Global Ready to Drink Beverages Market Report Analysis, Size and Forecast 2026-2033

Global Ready-to-Drink (RTD) Beverages Market Forecast Snapshot: 2026–2033

| Metric | Value |

|---|---|

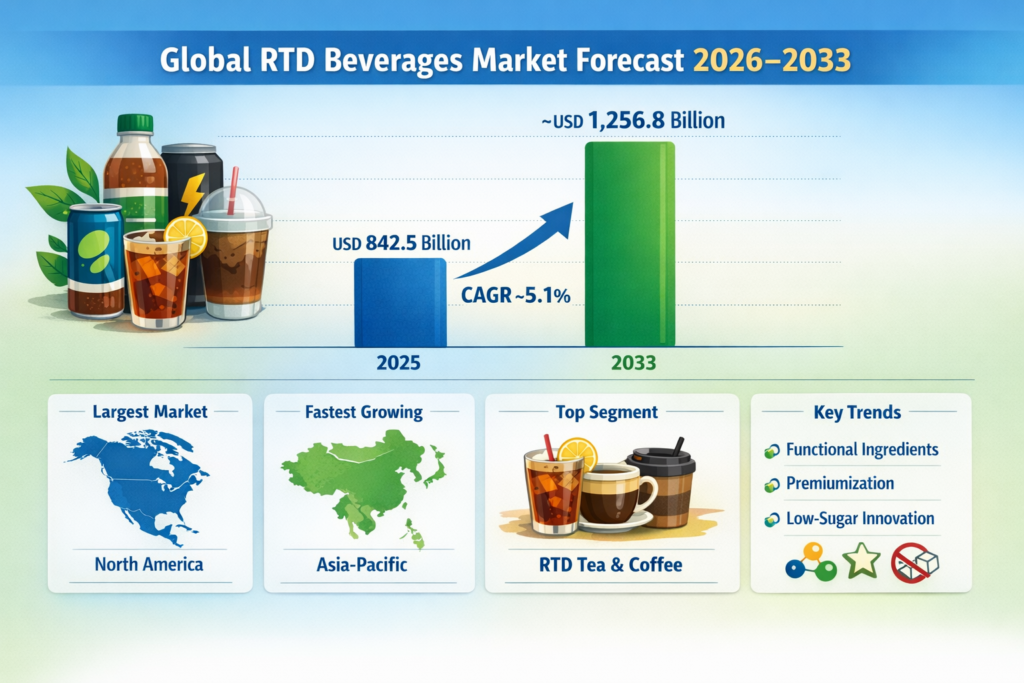

| 2025 Market Size | USD 842.5 Billion |

| 2033 Market Size | ~USD 1,256.8 Billion |

| CAGR (2026–2033) | ~5.1% |

| Largest Region | North America |

| Fastest Growing Region | Asia-Pacific |

| Top Segment | RTD Tea & Coffee |

| Key Trend | Functional Ingredients, Premiumization & Low-Sugar Innovation |

| Future Focus | Clean-Label Formulations, AI-Driven Supply Chains & Sustainable Packaging |

Global Ready-to-Drink (RTD) Beverages Market Overview

The Global Ready-to-Drink (RTD) Beverages Market includes RTD tea, RTD coffee, functional and energy drinks, dairy and plant-based beverages, flavored water, juices, sports drinks, and alcoholic RTDs distributed through retail, hospitality, and digital commerce platforms.

RTD beverages have evolved from simple convenience drinks into a diversified, innovation-driven category aligned with modern lifestyles. Growth is fueled by increasing demand for on-the-go consumption, rising health consciousness, premium and craft beverage experimentation, plant-based alternatives, and strong compatibility with e-commerce and subscription-based delivery models.

According to Pheonix Research, the Global Ready-to-Drink (RTD) Beverages Market is valued at USD 842.5 billion in 2025 and is projected to reach approximately USD 1,256.8 billion by 2033, reflecting a CAGR of ~5.1% during 2026–2033.

North America holds the largest market share, supported by diversified beverage portfolios, advanced retail infrastructure, and strong consumer purchasing power. Asia-Pacific represents the fastest-growing region, driven by rapid urbanization, expanding middle-class populations, rising disposable incomes, and growing demand for premium and functional beverages.

The Post-2025 outlook indicates accelerating innovation in functional ingredients, sugar-reduction strategies, AI-driven demand forecasting, sustainable packaging transformation, and expansion of plant-based and premium RTD formats across global markets.

