Global Cloud Service Market Report Size & Forecast 2026-2033

Global Cloud Service Market Report, Size, Share and Forecast 2026–2033

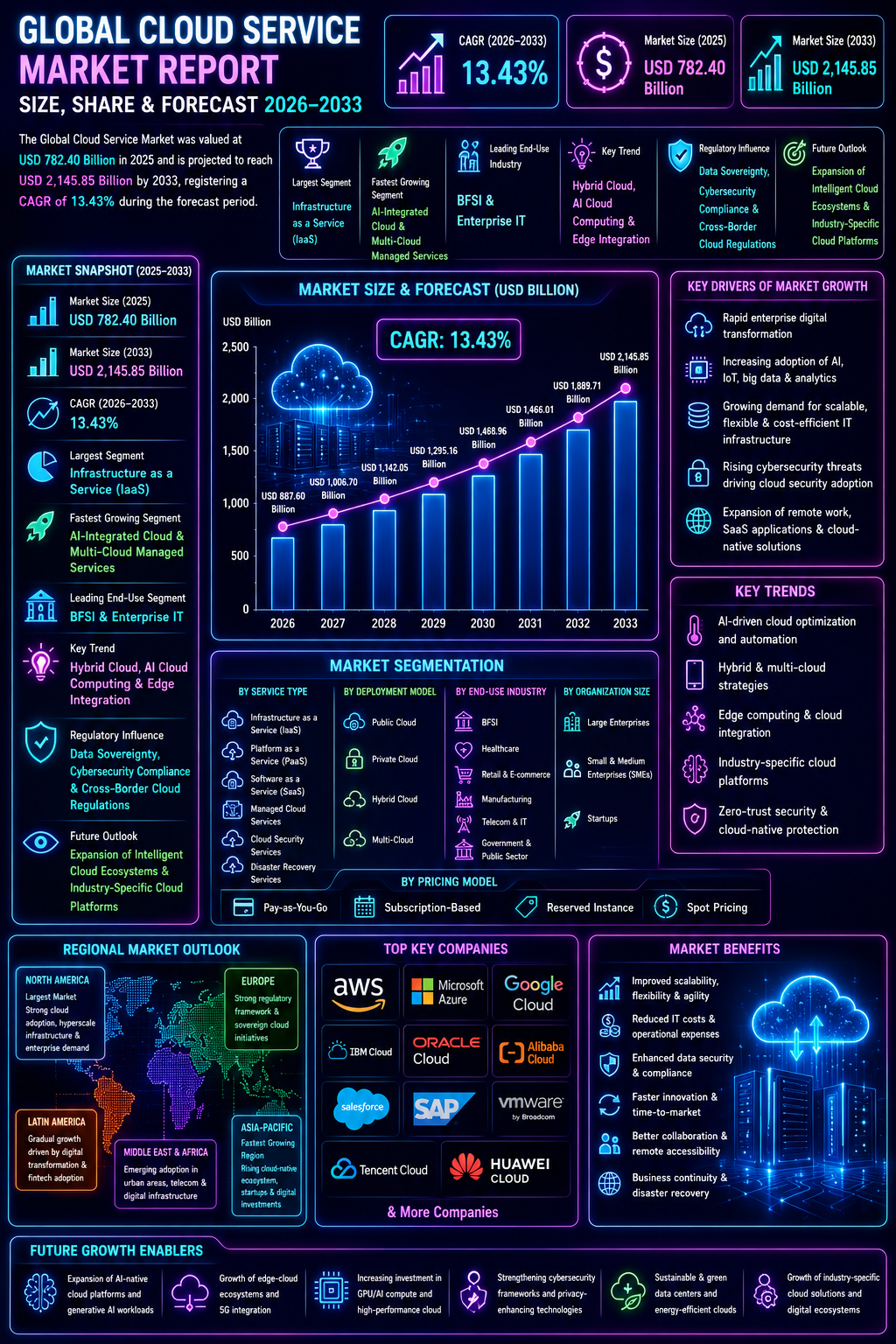

Market Forecast Snapshot (2025–2033)

| Metric | Value |

|---|---|

| Market Size (2025) | USD 782.40 Billion |

| Market Size (2033) | USD 2,145.85 Billion |

| CAGR (2026–2033) | 13.43% |

| Largest Segment | Infrastructure as a Service (IaaS) |

| Fastest Growing Segment | AI-Integrated Cloud & Multi-Cloud Managed Services |

| Leading End-Use Industry | BFSI & Enterprise IT |

| Key Trend | Hybrid Cloud, AI Cloud Computing & Edge Integration |

| Regulatory Influence | Data Sovereignty, Cybersecurity Compliance & Cross-Border Cloud Regulations |

| Future Outlook | Expansion of Intelligent Cloud Ecosystems & Industry-Specific Cloud Platforms |

Market Size & Forecast

The Global Cloud Service Market is expected to witness substantial expansion during the forecast period from 2026 to 2033. The market was valued at USD 782.40 billion in 2025 and is projected to reach approximately USD 2,145.85 billion by 2033, registering a CAGR of 13.43%. The market growth is primarily driven by rapid enterprise digital transformation, increasing adoption of SaaS applications, expansion of AI-driven workloads, rising hybrid cloud deployment, and growing data-intensive computing requirements. Cloud services are increasingly critical for data storage, infrastructure scalability, cybersecurity, analytics, remote collaboration, and application modernization. The adoption of AI, IoT, edge computing, big data, and serverless architecture is accelerating cloud demand across industries. In addition, strong growth in industry-specific cloud solutions, cloud-native applications, and global hyperscale infrastructure is supporting long-term market expansion.Global Cloud Service Market Overview

Cloud services refer to internet-based computing solutions that provide storage, networking, software, computing power, security, and application hosting without requiring physical on-premise infrastructure. The market includes Infrastructure as a Service (IaaS), Platform as a Service (PaaS), Software as a Service (SaaS), cloud security services, managed cloud solutions, disaster recovery services, and hybrid cloud ecosystems. Cloud services are widely used across BFSI, healthcare, retail, telecom, manufacturing, government, media, education, and enterprise IT environments. The market is shifting from standalone cloud deployment toward multi-cloud architecture, AI-optimized cloud workloads, cloud orchestration, edge-cloud integration, and industry-specific cloud platforms.Structural Drivers of Market Growth

