Global Ophthalmology Market Report, Size & Forecast 2026-2033

Global Ophthalmology Market Forecast Snapshot (2026???2033)

| Metric | Value |

|---|---|

| Market Size (2025) | ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ??USD 68.40 Billion |

| Market Size (2033) | ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ??USD 108.90 Billion |

| CAGR (2026???2033) | ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ??5.98% |

| Largest Segment | ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? Retinal Disorders Treatment |

| Fastest Growing Segment | ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ??Minimally Invasive Ophthalmic Surgery (MIOS) |

| Leading End-Use Segment | ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? ?? Hospitals & Ophthalmology Clinics |

| Key Trend | AI-Based Eye Diagnostics, Advanced Retinal Therapies & Minimally Invasive Surgical Technologies |

| Regulatory Influence | ?? ?? ?? ?? ?? ??Medical Device Regulations, Drug Approval Frameworks & Vision Care Standards |

| Future Outlook | Growth Driven by Aging Population, Rising Eye Disorders & Technological Advancements in Vision Care |

Global Ophthalmology Market

Global Ophthalmology Market Size & Forecast

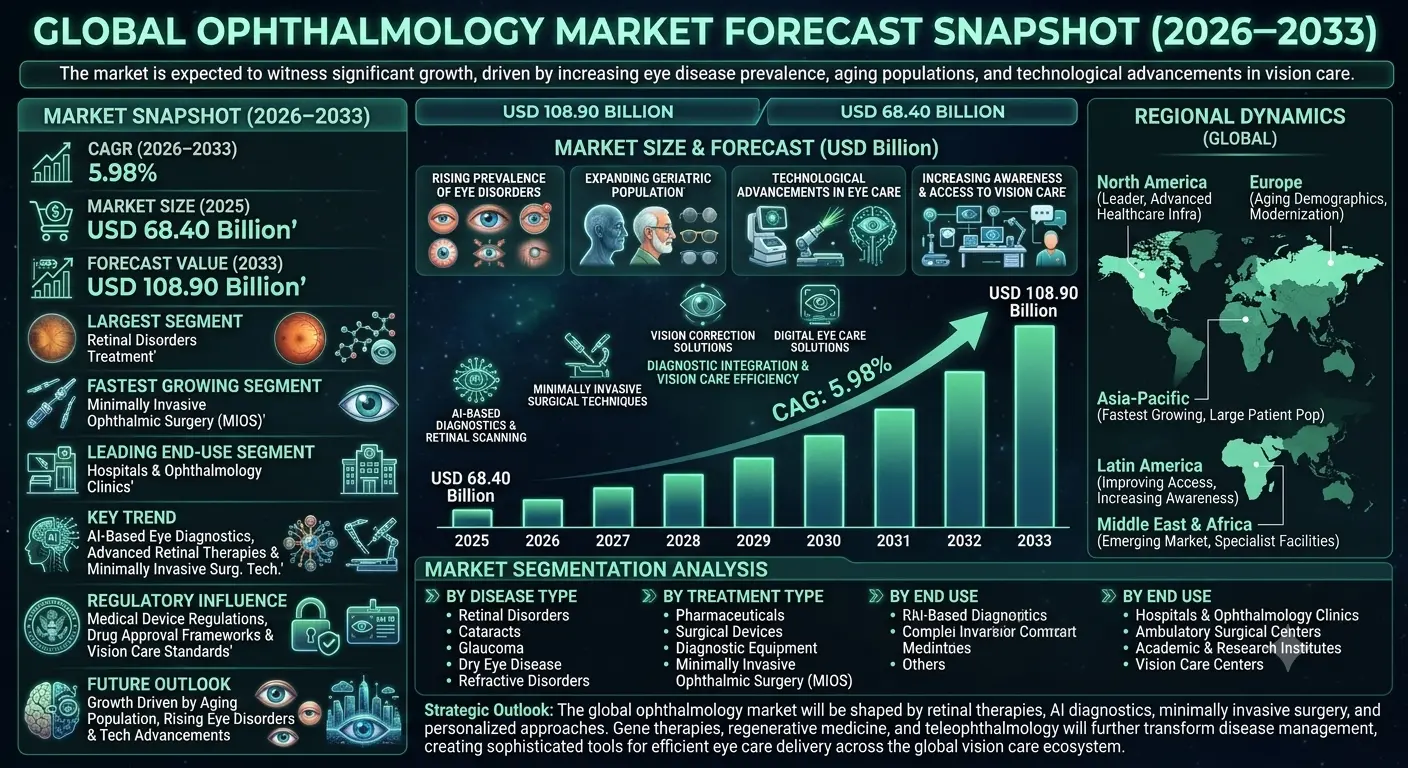

The Global Ophthalmology Market is expected to witness significant growth during the forecast period from 2026 to 2033. The market was valued at USD 68.40 billion in 2025 and is projected to reach approximately USD 108.90 billion by 2033, registering a CAGR of 5.98%. Market growth is primarily driven by the increasing prevalence of eye diseases, growing aging populations, rising incidence of diabetes-related vision disorders, and continuous advancements in ophthalmic diagnostics and treatment technologies. Increasing awareness regarding vision health and expanding access to specialized eye care services are further supporting market expansion.Global Ophthalmology Market Overview

Ophthalmology is a specialized branch of medicine focused on the diagnosis, treatment, and prevention of eye diseases and vision disorders. The market encompasses ophthalmic pharmaceuticals, surgical devices, diagnostic equipment, vision correction products, and specialized treatment procedures. Common conditions addressed within the market include cataracts, glaucoma, age-related macular degeneration (AMD), diabetic retinopathy, dry eye disease, and refractive disorders. Continuous innovation in retinal therapies, surgical techniques, and digital eye care solutions is transforming ophthalmic care globally.Structural Drivers of Market Growth

