Global Electric Vehicle (EV) Tyres Market Size, share & forecast 2026-2033

Market Forecast Snapshot (2026???2033)

| Metric | Value |

|---|---|

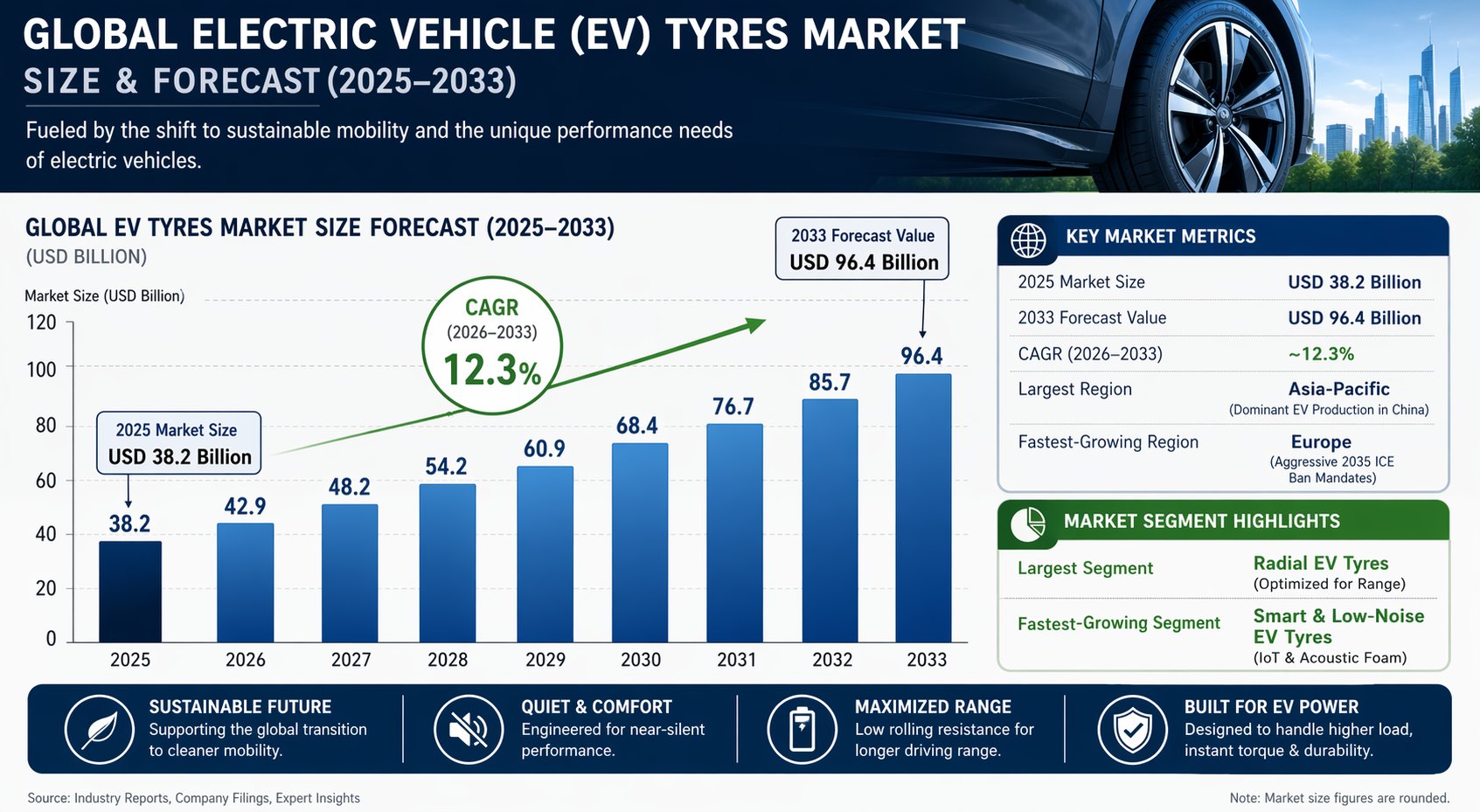

| 2025 Market Size | USD 38.2 Billion |

| 2033 Market Size | USD 96.4 Billion |

| CAGR (2026???2033) | ~12.3% |

| Largest Region | Asia-Pacific |

| Fastest-Growing Region | Europe |

| Largest Segment | Radial EV tyres |

| Fastest-Growing Segment | Smart & low-noise EV tyres |

| Key Trend | Range-optimized, quiet & sustainable tyres |

Global Electric Vehicle (EV) Tyres Market Overview

The Global Electric Vehicle (EV) Tyres Market is all about tyres made just for electric cars, SUVs, vans, and commercial EVs . Because EVs are heavier from big batteries, these tyres need to be stronger and handle instant torque without wearing out fast. They also focus on low rolling resistance to help extend driving range and keep road noise low for a smoother ride. You???ll find these tyres on brand-new EVs as original equipment and also as replacements in the aftermarket.

The Global Electric Vehicle (EV) Tyres Market is booming as more electric cars, SUVs, and vans hit the roads . Governments pushing clean energy and stricter emission rules are fueling this growth, along with cool new tyre tech. As the number of EVs worldwide increases, many early models need tyre replacements, boosting aftermarket demand too . So, tyre makers are hustling to keep up with this fast-growing market.

According to the Pheonix Demand Forecast Engine, the Global Electric Vehicle (EV) Tyres Market is estimated at USD 38.2 billion in 2025 and is projected to reach USD 96.4 billion by 2033, expanding at a CAGR of ~12.3% during the forecast period (2026???2033).

Asia-Pacific is the largest EV tyres market due to massive EV production in China and rapid electrification in India and Southeast Asia, while Europe is the fastest-growing region driven by aggressive EV mandates, premium EV penetration, and sustainability regulations.

Key Drivers of Global Electric Vehicle (EV) Tyres Market Growth

Rapid Growth in Electric Vehicle Adoption

Government incentives, falling battery costs, and expanding charging infrastructure are accelerating EV sales globally.

