Global Automotive Market Report, Size & Forecast 2026-2033

Global Automotive Market Forecast Snapshot (2026???2033)

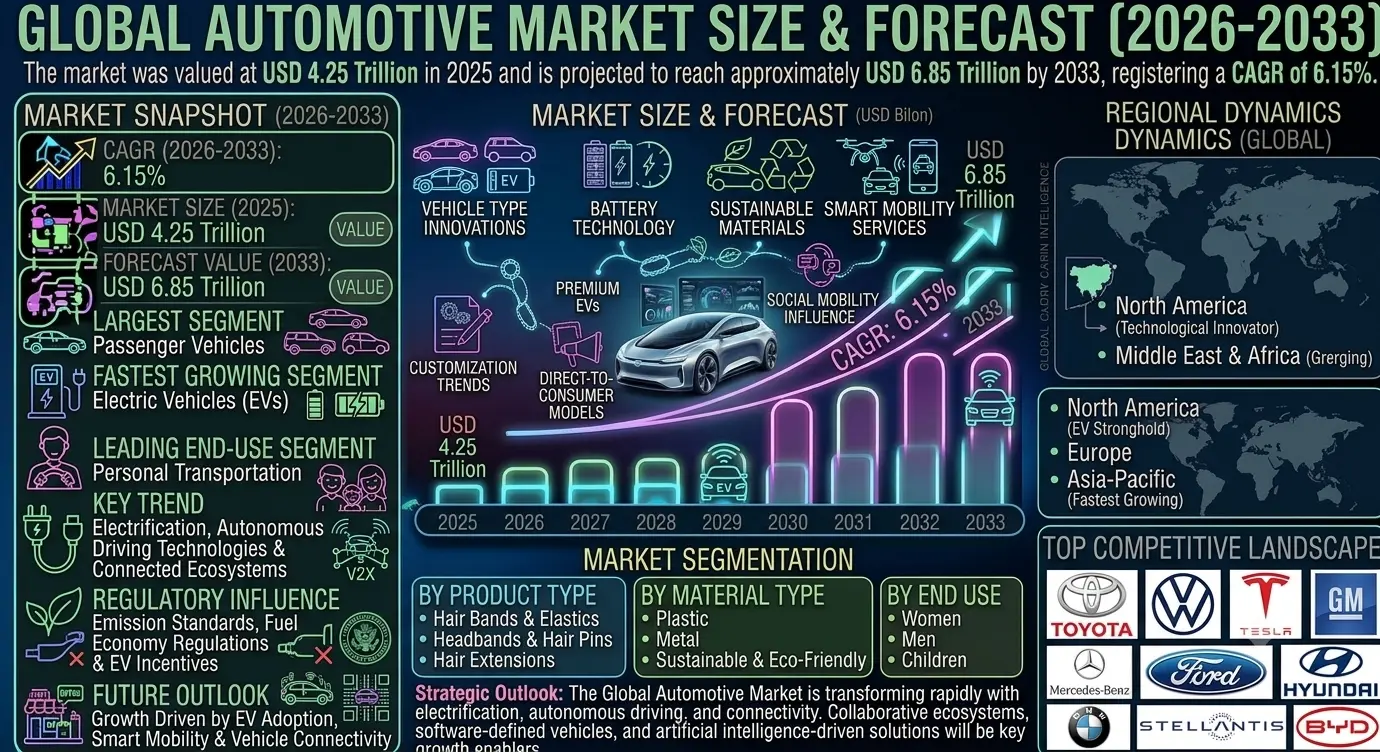

| Metric | Value |

|---|---|

| Market Size (2025) | ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? USD 4.25 Trillion |

| Market Size (2033) | ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ??USD 6.85 Trillion |

| CAGR (2026???2033) | ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? 6.15% |

| Largest Segment | ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ??Passenger Vehicles |

| Fastest Growing Segment | ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? Electric Vehicles (EVs) |

| Leading End-Use Segment | ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ??Personal Transportation |

| Key Trend | ?? ?? ?? ?? ?? ?? ??Electrification, Autonomous Driving Technologies & Connected Vehicle Ecosystems |

| Regulatory Influence | ?? ?? ?? ?? ?? ?? Emission Standards, Fuel Economy Regulations & EV Incentive Policies |

| Future Outlook | Growth Driven by EV Adoption, Smart Mobility Solutions & Advancements in Vehicle Connectivity |

Global Automotive Market Size & Forecast

The Global Automotive Market is expected to witness substantial growth during the forecast period from 2026 to 2033. The market was valued at USD 4.25 trillion in 2025 and is projected to reach approximately USD 6.85 trillion by 2033, registering a CAGR of 6.15%. Market growth is primarily driven by increasing vehicle ownership, rapid urbanization, rising demand for electric vehicles, technological advancements in autonomous driving systems, and expanding investments in smart mobility solutions. The transition toward sustainable transportation and connected vehicle technologies is further reshaping the global automotive landscape.Global Automotive Market Overview

The automotive industry encompasses the design, manufacturing, distribution, and servicing of passenger vehicles, commercial vehicles, electric vehicles, and mobility solutions. The market includes automotive OEMs, component suppliers, mobility service providers, technology firms, and aftermarket service providers. The industry is undergoing significant transformation driven by electrification, digitalization, autonomous driving technologies, and evolving consumer mobility preferences.Structural Drivers of Market Growth

1. Rising Adoption of Electric Vehicles

Growing environmental awareness, supportive government incentives, and advancements in battery technology are accelerating electric vehicle adoption globally. Market Implications: Automotive manufacturers are investing heavily in EV production capacity, battery development, and charging infrastructure partnerships.2. Technological Advancements in Connected and Autonomous Vehicles

Innovations in artificial intelligence, sensors, telematics, and vehicle-to-everything (V2X) communication are enhancing vehicle safety and user experiences. Market Implications: Automotive companies integrating advanced connectivity and autonomous features are strengthening competitive positioning.3. Increasing Urbanization and Mobility Demand

Growing urban populations and rising transportation needs are driving demand for efficient and technologically advanced mobility solutions. Market Implications: Manufacturers are expanding vehicle portfolios and investing in mobility-as-a-service platforms.4. Government Regulations Supporting Sustainable Transportation

Stringent emission regulations and carbon reduction targets are encouraging the adoption of cleaner vehicle technologies. Market Implications: Automotive OEMs are accelerating investments in electrification and fuel-efficient vehicle development.Market Segmentation Analysis

By Vehicle Type

- Passenger Vehicles Largest segment driven by increasing personal vehicle ownership and expanding middle-class populations worldwide.

