India Health and Wellness Food Market size and share Analysis 2026-2033

Key Drivers of India Health and Wellness Food Market Growth

Rising Health Awareness and Preventive Healthcare

Consumers are increasingly adopting healthy diets to prevent lifestyle diseases and maintain long-term wellness.

Increasing Urbanization and Disposable Income

Growing middle-class populations and urban lifestyles are supporting higher spending on premium health food products.

Expansion of E-commerce and Modern Retail

Online grocery platforms and modern retail stores are improving accessibility to health and wellness food products.

Growing Demand for Plant-Based and Organic Foods

Consumers are shifting toward natural, organic, and plant-based food products with clean-label ingredients.

Popularity of Traditional and Ayurvedic Ingredients

Indian superfoods and herbal ingredients such as turmeric, millets, moringa, and ashwagandha are driving innovation in functional nutrition products.

India Health and Wellness Food Market Segmentation

1. By Product Type

1.1 Functional and Fortified Foods

1.1.1 Vitamin-Enriched Foods

1.1.1.1 Fortified Cereals

1.1.1.1.1 Breakfast Cereals

1.1.1.1.2 Nutritional Snack Bars

1.1.2 Probiotic and Digestive Health Foods

1.1.2.1 Yogurt and Fermented Dairy

1.1.2.1.1 Probiotic Yogurt

1.1.2.1.2 Fermented Milk Drinks

1.2 Organic Foods

1.2.1 Organic Fruits and Vegetables

1.2.1.1 Fresh Organic Produce

1.2.1.1.1 Organic Vegetables

1.2.1.1.2 Organic Fruits

1.2.2 Organic Packaged Foods

1.2.2.1 Organic Snacks

1.2.2.1.1 Healthy Snack Products

1.2.2.1.2 Natural Ingredient Foods

1.3 Plant-Based Foods

1.3.1 Plant-Based Dairy Alternatives

1.3.1.1 Soy-Based Beverages

1.3.1.1.1 Soy Milk

1.3.1.1.2 Soy Yogurt

1.3.2 Plant-Based Protein Foods

1.3.2.1 Meat Alternatives

1.3.2.1.1 Soy Protein Products

1.3.2.1.2 Pea Protein Products

1.4 Low-Calorie and Diet Foods

1.4.1 Sugar-Free Foods

1.4.1.1 Low-Sugar Snacks

1.4.1.1.1 Diabetic-Friendly Foods

1.4.1.1.2 Reduced-Sugar Desserts

1.4.2 Low-Fat Foods

1.4.2.1 Healthy Dairy Products

1.4.2.1.1 Low-Fat Milk

1.4.2.1.2 Reduced-Fat Yogurt

2. By Distribution Channel

2.1 Supermarkets & Hypermarkets

2.1.1 Health Food Sections

2.1.1.1 Functional Food Shelves

2.1.1.1.1 Nutritional Food Products

2.1.1.1.2 Functional Beverage Products

2.1.2 Packaged Wellness Food Products

2.1.2.1 Health-Oriented Packaged Foods

2.1.2.1.1 Protein Snack Products

2.1.2.1.2 Organic Snack Products

2.2 Online Retail

2.2.1 E-commerce Grocery Platforms

2.2.1.1 Online Health Food Stores

2.2.1.1.1 Large E-commerce Platforms

2.2.1.1.2 Specialized Health Marketplaces

2.2.2 Direct-to-Consumer Health Food Brands

2.2.2.1 Brand-Owned E-commerce Stores

2.2.2.1.1 Nutrition Brands

2.2.2.1.2 Organic Product Brands

2.3 Specialty Health Stores

2.3.1 Organic Food Stores

2.3.1.1 Certified Organic Product Retailers

2.3.1.1.1 Organic Fruit Retailers

2.3.1.1.2 Organic Vegetable Retailers

2.3.2 Nutritional Supplement Retailers

2.3.2.1 Functional Nutrition Stores

2.3.2.1.1 Sports Nutrition Products

2.3.2.1.2 Functional Health Products

2.4 Traditional Retail

2.4.1 Local Grocery Stores

2.4.1.1 Neighborhood Convenience Stores

2.4.1.1.1 Packaged Wellness Foods

2.4.1.1.2 Healthy Snack Products

2.4.2 Independent Food Retailers

2.4.2.1 Specialty Food Shops

2.4.2.1.1 Local Organic Farmers

2.4.2.1.2 Health Food Vendors

India Health and Wellness Food Market Regional Insights

South India ??? Largest Market

South India leads the market due to higher health awareness, strong adoption of functional foods, and growing urban populations in cities such as Bengaluru, Chennai, and Hyderabad.