1. Rising Prevalence of Eye Disorders

The growing incidence of cataracts, glaucoma, diabetic retinopathy, and age-related macular degeneration is increasing demand for ophthalmic treatments. Market Implications: Healthcare providers and manufacturers are expanding diagnostic and treatment capabilities to address rising patient volumes.2. Expanding Geriatric Population

Aging populations worldwide are more susceptible to vision-related disorders and age-associated eye diseases. Market Implications: Demand for surgical procedures, retinal therapies, and vision correction solutions is expected to increase steadily.3. Technological Advancements in Eye Care

Innovations in imaging systems, laser technologies, AI-assisted diagnostics, and minimally invasive procedures are improving treatment outcomes. Market Implications: Technology-driven ophthalmology solutions are enhancing diagnostic accuracy and procedural efficiency.4. Increasing Awareness and Access to Vision Care

Growing public awareness and improved healthcare infrastructure are encouraging early diagnosis and treatment of eye conditions. Market Implications: Expanded access to ophthalmic services is supporting market penetration across both developed and emerging economies.Market Segmentation Analysis

By Disease Type

- Retinal Disorders Largest segment including age-related macular degeneration, diabetic retinopathy, and retinal vein occlusion treatments.

- Cataracts One of the most common vision disorders requiring surgical intervention and lens replacement procedures.

- Glaucoma Significant segment driven by increasing diagnosis rates and long-term treatment requirements.

- Dry Eye Disease Growing prevalence due to aging populations and increased screen exposure.

- Refractive Disorders Includes myopia, hyperopia, astigmatism, and presbyopia management solutions.

By Treatment Type

- Pharmaceuticals Includes anti-VEGF therapies, glaucoma medications, anti-inflammatory drugs, and dry eye treatments.

- Ophthalmic Surgical Devices Used in cataract surgeries, retinal procedures, glaucoma management, and refractive surgeries.

- Diagnostic Equipment Includes OCT systems, fundus cameras, visual field analyzers, and AI-powered diagnostic tools.

- Minimally Invasive Ophthalmic Surgery (MIOS) Fastest-growing segment driven by improved patient outcomes and shorter recovery periods.

By End Use

- Hospitals & Ophthalmology Clinics Largest segment due to high patient volumes and comprehensive treatment capabilities.

- Ambulatory Surgical Centers Growing adoption for cataract surgeries and outpatient ophthalmic procedures.

- Academic & Research Institutes Focused on innovation, clinical studies, and ophthalmic technology development.

- Vision Care Centers Provide routine eye examinations, vision correction services, and preventive care.

Regional Market Dynamics

North America

Leading region due to advanced healthcare infrastructure, high adoption of innovative ophthalmic technologies, and strong reimbursement systems.Europe

Driven by aging demographics, increasing investments in healthcare modernization, and widespread access to specialized eye care services.Asia-Pacific

Fastest-growing region supported by large patient populations, rising healthcare expenditure, and expanding ophthalmic care infrastructure.Latin America

Growing market driven by improving access to vision care services and increasing awareness regarding eye health.Middle East & Africa

Emerging market supported by healthcare infrastructure development, expanding specialist care facilities, and growing investments in ophthalmology services.Competitive Landscape

The Global Ophthalmology Market is highly competitive with the presence of pharmaceutical companies, medical device manufacturers, diagnostic equipment providers, and specialized eye care organizations. Market participants focus on product innovation, clinical advancements, strategic partnerships, and geographic expansion. Key Companies Operating in the Market Include:- Alcon Inc.

- Johnson & Johnson Vision

- Bausch + Lomb Corporation

- Carl Zeiss Meditec AG

- Topcon Corporation

- Novartis AG

- Roche Holding AG

- AbbVie Inc.

- NIDEK Co., Ltd.

- EssilorLuxottica S.A.

Strategic Outlook

The future of the ophthalmology market will be shaped by innovations in retinal therapies, artificial intelligence-based diagnostics, minimally invasive surgical procedures, and personalized treatment approaches. Advancements in gene therapies, regenerative medicine, and digital eye care platforms are expected to transform disease management and patient outcomes. Increasing adoption of teleophthalmology and remote diagnostic solutions will further improve access to specialized vision care services. Growing investments in research and development, coupled with expanding healthcare infrastructure in emerging markets, are expected to create substantial growth opportunities. Organizations that prioritize innovation, patient-centric care, and advanced treatment technologies will be well-positioned to benefit from the evolving ophthalmology landscape.Final Market Perspective

The Global Ophthalmology Market plays a vital role in addressing the growing burden of vision impairment and eye diseases worldwide. Rising prevalence of ophthalmic disorders, technological advancements in diagnostics and treatment, and increasing awareness regarding eye health are driving sustained market growth. As healthcare systems continue to emphasize preventive care and advanced therapeutic solutions, companies offering innovative, effective, and accessible ophthalmology products and services will be well-positioned to capitalize on long-term opportunities in the global vision care ecosystem.Table of Contents

Table of Contents

- Executive Summary

- Global Ophthalmology Market Snapshot (2026???2033)

- Market Size & Growth Overview

- Key Market Highlights

- Largest & Fastest-Growing Segments

- Leading End-Use Segment Overview

- Key Market Trends in Vision Care and Eye Health

- Strategic Outlook Through 2033

- Market Introduction & Overview

- Definition of Ophthalmology

- Scope of the Global Ophthalmology Market

- Evolution of Ophthalmic Diagnostics and Treatment Technologies

- Role of Ophthalmology in Vision Preservation and Eye Care

- Value Chain Analysis of the Ophthalmology Ecosystem

- Regulatory Influence (Medical Device Regulations, Drug Approval Frameworks & Vision Care Standards)

- Transition Toward AI-Based Diagnostics, Advanced Retinal Therapies & Minimally Invasive Surgical Technologies

- Research Methodology

- Primary Research Approach

- Secondary Research Sources

- Market Size Estimation Methodology

- Forecasting Assumptions (2026???2033)

