Global Light Commercial Vehicle Tyres Market size and share Analysis 2026-2033

Global Light Commercial Vehicle Tyres Market Forecast Snapshot (2026???2033)

| Metric | Value |

|---|---|

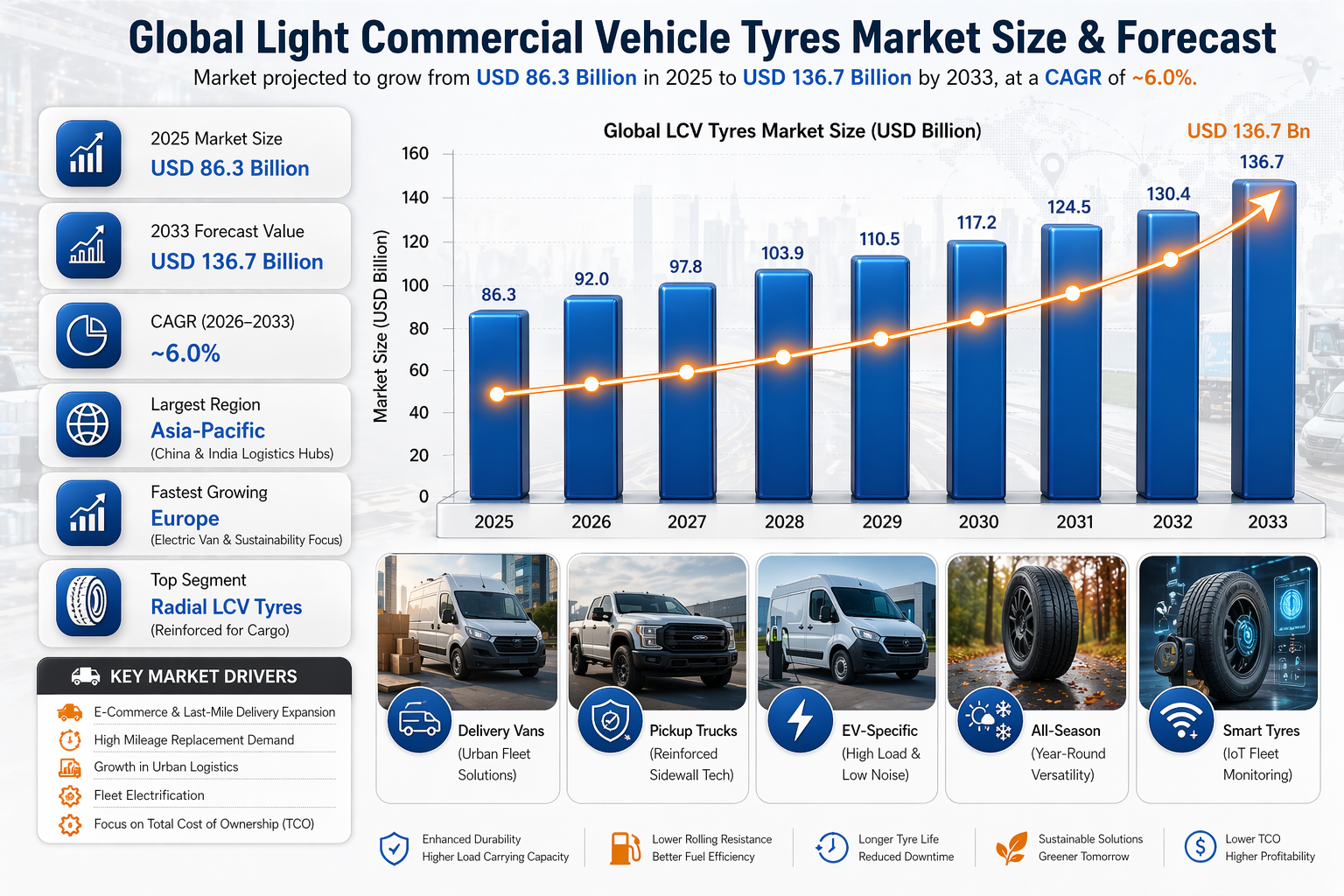

| 2025 Market Size | USD 86.3 Billion |

| 2033 Market Size | USD 136.7 Billion |

| CAGR (2026???2033) | ~6.0% |

| Largest Region | Asia-Pacific |

| Fastest-Growing Region | Europe |

| Largest Segment | Radial LCV tyres |

| Fastest-Growing Segment | EV-specific LCV tyres |

| Key Trend | Durable, fuel-efficient & fleet-optimized tyres |

Global Light Commercial Vehicle Tyres Market Overview

The Global Light Commercial Vehicle Tyres Market is all about tyres for vans, pickups, and other workhorses . They are built tough to handle heavy loads, crazy driving, and all sorts of roads - perfect for businesses that keep things moving. Whether it's delivering goods, transporting people, or supporting construction sites, these tyres are designed to take the beating and keep going . They're all about durability, safety, and keeping costs down, which is music to businesses' ears.

LCV tyres differ from passenger car tyres due to reinforced carcass construction, stronger sidewalls, higher ply ratings, and optimized tread patterns designed for commercial usage intensity. The Global Light Commercial Vehicle Tyres Market includes original equipment manufacturer (OEM) tyres fitted on new vehicles and a dominant aftermarket segment driven by high mileage accumulation and regular replacement cycles.

The Global Light Commercial Vehicle Tyres Market is expanding steadily, supported by rapid growth in e-commerce, last-mile delivery services, urban logistics, and infrastructure development. Electrification of commercial fleets is further reshaping tyre demand, with electric LCVs requiring tyres with higher load capacity, lower rolling resistance, improved durability, and reduced noise.

According to the Pheonix Demand Forecast Engine, the Global Light Commercial Vehicle Tyres Market size is estimated at USD 86.3 billion in 2025 and is projected to reach USD 136.7 billion by 2033, growing at a CAGR of ~6.0% during the forecast period (2026???2033).

Asia-Pacific is the largest market due to high vehicle production and replacement volumes in China and India, while Europe is the fastest-growing region driven by electric vans, fleet modernization, and sustainability regulations.

