Global Functional Confectionery Market Report, Size & Forecast 2026-2033

Global Functional Confectionery Market Forecast Snapshot: 2026???2033

| Metric | Value |

| 2025 Market Size | USD 68.5 Billion |

| 2033 Market Size | ~USD 104.2 Billion |

| CAGR (2026???2033) | ~5.4% |

| Largest Region | North America |

| Fastest Growing Region | Asia-Pacific |

| Top Segment | Functional Gummies |

| Key Trend | Immunity-Boosting, Sugar-Free & Fortified Confectionery Innovation |

| Future Focus | Clean-Label Formulations, Botanical Ingredients & Personalized Nutrition Confectionery |

Global Functional Confectionery Market Overview

The Global Functional Confectionery Market is booming, with candies, gummies, and chocolates now packed with things like vitamins, protein, or herbs. It's like having a treat and a health boost together! This trend is growing fast worldwide. Some sweets are now "functional" ??? they have extra good stuff like vitamins, herbs, or protein. Think gummies, mints, or chocolates that are good for you too. They're like a mix of candy and health supplements. Even Crispy Breakfast Treats are getting a health makeover, with added fiber, probiotics, or other nutrients to kickstart your day

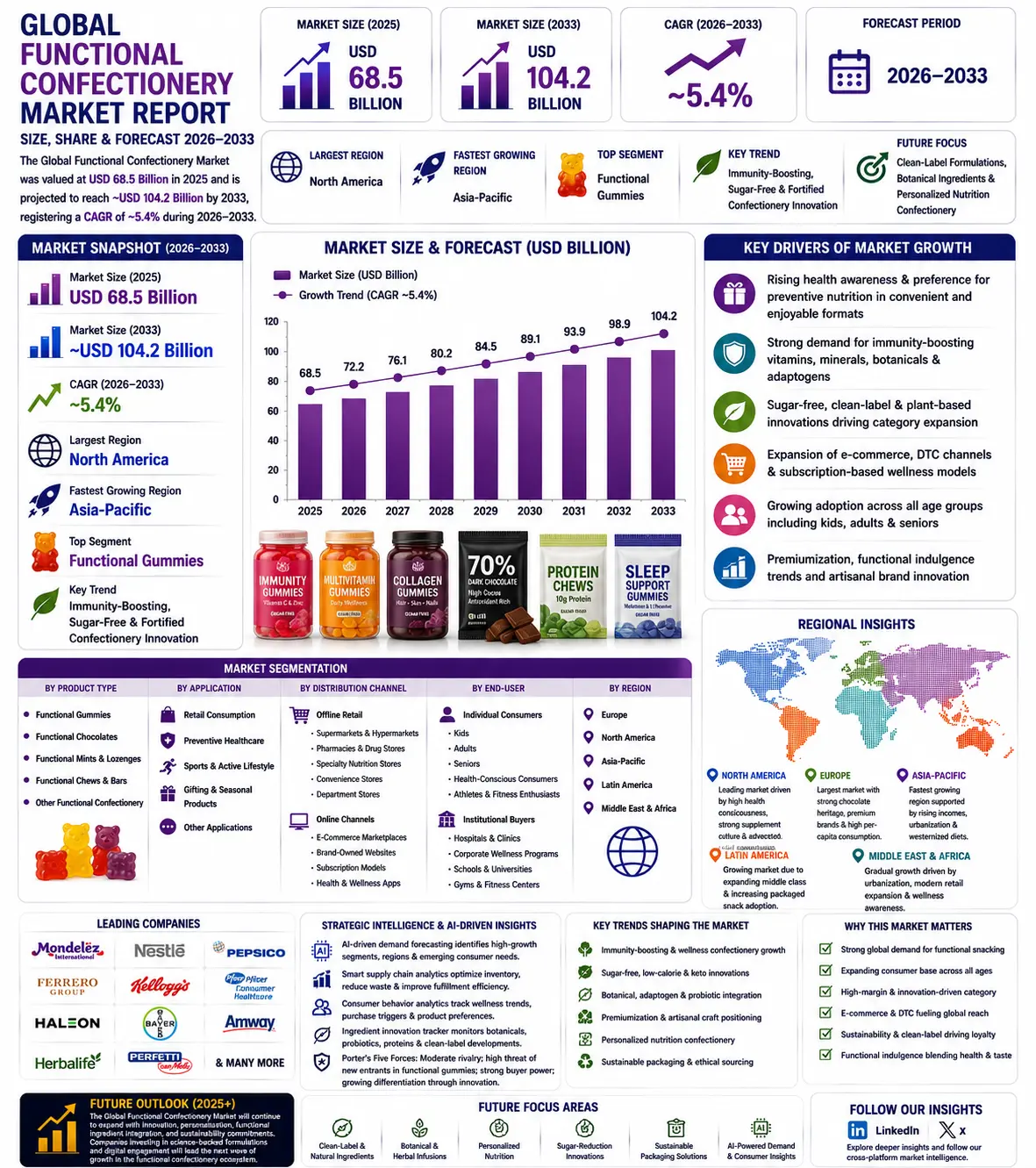

According to Pheonix Research, the Global Functional Confectionery Market is valued at USD 68.5 billion in 2025 and is projected to reach approximately USD 104.2 billion by 2033, registering a CAGR of ~5.4% (2026???2033). Growth is driven by rising health awareness, demand for convenient supplement formats, sugar-reduction trends, and preventive healthcare adoption.

North America leads due to strong nutraceutical consumption, high disposable income, and advanced retail penetration. Asia-Pacific is the fastest-growing region, supported by expanding middle-class populations, rising preventive health awareness, and growing e-commerce access.

The post-2025 outlook emphasizes botanical fortification, sugar-free innovation, collagen-infused confectionery, and AI-driven personalized nutrition solutions.Key Drivers of Global Functional Confectionery Market Growth

1. Rising Preventive Healthcare Awareness

Consumers increasingly prefer convenient daily supplement alternatives in enjoyable confectionery formats.