West India ??? Fastest Growing Region

West India is witnessing rapid growth driven by increasing disposable income, expanding retail infrastructure, and rising demand for organic and plant-based foods.

North India

North India shows strong demand for fortified foods, dietary supplements, and functional beverages across major metropolitan areas.

East India

East India is gradually expanding due to improving retail networks and increasing consumer awareness regarding nutritional food products.

Leading Companies in India Health and Wellness Food Market

Nestl?? India

ITC Limited

Amway India

Herbalife Nutrition

Dabur India

Hindustan Unilever Limited

Patanjali Ayurved

Tata Consumer Products

Strategic Intelligence & Market Insights

Pheonix Demand Forecast Engine identifies rising health awareness and plant-based nutrition adoption as key market drivers.

Consumer Behavior Analyzer highlights strong demand for clean-label, organic, and immunity-boosting food products.

Innovation Tracker focuses on functional beverages, Ayurvedic nutrition products, and plant-based protein foods.

Porter???s Five Forces Analysis indicates strong competition among wellness brands with growing opportunities in premium nutrition segments.

Why the India Health and Wellness Food Market Remains Critical

Supports preventive healthcare and balanced nutrition

Addresses rising lifestyle-related health conditions

Encourages innovation in organic and functional food industries

Strengthens India???s food processing and retail sectors

Promotes adoption of plant-based and clean-label nutrition products

Final Takeaway of India Health and Wellness Food Market

The India Health and Wellness Food Market is rapidly evolving into a nutrition-focused and preventive healthcare-driven food ecosystem.

With a projected CAGR of 10.3% during 2026???2033, the market is expected to witness strong expansion driven by health awareness, rising disposable incomes, and continuous innovation in functional nutrition products.

Companies focusing on organic food innovation, plant-based alternatives, Ayurvedic ingredient integration, and personalized nutrition solutions will be well positioned to capture long-term growth opportunities.

At Pheonix Research, our advanced forecasting models and market intelligence frameworks provide in-depth insights into consumer trends, product innovation, and regional demand patterns???empowering stakeholders to capitalize on emerging opportunities in the India health and wellness food market.

???? Social Mentions & Publication Channels

??Explore deeper insights and follow our cross-platform updates on??LinkedIn??and??X??for continuous intelligence and market coverage.