- Light Commercial Vehicles (LCVs) Widely used for logistics, urban transportation, and last-mile delivery operations.

- Heavy Commercial Vehicles (HCVs) Critical segment supporting freight transportation, construction, and industrial activities.

- Electric Vehicles (EVs) Fastest-growing segment driven by sustainability goals, government incentives, and battery technology improvements.

By Propulsion Type

- Internal Combustion Engine (ICE) Vehicles Currently the largest segment due to extensive global vehicle fleets and fueling infrastructure.

- Battery Electric Vehicles (BEVs) Rapidly expanding segment supported by zero-emission transportation initiatives.

- Hybrid Electric Vehicles (HEVs) Popular transitional technology offering improved fuel efficiency and reduced emissions.

- Plug-in Hybrid Electric Vehicles (PHEVs) Combines electric driving capabilities with extended range through conventional engines.

By End Use

- Personal Transportation Largest segment due to rising consumer demand for mobility, convenience, and vehicle ownership.

- Commercial Transportation Includes logistics, freight, public transportation, and fleet operations.

- Ride-Hailing & Mobility Services Growing segment supported by urban mobility platforms and shared transportation models.

- Government & Institutional Fleets Includes public service vehicles, defense fleets, and municipal transportation systems.

Regional Market Dynamics

North America

Leading market driven by strong automotive manufacturing capabilities, technological innovation, and increasing adoption of electric and connected vehicles.Europe

Driven by stringent emission regulations, strong EV adoption, and significant investments in sustainable mobility infrastructure.Asia-Pacific

Largest and fastest-growing region supported by high vehicle production volumes, expanding consumer markets, and strong government support for electrification.Latin America

Growing market driven by improving economic conditions, expanding automotive production, and rising transportation demand.Middle East & Africa

Emerging market supported by infrastructure development, increasing urbanization, and growing investments in transportation modernization.Competitive Landscape

The Global Automotive Market is highly competitive with established automotive manufacturers, emerging EV companies, mobility service providers, and technology firms competing through innovation, product diversification, and strategic partnerships. Key Companies Operating in the Market Include:- Toyota Motor Corporation

- Volkswagen AG

- Tesla, Inc.

- General Motors Company

- Ford Motor Company

- Hyundai Motor Company

- Mercedes-Benz Group AG

- BMW Group

- Stellantis N.V.

- BYD Company Ltd.

Strategic Outlook

The future of the automotive market will be shaped by rapid electrification, autonomous driving advancements, connected vehicle ecosystems, and evolving mobility services. Automotive manufacturers are expected to increase investments in battery technologies, software-defined vehicles, and artificial intelligence-driven mobility solutions. Strategic collaborations between automakers, technology providers, and energy companies will become increasingly important in supporting next-generation transportation ecosystems. Growing adoption of electric vehicles, expansion of charging infrastructure, and advancements in autonomous technologies are expected to create substantial opportunities across the automotive value chain. Additionally, digitalization, predictive maintenance, and over-the-air software updates will continue transforming vehicle ownership and user experiences.Final Market Perspective

The Global Automotive Market remains one of the largest and most dynamic industries worldwide. Increasing demand for sustainable transportation, rapid technological innovation, and evolving consumer mobility preferences are driving significant transformation across the sector. As electrification, connectivity, and automation continue to redefine transportation, companies investing in advanced technologies, sustainability initiatives, and customer-centric mobility solutions will be well-positioned to capitalize on long-term growth opportunities in the global automotive ecosystem.Table of Contents

Table of Contents

- Executive Summary

- Global Automotive Market Snapshot (2026???2033)

- Market Size & Growth Overview

- Key Market Highlights

- Largest & Fastest-Growing Segments

- Leading End-Use Segment Overview

- Key Market Trends & Mobility Transformation

- Strategic Outlook Through 2033

- Market Introduction & Overview

- Definition of Automotive Industry

- Scope of the Global Automotive Market

- Evolution of Global Transportation & Vehicle Technologies

- Role of Automotive Industry in Economic Development & Mobility

- Value Chain Analysis of the Automotive Ecosystem

- Regulatory Influence (Emission Standards, Fuel Economy Regulations & EV Incentive Policies)

- Transition Toward Electrified, Connected & Autonomous Mobility Solutions

- Research Methodology

- Primary Research Approach

- Secondary Research Sources

- Market Size Estimation Methodology

- Forecasting Assumptions (2026???2033)

- Data Validation & Triangulation Process

- Market Dynamics

- Structural Drivers of Market Growth

- Rising Adoption of Electric Vehicles

- Technological Advancements in Connected & Autonomous Vehicles

- Increasing Urbanization & Mobility Demand

- Government Regulations Supporting Sustainable Transportation

- Market Restraints

- High Cost of Electric Vehicles & Advanced Technologies

- Supply Chain Disruptions & Semiconductor Shortages

- Infrastructure Limitations in Emerging Markets

- Market Opportunities

- Expansion of EV Charging Infrastructure

- Growth of Mobility-as-a-Service (MaaS)