2. Growth of Vitamin & Immunity Gummies

Demand for Vitamin C, D, Zinc, and multivitamin gummies continues to expand across adult and pediatric segments.

3. Sugar-Free & Clean-Label Demand

Low-sugar, stevia-sweetened, gelatin-free, and plant-based formulations are gaining strong traction.

4. Expansion of E-Commerce & DTC Channels

Online platforms and subscription-based supplement models enhance recurring consumption.

5. Botanical & Adaptogen Integration

Ashwagandha, elderberry, turmeric, collagen, and probiotics are redefining confectionery positioning.

Global Functional Confectionery Market Segmentation

1. By Product Type

1.1 Functional Gummies

1.1.1 Vitamin Gummies

1.1.1.1 Multivitamin Gummies

1.1.1.2 Vitamin C & Immunity Gummies

1.1.1.3 Vitamin D Gummies

1.1.1.4 Kids??? Nutritional Gummies

1.1.2 Mineral & Supplement Gummies

1.1.2.1 Zinc-Infused

1.1.2.2 Iron Gummies

1.1.2.3 Calcium Gummies

1.1.2.4 Magnesium Gummies

1.1.3 Botanical & Adaptogen Gummies

1.1.3.1 Elderberry Gummies

1.1.3.2 Ashwagandha Gummies

1.1.3.3 Turmeric Gummies

1.1.3.4 Collagen Gummies

1.2.1 Protein-Enriched Chocolate

1.2.1.1 Whey Protein Chocolate

1.2.1.2 Plant-Based Protein Chocolate

1.2.1.3 Keto Chocolate

1.2.1.4 Sugar-Free Dark Chocolate

1.2.2 Probiotic & Fiber Chocolates

1.2.2.1 Gut Health Chocolate

1.2.2.2 Prebiotic-Enriched

1.2.2.3 High-Fiber Bars

1.2.2.4 Digestive Support Variants

1.3 Functional Mints & Lozenges

1.3.1 Throat & Immunity Lozenges

1.3.1.1 Herbal Lozenges

1.3.1.2 Vitamin C Lozenges

1.3.1.3 Zinc Lozenges

1.3.1.4 Honey-Based Lozenges

1.3.2 Energy & Focus Mints

1.3.2.1 Caffeine Mints

1.3.2.2 B-Vitamin Mints

1.3.2.3 Nootropic-Infused

1.3.2.4 Stress-Relief Variants

1.4 Functional Chews & Bars

1.4.1 Protein Chews

1.4.1.1 Sports Nutrition Chews

1.4.1.2 Meal Replacement Chews

1.4.1.3 Collagen Chews

1.4.1.4 Keto Chews

1.4.2 Wellness Snack Bars

1.4.2.1 Immunity Bars

1.4.2.2 Energy Bars

1.4.2.3 Gut Health Bars

1.4.2.4 Plant-Based Bars

?? ?? ?? ?? ?? ??2. By Application

2.1 Retail Consumption

2.1.1 Supermarkets & Hypermarkets

2.1.1.1 Organized Retail Chains

2.1.1.1.1 National Hypermarket Chains

2.1.1.1.2 Regional Supermarket Chains

2.1.1.1.3 Private Label Functional Brands

2.1.1.1.4 Promotional Wellness Displays

2.1.1.2 Health & Wellness Sections

2.1.1.2.1 Vitamin Gummy Aisles

2.1.1.2.2 Sugar-Free Confectionery Sections

2.1.1.2.3 Botanical & Herbal Products

2.1.1.2.4 Immunity Support Displays

2.1.2 Pharmacies & Drug Stores

2.1.2.1 OTC Supplement Integration

2.1.2.1.1 Vitamin Gummies

2.1.2.1.2 Mineral Lozenges

2.1.2.1.3 Collagen Chews

2.1.2.1.4 Probiotic Confectionery

2.1.2.2 Prescription-Adjacent Products

2.1.2.2.1 Pediatric Nutrition Gummies

2.1.2.2.2 Senior Wellness Chews

2.1.2.2.3 Iron & Calcium Gummies

2.1.2.2.4 Throat & Immunity Lozenges

2.1.3 Specialty Health Stores

2.1.3.1 Natural & Organic Retailers

2.1.3.1.1 Plant-Based Gummies

2.1.3.1.2 Gelatin-Free Formulations

2.1.3.1.3 Non-GMO Certified Products

2.1.3.1.4 Clean-Label Confectionery

2.1.3.2 Sports Nutrition Stores

2.1.3.2.1 Protein Chews

2.1.3.2.2 Energy Gummies

2.1.3.2.3 Pre-Workout Functional Mints

2.1.3.2.4 Recovery Support Products

2.1.4 Online Retail Platforms

2.1.4.1 E-Commerce Marketplaces

2.1.4.1.1 Bulk Purchase Options

2.1.4.1.2 Discounted Supplement Packs

2.1.4.1.3 Subscription Refills

2.1.4.1.4 Cross-Category Wellness Bundles

2.1.4.2 Direct-to-Consumer (DTC) Platforms

2.1.4.2.1 Personalized Nutrition Packs

2.1.4.2.2 Online Exclusive Formulations

2.1.4.2.3 Loyalty Programs

2.1.4.2.4 Auto-Replenishment Services

2.2 Preventive Healthcare

2.2.1 Daily Supplement Replacement

2.2.1.1 Multivitamin Alternatives

2.2.1.1.1 Adult Multivitamin Gummies

2.2.1.1.2 Women???s Health Formulations

2.2.1.1.3 Men???s Health Formulations

2.2.1.1.4 Teen Nutrition Gummies

2.2.2 Immune Support Programs

2.2.2.1 Immunity Boosting Formats

2.2.2.1.1 Vitamin C Gummies

2.2.2.1.2 Zinc Lozenges

2.2.2.1.3 Elderberry Gummies

2.2.2.1.4 Herbal Immunity Chews

2.2.3 Pediatric Nutrition

