Global Frozen Drinks Market Report Analysis, Size and Forecast 2026-2033

Market Forecast Snapshot (2026–2033)

| Metric | Value |

|---|---|

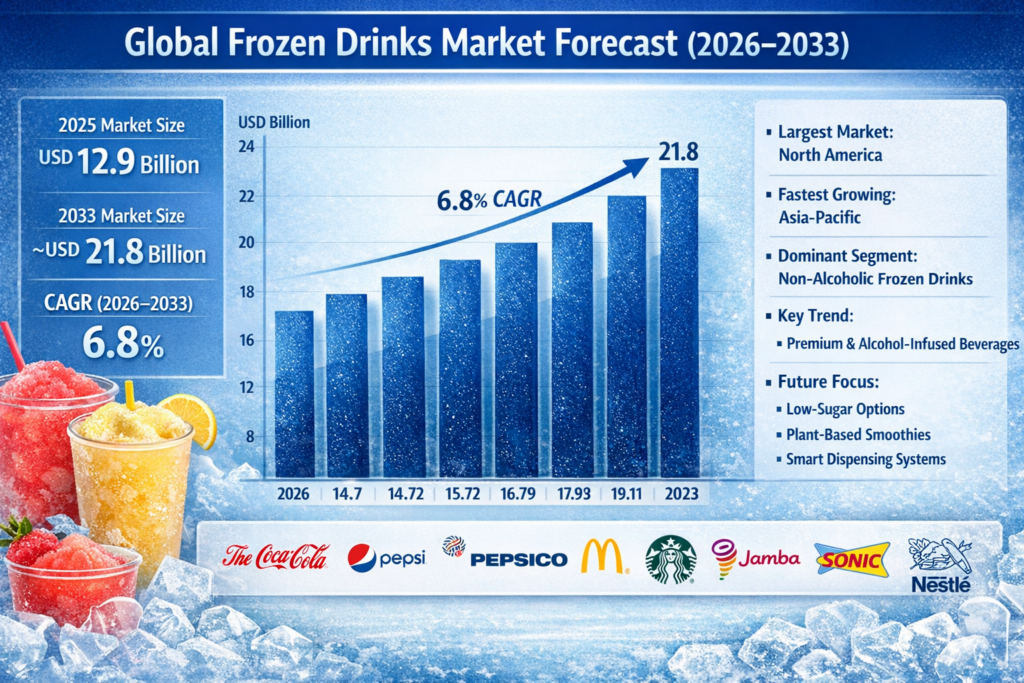

| 2025 Market Size | USD 12.9 Billion |

| 2033 Market Size | ~USD 21.8 Billion |

| CAGR (2026–2033) | 6.8% |

| Largest Market | North America |

| Fastest Growing Region | Asia-Pacific |

| Dominant Segment | Non-Alcoholic Frozen Drinks |

| Key Trend | Premium & Alcohol-Infused Frozen Beverages |

| Future Focus | Low-Sugar, Plant-Based, Smart Dispensing Systems |

Global Frozen Drinks Market Overview

The Global Frozen Drinks Market includes non-alcoholic and alcoholic beverages served in frozen or semi-frozen formats, such as slushies, smoothies, frozen carbonated beverages, frappes, frozen coffee drinks, and frozen cocktails. These products are widely distributed across quick-service restaurants (QSRs), cafés, bars, cinemas, theme parks, convenience stores, and entertainment venues, forming an important high-margin beverage category within the global foodservice industry.

Frozen drinks have evolved from seasonal refreshment products into a mainstream experiential beverage segment. Their popularity is driven by expanding QSR chains, rising urbanization, growing youth demographics, demand for visually appealing and customizable beverages, and increasing adoption of premium and alcohol-infused frozen formats. In addition, low-sugar recipes, fruit-based blends, plant-based smoothie innovations, and limited-edition seasonal flavors are supporting broader consumer appeal beyond summer months, aligning with trends favoring "low/zero-sugar and natural formulations" that resonate with health-conscious consumers seeking cleaner labels and functional benefits.

According to Pheonix Demand Forecast Engine, the Global Frozen Drinks Market is valued at USD 12.9 billion in 2025 and is projected to reach approximately USD 21.8 billion by 2033, reflecting a CAGR of ~6.8% during 2026–2033.

North America holds the largest market share, supported by strong QSR penetration, established frozen beverage brands, cinema and theme park consumption, and a growing frozen cocktail culture. Asia-Pacific represents the fastest-growing region, driven by rapid franchise expansion, rising disposable incomes, urban youth populations, and increasing adoption of Western-style café and QSR formats.

The post-2025 outlook indicates rising premiumization, alcohol-infused frozen beverage expansion, smart dispensing technology integration, sustainable packaging initiatives, and innovation in low-calorie, fruit-forward, and plant-based frozen drink formulations.

Key Drivers of Market Growth

1. Expansion of Global QSR and Franchise Networks

Growth of quick-service restaurants (QSRs) and franchise networks is boosting the availability and consumption of frozen and alcoholic beverages worldwide.

2. Rising Youth Population and Social Consumption Culture

A growing youth demographic, coupled with a culture of social drinking and sharing experiences, is driving demand for innovative, trendy, and functional and wellness-oriented beverages.

Increasing popularity of frozen cocktails, alcoholic slush beverages, and low-calorie, fruit-based drinks is fueling product diversification in the market.

4. Technological Advancements in Beverage Machines

Innovations in frozen beverage machinery are enabling better product quality, efficiency, and customization, supporting market expansion.

5. Premiumization and Functional & Wellness Trends

Rising focus on premiumization trends, and growing consumer preference for authentic, high-quality, and innovative spirit experiences is driving higher-value consumption globally.

