Global Fleet Management Market Report, Size and Forecast 2026-2033

Global Fleet Management Market Forecast Snapshot: 2026???2033

| Parameter | Value |

|---|---|

| Base Year | 2025 |

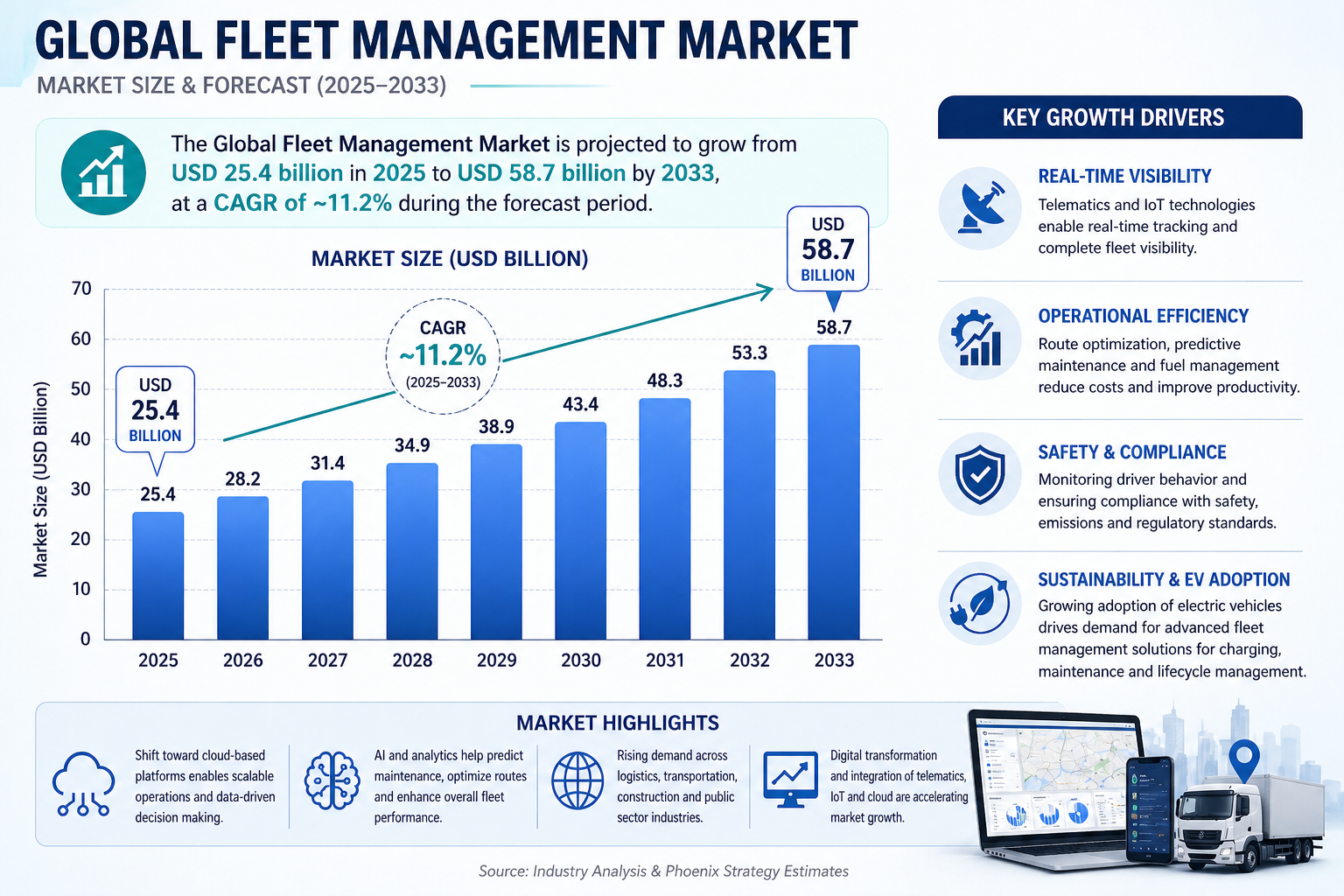

| Base Year Market Size | USD 25.4 Billion |

| Forecast Period | 2026???2033 |

| Forecasted CAGR | ~11.2% |

| Forecasted Market Size (2033) | USD 58.7 Billion |

Market Size & Forecast

The Global Fleet Management Market is projected to grow from USD 25.4 billion in 2025 to approximately USD 58.7 billion by 2033, reflecting a strong CAGR of ~11.2% over the forecast period. This growth is driven by increasing demand for real-time fleet visibility, operational efficiency, and regulatory compliance across transportation, logistics, construction, and public sector industries. A defining structural feature of this market is its transition from traditional fleet tracking to integrated digital platforms combining telematics, IoT, AI, and cloud-based analytics. These systems enable organizations to monitor vehicle performance, optimize routes, reduce fuel consumption, and enhance driver safety. Market expansion is further supported by the global push toward sustainability and electrification. Fleet operators are increasingly adopting electric vehicles (EVs), requiring advanced fleet management solutions for charging, maintenance, and lifecycle optimization. Additionally, rising compliance requirements related to emissions, driver behavior, and safety standards are accelerating adoption of digital fleet management platforms.Market Overview

