Global Procurement Software Market size and share Analysis 2026-2033

Global Procurement Software Market Forecast Snapshot (2026–2033)

| Metric | Value |

|---|---|

| Market Size (2025) | USD 8.9 Billion |

| Market Size (2033) | USD 21.7 Billion |

| CAGR (2026–2033) | 11.7% |

| Largest Segment | Procurement Software Solutions |

| Fastest Growing Segment | AI-Driven Procurement & Spend Analytics Platforms |

| Leading End-Use Segment | Large Enterprises |

| Key Trend | Shift Toward Cloud-Based Intelligent Procurement Ecosystems with AI Automation |

| Dominant Region | North America |

| Fastest Growing Region | Asia-Pacific |

| Primary Growth Driver | Enterprise Digital Transformation and Demand for Cost Optimization & Supply Chain Visibility |

Global Procurement Software Market Size & Forecast

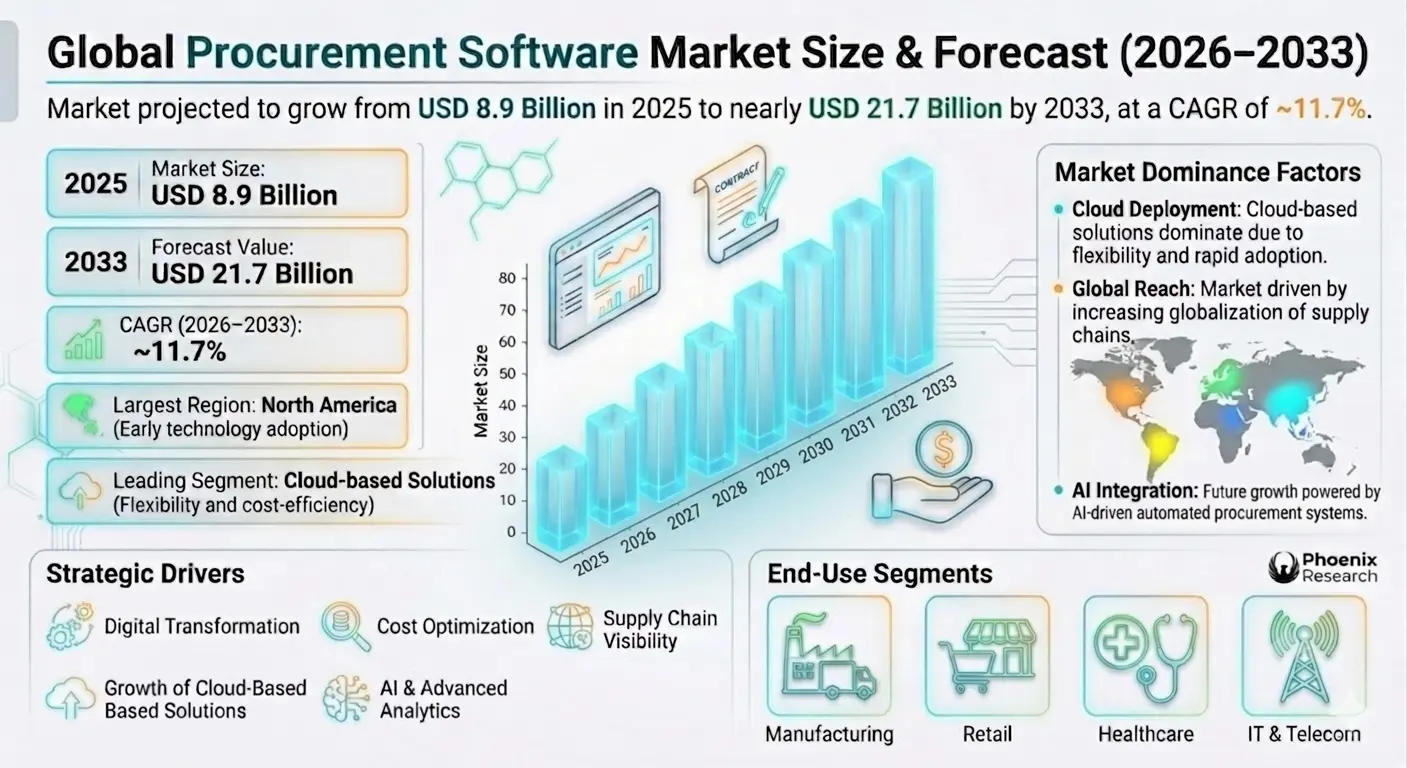

The global procurement software market is projected to witness strong and sustained growth during the forecast period from 2026 to 2033. The market was valued at approximately USD 8.9 billion in 2025 and is expected to reach nearly USD 21.7 billion by 2033, expanding at a CAGR of around 11.7%. This growth is driven by increasing digital transformation in enterprise procurement processes, rising demand for cost optimization, and growing adoption of cloud-based enterprise solutions across industries. Procurement software enables organizations to automate and manage sourcing, purchasing, supplier management, contract lifecycle management, spend analysis, and compliance processes. It plays a critical role in improving operational efficiency, reducing procurement costs, enhancing supplier relationships, and ensuring transparency across the procurement lifecycle. The market is experiencing rapid adoption of AI-powered procurement platforms, predictive analytics, and automation tools that streamline decision-making and reduce manual intervention. Organizations are increasingly shifting from traditional procurement systems to integrated digital procurement ecosystems. Additionally, globalization of supply chains, increasing supplier complexity, and the need for real-time visibility into procurement operations are accelerating the deployment of advanced procurement software solutions across enterprises of all sizes.Global Procurement Software Market Overview

The procurement software market is a key segment of the broader enterprise software and digital transformation ecosystem. It includes solutions designed to manage end-to-end procurement activities such as e-sourcing, e-procurement, supplier relationship management (SRM), contract management, and spend analytics. The market is highly dynamic, driven by the increasing need for operational efficiency and compliance in procurement functions. Organizations across manufacturing, retail, healthcare, IT & telecom, BFSI, and government sectors are rapidly adopting procurement software to enhance transparency and control over spending. Key industry participants include SAP Ariba, Oracle, Coupa Software, Jaggaer, GEP, Ivalua, Basware, Zycus, and other emerging SaaS-based procurement solution providers. These companies are focusing on AI integration, cloud migration, and modular procurement platforms to enhance scalability and usability. The shift toward cloud-based procurement platforms is significantly transforming the market landscape, enabling real-time collaboration, remote accessibility, and seamless integration with ERP and financial systems.Key Drivers of Global Procurement Software Market Growth

Digital Transformation of Procurement Processes

Enterprises are increasingly digitizing procurement operations to improve efficiency, reduce costs, and eliminate manual processes through automation and intelligent workflows.Rising Demand for Cost Optimization

Organizations are under pressure to reduce procurement costs and improve supplier negotiations, driving adoption of analytics-driven procurement platforms.Growth of Cloud-Based Solutions

Cloud deployment models are gaining traction due to scalability, lower upfront costs, and ease of integration with existing enterprise systems.Increasing Supply Chain Complexity

Global supply chain disruptions and supplier diversification strategies are increasing the need for real-time procurement visibility and supplier management tools.Adoption of AI and Advanced Analytics

AI-powered procurement software enables predictive insights, automated sourcing decisions, and improved contract management efficiency.Global Procurement Software Market Segmentation

By Component

The market is segmented into software and services. Software dominates the market due to high adoption of procurement platforms, while services include implementation, consulting, and support.By Deployment Mode