1. Innovation and Commercialization Acceleration

Rapid innovation in AI cloud infrastructure, containerization, serverless computing, and Kubernetes-based orchestration is accelerating enterprise cloud migration. Cloud-native applications, automated scaling, and workload optimization are improving operational efficiency.Market Implications

Companies investing in AI-driven cloud platforms, edge computing, and cloud automation are expected to strengthen market leadership.2. Compliance and Risk Repricing

Global data privacy laws, cybersecurity regulations, data residency requirements, and cloud governance standards are reshaping cloud adoption. Organizations are increasingly prioritizing secure cloud architecture, encryption, zero-trust security, and compliance-ready platforms.Market Implications

Cloud providers offering compliant, secure, and geographically optimized cloud services are likely to gain stronger enterprise trust.3. Competitive and Value-Chain Reconfiguration

The cloud market is highly competitive as hyperscalers, managed-service providers, SaaS firms, and cybersecurity vendors expand ecosystems. Strategic partnerships, cloud marketplaces, API-led ecosystems, and managed services are altering value-chain economics.Market Implications

Companies focusing on vertical cloud specialization, AI services, and hybrid cloud integration may gain higher margins.4. Capital and Capacity Scaling

Rising investment in hyperscale data centers, edge nodes, AI compute clusters, fiber connectivity, and GPU-based cloud infrastructure is supporting market expansion. Regional cloud zones and sovereign cloud deployment are also increasing.Market Implications

Cloud vendors scaling infrastructure, AI compute, and energy-efficient data centers are expected to capture future opportunities.Market Segmentation Analysis

By Service Type

1. Infrastructure as a Service (IaaS)

This remains the largest segment due to high demand for scalable storage, computing, and networking.2. Platform as a Service (PaaS)

Growing rapidly for app development and cloud-native deployment.3. Software as a Service (SaaS)

Widely used across enterprise productivity, CRM, ERP, and collaboration tools.4. Managed Cloud Services

Expanding due to enterprise outsourcing of cloud operations.5. Cloud Security Services

Growing due to rising cyber threats and compliance demands.By Deployment Model

1. Public Cloud

Largest segment due to scalability and cost optimization.2. Private Cloud

Strong adoption in regulated sectors.3. Hybrid Cloud

Fastest-growing segment due to flexibility and enterprise workload balancing.4. Multi-Cloud

Rapidly expanding in large enterprises.By End-Use Industry

1. BFSI

Largest end-use industry due to data processing, cybersecurity, and digital banking.2. Healthcare

Growing due to telehealth, EHR, and AI diagnostics.3. Retail & E-commerce

Driven by omnichannel and analytics demand.4. Manufacturing

Growing with IIoT and predictive maintenance.5. Telecom & IT

Critical for 5G and infrastructure scaling.6. Government & Public Sector

Rising adoption for secure digital governance.Regional Market Dynamics

North America

North America dominates the global cloud service market due to hyperscale cloud providers, enterprise IT maturity, and AI infrastructure deployment.Europe

Europe remains a major market supported by GDPR-driven cloud compliance and sovereign cloud demand.Asia-Pacific

Asia-Pacific is the fastest-growing region due to enterprise digitalization, cloud-native startups, and rising hyperscale investment.Latin America

Latin America is gradually expanding due to fintech growth and enterprise digital transformation.Middle East & Africa

The region is witnessing emerging adoption driven by smart city projects, telecom growth, and digital infrastructure expansion.Competitive Landscape

The Global Cloud Service Market is highly competitive with hyperscale providers, enterprise software firms, and managed cloud-service companies expanding globally. Key companies operating in the market include:- Amazon Web Services (AWS)

- Microsoft Azure

- Google Cloud

- IBM Cloud

- Oracle Cloud

- Alibaba Cloud

- Salesforce

- SAP

- VMware

- Tencent Cloud

Strategic Outlook

The future of the cloud service market will be shaped by AI-native cloud platforms, multi-cloud orchestration, edge-cloud computing, quantum-ready cloud infrastructure, and sovereign cloud ecosystems. Industry-specific clouds, zero-trust security, GPU cloud services, and autonomous cloud optimization are expected to significantly improve enterprise efficiency and scalability. The rise of generative AI workloads, cloud cybersecurity, and energy-efficient hyperscale infrastructure is expected to create strong long-term growth opportunities.Final Market Perspective

The Global Cloud Service Market remains one of the fastest-growing segments within enterprise technology and digital infrastructure. Rising cloud migration, AI computing demand, cybersecurity priorities, and multi-cloud deployment continue driving long-term market growth. Providers capable of delivering secure, scalable, AI-enabled, and compliance-ready cloud ecosystem.Table of Contents