The Global Fleet Management Market is characterized by high growth, strong technological integration, and increasing adoption across both commercial and passenger fleet segments. The market operates through a combination of software platforms, hardware devices (telematics and GPS), and value-added services. Fleet management solutions encompass a wide range of functionalities, including vehicle tracking, fuel management, driver monitoring, predictive maintenance, and compliance management. These capabilities are becoming essential for improving operational efficiency and reducing total cost of ownership (TCO). Technological innovation is a key differentiator, with cloud-based platforms, AI-driven analytics, and IoT-enabled devices transforming traditional fleet operations into data-driven ecosystems. Regionally, North America leads the market due to early adoption and technological maturity, while Asia-Pacific is the fastest-growing region driven by rapid digitalization, expanding logistics networks, and increasing vehicle fleets.Structural Drivers of Market Growth

- Rising Adoption of Telematics & IoT Real-time tracking, predictive maintenance, and improved driver performance are driving widespread adoption of telematics solutions.

- Fuel & Cost Optimization Fleet operators are increasingly focusing on reducing fuel consumption and operational costs through data-driven insights.

- Regulatory Compliance Requirements Stringent government regulations on vehicle safety, emissions, and driver working hours are accelerating adoption of compliance-focused fleet systems.

- Digital Transformation & Cloud Adoption Integration of AI, machine learning, and cloud-based platforms is enhancing scalability, efficiency, and decision-making.

- EV & Autonomous Fleet Integration Growing adoption of electric and autonomous vehicles is creating demand for advanced fleet management solutions.

Market Segmentation Analysis

Top-Level Segment Share Split

- By Component: 30%

- By Deployment Mode: 20%

- By Fleet Type: 20%

- By End-User Industry: 20%

- By Region: 10%

Regional Market Dynamics

- North America ??? Largest Market Driven by early adoption of telematics, strong regulatory frameworks, and advanced technological infrastructure.

- Europe Growth supported by sustainability initiatives, EV adoption, and strict safety and environmental regulations.

- Asia-Pacific ??? Fastest Growing Region Rapid growth driven by expanding logistics and e-commerce sectors, urbanization, and digital transformation in countries like China and India.

- Latin America Steady growth supported by modernization of transportation infrastructure and fleet operations.

- Middle East & Africa Increasing adoption of fleet digitalization and smart transport initiatives led by government investments.

Competitive Landscape

The Global Fleet Management Market includes leading players such as:- Geotab Inc.

- Trimble Inc.

- Verizon Connect

- Samsara Inc.

- Teletrac Navman

- MiX Telematics

- Omnitracs LLC

- TomTom Telematics

- AT&T Inc.

- Fleet Complete

Strategic Outlook

- AI-Driven Fleet Optimization Advanced analytics will enhance predictive maintenance, route optimization, and driver safety.

- Cloud & Mobility Integration Cloud-based platforms will enable scalable, real-time fleet management across geographies.

- EV Fleet Management Solutions Development of specialized tools for EV charging infrastructure, battery monitoring, and lifecycle management.

- Autonomous Fleet Readiness Preparation for integration of autonomous vehicles into fleet ecosystems.

Final Market Perspective

The Global Fleet Management Market is undergoing a rapid transformation driven by digitalization, sustainability, and evolving mobility trends. Its role in improving operational efficiency, reducing costs, and ensuring compliance makes it a critical component of modern transportation ecosystems. The shift toward connected, intelligent, and electric fleets is redefining competitive dynamics, with data-driven platforms becoming central to fleet operations. Companies that leverage AI, cloud technologies, and EV integration will be best positioned to capture long-term growth.Research Methodology

This study adopts a comprehensive mixed-methods research approach integrating primary and secondary data sources. Primary research includes insights from fleet operators, technology providers, OEMs, and industry experts, providing real-time understanding of market trends and adoption patterns. Secondary research involves triangulation of data from industry reports, regulatory frameworks, technology databases, and economic analyses to ensure accurate market sizing and forecasting. This methodology provides a robust and reliable foundation for strategic decision-making within the Global Fleet Management Market ecosystem.Table of Contents