- Development of Software-Defined Vehicles

- Increasing Adoption of Autonomous Driving Technologies

- Market Challenges

- Battery Raw Material Supply Constraints

- Cybersecurity Risks in Connected Vehicles

- Regulatory Complexity Across Global Markets

- Structural Drivers of Market Growth

- Global Automotive Market Size & Forecast (2026???2033)

- Market Revenue Analysis

- CAGR Analysis

- Vehicle Production & Sales Trends

- EV vs ICE Vehicle Adoption Analysis

- Investment Trends

- Future Market Outlook

- Market Segmentation Analysis (2026???2033)

- By Vehicle Type

- Passenger Vehicles (Largest Segment)

- Light Commercial Vehicles (LCVs)

- Heavy Commercial Vehicles (HCVs)

- Electric Vehicles (EVs) (Fastest-Growing Segment)

- By Propulsion Type

- Internal Combustion Engine (ICE) Vehicles (Largest Segment)

- Battery Electric Vehicles (BEVs)

- Hybrid Electric Vehicles (HEVs)

- Plug-in Hybrid Electric Vehicles (PHEVs)

- By End Use

- Personal Transportation (Largest Segment)

- Commercial Transportation

- Ride-Hailing & Mobility Services

- Government & Institutional Fleets

- By Vehicle Type

- Regional Market Analysis

- North America

- Europe

- Asia-Pacific (Largest & Fastest-Growing Regional Market)

- Latin America

- Middle East & Africa

- Competitive Landscape

- Market Structure & Competitive Analysis

- Key Player Benchmarking

- Strategic Developments

- EV, Autonomous Driving & Connected Vehicle Strategies

- Partnerships, Mergers, Acquisitions & Mobility Ecosystem Expansion

- Company Profiles

- Toyota Motor Corporation

- Volkswagen AG

- Tesla, Inc.

- General Motors Company

- Ford Motor Company

- Hyundai Motor Company

- Mercedes-Benz Group AG

- BMW Group

- Stellantis N.V.

- BYD Company Ltd.

- Strategic Outlook

- Future of Electric Mobility & Battery Technologies

- Expansion of Connected & Software-Defined Vehicles

- Growth of Autonomous Driving Systems

- Evolution of Smart Mobility & Shared Transportation Services

- Long-Term Market Outlook (2033+)

- Final Market Perspective

- Appendix

- About Pheonix Market Research

- Disclaimer

Competitive Landscape

Global Automotive Market Competitive Intensity & Market Structure Overview

The Global Automotive Market is highly competitive and moderately consolidated, characterized by the presence of multinational automotive manufacturers, electric vehicle (EV) producers, commercial vehicle companies, mobility service providers, and automotive technology firms. Competitive intensity is driven by vehicle innovation, pricing strategies, electrification capabilities, autonomous driving technologies, manufacturing scale, brand reputation, and global distribution networks.

Companies compete across multiple vehicle categories including passenger vehicles, commercial vehicles, electric vehicles, hybrid vehicles, luxury vehicles, and mobility solutions. Rapid advancements in electrification, software-defined vehicles, connected mobility, and autonomous driving technologies are intensifying competition across both traditional automotive manufacturers and emerging EV-focused companies.

The market structure is increasingly evolving toward technology-driven and sustainability-focused business models. Automotive manufacturers are investing heavily in battery technologies, charging infrastructure partnerships, artificial intelligence, advanced driver-assistance systems (ADAS), and connected vehicle ecosystems to strengthen long-term market positioning.

Global Automotive Market Competitive Intensity & Market Structure Current Scenario

Leading Global Automotive Companies

- Toyota Motor Corporation: One of the world’s largest automotive manufacturers with a diversified portfolio spanning passenger vehicles, hybrid vehicles, and commercial transportation solutions.

- Volkswagen AG: A global automotive leader operating multiple vehicle brands while aggressively expanding electric mobility and software-defined vehicle initiatives.

- Tesla, Inc.: A leading electric vehicle manufacturer recognized for advanced battery technology, autonomous driving capabilities, and direct-to-consumer sales models.

- General Motors Company: A major automotive manufacturer investing heavily in EV platforms, battery development, and autonomous vehicle technologies.

- Ford Motor Company: A prominent global automaker expanding its electric vehicle portfolio and connected mobility solutions across passenger and commercial segments.

- Hyundai Motor Company: A leading automotive manufacturer with strong positions in conventional, hybrid, electric, and hydrogen-powered vehicle markets.

- Mercedes-Benz Group AG: A premium automotive company focused on luxury vehicles, advanced mobility technologies, and electrification initiatives.

- BMW Group: A major luxury vehicle manufacturer investing in electric mobility, autonomous driving systems, and digital vehicle ecosystems.

- Stellantis N.V.: A diversified automotive group operating multiple global brands and accelerating investments in electrification and smart mobility technologies.

- BYD Company Ltd.: One of the fastest-growing EV manufacturers globally, benefiting from vertically integrated battery and electric vehicle production capabilities.

Key Competitive Intensity & Market Structure Drivers

Rapid electrification of the automotive industry is intensifying competition as manufacturers accelerate investments in battery technologies, EV production facilities, and charging infrastructure partnerships.

Growing demand for connected and software-defined vehicles is encouraging companies to expand investments in digital platforms, artificial intelligence, telematics, and over-the-air software update capabilities.

Increasing regulatory pressure regarding emissions reduction and sustainability targets is driving innovation across electric, hybrid, and alternative-fuel vehicle segments.

Strategic alliances among automotive manufacturers, battery suppliers, semiconductor companies, and technology providers are becoming increasingly important for maintaining competitive advantages.

