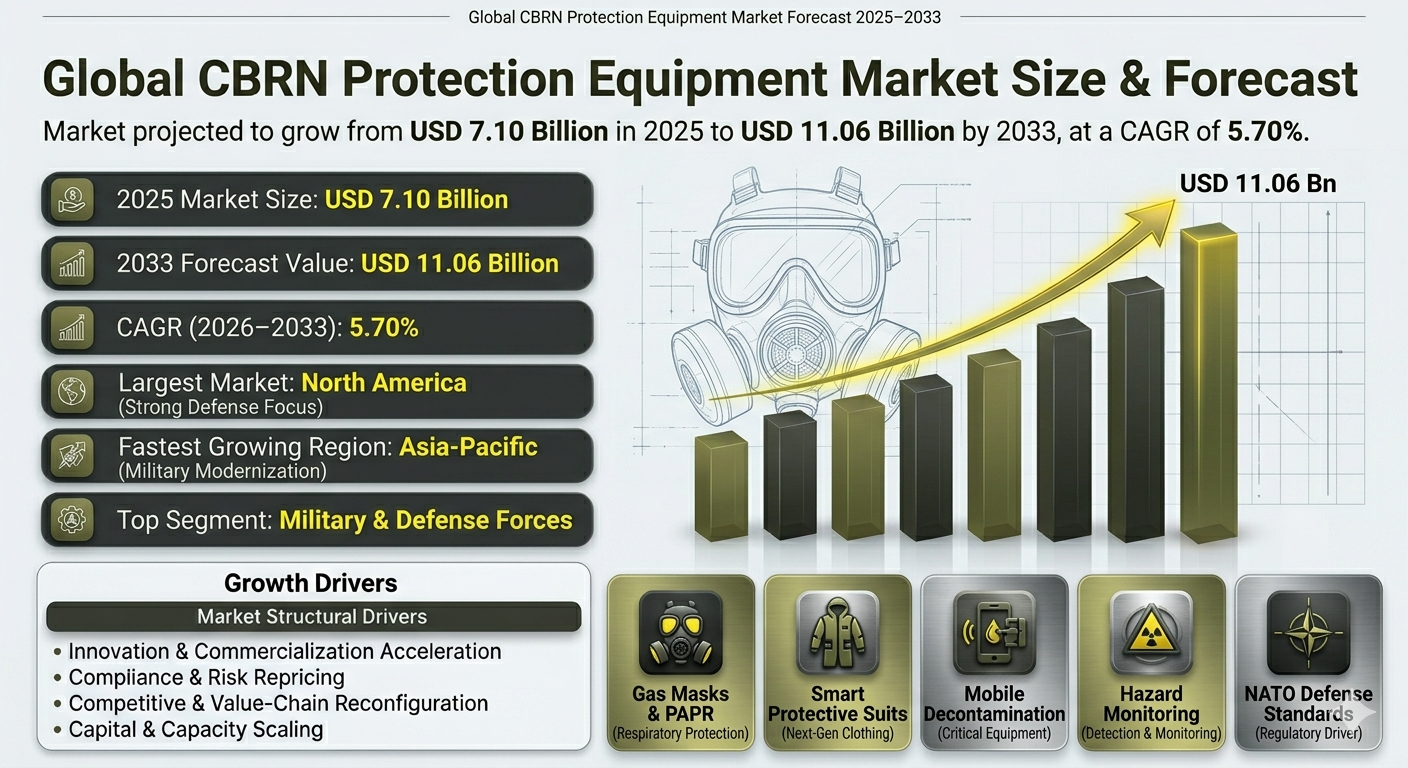

The Global CBRN Protection Equipment Market is projected to grow significantly from a base value of USD 7.10 billion in 2025 to an estimated USD 11.17 billion by 2033. This growth trajectory corresponds to a compound annual growth rate (CAGR) of approximately 5.82% during the forecast period of 2026 to 2033. The expansion in market size is underpinned by intensifying geopolitical tensions and the escalating frequency of chemical, biological, radiological, and nuclear (CBRN) threats worldwide, which collectively drive increased demand for advanced protective equipment. Several market dynamics converge to propel this growth. Rising global security concerns, including the persistent threat of terrorism and state-level defense modernization programs, have catalyzed significant investments in CBRN defense infrastructure. For instance, the NATO CBRN Defense Initiative launched in 2023 has stimulated funding and technology development aimed at accelerating innovation cycles. Similarly, governmental investments in homeland security and emergency preparedness further augment equipment adoption rates, especially in the military, civil protection, and emergency response sectors. Moreover, regulatory frameworks such as the EU PPE Regulation 2016/425 and evolving national standards in South Korea, the United States, and European countries impose stringent operational requirements, compelling manufacturers to innovate and comply with high safety standards. This regulatory tightening simultaneously elevates market entry barriers and enhances product quality, driving the market towards technologically sophisticated and compliant solutions. The projected market size reflects how these complex factors intertwine. The CAGR of 5.82% is not merely a function of increasing demand but is also shaped by the compression of development-to-commercialization cycles due to technology maturity and escalating capital deployment. For example, companies like Avon Protection and AirBoss Defense Group have introduced next-generation protective suits and secured strategic contracts, indicating market readiness for scaled adoption. In summary, the market size and forecast encapsulate a landscape where geopolitical imperatives, regulatory enforcement, technological innovation, and investment dynamics collectively reshape demand and supply, fostering robust and sustainable growth for the Global CBRN Protection Equipment Market over the next decade.

Market Overview

The Global CBRN Protection Equipment Market operates within a moderately consolidated competitive structure characterized by high competitive intensity. The market is populated by several tier 1 players, including 3M, Honeywell International Inc., Dr??gerwerk AG, Avon Protection, Thales Group, Rheinmetall AG, Smiths Detection, Teledyne FLIR, MSA Safety, and AirBoss of America Corporation. These incumbents dominate by leveraging extensive R&D capabilities, regulatory compliance expertise, and integrated value chains that accommodate high capital intensity and complex supply logistics. The market's demand profile is heavily influenced by geopolitical volatility and the rising frequency of industrial accidents and terrorist threats involving chemical, biological, radiological, and nuclear agents. Heightened global security concerns have prompted governments to increase defense budgets significantly???evidenced by Germany???s announced military expenditure increase and China???s rising military investments???and to prioritize modernization initiatives. These actions translate into accelerated procurement of advanced CBRN protective systems. Technological innovation serves as a critical differentiator, with companies focusing on smart protective suits, advanced filtration materials, and portable decontamination units. For example, in February 2026, Avon Protection introduced the EXOSKIN-S2 CBRN protective suit, incorporating cutting-edge materials and ergonomic design to enhance operational effectiveness for military and emergency response teams. Similarly, 3M???s launch of advanced respiratory protection products like the Scott AV-3000 HT facepiece reflects the growing emphasis on improving user safety and comfort. Regulatory pressures constitute a powerful shaping force in the market. Agencies such as NIOSH, the European Union, NATO, and the U.S. Department of Homeland Security enforce rigorous standards ranging from 42 CFR Part 84 to the 2017 EU CBRN Action Plan. These regulations elevate baseline requirements for equipment performance and certification, compelling manufacturers to invest heavily in compliance. The net effect is a market environment where product roadmaps are realigned to meet evolving standards, and execution standards are raised, thus supporting higher quality and more reliable protective solutions. Investment flows reinforce these dynamics. Despite the high capital intensity, defense and homeland security sectors attract rising investments aimed at expanding production capacity and improving process efficiency. The merger that created Airboss Defense Group exemplifies strategic consolidation to attain economies of scale and enhance competitive positioning. Government contracts, such as AirBoss Defense Group???s agreement with the Canadian Department of National Defense in November 2025, underscore the critical role of public sector spending in sustaining market momentum. However, the market faces notable challenges. High costs of advanced CBRN equipment and complex regulatory certification processes present barriers to entry and scaling, especially for newer players. The need to integrate emerging technologies, such as smart sensors and innovative materials, within existing supply chains further complicates product development. These factors maintain a moderately consolidated market structure where tier 1 companies with considerable resources dominate. Overall, the market overview reveals a complex interplay of drivers???geopolitical imperatives, regulatory demands, technological innovation, and investment trends???that collectively shape the competitive landscape and growth opportunities in the Global CBRN Protection Equipment Market.Structural Drivers of Market Growth