Executive Summary

1.1 Market Forecast Snapshot (2026???2033)

1.2 Global Market Size & CAGR Analysis

1.3 Largest & Fastest-Growing Segments

1.4 Region-Level Leadership & Growth Trends

1.5 Key Market Drivers

1.6 Competitive Landscape Overview

1.7 Strategic Outlook Through 2033

Introduction & Market Overview

1.1 Definition of the Global Fleet Management Market

1.2 Scope of the Study

1.3 Industry Evolution & Market Development

1.4 Supply Chain & Distribution Infrastructure

1.5 Impact of Digital Transformation & Mobility Trends

1.6 Regulatory & Compliance Landscape

1.7 Technology & Innovation Landscape

Research Methodology

1.1 Primary Research

1.2 Secondary Research

1.3 Market Size Estimation Model

1.4 Forecast Assumptions (2026???2033)

1.5 Data Validation & Triangulation

Market Dynamics

1.1 Drivers

1.1.1 Rising Adoption of Telematics & IoT

1.1.2 Fuel & Cost Optimization Requirements

1.1.3 Regulatory Compliance & Safety Mandates

1.1.4 Digital Transformation & Cloud Adoption

1.1.5 EV & Autonomous Fleet Integration

1.2 Restraints

1.2.1 High Initial Implementation Costs

1.2.2 Data Privacy & Cybersecurity Concerns

1.2.3 Integration Complexity with Legacy Systems

1.2.4 Limited Adoption in Small Fleet Operators

1.3 Opportunities

1.3.1 AI-Driven Fleet Analytics & Automation

1.3.2 Expansion of EV Fleet Management Solutions

1.3.3 Growth in Emerging Markets & Logistics Networks

1.3.4 SaaS-Based Fleet Management Platforms

1.4 Challenges

1.4.1 Managing Large-Scale Data Volumes

1.4.2 Standardization Across Multi-Region Fleets

1.4.3 Rapid Technological Evolution

1.4.4 Competitive Market Fragmentation

Global Fleet Management Market Analysis (USD Billion), 2026???2033

1.1 Market Size Overview

1.2 CAGR Analysis

1.3 Regional Revenue Distribution

1.4 Segment Revenue Analysis

1.5 Deployment Mode Analysis

1.6 End-User Industry Impact Analysis

Market Segmentation (USD Billion), 2026???2033

1.1 By Component

1.1.1 Solutions

1.1.1.1 Fleet Tracking & Telematics

1.1.1.1.1 Real-Time Vehicle Monitoring

1.1.2 Services

1.1.2.1 Managed Services

1.1.2.1.1 Consulting & Integration Services

1.2 By Deployment Mode

1.2.1 Cloud-Based

1.2.1.1 SaaS Platforms

1.2.1.1.1 Multi-Tenant Cloud Systems

1.2.2 On-Premise

1.2.2.1 Enterprise Deployment

1.2.2.1.1 Private Infrastructure Systems

1.3 By Fleet Type

1.3.1 Commercial Fleets

1.3.1.1 Logistics & Transportation Fleets

1.3.1.1.1 Freight & Delivery Vehicles

1.3.2 Passenger Fleets

1.3.2.1 Ride-Hailing & Mobility Services

1.3.2.1.1 Corporate Transport Fleets

1.4 By End-User Industry

1.4.1 Transportation & Logistics

1.4.1.1 Freight & Delivery Services

1.4.1.1.1 Last-Mile Delivery Operations

1.4.2 Construction

1.4.2.1 Heavy Equipment Fleets

1.4.2.1.1 Infrastructure Project Fleets

1.4.3 Government & Public Sector

1.4.3.1 Municipal Fleets

1.4.3.1.1 Emergency & Utility Vehicles

1.4.4 Retail & E-commerce

1.4.4.1 Delivery & Distribution Fleets

1.4.4.1.1 Warehouse Logistics Integration

1.5 By Technology

1.5.1 Telematics Systems

1.5.1.1 GPS Tracking

1.5.1.1.1 Real-Time Location Monitoring

1.5.2 AI & Analytics

1.5.2.1 Predictive Maintenance

1.5.2.1.1 Driver Behavior Analytics

1.5.3 IoT Integration

1.5.3.1 Connected Vehicle Systems

1.5.3.1.1 Sensor-Based Monitoring

Market Segmentation by Geography

1.1 North America

1.2 Europe

1.3 Asia-Pacific

1.4 Latin America

1.5 Middle East & Africa

Competitive Landscape

1.1 Market Share Analysis

1.2 Product Portfolio Benchmarking

1.3 Product Positioning Mapping

1.4 Strategic Partnerships & Ecosystem Development

1.5 Competitive Intensity & Differentiation

Company Profiles

Strategic Intelligence & Pheonix AI Insights

1.1 Pheonix Demand Forecast Engine

1.2 Fleet Efficiency & Cost Optimization Analyzer

1.3 Technology & Innovation Tracker

1.4 EV Fleet Transition Insights

1.5 Automated Porter???s Five Forces Analysis

Future Outlook & Strategic Recommendations

1.1 AI-Driven Fleet Optimization Strategies

1.2 Cloud & Platform Scalability Expansion

1.3 EV & Autonomous Fleet Integration

1.4 Regional Expansion & Market Penetration

1.5 Long-Term Market Outlook (2033+)

Appendix

About Pheonix Market Research

Disclaimer

Competitive Landscape

Global Fleet Management Market Competitive Intensity & Market Structure Overview

The Global Fleet Management Market is characterized by a moderately fragmented structure with high competitive intensity, driven by the presence of multiple global technology providers, telematics companies, and emerging SaaS-based platform players. The market exhibits a technology-driven competitive environment, where innovation, platform capabilities, and data analytics are key differentiators.

Leading companies such as Geotab Inc., Trimble Inc., Verizon Connect, and Samsara Inc. play a significant role in shaping market dynamics through cloud-based platforms, AI-driven analytics, and integrated telematics solutions. At the same time, companies like MiX Telematics and Teletrac Navman contribute to competitive diversity through specialized offerings and regional strengths.

Competitive intensity is primarily driven by rapid technological innovation, platform integration, pricing models, and the increasing demand for real-time data-driven fleet optimization. The shift toward connected, intelligent, and electric fleets further intensifies competition, creating a dynamic and evolving ecosystem.

Global Fleet Management Market Competitive Intensity & Market Structure Current Scenario

Leading Company Profiles

- Geotab Inc.: Leader in telematics and data analytics platforms with strong global presence.

- Trimble Inc.: Provides advanced fleet and asset management solutions across industries.

- Verizon Connect: Key player offering integrated telematics and connectivity solutions.