Table of Contents

1. Executive Summary

1.1 Market Snapshot

1.2 Key Growth Highlights

1.3 Largest Segment Analysis

1.4 Fastest Growing Segment Analysis

1.5 Regional Outlook

1.6 Competitive Landscape Snapshot

1.7 Future Market Outlook

2. Global Cloud Service Market Introduction

2.1 Market Definition

2.2 Scope of Study

2.3 Research Assumptions

2.4 Research Methodology

2.5 Forecast Parameters

3. Global Cloud Service Market Overview

3.1 Market Evolution

3.2 Industry Ecosystem Analysis

3.3 Value Chain Analysis

3.4 Pricing & Cost Structure Analysis

3.5 Supply Chain & Digital Infrastructure Overview

3.6 Technology Landscape

3.6.1 Hybrid Cloud Infrastructure

3.6.1.1 Multi-Cloud Deployment Models

3.6.1.1.1 Workload Optimization Systems

3.6.1.1.1.1 Intelligent Resource Allocation

3.6.1.1.1.2 Autonomous Cloud Scaling

3.6.2 AI Cloud Computing Platforms

3.6.2.1 GPU-Based Cloud Services

3.6.2.1.1 Generative AI Workload Management

3.6.2.1.1.1 AI Model Hosting & Processing

3.6.2.1.1.2 Intelligent Data Pipelines

3.6.3 Edge Computing & Cloud Integration

3.6.3.1 Low-Latency Cloud Architecture

3.6.3.1.1 Edge Node Expansion

3.6.3.1.1.1 Distributed Processing Networks

3.6.3.1.1.2 Real-Time Analytics Platforms

3.7 Regulatory Landscape

3.7.1 Data Sovereignty Compliance

3.7.1.1 Cybersecurity Regulations

3.7.1.1.1 Cross-Border Data Governance

3.7.1.1.1.1 Regional Data Residency Frameworks

3.7.1.1.1.2 Zero-Trust Security Models

3.8 Market Trends & Innovation Outlook

3.8.1 Industry-Specific Cloud Platforms

3.8.1.1 Cloud-Native Applications

3.8.1.1.1 Serverless Computing Adoption

3.8.1.1.1.1 Kubernetes-Based Automation

3.8.1.1.1.2 API-Led Ecosystems

4. Global Cloud Service Market Dynamics

4.1 Market Drivers

4.1.1 Rapid Enterprise Digital Transformation

4.1.1.1 Migration from On-Premise Infrastructure

4.1.1.1.1 Enterprise Cloud Scalability

4.1.1.1.1.1 IT Cost Optimization

4.1.2 Rising Adoption of SaaS Applications

4.1.2.1 Cloud Productivity Solutions

4.1.2.1.1 Business Workflow Automation

4.1.2.1.1.1 Remote Collaboration Growth

4.1.3 Expansion of AI-Driven Workloads

4.1.3.1 AI Infrastructure Demand

4.1.3.1.1 Machine Learning Platforms

4.1.3.1.1.1 GPU Cluster Expansion

4.1.4 Hybrid & Multi-Cloud Deployment Growth

4.1.4.1 Enterprise Flexibility Requirements

4.1.4.1.1 Cloud Redundancy Systems

4.1.4.1.1.1 Cross-Platform Integration

4.1.5 Growth in Data-Intensive Computing

4.1.5.1 Big Data Processing

4.1.5.1.1 High-Performance Analytics

4.1.5.1.1.1 Cloud Storage Optimization

4.2 Market Restraints

4.2.1 High Initial Infrastructure Cost

4.2.1.1 Hyperscale Data Center Expenses

4.2.1.1.1 GPU Resource Cost Pressure

4.2.1.1.1.1 Energy Consumption Challenges

4.2.2 Cybersecurity Risks

4.2.2.1 Data Breach Concerns

4.2.2.1.1 Zero-Day Threat Exposure

4.2.2.1.1.1 Cloud Security Complexity

4.2.3 Compliance Complexity

4.2.3.1 Data Residency Laws

4.2.3.1.1 Cross-Border Restrictions

4.2.3.1.1.1 Regulatory Fragmentation

4.2.4 Vendor Lock-In Challenges

4.2.4.1 Limited Portability

4.2.4.1.1 Multi-Cloud Cost Issues

4.2.4.1.1.1 Dependency Risks

4.3 Market Opportunities

4.3.1 AI-Native Cloud Platforms

4.3.1.1 Generative AI Hosting

4.3.1.1.1 AI Service Optimization

4.3.1.1.1.1 Model-as-a-Service Expansion

4.3.2 Sovereign Cloud Ecosystems

4.3.2.1 National Data Compliance

4.3.2.1.1 Government Cloud Infrastructure

4.3.2.1.1.1 Secure Public Cloud Solutions

4.3.3 Edge Cloud Growth

4.3.3.1 IoT Expansion

4.3.3.1.1 Low-Latency Processing

4.3.3.1.1.1 Smart Device Integration

4.3.4 Industry-Specific Cloud Solutions

4.3.4.1 BFSI Cloud Platforms

4.3.4.1.1 Healthcare Cloud Systems

4.3.4.1.1.1 Manufacturing Cloud Optimization

4.4 Market Challenges

4.4.1 Infrastructure Scalability Pressure

4.4.2 Energy Efficiency & Sustainability

4.4.3 Interoperability Issues

4.4.4 Data Privacy Risks

5. Global Cloud Service Market Size Analysis (USD Billion), 2026–2033

5.1 Revenue Forecast Analysis

5.2 CAGR Analysis

5.3 Demand-Supply Analysis

5.4 Segment Contribution Analysis

5.5 Pricing Trend Analysis

6. Global Cloud Service Market Segmentation Analysis

6.1 By Service Type

6.1.1 Infrastructure as a Service (IaaS)

6.1.1.1 Compute Infrastructure

6.1.1.1.1 Storage Services

6.1.1.1.1.1 Virtual Networking Solutions

6.1.2 Platform as a Service (PaaS)

6.1.2.1 Development Platforms

6.1.2.1.1 Cloud-Native Tools

6.1.2.1.1.1 Application Hosting Services

6.1.3 Software as a Service (SaaS)

6.1.3.1 Enterprise Productivity Tools

6.1.3.1.1 CRM & ERP Platforms

6.1.3.1.1.1 Workflow Automation Systems

6.1.4 Managed Cloud Services

6.1.4.1 Cloud Outsourcing

6.1.4.1.1 IT Monitoring Services

6.1.4.1.1.1 Infrastructure Management

6.1.5 Cloud Security Services

6.1.5.1 Identity Access Management

6.1.5.1.1 Threat Detection

6.1.5.1.1.1 Cloud Security Orchestration

6.2 By Deployment Model

6.2.1 Public Cloud

6.2.2 Private Cloud

6.2.3 Hybrid Cloud

6.2.4 Multi-Cloud

6.3 By End-Use Industry

6.3.1 BFSI

6.3.2 Healthcare

6.3.3 Retail & E-commerce

6.3.4 Manufacturing

6.3.5 Telecom & IT

6.3.6 Government & Public Sector

7. Regional Market Analysis

7.1 North America

7.1.1 U.S.

7.1.2 Canada

7.1.3 Mexico

7.2 Europe

7.2.1 Germany

7.2.2 U.K.

7.2.3 France

7.2.4 Italy

7.2.5 Spain

7.2.6 Rest of Europe

7.3 Asia-Pacific

7.3.1 China

7.3.2 Japan

7.3.3 India

7.3.4 South Korea

7.3.5 Australia

7.3.6 Rest of Asia-Pacific

7.4 Latin America

7.4.1 Brazil

7.4.2 Argentina

7.4.3 Rest of Latin America

7.5 Middle East & Africa

7.5.1 GCC Countries

7.5.2 South Africa

7.5.3 Rest of Middle East & Africa

8. Competitive Landscape

8.1 Market Share Analysis

8.2 Competitive Intensity Overview

8.3 Strategic Developments

8.4 Product Innovation & Platform Expansion

8.5 Partnerships, Mergers & Acquisitions

8.6 Cloud Ecosystem Positioning Analysis

