Global All-Season Car Tyres Market size and share Analysis 2026-2033

Market Forecast Snapshot (2026???2033)

| Metric | Value |

|---|---|

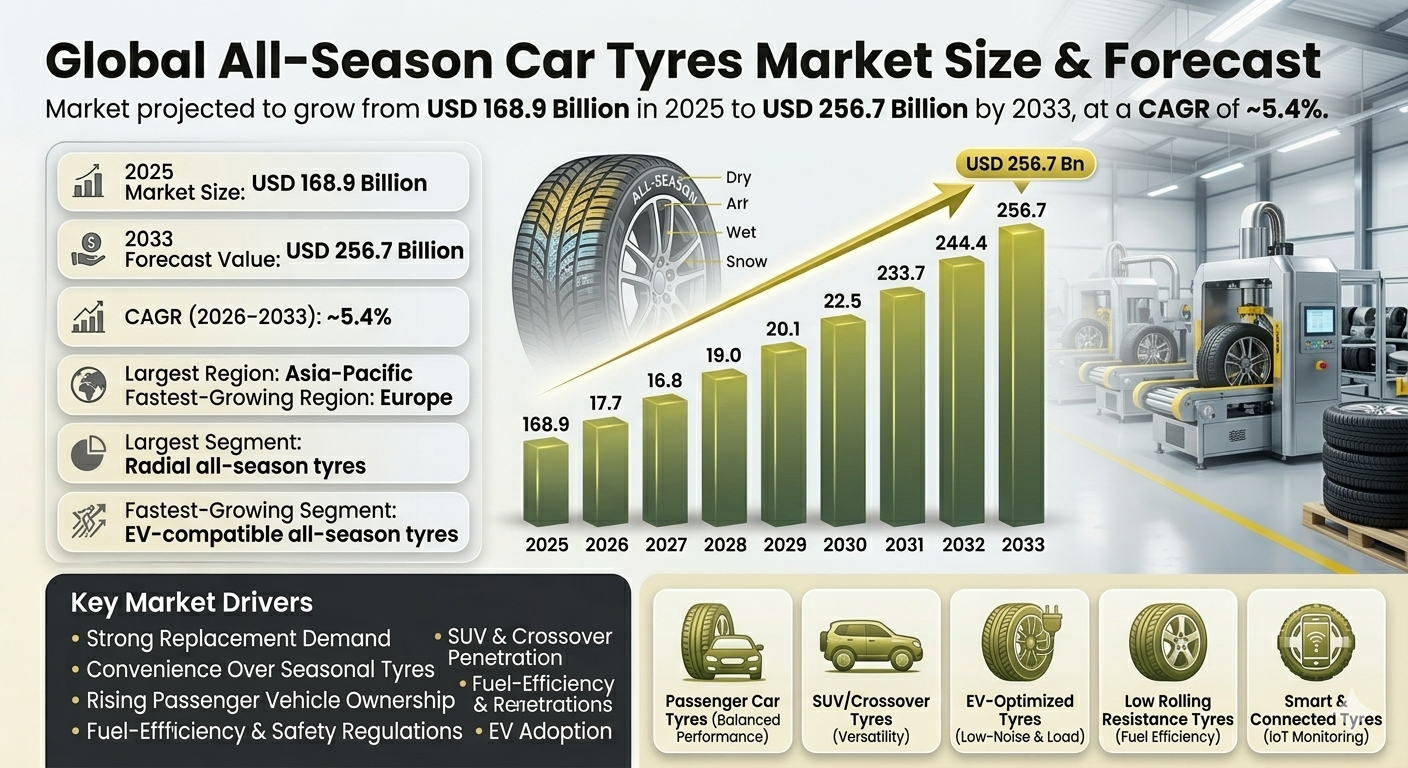

| 2025 Market Size | USD 168.9 Billion |

| 2033 Market Size | USD 256.7 Billion |

| CAGR (2026???2033) | ~5.4% |

| Largest Region | Asia-Pacific |

| Fastest-Growing Region | Europe |

| Largest Segment | Radial all-season tyres |

| Fastest-Growing Segment | EV-compatible all-season tyres |

| Key Trend | Convenience-driven & low rolling resistance tyres |

Global All-Season Car Tyres Market Overview

The Global All-Season Car Tyres Market focuses on tyres engineered to perform reliably across dry, wet, and light winter conditions, eliminating the need for seasonal tyre changes. These tyres combine balanced tread designs and adaptable rubber compounds to deliver year-round safety, ride comfort, durability, and fuel efficiency.

All-season tyres are super popular for everyday cars - hatchbacks, sedans, SUVs, you name it . They are a no-brainer for people who want convenience and decent performance in normal weather. Car makers fit 'em as standard in the Global All-Season Car Tyres Market, and people buy 'em again when they need replacements 'cause they're practical and easy on the pocket

According to the Pheonix Demand Forecast Engine, the Global All-Season Car Tyres Market size is estimated at USD 168.9 billion in 2025 and is projected to reach USD 256.7 billion by 2033, expanding at a CAGR of ~5.4% during the forecast period (2026???2033).

Asia-Pacific represents the largest regional market, supported by massive passenger vehicle parc, high replacement demand, and widespread use of all-season tyres in urban mobility across China and India. Europe is the fastest-growing region, driven by increasing preference for all-season tyres as an alternative to winter tyres, rising SUV adoption, and growing regulatory focus on fuel efficiency, safety, and low-noise tyre solutions.

Key Drivers of Global All-Season Car Tyres Market Growth

-

Strong Replacement Demand

Regular tread wear drives growth in aftermarket sales. People need replacements, so it's a win-win for tyre makers. -

Convenience Over Seasonal Tyres

Consumers prefer single-tyre solutions for year-round use, boosting growth in all-season tyre sales . No need to switch tyres seasonally, it's convenient and hassle-free. -

Rising Passenger Vehicle Ownership

More cars on the road in emerging and developed markets growth in tyre demand . As the vehicle parc expands, tyre makers are smiling . -

SUV & Crossover Penetration

The need for versatile tyres that handle mixed driving conditions is driving strong growth .People want tyres that can tackle city streets, highways, and a bit of off-roading, all year-round. -

Fuel-Efficiency & Safety Regulations

Tough tyre regulations are actually boosting growth in premium all-season tyres .With mandatory labelling and stricter rolling-resistance norms, top-notch tyres are in demand. -

EV Adoption

Demand for low-noise, high-load all-season tyres compatible with electric vehicles.

