Global Medical Aesthetic Market Report, Size and Forecast 2026-2033

Global Medical Aesthetic Market Report Size and Forecast 2026???2033

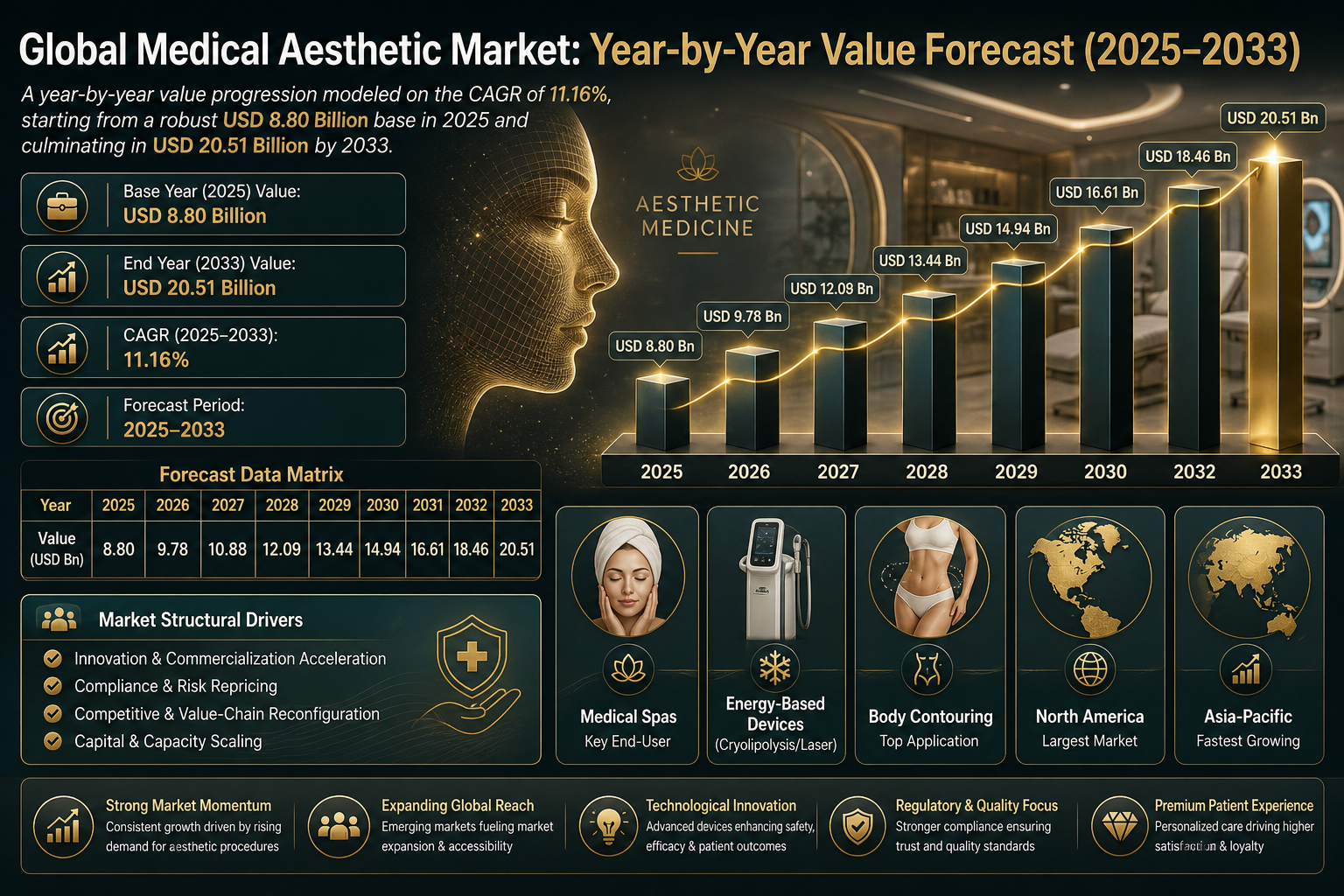

Market Forecast Snapshot (2025???2033)

| Metric | Value |

|---|---|

| Market Size (2025) | USD 8.80 Billion |

| Market Size (2033) | USD 20.51 Billion |

| CAGR (2026???2033) | ~11.16% |

| Largest Region | North America |

| Fastest Growing Region | Asia-Pacific |

| Leading Segment | Non-invasive Procedures |

| Key Trend | Personalized & minimally invasive aesthetic treatments |

Market Size & Forecast

The Global Medical Aesthetic Market is projected to grow from USD 8.80 billion in 2025 to USD 20.51 billion by 2033, registering a CAGR of 11.16% during the forecast period. This growth is primarily driven by rising demand for minimally invasive procedures, increasing disposable income, and a growing societal shift toward aesthetic wellness and self-care. Advancements in energy-based devices and injectable technologies are further accelerating market expansion.Market Overview

The Global Medical Aesthetic Market operates in a highly dynamic and competitive environment, characterized by rapid technological evolution and changing consumer preferences. The market is fragmented with high competitive intensity, featuring key players such as Bausch Health Companies Inc., Cutera, Inc., Venus Concept Inc., and AbbVie Inc.. Technological advancements such as AI-driven treatment customization and innovations in laser and radiofrequency platforms are significantly enhancing treatment outcomes. At the same time, regulatory tightening across major markets is raising compliance standards and influencing product development strategies.Key Drivers of Market Growth

- Increasing demand for non-invasive and minimally invasive procedures

- Rising disposable income and growing consumer spending on aesthetics

- Technological advancements in energy-based devices and injectables

- Growing acceptance of aesthetic treatments across genders and age groups

- Shift toward personalized and customized aesthetic solutions

Market Segmentation

By End User

- Hospitals

- Medical Spas (Fastest Growing)