The growth trajectory of the Global CBRN Protection Equipment Market is fundamentally driven by four interrelated structural drivers that synthesize competitive, technological, investment, regulatory, and risk signals into distinct causal mechanisms shaping the market???s evolution. Innovation and Commercialization Acceleration The first driver arises from technological maturation coupled with strategic funding allocation that compresses the timeline from development to commercialization. This mechanism is evidenced by initiatives such as the NATO CBRN Defense Initiative launched in 2023, which has spurred targeted investments and technology development cycles aimed at rapidly deploying advanced protective equipment. The expansion of emergency responder training programs further supports faster adoption by creating a skilled user base ready for new technologies. Rising investments in defense and law enforcement agencies amplify this effect, enabling manufacturers to scale innovative solutions quickly. Consequently, the market sees an expanding addressable application space for CBRN equipment, spanning military, industrial, and civil protection sectors, which accelerates overall demand growth. Compliance and Risk Repricing The second driver is regulatory tightening combined with heightened risk awareness, which reprices operational requirements and raises execution standards across the market. Regulatory frameworks such as the EU PPE Regulation 2016/425 and South Korea???s Defense Acquisition Program Administration policies enforce stricter compliance, while export controls and technology transfer restrictions limit the diffusion of certain advanced technologies. These regulatory shifts compel product developers to realign roadmaps toward higher safety and performance benchmarks. Concurrently, risk factors???including the rising threat of chemical or biological warfare, misuse of hazardous materials by non-state actors, and increasing frequency of industrial accidents???intensify the need for reliable protection. The combined effect is a market that prioritizes compliance-led innovation, resulting in higher-quality equipment but also increased development and certification costs, which reinforce barriers to entry. Competitive and Value-Chain Reconfiguration The third driver emerges from competitive maneuvers and value-chain constraints that reallocate bargaining power and reshape market portfolios. Notable competitive moves include AirBoss Defense Group???s acquisition of a specialized protective equipment manufacturer and Avon Protection???s introduction of next-generation respirators and suits, signaling active portfolio repositioning toward high-performance, differentiated products. Expansion of national defense modernization programs and government investments drive demand shifts, prompting companies to optimize their supply chains and production processes to capture emerging growth segments. The high cost of equipment development, complex certification requirements, and compatibility challenges create bottlenecks within the value chain, concentrating margins among firms able to manage these complexities effectively. As a result, the competitive landscape becomes more dynamic, with consolidation and strategic partnerships serving as key responses to systemic value-chain constraints. Capital and Capacity Scaling The fourth driver is the deployment of capital into capacity expansion and process upgrades, which enhances throughput and reduces friction in equipment deployment. This mechanism draws on rising investments from government and private sectors aimed at scaling production capabilities to meet surging demand, particularly in high-priority segments such as military-grade respiratory systems and rapid deployment decontamination units. The expansion of homeland security initiatives, combined with emergency responder training programs, creates pressure for faster availability of reliable equipment. Additionally, defense modernization programs facilitate capital inflows that fund technology upgrades and manufacturing efficiencies. The integration of new materials and smart technologies is accelerated by such investments, enabling the market to address complex threat environments more effectively. Consequently, capacity scaling reduces time-to-market and cost pressures, supporting sustained growth and market expansion. Together, these four structural drivers???Innovation and Commercialization Acceleration, Compliance and Risk Repricing, Competitive and Value-Chain Reconfiguration, and Capital and Capacity Scaling???interact to underpin the fundamental growth dynamics of the Global CBRN Protection Equipment Market. They explain not only the quantitative expansion forecasted but also the qualitative evolution in product sophistication, market structure, and operational efficiency.Market Segmentation Analysis

Top-Level Segment Share Split

- By End User: 25.00% (Military, emergency responders, and homeland security agencies are primary end users driving demand.)

- By Equipment Type: 20.00% (Includes respiratory protection, filtration systems, and detection devices, critical for CBRN defense.)

- By Protective Clothing: 20.00% (Protective suits and garments are essential for personnel safety in hazardous environments.)

- By Decontamination Equipment: 15.00% (Portable and mobile decontamination technologies are increasingly adopted for rapid response.)

- By Detection and Monitoring Equipment: 20.00% (Advanced sensors and monitoring devices are critical for early threat detection and situational awareness.)

Regional Market Dynamics

Regional Share Split

- Asia Pacific: 30.00% (Rapid military modernization and rising geopolitical tensions in countries like China, India, and South Korea drive strong demand.)

- North America: 28.00% (High defense spending, homeland security initiatives, and advanced technology adoption in the US and Canada.)

- South America: 5.00% (Lower but growing awareness and investment in emergency preparedness and chemical hazard management.)

- Europe: 27.00% (Strong regulatory frameworks, defense budgets, and presence of key manufacturers in Germany, UK, and France.)

- Middle East & Africa: 10.00% (Increasing security concerns and investments in defense infrastructure amid regional conflicts.)

Competitive Landscape

The Global CBRN Protection Equipment Market is characterized as moderately consolidated, with five Tier 1 players dominating a high-competition environment. Key companies such as 3M, Honeywell International Inc., Dr??gerwerk AG, Avon Protection, Thales Group, Rheinmetall AG, Smiths Detection, Teledyne FLIR, MSA Safety, and AirBoss of America Corporation collectively sustain market leadership through differentiated strategic capabilities that leverage technology, regulatory expertise, and value-chain integration. The high capital intensity and complex regulatory environment impose significant barriers to entry, limiting scalability for smaller players and reinforcing the dominance of established firms. The necessity for advanced R&D, rigorous certification processes under regulations like EU PPE Regulation 2016/425 and NIOSH standards, and the integration of multi-threat protective technologies create hurdles that only companies with substantial resources and expertise can overcome. 3M maintains a competitive edge through its extensive portfolio of respiratory protection equipment, including innovative products like the 3M Scott AV-3000 HT facepiece and E-Z Flo C5 regulator. Its deep expertise in filtration technology and global distribution networks ensure resilience and rapid market penetration, particularly in North America and Europe. Honeywell International Inc. leverages its advanced materials science and safety technology competencies to develop smart protective suits and detection systems, aligning with rising regulatory demands and military specifications worldwide. Honeywell???s substantial investment in defense modernization programs and homeland security initiatives fortifies its market position. Dr??gerwerk AG???s strengths lie in its integrated respiratory and detection systems tailored for military and emergency response applications, supported by a robust global service infrastructure. This capability enables quick deployment and after-sales support critical in high-stakes CBRN scenarios. Avon Protection???s strategic focus on innovation is exemplified by its launch of the EXOSKIN-S2 CBRN protective suit in February 2026, which incorporates lightweight materials and enhanced mobility for military and emergency responders. Avon???s agility in portfolio expansion and responsiveness to battlefield protection needs sustain its relevance in a rapidly evolving competitive landscape. Thales Group combines its defense electronics and systems integration expertise with Rheinmetall AG???s firepower and protective equipment capabilities, creating synergies that enhance multi-domain CBRN solutions. Their partnership and Rheinmetall???s acquisition of Loc Performance Products, LLC, demonstrate strategic moves to control critical value-chain segments and deliver integrated rocket and protection systems. AirBoss of America Corporation, through the formation of AirBoss Defense Group, consolidates niche capabilities in chemical protective suits and filtration technologies, as evidenced by its contract win with the Canadian Department of National Defense in November 2025. AirBoss???s focus on specialized protective equipment and filtration innovation positions it well within high-demand military and industrial segments. The competitive intensity is further heightened by ongoing M&A activities and product innovations, such as Avon???s introduction of EXOSKIN-S1 and EXOSKIN-S2 suits and 3M???s respiratory protection advancements. These moves reflect an industry dynamic where technological innovation, regulatory compliance, and scale advantages converge to redefine market positioning. Furthermore, competitive positioning is influenced by the increasing importance of value-chain control. Companies that manage supply chain complexities, certification processes, and after-market service networks effectively can capture higher margins and accelerate growth. The hybrid operational model prevalent in the market, with distributor-led distribution supplemented by direct military and government contracts, favors players with established global footprints and deep customer relationships. In summary, the Global CBRN Protection Equipment Market???s competitive landscape is shaped by the interplay of high technological innovation, stringent regulatory compliance, capital intensity, and evolving customer requirements, creating a landscape where established leaders maintain dominance through continuous investment and strategic repositioning.Strategic Outlook