Global Frozen Drinks Market Segmentation

1. By Product TypeGlobal Frozen Drinks Market

1.1 Non-Alcoholic Frozen Drinks

1.1.1 Slushies / Ice Slush

1.1.1.1 Carbonated Slush

1.1.1.2 Fruit-Based Slush

1.1.1.3 Functional / Vitamin-Infused Slush

1.1.2 Smoothies

1.1.2.1 Fruit Smoothies

1.1.2.2 Dairy-Based Smoothies

1.1.2.3 Plant-Based Smoothies

1.1.3 Frozen Carbonated Beverages

1.1.3.1 Cola-Based Frozen Drinks

1.1.3.2 Flavored Soda Frozen Drinks

1.1.3.3 Energy-Infused Frozen Drinks

1.1.4 Frozen Coffee & Frappes

1.1.4.1 Coffee-Based Frappes

1.1.4.2 Chocolate / Mocha Variants

1.1.4.3 Specialty / Premium Frappes

1.2 Alcoholic Frozen Drinks

1.2.1 Frozen Cocktails

1.2.1.1 Frozen Margaritas

1.2.1.2 Frozen Daiquiris

1.2.1.3 Frozen Piña Coladas

1.2.2 Frozen Beer & Malt-Based Drinks

1.2.2.1 Frozen Draft Beer

1.2.2.2 Malt-Based Frozen Slush

1.2.3 Frozen Wine-Based Beverages

1.2.3.1 Frozen Rosé (Frosé)

1.2.3.2 Sparkling Frozen Wine Blends

2. By Ingredient Type

2.1 Fruit-Based

2.1.1 Citrus-Based

2.1.1.1 Lemon & Lime Slush

2.1.1.2 Orange-Based Frozen Drinks

2.1.1.3 Grapefruit Variants

2.1.2 Berry-Based

2.1.2.1 Strawberry Blends

2.1.2.2 Blueberry & Raspberry Mixes

2.1.2.3 Mixed Berry Fusion

2.1.3 Tropical Fruit Blends

2.1.3.1 Mango-Based Frozen Drinks

2.1.3.2 Pineapple & Passionfruit

2.1.3.3 Exotic Multi-Fruit Combinations

2.2 Dairy-Based

2.2.1 Milk-Based

2.2.1.1 Classic Milkshakes

2.2.1.2 Flavored Frozen Milk Beverages

2.2.1.3 Chocolate-Based Variants

2.2.2 Yogurt-Based

2.2.2.1 Frozen Yogurt Smoothies

2.2.2.2 Probiotic-Enriched Blends

2.2.2.3 Greek Yogurt Frozen Drinks

2.2.3 Cream-Based

2.2.3.1 Ice Cream-Based Shakes

2.2.3.2 Premium Dessert Frozen Drinks

2.2.3.3 Whipped Cream-Topped Variants

2.3 Plant-Based

2.3.1 Almond / Soy / Oat-Based

2.3.1.1 Almond Milk Smoothies

2.3.1.2 Soy-Based Frozen Beverages

2.3.1.3 Oat Milk Frappes

2.3.2 Coconut-Based

2.3.2.1 Coconut Milk Smoothies

2.3.2.2 Coconut Cream Frozen Blends

2.3.2.3 Tropical Coconut Slush Variants

2.4 Alcohol-Infused

2.4.1 Spirit-Based

2.4.1.1 Vodka-Based Frozen Cocktails

2.4.1.2 Rum-Based Daiquiris

2.4.1.3 Tequila-Based Margaritas

2.4.2 Wine-Based

2.4.2.1 Frozen Sangria

2.4.2.2 Wine Slushies

2.4.2.3 Sparkling Wine Frozen Blends

2.4.3 Beer-Based

2.4.3.1 Frozen Beer Cocktails

2.4.3.2 Craft Beer Slush Variants

2.4.3.3 Beer-Mixed Frozen Blends

3. By Distribution Channel

3.1 Quick-Service Restaurants (QSRs)

3.1.1 Global QSR Chains

3.1.1.1 International Burger Chains

3.1.1.2 Fried Chicken Chains

3.1.1.3 Pizza & Combo Chains

3.1.2 Regional Franchise Chains

3.1.2.1 National QSR Brands

3.1.2.2 Mall-Based Franchises

3.1.2.3 Highway & Transit QSR Units

3.1.3 Independent Outlets

3.1.3.1 Standalone Frozen Drink Kiosks

3.1.3.2 Street-Level Beverage Shops

3.1.3.3 Seasonal Pop-Up Stalls

3.2 Cafés & Coffee Chains

3.2.1 International Coffee Brands

3.2.1.1 Frappes & Frozen Coffee

3.2.1.2 Signature Seasonal Beverages

3.2.1.3 Premium Blended Drinks

3.2.2 Local Café Chains

3.2.2.1 Artisan Beverage Cafés

3.2.2.2 Dessert & Beverage Boutiques

3.2.2.3 Youth-Centric Café Formats

3.3 Bars & Nightclubs

3.3.1 Premium Cocktail Bars

3.3.1.1 Signature Frozen Cocktails

3.3.1.2 Mixologist-Led Concepts

3.3.1.3 Luxury Rooftop Bars

3.3.2 Casual Bars & Lounges

3.3.2.1 Frozen Margarita Stations

3.3.2.2 Happy Hour Slush Cocktails

3.3.2.3 Music & Entertainment Bars

3.4 Entertainment & Leisure Venues

3.4.1 Cinemas

3.4.1.1 Multiplex Chains

3.4.1.2 Premium Cinema Lounges

3.4.1.3 Family Entertainment Centers

3.4.2 Theme Parks

3.4.2.1 International Theme Parks

3.4.2.2 Regional Amusement Parks

3.4.2.3 Water Parks

3.4.3 Sports Arenas

3.4.3.1 Stadium Concession Stands

3.4.3.2 VIP Lounge Beverage Services

3.4.3.3 Seasonal Tournament Events

3.5 Retail & Convenience

3.5.1 Convenience Stores

3.5.1.1 Self-Serve Slush Machines

3.5.1.2 Grab-and-Go Frozen Packs

3.5.1.3 Fuel Station Beverage Counters

3.5.2 Supermarkets (Ready-to-Freeze Packs)

3.5.2.1 DIY Frozen Cocktail Kits

3.5.2.2 Smoothie Freezer Packs

3.5.2.3 Family-Size Frozen Mixes

4. By End User

4.1 Individual Consumers

4.1.1 Youth / Teen Consumers

4.1.1.1 Social Media-Driven Buyers

4.1.1.2 Trend-Focused Flavor Seekers

4.1.1.3 After-School Consumption

4.1.2 Working Professionals

4.1.2.1 Office Break Purchases

4.1.2.2 Evening Social Drinkers

4.1.2.3 Weekend Leisure Buyers

4.1.3 Health-Conscious Consumers

4.1.3.1 Low-Sugar Seekers

4.1.3.2 Plant-Based Buyers

4.1.3.3 Functional Smoothie Consumers

4.2 Commercial & Hospitality

4.2.1 Hotels & Resorts