Regional Insights of Global All-Season Car Tyres Market

Asia-Pacific ??? Largest Market

High passenger vehicle ownership, massive replacement demand, and cost-sensitive preference for all-season tyres in China and India.

Europe ??? Fastest-Growing Region

Driven by fuel-efficiency regulations, premium all-season tyres, and increasing EV penetration.

North America

Strong SUV dominance, large vehicle parc, and preference for convenience-oriented tyres.

Latin America

Growing vehicle ownership and expanding replacement demand.

Middle East & Africa

Demand supported by urbanization and rising passenger vehicle fleets.

Leading Companies in the Global All-Season Car Tyres Market

-

Goodyear Tire & Rubber Company

-

Continental AG

-

Pirelli & C. S.p.A.

-

Sumitomo Rubber Industries

-

Hankook Tire

-

Yokohama Rubber Company

-

Toyo Tires

-

Apollo Tyres?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? Michelin and Bridgestone Corporation is the largest company in the Global All-Season Car Tyres Market.

Strategic Intelligence & Pheonix AI-Backed Insights

-

Pheonix Demand Forecast Engine

Tracks vehicle parc growth, replacement cycles, and SUV share. -

EV Tyre Compatibility Analyzer

Evaluates low-noise and low-rolling-resistance tyre demand. -

Raw Material Sensitivity Model

Assesses rubber, silica, and oil price impact on margins.

Why the Global All-Season Car Tyres Market Is Critical

All-season car tyres play a vital role in ensuring everyday vehicle safety, as they directly influence braking performance, road grip, steering control, and vehicle stability across dry, wet, and light winter conditions. For millions of daily commuters, these tyres provide a reliable, year-round solution without the complexity of seasonal tyre changes.

The market benefits from strong and predictable replacement demand, as all-season tyres experience regular wear due to continuous year-round usage. Unlike seasonal tyres that are rotated, all-season tyres remain on vehicles throughout the year, leading to consistent aftermarket sales and long-term revenue stability for manufacturers and distributors.

Final Takeaway of Global All-Season Car Tyres Market

The Global All-Season Car Tyres Market represents a resilient, replacement-driven, and steadily expanding segment of the global tyre industry, underpinned by strong consumer preference for convenience, year-round usability, and cost efficiency. As vehicle ownership continues to rise and urban mobility intensifies, all-season tyres remain the preferred choice for everyday passenger vehicles across moderate-climate regions.

Growth momentum is increasingly shaped by technological evolution and vehicle electrification. EV-compatible all-season tyres, designed with low rolling resistance, higher load capacity, and noise-reduction features, are emerging as a key growth engine. At the same time, premium comfort-focused all-season tyres with advanced tread designs, acoustic technologies, and improved wet-grip performance are gaining traction among urban and mid-to-high income consumers.

Competitive Landscape

Global All-Season Car Tyres Market Competitive Intensity & Market Structure Overview

The global all-season car tyres market exhibits a moderately fragmented to moderately consolidated structure, characterized by the presence of several dominant global players alongside strong regional and mid-tier manufacturers. Leading companies such as Michelin, Bridgestone Corporation, Goodyear Tire & Rubber Company, Continental AG, and Pirelli & C. S.p.A. form the competitive core, supported by a wide network of regional players including Hankook Tire, Yokohama Rubber Company, Sumitomo Rubber Industries, Toyo Tires, and Apollo Tyres. Despite this concentration, the market remains highly competitive due to the commoditized nature of all-season tyres and intense price sensitivity in mass-market segments. Entry barriers are moderate compared to premium tyre segments, as manufacturing capabilities are more standardized and regulatory requirements, while significant, are less technologically demanding than ultra-high-performance or luxury tyres. However, scale, distribution reach, brand trust, and OEM relationships create indirect barriers that favor established players. Differentiation is increasingly driven by performance enhancements such as low rolling resistance, noise reduction, durability, and EV compatibility, rather than purely structural innovation. The market’s structure is heavily influenced by the dominance of the aftermarket segment, which accounts for the majority of sales due to continuous year-round usage and regular replacement cycles. OEM fitments provide volume stability and brand visibility, but competition intensifies significantly in the replacement market where pricing, availability, and brand loyalty play critical roles. As a result, the market reflects a balance between scale-driven consolidation and widespread competitive participation.

Global All-Season Car Tyres Market Competitive Intensity & Market Structure Current Scenario

Leading Company Profiles

Michelin: Global leader with strong presence in fuel-efficient and long-lasting all-season tyres, leveraging advanced compound technologies and sustainability initiatives. Bridgestone Corporation: Major player with a broad portfolio of all-season tyres, focusing on durability, efficiency, and expanding digital retail capabilities. Goodyear Tire & Rubber Company: Strong in replacement markets with a wide distribution network and increasing focus on EV-compatible all-season tyres. Continental AG: Technology-driven manufacturer emphasizing safety, low rolling resistance, and smart tyre integration. Pirelli & C. S.p.A.: Premium-focused player expanding into high-end all-season tyres with performance and comfort features. Sumitomo Rubber Industries: Offers durable and cost-effective all-season tyres with a focus on balanced performance. Hankook Tire: Rapidly growing competitor strengthening its position through OEM partnerships and competitive pricing strategies. Yokohama Rubber Company: Performance-oriented tyre manufacturer with strong presence in Asia and North America. Toyo Tires: Known for value-driven all-season tyres with reliable performance in urban and highway conditions. Apollo Tyres: Expanding global footprint with cost-competitive offerings and strong presence in emerging markets.

Key Competitive Intensity & Market Structure Signals in Global All-Season Car Tyres Market

The competitive landscape of the all-season car tyres market is strongly influenced by high-volume replacement demand and increasing consumer preference for convenience-oriented products. Manufacturers are continuously enhancing tyre longevity, fuel efficiency, and wet-grip performance to differentiate within a largely standardized product category. Michelin and Bridgestone, for instance, are focusing on extending tyre life cycles and improving rolling resistance to align with regulatory requirements and consumer demand for cost efficiency. A significant competitive signal is the growing emphasis on EV-compatible all-season tyres. As electric vehicle adoption rises, tyre manufacturers are introducing products designed to handle higher vehicle weight, deliver lower noise levels, and reduce energy consumption. This shift is gradually redefining product benchmarks and intensifying R&D competition even within a traditionally stable segment. Distribution strategy also plays a crucial role in shaping competition. The expansion of online tyre retail platforms and direct-to-consumer channels is transforming the aftermarket landscape. Companies such as Goodyear and Continental are investing in digital ecosystems, offering online fitment tools, doorstep installation services, and integrated customer engagement platforms to strengthen market reach and brand loyalty. Regulatory pressures, particularly in Europe, are another key signal influencing competitive dynamics. Stricter labeling requirements related to fuel efficiency, wet grip, and noise levels are pushing manufacturers to upgrade product performance. These regulations are not only driving innovation but also increasing compliance costs, favoring larger players with established R&D and testing capabilities.