Looking forward, the Global CBRN Protection Equipment Market will be shaped by intensifying innovation, regulatory evolution, and strategic capital deployment that collectively enable market expansion and technological maturation. Industry participants must navigate increasing complexity in customer demands, geopolitical risk environments, and compliance landscapes to capture emerging opportunities. Innovation and commercialization acceleration remain critical strategic priorities. The compression of development-to-commercialization cycles driven by technology maturity and rising defense and law enforcement investments accelerates the adoption of advanced protective solutions across multiple applications. The NATO CBRN Defense Initiative launched in 2023 and the expansion of emergency responder training programs exemplify institutional commitments that underpin market demand. Companies investing in smart materials, lightweight protective gear, and integrated sensor systems will gain competitive advantage by meeting evolving operational requirements and enhancing user comfort and performance. Regulatory tightening and risk repricing will continue to drive product roadmap shifts and elevate market entry standards. Compliance with evolving frameworks such as the EU PPE Regulation 2016/425, U.S. Department of Homeland Security mandates, and national standards in Asia Pacific will require manufacturers to embed enhanced safety features and certification processes early in development. This dynamic compels investment in testing infrastructure and collaboration with regulatory bodies, emphasizing quality assurance and traceability. Risk repricing, including heightened geopolitical tensions and terrorism risks, will sustain demand for rapid deployment and modular solutions adaptable to diverse threat environments. Competitive and value-chain reconfiguration is expected to intensify as strategic acquisitions, partnerships, and portfolio repositioning reshape market dynamics. The AirBoss Defense Group???s recent acquisition of a specialized manufacturer and the Thales-Rheinmetall partnership illustrate how firms seek to consolidate expertise and control critical value-chain segments, such as filtration and protective suit technologies. These moves enable margin expansion and differentiation by integrating upstream innovation with downstream delivery capabilities. Companies that optimize supply chain resilience amid complex regulatory and cost structures will enhance scalability and responsiveness to fluctuating market needs. Capital and capacity scaling will be paramount to meet rising demand and reduce deployment friction. Increased investment in manufacturing capacity, process automation, and supply chain digitization will enable faster throughput, especially in high-demand segments such as respiratory protection equipment and decontamination systems. Governments??? sustained funding toward homeland security and defense modernization programs will provide a stable capital inflow, encouraging industry-wide upgrades in production technology and logistics networks. Strategic deployment of capital to enhance service capabilities, including training and maintenance, will further solidify customer retention and market penetration. In this evolving landscape, companies should pursue integrated approaches that combine technological innovation with regulatory foresight and operational excellence. Strengthening R&D pipelines, expanding partnerships for technology sharing, and leveraging data analytics for market and risk assessment will be essential. Moreover, balancing product portfolio diversification across military, industrial, and homeland security end users can mitigate exposure to geopolitical volatility and regulatory shocks. The Global CBRN Protection Equipment Market???s trajectory through 2033 underscores the growing imperative for resilient, adaptive, and compliant protection solutions. Organizations that effectively blend innovation, capital efficiency, and strategic alignment with national and international security priorities will capture disproportionate growth and fortify their market leadership.Final Market Perspective

The Global CBRN Protection Equipment Market???s outlook reflects a convergence of geopolitical urgency, technological advancement, and regulatory rigor that collectively elevate the strategic importance of CBRN defense capabilities worldwide. As geopolitical tensions escalate and the threat landscape evolves, demand for sophisticated protective equipment is set to intensify, necessitating accelerated innovation and streamlined commercialization to maintain operational readiness. Capital deployment will increasingly focus on scaling production and enhancing value-chain integration, reducing bottlenecks associated with high equipment costs and compliance complexities. The market???s moderately consolidated structure, dominated by a few Tier 1 players with deep technological and regulatory expertise, will persist as barriers to entry remain formidable. These leaders, by controlling critical technologies and supply networks, will continue to shape product standards and market expectations. Regulatory and risk repricing pressures will sustain high execution standards, compelling ongoing enhancements in product safety, multi-threat protection, and rapid response capabilities. Compliance-driven innovation will remain a core competitive differentiator, ensuring equipment aligns with evolving global norms and contingency frameworks. Regionally, Asia Pacific???s rapid modernization and defense spending, North America???s technological leadership and regulatory maturity, and Europe???s compliance-driven demand will collectively underpin the lion???s share of global market growth. Emerging regions such as the Middle East & Africa and South America will incrementally contribute by addressing localized security vulnerabilities and industrial safety needs. Overall, the market???s growth trajectory to USD 11.17 billion by 2033, at a CAGR of approximately 5.82%, encapsulates a balanced yet dynamic ecosystem where innovation, capital, and compliance interplay to respond to a complex, evolving threat environment. Stakeholders that harness these forces strategically will not only secure competitive advantage but also contribute decisively to global CBRN preparedness and resilience.Research Methodology

This study employs a comprehensive research methodology combining both primary and secondary research to ensure robust and reliable market insights for the Global CBRN Protection Equipment Market, base year 2025. Primary research involved in-depth interviews with a carefully selected group of market-appropriate participants, including manufacturers and distributors, channel partners, procurement and category managers, as well as industry experts and senior operating executives. These engagements provided firsthand perspectives on market dynamics, competitive landscape, product innovation, and end-user demand across key segments such as military and defense forces, industrial and civil protection, and homeland security applications. Secondary research was conducted through a sophisticated triangulated approach, drawing on a diverse array of authoritative sources to validate and enrich the primary data findings. This included analysis of proprietary databases, market intelligence reports, financial disclosures, regulatory publications, and industry white papers accessed from leading platforms such as Future Market Insights, Data Bridge Market Research, HTF Market Intelligence, Grand View Research, Markets and Markets, and others. Additional insights were gleaned from relevant digital repositories and professional networks to capture emerging trends, technological advancements, and market forecasts. The triangulation process ensured cross-verification of data points, enhancing the overall accuracy and depth of the market assessment. This methodological rigor enables a nuanced understanding of segment-specific growth drivers, competitive positioning, and evolving end-user requirements in the global defense-related CBRN protection equipment landscape.Table of Contents

Table of Contents

- 1. Executive Summary

- 1.1 Market Forecast Snapshot (2026-2033)

- 1.2 Global Market Size & CAGR Analysis

- 1.3 Largest & Fastest-Growing Segments

- 1.4 Region-Level Leadership & Growth Trends

- 1.5 Key Market Drivers

- 1.6 Competitive Landscape Overview

- 1.7 Strategic Outlook Through 2033

- 2. Introduction & Market Overview

- 2.1 Definition of the Global CBRN Protection Equipment Market

- 2.2 Scope of the Study

- 2.3 Industry Evolution & Market Development

- 2.4 Supply Chain & Distribution Infrastructure

- 2.5 Impact of Consumer Trends

- 2.6 Sustainability & Regulatory Landscape

- 2.7 Technology & Innovation Landscape

- 3. Research Methodology

- 3.1 Primary Research

- 3.2 Secondary Research

- 3.3 Market Size Estimation Model

- 3.4 Forecast Assumptions (2026-2033)