The market includes cloud-based and on-premise solutions. Cloud-based procurement software is witnessing rapid growth due to flexibility, scalability, and cost-effectiveness.By Organization Size

The market is segmented into large enterprises and small & medium enterprises (SMEs). Large enterprises account for the largest share due to complex procurement requirements.By Application

Applications include sourcing, supplier management, contract lifecycle management, spend analysis, e-procurement, and procurement analytics. Spend analysis and supplier management are key growth areas.By End User

End users include manufacturing, retail, healthcare, IT & telecom, BFSI, government, and energy & utilities. Manufacturing and retail sectors dominate due to large-scale procurement needs.Regional Market Dynamics

North America leads the global procurement software market due to early adoption of digital technologies, strong presence of major vendors, and high enterprise IT spending in the United States and Canada. Europe shows steady growth driven by regulatory compliance requirements, supply chain transparency initiatives, and increasing cloud adoption across industries. Asia-Pacific is the fastest-growing region due to rapid industrialization, digital transformation initiatives, and expanding enterprise IT infrastructure in China, India, Japan, and Southeast Asia. Latin America is witnessing moderate growth with increasing adoption of cloud-based enterprise solutions and supply chain modernization efforts. Middle East & Africa is emerging as a developing market supported by government digitalization initiatives and growing enterprise software investments.Competitive Landscape

The global procurement software market is highly competitive and dominated by established enterprise software vendors and emerging SaaS providers. Key players include SAP Ariba, Oracle Corporation, Coupa Software, Jaggaer, GEP, Ivalua, Basware, Zycus, and Tradeshift. Companies are focusing on AI integration, predictive analytics, automation, and end-to-end procurement platform development to strengthen market positioning. Strategic acquisitions and partnerships are common as vendors aim to expand product capabilities and geographic reach. SAP Ariba and Oracle lead in enterprise-scale procurement solutions, while Coupa Software is known for its user-friendly cloud-based spend management platform. Emerging players are focusing on niche procurement solutions and industry-specific offerings. Competition is driven by innovation, system integration capabilities, ease of use, and the ability to deliver measurable cost savings for enterprises.Strategic Outlook

The strategic outlook for the procurement software market remains highly positive, driven by accelerating enterprise digital transformation and increasing focus on supply chain resilience. Procurement is evolving from a transactional function to a strategic business driver. Future growth opportunities include AI-driven autonomous procurement systems, blockchain-enabled supplier verification, and advanced predictive analytics for demand forecasting and risk management. Integration with ERP systems, financial platforms, and supply chain management tools will continue to enhance procurement software value propositions. Vendors that offer unified, intelligent, and scalable procurement ecosystems are expected to lead the market.Final Market Perspective

The global procurement software market is undergoing a significant transformation, shifting from traditional procurement systems to intelligent, cloud-based, and data-driven platforms. This evolution is improving operational efficiency, transparency, and cost control across enterprises worldwide. As organizations increasingly prioritize digital supply chain management and procurement optimization, demand for advanced procurement software solutions will continue to grow. Companies that invest in AI, automation, and integrated procurement ecosystems will remain highly competitive in the evolving global market.Table of Contents

Table of Contents

- 1. Executive Summary

- 1.1 Global Procurement Software Market Snapshot (2026-2033)

- 1.2 Market Size & CAGR Analysis

- 1.3 Largest & Fastest-Growing Segments

- 1.4 Key Regional Insights

- 1.5 Major Market Growth Drivers

- 1.6 Competitive Landscape Overview

- 1.7 Strategic Outlook Through 2033

- 2. Introduction & Market Overview

- 2.1 Definition of Procurement Software

- 2.2 Scope of the Study

- 2.3 Evolution of Procurement Digitalization

- 2.4 Procurement Software Value Chain & Ecosystem

- 2.5 Procurement Function Transformation in Enterprises

- 2.6 Compliance, Risk & Governance Landscape

- 2.7 AI, Automation & Cloud Transformation Trends

- 3. Research Methodology

- 3.1 Primary Research

- 3.2 Secondary Research

- 3.3 Market Size Estimation Model

- 3.4 Forecast Assumptions (2026-2033)

- 3.5 Data Validation & Market Triangulation

- 4. Market Dynamics

- 4.1 Drivers

- 4.1.1 Digital Transformation of Procurement Processes

- 4.1.2 Rising Demand for Cost Optimization

- 4.1.3 Growth of Cloud-Based Enterprise Solutions

- 4.1.4 Increasing Supply Chain Complexity

- 4.1.5 Adoption of AI & Advanced Analytics

- 4.2 Restraints

- 4.2.1 High Implementation & Integration Costs

- 4.2.2 Data Security & Compliance Concerns

- 4.2.3 Resistance to Digital Adoption in SMEs

- 4.2.4 Legacy System Integration Challenges

- 4.3 Opportunities

- 4.3.1 AI-Driven Autonomous Procurement Systems

- 4.3.2 Blockchain-Based Supplier Verification

- 4.3.3 Predictive Spend Analytics Expansion

- 4.3.4 Integrated ERP & Procurement Ecosystems

- 4.4 Challenges

- 4.4.1 Vendor Lock-in Risks

- 4.4.2 Data Migration Complexity

- 4.4.3 Cybersecurity Threats

- 4.4.4 Standardization Across Global Enterprises

- 4.1 Drivers

- 5. Global Procurement Software Market Analysis (USD Billion), 2026-2033

- 5.1 Market Size Overview

- 5.2 CAGR Analysis

- 5.3 Regional Revenue Distribution

- 5.4 Segment Revenue Analysis

- 5.5 Cloud vs On-Premise Adoption Trends

- 5.6 Enterprise Digital Procurement Trends

- 6. Market Segmentation (USD Billion), 2026-2033

- 6.1 By Component

- 6.1.1 Software

- 6.1.2 Services (Implementation, Consulting & Support)

- 6.2 By Deployment Mode

- 6.2.1 Cloud-Based Solutions

- 6.2.2 On-Premise Solutions

- 6.3 By Organization Size

- 6.3.1 Large Enterprises

- 6.3.2 Small & Medium Enterprises (SMEs)

- 6.4 By Application

- 6.4.1 Sourcing

- 6.4.2 Supplier Management

- 6.4.3 Contract Lifecycle Management

- 6.4.4 Spend Analysis

- 6.4.5 E-Procurement

- 6.4.6 Procurement Analytics

- 6.5 By End User

- 6.5.1 Manufacturing

- 6.5.2 Retail

- 6.5.3 Healthcare

- 6.5.4 IT & Telecom

- 6.5.5 BFSI

- 6.5.6 Government

- 6.5.7 Energy & Utilities

- 6.1 By Component

- 7. Market Segmentation by Geography

- 7.1 North America

- 7.2 Europe

- 7.3 Asia-Pacific

- 7.4 Latin America

- 7.5 Middle East & Africa

- 8. Competitive Landscape

- 8.1 Market Share Analysis

- 8.2 Vendor Positioning Matrix

- 8.3 Cloud Procurement Platform Benchmarking

- 8.4 Strategic Partnerships & Acquisitions

- 8.5 AI & Automation Capability Comparison

- 9. Company Profiles

- 9.1 SAP Ariba

- 9.2 Oracle Corporation

- 9.3 Coupa Software

- 9.4 Jaggaer

- 9.5 GEP

- 9.6 Ivalua

- 9.7 Basware

- 9.8 Zycus

- 9.9 Tradeshift

- 9.10 Emerging SaaS Procurement Providers

- 10. Strategic Intelligence & Procurement AI Insights

- 10.1 AI-Powered Spend Optimization Engines

- 10.2 Supplier Risk Intelligence Systems

- 10.3 Predictive Procurement Analytics

- 10.4 Automated Contract Lifecycle Intelligence

- 10.5 ERP Integration & Digital Procurement Ecosystems

- 11. Future Outlook & Strategic Recommendations

- 11.1 Expansion of Autonomous Procurement Systems

- 11.2 Growth of Fully Integrated Digital Supply Chains

- 11.3 AI-Driven Decision-Making in Procurement

- 11.4 Blockchain Adoption in Supplier Management

- 11.5 Long-Term Market Outlook (2033+)