Global Ready-to-Drink (RTD) Beverages Market Segmentation

1. By Product Type

1.1 RTD Tea

1.1.1 Black Tea

1.1.1.1 Sweetened Black Tea

1.1.1.2 Unsweetened Black Tea

1.1.1.3 Lemon-Flavored Black Tea

1.1.1.4 Herbal-Infused Black Tea

1.1.2 Green Tea

1.1.2.1 Matcha-Based Green Tea

1.1.2.2 Antioxidant-Enriched Green Tea

1.1.2.3 Organic Certified Green Tea

1.1.2.4 Functional Blend Green Tea

1.2 RTD Coffee

1.2.1 Cold Brew Coffee

1.2.1.1 Nitro Cold Brew

1.2.1.2 High-Caffeine Cold Brew

1.2.1.3 Dairy-Based Cold Brew

1.2.1.4 Plant-Based Cold Brew (Oat/Almond)

1.2.2 Iced Coffee

1.2.2.1 Flavored Iced Coffee

1.2.2.2 Sugar-Free Iced Coffee

1.2.2.3 Protein-Enriched Iced Coffee

1.2.2.4 Premium Café-Style Editions

1.3 Functional & Energy Drinks

1.3.1 Vitamin-Fortified Functional Drinks

1.3.1.1 Multivitamin-Infused

1.3.1.2 Immunity-Boost Variants

1.3.1.3 Mineral-Enriched Blends

1.3.1.4 Antioxidant-Focused Formulations

1.3.2 Electrolyte & Performance Drinks

1.3.2.1 Hydration-Focused Variants

1.3.2.2 Sports Recovery Blends

1.3.2.3 Endurance Support Drinks

1.3.2.4 Thermogenic Performance Formulations

1.4 Dairy & Plant-Based Beverages

1.4.1 Flavored Milk

1.4.1.1 Chocolate Variants

1.4.1.2 Fruit-Flavored Milk

1.4.1.3 High-Protein Milk

1.4.1.4 Lactose-Free Options

1.4.2 Plant-Based Beverages

1.4.2.1 Oat-Based Drinks

1.4.2.2 Soy-Based Drinks

1.4.2.3 Almond-Based Drinks

1.4.2.4 Functional Plant Blends

1.5 Alcoholic RTDs

1.5.1 Hard Seltzers

1.5.1.1 Low-Calorie Seltzers

1.5.1.2 Fruit-Infused Variants

1.5.1.3 Zero-Sugar Seltzers

1.5.1.4 Premium Craft Seltzers

1.5.2 RTD Cocktails & Spirits

1.5.2.1 Classic Cocktail Mixes

1.5.2.2 Canned Spirits

1.5.2.3 Low-ABV Craft Mixers

1.5.2.4 Premium Imported Variants

2. By Packaging Type

2.1 Cans

2.1.1 Standard Aluminum Cans

2.1.1.1 250 ml

2.1.1.2 330 ml

2.1.1.3 500 ml

2.1.1.4 Limited-Edition Designs

2.2 Bottles

2.2.1 PET Bottles

2.2.1.1 Resealable Bottles

2.2.1.2 Recycled PET

2.2.1.3 Bulk Value Packs

2.2.1.4 Travel-Friendly Formats

2.2.2 Glass Bottles

2.2.2.1 Premium Glass Packaging

2.2.2.2 Specialty Café Editions

2.2.2.3 Limited Vintage Designs

2.2.2.4 Sustainable Reusable Glass

2.3 Sustainable Packaging

2.3.1 Biodegradable Formats

2.3.1.1 Compostable Materials

2.3.1.2 Plant-Based Plastics

2.3.1.3 Carbon-Neutral Packaging

2.3.1.4 Refillable Concepts

3. By Distribution Channel

3.1 Off-Trade / Retail

3.1.1 Supermarkets & Hypermarkets

3.1.1.1 Premium Shelf Placement

3.1.1.2 Promotional Multipacks

3.1.1.3 Private Label Variants

3.1.1.4 Seasonal Campaign Displays

3.1.2 Convenience Stores

3.1.2.1 Urban High-Traffic Locations

3.1.2.2 Highway & Travel Retail

3.1.2.3 24/7 Quick-Service Outlets

3.1.2.4 Impulse Purchase Displays

3.2 On-Trade / Hospitality

3.2.1 Cafés & Coffee Chains

3.2.1.1 Branded RTD Offerings

3.2.1.2 Seasonal Specials

3.2.1.3 Premium Menu Integration

3.2.1.4 Event Collaborations

3.3 E-Commerce

3.3.1 Online Retail Platforms

3.3.1.1 National Grocery Platforms

3.3.1.2 Cross-Border Marketplaces

3.3.1.3 Flash Sale Channels

3.3.1.4 Subscription Models

4. By End-User

4.1 Individual Consumers

4.1.1 Millennials & Gen Z

4.1.1.1 Trend-Driven Buyers

4.1.1.2 Gaming & Digital Consumers

4.1.1.3 Fitness-Oriented Buyers

4.1.1.4 Social Lifestyle Consumers