Key Competitive Intensity & Market Structure Signals in Global All-Season Car Tyres Market

A deeper analysis indicates that competition is increasingly shifting from price-driven dynamics toward performance and efficiency differentiation. While cost competitiveness remains critical in emerging markets, developed regions are witnessing a transition toward premium all-season tyres offering enhanced safety, comfort, and fuel efficiency. This evolution is narrowing the gap between standard and premium segments, intensifying competition among leading brands. OEM relationships continue to influence competitive positioning, although their impact is less pronounced compared to premium tyre markets. Securing OEM contracts still provides brand credibility and steady volumes, but the real competitive battleground lies in the aftermarket, where consumer choice, retailer influence, and pricing strategies determine market share. Supply chain optimization and raw material management are also emerging as critical competitive factors. Fluctuations in rubber and oil prices directly impact production costs and margins, compelling companies to invest in procurement efficiency and alternative materials. Larger players benefit from economies of scale and global sourcing capabilities, further strengthening their competitive advantage. Additionally, regional market dynamics play a significant role in shaping competition. Asia-Pacific, as the largest market, is highly price-sensitive and volume-driven, favoring cost-efficient manufacturers. In contrast, Europe’s regulatory environment and consumer preferences for high-performance tyres are pushing companies toward premiumization, creating a dual-speed competitive landscape globally.

Strategic Implications of Competitive Intensity & Market Structure in Global All-Season Car Tyres Market

The current competitive environment necessitates a balanced strategic approach combining cost efficiency, product innovation, and distribution strength. Firstly, manufacturers must focus on optimizing production costs while maintaining consistent quality, particularly to remain competitive in price-sensitive markets such as Asia-Pacific and Latin America. Secondly, innovation in EV-compatible and low rolling resistance tyres is becoming increasingly important. As electrification accelerates, companies that proactively develop tyres tailored to EV requirements will gain a competitive edge and capture emerging demand segments. Thirdly, strengthening aftermarket presence is critical for sustained revenue growth. Investments in digital sales channels, partnerships with retailers, and enhanced customer engagement strategies will be essential to capture replacement demand and build long-term brand loyalty. Additionally, geographic diversification and localization strategies are key to addressing varying regional demand patterns. Companies must tailor their product offerings, pricing strategies, and distribution models to align with local market conditions, regulatory environments, and consumer preferences. Finally, regulatory compliance and sustainability initiatives are becoming strategic priorities. Companies that successfully meet evolving environmental standards while maintaining performance and affordability will strengthen their competitive positioning, particularly in developed markets.

Global All-Season Car Tyres Market Competitive Intensity & Market Structure Forward Outlook

Looking ahead to 2026-2033, the global all-season car tyres market is expected to maintain a moderately fragmented yet highly competitive structure. While leading global players will continue to dominate through scale and brand strength, regional manufacturers will remain relevant by leveraging cost advantages and localized strategies. The increasing adoption of electric vehicles will act as a key catalyst for competitive evolution, driving demand for advanced all-season tyres with enhanced efficiency, durability, and noise reduction capabilities. This trend will gradually elevate technological requirements and intensify competition among established players. Digital transformation of the aftermarket is expected to accelerate, reshaping distribution models and customer engagement. Companies that successfully integrate online and offline channels will gain a significant competitive advantage in capturing replacement demand. Europe’s regulatory landscape and Asia-Pacific’s volume-driven growth will continue to create distinct competitive environments, requiring differentiated strategies. Meanwhile, ongoing innovation in materials, tread design, and smart tyre technologies will further redefine product differentiation. In conclusion, the global all-season car tyres market will remain a high-volume, resilience-driven segment marked by steady growth, evolving technology, and sustained competitive intensity. Companies that effectively balance cost leadership with innovation and distribution excellence will be best positioned to succeed in this dynamic market.

Value Chain

Global All-Season Car Tyres Market Value Chain & Supply Chain Evolution Overview

The value chain and supply chain dynamics within the global all-season car tyres market are fundamental in shaping production efficiency, cost structures, and competitive positioning. The market operates through a hybrid structure that integrates raw material suppliers, tyre manufacturers, OEM partnerships, distributor networks, and aftermarket service providers. This interconnected ecosystem ensures the continuous flow of products from manufacturing facilities to end consumers across both OEM and replacement channels. The complexity of the supply chain stems primarily from the diverse range of raw materials required, including natural rubber, synthetic rubber, carbon black, silica, steel cords, and specialty chemicals. Leading tyre manufacturers such as Michelin, Bridgestone Corporation, Goodyear Tire & Rubber Company, and Continental AG maintain strong upstream supplier relationships and, in many cases, vertically integrated procurement strategies to manage price volatility and ensure consistent quality. Manufacturing processes represent a critical stage in the value chain, involving compounding, tread design engineering, curing, and testing. Advanced technologies such as low rolling resistance compounds and noise-reduction designs further increase manufacturing complexity. These innovations are essential for meeting evolving regulatory requirements and consumer expectations, particularly in fuel efficiency and EV compatibility. Distribution in the all-season tyre market is characterized by a dual-channel model, combining OEM fitment and a dominant aftermarket segment. The aftermarket channel, comprising authorized dealers, independent retailers, and online platforms, plays a crucial role in driving volume due to recurring replacement demand. This structure adds layers to the supply chain but enhances market penetration and accessibility. Supply chain bottlenecks are largely influenced by fluctuations in raw material prices, logistics disruptions, and regulatory compliance requirements. Additionally, the need to balance cost efficiency with performance innovation places pressure on manufacturers’ margins. Companies that effectively manage procurement, optimize production, and strengthen distribution networks are better positioned to maintain profitability and market share.