2.2.3.1 Children-Focused Supplements

2.2.3.1.1 Growth Support Gummies

2.2.3.1.2 Brain Development Gummies

2.2.3.1.3 Iron & Calcium Chews

2.2.3.1.4 Sugar-Free Kids??? Vitamins

2.2.4 Senior Wellness

2.2.4.1 Age-Specific Formulations

2.2.4.1.1 Bone Health Gummies

2.2.4.1.2 Joint Support Chews

2.2.4.1.3 Heart Health Lozenges

2.2.4.1.4 Memory Support Mints

2.3 Sports & Active Lifestyle

2.3.1 Energy Support

2.3.1.1 Performance Enhancement Products

2.3.1.1.1 Caffeine Gummies

2.3.1.1.2 B-Vitamin Mints

2.3.1.1.3 Adaptogen Chews

2.3.1.1.4 Nootropic Functional Candy

2.3.2 Muscle Recovery

2.3.2.1 Recovery-Focused Formats

2.3.2.1.1 Collagen Gummies

2.3.2.1.2 Protein Chews

2.3.2.1.3 Magnesium Lozenges

2.3.2.1.4 Anti-Inflammatory Botanicals

2.3.3 Hydration Support

2.3.3.1 Electrolyte Confectionery

2.3.3.1.1 Electrolyte Gummies

2.3.3.1.2 Sodium & Potassium Chews

2.3.3.1.3 Oral Rehydration Lozenges

2.3.3.1.4 Endurance Support Candy

2.3.4 Performance Enhancement

2.3.4.1 Functional Enhancement Products

2.3.4.1.1 Pre-Workout Gummies

2.3.4.1.2 Focus & Cognitive Mints

2.3.4.1.3 Stress-Relief Chews

2.3.4.1.4 Adaptogenic Confectionery

?? ?? ?? ?? ?? ?? ??3. By Distribution Channel

3.1 Offline Retail

3.1.1 Supermarkets & Hypermarkets

3.1.1.1 Organized Retail Networks

3.1.1.1.1 National Chains

3.1.1.1.2 Regional Chains

3.1.1.1.3 Private Label Health Brands

3.1.1.1.4 Wellness Promotional Displays

3.1.2 Pharmacies & Drug Stores

3.1.2.1 Health & OTC Distribution

3.1.2.1.1 Prescription-Adjacent Sales

3.1.2.1.2 Pharmacist-Recommended Brands

3.1.2.1.3 Immunity-Focused Displays

3.1.2.1.4 Pediatric Supplement Counters

3.1.3 Specialty Nutrition Stores

3.1.3.1 Wellness-Focused Retailers

3.1.3.1.1 Sports Nutrition Chains

3.1.3.1.2 Organic Health Stores

3.1.3.1.3 Herbal Supplement Retailers

3.1.3.1.4 Clean-Label Specialty Stores

3.1.4 Convenience Stores

3.1.4.1 Impulse & Travel Retail

3.1.4.1.1 Single-Serve Functional Packs

3.1.4.1.2 Energy Mints at Checkout

3.1.4.1.3 Transit & Airport Kiosks

3.1.4.1.4 Fuel Station Retail

3.2 Online Channels

3.2.1 E-Commerce Marketplaces

3.2.1.1 Large-Scale Digital Platforms

3.2.1.1.1 Subscription Bundles

3.2.1.1.2 Bulk Purchase Discounts

3.2.1.1.3 Flash Wellness Sales

3.2.1.1.4 Cross-Brand Bundling

3.2.2 Brand-Owned Websites

3.2.2.1 Direct-to-Consumer Models

3.2.2.1.1 Personalized Nutrition Packs

3.2.2.1.2 Auto-Replenishment Services

3.2.2.1.3 Exclusive Product Launches

3.2.2.1.4 Loyalty & Reward Programs

3.2.3 Subscription Models

3.2.3.1 Recurring Wellness Programs

3.2.3.1.1 Monthly Vitamin Gummies

3.2.3.1.2 Immunity Booster Packs

3.2.3.1.3 Senior Wellness Kits

3.2.3.1.4 Kids??? Nutrition Plans

3.2.4 Health & Wellness Apps

3.2.4.1 Digital Health Integration

3.2.4.1.1 App-Based Supplement Recommendations

3.2.4.1.2 AI-Driven Personalization

3.2.4.1.3 Health Data-Linked Purchases

3.2.4.1.4 Preventive Care Subscriptions

?? ?? ?? ?? ?? ??4. By Region

4.1 North America

4.2 Europe

4.3 Asia-Pacific

4.4 Latin America

4.5 Middle East & Africa

Leading Companies in the Global Functional Confectionery Market

- Nestl?? Health Science

- Church & Dwight (Vitafusion)

- Pfizer Consumer Healthcare

- Haleon (Centrum, Emergen-C)

- Bayer AG

- Mondelez International (Functional Chocolate Innovations)

- Amway

- Herbalife

Regional Insights of the Global Functional Confectionery Market

North America ??? Market Leader

North America leads the global functional confectionery market, supported by high nutraceutical consumption, advanced regulatory structures, and extensive retail and pharmacy penetration. Strong consumer awareness of preventive healthcare and well-established vitamin gummy brands reinforce regional dominance.

Asia-Pacific ??? Fastest Growing Region

Asia-Pacific is experiencing rapid growth driven by increasing preventive health awareness, expanding middle-class populations, and accelerating digital commerce adoption. Rising demand for immunity, collagen, and botanical-based formats continues to fuel regional expansion.