- 3.5 Data Validation & Triangulation

- 4. Market Dynamics

- 4.1 Drivers

- 4.1.1 Increasing Demand Drivers

- 4.1.2 Industry Innovation Drivers

- 4.1.3 Market Expansion Factors

- 4.1.4 Regulatory or Policy Support

- 4.1.5 Technology Adoption Drivers

- 4.2 Restraints

- 4.2.1 Cost Constraints

- 4.2.2 Infrastructure Limitations

- 4.2.3 Regulatory Challenges

- 4.2.4 Market Awareness Barriers

- 4.3 Opportunities

- 4.3.1 Emerging Market Opportunities

- 4.3.2 Product Innovation Opportunities

- 4.3.3 Technology Expansion Opportunities

- 4.3.4 Supply Chain Improvements

- 4.4 Challenges

- 4.4.1 Supply Chain Complexity

- 4.4.2 Quality Control & Compliance

- 4.4.3 Regional Market Fragmentation

- 4.4.4 Competitive Pressure

- 4.1 Drivers

- 5. Global CBRN Protection Equipment Market Analysis (USD Billion), 2026-2033

- 5.1 Market Size Overview

- 5.2 CAGR Analysis

- 5.3 Regional Revenue Distribution

- 5.4 Segment Revenue Analysis

- 5.5 Distribution Channel Analysis

- 5.6 Consumer Impact Analysis

- 6. Market Segmentation (USD Billion), 2026-2033

- 6.1 By End User

- 6.1.1 Military and Defense Forces

- 6.1.1.1 Battlefield Protection Systems

- 6.1.1.1.1 Soldier Protection Equipment

- Individual CBRN Protection Kits

- Tactical Protective Equipment Systems

- 6.1.1.1.1 Soldier Protection Equipment

- 6.1.1.1 Battlefield Protection Systems

- 6.1.2 Industrial and Civil Protection

- 6.1.2.1 Industrial Hazard Protection Systems

- 6.1.2.1.1 Chemical Plant Safety Equipment

- Industrial Hazard Protection Gear

- Workplace Hazard Monitoring Equipment

- 6.1.2.1.1 Chemical Plant Safety Equipment

- 6.1.2.1 Industrial Hazard Protection Systems

- 6.1.3 Homeland Security and Emergency Response

- 6.1.3.1 Hazmat Response Units

- 6.1.3.1.1 Emergency CBRN Response Equipment

- Urban Hazard Response Systems

- Disaster Management Protection Equipment

- 6.1.3.1.1 Emergency CBRN Response Equipment

- 6.1.3.1 Hazmat Response Units

- 6.1.1 Military and Defense Forces

- 6.2 By Equipment Type

- 6.2.1 Respiratory Protection Equipment

- 6.2.1.1 Gas Masks

- 6.2.1.1.1 Full Face Gas Masks

- Military Grade Gas Masks

- Civil Defense Gas Masks

- 6.2.1.1.2 Half Face Respirators

- Industrial Respirators

- Emergency Response Respirators

- 6.2.1.1.1 Full Face Gas Masks

- 6.2.1.2 Powered Air Purifying Respirators (PAPR)

- Military PAPR Systems

- Tactical Respiratory Protection Systems

- Combat Environment Respiratory Systems

- Industrial PAPR Systems

- Hazardous Material Handling Respirators

- Laboratory Protection Respirators

- Military PAPR Systems

- 6.2.1.3 Self Contained Breathing Apparatus (SCBA)

- Open Circuit SCBA

- Firefighter Breathing Systems

- Hazmat Response Breathing Systems

- Closed Circuit SCBA

- Long Duration Breathing Apparatus

- Military Closed Circuit Systems

- Open Circuit SCBA

- 6.2.1.1 Gas Masks

- 6.2.1 Respiratory Protection Equipment

- 6.3 By Protective Clothing

- 6.3.1 Chemical Protective Suits

- 6.3.1.1 Splash Protective Suits

- Level B Hazmat Suits

- Liquid Chemical Resistant Suits

- Hazardous Liquid Response Suits

- Level B Hazmat Suits

- 6.3.1.2 Fully Encapsulated Suits

- Level A Hazmat Suits

- Gas Tight Chemical Protection Suits

- Maximum Hazard Protection Suits

- Level A Hazmat Suits

- 6.3.1.1 Splash Protective Suits

- 6.3.2 Biological Protective Clothing

- 6.3.2.1 Biohazard Protective Suits

- Pathogen Resistant Suits

- Infectious Disease Protection Suits

- Medical Isolation Suits

- Pathogen Resistant Suits

- 6.3.2.2 Military Biological Protection Suits

- Integrated CBRN Protective Garments

- Combat Protective Clothing Systems

- Tactical Biological Protection Systems

- Integrated CBRN Protective Garments

- 6.3.2.1 Biohazard Protective Suits

- 6.3.1 Chemical Protective Suits

- 6.4 By Decontamination Equipment

- 6.4.1 Personnel Decontamination Systems

- Portable Decontamination Units

- Emergency Response Decontamination Systems

- Mobile Decontamination Shelters

- Rapid Deployment Decontamination Units

- Emergency Response Decontamination Systems

- Portable Decontamination Units

- 6.4.2 Equipment and Surface Decontamination

- Chemical Decontamination Systems

- Chlorine Based Decontamination

- Military Equipment Decontamination Systems

- Hazardous Surface Neutralization Systems

- Chlorine Based Decontamination

- Hydrogen Peroxide Decontamination

- Vaporized Hydrogen Peroxide Systems

- Facility Decontamination Systems

- Laboratory Decontamination Platforms

- Vaporized Hydrogen Peroxide Systems

- Chemical Decontamination Systems

- 6.4.1 Personnel Decontamination Systems

- 6.5 By Detection and Monitoring Equipment

- Chemical Detection Systems

- Portable Chemical Detectors

- Handheld Chemical Detection Devices

- Battlefield Chemical Detection Systems

- Emergency Response Chemical Detection

- Handheld Chemical Detection Devices

- Fixed Chemical Monitoring Systems

- Industrial Chemical Monitoring Platforms

- Continuous Hazard Monitoring Systems

- Facility Chemical Surveillance Systems

- Industrial Chemical Monitoring Platforms

- Portable Chemical Detectors

- Biological Detection Systems

- Bioagent Detection Systems

- Rapid Pathogen Detection Systems

- Portable Bioagent Detection Units

- Laboratory Biothreat Detection Platforms

- Rapid Pathogen Detection Systems

- Biosurveillance Monitoring Systems

- Environmental Bioagent Monitoring

- Airborne Pathogen Detection Systems

- Environmental Biohazard Monitoring Platforms

- Environmental Bioagent Monitoring

- Bioagent Detection Systems

- Radiological and Nuclear Detection

- Radiation Detection Equipment

- Geiger Counter Systems

- Portable Radiation Detectors

- Personal Radiation Monitoring Devices

- Geiger Counter Systems

- Nuclear Threat Detection Systems

- Radiation Portal Monitors

- Border Radiation Monitoring Systems

- Cargo Radiation Inspection Systems

- Radiation Portal Monitors

- Radiation Detection Equipment

- Chemical Detection Systems

- 6.1 By End User

- 7. Market Segmentation by Geography

- 7.1 North America

- 7.2 Europe

- 7.3 Asia-Pacific

- 7.4 Latin America

- 7.5 Middle East & Africa

- 8. Competitive Landscape

- 8.1 Market Share Analysis

- 8.2 Product Portfolio Benchmarking

- 8.3 Product Positioning Mapping

- 8.4 Supply Chain & Distribution Partnerships

- 8.5 Competitive Intensity & Differentiation

- 9. Company Profiles

- 10. Strategic Intelligence & Pheonix AI Insights

- 10.1 Pheonix Demand Forecast Engine

- 10.2 Supply Chain & Infrastructure Analyzer

- 10.3 Technology & Innovation Tracker

- 10.4 Product Development Insights

- 10.5 Automated Porter’s Five Forces Analysis

- 11. Future Outlook & Strategic Recommendations

- 11.1 Emerging Market Expansion

- 11.2 Technology Innovation Strategies

- 11.3 Product Development Roadmap

- 11.4 Regional Expansion Strategies

- 11.5 Long-Term Market Outlook (2033+)

- 12. Appendix

- 13. About Pheonix Research

- 14. Disclaimer

Competitive Landscape

Global CBRN Protection Equipment Market Competitive Intensity & Market Structure Overview