4.1.2 Working Professionals

4.1.2.1 Corporate Employees

4.1.2.2 Entrepreneurs & Freelancers

4.1.2.3 Shift Workers

4.1.2.4 Long-Hour Commuters

4.2 Corporate & Institutional Buyers

4.2.1 Office Procurement

4.2.1.1 Pantry Supply Contracts

4.2.1.2 Employee Wellness Programs

4.2.1.3 Bulk Subscription Agreements

4.2.1.4 Corporate Event Supply

4.2.2 Hospitality & Events

4.2.2.1 Hotel Chains

4.2.2.2 Catering Services

4.2.2.3 Conference & Exhibition Supply

4.2.2.4 Airline & Travel Catering

5. By Region

5.1 North America

5.2 Europe

5.3 Asia-Pacific

5.4 Latin America

5.5 Middle East & Africa

Leading Companies in the Global RTD Beverages Market

PepsiCo Inc.

The Coca-Cola Company

Nestlé S.A.

Starbucks Corporation

Danone S.A.

Keurig Dr Pepper

Asahi Group Holdings

Suntory Beverage & Food

Monster Beverage Corporation

PepsiCo Inc. remains one of the largest players in the RTD beverages market in terms of portfolio diversification and global distribution strength. The company operates across tea, coffee, energy, and functional beverage segments, supported by extensive international retail penetration.

Why the Global RTD Beverages Market Remains Critical

-

Strong alignment with convenience-driven consumption trends

-

High scalability across premium and mass-market formats

-

Rapid innovation in functional and plant-based beverages

-

Expansion of low-sugar and clean-label product lines

-

Growing penetration of subscription and digital commerce models

Strategic Intelligence & AI-Driven Insights

Pheonix Demand Forecast Engine

Identifies steady global expansion supported by urbanization, premiumization, and functional beverage growth acceleration.

Consumer Behavior Analyzer

Highlights rising demand for low-sugar, plant-based, and functional RTD variants among younger demographics.

Innovation & Formulation Tracker

Monitors adaptogens, probiotics, protein enrichment, and sustainable ingredient sourcing trends.

Supply Chain & Retail Optimization Analytics

AI-powered tools enhance inventory forecasting, pricing optimization, and channel performance benchmarking.

Final Takeaway of the Global Ready-to-Drink (RTD) Beverages Market

The Global RTD Beverages Market is transitioning into a premium-focused, health-oriented, and digitally optimized ecosystem. The projected CAGR of ~5.1% (2026–2033) reflects stable long-term expansion supported by functional ingredient innovation, sugar reduction strategies, and omnichannel distribution growth.

Future competitive leadership will be defined by companies that integrate AI-driven demand intelligence, sustainable packaging solutions, clean-label reformulation strategies, and diversified portfolio expansion across tea, coffee, dairy, energy, and alcoholic RTDs.

At Pheonix Research, our advanced forecasting frameworks deliver comprehensive RTD Beverages Market revenue projections, competitive benchmarking, and AI-backed strategic intelligence — enabling stakeholders to capitalize on the Post-2025 beverage landscape with data-driven precision and scalable growth strategies.

📢 Social Mentions & Publication Channels

Explore deeper insights and follow our cross-platform updates on LinkedIn, and X for continuous intelligence and market coverage.

LinkedIn : https://www.linkedin.com/feed/update/urn:li:activity:7430987871366496257