EV-Specific Performance Requirements

Higher torque, heavier battery packs, and range sensitivity drive demand for specialized EV-optimized tyres.

Expansion of EV Replacement Cycles

As EV parc grows, replacement tyre demand is emerging as a long-term growth engine.

Noise Reduction & Ride Comfort Needs

Quieter EV cabins amplify tyre noise, increasing demand for low-noise and foam-lined tyres.

Regulatory Push for Energy Efficiency

Low rolling resistance tyres help automakers meet energy efficiency and emission-equivalent targets.

Technological Advancements

Smart tyres, sustainable materials, silica compounds, and sensor integration enhance EV tyre value.

Global Electric Vehicle (EV) Tyres Market Segmentation

1. By Tyre Construction

1.1 Radial Tyres??

1.1.1 Steel-Belted Radial Tyres

1.1.1.1 Single steel belt

1.1.1.2 Double steel belt

1.1.1.3 Multi-layer steel belt

1.1.2 Fabric-Belted Radial Tyres

1.1.2.1 Polyester radial

1.1.2.2 Nylon radial

1.2 Bias (Cross-Ply) Tyres

1.2.1 Nylon bias tyres

1.2.2 Polyester bias tyres

2. By Vehicle Category

2.1 Electric Passenger Cars??

2.1.1 Hatchbacks

2.1.1.1 Entry-level EV hatchbacks

2.1.1.2 Premium compact EVs

2.1.2 Sedans

2.1.2.1 Mid-size EV sedans

2.1.2.2 Luxury EV sedans

2.2 Electric SUVs & Crossovers (Fastest-Growing)

2.2.1 Compact electric SUVs

2.2.2 Mid-size electric SUVs

2.2.3 Full-size electric SUVs

2.3 Electric Vans & Light Commercial EVs

2.3.1 Delivery vans

2.3.2 Fleet electric vans

3.1 Summer EV Tyres

3.1.1 Performance-Focused Summer EV Tyres

3.1.1.1 High-grip silica compounds

3.1.1.2 Optimized tread stiffness for instant EV torque

3.1.2 Touring EV Tyres

3.1.2.1 Comfort-oriented tread designs

3.1.2 2 Reduced road noise for silent EV cabins

3.2 Winter EV Tyres

3.2.1 Studded Winter EV Tyres

3.2.1 1 Ice-specific traction

3.2.1.2 Reinforced tread blocks for heavy EV loads

3.2.2 Studless Winter EV Tyres

3.2.2.1 Advanced rubber compounds for cold flexibility

3.2.2.2 Low-noise winter performance

3.3 All-Season EV Tyres (Largest Segment)

3.3.1 Standard All-Season EV Tyres

3.3.1.1 Balanced wet, dry, and mild winter performance

3.3.1.2 Cost-effective year-round solution

3.3.2 Performance All-Season EV Tyres

3.3.2.1 Enhanced grip across temperature ranges

3.3.2.2 Torque-optimized tread patterns

4. By Sales Channel

4.1 OEM (Original Equipment Manufacturer)

4.1.1 Passenger EV OEM Fitment

4.1.1.1 Hatchbacks

4.1.1.2 Electric sedans

4.1.2 Electric SUV OEM Fitment

4.1.2.1 Compact electric SUVs

4.1.2.2 Full-size electric SUVs

4.1.3 Electric Van OEM Fitment

4.1.3.1 Urban delivery EVs

4.1.3.2 Fleet electric vans

4.2 Aftermarket / Replacement (Fastest-Growing Segment)

4.2.1 Authorized EV Tyre Dealers

4.2.1.1 OEM-approved replacements

4.2.2 Independent Tyre Retailers

4.2.2.1 Multi-brand EV tyre offerings

4.2.3 EV Service Centers

4.2.3.1 Integrated tyre and battery services

4.2.4 Online & E-Commerce Platforms

4.2.4.1 Direct-to-consumer sales

5. By Rim Size

5.1 Below 16 Inches

5.1.1 Entry-Level Electric Vehicles

5.1.1.1 Compact EV hatchbacks

5.2 16???18 Inches (Largest Segment)

5.2.1 Electric Sedans

5.2.1.1 Mid-size EV sedans

5.2.1.2 Premium EV sedans

5.2.2 Compact Electric SUVs

5.2.2.1 Urban and suburban usage

5.3 Above 18 Inches (Fastest-Growing)

5.3.1 Premium EVs

5.3.1.1 Luxury electric sedans

5.3.2 High-Performance Electric SUVs

5.3.2.1Performance and luxury EV SUVs

6. By Tyre Technology

6.1 Conventional Pneumatic EV Tyres

6.2 Low Rolling Resistance Tyres

6.2.1 Energy-efficient compound tyres

6.2.2 Extended range EV tyres

6.3 Noise-Reduction Tyres

6.3.1 Acoustic foam-lined tyres

6.3.2 Vibration-optimized tread designs

6.4 High Load-Bearing Tyres

6.4.1 Reinforced sidewall tyres

6.4.2 Battery-weight optimized tyres

6.5 Smart & Connected Tyres (Emerging)

6.5.1 Embedded pressure & temperature sensors

6.5.2 Real-time tyre health monitoring

7. By Performance Category

7.1 Economy EV Tyres

7.1.1 Long-life tread focus

7.2 Premium EV Tyres

7.2.1 Comfort & noise reduction focus

7.3 High-Performance EV Tyres

7.3.1 High torque handling

7.3.2 Sport electric vehicles

8. By Propulsion Type

8.1 Battery Electric Vehicles (BEVs) (Largest Segment)

8.2 Plug-in Hybrid Electric Vehicles (PHEVs)

8.3 Fuel Cell Electric Vehicles (FCEVs) (Niche)

9. By Geography

9.1 Asia-Pacific (Largest Region)

China

India

Japan

South Korea

Southeast Asia

9.2 Europe (Fastest-Growing)

Germany

France

U.K.

Norway

Netherlands

9.3 North America

U.S.