Global All-Season Car Tyres Market Value Chain & Supply Chain Evolution Current Scenario

Currently, the global all-season car tyres market reflects a stable yet evolving supply chain landscape driven by strong replacement demand and shifting automotive trends. At the upstream level, raw material price volatility’particularly in natural rubber and petrochemical derivatives’continues to influence cost structures and pricing strategies. Manufacturers are increasingly adopting strategic sourcing and long-term supplier agreements to mitigate these risks. In the manufacturing stage, leading players such as Michelin, Bridgestone, and Continental are investing heavily in advanced tread compounds and EV-compatible tyre technologies. The integration of low rolling resistance materials and noise-reduction features has become a priority, especially as electric vehicle adoption accelerates. However, these innovations come with higher production costs and increased R&D expenditure. OEM partnerships remain a critical channel, with automakers increasingly demanding tyres that align with vehicle performance, fuel efficiency, and sustainability goals. At the same time, the aftermarket segment continues to dominate revenue generation due to predictable replacement cycles. Independent retailers and digital sales platforms are expanding their footprint, improving accessibility and customer reach. Logistics and distribution networks have become more resilient post-pandemic, yet challenges persist in terms of inventory management and last-mile delivery. The growing importance of e-commerce in tyre sales is reshaping distribution strategies, requiring manufacturers and distributors to integrate digital capabilities into traditional supply chains. After-sales services, including installation, maintenance, and tyre monitoring, are gaining prominence as key differentiators. Companies are leveraging these services to enhance customer retention and generate additional revenue streams, particularly in urban markets with high vehicle density.

Key Value Chain & Supply Chain Evolution Signals in Global All-Season Car Tyres Market

Several important signals are shaping the evolution of the value chain and supply chain in this market. First, the rise of electric vehicles is significantly altering product design and manufacturing requirements, driving demand for specialized all-season tyres with enhanced load capacity, durability, and low noise characteristics. Second, increasing regulatory pressure related to fuel efficiency, rolling resistance, and environmental sustainability is pushing manufacturers toward innovation in materials and production processes. Compliance with these standards adds complexity but also creates opportunities for premium product differentiation. Third, the dominance of the replacement market highlights the importance of efficient distribution networks and strong retailer relationships. Companies are focusing on strengthening their aftermarket presence through both offline and online channels to capture recurring demand. Fourth, raw material price fluctuations remain a persistent challenge, impacting margins and necessitating cost optimization strategies. Manufacturers are exploring alternative materials and recycling initiatives to reduce dependency on traditional inputs. Finally, digital transformation is emerging as a critical enabler across the value chain. From predictive demand forecasting to connected tyre technologies, digital tools are improving operational efficiency, inventory management, and customer engagement.

Strategic Implications of Value Chain & Supply Chain Evolution in Global All-Season Car Tyres Market

The evolving value chain dynamics present significant strategic implications for industry participants. Large multinational tyre manufacturers such as Michelin, Bridgestone, and Goodyear benefit from economies of scale, strong supplier networks, and extensive distribution channels, enabling them to maintain competitive advantage and margin stability. The increasing complexity of manufacturing and regulatory compliance creates high entry barriers, limiting the ability of smaller players to compete effectively. As a result, market consolidation is likely to intensify, with leading companies strengthening their positions through innovation and strategic partnerships. Distributors and retailers are also undergoing transformation, with a growing emphasis on value-added services such as tyre installation, maintenance, and digital sales platforms. These capabilities are essential for maintaining relevance in an increasingly competitive aftermarket landscape. From a cost perspective, managing raw material volatility and optimizing production efficiency are critical for sustaining profitability. Companies that invest in advanced manufacturing technologies and supply chain optimization are better equipped to navigate these challenges. Additionally, the shift toward EV-compatible tyres presents both opportunities and risks. While it opens new revenue streams, it also requires substantial investment in R&D and production capabilities. Firms that can align their product portfolios with EV trends will gain a significant competitive edge.

Global All-Season Car Tyres Market Value Chain & Supply Chain Evolution Forward Outlook

Looking ahead to the 2026-2033 period, the value chain and supply chain of the global all-season car tyres market are expected to evolve in response to technological advancements, regulatory changes, and shifting consumer preferences. The increasing adoption of electric vehicles will remain a key driver, necessitating continuous innovation in tyre design and materials. Manufacturers are likely to deepen their focus on sustainability, incorporating eco-friendly materials and energy-efficient production processes. This shift will not only address regulatory requirements but also align with growing consumer awareness of environmental impact. The aftermarket segment will continue to dominate, supported by expanding vehicle parc and consistent replacement demand. Digital platforms and e-commerce channels are expected to play an increasingly important role in distribution, enhancing convenience and accessibility for consumers. Supply chain resilience will remain a priority, with companies investing in diversified sourcing strategies and advanced logistics solutions to mitigate risks associated with disruptions. Collaboration across the value chain’from raw material suppliers to distributors’will be essential for maintaining efficiency and responsiveness. In summary, the future of the all-season car tyres market value chain will be defined by innovation, digitalization, and sustainability. Companies that successfully integrate these elements into their operations will be well-positioned to capture growth opportunities and maintain competitive advantage in a dynamic global market.

Market-Specific Value Chain

- Raw Material Procurement: Natural rubber, synthetic rubber, silica, carbon black, and steel cords sourcing

- Research & Development: Tread design, compound innovation, and EV-compatible tyre development

- Manufacturing: Tyre compounding, molding, curing, and quality testing

- OEM Integration: Supply of tyres for new passenger cars, SUVs, and EVs

- Distribution & Retail: Dealer networks, independent retailers, and e-commerce platforms

- Aftermarket Services: Installation, maintenance, replacement, and tyre monitoring

Company-to-Stage Mapping

- Raw Material Procurement: Michelin, Bridgestone Corporation, Continental AG, Goodyear Tire & Rubber Company

- Research & Development: Michelin, Continental AG, Pirelli & C. S.p.A., Sumitomo Rubber Industries

- Manufacturing: Bridgestone Corporation, Goodyear Tire & Rubber Company, Hankook Tire, Yokohama Rubber Company

- OEM Integration: Michelin, Bridgestone Corporation, Continental AG, Apollo Tyres

- Distribution & Retail: Goodyear Tire & Rubber Company, Apollo Tyres, Toyo Tires, Yokohama Rubber Company

- Aftermarket Services: Michelin, Bridgestone Corporation, Goodyear Tire & Rubber Company, Continental AG