Key Drivers of Global Light Commercial Vehicle Tyres Market Growth

Expansion of E-Commerce & Last-Mile Delivery

The online shopping boom is fueling demand for delivery vans, and that means more tyres are needed . With all the stop-and-go driving, tyre replacement is a regular thing, driving growth in the aftermarket.

Strong Replacement Demand

Delivery vans are clocking in high mileage and carrying heavy loads, so tyres don't last forever . That means aftermarket tyre sales are booming, driving growth in the market.

Growth in Urban Logistics & Infrastructure Development

LCVs are the backbone of construction, utilities, and municipal services . They're always on the go, so these industries need tyres that can keep up - fuelling demand for tough, reliable tyres.

Fleet Electrification

Electric LCVs are the new kids on the block, and they need tyres that match their vibe . That means specialized tyres with higher load ratings, low rolling resistance, and quieter rides - perfect fit for these eco-friendly workhorses.

Cost & Efficiency Focus by Fleet Operators

Commercial fleets are all about saving money and reducing waste . That's why they're looking for tyres that last longer, save fuel, and can be retreaded - driving growth in the market.

Global Light Commercial Vehicle Tyres Market Segmentation

1. By Tyre Construction

1.1 Radial Tyres (Largest Segment)

1.1.1 Steel-Belted Radial Tyres

??? Single steel belt

??? Double steel belt

??? Multi-layer steel belt

1.1.2 Fabric-Belted Radial Tyres

??? Polyester radial tyres

??? Nylon radial tyres

1.2 Bias (Cross-Ply) Tyres

1.2.1 Nylon bias tyres

1.2.2 Polyester bias tyres

2. By Vehicle Category

2.1 Light Commercial Vans (Largest Segment)

2.1.1 Cargo vans

2.1.2 Panel vans

2.1.3 Passenger vans

2.2 Pickup Trucks

2.2.1 Single-cab pickups

2.2.2 Double-cab pickups

2.3 Mini-Trucks & Compact LCVs

2.3.1 Urban delivery trucks

2.3.2 Small payload carriers

2.4 Electric Light Commercial Vehicles (Fastest-Growing)

2.4.1 Battery electric vans

2.4.2 Electric mini-trucks

3. By Seasonality

3.1 Summer Tyres

3.1.1 Highway summer tyres

3.1.2 Performance summer tyres

3.2 Winter Tyres

3.2.1 Studded winter tyres

3.2.2 Studless winter tyres

3.3 All-Season Tyres (Largest Segment)

3.3.1 Standard all-season tyres

3.3.2 Heavy-duty all-season tyres

4. By Sales Channel

4.1 OEM (Original Equipment Manufacturer)

4.1.1 Van OEM fitment

4.1.2 Pickup & electric LCV OEM fitment

4.2 Aftermarket / Replacement (Largest Segment)

4.2.1 Authorized dealer networks

4.2.2 Independent commercial tyre retailers

4.2.3 Fleet service providers

4.2.4 Online & e-commerce platforms

5. By Rim Size

5.1 Below 14 Inches

5.1.1 Mini-trucks

5.1.2 Entry-level urban vans

5.2 14???16 Inches (Largest Segment)

5.2.1 Cargo vans

5.2.2 Pickup trucks

5.3 Above 16 Inches (Fastest-Growing)

5.3.1 Heavy-duty vans

5.3.2 Electric LCVs

6. By Tyre Technology

6.1 Conventional Pneumatic Tyres

6.2 Low Rolling Resistance Tyres

6.2.1 Fuel-efficient compound tyres

6.2.2 EV-optimized LCV tyres

6.3 Run-Flat Tyres

6.3.1 Self-supporting run-flat tyres

6.3.2 Support-ring run-flat tyres

6.4 High-Durability & Retreadable Tyres

6.4.1 Reinforced carcass tyres

6.4.2 Multiple-life retread tyres

6.5 Smart & Connected Tyres

6.5.1 Embedded pressure & temperature sensors

6.5.2 Fleet-based tyre monitoring systems

7. By Geography

7.1 Asia-Pacific (Largest Region)

China

India

Japan

South Korea

Southeast Asia

7.2 Europe (Fastest-Growing)

Germany

France

U.K.

Italy

7.3 North America

U.S.

Canada

7.4 Latin America

Brazil

Mexico

7.5 Middle East & Africa

Regional Insights of Global Light Commercial Vehicle Tyres Market

Asia-Pacific ??? Largest Market

High LCV production, expanding logistics networks, and strong replacement demand in China and India.

Europe ??? Fastest-Growing Region

Electric van adoption, strict emissions regulations, and fleet efficiency initiatives drive growth.

North America

Large pickup truck parc, mature aftermarket, and strong fleet operations.

Latin America & Middle East & Africa

Infrastructure development and rising commercial vehicle usage support steady demand.

Global Light Commercial Vehicle Tyres Market Forecast Snapshot (2025???2033)

| Metric | Value |

|---|---|

| 2025 Market Size | USD 86.3 Billion |

| 2033 Market Size | USD 136.7 Billion |

| CAGR (2026???2033) | ~6.0% |

| Largest Region | Asia-Pacific |

| Fastest-Growing Region | Europe |

| Largest Segment | Radial LCV tyres |

| Fastest-Growing Segment | EV-specific LCV tyres |

| Key Trend | Durable, fuel-efficient & fleet-optimized tyres |

Strategic Intelligence & Pheonix AI-Backed Insights

Pheonix Demand Forecast Engine:

Analyzes LCV parc expansion, e-commerce???driven mileage intensity, replacement cycles, and urban logistics growth, confirming aftermarket demand as the primary revenue engine.

EV Tyre Requirement Analyzer:

Tracks rising demand for high-load, low rolling resistance, and low-noise tyres driven by electric vans and fleet electrification programs.

Fleet Cost Optimization Model:

Highlights strong preference for long-life, fuel-efficient, and retreadable tyres to reduce total cost of ownership (TCO) for commercial fleets.

Raw Material Sensitivity Model:

Monitors natural rubber, carbon black, steel cord, and oil price volatility impacting LCV tyre pricing and margins.

