Global Targeting Pods Market Size and Share Analysis 2026-2033

Global Targeting Pods Market Size & Forecast

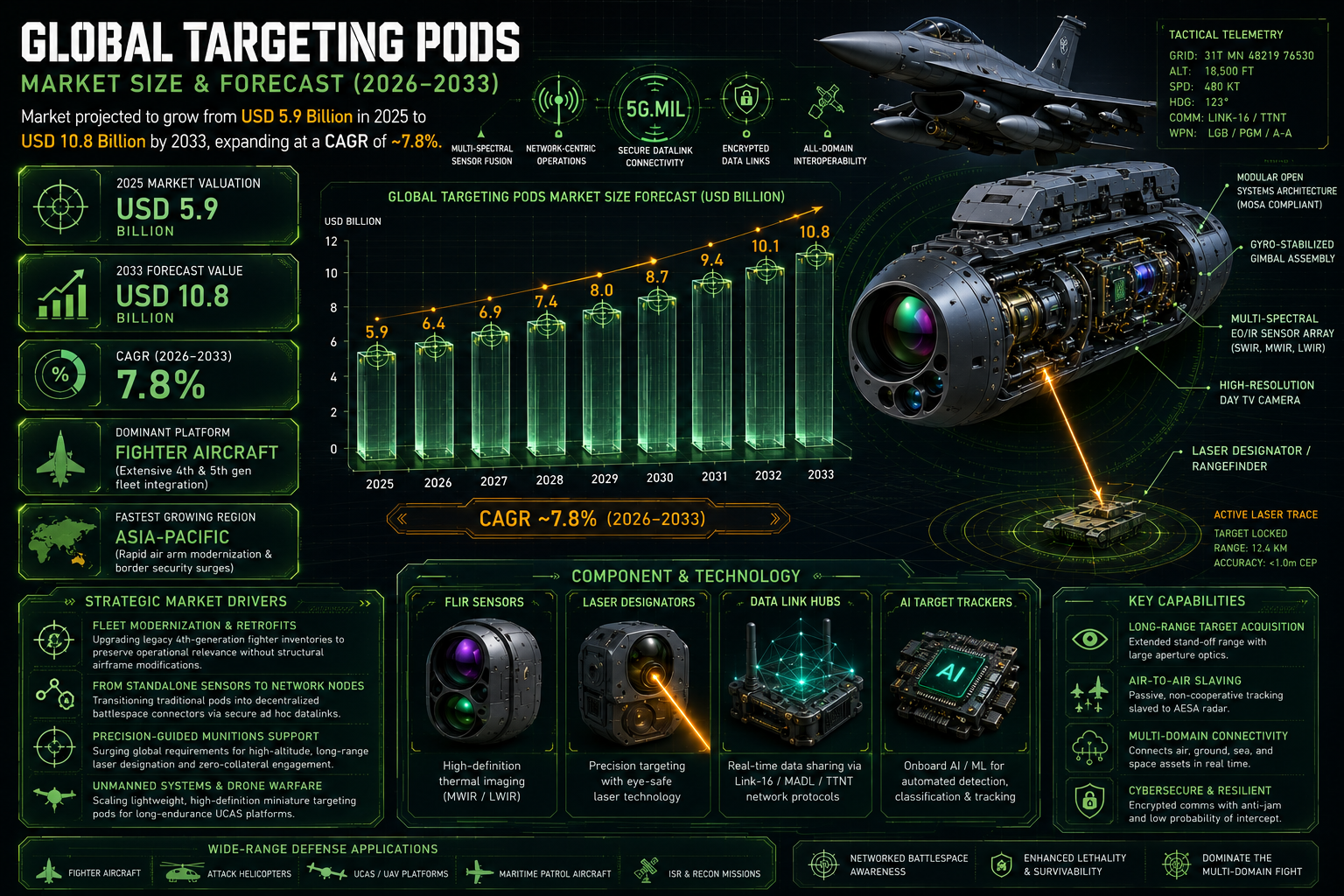

The global targeting pods market is projected to witness strong growth during the forecast period from 2026 to 2033. The market was valued at approximately USD 5.9 billion in 2025 and is expected to reach nearly USD 10.8 billion by 2033, expanding at a CAGR of around 7.8%. The market growth is driven by rising defense modernization programs, increasing procurement of advanced fighter aircraft, growing demand for precision-guided weapon systems, and continuous advancements in military surveillance and targeting technologies. Targeting pods are externally mounted avionics systems integrated with military aircraft to provide enhanced target detection, tracking, laser designation, infrared imaging, navigation, and reconnaissance capabilities. These systems significantly improve precision strike effectiveness and operational situational awareness during combat missions. The market is witnessing rapid technological evolution through integration of high-definition electro-optical sensors, infrared imaging systems, AI-assisted target recognition, advanced laser designators, and real-time battlefield communication systems. Additionally, increasing geopolitical tensions, cross-border conflicts, and growing investments in next-generation air combat systems are accelerating global demand for advanced targeting pod solutions.

Global Targeting Pods Market Overview

The targeting pods market forms a critical segment of the global military avionics and airborne defense systems industry.Targeting pods are widely deployed on fighter jets, attack helicopters, unmanned aerial vehicles (UAVs), and surveillance aircraft to support precision strike operations and tactical reconnaissance missions. The market includes targeting pods, navigation pods, reconnaissance pods, FLIR (Forward Looking Infrared) systems, and laser designation systems integrated into modern military platforms. Modern targeting pods enable pilots and operators to identify, track, and engage targets with high precision under both day and night operational conditions. Advancements in sensor fusion, real-time image processing, AI-driven battlefield analytics, and long-range targeting systems are reshaping the competitive landscape of the market. Major market participants include Lockheed Martin Corporation, Northrop Grumman Corporation, Raytheon Technologies, L3Harris Technologies, Thales Group, Leonardo S.p.A., BAE Systems, Saab AB, ASELSAN A.S., and Rafael Advanced Defense Systems.Key Drivers of Global Targeting Pods Market Growth

Increasing Defense Modernization Programs

Governments worldwide are investing heavily in modernizing military aircraft fleets and upgrading airborne targeting capabilities. Targeting pods play a critical role in improving mission accuracy, surveillance efficiency, and combat effectiveness.Growing Demand for Precision-Guided Munitions

The increasing use of precision-guided bombs, missiles, and laser-guided weapons is driving demand for advanced targeting systems. Targeting pods provide accurate laser designation and real-time targeting intelligence for precision strikes.Advancements in Electro-Optical and Infrared Technologies

Continuous improvements in infrared sensors, thermal imaging systems, and electro-optical targeting capabilities are enhancing pod performance. Modern systems offer improved detection range, target clarity, and operational flexibility.Rising Adoption of Unmanned Aerial Vehicles (UAVs)

Military UAVs increasingly require compact targeting pod systems for intelligence gathering, surveillance, reconnaissance (ISR), and combat operations. The growth of drone warfare is creating significant opportunities for lightweight targeting solutions.Increasing Geopolitical Tensions and Border Security Concerns