Europe ??? Innovation & Clean-Label Focused Market

Europe???s market growth is shaped by stringent clean-label regulations, growing demand for plant-based and botanical ingredients, and strong consumer preference for natural, sugar-free formulations.

Latin America ??? Emerging Health Adoption

Latin America is witnessing steady expansion due to rising immunity awareness, growing pharmacy distribution networks, and increasing accessibility to vitamin and mineral-infused confectionery products.

Middle East & Africa ??? Developing Growth Potential

The Middle East & Africa region is gradually strengthening due to urbanization, improving retail infrastructure, and rising consumer focus on wellness and preventive nutrition solutions.

Why the Global Functional Confectionery Market Remains Critical

Bridges the gap between indulgence and preventive healthcare.

Expands nutraceutical consumption into convenient daily formats.

Supports sugar-reduction and clean-label industry transformation.

Enhances recurring consumption via subscription and pharmacy channels.

Strengthens cross-industry integration between food, pharma, and wellness sectors.

Final Takeaway of the Global Functional Confectionery Market

The Global Functional Confectionery Market is transitioning into a high-growth hybrid category integrating indulgence, wellness, and preventive healthcare. With a projected CAGR of ~5.4% (2026???2033), the market presents strong opportunities across vitamin gummies, botanical chocolates, and personalized nutrition formats.Future competitive advantage will be driven by clean-label innovation, botanical fortification, AI-enabled personalization, and strategic expansion across pharmacy and digital retail channels.

At Pheonix Research, our advanced forecasting models provide comprehensive Functional Confectionery Market revenue projections, competitive benchmarking, and AI-powered strategic intelligence ??? enabling stakeholders to capitalize on the evolving wellness-driven confectionery landscape with precision and sustainable growth strategies.

???? Social Mentions & Publication Channels

?? ??Explore deeper insights and follow our cross-platform updates on??LinkedIn, and??X??for continuous intelligence and market coverage.

LinkedIn : https://www.linkedin.com/feed/update/urn:li:activity:7431721404800225280