- Data Validation & Triangulation Process

- Market Dynamics

- Structural Drivers of Market Growth

- Rising Prevalence of Eye Disorders

- Expanding Geriatric Population

- Technological Advancements in Eye Care

- Increasing Awareness and Access to Vision Care

- Market Restraints

- High Cost of Advanced Ophthalmic Treatments

- Limited Access to Specialized Eye Care in Developing Regions

- Regulatory and Reimbursement Challenges

- Market Opportunities

- Expansion of AI-Powered Eye Diagnostics

- Growth of Teleophthalmology Services

- Advancements in Gene and Regenerative Therapies

- Increasing Adoption of Minimally Invasive Ophthalmic Surgery (MIOS)

- Market Challenges

- Shortage of Skilled Ophthalmologists in Certain Regions

- Management of Chronic Eye Diseases

- Rising Burden of Diabetes-Related Vision Disorders

- Structural Drivers of Market Growth

- Global Ophthalmology Market Size & Forecast (2026???2033)

- Market Revenue Analysis

- CAGR Analysis

- Ophthalmic Disease Prevalence Trends

- Treatment and Surgical Procedure Analysis

- Investment Trends

- Future Market Outlook

- Market Segmentation Analysis (2026???2033)

- By Disease Type

- Retinal Disorders (Largest Segment)

- Cataracts

- Glaucoma

- Dry Eye Disease

- Refractive Disorders

- By Treatment Type

- Pharmaceuticals

- Ophthalmic Surgical Devices

- Diagnostic Equipment

- Minimally Invasive Ophthalmic Surgery (MIOS) (Fastest-Growing Segment)

- By End Use

- Hospitals & Ophthalmology Clinics (Largest Segment)

- Ambulatory Surgical Centers

- Academic & Research Institutes

- Vision Care Centers

- By Disease Type

- Regional Market Analysis

- North America (Largest Regional Market)

- Europe

- Asia-Pacific (Fastest-Growing Regional Market)

- Latin America

- Middle East & Africa

- Competitive Landscape

- Market Structure & Competitive Analysis

- Key Player Benchmarking

- Strategic Developments

- AI Diagnostics and Advanced Therapeutics Strategies

- Partnerships, Acquisitions & Product Innovation Initiatives

- Company Profiles

- Alcon Inc.

- Johnson & Johnson Vision

- Bausch + Lomb Corporation

- Carl Zeiss Meditec AG

- Topcon Corporation

- Novartis AG

- Roche Holding AG

- AbbVie Inc.

- NIDEK Co., Ltd.

- EssilorLuxottica S.A.

- Strategic Outlook

- Future of AI-Based Ophthalmic Diagnostics

- Expansion of Advanced Retinal and Gene Therapies

- Growth of Minimally Invasive Ophthalmic Procedures

- Integration of Digital Eye Care and Teleophthalmology Platforms

- Long-Term Market Outlook (2033+)

- Final Market Perspective

- Appendix

- About Pheonix Market Research

- Disclaimer

Competitive Landscape

Global Ophthalmology Market Competitive Intensity & Market Structure Overview

The Global Ophthalmology Market is highly competitive and innovation-driven, characterized by the presence of multinational pharmaceutical companies, ophthalmic device manufacturers, diagnostic technology providers, vision care companies, and specialized healthcare organizations. Competitive intensity is driven by technological innovation, clinical efficacy, regulatory approvals, product portfolio breadth, physician adoption, and global distribution capabilities.

Companies compete across multiple market segments including retinal disease treatments, glaucoma therapies, cataract surgery devices, ophthalmic diagnostics, vision correction solutions, dry eye disease management, and minimally invasive ophthalmic surgical technologies. Continuous advancements in eye care technologies and increasing demand for specialized ophthalmic treatments are intensifying competition across the industry.

The market structure is evolving toward technology-enabled, patient-centric, and precision medicine-focused business models. Manufacturers are increasingly investing in artificial intelligence-based diagnostics, advanced imaging systems, gene therapies, digital eye care platforms, and next-generation surgical solutions to strengthen market positioning and capture emerging growth opportunities.

Global Ophthalmology Market Competitive Intensity & Market Structure Current Scenario

Leading Global Ophthalmology Companies

- Alcon Inc.: A global leader in eye care products, offering ophthalmic surgical equipment, vision care solutions, intraocular lenses, and contact lens products.

- Johnson & Johnson Vision: Provides a broad portfolio of contact lenses, ophthalmic surgical technologies, and vision correction solutions for eye care professionals and patients.

- Bausch + Lomb Corporation: A major ophthalmology company specializing in eye health products, contact lenses, pharmaceuticals, and surgical devices.

- Carl Zeiss Meditec AG: A leading provider of ophthalmic diagnostic systems, surgical microscopes, imaging technologies, and laser-based treatment solutions.

- Topcon Corporation: Specializes in ophthalmic diagnostic equipment, retinal imaging systems, and digital healthcare technologies for eye care professionals.

- Novartis AG: A prominent pharmaceutical company with a strong ophthalmology portfolio focused on retinal disease therapies and innovative eye care treatments.

- Roche Holding AG: Actively involved in ophthalmic therapeutics, particularly retinal disease treatments and advanced biologic therapies.

- AbbVie Inc.: Expanding its ophthalmology presence through innovative pharmaceutical products targeting retinal disorders and vision-related diseases.

- NIDEK Co., Ltd.: A recognized manufacturer of ophthalmic diagnostic instruments, refractive surgery systems, and eye examination equipment.

- EssilorLuxottica S.A.: A global leader in vision care, eyewear, ophthalmic lenses, and vision correction solutions serving consumers worldwide.

Key Competitive Intensity & Market Structure Drivers

The increasing prevalence of retinal diseases, glaucoma, cataracts, and diabetic eye disorders is intensifying competition as companies expand treatment portfolios and improve clinical outcomes.

Rapid advancements in artificial intelligence, optical coherence tomography (OCT), digital diagnostics, and imaging technologies are driving innovation and product differentiation across the market.