Canada

9.4 Latin America

Brazil

Mexico

9.5 Middle East & Africa

Regional Insights of Global Electric Vehicle (EV) Tyres Market

Asia-Pacific ??? Largest Market

China dominates EV production and OEM tyre demand, supported by strong government incentives and local tyre manufacturing.

Europe ??? Fastest-Growing Region

Premium EV penetration, sustainability regulations, and winter tyre requirements drive advanced EV tyre demand.

North America

Strong growth in electric SUVs, luxury EVs, and aftermarket replacement demand.

Latin America & Middle East & Africa

Gradual EV adoption with early-stage tyre market development.

Leading Companies in the Global Electric Vehicle (EV) Tyres Market

Michelin

Bridgestone Corporation

Goodyear Tire & Rubber Company

Continental AG

Pirelli & C. S.p.A.

Hankook Tire

Yokohama Rubber Company

Sumitomo Rubber Industries

Toyo Tires

Apollo Tyres

Michelin is the largest company in the Global Electric Vehicle (EV) Tyres Market

Strategic Intelligence & Pheonix AI-Backed Insights

Pheonix Demand Forecast Engine

Models EV parc growth, OEM production, and replacement cycles.

EV Tyre Requirement Analyzer

Evaluates demand for low-noise, high-load, and energy-efficient tyres.

Sustainability Impact Model

Tracks recycled materials, bio-rubber adoption, and carbon footprint reduction.

Automated Porter???s Five Forces (Concise)

Buyer Power: Moderate ??? OEM concentration but growing aftermarket

Supplier Power: Moderate ??? rubber and advanced material dependency

Threat of New Entrants: Low ??? high R&D and OEM qualification barriers

Threat of Substitutes: Low ??? tyres are essential consumables

Competitive Rivalry: High ??? intense innovation-led competition

Why the Electric Vehicle Tyres Market Is Critical

??? Directly impacts EV driving range and efficiency

??? Essential for handling instant torque and heavy batteries

??? Strong long-term replacement demand as EV parc expands

??? Key enabler of quiet, premium EV driving experience

Final Takeaway of Global Electric Vehicle (EV) Tyres Market

The Global Electric Vehicle Tyres Market is a high-growth, innovation-driven market shaped by electrification, sustainability, and performance optimization. EV-specific tyres are transitioning from niche products to mainstream automotive essentials. Manufacturers that invest in low rolling resistance technologies, noise reduction solutions, smart connectivity, and sustainable materials, while building strong OEM and aftermarket partnerships, will dominate the EV tyre landscape through 2033.

Competitive Landscape

Global Electric Vehicle (EV) Tyres Market Competitive Intensity & Market Structure Overview

The Global Electric Vehicle (EV) Tyres Market is characterized by a highly innovation-driven yet intensely competitive ecosystem, shaped by rapid EV adoption and strict performance requirements from OEMs and fleet operators. The market operates on a dual-layer structure where OEM supply contracts ensure baseline stability, while the aftermarket is expanding rapidly as early EV fleets enter replacement cycles.

Competitive intensity is high due to the technical complexity of EV tyre design. Manufacturers must balance low rolling resistance, high load-bearing capacity, noise reduction, and durability under instant torque conditions. This forces companies to compete more on R&D capability and material innovation than on price alone.

The market is moderately consolidated at the top, with Tier 1 global players dominating OEM EV fitment across passenger EVs, SUVs, and electric commercial vehicles. However, the aftermarket remains fragmented, with regional and mid-tier brands competing aggressively on pricing, availability, and localized EV service networks.

Global Electric Vehicle (EV) Tyres Market Competitive Intensity & Market Structure Current Scenario

Leading Company Profiles

Michelin: Global Tyre Manufacturer. Leader in EV-optimized low rolling resistance tyres, range-maximization technology, and sustainable tyre innovation.

Bridgestone Corporation: Global Tyre Manufacturer. Strong OEM partnerships and advanced EV fleet tyre solutions with focus on durability and efficiency.

Goodyear Tire & Rubber Company: Tyre Manufacturer. Focused on smart tyres, connected mobility solutions, and EV performance optimization.

Continental AG: Technology-Driven Tyre Manufacturer. Strong in sensor-based tyres, acoustic comfort solutions, and EV safety systems.

Pirelli & C. S.p.A.: Premium Tyre Manufacturer. Strong presence in high-performance EV and luxury electric vehicle segments.

Hankook Tire: Fast-Growing Global Player. Expanding EV OEM contracts with focus on high-value SUV and passenger EV tyres.

Yokohama Rubber Company: Tyre Manufacturer. Known for energy-efficient and durable EV-compatible tyre technologies.

Sumitomo Rubber Industries: Tyre Manufacturer. Strong presence in Asia-Pacific EV OEM and replacement markets.

Toyo Tires: Emerging EV-Focused Player. Expanding portfolio in performance EV and SUV tyre categories.

Apollo Tyres: Cost-Competitive Global Player. Building EV-ready tyre portfolio for emerging markets.

Key Competitive Intensity & Market Structure Signals in EV Tyres

A key structural signal in the EV tyres market is the strong influence of OEM specifications. Automakers define strict performance benchmarks for range, noise, and load handling, making compliance capability a critical entry barrier for suppliers.

The rapid growth of EV fleets is creating a future-heavy replacement cycle opportunity. As early-generation EVs age, aftermarket demand is expected to accelerate significantly, shifting competition toward long-life and performance-retention tyres.

Another defining factor is the shift toward sustainability-driven procurement. OEMs and fleet operators are increasingly demanding tyres made with recycled materials, bio-based rubber, and low-carbon production processes.

Noise reduction and range optimization have emerged as key differentiators. EVs amplify road and tyre noise due to lack of engine sound, pushing manufacturers to innovate acoustic foam tyres and advanced tread designs.

Despite global consolidation, regional players still play a role in cost-sensitive EV segments, particularly in emerging markets where affordability outweighs premium performance features.

Strategic Implications of Competitive Intensity & Market Structure in EV Tyres

The competitive landscape is forcing tyre manufacturers to evolve into technology providers rather than pure product suppliers. Companies integrating tyre design with vehicle efficiency systems, telemetry, and smart monitoring gain a strong advantage in OEM partnerships.