Global geopolitical instability and regional conflicts are increasing defense budgets and procurement of advanced airborne combat technologies. Air superiority and precision targeting capabilities remain strategic priorities for military forces worldwide.Global Targeting Pods Market Segmentation

By Type

The market is segmented into targeting pods, navigation pods, reconnaissance pods, and multi-function pods. Targeting pods account for the largest market share due to widespread deployment in combat aircraft.By Platform

The market includes fighter aircraft, combat helicopters, UAVs, surveillance aircraft, and trainer aircraft. Fighter aircraft dominate the market due to extensive integration of advanced targeting systems in modern air forces.By Component

The market includes FLIR sensors, CCD cameras, laser designators, tracking systems, processors, and communication systems. Infrared imaging and laser designation systems represent major revenue-generating segments.By End User

End users include air forces, naval aviation units, defense organizations, and homeland security agencies. Air force modernization programs remain the primary driver of market demand globally.Regional Market Dynamics

North America

North America holds the largest share of the targeting pods market due to high defense spending, advanced military aviation infrastructure, and strong presence of major defense contractors. The United States leads regional demand supported by continuous modernization of combat aircraft and advanced ISR capabilities.Europe

Europe represents a significant market driven by NATO defense initiatives, rising military procurement, and modernization of fighter aircraft fleets. Countries such as the United Kingdom, France, Germany, and Italy are key regional contributors.Asia-Pacific

Asia-Pacific is the fastest-growing region due to increasing defense budgets, geopolitical tensions, and rapid military modernization programs. China, India, Japan, and South Korea are heavily investing in next-generation combat aviation technologies.Middle East

The Middle East is a major market due to high military expenditure, regional security challenges, and procurement of advanced fighter aircraft. Countries including Saudi Arabia, UAE, and Israel are key adopters of advanced targeting pod systems.Latin America & Africa

These regions are witnessing gradual growth driven by defense modernization initiatives and increasing investments in border surveillance capabilities.Competitive Landscape

The global targeting pods market is highly competitive and technology-intensive, with major defense companies competing through advanced sensor integration and military platform compatibility. Key companies include Lockheed Martin Corporation, Northrop Grumman Corporation, Raytheon Technologies, L3Harris Technologies, Thales Group, Leonardo S.p.A., BAE Systems, Saab AB, ASELSAN A.S., and Rafael Advanced Defense Systems. Companies are increasingly investing in AI-enabled targeting systems, enhanced thermal imaging technologies, lightweight pod architectures, and integrated battlefield communication capabilities. Strategic defense contracts, military partnerships, and long-term aircraft modernization programs remain central to competitive positioning.Strategic Outlook

The strategic outlook for the global targeting pods market remains highly positive due to increasing demand for precision warfare systems and advanced airborne surveillance technologies. Future growth opportunities include AI-driven autonomous targeting systems, multi-sensor fusion technologies, next-generation UAV targeting pods, and integrated electronic warfare capabilities. Advancements in miniaturized sensors, hyperspectral imaging, and real-time tactical data analytics are expected to further transform the market landscape. Defense companies investing in interoperability, sensor accuracy, and next-generation battlefield networking technologies are likely to strengthen their competitive advantages.Final Market Perspective

The global targeting pods market continues to play a vital role in modern military operations by enhancing airborne targeting precision, surveillance capabilities, and combat effectiveness. Growing geopolitical tensions, increasing defense modernization programs, and rising adoption of precision-guided munitions will continue driving market expansion throughout the forecast period. Organizations that successfully combine advanced sensor technologies, AI-enabled targeting systems, and integrated battlefield connectivity solutions will remain strongly positioned in the evolving global targeting pods market.Table of Contents

Table of Contents

1. Executive Summary

- 1.1 Global Targeting Pods Market Snapshot (2026???2033)

- 1.2 Market Size & CAGR Analysis

- 1.3 Key Market Drivers & Growth Opportunities

- 1.4 Largest & Fastest-Growing Segments

- 1.5 Regional Defense Spending Insights

- 1.6 Competitive Landscape Overview

- 1.7 Strategic Outlook Through 2033

2. Introduction & Market Overview

- 2.1 Definition of Targeting Pods

- 2.2 Scope of the Global Targeting Pods Market

- 2.3 Market Size & Forecast (2026???2033)

- 2.4 Evolution of Airborne Targeting Systems

- 2.5 Role of Targeting Pods in Modern Warfare

- 2.6 Defense Procurement & Modernization Trends

- 2.7 Regulatory & Military Compliance Landscape

3. Research Methodology

- 3.1 Primary Research

- 3.2 Secondary Research

- 3.3 Data Collection & Validation Framework

- 3.4 Market Estimation Methodology

- 3.5 Forecast Assumptions (2026???2033)

- 3.6 Data Triangulation & Analytical Modeling

4. Market Dynamics

4.1 Market Drivers

- 4.1.1 Increasing Defense Modernization Programs

- 4.1.2 Growing Demand for Precision-Guided Munitions

- 4.1.3 Advancements in Electro-Optical & Infrared Technologies

- 4.1.4 Rising Adoption of Unmanned Aerial Vehicles (UAVs)