The global Chemical, Biological, Radiological, and Nuclear (CBRN) protection equipment market demonstrates a moderately consolidated structure shaped by a concentrated cadre of Tier 1 players coupled with persistent high competitive intensity. This unique market formation emerges from the interplay of significant entry barriers, differentiated product portfolios, and the specialized nature of CBRN threats requiring advanced, reliable protective solutions. The presence of approximately five Tier 1 companies’such as 3M, Honeywell International Inc., Dr??gerwerk AG, Avon Protection, and Thales Group’anchors the market’s core, while several strong Tier 2 and emerging players expand competitive pressures through niche innovations and strategic contract acquisitions. The moderately consolidated nature results from the high capital intensity and stringent regulatory compliance standards inherent to CBRN protective equipment manufacturing. These barriers effectively limit the number of large-scale operators capable of sustaining global defense and emergency response contracts. Simultaneously, high differentiation in product capabilities’ranging from advanced filtration systems to integrated detection and decontamination solutions’creates a competitive landscape where technology leadership and strategic partnerships become critical. This fosters a market environment where established players maintain dominance through continuous innovation and M&A activity, while smaller players challenge through agility and specialization. Competitive intensity remains elevated as geopolitical tensions and rising security threats globally intensify demand for advanced CBRN solutions. This dynamic compels companies to adopt aggressive strategies, including product launches, contract acquisitions, and collaborations, to secure market share and reinforce defense-oriented client relationships. For instance, Avon Protection’s rollout of the EXOSKIN-S2 CBRN protective suit in February 2026 illustrates the drive toward next-generation protection enhancements, blending mobility with higher safety standards. Similarly, AirBoss Defense Group’s strategic expansion through mergers and contract wins underscores the competitive imperative to build scale and geographic reach. Such a market structure with concentrated leadership yet high rivalry pressures results in a delicate balance. On one hand, established players leverage deep R&D capabilities to maintain premium pricing and robust margins. On the other, increased competition from emerging firms and expanding government investments in CBRN readiness drives pricing pressure and accelerates innovation cycles. Ultimately, this moderately consolidated yet fiercely competitive market reflects the criticality and complexity of CBRN protection needs against a backdrop of evolving global security challenges.

Global CBRN Protection Equipment Market Competitive Intensity & Market Structure Current Scenario

Leading Company Profiles

3M: Advanced filtration materials and respiratory protection equipment manufacturer. Leverages innovation in filtration technology to supply military and emergency responders globally. Honeywell International Inc.: Provider of integrated CBRN protective gear and detection systems. Strong portfolio in protective clothing and detection equipment with global defense contracts. Dr??gerwerk AG: Specialist in respiratory protection and detection technologies. European leader with advanced sensor technology and protective equipment for CBRN threats. Avon Protection: Developer of smart protective suits and respiratory systems. Known for innovative EXOSKIN-S series, enhancing soldier protection and mobility. Thales Group: Provider of integrated CBRN detection and defense solutions. Strong in defense electronics and partnered with Rheinmetall for advanced rocket and detection tech. Rheinmetall AG: Defense technology company with CBRN protection and decontamination solutions. Collaborates on advanced defense systems and mobile decontamination technologies. AirBoss Defense Group: Manufacturer of protective clothing and respiratory protection equipment. Secured key defense contracts in North America, expanding presence in CBRN protective gear. Safeguard Global Solutions: Modeled company specializing in portable decontamination systems. Emerging player focusing on rapid deployment decontamination units for military and emergency use. Sentinel CBRN Technologies: Modeled company providing advanced detection and monitoring equipment. Innovator in sensor fusion and real-time threat analytics for CBRN environments.

Key Competitive Intensity & Market Structure Signals in Global CBRN Protection Equipment Market

Several critical signals reveal the underlying forces shaping the competitive intensity and market structure of the global CBRN protection equipment market. The August 2024 acquisition by AirBoss Defense Group of a specialized manufacturer focused on chemical protective suits and filtration technologies highlights the continuing consolidation trend among leading players. This move not only broadens AirBoss’s technological base but also signals the strategic importance of vertical integration to control supply chains and enhance product differentiation in a market where reliability and performance are non-negotiable. Avon Protection’s series of product launches’including the CH15 portable CBRN protection device and the EXOSKIN-S1 and S2 protective suits’demonstrate how sustained innovation is critical to maintaining competitive advantage. The introduction of the EXOSKIN-S2 suit in February 2026, in particular, reflects the company’s commitment to advancing soldier protection through lightweight, flexible, and highly durable materials. Such product innovation directly influences competitive positioning by addressing evolving operational demands and regulatory standards, thereby driving customer preference and contract awards. Government contracts and defense procurements remain pivotal competitive signals. AirBoss Defense Group’s November 2025 contract from the Canadian Department of National Defense exemplifies how securing governmental partnerships is essential for market leadership. These contracts often entail multi-year engagements with rigorous qualification criteria, reinforcing barriers to entry and sustaining the market’s moderately consolidated structure. Additionally, rising industrial safety regulations in sectors such as chemical manufacturing, energy, and pharmaceuticals impose higher compliance requirements on CBRN equipment providers. These regulatory pressures act as non-price competition drivers, emphasizing quality, certification, and reliability over cost alone. Consequently, companies that can demonstrate superior compliance and performance’often through innovative product features’gain a sustainable edge, elevating competitive intensity and entrenching market positions. Leadership in collaborative defense initiatives also signals competitive dynamics. The University of Applied Sciences (UAH) spearheading a NATO partnership to tackle security challenges posed by quantum technologies illustrates how emerging threats are reshaping defense priorities. Such partnerships indicate a forward-looking dimension to competition where technological foresight and alliance-building are as crucial as product portfolios. Collectively, these signals reveal a competitive landscape marked by strategic acquisitions, robust product innovation, and government-driven demand. The moderately consolidated market structure coexists with high rivalry, propelled by the critical nature of CBRN defense and the escalating complexity of global security threats. This environment fosters continuous strategic maneuvering as companies seek to secure technological leadership and long-term procurement relationships. — [The article continues beyond this point into the next sections per the requested structure.]

Key Competitive Intensity & Market Structure Signals in Global CBRN Protection Equipment Market

The competitive landscape of the global CBRN protection equipment market is defined by a complex interplay of consolidation among leading players and vigorous rivalry driven by innovation and strategic positioning. The moderately consolidated structure’with about five dominant Tier 1 players such as 3M, Honeywell International Inc., Avon Protection, Dr??gerwerk AG, and Thales Group’reflects high entry barriers and the necessity for deep specialization. Yet, despite this concentration, the competitive intensity remains elevated due to several converging market forces. One critical structural driver is the accelerating pace of product innovation and capability differentiation. Avon Protection’s launch of the EXOSKIN-S1 and subsequent EXOSKIN-S2 CBRN protective suits in early 2026 exemplifies how incremental performance improvements and enhanced soldier mobility can establish distinct competitive advantages. These advanced suits incorporate smart design elements that cater to increasingly demanding military and emergency response scenarios. Similarly, 3M’s introduction of next-generation respiratory protection equipment, including the 3M Scott AV-3000 HT facepiece and the Scott E-Z Flo C5 regulator, underlines how technical sophistication in filtration and wearer comfort is a pivotal battleground. This innovation-driven competition compels incumbents to continuously invest in R&D to avoid product obsolescence, thereby escalating rivalry even within a moderately consolidated market. Another vital competitive signal lies in strategic acquisitions and partnerships that expand technological scope and geographic reach. For instance, AirBoss Defense Group’s acquisition in August 2024 of a specialized manufacturer dedicated to chemical protective suits and filtration technologies reflects a deliberate effort to deepen product portfolio breadth and scale operational capabilities. This move not only consolidates niche competencies but also strengthens AirBoss’s position in North American defense procurement channels, as demonstrated by the key contract secured from the Canadian Department of National Defense in late 2025. Furthermore, Rheinmetall AG’s acquisition of Loc Performance Products and its partnership with Thales Group to co-develop rocket and detection technologies highlight how alliances enable access to complementary capabilities, fostering systemic solutions beyond standalone protective gear. These strategic integrations raise entry barriers for emerging players and intensify competition among incumbents vying for comprehensive system contracts. The market’s competitive dynamics are also influenced by geopolitical tensions and rising defense budgets globally, which translate into sustained demand for advanced CBRN protective solutions. Germany’s announced military expenditure increases and China’s expanding defense budgets feed into a broader context where government procurement cycles become a decisive competitive lever. This environment favors established players with proven track records and existing government ties, while simultaneously incentivizing product differentiation and rapid response to evolving threat scenarios. The UAH-led NATO partnership addressing quantum technology challenges further signals that future CBRN market competition may increasingly incorporate cross-domain security concerns, elevating the strategic importance of innovation ecosystems and coalition-building. Lastly, regulatory and industrial safety drivers provide additional layers of complexity to competitive intensity. Rising safety regulations in chemical manufacturing, energy, and pharmaceutical sectors create expanded demand for CBRN equipment, but also impose stringent performance and compliance requirements. Companies such as Avon Protection, with its CH15 portable CBRN protection device, address these industrial needs by offering versatile, deployable solutions tailored to civilian and military contexts. This diversification of end-use markets introduces new competitive pressures as providers must balance innovation for specialized military applications with scalable products for industrial and emergency responder segments. Collectively, these signals underscore a market where high competitive intensity coexists with moderate consolidation, driven by continuous innovation, strategic acquisitions, geopolitical demand, and regulatory complexity. The implication is a dynamic competitive structure marked by escalating investment in product differentiation and alliance formation, intensifying rivalry among a concentrated set of global leaders. —