??X : https://x.com/Pheonix_Insight/status/2025962857813405700?s=20

Table of Contents

1. Executive Summary

1.1 Market Snapshot (2026???2033)

1.2 Key Growth Highlights

1.3 Category Evolution Overview

1.4 Strategic Opportunity Assessment

1.5 Analyst Perspective

2. Market Overview

2.1 Introduction to Functional Confectionery

2.2 Industry Convergence: Food, Pharma & Nutraceuticals

2.3 Value Chain & Ecosystem Analysis

2.4 Preventive Healthcare Integration

2.5 Consumer Behavior Transformation

2.6 Clean-Label & Botanical Innovation Trends

3. Global Market Forecast Snapshot (USD Billion), 2026???2033

3.1 2025 Market Size

3.2 2033 Market Size

3.3 CAGR (2026???2033)

3.4 Largest Region

3.5 Fastest Growing Region

3.6 Top Segment

3.7 Key Trend

3.8 Future Focus

4. Key Market Drivers

4.1 Rising Preventive Healthcare Awareness

4.2 Growth of Vitamin & Immunity Gummies

4.3 Sugar-Free & Clean-Label Demand

4.4 Expansion of E-Commerce & DTC Channels

4.5 Botanical & Adaptogen Integration

5. Key Market Restraints & Challenges

5.1 Regulatory & Compliance Complexity

5.2 High Cost of Functional Ingredients

5.3 Consumer Skepticism in Emerging Markets

5.4 Supply Chain & Ingredient Volatility

6. Market Segmentation by Product Type (USD Billion), 2026???2033

6.1 Functional Gummies

6.1.1 Vitamin Gummies

6.1.1.1 Multivitamin Gummies

6.1.1.2 Vitamin C & Immunity Gummies

6.1.1.3 Vitamin D Gummies

6.1.1.4 Kids??? Nutritional Gummies

6.1.2 Mineral & Supplement Gummies

6.1.2.1 Zinc-Infused Gummies

6.1.2.2 Iron Gummies

6.1.2.3 Calcium Gummies

6.1.2.4 Magnesium Gummies

6.1.3 Botanical & Adaptogen Gummies

6.1.3.1 Elderberry Gummies

6.1.3.2 Ashwagandha Gummies

6.1.3.3 Turmeric Gummies

6.1.3.4 Collagen Gummies

6.1.4 Specialized Wellness Gummies

6.1.4.1 Sleep Support Gummies

6.1.4.2 Stress Relief Gummies

6.1.4.3 Hair, Skin & Nail Gummies

6.1.4.4 Probiotic Gummies

6.2 Functional Chocolates

6.2.1 Protein-Enriched Chocolate

6.2.1.1 Whey Protein Chocolate

6.2.1.2 Plant-Based Protein Chocolate

6.2.1.3 Keto Chocolate

6.2.1.4 Sugar-Free Dark Chocolate

6.2.2 Probiotic & Fiber Chocolates

6.2.2.1 Gut Health Chocolate

6.2.2.2 Prebiotic-Enriched Chocolate

6.2.2.3 High-Fiber Chocolate Bars

6.2.2.4 Digestive Support Variants

6.2.3 Botanical-Infused Chocolates

6.2.3.1 Adaptogen Chocolate

6.2.3.2 Collagen Chocolate

6.2.3.3 Herbal Extract Chocolate

6.2.3.4 Immunity-Boosting Chocolate

6.3 Functional Mints & Lozenges

6.3.1 Throat & Immunity Lozenges

6.3.1.1 Herbal Lozenges

6.3.1.2 Vitamin C Lozenges

6.3.1.3 Zinc Lozenges

6.3.1.4 Honey-Based Lozenges

6.3.2 Energy & Focus Mints

6.3.2.1 Caffeine Mints

6.3.2.2 B-Vitamin Mints

6.3.2.3 Nootropic-Infused Mints

6.3.2.4 Stress-Relief Variants

6.4 Functional Chews & Bars

6.4.1 Protein Chews

6.4.1.1 Sports Nutrition Chews

6.4.1.2 Meal Replacement Chews

6.4.1.3 Collagen Chews

6.4.1.4 Keto Chews

6.4.2 Wellness Snack Bars

6.4.2.1 Immunity Bars

6.4.2.2 Energy Bars

6.4.2.3 Gut Health Bars

6.4.2.4 Plant-Based Bars

7. Market Segmentation by Application (USD Billion), 2026???2033

7.1 Retail Consumption

7.1.1 Supermarkets & Hypermarkets

7.1.1.1 Organized Retail Chains

7.1.1.1.1 National Hypermarket Chains

7.1.1.1.2 Regional Supermarket Chains

7.1.1.1.3 Private Label Functional Brands

7.1.1.1.4 Wellness Promotional Displays

7.1.2 Pharmacies & Drug Stores

7.1.2.1 OTC Supplement Integration

7.1.2.1.1 Vitamin Gummies

7.1.2.1.2 Mineral Lozenges

7.1.2.1.3 Collagen Chews

7.1.2.1.4 Probiotic Confectionery

7.1.3 Specialty Health Stores

7.1.3.1 Natural & Organic Retailers

7.1.3.1.1 Plant-Based Gummies

7.1.3.1.2 Gelatin-Free Formulations

7.1.3.1.3 Non-GMO Certified Products

7.1.3.1.4 Clean-Label Confectionery

7.1.4 Online Retail Platforms

7.1.4.1 E-Commerce Marketplaces

7.1.4.1.1 Bulk Purchase Options

7.1.4.1.2 Discounted Supplement Packs

7.1.4.1.3 Subscription Refills

7.1.4.1.4 Cross-Category Wellness Bundles

7.2 Preventive Healthcare

7.2.1 Daily Supplement Replacement

7.2.1.1 Adult Multivitamin Gummies

7.2.1.2 Women???s Health Formulations

7.2.1.3 Men???s Health Formulations

7.2.1.4 Teen Nutrition Gummies

7.2.2 Immune Support Programs

7.2.2.1 Vitamin C Gummies

7.2.2.2 Zinc Lozenges

7.2.2.3 Elderberry Gummies

7.2.2.4 Herbal Immunity Chews

7.2.3 Pediatric Nutrition

7.2.3.1 Growth Support Gummies

7.2.3.2 Brain Development Gummies

7.2.3.3 Iron & Calcium Chews

7.2.3.4 Sugar-Free Kids??? Vitamins

7.2.4 Senior Wellness

7.2.4.1 Bone Health Gummies

7.2.4.2 Joint Support Chews

7.2.4.3 Heart Health Lozenges

7.2.4.4 Memory Support Mints

7.3 Sports & Active Lifestyle

7.3.1 Energy Support

7.3.1.1 Caffeine Gummies

7.3.1.2 B-Vitamin Mints

7.3.1.3 Adaptogen Chews

7.3.1.4 Nootropic Functional Candy

7.3.2 Muscle Recovery

7.3.2.1 Collagen Gummies

7.3.2.2 Protein Chews

7.3.2.3 Magnesium Lozenges

7.3.2.4 Anti-Inflammatory Botanicals

7.3.3 Hydration Support

7.3.3.1 Electrolyte Gummies

7.3.3.2 Sodium & Potassium Chews

7.3.3.3 Oral Rehydration Lozenges

7.3.3.4 Endurance Support Candy

7.3.4 Performance Enhancement

7.3.4.1 Pre-Workout Gummies

7.3.4.2 Focus & Cognitive Mints

7.3.4.3 Stress-Relief Chews

7.3.4.4 Adaptogenic Confectionery

8. Market Segmentation by Distribution Channel (USD Billion), 2026???2033

8.1 Offline Retail

8.1.1 Supermarkets & Hypermarkets

8.1.1.1 National Chains

8.1.1.2 Regional Chains

8.1.1.3 Private Label Health Brands

8.1.1.4 Wellness Promotional Displays

8.1.2 Pharmacies & Drug Stores

8.1.2.1 Pharmacist-Recommended Brands

8.1.2.2 Prescription-Adjacent Sales

8.1.2.3 Immunity-Focused Displays

8.1.2.4 Pediatric Supplement Counters

8.1.3 Specialty Nutrition Stores

8.1.3.1 Sports Nutrition Chains

8.1.3.2 Organic Health Stores

8.1.3.3 Herbal Supplement Retailers

8.1.3.4 Clean-Label Specialty Stores

8.1.4 Convenience Stores

8.1.4.1 Single-Serve Functional Packs

8.1.4.2 Energy Mints at Checkout

8.1.4.3 Transit & Airport Kiosks

8.1.4.4 Fuel Station Retail

8.2 Online Channels

8.2.1 E-Commerce Marketplaces

8.2.1.1 Subscription Bundles

8.2.1.2 Bulk Purchase Discounts

8.2.1.3 Flash Wellness Sales

8.2.1.4 Cross-Brand Bundling

8.2.2 Brand-Owned Websites (DTC)

8.2.2.1 Personalized Nutrition Packs

8.2.2.2 Auto-Replenishment Services

8.2.2.3 Exclusive Product Launches

8.2.2.4 Loyalty & Reward Programs

8.2.3 Subscription Models

8.2.3.1 Monthly Vitamin Gummies

8.2.3.2 Immunity Booster Packs