4.2.1.1 Poolside Beverage Services

4.2.1.2 All-Inclusive Resort Packages

4.2.1.3 Luxury Hospitality Chains

4.2.2 Catering & Event Services

4.2.2.1 Wedding & Private Events

4.2.2.2 Corporate Catering

4.2.2.3 Festival & Outdoor Events

4.2.3 Cruise & Tourism Operators

4.2.3.1 Cruise Line Beverage Programs

4.2.3.2 Tourist Destination Kiosks

4.2.3.3 Seasonal Vacation Hubs

5. By Region

5.1 North America

5.2 Europe

5.3 Asia-Pacific

5.4 Latin America

5.5 Middle East & Africa

Regional Insights – Global Frozen Drinks Market

North America:

North America dominates the frozen drinks market, fueled by a strong quick-service restaurant (QSR) presence, a vibrant frozen cocktail culture, and high summer consumption. The U.S. leads in innovation, particularly in premium frozen beverages that often incorporate craft spirits, appealing to affluent urban consumers seeking sophisticated experiences. Beer remains widely consumed, but younger adults are increasingly exploring frozen alcoholic drinks as a refreshing alternative during social gatherings.

Europe:

Europe’s growth is supported by its café culture, the rising popularity of frozen wine-based drinks, and robust tourism, especially in Southern Europe. Cities like Paris, Barcelona, and Rome are seeing frozen cocktails that blend premium spirits with local flavors gaining traction among urban professionals and tourists. While traditional beer continues to be a staple, the trend toward upscale, frozen cocktails and craft spirits is gradually shaping beverage preferences in metropolitan areas.

Asia-Pacific:

Rapid urbanization, expanding international QSR franchises, and a large youth demographic in China, India, and Southeast Asia are driving demand for frozen drinks. Premium and craft spirits are increasingly featured in frozen cocktails at bars, hotels, and lounges, targeting affluent urban consumers. Traditional beer consumption remains strong, but frozen alcoholic drinks are carving out a niche, particularly among millennials and young professionals seeking trendy, Instagram-worthy beverages.

Latin America:

Warm climates and a rich social beverage culture make Latin America a strong market for fruit-based frozen drinks. Cocktails featuring rum, tequila, or other spirits are popular in Brazil, Mexico, and Argentina. Beer remains the go-to casual beverage, yet premium frozen cocktails and craft spirits are gaining attention among urban millennials and high-income consumers who enjoy experimenting with unique flavors and upscale drinking experiences.

Middle East & Africa:

High temperatures, coupled with the growth of mall-based QSRs and leisure venues, boost frozen drink consumption. Premium and craft spirits targeting affluent urban consumers are gradually gaining traction in metropolitan areas, often in resorts and high-end bars. While beer consumption is limited in certain regions due to cultural and regulatory factors, frozen non-alcoholic cocktails and mocktails are widely embraced as refreshing alternatives.

Leading Companies in the Global Frozen Drinks Market

-

The Coca-Cola Company (Frozen Fanta, Frozen Coke)

-

PepsiCo Inc. (Frozen Mountain Dew, Slurpee partnerships)

-

McDonald’s Corporation (Frozen beverages & frappes)

-

Starbucks Corporation (Frappuccino range)

-

Jamba (GoTo Foods)

-

Sonic Drive-In

-

Taco Bell (Frozen Baja Blast)

-

Keurig Dr Pepper

-

Nestlé S.A.

Large beverage conglomerates dominate syrup supply chains, while QSR brands control end-consumer distribution channels. The coca-cola company is the largest company in the Global Frozen Drinks Market

Strategic Intelligence & AI-Backed Insights

Market modeling: Pheonix Demand Forecast Engine analyzed seasonal demand patterns, QSR growth rates, climate data, and alcohol adoption trends.

Production mapping: Increasing investments in frozen beverage dispensing equipment, syrup production, and centralized beverage hubs.

Consumer sentiment: Strong shift toward fruit-based, Instagram-friendly, low-sugar, and premium frozen drinks.

Porter’s Five Forces Analysis: Moderate supplier power (flavor concentrates & equipment providers); high buyer power in QSR channel due to competitive pricing and brand substitution.

Why the Global Frozen Drinks Market Remains Critical

-

Strong alignment with youth and social consumption culture.

-

High-margin category for QSR and entertainment operators.

-

Seasonal revenue booster in hot-weather markets.

-

Growing crossover with alcoholic beverage innovation.

-

Technology-driven efficiency via automated dispensing systems.