Total cost of ownership (TCO) is becoming a dominant purchasing metric. EV tyre manufacturers that deliver extended range, longer tread life, and lower energy consumption are positioned to capture premium OEM contracts.

Electrification is also accelerating product differentiation. High torque, heavier vehicle weight, and regenerative braking systems are reshaping tyre engineering priorities, increasing demand for reinforced and high-load EV tyres.

Additionally, smart tyre ecosystems are emerging as a new competitive frontier. IoT-enabled tyres with real-time monitoring and predictive maintenance capabilities are increasingly becoming standard in premium EV platforms.

EV Tyres Competitive Intensity & Market Structure Forward Outlook

The EV Tyres Market is expected to remain highly competitive and innovation-led, with increasing dominance of Tier 1 global manufacturers across OEM channels. However, the aftermarket segment will expand rapidly as EV adoption matures globally.

Consolidation is expected to accelerate as leading players invest in acquisitions, material science innovation, and EV-focused R&D expansion. Partnerships with EV manufacturers, mobility platforms, and battery OEMs will become strategically important.

Regulatory frameworks promoting carbon neutrality, recycling, and energy efficiency will continue to reshape product development priorities, further strengthening the position of technologically advanced manufacturers.

In the long term, the market will be defined by three core competitive pillars: range optimization efficiency, acoustic comfort innovation, and sustainable tyre ecosystems. Companies that successfully align with EV architecture requirements while scaling smart and eco-friendly solutions will lead the EV Tyres Market through 2033.

Value Chain

Global Electric Vehicle (EV) Tyres Market Value Chain & Supply Chain Evolution Overview

The value chain and supply chain structure of the Global Electric Vehicle (EV) Tyres Market is rapidly evolving alongside the global shift toward electrification. The ecosystem is closely integrated with EV OEMs, battery-driven vehicle platforms, smart mobility providers, and advanced material suppliers, making it one of the most innovation-sensitive segments in the tyre industry.

The market operates through a multi-layered structure involving raw material suppliers, advanced compound developers, tyre manufacturers, EV OEM partnerships, aftermarket distributors, and digital mobility platforms. Demand flows through two primary channels: OEM fitment for new electric vehicles and replacement demand driven by expanding EV parc globally.

Compared to conventional tyres, EV tyres require specialized input materials such as high-silica compounds, reinforced steel belts, noise-dampening foams, and low rolling resistance polymers. These materials are critical to improving driving range, load handling, and cabin comfort in electric vehicles.

Manufacturing is highly R&D intensive, focusing on torque-resistant tread designs, weight-optimized construction, acoustic engineering, and durability enhancement. EV tyre production also increasingly integrates sensor-based monitoring systems and sustainable materials to align with automotive decarbonization goals.

Distribution is strongly OEM-driven at the initial stage of adoption, while the aftermarket is rapidly expanding as early EV adopters begin replacing tyres. EV service centers, branded tyre retail networks, and online D2C platforms are becoming increasingly important in the distribution ecosystem.

Key supply chain challenges include high dependency on advanced raw materials, volatility in rubber and petrochemical inputs, high R&D costs, and the need for continuous innovation to match evolving EV platform requirements. Additionally, manufacturers face pressure to reduce carbon footprint and adopt circular economy practices.

Global Electric Vehicle (EV) Tyres Market Value Chain & Supply Chain Evolution Current Scenario

The Global Electric Vehicle (EV) Tyres Market is currently in a transition phase, moving from early-stage specialization to large-scale mainstream adoption as EV penetration accelerates globally.

At the upstream level, manufacturers face rising costs of advanced materials such as silica, synthetic rubber, and acoustic foam compounds. To manage volatility, companies are diversifying sourcing strategies and investing in long-term supplier partnerships and material innovation programs.

In manufacturing, companies such as Michelin, Bridgestone, Continental, Goodyear, and Pirelli are leading EV tyre development through innovations in low rolling resistance technology, high-load structural reinforcement, and noise reduction engineering. Standardization is emerging across EV platforms, enabling economies of scale.

OEM integration is highly strategic, with tyre manufacturers working directly with EV automakers to optimize range efficiency, safety, and performance. EV tyre specifications are increasingly embedded in vehicle design stages rather than treated as aftermarket components.

The aftermarket segment is expanding rapidly as early-generation EVs enter replacement cycles. Demand is particularly strong for high-performance, low-noise, and energy-efficient replacement tyres across passenger EVs and electric SUVs.

Digitalization is reshaping the ecosystem, with smart tyres, IoT-enabled monitoring systems, and AI-driven predictive maintenance platforms enhancing performance tracking and lifecycle optimization for EV fleets.

Key Value Chain & Supply Chain Evolution Signals in Global Electric Vehicle (EV) Tyres Market

Several structural signals are defining the evolution of the EV tyres value chain.

First, rapid EV adoption is driving demand for specialized tyres designed for higher torque, heavier vehicle weight, and extended driving range requirements.

Second, noise reduction and ride comfort have become critical performance factors due to the near-silent nature of EV drivetrains, increasing adoption of foam-lined and acoustic tyres.

Third, sustainability pressures are accelerating the use of bio-based materials, recycled rubber, and low-emission manufacturing processes across the supply chain.

Fourth, OEM collaboration is deepening, with tyre development increasingly integrated into EV platform engineering to optimize efficiency and performance from the design stage.

Finally, smart tyre technologies are emerging as a key differentiator, enabling real-time monitoring of pressure, temperature, wear, and energy efficiency in connected EV ecosystems.

Strategic Implications of Value Chain & Supply Chain Evolution in Global Electric Vehicle (EV) Tyres Market

Leading manufacturers such as Michelin, Bridgestone, Goodyear, Continental, and Pirelli are strengthening their competitive position through heavy investments in EV-specific R&D, OEM partnerships, and smart mobility solutions.

The market presents high entry barriers due to complex technical requirements, stringent OEM certifications, and continuous innovation demands, resulting in strong dominance by established global players.