Growing demand for minimally invasive ophthalmic procedures is encouraging manufacturers to develop advanced surgical systems that improve precision, safety, and recovery times.

Stringent regulatory requirements and clinical validation standards are increasing the importance of research capabilities, regulatory expertise, and product quality assurance.

Expanding access to vision care services in emerging markets is creating new growth opportunities while encouraging global companies to strengthen regional presence and distribution networks.

Strategic Implications of Competitive Intensity & Market Structure

Companies with strong research and development capabilities, extensive clinical data, and diversified ophthalmology portfolios are expected to maintain significant competitive advantages.

Investment in AI-powered diagnostics, advanced retinal therapies, minimally invasive surgical technologies, and digital eye care platforms is becoming increasingly important for market differentiation.

Strategic collaborations between pharmaceutical companies, medical device manufacturers, healthcare providers, and research institutions are accelerating innovation and commercialization efforts.

Manufacturers focusing on patient outcomes, treatment accessibility, physician training, and integrated care solutions are likely to strengthen customer loyalty and market share.

Organizations capable of combining technological innovation, clinical effectiveness, regulatory compliance, and global market reach will be best positioned to compete effectively in the evolving ophthalmology industry.

Global Ophthalmology Market Competitive Intensity & Market Structure Forward Outlook

The competitive landscape of the global ophthalmology market is expected to become increasingly technology-driven, precision-focused, and innovation-oriented as healthcare providers seek more effective vision care solutions.

Future competition will be shaped by advancements in gene therapies, regenerative medicine, AI-assisted diagnostics, teleophthalmology platforms, and personalized treatment approaches.

Market participants are expected to increase investments in clinical research, digital healthcare integration, next-generation surgical technologies, and advanced retinal disease management solutions to strengthen competitive positioning.

Over the forecast period, companies that successfully balance innovation, clinical excellence, patient accessibility, technological advancement, and regulatory compliance will be best positioned to lead the evolving global ophthalmology market.

Value Chain

Global Ophthalmology Market Value Chain & Supply Chain Evolution Overview

The Global Ophthalmology Market operates through a highly specialized value chain encompassing research & development, raw material and component sourcing, pharmaceutical and device manufacturing, regulatory approvals, distribution, healthcare delivery, and patient care. The market includes ophthalmic pharmaceuticals, surgical devices, diagnostic equipment, vision correction products, and advanced treatment solutions addressing a wide range of eye disorders.

The industry is being transformed by advancements in retinal therapies, AI-powered diagnostics, minimally invasive ophthalmic surgery, gene therapies, and digital eye care technologies. Growing prevalence of age-related eye diseases, increasing healthcare investments, and rising awareness of vision health continue to drive innovation across the value chain.

Manufacturers are increasingly focusing on precision medicine, digital diagnostics, integrated treatment platforms, and global expansion strategies to improve patient outcomes and strengthen market competitiveness. Strategic collaborations among pharmaceutical companies, medical device manufacturers, healthcare providers, and research institutions are further accelerating innovation.

Advancements in teleophthalmology, automated imaging systems, cloud-based diagnostic platforms, and personalized treatment approaches are reshaping supply chain operations and enhancing access to ophthalmic care worldwide.

Global Ophthalmology Market Value Chain & Supply Chain Evolution Current Scenario

Market-Specific Value Chain

- Research & Drug Discovery: Development of ophthalmic drugs, biologics, retinal therapies, gene therapies, and vision care technologies.

- Raw Material & Component Sourcing: Procurement of active pharmaceutical ingredients (APIs), medical-grade polymers, lenses, optical components, sensors, imaging modules, and surgical materials.

- Manufacturing & Production: Production of ophthalmic pharmaceuticals, surgical devices, diagnostic systems, intraocular lenses, and vision correction products.

- Regulatory Approval & Quality Assurance: Clinical trials, product validation, regulatory compliance, and quality control activities.

- Distribution & Logistics: Global distribution of ophthalmic medicines, devices, diagnostic equipment, and healthcare supplies through specialized medical supply networks.

- Healthcare Delivery & Clinical Services: Deployment of ophthalmic products and services through hospitals, ophthalmology clinics, ambulatory surgical centers, and vision care centers.

- Patient Care & Vision Management: Diagnosis, treatment, surgical intervention, vision correction, and long-term disease management for patients.

Company-to-Stage Mapping

- Research & Drug Discovery: Novartis AG, Roche Holding AG, AbbVie Inc., academic research institutions, and ophthalmic innovation centers.

- Raw Material & Component Sourcing: API suppliers, optical component manufacturers, lens material providers, semiconductor suppliers, and medical-grade material manufacturers.

- Manufacturing & Production: Alcon Inc., Johnson & Johnson Vision, Bausch + Lomb Corporation, Carl Zeiss Meditec AG, Topcon Corporation, and NIDEK Co., Ltd.

- Regulatory Approval & Quality Assurance: Regulatory agencies, clinical research organizations (CROs), quality assurance providers, and certification bodies.

- Distribution & Logistics: Medical distributors, healthcare logistics providers, pharmaceutical wholesalers, and specialized healthcare supply chain companies.

- Healthcare Delivery & Clinical Services: Hospitals, ophthalmology clinics, ambulatory surgical centers, vision care centers, and teleophthalmology service providers.

- Patient Care & Vision Management: Ophthalmologists, optometrists, eye surgeons, healthcare professionals, and patients.

Key Value Chain & Supply Chain Evolution Signals in Global Ophthalmology Market

Growing Adoption of AI-Based Eye Diagnostics

Artificial intelligence is improving early disease detection, diagnostic accuracy, workflow efficiency, and clinical decision-making in ophthalmology.

Expansion of Advanced Retinal Therapies

Innovative biologics, anti-VEGF treatments, gene therapies, and regenerative medicine approaches are transforming retinal disease management.

Increasing Demand for Minimally Invasive Ophthalmic Surgery

Healthcare providers are increasingly adopting minimally invasive surgical techniques to improve patient outcomes and reduce recovery times.