9. Company Profiles

9.1 Amazon Web Services (AWS)

9.2 Microsoft Azure

9.3 Google Cloud

9.4 IBM Cloud

9.5 Oracle Cloud

9.6 Alibaba Cloud

9.7 Salesforce

9.8 SAP

9.9 VMware

9.10 Tencent Cloud

10. Strategic Intelligence & Pheonix AI Insights

10.1 Pheonix Demand Forecast Engine

10.2 AI Cloud Infrastructure Analyzer

10.3 Cloud Security Risk Tracker

10.4 Product Innovation Insights

10.5 Automated Porter’s Five Forces Analysis

11. Future Outlook & Strategic Recommendations

11.1 AI-Native Cloud Growth

11.2 Multi-Cloud Expansion Strategies

11.3 Edge Cloud & IoT Opportunities

11.4 Sustainable Data Center Innovation

11.5 Long-Term Market Outlook (2033+)

12. Appendix

12.1 Abbreviations

12.2 Research References

12.3 Data Sources

13. About Pheonix

14. Market Research

14. Disclaimer

Competitive Landscape

Global Cloud Service Market Competitive Intensity & Market Structure Overview

The Global Cloud Service Market is characterized by a moderately consolidated and hyperscaler-dominated competitive structure, where a few major cloud providers control a significant share of infrastructure, platform, and enterprise cloud ecosystems. Competition is primarily driven by hyperscale infrastructure, AI-cloud capabilities, hybrid & multi-cloud integration, cybersecurity strength, global data center footprint, cloud-native services, and industry-specific platform expansion.

The market is dominated by major players such as Amazon Web Services (AWS), Microsoft Azure, Google Cloud, IBM Cloud, Oracle Cloud, Alibaba Cloud, Salesforce, SAP, VMware, and Tencent Cloud, which compete through scale, AI services, enterprise ecosystem integration, compliance capabilities, and advanced cloud automation.

Rising enterprise demand across BFSI, healthcare, telecom, retail, manufacturing, government, and enterprise IT is intensifying competition. Companies are increasingly investing in AI-native cloud platforms, GPU cloud infrastructure, sovereign cloud, edge-cloud integration, zero-trust security, and multi-cloud orchestration.

Global Cloud Service Market Competitive Landscape

Leading Company Profiles

- Amazon Web Services (AWS) – Global leader in IaaS, cloud compute, storage, AI/ML services, and hyperscale cloud infrastructure.

- Microsoft Azure – Strong enterprise cloud provider with hybrid cloud leadership, AI integration, and deep enterprise software ecosystem.

- Google Cloud – Major provider in AI cloud services, data analytics, Kubernetes, and cloud-native workloads.

- IBM Cloud – Focused on hybrid cloud, enterprise transformation, and regulated-industry cloud solutions.

- Oracle Cloud – Strong presence in enterprise cloud databases, ERP ecosystems, and industry cloud infrastructure.

- Alibaba Cloud – Leading Asia-based hyperscaler with strong e-commerce, AI, and enterprise cloud expansion.

- Salesforce – Dominant SaaS cloud provider with CRM-led cloud ecosystem expansion.

- SAP – Strong enterprise SaaS and cloud ERP player with industry-specific digital transformation solutions.

- VMware – Key provider in hybrid cloud, virtualization, and multi-cloud orchestration platforms.

- Tencent Cloud – Expanding presence in Asia through cloud infrastructure, gaming, and enterprise digital ecosystems.

Key Competitive Intensity Signals

- Competition among hyperscalers for AI compute, GPU cloud, and generative AI workloads is rapidly intensifying.

- Hybrid cloud and multi-cloud orchestration are becoming major enterprise differentiators.

- Sovereign cloud and regional compliance-ready infrastructure are reshaping geographic competition.

- Cybersecurity, zero-trust architecture, and cloud governance capabilities are key trust-based barriers.

- Edge computing and low-latency workloads are increasing infrastructure differentiation.

- Vertical cloud solutions (BFSI, healthcare, manufacturing, government) are expanding high-margin competition.

- Strategic partnerships, cloud marketplaces, and API ecosystems are strengthening platform lock-in.

Strategic Implications

- AI-native cloud platforms and GPU infrastructure will remain core long-term differentiators.

- Providers with strong enterprise ecosystems and hybrid-cloud capabilities are expected to gain larger market share.

- Sovereign cloud and data residency compliance will increasingly shape regional growth.

- Cloud security and automation-led infrastructure optimization can improve recurring enterprise retention.

- Industry-specific cloud platforms are creating premium growth opportunities.

Forward Outlook

The Global Cloud Service Market is expected to remain moderately consolidated with very high competitive intensity, supported by AI-cloud expansion, hyperscale investment, and enterprise digital transformation.

Future competition will increasingly focus on:

- AI-native and GPU cloud infrastructure

- Hybrid cloud and multi-cloud orchestration

- Edge-cloud and low-latency compute ecosystems

- Sovereign cloud and compliance-ready data centers

- Zero-trust cloud cybersecurity platforms

- Industry-specific vertical cloud ecosystems

- Energy-efficient hyperscale infrastructure and autonomous cloud optimization

The convergence of AI, cloud automation, edge computing, cybersecurity, multi-cloud orchestration, and digital transformation will continue reshaping the long-term competitive landscape.

Value Chain

Global Cloud Service Market Value Chain & Supply Chain Evolution Overview

The Global Cloud Service Market operates through a digital infrastructure-driven ecosystem supported by hyperscale data centers, software development, cloud platform integration, cybersecurity frameworks, network connectivity, and enterprise service delivery. The market is increasingly shaped by AI-native cloud platforms, hybrid cloud deployment, edge computing, and multi-cloud orchestration.