- Samsara Inc.: Rapidly growing player focusing on IoT-enabled fleet visibility and AI analytics.

- Teletrac Navman: Strong presence in telematics and compliance solutions.

- MiX Telematics: Focused on enterprise fleet management and safety solutions.

- Omnitracs LLC: Established provider in transportation and logistics fleet solutions.

- TomTom Telematics: Known for navigation and fleet optimization technologies.

- AT&T Inc.: Provides connectivity-driven fleet management solutions.

- Fleet Complete: Offers comprehensive telematics and asset tracking services.

Key Competitive Intensity & Market Structure Signals in Global Fleet Management Market

Several signals define the competitive dynamics of the market:

- The presence of multiple global and regional players indicates a moderately fragmented structure with no single dominant player, intensifying competition across segments.

- Rapid technological evolution, including AI, IoT, and cloud-based platforms, creates continuous innovation pressure among competitors.

- The shift toward subscription-based SaaS models introduces recurring revenue streams but increases competition on pricing and feature differentiation.

- Increasing demand for EV fleet management and sustainability solutions is creating new competitive battlegrounds.

- Integration capabilities across telematics, analytics, and enterprise systems act as a key differentiation factor, influencing customer adoption.

- Strategic partnerships and ecosystem expansion (OEMs, telecom providers, and software platforms) are strengthening competitive positioning and market reach.

Strategic Implications of Competitive Intensity & Market Structure in Global Fleet Management Market

The competitive structure leads to several strategic implications:

- Continuous innovation is essential, particularly in AI-driven analytics, predictive maintenance, and automation.

- Platform scalability and integration capabilities are critical, enabling seamless connectivity across fleets and geographies.

- Pricing and subscription models must be optimized, balancing affordability with advanced feature offerings.

- Data-driven value creation is a key differentiator, with insights and analytics driving customer retention.

- Partnership ecosystems are increasingly important, enabling companies to expand capabilities and market access.

- EV and autonomous fleet readiness is a strategic priority, shaping future product development.

Global Fleet Management Market Competitive Intensity & Market Structure Forward Outlook

Looking ahead, the Global Fleet Management Market is expected to maintain its moderately fragmented structure with high competitive intensity, driven by rapid digital transformation and evolving mobility trends.

- AI and machine learning will enhance predictive analytics, route optimization, and operational efficiency.

- Cloud-based platforms will drive scalable and real-time fleet management solutions globally.

- Increasing adoption of electric and autonomous vehicles will accelerate demand for advanced fleet management capabilities.

- Competition will intensify as new entrants and technology providers expand into the market with innovative SaaS solutions.

- Consolidation and strategic partnerships may increase as companies aim to strengthen technological capabilities and expand market presence.

In conclusion, the Global Fleet Management Market represents a high-growth, technology-driven competitive landscape, where innovation, data capabilities, and platform integration determine long-term success.

Value Chain

Global Fleet Management Market Value Chain & Supply Chain Evolution Overview

The Global Fleet Management Market is undergoing a rapid structural transformation driven by digitalization, real-time data analytics, and the integration of advanced technologies such as telematics, IoT, AI, and cloud computing. The market???s value chain is characterized by a hybrid operational model, supported by a hybrid distribution structure that combines direct enterprise sales with partner-led and platform-based delivery models. This framework plays a critical role in shaping revenue streams, service delivery, and competitive differentiation across solution providers.

A defining feature of this value chain is its transition from hardware-centric tracking systems to software-driven, platform-based ecosystems. Fleet management solutions now operate as integrated service models combining hardware devices (GPS, sensors), software platforms (cloud dashboards), and value-added analytics services. This shift places recurring subscription-based revenues at the center of the value chain, emphasizing long-term customer engagement and lifecycle management.

Supply chain complexity is moderate but increasingly technology-driven. It involves coordination between hardware manufacturers, software developers, connectivity providers, and service integrators. The growing adoption of electric vehicles (EVs), autonomous technologies, and regulatory compliance requirements is adding new layers of complexity, particularly in data management, system integration, and cybersecurity.

In response, companies are investing in cloud infrastructure, AI-driven analytics, and scalable SaaS platforms to enhance operational efficiency, improve real-time decision-making, and deliver end-to-end fleet intelligence. The value chain is evolving into a connected, data-centric ecosystem focused on efficiency, compliance, and sustainability.

Global Fleet Management Market Value Chain & Supply Chain Evolution Current Scenario

Market-Specific Value Chain

- Hardware Manufacturing: GPS devices, telematics units, sensors, and onboard diagnostics systems

- Software Development: Fleet management platforms, analytics tools, AI-driven optimization systems

- Connectivity & Integration: Telecom networks, IoT connectivity, cloud infrastructure integration

- Distribution & Deployment: Direct enterprise sales, system integrators, channel partners

- Service & Support: Data analytics, predictive maintenance, compliance management, customer support

- End User Utilization: Fleet operators across logistics, transportation, construction, and public sector

Company-to-Stage Mapping

- Hardware Manufacturing: Telematics device manufacturers, IoT hardware providers

- Software Development: Samsara Inc., Geotab Inc., Trimble Inc.