Table of Contents

1. Executive Summary

1.1 Market Forecast Snapshot (2026–2033)

1.2 Global Market Size & CAGR Analysis

1.3 Largest & Fastest-Growing Segments

1.4 Region-Level Leadership & Growth Trends

1.5 Key Market Drivers

1.6 Competitive Landscape Overview

1.7 Strategic Outlook Through 2033

2. Introduction & Market Overview

2.1 Definition of the Global Frozen Drinks Market

2.2 Scope of the Study

2.3 Evolution from Seasonal Slush to Premium Frozen Beverage Culture

2.4 Role of QSRs, Cafés, Bars & Entertainment Venues

2.5 Alcohol-Infused Frozen Beverage Expansion

2.6 Smart Dispensing Systems & Automation Integration

2.7 Sustainability, Low-Sugar & Plant-Based Innovations

3. Research Methodology

3.1 Primary Research

3.2 Secondary Research

3.3 Market Size Estimation Model

3.4 Forecast Assumptions (2026–2033)

3.5 Data Validation & Triangulation

4. Market Dynamics

4.1 Drivers

4.1.1 Expansion of Global QSR & Franchise Networks

4.1.2 Rising Youth & Social Consumption Culture

4.1.3 Growth in Frozen Cocktails & Alcoholic Slush

4.1.4 Demand for Low-Calorie & Fruit-Based Drinks

4.1.5 Climate-Driven Seasonal Demand

4.1.6 Technological Advancements in Frozen Beverage Machines

4.2 Restraints

4.2.1 Raw Material & Flavor Concentrate Price Volatility

4.2.2 Equipment Installation & Maintenance Costs

4.2.3 Regulatory Restrictions on Alcoholic Variants

4.2.4 Health & Sugar Tax Regulations

4.3 Opportunities

4.3.1 Premium & Craft Frozen Cocktail Concepts

4.3.2 Plant-Based & Functional Smoothie Expansion

4.3.3 Smart Self-Serve Dispensing Systems

4.3.4 Emerging Market Franchise Expansion

4.4 Challenges

4.4.1 Seasonal Revenue Volatility

4.4.2 Competitive QSR Pricing Pressure

4.4.3 Aggregator Commission Margin Impact

4.4.4 Supply Chain Sensitivity

5. Global Frozen Drinks Market Analysis (USD Billion), 2026–2033

5.1 Market Size Overview

5.2 CAGR Analysis

5.3 Region-Wise Revenue Distribution

5.4 Product-Wise Revenue Split

5.5 Margin & Pricing Trend Analysis

6. Market Segmentation by Product Type (USD Billion), 2026–2033

6.1 Non-Alcoholic Frozen Drinks

6.1.1 Slushies / Ice Slush

6.1.1.1 Carbonated Slush

6.1.1.2 Fruit-Based Slush

6.1.1.3 Functional / Vitamin-Infused Slush

6.1.2 Smoothies

6.1.2.1 Fruit Smoothies

6.1.2.2 Dairy-Based Smoothies

6.1.2.3 Plant-Based Smoothies

6.1.3 Frozen Carbonated Beverages

6.1.3.1 Cola-Based Frozen Drinks

6.1.3.2 Flavored Soda Frozen Drinks

6.1.3.3 Energy-Infused Frozen Drinks

6.1.4 Frozen Coffee & Frappes

6.1.4.1 Coffee-Based Frappes

6.1.4.2 Chocolate / Mocha Variants

6.1.4.3 Specialty / Premium Frappes

6.2 Alcoholic Frozen Drinks

6.2.1 Frozen Cocktails

6.2.1.1 Frozen Margaritas

6.2.1.2 Frozen Daiquiris

6.2.1.3 Frozen Piña Coladas

6.2.2 Frozen Beer & Malt-Based Drinks

6.2.2.1 Frozen Draft Beer

6.2.2.2 Malt-Based Frozen Slush

6.2.3 Frozen Wine-Based Beverages

6.2.3.1 Frozen Rosé (Frosé)

6.2.3.2 Sparkling Frozen Wine Blends

7. Market Segmentation by Ingredient Type (USD Billion), 2026–2033

7.1 Fruit-Based

7.1.1 Citrus-Based

7.1.1.1 Lemon & Lime Slush

7.1.1.2 Orange-Based Frozen Drinks

7.1.1.3 Grapefruit Variants

7.1.2 Berry-Based

7.1.2.1 Strawberry Blends

7.1.2.2 Blueberry & Raspberry Mixes

7.1.2.3 Mixed Berry Fusion

7.1.3 Tropical Fruit Blends

7.1.3.1 Mango-Based Frozen Drinks

7.1.3.2 Pineapple & Passionfruit

7.1.3.3 Exotic Multi-Fruit Combinations

7.2 Dairy-Based

7.2.1 Milk-Based

7.2.1.1 Classic Milkshakes

7.2.1.2 Flavored Frozen Milk Beverages

7.2.1.3 Chocolate-Based Variants

7.2.2 Yogurt-Based

7.2.2.1 Frozen Yogurt Smoothies

7.2.2.2 Probiotic-Enriched Blends

7.2.2.3 Greek Yogurt Frozen Drinks

7.2.3 Cream-Based

7.2.3.1 Ice Cream-Based Shakes

7.2.3.2 Premium Dessert Frozen Drinks

7.2.3.3 Whipped Cream-Topped Variants

7.3 Plant-Based

7.3.1 Almond / Soy / Oat-Based

7.3.1.1 Almond Milk Smoothies

7.3.1.2 Soy-Based Frozen Beverages

7.3.1.3 Oat Milk Frappes

7.3.2 Coconut-Based

7.3.2.1 Coconut Milk Smoothies

7.3.2.2 Coconut Cream Frozen Blends

7.3.2.3 Tropical Coconut Slush Variants

7.4 Alcohol-Infused

7.4.1 Spirit-Based

7.4.1.1 Vodka-Based Frozen Cocktails

7.4.1.2 Rum-Based Daiquiris

7.4.1.3 Tequila-Based Margaritas

7.4.2 Wine-Based

7.4.2.1 Frozen Sangria

7.4.2.2 Wine Slushies

7.4.2.3 Sparkling Wine Frozen Blends

7.4.3 Beer-Based

7.4.3.1 Frozen Beer Cocktails

7.4.3.2 Craft Beer Slush Variants

7.4.3.3 Beer-Mixed Frozen Blends

8. Market Segmentation by Distribution Channel (USD Billion), 2026–2033

8.1 Quick-Service Restaurants (QSRs)

8.1.1 Global QSR Chains

8.1.2 Regional Franchise Chains

8.1.3 Independent Outlets

8.2 Cafés & Coffee Chains

8.2.1 International Coffee Brands

8.2.2 Local Café Chains

8.3 Bars & Nightclubs

8.3.1 Premium Cocktail Bars

8.3.2 Casual Bars & Lounges

8.4 Entertainment & Leisure Venues