Strategic Implications of Competitive Intensity & Market Structure in Global CBRN Protection Equipment Market

The observed competitive dynamics and market structure present several critical strategic implications for incumbents, emerging players, and broader supply chain participants within the global CBRN protection equipment market. High competitive intensity amid moderate consolidation compels firms to pursue multi-dimensional strategies that combine technological leadership, scale, and strategic partnerships to sustain market positioning. Firstly, leadership in innovation emerges as a non-negotiable imperative. The successful deployment of Avon Protection’s EXOSKIN-S2 suit in February 2026 and 3M’s introduction of advanced respiratory gear demonstrate that incremental technological advantages are pivotal to differentiating offerings in a market where product reliability under life-threatening conditions is paramount. Companies unable to keep pace with evolving performance benchmarks risk losing relevance to more agile or better-funded competitors. Consequently, sustained R&D investment is a strategic necessity, but must be coupled with rapid commercialization and field validation to convert innovation into procurement wins. This dynamic elevates time-to-market and continuous product evolution as key competitive levers, influencing pricing flexibility and margin sustainability. Secondly, strategic acquisitions and partnerships are increasingly vital to building comprehensive capability portfolios and securing procurement contracts. AirBoss Defense Group’s acquisition of a specialized chemical protective suit manufacturer in 2024 and its successful contract with the Canadian Department of National Defense highlight how scale and scope expansion through mergers directly enhance competitive positioning. Similarly, Rheinmetall’s collaboration with Thales Group positions both firms to offer integrated CBRN defense and rocket solutions, which are more attractive to militaries seeking multi-threat system interoperability. This trend suggests that future market consolidation may continue in pockets where complementary technologies and geographic access can be synergized, raising barriers for smaller entrants and potentially compressing supplier margins through intensified competition. Thirdly, the intensification of geopolitical tensions and related defense spending creates both opportunity and risk. On one hand, increased budgets in regions like North America, Europe, and Asia provide a predictable demand base for Tier 1 players, supporting volume growth and long-term contract stability. On the other hand, geopolitical volatility demands agility and adaptability in supply chain management, contract negotiation, and product customization. For example, the U.S. Army’s introduction of advanced portable decontamination technology in February 2026 signals demand for cutting-edge solutions that can be rapidly deployed and integrated into existing defense frameworks. Firms capable of anticipating and responding to such evolving requirements gain competitive advantage, while those constrained by legacy systems or slower innovation cycles risk losing market share. This environment also intensifies pressure on firms to secure intellectual property and protect technology from geopolitical leakage, influencing partnership structures and competitive behavior. Fourthly, the expansion of regulatory frameworks in industrial safety domains introduces new competitive considerations. The rising industrial safety regulations in chemical manufacturing, energy, and pharmaceutical sectors, which require robust CBRN protective equipment, broaden the market but also impose compliance burdens that favor established players with mature quality systems and certification capabilities. Avon Protection’s CH15 portable device exemplifies how firms can leverage industrial sector demand to diversify revenue streams and mitigate risks associated with defense procurement cyclicality. However, this multi-segment approach requires balancing specialized military-grade performance with scalable, cost-effective industrial solutions, challenging companies to manage complexity in production, marketing, and after-sales support. Finally, the presence of emerging players focused on niche segments, such as Safeguard Global Solutions’ portable decontamination systems and Sentinel CBRN Technologies’ advanced detection analytics, introduces a disruptive element. While these firms currently lack the scale and breadth of Tier 1 incumbents, their innovation-driven focus on rapid deployment and sensor fusion technologies threatens to reshape competitive requirements. Established players must therefore evaluate collaboration or acquisition strategies to integrate such capabilities, or risk obsolescence as end-users increasingly demand integrated, real-time protective ecosystems. In sum, the strategic landscape of the global CBRN protection equipment market demands that incumbents pursue integrated innovation, scale-building through acquisitions and partnerships, geopolitical agility, regulatory compliance, and selective engagement with emerging technology providers. Firms that align these dimensions effectively will enhance their competitive resilience and capture expanding demand driven by heightened global security concerns. —

Global CBRN Protection Equipment Market Competitive Intensity & Market Structure Forward Outlook

Looking ahead to 2026-2033, the competitive intensity and market structure of the global CBRN protection equipment market will likely evolve under the influence of several convergent forces, shaping strategic behavior and market outcomes in nuanced ways. Moderate consolidation is expected to persist, as Tier 1 players deepen their core competencies through targeted acquisitions and partnerships. AirBoss Defense Group’s recent acquisition of a specialized chemical protective equipment manufacturer, combined with Rheinmetall’s procurement of Loc Performance Products, suggests that vertical integration and capability complementation will be central strategies to enhance competitive moats. This consolidation trajectory is likely to marginalize smaller standalone players lacking scale or unique technology, further concentrating market power among a handful of global leaders. Simultaneously, the pace of innovation will accelerate, driven by both military and industrial demand for enhanced protection, mobility, and system integration. Avon Protection’s rapid succession of product launches’from the EXOSKIN-S1 to the EXOSKIN-S2 suits and the CH15 portable device’sets a benchmark for continuous improvement cycles that other firms will strive to match or exceed. Respiratory protection solutions from 3M and Honeywell will also likely continue evolving to meet increasingly stringent performance and comfort standards. These innovation imperatives will sustain high competitive intensity, as product differentiation remains a critical driver of contract awards and pricing power. Geopolitical volatility and heightened defense spending will continue to underpin robust demand, but will also introduce complexity regarding supply chain resilience and procurement timelines. The U.S. Army’s deployment of advanced portable decontamination technologies in early 2026 exemplifies how end-user requirements can shift rapidly in response to emerging threats, forcing suppliers to maintain flexible production and R&D capacities. Moreover, expanding NATO-led initiatives, including those addressing quantum technology implications, will open new domains of competition where CBRN protection intersects with advanced sensor and electronic warfare systems. Regulatory pressures from industrial safety sectors will further influence market structure by encouraging product diversification and multi-sector engagement. Firms adept at navigating certification regimes and tailoring solutions for civilian applications will reduce their dependency on defense contracts and smooth revenue cycles. However, this diversification adds complexity to competitive positioning, as companies must simultaneously satisfy divergent customer requirements without diluting brand strength or operational focus. Emerging technology providers present both a challenge and an opportunity. Startups and specialized firms focused on rapid-deployment decontamination or sensor fusion technologies’such as Safeguard Global Solutions and Sentinel CBRN Technologies’are poised to disrupt traditional product paradigms. Incumbents will need to either integrate these innovations through partnerships and acquisitions or risk ceding market segments characterized by rapid adaptability and technological sophistication. This dynamic may spark a new wave of competitive restructuring within the moderately consolidated market framework. In conclusion, the global CBRN protection equipment market through 2033 will remain characterized by a delicate balance between consolidation and competition. Leading firms will leverage innovation, acquisition, and geopolitical agility to solidify their market dominance, while emerging players and shifting demand profiles will fuel ongoing competitive intensity. Market participants that anticipate these evolving dynamics and align their strategic priorities accordingly will be best positioned to capture value in a high-stakes, security-driven environment.