- 12. Appendix

- 13. About Pheonix Research

- 14. Disclaimer

Competitive Landscape

Global Procurement Software Market Competitive Intensity & Market Structure Overview

The Global Procurement Software Market is characterized by intense competition, rapid technological innovation, and increasing consolidation among enterprise software providers. The market operates within the broader enterprise digital transformation ecosystem, where procurement is evolving from a transactional operational function into a strategic, data-driven business capability.

Competitive intensity is high due to rising enterprise demand for cloud-based procurement platforms, AI-powered sourcing tools, spend optimization systems, and supplier management solutions. Vendors are aggressively competing through product innovation, AI integration, automation capabilities, ERP interoperability, and advanced analytics functionalities.

The market structure is moderately consolidated, with global enterprise software leaders controlling a significant share of large enterprise deployments, while emerging SaaS providers and niche procurement technology firms compete through specialized offerings, flexible pricing models, and industry-specific procurement solutions.

Global Procurement Software Market Competitive Intensity & Market Structure Current Scenario

Leading Procurement Software Providers

SAP Ariba: Global leader in enterprise procurement and supply chain collaboration platforms with strong integration capabilities across ERP ecosystems.

Oracle Corporation: Major enterprise procurement software provider offering cloud-based sourcing, supplier management, and procurement automation solutions.

Coupa Software: Leading cloud-native spend management platform focused on AI-driven procurement optimization and user-friendly procurement workflows.

Jaggaer: Specialized procurement software company with strong capabilities in strategic sourcing, contract management, and supplier lifecycle management.

Ivalua: Known for flexible and configurable procurement platforms supporting complex global procurement operations and supplier ecosystems.

GEP: Provider of AI-powered procurement and supply chain solutions with strong consulting and managed procurement services integration.

Basware: Focused on e-invoicing, procure-to-pay automation, and financial process integration across enterprise procurement systems.

Zycus: AI-driven procurement software provider emphasizing cognitive procurement, spend analysis, and autonomous sourcing technologies.

Tradeshift: Cloud-based procurement and supply chain platform enabling digital supplier collaboration and B2B commerce integration.

Emerging SaaS Procurement Vendors: Numerous startups and mid-sized providers are gaining traction through modular procurement platforms, low-code automation, and industry-focused procurement applications.

Key Competitive Intensity & Market Structure Signals in Global Procurement Software Market

One of the strongest competitive signals is the accelerating transition toward AI-powered procurement ecosystems. Vendors are increasingly embedding machine learning, predictive analytics, and intelligent automation into sourcing, supplier evaluation, spend management, and contract lifecycle management processes.

Cloud migration continues to reshape the competitive landscape, with enterprises rapidly replacing legacy on-premise procurement systems with scalable SaaS-based procurement platforms that support remote accessibility and real-time collaboration.

Another major market signal is the increasing importance of supplier risk management and supply chain resilience. Procurement software vendors are expanding capabilities around supplier monitoring, ESG compliance tracking, and real-time procurement visibility in response to global supply chain disruptions.

ERP integration capability has become a critical competitive differentiator. Vendors offering seamless interoperability with financial systems, inventory management platforms, and enterprise resource planning software are gaining stronger enterprise adoption.

Digital procurement marketplaces and supplier collaboration networks are also expanding rapidly, creating new competitive dynamics where procurement platforms increasingly function as interconnected business ecosystems rather than standalone software tools.

Strategic Implications of Competitive Intensity & Market Structure in Global Procurement Software Market

Procurement software providers are increasingly shifting from standalone procurement applications toward unified source-to-pay ecosystems that combine sourcing, purchasing, supplier management, invoicing, analytics, and compliance within a single platform architecture.

Artificial intelligence and automation investment are becoming essential strategic priorities, as enterprises seek autonomous procurement systems capable of reducing manual intervention, improving forecasting accuracy, and optimizing supplier negotiations.

Strategic acquisitions and partnerships are intensifying across the market as larger enterprise software providers acquire niche procurement technology firms to strengthen AI capabilities, expand geographic presence, and enhance vertical specialization.

Customer retention strategies are increasingly centered around platform scalability, ease of implementation, and measurable procurement cost savings. Vendors capable of delivering rapid ROI and seamless user experience are gaining competitive advantage.

Cybersecurity, data privacy, and regulatory compliance are becoming increasingly important strategic considerations as procurement systems handle large volumes of supplier, contract, and financial transaction data across global enterprise networks.

Global Procurement Software Market Competitive Intensity & Market Structure Forward Outlook

The Global Procurement Software Market is expected to become increasingly intelligent, automated, and ecosystem-driven over the forecast period. Future competition will focus heavily on AI-enabled autonomous procurement systems capable of predictive sourcing, dynamic supplier selection, and real-time spend optimization.

Blockchain-based procurement verification systems, ESG-focused supplier analytics, and digital procurement marketplaces are expected to reshape procurement operations and create new competitive opportunities for software providers.

Cloud-native procurement platforms will continue dominating future deployments as enterprises prioritize scalability, remote accessibility, and rapid system integration across global operations.

Asia-Pacific is expected to witness the fastest competitive expansion due to rapid enterprise digitalization, growing cloud adoption, and increasing procurement modernization initiatives across manufacturing, retail, and technology sectors.

Overall, the market will remain highly competitive and innovation-driven, with success increasingly dependent on AI capabilities, interoperability, automation efficiency, and the ability to deliver integrated procurement intelligence across enterprise supply chains. Vendors that successfully combine advanced analytics, intelligent automation, and scalable cloud ecosystems will lead the Global Procurement Software Market through 2033.

Value Chain

Global Procurement Software Market Value Chain & Supply Chain Evolution Overview

The Global Procurement Software Market value chain is evolving rapidly as enterprises increasingly transition from traditional manual procurement operations toward highly automated, cloud-based, AI-driven, and integrated digital procurement ecosystems. This transformation is being fueled by rising enterprise demand for procurement transparency, operational efficiency, supplier optimization, real-time spend visibility, and cost control across increasingly complex global supply chains. Procurement software is no longer viewed solely as a purchasing automation tool but as a strategic enterprise platform that enables organizations to improve sourcing efficiency, strengthen supplier relationships, minimize procurement risks, and support long-term business resilience through intelligent data-driven procurement management.

The procurement software ecosystem encompasses a wide range of interconnected solutions including e-sourcing platforms, supplier relationship management systems, contract lifecycle management tools, spend analytics software, procurement automation systems, invoice management platforms, and AI-powered procurement intelligence solutions. Enterprises across manufacturing, retail, healthcare, BFSI, IT & telecom, government, and energy sectors are increasingly integrating procurement software into broader enterprise digital transformation initiatives to streamline procurement workflows, eliminate manual inefficiencies, and improve compliance monitoring across supplier networks and procurement operations.