8.4.1 Cinemas

8.4.2 Theme Parks

8.4.3 Sports Arenas

8.5 Retail & Convenience

8.5.1 Convenience Stores

8.5.2 Supermarkets (Ready-to-Freeze Packs)

9. Market Segmentation by End-User (USD Billion), 2026–2033

9.1 Individual Consumers

9.1.1 Youth / Teen Consumers

9.1.2 Working Professionals

9.1.3 Health-Conscious Consumers

9.2 Commercial & Hospitality

9.2.1 Hotels & Resorts

9.2.2 Catering & Event Services

9.2.3 Cruise & Tourism Operators

10. Market Segmentation by Geography

10.1 North America

10.2 Europe

10.3 Asia-Pacific

10.4 Latin America

10.5 Middle East & Africa

11. Competitive Landscape – Global

11.1 Market Share Analysis

11.2 Brand Positioning Matrix

11.3 QSR Partnership & Syrup Supply Chain Analysis

11.4 Competitive Intensity Mapping

11.5 Strategic Expansion Trends

12. Company Profiles

12.1 The Coca-Cola Company

12.2 PepsiCo Inc.

12.3 McDonald’s Corporation

12.4 Starbucks Corporation

12.5 Jamba (GoTo Foods)

12.6 Sonic Drive-In

12.7 Taco Bell

12.8 Keurig Dr Pepper

12.9 Nestlé S.A.

13. Regional Insights

13.1 North America – Largest Market

13.2 Europe – Tourism & Wine-Based Frozen Growth

13.3 Asia-Pacific – Fastest Growing Region

13.4 Latin America – Climate & Fruit Culture

13.5 Middle East & Africa – High-Temperature Demand

14. Strategic Intelligence & Pheonix AI-Backed Insights

14.1 Pheonix Demand Forecast Engine

14.2 Climate-Based Demand Modeling

14.3 Alcohol Adoption Trend Mapping

14.4 Smart Dispensing & Automation Analytics

14.5 Automated Porter’s Five Forces Analysis

15. Future Outlook & Strategic Recommendations

15.1 Premiumization & Craft Frozen Cocktail Growth

15.2 Low-Sugar & Functional Beverage Expansion

15.3 Plant-Based Product Innovation

15.4 Smart Dispensing System Investments

15.5 Long-Term Market Outlook (2033+)

16. Appendix

17. About Us

18. Disclaimer

Competitive Landscape

Competitive Landscape of the Global Frozen Drinks Market

Executive Framing

The Global Frozen Drinks Market is a dynamic and high-growth segment within the global foodservice and beverage industry. Characterized by intense competition among major QSR brands, beverage conglomerates, and emerging craft frozen drink innovators, the market demands constant innovation, premiumization, and digital engagement. With Tier 1 players such as The Coca-Cola Company, PepsiCo Inc., McDonald’s Corporation, and Starbucks Corporation dominating large-scale distribution, the competitive intensity is complemented by a growing number of specialty and regional players offering plant-based, alcohol-infused, and low-sugar frozen beverages. Strategic positioning through product innovation, sustainability, and technology integration has become critical for long-term market leadership.

Current Market Reality

The market is witnessing a surge in both non-alcoholic and alcoholic frozen beverages, including slushies, smoothies, frappes, and frozen cocktails. North America currently dominates, driven by QSR expansion, frozen cocktail culture, and summer-season demand. Asia-Pacific represents the fastest-growing region due to rapid urbanization, rising youth populations, and adoption of international café and franchise formats.

Premium and alcohol-infused frozen beverages are gaining traction, while low-sugar, plant-based, and visually appealing formulations are attracting health-conscious and social media-savvy consumers. Investments in smart dispensing systems, climate-adaptive recipes, and centralized beverage hubs illustrate the technological advancements shaping competitive differentiation. Strategic alliances and partnerships, such as syrup supply collaborations and franchise expansions, further underscore the need for agility and innovation in maintaining market relevance.

Key Signals and Evidence

- Rapid expansion of QSR and café franchises, particularly in Asia-Pacific, signals strong growth potential in emerging markets.

- High adoption of premium, alcohol-infused, and low-sugar frozen drinks reflects evolving consumer tastes and health-conscious trends.

- Investment in smart dispensing systems, automated beverage machines, and operational automation highlights technological differentiation.

- Social media-driven, Instagram-friendly frozen drinks drive brand visibility and influence consumer choice.

- Sustainability initiatives, including recyclable cups and plant-based formulations, increasingly impact consumer perception and competitive positioning.

Strategic Implications

- Brand & Product Differentiation: Launching premium, alcohol-infused, plant-based, or fruit-forward frozen beverages to capture niche and high-margin segments.

- Geographic Expansion: Targeting fast-growing regions in Asia-Pacific and Latin America through franchise partnerships and localized offerings.