Automated Porter???s Five Forces (Concise)

Buyer Power: Moderate ??? fleet contracts balanced by fragmented aftermarket

Supplier Power: Moderate ??? reliance on rubber and petrochemical inputs

Threat of New Entrants: Low ??? capital-intensive manufacturing and OEM approvals

Threat of Substitutes: Low ??? tyres are essential consumables

Competitive Rivalry: High ??? global majors and regional players compete on durability and cost efficiency

Leading Companies in the Global Light Commercial Vehicle Tyres Market

Michelin

Bridgestone Corporation

Goodyear Tire & Rubber Company

Continental AG

Pirelli & C. S.p.A.

Sumitomo Rubber Industries

Hankook Tire

Yokohama Rubber Company

Toyo Tires

Apollo Tyres

Michelin and Bridgestone Corporation are the largest company in the Global Light Commercial Vehicle Tyres Market.

Why the Light Commercial Vehicle Tyres Market Is Critical

The Global Light Commercial Vehicle Tyres Market is a big deal . It's critical because logistics, deliveries, and services rely on these tyres to keep things moving. High mileage means tyres wear out fast, creating steady demand. Tyres directly impact costs and fuel efficiency - that's money talking . Plus, they're crucial for making electric commercial vehicles more sustainable. It's a market that's always on the go, playing a vital role in keeping businesses running smoothly.

Final Takeaway of the Global Light Commercial Vehicle Tyres Market

The Global Light Commercial Vehicle Tyres Market is a structurally strong and steadily expanding market supported by logistics growth, urbanization, and fleet electrification. Replacement demand remains the backbone of revenues, while EV-optimized, durable, and smart tyre solutions represent the next wave of opportunity. Manufacturers that focus on total cost of ownership, fleet partnerships, and advanced tyre technologies will remain competitive through 2033.

Competitive Landscape

Global Light Commercial Vehicle Tyres Market Competitive Intensity & Market Structure Overview

The Global Light Commercial Vehicle (LCV) Tyres Market exhibits a moderately consolidated structure combined with high competitive intensity, driven by the presence of global Tier 1 manufacturers and a wide base of regional and local players. This market structure is shaped by high-volume demand from logistics, e-commerce, and fleet operations, alongside strong replacement cycles that continuously attract competition across both premium and value segments. Approximately five to six Tier 1 players’including Michelin, Bridgestone Corporation, Goodyear Tire & Rubber Company, Continental AG, and Pirelli & C. S.p.A. dominate the competitive landscape. These companies leverage large-scale production capabilities, advanced R&D, strong OEM relationships, and global distribution networks to maintain leadership positions. Their strategic focus is increasingly aligned toward EV-specific LCV tyres, fuel-efficient designs, and smart tyre technologies tailored for fleet optimization. The market also includes strong Tier 2 and regional players such as Hankook Tire, Yokohama Rubber Company, Toyo Tires, Sumitomo Rubber Industries, and Apollo Tyres, which intensify competition through cost-effective offerings, localized manufacturing, and aggressive aftermarket expansion. Their ability to cater to price-sensitive markets and regional fleet requirements strengthens overall competitive pressure. High competitive intensity is further reinforced by the dominance of the aftermarket segment, where frequent tyre replacement due to heavy usage, high mileage, and load-bearing requirements creates continuous demand. This results in ongoing price competition, brand switching, and distribution-driven rivalry across global and regional markets.

Global Light Commercial Vehicle Tyres Market Competitive Intensity & Market Structure Current Scenario

Leading Company Profiles

Michelin: Global leader in premium LCV tyres with strong focus on durability, fuel efficiency, and EV-compatible tyre solutions. Bridgestone Corporation: Leading OEM supplier with a broad portfolio of high-performance and long-life commercial tyres. Goodyear Tire & Rubber Company: Specializes in fleet-focused tyre solutions and smart tyre monitoring systems. Continental AG: Focuses on safety, efficiency, and connected tyre technologies for commercial fleets. Pirelli & C. S.p.A.: Premium tyre manufacturer with growing presence in high-performance and electric LCV segments. Sumitomo Rubber Industries: Strong presence in cost-efficient and durable LCV tyres, particularly in Asia-Pacific. Hankook Tire: Expanding global footprint with value-driven and performance-oriented LCV tyre offerings. Yokohama Rubber Company: Known for robust commercial tyre solutions with strong aftermarket penetration. Toyo Tires: Focuses on durable and high-load capacity tyres for commercial and logistics applications. Apollo Tyres: Key regional player with competitive pricing and growing presence in emerging markets.

Key Competitive Intensity & Market Structure Signals in Light Commercial Vehicle Tyres

The dominance of the aftermarket segment is a primary signal shaping market dynamics. High mileage accumulation and frequent replacement cycles in delivery vans and pickups create a continuous demand environment, intensifying competition among manufacturers and distributors. Fleet electrification is another critical signal transforming the competitive landscape. Electric LCVs require tyres with higher load capacity, lower rolling resistance, and reduced noise, pushing companies to innovate rapidly and differentiate through EV-specific product lines. OEM partnerships remain a strategic battleground, as tyre manufacturers compete to secure long-term supply agreements with vehicle producers. These partnerships provide volume stability but also create high entry barriers for smaller players. Price sensitivity among fleet operators significantly influences competition. Businesses prioritize total cost of ownership (TCO), driving demand for durable, retreadable, and fuel-efficient tyres, thereby intensifying competition on both performance and cost efficiency. Technological advancements such as smart tyre systems, predictive maintenance solutions, and connected fleet monitoring are emerging as key differentiators, particularly in developed markets.

Strategic Implications of Competitive Intensity & Market Structure

Innovation in durability, fuel efficiency, and EV compatibility has become essential for maintaining competitive advantage. Companies investing in advanced materials and smart technologies are better positioned to capture future demand. The strong aftermarket dependency requires companies to build extensive distribution networks and strengthen dealer and fleet relationships to ensure consistent revenue streams. Tier 1 players are expected to continue expanding through strategic acquisitions, partnerships, and capacity enhancements, while Tier 2 players focus on regional dominance and cost leadership strategies. Fleet-centric solutions, including tyre leasing, predictive maintenance, and lifecycle management, are emerging as key competitive strategies to enhance customer retention and profitability.