Unlike physical product-heavy industries, cloud services rely on infrastructure scalability, software ecosystems, API-based integrations, and distributed digital delivery networks. The value chain centers around compute infrastructure, platform engineering, managed services, cloud security, and enterprise deployment.

Supply chain complexity is high due to global data center dependency, cybersecurity compliance, cross-border regulations, network infrastructure coordination, multi-vendor integrations, energy requirements, and continuous software-service optimization.

Global Cloud Service Market Value Chain & Supply Chain Evolution Current Scenario

Market-Specific Value Chain

1. Infrastructure & Core Technology Sourcing

Servers, GPUs, semiconductors, storage systems, fiber connectivity, networking hardware, cooling systems, and power infrastructure.

2. Cloud Platform Development & Software Engineering

IaaS, PaaS, SaaS platforms, virtualization, containerization, orchestration, APIs, automation tools, and cloud-native software.

3. Data Center Operations & Capacity Management

Hyperscale data centers, edge nodes, compute clusters, workload balancing, storage optimization, redundancy, and disaster recovery.

4. Cybersecurity, Compliance & Governance

Encryption, IAM, zero-trust security, compliance frameworks, data sovereignty, privacy controls, and audit systems.

5. Service Delivery & Distribution Networks

Direct enterprise sales, managed service providers (MSPs), channel partners, cloud marketplaces, SaaS ecosystems, and API-led delivery.

6. End-Use Deployment & Enterprise Ecosystem

BFSI, healthcare, retail, telecom, government, manufacturing, IT enterprises, and cloud-native startups.

Key Value Chain Evolution Signals

1. Shift Toward Hybrid & Multi-Cloud

Enterprises increasingly diversify workloads across providers.

2. AI Cloud Infrastructure Growth

GPU clusters and AI-optimized cloud are expanding rapidly.

3. Edge Computing Expansion

Regional edge nodes improve latency-sensitive services.

4. Compliance-Driven Architecture

Data sovereignty and cybersecurity are critical.

5. Hyperscale Data Center Investments

Capacity scaling remains a major competitive factor.

6. API & Marketplace Ecosystems

Partner-led service ecosystems strengthen distribution.

Strategic Implications

1. Infrastructure Scale Advantage

Large data center and compute capacity improves competitiveness.

2. Security & Compliance Leadership

Enterprise trust depends on governance and security readiness.

3. Ecosystem Integration

APIs, marketplaces, and managed services improve retention.

4. AI & Automation Differentiation

AI-native services improve workload optimization.

5. Geographic Cloud Expansion

Regional cloud zones strengthen compliance and latency performance.

Forward Outlook

The market is expected to evolve toward an AI-first, distributed, and autonomous cloud ecosystem driven by:

- AI-native cloud platforms

- Multi-cloud orchestration

- Edge-cloud integration

- Sovereign cloud zones

- Zero-trust security

- GPU-intensive compute infrastructure

- Industry-specific cloud ecosystems

Investment Activity

Global Cloud Service Market Investment & Funding Dynamics Overview

The Global Cloud Service Market is witnessing strong investment momentum driven by rapid enterprise digital transformation, AI-driven cloud computing, and growing demand for scalable digital infrastructure. Hyperscale cloud providers, enterprise software firms, managed cloud-service companies, cybersecurity vendors, and AI infrastructure providers are actively investing in data centers, GPU-based computing clusters, hybrid cloud ecosystems, and intelligent cloud orchestration platforms.

Investment activity is being accelerated by rising adoption of SaaS applications, AI workloads, multi-cloud strategies, edge computing, and cloud-native application development. The growing shift toward AI-integrated cloud services, industry-specific cloud platforms, serverless computing, and automation-led cloud optimization is significantly reshaping capital allocation across the market.

Additionally, expanding investments in hyperscale data centers, sovereign cloud deployments, cybersecurity frameworks, fiber connectivity, and regional cloud zones are strengthening long-term growth opportunities globally.

Global Cloud Service Market Investment & Funding Dynamics Current Scenario

Currently, the Global Cloud Service Market demonstrates rising investment activity with very high capital intensity due to hyperscale infrastructure expansion, AI compute requirements, GPU clusters, fiber networks, and cloud security architecture. Major players are heavily investing in IaaS platforms, hybrid cloud ecosystems, AI-integrated cloud services, edge-cloud integration, and sovereign cloud solutions.

The market is attracting strong funding into Kubernetes-based orchestration, serverless computing, cloud-native workloads, disaster recovery platforms, and zero-trust cloud security systems. Rising enterprise migration to AI-ready infrastructure and vertical cloud specialization is further strengthening investment flow.

The industry is witnessing active merger and acquisition activity as hyperscalers, SaaS firms, cybersecurity vendors, and cloud-service providers pursue strategic acquisitions, ecosystem expansion, and AI/cloud integration.

Key Investment & Funding Dynamics Signals in Global Cloud Service Market

- Rising adoption of AI workloads, multi-cloud strategies, edge computing, and cloud-native applications is accelerating cloud infrastructure investments.

- Expansion of hyperscale data centers, GPU clusters, sovereign cloud deployments, and fiber connectivity is increasing long-term capital deployment.

- Growing demand for hybrid cloud, managed cloud services, and industry-specific cloud ecosystems is strengthening infrastructure and software funding.

- Strategic investments in zero-trust security, cloud automation, and disaster recovery solutions are reshaping value-chain economics.

- Partnerships between hyperscalers, enterprise software firms, AI companies, and telecom operators are strengthening innovation ecosystems.

- Increasing regulatory focus on data sovereignty, cybersecurity compliance, and cross-border cloud governance is improving investor confidence.

- Rising demand for secure, scalable, AI-enabled, and compliance-ready cloud ecosystems is accelerating R&D and infrastructure spending.

Strategic Implications of Investment & Funding Dynamics in Global Cloud Service Market

- Continuous investment in AI-native cloud platforms, automation, and edge-cloud integration is essential for long-term competitiveness.

- Very high capital intensity requires strong allocation toward data centers, AI compute clusters, networking, and security architecture.

- Companies capable of delivering secure, scalable, and industry-specialized cloud ecosystems will strengthen market positioning significantly.