OEM relationships are becoming more integrated and long-term in nature, with tyre suppliers playing a critical role in EV range optimization and vehicle performance engineering.

Cost optimization remains a key challenge, as manufacturers balance high R&D expenditure with scaling production of EV-specific tyre lines while managing raw material price volatility.

The transition to EV mobility creates both disruption and opportunity, requiring innovation in energy efficiency, acoustic performance, and structural reinforcement while opening high-value premium tyre segments.

Global Electric Vehicle (EV) Tyres Market Value Chain & Supply Chain Evolution Forward Outlook

Between 2026 and 2033, the EV tyres value chain is expected to become increasingly technology-driven, sustainability-focused, and deeply integrated with digital mobility ecosystems.

Manufacturers will prioritize ultra-low rolling resistance tyres, advanced noise suppression systems, and next-generation smart tyres with embedded sensors for predictive analytics and fleet optimization.

The aftermarket segment will expand significantly as global EV fleets mature, creating strong long-term replacement demand across passenger EVs, SUVs, and light commercial electric vehicles.

Digital integration will become standard, with AI-powered tyre monitoring systems, connected vehicle platforms, and real-time performance tracking becoming core components of EV mobility ecosystems.

Overall, the future value chain will be defined by electrification, intelligence, sustainability, and performance efficiency, with companies that align innovation with EV platform requirements positioned for long-term leadership.

Market-Specific Value Chain

- Raw Material Procurement: High-silica compounds, synthetic rubber, carbon black, steel belts, acoustic foam materials

- Research & Development: Low rolling resistance design, noise reduction engineering, EV load optimization, smart tyre technologies

- Manufacturing: High-precision radial tyre production, reinforcement engineering, and EV-specific performance testing

- OEM Integration: Supply of tyres for electric passenger cars, SUVs, vans, and commercial EV platforms

- Distribution & Fleet Supply: EV OEM contracts, branded retail networks, EV service centers, and online tyre platforms

- Aftermarket Services: Replacement tyres, smart monitoring services, predictive maintenance, and lifecycle optimization solutions

Company-to-Stage Mapping

- Raw Material Procurement: Michelin, Bridgestone Corporation, Continental AG, Goodyear Tire & Rubber Company

- Research & Development: Michelin, Continental AG, Pirelli & C. S.p.A., Hankook Tire

- Manufacturing: Bridgestone Corporation, Goodyear Tire & Rubber Company, Yokohama Rubber Company, Sumitomo Rubber Industries

- OEM Integration: Michelin, Bridgestone Corporation, Continental AG, Pirelli & C. S.p.A.

- Distribution & Fleet Supply: Apollo Tyres, Hankook Tire, Yokohama Rubber Company, Toyo Tires

- Aftermarket Services: Michelin, Bridgestone Corporation, Continental AG, Goodyear Tire & Rubber Company

Investment Activity

Global Electric Vehicle (EV) Tyres Market Investment & Funding Dynamics Overview

Investment and funding dynamics in the Global Electric Vehicle (EV) Tyres Market are being driven by rapid global electrification, strict emission regulations, and increasing demand for energy-efficient mobility solutions. Between 2026 and 2033, capital allocation is expected to concentrate heavily on low rolling resistance technologies, noise-reduction tyre systems, smart connected tyres, and sustainable material innovation tailored specifically for electric vehicles. The market is highly R&D intensive, requiring continuous investment in advanced rubber compounds, reinforced casing structures, silica-based tread formulations, and acoustic engineering solutions. Leading manufacturers such as Michelin, Bridgestone, Continental, Goodyear, and Pirelli are significantly increasing R&D spending and expanding EV-dedicated production lines to support rising OEM and aftermarket demand. A key structural shift shaping investment flows is the increasing EV parc expansion across passenger cars, SUVs, and light commercial vehicles. This is accelerating funding into EV-specific tyre platforms designed to handle higher torque, heavier vehicle weight, and extended driving range requirements.

Global Electric Vehicle (EV) Tyres Market Investment & Funding Dynamics Current Scenario

Currently, investment activity is strongly supported by rising EV production volumes, government incentives for clean mobility, and stricter global emission standards. OEM partnerships between automakers and tyre manufacturers remain a primary focus area for securing long-term supply agreements. Asia-Pacific leads global investment activity due to China’s dominant EV production ecosystem and strong local tyre manufacturing capabilities supporting large-scale OEM demand. Europe is the fastest-growing investment region, driven by aggressive EV adoption targets, premium electric vehicle penetration, and sustainability-focused regulations that promote low-emission mobility solutions. North America continues to attract strong investments in premium EV segments, particularly electric SUVs and performance vehicles, along with expanding aftermarket replacement demand. Latin America and Middle East & Africa are emerging investment regions, supported by gradual EV adoption, infrastructure development, and increasing awareness of sustainable transportation solutions.

Key Investment & Funding Dynamics Signals in Global Electric Vehicle (EV) Tyres Market

A major investment signal is the rapid expansion of global EV sales, which is directly increasing demand for specialized tyres optimized for range efficiency, torque handling, and noise reduction. Growing focus on low rolling resistance technology is driving significant capital inflows into advanced silica compounds, lightweight construction methods, and energy-efficient tread designs. Rising demand for quiet cabin experiences in EVs is pushing investments into acoustic foam technology and vibration-dampening tyre structures. Expansion of EV aftermarket replacement cycles is creating long-term recurring revenue opportunities, encouraging sustained investment in distribution networks and service infrastructure. The increasing adoption of smart tyres with embedded sensors for real-time monitoring is unlocking new investment opportunities in connected mobility ecosystems and predictive maintenance platforms.