- Technology Integration: Leveraging smart dispensing, automated systems, and AI-driven demand forecasting for operational efficiency and enhanced consumer experience.

- Sustainability Initiatives: Implementing eco-friendly packaging, climate-responsive beverage solutions, and plant-based ingredients to align with consumer and regulatory expectations.

- Consumer Engagement: Utilizing social media and experiential campaigns to drive brand loyalty among youth and urban consumers.

Forward Outlook

The Global Frozen Drinks Market is projected to grow from USD 12.9 billion in 2025 to ~USD 21.8 billion by 2033, representing a CAGR of ~6.8%. Growth will be fueled by premiumization, alcohol-infused frozen beverages, low-sugar and plant-based innovations, and smart dispensing technology. North America will remain the largest market, while Asia-Pacific emerges as the fastest-growing region, driven by youth-focused, urban, and franchise-led consumption.

The market is expected to evolve along a dual-structure model: high-margin specialty offerings, including craft frappes, premium smoothies, and alcohol-infused frozen beverages for urban and hospitality-driven consumers, alongside scalable non-alcoholic frozen drinks like slushies and frappes for mass-market QSR, cinema, and theme park distribution. Companies investing in AI-driven forecasting, automated dispensing, sustainable practices, and climate-adaptive product innovation will secure competitive advantage and long-term profitability.

Value Chain

Global Frozen Drinks Market: Value Chain & Market Dynamics

Executive Framing

The global frozen drinks market has evolved into a high-margin, experiential beverage category, encompassing non-alcoholic and alcoholic frozen beverages such as slushies, smoothies, frappes, frozen coffee drinks, and frozen cocktails. Market dynamics are shaped by urbanization, youth-driven consumption, QSR expansion, premiumization trends, and technological advancements in dispensing systems.

The market operates through a hybrid value chain, combining large-scale beverage production with agile, innovation-led formulation ecosystems. While global beverage conglomerates leverage centralized syrup production and wide distribution networks, smaller players focus on localized flavors, plant-based ingredients, and direct-to-consumer or seasonal sales models. This dual structure creates both efficiency and fragmentation across the value chain.

Challenges include ingredient traceability (e.g., fruit blends, plant-based milk, alcohol-infused mixes), regulatory oversight on sugar and alcohol content, and compliance with labeling and health claims. Packaging sustainability and climate-driven consumption patterns add further operational complexity.

Current Market Reality

The current frozen drinks value chain exhibits moderate-to-high complexity, balancing mass production efficiency with premium, differentiated offerings. Leading companies such as The Coca-Cola Company (Frozen Fanta, Frozen Coke) and PepsiCo (Slurpee, Frozen Mountain Dew) control upstream syrup production and downstream distribution through integrated operations.

Upstream, ingredient sourcing ranges from standardized syrup bases and alcohol extracts to fresh fruit blends and plant-based alternatives, creating variability in cost, quality, and supply reliability. This supports tiered production strategies and varied pricing models.

Midstream operations focus on formulation, blending, and freezing across multiple formats: slushies, smoothies, frozen carbonated beverages, frappes, and alcoholic frozen cocktails. Product innovation emphasizes low-sugar, fruit-forward, plant-based, and alcohol-infused variants, increasing R&D intensity and demand for smart dispensing technologies.

Downstream distribution is highly diversified, including QSRs, cafés, bars, entertainment venues, cinemas, theme parks, convenience stores, supermarkets, and online channels. Direct-to-consumer subscription models, seasonal pop-ups, and experiential outlets are reshaping traditional retail dominance, enabling smaller brands to reach consumers without major infrastructure investments.

Despite operational sophistication, key bottlenecks remain: ingredient traceability for natural or plant-based inputs, sustainability challenges in packaging, and seasonality-driven supply-demand imbalances.

Key Signals and Evidence

Critical indicators shaping the frozen drinks value chain include:

- Market growth from USD 12.9 billion (2025) to ~USD 21.8 billion (2033) at a CAGR of ~6.8%, reflecting steady adoption of premium and alcohol-infused frozen beverages.

- Rising demand for low-sugar, plant-based, and alcohol-infused frozen drinks, driving upstream ingredient diversification and midstream formulation innovation.

- Dual product structure: non-alcoholic frozen drinks for mass-market and premium alcoholic frozen cocktails for urban and hospitality-driven consumption.

- Rapid growth in Asia-Pacific highlights localized sourcing, seasonal distribution, and cost-efficient production models.

- Expansion of e-commerce, subscription, and smart dispensing systems strengthens direct-to-consumer channels and reduces reliance on traditional retail.

Supplier power is moderate for fruit concentrates, plant-based ingredients, and equipment providers, while buyer power is high in QSR and retail segments due to brand switching, seasonal promotions, and price sensitivity.

Strategic Implications

The frozen drinks value chain presents both opportunities and structural challenges. Companies must navigate the trade-off between scale efficiency and product differentiation.

Global beverage conglomerates leverage centralized syrup production, QSR partnerships, and retail distribution while simultaneously innovating in plant-based, low-sugar, and premium frozen beverages to defend market share.

Emerging and niche players gain advantage through value chain agility, sourcing unique ingredients, experimenting with plant-based or alcohol-infused recipes, and leveraging digital or seasonal distribution models.

Technology integration is critical: AI-assisted demand forecasting, smart dispensing systems, and supply chain analytics improve production efficiency, optimize distribution, and enhance consumer targeting. Sustainable packaging initiatives also become a differentiator for environmentally conscious consumers and regulatory compliance.

Forward Outlook

The frozen drinks market value chain is expected to evolve significantly over the next decade, driven by innovation, digitalization, and sustainability imperatives.

- Greater integration of premium and alcoholic frozen drinks with mass-market non-alcoholic offerings.

- Expansion of personalized and subscription-based delivery models enabled by data-driven insights.