Investment Activity

Global All-Season Car Tyres Market Investment & Funding Dynamics Overview

Investment and funding dynamics play a foundational role in shaping the competitive intensity and long-term evolution of the global all-season car tyres market. Between 2026 and 2033, capital allocation will increasingly determine the ability of manufacturers to scale production efficiently, enhance material innovation, and align product portfolios with shifting consumer preferences toward convenience-driven and fuel-efficient tyre solutions. Unlike premium niche segments, the all-season tyre market operates on a high-volume, cost-optimized model, where investment decisions are closely tied to manufacturing efficiency, raw material optimization, and distribution scale. The market’s capital structure is influenced by its strong reliance on replacement demand and widespread adoption across passenger vehicles, SUVs, and crossovers. This creates a stable and predictable investment environment, attracting sustained capital flows from both global tyre majors and regional manufacturers. Leading players such as Michelin, Bridgestone Corporation, Goodyear, and Continental AG continue to invest heavily in expanding production capacity, particularly in Asia-Pacific, where large vehicle parc and high replacement cycles drive volume growth. Additionally, the increasing focus on regulatory compliance related to fuel efficiency, rolling resistance, and tyre labelling standards is reshaping investment priorities. Companies are channeling funds toward developing low rolling resistance tyres and environmentally sustainable compounds, ensuring compliance while maintaining performance standards. The emergence of EV-compatible all-season tyres further intensifies capital requirements, as manufacturers must invest in advanced compound technologies and structural designs capable of supporting higher loads and reducing noise.

Global All-Season Car Tyres Market Investment & Funding Dynamics Current Scenario

In the current scenario, investment flows into the global all-season car tyres market are steady and volume-driven, reflecting its position as a core segment within the broader tyre industry. Manufacturers are prioritizing capital allocation toward capacity expansion, automation, and supply chain optimization to meet the consistent demand generated by the aftermarket segment, which remains the largest revenue contributor. Asia-Pacific continues to attract the highest level of investment due to its dominant market share and expanding passenger vehicle base. Companies are establishing new manufacturing plants and enhancing existing facilities in countries such as China and India to capitalize on cost advantages and proximity to demand centers. This regional focus also enables firms to strengthen distribution networks and improve responsiveness to replacement demand. Simultaneously, Europe is witnessing increasing investment momentum, driven by regulatory shifts favoring fuel-efficient and low-noise tyres. Companies such as Continental AG and Michelin are investing in R&D to develop advanced all-season tyres that meet stringent EU standards while delivering enhanced wet grip and durability. The region’s growing preference for all-season tyres over winter tyres further reinforces investment in product innovation and marketing. Technological investments are also gaining prominence, particularly in the development of EV-compatible all-season tyres. Bridgestone and Goodyear, for instance, are focusing on integrating low rolling resistance compounds and noise-reduction technologies to cater to electric vehicle requirements. These investments are complemented by digital initiatives, including online sales platforms and smart tyre monitoring systems, which enhance customer engagement and operational efficiency. From a financial standpoint, the market’s projected growth from USD 168.9 billion in 2025 to USD 256.7 billion by 2033, at a CAGR of approximately 5.4%, supports continued capital inflows. The relatively moderate growth rate, combined with high volume sales, positions the market as a stable investment avenue with predictable returns.

Key Investment & Funding Dynamics Signals in Global All-Season Car Tyres Market

One of the most significant investment signals in the market is the sustained strength of replacement demand. Continuous year-round usage of all-season tyres leads to regular wear and replacement cycles, ensuring consistent revenue streams and encouraging investment in aftermarket distribution and retail networks. Another critical signal is the rising demand for convenience-oriented mobility solutions. Consumers increasingly prefer single-tyre solutions that eliminate the need for seasonal changes, prompting manufacturers to invest in versatile tread designs and adaptive rubber compounds that perform across varying conditions. The growing penetration of SUVs and crossovers represents an additional funding driver, as these vehicles require durable and performance-oriented all-season tyres. This trend is directing investment toward larger rim sizes and reinforced tyre structures capable of handling diverse driving conditions. Electrification is emerging as a transformative investment signal, with EV-compatible all-season tyres gaining traction. These tyres require specialized features such as higher load capacity, reduced rolling resistance, and lower noise levels, leading to increased R&D expenditure and technological innovation. Lastly, regulatory pressures related to fuel efficiency, safety, and environmental sustainability are shaping capital allocation decisions. Investments in low rolling resistance technologies, eco-friendly materials, and compliance-driven product development are becoming central to maintaining market competitiveness.

Strategic Implications of Investment & Funding Dynamics in Global All-Season Car Tyres Market

The evolving investment landscape has several strategic implications for industry participants. The emphasis on scale and efficiency reinforces the dominance of global leaders such as Michelin and Bridgestone, who possess the financial resources and manufacturing capabilities to operate at high volumes while maintaining cost competitiveness. The strong dependence on aftermarket sales necessitates a dual focus on production efficiency and distribution reach. Companies must invest in both manufacturing infrastructure and retail networks to ensure consistent product availability and customer accessibility, particularly in emerging markets. The shift toward EV-compatible and low rolling resistance tyres is driving a transition toward technology-driven differentiation, even within a traditionally volume-focused market. Firms that successfully integrate performance, efficiency, and affordability will gain a competitive edge. Geographic diversification is becoming increasingly important, as companies balance investments between high-growth regions such as Asia-Pacific and technologically advanced markets like Europe. This approach helps mitigate risks associated with economic fluctuations and regulatory changes. However, the market’s reliance on raw materials such as natural rubber and synthetic compounds introduces cost volatility, requiring careful capital planning and supply chain management to protect margins.

Global All-Season Car Tyres Market Investment & Funding Dynamics Forward Outlook

Looking ahead, the investment and funding dynamics of the global all-season car tyres market are expected to remain stable yet strategically evolving. The continued expansion of the global vehicle parc, combined with rising urban mobility, will sustain strong replacement demand and support ongoing capital investment in production and distribution infrastructure. Electrification will play a central role in shaping future investment priorities, with manufacturers increasingly focusing on EV-compatible all-season tyres that enhance energy efficiency and driving comfort. This will drive further innovation in materials, tread design, and noise-reduction technologies. Asia-Pacific will continue to dominate investment flows due to its scale and growth potential, while Europe is expected to lead in regulatory-driven innovation and premium product development. North America will remain a stable market, supported by strong SUV adoption and consumer preference for convenience-oriented tyres. Digital transformation will also influence capital allocation, with increased investment in e-commerce platforms, direct-to-consumer channels, and connected tyre technologies. These initiatives will enhance customer experience and create new revenue opportunities. Overall, the market’s combination of steady growth, predictable demand, and evolving technological requirements will sustain long-term investment attractiveness. Companies that align their funding strategies with emerging trends such as electrification, sustainability, and digitalization will be best positioned to maintain competitive advantage through 2033.