8.2.3.3 Senior Wellness Kits

8.2.3.4 Kids??? Nutrition Plans

8.2.4 Health & Wellness Apps

8.2.4.1 App-Based Supplement Recommendations

8.2.4.2 AI-Driven Personalization

8.2.4.3 Health Data-Linked Purchases

8.2.4.4 Preventive Care Subscriptions

9. Market Segmentation by Region (USD Billion), 2026???2033

9.1 North America

9.2 Europe

9.3 Asia-Pacific

9.4 Latin America

9.5 Middle East & Africa

10. Leading Companies & Competitive Landscape

10.1 Nestl?? Health Science

10.2 Church & Dwight (Vitafusion)

10.3 Pfizer Consumer Healthcare

10.4 Haleon (Centrum, Emergen-C)

10.5 Bayer AG

10.6 Mondelez International (Functional Chocolate Innovations)

10.7 Amway

10.8 Herbalife

11. Regional Insights

11.1 North America ??? Market Leader

11.2 Asia-Pacific ??? Fastest Growing Region

11.3 Europe ??? Innovation & Clean-Label Focused Market

11.4 Latin America ??? Emerging Health Adoption

11.5 Middle East & Africa ??? Developing Growth Potential

12. Strategic Insights & Opportunities

12.1 Clean-Label Ingredient Adoption

12.2 AI-Driven Personalized Nutrition

12.3 Subscription & DTC Expansion

12.4 Botanical & Adaptogen Fortification

12.5 Functional Chocolate Innovations

12.6 Preventive Healthcare Partnerships

13. Key Trends & Innovations

13.1 Immunity-Boosting Confectionery

13.2 Sugar-Free & Stevia-Based Products

13.3 Collagen & Protein-Enriched Formats

13.4 Adaptogen & Botanical Inclusion

13.5 Sports Nutrition & Active Lifestyle Products

13.6 Pediatric & Senior Wellness Specialization

14. Pricing & Margin Analysis

14.1 Regional Pricing Overview

14.2 Premium vs Mass-Market Product Pricing

14.3 Raw Material & Ingredient Cost Trends

14.4 Profitability Benchmarks

15. Regulatory Landscape

15.1 North America

15.2 Europe

15.3 Asia-Pacific

15.4 Latin America

15.5 Middle East & Africa

16. Market Forecast Methodology

16.1 Data Sources & Validation

16.2 Forecasting Models & Assumptions

16.3 Segment-Level Projection Approach

16.4 Regional Modeling Methodology

17. Key Takeaways & Future Outlook

17.1 Market Growth Summary

17.2 Emerging Opportunities & Risks

17.3 Investment & Innovation Priorities

17.4 Post-2025 Strategic Implications

18. Appendix??

19 . Disclaimer

Competitive Landscape

Competitive Landscape of the Global Functional Confectionery Market

Executive Framing

The Global Functional Confectionery Market is moderately fragmented with high competitive intensity, driven by the convergence of food, nutraceutical, and pharmaceutical players. Leading companies such as Nestl?? Health Science, Bayer AG, Haleon, Church & Dwight, and Mondelez International compete alongside wellness-focused firms like Amway and Herbalife. The competitive landscape is shaped by innovation in functional ingredients, strong R&D capabilities, and expansion across pharmacy, retail, and digital health channels.

Current Market Reality

The market is rapidly evolving as consumers shift toward preventive healthcare and convenient supplement formats. Functional gummies dominate due to ease of consumption and strong appeal across age groups, while functional chocolates, mints, and chews are expanding into niche wellness segments.

Large players leverage clinical validation, regulatory compliance, and global distribution networks, while emerging brands differentiate through clean-label formulations, plant-based ingredients, and targeted health benefits such as immunity, sleep, stress relief, and gut health.

E-commerce, subscription-based wellness models, and direct-to-consumer platforms are reshaping competitive dynamics by enabling personalized nutrition solutions and recurring revenue streams.

Key Signals and Evidence

- Rapid growth of vitamin, immunity, and collagen-based gummies across global markets.

- Increasing demand for sugar-free, plant-based, and clean-label confectionery products.

- Strong entry of pharmaceutical and nutraceutical companies into confectionery formats.

- Expansion of DTC and subscription-based supplement delivery models.

- Rising innovation in botanical, adaptogen, and probiotic-infused confectionery.

Strategic Implications

- R&D Investment: Focus on clinically backed formulations and functional ingredient innovation.

- Product Diversification: Expanding portfolios across gummies, chocolates, mints, and chews.

- Personalization Strategy: Leveraging AI-driven nutrition and customized supplement solutions.

- Omnichannel Expansion: Strengthening presence across pharmacies, e-commerce, and DTC platforms.

- Clean-Label Positioning: Prioritizing natural, plant-based, and sugar-free product development.

Forward Outlook

By 2033, the Global Functional Confectionery Market is projected to reach approximately USD 104.2 billion, growing at a CAGR of ~5.4%. North America will maintain its leadership due to strong nutraceutical consumption, while Asia-Pacific will emerge as the fastest-growing region driven by rising health awareness and digital commerce expansion.

The competitive landscape will continue to evolve through deeper integration of food and pharma, increased personalization, and accelerated innovation in functional ingredients. Companies that successfully combine taste, efficacy, regulatory compliance, and digital engagement will secure long-term leadership in the global functional confectionery ecosystem.

Value Chain

Global Functional Confectionery Market: Value Chain & Market Dynamics

Executive Framing

The global functional confectionery market operates within a health-driven, innovation-intensive, and nutraceutical-integrated value chain, shaped by increasing consumer demand for convenient, enjoyable, and health-enhancing consumption formats. Functional confectionery bridges the gap between traditional sweets and dietary supplements, offering vitamin-fortified, sugar-free, and botanical-infused products.

The market follows a hybrid structure, where large multinational players leverage advanced R&D, large-scale manufacturing, and global distribution networks, while emerging brands focus on clean-label innovation, personalized nutrition, and direct-to-consumer (DTC) engagement. This dual model supports both scalability and rapid product innovation.

However, the industry faces challenges related to regulatory compliance for nutraceutical claims, ingredient stability, sourcing of functional actives, and sugar reduction requirements, alongside increasing pressure for sustainable packaging and transparency.