X : https://x.com/Pheonix_Insight/status/2025227170453545192?s=20

Table of Contents

1. Executive Summary

1.1 Market Snapshot (2026–2033)

1.2 Key Growth Highlights

1.3 Largest & Fastest Growing Regions

1.4 Dominant & Emerging Segments

1.5 Strategic Opportunity Areas

2. Global Ready-to-Drink (RTD) Beverages Market Overview

2.1 Market Definition & Scope

2.2 Industry Evolution & Category Diversification

2.3 Value Chain Analysis

2.4 Business Models & Revenue Streams

2.5 Regulatory & Compliance Landscape

2.6 Pricing Trends & Margin Structure

3. Market Forecast Snapshot (2026–2033)

3.1 2025 Market Size: USD 842.5 Billion

3.2 2033 Market Size: ~USD 1,256.8 Billion

3.3 CAGR (2026–2033): ~5.1%

3.4 Largest Region: North America

3.5 Fastest Growing Region: Asia-Pacific

3.6 Top Segment: RTD Tea & Coffee

3.7 Key Trend: Functional Ingredients, Premiumization & Low-Sugar Innovation

3.8 Future Focus: Clean-Label Formulations, AI-Driven Supply Chains & Sustainable Packaging

4. Market Dynamics

4.1 Key Growth Drivers

4.2 Market Restraints

4.3 Emerging Opportunities

4.4 Industry Challenges

4.5 Impact of Macroeconomic Factors

5. Market Segmentation by Product Type (USD Billion), 2026–2033

5.1 RTD Tea

5.1.1 Black Tea

5.1.1.1 Sweetened Black Tea

5.1.1.2 Unsweetened Black Tea

5.1.1.3 Lemon-Flavored Black Tea

5.1.1.4 Herbal-Infused Black Tea

5.1.2 Green Tea

5.1.2.1 Matcha-Based Green Tea

5.1.2.2 Antioxidant-Enriched Green Tea

5.1.2.3 Organic Certified Green Tea

5.1.2.4 Functional Blend Green Tea

5.2 RTD Coffee

5.2.1 Cold Brew Coffee

5.2.1.1 Nitro Cold Brew

5.2.1.2 High-Caffeine Cold Brew

5.2.1.3 Dairy-Based Cold Brew

5.2.1.4 Plant-Based Cold Brew (Oat/Almond)

5.2.2 Iced Coffee

5.2.2.1 Flavored Iced Coffee

5.2.2.2 Sugar-Free Iced Coffee

5.2.2.3 Protein-Enriched Iced Coffee

5.2.2.4 Premium Café-Style Editions

5.3 Functional & Energy Drinks

5.3.1 Vitamin-Fortified Functional Drinks

5.3.1.1 Multivitamin-Infused

5.3.1.2 Immunity-Boost Variants

5.3.1.3 Mineral-Enriched Blends

5.3.1.4 Antioxidant-Focused Formulations

5.3.2 Electrolyte & Performance Drinks

5.3.2.1 Hydration-Focused Variants

5.3.2.2 Sports Recovery Blends

5.3.2.3 Endurance Support Drinks

5.3.2.4 Thermogenic Performance Formulations

5.4 Dairy & Plant-Based Beverages

5.4.1 Flavored Milk

5.4.1.1 Chocolate Variants

5.4.1.2 Fruit-Flavored Milk

5.4.1.3 High-Protein Milk

5.4.1.4 Lactose-Free Options

5.4.2 Plant-Based Beverages

5.4.2.1 Oat-Based Drinks

5.4.2.2 Soy-Based Drinks

5.4.2.3 Almond-Based Drinks

5.4.2.4 Functional Plant Blends

5.5 Alcoholic RTDs

5.5.1 Hard Seltzers

5.5.1.1 Low-Calorie Seltzers

5.5.1.2 Fruit-Infused Variants

5.5.1.3 Zero-Sugar Seltzers

5.5.1.4 Premium Craft Seltzers

5.5.2 RTD Cocktails & Spirits

5.5.2.1 Classic Cocktail Mixes

5.5.2.2 Canned Spirits

5.5.2.3 Low-ABV Craft Mixers

5.5.2.4 Premium Imported Variants

6. Market Segmentation by Packaging Type (USD Billion), 2026–2033

6.1 Cans

6.1.1 Standard Aluminum Cans

6.1.1.1 250 ml

6.1.1.2 330 ml

6.1.1.3 500 ml

6.1.1.4 Limited-Edition Designs

6.2 Bottles

6.2.1 PET Bottles

6.2.1.1 Resealable Bottles

6.2.1.2 Recycled PET

6.2.1.3 Bulk Value Packs

6.2.1.4 Travel-Friendly Formats

6.2.2 Glass Bottles

6.2.2.1 Premium Glass Packaging

6.2.2.2 Specialty Café Editions

6.2.2.3 Limited Vintage Designs

6.2.2.4 Sustainable Reusable Glass

6.3 Sustainable Packaging

6.3.1 Biodegradable Formats

6.3.1.1 Compostable Materials

6.3.1.2 Plant-Based Plastics

6.3.1.3 Carbon-Neutral Packaging

6.3.1.4 Refillable Concepts

7. Market Segmentation by Distribution Channel (USD Billion), 2026–2033

7.1 Off-Trade / Retail

7.1.1 Supermarkets & Hypermarkets

7.1.1.1 Premium Shelf Placement

7.1.1.2 Promotional Multipacks

7.1.1.3 Private Label Variants

7.1.1.4 Seasonal Campaign Displays

7.1.2 Convenience Stores

7.1.2.1 Urban High-Traffic Locations

7.1.2.2 Highway & Travel Retail

7.1.2.3 24/7 Quick-Service Outlets

7.1.2.4 Impulse Purchase Displays

7.2 On-Trade / Hospitality

7.2.1 Cafés & Coffee Chains

7.2.1.1 Branded RTD Offerings

7.2.1.2 Seasonal Specials

7.2.1.3 Premium Menu Integration

7.2.1.4 Event Collaborations

7.3 E-Commerce

7.3.1 Online Retail Platforms

7.3.1.1 National Grocery Platforms

7.3.1.2 Cross-Border Marketplaces

7.3.1.3 Flash Sale Channels

7.3.1.4 Subscription Models