Growth of Teleophthalmology and Remote Eye Care

Digital healthcare platforms are expanding access to vision care services, particularly in underserved and remote regions.

Rising Integration of Digital Imaging Technologies

Advanced imaging systems such as OCT, fundus cameras, and cloud-connected diagnostic platforms are enhancing disease monitoring capabilities.

Focus on Personalized and Precision Eye Care

Manufacturers and healthcare providers are developing individualized treatment strategies based on patient-specific disease profiles and clinical data.

Strategic Implications of Value Chain & Supply Chain Evolution

Investment in Next-Generation Ophthalmic Technologies

Companies developing advanced diagnostics, retinal therapies, and surgical innovations can strengthen market leadership and clinical outcomes.

Expansion of Digital Eye Care Ecosystems

Integration of AI, telemedicine, and cloud-based diagnostic platforms can improve accessibility, efficiency, and patient engagement.

Strengthening Regulatory Compliance Capabilities

Robust quality systems and regulatory expertise are essential for successful commercialization of ophthalmic products globally.

Enhancement of Clinical Partnerships

Collaboration with healthcare providers and research institutions can accelerate innovation and support product adoption.

Optimization of Specialized Healthcare Supply Chains

Efficient distribution networks can ensure timely availability of ophthalmic medicines, devices, and diagnostic equipment.

Focus on Emerging Market Expansion

Growing healthcare infrastructure and rising awareness of eye health in emerging economies are creating significant growth opportunities.

Global Ophthalmology Market Value Chain & Supply Chain Evolution Forward Outlook

Looking ahead, the ophthalmology value chain is expected to become increasingly technology-driven, patient-centric, and digitally integrated. Advances in AI diagnostics, personalized therapies, minimally invasive surgical techniques, and remote care platforms will continue transforming vision care delivery worldwide.

Key Future Developments Include:

- Expansion of AI-powered diagnostic and screening platforms.

- Increased adoption of gene therapies and regenerative ophthalmic treatments.

- Growth of minimally invasive ophthalmic surgical technologies.

- Wider implementation of teleophthalmology and remote monitoring solutions.

- Greater integration of cloud-based imaging and patient management systems.

- Rising investment in precision medicine and personalized vision care approaches.

As the market evolves, competitive advantage will increasingly depend on technological innovation, clinical effectiveness, regulatory expertise, digital healthcare integration, and patient-centered treatment strategies.

Companies that successfully integrate advanced diagnostics, innovative therapies, digital care solutions, and efficient healthcare delivery models will be well-positioned to achieve long-term growth in the Global Ophthalmology Market.

Investment Activity

Global Ophthalmology Market Investment & Funding Dynamics Overview (2026???2033)

The Global Ophthalmology Market is witnessing strong investment activity driven by the rising prevalence of eye disorders, growing aging populations, increasing healthcare expenditure, and rapid advancements in ophthalmic diagnostics, therapeutics, and surgical technologies. Pharmaceutical companies, medical device manufacturers, healthcare investors, venture capital firms, private equity groups, and research institutions are actively investing in retinal therapies, AI-powered diagnostic platforms, minimally invasive ophthalmic surgery technologies, advanced imaging systems, and next-generation vision care solutions.

Investment momentum is accelerating as healthcare providers and technology developers seek to address the growing global burden of vision impairment and chronic eye diseases. Capital allocation is increasingly focused on innovative drug development, ophthalmic device innovation, digital eye care platforms, precision diagnostics, and expansion of specialized eye care infrastructure.

Additionally, increasing investments in gene therapies, regenerative medicine, teleophthalmology platforms, artificial intelligence-driven screening systems, and advanced retinal treatment technologies are creating significant long-term opportunities across the global ophthalmology ecosystem.

Current Investment & Funding Landscape

The current market environment reflects growing investor confidence in vision care technologies, ophthalmic pharmaceuticals, and advanced medical devices. Industry participants are investing heavily in clinical research programs, ophthalmic surgical equipment, diagnostic imaging technologies, and expansion of specialized eye care services.

Significant funding is being directed toward AI-based diagnostic solutions, retinal disease treatment development, minimally invasive surgical platforms, telemedicine integration, and digital patient management systems to improve treatment outcomes and healthcare accessibility.

Strategic collaborations among pharmaceutical companies, medical device manufacturers, healthcare providers, research institutes, and technology firms are accelerating innovation and shaping investment flows throughout the ophthalmology value chain.

Key Investment & Funding Dynamics Signals

- Growing prevalence of retinal disorders, glaucoma, cataracts, and diabetic retinopathy is driving investment across ophthalmic treatment and diagnostic segments.

- Increasing adoption of AI-powered eye diagnostics and imaging technologies is attracting substantial technology-focused funding.

- Rising demand for minimally invasive ophthalmic surgery solutions is encouraging investments in advanced surgical devices and treatment platforms.

- Expansion of teleophthalmology and remote vision care services is creating new opportunities for digital healthcare investments.

- Growing focus on gene therapies, biologics, and regenerative ophthalmology treatments is supporting high-value research and development funding.

- Increasing healthcare infrastructure development across emerging markets is strengthening investment in specialized eye care facilities.

- Strategic investments in personalized vision care, smart diagnostic systems, and patient-centric treatment models are enhancing long-term growth opportunities.

Strategic Implications of Investment & Funding Dynamics

- Continuous investment in advanced diagnostics, ophthalmic pharmaceuticals, and surgical innovation is essential for maintaining competitive differentiation.

- Capital allocation toward AI integration, digital health platforms, and data-driven ophthalmology solutions will improve patient outcomes and operational efficiency.

- Companies developing next-generation retinal therapies, minimally invasive procedures, and precision treatment approaches are expected to attract strong investor interest.

- Strategic partnerships between healthcare providers, technology companies, research institutions, and medical device manufacturers will accelerate commercialization and market expansion.

- Investments in clinical trials, regulatory approvals, and advanced manufacturing capabilities will strengthen product pipelines and market access.