The market value chain extends far beyond software development and deployment into a highly interconnected ecosystem involving cloud infrastructure providers, enterprise resource planning (ERP) vendors, AI and analytics technology providers, cybersecurity firms, implementation consultants, procurement service providers, and supply chain integration specialists. Major procurement software companies including SAP Ariba, Oracle, Coupa Software, Jaggaer, GEP, Ivalua, Basware, and Zycus are continuously investing in AI-enabled procurement automation, predictive analytics, intelligent supplier management systems, and cloud-native procurement platforms in order to strengthen scalability, interoperability, and user experience across enterprise procurement environments.

Upstream supply chain operations increasingly depend on cloud computing infrastructure, advanced cybersecurity systems, API integration technologies, enterprise databases, machine learning algorithms, digital workflow automation tools, and real-time analytics engines that enable procurement software platforms to operate efficiently across global enterprise environments. Procurement software vendors are also strengthening collaboration with ERP providers, financial software companies, supply chain management platforms, and third-party procurement service firms to create highly integrated procurement ecosystems capable of supporting end-to-end enterprise procurement operations.

Operational strategies across the procurement software value chain increasingly focus on automation, scalability, AI integration, supplier collaboration, regulatory compliance, user experience optimization, and real-time procurement intelligence. Organizations are prioritizing intelligent procurement systems capable of automating sourcing decisions, monitoring supplier performance, managing contracts digitally, and delivering predictive spend analytics that improve procurement efficiency and strategic decision-making. However, despite strong technological progress, the market continues to face challenges related to data security, integration complexity, legacy system compatibility, supplier onboarding difficulties, regulatory compliance requirements, and increasing cybersecurity risks associated with cloud-based procurement environments.

Global Procurement Software Market Value Chain & Supply Chain Evolution Current Scenario

The current procurement software ecosystem is being shaped by accelerating enterprise digital transformation initiatives, growing adoption of cloud-based procurement platforms, increasing supplier network complexity, and rising demand for procurement visibility across global supply chains. Enterprises are increasingly replacing fragmented procurement processes and legacy purchasing systems with unified digital procurement platforms capable of delivering centralized control, real-time analytics, automated workflows, and enhanced supplier collaboration capabilities.

Procurement software vendors across North America, Europe, and Asia-Pacific are aggressively investing in AI-powered procurement intelligence, low-code procurement automation platforms, predictive analytics engines, and integrated supplier management ecosystems designed to improve procurement agility and operational efficiency. Organizations are increasingly demanding procurement software solutions capable of integrating seamlessly with ERP systems, financial management tools, inventory systems, and broader enterprise digital infrastructure in order to create unified operational environments.

Cloud deployment models continue to dominate market expansion as enterprises prioritize scalability, flexibility, remote accessibility, and lower infrastructure costs. At the same time, procurement software providers are strengthening investments in cybersecurity frameworks, blockchain-enabled procurement traceability systems, and AI-assisted risk monitoring solutions to improve supplier transparency and procurement governance across increasingly globalized supplier networks.

Demand for automated sourcing, spend management, supplier risk assessment, contract lifecycle management, procurement analytics, and invoice automation continues to increase rapidly across industries facing rising procurement complexity and cost pressures. Additionally, organizations are increasingly leveraging AI-powered procurement assistants, conversational procurement interfaces, and predictive supplier analytics to improve procurement decision-making, reduce operational inefficiencies, and enhance procurement strategy execution.

Key Value Chain & Supply Chain Evolution Signals in Global Procurement Software Market

Several transformative trends are reshaping the global procurement software market value chain and significantly influencing long-term competitive dynamics across the enterprise procurement ecosystem. One of the most significant signals is the rapid acceleration of enterprise-wide digital procurement transformation initiatives aimed at reducing manual procurement inefficiencies, improving spend visibility, and enabling data-driven procurement strategies across global operations. Procurement functions are increasingly transitioning from administrative purchasing activities into strategic business operations supported by intelligent automation and predictive analytics capabilities.

Another major transformation signal is the growing adoption of artificial intelligence and machine learning technologies across procurement platforms. AI-powered procurement systems are enabling automated sourcing recommendations, predictive supplier risk analysis, intelligent contract management, fraud detection, and spend optimization capabilities that significantly improve procurement performance and operational decision-making efficiency. Enterprises are increasingly prioritizing procurement software platforms capable of delivering proactive insights rather than merely supporting transactional procurement functions.

The expansion of cloud-based procurement ecosystems is also playing a critical role in reshaping market dynamics by enabling real-time collaboration, multi-location procurement management, remote accessibility, and seamless enterprise integration. In parallel, rising supply chain disruptions, geopolitical uncertainty, and supplier diversification strategies are increasing enterprise demand for procurement visibility, supplier intelligence, and procurement risk management tools that strengthen operational resilience across global supplier networks.

Another important market signal is the increasing convergence between procurement software, supply chain management systems, ERP platforms, and financial technology solutions. Enterprises are seeking highly integrated procurement ecosystems capable of centralizing procurement operations, automating workflows, synchronizing supplier data, and improving financial transparency across end-to-end enterprise operations. This growing integration trend is accelerating strategic collaboration between procurement software vendors, ERP providers, cloud infrastructure companies, and enterprise automation technology firms.

Strategic Implications of Value Chain & Supply Chain Evolution in Global Procurement Software Market

Leading procurement software providers including SAP Ariba, Oracle, Coupa Software, Jaggaer, GEP, Ivalua, Basware, and Zycus are actively strengthening market positioning through AI integration, cloud-native procurement architecture development, strategic acquisitions, and expansion of intelligent procurement automation capabilities. Competitive differentiation increasingly depends on the ability to deliver scalable, interoperable, and user-friendly procurement ecosystems that improve procurement visibility, reduce operational costs, and enhance supplier collaboration across enterprise environments.

Procurement software companies capable of integrating advanced analytics, AI-driven procurement intelligence, predictive risk management tools, and seamless ERP interoperability are expected to capture premium growth opportunities as enterprises prioritize digital procurement modernization. Vendors are increasingly investing in modular procurement platforms, configurable automation systems, and industry-specific procurement solutions that address the unique procurement requirements of sectors such as manufacturing, healthcare, retail, BFSI, and government procurement operations.

Strategic partnerships between procurement software providers, cloud infrastructure companies, cybersecurity firms, ERP vendors, and supply chain technology providers are becoming increasingly important for improving platform scalability, strengthening data security, enhancing procurement automation capabilities, and expanding enterprise integration functionality. Long-term competitive success will increasingly depend on the ability to balance automation efficiency, procurement intelligence, cybersecurity compliance, supplier transparency, and operational flexibility across highly interconnected procurement ecosystems.

In addition, procurement software providers are increasingly focusing on sustainability monitoring, ESG-focused supplier management, ethical sourcing analytics, and carbon footprint tracking capabilities as enterprises face growing pressure to improve sustainability reporting and responsible procurement practices. This evolution is expected to further expand the strategic role of procurement software within broader enterprise governance and sustainability initiatives.

Global Procurement Software Market Value Chain & Supply Chain Evolution Forward Outlook

Between 2026 and 2033, the procurement software value chain is expected to become significantly more intelligent, autonomous, AI-driven, and deeply integrated with broader enterprise digital ecosystems. Procurement operations will increasingly rely on AI-powered sourcing systems, predictive supplier analytics, autonomous procurement workflows, blockchain-enabled supplier verification frameworks, and intelligent procurement assistants capable of automating large portions of enterprise procurement decision-making processes.