- 4.1.5 Increasing Geopolitical Tensions & Border Security Concerns

4.2 Market Restraints

- 4.2.1 High Development & Procurement Costs

- 4.2.2 Export Restrictions & Defense Regulations

- 4.2.3 Complex Integration with Legacy Aircraft Systems

- 4.2.4 Maintenance & Lifecycle Management Challenges

4.3 Market Opportunities

- 4.3.1 AI-Enabled Autonomous Target Recognition

- 4.3.2 Multi-Sensor Fusion Technologies

- 4.3.3 Expansion of Next-Generation UAV Targeting Pods

- 4.3.4 Integrated Electronic Warfare Capabilities

4.4 Market Challenges

- 4.4.1 Cybersecurity Risks in Defense Avionics

- 4.4.2 Rapidly Evolving Battlefield Requirements

- 4.4.3 Supply Chain Dependence on Advanced Electronics

- 4.4.4 Interoperability Across Military Platforms

5. Global Targeting Pods Market Analysis (USD Billion), 2026???2033

- 5.1 Market Revenue Analysis

- 5.2 CAGR Analysis

- 5.3 Regional Revenue Distribution

- 5.4 Platform-Wise Demand Analysis

- 5.5 Defense Procurement Trends

- 5.6 Sensor & Imaging Technology Analysis

6. Market Segmentation (USD Billion), 2026???2033

6.1 By Type

- 6.1.1 Targeting Pods

- 6.1.2 Navigation Pods

- 6.1.3 Reconnaissance Pods

- 6.1.4 Multi-Function Pods

6.2 By Platform

- 6.2.1 Fighter Aircraft

- 6.2.2 Combat Helicopters

- 6.2.3 UAVs

- 6.2.4 Surveillance Aircraft

- 6.2.5 Trainer Aircraft

6.3 By Component

- 6.3.1 FLIR Sensors

- 6.3.2 CCD Cameras

- 6.3.3 Laser Designators

- 6.3.4 Tracking Systems

- 6.3.5 Processors

- 6.3.6 Communication Systems

6.4 By End User

- 6.4.1 Air Forces

- 6.4.2 Naval Aviation Units

- 6.4.3 Defense Organizations

- 6.4.4 Homeland Security Agencies

7. Market Segmentation by Region

- 7.1 North America

- 7.2 Europe

- 7.3 Asia-Pacific

- 7.4 Middle East

- 7.5 Latin America & Africa

8. Regional Market Insights

- 8.1 North America Market Analysis

- 8.2 Europe Market Analysis

- 8.3 Asia-Pacific Market Analysis

- 8.4 Middle East Market Analysis

- 8.5 Latin America & Africa Market Analysis

9. Competitive Landscape

- 9.1 Market Share Analysis

- 9.2 Product Portfolio Benchmarking

- 9.3 Defense Contract & Procurement Analysis

- 9.4 AI & Sensor Integration Strategies

- 9.5 Military Platform Compatibility Mapping

- 9.6 Strategic Partnerships & Collaborations

10. Company Profiles

- 10.1 Lockheed Martin Corporation

- 10.2 Northrop Grumman Corporation

- 10.3 Raytheon Technologies

- 10.4 L3Harris Technologies

- 10.5 Thales Group

- 10.6 Leonardo S.p.A.

- 10.7 BAE Systems

- 10.8 Saab AB

- 10.9 ASELSAN A.S.

- 10.10 Rafael Advanced Defense Systems

11. Strategic Intelligence & AI Insights

- 11.1 AI-Driven Target Recognition Systems

- 11.2 Sensor Fusion & Battlefield Analytics

- 11.3 UAV Combat Integration Trends

- 11.4 Next-Generation Infrared Imaging Outlook

- 11.5 Porter???s Five Forces Analysis

12. Future Outlook & Strategic Recommendations

- 12.1 Evolution of Autonomous Combat Targeting

- 12.2 Expansion of Multi-Role Pod Systems

- 12.3 Growth of AI-Integrated Defense Avionics

- 12.4 Advanced Battlefield Networking Strategies

- 12.5 Long-Term Market Outlook (2033+)

13. Appendix

14. About Pheonix Research

15. Disclaimer

Competitive Landscape

Global Targeting Pods Market Competitive Intensity & Market Structure Overview

The global targeting pods market is highly competitive, technology-intensive, and moderately consolidated, with dominance by major defense contractors and military avionics manufacturers. Competition is primarily driven by sensor accuracy, targeting precision, infrared imaging capabilities, platform compatibility, battlefield networking integration, and long-term defense procurement contracts.

The market structure is characterized by a limited number of established defense companies with strong expertise in airborne surveillance systems, electro-optical technologies, and military avionics integration. High barriers to entry, strict defense regulations, and long product development cycles significantly limit new market participation.

Strategic collaboration between governments, military organizations, and defense technology providers plays a critical role in shaping market dynamics, particularly through aircraft modernization programs and multi-year defense procurement agreements.

Global Targeting Pods Market Competitive Intensity & Market Structure Current Scenario

Leading Defense & Military Avionics Companies

Lockheed Martin Corporation: One of the leading providers of advanced targeting pod systems integrated into fighter aircraft and airborne combat platforms, with strong expertise in precision targeting and ISR technologies.

Northrop Grumman Corporation: Major defense contractor specializing in airborne surveillance systems, electro-optical targeting technologies, and integrated battlefield solutions.

Raytheon Technologies: Key market participant known for advanced targeting systems, precision-guided weapon integration, and high-performance infrared imaging technologies.

L3Harris Technologies: Strong player in military avionics, ISR systems, and airborne communication technologies supporting advanced targeting operations.

Thales Group: European defense technology leader focused on multi-sensor targeting systems, advanced surveillance solutions, and integrated combat avionics.

Leonardo S.p.A.: Important market participant offering electro-optical targeting systems and airborne defense electronics for military aircraft platforms.

BAE Systems: Major defense company actively involved in combat avionics, sensor integration, and next-generation military targeting technologies.

Saab AB: Defense and aerospace company focused on advanced reconnaissance, surveillance, and airborne combat support systems.

ASELSAN A.S.: Rapidly expanding defense electronics company specializing in electro-optical targeting pods and infrared surveillance systems.

Rafael Advanced Defense Systems: Leading provider of precision targeting and airborne combat systems integrated into advanced military platforms.

Key Competitive Intensity & Market Structure Drivers

Continuous advancements in electro-optical and infrared sensor technologies are intensifying competition among defense companies seeking superior targeting accuracy and battlefield visibility.

Military aircraft modernization programs remain a major competitive driver, as countries increasingly upgrade existing fighter fleets with advanced targeting and surveillance systems.

The growing demand for precision-guided munitions and real-time battlefield intelligence is increasing the importance of advanced targeting pod integration within combat aircraft ecosystems.

Artificial intelligence, sensor fusion, and autonomous target recognition technologies are emerging as major differentiators within next-generation targeting systems.

Compatibility with multiple aircraft platforms, including fighter jets, UAVs, helicopters, and surveillance aircraft, is becoming increasingly important for securing international defense contracts.

Strategic Implications of Competitive Intensity & Market Structure

Defense companies are increasingly investing in AI-enabled targeting systems, real-time tactical analytics, and multi-sensor fusion technologies to improve operational effectiveness and competitive positioning.

Long-term government defense contracts and military procurement agreements remain critical for sustaining revenue stability and securing technological leadership within the market.

Strategic partnerships between aircraft manufacturers, avionics providers, and defense agencies are becoming increasingly important for integrated combat system development.

Miniaturization of targeting pod systems is emerging as a major strategic focus area, particularly for UAV integration and lightweight airborne combat platforms.

Cybersecurity and secure battlefield communication capabilities are also becoming increasingly important due to the growing reliance on network-centric warfare systems.

Global Targeting Pods Market Competitive Intensity & Market Structure Forward Outlook

The global targeting pods market is expected to remain highly innovation-driven as military forces increasingly prioritize precision warfare, real-time situational awareness, and integrated combat operations.

Future competition is likely to intensify around AI-driven autonomous targeting systems, advanced thermal imaging technologies, hyperspectral sensing, and integrated electronic warfare capabilities.

The rapid expansion of military UAV deployments and next-generation fighter aircraft programs is expected to create substantial opportunities for compact and multi-functional targeting pod systems.

North America and Europe are expected to maintain technological leadership, while Asia-Pacific and the Middle East continue expanding defense procurement and indigenous military manufacturing capabilities.