8. Market Segmentation by End-User (USD Billion), 2026–2033

8.1 Individual Consumers

8.1.1 Millennials & Gen Z

8.1.1.1 Trend-Driven Buyers

8.1.1.2 Gaming & Digital Consumers

8.1.1.3 Fitness-Oriented Buyers

8.1.1.4 Social Lifestyle Consumers

8.1.2 Working Professionals

8.1.2.1 Corporate Employees

8.1.2.2 Entrepreneurs & Freelancers

8.1.2.3 Shift Workers

8.1.2.4 Long-Hour Commuters

8.2 Corporate & Institutional Buyers

8.2.1 Office Procurement

8.2.1.1 Pantry Supply Contracts

8.2.1.2 Employee Wellness Programs

8.2.1.3 Bulk Subscription Agreements

8.2.1.4 Corporate Event Supply

8.2.2 Hospitality & Events

8.2.2.1 Hotel Chains

8.2.2.2 Catering Services

8.2.2.3 Conference & Exhibition Supply

8.2.2.4 Airline & Travel Catering

9. Market Segmentation by Region (USD Billion), 2026–2033

9.1 North America

9.2 Europe

9.3 Asia-Pacific

9.4 Latin America

9.5 Middle East & Africa

10. Regional Insights

10.1 North America – Market Leadership

10.2 Asia-Pacific – Rapid Expansion

10.3 Europe – Clean-Label Innovation Focus

10.4 Latin America – Youth-Driven Growth

10.5 Middle East & Africa – Urban Consumption Growth

11. Competitive Landscape

11.1 Market Share Analysis

11.2 Competitive Positioning Matrix

11.3 Mergers & Acquisitions

11.4 Product Launch & Innovation Trends

12. Company Profiles

12.1 PepsiCo Inc.

12.2 The Coca-Cola Company

12.3 Nestlé S.A.

12.4 Starbucks Corporation

12.5 Danone S.A.

12.6 Keurig Dr Pepper

12.7 Asahi Group Holdings

12.8 Suntory Beverage & Food

12.9 Monster Beverage Corporation

13. Strategic Intelligence & AI-Backed Insights

13.1 Pheonix Demand Forecast Engine

13.2 Consumer Behavior Analytics

13.3 Innovation & Formulation Tracker

13.4 Supply Chain & Retail Optimization Intelligence

13.5 Porter’s Five Forces Analysis

14. Why the Global RTD Beverages Market Remains Critical

14.1 Convenience-Driven Consumption Alignment

14.2 Premium Margin Expansion

14.3 Functional & Plant-Based Acceleration

14.4 Digital Commerce & Subscription Scalability

15. Appendix

16. About Pheonix Research

17. Disclaimer

Competitive Landscape

Competitive Landscape of the Global Ready-to-Drink (RTD) Beverages Market

Executive Framing

The Global Ready-to-Drink (RTD) Beverages Market is characterized by high competitive intensity and a moderately consolidated structure, driven by a mix of global beverage giants and emerging niche brands. Industry leaders such as PepsiCo, The Coca-Cola Company, Nestlé, and Danone dominate through diversified product portfolios and extensive global distribution networks. At the same time, innovation-led startups and regional players are intensifying competition by targeting functional, plant-based, and premium segments.

Current Market Reality

The RTD beverages market operates as a multi-category ecosystem, where companies compete across tea, coffee, energy drinks, dairy, plant-based beverages, and alcoholic RTDs. Large corporations leverage scale, brand equity, and retail penetration, while smaller brands focus on differentiation through clean-label ingredients, functional benefits, and premium positioning.

E-commerce, convenience retail, and direct-to-consumer (DTC) channels are rapidly reshaping market dynamics, enabling faster product launches and deeper consumer engagement. Additionally, partnerships with cafés, quick-service restaurants, and hospitality chains are expanding consumption occasions and strengthening brand visibility.

Key Signals and Evidence

Several signals highlight the evolving competitive landscape:

- Diversification across multiple beverage categories, increasing cross-segment competition.

- Strong growth of functional, low-sugar, and plant-based RTD products.

- Expansion of premium and lifestyle-oriented beverage branding strategies.

- Rapid adoption of e-commerce, subscription models, and DTC distribution channels.

- Increasing investment in sustainable packaging and clean-label formulations.

Strategic Implications

Market participants must adopt multi-dimensional strategies to remain competitive:

- Portfolio Diversification: Expanding across tea, coffee, energy, dairy, and alcoholic RTD segments.

- Innovation & Health Positioning: Developing functional, low-sugar, and plant-based beverages.

- Omnichannel Expansion: Strengthening retail, e-commerce, and DTC presence.