- Increased investment in regional manufacturing and dispensing hubs, particularly in Asia-Pacific and North America.

- Enhanced focus on sustainable sourcing, low-sugar formulations, and plant-based ingredients to align with regulatory and consumer expectations.

Companies that ensure ingredient transparency, multi-format production efficiency, and omnichannel distribution resilience will be best positioned to capture long-term market value.

In conclusion, the frozen drinks market is transitioning from a seasonal beverage category into a premium, innovation-driven, multi-format ecosystem, where operational efficiency, product differentiation, and sustainability collectively define competitive leadership.

Investment Activity

Investment & Funding Dynamics – Global Frozen Drinks Market

Executive Framing

Current Market Reality

The Global Frozen Drinks Market is experiencing a rising trend in investment activity, fueled by premiumization, alcohol-infused frozen beverages, and technological advancements in smart dispensing systems. Key investors include private equity firms, franchise-focused funds, and beverage conglomerates seeking to capture growth in both non-alcoholic and alcoholic frozen beverage segments. Mergers and acquisitions (M&A) are occurring selectively, often aimed at acquiring innovative beverage technologies, proprietary recipes, or distribution networks to enhance competitive positioning. Companies such as The Coca-Cola Company, PepsiCo, and Starbucks are actively investing in product development, seasonal flavor launches, and AI-enabled operational efficiency, reflecting strategic emphasis on brand growth and experiential beverage offerings.

Key Signals and Evidence

- Premium & Alcohol-Infused Growth: Rising consumer interest in craft frozen cocktails and limited-edition beverage blends encourages capital inflow into product innovation.

- Technology Integration: Investments in smart dispensing systems and automated frozen beverage machines increase operational efficiency and enhance consumer experience.

- Sustainability & Health Trends: Growing demand for plant-based, low-sugar, and environmentally friendly packaging solutions attracts investor focus on sustainable product development.

- Franchise & QSR Expansion: Rapid growth of global and regional QSR chains presents scalable investment opportunities in beverage deployment infrastructure.

- Consumer Experience & Digital Engagement: Social media-driven marketing, seasonal flavor campaigns, and experiential beverage offerings drive higher brand visibility, influencing investor confidence.

- M&A Activity: Selective acquisitions target proprietary recipes, innovative dispensing technologies, and premium brand portfolios to strengthen market share.

Strategic Implications

For market players, aligning product innovation with premiumization, alcohol-infused offerings, and sustainable practices is critical. Companies investing strategically in technology-enabled dispensing systems and seasonal flavor innovation gain a competitive edge. For investors, the market presents opportunities for high-margin returns in urban and youth-centric consumption segments, while also offering scalability in mass-market frozen drinks across QSRs, cinemas, and theme parks. Strategic M&A activity allows for consolidation and rapid capability expansion, particularly in premium or specialty frozen beverage categories.

Forward Outlook

The Global Frozen Drinks Market is expected to see continued investment growth from 2026 to 2033. Capital will flow toward premiumization, alcohol-infused beverages, plant-based formulations, and AI-enabled operational optimization. M&A activity will remain selective, focused on acquiring technologies, recipes, and distribution networks that accelerate innovation and market expansion. Investors who prioritize sustainable packaging, low-sugar product lines, and smart dispensing systems will capture long-term value in both premium and mass-market segments.

Technology & Innovation

Global Frozen Drinks Market: Technology & Innovation

Executive Framing

In the evolving landscape of the global frozen drinks market, technology and innovation are key drivers shaping growth and competitive advantage. Consumer demand is shifting toward premium, alcohol-infused, plant-based, and low-sugar beverages, encouraging manufacturers to leverage smart dispensing systems, advanced blending technologies, and sustainable packaging solutions. Digital marketing, AI-driven consumer insights, and seasonal flavor experimentation are also central to differentiation and engagement. These technological and innovative efforts are crucial for efficiency, environmental compliance, and brand loyalty in a highly competitive and seasonal market.

Current Market Reality

The current frozen drinks market is characterized by innovation in beverage machines, flavor experimentation, and premiumized offerings. QSR chains, cafés, and entertainment venues are adopting automated dispensing systems, while plant-based, low-sugar, and functional blends are gaining traction. Alcohol-infused frozen beverages are emerging as a high-margin segment. Companies are integrating digital ordering, subscription services, and social media-driven campaigns to enhance visibility and consumer engagement. Sustainability efforts, such as recyclable cups and eco-friendly ingredients, are increasingly influencing brand perception.

Key Signals and Evidence

- Premiumization & Alcohol-Infused Expansion: Demand for high-margin, experiential frozen beverages drives innovation in flavor, ingredients, and presentation.

- Smart Dispensing Technology: Automated machines, IoT-enabled beverage systems, and efficient cold-chain equipment improve consistency, speed, and operational efficiency.

- Plant-Based & Low-Sugar Innovations: Rising health-conscious consumption supports new formulations and functional beverage development.

- Digital & AI-Driven Insights: Analytics platforms inform menu design, seasonal offerings, and consumer targeting across QSRs, cafés, and online channels.

- Sustainability Practices: Eco-friendly packaging, energy-efficient equipment, and responsibly sourced ingredients align with consumer expectations and regulatory requirements.

Strategic Implications

For operators and manufacturers, technology and innovation enhance operational efficiency, product differentiation, and consumer experience. High-margin specialty offerings, such as alcohol-infused frozen cocktails, plant-based smoothies, and limited-edition flavors, drive profitability in premium channels. Scalable solutions, like automated slush machines and frozen beverage kits, optimize mass-market distribution. Investment in AI analytics, climate-responsive planning, and sustainable production strengthens competitive positioning while supporting environmental and regulatory compliance.