Overall, organizations that successfully combine advanced sensor innovation, platform interoperability, AI-enabled targeting intelligence, and long-term defense partnerships will remain strongly positioned in the evolving global targeting pods market.

Value Chain

Global Targeting Pods Market Value Chain & Supply Chain Evolution Overview

The global targeting pods market value chain is evolving into a highly sophisticated, defense-driven, and technology-intensive ecosystem supported by advancements in electro-optical systems, infrared imaging technologies, AI-assisted targeting solutions, and integrated battlefield communication networks. The industry is transitioning from conventional targeting hardware toward multi-sensor, network-centric, and software-integrated airborne combat systems.

The value chain begins with upstream raw material sourcing and advanced component manufacturing, including semiconductors, optical lenses, thermal sensors, radar modules, laser systems, avionics processors, composite materials, and precision electronic assemblies. Suppliers of military-grade electronics, infrared detectors, and aerospace-grade materials play a critical role in ensuring system durability, accuracy, and operational reliability.

The subsystem development and sensor integration stage forms the technological core of the market. Defense electronics companies develop FLIR systems, CCD cameras, laser designators, targeting processors, stabilization systems, communication modules, and AI-enabled image recognition technologies. Continuous innovation in sensor fusion, thermal imaging, hyperspectral detection, and long-range surveillance systems is enhancing operational performance.

The targeting pod assembly and platform integration layer includes defense OEMs and aerospace manufacturers integrating targeting systems into fighter aircraft, combat helicopters, UAVs, and surveillance platforms. Manufacturers focus on lightweight pod architectures, aerodynamic compatibility, modular integration, and interoperability with modern precision-guided munitions and aircraft avionics systems.

Post-deployment activities include software upgrades, mission system integration, predictive maintenance, battlefield analytics support, and lifecycle sustainment services. Defense contractors increasingly provide long-term support contracts, software-defined capability enhancements, and real-time mission optimization solutions.

The distribution and commercialization layer primarily operates through government defense procurement systems, military modernization contracts, strategic defense alliances, and international aerospace partnerships. Long-term defense agreements and geopolitical alliances significantly influence global supply chain structures.

Cybersecurity, supply chain resilience, and defense sovereignty are becoming increasingly important across the targeting pod ecosystem. Governments and defense contractors are investing in secure semiconductor sourcing, domestic manufacturing capabilities, and encrypted communication architectures to strengthen national defense readiness.

Global Targeting Pods Market Value Chain & Supply Chain Evolution Current Scenario

The current targeting pods supply chain is characterized by high technological complexity, strong government oversight, and concentrated participation from major global defense contractors. The industry relies heavily on specialized military-grade electronics suppliers, advanced optics manufacturers, and secure aerospace integration networks.

North America dominates the market due to advanced military aviation infrastructure, high defense spending, and strong presence of leading defense technology companies. The United States remains the largest developer and deployer of advanced targeting pod systems globally.

Europe maintains a strong position through NATO modernization programs, collaborative defense projects, and advanced aerospace engineering capabilities. Countries such as France, the United Kingdom, Italy, and Germany continue investing in next-generation combat aircraft targeting systems.

Asia-Pacific is emerging as the fastest-growing region due to increasing geopolitical tensions, rising defense budgets, and modernization of air combat fleets. China, India, Japan, and South Korea are expanding indigenous defense manufacturing capabilities and targeting pod procurement programs.

The industry is increasingly transitioning toward AI-enabled targeting systems capable of autonomous threat identification, real-time battlefield analytics, and multi-sensor data fusion. Integration with network-centric warfare systems is becoming a key operational requirement.

However, the market continues to face challenges related to export regulations, defense procurement complexities, semiconductor supply constraints, cybersecurity risks, and high development costs associated with advanced military avionics systems.

Key Value Chain & Supply Chain Evolution Signals in Global Targeting Pods Market

One of the most significant transformation signals is the rapid integration of artificial intelligence and machine learning technologies into targeting systems for autonomous target recognition, predictive threat analysis, and enhanced situational awareness.

Another major signal is the increasing convergence of targeting pods with ISR (Intelligence, Surveillance, and Reconnaissance) systems, enabling multi-role mission capabilities across combat aircraft and unmanned platforms.

The growing adoption of UAVs and unmanned combat aerial systems is significantly increasing demand for lightweight, compact, and energy-efficient targeting pod architectures.

Sensor fusion technologies combining infrared imaging, electro-optical systems, laser designation, radar tracking, and real-time battlefield networking are becoming essential for next-generation precision warfare systems.

Defense supply chain localization and sovereign manufacturing initiatives are accelerating as governments seek to reduce dependence on foreign defense technologies and strengthen national security resilience.

Additionally, advancements in hyperspectral imaging, miniaturized electronics, edge computing, and encrypted communication systems are further reshaping product innovation and military deployment strategies.

Strategic Implications of Value Chain & Supply Chain Evolution in Global Targeting Pods Market

The evolving value chain presents significant strategic implications for defense contractors, aerospace manufacturers, military electronics suppliers, and government procurement agencies. Companies with advanced sensor integration capabilities and AI-enabled targeting technologies are gaining strong competitive advantages.

Vertical integration across optics manufacturing, avionics systems, software development, and aerospace platform integration is becoming increasingly important for ensuring operational compatibility and supply chain security.

Investment in indigenous defense manufacturing capabilities and secure semiconductor supply chains is emerging as a strategic priority for governments seeking defense autonomy and reduced geopolitical dependency.

Long-term military modernization programs and strategic defense partnerships are creating stable demand opportunities for companies capable of supporting lifecycle maintenance, software upgrades, and multi-platform integration.

Technological investment in real-time analytics, edge AI processing, multi-sensor fusion, and secure battlefield networking is enabling defense companies to strengthen their positioning in next-generation warfare ecosystems.

Long-term competitiveness in the targeting pods market will depend on balancing technological superiority, cybersecurity resilience, interoperability, operational reliability, and cost-efficient defense production capabilities.

Global Targeting Pods Market Value Chain & Supply Chain Evolution Forward Outlook

Between 2026 and 2033, the targeting pods value chain is expected to become increasingly AI-driven, software-defined, and network-centric. Future systems will integrate autonomous targeting capabilities, real-time tactical analytics, and seamless interoperability across manned and unmanned combat platforms.

Advancements in miniaturized sensors, quantum imaging technologies, edge computing, and hyperspectral surveillance systems will significantly enhance targeting precision, operational range, and battlefield awareness.

Defense supply chains are expected to become more regionally diversified and cybersecurity-focused through sovereign semiconductor initiatives, secure communication infrastructure, and localized defense manufacturing ecosystems.

The expansion of next-generation fighter aircraft programs, autonomous combat drones, and integrated air defense systems will continue increasing demand for advanced targeting and reconnaissance technologies worldwide.

Digital battlefield integration and cloud-enabled combat management systems are expected to strengthen real-time coordination between airborne targeting systems, ground forces, and command centers.