Strategic Implications of Investment & Funding Dynamics in Global Electric Vehicle (EV) Tyres Market

The investment landscape strongly favors established tyre manufacturers with deep OEM relationships and advanced EV-specific R&D capabilities, creating high entry barriers for new entrants. OEM collaborations with global EV manufacturers are critical for securing long-term contracts and ensuring early product integration into next-generation vehicle platforms. Technological innovation is becoming a key competitive differentiator, particularly in areas such as range optimization, noise reduction, and high-load structural reinforcement. Regional diversification remains essential, with Asia-Pacific leading volume production, Europe driving sustainability-led innovation, and North America focusing on premium EV performance segments. Volatility in raw material costs, particularly synthetic rubber, silica compounds, and petroleum-based inputs, continues to impact profitability, necessitating strategic sourcing and material innovation investments.

Global Electric Vehicle (EV) Tyres Market Investment & Funding Dynamics Forward Outlook

Looking ahead, the Global Electric Vehicle Tyres Market is expected to attract robust and sustained investment driven by accelerating global EV adoption and tightening environmental regulations. Future capital allocation will prioritize ultra-low rolling resistance tyres, next-generation noise-reduction systems, and high-durability EV tyres capable of supporting heavier and faster electric vehicles. Asia-Pacific will remain the dominant investment hub, while Europe will lead innovation in sustainable and premium EV tyre technologies. North America will continue to drive demand for high-performance electric SUVs and luxury EV segments. Digital transformation will further reshape investment patterns, with increased focus on smart tyres, real-time monitoring systems, and AI-driven predictive maintenance solutions for EV fleets. Overall, the market will continue its strong growth trajectory, supported by its critical role in improving EV efficiency, range, safety, and driving comfort. Companies that align innovation with sustainability, performance, and connectivity will be best positioned to lead through 2033.

Technology & Innovation

Global Electric Vehicle (EV) Tyres Market Technology & Innovation Landscape Overview

The technology and innovation landscape within the global electric vehicle (EV) tyres market is driven by electrification, sustainability, performance efficiency, and noise reduction requirements. EVs introduce unique challenges such as higher vehicle weight from batteries, instant torque delivery, and range sensitivity, all of which require highly specialized tyre engineering.

Innovation intensity in this market is very high compared to conventional tyre segments, with continuous advancements in low rolling resistance compounds, noise-reduction architectures, reinforced sidewall designs, and smart sensor integration. Leading manufacturers such as Michelin, Bridgestone Corporation, Goodyear Tire & Rubber Company, Continental AG, and Pirelli & C. S.p.A. are heavily investing in EV-specific tyre platforms designed to maximize range, durability, and comfort.

A major technological shift is the development of EV-optimized tyres engineered to handle higher torque loads and heavier vehicle mass while improving energy efficiency. These tyres also incorporate acoustic engineering solutions such as foam inserts and optimized tread sequencing to reduce cabin noise, which is more noticeable in silent EV environments.

Additionally, smart tyre technologies are emerging as a key innovation frontier, enabling real-time monitoring of tyre health, pressure, temperature, and wear to enhance safety and predictive maintenance capabilities.

Global Electric Vehicle (EV) Tyres Market Technology & Innovation Landscape Current Scenario

Currently, the EV tyre technology landscape is centered on improving driving range, durability, and comfort. Low rolling resistance tyres dominate innovation focus, as they directly contribute to extending EV battery range by minimizing energy loss during motion.

Silica-enhanced compounds and lightweight construction materials are widely used to reduce rolling resistance without compromising grip or braking performance. At the same time, reinforced carcass structures are being developed to support heavier EV battery loads and improve stability during high torque acceleration.

Noise reduction is another critical innovation area. Acoustic foam technology, variable pitch tread designs, and vibration-optimized patterns are being integrated into EV tyres to enhance cabin comfort and meet premium vehicle expectations.

High load-bearing EV tyres are gaining importance, especially in electric SUVs and commercial EVs, where battery weight significantly increases stress on tyres. These tyres use reinforced sidewalls and stronger internal structures to maintain durability and safety.

Smart and connected tyre technologies are gradually entering the EV ecosystem. Embedded sensors allow continuous monitoring of tyre pressure, temperature, and wear conditions, enabling predictive maintenance and improving fleet efficiency in electric mobility services.

Manufacturing innovation is also evolving, with increased use of automation, AI-driven quality control, and sustainable materials such as bio-based rubber and recycled compounds. These advancements align with global carbon reduction goals and EV ecosystem sustainability requirements.

Key Technology & Innovation Landscape Signals in Global Electric Vehicle (EV) Tyres Market

- Low Rolling Resistance Technology: Enhances EV driving range and energy efficiency.

- Noise Reduction Engineering: Acoustic foam and optimized tread patterns for quieter cabins.

- High Load-Bearing Structures: Reinforced sidewalls for heavy EV battery packs.

- EV-Specific Compound Materials: Silica-rich and lightweight rubber blends for efficiency and grip.

- Smart & Connected Tyres: IoT-enabled sensors for real-time monitoring and predictive maintenance.

- High Torque Resistance Design: Tread patterns optimized for instant EV acceleration.

- Sustainable Materials Adoption: Use of bio-rubber and recycled compounds to reduce carbon footprint.

Strategic Implications of Technology & Innovation Landscape in Global Electric Vehicle (EV) Tyres Market

The evolving EV tyre technology landscape has major strategic implications for tyre manufacturers, OEMs, and mobility providers. Continuous R&D investment is essential to meet evolving EV performance requirements such as extended range, durability under high torque, and noise reduction.

The rapid expansion of electric vehicle adoption is reshaping product development priorities. Tyre manufacturers must collaborate closely with EV OEMs to design vehicle-specific tyre solutions optimized for weight distribution, battery load, and aerodynamic efficiency.

Smart tyre technologies are enabling a shift toward data-driven mobility ecosystems. Predictive maintenance, real-time analytics, and fleet monitoring capabilities are creating new service-based revenue models beyond traditional tyre sales.

Sustainability is a key strategic pillar, with increasing adoption of eco-friendly materials, circular economy practices, and low-carbon manufacturing processes. Regulatory pressure and consumer expectations are accelerating this transition.

For EV manufacturers and fleet operators, tyres play a critical role in overall vehicle efficiency. Optimized tyres directly influence driving range, energy consumption, safety, and passenger comfort, making them a core component of EV performance engineering.