- Dermatology Clinics

By Application

- Skin Treatments (Largest Segment)

- Body Aesthetic Treatments

- Facial Aesthetic Treatments

By Product Type

- Energy-Based Devices (Laser, RF, Ultrasound, Cryolipolysis)

- Aesthetic Treatment Devices

By Procedure Type

- Non-Invasive Procedures (Dominant Segment)

- Minimally Invasive Procedures

By Injectable Products

- Dermal Fillers

- Botulinum Toxin

Regional Insights

- North America ??? Largest market driven by advanced healthcare infrastructure and high consumer awareness

- Europe ??? Growth supported by technological adoption and strong regulatory frameworks

- Asia-Pacific ??? Fastest growing region due to rising income and expanding middle class

- Latin America ??? Emerging market with increasing demand for minimally invasive procedures

- Middle East & Africa ??? Growing market driven by lifestyle changes and rising awareness

Competitive Landscape

- Bausch Health Companies Inc.

- Cutera, Inc.

- Venus Concept Inc.

- AbbVie Inc.

- Cynosure

- Alma Lasers

Strategic Insights & Trends

- Increasing adoption of AI-driven personalized treatment planning

- Growth in non-surgical body contouring procedures

- Rising demand for injectable aesthetics globally

- Expansion of dermatology clinics and medical spas

- Increasing consolidation through mergers and acquisitions

Why This Market Matters

- Reflects global shift toward wellness and appearance-driven healthcare

- Enables safer, faster, and minimally invasive treatment options

- Drives innovation in personalized medical treatments

- Expands access to aesthetic procedures across emerging markets

- Supports growth of preventive and lifestyle healthcare segments

Final Market Perspective

The Global Medical Aesthetic Market is on a strong growth trajectory, supported by technological innovation, evolving consumer behavior, and expanding healthcare access. The transition toward minimally invasive, AI-driven, and personalized aesthetic treatments is reshaping the competitive landscape. Companies that effectively balance innovation, regulatory compliance, and consumer-centric strategies will be best positioned to capture long-term growth opportunities in this rapidly evolving market.Table of Contents

Table of Contents

- 1. Executive Summary

- 1.1 Market Forecast Snapshot (2026-2033)

- 1.2 Global Market Size & CAGR Analysis

- 1.3 Largest & Fastest-Growing Segments

- 1.4 Region-Level Leadership & Growth Trends

- 1.5 Key Market Drivers

- 1.6 Competitive Landscape Overview

- 1.7 Strategic Outlook Through 2033

- 2. Introduction & Market Overview

- 2.1 Definition of the Global Medical Aesthetic Market

- 2.2 Scope of the Study

- 2.3 Industry Evolution & Market Development

- 2.4 Supply Chain & Distribution Infrastructure

- 2.5 Impact of Consumer Trends

- 2.6 Sustainability & Regulatory Landscape

- 2.7 Technology & Innovation Landscape

- 3. Research Methodology

- 3.1 Primary Research

- 3.2 Secondary Research

- 3.3 Market Size Estimation Model

- 3.4 Forecast Assumptions (2026-2033)