- Connectivity & Integration: AT&T Inc., Verizon Connect

- Distribution: Channel partners, system integrators, enterprise sales teams

- Service & Support: Teletrac Navman, MiX Telematics

- End User Utilization: Logistics companies, fleet operators, government transport agencies

Key Value Chain & Supply Chain Evolution Signals in Global Fleet Management Market

- Shift to SaaS & Subscription-Based Models

Recurring revenue models are replacing one-time hardware sales, increasing long-term customer value. - Integration of AI & Predictive Analytics

Advanced analytics is enabling predictive maintenance, route optimization, and driver behavior monitoring. - Expansion of IoT & Connected Devices

Increased deployment of sensors and telematics devices is enhancing real-time fleet visibility. - EV Fleet Management Integration

Electric vehicle adoption is driving demand for specialized fleet solutions, including charging and battery management. - Regulatory Compliance & Data Governance

Stringent regulations are increasing demand for compliance monitoring and reporting capabilities. - Cloud & Platform-Based Ecosystems

Cloud infrastructure is enabling scalable, centralized fleet management across multiple geographies.

Strategic Implications of Value Chain & Supply Chain Evolution

- Focus on Platform-Based Differentiation

Companies must develop integrated platforms combining hardware, software, and analytics capabilities. - Strengthening Partner & Ecosystem Networks

Collaboration with telecom providers, OEMs, and system integrators is essential for scalability. - Investment in AI & Data Capabilities

Data-driven insights are becoming a key competitive advantage in fleet optimization. - Enhancing Cybersecurity & Data Protection

Increased connectivity requires robust cybersecurity frameworks to protect fleet data. - Expansion into EV & Autonomous Fleet Solutions

Developing solutions for EV and autonomous fleets is critical for future growth. - Global Scalability & Localization

Platforms must adapt to regional regulations, infrastructure, and fleet requirements.

Global Fleet Management Market Value Chain & Supply Chain Evolution Forward Outlook

Looking ahead, the value chain is expected to evolve into a highly integrated, AI-driven, and cloud-based ecosystem.

Key future developments include:

- Widespread adoption of AI-powered predictive fleet management systems

- Expansion of EV fleet management and charging infrastructure solutions

- Integration of autonomous vehicle management capabilities

- Growth of real-time data analytics and digital twin technologies

- Increased use of cloud-native and edge computing architectures

As the market evolves, success will depend on the ability to integrate technology, data, and service capabilities into a unified platform.

Companies that effectively combine advanced analytics, scalable cloud platforms, and strong ecosystem partnerships will achieve superior operational efficiency, customer retention, and long-term competitive advantage in the Global Fleet Management Market.

Investment Activity

Global Fleet Management Market Investment & Funding Dynamics Overview

The investment and funding landscape within the Global Fleet Management Market is characterized by rapidly rising investment activity and high capital intensity, driven by the market???s strong digital transformation and its critical role in optimizing modern transportation ecosystems. Structural drivers such as increasing adoption of telematics, IoT-enabled devices, AI-driven analytics, and cloud-based platforms are attracting significant capital inflows into the sector. These investments are primarily focused on enhancing software capabilities, expanding data analytics infrastructure, and integrating advanced technologies to improve fleet efficiency, safety, and compliance.

A key factor shaping investment dynamics in this market is the transition from traditional fleet tracking systems to fully integrated, intelligent fleet management platforms. This shift requires substantial investment in software development, data processing infrastructure, and connected hardware ecosystems. Companies are increasingly allocating capital toward AI-based predictive maintenance, real-time vehicle diagnostics, and advanced route optimization solutions. Additionally, the growing adoption of electric vehicles (EVs) is driving investment in specialized fleet management systems capable of handling charging infrastructure, battery analytics, and lifecycle optimization.

Furthermore, capital allocation is influenced by the need to address operational challenges such as rising fuel costs, regulatory compliance requirements, and demand for real-time decision-making. As a result, organizations are investing in end-to-end digital platforms that enhance visibility, reduce operational costs, and improve overall fleet performance.

Global Fleet Management Market Investment & Funding Dynamics Current Scenario

In the current scenario, the Global Fleet Management Market is witnessing a strong influx of investment, supported by its high growth trajectory and increasing enterprise reliance on data-driven fleet operations. The high capital intensity reflects significant financial commitments toward technology development, platform scalability, and infrastructure integration.

Investment activity is particularly concentrated in areas such as AI-driven analytics, cloud-based fleet platforms, IoT-enabled telematics devices, and EV fleet management solutions. Companies are allocating capital toward developing advanced software ecosystems that integrate vehicle tracking, driver behavior monitoring, predictive maintenance, and compliance management into unified platforms.

The market is also experiencing active merger and acquisition (M&A) activity, as companies seek to strengthen their technological capabilities, expand global reach, and enhance service offerings. Strategic acquisitions and partnerships are increasingly focused on integrating AI, expanding telematics capabilities, and building comprehensive mobility solutions.

Additionally, the funding landscape is dominated by venture capital and growth-stage investments, particularly in technology-driven startups offering innovative fleet management solutions. Companies are prioritizing platform scalability, geographic expansion, and integration of advanced technologies to capture market share in a highly competitive environment.

Key Investment & Funding Dynamics Signals in Global Fleet Management Market

The investment and funding dynamics in the Global Fleet Management Market are shaped by several key signals reflecting evolving industry priorities. One of the primary signals is the rapid digitalization of fleet operations, which is driving continuous investment in connected technologies, data analytics, and cloud infrastructure.