LinkedIn??: https://www.linkedin.com/in/pheonix-research-media/

X??: https://x.com/Pheonix_Insight

Table of Contents

1. Executive Summary

1.1 Market Forecast Snapshot (2026???2033)

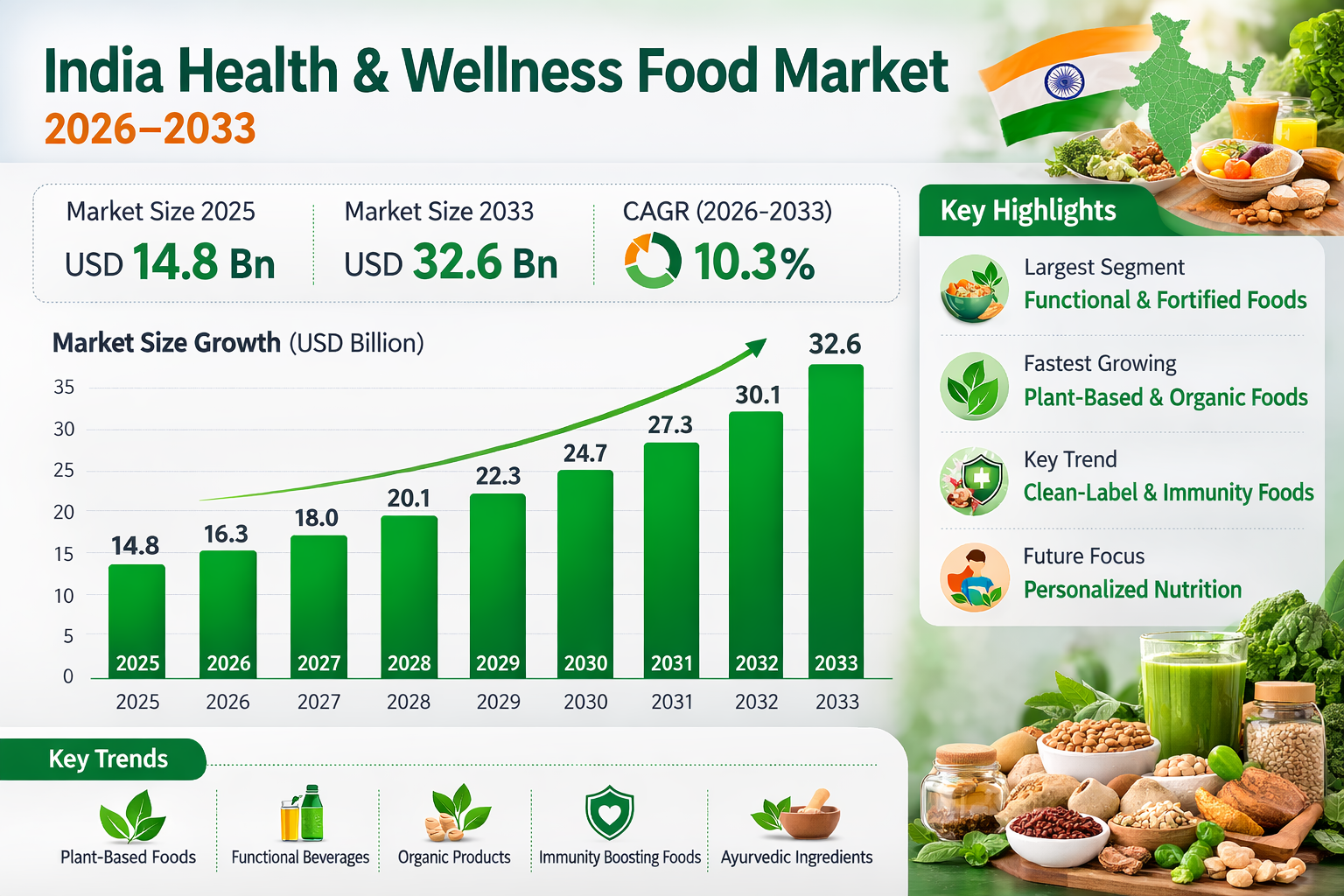

The India Health and Wellness Food Market is projected to grow from USD 14.8 Billion in 2025 to USD 32.6 Billion by 2033, registering a CAGR of 10.3% during 2026???2033.

1.2 Global Market Size & CAGR Analysis

The market reflects strong expansion driven by rising consumer awareness of preventive healthcare, increasing adoption of functional foods, and growing demand for plant-based and organic nutrition products.

1.3 Largest & Fastest-Growing Segments

Largest Segment: Functional & Fortified Foods

Fastest-Growing Segment: Plant-Based and Organic Foods

1.4 Region-Level Leadership & Growth Trends

South India currently leads the market due to strong adoption of functional foods and growing urban health awareness, while West India is projected to be the fastest-growing region through 2033.

1.5 Key Market Drivers

Rising consumer awareness regarding healthy diets and preventive healthcare

Increasing disposable income and urbanization across major cities

Expansion of e-commerce and modern grocery retail platforms

Growing demand for plant-based, organic, and clean-label food products

Popularity of traditional Ayurvedic ingredients and Indian superfoods

1.6 Competitive Landscape Overview

Moderately competitive landscape with major food companies and nutrition brands focusing on product innovation, herbal ingredient integration, and expansion of health-focused food portfolios.

1.7 Strategic Outlook Through 2033

Focus on plant-based food innovation, functional beverage development, expansion of organic food production, and personalized nutrition solutions tailored to health-conscious consumers.

2. Introduction & Market Overview

2.1 Definition of the India Health and Wellness Food Market

Covers functional foods, fortified foods, plant-based products, organic foods, low-calorie foods, and dietary nutrition products designed to improve overall health and wellness.

2.2 Scope of the Study

Comprehensive revenue analysis, product innovation trends, distribution channels, consumer behavior insights, and market forecasts for India???s health and wellness food industry during 2026???2033.

2.3 Evolution from Traditional Diets to Functional Nutrition

The market is evolving from traditional healthy foods toward scientifically formulated functional nutrition products enriched with vitamins, minerals, probiotics, and plant-based proteins.

2.4 Role of Modern Retail Infrastructure & Supply Optimization

Expansion of organized retail chains, supermarkets, specialty health stores, and online grocery platforms is improving accessibility to health-focused food products.

2.5 Impact of Health & Wellness Trends

Rising lifestyle diseases such as obesity, diabetes, and cardiovascular disorders are encouraging consumers to adopt healthier dietary habits.

2.6 Integration of Sustainable & Organic Farming Practices

Organic farming initiatives, eco-friendly agricultural methods, and sustainable ingredient sourcing are supporting the expansion of organic food products.