- 3.5 Data Validation & Triangulation

- 4. Market Dynamics

- 4.1 Drivers

- 4.1.1 Increasing Demand Drivers

- 4.1.2 Industry Innovation Drivers

- 4.1.3 Market Expansion Factors

- 4.1.4 Regulatory or Policy Support

- 4.1.5 Technology Adoption Drivers

- 4.2 Restraints

- 4.2.1 Cost Constraints

- 4.2.2 Infrastructure Limitations

- 4.2.3 Regulatory Challenges

- 4.2.4 Market Awareness Barriers

- 4.3 Opportunities

- 4.3.1 Emerging Market Opportunities

- 4.3.2 Product Innovation Opportunities

- 4.3.3 Technology Expansion Opportunities

- 4.3.4 Supply Chain Improvements

- 4.4 Challenges

- 4.4.1 Supply Chain Complexity

- 4.4.2 Quality Control & Compliance

- 4.4.3 Regional Market Fragmentation

- 4.4.4 Competitive Pressure

- 4.1 Drivers

- 5. Global Medical Aesthetic Market Analysis (USD Billion), 2026-2033

- 5.1 Market Size Overview

- 5.2 CAGR Analysis

- 5.3 Regional Revenue Distribution

- 5.4 Segment Revenue Analysis

- 5.5 Distribution Channel Analysis

- 5.6 Consumer Impact Analysis

- 6. Market Segmentation (USD Billion), 2026-2033

- 6.1 By End User

- 6.1.1 Hospitals

- 6.1.1.1 Cosmetic Surgery Departments

- 6.1.1.1.1 Plastic Surgery Units

- 6.1.1.1.1.1 Facial Cosmetic Surgery Centers

- 6.1.1.1.1.2 Body Contouring Surgery Units

- 6.1.1.1.1 Plastic Surgery Units

- 6.1.1.1 Cosmetic Surgery Departments

- 6.1.2 Medical Spas

- 6.1.2.1 Aesthetic Treatment Centers

- 6.1.2.1.1 Non-Surgical Cosmetic Treatment Clinics

- 6.1.2.1.1.1 Skin Rejuvenation Treatment Centers

- 6.1.2.1.1.2 Laser Aesthetic Treatment Clinics

- 6.1.2.1.1 Non-Surgical Cosmetic Treatment Clinics

- 6.1.2.1 Aesthetic Treatment Centers

- 6.1.3 Dermatology Clinics

- 6.1.3.1 Medical Aesthetic Clinics

- 6.1.3.1.1 Cosmetic Dermatology Centers

- 6.1.3.1.1.1 Anti-Aging Treatment Clinics

- 6.1.3.1.1.2 Skin Rejuvenation Clinics

- 6.1.3.1.1 Cosmetic Dermatology Centers

- 6.1.3.1 Medical Aesthetic Clinics

- 6.1.1 Hospitals

- 6.2 By Application

- 6.2.1 Skin Treatments

- 6.2.1.1 Dermatological Aesthetic Procedures

- 6.2.1.1.1 Pigmentation Treatment

- 6.2.1.1.1.1 Hyperpigmentation Reduction Procedures

- 6.2.1.1.1.2 Melasma Treatment Procedures

- 6.2.1.1.1 Pigmentation Treatment

- 6.2.1.1 Dermatological Aesthetic Procedures

- 6.2.2 Body Aesthetic Treatments

- 6.2.2.1 Body Contouring

- 6.2.2.1.1 Non-Surgical Fat Reduction

- 6.2.2.1.1.1 Abdominal Fat Reduction Procedures

- 6.2.2.1.1.2 Thigh and Arm Contouring Treatments

- 6.2.2.1.1 Non-Surgical Fat Reduction

- 6.2.2.1 Body Contouring

- 6.2.3 Facial Aesthetic Treatments

- 6.2.3.1 Facial Rejuvenation

- 6.2.3.1.1 Anti-Aging Treatments

- 6.2.3.1.1.1 Wrinkle Reduction Procedures

- 6.2.3.1.1.2 Skin Tightening Treatments

- 6.2.3.1.1 Anti-Aging Treatments

- 6.2.3.1 Facial Rejuvenation

- 6.2.1 Skin Treatments

- 6.3 By Product Type

- 6.3.1 Energy-Based Aesthetic Devices

- 6.3.1.1 Cryolipolysis Devices

- 6.3.1.1.1 Fat Freezing Systems

- 6.3.1.1.1.1 Non-Invasive Fat Reduction Devices

- 6.3.1.1.1.2 Body Contouring Cryotherapy Devices

- 6.3.1.1.1 Fat Freezing Systems

- 6.3.1.2 Ultrasound Aesthetic Devices

- 6.3.1.2.1 Focused Ultrasound Systems

- 6.3.1.2.1.1 High Intensity Focused Ultrasound (HIFU) Devices

- 6.3.1.2.1.2 Non-Invasive Skin Lifting Systems

- 6.3.1.2.1 Focused Ultrasound Systems

- 6.3.1.3 Laser-Based Aesthetic Devices

- 6.3.1.3.1 Ablative Laser Systems

- 6.3.1.3.1.1 CO2 Laser Resurfacing Systems

- 6.3.1.3.1.2 Er:YAG Skin Resurfacing Lasers

- 6.3.1.3.2 Non-Ablative Laser Systems

- 6.3.1.3.2.1 Fractional Laser Therapy Devices

- 6.3.1.3.2.2 Skin Rejuvenation Laser Systems

- 6.3.1.3.1 Ablative Laser Systems

- 6.3.1.4 Radiofrequency (RF) Aesthetic Devices

- 6.3.1.4.1 Skin Tightening RF Devices

- 6.3.1.4.1.1 Monopolar RF Skin Tightening Systems

- 6.3.1.4.1.2 Bipolar RF Skin Rejuvenation Devices

- 6.3.1.4.1 Skin Tightening RF Devices

- 6.3.1.1 Cryolipolysis Devices

- 6.3.1 Energy-Based Aesthetic Devices

- 6.4 By Procedure Type

- 6.4.1 Non-Invasive Procedures

- 6.4.1.1 Body Contouring Procedures

- 6.4.1.1.1 Non-Surgical Fat Reduction

- 6.4.1.1.1.1 Cryolipolysis Fat Reduction

- 6.4.1.1.1.2 RF Body Contouring Treatments

- 6.4.1.1.1 Non-Surgical Fat Reduction

- 6.4.1.2 Skin Rejuvenation Procedures

- 6.4.1.2.1 Laser Skin Resurfacing

- 6.4.1.2.1.1 Anti-Aging Laser Treatments

- 6.4.1.2.1.2 Skin Texture Improvement Procedures

- 6.4.1.2.1 Laser Skin Resurfacing

- 6.4.1.1 Body Contouring Procedures

- 6.4.2 Minimally Invasive Procedures

- 6.4.2.1 Dermal Filler Procedures

- 6.4.2.1.1 Facial Contouring Treatments

- 6.4.2.1.1.1 Lip Augmentation Procedures

- 6.4.2.1.1.2 Facial Volume Restoration Treatments

- 6.4.2.1.1 Facial Contouring Treatments

- 6.4.2.2 Injectable Cosmetic Treatments

- 6.4.2.2.1 Botulinum Toxin Injections

- 6.4.2.2.1.1 Facial Wrinkle Reduction

- 6.4.2.2.1.2 Facial Muscle Relaxation Treatments

- 6.4.2.2.1 Botulinum Toxin Injections

- 6.4.2.1 Dermal Filler Procedures

- 6.4.1 Non-Invasive Procedures

- 6.5 By Injectable Aesthetic Products

- 6.5.1 Dermal Fillers

- 6.5.1.1 Collagen-Based Fillers

- 6.5.1.1.1 Facial Wrinkle Fillers

- 6.5.1.1.1.1 Nasolabial Fold Fillers

- 6.5.1.1.1.2 Skin Contouring Fillers

- 6.5.1.1.1 Facial Wrinkle Fillers

- 6.5.1.2 Hyaluronic Acid Fillers

- 6.5.1.2.1 Facial Volume Restoration

- 6.5.1.2.1.1 Cheek Augmentation Fillers

- 6.5.1.2.1.2 Lip Enhancement Fillers

- 6.5.1.2.1 Facial Volume Restoration

- 6.5.1.1 Collagen-Based Fillers

- 6.5.2 Botulinum Toxin Products

- 6.5.2.1 Cosmetic Botulinum Toxin

- 6.5.2.1.1 Wrinkle Reduction Treatments

- 6.5.2.1.1.1 Forehead Line Treatments

- 6.5.2.1.1.2 Crows Feet Treatment

- 6.5.2.1.1 Wrinkle Reduction Treatments

- 6.5.2.1 Cosmetic Botulinum Toxin

- 6.5.1 Dermal Fillers

- 6.1 By End User

- 7. Market Segmentation by Geography

- 7.1 North America

- 7.2 Europe

- 7.3 Asia-Pacific

- 7.4 Latin America

- 7.5 Middle East & Africa

- 8. Competitive Landscape