- Strategic M&A and AI/cloud ecosystem integration are accelerating service diversification.

- Investments in sovereign cloud, cybersecurity, and energy-efficient infrastructure will remain major priorities.

- Compliance with global privacy, security, and cloud governance standards is critical for enterprise trust and long-term adoption.

- Companies investing in generative AI infrastructure, autonomous cloud optimization, and multi-cloud orchestration are expected to capture substantial future opportunities.

Global Cloud Service Market Investment & Funding Dynamics Forward Outlook

Looking ahead, the Global Cloud Service Market is expected to maintain strong investment growth driven by AI-native cloud computing, hybrid cloud adoption, edge-cloud integration, and intelligent digital infrastructure.

Future capital deployment will increasingly focus on GPU cloud services, quantum-ready cloud infrastructure, sovereign cloud ecosystems, zero-trust architectures, autonomous workload optimization, and industry-specific cloud platforms. AI-driven compute expansion and sustainable hyperscale infrastructure are expected to become major innovation priorities.

In conclusion, the Global Cloud Service Market represents a high-growth, infrastructure-intensive investment landscape where AI integration, hyperscale scalability, cybersecurity, and multi-cloud ecosystems will define future capital strategies.

Technology & Innovation

Global Cloud Service Market Technology & Innovation Landscape Overview

The Global Cloud Service Market is undergoing rapid transformation driven by advancements in AI-native cloud computing, multi-cloud orchestration, edge computing, containerization, serverless architecture, quantum-ready infrastructure, and autonomous cloud optimization. The market demonstrates a high innovation intensity level, supported by rising enterprise digital transformation, AI workload growth, and demand for scalable intelligent cloud ecosystems.

At the center of this transformation is the shift from traditional hosted infrastructure toward AI-integrated intelligent cloud platforms capable of automated scaling, workload optimization, predictive resource allocation, and real-time analytics. Providers are increasingly investing in GPU-based cloud infrastructure, cloud AI accelerators, and autonomous compute management systems to support generative AI, big data, and high-performance enterprise workloads.

A major innovation area is hybrid cloud and multi-cloud orchestration, where businesses are deploying flexible architectures that combine public, private, and distributed cloud environments. These systems improve resiliency, vendor diversification, and workload balancing.

The market is also seeing rapid development in containerization, Kubernetes orchestration, serverless computing, and cloud-native microservices, allowing organizations to improve deployment agility, cost optimization, and application scalability.

Edge-cloud integration remains critical, with increasing adoption of distributed edge nodes, low-latency cloud processing, IoT-integrated compute layers, and real-time localized data processing for telecom, manufacturing, autonomous systems, and smart cities.

Cloud providers are innovating in zero-trust security, confidential computing, sovereign cloud infrastructure, automated compliance systems, and encryption-driven architectures, helping improve cybersecurity and regulatory alignment.

Additionally, advances in AI-driven observability, cloud automation, predictive infrastructure analytics, green hyperscale data centers, and energy-efficient compute optimization are reshaping competitive differentiation.

The convergence of AI, distributed computing, cybersecurity, automation, and cloud-native infrastructure is redefining the future technology landscape of the global cloud service market.

Global Cloud Service Market Technology & Innovation Landscape Current Scenario

Currently, the Global Cloud Service Market demonstrates very high patent activity and strong commercialization across hyperscale infrastructure, AI cloud platforms, hybrid architectures, and intelligent cloud software ecosystems.

1. AI-Native Cloud Infrastructure Innovation

GPU cloud, AI accelerators, and automated compute optimization are driving cloud evolution.

2. Hybrid & Multi-Cloud Orchestration

Flexible workload balancing across distributed cloud environments is expanding rapidly.

3. Edge Computing & Distributed Cloud Systems

Low-latency computing and localized cloud intelligence are supporting real-time applications.

4. Containerization & Serverless Architecture

Cloud-native development is accelerating application agility and operational efficiency.

5. Zero-Trust Security & Sovereign Cloud Systems

Compliance-ready security and regionalized cloud environments are strengthening enterprise trust.

6. Green Data Center & Energy Optimization Technologies

Efficient cooling, renewable power integration, and carbon-aware cloud systems are gaining importance.

Key Technology & Innovation Landscape Signals in Global Cloud Service Market

Several innovation signals are shaping the market:

1. Rising Demand for Generative AI Cloud Infrastructure

AI workloads are significantly increasing compute and GPU cloud demand.

2. Expansion of Hybrid & Multi-Cloud Strategies

Enterprises are prioritizing flexibility, resilience, and workload portability.

3. Increasing Cloud-Native Application Development

Microservices, containers, and serverless functions are becoming standard.

4. Growth of Edge & IoT Cloud Integration

Distributed processing is strengthening real-time industrial and telecom applications.

5. Cybersecurity & Compliance Innovation

Zero-trust, encryption, and data sovereignty solutions are becoming key differentiators.

6. Sustainability & Green Cloud Priorities

Energy-efficient hyperscale infrastructure is receiving stronger R&D focus.

Strategic Implications of Technology & Innovation Landscape in Global Cloud Service Market

The evolving technology landscape is significantly reshaping competition across the cloud service market. Companies are increasingly competing on AI compute capabilities, cloud scalability, cybersecurity architecture, workload automation, hybrid flexibility, regulatory readiness, and infrastructure efficiency.

Providers investing in AI-native clouds, edge platforms, sovereign infrastructure, Kubernetes orchestration, and cloud automation are expected to strengthen long-term market positioning.

Strategic collaborations between hyperscalers, semiconductor companies, telecom providers, cybersecurity vendors, and SaaS ecosystems are accelerating commercialization and reshaping digital infrastructure globally.

The growing convergence of AI, multi-cloud computing, edge processing, cybersecurity, automation, and industry-specific cloud platforms is creating strong long-term differentiation opportunities.

Additionally, regulatory emphasis on data sovereignty, cross-border cloud governance, privacy protection, and energy efficiency is encouraging stronger innovation and infrastructure localization.

Global Cloud Service Market Technology & Innovation Landscape Forward Outlook

Looking ahead to 2026–2033, the Global Cloud Service Market is expected to evolve toward highly autonomous, AI-optimized, and distributed intelligent cloud ecosystems.