- Compliance with medical device regulations, drug approval frameworks, and patient safety standards will remain a critical factor influencing investment decisions.

- Organizations building integrated capabilities across diagnostics, therapeutics, digital healthcare, and specialized vision care services are expected to capture substantial long-term value.

Forward Outlook

Looking ahead, the Global Ophthalmology Market is expected to maintain strong investment momentum driven by increasing demand for vision care services, technological innovation, and expanding treatment options for chronic eye diseases.

Future capital deployment will increasingly focus on AI-enabled diagnostics, advanced retinal therapies, minimally invasive surgical technologies, teleophthalmology platforms, and personalized ophthalmic treatment solutions.

As healthcare systems continue prioritizing early diagnosis, preventive eye care, and improved patient outcomes, investment activity is expected to expand across ophthalmic pharmaceuticals, medical devices, digital health infrastructure, and specialized eye care networks.

In conclusion, the Global Ophthalmology Market represents an attractive healthcare investment landscape where clinical innovation, digital transformation, advanced therapeutics, precision diagnostics, and patient-centric vision care will define future funding priorities, competitive differentiation, and long-term market expansion.

Technology & Innovation

Global Ophthalmology Market Technology & Innovation Landscape Overview

The Global Ophthalmology Market is undergoing rapid technological advancement as healthcare providers and industry participants focus on improving diagnostic accuracy, treatment effectiveness, surgical precision, and patient outcomes. Innovations in artificial intelligence, retinal imaging technologies, minimally invasive surgical systems, gene therapies, and digital eye care solutions are transforming the ophthalmology landscape. Companies are making substantial investments in research and development to introduce advanced ophthalmic devices, next-generation therapeutics, and intelligent diagnostic platforms capable of supporting early disease detection and personalized treatment strategies. As the prevalence of vision disorders continues to increase globally, technology-driven innovation is becoming a critical factor in enhancing eye care delivery and clinical efficiency.

The market is also benefiting from advancements in optical coherence tomography (OCT), robotic-assisted surgical technologies, teleophthalmology platforms, cloud-based patient management systems, and AI-powered diagnostic tools. These innovations are enabling ophthalmologists to improve disease monitoring, optimize treatment planning, reduce procedural risks, and expand access to specialized eye care services. Growing demand for precision medicine and advanced vision care solutions is further accelerating technological adoption across the global ophthalmology industry.

Global Ophthalmology Market Technology & Innovation Current Scenario

Current innovation within the Global Ophthalmology Market is primarily focused on AI-assisted diagnostics, advanced retinal therapies, minimally invasive ophthalmic surgeries, and digital patient management solutions. Healthcare providers are increasingly utilizing artificial intelligence algorithms to analyze retinal images, detect eye diseases at earlier stages, and improve clinical decision-making. Advances in retinal imaging technologies and diagnostic equipment are enhancing the accuracy and speed of disease identification for conditions such as diabetic retinopathy, glaucoma, and age-related macular degeneration.

Technological progress is also reshaping ophthalmic treatment procedures through the adoption of minimally invasive surgical systems, premium intraocular lenses, laser-assisted interventions, and regenerative medicine approaches. In addition, teleophthalmology platforms and connected healthcare solutions are helping improve patient accessibility, facilitate remote consultations, and support continuous monitoring of chronic eye conditions. These developments are contributing to better patient outcomes while increasing operational efficiency across ophthalmology practices and healthcare institutions.

Key Technology & Innovation Trends in Global Ophthalmology Market

- AI-Based Eye Diagnostics: Improving early disease detection, image analysis accuracy, and clinical decision support.

- Advanced Retinal Imaging Technologies: Enhancing visualization and diagnosis of retinal disorders through high-resolution imaging systems.

- Minimally Invasive Ophthalmic Surgery (MIOS): Supporting faster recovery, reduced complications, and improved surgical outcomes.

- Optical Coherence Tomography (OCT) Innovations: Providing detailed retinal and optic nerve imaging for disease monitoring and treatment planning.

- Gene and Cell-Based Therapies: Advancing treatment options for inherited retinal diseases and degenerative eye conditions.

- Laser-Assisted Surgical Technologies: Improving precision and efficiency in cataract, glaucoma, and refractive surgeries.

- Teleophthalmology Platforms: Expanding access to vision care services through remote consultation and digital diagnostics.

- Smart Intraocular Lens Technologies: Enhancing vision correction outcomes through advanced lens designs and customization.

- Cloud-Based Eye Care Management Systems: Supporting patient data integration, workflow optimization, and clinical collaboration.

- Digital Vision Monitoring Solutions: Enabling continuous disease tracking and proactive management of chronic ophthalmic conditions.

Strategic Implications of Technology & Innovation

Technological advancements are enabling ophthalmology companies and healthcare providers to improve diagnostic capabilities, enhance treatment precision, and deliver more personalized patient care. Organizations investing in artificial intelligence, advanced imaging systems, innovative therapeutics, and minimally invasive surgical technologies are strengthening their competitive positions while improving clinical outcomes. Innovation is helping industry participants address the growing burden of vision disorders through more effective and accessible eye care solutions.

As patient expectations and healthcare requirements continue to evolve, ophthalmology stakeholders are increasingly focusing on technology-driven strategies to improve efficiency, accessibility, and treatment success rates. Digital health platforms, advanced diagnostics, and precision medicine approaches are creating new opportunities for market expansion. However, regulatory approval requirements, reimbursement challenges, and technology adoption costs remain important considerations for companies pursuing long-term growth.

Global Ophthalmology Market Technology & Innovation Forward Outlook

The future of the Global Ophthalmology Market is expected to be shaped by continued advancements in artificial intelligence, gene therapies, robotic-assisted surgical systems, digital diagnostics, and personalized vision care solutions. Emerging innovations such as AI-powered disease prediction models, regenerative ophthalmic treatments, smart wearable vision monitoring devices, and next-generation retinal therapies are expected to further improve patient outcomes and clinical efficiency. Industry participants are likely to increase investments in research and innovation to address the growing global burden of eye diseases and vision impairment.