Technology & Innovation

Global All-Season Car Tyres Market Technology & Innovation Landscape Overview

The technology and innovation landscape within the global all-season car tyres market plays a fundamental role in shaping product performance, efficiency, and long-term market competitiveness. Innovation in this space is not incremental but evolutionary, driven by the need to balance durability, safety, fuel efficiency, and adaptability across diverse driving conditions. As mobility ecosystems evolve’particularly with the rise of electric vehicles (EVs) and stricter environmental regulations’technology becomes the central lever redefining tyre design, material science, and manufacturing processes. Innovation intensity in the market is high, supported by steady advancements in rubber chemistry, tread pattern engineering, and smart sensing capabilities. However, the overall technology maturity remains in the growth phase, where foundational technologies such as radial construction and silica-based compounds are well established, yet continuously refined. Leading players including Michelin, Bridgestone Corporation, Goodyear Tire & Rubber Company, and Continental AG are heavily investing in next-generation compounds, low rolling resistance technologies, and intelligent tyre systems that enhance both vehicle efficiency and driving safety. A major technological shift is the transition toward EV-compatible all-season tyres, which require higher load-bearing capacity, reduced rolling resistance, and noise optimization. Additionally, the emergence of smart and connected tyres with embedded sensors is transforming tyres from passive components into active data-generating systems. These innovations are reshaping consumer expectations and enabling predictive maintenance, improved safety, and optimized vehicle performance, thereby redefining the role of tyres within the broader automotive ecosystem.

Global All-Season Car Tyres Market Technology & Innovation Landscape Current Scenario

Currently, the technology landscape in the global all-season car tyres market is characterized by continuous refinement of core technologies alongside the integration of advanced features aimed at improving efficiency and user experience. Manufacturers are focusing on enhancing tread design and compound formulations to deliver better grip, longer lifespan, and improved performance across varying weather conditions. One of the most prominent developments is the advancement of low rolling resistance tyre technology, which directly contributes to improved fuel efficiency and extended EV battery range. Tyre manufacturers are increasingly incorporating silica-rich compounds and optimized tread patterns to reduce energy loss during motion. This not only aligns with stringent fuel-efficiency regulations but also supports automakers in meeting emission reduction targets. Noise-reduction technologies are also gaining traction, particularly with the growth of electric vehicles where tyre noise becomes more noticeable in the absence of engine sound. Innovations such as acoustic foam technology and optimized tread pitch designs are being widely adopted to minimize cabin noise and enhance driving comfort. Companies like Continental AG and Pirelli & C. S.p.A. are leading advancements in this area, integrating sound-dampening materials within tyre structures. Furthermore, the integration of smart tyre technologies is gradually transforming the market. Embedded pressure and temperature sensors, along with IoT-enabled monitoring systems, allow real-time tracking of tyre health and performance. This capability enhances safety by enabling predictive maintenance and reducing the risk of sudden tyre failures. As connected vehicle ecosystems expand, these smart tyre solutions are expected to become increasingly standardized across vehicle segments. Manufacturing innovation is another critical component of the current scenario. Automation, digital quality control systems, and sustainable production processes are being adopted to improve efficiency and reduce environmental impact. Companies are also exploring the use of sustainable raw materials such as bio-based rubber and recycled inputs to align with global sustainability goals and regulatory requirements.

Key Technology & Innovation Landscape Signals in Global All-Season Car Tyres Market

The global all-season car tyres market exhibits several important technology and innovation signals that indicate the direction of future development. One key signal is the rapid growth of EV-compatible tyre technologies, driven by the increasing adoption of electric vehicles. These tyres are specifically engineered to handle higher torque, increased vehicle weight, and the need for extended range, highlighting a clear shift in design priorities. Another significant signal is the rising adoption of low rolling resistance technologies, which are becoming a standard requirement due to fuel efficiency regulations and consumer demand for cost-effective mobility solutions. This trend is accelerating innovation in compound materials and tread engineering, pushing manufacturers to develop tyres that minimize energy loss without compromising safety. The emergence of smart and connected tyre systems represents a transformative signal in the market. The integration of IoT and sensor technologies enables real-time monitoring of tyre conditions, supporting predictive maintenance and enhancing overall vehicle safety. This shift indicates a broader trend toward digitalization within the automotive industry, where tyres become an integral part of connected vehicle ecosystems. Noise reduction innovation is also a notable signal, particularly in response to the rapid growth of electric vehicles. Technologies such as acoustic foam and advanced tread designs are becoming increasingly important as manufacturers strive to enhance in-cabin comfort and meet noise regulation standards. Additionally, sustainability-driven innovation is gaining momentum as environmental regulations tighten globally. The use of recycled materials, bio-based compounds, and eco-friendly manufacturing processes reflects a growing commitment to reducing the environmental footprint of tyre production. This trend is not only regulatory-driven but also aligned with consumer preferences for sustainable products.

Strategic Implications of Technology & Innovation Landscape in Global All-Season Car Tyres Market

The evolving technology landscape has significant strategic implications for stakeholders across the global all-season car tyres market. For manufacturers, continuous investment in R&D is becoming essential to remain competitive, particularly in areas such as EV tyre optimization, smart tyre integration, and sustainable material development. Companies that successfully innovate in these domains are likely to gain a competitive edge through product differentiation and premium pricing opportunities. The shift toward EV-compatible tyres introduces new competitive dynamics, as traditional tyre performance metrics are redefined to accommodate electric mobility requirements. Manufacturers must adapt their product portfolios to align with automaker specifications and evolving consumer expectations, ensuring compatibility with next-generation vehicles. The integration of smart technologies also creates opportunities for value-added services, such as predictive maintenance and fleet management solutions. This opens new revenue streams beyond traditional tyre sales, enabling companies to position themselves as mobility solution providers rather than just product manufacturers. Sustainability considerations further influence strategic decision-making, as companies are increasingly required to comply with environmental regulations and adopt eco-friendly practices. This includes investment in sustainable raw materials, energy-efficient manufacturing processes, and circular economy initiatives such as tyre recycling programs. For OEMs and automotive stakeholders, collaboration with tyre manufacturers becomes more critical as technology integration deepens. Joint development initiatives focused on EV optimization, safety enhancements, and connected vehicle systems are likely to shape the future competitive landscape.