- 8.1 Market Share Analysis

- 8.2 Product Portfolio Benchmarking

- 8.3 Product Positioning Mapping

- 8.4 Supply Chain & Distribution Partnerships

- 8.5 Competitive Intensity & Differentiation

- 9. Company Profiles

- 10. Strategic Intelligence & Pheonix AI Insights

- 10.1 Pheonix Demand Forecast Engine

- 10.2 Supply Chain & Infrastructure Analyzer

- 10.3 Technology & Innovation Tracker

- 10.4 Product Development Insights

- 10.5 Automated Porter’s Five Forces Analysis

- 11. Future Outlook & Strategic Recommendations

- 11.1 Emerging Market Expansion

- 11.2 Technology Innovation Strategies

- 11.3 Product Development Roadmap

- 11.4 Regional Expansion Strategies

- 11.5 Long-Term Market Outlook (2033+)

- 12. Appendix

- 13. About Pheonix Research

- 14. Disclaimer

Competitive Landscape

Competitive Landscape of the Global Medical Aesthetic Market

Executive Framing

In the evolving landscape of global medical aesthetics, the dimension of competitive intensity and market structure emerges as a crucial focal point. This dimension is not merely about the number of players in the market but the dynamics that shape and inform competitive strategies and market positioning. With a market structure identified as fragmented and competitive intensity rated high, stakeholders are navigating a complex environment characterized by rapid innovations, strategic collaborations, and aggressive market maneuvers. Understanding these dynamics is imperative for companies aiming to secure their strategic foothold and capitalize on emerging opportunities. The current period leading up to 2033 is particularly significant due to several transformative trends that are reshaping the competitive landscape. Companies like AbbVie, Bausch Health Companies Inc., and Cynosure are not just reacting to market demands; they are actively shaping the future of the industry through strategic initiatives. This involves launching cutting-edge products, forming strategic partnerships, and leveraging technological advancements to meet the burgeoning demand for minimally invasive and non-invasive aesthetic procedures. The stakes are high, and the moves made today will have long-lasting effects on competitive positioning and market share.

Current Market Reality

The global medical aesthetic market is characterized by a fragmented structure where a handful of tier 1 players, including AbbVie, Bausch Health Companies Inc., and Cutera, Inc., vie for dominance. This fragmentation, however, does not dilute competitive intensity; rather, it amplifies it. With each player striving to differentiate itself through innovation and strategic alliances, the market is a hotbed of activity and competition.

A key manifestation of this competitive intensity is the wave of product launches and technological advancements. For instance, AbbVie???s introduction of a next-generation RF-based fat reduction device in 2024 exemplifies how companies are leveraging technology to gain a competitive edge. Similarly, Fotona’s launch of a new 4D laser treatment for body contouring in 2023 underscores the commitment to technological innovation as a means of differentiation. These moves not only cater to the rising consumer demand for advanced aesthetic solutions but also set new benchmarks for competitors.

Furthermore, the strategic acquisition activities, such as Hologic’s acquisition of Gynesonics for $350 million, signal an aggressive approach to expanding capabilities and market reach. Such acquisitions are not merely about acquiring new technologies or products but also about consolidating market positions and mitigating competitive threats. By integrating complementary technologies and expanding product portfolios, companies are better positioned to cater to diverse consumer preferences and enhance their value propositions.

The market is also witnessing a surge in strategic collaborations aimed at enhancing brand visibility and broadening market reach. Cutera, Inc.’s collaboration with professional tennis players during the Australian Open tournament is a prime example of how companies are leveraging partnerships to enhance brand recognition and appeal to a wider audience. This strategy is particularly effective in a fragmented market where brand differentiation can significantly influence consumer choice.

Additionally, the increasing number of aesthetic procedures, driven by rising consumer awareness and technological advancements, is reshaping the market landscape. The growing demand for minimally invasive procedures, as evidenced by the popularity of botulinum toxin procedures, is compelling companies to innovate and expand their service offerings. This trend is further accentuated by the rise of med-spas, which are redefining the consumer experience by offering personalized and integrated aesthetic solutions.

Key Signals and Evidence

- Product Launches: AbbVie???s next-generation RF-based fat reduction device (2024), Fotona’s 4D laser treatment (2023), Lumenis’ Stellar M22 system (2024), and Alma Lasers’ Harmony XL PRO (2023) exemplify technological differentiation.

- Regulatory Approvals: FDA approval of Evolus, Inc.’s Evolysse Form and Evolysse Smooth injectable HA gels demonstrates the importance of compliance in enhancing credibility and competitive positioning.

- Strategic Acquisitions: Hologic’s acquisition of Gynesonics ($350M) illustrates market consolidation and capability expansion as a competitive strategy.

- Strategic Collaborations: Partnerships like Cutera, Inc.’s collaboration with professional athletes enhance brand visibility and reach within a fragmented market.

- Consumer Trends: High adoption of minimally invasive procedures such as Botulinum Toxin treatments underscores the need for diversified and innovative product portfolios.

Strategic Implications

- Continuous Innovation: Companies must invest in R&D to maintain a competitive edge and meet evolving consumer demands.