As healthcare systems increasingly prioritize preventive care, early diagnosis, and personalized treatment approaches, technology will play an increasingly important role in supporting ophthalmology market expansion. The combination of advanced diagnostics, minimally invasive treatment technologies, digital healthcare integration, and innovative therapeutic developments is expected to create substantial growth opportunities while strengthening the long-term evolution of the Global Ophthalmology Market.

Market Risk

Global Ophthalmology Market Risk Factors & Disruption Threats Overview

The Global Ophthalmology Market operates within the broader healthcare, medical devices, pharmaceuticals, and vision care ecosystem. While the market benefits from rising prevalence of eye disorders, growing aging populations, and continuous technological advancements, it faces significant risks related to regulatory approvals, reimbursement pressures, treatment affordability, supply chain complexities, and rapid technological disruption.

One of the most significant structural risks is the stringent regulatory environment governing ophthalmic pharmaceuticals, surgical devices, implants, and diagnostic technologies. Delays in product approvals, clinical trial setbacks, safety concerns, or evolving regulatory requirements can significantly impact commercialization timelines and market adoption.

The market is also exposed to pricing and reimbursement challenges, particularly in regions where healthcare providers and payers seek to control treatment costs. High-cost retinal therapies, advanced surgical technologies, and innovative biologic treatments may face reimbursement limitations that can restrict patient access.

Another major disruption factor is the increasing complexity of global supply chains supporting ophthalmic drugs, surgical instruments, intraocular lenses, diagnostic equipment, and specialized medical components. Manufacturing disruptions, raw material shortages, and logistics constraints can affect product availability and operational efficiency.

Additionally, growing competition from alternative treatment approaches, emerging technologies, and biosimilar products may place pressure on market participants to continuously innovate and demonstrate clinical value.

Global Ophthalmology Market Risk Factors & Disruption Threats Current Scenario

The current market environment is characterized by rising demand for ophthalmic treatments due to increasing incidence of cataracts, glaucoma, diabetic retinopathy, age-related macular degeneration, and refractive disorders. Healthcare systems are investing in advanced diagnostic and therapeutic technologies to improve patient outcomes.

However, healthcare providers and manufacturers continue to face challenges associated with rising treatment costs, workforce shortages, unequal access to specialized eye care services, and growing regulatory scrutiny surrounding product safety and effectiveness.

Regulatory authorities are increasing oversight of ophthalmic drugs, medical devices, artificial intelligence-based diagnostic systems, and surgical technologies. Compliance with evolving standards requires continuous investment in clinical validation, quality assurance, and post-market surveillance.

Healthcare infrastructure limitations in several developing regions continue to restrict access to advanced ophthalmology services, creating disparities in diagnosis and treatment availability.

At the same time, competitive intensity is increasing as pharmaceutical companies, device manufacturers, and digital health providers introduce innovative solutions targeting both established and emerging ophthalmic conditions.

Key Risk Factors & Disruption Threat Signals in Global Ophthalmology Market

A major disruption signal is the rapid adoption of artificial intelligence and digital diagnostic technologies. AI-powered imaging systems and automated screening tools have the potential to reshape traditional ophthalmic care pathways and competitive dynamics.

Another important signal is the increasing emergence of biosimilars and alternative therapies for retinal disorders and chronic eye diseases, which may influence pricing structures and market share distribution.

The growing prevalence of diabetes, aging-related vision disorders, and screen-related eye conditions is increasing demand for ophthalmic services while simultaneously creating capacity challenges for healthcare systems.

Advancements in gene therapies, regenerative medicine, and personalized ophthalmic treatments are introducing new opportunities while increasing development costs and regulatory complexity.

The expansion of teleophthalmology and remote vision care services is transforming patient engagement models and improving access to care, particularly in underserved regions.

Cybersecurity and patient data protection concerns are becoming increasingly important as ophthalmology providers adopt connected diagnostic devices, cloud-based platforms, and digital health technologies.

Strategic Implications of Risk Factors & Disruption Threats in Global Ophthalmology Market

Manufacturers should prioritize regulatory compliance, clinical validation, and continuous quality assurance to maintain product safety, market access, and healthcare provider confidence.

Investment in research and development will remain critical for advancing retinal therapies, minimally invasive surgical technologies, AI-based diagnostics, and next-generation vision care solutions.

Companies should strengthen supply chain resilience through supplier diversification, strategic inventory management, and localized manufacturing capabilities where feasible.

Collaboration with healthcare providers, academic institutions, research organizations, and regulatory agencies can accelerate innovation and support successful commercialization efforts.

Organizations should develop strategies to address affordability and reimbursement challenges by demonstrating clinical effectiveness, long-term outcomes, and healthcare economic value.

Digital transformation initiatives, including teleophthalmology platforms, remote diagnostics, and integrated patient management systems, can improve accessibility and strengthen competitive positioning.

Global Ophthalmology Market Risk Factors & Disruption Threats Forward Outlook

Looking ahead to 2026???2033, the Global Ophthalmology Market is expected to experience continued growth as aging populations expand and the burden of vision-related disorders increases globally. However, future market performance will increasingly depend on innovation, affordability, and healthcare accessibility.

Regulatory frameworks are expected to become more comprehensive, particularly for AI-driven diagnostic systems, digital health solutions, biologic therapies, and advanced surgical technologies. Companies will need to adapt quickly to evolving compliance requirements.

Technological advancements will continue to reshape the market, with artificial intelligence, gene therapies, robotic-assisted procedures, and personalized medicine creating both opportunities and competitive challenges.

Healthcare systems are likely to place greater emphasis on early diagnosis, preventive eye care, and value-based treatment models, influencing product development and reimbursement strategies.

Emerging economies are expected to become increasingly important growth markets as investments in healthcare infrastructure, specialist training, and vision care accessibility continue to expand.