Rising consumer demand for vehicle connectivity, advanced safety systems, and autonomous driving features is accelerating technology-focused competition throughout the industry.

Strategic Implications of Competitive Intensity & Market Structure

Automotive companies with strong manufacturing capabilities, extensive distribution networks, and advanced technology ecosystems are expected to maintain significant competitive advantages.

Investment in battery innovation, software development, and connected mobility solutions is becoming essential for long-term market leadership.

Manufacturers focusing on vehicle electrification, sustainability initiatives, and digital customer experiences are likely to strengthen brand loyalty and market share.

Expansion of charging infrastructure partnerships, mobility services, and autonomous driving capabilities is creating new opportunities for revenue diversification.

Organizations capable of combining vehicle quality, technological innovation, operational efficiency, sustainability, and customer-centric mobility solutions will be best positioned to compete effectively in the evolving automotive market.

Global Automotive Market Competitive Intensity & Market Structure Forward Outlook

The competitive landscape of the global automotive market is expected to become increasingly technology-driven, software-centric, and sustainability-focused throughout the forecast period.

Future competition will be shaped by advancements in electric vehicle technologies, autonomous driving systems, connected mobility platforms, battery innovation, and intelligent transportation ecosystems.

Market participants are expected to increase investments in artificial intelligence, software-defined vehicles, smart manufacturing, and sustainable mobility solutions to strengthen competitive positioning.

Over the forecast period, companies that successfully balance innovation, electrification, software capabilities, sustainability, affordability, and customer experience will be best positioned to lead the evolving global automotive market.

Value Chain

Global Automotive Market Value Chain & Supply Chain Evolution Overview

The Global Automotive Market operates through a highly complex and interconnected value chain that spans raw material procurement, component manufacturing, vehicle assembly, software integration, distribution, retailing, aftersales services, and end-user mobility solutions. The industry includes passenger vehicles, commercial vehicles, electric vehicles (EVs), hybrid vehicles, autonomous vehicles, and connected mobility platforms.

The market is undergoing significant transformation driven by electrification, digitalization, autonomous driving technologies, sustainability initiatives, and evolving consumer mobility preferences. Automotive manufacturers are increasingly investing in battery technologies, vehicle software platforms, connected services, and smart manufacturing capabilities to strengthen competitive positioning.

The expansion of electric vehicle production, growing demand for connected vehicles, and increasing integration of artificial intelligence are reshaping global supply chains. Companies are adopting localized sourcing strategies, digital supply chain management systems, and strategic partnerships to improve resilience and operational efficiency.

Advancements in battery manufacturing, software-defined vehicles, autonomous systems, and mobility-as-a-service platforms are fundamentally transforming the automotive value chain while creating new revenue streams and business models.

Global Automotive Market Value Chain & Supply Chain Evolution Current Scenario

Market-Specific Value Chain

- Raw Material Sourcing: Procurement of steel, aluminum, copper, plastics, semiconductors, lithium, nickel, cobalt, rare earth materials, and other critical automotive inputs.

- Component Manufacturing: Production of engines, transmissions, batteries, electric drivetrains, semiconductors, infotainment systems, sensors, braking systems, and vehicle electronics.

- Vehicle Design & Engineering: Research and development, product design, software development, safety engineering, autonomous driving technologies, and vehicle testing.

- Vehicle Manufacturing & Assembly: Assembly of passenger vehicles, commercial vehicles, electric vehicles, and specialty mobility solutions.

- Software Integration & Connectivity: Deployment of connected vehicle systems, telematics platforms, autonomous driving software, and over-the-air update capabilities.

- Distribution & Logistics: Vehicle transportation, inventory management, warehousing, dealer network operations, and export logistics.

- Retail & Sales Channels: Sales through dealerships, direct-to-consumer channels, fleet sales networks, leasing providers, and digital vehicle marketplaces.

- Aftermarket & Mobility Services: Vehicle maintenance, spare parts, charging services, fleet management, ride-sharing platforms, and mobility solutions.

- End User Consumption: Individual vehicle owners, commercial fleet operators, logistics companies, government agencies, and mobility service providers.

Company-to-Stage Mapping

- Raw Material Sourcing: Rio Tinto, BHP Group, Glencore plc, Vale S.A., Albemarle Corporation, and critical mineral suppliers.

- Component Manufacturing: Bosch, Denso Corporation, Continental AG, Magna International, ZF Friedrichshafen AG, Aptiv PLC, and semiconductor manufacturers.

- Vehicle Design & Engineering: Toyota Motor Corporation, Volkswagen AG, Tesla, Inc., BMW Group, Mercedes-Benz Group AG, Hyundai Motor Company, and automotive engineering firms.

- Vehicle Manufacturing & Assembly: Toyota Motor Corporation, Ford Motor Company, General Motors Company, Stellantis N.V., BYD Company Ltd., and global automotive OEMs.

- Software Integration & Connectivity: Tesla, NVIDIA Corporation, Qualcomm Technologies, Mobileye Global Inc., and automotive software providers.

- Distribution & Logistics: DHL Supply Chain, Kuehne+Nagel, CEVA Logistics, DB Schenker, and automotive logistics specialists.

- Retail & Sales Channels: Automotive dealerships, direct sales platforms, leasing companies, fleet management providers, and online vehicle marketplaces.

- Aftermarket & Mobility Services: Bosch Car Service, Bridgestone Corporation, Michelin Group, Uber Technologies, Lyft, and mobility service providers.

- End User Consumption: Individual consumers, commercial fleet operators, logistics companies, government agencies, public transportation providers, and mobility platform users.

Key Value Chain & Supply Chain Evolution Signals in Global Automotive Market

Growth of Electric Vehicle Ecosystems

Electric vehicle adoption is accelerating investments in battery manufacturing, charging infrastructure, power electronics, and critical mineral supply chains across major automotive markets.