2.7 AI-Driven Food Innovation & Value-Added Nutrition Products

Food manufacturers are increasingly integrating AI-driven research, nutritional analytics, and personalized diet platforms to develop innovative wellness food products.

3. Research Methodology

3.1 Primary Research

Interviews with food manufacturers, nutrition experts, distributors, retailers, and healthcare professionals.

3.2 Secondary Research

Industry publications, government nutrition databases, trade reports, agricultural statistics, and corporate filings.

3.3 Market Size Estimation Model

Combination of bottom-up consumption analysis and top-down revenue modeling based on regional demand patterns.

3.4 Forecast Assumptions (2026???2033)

Based on rising health awareness, increasing disposable incomes, plant-based diet adoption, and expansion of retail infrastructure.

3.5 Data Validation & Triangulation

Cross-verification of market data using industry benchmarks, supply chain analytics, and regional consumption trends.

4. Market Dynamics

4.1 Drivers

4.1.1 Rising Health Awareness and Preventive Healthcare

Increasing consumer focus on healthier diets and long-term wellness.

4.1.2 Increasing Urbanization and Disposable Income

Urban lifestyles and growing middle-class populations supporting higher spending on premium health foods.

4.1.3 Expansion of E-commerce and Modern Retail

Digital grocery platforms and organized retail chains improving product accessibility.

4.1.4 Growing Demand for Plant-Based and Organic Foods

Consumers increasingly choosing natural and organic foods with clean-label ingredients.

4.1.5 Popularity of Traditional and Ayurvedic Ingredients

Turmeric, millets, moringa, and ashwagandha are widely used in functional nutrition products.