Another critical signal is the increasing adoption of electric vehicles, which is creating demand for specialized fleet management solutions. This shift is prompting significant investment in EV-focused analytics, charging management systems, and energy optimization tools.

Regulatory compliance requirements also act as a major investment driver. Governments across regions are enforcing stricter regulations related to emissions, driver safety, and operational transparency, encouraging companies to invest in compliance-focused digital solutions.

The growing importance of cost optimization is another key signal. Fleet operators are investing in technologies that reduce fuel consumption, improve route efficiency, and minimize maintenance costs, thereby enhancing overall profitability.

Additionally, the emergence of autonomous vehicle technologies is influencing long-term investment strategies. Companies are allocating resources toward developing platforms capable of supporting future autonomous fleet operations, ensuring readiness for next-generation mobility ecosystems.

Strategic Implications of Investment & Funding Dynamics in Global Fleet Management Market

The current investment dynamics have significant strategic implications for companies operating in the Global Fleet Management Market. One of the primary implications is the need for continuous technological innovation to remain competitive in a rapidly evolving digital landscape. Companies must invest heavily in AI, IoT, and cloud technologies to deliver differentiated and scalable solutions.

High capital intensity also necessitates efficient capital allocation and strategic prioritization. Companies must balance investments in technology development with the need to achieve profitability and sustainable growth. This creates a strong focus on platform efficiency, customer acquisition, and long-term value creation.

The increasing role of M&A activity highlights the importance of strategic consolidation and capability expansion. Companies are leveraging acquisitions to gain access to new technologies, expand into new markets, and strengthen their competitive positioning.

Furthermore, the shift toward integrated mobility ecosystems is reshaping business strategies. Companies are investing in end-to-end solutions that combine hardware, software, and services, enabling them to offer comprehensive fleet management platforms and create recurring revenue streams.

Global Fleet Management Market Investment & Funding Dynamics Forward Outlook

Looking ahead, the investment and funding dynamics in the Global Fleet Management Market are expected to remain highly robust, driven by ongoing digital transformation, increasing EV adoption, and advancements in connected mobility technologies. The continued integration of AI, machine learning, and IoT will act as a major catalyst for sustained investment.

Technological innovation will remain a central focus, with increasing investment in predictive analytics, autonomous fleet management capabilities, and real-time data processing systems. These advancements are expected to enhance operational efficiency, improve safety, and reduce costs for fleet operators.

Sustainability will also play a critical role in shaping future investment trends. Companies are likely to increase investments in EV fleet management solutions, carbon tracking systems, and energy optimization tools to align with global environmental goals and regulatory requirements.

Additionally, the expansion of cloud-based platforms and mobile applications will drive further investment in scalable and flexible fleet management solutions. This digital transformation will enable organizations to manage fleets more efficiently across geographies and operational environments.

In summary, the Global Fleet Management Market is positioned for sustained investment growth, supported by its high-growth potential and critical role in modern transportation systems. Companies that strategically invest in technology, scalability, and innovation will be best positioned to capture long-term opportunities and maintain a competitive edge in this rapidly evolving market.

Technology & Innovation

Global Fleet Management Market Technology & Innovation Landscape Overview

The Global Fleet Management Market is undergoing a rapid transformation driven by advanced digital technologies and data-centric innovation. This landscape is characterized by a high technology maturity in core systems and a high innovation intensity, reflecting the market???s evolution into a fully integrated, intelligent mobility ecosystem. The convergence of telematics, IoT, artificial intelligence (AI), and cloud computing is redefining fleet operations, enabling real-time visibility, predictive insights, and automated decision-making.

At the core of this transformation are IoT-enabled telematics systems, which provide continuous tracking of vehicle location, performance, fuel usage, and driver behavior. These systems form the backbone of modern fleet management, enabling organizations to optimize operations, reduce costs, and improve safety.

Another major innovation driver is AI-driven analytics, which enables predictive maintenance, route optimization, and driver risk assessment. By leveraging machine learning algorithms, fleet operators can proactively address maintenance issues, minimize downtime, and enhance overall efficiency.

Cloud-based platforms are also playing a crucial role by offering scalable and centralized fleet management solutions. These platforms enable seamless data integration, real-time monitoring, and cross-geographical fleet coordination, making them essential for large and distributed fleet operations.

Additionally, the growing adoption of electric and autonomous vehicles is driving innovation in fleet management solutions, including battery monitoring, charging optimization, and autonomous fleet integration.

Global Fleet Management Market Technology & Innovation Landscape Current Scenario

Currently, the Global Fleet Management Market exhibits a high level of patent activity and continuous technological advancement, driven by intense competition and rapid digital transformation.

- Telematics & IoT Integration

Advanced telematics devices and IoT sensors enable real-time data collection and vehicle monitoring. - AI & Predictive Analytics

Increasing use of AI for predictive maintenance, route optimization, and driver behavior analysis. - Cloud-Based Fleet Platforms

Widespread adoption of cloud solutions for scalable, centralized, and data-driven fleet operations. - EV Fleet Management Technologies

Development of tools for battery health monitoring, charging infrastructure management, and energy optimization. - Automation & Autonomous Readiness

Early-stage integration of technologies supporting autonomous vehicle fleet management.