Current Market Reality

The functional confectionery value chain exhibits high complexity, driven by the integration of food and pharmaceutical-grade ingredients, diverse formulations, and strict regulatory frameworks. Leading companies such as Nestl?? Health Science, Haleon, and Bayer operate with globally integrated supply chains and strong pharmacy and retail presence.

Upstream activities involve sourcing vitamins, minerals, botanicals, probiotics, sweeteners, gelatin or plant-based alternatives, and flavoring agents. Supplier dependency and ingredient standardization significantly influence procurement strategies.

Midstream operations include formulation, blending, fortification, molding, coating, and packaging across formats such as gummies, lozenges, chocolates, and chews. Innovation is heavily focused on immunity, energy, gut health, beauty-from-within, and personalized nutrition solutions.

Downstream distribution spans pharmacies, supermarkets, specialty health stores, e-commerce platforms, and subscription-based wellness models, enabling both mass reach and targeted health-focused consumption.

Key Signals and Evidence

Key indicators highlighting the evolution of the global functional confectionery market include:

- Market growth from USD 68.5 billion (2025) to ~USD 104.2 billion (2033) at a CAGR of ~5.4%.

- Rising demand for vitamin gummies, immunity-boosting products, and convenient supplement formats.

- Expansion of sugar-free, plant-based, and clean-label confectionery products.

- Strong growth in pharmacy-based distribution and e-commerce-driven DTC models.

- Increasing integration of botanical ingredients, adaptogens, and collagen-based formulations.

Buyer power remains high due to product variety and health-driven preferences, while supplier power is moderate-to-high, influenced by dependency on specialized nutraceutical ingredients and regulatory compliance requirements.

Strategic Implications

Companies must balance scientific validation, product innovation, and cost efficiency to remain competitive in this evolving market. Large players are expected to expand through portfolio diversification, clinical positioning, and global distribution strength.

Emerging brands can differentiate through clean-label transparency, plant-based formulations, niche health positioning, and digital-first DTC strategies.

Integration of technologies such as AI-driven personalization, demand forecasting, and consumer health analytics will be critical in optimizing product development and enhancing customer engagement.

Sustainability is becoming increasingly important, with emphasis on eco-friendly packaging, ethical sourcing of botanicals, and reduced environmental impact.

Forward Outlook

The global functional confectionery market is expected to evolve into a health-centric, personalized, and innovation-driven ecosystem, supported by preventive healthcare trends and consumer lifestyle shifts.

Key future developments include:

- Expansion of personalized nutrition and AI-driven supplement solutions

- Growth in clean-label, plant-based, and sugar-free product offerings

- Adoption of sustainable and biodegradable packaging solutions

- Increasing use of clinical validation and functional health claims

Companies that successfully integrate innovation, regulatory compliance, and omnichannel distribution will be best positioned for long-term growth.

In conclusion, the global functional confectionery market is transforming into a high-growth, health-focused, and technology-enabled ecosystem, where functionality, transparency, and accessibility define competitive advantage.

Investment Activity

Investment & Funding Dynamics ??? Global Functional Confectionery Market

Executive Framing

Current Market Reality

Valued at USD 68.5 billion in 2025 and projected to reach ~USD 104.2 billion by 2033 (CAGR ~5.4%), the market is led by North America, with Asia-Pacific emerging as the fastest-growing region. Major players such as Nestl?? Health Science, Haleon, Bayer, and Church & Dwight are investing heavily in vitamin gummies, botanical formulations, and personalized nutrition platforms to strengthen market positioning and capture evolving consumer demand.

Key Signals and Evidence

- R&D and Formulation Innovation: Significant investment in vitamin fortification, botanical extracts, adaptogens, probiotics, and collagen-based confectionery.

- Regulatory & Compliance Infrastructure: Capital allocation toward clinical validation, labeling compliance, and global nutraceutical regulations.

- Expansion of Gummy Manufacturing: Large-scale production facilities for vitamin gummies and chewable supplements.

- Sugar-Free & Clean-Label Technologies: Investment in alternative sweeteners, plant-based gelatin substitutes, and additive-free formulations.

- DTC & Subscription Models: Growth in personalized nutrition platforms and recurring revenue subscription ecosystems.

- Cross-Industry M&A Activity: Acquisitions and partnerships between pharmaceutical, nutraceutical, and confectionery companies.

- Digital Health Integration: Funding for AI-driven personalization, health tracking apps, and data-integrated supplement delivery systems.

Strategic Implications

Companies investing in clinical-grade formulation, regulatory compliance, and personalized nutrition capabilities are expected to gain long-term competitive advantage. Investors are prioritizing scalable brands that successfully blend taste, functionality, and health benefits while maintaining strong distribution across pharmacy, retail, and digital ecosystems.

Forward Outlook

Between 2026 and 2033, investment activity is expected to accelerate, particularly in botanical ingredients, collagen-based products, and AI-powered personalized nutrition. Strategic partnerships between food, pharma, and tech players will intensify, while emerging markets will attract increasing capital for expansion and localization.

Technology & Innovation

Global Functional Confectionery Market: Technology & Innovation

Executive Framing

Technology and innovation in the Global Functional Confectionery Market are highly dynamic, driven by the convergence of food science, nutraceutical formulation, and personalized health technologies. The category is evolving rapidly as manufacturers integrate active ingredients into confectionery formats while maintaining taste, stability, and bioavailability.

Current Market Reality

Companies are leveraging advanced encapsulation technologies, controlled-release systems, and precision dosing mechanisms to incorporate vitamins, minerals, probiotics, and botanical extracts into gummies, chocolates, and lozenges. AI-driven personalization platforms and digital health integrations are further transforming how consumers select and consume functional confectionery products.

Key Signals and Evidence

- Encapsulation & Delivery Technologies: Protect sensitive ingredients like probiotics, vitamins, and botanicals while ensuring stability and absorption.