Ultimately, the future targeting pods value chain will evolve into a highly integrated, AI-powered, and secure defense technology ecosystem where sensor accuracy, autonomous decision support, interoperability, and network-centric warfare capabilities define long-term market competitiveness.

Market-Specific Value Chain

- Raw Material & Electronic Component Sourcing: Semiconductor suppliers, infrared detector manufacturers, optical lens providers, aerospace composite material suppliers, avionics electronics manufacturers

- Subsystem Development & Sensor Integration: FLIR system developers, laser designation technology providers, radar module manufacturers, AI targeting software developers, communication system integrators

- Targeting Pod Manufacturing & Aircraft Integration: Defense OEMs, aerospace system integrators, fighter aircraft manufacturers, UAV integration companies

- Software, Analytics & Lifecycle Support: Battlefield analytics providers, predictive maintenance software developers, cybersecurity solution companies, mission system support providers

- Defense Procurement & Distribution: Government defense agencies, military procurement organizations, defense contractors, strategic aerospace alliance networks

- End-Use Applications: Fighter aircraft targeting, UAV surveillance, precision-guided munitions, ISR missions, naval aviation operations, border surveillance, tactical reconnaissance

Investment Activity

Global Targeting Pods Market Investment & Funding Dynamics Overview

Investment and funding activity in the global targeting pods market is accelerating steadily due to increasing defense modernization programs, rising geopolitical tensions, expanding procurement of advanced combat aircraft, and growing demand for precision-guided warfare systems. Between 2026 and 2033, investments are expected to increasingly focus on AI-enabled targeting systems, next-generation electro-optical sensors, infrared imaging technologies, multi-sensor fusion platforms, and integrated battlefield communication solutions.

The targeting pods industry is evolving into a highly strategic segment of the global military avionics and airborne defense ecosystem. Defense contractors, military technology providers, and government defense agencies are significantly increasing investments in advanced surveillance, reconnaissance, laser designation, and precision targeting technologies designed to enhance operational superiority and mission effectiveness.

A major structural transformation influencing investment activity is the growing global emphasis on precision warfare, network-centric combat operations, and real-time battlefield intelligence. Modern air forces are increasingly investing in advanced targeting pods capable of supporting high-precision strike missions, autonomous threat detection, and integrated ISR (intelligence, surveillance, and reconnaissance) operations.

The market is also benefiting from rising investments in unmanned aerial systems (UAS), next-generation fighter aircraft programs, AI-assisted target recognition systems, and electronic warfare integration technologies. Expansion of military digitization initiatives and sensor-driven combat platforms is creating substantial long-term funding opportunities globally.

Global Targeting Pods Market Investment & Funding Dynamics Current Scenario

Current investment activity in the targeting pods market is strongly supported by rising defense budgets, increasing combat aircraft upgrades, and growing adoption of advanced surveillance technologies across military aviation platforms. Companies are actively investing in lightweight pod architectures, enhanced thermal imaging systems, long-range targeting capabilities, and real-time tactical data processing technologies to strengthen operational efficiency and platform compatibility.

- North America: Dominates global investment activity due to high defense expenditure, extensive military modernization programs, and strong presence of major defense contractors including Lockheed Martin, Raytheon Technologies, and Northrop Grumman.

- Europe: Witnessing strong investment growth supported by NATO defense initiatives, next-generation combat aircraft development programs, and rising investments in integrated airborne surveillance systems.

- Asia-Pacific: Emerging as the fastest-growing investment region due to increasing defense budgets, geopolitical tensions, and rapid military aviation modernization across China, India, Japan, and South Korea.

- Middle East: Continues attracting substantial investments driven by regional security challenges, procurement of advanced fighter aircraft, and growing demand for precision strike capabilities.

Key Investment & Funding Dynamics Signals in Global Targeting Pods Market

- Growing adoption of precision-guided munitions is driving investments into advanced laser designation and target tracking technologies.

- Expansion of AI-driven battlefield analytics is increasing funding for autonomous target recognition, sensor fusion, and real-time mission intelligence systems.

- Advancements in electro-optical and infrared imaging technologies are supporting investments in long-range surveillance and all-weather targeting capabilities.

- Rising deployment of UAVs and autonomous combat platforms is creating strong investment demand for compact and lightweight targeting pod systems.

- Military modernization programs are encouraging investments in integrated communication systems, tactical networking technologies, and interoperable airborne combat platforms.

- Electronic warfare integration and cyber-secure avionics architectures are emerging as important innovation areas attracting defense technology investments.

- Governments are increasingly funding indigenous defense manufacturing and advanced aerospace technology development to strengthen national security capabilities.

Strategic Implications of Investment & Funding Dynamics in Global Targeting Pods Market

- The investment landscape increasingly favors companies capable of combining advanced sensor technologies, AI-enabled targeting systems, and integrated avionics expertise.

- Technological innovation is becoming a major competitive differentiator, particularly in thermal imaging accuracy, autonomous targeting, sensor miniaturization, and battlefield connectivity.

- Strategic partnerships between defense contractors, aerospace manufacturers, AI technology firms, and government agencies are becoming increasingly important for next-generation combat system development.

- Regional diversification strategies remain critical, with North America leading defense technology innovation, Europe emphasizing integrated military modernization, and Asia-Pacific driving rapid procurement growth.

- Companies investing in modular targeting pod architectures and cross-platform compatibility are expected to achieve stronger long-term competitive positioning.

- Defense digitization and network-centric warfare strategies are accelerating investments into cloud-enabled mission systems, predictive targeting analytics, and real-time combat data integration.

- Organizations with strong R&D capabilities, long-term defense contracts, and advanced ISR integration expertise are expected to maintain stronger market leadership globally.

Global Targeting Pods Market Investment & Funding Dynamics Forward Outlook

Looking ahead, the global targeting pods market is expected to attract strong long-term investment supported by increasing global defense expenditure, expansion of next-generation combat aviation systems, and rising adoption of AI-enabled military technologies.

Future capital allocation will prioritize hyperspectral imaging systems, autonomous targeting technologies, multi-domain combat integration, next-generation UAV targeting pods, advanced sensor fusion platforms, and AI-powered mission management systems.

- North America: Will remain the leading investment region due to continuous military aircraft modernization, advanced aerospace innovation, and strong defense technology ecosystems.

- Asia-Pacific: Will continue strengthening its market position through increasing procurement of advanced combat aircraft and expanding indigenous defense manufacturing capabilities.

- Europe: Will increasingly focus on collaborative defense programs, integrated battlefield networking, and next-generation surveillance technologies.

Future funding activity is also expected to accelerate across electronic warfare integration, miniaturized targeting systems, AI-assisted autonomous combat operations, and real-time tactical intelligence platforms.

Defense modernization initiatives, AI-enabled warfare systems, and advanced airborne surveillance technologies will remain central investment priorities across the targeting pods industry. The increasing integration of precision targeting, ISR operations, and digital battlefield ecosystems will continue reshaping competitive dynamics globally.