Cloud-native procurement ecosystems are expected to dominate future market expansion as organizations continue prioritizing scalability, real-time collaboration, centralized procurement governance, and remote operational accessibility across geographically distributed enterprise environments. Procurement software platforms will increasingly incorporate advanced machine learning algorithms, natural language processing capabilities, and conversational AI interfaces that simplify procurement operations and improve user interaction across procurement teams.

Advanced technologies such as blockchain-based procurement traceability, digital supplier identity systems, AI-driven procurement forecasting, robotic process automation, and predictive compliance management tools are expected to reshape the next generation of procurement ecosystems. Enterprises will increasingly prioritize intelligent procurement platforms capable of integrating procurement, finance, inventory management, supplier collaboration, and supply chain visibility into unified enterprise operational environments.

Sustainability-focused procurement analytics, ESG compliance monitoring, ethical sourcing transparency tools, and carbon emissions tracking systems are also expected to become mainstream components of future procurement software platforms as organizations strengthen environmental and governance reporting initiatives. At the same time, growing cybersecurity threats and increasing regulatory scrutiny surrounding enterprise procurement data will accelerate investment in advanced cybersecurity infrastructure, secure cloud architecture, and AI-driven fraud prevention systems.

Ultimately, the future procurement software value chain will evolve from standalone procurement management applications into fully integrated intelligent procurement ecosystems capable of delivering autonomous procurement operations, predictive enterprise intelligence, supplier ecosystem optimization, and real-time strategic procurement decision support across global enterprise environments.

Market-Specific Value Chain

- Software Development & Cloud Infrastructure: Procurement software architecture development, cloud hosting infrastructure, AI and analytics engines, cybersecurity systems, API integration frameworks, enterprise database management, and workflow automation technologies.

- Procurement Platform & Enterprise Integration: E-procurement platforms, supplier relationship management systems, contract lifecycle management software, spend analytics tools, ERP integration systems, and financial management connectivity solutions.

- Implementation & Procurement Process Automation: Software deployment, procurement workflow customization, supplier onboarding services, process digitization, procurement consulting, employee training, and operational integration support.

- Supplier Management & Procurement Operations: Supplier collaboration systems, sourcing automation, procurement execution platforms, contract compliance monitoring, invoice processing automation, and procurement performance tracking solutions.

- Analytics, AI & Risk Management: Predictive procurement analytics, AI-powered sourcing intelligence, supplier risk assessment, spend optimization, procurement forecasting, fraud detection systems, and compliance monitoring tools.

- Long-Term Procurement Intelligence & Ecosystem Optimization: Autonomous procurement systems, ESG procurement analytics, blockchain supplier verification, procurement strategy optimization, sustainability monitoring, and continuous procurement performance improvement solutions.

Company-to-Stage Mapping

- Software Development & Cloud Infrastructure: Microsoft Azure, Amazon Web Services (AWS), Google Cloud, Oracle Cloud Infrastructure, cybersecurity solution providers.

- Procurement Platform & Enterprise Integration: SAP Ariba, Oracle, Coupa Software, Jaggaer, Ivalua, Basware, Zycus.

- Implementation & Procurement Process Automation: Accenture, Deloitte, IBM Consulting, Capgemini, Infosys, Tata Consultancy Services (TCS).

- Supplier Management & Procurement Operations: GEP, Tradeshift, Jaggaer, Coupa Software, SAP Ariba supplier network solutions.

- Analytics, AI & Risk Management: Coupa AI, Zycus Merlin AI, IBM Watson procurement solutions, SAP analytics systems, Oracle AI procurement tools.

- Long-Term Procurement Intelligence & Ecosystem Optimization: AI procurement automation firms, blockchain procurement technology providers, ESG analytics companies, enterprise procurement intelligence platforms.

Investment Activity

Global Procurement Software Market Investment & Funding Dynamics Overview

Investment and funding activity in the Global Procurement Software Market is witnessing strong acceleration due to the rapid digital transformation of enterprise procurement functions, rising demand for cost optimization tools, and the shift toward cloud-based business applications. Between 2026 and 2033, capital inflows are expected to increase significantly as organizations prioritize intelligent procurement ecosystems that integrate automation, analytics, and AI-driven decision-making capabilities.

A major portion of investments is being directed toward SaaS-based procurement platforms, AI-powered sourcing tools, supplier risk management systems, and end-to-end procurement suites that offer real-time visibility across enterprise spending. Venture capital firms, private equity investors, and strategic corporate investors are actively funding procurement technology startups that demonstrate strong scalability, modular architecture, and enterprise integration capabilities.

Large enterprise software providers such as SAP, Oracle, Coupa, Jaggaer, GEP, Ivalua, Basware, and Zycus are significantly increasing R&D investments to strengthen cloud infrastructure, enhance AI and machine learning capabilities, and expand product ecosystems. These investments are also focused on improving predictive analytics, autonomous procurement workflows, and advanced contract lifecycle intelligence systems.

Global Procurement Software Market Investment & Funding Dynamics Current Scenario

The current investment environment is strongly influenced by the growing need for supply chain resilience, procurement transparency, and cost efficiency across industries such as manufacturing, retail, healthcare, BFSI, IT & telecom, and government sectors. Enterprises are increasingly allocating IT budgets toward procurement modernization projects that replace legacy systems with cloud-native, AI-enabled platforms.

- North America: Leads global investment activity due to high enterprise software adoption, strong presence of major vendors, and significant venture capital funding for SaaS procurement startups.

- Europe: Attracts steady investments driven by regulatory compliance requirements, sustainability-focused procurement initiatives, and increasing cloud transformation programs across enterprises.

- Asia-Pacific: Emerging as a high-growth investment hub supported by rapid digitalization, expanding SME adoption of procurement software, and increasing foreign direct investment in enterprise IT infrastructure.

- Middle East & Africa: Witnessing rising investments driven by government-led digital transformation initiatives and increasing adoption of enterprise procurement platforms in large infrastructure and energy projects.

- Latin America: Experiencing gradual investment growth supported by cloud adoption trends and modernization of procurement processes in retail, manufacturing, and public sector organizations.

Key Investment & Funding Dynamics Signals in Global Procurement Software Market

- Strong venture capital inflows into AI-driven procurement startups focusing on automation, predictive analytics, and supplier intelligence platforms.

- Increased corporate investments in cloud migration projects aimed at replacing legacy procurement systems with integrated SaaS platforms.

- Growing private equity interest in mature procurement software companies with recurring revenue models and strong enterprise client bases.

- Rising funding for AI and machine learning integration to enhance procurement decision-making, spend visibility, and contract optimization.

- Expansion of strategic partnerships between software vendors and consulting firms to accelerate enterprise procurement digital transformation programs.

Strategic Implications of Investment & Funding Dynamics in Global Procurement Software Market

- The market strongly favors cloud-native SaaS providers offering scalable, modular, and AI-enabled procurement platforms.

- Companies with advanced data analytics, automation capabilities, and ERP integration features are attracting higher valuations and investor interest.

- Strategic acquisitions are increasing as large enterprise software firms acquire niche procurement technology startups to expand product portfolios.

- Investment strategies are shifting toward platforms that deliver measurable ROI through cost reduction, supplier optimization, and procurement efficiency gains.

- Geographic expansion strategies are becoming a key focus area, with vendors investing in regional data centers, localized solutions, and compliance-ready platforms.