- Brand Premiumization: Leveraging lifestyle marketing and premium product lines.

- Sustainability Focus: Investing in eco-friendly packaging and responsible sourcing practices.

Forward Outlook

By 2033, the Global RTD Beverages Market is projected to reach approximately USD 1,256.8 billion, growing at a CAGR of ~5.1%. North America will remain the largest market, while Asia-Pacific will continue to be the fastest-growing region driven by urbanization and rising consumer demand.

The market will evolve through a combination of functional innovation, premiumization, and digital retail transformation. Companies that effectively integrate AI-driven analytics, sustainable packaging, and diversified product portfolios will secure long-term competitive advantage in this expansive and rapidly evolving beverage ecosystem.

Value Chain

Global Ready-to-Drink (RTD) Beverages Market: Value Chain & Market Dynamics

Executive Framing

The global RTD beverages market operates within a highly diversified and scalable value chain, driven by rising demand for convenience, functional nutrition, and premium beverage experiences. As consumers increasingly shift toward on-the-go consumption, the market has evolved into a multi-category ecosystem spanning tea, coffee, energy drinks, dairy, plant-based beverages, and alcoholic RTDs.

The value chain follows a hybrid operational structure, where large multinational beverage companies leverage mass production, global sourcing, and extensive retail networks, while emerging brands focus on niche innovation, clean-label formulations, and direct-to-consumer (DTC) strategies. This dual ecosystem supports both high-volume scalability and rapid product innovation.

However, increasing regulatory scrutiny around sugar content, labeling standards, and sustainability practices, along with rising raw material costs and packaging challenges, continue to shape operational strategies across the market.

Current Market Reality

The RTD beverages value chain is characterized by high complexity, reflecting the wide range of product categories, ingredient diversity, and global distribution networks. Leading players such as PepsiCo, Coca-Cola, and Nestlé operate through vertically integrated and globally optimized supply chains.

Upstream sourcing includes tea leaves, coffee beans, dairy inputs, plant-based ingredients, functional additives, and sweeteners. Variability in agricultural supply, especially for coffee and plant-based inputs, adds complexity to procurement and pricing.

Midstream operations involve processing, blending, pasteurization, carbonation, and packaging across multiple formats such as cans, bottles, and sustainable packaging solutions. Continuous innovation in low-sugar, fortified, and plant-based formulations is driving R&D intensity.

Downstream distribution is highly diversified, spanning supermarkets, convenience stores, cafés, hospitality channels, e-commerce platforms, and subscription-based delivery models, ensuring strong global accessibility.

Key Signals and Evidence

Key indicators highlighting the evolution of the RTD beverages market include:

- Market growth from USD 842.5 billion (2025) to ~USD 1,256.8 billion (2033) at a CAGR of ~5.1%, reflecting stable global expansion.

- Strong demand for functional, low-sugar, and plant-based beverages reshaping product development strategies.

- Dominance of RTD tea and coffee as high-volume, high-frequency consumption categories.

- Rapid expansion in Asia-Pacific, driven by urbanization and rising disposable incomes.

- Growth of e-commerce and subscription-based models, enhancing direct consumer engagement.

Additionally, buyer power remains high due to brand competition and product availability, while supplier power is moderate, influenced by agricultural dependency and commodity price fluctuations.

Strategic Implications

Companies must balance portfolio diversification with operational efficiency to remain competitive in this complex ecosystem. Large players are expected to strengthen their position through global scale, acquisitions, and continuous product innovation.

Emerging brands can capitalize on clean-label positioning, functional ingredients, and digital-first distribution to differentiate and capture niche consumer segments.

Technology integration, including AI-driven demand forecasting, supply chain optimization, and personalized marketing, will play a crucial role in enhancing efficiency and responsiveness.

Sustainability is becoming a core strategic priority, with increasing focus on recyclable packaging, carbon reduction, and responsible sourcing.

Forward Outlook

The RTD beverages market is expected to witness continued transformation driven by health trends, digitalization, and sustainability initiatives.

Key future developments include:

- Expansion of functional and fortified beverage categories

- Growth in plant-based and alternative dairy RTD products

- Increased adoption of sustainable and biodegradable packaging

- Rising importance of AI-powered supply chain and retail analytics

Companies that successfully integrate innovation, ensure supply chain resilience, and build strong omnichannel distribution networks will be best positioned for long-term growth.

In conclusion, the RTD beverages market is evolving into a highly integrated, innovation-driven, and consumer-centric ecosystem, where scale, agility, and sustainability define competitive success.