- Functional Ingredient Innovation: Rapid expansion in adaptogens, collagen, nootropics, and immunity-boosting compounds.

- AI-Driven Personalization: Integration with health apps and data platforms for customized nutrition-based confectionery solutions.

- Sugar-Free & Clean-Label Formulation: Use of alternative sweeteners, plant-based gelling agents, and natural color/flavor systems.

- Pharma-Food Convergence: Increasing overlap between OTC supplements and confectionery formats, especially in gummies and lozenges.

Strategic Implications

Innovation is a core competitive driver in this market, requiring continuous R&D investment and regulatory alignment. Companies that can balance efficacy, taste, and compliance will gain a significant advantage. Partnerships across nutraceutical, pharmaceutical, and food technology domains are becoming essential to accelerate product development and market penetration.

Forward Outlook

The market is expected to move toward highly personalized, function-specific, and clinically backed confectionery solutions. Future innovation will focus on precision nutrition, bioavailability enhancement, and digital health integration, positioning functional confectionery as a key delivery format in preventive healthcare ecosystems.

Market Risk

Risk Factors and Disruption Threats in the Global Functional Confectionery Market

Executive Framing

The Global Functional Confectionery Market is projected to grow from USD 68.5 billion in 2025 to ~USD 104.2 billion by 2033 at a CAGR of ~5.4%. The market sits at the intersection of food and nutraceuticals, benefiting from rising preventive healthcare demand and convenient supplement formats. However, regulatory complexity and product credibility challenges introduce a moderate-to-high risk profile.

Current Market Reality

North America dominates due to strong supplement consumption and regulatory infrastructure, while Asia-Pacific is rapidly expanding with increasing health awareness and digital commerce penetration. The market operates in a hybrid space between confectionery and dietary supplements, leading to varying regulatory frameworks across regions. Consumer trust, efficacy perception, and ingredient transparency are critical success factors.

Key Signals and Evidence

Key indicators include tightening regulations on health claims, labeling, and ingredient approvals across major markets. Rising scrutiny on sugar content???even in functional formats???adds formulation pressure. Additionally, variability in raw material costs (vitamins, botanicals, gelatin, sweeteners) and increasing competition from traditional supplements (capsules, powders) and functional beverages highlight structural risks.

Strategic Implications

Companies must invest in clinically backed formulations, transparent labeling, and regulatory compliance across geographies. Expanding sugar-free, plant-based, and clean-label offerings will be essential to maintain consumer trust. Leveraging DTC models, subscription-based consumption, and AI-driven personalized nutrition platforms can enhance customer retention and differentiation in a crowded market.

Forward Outlook

The Global Functional Confectionery Market will continue to expand as consumers seek convenient wellness solutions, but long-term growth will depend on regulatory navigation, scientific validation, and maintaining a balance between indulgence and health credibility.

Regulatory Landscape

Regulatory & Policy Landscape: Global Functional Confectionery Market

Executive Framing

The global functional confectionery market operates at the intersection of food, nutraceuticals, and dietary supplements, making it subject to a highly complex and evolving regulatory environment. Authorities such as the U.S. FDA, European Food Safety Authority (EFSA), FSSAI (India), and other national health agencies regulate product classification, ingredient usage, health claims, labeling, and safety standards.

Unlike traditional confectionery, functional variants???such as vitamin gummies, probiotic chocolates, and botanical lozenges???face additional scrutiny due to their health positioning and active ingredient inclusion. Regulatory classification (food vs. supplement vs. OTC product) significantly impacts product approvals, marketing claims, and distribution channels.

Current Market Reality

Functional confectionery products must comply with both food safety regulations and nutraceutical guidelines, particularly when incorporating vitamins, minerals, adaptogens, or bioactive compounds. Labeling requirements include detailed disclosure of active ingredients, dosage levels, recommended intake, and potential side effects.

Health claims???such as immunity boosting, stress relief, or digestive support???are tightly regulated and often require scientific substantiation. Misleading claims can result in product recalls, fines, or market restrictions.

Additionally, sugar-free and clean-label formulations must adhere to regulations governing alternative sweeteners (e.g., stevia, monk fruit, sugar alcohols), while pediatric-targeted products face stricter safety and dosage guidelines.

Global regulatory fragmentation further complicates market entry, as product classification and permissible claims vary significantly across regions.

Key Signals and Evidence

- Dual regulatory oversight across food and dietary supplement frameworks.

- Strict control over health and functional claims requiring clinical validation.

- Detailed labeling requirements for active ingredients, dosage, and warnings.

- Regional variation in classification (food vs. supplement vs. OTC).

- Regulation of alternative sweeteners and sugar-free formulations.

- Enhanced scrutiny for pediatric and immunity-focused products.

Strategic Implications

Companies must invest heavily in regulatory compliance, clinical validation, and transparent labeling to successfully compete in the functional confectionery market. Regulatory strategy becomes a key differentiator, particularly in managing cross-border product approvals and claim standardization.

Formulation flexibility is critical, as companies may need to adapt ingredient composition and labeling based on regional regulations. Partnerships with regulatory experts and investment in scientific research are essential to support product claims and ensure long-term compliance.

Brands that align with clean-label standards, evidence-based health positioning, and responsible marketing practices can build stronger consumer trust and regulatory resilience.

Forward Outlook

Regulatory frameworks are expected to become more stringent, particularly around health claims, pediatric safety, and functional ingredient efficacy. Governments may introduce tighter controls on supplement-like confectionery formats to prevent misleading marketing.

Harmonization efforts may emerge across global markets, but regional differences will continue to create complexity for multinational players. Digital health integration and AI-driven personalized nutrition may introduce new regulatory considerations related to data usage and product customization.

Overall, regulatory compliance will remain a critical barrier to entry and a strategic capability, with companies that proactively adapt to evolving policies gaining a competitive advantage.