Overall, the market will remain strongly growth-oriented but increasingly shaped by regulatory compliance, technological innovation, treatment affordability, digital transformation, and patient access considerations. Long-term market leaders will be defined by their ability to deliver safe, effective, technologically advanced, and accessible ophthalmic solutions that address the evolving global burden of eye disease and vision impairment.

Regulatory Landscape

Global Ophthalmology Market Regulatory & Policy Environment Overview

The regulatory and policy environment governing the Global Ophthalmology Market is highly structured due to the critical importance of vision care, patient safety, medical device performance, pharmaceutical efficacy, and clinical treatment standards. Regulatory authorities, healthcare agencies, medical device organizations, and pharmaceutical oversight bodies establish comprehensive frameworks that govern ophthalmic drugs, surgical equipment, diagnostic technologies, vision correction products, and clinical care practices.

Ophthalmic pharmaceutical manufacturers, medical device companies, healthcare providers, diagnostic equipment suppliers, and ophthalmology clinics must comply with stringent regulations covering product approvals, clinical validation, manufacturing quality standards, post-market surveillance, and patient safety requirements. Regulatory compliance plays a fundamental role in ensuring effective treatment outcomes and maintaining public confidence in vision care services.

As the prevalence of eye disorders continues to rise globally, regulators are increasingly supporting innovation in ophthalmic therapeutics, minimally invasive procedures, digital diagnostics, and AI-assisted eye care technologies while maintaining rigorous safety and performance standards.

Global Ophthalmology Market Regulatory & Policy Environment Current Scenario

The current regulatory landscape is centered on medical device approvals, pharmaceutical safety requirements, and clinical quality standards. Regulatory authorities require ophthalmic products and technologies to undergo extensive testing and clinical evaluation before commercialization to ensure safety, efficacy, and long-term reliability.

Medical device regulations play a significant role in governing ophthalmic diagnostic systems, surgical instruments, intraocular lenses, retinal imaging devices, laser technologies, and minimally invasive surgical equipment. Manufacturers must demonstrate product performance and compliance with established quality standards.

Drug approval frameworks continue to influence the development and commercialization of ophthalmic pharmaceuticals, including anti-VEGF therapies, glaucoma medications, anti-inflammatory treatments, and emerging gene therapies. Regulatory agencies require comprehensive clinical evidence supporting product safety and therapeutic effectiveness.

Vision care standards and clinical practice guidelines are increasingly important in promoting early diagnosis, standardized treatment protocols, and improved patient outcomes across ophthalmology services. Healthcare providers are expected to follow evidence-based treatment pathways and quality care measures.

Additionally, the growing adoption of artificial intelligence and digital health solutions in ophthalmology is encouraging regulators to establish guidance related to software validation, algorithm transparency, cybersecurity, and patient data protection.

Key Regulatory & Policy Environment Signals in Global Ophthalmology Market

- Medical Device Regulations:

Frameworks governing the approval, manufacturing, performance validation, and post-market monitoring of ophthalmic diagnostic and surgical devices. - Drug Approval & Clinical Evaluation Requirements:

Regulations ensuring the safety, efficacy, quality, and clinical effectiveness of ophthalmic pharmaceuticals and biologic therapies. - Vision Care Standards & Clinical Practice Guidelines:

Policies supporting standardized diagnosis, treatment protocols, patient care quality, and evidence-based ophthalmology practices. - Quality Management & Manufacturing Compliance Standards:

Requirements related to Good Manufacturing Practices (GMP), product consistency, quality assurance, and risk management systems. - Artificial Intelligence & Digital Health Governance:

Emerging regulations governing AI-powered diagnostics, software-based medical devices, teleophthalmology platforms, and algorithm accountability. - Patient Data Privacy & Cybersecurity Requirements:

Policies protecting sensitive health information, digital imaging records, and connected ophthalmology system infrastructure.

Strategic Implications of Regulatory & Policy Environment

The evolving regulatory environment is encouraging companies to invest heavily in clinical research, product validation, regulatory affairs expertise, and quality management systems. Strong compliance capabilities are becoming increasingly important for market access and competitive differentiation.

Medical device regulations are driving investments in advanced testing procedures, performance verification programs, and post-market surveillance systems to ensure long-term product safety and reliability.

Drug approval requirements are encouraging pharmaceutical companies to expand clinical trial activities, strengthen evidence generation strategies, and accelerate innovation in retinal therapies, glaucoma treatments, and regenerative ophthalmic medicine.

The emergence of AI-based diagnostics is motivating technology developers to strengthen software validation, explainability, cybersecurity controls, and regulatory readiness for digital healthcare solutions.

Patient safety and healthcare quality requirements are encouraging ophthalmology providers to adopt standardized care pathways, advanced diagnostic technologies, and continuous quality improvement programs.

Global Ophthalmology Market Regulatory & Policy Environment Forward Outlook

Between 2026 and 2033, the regulatory environment for the Global Ophthalmology Market is expected to become increasingly sophisticated as innovation accelerates across pharmaceuticals, medical devices, digital health platforms, and advanced vision care technologies.

Regulators are likely to strengthen oversight of AI-powered diagnostic systems, digital imaging platforms, and software-enabled ophthalmology solutions while supporting responsible innovation and clinical adoption.

Clinical evidence requirements may expand for emerging therapies such as gene therapies, regenerative medicine solutions, and personalized ophthalmic treatments, emphasizing long-term safety and treatment effectiveness.

Global harmonization efforts among regulatory agencies may improve market access opportunities while increasing expectations related to product quality, traceability, and post-market monitoring across international markets.

Overall, the future regulatory landscape will be shaped by the convergence of medical device regulations, pharmaceutical approval frameworks, vision care standards, AI governance policies, and patient data protection requirements. Organizations capable of delivering safe, compliant, innovative, and clinically validated ophthalmology solutions will be best positioned to capitalize on long-term opportunities within the expanding global vision care industry.