Investment Activity

Investment & Funding Dynamics – Global Ready-to-Drink (RTD) Beverages Market

Executive Framing

Current Market Reality

Valued at USD 842.5 billion in 2025 and projected to reach ~USD 1,256.8 billion by 2033 (CAGR ~5.1%), the market demonstrates stable and diversified investment inflows. North America leads in capital deployment due to advanced retail infrastructure and strong brand portfolios, while Asia-Pacific is emerging as a high-growth investment destination supported by urbanization and rising consumer demand. Major players such as PepsiCo, Coca-Cola, Nestlé, and Suntory are actively investing in product diversification, sustainable packaging, and global distribution expansion.

Key Signals and Evidence

- Large-Scale Production Investments: High capital allocation toward manufacturing plants, bottling facilities, and global supply chain infrastructure.

- Product Diversification: Continuous investment in RTD tea, coffee, energy drinks, plant-based beverages, and alcoholic RTDs.

- Functional Innovation: Rising R&D spending on probiotics, adaptogens, protein enrichment, and low-sugar formulations.

- Sustainable Packaging: Strong funding toward recyclable materials, biodegradable packaging, and carbon-neutral production initiatives.

- E-Commerce & DTC Growth: Investments in digital platforms, subscription models, and AI-driven retail analytics.

- Emerging Market Expansion: Capital inflow into Asia-Pacific and Latin America to capture high-growth consumer segments.

- M&A Activity: Frequent acquisitions and partnerships to strengthen product portfolios and geographic presence.

Strategic Implications

Market leaders with diversified portfolios, strong distribution networks, and continuous innovation capabilities are best positioned to capture long-term value. Investors are prioritizing companies that can balance scale with agility, leveraging AI-driven demand forecasting, sustainable production practices, and omnichannel retail strategies. Strategic acquisitions and partnerships remain critical to expanding product categories and entering new markets.

Forward Outlook

From 2026 to 2033, investment in the Global RTD Beverages Market is expected to remain robust, with increasing emphasis on functional beverage innovation, plant-based product expansion, and sustainable packaging transformation. AI-enabled supply chain optimization and digital commerce integration will play a pivotal role in shaping future capital allocation. M&A activity is expected to remain strong as companies pursue consolidation and portfolio diversification strategies.

Technology & Innovation

Global Ready-to-Drink (RTD) Beverages Market: Technology & Innovation

Executive Framing

Technology and innovation are at the core of the global RTD beverages market, enabling the transition from convenience-driven products to highly functional, personalized, and premium beverage ecosystems. Advances in formulation science, AI-driven analytics, and sustainable packaging are reshaping how RTD beverages are developed, produced, and distributed. Innovation is increasingly focused on enhancing nutritional value, improving shelf stability, and aligning with clean-label and low-sugar consumer preferences.

Current Market Reality

The RTD beverages market is experiencing rapid innovation across multiple product categories, including tea, coffee, functional drinks, plant-based beverages, and alcoholic RTDs. Manufacturers are integrating functional ingredients such as adaptogens, probiotics, protein, and electrolytes to meet evolving health and wellness demands. AI-driven demand forecasting and smart supply chain systems are improving inventory management and reducing waste. Additionally, sustainable packaging solutions—such as recyclable cans, biodegradable materials, and lightweight bottles—are gaining strong traction across global markets.

Key Signals and Evidence

- Functional Ingredient Innovation: Expansion of probiotics, adaptogens, protein enrichment, and electrolyte formulations enhances product differentiation.

- Clean-Label & Low-Sugar Reformulation: Increasing adoption of natural sweeteners, plant-based ingredients, and transparent labeling practices.

- AI-Driven Supply Chain Optimization: Advanced analytics improve demand forecasting, inventory control, and distribution efficiency.

- Product Diversification & Premiumization: Growth of plant-based, organic, and specialty RTD formats supports higher-margin segments.

- Sustainable Packaging Transformation: Adoption of recyclable, biodegradable, and carbon-neutral packaging solutions aligns with ESG goals.

Strategic Implications

For RTD beverage companies, innovation is essential to maintaining competitiveness in a highly fragmented and dynamic market. Functional and premium product offerings enable higher margins and stronger brand loyalty. AI-enabled insights enhance operational efficiency, optimize product portfolios, and support targeted marketing strategies. Sustainability initiatives improve regulatory compliance and consumer trust. Companies that effectively integrate product innovation, digital intelligence, and sustainable practices will strengthen their market positioning and long-term growth potential.

Forward Outlook

The global RTD beverages market will continue to witness strong innovation momentum, driven by advancements in functional nutrition, personalized beverages, and digital supply chain integration. Future developments will focus on AI-powered product customization, next-generation plant-based formulations, circular packaging systems, and expanded DTC ecosystems. As consumer demand evolves toward convenience, health, and sustainability, innovation will remain a key driver of growth and differentiation in the post-2026 beverage landscape.