Global Procurement Software Market Investment & Funding Dynamics Forward Outlook

Looking ahead, investment activity in the Global Procurement Software Market is expected to remain strong, supported by increasing enterprise digitization, expansion of global supply chains, and rising demand for intelligent procurement ecosystems. Funding will continue to prioritize AI-driven procurement automation, predictive sourcing technologies, and real-time spend analytics platforms.

Future capital allocation will increasingly focus on autonomous procurement systems, blockchain-based supplier verification solutions, advanced contract intelligence platforms, and integrated enterprise resource planning ecosystems that unify procurement, finance, and supply chain operations.

- North America: Will continue to dominate investments due to strong SaaS ecosystem maturity and high enterprise IT spending.

- Asia-Pacific: Will witness the fastest investment growth driven by rapid digital transformation and expanding enterprise software adoption.

- Europe: Will maintain steady investment momentum supported by compliance-driven procurement modernization initiatives.

Sustainability and ESG-focused procurement solutions are also expected to attract increasing investment interest, as enterprises prioritize responsible sourcing, carbon tracking, and ethical supply chain management.

Overall, the market is expected to remain highly attractive for investors due to its recurring revenue models, strong enterprise demand, and deep integration into global business operations. Companies that successfully combine AI innovation, cloud scalability, and enterprise-grade security will continue to attract the strongest funding and valuation growth through 2033.

Technology & Innovation

Global Procurement Software Market Technology & Innovation Landscape Overview

The technology and innovation landscape of the Global Procurement Software Market is rapidly evolving as enterprises increasingly transition from traditional procurement systems to intelligent, cloud-based, and AI-driven procurement ecosystems. Modern procurement platforms are integrating advanced capabilities such as artificial intelligence, machine learning, predictive analytics, robotic process automation (RPA), blockchain-based verification, and real-time supplier intelligence to enhance decision-making, improve transparency, and optimize end-to-end procurement operations.

Digital transformation is fundamentally reshaping procurement functions across industries. Organizations are adopting unified procurement platforms that consolidate sourcing, supplier management, contract lifecycle management, spend analysis, and compliance tracking into a single integrated system. This shift is enabling greater operational efficiency, reduced procurement cycle times, and improved cost control across enterprise procurement departments.

Artificial intelligence and machine learning are becoming central to procurement innovation. AI-powered systems are being used for intelligent supplier selection, predictive spend forecasting, risk assessment, and automated purchasing decisions. These technologies help enterprises identify cost-saving opportunities, anticipate supply chain disruptions, and improve procurement strategy through data-driven insights.

Automation technologies such as robotic process automation are also playing a key role in eliminating manual procurement tasks. RPA tools are being deployed to automate invoice processing, purchase order creation, contract management workflows, and compliance reporting. This reduces human error, improves processing speed, and enhances overall procurement efficiency.

The integration of cloud computing is another major innovation driver in the procurement software market. Cloud-based procurement platforms offer scalability, real-time collaboration, remote accessibility, and seamless integration with ERP and financial systems. These capabilities are enabling enterprises to modernize procurement operations and support global, multi-location supply chains more effectively.

In addition, blockchain technology is emerging as a promising innovation in procurement ecosystems. It is being used to enhance supplier verification, ensure contract authenticity, improve traceability in procurement transactions, and strengthen data security across multi-party supply chain networks.

Global Procurement Software Market Technology & Innovation Landscape Current Scenario

Currently, the global procurement software market is witnessing strong adoption of AI-enabled procurement platforms and cloud-based enterprise solutions across large organizations and SMEs. Leading vendors such as SAP Ariba, Oracle, Coupa, Jaggaer, GEP, Ivalua, Basware, and Zycus are continuously enhancing their platforms with advanced analytics, automation features, and integrated procurement intelligence capabilities.

Enterprises are increasingly shifting away from legacy procurement systems toward integrated digital procurement ecosystems that offer real-time visibility into spending patterns, supplier performance, and contract compliance. This transition is improving procurement transparency and enabling better financial governance across organizations.

Spend analytics tools are widely being adopted to identify cost-saving opportunities and optimize procurement budgets. These tools analyze historical and real-time procurement data to provide actionable insights on supplier pricing, category spend behavior, and procurement inefficiencies.

Supplier relationship management platforms are also gaining traction, enabling organizations to evaluate supplier performance, manage risks, and strengthen collaboration across global supply chains. These systems are particularly important in industries with complex and multi-tier supplier networks such as manufacturing, retail, and healthcare.

Additionally, AI-driven contract lifecycle management solutions are improving contract creation, negotiation, compliance monitoring, and renewal processes. These tools are reducing legal risks and ensuring better enforcement of procurement agreements.

Cloud-native procurement platforms are now the dominant deployment model, offering enterprises flexibility, faster implementation, and seamless integration with other enterprise software systems such as ERP, CRM, and financial management tools.

Key Technology & Innovation Trends in Global Procurement Software Market

- AI-Powered Procurement Analytics: Machine learning systems enabling predictive spending insights, supplier evaluation, and risk forecasting.

- Robotic Process Automation (RPA): Automation of repetitive procurement tasks such as invoicing, purchase orders, and compliance workflows.

- Cloud-Based Procurement Platforms: Scalable and integrated procurement ecosystems enabling real-time collaboration and global accessibility.

- Blockchain for Supplier Verification: Secure digital frameworks ensuring transparency, traceability, and authenticity in procurement transactions.

- Autonomous Procurement Systems: AI-driven systems capable of automating sourcing decisions and purchase approvals with minimal human intervention.

- Advanced Spend Analytics: Real-time analysis tools for optimizing procurement budgets and identifying cost-saving opportunities.

- Integrated ERP Procurement Solutions: Seamless connectivity between procurement platforms and enterprise resource planning systems.

- Supplier Risk Management Technologies: Tools assessing financial, operational, and geopolitical risks across supplier networks.

- Digital Contract Lifecycle Management: AI-enabled systems improving contract creation, monitoring, and compliance enforcement.

- Predictive Supply Chain Intelligence: Data-driven platforms forecasting procurement needs and supply chain disruptions.

Strategic Implications of Technology & Innovation

Technological innovation is fundamentally transforming procurement from a transactional function into a strategic enterprise capability. AI, automation, and cloud technologies are enabling organizations to shift toward proactive procurement strategies that focus on cost optimization, supplier resilience, and data-driven decision-making.

For enterprises, the adoption of intelligent procurement platforms is improving operational efficiency, reducing procurement cycle times, and enhancing financial transparency. Organizations leveraging advanced analytics and automation tools are achieving stronger control over spending and improved supplier performance management.

The increasing use of integrated procurement ecosystems is also enabling better cross-functional collaboration between procurement, finance, and supply chain teams. This integration is helping organizations align procurement strategies with broader business objectives and improve overall enterprise performance.

At the same time, AI-driven insights are allowing procurement leaders to anticipate market fluctuations, mitigate supply chain risks, and identify strategic sourcing opportunities. This is particularly important in a global environment characterized by supply chain disruptions and rising cost pressures.

However, challenges such as data security risks, system integration complexities, high implementation costs, and resistance to digital transformation continue to impact market adoption. Organizations must invest in secure cloud infrastructure, employee training, and scalable procurement architectures to maximize ROI from digital procurement solutions.

Global Procurement Software Market Technology & Innovation Forward Outlook

Looking ahead, the global procurement software market is expected to evolve into a highly intelligent, autonomous, and fully integrated digital ecosystem. AI-driven autonomous procurement systems will increasingly handle sourcing decisions, supplier selection, and contract execution with minimal human involvement.