Global Electric Vehicle (EV) Tyres Market Technology & Innovation Landscape Forward Outlook

Looking ahead, the EV tyres market is expected to evolve rapidly toward intelligent, ultra-efficient, and highly sustainable tyre solutions. Electrification will remain the dominant driver, pushing demand for specialized tyres that maximize range and minimize energy loss.

Smart tyre systems are expected to become standard across EV platforms, enabling real-time diagnostics, AI-driven performance optimization, and predictive maintenance integration with vehicle systems.

Material innovation will continue to advance, focusing on ultra-lightweight compounds, high-durability formulations, and sustainable raw materials that reduce environmental impact while improving performance.

Manufacturing processes will become increasingly automated and digitally optimized, with AI-based inspection systems improving quality consistency and accelerating innovation cycles.

In conclusion, the Global Electric Vehicle (EV) Tyres Market is undergoing rapid technological transformation where efficiency, connectivity, and sustainability are the core innovation pillars. Companies that successfully develop low rolling resistance technologies, advanced noise reduction systems, smart tyre solutions, and sustainable materials will lead the EV tyre ecosystem through 2033.

Market Risk

Global Electric Vehicle (EV) Tyres Market Risk Factors & Disruption Threats Overview

The Global Electric Vehicle (EV) Tyres Market operates in a fast-scaling, innovation-heavy environment, driven by rapid EV adoption, stricter emission regulations, and shifting consumer preferences toward sustainable mobility. While the market benefits from strong OEM integration and rising replacement demand, it carries a high risk profile due to rapid technology evolution, cost pressures, and intense performance requirements. A major structural risk is raw material volatility, particularly natural rubber, synthetic rubber, silica compounds, steel, and specialty polymers. EV tyres require advanced material blends for low rolling resistance and durability, meaning cost fluctuations directly impact profitability and pricing stability across OEM contracts. Another key disruption factor is fast-changing EV platform design cycles. Automakers frequently update EV architectures, battery sizes, and vehicle weight structures, forcing tyre manufacturers to continuously redesign products and shorten development cycles, increasing R&D costs and execution risk. Higher vehicle weight and instant torque in EVs also create accelerated tyre wear. This leads to shorter replacement cycles but increases technical pressure on manufacturers to improve durability, grip, and load-bearing capacity without compromising energy efficiency. Additionally, intense competition from both global tyre majors and emerging regional EV-focused players is increasing pricing pressure and innovation speed, making differentiation increasingly dependent on technology leadership rather than cost alone.

Global Electric Vehicle (EV) Tyres Market Risk Factors & Disruption Threats Current Scenario

The current market scenario reflects strong expansion supported by rising EV penetration, government incentives, and OEM electrification targets. However, this growth is accompanied by rising material costs, technological complexity, and supply chain dependencies. Raw material inflation and dependency on advanced compounds remain a key challenge, especially for low rolling resistance and noise-reduction tyres, which require specialized inputs and precision manufacturing processes. The OEM segment dominates EV tyre demand, but automakers exert strong pricing pressure through bundled supply agreements, limiting margin expansion for tyre manufacturers despite rising volumes. Aftermarket demand is growing rapidly as early EV fleets age, but it is fragmented and highly competitive, with increasing presence of online tyre platforms and multi-brand retail channels intensifying price transparency. At the same time, supply chain disruptions in specialty chemicals, silica, and sensor components continue to impact production stability, particularly for smart and connected EV tyres.

Key Risk Factors & Disruption Threats Signals in Global Electric Vehicle (EV) Tyres Market

A key risk signal is the rapid acceleration of EV adoption across multiple vehicle categories, including SUVs, commercial vans, and performance EVs. This is increasing demand variability and forcing faster product adaptation cycles. Another major signal is the rising importance of smart mobility ecosystems. The integration of connected tyres, vehicle telematics, and predictive maintenance systems is shifting competition toward data-driven tyre performance solutions. The increasing dominance of EV SUVs and high-performance electric vehicles is also reshaping demand toward larger rim sizes, reinforced sidewalls, and high-load tyre architectures. Sustainability regulations and ESG-driven procurement policies are becoming stronger signals, pushing manufacturers toward bio-based materials, recyclable compounds, and low-carbon production processes. Additionally, the expansion of EV-focused aftermarket ecosystems is increasing competition from digital tyre retailers, subscription-based tyre services, and fleet maintenance platforms.

Strategic Implications of Risk Factors & Disruption Threats in Global Electric Vehicle (EV) Tyres Market

Manufacturers must prioritize low rolling resistance, high load-bearing strength, and noise reduction as core engineering requirements to remain competitive in the EV ecosystem. Strong collaboration with OEMs is essential, as EV platforms are tightly integrated with tyre specifications, making early-stage design partnerships critical for long-term contracts. Investment in smart tyre technologies, including embedded sensors and real-time monitoring systems, is becoming a key differentiator in premium EV segments. Supply chain resilience and material innovation strategies are necessary to manage dependency on specialized compounds while ensuring consistent performance standards across global markets. Digital transformation, including data-driven tyre analytics and predictive maintenance platforms, is emerging as a strategic lever for value-added services and recurring revenue generation.

Global Electric Vehicle (EV) Tyres Market Risk Factors & Disruption Threats Forward Outlook

Looking ahead to 2026-2033, the Global EV Tyres Market will continue to expand rapidly, driven by electrification mandates, EV adoption growth, and technological innovation. However, the risk landscape will become increasingly technology-intensive and competitive. EV platform diversification will remain a major disruptive force, requiring continuous innovation across passenger EVs, SUVs, and electric commercial fleets with varying load and performance requirements. Smart mobility integration will accelerate, with connected tyres becoming a standard feature in premium and fleet EV segments, shifting industry competition toward data-enabled ecosystems. Sustainability pressures will further reshape material innovation, increasing adoption of eco-friendly compounds, recyclable materials, and carbon-neutral manufacturing practices. Overall, the market will remain high-growth but innovation-intensive, with success depending on manufacturers’ ability to balance performance, efficiency, durability, and sustainability while aligning closely with rapidly evolving EV platforms.