Global Light Commercial Vehicle Tyres Market Competitive Intensity & Market Structure Forward Outlook

The market is expected to remain highly competitive, with global leaders maintaining dominance while regional players continue to expand their footprint in emerging markets. Consolidation is likely as companies pursue acquisitions to strengthen technological capabilities and geographic reach. EV-specific tyre innovation will accelerate, becoming a central focus area as electric commercial fleets expand globally. Manufacturers that align product development with electrification trends will gain a significant competitive edge. The aftermarket segment will continue to drive revenue growth, supported by rising logistics activity and increasing vehicle utilization rates. However, pricing pressure and competition will remain intense. Overall, the market will evolve into a technology-driven and fleet-centric ecosystem, where durability, efficiency, and smart capabilities define long-term success and competitive leadership.

Value Chain

Global Light Commercial Vehicle (LCV) Tyres Market Value Chain & Supply Chain Evolution Overview

The value chain and supply chain dynamics within the Global Light Commercial Vehicle (LCV) Tyres Market play a critical role in determining production efficiency, cost optimization, and competitive positioning. The market operates through an integrated ecosystem comprising raw material suppliers, tyre manufacturers, OEM partnerships, distribution networks, and aftermarket service providers. This interconnected structure ensures efficient product movement from manufacturing units to end users across both OEM and replacement channels.

The supply chain complexity is driven by the diverse range of raw materials required, including natural rubber, synthetic rubber, carbon black, silica, steel cords, and advanced chemical compounds. Leading players such as Michelin, Bridgestone Corporation, Goodyear Tire & Rubber Company, and Continental AG maintain strategic sourcing partnerships and long-term contracts to manage price volatility and ensure consistent supply quality.

Manufacturing in the LCV tyres segment involves advanced processes such as reinforced carcass construction, tread pattern optimization, compounding, molding, curing, and durability testing. The increasing focus on load-bearing capacity, fuel efficiency, long lifecycle performance, and EV compatibility has significantly enhanced manufacturing complexity and technological requirements.

Distribution follows a dual-channel model, with OEM supply for new vehicle fitment and a dominant aftermarket segment driven by high mileage usage and frequent replacement cycles. The aftermarket channel includes authorized dealers, independent retailers, fleet service providers, and digital B2B platforms.

Supply chain challenges include fluctuations in raw material prices, logistics disruptions, regulatory compliance pressures, and rising costs associated with R&D investments in EV-specific and fuel-efficient tyre technologies. These factors continue to influence pricing strategies and margin structures across the industry.

Global Light Commercial Vehicle (LCV) Tyres Market Value Chain & Supply Chain Evolution Current Scenario

The Global LCV Tyres Market is currently witnessing a stable yet evolving supply chain environment, driven by rapid expansion in e-commerce, urban logistics, and fleet operations. At the upstream level, volatility in natural rubber and petrochemical-derived inputs continues to impact cost structures, prompting manufacturers to adopt hedging strategies and diversified sourcing approaches.

Manufacturers such as Michelin, Bridgestone, and Goodyear are increasingly focusing on developing advanced LCV tyre solutions with enhanced durability, low rolling resistance, and EV compatibility. Innovations targeting improved load capacity and extended tyre life are becoming critical differentiators in the market.

OEM partnerships remain important, particularly with the rise of electric vans and fleet modernization initiatives. However, the aftermarket segment continues to dominate due to predictable replacement demand driven by high mileage accumulation and intensive usage patterns.

Distribution channels are undergoing digital transformation, with increasing adoption of online procurement platforms, fleet management solutions, and integrated service models. These developments are improving accessibility and operational efficiency across the supply chain.

Aftermarket services such as tyre installation, retreading, fleet maintenance, and tyre monitoring systems are gaining prominence as value-added offerings, enhancing revenue streams for both manufacturers and distributors.

Key Value Chain & Supply Chain Evolution Signals in Global Light Commercial Vehicle (LCV) Tyres Market

Several key trends are shaping the evolution of the LCV tyres value chain. First, the rapid growth of e-commerce and last-mile delivery is increasing demand for durable, high-mileage tyres, strengthening the aftermarket segment.

Second, fleet electrification is driving demand for specialized LCV tyres with higher load capacity, lower rolling resistance, and reduced noise levels, particularly for electric vans and urban delivery vehicles.

Third, cost optimization remains a priority for fleet operators, increasing demand for long-life, retreadable, and fuel-efficient tyres that reduce total cost of ownership.

Fourth, raw material price volatility continues to challenge manufacturers, encouraging the adoption of alternative materials, recycling initiatives, and circular economy practices.

Finally, digital transformation, including IoT-enabled tyre monitoring and predictive maintenance systems, is enhancing supply chain efficiency, inventory management, and fleet performance optimization.

Strategic Implications of Value Chain & Supply Chain Evolution in Global Light Commercial Vehicle (LCV) Tyres Market

Leading companies such as Michelin, Bridgestone, Continental, and Goodyear leverage their global manufacturing footprint, strong supplier networks, and advanced R&D capabilities to maintain competitive advantage in the LCV tyres market.

The increasing complexity of product innovation, regulatory requirements, and OEM approvals creates significant entry barriers, leading to market consolidation and reinforcing the dominance of established players.

Distributors and retailers are shifting toward integrated service models, including fleet management solutions, retreading services, and digital platforms, to enhance profitability and customer retention.

Cost efficiency and supply chain resilience remain strategic priorities as manufacturers balance rising input costs with investments in advanced and EV-compatible tyre technologies.

The transition toward electric commercial fleets presents both growth opportunities and operational challenges, requiring continuous innovation in tyre design, materials, and performance capabilities.

Global Light Commercial Vehicle (LCV) Tyres Market Value Chain & Supply Chain Evolution Forward Outlook

Between 2026 and 2033, the LCV tyres value chain is expected to undergo significant transformation driven by fleet electrification, digitalization, and evolving logistics requirements.