Increasing Software Content per Vehicle

Software-defined vehicles are becoming a key differentiator as manufacturers integrate connectivity, advanced driver assistance systems, and subscription-based digital services.

Expansion of Autonomous Driving Technologies

Automotive companies are investing heavily in sensors, artificial intelligence, machine learning, and autonomous mobility platforms to enhance safety and automation capabilities.

Regionalization of Automotive Supply Chains

Manufacturers are diversifying sourcing strategies and establishing localized production facilities to reduce geopolitical and supply chain risks.

Sustainability and Circular Economy Initiatives

The industry is increasingly adopting battery recycling, renewable energy-powered manufacturing, and sustainable material sourcing practices.

Digitalization of Manufacturing and Logistics

Industry 4.0 technologies, predictive analytics, robotics, and digital twins are improving production efficiency and supply chain visibility.

Strategic Implications of Value Chain & Supply Chain Evolution

Investment in Battery Manufacturing and EV Infrastructure

Companies that secure battery supply chains and expand charging ecosystem partnerships can strengthen long-term market competitiveness.

Strengthening Technology Partnerships

Collaborations with software developers, semiconductor manufacturers, and AI technology providers can accelerate automotive innovation.

Enhancing Supply Chain Resilience

Regional sourcing strategies and supplier diversification can improve operational stability and reduce disruption risks.

Expansion of Connected Vehicle Revenue Streams

Digital services, software subscriptions, and connected mobility offerings are creating new recurring revenue opportunities for OEMs.

Accelerating Sustainability Programs

Investments in low-carbon manufacturing, battery recycling, and sustainable sourcing can improve regulatory compliance and corporate reputation.

Optimizing Omnichannel Sales Models

Combining dealership networks with digital retail platforms can improve customer engagement and purchasing experiences.

Global Automotive Market Value Chain & Supply Chain Evolution Forward Outlook

Looking ahead, the automotive value chain is expected to become increasingly electrified, software-driven, connected, and sustainability-focused. Technological innovation and evolving mobility models will continue reshaping competitive dynamics across the industry.

Key Future Developments Include:

- Expansion of battery gigafactories and localized EV supply chains.

- Increased adoption of software-defined vehicles and connected mobility services.

- Growth of autonomous driving and advanced driver assistance technologies.

- Rising investments in battery recycling and circular economy initiatives.

- Greater utilization of AI-driven manufacturing and predictive supply chain management.

- Strengthening of regional sourcing and resilient production strategies.

As the market evolves, competitive advantage will increasingly depend on battery technology leadership, software capabilities, manufacturing efficiency, supply chain resilience, and sustainability performance.

Companies that successfully integrate electrification, connectivity, automation, digital mobility solutions, and sustainable manufacturing practices will be well-positioned to achieve long-term growth in the Global Automotive Market.

Investment Activity

Global Automotive Market Investment & Funding Dynamics Overview (2026???2033)

The Global Automotive Market is witnessing substantial investment activity driven by accelerating vehicle electrification, increasing adoption of connected vehicle technologies, advancements in autonomous driving systems, and growing demand for sustainable mobility solutions. Automotive manufacturers, technology companies, battery producers, venture capital firms, private equity investors, mobility service providers, and infrastructure developers are actively investing in electric vehicle production, battery technologies, charging infrastructure, autonomous mobility platforms, connected vehicle ecosystems, and software-defined vehicle architectures.

Investment momentum is accelerating as industry participants seek to capitalize on evolving transportation trends, stringent emission regulations, and increasing consumer demand for intelligent mobility solutions. Capital allocation is increasingly focused on battery manufacturing facilities, next-generation powertrain technologies, vehicle connectivity platforms, artificial intelligence integration, mobility-as-a-service solutions, and digital automotive ecosystems.

Additionally, growing investments in autonomous driving technologies, advanced driver-assistance systems (ADAS), battery recycling infrastructure, vehicle software platforms, and smart transportation networks are creating significant long-term opportunities across the global automotive ecosystem.

Current Investment & Funding Landscape

The current market environment reflects strong investor confidence in electrification, mobility innovation, and automotive digital transformation. Industry participants are investing heavily in electric vehicle manufacturing capacity, battery supply chains, connected vehicle technologies, charging infrastructure development, and advanced mobility services.

Significant funding is being directed toward EV startups, battery technology companies, autonomous vehicle developers, automotive software providers, semiconductor manufacturers, and intelligent transportation platforms to strengthen innovation capabilities and competitive positioning.

Strategic collaborations among automotive OEMs, battery manufacturers, technology firms, charging infrastructure providers, and mobility operators are reshaping investment flows and accelerating next-generation transportation development worldwide.

Key Investment & Funding Dynamics Signals

- Growing demand for electric vehicles and sustainable transportation solutions is driving investment across manufacturing and technology development.

- Expansion of battery production facilities and energy storage technologies is attracting substantial long-term capital investments.

- Increasing deployment of connected vehicle platforms and automotive software solutions is creating new technology-focused funding opportunities.

- Rising investments in autonomous driving systems, AI-powered mobility solutions, and advanced driver-assistance technologies are accelerating market innovation.

- Strategic funding for charging infrastructure networks and smart mobility ecosystems is supporting EV adoption globally.

- Growing focus on battery recycling, sustainable manufacturing, and carbon-neutral production initiatives is strengthening environmental investment activity.

- Expansion into high-growth emerging automotive markets is generating attractive investment opportunities for manufacturers and infrastructure providers.

Strategic Implications of Investment & Funding Dynamics

- Continuous investment in electrification technologies, software innovation, and autonomous mobility systems is essential for maintaining long-term competitiveness.

- Capital allocation toward battery development, charging infrastructure, and sustainable manufacturing capabilities will strengthen future market positioning.