Overall, the market is expected to maintain strong long-term investment momentum due to its critical role in modern precision warfare, airborne surveillance, and combat mission effectiveness. Companies that successfully combine advanced targeting technologies, AI-driven battlefield intelligence, scalable defense integration capabilities, and global military partnerships will remain strongly positioned to lead the global targeting pods market through 2033.

Technology & Innovation

Global Targeting Pods Market Technology & Innovation Landscape Overview

The global targeting pods market is undergoing rapid technological advancement driven by the evolution of electro-optical systems, artificial intelligence, sensor fusion, and real-time battlefield networking technologies. Innovation across the market is primarily focused on enhancing target acquisition accuracy, improving situational awareness, extending operational range, and enabling multi-domain combat integration for modern air warfare systems.

Targeting pod technologies are increasingly integrating high-definition infrared sensors, advanced laser designation systems, AI-assisted image recognition, and multi-spectral imaging capabilities to support precision-guided strike missions under complex operational environments. These advancements are significantly improving day/night targeting effectiveness, surveillance performance, and combat mission flexibility.

The market is also witnessing strong innovation in miniaturization, lightweight pod architectures, and modular avionics integration, enabling deployment across fighter aircraft, helicopters, unmanned aerial vehicles (UAVs), and next-generation combat platforms. Modern targeting pods are becoming increasingly software-defined, network-enabled, and interoperable with advanced command-and-control ecosystems.

Global Targeting Pods Market Technology & Innovation Current Scenario

Currently, defense manufacturers are focusing heavily on sensor fusion technologies that combine infrared imaging, electro-optical cameras, laser tracking systems, and real-time targeting analytics into unified airborne targeting solutions. These integrated systems improve target identification accuracy while reducing pilot workload during combat operations.

Forward Looking Infrared (FLIR) systems remain a core technological component within modern targeting pods. New-generation FLIR sensors provide enhanced thermal imaging resolution, longer detection ranges, and improved target tracking under adverse weather and low-visibility conditions.

Artificial intelligence and machine learning are increasingly being integrated into targeting pod systems to support automated target recognition, threat classification, predictive tracking, and battlefield analytics. AI-enabled systems can rapidly analyze sensor data and identify potential threats with greater operational speed and precision.

Real-time data link integration is also becoming a major technological priority. Modern targeting pods are increasingly connected with tactical communication networks, enabling live transmission of targeting intelligence, ISR data, and mission-critical battlefield information between aircraft, ground forces, and command centers.

Hyperspectral imaging technologies are emerging as advanced surveillance tools capable of detecting concealed targets, camouflaged objects, and heat signatures across multiple spectral bands. These technologies are enhancing reconnaissance and battlefield awareness capabilities for next-generation military operations.

The increasing deployment of targeting pods on UAV platforms is driving innovation in compact, lightweight, and low-power targeting systems optimized for drone-based surveillance and precision strike missions.

Key Technology & Innovation Trends in Global Targeting Pods Market

- AI-Assisted Target Recognition: Artificial intelligence systems enabling automated target identification, tracking, and threat classification.

- Advanced FLIR Imaging Systems: High-resolution thermal imaging technologies improving long-range detection and night operation capabilities.

- Sensor Fusion Technologies: Integration of electro-optical, infrared, laser, and radar systems into unified targeting platforms.

- Hyperspectral Imaging: Multi-spectrum imaging technologies enhancing target detection and battlefield reconnaissance.

- Real-Time Tactical Data Links: Network-enabled targeting pods supporting live battlefield communication and ISR data sharing.

- Lightweight & Modular Pod Architectures: Compact targeting systems optimized for fighter aircraft, UAVs, and multi-platform deployment.

- Laser Designation & Precision Guidance: Advanced laser targeting systems improving accuracy of guided munitions and strike operations.

- Digital Battlefield Integration: Integration with command-and-control systems and next-generation combat management platforms.

- Autonomous UAV Targeting Systems: AI-enabled targeting technologies supporting autonomous drone surveillance and strike missions.

- Enhanced Image Processing Algorithms: Real-time image enhancement and object tracking improving operational accuracy and decision-making.

Strategic Implications of Technology & Innovation

Technology and innovation are fundamentally transforming the targeting pods market by improving combat precision, reducing response times, and enhancing situational awareness in modern military operations. Defense organizations are increasingly prioritizing AI-driven targeting systems and integrated ISR capabilities to support network-centric warfare strategies.

The adoption of sensor fusion and real-time battlefield networking technologies is enabling faster decision-making and improved coordination between airborne platforms, ground units, and command centers. This is significantly enhancing operational efficiency during precision strike missions and surveillance operations.

The growing importance of UAV warfare is also reshaping the innovation landscape, creating demand for compact and lightweight targeting systems capable of autonomous surveillance and combat support functions. Companies investing in drone-compatible targeting technologies are expected to gain strong competitive advantages.

At the same time, increasing technological complexity and integration requirements are raising development costs and creating significant barriers to entry for smaller defense manufacturers. Cybersecurity and secure communication infrastructure are also becoming critical strategic priorities due to rising electronic warfare threats and cyberattack risks.

Global Targeting Pods Market Technology & Innovation Forward Outlook

Looking ahead, the targeting pods market is expected to evolve toward highly autonomous, AI-enabled, and network-centric combat systems integrated with next-generation military aviation platforms. Future targeting pods will increasingly function as intelligent battlefield nodes capable of autonomous threat analysis and mission coordination.

Advancements in edge computing, AI-driven battlefield analytics, and real-time sensor processing are expected to significantly improve operational responsiveness and reduce pilot cognitive burden during high-intensity combat scenarios.

Next-generation targeting pods are also likely to incorporate enhanced electronic warfare capabilities, cyber-resilient communication systems, and advanced multi-domain interoperability supporting integrated air, land, sea, and space operations.

Hyperspectral sensing, quantum imaging technologies, and ultra-long-range infrared detection systems are expected to further transform surveillance and target acquisition capabilities over the coming decade.

Miniaturization and power-efficiency advancements will support wider deployment of advanced targeting systems across UAV fleets, unmanned combat aerial vehicles (UCAVs), and autonomous defense platforms.

Overall, the technology and innovation landscape of the global targeting pods market is rapidly advancing toward intelligent, interconnected, and AI-driven combat ecosystems designed to support future precision warfare and next-generation military operations.

Market Risk

Global Targeting Pods Market Risk Factors & Disruption Threats Overview

The global targeting pods market is experiencing significant growth driven by rising defense modernization programs, increasing procurement of advanced combat aircraft, and expanding adoption of precision-guided weapon systems. However, despite strong long-term demand, the market faces multiple operational, geopolitical, technological, and budgetary risks that may disrupt future growth trajectories.