Future technological developments are likely to include:

1. Autonomous AI-Driven Cloud Management

Self-optimizing cloud environments will improve efficiency and workload balancing.

2. Quantum-Ready Cloud Infrastructure

Early-stage quantum-access cloud services may strengthen high-performance workloads.

3. Advanced Multi-Cloud Orchestration

Cross-cloud automation and vendor-neutral portability will expand rapidly.

4. Edge-Native Distributed Computing

Localized processing will become central to IoT, telecom, and real-time applications.

5. Green Hyperscale Cloud Systems

Low-carbon, energy-efficient infrastructure will become a major differentiator.

6. Sovereign & Compliance-Driven Cloud Zones

Localized regulatory cloud environments will strengthen trust and adoption.

7. AI-Integrated Security & Predictive Cyber Defense

Autonomous threat detection and cloud risk intelligence will improve resilience.

Overall, companies capable of combining AI infrastructure, scalable cloud engineering, cybersecurity innovation, edge integration, automation, regulatory alignment, and sustainable hyperscale operations will be best positioned to lead the future evolution of the Global Cloud Service Market.

Market Risk

Global Cloud Service Market Risk & Disruption Analysis

The Global Cloud Service Market operates within a high disruption and high strategic-dependency environment, driven by AI workload acceleration, cybersecurity threats, data sovereignty laws, hyperscaler concentration, energy constraints, and evolving multi-cloud ecosystems. While the market demonstrates exceptional long-term growth due to enterprise digital transformation, SaaS adoption, and AI-native computing expansion, it remains exposed to regulatory fragmentation, infrastructure concentration risk, vendor lock-in, geopolitical tension, and fast-moving technology disruption.

A defining structural characteristic of the market is its evolution from scalable compute/storage infrastructure toward intelligent, AI-integrated, multi-layer cloud ecosystems. Traditional IaaS, PaaS, and SaaS remain foundational, but value creation is rapidly shifting toward GPU cloud services, AI model hosting, edge-cloud orchestration, zero-trust security, sovereign cloud infrastructure, and industry-specific cloud platforms.

The market is also increasingly concentrated around hyperscalers and ecosystem-driven cloud stacks, creating strategic dependency on compute infrastructure, data-center geography, semiconductor access, and software interoperability.

Global Cloud Service Market Current Risk Environment

The current market environment is characterized by rapid growth, high infrastructure concentration, and strong regulatory complexity.

One of the most significant disruption factors involves cybersecurity and operational resilience risk. Cloud providers manage mission-critical enterprise data, applications, identity systems, and AI workloads. Ransomware, cloud misconfigurations, API breaches, insider threats, and zero-day vulnerabilities can cause major reputational and operational disruption.

Another major risk area is data sovereignty and regulatory fragmentation. Governments increasingly require localized data hosting, sovereign cloud architecture, privacy compliance, and cross-border transfer restrictions. This directly affects cloud architecture, regional expansion, and compliance costs.

The market also faces vendor concentration and hyperscaler dependency risk. Enterprises often rely heavily on a limited number of providers, creating pricing power imbalance, lock-in challenges, and ecosystem concentration.

Additionally, semiconductor, GPU, and power-infrastructure dependency are becoming major strategic risks. AI-integrated cloud growth depends on advanced chips, high-density compute, fiber connectivity, and energy-intensive data centers.

In parallel, cloud cost optimization pressure, multi-cloud orchestration complexity, and interoperability demands are reshaping enterprise buying behavior.

Key Market Risk & Disruption Signals in Global Cloud Service Market

1. Cybersecurity & Data Breach Exposure

Cloud ecosystems remain high-value targets for ransomware, API attacks, identity compromise, and data leakage.

2. Data Sovereignty & Regulatory Fragmentation

Regional privacy laws, sovereign cloud mandates, and cross-border restrictions increase architecture complexity.

3. Hyperscaler Concentration & Vendor Lock-In

Heavy enterprise dependency on major cloud vendors increases pricing, migration, and resilience risks.

4. Semiconductor, GPU & Infrastructure Dependency

AI cloud growth relies on chip availability, compute density, network scaling, and energy supply.

5. Rising Cloud Cost & Optimization Pressure

FinOps, overprovisioning, storage costs, and AI compute economics are becoming major enterprise concerns.

6. Multi-Cloud Complexity & Interoperability Risk

Cross-platform orchestration, latency, workload portability, and API compatibility increase operational burden.

7. Energy & Sustainability Exposure

Hyperscale data centers face rising electricity demand, cooling requirements, and carbon-efficiency pressure.

8. Fast Technology Obsolescence

AI-native infrastructure, edge-cloud computing, quantum-readiness, and autonomous cloud systems shorten innovation cycles.

Strategic Implications of Market Risk & Disruption in Global Cloud Service Market

The evolving disruption environment creates both major growth opportunities and strategic infrastructure risk.

One of the most important strategic implications is the need for AI-first, secure, and sovereign-capable cloud ecosystems. Providers increasingly must combine compute, storage, AI services, networking, security, and governance into integrated enterprise platforms.

Companies are required to invest in GPU cloud capacity, zero-trust security, sovereign cloud deployment, edge integration, automation, and cloud-native orchestration to maintain competitiveness.

Vertical integration across chips, networking, data centers, cloud software, and AI stacks is becoming increasingly valuable for performance and resilience.

The convergence of AI, cybersecurity, edge computing, IoT, and industry-specific cloud environments is also reshaping the value chain. Firms with stronger interoperability across enterprise IT, SaaS, analytics, and AI workloads may gain higher stickiness and long-term recurring revenue.

Additionally, regional expansion through sovereign cloud zones and localized infrastructure will become strategically critical.

Companies focusing on AI-integrated cloud services, hybrid cloud, industry-specific cloud platforms, cybersecurity-first architecture, and scalable hyperscale ecosystems are expected to strengthen long-term market leadership.

Global Cloud Service Market Risk & Disruption Forward Outlook

Looking ahead to 2026–2033, the Global Cloud Service Market is expected to become increasingly AI-native, regulated, and infrastructure-sensitive.

1. Expansion of AI-Native Cloud Platforms

AI training, inference hosting, and GPU cloud ecosystems will become major growth drivers.