4.2 Restraints

4.2.1 Higher pricing of premium organic and functional foods

4.2.2 Limited awareness in rural and semi-urban markets

4.2.3 Regulatory compliance requirements for functional food labeling

4.2.4 Supply chain challenges for organic ingredients

4.3 Opportunities

4.3.1 Expansion of plant-based food innovations

4.3.2 Growth of functional beverages and wellness drinks

4.3.3 Rising demand for personalized nutrition solutions

4.3.4 Expansion of organic packaged food products

4.4 Challenges

4.4.1 Maintaining consistent quality of organic and natural ingredients

4.4.2 Competitive pricing in price-sensitive consumer segments

4.4.3 Managing large-scale supply chains for health foods

4.4.4 Competition from conventional packaged food products

5. India Health and Wellness Food Market Analysis (USD Billion), 2026???2033

5.1 Market Size Overview

5.2 CAGR Analysis

5.3 Region-Wise Revenue Distribution

5.4 Product Type Revenue Split

5.5 Distribution Channel Revenue Trends

5.6 Consumer Segment Impact Analysis

6. Market Segmentation by Product Type (USD Billion), 2026???2033

6.1 Functional and Fortified Foods

6.1.1 Vitamin-Enriched Foods

6.1.1.1 Fortified Cereals

6.1.1.1.1 Breakfast Cereals

6.1.1.1.2 Nutritional Snack Bars

6.1.2 Probiotic and Digestive Health Foods

6.1.2.1 Yogurt and Fermented Dairy

6.1.2.1.1 Probiotic Yogurt

6.1.2.1.2 Fermented Milk Drinks

6.2 Organic Foods

6.2.1 Organic Fruits and Vegetables

6.2.1.1 Fresh Organic Produce

6.2.1.1.1 Organic Vegetables

6.2.1.1.2 Organic Fruits

6.2.2 Organic Packaged Foods

6.2.2.1 Organic Snacks

6.2.2.1.1 Healthy Snack Products

6.2.2.1.2 Natural Ingredient Foods

6.3 Plant-Based Foods

6.3.1 Plant-Based Dairy Alternatives

6.3.1.1 Soy-Based Beverages

6.3.1.1.1 Soy Milk

6.3.1.1.2 Soy Yogurt

6.3.2 Plant-Based Protein Foods

6.3.2.1 Meat Alternatives

6.3.2.1.1 Soy Protein Products

6.3.2.1.2 Pea Protein Products

6.4 Low-Calorie and Diet Foods

6.4.1 Sugar-Free Foods

6.4.1.1 Low-Sugar Snacks

6.4.1.1.1 Diabetic-Friendly Foods

6.4.1.1.2 Reduced-Sugar Desserts

6.4.2 Low-Fat Foods

6.4.2.1 Healthy Dairy Products

6.4.2.1.1 Low-Fat Milk

6.4.2.1.2 Reduced-Fat Yogurt

7. Market Segmentation by Distribution Channel (USD Billion), 2026???2033

7.1 Supermarkets & Hypermarkets

7.1.1 Health Food Sections

7.1.1.1 Functional Food Shelves

7.1.1.1.1 Nutritional Food Products

7.1.1.1.2 Functional Beverage Products

7.1.2 Packaged Wellness Food Products

7.1.2.1 Health-Oriented Packaged Foods

7.1.2.1.1 Protein Snack Products

7.1.2.1.2 Organic Snack Products

7.2 Online Retail

7.2.1 E-commerce Grocery Platforms

7.2.1.1 Online Health Food Stores

7.2.1.1.1 Large E-commerce Platforms

7.2.1.1.2 Specialized Health Marketplaces

7.2.2 Direct-to-Consumer Health Food Brands

7.2.2.1 Brand-Owned E-commerce Stores

7.2.2.1.1 Nutrition Brands

7.2.2.1.2 Organic Product Brands

7.3 Specialty Health Stores

7.3.1 Organic Food Stores

7.3.1.1 Certified Organic Product Retailers

7.3.1.1.1 Organic Fruit Retailers

7.3.1.1.2 Organic Vegetable Retailers

7.3.2 Nutritional Supplement Retailers

7.3.2.1 Functional Nutrition Stores

7.3.2.1.1 Sports Nutrition Products

7.3.2.1.2 Functional Health Products

7.4 Traditional Retail

7.4.1 Local Grocery Stores

7.4.1.1 Neighborhood Convenience Stores

7.4.1.1.1 Packaged Wellness Foods

7.4.1.1.2 Healthy Snack Products

7.4.2 Independent Food Retailers

7.4.2.1 Specialty Food Shops

7.4.2.1.1 Local Organic Farmers

7.4.2.1.2 Health Food Vendors

8. Market Segmentation by Consumer Group (USD Billion), 2026???2033

8.1 Health-Conscious Consumers

8.1.1 Fitness Enthusiasts

8.1.1.1 Gym and Sports Nutrition Consumers

8.1.1.1.1 Protein Food Consumers

8.1.1.1.2 Energy Food Consumers

8.1.2 Lifestyle Diet Followers

8.1.2.1 Keto Diet Consumers

8.1.2.1.1 Low-Carb Food Products

8.1.2.1.2 High-Protein Diet Foods

8.2 Medical Nutrition Consumers

8.2.1 Diabetic Patients

8.2.1.1 Low-Glycemic Food Products

8.2.1.1.1 Sugar-Free Foods

8.2.1.1.2 Diabetic Diet Products

8.2.2 Weight Management Consumers

8.2.2.1 Low-Calorie Diet Consumers

8.2.2.1.1 Weight Loss Meal Products

8.2.2.1.2 Portion-Control Foods

8.3 Young Urban Consumers

8.3.1 Millennials

8.3.1.1 Health-Oriented Lifestyle Consumers

8.3.1.1.1 Organic Food Buyers

8.3.1.1.2 Plant-Based Food Consumers

8.3.2 Gen Z Consumers

8.3.2.1 Trend-Driven Health Food Buyers

8.3.2.1.1 Functional Beverage Consumers

8.3.2.1.2 Healthy Snack Consumers

9. Market Segmentation by Geography

9.1 South India ??? Largest Market

9.2 West India ??? Fastest Growing Market

9.3 North India

9.4 East India

10. Competitive Landscape ??? India

10.1 Market Share Analysis

10.2 Product Portfolio Benchmarking

10.3 Organic vs Conventional Product Mapping

10.4 Supply Chain & Retail Partnerships

10.5 Competitive Intensity & Differentiation Strategies

11. Company Profiles

11.1 Nestl?? India

11.2 ITC Limited

11.3 Amway India

11.4 Herbalife Nutrition

11.5 Dabur India

11.6 Hindustan Unilever Limited

11.7 Patanjali Ayurved

11.8 Tata Consumer Products

12. Strategic Intelligence & Pheonix AI-Backed Insights

12.1 Pheonix Demand Forecast Engine

12.2 Consumer Behavior Analyzer

12.3 AI-Driven Nutrition Innovation Tracker

12.4 Functional Food Product Innovation Insights

12.5 Automated Porter???s Five Forces Analysis

13. Future Outlook & Strategic Recommendations

13.1 Expansion of organic and plant-based food production

13.2 Growth of functional beverage categories

13.3 AI-driven personalized nutrition development

13.4 Expansion of e-commerce health food retail

13.5 Long-Term Market Outlook (2033+)

14. Appendix

15. About Pheonix Research

16. Disclaimer

Competitive Landscape

Competitive Landscape of the India Health & Wellness Food Market

Executive Framing

The India Health & Wellness Food Market is highly fragmented with intense competition among multinational corporations, domestic FMCG giants, and emerging health-focused startups. Key players such as Nestl?? India, ITC Limited, Hindustan Unilever Limited, Dabur India, Tata Consumer Products, Amway India, Herbalife Nutrition, and Patanjali Ayurved dominate the organized segment, while numerous regional and niche brands compete in organic, plant-based, and Ayurvedic product categories.