Key Technology & Innovation Landscape Signals in Global Fleet Management Market

The market is shaped by several strong innovation signals:

- Shift Toward Data-Driven Fleet Ecosystems

Transition from basic tracking systems to intelligent, analytics-driven platforms. - Rapid AI Adoption Across Operations

Increasing reliance on AI for optimization, safety, and cost reduction. - Cloud-Native Platform Expansion

Growth of cloud-based solutions enabling real-time global fleet management. - Electrification-Driven Innovation

Rising demand for EV-specific fleet management capabilities. - Emergence of Autonomous Fleet Technologies

Preparatory development for managing self-driving vehicle fleets.

Strategic Implications of Technology & Innovation Landscape in Global Fleet Management Market

The technology landscape is shifting competition toward platform capabilities, data intelligence, and integration ecosystems. Companies must invest in AI, IoT, and cloud technologies to remain competitive in an increasingly digital environment.

The rise of EVs and autonomous vehicles is creating new strategic opportunities, requiring specialized solutions for energy management, vehicle coordination, and predictive analytics. Additionally, data security, system interoperability, and scalability are becoming critical success factors.

Organizations that successfully integrate advanced analytics, real-time monitoring, and automation into their platforms will gain a strong competitive advantage. Strategic partnerships with OEMs, technology providers, and mobility platforms will further enhance market positioning.

Global Fleet Management Market Technology & Innovation Landscape Forward Outlook

Looking ahead to 2026???2033, the technology and innovation landscape is expected to evolve toward fully connected, AI-driven, and autonomous fleet ecosystems.

Future developments will include deeper integration of AI and machine learning, expansion of 5G-enabled real-time connectivity, and widespread adoption of smart, connected fleet platforms. EV fleet management solutions will become more sophisticated, with advanced battery analytics and energy optimization capabilities.

Autonomous vehicle integration will further redefine fleet operations, requiring advanced coordination systems and regulatory-compliant frameworks. Sustainability-driven innovation, including carbon tracking and ESG-focused analytics, will also gain prominence.

Overall, companies that invest in intelligent platforms, EV integration, and automation technologies will be best positioned to lead the next phase of growth in the Global Fleet Management Market.

Market Risk

Global Fleet Management Market Risk Factors & Disruption Threats Overview

The Global Fleet Management Market operates within a rapidly evolving, technology-driven ecosystem, exposing it to a diverse range of structural risks and disruption threats. The overall market risk level is moderate, supported by strong growth fundamentals but influenced by technological dependency, cybersecurity concerns, and regulatory complexity. While increasing digital adoption and operational necessity provide stability, the pace of innovation and integration introduces execution and compliance risks.

Geopolitical exposure is moderate, as the market relies on global connectivity infrastructure, semiconductor supply chains, and cross-border data flows. Trade restrictions, data localization laws, and regional regulatory differences can impact deployment, scalability, and operational efficiency of fleet management solutions.

Substitution risk is low, given the essential role of fleet management systems in optimizing operations, ensuring compliance, and reducing costs. While basic tracking alternatives exist, they cannot replace the comprehensive capabilities of integrated telematics and AI-driven platforms.

Global Fleet Management Market Risk Factors & Disruption Threats Current Scenario

Currently, the market is navigating a complex risk landscape driven by rapid technological advancement, regulatory pressures, and data security concerns. One of the most significant risk factors is cybersecurity vulnerability. As fleet management systems rely heavily on cloud platforms, IoT devices, and real-time data exchange, they are increasingly exposed to cyber threats, data breaches, and system disruptions.

Another key challenge is regulatory fragmentation across regions. Differences in data privacy laws, telematics regulations, and compliance requirements create operational complexity for global fleet operators and solution providers.

High implementation and integration costs also pose a barrier, particularly for small and medium-sized fleet operators. The transition from legacy systems to advanced digital platforms requires significant investment in hardware, software, and training.

Additionally, the rapid evolution of electric and autonomous vehicles introduces technological uncertainty. Fleet management systems must continuously adapt to new vehicle architectures, charging infrastructure, and regulatory frameworks, increasing development complexity.

Key Risk Factors & Disruption Threats Signals in Global Fleet Management Market

- Cybersecurity Risks: Increasing exposure to data breaches and system vulnerabilities due to digital and cloud-based operations.

- Regulatory Complexity: Variations in data privacy, telematics, and compliance regulations across regions.

- High Implementation Costs: Significant investment required for system integration, hardware deployment, and workforce training.

- Technological Obsolescence: Rapid pace of innovation increasing the risk of outdated systems and continuous upgrade requirements.

- Dependence on Connectivity Infrastructure: Reliance on GPS, IoT networks, and cloud services for real-time operations.

- EV & Autonomous Transition Challenges: Evolving requirements for managing electric and autonomous fleets.

Strategic Implications of Risk Factors & Disruption Threats in Global Fleet Management Market

The moderate risk environment requires companies to prioritize cybersecurity, scalability, and regulatory compliance. Investment in secure cloud architectures, data encryption, and real-time threat monitoring is essential to protect sensitive fleet data and ensure operational continuity.

Developing flexible and modular platforms can help address regulatory variations and enable easier customization across regions. This adaptability is critical for global expansion and long-term competitiveness.

Cost optimization strategies, including SaaS-based models and subscription pricing, can help lower entry barriers and expand adoption among smaller fleet operators.