- Strategic Collaborations: Partnerships with influencers, athletes, and other stakeholders enhance brand equity and market reach in a fragmented market.

- Acquisitions and Investments: Acquiring complementary technologies or companies expands capabilities, diversifies offerings, and strengthens market positioning.

- Regulatory Navigation: Securing approvals for new products and treatments builds credibility and differentiates companies in a crowded competitive landscape.

- Consumer-Centric Strategies: Offering personalized and minimally invasive treatments aligns with rising consumer aesthetic consciousness, enhancing loyalty and market share.

Forward Outlook

Looking ahead, the competitive intensity and fragmented structure of the global medical aesthetics market are likely to persist, driven by ongoing technological advancements and evolving consumer demands. Companies that can successfully navigate this complex landscape by leveraging innovation, strategic partnerships, and regulatory compliance are well-positioned to thrive in the near-to-medium term.

The rise of personalized treatment plans and non-invasive procedures is expected to continue, fueled by increasing consumer awareness and demand for customized solutions. Firms offering tailored treatments that cater to individual preferences are likely to capture a larger share of the market.

Technological innovation will remain a key driver of market evolution, with companies investing heavily in R&D to enhance their product offerings and sustain a competitive edge. Strategic collaborations and acquisitions will also continue to shape the market landscape, enabling firms to expand capabilities, enter new segments, and strengthen their positioning.

Value Chain

Value Chain and Supply Chain Dynamics in theGlobal medical aesthetic market

Executive Framing

In the global medical aesthetic market, the value chain dimension plays a pivotal role in shaping the industry’s structure and competitive dynamics. As the market evolves from 2026 through 2033, understanding the intricacies of the value chain becomes imperative for stakeholders. The hybrid operational model, coupled with a direct-to-consumer distribution structure, highlights ongoing transformations in how products and services reach end users.

However, this transformation faces challenges such as workforce shortages, regulatory complexities, and capital intensity, which collectively influence margins, bargaining power, and overall supply chain efficacy. The surge in demand for minimally invasive procedures is constrained by limited capacity due to skilled practitioner shortages, stringent regulatory and safety compliance requirements, and financial challenges associated with adopting advanced technologies. These factors reconfigure power dynamics within the value chain, necessitating strategic reevaluation by firms seeking to optimize operational models.

Current Market Reality

The global medical aesthetic market currently exhibits moderate supply chain complexity across stages such as raw material sourcing, manufacturing, distribution, and consumer engagement. Companies are taking strategic steps to adapt to this landscape. For example, AbbVie’s launch of a next-generation RF-based fat reduction device in 2024 and Fotona’s 4D laser treatment for body contouring in 2023 highlight technological advancements shaping consumer offerings.

Operational challenges remain pronounced due to administrative layers required for regulatory compliance and safety standards, especially impacting smaller clinics. Compliance thresholds, high device costs, and specialized practitioner training requirements favor well-resourced entities. The rise of digital-integrated clinic???spa experiences reflects a shift toward holistic consumer engagement, offering competitive advantage for companies that leverage digital tools effectively.

Strategic consolidations, such as Hologic’s acquisition of Gynesonics for $350 million, illustrate market responses to these pressures. Similarly, Evolus, Inc.???s FDA-approved Evolysse injectable hyaluronic acid gels underscore the importance of regulatory compliance in product development and market entry.

Key Signals and Evidence

- Capital Intensity of Technology Adoption: Advanced systems like Lumenis??? Stellar M22 and Alma Lasers??? Harmony XL PRO reflect the industry’s push toward innovation. High capital requirements can create barriers for smaller firms, consolidating market power among established players.

- Workforce Shortages: Limited availability of skilled aesthetic practitioners constrains capacity utilization, shifts bargaining power toward practitioners, and drives up labor costs.

- Stringent Regulatory and Safety Compliance: Regulatory requirements add administrative layers and increase operational costs. Smaller clinics face challenges meeting compliance thresholds, impacting viability and margins.

- Rising Consumer Awareness: Growing demand for minimally invasive treatments is driven by aging populations and increasing obesity rates. Companies like Evolus capitalize on this trend with FDA-approved products aligned with consumer preferences.

- Administrative Layers from Regulations: Complex compliance tasks divert resources from core operations, slowing decision-making and product rollout, affecting supply chain agility.

Strategic Implications

- Shifting Margins and Bargaining Power: High capital intensity and practitioner scarcity favor larger firms, enabling them to maintain a competitive edge and influence market terms.

- Capacity Utilization and Operational Efficiency: Recruiting and retaining skilled practitioners is critical to optimizing throughput and reducing wait times, directly impacting revenue and consumer satisfaction.

- Regulatory Compliance as Strategic Priority: Allocating resources to ensure adherence to safety and efficacy standards serves as a competitive differentiator and enhances consumer trust.

- Consumer-Driven Demand and Market Positioning: Companies must align offerings with consumer expectations for minimally invasive, effective treatments, leveraging innovation to remain competitive.

Forward Outlook

Looking ahead, the global medical aesthetic market is poised for continued evolution, driven by technological advancements, regulatory developments, and shifting consumer dynamics. Stakeholders must remain vigilant, adapting strategies to navigate workforce constraints, regulatory complexity, and capital-intensive technology adoption. Firms that optimize their value chains, invest in skilled personnel, and align with regulatory expectations will be well-positioned to capitalize on market growth and maintain competitive advantage.

Investment Activity

Investment Activity of the Global Medical Aesthetic Market

Executive Framing

In the evolving landscape of global medical aesthetics, investment and funding dynamics are pivotal in shaping the market’s structure and trajectory. As consumer demand for aesthetic procedures escalates, so too does the interest from investors eager to capitalize on this burgeoning field. The investment trend direction is notably rising, indicating a robust influx of capital that is reshaping competitive behaviors, market consolidation, and strategic asset allocations. With a medium capital intensity level, investors are strategically positioning themselves in areas that promise high returns and sustainable growth. The recent surge in mergers and acquisitions (M&A) activity underscores this trend, highlighting the market’s attractiveness to both private equity and strategic investors.