Global All-Season Car Tyres Market Technology & Innovation Landscape Forward Outlook

Looking ahead, the technology and innovation landscape of the global all-season car tyres market is expected to evolve rapidly, driven by advancements in electrification, digitalization, and sustainability. The continued growth of electric vehicles will remain a primary catalyst, accelerating the development of specialized tyres that offer enhanced efficiency, durability, and noise reduction. Smart tyre technologies are projected to gain widespread adoption, becoming a standard feature in connected and autonomous vehicles. The integration of advanced sensors, AI-driven analytics, and real-time data communication will transform tyres into intelligent components capable of interacting with vehicle systems and external infrastructure. Material innovation will also play a crucial role in shaping the future of the market. The development of next-generation compounds, including bio-based and recyclable materials, will support sustainability goals while maintaining high performance standards. These advancements will help manufacturers reduce environmental impact and comply with increasingly stringent regulations. Automation and digitalization in manufacturing processes are expected to enhance production efficiency, reduce costs, and improve product consistency. Advanced manufacturing technologies, including AI-driven quality control and smart factories, will enable faster innovation cycles and scalable production capabilities. In conclusion, the global all-season car tyres market is entering a phase of accelerated technological transformation, where innovation is redefining product capabilities and market dynamics. Companies that can effectively leverage advancements in EV compatibility, smart technologies, and sustainable materials will be well-positioned to lead the market, while those that fail to adapt may face increasing competitive pressures in an evolving automotive ecosystem.

Market Risk

Global All-Season Car Tyres Market Risk Factors & Disruption Threats Overview

The Global All-Season Car Tyres Market operates within a relatively stable yet cost-sensitive environment, characterized by high volume demand, strong aftermarket dependence, and increasing regulatory oversight. While the overall risk profile of the market remains moderate, it is significantly influenced by raw material price volatility, intense price competition, and evolving mobility trends. These structural dynamics shape profitability, supply chain resilience, and competitive positioning across both developed and emerging markets. A primary risk factor is the heavy dependence on raw materials such as natural rubber, synthetic rubber, and petroleum-based derivatives. Price fluctuations in these inputs’often linked to crude oil volatility and supply disruptions’directly impact manufacturing costs. Unlike premium tyre segments, pricing power in the all-season category is relatively limited due to its mass-market nature, making margin management a persistent challenge for manufacturers. Another key structural constraint is the highly competitive and fragmented market landscape. Numerous global and regional players compete aggressively on pricing, particularly in emerging markets where cost sensitivity is high. This intensifies margin pressure and increases the risk of commoditization, especially in standard all-season tyre categories. The market also faces regulatory risks related to fuel efficiency, rolling resistance, and tyre labelling standards, particularly in Europe and North America. Compliance with these evolving regulations requires continuous investment in R&D and manufacturing upgrades, increasing operational complexity and cost structures. Additionally, the rise of electric vehicles (EVs) introduces both opportunities and disruption risks. EV-compatible all-season tyres require enhanced load capacity, low rolling resistance, and noise reduction capabilities. Manufacturers that fail to adapt to these evolving requirements risk losing relevance in future OEM and replacement markets.

Global All-Season Car Tyres Market Risk Factors & Disruption Threats Current Scenario

The current market scenario reflects steady growth supported by strong replacement demand and rising vehicle parc; however, it is also marked by increasing cost pressures and competitive intensity. One of the most prominent challenges is the ongoing volatility in raw material prices, which continues to impact production costs and profitability across the value chain. At the same time, the aftermarket segment’while dominant’is undergoing structural shifts due to digitalization. The rise of e-commerce platforms and direct-to-consumer tyre sales is increasing price transparency, intensifying competition, and reshaping traditional distribution models. This shift poses a disruption threat to conventional dealer networks while creating new growth avenues for digitally agile players. Another defining feature of the current landscape is the growing preference for SUVs and crossovers, which require more durable and versatile all-season tyres. While this trend supports volume growth, it also increases performance expectations, pushing manufacturers to enhance product quality without significantly increasing prices. Regulatory pressures are also intensifying, particularly in Europe, where stricter standards on rolling resistance, wet grip, and noise emissions are influencing product development strategies. Compliance costs are rising, especially for smaller manufacturers with limited R&D capabilities. Furthermore, EV adoption is beginning to reshape demand patterns. Although still an emerging segment, EV-compatible all-season tyres are gaining traction, requiring manufacturers to invest in advanced materials and design innovations while managing cost efficiency.

Key Risk Factors & Disruption Threats Signals in Global All-Season Car Tyres Market

One of the most prominent risk signals is the increasing commoditization of standard all-season tyres. As product differentiation narrows in the mass-market segment, price competition intensifies, leading to margin compression and reduced brand loyalty among cost-conscious consumers. Raw material cost volatility remains a persistent structural signal. Fluctuations in rubber and oil prices create uncertainty in cost structures, compelling manufacturers to adopt flexible pricing and procurement strategies. Another key signal is the rapid expansion of digital sales channels. E-commerce platforms are transforming how consumers purchase tyres, increasing transparency and enabling easy price comparisons. While this benefits consumers, it disrupts traditional retail models and pressures margins across the distribution chain. The shift toward EV-compatible tyres is also emerging as a critical signal. As electric vehicle adoption accelerates, demand for low rolling resistance and low-noise tyres is expected to rise. This trend favors technologically advanced players while posing a risk to manufacturers reliant on conventional product lines. Additionally, regulatory tightening around fuel efficiency and environmental impact continues to shape market dynamics. Compliance with these standards is becoming a key competitive differentiator, particularly in developed markets.

Strategic Implications of Risk Factors & Disruption Threats in Global All-Season Car Tyres Market

The identified risks and disruption signals have significant strategic implications for market participants. Cost optimization and supply chain efficiency are critical priorities, as manufacturers must navigate raw material volatility while maintaining competitive pricing in a highly price-sensitive market. Product differentiation through technology is becoming increasingly important. Investments in low rolling resistance, noise reduction, and EV-compatible designs are essential to sustain competitiveness and capture emerging demand segments. Digital transformation is another key strategic imperative. Companies must strengthen their online presence, develop direct-to-consumer channels, and leverage data analytics to enhance customer engagement and sales efficiency. OEM partnerships remain crucial for long-term growth, particularly as automakers increasingly seek integrated and vehicle-specific tyre solutions. However, manufacturers must balance OEM dependence with a strong aftermarket strategy to mitigate demand concentration risks. Additionally, regulatory compliance and sustainability initiatives must be embedded into core business strategies. Investments in eco-friendly materials, energy-efficient manufacturing, and circular economy practices are becoming essential for long-term viability.