Manufacturers will increasingly focus on sustainability through the use of eco-friendly materials, energy-efficient production processes, and expansion of retreading and recycling practices.

The aftermarket segment will continue to dominate, supported by high vehicle utilization rates and consistent replacement cycles, while digital sales and service platforms will expand rapidly.

Supply chain resilience will remain a key focus area, with companies investing in diversified sourcing strategies, localized production, and advanced supply chain management technologies.

Overall, the future value chain will be shaped by durability, efficiency, electrification, and digital integration, with companies that align with fleet-centric requirements expected to gain long-term competitive advantage.

Market-Specific Value Chain

- Raw Material Procurement: Natural rubber, synthetic rubber, carbon black, silica, steel cords sourcing

- Research & Development: Load optimization, durability engineering, EV-compatible LCV tyre development

- Manufacturing: Reinforced construction, compounding, molding, curing, and testing

- OEM Integration: Supply of tyres for vans, pickups, and electric LCVs

- Distribution & Retail: Dealer networks, fleet service providers, independent retailers, e-commerce platforms

- Aftermarket Services: Installation, replacement, retreading, fleet maintenance, tyre monitoring

Company-to-Stage Mapping

- Raw Material Procurement: Michelin, Bridgestone Corporation, Continental AG, Goodyear Tire & Rubber Company

- Research & Development: Michelin, Continental AG, Pirelli & C. S.p.A., Hankook Tire

- Manufacturing: Bridgestone Corporation, Goodyear Tire & Rubber Company, Yokohama Rubber Company, Hankook Tire

- OEM Integration: Michelin, Bridgestone Corporation, Continental AG, Apollo Tyres

- Distribution & Retail: Goodyear Tire & Rubber Company, Apollo Tyres, Toyo Tires, Yokohama Rubber Company

- Aftermarket Services: Michelin, Bridgestone Corporation, Goodyear Tire & Rubber Company, Continental AG

Investment Activity

Global Light Commercial Vehicle Tyres Market Investment & Funding Dynamics Overview

Investment and funding dynamics in the Global Light Commercial Vehicle (LCV) Tyres Market are strongly influenced by rapid expansion in e-commerce, last-mile delivery ecosystems, and increasing fleet utilization across urban logistics and infrastructure sectors. Between 2026 and 2033, capital allocation is expected to focus on high-durability tyre designs, fuel-efficient compounds, and EV-compatible technologies tailored for intensive commercial usage. The market reflects a moderately high capital intensity profile due to the need for reinforced tyre construction, advanced material engineering, and continuous production scale optimization. LCV tyres require stronger carcass structures, higher load-bearing capabilities, and longer lifecycle performance, driving consistent investment in R&D and manufacturing upgrades. Leading players such as Michelin, Bridgestone, Goodyear, Continental AG, and Pirelli are actively investing in expanding fleet-oriented tyre portfolios and strengthening distribution capabilities. A major structural shift shaping investment is fleet electrification. The transition toward electric vans and light commercial vehicles is accelerating funding toward low rolling resistance compounds, noise-reduction technologies, and high-load EV-specific tyre designs. This is pushing capital flows toward innovation strategies that balance durability, efficiency, and sustainability.

Global Light Commercial Vehicle Tyres Market Investment & Funding Dynamics Current Scenario

Currently, investment activity is largely driven by the surge in last-mile delivery demand and increasing fleet sizes globally. Manufacturers are expanding production capacity for radial LCV tyres, which dominate the market due to their superior durability, fuel efficiency, and load-handling capabilities. Asia-Pacific remains the largest investment hub, supported by high vehicle production volumes and strong replacement demand in China and India. Companies are focusing on capacity expansion, localized manufacturing, and cost optimization strategies to meet large-scale demand efficiently. In Europe, investment is increasingly directed toward EV-compatible LCV tyres and regulatory compliance. Companies are allocating capital toward low-emission tyre technologies, noise reduction solutions, and advanced tread designs aligned with sustainability mandates. North America continues to attract steady investment due to its large pickup and van parc and mature aftermarket ecosystem. Investment focus remains on premium fleet tyres, durability enhancement, and expanding service networks. Meanwhile, Latin America and the Middle East & Africa are witnessing gradual investment growth driven by infrastructure development and rising commercial vehicle usage. The market’s expansion from USD 86.3 billion in 2025 to USD 136.7 billion by 2033, at a CAGR of ~6.0%, reinforces its position as a stable, replacement-driven investment segment with strong long-term fundamentals.

Key Investment & Funding Dynamics Signals in Global Light Commercial Vehicle Tyres Market

A major investment signal is the continuous rise in e-commerce and urban delivery networks, driving sustained demand for high-performance LCV tyres and encouraging expansion of manufacturing capacity. Strong replacement demand remains a fundamental driver, as LCV tyres experience high wear due to intensive usage, ensuring recurring revenue streams and attracting consistent capital inflows. Fleet electrification is another critical signal, pushing investment toward EV-specific tyre solutions with enhanced load capacity, reduced rolling resistance, and improved acoustic performance. Increasing focus on total cost of ownership (TCO) by fleet operators is driving funding toward long-life, fuel-efficient, and retreadable tyre technologies. Technological advancements, including smart tyre systems and predictive maintenance solutions, are further shaping investment strategies across the value chain.

Strategic Implications of Investment & Funding Dynamics in Global Light Commercial Vehicle Tyres Market

The investment landscape highlights a competitive market dominated by global tyre manufacturers with strong technological capabilities and economies of scale. High capital requirements and technical complexity act as barriers to entry for new players. The balance between OEM and aftermarket channels remains critical. OEM partnerships ensure consistent volumes, while the aftermarket segment drives higher margins due to frequent replacement cycles in commercial operations. The transition toward EV-compatible tyres is transforming the market into a more innovation-driven segment, increasing the importance of R&D-led capital allocation. Regional diversification plays a key role, with Asia-Pacific driving volume growth, Europe leading regulatory innovation, and North America contributing stable aftermarket demand. Raw material price volatility continues to impact margins, prompting investments in supply chain optimization, alternative materials, and cost management strategies.