This dimension matters now more than ever as it influences the allocation of resources, the pace of innovation, and ultimately, the value delivered to consumers. Strategic allocation of capital is crucial for sustaining growth, fostering innovation, and capturing market share in a fragmented industry characterized by high profit margins and a growing focus on personalized and integrative wellness solutions. As traditional beauty transforms into a broader wellness paradigm, the dynamics of investment and funding become central to understanding competitive positioning and long-term market viability.

Current Market Reality

The present state of the global medical aesthetic market reveals a landscape ripe for investment, driven by several key players and emerging trends. Active investors such as VSS Capital Partners, BC Partners, Incline Equity Partners, and others are at the forefront, channeling capital into promising ventures and technologies. These investors are drawn by the sector’s potential for high returns, driven by increased consumer awareness and technological advancements.

Recent M&A activities, such as Hologic’s acquisition of Gynesonics for $350 million, demonstrate strategic moves to consolidate and enhance market offerings. Such acquisitions not only expand operational capabilities but also align with broader investment themes like non-invasive treatments and regenerative aesthetics. The rise of technology adoption is evident with companies like Lumenis launching the Stellar M22 system and Alma Lasers introducing the Harmony XL PRO, showcasing advancements that appeal to tech-savvy consumers and investors alike.

The market is witnessing a fragmentation ripe for consolidation, presenting opportunities for investors to strategically acquire niche players and integrate them into larger entities. This consolidation is fueled by the expansion of treatment options and clinics, catering to a growing patient base and increased consumer demand. The shortage of dermatologists, however, presents a challenge, amplifying the need for investment in training and technology to meet the rising demand.

Furthermore, the expansion of med spas and dermatology clinics is a direct response to the increasing adoption of customized anti-aging plans and skin rejuvenation therapies. Investors are backing business models that emphasize personalization, integrative wellness, and subscription-based revenue models, aligning with consumer preferences for tailored and accessible aesthetic treatments.

Key Signals and Evidence

- Increasing Consumer Demand and Personalized Beauty: Rising interest in skin rejuvenation therapies and normalization of aesthetic procedures, especially among younger generations, drives investment in personalized solutions.

- Expansion of Treatment Options and Technology Adoption: Launches such as AbbVie’s RF-based fat reduction device and Fotona’s 4D laser treatment illustrate the technological advancements attracting investor interest.

- Private Equity Investment and Market Consolidation: Firms like Shore Capital Partners and The Thurston Group actively pursue consolidation, leveraging high-profit margins to acquire niche players and integrate them for synergies.

- Expansion of Med Spas and Dermatology Clinics: Growing patient bases and the shortage of dermatologists fuel investment in alternative service delivery models and clinic expansion.

- Non-Invasive Treatments and Integrative Wellness: Investment focuses on non-invasive procedures and wellness integration, reflecting consumer preference for holistic, less invasive solutions with sustainable growth potential.

Strategic Implications

- Market Consolidation and Competitive Behavior: High investment activity drives M&A, enabling companies to achieve economies of scale, diversify product portfolios, and enhance technological capabilities.

- Private Equity and Strategic Positioning: PE firms provide capital and strategic guidance, accelerating innovation and expansion in areas like non-invasive treatments and regenerative aesthetics.

- Technology Adoption and Consumer Alignment: Investment in advanced technologies (e.g., Stellar M22, Harmony XL PRO) enhances procedure efficacy, safety, and alignment with personalized consumer preferences.

- Expansion of Med Spas and Dermatology Clinics: Funding for clinic expansion addresses rising demand and dermatology shortages, supporting decentralized service delivery and greater market penetration.

- Risk and Opportunity in a Fragmented Market: Fragmentation allows strategic investors to acquire undervalued assets and integrate them into cohesive portfolios, but requires careful risk and scalability assessment.

Forward Outlook

Looking ahead to the forecast period of 2026-2033, the global medical aesthetic market is poised for continued evolution underpinned by strategic investment and funding dynamics. The rising trend in capital allocation will likely sustain momentum, driven by consumer demand, technological advancements, and the pursuit of personalized and integrative wellness solutions.

Sustained Investment and Growth Trajectories: Continued inflows from private equity and strategic investors will fuel innovation, expand treatment options, and enhance consumer experiences, supporting market growth.

Evolving Consumer Preferences and Market Adaptation: Companies will increasingly integrate wellness and aesthetics, adopt subscription-based models, and deliver personalized solutions to align with consumer expectations and build loyalty.

Regulatory and Economic Considerations: Stakeholders must navigate regulatory frameworks and economic factors to ensure sustainable growth, while capitalizing on emerging opportunities.

The Role of Innovation in Shaping the Future: Continued investment in R&D will drive new solutions, enhance existing treatments, and establish technological differentiation, positioning companies for long-term success.

In conclusion, investment and funding dynamics are central to shaping the global medical aesthetic market’s trajectory. Strategic allocation of capital will drive innovation, consumer engagement, and sustainable growth, ultimately determining the market???s future direction and success.

Technology & Innovation

Technology and Innovation Landscape in the Global medical aesthetic market

Executive Framing

As technology continues to reshape the global medical aesthetic market, its influence is both profound and multifaceted. This dimension holds particular significance due to its capacity to redefine procedural economics, enhance clinical outcomes, and transform patient throughput. The technological landscape within the medical aesthetic sector is marked by high innovation intensity and moderate patent activity levels, indicative of a vibrant yet competitive environment. Currently, technology is in the growth stage of maturity, presenting unique opportunities for companies to leverage emerging solutions to capture market share.