Global All-Season Car Tyres Market Risk Factors & Disruption Threats Forward Outlook

Looking ahead to the 2026-2033 period, the Global All-Season Car Tyres Market is expected to maintain steady growth, supported by rising vehicle ownership and strong replacement demand. However, the market will continue to face moderate risk levels driven by cost pressures, competitive intensity, and technological disruption. EV adoption will play a transformative role, driving demand for specialized all-season tyres with enhanced efficiency and performance characteristics. Manufacturers that invest early in EV-compatible technologies are likely to gain a competitive advantage. Sustainability will emerge as a central theme, with increasing emphasis on recyclable materials, reduced carbon emissions, and environmentally friendly production processes. Regulatory frameworks will continue to evolve, shaping product development and market entry strategies. Digitalization will further disrupt traditional sales channels, accelerating the shift toward online platforms and direct-to-consumer models. Companies must adapt to this changing landscape to remain competitive and protect margins. Overall, the market’s moderate risk profile reflects a balance between stable demand fundamentals and emerging disruption forces. Success will depend on the ability to manage costs, innovate products, and adapt to evolving consumer and regulatory expectations.

Regulatory Landscape

Global All-Season Car Tyres Market Regulatory & Policy Environment Overview

The regulatory and policy environment governing the global All-Season Car Tyres market plays a crucial role in shaping product standards, market accessibility, and competitive dynamics. Regulations in this segment are heavily focused on safety, fuel efficiency, environmental sustainability, and performance transparency. As all-season tyres are widely used across mass-market passenger vehicles, regulatory frameworks act as a baseline for quality assurance while also driving innovation in efficiency and durability. At the core, global standards such as the European Union Tyre Labeling Regulation (EU 2020/740), UNECE regulations, and U.S. Department of Transportation (DOT) requirements define minimum thresholds for rolling resistance, wet grip performance, and external noise emissions. These frameworks enforce mandatory testing, certification, and labeling, ensuring that tyres meet safety and environmental benchmarks. For manufacturers, this translates into higher compliance costs and the need for continuous product optimization. Additionally, fuel-efficiency and emission reduction policies are directly influencing tyre design. Governments worldwide are implementing stricter CO emission norms, pushing tyre manufacturers to develop low rolling resistance products that enhance vehicle fuel economy. This is particularly significant in the all-season tyre segment, where efficiency and durability must be balanced with year-round performance. Regional policy diversity further adds complexity to the market. While Europe leads in environmental and labeling regulations, North America emphasizes safety and durability standards. Asia-Pacific markets, including China and India, are strengthening regulatory frameworks, aligning more closely with global standards while maintaining localized compliance requirements.

Global All-Season Car Tyres Market Regulatory & Policy Environment Current Scenario

Currently, the regulatory environment is becoming increasingly stringent, with a strong focus on sustainability, transparency, and safety. The EU Tyre Labeling Regulation (EU 2020/740) remains a key benchmark, requiring detailed labeling on fuel efficiency, wet grip, and noise levels. This regulation directly influences consumer purchasing behavior and intensifies competition among manufacturers. In the United States, DOT and NHTSA regulations ensure tyre safety through rigorous testing for durability, traction, and treadwear. These standards are particularly relevant for all-season tyres, which must perform consistently across varying conditions throughout the year. Asia-Pacific is witnessing rapid regulatory evolution. China’s GB standards and India’s BIS certification requirements are becoming more comprehensive, emphasizing quality, safety, and environmental performance. These developments are increasing compliance requirements for both domestic and international tyre manufacturers. Simultaneously, environmental policies are accelerating the adoption of low rolling resistance tyres and sustainable materials. Governments are promoting eco-friendly manufacturing processes and encouraging tyre recycling initiatives, further shaping the competitive landscape.

Key Regulatory & Policy Environment Signals in Global All-Season Car Tyres Market

- EU Tyre Labeling Regulation (EU 2020/740): Drives transparency in fuel efficiency, wet grip, and noise performance.

- U.S. DOT & NHTSA Standards: Enforce safety, durability, and treadwear requirements.

- UNECE Regulations: Support global harmonization of tyre performance and safety standards.

- China GB & India BIS Frameworks: Strengthen compliance requirements in high-growth markets.

- Fuel Efficiency & CO Policies: Promote low rolling resistance tyre adoption.

- Noise & Environmental Norms: Encourage development of quieter and eco-friendly tyre solutions.

Strategic Implications of Regulatory & Policy Environment in Global All-Season Car Tyres Market

Regulatory compliance raises entry barriers, particularly for smaller manufacturers lacking advanced testing and certification capabilities. Established players benefit from economies of scale and well-developed R&D infrastructure, enabling them to meet evolving standards efficiently. The increasing focus on fuel efficiency and environmental sustainability is driving innovation in tyre materials, tread design, and manufacturing processes. Companies are investing in silica-based compounds, advanced polymers, and optimized tread patterns to achieve regulatory compliance while enhancing performance. Regional regulatory variations necessitate adaptive strategies, including localized production, strategic partnerships, and multi-certification approaches. Manufacturers must balance cost efficiency with compliance to remain competitive across diverse markets. Pricing strategies are also influenced by regulatory costs, with compliant, high-performance tyres commanding premium pricing. Labeling and certification serve as key differentiators, influencing both OEM partnerships and aftermarket demand.

Global All-Season Car Tyres Market Regulatory & Policy Environment Forward Outlook

Between 2026 and 2033, the regulatory environment is expected to become more stringent and sustainability-driven. Future updates to EU and UNECE standards will likely introduce tighter limits on rolling resistance, noise emissions, and material sustainability, pushing manufacturers toward continuous innovation. The transition toward electric mobility will further reshape regulatory requirements. EV-specific policies will emphasize low rolling resistance, higher load capacity, and reduced noise levels, accelerating the development of EV-compatible all-season tyres. Emerging markets will continue aligning with global standards, reducing regulatory fragmentation while increasing compliance complexity. This trend will favor multinational tyre manufacturers capable of navigating diverse regulatory landscapes. Sustainability will remain a central focus, with increased emphasis on circular economy practices, recycling, and eco-friendly raw materials. Regulatory frameworks will increasingly reward manufacturers that adopt sustainable practices and innovative technologies. Overall, the regulatory landscape will act as both a constraint and a catalyst’raising compliance requirements while driving technological advancement and product differentiation. Companies that proactively align with evolving regulations will secure long-term competitive advantages in the global all-season tyre market.