Current Market Reality

The market is characterized by rapid product innovation, strong regional diversity, and increasing penetration of health-focused products across urban and semi-urban areas. Functional and fortified foods dominate, while plant-based and organic foods are the fastest-growing segments.

Large FMCG companies leverage strong distribution networks and brand trust, whereas startups and D2C brands compete through clean-label positioning, premium offerings, and digital-first strategies. Traditional Indian ingredients such as turmeric, millets, and ashwagandha are widely integrated into modern functional food formulations, creating a unique competitive advantage for domestic players.

Key Signals and Evidence

- Strong growth in plant-based, organic, and clean-label food categories.

- Expansion of D2C health brands and online wellness marketplaces.

- High adoption of functional beverages and fortified food products.

- Integration of Ayurvedic and traditional ingredients into modern nutrition products.

- Increasing competition from regional and private-label health food brands.

Strategic Implications

- Localization Strategy: Leveraging traditional Indian ingredients and regional taste preferences.

- Product Innovation: Expanding plant-based, organic, and functional food portfolios.

- Digital Expansion: Strengthening D2C channels and e-commerce presence.

- Brand Positioning: Building trust through clean-label and natural product claims.

- Distribution Strength: Expanding reach across Tier II and Tier III cities.

Forward Outlook

By 2033, the India Health & Wellness Food Market is expected to reach approximately USD 32.6 billion, growing at a CAGR of ~10.3%. South India will continue to dominate due to higher awareness and consumption, while West India will emerge as a key growth engine.

The competitive landscape will further intensify with the rise of personalized nutrition, plant-based innovation, and functional beverages. Companies that successfully integrate Ayurveda with modern nutrition science, invest in digital distribution, and deliver affordable health solutions will gain a strong competitive edge in the evolving Indian wellness food ecosystem.

Value Chain

India Health and Wellness Food Market: Value Chain & Market Dynamics

Executive Framing

The India Health and Wellness Food Market is evolving into a nutrition-driven, consumer-centric, and innovation-led food ecosystem. Rising awareness around preventive healthcare, immunity, and balanced nutrition is accelerating product diversification, clean-label adoption, and digital retail expansion.

The operational model is integrated, where large FMCG players leverage scale, distribution, and brand strength, while emerging startups and D2C brands focus on organic, plant-based, and functional food innovation.

Current Market Reality

South India dominates the market due to higher health awareness and strong urban consumption, while West India is the fastest-growing region driven by rising disposable income and expanding retail infrastructure. Upstream supply includes agricultural raw materials, organic produce, and functional ingredients, midstream involves processing, fortification, packaging, and quality assurance, and downstream distribution spans modern retail, traditional stores, e-commerce platforms, and direct-to-consumer channels.

Key Signals and Evidence

- Market growth from USD 14.8 billion (2025) to USD 32.6 billion (2033) at a CAGR of 10.3%.

- Rising demand for functional, fortified, and immunity-boosting food products.

- Expansion of plant-based, organic, and clean-label food segments.

- Growth of e-commerce, health-focused retail chains, and D2C brands.

- Increasing adoption of Ayurvedic and traditional Indian superfood ingredients.

Strategic Implications

Companies must balance product innovation, affordability, and wide distribution reach. Established players focus on mass-market penetration and fortified product lines, while emerging brands can differentiate through premium organic products, plant-based alternatives, and niche wellness offerings.

Technology adoption, including AI-driven demand forecasting, personalized nutrition platforms, and digital marketing, will enhance consumer engagement and operational efficiency.

Sustainability is gaining importance, with focus on clean-label transparency, eco-friendly packaging, and responsible sourcing of raw materials.

Forward Outlook

The India Health and Wellness Food Market is expected to evolve into a technology-enabled, personalized, and preventive nutrition ecosystem. Key future trends include:

- Expansion of personalized and functional nutrition solutions

- Growth in plant-based, organic, and clean-label food products

- Rise of functional beverages and ready-to-consume wellness foods

- Integration of digital health platforms and subscription-based nutrition models

Companies aligning with consumer health trends, innovation, and omnichannel distribution strategies will capture long-term growth opportunities in the India health and wellness food market.