- Companies developing connected vehicle ecosystems, digital mobility services, and AI-powered transportation solutions are expected to secure stronger growth opportunities.

- Strategic partnerships between automakers, technology companies, battery suppliers, and energy providers will accelerate innovation and commercialization.

- Investments in supply chain resilience, semiconductor sourcing, and advanced manufacturing technologies will improve operational efficiency and scalability.

- Compliance with emission regulations, vehicle safety standards, and sustainability mandates will continue influencing capital deployment decisions.

- Organizations building integrated capabilities across vehicle production, software development, mobility services, and energy infrastructure are expected to capture substantial future value.

Forward Outlook

Looking ahead, the Global Automotive Market is expected to maintain strong investment momentum driven by EV adoption, connected mobility expansion, autonomous driving advancements, and increasing demand for sustainable transportation solutions.

Future capital deployment will increasingly focus on next-generation battery technologies, autonomous vehicle platforms, charging infrastructure expansion, software-defined vehicles, smart mobility ecosystems, and advanced vehicle connectivity solutions.

As governments, businesses, and consumers continue prioritizing sustainable transportation and intelligent mobility, investment activity is expected to expand across electric mobility, automotive software, battery manufacturing, mobility services, and digital transportation infrastructure.

In conclusion, the Global Automotive Market represents one of the most attractive industrial investment landscapes where electrification, connectivity, autonomy, sustainability, and digital transformation will define future funding priorities, competitive differentiation, and long-term market expansion.

Technology & Innovation

Global Automotive Market Technology & Innovation Landscape Overview

The global automotive market is undergoing a major technological transformation driven by advancements in electric mobility, autonomous driving systems, connected vehicle platforms, artificial intelligence, and software-defined vehicle architectures. Automotive manufacturers are increasingly investing in next-generation technologies that improve vehicle efficiency, safety, connectivity, and user experience while supporting global sustainability objectives. The industry is rapidly evolving from traditional vehicle manufacturing toward intelligent mobility ecosystems where digital technologies, electrification, and advanced software capabilities play a central role in product development and competitive differentiation.

Technological innovation is also accelerating the adoption of advanced battery technologies, vehicle-to-everything (V2X) communication systems, over-the-air software update capabilities, and smart manufacturing platforms. These developments are enabling automakers to improve vehicle performance, reduce emissions, optimize production processes, and deliver highly connected driving experiences. As consumer expectations continue to evolve, technology is becoming one of the most important factors influencing automotive market growth worldwide.

Global Automotive Market Technology & Innovation Current Scenario

Current innovation activities within the automotive market are primarily focused on vehicle electrification, autonomous mobility, digital connectivity, and intelligent transportation solutions. Automotive manufacturers are expanding electric vehicle portfolios while investing in high-performance battery systems, energy management technologies, and charging infrastructure development. Artificial intelligence is increasingly being integrated into advanced driver assistance systems, predictive maintenance solutions, and vehicle safety platforms to improve operational efficiency and enhance driving experiences.

Connected vehicle technologies are becoming standard across many vehicle categories, enabling real-time data exchange, remote diagnostics, navigation optimization, and software upgrades. At the same time, smart manufacturing technologies, robotics, digital twins, and industrial automation systems are helping automotive companies improve production efficiency, quality control, and supply chain visibility. These innovations are supporting the industry’s transition toward more intelligent, sustainable, and technology-driven mobility solutions.

Key Technology & Innovation Trends in Global Automotive Market

- Electric Vehicle Technologies: Advanced battery systems, power electronics, and energy management solutions supporting vehicle electrification.

- Autonomous Driving Systems: Integration of artificial intelligence, sensors, cameras, radar, and LiDAR technologies for enhanced vehicle automation.

- Connected Vehicle Platforms: Real-time communication, remote diagnostics, and cloud-based vehicle management capabilities.

- Software-Defined Vehicles: Increasing reliance on software platforms for vehicle functionality, performance upgrades, and feature management.

- Vehicle-to-Everything (V2X) Communication: Supporting intelligent transportation systems and improved road safety.

- Advanced Driver Assistance Systems (ADAS): Enhancing driver safety through automated braking, lane assistance, and collision avoidance technologies.

- Over-the-Air Software Updates: Enabling continuous vehicle improvement and remote feature deployment.

- Smart Manufacturing & Robotics: Improving production efficiency, automation, and quality management across automotive facilities.

- Digital Twin Technologies: Supporting product development, simulation, and manufacturing optimization.

- Next-Generation Battery Innovation: Advancements in solid-state batteries, fast charging technologies, and energy storage performance.

Strategic Implications of Technology & Innovation

Technological innovation is fundamentally reshaping the automotive industry by creating new opportunities for growth, operational efficiency, and customer engagement. Companies investing in electric mobility, connected vehicle ecosystems, autonomous driving technologies, and software platforms are strengthening their competitive positions while responding to evolving consumer and regulatory requirements. The convergence of artificial intelligence, connectivity, electrification, and digital services is enabling manufacturers to generate new revenue streams while improving vehicle functionality and ownership experiences.

As technology becomes increasingly integrated into vehicle design and mobility services, automotive companies are expanding collaborations with software developers, semiconductor manufacturers, battery suppliers, and technology providers. While innovation continues to create significant opportunities, challenges related to cybersecurity, infrastructure development, software complexity, regulatory compliance, and technology investment requirements remain important strategic considerations for market participants.

Global Automotive Market Technology & Innovation Forward Outlook

The future of the automotive market is expected to be driven by continued advancements in electric propulsion systems, autonomous mobility platforms, intelligent transportation networks, and software-centric vehicle architectures. Emerging technologies such as solid-state batteries, generative artificial intelligence, advanced mobility analytics, autonomous fleet management systems, and smart city integration platforms are expected to further transform the automotive ecosystem. Manufacturers are increasingly focusing on sustainability, digitalization, and connected mobility solutions to meet long-term industry requirements.