Forward Outlook

The global frozen drinks market is expected to continue a dual-growth path: premium, experiential, and specialty offerings capturing high margins, while scalable, standardized frozen beverages maintain mass-market accessibility. Innovation will focus on smart dispensing, plant-based formulations, low-sugar recipes, flavor experimentation, and immersive digital engagement. Companies that successfully combine operational technology, consumer-centric product development, and sustainability initiatives will secure competitive advantage, brand loyalty, and long-term profitability in the post-2026 market landscape.

Market Risk

Risk Factors and Disruption Threats in the Global Frozen Drinks Market

Executive Framing

The Global Frozen Drinks Market is a rapidly evolving beverage segment, encompassing non-alcoholic and alcoholic frozen beverages, smoothies, slushies, frappes, and frozen cocktails. Despite a healthy CAGR of ~6.8% from 2026–2033, the market faces operational and strategic risks related to seasonal demand fluctuations, raw material availability, regulatory compliance, and competition in the QSR and hospitality sectors. Consumer trends toward low-sugar, plant-based, and premium beverages further shape risk exposure for manufacturers and distributors.

Current Market Reality

North America currently holds the largest market share, while Asia-Pacific is the fastest-growing region. Risks stem from dependence on QSR channels, seasonal and climate-driven consumption patterns, and rising input costs for fruit-based, plant-based, and alcohol-infused ingredients. Supply chain disruptions, particularly in flavor concentrates and frozen beverage equipment, can affect production and timely delivery. Additionally, regulatory compliance regarding alcohol-infused frozen drinks, health claims, and labeling adds complexity for multi-jurisdiction operations.

Key Signals and Evidence

Indicators of risk include fluctuations in youth-driven and social consumption trends, climate-dependent sales patterns, and high buyer power within QSR and entertainment channels due to brand substitution options. Emerging premium and alcohol-infused frozen drink products provide growth opportunities but also increase operational complexity. Investments in smart dispensing systems, automated freezing equipment, and sustainable packaging are essential to mitigate production and environmental risks.

Strategic Implications

Companies must manage operational risks through diversified distribution channels (QSRs, cafés, entertainment venues, retail, and online), scalable production, and climate-sensitive demand planning. Strategic investment in AI-driven forecasting, advanced dispensing technology, low-sugar and plant-based formulations, and sustainable packaging can reduce supply chain and reputational risks. Regional expansion into high-growth APAC markets requires careful navigation of regulatory compliance, cultural consumption patterns, and localized flavor preferences.

Forward Outlook

The Global Frozen Drinks Market is expected to grow steadily, driven by QSR expansion, premiumization, and innovative product offerings. However, stakeholders must remain vigilant about seasonal demand fluctuations, supply chain dependencies, and evolving consumer preferences. Proactive investments in technology, sustainable practices, and product innovation will enable companies to minimize risks and maximize long-term competitive advantage.

Regulatory Landscape

Regulatory & Policy Landscape: Global Frozen Drinks Market

Executive Framing

The Global Frozen Drinks Market is governed by a mix of food safety, labeling, alcohol, and health regulations depending on product type (non-alcoholic vs. alcoholic). Compliance is critical for product safety, market access, and brand credibility. Regulatory requirements differ by region, covering ingredients, nutritional labeling, allergen declaration, alcohol content, marketing, and online sales.

Current Market Reality

North America has stringent regulations for both non-alcoholic and alcoholic frozen beverages. Agencies like the U.S. Food & Drug Administration (FDA) and Alcohol and Tobacco Tax and Trade Bureau (TTB) regulate ingredients, nutritional labeling, alcohol content, and advertising practices. E-commerce and QSR delivery must adhere to age verification and responsible service guidelines.

Europe enforces strict food safety and labeling standards under EFSA, with additional country-specific alcohol and health regulations. Seasonal, fruit-based, and alcohol-infused frozen drinks must comply with allergen disclosures, sugar content labeling, and responsible marketing initiatives.

Asia-Pacific presents a fragmented regulatory landscape, where countries like China, India, and Japan have separate rules for dairy-based, plant-based, and alcoholic frozen beverages. Labeling, alcohol permits, and health-related claims require localized compliance. Latin America follows regional guidelines for sugar content, beverage classification, and promotional restrictions. The Middle East & Africa maintain strict alcohol licensing laws, though non-alcoholic frozen drinks face fewer restrictions.

Key Signals and Evidence

- Mandatory nutritional labeling for sugar, calorie, and allergen content.

- Alcohol content labeling for frozen cocktails and slush beverages.

- Age restrictions and verification for alcoholic frozen drinks.

- Advertising limitations targeting minors or health claims.

- Food safety certification and hygiene compliance for QSR outlets and production units.

- Sustainability and packaging directives affecting frozen beverage cups, straws, and disposables.

Strategic Implications

Regulatory compliance is critical for both product safety and consumer trust. Premium frozen beverages, plant-based drinks, and alcoholic slush products gain competitive advantage through adherence to labeling, allergen, and environmental standards. QSRs, cafés, and online delivery platforms must ensure age verification, hygiene, and responsible marketing to mitigate legal and reputational risks.

Emerging markets require careful navigation of local food and beverage laws, import regulations, and licensing requirements. Brands innovating in low-sugar, plant-based, or alcohol-infused frozen formats must align new product launches with local compliance frameworks to maintain market access and growth momentum.

Forward Outlook

Regulatory oversight is expected to tighten, particularly around nutritional labeling, low-sugar claims, plant-based beverage standards, and alcohol-infused frozen drink marketing. E-commerce and direct-to-consumer frozen beverage delivery will face stricter age verification and hygiene requirements. Sustainable packaging, biodegradable cups, and eco-friendly straws will likely become mandatory in multiple regions.

Companies proactively implementing compliance, sustainability practices, and transparent labeling will be well-positioned to capitalize on premiumization trends, regulatory alignment, and evolving consumer preferences in both mature and emerging markets.