One of the primary risk factors affecting the targeting pods market is geopolitical uncertainty and fluctuations in defense spending. Military procurement programs are heavily dependent on government defense budgets, which can be influenced by political changes, economic slowdowns, fiscal deficits, and shifting national security priorities. Delays or reductions in defense allocations may negatively impact targeting pod procurement programs and modernization projects.

The market also faces risks associated with rapid technological evolution in airborne warfare systems. Continuous advancements in AI-enabled targeting, sensor fusion, electronic warfare systems, and autonomous combat technologies require defense contractors to maintain substantial R&D investments. Companies unable to keep pace with emerging military technologies may lose competitiveness in future procurement cycles.

Supply chain vulnerabilities represent another major disruption threat for the industry. Targeting pods rely on highly specialized components including infrared sensors, semiconductor chips, optical systems, thermal imaging modules, laser designators, and advanced processors. Geopolitical trade restrictions, semiconductor shortages, export control regulations, and global logistics disruptions may impact production schedules and delivery timelines.

Cybersecurity threats are becoming increasingly important as modern targeting pods integrate real-time battlefield communication, AI-driven analytics, and network-centric warfare systems. Cyberattacks, electronic jamming, signal interception, and software vulnerabilities could compromise operational effectiveness and national security infrastructure.

Stringent defense export regulations and international arms control policies may also restrict market expansion opportunities. Export licensing requirements, geopolitical sanctions, and regional defense agreements can limit cross-border defense sales and reduce addressable market opportunities for manufacturers.

In addition, rising competition from alternative surveillance and targeting technologies such as advanced drones, satellite-based ISR systems, autonomous combat platforms, and integrated battlefield intelligence systems may reshape future market demand dynamics.

Global Targeting Pods Market Risk Factors & Disruption Threats Current Scenario

The current targeting pods market environment reflects increasing global investments in air force modernization, precision strike capabilities, and intelligence, surveillance, and reconnaissance (ISR) systems. Military forces worldwide are prioritizing enhanced situational awareness and advanced targeting accuracy in modern combat environments.

The growing use of unmanned aerial vehicles (UAVs), next-generation fighter aircraft, and multi-domain combat systems is driving demand for compact, AI-enabled, and highly integrated targeting pod solutions. However, this transition is also increasing technological complexity and competitive pressure among defense contractors.

Rising geopolitical tensions in Eastern Europe, the Middle East, and Asia-Pacific are accelerating defense procurement activities. At the same time, defense manufacturers face increased pressure to comply with cybersecurity standards, export regulations, and interoperability requirements across allied military platforms.

The market is also witnessing increasing emphasis on electronic warfare resilience, sensor accuracy, real-time data processing, and secure battlefield communication capabilities. Manufacturers must continuously upgrade targeting pod systems to address evolving battlefield threats and countermeasure technologies.

Additionally, inflationary pressure, supply chain disruptions, and rising raw material costs are increasing production expenses across the aerospace and defense industry, potentially affecting profitability and procurement timelines.

Global Targeting Pods Market Key Risk Factors & Disruption Threat Signals

- Defense Budget Volatility: Changes in military spending priorities and government budget constraints affecting procurement programs.

- Rapid Technological Obsolescence: Continuous innovation cycles in AI, sensor fusion, and electronic warfare systems requiring high R&D investment.

- Supply Chain Disruptions: Dependence on semiconductors, infrared sensors, optical systems, and specialized aerospace components.

- Cybersecurity & Electronic Warfare Threats: Risks associated with cyberattacks, signal jamming, and network vulnerabilities in connected combat systems.

- Export Control & Regulatory Restrictions: International arms regulations and geopolitical sanctions limiting global defense exports.

- Geopolitical Instability: Regional conflicts and diplomatic tensions influencing defense procurement cycles and international collaborations.

- Rising Competition from Alternative ISR Technologies: Growth of drones, autonomous systems, and satellite-based surveillance platforms.

- Program Delays & Procurement Complexities: Long defense acquisition cycles and integration challenges delaying deployments.

- High Development & Integration Costs: Significant investment required for advanced targeting technologies and aircraft compatibility.

- Interoperability Challenges: Need for compatibility across multiple aircraft platforms, allied systems, and network-centric warfare architectures.

Strategic Implications of Risk Factors

Defense contractors and avionics manufacturers must prioritize continuous innovation in AI-assisted targeting, sensor fusion technologies, electronic warfare resistance, and real-time battlefield analytics to maintain competitive positioning.

Companies should diversify semiconductor and critical component sourcing strategies to strengthen supply chain resilience and reduce dependency on single-region suppliers or geopolitically sensitive markets.

Cybersecurity investments will become increasingly critical as targeting pods evolve into interconnected battlefield intelligence systems integrated with military communication networks and autonomous combat platforms.

Manufacturers are also expected to focus on lightweight pod architectures, modular upgrade capabilities, and multi-platform interoperability to support next-generation fighter aircraft, UAVs, and joint military operations.

Strategic partnerships with defense agencies, aircraft OEMs, and allied military organizations will remain essential for securing long-term procurement contracts and technology integration opportunities.

Global Targeting Pods Market Forward Risk Outlook

Looking ahead to 2026???2033, the targeting pods market is expected to remain highly technology-driven and strategically important within global defense modernization programs. Precision warfare, autonomous targeting, and advanced ISR capabilities will continue shaping future procurement priorities.

AI-powered targeting systems, hyperspectral imaging, sensor miniaturization, cloud-connected battlefield intelligence, and integrated electronic warfare platforms are expected to redefine future competitive dynamics across the industry.

However, increasing cybersecurity threats, geopolitical instability, semiconductor dependency, and evolving export regulations are likely to remain key operational and strategic challenges for market participants.

The growing convergence between manned combat aircraft, UAV ecosystems, and multi-domain warfare platforms may also increase competitive pressure and accelerate technological disruption across airborne targeting systems.

Overall, while the global targeting pods market offers strong long-term opportunities driven by military modernization and precision strike requirements, sustainable competitiveness will depend on technological leadership, supply chain resilience, cybersecurity capabilities, and global defense partnerships.

Regulatory Landscape

Global Targeting Pods Market Regulatory & Policy Environment Overview

The global targeting pods market operates within a highly regulated defense and aerospace environment governed by military procurement regulations, export control laws, defense technology transfer policies, cybersecurity standards, and aviation safety compliance frameworks. Since targeting pods contain highly sensitive military technologies including infrared imaging systems, laser designation equipment, electro-optical sensors, and battlefield communication systems, governments maintain strict oversight over their development, deployment, and international trade.

Regulatory frameworks primarily focus on national security protection, weapons export control, operational safety, defense interoperability, cybersecurity resilience, and compliance with international arms transfer agreements. The increasing integration of AI-enabled targeting systems and autonomous battlefield technologies is also expanding the scope of future defense regulatory oversight globally.

Governments worldwide are increasing investments in next-generation airborne targeting technologies while simultaneously tightening export licensing procedures and defense cybersecurity requirements. This evolving policy environment is significantly influencing procurement strategies, international defense collaborations, and technological innovation within the targeting pods market.