Regulatory Landscape

Global Electric Vehicle (EV) Tyres Market Regulatory & Policy Environment Overview

The regulatory and policy environment governing the Global Electric Vehicle (EV) Tyres Market is becoming increasingly important as governments accelerate the transition toward electric mobility. EV tyres directly influence vehicle range, energy efficiency, safety, and noise levels, making them a key focus area within broader transport decarbonization frameworks and automotive compliance regulations. Key global regulatory frameworks such as the European Union Tyre Labelling Regulation (EU) 2020/740 and UNECE tyre performance standards define mandatory benchmarks for rolling resistance, wet grip, and external noise. In the EV segment, these parameters carry additional importance, as even minor efficiency gains can significantly extend driving range and reduce battery consumption. In addition, national and regional EV adoption policies’such as zero-emission vehicle (ZEV) mandates, fuel economy regulations, and carbon neutrality roadmaps’are indirectly shaping tyre innovation. These frameworks are pushing manufacturers to develop low rolling resistance, high-load-bearing, and noise-optimized tyres tailored specifically for electric passenger cars, SUVs, vans, and commercial EV fleets. Environmental regulations focused on sustainability are also influencing material innovation in EV tyres. Requirements related to carbon footprint reduction, recycled content usage, and sustainable raw material sourcing are encouraging the adoption of bio-based rubber compounds, silica-enhanced formulations, and circular economy-driven tyre designs.

Global Electric Vehicle (EV) Tyres Market Regulatory & Policy Environment Current Scenario

The current regulatory landscape is strongly shaped by accelerating EV adoption targets and tightening emissions standards across major automotive markets. Europe leads in regulatory maturity, where strict CO reduction targets and EV incentives are directly accelerating demand for EV-optimized tyre technologies across OEM and replacement channels. In Europe, low noise regulations in urban mobility zones are particularly influential, driving adoption of acoustic foam-lined tyres and advanced tread designs that reduce cabin noise in electric vehicles. Fleet operators and OEMs are increasingly required to meet strict efficiency and sustainability criteria when selecting tyres for EV platforms. In Asia-Pacific, large-scale EV manufacturing hubs such as China are enforcing stringent NEV (New Energy Vehicle) policies that indirectly impact tyre performance standards. Government subsidies, local EV production mandates, and fleet electrification programs are driving rapid OEM adoption of EV-specific tyres optimized for high torque and heavy battery loads. North America continues to evolve through federal and state-level EV incentives, combined with fuel efficiency and safety standards that encourage adoption of low rolling resistance tyres. The growing penetration of electric SUVs and pickup trucks is further influencing demand for high-load EV tyre solutions. At the same time, global safety authorities are placing increased emphasis on tyre durability and thermal stability due to the higher weight and torque characteristics of EVs, prompting updated testing and certification requirements across multiple regions.

Key Regulatory & Policy Environment Signals in Global Electric Vehicle (EV) Tyres Market

- EU Tyre Labelling Regulation (EU 2020/740): Drives performance transparency in rolling resistance, wet grip, and noise levels for EV efficiency optimization.

- UNECE Tyre Safety Standards: Establish global safety and durability benchmarks, increasingly relevant for high-torque EV applications.

- Zero-Emission Vehicle (ZEV) Mandates: Accelerate EV adoption, indirectly boosting demand for EV-optimized tyre technologies.

- Fuel Efficiency & CO Reduction Policies: Encourage adoption of low rolling resistance tyres to improve vehicle energy efficiency and range.

- Urban Noise Pollution Regulations: Drive demand for acoustic and low-noise EV tyre solutions in dense city environments.

- Sustainability & Circular Economy Policies: Promote use of recycled materials, bio-based rubber, and eco-friendly tyre manufacturing processes.

Strategic Implications of Regulatory & Policy Environment in Global Electric Vehicle (EV) Tyres Market

The evolving regulatory framework is significantly increasing technological barriers to entry, favoring established tyre manufacturers with strong R&D capabilities and OEM partnerships. Compliance with EV-specific performance requirements’such as torque resistance, thermal stability, and noise reduction’is becoming a critical differentiator in the market. Manufacturers are increasingly investing in advanced material science, including silica-based compounds, lightweight structures, and sustainable rubber alternatives to align with tightening environmental and efficiency regulations. Smart tyre technologies with embedded sensors are also gaining importance as regulatory focus shifts toward real-time monitoring and predictive safety systems. OEMs are playing a more dominant role in tyre selection due to stricter EV platform integration requirements. As a result, tyre suppliers are forming deeper strategic partnerships with EV manufacturers to co-develop application-specific solutions tailored for range optimization and vehicle performance. Regional regulatory differences are also influencing market strategies, with companies adapting product portfolios to meet Europe’s strict sustainability standards, Asia-Pacific’s large-scale EV deployment programs, and North America’s performance-focused regulatory environment.

Global Electric Vehicle (EV) Tyres Market Regulatory & Policy Environment Forward Outlook

Between 2026 and 2033, the regulatory environment is expected to become significantly more stringent as global EV penetration accelerates and governments intensify decarbonization efforts. Regulations will increasingly focus on lifecycle emissions, energy efficiency, and sustainable material usage in tyre manufacturing. Europe is expected to lead in regulatory advancement, expanding requirements for carbon footprint disclosure, recycled material integration, and lifecycle sustainability reporting for tyre manufacturers. Asia-Pacific will continue strengthening EV-specific safety and performance standards as production volumes scale. The rise of next-generation EVs’including long-range SUVs, autonomous electric vehicles, and commercial electric fleets’will introduce new regulatory expectations around load capacity, energy efficiency, and acoustic performance. This will further drive innovation in smart, connected, and high-efficiency tyre technologies. Overall, the regulatory and policy environment will remain a powerful growth catalyst while simultaneously increasing compliance complexity. Manufacturers that align product innovation with sustainability goals, EV performance requirements, and digital tyre intelligence will be best positioned to lead the Global Electric Vehicle (EV) Tyres Market through 2033.