Global Light Commercial Vehicle Tyres Market Investment & Funding Dynamics Forward Outlook

Looking ahead, investment trends in the LCV tyres market will remain growth-oriented, supported by expanding logistics networks, increasing vehicle utilization, and ongoing electrification of fleets. Capital deployment will focus on enhancing durability, fuel efficiency, and EV compatibility. Asia-Pacific will continue to dominate investment flows due to its scale and demand intensity, while Europe will lead in sustainability-driven innovation and EV tyre development. North America will maintain steady investment driven by fleet operations and aftermarket demand. Future investment cycles will increasingly prioritize smart tyre technologies, IoT-enabled monitoring systems, and predictive maintenance solutions to enhance fleet efficiency and reduce downtime. Digital transformation and data-driven fleet management will further influence capital allocation, with growing investments in connected tyre ecosystems and analytics platforms. Overall, the Global Light Commercial Vehicle Tyres Market will continue to attract stable and long-term investment due to its essential role in logistics and transportation. Companies that align durability, efficiency, and technological innovation with fleet requirements will be best positioned for sustained growth through 2033.

Technology & Innovation

Global Light Commercial Vehicle Tyres Market Technology & Innovation Landscape Overview

The technology and innovation landscape within the global light commercial vehicle (LCV) tyres market is driven by the need for durability, load-bearing efficiency, fuel optimization, and cost-effective lifecycle performance. Unlike passenger tyres, innovation in this segment is highly utility-focused, aimed at supporting high-mileage operations, frequent stop-and-go driving, and heavy payload conditions typical of logistics, delivery, and service fleets.

Innovation intensity in the market is moderate-to-high, with continuous advancements in radial construction, reinforced carcass design, and tread compound engineering. While core technologies are mature, ongoing improvements in low rolling resistance materials, wear-resistant compounds, and retreadable structures are enhancing tyre longevity and efficiency. Leading manufacturers such as Michelin, Bridgestone Corporation, Goodyear Tire & Rubber Company, Continental AG, and Pirelli & C. S.p.A. are focusing on fleet-optimized tyres, EV-compatible designs, and smart tyre systems.

A major technological shift is the emergence of EV-specific LCV tyres, driven by the electrification of delivery vans and urban fleets. These tyres require higher load capacity, lower rolling resistance, enhanced durability, and reduced noise levels. Additionally, smart tyre technologies are transforming LCV tyres into connected assets capable of real-time monitoring and predictive maintenance, supporting fleet efficiency and safety.

Global Light Commercial Vehicle Tyres Market Technology & Innovation Landscape Current Scenario

Currently, the technology landscape in the global LCV tyres market is centered on improving durability, fuel efficiency, and lifecycle cost performance. Manufacturers are refining tread designs and rubber compounds to enhance mileage, reduce wear, and maintain consistent performance under varying load and road conditions.

Low rolling resistance tyre technology is one of the most critical advancements, helping reduce fuel consumption in conventional vehicles and extend driving range in electric LCVs. Silica-based compounds and optimized tread geometries are widely adopted to minimize energy loss without compromising traction and braking efficiency.

Durability-focused innovation is also prominent, with reinforced sidewalls, stronger carcass structures, and high-ply ratings designed to withstand heavy loads and rough urban operating conditions. Retreadable tyre technologies are gaining traction as fleet operators seek to reduce total cost of ownership through extended tyre life cycles.

Smart and connected tyre technologies are increasingly being integrated into fleet operations. Embedded sensors enable real-time monitoring of pressure, temperature, and wear, allowing predictive maintenance and reducing downtime. These solutions are particularly valuable in logistics and delivery fleets where uptime is critical.

Noise reduction technologies are gaining importance with the growth of electric LCVs, where tyre noise becomes more noticeable. Optimized tread patterns and acoustic solutions are being developed to enhance driver comfort and meet regulatory standards.

Manufacturing innovation is also advancing, with automation, AI-driven quality control, and sustainable production practices improving efficiency and consistency. Use of recycled materials and eco-friendly processes is increasing in response to regulatory and sustainability pressures.

Key Technology & Innovation Landscape Signals in Global Light Commercial Vehicle Tyres Market

- EV-Specific LCV Tyres: Growing demand for tyres designed for electric vans with higher load capacity and energy efficiency.

- Low Rolling Resistance Adoption: Increasing focus on fuel-saving and energy-efficient tyre technologies across fleets.

- High-Durability & Retreadable Designs: Strong emphasis on multi-life tyres to reduce operational costs.

- Smart & Connected Tyres: Integration of IoT-enabled sensors for real-time fleet monitoring and predictive maintenance.

- Reinforced Structural Engineering: Advanced carcass and sidewall designs to support heavy loads and intensive usage.

- Noise Optimization Technologies: Development of quieter tyres, especially for electric LCV applications.

- Sustainability Initiatives: Adoption of recycled materials and energy-efficient manufacturing processes.

Strategic Implications of Technology & Innovation Landscape in Global Light Commercial Vehicle Tyres Market

The evolving technology landscape has significant strategic implications for manufacturers and fleet operators. Continuous investment in R&D is essential to enhance durability, efficiency, and EV compatibility. Companies that deliver high-mileage, low-cost-per-kilometer tyre solutions will gain strong competitive advantage in fleet-driven markets.

The shift toward electric commercial fleets is reshaping product development priorities, requiring tyres with higher load capacity, lower rolling resistance, and improved noise characteristics. This is increasing collaboration between tyre manufacturers and OEMs for EV-specific solutions.

Smart tyre technologies are unlocking new value-added services such as predictive maintenance, fleet analytics, and operational optimization. This enables manufacturers to expand beyond product sales into service-oriented business models.

Sustainability is becoming a key strategic focus, with increasing adoption of circular economy practices, retreading programs, and eco-friendly materials. Companies aligning with environmental regulations and fleet sustainability goals will strengthen their market positioning.

For fleet operators, tyre technology is directly linked to operational efficiency and cost management. Adoption of advanced tyre solutions is critical for reducing fuel consumption, minimizing downtime, and optimizing fleet performance.