Market Risk

Risk Factors and Disruption Threats in the Global Ready-to-Drink (RTD) Beverages Market

Executive Framing

The Global Ready-to-Drink (RTD) Beverages Market is a highly diversified and large-scale segment within the global beverage industry, driven by convenience, functional innovation, and premiumization. With a projected CAGR of ~5.1% from 2026–2033, the market demonstrates stable growth; however, its complexity and broad product portfolio expose it to multiple structural and operational risks.

Current Market Reality

North America leads in consumption, while Asia-Pacific drives growth momentum. The market spans multiple categories including tea, coffee, energy drinks, dairy, plant-based beverages, and alcoholic RTDs, creating intense competition and pricing pressure. Additionally, rising regulatory scrutiny on sugar content, labeling, and sustainability standards is increasing compliance complexity across regions.

Key Signals and Evidence

Key signals include rapid growth in low-sugar and clean-label products, expansion of functional and plant-based beverages, and strong e-commerce penetration. However, increasing input costs (packaging, raw materials), supply chain volatility, and growing competition from both global giants and niche premium brands are key risk indicators. Shifting consumer preferences toward healthier and natural alternatives further accelerate reformulation pressures.

Strategic Implications

Companies must optimize product portfolios by focusing on high-growth segments such as RTD coffee, functional beverages, and plant-based drinks. Investment in sustainable packaging, AI-driven demand forecasting, and supply chain resilience will be critical. Additionally, brands need to continuously innovate in low-sugar, organic, and functional formulations to stay competitive while maintaining cost efficiency.The Global RTD Beverages Market is expected to maintain steady growth supported by convenience and functional demand. However, long-term success will depend on managing cost pressures, regulatory compliance, and intense competition across multiple beverage categories.

Regulatory Landscape

Regulatory & Policy Landscape: Global Ready-to-Drink (RTD) Beverages Market

Executive Framing

The Global RTD Beverages Market operates within a broad and multi-layered regulatory framework, as it spans multiple beverage categories including tea, coffee, functional drinks, dairy, plant-based beverages, and alcoholic RTDs. Regulatory oversight is driven by food safety laws, ingredient compliance, labeling standards, sugar regulations, and environmental policies.

Key regulatory bodies include the U.S. Food and Drug Administration (FDA), European Food Safety Authority (EFSA), Food Safety and Standards Authority of India (FSSAI), and various national food and beverage authorities. These organizations govern product formulation, permissible additives, nutritional labeling, health claims, and packaging compliance.

Current Market Reality

In North America, RTD beverages are regulated as conventional food and beverage products, with strict requirements on ingredient disclosure, nutritional labeling, and health claims. Increasing regulatory focus on sugar reduction and transparency is influencing product reformulation strategies.

Europe enforces stringent food safety and labeling regulations, including mandatory nutritional information, allergen disclosure, and restrictions on health claims. Sugar taxation policies in several countries are accelerating the shift toward low-calorie and sugar-free RTD formulations.

Asia-Pacific presents a highly diverse regulatory landscape, with country-specific standards for additives, preservatives, caffeine levels, and import/export compliance. Rapidly evolving policies around functional ingredients and plant-based beverages are shaping innovation and market entry strategies.

Additionally, alcoholic RTD beverages are subject to separate and stricter alcohol regulations, including licensing, taxation, age restrictions, and marketing controls, further increasing regulatory complexity across the category.

Key Signals and Evidence

- Strict food safety and ingredient approval regulations across beverage categories.

- Mandatory labeling requirements including nutrition facts, allergens, and ingredient transparency.

- Rising sugar taxes and government-led reformulation initiatives.

- Regulation of functional and health-related claims for fortified beverages.

- Separate regulatory frameworks for alcoholic RTD products.

- Growing environmental regulations related to sustainable and recyclable packaging.

Strategic Implications

Regulatory complexity directly impacts product development, market entry, and operational costs. Companies must tailor formulations and labeling strategies to meet region-specific compliance requirements, particularly for functional, plant-based, and fortified RTD beverages.

Sugar reduction policies and clean-label expectations are driving continuous innovation, while sustainability regulations are accelerating the transition toward recyclable, biodegradable, and low-carbon packaging solutions. Companies with strong compliance capabilities and flexible supply chains are better positioned to scale globally.

Forward Outlook

The regulatory landscape is expected to intensify, with stricter controls on sugar content, functional ingredient claims, and environmental sustainability. Governments may introduce broader sugar taxes, enhanced labeling requirements, and tighter regulations on marketing practices.

Functional beverages incorporating adaptogens, probiotics, and plant-based ingredients will require clearer regulatory definitions and scientific validation. Packaging regulations will increasingly focus on recyclability, waste reduction, and carbon footprint disclosure.

Companies that proactively invest in compliance systems, clean-label innovation, and sustainable packaging will gain a competitive advantage while ensuring long-term market access and consumer trust.