The convergence of AI, blockchain, and advanced analytics will further enhance transparency, security, and efficiency across global procurement networks. Blockchain-enabled procurement systems will play a larger role in supplier verification, fraud prevention, and contract authenticity management.

Predictive procurement platforms will become more advanced, enabling organizations to forecast demand, anticipate supply disruptions, and optimize procurement strategies in real time. These systems will significantly improve supply chain resilience and business continuity.

The integration of procurement software with broader enterprise ecosystems, including ERP, finance, logistics, and supply chain platforms, will continue to expand. This will create unified digital business environments where procurement functions operate as fully integrated strategic components.

In conclusion, the Global Procurement Software Market is undergoing a major technological transformation driven by AI, automation, cloud computing, and advanced analytics. Organizations that adopt intelligent, scalable, and integrated procurement platforms will gain a strong competitive advantage in cost optimization, operational efficiency, and supply chain resilience.

Market Risk

Global Procurement Software Market Risk Factors & Disruption Threats Overview

The global procurement software market is experiencing rapid expansion driven by enterprise digital transformation, cloud adoption, and increasing demand for automated procurement workflows. However, despite strong growth fundamentals, the market is exposed to a range of structural, technological, operational, and regulatory risks that can significantly influence adoption patterns, vendor performance, and long-term market stability. As procurement systems become more deeply integrated into enterprise financial and supply chain ecosystems, any disruption in software performance, data integrity, or system connectivity can have cascading effects on organizational operations and decision-making processes.

One of the primary risk factors in the procurement software market is cybersecurity and data privacy exposure. Procurement platforms handle highly sensitive corporate data, including supplier contracts, pricing agreements, financial transactions, and strategic sourcing information. As cloud-based deployment becomes dominant, these systems become attractive targets for cyberattacks, ransomware incidents, data breaches, and unauthorized access. Any compromise in procurement data security can lead to financial losses, regulatory penalties, reputational damage, and breakdowns in supplier trust, making cybersecurity resilience a critical priority for vendors and enterprises alike.

Another major risk factor is system integration complexity across enterprise IT environments. Procurement software must integrate seamlessly with ERP systems, accounting platforms, supply chain management tools, and financial reporting systems. However, differences in legacy infrastructure, data formats, and vendor ecosystems often create integration challenges. Poor system interoperability can result in data inconsistencies, workflow inefficiencies, delayed procurement cycles, and reduced user adoption, particularly in large enterprises with complex operational structures.

Vendor dependency and platform lock-in risks also represent a significant concern in the procurement software market. Many enterprises rely heavily on a single procurement ecosystem provider for critical sourcing and contract management functions. This dependence can limit flexibility, increase switching costs, and reduce negotiating power over pricing and service terms. In cases where vendors experience operational outages, product limitations, or strategic shifts, enterprises may face disruptions in procurement continuity and supplier management processes.

Additionally, the rapid pace of technological change in AI, automation, and analytics introduces product obsolescence risk. Procurement software providers must continuously innovate to remain competitive, as enterprises increasingly demand advanced capabilities such as predictive analytics, autonomous procurement, and AI-driven decision-making. Vendors that fail to keep pace with innovation may lose market share to more agile competitors offering more advanced, integrated, and intelligent procurement solutions.

Global Procurement Software Market Risk Factors & Disruption Threats Current Scenario

The current market environment reflects strong enterprise demand for procurement automation, cost optimization, and supply chain transparency. However, organizations are simultaneously facing budget constraints, economic uncertainty, and heightened scrutiny over software investments, which can slow down procurement software adoption cycles. While large enterprises continue to invest in digital procurement platforms, small and medium-sized enterprises often face challenges related to implementation costs, training requirements, and change management complexities.

Cloud migration continues to reshape the procurement software landscape, but it also introduces operational risks related to uptime reliability, data sovereignty, and third-party cloud dependency. Enterprises increasingly rely on SaaS-based procurement platforms hosted on external infrastructure, which can create vulnerabilities during service outages, maintenance disruptions, or cloud provider failures. These risks are particularly critical for organizations operating in highly regulated industries such as BFSI, healthcare, and government sectors.

The competitive landscape is intensifying as established enterprise software vendors and emerging SaaS providers aggressively innovate to capture market share. This has led to pricing pressure, increased customer acquisition costs, and accelerated product differentiation cycles. While innovation benefits end users, it also increases pressure on vendors to continuously invest in research and development, potentially impacting profitability and long-term sustainability for smaller players.

Another key risk in the current scenario is the shortage of skilled professionals capable of implementing and managing advanced procurement systems. Enterprises often face difficulties in aligning procurement teams with digital tools, analytics platforms, and AI-driven systems. This skills gap can slow down digital transformation initiatives and reduce the overall return on investment from procurement software deployments.

In addition, global supply chain volatility continues to influence procurement software demand patterns. While disruptions increase demand for visibility and risk management tools, they also create uncertainty in enterprise budgets and procurement planning cycles. This dual impact results in fluctuating adoption rates across different industry verticals and geographic regions.

Global Procurement Software Market Key Risk Factors & Disruption Threat Signals

A major disruption signal is the rapid evolution of AI-driven autonomous procurement systems. These platforms are increasingly capable of automating sourcing decisions, supplier selection, and contract optimization with minimal human intervention. While this improves efficiency, it also raises concerns regarding algorithmic bias, decision transparency, and over-reliance on automated systems for critical procurement decisions.

Another significant trend is the increasing adoption of blockchain-based procurement and supplier verification systems. While blockchain offers enhanced transparency and traceability, its integration into existing procurement ecosystems remains complex and costly. Scalability limitations and interoperability challenges may slow widespread adoption despite its long-term potential.

The rise of hyper-integrated enterprise platforms combining ERP, supply chain management, and procurement functions is also reshaping market dynamics. While integration improves operational efficiency, it increases systemic risk, where failures in one module can impact the entire enterprise workflow. This interconnectedness amplifies the potential impact of software outages or configuration errors.

Regulatory compliance requirements are becoming increasingly stringent across global markets, particularly regarding data privacy, cross-border data transfer, and supplier transparency. Procurement software vendors must continuously adapt to evolving regulations such as GDPR-like frameworks and regional data governance laws. Non-compliance can result in penalties, legal challenges, and restricted market access.

Additionally, rising customer expectations for real-time analytics, intuitive user interfaces, and seamless mobile access are placing pressure on vendors to continuously enhance product usability. Failure to meet these expectations can lead to customer churn and reduced platform adoption rates, especially as competitors introduce more user-centric and AI-enhanced procurement solutions.

Global Procurement Software Market Strategic Implications of Risk Factors

To address increasing risk complexity, procurement software providers must prioritize cybersecurity enhancement, multi-layer data protection, and compliance-first architecture design. Strengthening encryption protocols, access controls, and continuous threat monitoring will be essential to maintaining enterprise trust and regulatory compliance in highly sensitive procurement environments.

Enterprises adopting procurement software should focus on robust integration strategies that minimize dependency on fragmented IT systems. Standardized APIs, modular architecture, and scalable cloud infrastructure will play a key role in reducing integration risks and improving system interoperability across enterprise ecosystems.

Vendors must also invest heavily in AI governance frameworks to ensure transparency, fairness, and accountability in automated procurement decisions. Establishing explainable AI models and audit-friendly decision systems will be critical for enterprise adoption in regulated industries and high-value procurement environments.