2. Greater Sovereign Cloud & Regional Data Zones

Localized compliance-driven infrastructure will expand globally.

3. Rising Multi-Cloud & Hybrid Cloud Complexity

Enterprises will continue balancing resilience, flexibility, and cost across platforms.

4. Higher Cybersecurity & Zero-Trust Standards

Cloud security architectures will become more embedded and compliance-intensive.

5. Greater Edge-Cloud Convergence

Low-latency applications and IoT workloads will strengthen distributed cloud adoption.

6. Stronger Energy & Sustainability Constraints

Green data centers, efficient cooling, and carbon-aware computing will become more important.

7. Competitive Consolidation & Ecosystem Lock-In

Large providers may strengthen platform dominance through AI and integrated services.

8. Growth in Industry-Specific Cloud Platforms

Healthcare, BFSI, government, and manufacturing clouds will expand rapidly.

In conclusion, the Global Cloud Service Market represents a high-growth, mission-critical, and ecosystem-dominant digital infrastructure environment, where cybersecurity resilience, sovereign compliance, AI compute capacity, interoperability, and energy-efficient scale will define long-term competitive success.

Regulatory Landscape

Global Cloud Service Market Regulatory & Policy Environment Overview

The regulatory and policy environment plays a critical role in shaping the Global Cloud Service Market as governments, cybersecurity authorities, and digital infrastructure regulators increasingly emphasize data sovereignty, privacy protection, cyber resilience, and cross-border cloud governance. Regulatory frameworks governing cloud storage, data residency, cybersecurity controls, encryption standards, digital trust, and industry-specific cloud compliance significantly influence infrastructure deployment, enterprise adoption, and international scalability.

Cloud services operate at the center of enterprise IT, digital transformation, AI computing, financial services, healthcare, telecom, and public-sector modernization. As organizations increasingly migrate mission-critical workloads to public, private, hybrid, and multi-cloud environments, regulatory oversight around data protection, cloud reliability, access controls, and operational continuity is becoming increasingly important.

The market is also influenced by evolving policies related to AI governance, cross-border data transfer, sovereign cloud frameworks, zero-trust cybersecurity, sector-specific cloud regulations, and energy-efficient hyperscale infrastructure. Governments are increasingly balancing cloud innovation with national data protection and digital sovereignty requirements.

In addition, digital economy policies, smart infrastructure programs, and enterprise modernization initiatives are further strengthening regulatory support for secure cloud adoption globally.

Global Cloud Service Market Regulatory & Policy Environment Current Scenario

Currently, the Global Cloud Service Market operates under a highly structured digital infrastructure and compliance-driven regulatory framework involving data privacy laws, cybersecurity mandates, cloud governance policies, sector-specific IT compliance, and cross-border digital regulations.

One of the most important regulatory trends influencing the market is the growing focus on data sovereignty and residency. Enterprises increasingly require geographically optimized cloud services that comply with national storage laws and local data processing obligations.

Another major regulatory development involves increasing cybersecurity and zero-trust requirements. Cloud providers must ensure strong encryption, identity management, access controls, disaster recovery, threat detection, and operational resilience.

Cross-border cloud governance also remains a major factor. Different jurisdictions apply varying rules on digital privacy, data portability, AI processing, and inter-country cloud access.

Sector-specific compliance is especially important across BFSI, healthcare, government, telecom, and enterprise IT, where cloud providers must meet strict regulatory certifications.

Additionally, sustainability and energy-efficiency policies are gradually influencing hyperscale data center operations and cloud infrastructure expansion.

Key Regulatory & Policy Environment Signals in Global Cloud Service Market

1. Rising Data Sovereignty & Residency Requirements

Cloud providers increasingly require region-specific infrastructure and local compliance capabilities.

2. Expansion of Cybersecurity & Zero-Trust Standards

Encryption, identity access management, and resilient cloud architecture are becoming essential.

3. Growing Cross-Border Cloud Governance Complexity

Global cloud operations must adapt to jurisdiction-specific digital regulations.

4. Sector-Specific Cloud Compliance Expansion

BFSI, healthcare, government, and telecom require stronger certification and audit-readiness.

5. AI Governance & Sustainable Infrastructure Influence

AI workloads and energy-efficient hyperscale operations are increasing regulatory focus.

Strategic Implications of Regulatory & Policy Environment in Global Cloud Service Market

The evolving regulatory environment creates major strategic implications for hyperscalers, managed cloud-service providers, SaaS firms, cybersecurity vendors, and enterprise clients. One of the most important implications is the growing need for secure, compliant, and regionally optimized cloud ecosystems.

Cloud providers must invest heavily in cyber resilience, sovereign cloud zones, compliance automation, encryption frameworks, AI governance, and audit-ready infrastructure to remain globally competitive.

The increasing convergence of AI, edge computing, multi-cloud orchestration, and industry-specific cloud platforms is also pushing vendors toward compliance-led cloud innovation.

Companies capable of balancing scalability, security, regional compliance, and operational efficiency will likely strengthen long-term market positioning.

Additionally, firms with strong hybrid-cloud integration, data localization strategies, and sector-specialized compliance capabilities will gain stronger competitive advantages.

Global Cloud Service Market Regulatory & Policy Environment Forward Outlook

Looking ahead to 2026–2033, the regulatory environment for cloud services is expected to become increasingly sovereignty-focused, cybersecurity-driven, and AI-governed as intelligent cloud ecosystems continue expanding globally.

Future regulations are likely to place stronger emphasis on AI transparency, cross-border digital trust, cloud resilience, sovereign infrastructure, quantum-ready security, and data lifecycle governance.

Governments may continue strengthening cloud privacy laws, cybersecurity mandates, sector-specific compliance, and national digital infrastructure strategies.

The expansion of AI-native cloud platforms, sovereign clouds, multi-cloud orchestration, and edge-cloud integration may further increase regulatory complexity.

Overall, the regulatory and policy environment will remain a critical factor influencing trust, scalability, infrastructure expansion, security validation, and competitive positioning within the Global Cloud Service Market. Companies capable of balancing innovation, cyber resilience, regulatory compliance, sovereign cloud readiness, and infrastructure efficiency will be best positioned to capture long-term growth opportunities.