Additionally, continuous innovation and integration with emerging technologies such as AI, EV systems, and autonomous platforms will be key to maintaining relevance in a rapidly evolving market.

Global Fleet Management Market Risk Factors & Disruption Threats Forward Outlook

Looking ahead to 2026???2033, the market???s risk profile is expected to remain moderate, with emerging disruptions driven by digital transformation, regulatory evolution, and technological convergence.

- Increasing cybersecurity threats targeting connected fleet ecosystems

- Expansion of data privacy and localization regulations across global markets

- Rapid technological advancements requiring continuous system upgrades

- Growing complexity in managing electric and autonomous fleets

- Dependence on reliable connectivity and cloud infrastructure

Despite these risks, the market???s strong growth trajectory and critical role in modern transportation systems provide a stable foundation. Companies that effectively manage cybersecurity, adapt to regulatory changes, and invest in scalable, future-ready platforms will be best positioned to navigate disruptions and capture long-term growth in the Global Fleet Management Market.

Regulatory Landscape

Global Fleet Management Market Regulatory & Policy Environment Overview

The regulatory and policy environment plays a central role in shaping the structure and growth trajectory of the Global Fleet Management Market. Regulatory frameworks govern critical aspects such as vehicle safety, emissions control, driver behavior monitoring, data privacy, and operational compliance. As fleet management solutions are deeply integrated with transportation systems and public infrastructure, compliance with regulatory standards is not optional but a fundamental requirement for market participation.

Governments and regulatory bodies worldwide are increasingly mandating the adoption of digital monitoring systems to enhance road safety, reduce emissions, and improve operational transparency. Regulations related to electronic logging devices (ELDs), driver working hours, and vehicle tracking are accelerating the adoption of telematics and fleet management platforms. At the same time, environmental policies targeting carbon emissions are pushing fleet operators toward electrification and sustainable practices, further increasing reliance on advanced fleet management systems.

In addition, the integration of IoT, AI, and cloud technologies introduces new regulatory considerations related to cybersecurity, data protection, and system interoperability. This evolving regulatory landscape is creating both compliance challenges and growth opportunities for solution providers.

Global Fleet Management Market Regulatory & Policy Environment Current Scenario

Currently, the Global Fleet Management Market operates within a highly regulated and multi-layered compliance environment that varies across regions and industries.

- Vehicle Safety & Driver Compliance Regulations

Authorities enforce strict rules on driver working hours, vehicle maintenance, and safety monitoring. Compliance with ELD mandates and driver behavior tracking systems is becoming standard across major markets. - Emissions & Environmental Policies

Stringent emission norms and sustainability targets are driving adoption of fleet management solutions that optimize fuel consumption and support EV integration. - Data Privacy & Cybersecurity Regulations

With increasing reliance on telematics and cloud platforms, regulations governing data security, user privacy, and cross-border data transfer are becoming more stringent. - Digital Infrastructure & Connectivity Standards

Governments are promoting smart mobility and connected vehicle ecosystems, requiring interoperability and compliance with digital communication standards. - EV & Smart Mobility Regulations

The transition toward electric and autonomous fleets is introducing new regulatory frameworks focused on charging infrastructure, battery management, and system integration.

Key Regulatory & Policy Environment Signals in Global Fleet Management Market

- Expansion of Telematics Mandates

Governments are increasingly requiring GPS tracking, ELDs, and real-time monitoring systems to enhance safety and compliance. - Strengthening Emission Control Policies

Global efforts to reduce carbon emissions are accelerating the adoption of fleet optimization and electrification solutions. - Rising Importance of Data Governance

Regulations around data privacy and cybersecurity are becoming critical as fleet management platforms handle large volumes of sensitive data. - Growth of Smart Transport Initiatives

Public sector investments in smart cities and intelligent transport systems are driving regulatory support for connected fleet solutions. - Increasing Complexity of Cross-Regional Compliance

Global fleet operators must navigate diverse regulatory frameworks across regions, adding layers of compliance complexity.

Strategic Implications of Regulatory & Policy Environment in Global Fleet Management Market

The regulatory environment significantly influences competitive dynamics and strategic decision-making. Companies must invest in compliance capabilities, including software updates, data security systems, and regulatory certifications, to remain competitive.

The growing complexity of regulations creates high entry barriers, favoring established players with strong technological infrastructure and compliance expertise. At the same time, regulatory-driven demand for telematics, AI analytics, and EV fleet management solutions is creating new growth opportunities.

Organizations that proactively align with regulatory requirements???particularly in emissions, safety, and data governance???can achieve competitive advantage through improved operational efficiency and enhanced customer trust.

Global Fleet Management Market Regulatory & Policy Environment Forward Outlook

Looking ahead, the regulatory environment is expected to become increasingly stringent and technology-driven through 2033. Future regulations will likely focus on deeper integration of AI, stricter emission targets, enhanced data protection laws, and standardization of autonomous vehicle operations.

The expansion of electric and autonomous fleets will introduce new compliance frameworks, further increasing regulatory complexity. Additionally, real-time monitoring and reporting requirements are expected to become more widespread, reinforcing the importance of advanced fleet management platforms.

Overall, companies that can effectively navigate multi-layered regulatory requirements while leveraging technology for compliance and optimization will be best positioned to capitalize on long-term growth opportunities in the Global Fleet Management Market.