Investment Activity

Investment & Funding Dynamics ??? India Health and Wellness Food Market

Executive Framing

Current Market Reality

Valued at USD 14.8 billion in 2025 and projected to reach ~USD 32.6 billion by 2033 (CAGR ~10.3%), the market demonstrates strong and accelerating investment momentum. South India leads in investment activity due to higher health awareness and established urban consumption patterns, while West India is emerging as a key investment hub driven by expanding retail infrastructure and rising disposable income. Leading players such as Nestl?? India, ITC Limited, and Dabur India are investing in functional product development, supply chain expansion, and digital retail ecosystems.

Key Signals and Evidence

- Functional & Fortified Food Innovation: Strong investments in probiotic foods, fortified cereals, and functional beverages.

- Plant-Based & Organic Expansion: Increasing capital flows into plant-based proteins, dairy alternatives, and organic food segments.

- Ayurvedic & Traditional Ingredient Integration: Investments in turmeric, ashwagandha, millets, and herbal superfoods.

- E-Commerce & D2C Growth: Rapid expansion of online grocery platforms and direct-to-consumer wellness brands.

- Clean-Label Product Development: Rising focus on preservative-free, natural, and minimally processed food products.

- Supply Chain & Cold Storage Infrastructure: Investments in logistics, storage, and food processing capabilities.

- Startup & VC Activity: Increasing venture capital funding in health-focused food startups and nutrition brands.

Strategic Implications

Companies that integrate traditional nutrition knowledge with modern product innovation and strong digital distribution capabilities are best positioned for growth. Investors are prioritizing scalable brands with clean-label positioning, diversified product portfolios, and strong regional penetration. Strategic partnerships with e-commerce platforms, retail chains, and wellness ecosystems will be critical to expand market reach and enhance competitiveness.

Forward Outlook

From 2026 to 2033, investment in the India Health and Wellness Food Market is expected to accelerate significantly, particularly in plant-based innovation, functional beverages, and personalized nutrition solutions. Funding will increasingly focus on AI-driven consumer insights, sustainable sourcing, and premium health food product development. M&A activity and startup investments are likely to rise as companies aim to consolidate market share and expand across high-growth regions.

Technology & Innovation

India Health & Wellness Food Market: Technology & Innovation

Executive Framing

Technology and innovation in the India Health & Wellness Food Market are increasingly focused on integrating traditional nutrition systems with modern food science, enhancing product functionality, and expanding digital health ecosystems. Companies are leveraging AI-driven product development, functional ingredient innovation, and advanced food processing technologies to deliver clean-label, nutrient-dense, and personalized nutrition solutions.

Current Market Reality

With the market valued at USD 14.8 billion in 2025 and projected to reach USD 32.6 billion by 2033 at a CAGR of 10.3%, India is witnessing rapid innovation across functional foods, plant-based products, and digital nutrition platforms. South India leads in adoption due to higher health awareness, while West India is emerging as a fast-growing innovation hub driven by modern retail expansion and increasing consumer spending.

Key Signals and Evidence

- Integration of Ayurvedic & Functional Ingredients: Use of traditional ingredients such as turmeric, ashwagandha, moringa, and millets in modern functional food formulations.

- Plant-Based Food Innovation: Rapid development of plant-based dairy alternatives, protein-rich foods, and vegan nutrition products using advanced processing technologies.

- Clean-Label & Natural Formulations: Growing focus on preservative-free, minimally processed foods with transparent ingredient sourcing and labeling.

- AI-Driven Personalized Nutrition: Emergence of digital platforms offering customized diet plans, health tracking, and subscription-based nutrition solutions.

- Functional Beverage Development: Expansion of probiotic drinks, herbal beverages, fortified juices, and wellness shots targeting immunity and digestive health.

- Digital Retail & Supply Chain Innovation: Growth of e-commerce platforms, direct-to-consumer brands, and tech-enabled distribution networks improving accessibility across urban and semi-urban markets.

Strategic Implications

Companies investing in functional ingredient innovation, plant-based product development, and digital nutrition platforms will gain a strong competitive advantage in India???s evolving market. Leveraging traditional Indian superfoods with modern scientific validation can enhance product differentiation. Additionally, expanding e-commerce capabilities and clean-label positioning will be critical to capturing health-conscious consumers.

Forward Outlook

The market is expected to evolve toward AI-driven personalized nutrition ecosystems, increased adoption of plant-based and functional foods, and deeper integration of traditional Ayurvedic knowledge with modern food technology. Future innovation will focus on improving nutritional efficacy, scalability, and accessibility, positioning India as a key growth hub in the global health and wellness food industry.