Global Targeting Pods Market Regulatory & Policy Environment Current Scenario

The current regulatory landscape for targeting pods is characterized by strict military export regulations, advanced defense procurement standards, and growing cybersecurity compliance obligations. Due to their strategic military importance, targeting pods are classified as controlled defense systems under multiple international arms control frameworks.

In the United States, targeting pods are regulated under the International Traffic in Arms Regulations (ITAR), Export Administration Regulations (EAR), and oversight by the U.S. Department of Defense (DoD) and Directorate of Defense Trade Controls (DDTC). Export approvals are required for the transfer of advanced targeting technologies, thermal imaging systems, and laser-guided targeting equipment.

The Federal Aviation Administration (FAA) and military airworthiness authorities also regulate aircraft integration and operational certification of targeting pod systems deployed on military platforms.

In Europe, targeting pod systems are regulated under the European Union Common Position on Arms Export Controls, NATO interoperability standards, and national defense procurement agencies. European defense manufacturers must comply with strict export authorization procedures, cybersecurity protocols, and military system certification requirements.

Asia-Pacific countries maintain region-specific defense technology regulations. China controls military avionics technologies through national defense export regulations, while India increasingly emphasizes localization and domestic manufacturing through the Defense Acquisition Procedure (DAP) and ???Make in India??? defense policies.

Middle Eastern countries primarily regulate targeting pod procurement through military acquisition agreements, strategic defense partnerships, and government-controlled defense import frameworks.

Key Regulatory & Policy Environment Signals in Global Targeting Pods Market

- Defense Export Control Regulations: Strict licensing procedures govern international transfer of targeting pods, infrared imaging systems, and advanced military avionics technologies.

- Military Procurement Standards: Governments require compliance with airworthiness certification, combat performance validation, and operational reliability standards.

- Cybersecurity & Defense Network Protection: Increasingly connected battlefield systems are subject to strict cybersecurity compliance frameworks and encrypted communication standards.

- AI & Autonomous Warfare Governance: Regulatory focus is increasing on ethical deployment and operational oversight of AI-assisted targeting systems and autonomous combat technologies.

- NATO & Defense Interoperability Standards: Military alliances require compatibility across airborne targeting, communication, and sensor systems.

- Defense Localization Policies: Governments are promoting domestic defense manufacturing, technology transfer agreements, and local industrial participation requirements.

Military Export Control & Arms Transfer Regulations

Targeting pods are classified as strategic military systems under global arms transfer regulations due to their direct role in precision strike operations and battlefield intelligence gathering.

Key export control frameworks affecting the market include:

- International Traffic in Arms Regulations (ITAR)

- Export Administration Regulations (EAR)

- Wassenaar Arrangement

- Arms Trade Treaty (ATT)

- Missile Technology Control Regime (MTCR)

- National military export licensing systems

Manufacturers exporting targeting systems must comply with:

- End-user verification procedures

- Restricted technology transfer rules

- Sanctions and embargo compliance

- Cross-border defense trade approvals

- Military equipment documentation standards

Export restrictions are particularly strict for advanced infrared targeting sensors, AI-enabled battlefield analytics, encrypted communication modules, and long-range surveillance technologies.

Military Aviation & Airworthiness Regulations

Targeting pods integrated into combat aircraft, helicopters, and UAVs must undergo rigorous military aviation certification and airworthiness approval procedures before operational deployment.

Regulatory requirements typically include:

- Electromagnetic compatibility (EMC) testing

- Vibration and environmental stress testing

- Thermal and altitude performance validation

- Combat survivability assessments

- Software reliability certification

- Operational integration testing with aircraft avionics

Defense agencies and military aviation authorities closely evaluate targeting pod performance under real-world combat conditions to ensure mission reliability and pilot safety.

Cybersecurity & Defense Data Protection Regulations

As targeting pods become increasingly software-defined and connected through network-centric warfare systems, cybersecurity compliance is becoming a major regulatory priority.

Military targeting systems are required to comply with:

- NIST cybersecurity standards

- CMMC (Cybersecurity Maturity Model Certification)

- Defense encrypted communication protocols

- NATO cyber defense frameworks

- Secure tactical data transmission standards

- Anti-jamming and anti-spoofing requirements

Defense contractors are increasingly investing in secure software architectures, encrypted battlefield communication systems, and resilient electronic warfare protection technologies to maintain regulatory compliance.

Environmental & Hazardous Material Compliance

Although targeting pods are military systems, manufacturers must still comply with environmental and hazardous material regulations governing electronics manufacturing and industrial production processes.

Important compliance frameworks include:

- RoHS (Restriction of Hazardous Substances)

- REACH regulations

- Electronic waste disposal standards

- Defense environmental management policies

- Energy-efficient avionics guidelines

Manufacturers are increasingly adopting lightweight materials, low-power electronic architectures, and sustainable production methods to align with evolving environmental compliance expectations.

Defense Procurement & Localization Policies

Governments worldwide are strengthening domestic defense industrial policies to reduce dependency on foreign military technologies and improve national security capabilities.

Defense procurement regulations increasingly require:

- Technology transfer agreements

- Local assembly and manufacturing

- Domestic supplier participation

- Offset obligations

- Indigenous defense R&D collaboration

Programs such as India???s ???Make in India,??? European defense industrial cooperation initiatives, and Middle Eastern defense localization strategies are reshaping supplier access to major military procurement contracts.

Strategic Implications of Regulatory & Policy Environment

The evolving regulatory environment is significantly influencing strategic decision-making across the targeting pods market.

Companies are increasingly investing in:

- Compliance-ready defense manufacturing systems

- Secure AI-enabled targeting technologies

- Cyber-resilient avionics platforms

- Export-compliant system architectures

- Localized production partnerships

- Interoperable battlefield communication capabilities

Regulatory compliance is becoming a critical competitive differentiator, particularly for companies seeking participation in multinational defense programs and long-term military modernization initiatives.

Global Targeting Pods Market Regulatory & Policy Environment Forward Outlook

Between 2026 and 2033, the regulatory environment for the targeting pods market is expected to become increasingly complex due to rapid advancements in AI-assisted warfare systems, autonomous combat technologies, and integrated digital battlefield ecosystems.

Future regulations are likely to focus on:

- AI governance and human oversight requirements

- Enhanced military cybersecurity certification

- Cross-platform interoperability standards

- Advanced export restrictions on sensitive defense technologies

- Autonomous targeting system accountability frameworks

- Secure cloud-based battlefield integration regulations

International geopolitical tensions and defense modernization efforts are expected to further strengthen regulatory oversight of airborne targeting systems and military avionics technologies globally.

Overall, the regulatory and policy environment will remain a major factor shaping technology development, defense procurement strategies, and global competitive dynamics within the targeting pods market. Companies that successfully align with evolving military standards, cybersecurity requirements, and export compliance frameworks are expected to maintain long-term strategic advantages.