As global adoption of electric vehicles accelerates and connected transportation infrastructure expands, automotive innovation will continue to redefine mobility experiences for consumers and businesses alike. The integration of advanced software, artificial intelligence, cloud computing, and next-generation vehicle technologies will create a more intelligent, efficient, and sustainable transportation ecosystem, positioning the automotive market for continued technological evolution and long-term growth.

Market Risk

Global Automotive Market Risk Factors & Disruption Threats Overview

The Global Automotive Market operates within a highly complex ecosystem involving vehicle manufacturers, component suppliers, battery producers, software developers, mobility service providers, and infrastructure stakeholders. While the industry continues to benefit from growing mobility demand, technological innovation, and vehicle electrification, it faces substantial risks related to supply chain disruptions, regulatory uncertainty, technological transitions, and changing consumer behavior.

One of the most significant structural risks is the industry’s ongoing transition from internal combustion engine (ICE) vehicles to electric and software-defined vehicles. This shift requires substantial investments in battery technologies, manufacturing infrastructure, charging networks, and workforce transformation, creating financial and operational challenges for automotive manufacturers.

The market is also highly vulnerable to supply chain disruptions involving semiconductors, battery materials, electronic components, rare earth elements, and critical minerals. Shortages of key inputs can significantly affect vehicle production schedules, inventory availability, and profitability.

Another major disruption factor involves increasingly stringent environmental regulations, fuel economy standards, carbon emission targets, and vehicle safety requirements. Compliance with evolving regulatory frameworks often requires substantial investments in research, development, testing, and certification processes.

Additionally, geopolitical tensions, trade restrictions, tariffs, and regional manufacturing dependencies continue to create uncertainty across global automotive supply chains and international vehicle trade.

Global Automotive Market Risk Factors & Disruption Threats Current Scenario

The current automotive landscape is characterized by accelerating electric vehicle adoption, growing investments in autonomous driving technologies, and increasing integration of connected vehicle ecosystems. Automakers are rapidly transforming product portfolios to align with changing consumer preferences and regulatory requirements.

However, manufacturers continue to face challenges associated with rising raw material costs, battery supply constraints, labor shortages, and elevated capital expenditure requirements for electrification initiatives.

Supply chain resilience remains a key concern as disruptions involving semiconductors, battery cells, logistics networks, and critical mineral sourcing continue to affect production efficiency across multiple regions.

Consumer purchasing decisions are increasingly influenced by economic conditions, interest rates, inflationary pressures, fuel prices, and government incentives for electric vehicle adoption. These factors can create demand fluctuations across vehicle segments.

At the same time, cybersecurity concerns are growing as connected vehicles, software-defined architectures, and over-the-air update systems become more prevalent throughout the industry.

Key Risk Factors & Disruption Threat Signals in Global Automotive Market

A major disruption signal is the rapid acceleration of electric vehicle adoption, which is reshaping traditional automotive business models, supplier relationships, and manufacturing strategies across global markets.

Another important signal is the growing dependence on battery materials such as lithium, nickel, cobalt, graphite, and rare earth elements. Supply constraints or price volatility involving these materials may significantly impact EV production economics.

The increasing integration of software, artificial intelligence, autonomous driving systems, and connected vehicle technologies is creating new cybersecurity, data privacy, and system reliability risks for manufacturers and consumers.

Growing regulatory pressure related to emissions reduction, sustainability reporting, vehicle safety standards, and lifecycle environmental performance is influencing product development priorities and investment decisions.

The emergence of mobility-as-a-service platforms, ride-sharing services, subscription-based transportation models, and autonomous mobility solutions may gradually alter traditional vehicle ownership patterns.

Global geopolitical instability, trade disputes, and regional manufacturing concentration continue to pose risks to automotive production networks, sourcing strategies, and international market access.

Strategic Implications of Risk Factors & Disruption Threats in Global Automotive Market

Automotive manufacturers must diversify supply chains and secure long-term sourcing agreements for semiconductors, battery materials, and critical components to improve operational resilience and reduce production risks.

Investment in battery technology innovation, alternative chemistries, recycling capabilities, and localized production facilities will be essential to address long-term resource security concerns.

Companies should strengthen cybersecurity frameworks, software validation processes, and data protection measures as vehicles become increasingly connected and software dependent.

Strategic partnerships with technology providers, battery manufacturers, charging infrastructure companies, and mobility service operators will remain critical for supporting future growth and innovation.

Automakers must maintain regulatory readiness by continuously adapting to evolving emission standards, vehicle safety regulations, sustainability requirements, and regional compliance frameworks.

Advanced manufacturing technologies, digital supply chain management systems, and predictive analytics tools can help improve production efficiency, inventory management, and risk mitigation capabilities.

Global Automotive Market Risk Factors & Disruption Threats Forward Outlook

Looking ahead to 2026???2033, the Global Automotive Market is expected to undergo one of the most significant transformations in its history as electrification, automation, connectivity, and sustainable mobility solutions become central industry priorities.

Regulatory requirements are expected to become increasingly stringent, particularly regarding carbon emissions, battery sustainability, vehicle safety technologies, and environmental reporting standards. Manufacturers that proactively invest in compliance and innovation will be better positioned to maintain competitiveness.

Supply chain resilience will remain a strategic priority as companies seek greater control over battery materials, semiconductor sourcing, and regional manufacturing capabilities.

Cybersecurity and software reliability will become increasingly important as connected and autonomous vehicle adoption expands globally. Robust digital security frameworks will be essential for protecting consumer data and vehicle systems.