The integration of key technologies such as cryolipolysis, radiofrequency, and high-intensity focused ultrasound (HIFU) is driving a paradigm shift from invasive to non-invasive solutions, meeting the growing demand for less intrusive treatments while aligning with societal emphasis on skin health and personalized treatment plans. Companies like Candela Corporation, Lumenis Ltd., Cynosure, Alma Lasers, and Cutera are at the forefront, exploring new technologies to maintain competitive edge. Emerging trends like AI-driven treatment customization and heightened consumer awareness of skincare further underscore the strategic importance of technology in shaping the market’s future.

Current Market Reality

The global medical aesthetic market is evolving rapidly, driven by technological advancements that enhance efficacy, safety, and accessibility of treatments. Adoption of non-invasive and minimally invasive procedures is at the forefront, supported by multi-technology platforms such as Lumenis’ Stellar M22 system and Alma Lasers’ Harmony XL PRO. These platforms allow practitioners to tailor treatments to individual patient needs, reflecting a trend toward device versatility and personalization.

Consumer preference for non-invasive treatments is evident in the 92% increase in demand for body contouring treatments since 2019. Concurrently, awareness of the global burden of skin diseases is prompting demand for solutions that promote long-term skin health. Technologies like non-thermal green lasers and muscle-stimulating devices improve skin texture and collagen production, complementing aesthetic enhancement with overall skin wellness.

Artificial intelligence integration further enables personalized treatment plans, optimizing clinical outcomes and patient satisfaction. Clinical studies show an 86% improvement in results when AI-driven approaches are applied, highlighting their effectiveness in personalizing care and enhancing operational efficiency.

Key Signals and Evidence

- Energy-based Devices Market: Projected at USD 6 billion by 2024, highlighting rapid adoption of technologies like radiofrequency and ultrasound for non-invasive procedures.

- Consumer Awareness & Long-Term Skin Health: Rising demand for preventative care solutions is driving adoption of technologies that improve skin texture and stimulate collagen production.

- AI Integration: Use of AI for treatment customization enhances efficacy, operational efficiency, and patient satisfaction.

- FDA Approvals: Regulatory validation of new devices ensures safety, builds consumer trust, and facilitates market adoption.

Strategic Implications

- Shift to Personalized & Preventative Care: Companies must leverage AI and patient data to offer tailored treatment plans, improving outcomes and operational efficiency.

- Non-Invasive Treatments as Growth Driver: Significant market opportunity exists in minimally invasive solutions, with body contouring demand up 92% since 2019. Investments in compatible technologies are crucial for market share.

- Regulatory Alignment: FDA approvals are pivotal for adoption, trust, and market expansion. Companies that secure approvals for their devices gain a competitive advantage.

- Operational Efficiency & Economic Impact: Integration of AI and advanced technologies streamlines workflows, reduces procedural costs, improves margins, and enhances patient satisfaction.

- Competitive Differentiation: Early adoption of innovative platforms by companies like Candela, Lumenis, and Evolus enhances market positioning and long-term sustainability.

Forward Outlook

The global medical aesthetic market is poised for transformation driven by ongoing technological advancements. Companies that effectively leverage AI, non-invasive solutions, and personalized care will likely emerge as market leaders. Collaboration between technology firms and medical aesthetic companies will accelerate innovation, resulting in new solutions that improve outcomes and patient satisfaction.

Consumer demand for long-term skin health and preventative care will continue shaping market dynamics, favoring companies offering holistic treatment plans. Regulatory compliance, especially FDA approvals, will remain critical for market entry, consumer trust, and competitive positioning.

In conclusion, the strategic implications of technology in the global medical aesthetic market are profound. Companies that align innovation with consumer demand, regulatory requirements, and operational efficiency will define the industry’s future. Technology, personalization, and long-term skin health will be the key drivers of growth and competitive advantage.

Market Risk

Risk Factors and Disruption Threats in the Global Medical Aesthetic Market

Executive Framing

The global medical aesthetics market is entering a critical phase marked by significant structural constraints and market risks that could redefine the industry’s landscape between 2026 and 2033. At the forefront of these challenges is the high overall market risk level, driven by complications from procedures, lack of regulation, and the presence of unqualified practitioners. These factors collectively threaten consumer confidence and market stability, potentially disrupting demand and pricing structures.

Geopolitical exposure and substitution risk are moderate but significant. The lack of stringent regulation, combined with high-pressure sales tactics and complications such as infections and nerve damage, exacerbates the market’s vulnerability. These risks manifest in increased calls for regulation, public demand for transparency in physician disciplinary actions, and consumer warnings. Strategic implications for companies, regulators, and consumers are profound, necessitating a reevaluation of operational and strategic priorities.

Current Market Reality

The global medical aesthetics industry currently faces a regulatory void with wide-reaching implications for market structure and operational resilience. Unqualified practitioners can operate with minimal oversight, creating a structural risk amplified by potential procedural complications including infections, hematomas, and nerve damage. This situation contributes to growing medical malpractice lawsuits and public safety concerns.

Government initiatives, such as amendments to the Health and Care Act 2022, aim to address these gaps but are not yet fully effective. Meanwhile, technological advancements like AbbVie’s RF-based fat reduction devices and Fotona’s 4D laser treatments introduce both growth potential and new risks. Reports of adverse events and FDA warnings regarding RF microneedling highlight the urgency of robust regulatory oversight to ensure that innovation does not outpace safety.

Key Signals and Evidence

- Lack of Regulation: Regulatory gaps allow unqualified practitioners and unsupervised procedures, increasing market risk and patient safety concerns.

- Public Demand for Transparency: Growing consumer awareness is driving calls for stricter oversight, reflecting a shift toward higher accountability.