Global Light Commercial Vehicle Tyres Market Technology & Innovation Landscape Forward Outlook

Looking ahead, the global LCV tyres market is expected to evolve steadily toward more efficient, durable, and connected tyre solutions. Electrification will remain a major growth driver, increasing demand for EV-optimized tyres with enhanced load handling and energy efficiency.

Smart tyre technologies are expected to become increasingly standard in fleet operations, enabling real-time data integration, AI-driven analytics, and predictive maintenance capabilities. This will significantly improve fleet uptime and operational efficiency.

Material innovation will continue to advance, with development of high-durability compounds, sustainable materials, and improved tread designs that balance performance with environmental impact.

Manufacturing processes will become more automated and digitally integrated, enhancing production efficiency, quality consistency, and scalability. Smart factories and advanced quality systems will accelerate innovation cycles.

In conclusion, the Global Light Commercial Vehicle Tyres Market is undergoing a steady technological transformation where durability, efficiency, and fleet intelligence are the key innovation pillars. Companies that successfully integrate EV compatibility, smart technologies, and cost-efficient solutions will be best positioned to lead the market through 2033.

Market Risk

Global Light Commercial Vehicle Tyres Market Risk Factors & Disruption Threats Overview

The Global Light Commercial Vehicle (LCV) Tyres Market operates within a highly utilization-driven and logistics-dependent environment, where demand is closely tied to e-commerce growth, urban mobility, and fleet operations. The market carries a moderate overall risk profile, supported by strong replacement demand but exposed to cost pressures, fleet dynamics, and technological transitions such as electrification. A major structural risk factor is the volatility of raw material prices, including natural rubber, synthetic rubber, carbon black, and steel reinforcements. Since LCV tyres are produced in high volumes and operate under cost-sensitive fleet contracts, fluctuations in input costs can directly impact manufacturer margins and pricing strategies. Another key disruption driver is the rapid electrification of light commercial fleets. Electric vans and delivery vehicles require tyres with higher load capacity, lower rolling resistance, and enhanced durability. This shift is increasing R&D requirements and accelerating product innovation cycles, creating pressure on manufacturers to continuously upgrade their portfolios. The market is also influenced by intense operational usage patterns. High mileage, stop-and-go driving, and heavy payloads lead to faster wear and tear, which strengthens replacement demand but also increases performance expectations. Failure to deliver durability and cost efficiency can impact brand preference among fleet operators. Additionally, the growing role of organized fleet operators and digital procurement platforms is reshaping distribution dynamics. Large fleets are gaining pricing power and demanding integrated solutions, increasing competitive pressure on tyre manufacturers.

Global Light Commercial Vehicle Tyres Market Risk Factors & Disruption Threats Current Scenario

The current market scenario reflects strong growth driven by e-commerce and last-mile delivery expansion, but it is simultaneously challenged by rising input costs and competitive pricing pressures. Raw material volatility remains a key concern, affecting production economics across global and regional players. Fleet operators are increasingly prioritizing total cost of ownership (TCO), pushing demand toward long-lasting, fuel-efficient, and retreadable tyres. While this supports premiumization, it also intensifies competition, particularly in the high-volume radial tyre segment. Supply chain disruptions and logistics inefficiencies continue to pose short-term risks, especially in sourcing raw materials and managing inventory across regions. These challenges can impact both OEM production schedules and aftermarket availability. The aftermarket segment remains dominant, but digitalization is transforming purchasing behavior. Online platforms and fleet procurement systems are increasing price transparency, reducing dependence on traditional dealer networks, and shifting bargaining power toward large buyers. At the same time, electrification is gaining momentum, particularly in Europe and urban Asia. This is creating parallel demand for EV-specific LCV tyres, increasing complexity in product portfolios and supply chains.

Key Risk Factors & Disruption Threats Signals in Global Light Commercial Vehicle Tyres Market

A key risk signal is the accelerating adoption of electric light commercial vehicles. EVs require specialized tyres with enhanced load-bearing capacity and energy efficiency, pushing manufacturers to invest heavily in innovation and testing capabilities. Raw material price instability continues to act as a persistent structural signal. Dependence on global commodity markets introduces cost uncertainty, particularly in high-volume production environments. Another important signal is the increasing dominance of fleet-based procurement. Large logistics companies are centralizing purchasing decisions, demanding performance guarantees, and negotiating pricing aggressively, which impacts manufacturer margins. Digital transformation is also emerging as a disruption signal. The shift toward online tyre sales, telematics integration, and smart fleet systems is redefining how tyres are marketed, sold, and managed throughout their lifecycle. Finally, sustainability pressures are gaining traction. Regulations around emissions, fuel efficiency, and material usage are driving demand for eco-friendly and low rolling resistance tyres, requiring continuous innovation.

Strategic Implications of Risk Factors & Disruption Threats in Global Light Commercial Vehicle Tyres Market

The evolving risk landscape highlights the need for continuous product innovation focused on durability, efficiency, and EV compatibility. Manufacturers must invest in advanced materials and tread designs to meet changing fleet requirements. Strengthening relationships with fleet operators is becoming increasingly important. Companies must move beyond product sales and offer integrated solutions, including tyre management, monitoring, and lifecycle services. Supply chain resilience is a critical priority. Diversifying sourcing strategies and optimizing regional manufacturing networks can help mitigate risks associated with raw material volatility and global disruptions. Pricing strategies must align with total cost of ownership models. Fleet operators prioritize long-term savings over upfront costs, creating opportunities for premium, high-performance tyre solutions. Digital capabilities are also essential. Investment in e-commerce platforms, connected tyre technologies, and predictive maintenance systems will enhance competitiveness and customer retention.