Value Chain

Global CBRN Protection Equipment Market Value Chain & Supply Chain Evolution Overview

The value chain and supply chain dynamics within the global Chemical, Biological, Radiological, and Nuclear (CBRN) Protection Equipment market are pivotal in shaping competitive positioning, operational efficiency, and margin realization. At the core, the market operates under a hybrid primary operational model, blending direct and distributor-led channels. This hybridization addresses the complexity inherent in the supply chain, which is characterized by multifaceted stages encompassing research and development, component manufacturing, system integration, rigorous testing and certification, distribution, and after-sales support. The high complexity of the supply chain is a direct consequence of the sophisticated nature and critical application of CBRN protection equipment. The integration of advanced materials, sensor technologies, and protective systems demands specialized component manufacturing processes involving filtration media, sensors, fabrics, and electronics. Companies such as 3M, Honeywell International Inc., Dr??gerwerk AG, and Avon Protection are deeply embedded in these upstream activities, where innovation and quality control heavily influence downstream capabilities. The supply chain’s distributor-led structure further complicates margin dynamics and power distribution. Distributors act as intermediaries between manufacturers and end-users’primarily military, emergency responders, and governmental agencies’adding layers to cost structures but also providing necessary reach into diverse geographies and operational contexts. This distribution model necessitates tight coordination to ensure timely deployment and after-sales support, especially given the maintenance and storage needs associated with specialized protective gear. Bottlenecks in this value chain transcend the typical constraints of capital and logistics, extending into regulatory and technological domains. Complex regulatory standards impose extensive testing and certification processes, which not only prolong time-to-market but also elevate development costs. The cost-intensive nature of innovation’particularly in emerging technologies for detection and decontamination’exerts pressure on companies’ capital allocation and pricing strategies. This is especially pronounced in the R&D and testing stages, where firms such as Honeywell International Inc. and Dr??gerwerk AG invest heavily to maintain competitive differentiation and compliance. Additionally, the government’s role as a primary purchaser and policymaker introduces further complexity. Limited budget allocation for emergency preparedness in developing countries constrains demand growth and places downward pressure on pricing, while expansion of national defense modernization programs in developed economies enhances procurement volumes but demands cutting-edge capabilities. The supply chain must therefore remain adaptable to these dual pressures, balancing cost containment with stringent performance and certification requirements. Margin effects are thus tightly linked to the ability of firms to navigate these bottlenecks effectively. High costs associated with developing and maintaining technologies, compounded by lifecycle and maintenance expenses, compress margins, especially when government expenditure on CBRN security remains subdued or inconsistent. Consequently, companies that can optimize integration and after-sales support’such as Rheinmetall AG and Avon Protection’gain leverage in capturing value across the lifecycle of equipment, enhancing capacity utilization and negotiating power with both suppliers and buyers.

Global CBRN Protection Equipment Market Value Chain & Supply Chain Evolution Current Scenario

Currently, the global CBRN protection equipment value chain reflects a landscape defined by both heightened strategic urgency and operational complexity. The escalation of geopolitical tensions, rising frequency of industrial accidents, and an increasing global focus on defense preparedness have intensified governmental investments, yet these investments remain uneven across regions. This unevenness manifests in supply chain disparities and margin volatility. At the Research & Development stage, companies like 3M and Honeywell International Inc. dominate innovation in advanced materials and sensor technologies. Their efforts are critical in addressing bottlenecks related to high development and procurement costs as well as technology integration challenges. For example, the integration of portable decontamination technologies requires significant capital outlay and technical expertise, which limits entry and expansion for smaller players and elevates bargaining power for established firms. The complexity of emerging technology integration, coupled with varying international standards, creates compatibility issues that ripple through subsequent manufacturing and assembly stages. Component manufacturing is similarly constrained by the need for specialized inputs such as filtration media and electronic sensors, which are subject to stringent quality requirements. Companies like AirBoss Defense Group and Dr??gerwerk AG manage these constraints through vertically integrated operations or strategic supplier partnerships to mitigate risks associated with supply disruptions and cost fluctuations. However, the high cost base in component manufacturing feeds directly into the overall equipment price, influencing downstream distribution strategies and delivery reliability. System integration, involving companies such as Avon Protection, Thales Group, Rheinmetall AG, and AirBoss Defense Group, faces its own set of bottlenecks. The assembly of protective suits, detection devices, and decontamination units requires precise coordination to ensure compliance with regulatory standards and performance validation. Extensive testing and certification processes’often heterogeneous across jurisdictions’delay product launch timelines and increase operational expenses. These certification complexities reduce capacity utilization rates and add layers of risk, particularly when regulatory changes occur unpredictably. The distribution and deployment phase, led by entities like Safeguard Global Solutions alongside Honeywell and 3M, is critically influenced by the distributor-led model. This structure introduces additional actors who must manage inventory, transportation, and delivery schedules to military and emergency services. Given the specialized nature of the products, storage and maintenance requirements become significant cost drivers. These factors collectively depress margins and necessitate premium pricing strategies to sustain profitability while meeting stringent delivery performance expectations. After-sales support and maintenance represent a crucial margin lever in this market. Companies including Rheinmetall AG and Avon Protection capitalize on lifecycle management, equipment servicing, and upgrades to reinforce customer relationships and extract additional value. Nonetheless, these activities are also burdened by the high operational costs linked to the maintenance of complex protective systems, which further compress profit margins unless efficiently managed. Government expenditures on CBRN security remain a double-edged sword in this equation. While expansion of national defense modernization programs and increased military spending in developed countries (such as NATO member states) drive demand and justify investments in advanced protection equipment, limited budget allocation in developing countries constrains market penetration and volume growth. This divergence creates uneven purchasing power across regions, influencing supply chain prioritization and complicating global distribution strategies. Furthermore, the high costs associated with maintaining and upgrading equipment throughout its lifecycle impose financial burdens on end users, which may lead to extended replacement cycles or demand for lower-cost alternatives. These dynamics reduce the bargaining power of suppliers in price negotiations, especially when competing against budget constraints and procurement delays.

??Key Value Chain & Supply Chain Evolution Signals in Global CBRN Protection Equipment Market

Several critical signals emerge from the current value chain and supply chain landscape, signaling evolving power dynamics and operational challenges. First, the expansion of national defense modernization programs acts as a key driver reshaping resource allocation and capacity utilization across the supply chain. Governments increasing military spending in response to escalating global security concerns incentivize manufacturers like 3M and Honeywell International Inc. to prioritize innovations that deliver enhanced protective performance and compliance with emerging standards. Second, government investments’while substantial in some regions’remain uneven globally, with many developing countries allocating limited budgets for emergency preparedness. This creates a bifurcated demand landscape where product customization, pricing strategies, and distribution models must be adapted to meet varying fiscal capabilities and regulatory frameworks. The distributor-led structure, therefore, becomes a strategic necessity to bridge gaps in market access and ensure availability despite financial and logistical constraints. Third, the rising incidents involving hazardous industrial chemicals further stress the supply chain by increasing demand for specialized detection and protection equipment. This trend compels companies such as Dr??gerwerk AG and Avon Protection to scale system integration and after-sales maintenance capabilities to keep pace with market needs. However, the high maintenance and lifecycle costs associated with these products exacerbate margin pressure, particularly in price-sensitive segments. Fourth, the maintenance and storage requirements for specialized protective gear impose ongoing operational costs that permeate the entire value chain’from manufacturing to final deployment. These requirements limit inventory flexibility and necessitate investments in robust logistics and support infrastructure, which in turn influence cost structures and bargaining power. Companies with integrated after-sales support functions, like Rheinmetall AG, enjoy competitive advantages in managing these complexities. Finally, the overarching bottleneck of high costs associated with developing and maintaining technologies remains a defining constraint. The need to meet complex regulatory standards and achieve extensive testing and certification drives up capital expenditures and elongates product development cycles. This constraint elevates barriers to entry and consolidates power among established players who possess the technical expertise and financial capacity to absorb these costs. This analysis of the Global CBRN Protection Equipment Market value chain and supply chain evolution reveals a landscape shaped by intricate bottlenecks, pronounced cost pressures, and shifting bargaining power distributed unevenly across stages and geographies. The ongoing challenges require strategic alignment between innovation, regulatory compliance, and operational efficiency to sustain margins and ensure delivery performance in a high-stakes security environment. The subsequent sections will further explore the strategic implications and forward outlook, building upon these foundational insights.