- Lower-than-Average Pricing: Price-sensitive market segments often compromise on safety standards, potentially eroding consumer trust and increasing liability.

- Technological Advancement Risks: New devices from Lumenis (Stellar M22) and Alma Lasers (Harmony XL PRO) expand capabilities but introduce procedural risks, highlighting the need for safety compliance and qualified operators.

- Regulatory Initiatives: Amendments like the Health and Care Act 2022 indicate legislative intent to improve oversight, with success dependent on effective implementation and industry compliance.

Strategic Implications

- Regulatory Compliance and Safety: Aligning with accredited facilities and certified practitioners is critical for mitigating risks, enhancing consumer confidence, and protecting against reputational damage.

- Pricing and Quality Balance: Competitive pricing must be weighed against safety and quality standards, with clear communication of value to justify premium offerings.

- Technology Integration and Risk Management: Investing in R&D and vetting new technologies ensures innovation while maintaining compliance with evolving regulatory standards.

- Operational Resilience: Companies must develop strategies to handle complications, manage liability, and uphold consumer trust amid a volatile and partially regulated market.

Forward Outlook

Looking forward, the global medical aesthetics market is set for significant transformation. Increasing public demand for regulation is expected to drive more stringent frameworks, redefining market dynamics. Companies that proactively adopt robust safety protocols, employ qualified personnel, and comply with evolving regulations will gain a competitive advantage.

Technological innovation will continue to shape market evolution, but adoption must be coupled with rigorous safety assessments and regulatory compliance. Companies like Lumenis and Alma Lasers will lead innovation, but all stakeholders must ensure that advancements do not compromise patient safety.

In conclusion, the market is at a crossroads where structural constraints and risks create both challenges and opportunities. Strategic agility???focused on regulatory compliance, safety, and responsible innovation???will be crucial for sustaining growth and maintaining competitive advantage. Companies that adapt to evolving regulations and consumer expectations will be well-positioned for long-term success in this dynamic industry.

Regulatory Landscape

Regulatory and Policy Landscape of the Global medical aesthetic market

Executive Framing

The global medical aesthetic market is navigating a complex and evolving regulatory and policy landscape that is poised to reshape its structure significantly by 2033. As consumer demand for aesthetic procedures continues to rise, regulatory bodies worldwide are introducing new guidelines and tightening existing regulations to address ongoing concerns about patient safety and the ethical marketing of these services. This regulatory dimension is crucial as it directly influences market entry barriers, operational costs, and competitive dynamics.

Increasing scrutiny on non-surgical cosmetic procedures, coupled with heightened enforcement actions, is expected to redefine how companies operate within this space. The implications are far-reaching, affecting everything from advertising strategies to compliance costs, making it essential for stakeholders to stay abreast of these developments to navigate the market effectively.

Current Market Reality

The current state of the global medical aesthetic market is characterized by a mix of opportunity and caution. Increased demand for non-invasive cosmetic enhancements is accompanied by heightened regulatory scrutiny aimed at ensuring patient safety and ethical practices. Key regulatory bodies such as the U.S. FDA and the Australian Health Practitioner Regulation Agency (Ahpra) are at the forefront of implementing new guidelines that will shape the industry’s future.

In the U.S., the FDA has been intensifying oversight on healthcare advertising regulations, particularly for non-surgical cosmetic procedures, to address public safety concerns and misleading marketing. Similarly, in Australia, the Medical Board of Australia and Ahpra are implementing regulations for non-surgical cosmetic procedures effective September 2, 2025, requiring stricter practitioner qualifications and facility standards, thereby increasing operational compliance costs.

Regional variations, such as Florida’s medical spa laws and Kentucky’s supervision model, create uneven competitive landscapes, where companies in stricter regulatory states may face higher compliance costs and longer timelines for service delivery.

Key Signals and Evidence

- Emerging Regulations: New rules for non-surgical procedures highlight gaps in oversight and require companies to ensure compliance through staff training, safer technologies, and internal audits.

- Staffing Challenges: Stricter regulations increase the need for qualified personnel, while the pool of licensed professionals is not expanding at the same rate, driving investment in recruitment and training.

- Global Benchmarks: South Korea???s rigorous cosmetic procedure regulations serve as a model for future global trends, emphasizing patient safety and ethical marketing.

- Advertising Oversight: FDA tightening of healthcare advertising rules ensures accurate risk-benefit communication and protects consumers from misleading claims.

- Federal Regulation Shifts: Ongoing policy changes may alter competitive dynamics, requiring companies to enhance compliance frameworks and adopt best practices in patient safety and marketing.

Strategic Implications

- Compliance Frameworks: Investment in robust compliance systems is critical to avoid legal repercussions, maintain licenses, and build consumer trust.

- Ethical Marketing: Transparent and evidence-based advertising differentiates companies and attracts informed customers.

- Staffing Strategies: Companies must address regulatory-driven staffing challenges through competitive compensation, training, and supportive work environments.

- Competitive Positioning: Proactive adaptation to regulatory changes can provide a market advantage, as seen with AbbVie’s RF-based fat reduction device and Evolus, Inc.’s FDA-approved HA gels.

Forward Outlook

The regulatory and policy environment in the global medical aesthetic market is expected to continue evolving, with increased public concern driving stricter oversight. Companies that prioritize compliance, patient safety, and ethical practices will gain a competitive edge.

Collaboration with regulatory bodies through public consultations and proactive engagement will allow companies to help shape feasible policies while ensuring consumer protection. Technological innovation will continue, but adoption must be balanced with rigorous safety and compliance standards to mitigate risks.

In conclusion, the market is entering a period of significant regulatory transformation. Companies that remain vigilant, adaptable, and patient-centric, while aligning with evolving regulations, will achieve sustainable growth and maintain competitiveness in this dynamic industry.