Additionally, companies should diversify product offerings to include modular procurement solutions that cater to both large enterprises and SMEs. This will reduce market concentration risk and improve resilience against cyclical enterprise spending patterns.

Strategic partnerships with ERP providers, cloud infrastructure companies, and supply chain technology vendors will further enhance ecosystem integration and improve market competitiveness. Collaboration will be a key enabler for delivering end-to-end procurement visibility and unified enterprise resource planning capabilities.

Global Procurement Software Market Forward Risk Outlook

Looking ahead, the procurement software market is expected to face increasing complexity driven by rapid technological evolution, regulatory tightening, and rising enterprise dependency on digital procurement ecosystems. While long-term growth prospects remain strong, short-term volatility may persist due to economic uncertainty and fluctuating enterprise IT spending cycles.

The future risk landscape will be shaped by AI autonomy, cybersecurity resilience, cloud dependency, and regulatory compliance pressures. Vendors that successfully balance innovation with security, scalability, and compliance will be best positioned to maintain leadership in an increasingly competitive market.

Overall, while the procurement software market continues to expand as a core component of enterprise digital transformation, sustainable growth will depend on the ability of stakeholders to manage operational risks, strengthen system resilience, and ensure secure, transparent, and intelligent procurement ecosystems across global industries.

Regulatory Landscape

Global Procurement Software Market Regulatory & Policy Environment Overview

The regulatory and policy environment governing the global procurement software market is evolving rapidly as governments, industry regulators, and data protection authorities place greater emphasis on digital governance, enterprise transparency, cybersecurity, and fair competition in enterprise software ecosystems. Procurement software operates at the intersection of financial data management, supplier ecosystems, and enterprise decision-making, making it subject to a wide range of regulatory frameworks related to data privacy, digital transactions, contract governance, and cross-border information flow.

As organizations increasingly digitize procurement functions, regulatory scrutiny has expanded to include cloud computing compliance, AI-based decision systems, supplier data handling, and automated contract lifecycle management. Governments across major economies are introducing stricter rules to ensure that procurement platforms maintain data integrity, prevent manipulation in supplier selection processes, and provide transparent audit trails for all procurement activities.

Additionally, global procurement software providers must comply with evolving cybersecurity standards and enterprise risk management regulations. These frameworks require strong encryption protocols, secure identity management, access control systems, and continuous monitoring of enterprise procurement data to prevent breaches, fraud, and unauthorized access across multi-tier supplier networks.

The increasing globalization of supply chains has further intensified the need for regulatory alignment across jurisdictions, particularly in areas such as cross-border data transfer, digital contracting standards, and cloud infrastructure compliance. This is especially important for multinational enterprises that rely on unified procurement platforms operating across multiple regulatory environments.

Global Procurement Software Market Regulatory & Policy Environment Current Scenario

The current regulatory landscape for procurement software is shaped by strong data protection laws, enterprise IT governance frameworks, and increasing oversight of AI-driven enterprise decision systems. Developed regions such as North America and Europe maintain strict compliance requirements under regulations such as GDPR, CCPA, and other data privacy laws that directly impact procurement data storage, processing, and sharing.

In Europe, procurement software providers must comply with GDPR requirements related to personal and corporate data handling, ensuring transparency in data usage, user consent management, and strict limitations on cross-border data transfers. Additionally, EU digital market regulations are influencing competition within enterprise software ecosystems, particularly regarding platform interoperability and fair access to digital procurement tools.

North America is focused on cybersecurity compliance, enterprise risk governance, and digital transaction security standards. Regulatory bodies are increasingly emphasizing supply chain resilience, vendor risk management, and software accountability in enterprise procurement systems, especially in sectors such as government, defense, and critical infrastructure.

In Asia-Pacific, regulatory frameworks are evolving quickly as countries modernize their digital economies. Governments are introducing cloud computing regulations, data localization requirements, and cybersecurity laws that directly affect procurement software deployment models and cross-border enterprise operations.

Emerging markets in Latin America, the Middle East, and Africa are gradually strengthening digital governance frameworks, focusing on enterprise software licensing, cybersecurity readiness, and digital trade compliance. These regions are also aligning their policies with international data protection and enterprise IT governance standards to attract global SaaS vendors and digital transformation investments.

Key Regulatory & Policy Environment Signals in Global Procurement Software Market

- Data Privacy & Protection Regulations: Strict enforcement of GDPR, CCPA, and similar frameworks governing enterprise procurement data collection, storage, and processing across cloud-based systems.

- Cybersecurity & Enterprise Risk Governance: Mandatory security standards requiring encryption, multi-factor authentication, access control, and continuous monitoring of procurement platforms.

- AI & Automated Decision-Making Compliance: Increasing scrutiny of AI-driven procurement decisions to ensure transparency, fairness, and accountability in supplier selection and contract management.

- Cloud Infrastructure & Data Residency Rules: Regulations requiring local data storage and compliance with regional cloud hosting standards for enterprise procurement systems.

- Digital Contracting & E-Procurement Standards: Legal frameworks governing electronic signatures, digital contracts, and audit trails for procurement transactions.

- Competition & Antitrust Regulations: Policies aimed at preventing monopolistic practices in enterprise software markets and ensuring fair competition among procurement solution providers.

Strategic Implications of Regulatory & Policy Environment

The evolving regulatory landscape is significantly influencing the architecture and deployment of procurement software solutions. Vendors are increasingly required to embed compliance-by-design principles into their platforms, ensuring that data protection, auditability, and security controls are integrated into core system functionalities rather than added as external layers.

Compliance requirements are also driving greater adoption of cloud security frameworks, zero-trust architectures, and advanced encryption technologies within procurement software ecosystems. This is increasing development costs but simultaneously improving system reliability, trust, and enterprise adoption rates.

AI governance regulations are reshaping how procurement platforms design predictive analytics, supplier scoring systems, and automated sourcing tools. Vendors are now required to ensure explainability in AI-driven decisions, particularly in procurement workflows involving high-value contracts and strategic supplier selection.

Global enterprises are also prioritizing procurement software solutions that offer multi-jurisdiction compliance capabilities, enabling seamless operations across regions with differing regulatory requirements. This is accelerating demand for flexible, modular, and scalable procurement platforms.

Global Procurement Software Market Regulatory & Policy Environment Forward Outlook

Between 2026 and 2033, the regulatory environment for procurement software is expected to become more stringent, technology-driven, and globally harmonized. Governments are likely to introduce more detailed frameworks governing AI usage in enterprise systems, cross-border data flows, and digital procurement transparency standards.

AI governance will play a central role in future regulations, with increased emphasis on explainable AI, bias mitigation, and accountability in automated procurement decisions. Procurement platforms will be required to provide clear audit trails and decision justification mechanisms for regulatory compliance.

Cybersecurity regulations are expected to intensify further, particularly in sectors handling sensitive procurement data such as defense, healthcare, and critical infrastructure. This will drive greater adoption of advanced threat detection, blockchain-based verification, and real-time monitoring systems.

Cloud computing regulations will continue to evolve, with more countries implementing data sovereignty laws and regional hosting requirements. This will influence how procurement software vendors design their infrastructure and deploy global SaaS solutions.

Overall, the regulatory and policy environment will play a critical role in shaping the future of the procurement software market. Vendors that prioritize compliance, transparency, AI governance, and cybersecurity resilience will be best positioned to succeed in an increasingly regulated global enterprise software ecosystem.