Market Risk

Risk Factors and Disruption Threats in the India Health and Wellness Food Market

Executive Framing

The India Health and Wellness Food Market is experiencing rapid growth, driven by increasing consumer awareness of preventive healthcare, nutrition, and wellness-focused lifestyles. Valued at USD 14.8 billion in 2025 and projected to reach USD 32.6 billion by 2033 at a CAGR of 10.3%, the market reflects strong demand for functional, organic, and plant-based food products across urban and semi-urban populations.

Current Market Reality

South India dominates the market due to higher health awareness, strong urbanization, and widespread adoption of functional foods. West India is the fastest-growing region, supported by rising disposable incomes and expanding modern retail infrastructure. Functional and fortified foods lead the market, while plant-based and organic food segments are gaining rapid momentum among health-conscious consumers.

Key Signals and Evidence

- Rising consumer focus on immunity, preventive healthcare, and balanced nutrition.

- Growing demand for clean-label, organic, and plant-based food products.

- Increased adoption of traditional and Ayurvedic ingredients such as turmeric, millets, and ashwagandha.

- Rapid expansion of e-commerce, digital grocery platforms, and modern retail channels.

- Innovation in functional beverages, probiotic foods, and fortified nutrition products.

Strategic Implications

- Invest in plant-based, organic, and functional food product innovation.

- Leverage Ayurvedic and traditional ingredients for product differentiation.

- Expand digital and e-commerce distribution strategies to reach wider consumers.

- Focus on clean-label transparency and health-focused branding.

- Target emerging urban and semi-urban markets with rising health awareness.

Forward Outlook

The market is expected to evolve into a high-growth, innovation-driven ecosystem centered on preventive healthcare, personalized nutrition, and plant-based diets. Growth will be fueled by increasing consumer awareness, expanding middle-class populations, and continuous innovation in functional and clean-label food products, positioning India as a key market in the global health and wellness food industry.

Regulatory Landscape

Regulatory & Policy Landscape: India Health and Wellness Food Market

Executive Framing

The India Health and Wellness Food Market is governed by the Food Safety and Standards Authority of India (FSSAI), which regulates food safety, labeling, ingredient standards, and health claims. Products such as functional foods, organic foods, plant-based products, and fortified foods must comply with FSSAI regulations, including the Food Safety and Standards (Health Supplements, Nutraceuticals, and Functional Foods) Regulations.

Given the increasing demand for immunity-boosting, clean-label, and functional products, regulatory authorities are placing stronger emphasis on ingredient transparency, nutritional labeling, and substantiation of health claims.

Current Market Reality

The market operates under moderate to high regulatory complexity, particularly for functional and fortified food products making health-related claims. While traditional food products follow standard food safety norms, categories such as nutraceuticals, organic foods, and plant-based alternatives require additional certifications and approvals.

FSSAI has strengthened compliance requirements around fortification standards, organic certification (Jaivik Bharat), and labeling norms. The rapid growth of e-commerce and direct-to-consumer brands has also increased regulatory scrutiny on packaging, product claims, and interstate distribution compliance.

Key Signals and Evidence

- Mandatory FSSAI approval and licensing for all food products.

- Strict labeling requirements including nutritional information, ingredients, and allergen declarations.

- Regulations governing health claims for functional and fortified foods.

- Certification frameworks for organic (Jaivik Bharat) and clean-label products.

- Standards for food fortification (iron, iodine, vitamins) under national nutrition programs.

- Increased monitoring of online food sales and D2C health brands.

Strategic Implications

Companies must ensure full regulatory compliance with FSSAI standards to maintain market access and consumer trust. Investment in product validation, transparent labeling, and certification (organic, fortified, plant-based) is essential for brand differentiation.

Aligning product innovation???such as functional beverages, Ayurvedic nutrition, and plant-based foods???with regulatory frameworks will enable smoother market expansion. Companies leveraging compliant health claims and quality certifications can strengthen their competitive positioning.

Forward Outlook (2026???2033)

Regulatory frameworks in India are expected to become more stringent, particularly regarding clean-label transparency, sugar and fat disclosures, and health claim validation. Government initiatives promoting nutrition awareness and food fortification will further shape the market landscape.

Digital compliance systems, traceability technologies, and stricter monitoring of e-commerce channels will play a key role in ensuring product authenticity and safety. Companies proactively adapting to evolving regulations and sustainability standards will gain long-term advantages.Market Forecast Snapshot (2026???2033)