Global Light Commercial Vehicle Tyres Market Risk Factors & Disruption Threats Forward Outlook

Looking ahead to 2026-2033, the Global Light Commercial Vehicle Tyres Market is expected to maintain steady growth, driven by logistics expansion, urbanization, and fleet electrification. However, the risk environment will become more complex due to technological advancements and evolving procurement models. Electrification will remain the most transformative force, driving demand for EV-specific tyres and reshaping product development priorities. Manufacturers that lead in EV tyre innovation will gain a competitive edge. Sustainability initiatives and regulatory pressures will further influence material selection and manufacturing processes. Eco-friendly and recyclable tyre solutions will become increasingly important. Digital fleet ecosystems will expand, increasing demand for smart tyres and real-time performance monitoring. This will shift competition toward integrated solution providers rather than standalone product manufacturers. Overall, the market will remain structurally strong but moderately risk-exposed, with success dependent on balancing cost efficiency, innovation, and strategic partnerships across the value chain.

Regulatory Landscape

Global Light Commercial Vehicle (LCV) Tyres Market Regulatory & Policy Environment Overview

The regulatory and policy environment governing the Global Light Commercial Vehicle (LCV) Tyres Market plays a critical role in shaping product standards, fleet efficiency, and market competitiveness. Given the commercial nature of LCV operations’characterized by high mileage, heavy loads, and urban usage’regulations focus heavily on safety, durability, fuel efficiency, emissions reduction, and lifecycle performance. These frameworks directly influence tyre design, manufacturing processes, and fleet procurement strategies. Global regulatory systems such as the European Union Tyre Labeling Regulation (EU 2020/740), UNECE standards, and U.S. Department of Transportation (DOT) requirements establish minimum benchmarks for rolling resistance, wet grip, load capacity, and external noise. These standards ensure that LCV tyres deliver reliable performance under demanding operating conditions while contributing to broader environmental and safety objectives. Compliance increases R&D intensity and certification costs, particularly for OEM-approved tyres. Environmental and emissions-related policies are especially influential in this market. Governments worldwide are tightening CO emission norms and promoting fuel-efficient transport systems, driving adoption of low rolling resistance tyres. Additionally, urban noise regulations are encouraging quieter tyre designs, particularly in densely populated cities where LCVs operate extensively. Regional policy diversity adds complexity. Europe leads in sustainability and regulatory enforcement, North America emphasizes safety and durability standards, while Asia-Pacific is rapidly strengthening compliance frameworks to support expanding logistics and infrastructure sectors.

Global Light Commercial Vehicle (LCV) Tyres Market Regulatory & Policy Environment Current Scenario

Currently, the regulatory environment is becoming more stringent, with a strong focus on fleet efficiency, sustainability, and safety. The EU Tyre Labeling Regulation (EU 2020/740) remains a key global benchmark, mandating clear disclosure of fuel efficiency, wet grip, and noise levels. These parameters are particularly important for fleet operators aiming to optimize operating costs and regulatory compliance. In the United States, DOT and NHTSA regulations enforce strict standards for load-bearing capacity, tread durability, and high-mileage performance. These requirements are critical for LCV tyres, which are subjected to continuous usage in logistics and delivery operations. Asia-Pacific markets, including China and India, are strengthening regulatory frameworks through GB standards and BIS certification systems. These initiatives are improving tyre quality and safety compliance while raising entry barriers for substandard products. Sustainability-focused policies are also gaining traction. Governments are promoting electric LCV adoption, fuel efficiency improvements, and circular economy practices such as retreading and recycling. These policies are influencing tyre innovation, particularly in EV-compatible and high-durability tyre segments.

Key Regulatory & Policy Environment Signals in Global Light Commercial Vehicle (LCV) Tyres Market

- EU Tyre Labeling Regulation (EU 2020/740): Drives transparency in fuel efficiency, wet grip, and noise performance.

- UNECE Tyre Standards: Provide global benchmarks for safety, durability, and load capacity.

- U.S. DOT & NHTSA Regulations: Ensure compliance with safety and high-mileage durability requirements.

- China GB & India BIS Standards: Strengthen quality control in high-growth LCV markets.

- CO Emission & Fuel Efficiency Policies: Promote low rolling resistance and energy-efficient tyres.

- Urban Noise & Sustainability Regulations: Encourage quieter, eco-friendly tyre technologies.

Strategic Implications of Regulatory & Policy Environment in Global Light Commercial Vehicle (LCV) Tyres Market

Regulatory compliance creates significant entry barriers, particularly in OEM and fleet supply contracts where certification and performance validation are mandatory. Established global manufacturers benefit from strong R&D capabilities and regulatory expertise, enabling them to maintain market leadership. The increasing focus on fuel efficiency and sustainability is driving innovation in tyre compounds, tread design, and structural reinforcement. Manufacturers are investing in low rolling resistance technologies, high-durability casings, and EV-compatible designs to meet regulatory expectations and fleet requirements. Retreading and lifecycle regulations are shaping market dynamics by promoting extended tyre usage and cost efficiency. Companies offering retreadable tyres gain a competitive advantage in cost-sensitive fleet operations. Regional regulatory differences require flexible compliance strategies, including localized production and multi-certification processes. This increases operational complexity but also enables targeted product positioning across markets. Pricing strategies are influenced by compliance costs and performance requirements. Premium, fuel-efficient, and EV-ready LCV tyres command higher margins due to their ability to reduce total cost of ownership for fleet operators.

Global Light Commercial Vehicle (LCV) Tyres Market Regulatory & Policy Environment Forward Outlook

Between 2026 and 2033, regulatory frameworks are expected to become more stringent and sustainability-focused. Future updates to EU and UNECE standards will likely impose tighter limits on rolling resistance, noise emissions, and material sustainability, driving continuous innovation in LCV tyre technologies. The rapid electrification of commercial fleets will introduce new regulatory requirements focusing on load capacity, energy efficiency, and noise reduction. This will accelerate demand for EV-specific LCV tyres designed for higher weight loads and urban operating conditions. Emerging markets will continue aligning with global regulatory standards, reducing fragmentation while increasing compliance complexity. This will favor multinational tyre manufacturers with strong global certification capabilities. Sustainability will remain a key regulatory priority, with increased emphasis on circular economy practices, retreading expansion, and reduced environmental footprint in tyre manufacturing. Overall, the regulatory environment will act as both a constraint and a catalyst’raising compliance requirements while driving innovation in durability, efficiency, and smart fleet integration. Companies that proactively align with evolving policies will secure long-term competitive advantages in the LCV tyre market.