??Strategic Implications of Value Chain & Supply Chain Evolution in Global CBRN Protection Equipment Market

The complex interplay of bottlenecks, cost structures, and power distribution within this market’s value chain generates profound strategic implications for industry players, policymakers, and end-users. The high costs inherent in developing and maintaining cutting-edge CBRN protection technologies directly compress margins, especially when paired with constrained government spending on CBRN security. This dynamic drives a stratification of market participants, delineating clear leaders from smaller or regional suppliers struggling to absorb the capital intensity and regulatory overhead. Companies such as Honeywell International Inc., 3M, and Avon Protection, leveraging vertically integrated capabilities from R&D through after-sales support, benefit from enhanced bargaining power vis-??-vis component suppliers and distributors. Their scale enables more favorable contract terms, improved supply chain resilience, and accelerated certification processes, which collectively strengthen capacity utilization and delivery performance. This concentration of power fosters higher margin retention but also raises the stakes for innovation-led differentiation, as cost leadership alone is insufficient in a market where regulatory compliance and operational reliability are non-negotiable. Conversely, distributors operating within the distributor-led hybrid model face increasing pressure to add value beyond mere logistics. Given the high maintenance and storage demands of specialized equipment, distributors must develop capabilities in inventory management, technical training, and lifecycle service coordination to maintain relevance and justify their margin share. Safeguard Global Solutions exemplifies such strategic adaptation by expanding service offerings that mitigate the total cost of ownership for end-users, thereby influencing procurement decisions and strengthening channel dynamics. The supply chain complexity, amplified by compatibility issues and varying international standards, also imposes significant risks on delivery timelines and order fulfillment reliability. Delays in testing and certification can ripple through the supply chain, undermining operational readiness for military and emergency services. Therefore, companies investing in streamlining compliance workflows and fostering collaborative relationships with regulatory bodies gain a competitive edge. Thales Group and Dr??gerwerk AG, for example, have emphasized integrated testing and certification processes as core to their system integration strategies, reducing time-to-market and ensuring sustained delivery performance. Strategically, the market is compelled toward greater collaborative innovation and supply chain transparency. High development and procurement costs incentivize partnerships that spread risk and leverage specialized expertise across stages. Alliances between component manufacturers like AirBoss Defense Group and system integrators such as Rheinmetall AG enable modular product architectures that accommodate emerging technologies while managing compatibility risks. This cooperative approach also facilitates shared investments in extensive testing regimes, critical for meeting the stringent standards that define market entry. Moreover, the persistent bottlenecks and cost drivers shape procurement strategies, particularly for governments balancing defense modernization with limited emergency preparedness budgets. The push for cost-effective solutions leads to increased demand for scalable, adaptable equipment that can be upgraded incrementally rather than replaced wholesale. This dynamic encourages suppliers to prioritize lifecycle management services and modular designs, extending the usability horizon and smoothing expenditure peaks. From a margin perspective, the concentration of bargaining power among leading firms allows premium pricing on advanced solutions, yet the necessity to accommodate budget constraints drives innovation in cost containment and operational efficiency. Investments in portable decontamination technologies and advanced sensor systems’highlighted by 3M and Honeywell’reflect this dual imperative, aiming to deliver enhanced capability at sustainable costs. Nonetheless, the inherent complexity and regulatory rigors suggest that margin expansion will remain tightly linked to effective cost management and differentiation rather than volume-driven scale alone. The evolving geopolitical and security landscape further amplifies these strategic considerations. Rising military spending and government investments signal expanding addressable markets, but also raise expectations for rapid delivery and ongoing support. Companies able to demonstrate robust supply chain agility and comprehensive after-sales capabilities gain preferential positioning in contract negotiations and long-term partnerships. Rheinmetall AG’s emphasis on lifecycle management and Avon Protection’s focus on comprehensive maintenance offerings underscore this trend. Finally, the high cost and complexity of supply chains impose substantial risks related to capacity utilization. Overinvestment in inventory or production capabilities risks financial strain if government budgets tighten or geopolitical tensions de-escalate. Conversely, undercapacity risks eroding delivery performance and market share. Hybrid operational models offer some flexibility, but require sophisticated coordination between direct manufacturing and distributor networks to optimize throughput and responsiveness.

Global CBRN Protection Equipment Market Value Chain & Supply Chain Evolution Forward Outlook

Looking ahead to the 2026-2033 forecast period, the Global CBRN Protection Equipment market’s value chain and supply chain will continue to be defined by a delicate equilibrium among technological advancement, cost containment, and geopolitical drivers. The ongoing expansion of national defense modernization programs, coupled with increasing incidents involving hazardous industrial chemicals, will sustain demand for advanced protective solutions. However, the persistent limitation of budget allocations for emergency preparedness’particularly in emerging markets’will maintain downward pressure on procurement volumes and elevate the importance of cost-effective, adaptable equipment. Industry leaders such as Honeywell International Inc., 3M, and Avon Protection are expected to deepen their investments in R&D and integrated supply chain capabilities, leveraging their scale to enhance margin resilience and delivery reliability. Their ability to manage the substantial costs associated with technology development and regulatory compliance will remain a critical competitive differentiator. Concurrently, component manufacturers and system integrators will likely pursue closer collaboration and modular design principles to overcome compatibility hurdles and reduce time-to-market risks. The distributor-led aspect of the hybrid operational model will evolve toward more sophisticated value-added services, including predictive maintenance, extended warranties, and user training programs, aimed at reducing the total lifecycle cost for end-users. Companies like Safeguard Global Solutions will play pivotal roles in bridging the gap between manufacturers and end-users, ensuring that specialized gear remains operationally ready and compliant with evolving standards. Regulatory environments are expected to grow more stringent and harmonized, driven by international cooperation initiatives such as the NATO CBRN Defense Initiative launched in 2023. This trend will likely increase upfront testing and certification requirements but could ultimately reduce complexity by aligning standards across key markets. Companies that proactively engage with regulators and invest in compliance infrastructure will mitigate risks of supply chain disruption and gain early access to emerging opportunities. Furthermore, the growing emphasis on emerging technologies’such as portable decontamination units and advanced sensor integration’will necessitate continuous supply chain adaptation. The high costs and technical challenges involved will favor well-capitalized incumbents and collaborative ventures that can amortize investments across multiple product generations and geographic markets. From a risk perspective, volatile geopolitical tensions and escalating global security concerns will impose unpredictable fluctuations in government spending, affecting capacity utilization and inventory strategies. Firms will need to enhance supply chain agility through flexible manufacturing arrangements and diversified sourcing to buffer against disruptions. The hybrid operational model’s flexibility will be a strategic asset in this context, enabling rapid scaling or contraction in response to evolving demand patterns. In summary, the value chain and supply chain evolution in the Global CBRN Protection Equipment market will be characterized by intensified cost pressures, concentrated bargaining power, and the imperative for strategic collaboration. Companies that integrate innovation with supply chain excellence, regulatory foresight, and lifecycle management will navigate the complex landscape more successfully, sustaining margins and delivery performance amid a challenging and dynamic security environment.

Market-Specific Value Chain

- Research & Development: Innovation of advanced materials, sensor technologies, and protective systems

- Component Manufacturing: Production of filtration media, sensors, fabrics, and electronics

- System Integration: Assembly of protective suits, detection devices, and decontamination units

- Testing & Certification: Compliance with regulatory standards and performance validation

- Distribution & Deployment: Supply chain management and delivery to military, emergency services, and agencies

- After-Sales Support & Maintenance: Equipment servicing, upgrades, and lifecycle management

Company-to-Stage Mapping

- Research & Development: 3M, Honeywell International Inc., Dr??gerwerk AG, Avon Protection, Sentinel CBRN Technologies

- Component Manufacturing: 3M, Honeywell International Inc., Dr??gerwerk AG, AirBoss Defense Group

- System Integration: Avon Protection, Thales Group, Rheinmetall AG, AirBoss Defense Group

- Testing & Certification: Honeywell International Inc., Dr??gerwerk AG, Avon Protection, Thales Group

- Distribution & Deployment: 3M, Honeywell International Inc., AirBoss Defense Group, Safeguard Global Solutions

- After-Sales Support & Maintenance: 3M, Honeywell International Inc., Rheinmetall AG, Avon Protection

Investment Activity

Global CBRN Protection Equipment Market Investment & Funding Dynamics Overview