Sustainability initiatives, including battery recycling, circular manufacturing models, renewable energy integration, and responsible sourcing practices, are expected to gain greater importance throughout the automotive value chain.

Overall, the market will remain highly growth-oriented but increasingly influenced by technological disruption, regulatory evolution, resource availability, and shifting mobility preferences. Long-term industry leaders will be defined by their ability to successfully manage electrification, digital transformation, supply chain resilience, and sustainability objectives while maintaining profitability and consumer trust.

Regulatory Landscape

Global Automotive Market Regulatory & Policy Environment Overview

The regulatory and policy environment governing the Global Automotive Market is undergoing significant transformation as governments, transportation authorities, environmental agencies, and safety regulators implement policies aimed at reducing emissions, improving vehicle safety, accelerating electrification, and supporting sustainable mobility solutions. Regulatory frameworks increasingly influence vehicle design, manufacturing processes, fuel efficiency standards, autonomous driving deployment, and connected vehicle technologies.

Automotive manufacturers, component suppliers, mobility service providers, battery producers, and technology companies must comply with a broad range of regulations related to vehicle safety, emissions control, cybersecurity, data privacy, battery management, and environmental sustainability. Regulatory compliance has become a critical factor influencing product development strategies, capital investments, and market competitiveness.

The rapid adoption of electric vehicles (EVs), connected transportation systems, and autonomous driving technologies is encouraging policymakers to modernize automotive regulations while balancing innovation, consumer safety, environmental objectives, and infrastructure development requirements.

Global Automotive Market Regulatory & Policy Environment Current Scenario

The current regulatory landscape is primarily driven by increasingly stringent emission standards and fuel economy requirements aimed at reducing greenhouse gas emissions and improving air quality. Governments across major automotive markets are introducing stricter regulations that encourage the adoption of low-emission and zero-emission vehicles.

Electric vehicle incentive policies continue to play a major role in market development. Financial incentives, tax credits, vehicle purchase subsidies, and charging infrastructure investments are supporting EV adoption and accelerating the transition toward sustainable transportation systems.

Vehicle safety regulations remain a critical focus area as authorities implement stricter standards governing crash protection, advanced driver assistance systems (ADAS), pedestrian safety, occupant protection technologies, and vehicle performance requirements.

Connected vehicle and autonomous driving regulations are evolving rapidly to address cybersecurity risks, software reliability, data privacy concerns, and operational safety standards associated with increasingly digitalized transportation systems.

In parallel, battery manufacturing regulations and supply chain sustainability requirements are becoming increasingly important as governments seek to secure critical mineral supplies, promote responsible sourcing practices, and strengthen circular economy initiatives for battery recycling and reuse.

Key Regulatory & Policy Environment Signals in Global Automotive Market

- Emission Standards & Carbon Reduction Policies:

Regulations targeting reductions in vehicle emissions, fuel consumption, and greenhouse gas output across automotive fleets. - Fuel Economy Regulations:

Requirements encouraging improved vehicle efficiency, reduced energy consumption, and adoption of alternative propulsion technologies. - Electric Vehicle Incentive Programs:

Government policies supporting EV adoption through subsidies, tax incentives, charging infrastructure development, and procurement initiatives. - Vehicle Safety & ADAS Requirements:

Standards governing crashworthiness, occupant protection, advanced safety technologies, and road safety performance. - Autonomous Vehicle & Connected Mobility Regulations:

Frameworks addressing testing, deployment, cybersecurity, software validation, and operational safety of autonomous and connected vehicles. - Battery Supply Chain & Sustainability Regulations:

Policies promoting responsible sourcing, battery recycling, environmental compliance, and circular economy practices.

Strategic Implications of Regulatory & Policy Environment

The evolving regulatory environment is encouraging automotive manufacturers to accelerate investments in electric vehicle platforms, battery technologies, low-emission propulsion systems, and next-generation mobility solutions. Regulatory readiness is increasingly becoming a competitive differentiator across global automotive markets.

Emission and fuel economy regulations are driving substantial capital allocation toward electrification programs, lightweight materials, energy-efficient vehicle architectures, and alternative fuel technologies.

Vehicle safety requirements are encouraging manufacturers to integrate advanced driver assistance systems, collision avoidance technologies, and intelligent safety solutions across a broader range of vehicle categories.

Connected vehicle and autonomous driving regulations are increasing investment in software development, cybersecurity infrastructure, artificial intelligence systems, and vehicle communication technologies to ensure regulatory compliance and consumer trust.

Sustainability regulations are prompting industry participants to strengthen responsible sourcing programs, improve battery recycling capabilities, and implement environmentally responsible manufacturing practices throughout the automotive value chain.

Global Automotive Market Regulatory & Policy Environment Forward Outlook

Between 2026 and 2033, the regulatory environment for the Global Automotive Market is expected to become increasingly comprehensive as governments pursue ambitious climate targets, transportation modernization strategies, and road safety initiatives.

Emission standards are likely to become more stringent, accelerating the transition toward electric mobility, alternative fuel vehicles, and carbon-neutral transportation systems. Regulatory support for charging infrastructure and clean mobility ecosystems is expected to expand significantly.

Autonomous vehicle regulations are anticipated to mature further, providing clearer frameworks for large-scale deployment, software certification, operational safety monitoring, and liability management.

Battery sustainability regulations are expected to strengthen oversight of raw material sourcing, recycling requirements, lifecycle management, and environmental reporting across global battery supply chains.

Overall, the future regulatory landscape will be defined by the convergence of emission standards, fuel economy regulations, EV incentive policies, autonomous vehicle frameworks, cybersecurity requirements, and sustainability mandates. Companies capable of delivering safe, compliant, connected, and environmentally responsible mobility solutions will be best positioned to capitalize on long-term opportunities within the evolving global automotive industry.